journal of insurance regulation - naic.org · ernst csiszar, university of south carolina,...

TRANSCRIPT

Journal of Insurance Regulation

Cassandra Cole and Kathleen McCullough

Co-Editors

Vol. 33, No. 5

The State of the National Flood Insurance

Program: Treading Water or Sinking Fast?

Stephen G. FierKevin M. GatzlaffDavid M. Pooser

JIR-ZA-33-05

Accounting & ReportingInformation about statutory accounting principles and the procedures necessary for fi ling fi nancial annual statements and conducting risk-based capital calculations.

Consumer InformationImportant answers to common questions about auto, home, health and life insurance — as well as buyer’s guides on annuities, long-term care insurance and Medicare supplement plans.

Financial Regulation Useful handbooks, compliance guides and reports on fi nancial analysis, company licensing, state audit requirements and receiverships.

LegalComprehensive collection of NAIC model laws, regulations and guidelines; state laws on insurance topics; and other regulatory guidance on antifraud and consumer privacy.

Market RegulationRegulatory and industry guidance on market-related issues, including antifraud, product fi ling requirements, producer licensing and market analysis.

NAIC ActivitiesNAIC member directories, in-depth reporting of state regulatory activities and offi cial historical records of NAIC national meetings and other activities.

For more information about NAIC publications, view our online catalog at:

http://store.naic.org

Special StudiesStudies, reports, handbooks and regulatory research conducted by NAIC members on a variety of insurance-related topics.

Statistical ReportsValuable and in-demand insurance industry-wide statistical data for various lines of business, including auto, home, health and life insurance.

Supplementary ProductsGuidance manuals, handbooks, surveys and research on a wide variety of issues.

Securities Valuation Offi ceInformation regarding portfolio values and procedures for complying with NAIC reporting requirements.

White Papers Relevant studies, guidance and NAIC policy positions on a variety of insurance topics.

© 2014 National Association of Insurance Commissioners. All rights reserved.

Printed in the United States of America

No part of this book may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic or mechanical, including photocopying, recording, or any storage or retrieval system, without written permission from the NAIC.

NAIC Executive Offi ce444 North Capitol Street, NWSuite 700Washington, DC 20001 202.471.3990

NAIC Central Offi ce1100 Walnut StreetSuite 1500Kansas City, MO 64106816.842.3600

NAIC Capital Markets& Investment Analysis Offi ceOne New York Plaza, Suite 4210New York, NY 10004212.398.9000

The NAIC is the authoritative source for insurance industry information. Our expert solutions support the efforts of regulators, insurers and researchers by providing detailed and comprehensive insurance information. The NAIC offers a wide range of publications in the following categories:

The following companion products provide additional information on the same or similar subject matter. Many

customers who purchase the Journal of Insurance Regulation also purchase one or more of the following

products:

Companion Products

Federalism and Insurance Regulation

This publication presents a factual historical account of the development of the

framework for insurance regulation in the United States. It does so in part by

using illustrative early statutes, presenting them chronologically, and in part by

using cases that illustrate the interpretation of the crucial later statutes.

Copyright 1995.

Regulation and the Casualty Actuary

This anthology reprints 20 important papers from past issues of the Journal of

Insurance Regulation that are most relevant for practicing actuaries and state

insurance regulators. It covers a wide range of issues, such as ratemaking,

auto insurance pricing, residual markets, reserving and solvency monitoring.

This invaluable reference explains these complex topics in straightforward,

non-technical language. Copyright 1996.

International orders must be prepaid, including shipping charges. Please contact an NAIC Customer Service Representative, Monday - Friday, 8:30 am - 5 pm CT.

Editorial Board of the Journal of Insurance Regulation Vacant, Chair Robert Hoyt, Ph.D. University of Georgia Athens, GA James L. Nelson, Esq. Austin, TX Ex Officio Julienne Fritz, NAIC Director, Insurance Products & Services Division

Editorial Staff Editors Cassandra Cole and Kathleen McCullough Florida State University Tallahassee, FL Legal Editor Kay G. Noonan, J.D. NAIC General Counsel

Editorial Review Board Cassandra Cole, Florida State University, Tallahassee, FL

Lee Covington, Insured Retirement Institute, Arlington, VA

Brenda Cude, University of Georgia, Athens, GA

Ernst Csiszar, University of South Carolina, Columbia, SC

Robert Detlefsen, National Association of Mutual Insurance Companies, Indianapolis, IN

Sholom Feldblum, Liberty Mutual Insurance Co., Boston, MA

Bruce Ferguson, American Council of Life Insurers, Washington, DC

Kevin Fitzgerald, Foley & Lardner, Milwaukee, WI

Bob Ridgeway, America’s Health Insurance Plans, Washington, DC

Robert Gibbons, International Insurance Foundation, Wayne, PA

Martin Grace, Georgia State University, Atlanta, GA

Scott Harrington, University of Pennsylvania, Philadelphia, PA

Robert Hoyt, University of Georgia, Athens, GA

Robert Klein, Georgia State University, Atlanta, GA

Alessandro Iuppa, Zurich North America, Washington, DC

Andre Liebenberg, University of Mississippi, Oxford, MS

J. Tyler Leverty, University of Iowa, Iowa City, IA

Kathleen McCullough, Florida State University, Tallahassee, FL

Mike Pickens, Mike Pickens Law Firm, Little Rock, AR

Harold Skipper, Georgia State University, Atlanta, GA

David Snyder, American Insurance Association, Washington, DC

David Sommer, St. Mary’s University, San Antonio, TX

Sharon Tennyson, Cornell University, Ithaca, NY

Purpose

The Journal of Insurance Regulation is sponsored by the National Association

of Insurance Commissioners. The objectives of the NAIC in sponsoring the

Journal of Insurance Regulation are:

1. To provide a forum for opinion and discussion on major insurance

regulatory issues;

2. To provide wide distribution of rigorous, high-quality research

regarding insurance regulatory issues;

3. To make state insurance departments more aware of insurance

regulatory research efforts;

4. To increase the rigor, quality and quantity of the research efforts on

insurance regulatory issues; and

5. To be an important force for the overall improvement of insurance

regulation.

To meet these objectives, the NAIC will provide an open forum for the

discussion of a broad spectrum of ideas. However, the ideas expressed in the

Journal are not endorsed by the NAIC, the Journal’s editorial staff, or the

Journal’s board.

* Assistant Professor, University of Mississippi, 338 Holman Hall, University, MS 38677; [email protected].

** Assistant Professor, Ball State University, 357 Whitinger Business Building, 2000 W. University Avenue, Muncie, IN; [email protected].

*** Assistant Professor, St. John’s University, 101 Murray Street, Room 504, New York, NY 10007; [email protected]. © 2014 National Association of Insurance Commissioners

The State of the National Flood Insurance Program:

Treading Water or Sinking Fast?

Stephen G. Fier* Kevin M. Gatzlaff** David M. Pooser***

Abstract

The primary source of flood insurance for property owners in the United States since the 1960s has been the National Flood Insurance Program (NFIP). The program has been a valuable resource to those in need of flood coverage while the private insurance market largely avoided the flood peril. Although the federal program currently fills an important void that exists within the insurance market, the NFIP has not been without its critics. Over the past decade, the NFIP has received constant criticism directed at its subsidized rate structure, its debt to the U.S. Treasury and its long-term viability. In this paper, we discuss the history of the NFIP and flood insurance in the U.S., perceived weaknesses of the NFIP, recent legislation related to the NFIP, and recommendations that have been offered to improve the current flood insurance market in the U.S.

Journal of Insurance Regulation

© 2014 National Association of Insurance Commissioners

Introduction

It has long been recognized that private insurers in the U.S. insurance market view the flood risk as uninsurable (Anderson, 1974). In order to provide a stable insurance solution to property owners in flood-prone areas, the U.S. Congress created the National Flood Insurance Program (NFIP) through the passage of the National Flood Insurance Act of 1968 (NFIA). By passing the NFIA and creating the NFIP, Congress was able to provide many property owners with flood insurance coverage while simultaneously encouraging communities across the country to emphasize flood loss mitigation and building ordinance management. However, while the NFIP has been successful in increasing the availability of flood insurance coverage across the U.S., the program has faced several financial and non-financial problems that have called into question the way in which the program is structured and administered. Some of the most commonly cited problems that exist within the NFIP include increasing financial deficits, a continued adverse selection problem, uncertainty regarding the extension of the program and concerns regarding the administration of the Write Your Own (WYO) program that is used to market flood insurance to consumers.

As a result of some of the aforementioned problems, legislators have actively worked to alleviate these issues by recommending various changes to the NFIP. Several recommendations were made over the past decade, but one of the most recent legislative attempts to address the problems that plague the NFIP was passed through Congress in the form of the Biggert-Waters Flood Insurance Reform and Modernization Act of 2012 (Biggert-Waters Act). In addition to extending the NFIP for an additional five years, the Biggert-Waters Act implemented several changes to the program, including a phasing out of (and in some cases outright removal of) premium subsidies for certain properties, as well as greater oversight of expense reimbursement for WYO participants (NAIC, 2012). At the time of passage, many legislators, insurers and regulators heralded the legislation as a step in the right direction for the NFIP. However, as the Biggert-Waters Act began to be implemented, it became apparent that the use of actuarially fair (non-subsidized) rates would not simply increase insurance premiums, but that increases could be dramatic, with some insureds experiencing increases of up to 3,000% (Pettus, 2013). These rate increases resulted in an outcry from affected homeowners and uncertainty within some housing markets, ultimately leading to legislation that substantially modified the key provisions of the Biggert-Waters Act (Simpson, 2014a). While the Biggert-Waters Act was eventually altered through the passage of the Homeowner Flood Insurance Affordability Act, the rate increases and initial fallout from the Biggert-Waters Act have led to further debate regarding the current state of the NFIP, as well as the future of flood insurance in the U.S.

The remainder of this paper is organized as follows. We first provide a brief overview of the NFIP’s history and discuss its creation, as well as the role of private insurers in the NFIP. The evidence suggests that while the NFIP represents

The State of the National Flood Insurance Program

© 2014 National Association of Insurance Commissioners

a public-private partnership between the federal government and private insurers, the market is highly concentrated and relies heavily on the top 10 WYO participants to market nearly 80% of total federal flood insurance policies. Next, we address some of the problems that currently exist within the NFIP and concerns from regulators, legislators, insurers and consumers. These problems include (among others) a lack of involvement in the market by private insurers, increasing financial deficits in the NFIP, a reliance on large subsidies to encourage some property owners to purchase policies, and a program structure that allows for continued adverse selection to exist. We then discuss NFIP-related legislation that was recently passed in an effort to alleviate some of these problems, and we outline the costs and benefits of that legislation. Finally, we review the recommendations outside of recent legislation that have been proposed to fix what many view as a flawed system for providing flood insurance coverage.

The NFIP and the WYO Program The National Flood Insurance Program

Prior to 1927, property owners in the U.S. had the ability to obtain coverage for flood losses through “several dozen” insurers in the private insurance market by adding the flood peril to the other perils that were covered in fire insurance policies (King, 2005; Scales, 2006). However, in 1927, major flooding took place along the Mississippi River, resulting in 250 deaths and between $250 million and $350 million in total losses across seven states (Risk Management Solutions, 2007). Following the large losses from the flooding in 1927 and 1928, private insurers began to cease writing flood coverage (King, 2005). During this period of time, the federal government began to work on developing solutions to mitigate flood losses. This was done in part through the Flood Control Act of 1936, which created a program that was intended to structurally control floods (Pasterick, 1998).1 Following the passage of the Flood Control Act, the most prevalent method of providing disaster assistance to victims was through the use of federal disaster loans and grants. Over time, however, concern began to grow about the increasing costs associated with this federal assistance (Pasterick, 1998).2 It took more than three decades after the passage of the Flood Control Act and four decades after the floods along the Mississippi River for the federal government to formally create a federal program to address flood insurance in the U.S.3

1. It has been argued that the attempt to structurally control floods actually further

encouraged individuals to “encroach” on flood-prone areas (Maloney and Dambly, 1976). 2. King (2005) notes that some of the major concerns at this time included: 1) continued

growth in vulnerable areas; 2) the lack of long-run effectiveness of the flood controls; and 3) the unpredictable nature of the disaster relief payments.

3. See The American Institutes for Research et al. (2005) for a more detailed chronology of events related to the NFIP’s development.

Journal of Insurance Regulation

© 2014 National Association of Insurance Commissioners

Congress created the National Flood Insurance Program (NFIP) following the passage of the National Flood Insurance Act of 1968 (NFIA). While some legislation related to a federal flood insurance program had been enacted prior to 1968, it was not until after large flood-related losses from Hurricane Betsy in 1965 that movement was made towards the creation of a federal flood insurance program.4 The passage of the NFIA in 1968 and the creation of the NFIP were necessitated not only as a result of past large flood losses, but also because private insurers did not view flood as an insurable peril.5,6 While there were several reasons for this perspective, some of the insurers’ primary concerns included: 1) areas that experienced recurring flood activity were almost certain to experience future losses; 2) given the frequency and severity of flood events, the premiums required to offer such coverage would be economically unfeasible for insureds in flood-prone areas; and 3) adverse selection was likely to be a major problem in the flood insurance market (Anderson, 1974).

Given the large prior flood losses and the insurance industry’s unwillingness to offer flood insurance, Congress passed the NFIA in 1968. The purpose of the NFIA was twofold: 1) it would encourage communities to focus on greater flood loss mitigation through improved building codes and zoning ordinances; and 2) the NFIA would increase the availability of flood insurance coverage by allowing the federal government to offer coverage to communities that utilized floodplain management (Federal Emergency Management Agency (FEMA), 2011).7 The combination of insurance coverage tied to community involvement in floodplain management meant that insureds could receive coverage (possibly at subsidized rates) while communities would improve mitigation standards designed to reduce future flood-related losses (Anderson, 1974).

4. The Federal Flood Insurance Act (FFIA) of 1956 was enacted but was not implemented

due to a lack of involvement and interest by private insurance companies (Michel-Kerjan, 2010). Anderson (1974) notes that the FFIA of 1956 had many provisions that were similar to those found in the NFIA of 1968.

5. The standard NFIP flood policy defines “flood” as: “1. A general and temporary condition of partial or complete inundation of two or more acres of normally dry land area or of two or more properties (at least one of which is your property) from: a) overflow of inland or tidal waters; b) unusual and rapid accumulation or runoff of surface waters from any source; c) mudflow, 2. Collapse or subsidence of land along the shore of a lake or similar body of water as a result of erosion or undermining caused by waves or currents of water exceeding anticipated cyclical levels that result in a flood as defined in A.1.a. above.”

6. While this represents the experience in the U.S., it should be noted that experience differs outside of the U.S. For instance, several European countries also commonly experience flood losses and have developed other methods to treat these exposures (outside of government intervention), including involvement by the private insurance market. As one example, Medders, McCullough and Jager (2011) note that flood insurance is not subsidized by the state in Germany and that premiums tend to be high.

7. While we focus almost exclusively on the insurance component of the NFIP program, prior studies have more explicitly investigated the mitigation aspects of the NFIP and the more general decision to mitigate (e.g., Kelly and Kleffner, 2003; Michel-Kerjan, 2010; Carson, McCullough and Pooser, 2013).

The State of the National Flood Insurance Program

© 2014 National Association of Insurance Commissioners

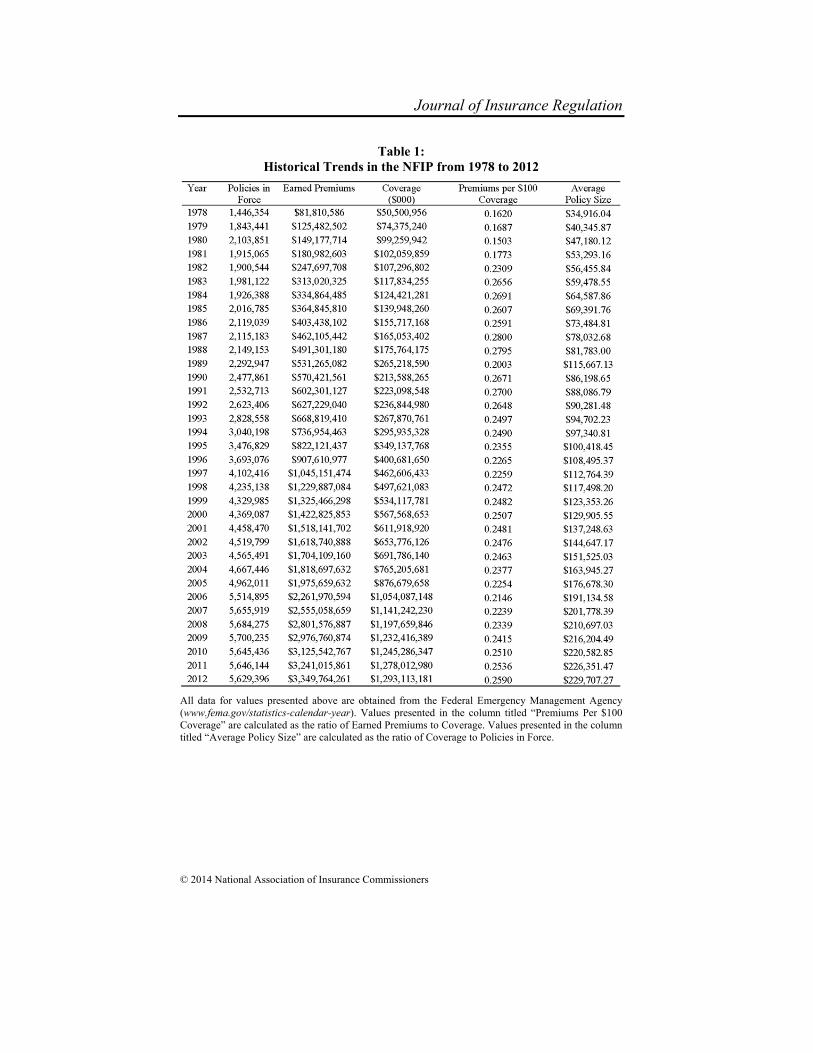

As an initial evaluation of the NFIP, we present data that illustrate the role that the NFIP plays in the U.S. flood insurance market. Table 1 presents historical information pertaining to policies in force, premiums and coverage limits for federal flood policies issued between 1978 and 2012. The table suggests that as of 2012, nearly 5.63 million flood insurance policies were in force in the U.S., accounting for total coverage limits of more than $1.29 trillion and total earned premiums of almost $3.35 billion. The table also shows that the average price of coverage is around $0.25 per $100 of coverage and that the average policy in 2012 provided coverage of $229,707.8,9

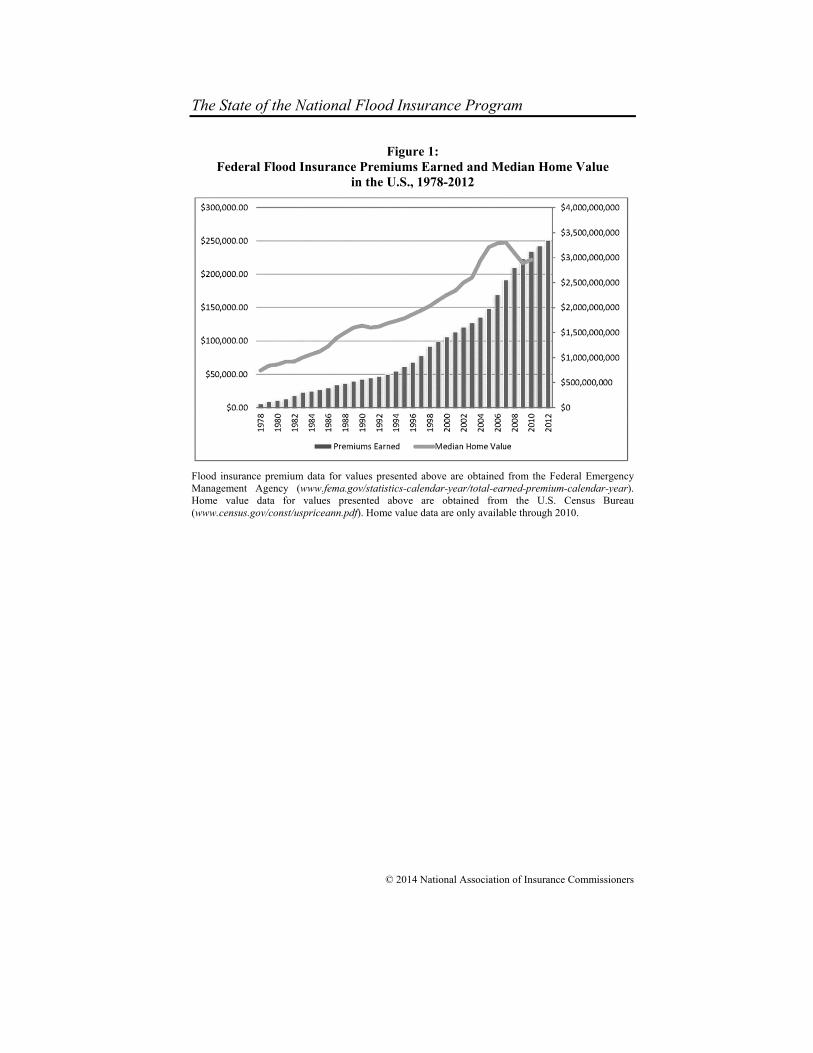

When examining the development of the federal flood insurance market over the 10-year period from 2003 to 2012, there is evidence of significant growth. Specifically, Table 1 shows that there was more than a 20% increase in the total number of policies issued between 2003 and 2012. Even more striking is the growth in the coverage limits, which jumped from $691.78 billion to $1.29 trillion. This amounts to an 87% increase in coverage limits during the 10-year span. The increase in coverage limits is most dramatic during the one-year period following Hurricane Katrina (from 2005 to 2006), when the number of policies in force increased by 14% and the coverage limits increased by 20%.10 The trends in policies in force and premiums earned by the NFIP are also illustrated in Figure 1 and Figure 2. It is likely that these increasing trends are a function of several factors, including greater awareness of the flood peril, more pervasive knowledge that the flood peril is not covered under the standard homeowners’ insurance policy, and the fact that development along the U.S. coastlines continues to increase, despite the potential for flood-related losses.11 Figure 1 illustrates that significant growth in earned premiums and coverage limits occurred in the mid-2000s despite a sharp decline in home values beginning in 2007.

8. The information contained in Table 1 does not differentiate between dwelling form

coverages and general property form coverages. The dwelling form is used for residential property (one- to four-family residential buildings) and limits coverage to $250,000 for the building and $100,000 for personal property (FEMA, 2014a). The general property form is for commercial entities (five or more residential buildings and non-residential buildings) and limits coverage to $500,000 for buildings and $500,000 for personal property (FEMA, 2014b). Additionally, Table 1 does not differentiate between those property owners in the emergency program and those in the regular program.

9. These values are a rough approximation of the average cost and do not consider location-based differences, which can greatly influence the rate.

10. The evidence that demand increased following the occurrence of Hurricane Katrina in 2005 is consistent with the findings of Browne and Hoyt (2000), who find that the demand for flood insurance increased following the experience of past flood losses.

11. Kriesel and Landry (2004) find that nearly 50% of eligible properties in sample coastal areas participate in the NFIP.

Journal of Insurance Regulation

© 2014 National Association of Insurance Commissioners

Table 1: Historical Trends in the NFIP from 1978 to 2012

All data for values presented above are obtained from the Federal Emergency Management Agency (www.fema.gov/statistics-calendar-year). Values presented in the column titled “Premiums Per $100 Coverage” are calculated as the ratio of Earned Premiums to Coverage. Values presented in the column titled “Average Policy Size” are calculated as the ratio of Coverage to Policies in Force.

The State of the National Flood Insurance Program

© 2014 National Association of Insurance Commissioners

Figure 1: Federal Flood Insurance Premiums Earned and Median Home Value

in the U.S., 1978-2012

Flood insurance premium data for values presented above are obtained from the Federal Emergency Management Agency (www.fema.gov/statistics-calendar-year/total-earned-premium-calendar-year). Home value data for values presented above are obtained from the U.S. Census Bureau (www.census.gov/const/uspriceann.pdf). Home value data are only available through 2010.

Journal of Insurance Regulation

© 2014 National Association of Insurance Commissioners

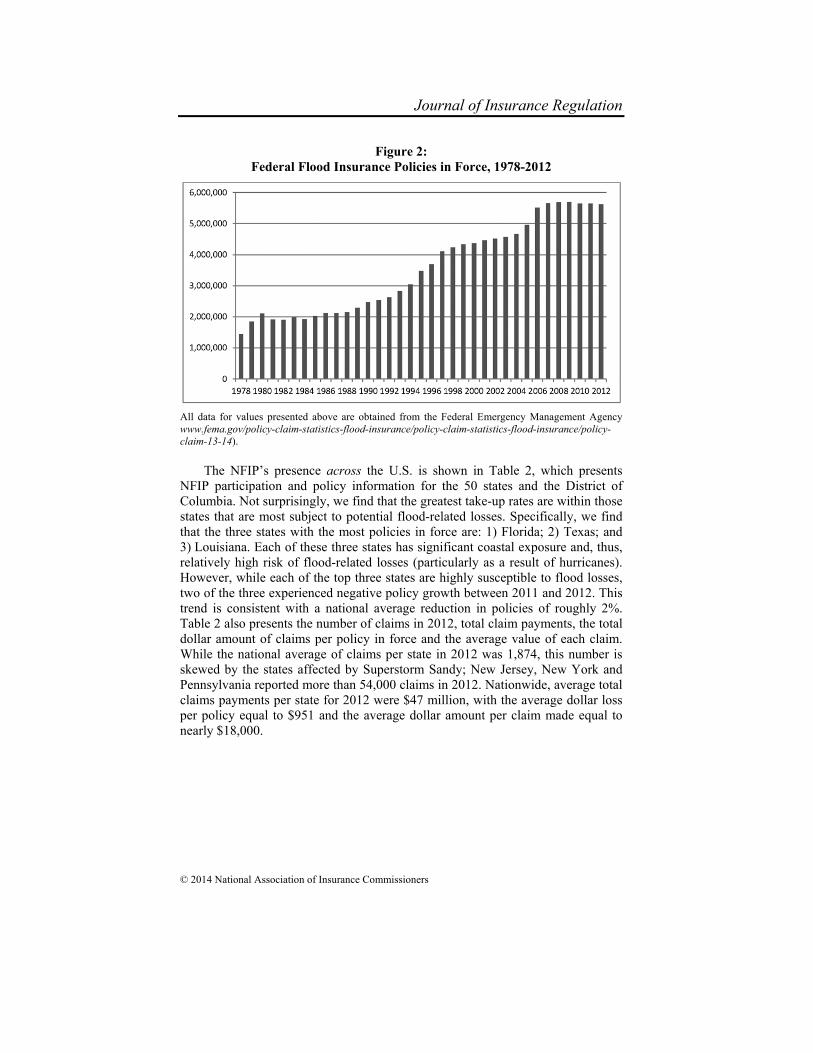

Figure 2: Federal Flood Insurance Policies in Force, 1978-2012

All data for values presented above are obtained from the Federal Emergency Management Agency www.fema.gov/policy-claim-statistics-flood-insurance/policy-claim-statistics-flood-insurance/policy-claim-13-14).

The NFIP’s presence across the U.S. is shown in Table 2, which presents

NFIP participation and policy information for the 50 states and the District of Columbia. Not surprisingly, we find that the greatest take-up rates are within those states that are most subject to potential flood-related losses. Specifically, we find that the three states with the most policies in force are: 1) Florida; 2) Texas; and 3) Louisiana. Each of these three states has significant coastal exposure and, thus, relatively high risk of flood-related losses (particularly as a result of hurricanes). However, while each of the top three states are highly susceptible to flood losses, two of the three experienced negative policy growth between 2011 and 2012. This trend is consistent with a national average reduction in policies of roughly 2%. Table 2 also presents the number of claims in 2012, total claim payments, the total dollar amount of claims per policy in force and the average value of each claim. While the national average of claims per state in 2012 was 1,874, this number is skewed by the states affected by Superstorm Sandy; New Jersey, New York and Pennsylvania reported more than 54,000 claims in 2012. Nationwide, average total claims payments per state for 2012 were $47 million, with the average dollar loss per policy equal to $951 and the average dollar amount per claim made equal to nearly $18,000.

The State of the National Flood Insurance Program

© 2014 National Association of Insurance Commissioners

Table 2: Federal Flood Insurance by State in 2012

All data for values presented above are obtained from the Federal Emergency Management Agency (www.fema.gov/policy-claim-statistics-flood-insurance/policy-claim-statistics-flood-insurance/policy-claim-13-0). Policy growth values represent the change from Oct. 1, 2011, through Sept. 30, 2012. Values presented in the column titled “$ Claim Per Policy” are calculated as the ratio of Total Claim Payments to Policies in Force. Values presented in the column titled “$ Average Claim” are calculated as the ratio of Total Claim Payments to Total Number of Claims.

Journal of Insurance Regulation

© 2014 National Association of Insurance Commissioners

The Write Your Own Program

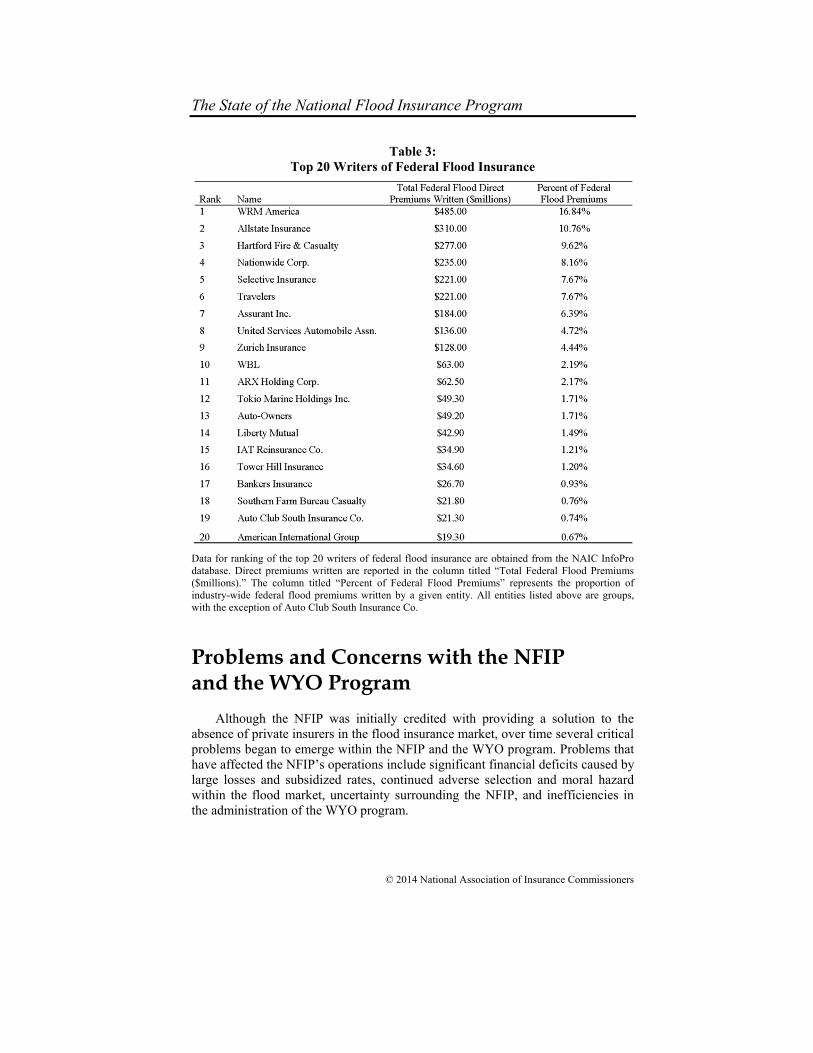

The WYO program is a partnership between the NFIP and private insurance carriers that the federal government created in 1983 in an effort to increase the geographic distribution of flood insurance policies, improve the servicing of policies by taking advantage of private insurer knowledge and allow private insurers to interact with consumers in the flood insurance market (Government Accountability Office, 2009). Under the WYO program, private insurers offer standardized flood insurance coverage to insureds but do not bear the underwriting risk associated with these policies.12 Rather, the federal government assumes the financial risks associated with writing flood insurance while the WYO participants market the policies, write the policies under their own names, service the policies, and investigate and pay any claims associated with the policies. In return for issuing and administering the policies, WYO participants receive a portion of the flood insurance premiums to pay for marketing, administrative costs and operating expenses (Government Accountability Office, 2009).13 As the Government Accountability Office (GAO) noted, as of September 2008, about 90 WYO participants issued and administered approximately 97% of the NFIP policies in force (Government Accountability Office, 2009). The top 20 writers of federal flood insurance in 2012 are presented in Table 3, along with the total federal flood direct premiums written and the proportion of firm-specific premiums to total industry federal flood premiums written. More than $2.8 billion in direct premiums were written in the federal flood line of business in 2012.14 As presented in Table 3, the federal flood insurance market is highly concentrated, with the top 10 insurers writing more than 75% of premiums.15

12. Three standard flood insurance coverage forms exist under the NFIP: the dwelling form,

the general property form and the residential condominium building association policy form. 13. According to a 2009 GAO study, WYO insurers received the following expense

allowances: 1) 15% of net premiums written for commission expenses; 2) 15.2% of net premiums written in 2007 to cover operating expenses; 3) 0.5% to 2% of net premiums written for incentive bonuses; 4) flat fees to cover claims ranging from $60 to $1,250 for claims up to $50,000 and percentage fees between 2.1% and 3% of the claim loss; 5) 3.3% per claim loss incurred for claims processing; and 6) additional amounts to cover additional loss adjustment expenditures (including engineering, adjusting, litigation and appraisal) (GAO, 2009).

14. As reported in Table 1, FEMA reports a total of approximately $3.35 billion in direct premiums earned in 2012. We attribute part of the difference between the value we calculate and the values calculated by FEMA to the fact that while FEMA reports that more than 80 private insurers write the federal flood line of business, only 69 insurers in the NAIC InfoPro database report positive premiums written in this line. We provide a listing of the 84 insurers participating in the 2014 WYO program as reported by FEMA in the Appendix.

15. While Travelers Group was the sixth-largest writer of federal flood insurance coverage in 2012, it announced in August 2013 that it would no longer offer federal flood insurance coverage (Insurance Journal, 2013).

The State of the National Flood Insurance Program

© 2014 National Association of Insurance Commissioners

Table 3: Top 20 Writers of Federal Flood Insurance

Data for ranking of the top 20 writers of federal flood insurance are obtained from the NAIC InfoPro database. Direct premiums written are reported in the column titled “Total Federal Flood Premiums ($millions).” The column titled “Percent of Federal Flood Premiums” represents the proportion of industry-wide federal flood premiums written by a given entity. All entities listed above are groups, with the exception of Auto Club South Insurance Co.

Problems and Concerns with the NFIP and the WYO Program

Although the NFIP was initially credited with providing a solution to the absence of private insurers in the flood insurance market, over time several critical problems began to emerge within the NFIP and the WYO program. Problems that have affected the NFIP’s operations include significant financial deficits caused by large losses and subsidized rates, continued adverse selection and moral hazard within the flood market, uncertainty surrounding the NFIP, and inefficiencies in the administration of the WYO program.

Journal of Insurance Regulation

© 2014 National Association of Insurance Commissioners

Financial Deficits

The NFIP’s most commonly cited problem is that since the enactment and implementation of the NFIA of 1968, the rates for many of the most at-risk insureds have been subsidized in order to encourage greater community and consumer participation in the flood insurance program. Prior to the passage of the Biggert-Waters Act in 2012, approximately 21% of NFIP policies (approximately 1.15 million policies) received subsidies, while the remaining 79% were charged the “full-risk rates” (Government Accountability Office, 2013).16 Although less than a quarter of all NFIP policies were receiving subsidies, the GAO (2013) report notes that almost all of those subsidized policies protect structures that were located in high-risk locations. Additionally, while nearly 80% of NFIP policyholders pay the “full-risk rates” (i.e., an actuarially fair premium), the GAO has stated that those rates may not fully capture the risk of flooding due to outdated flood maps and inaccurate data regarding the probability of flooding (Government Accountability Office, 2010).

Although the NFIP’s premium structure was sufficient to cover flood losses prior to 2005, this can mostly be credited to the fact that past flood losses were less costly than losses recorded in the last decade and that policies were more geographically diversified; i.e., not concentrated in flood-prone areas. Within the last decade, several significant flood-related events occurred that rapidly deteriorated the NFIP’s financial standing. As illustrated in Table 4, in terms of nominal dollar losses, the NFIP’s five highest flood loss years all occurred in the 2000s. The losses that occurred in three of those years were greater than premiums that the NFIP collected in those particular years (King, 2013). Due to the premium shortfalls, the NFIP has relied on borrowing from the U.S. Treasury to cover the cost of paying claims since 2005 (King, 2013).17 By 2013, the NFIP’s deficit had grown to approximately $24 billion (Kousky and Kunreuther, 2013). Figure 3 presents the cumulative debt of the NFIP from 2005 through 2011, as reported in King (2013).

16. According to a 2010 GAO report, subsidized policyholders pay a premium equal to

roughly 35% to 40% of the actuarially fair premium. 17. While the NFIP has become reliant on debt since 2005, it had borrowed funds from the

Treasury prior to 2005 (King, 2005). However, prior to 2005, the largest cumulative debt had always been less than $1 billion and was commonly less than $500 million.

The State of the National Flood Insurance Program

© 2014 National Association of Insurance Commissioners

Table 4: NFIP Significant Flood Events

The Federal Emergency Management Agency (FEMA) defines a significant flood event as a flood event that results in 1,500 claims or more. Significant flood events are identified through FEMA (www.fema.gov/significant-flood-events). No significant flood events were reported by the NFIP for 1987 or 1990. The five years resulting in the largest payments (in nominal dollars) for significant flood events are highlighted above.

Journal of Insurance Regulation

© 2014 National Association of Insurance Commissioners

Figure 3: NFIP Cumulative Debt, 2005-2011

Values presented above are in millions, and all values are obtained from King (2013).

Adverse Selection, Moral Hazard and Repetitive Loss Properties

Another problem the NFIP faces is adverse selection. One reason why private insurers have largely avoided the flood insurance market is that the individuals and businesses that demand flood insurance are often those most likely to experience a loss, especially because many of the NFIP’s policyholders are located in high-risk flood zones.18 The existence of moral hazard within the federal flood insurance market further compounds this issue. Specifically, when the NFIP was created, there was no deterrent for policyholders who experienced a loss to rebuild outside high-risk flood zones. This meant that policyholders could experience a flood loss, rebuild their property at the same high-risk location and then experience subsequent flood losses. (These locations are commonly referred to as “repetitive loss properties.”).19 The NFIP’s decision to provide insurance for high risk property, to offer no deterrence to rebuilding homes and businesses in flood-prone areas, and the fact that rates were often subsidized meant there was little incentive or reason for policyholders to rebuild their homes and businesses in safer locations. There is significant anecdotal evidence that adverse selection and moral hazard are both present in the NFIP market. For example, it has been reported that a home in Mississippi that was valued at $69,900 had been flooded 34 times during a 32 year period. Over the course of those 32 years, a total of $663,000 in

18. Some of their properties were built before Flood Insurance Rate Maps (FIRMs) were

developed for their communities. FEMA reports that nearly 580,000 policies issued on pre-FIRM primary residences receive subsidies (FEMA, 2013a).

19. FEMA defines a repetitive loss property as any property that experiences two or more flood losses that are greater than $1,000 during a 10-year period.

The State of the National Flood Insurance Program

© 2014 National Association of Insurance Commissioners

benefits was paid to cover flood-related damages to that home (Frank, 2010). In another instance, an Alabama home valued at $153,000 cost the NFIP $2.3 million in claims (Frank, 2010).

Evidence suggests that the total number of repetitive loss properties is relatively low within the NFIP, but that aggregate claims attributed to these properties are significant. While these repetitive loss properties represent only a small fraction of the total number of homes covered under the federal flood insurance program (roughly 1%), historically they have accounted for nearly 38% of total program claims (Government Accountability Office, 2004). One way in which Congress has attempted to address the problem of repetitive loss properties is through the passage of the Bunning-Bereuter-Blumenauer Flood Insurance Reform Act of 2004 (BBB Act). The BBB Act created a pilot program that provided grants to severe repetitive loss properties.20 The grant allowed high-risk property owners to mitigate against future potential flood losses. Under the pilot program, owners of severe repetitive loss properties could receive the grant offer (once FEMA awarded the grant to the given state) and choose to either accept the grant or reject the grant; however, those who declined the grant could be charged higher flood insurance premiums in the future. While a major goal of the BBB Act was to reduce the number of severe repetitive loss properties, a 2009 report from the U.S. Office of Inspector General states that “[t]he number of repetitive and severe repetitive loss properties and insurance claims has steadily increased over the past eight years and is outpacing FEMA mitigation efforts.”

Uncertainty Surrounding the NFIP Program The NFIA of 1968 included a provision that called for the expiration of the

NFIP in 1997.21 Thus, the NFIPs continuation is reliant on Congress’ ability to pass extensions. Following the large flood losses stemming from Hurricane Katrina and Hurricane Rita, considerable time was spent developing a plan to modernize the NFIP and minimize/avoid the financial strains that had enveloped the program. Because of the vigorous debate (and disagreements) that ensued regarding viability and modernization of the NFIP, uncertainty surrounding the NFIP’s future developed because the program had operated for several years entirely on the basis of short-term extensions. Specifically, from 2008 to 2012, the NFIP was extended 17 times, and it was allowed to lapse twice (Widmer, 2012).

20. The language of the BBB Act defines a severe repetitive loss property as a property that

meets the following conditions: a) the property consists of one to four residences; b) the property is covered by federal flood insurance; c) the property had experienced four or more claims payments under the flood policy, with each claim exceeding a $5,000 threshold and the total amount exceeding a $20,000 threshold; or d) the property had experienced at least two or more claims payments with the total amount exceeding the total value of the property (BBB Act, 2004) .

21. Section 1319 of the NFIA contains the “Expiration of Program” provision, which states, “No new contract for flood insurance under this chapter shall be entered into after September 30, 1997.”

Journal of Insurance Regulation

© 2014 National Association of Insurance Commissioners

It was not until the passage of the Biggert-Waters Act (discussed below) that Congress agreed upon a long-term (five-year) extension of the NFIP.

The short-term extensions caused uncertainty for property owners, the real estate market and insurers, as there were concerns over whether flood insurance coverage would be available for homes with the highest risk for flood loss. For many homeowners, flood insurance is required in order to receive federal financial assistance (either through the Federal National Mortgage Association or the Federal Home Loan Mortgage Corporation) to purchase or build a home in a Special Flood Hazard Area (SHFA).22 If NFIP coverage is allowed to lapse or, based on legislative changes, when uncertainty exists regarding the NFIP’s future, current property owners in SFHAs and those considering purchasing property in SFHAs are affected. Uncertainty over the NFIP’s future affects the entire real estate market in flood-prone areas, often causing buyer reticence and potentially reducing home values (The Times-Picayune, 2014; Garrison, 2014; Ballard, 2014; Koba, 2014). While the Biggert-Waters Act affords stakeholders the peace of mind that the NFIP will be in effect for five years, the future may hold that legislators will again rely on short-term extensions for a program that protects millions of property owners.

While regulators and legislators are most worried about the impact of NFIP uncertainty on consumers, uncertainty surrounding the NFIP also affects the U.S. private insurance industry.23 There is evidence that the private insurance industry is willing to write flood insurance for homeowners and small business owners, but that their willingness is being tempered by the uncertain future of the NFIP, especially with regard to the NFIP’s premium structure (Scism, 2014; Singer, 2014). Private insurers struggle to compete against a subsidized premium

22. This requirement was created through the passage of the Flood Disaster Protection Act

of 1973 and is restated in the National Flood Insurance Reform Act of 1994. 23. For instance, State Farm announced in 2010 that it would cease participation in the

WYO program. The decision to exit the program was due to “… numerous stop-starts to the program since 2002, and because procedural changes in claims handling are forcing it to divert too much of its resources to the program” (Postal, 2010).

The State of the National Flood Insurance Program

© 2014 National Association of Insurance Commissioners

structure, keeping many participants out of the market.24 We discuss this element of the NFIP below.

Inefficiencies in the Administration of the WYO Program

The WYO program is the primary method the federal government uses to

market flood insurance coverage to property owners and to administer the claims associated with flood-related losses. As noted previously, the WYO program represents a public-private relationship in which private insurance companies write flood insurance coverage, while the federal government bears the underwriting risk associated with the policies. The WYO program has been instrumental in providing policies to property owners, but some critics have argued that the WYO program has several inefficiencies that cause further financial strain on the NFIP. One of the biggest concerns is that, according to some sources, the WYO participants (i.e., private market insurance companies) are overcompensated for the services that they provide. A 2009 GAO report concluded that some of the problems that exist in the WYO program include: 1) FEMA did not know what proportion of payments going to WYO participants were necessary to cover expenses versus what proportion represented insurer profit; 2) FEMA did not ensure that WYO participants complied with the NFIP requirements; and 3) FEMA’s bonus structure was not aligned with long-term goals of the NFIP. It is seemingly in the best interest of the federal government to continue this relationship with the insurance industry, as it allows the industry greater exposure and experience in the flood insurance market while also providing policyowners with potentially more responsive service than would be received otherwise. However, given the current financial strains the NFIP faces, it is clear that one source of potential improvement would be to focus on the manner in which WYO participants are compensated, while recognizing that one of the largest WYO participants, writing nearly 8% of all flood insurance policies (see Table 3),

24. It should be noted that there is a private market for flood insurance in the U.S., although

the market is small relative to the total U.S. flood market, and coverage is typically limited to dwellings and businesses with values that exceed NFIP limits. Browne and Halek (2010) indicate that the private insurance market accounts for 50,000 to 75,000 voluntarily placed flood insurance policies, while the NFIP accounts for more than 5 million policies. While insurers do offer this excess coverage, evidence suggests that consumers do not typically take advantage of this option. The relatively low take-up rate is likely due to a number of factors, including lack of availability of coverage, cost and consumer preference. As Wells noted (2006), excess coverage is offered on a voluntary basis, and many insurers that offer this coverage are reluctant to offer the coverage in those areas that are likely to be most affected by floods. Additionally, some consumers may prefer to either select the coverage that will satisfy their bank’s minimum requirements or opt for the least costly coverage. Finally, it is possible that some agents do not inform insureds of the existence of excess coverage. For instance, following Hurricane Katrina, there were several errors and omissions claims against insurance agents asserting that agents failed to disclose the existence of this coverage to consumers (Wells, 2006).

Journal of Insurance Regulation

© 2014 National Association of Insurance Commissioners

recently withdrew from the market.25 This suggests that the fears of carrier overcompensation may be unfounded or that program requirements may act as a deterrent for some private insurers.

Recent NFIP Legislation

The Biggert-Waters Flood Insurance Reform and Modernization Act of 2012

The Biggert-Waters Act is the largest single legislative reform to the NFIP since its inception (Lehrer, 2013). The Biggert-Waters Act was passed in an effort to reduce the federal government’s subsidization of flood insurance and, ultimately, reduce the financial strain of the NFIP on taxpayers.26 As discussed briefly above, the Biggert-Waters Act introduced numerous changes to the NFIP. Notably, premium subsidies for “second homes, business properties, severe repetitive loss properties or substantially improved/damaged properties” were to be phased out until premiums reflected actuarially fair rates (NAIC, 2012); premiums for new policies needed to be actuarially fair; and the cap on premium increases had been increased from 10% to 20% per year for all properties except those mentioned above (which were allowed to increase up to 25% per year). Additionally, the Biggert-Waters Act mandated FEMA to create new flood maps, which would help determine the rate structure and rate changes for the NFIP. The Biggert-Waters Act also allowed the NFIP to purchase reinsurance from private reinsurers in order to reduce the financial strain of the NFIP on taxpayers.

As previously mentioned, the Biggert-Waters Act mandated that premiums for new policies be actuarially sound. In effect, this allowed current property owners to continue to benefit from significant subsidies in some cases, while delaying the imposition of new, actuarially fair rates until the subsidies were gradually phased out or until the title to the property changed hands. This provision most affected pre-FIRM primary residences because flood insurance subsidies are concentrated in these properties. The effect of this policy change was potential disruption in the real estate market, which was an important major consideration in the eventual passage of the Homeowner Flood Insurance Affordability Act (discussed below).

While the Biggert-Waters Act also authorized or mandated numerous other changes to the NFIP and FEMA, the changes listed above, which may have had the greatest impact on the NFIP’s future, were especially important to the

25. In August 2013, Travelers announced its intention to withdraw from the flood insurance

market, describing it as “… a small, non-core part of our business” while noting that “… exiting the program eliminates the operational complexity associated with maintaining separate underwriting and claim processes required for participating.” (Insurance Journal, 2013).

26. Subsidies are largely concentrated among pre-FIRM primary residences and in high-risk and undetermined-risk areas (FEMA, 2013b).

The State of the National Flood Insurance Program

© 2014 National Association of Insurance Commissioners

U.S. private insurance market. Since before the NFIP’s inception, there has been no stable private insurance market for flood coverage in the U.S. One of the primary reasons given for the lack of a private market is that insurance cannot generally cover catastrophic risks. However, private insurance coverage has been available for hurricanes, earthquakes, tornadoes and other catastrophic perils for decades. So, perhaps more importantly than the flight from catastrophe risk, private insurers have not been present in the flood insurance market because of premium subsidies the NFIP provided to consumers. By phasing out premium subsidies and increasing rates on many of the NFIP’s insureds, it was believed that the Biggert-Waters Act may have eventually created a path for private insurers to enter and compete in the U.S. flood insurance market.

While private entities in the U.S. sell some flood insurance each year, there has not been a stable flood insurance market for individuals, families and small businesses since the passage of the NFIA. With the passage of the Biggert-Waters Act in 2012, a private insurance market began to emerge. Reports indicated that some private insurers established initial markets in Florida, Connecticut and other states (Scism, 2014; Singer, 2014).

Reaction to the Biggert-Waters Act

Following the passage of the Biggert-Waters Act, legislators and insurance industry representatives both praised its passage as it would finally provide for a long-term extension of the NFIP after four years of short-term extensions. Additionally, subsidies would be phased out, which would reduce the financial strains on the program. However, as implementation of the Biggert-Waters Act began, it became apparent that some property owners would experience significant increases in flood insurance rates, in some instances as high as 3,000% (Pettus, 2013). The Biggert-Waters Act sheltered some properties from drastic rate increases through “grandfathering,” but properties that were sold were subject to the full (unsubsidized) rates. Some believed the rate increases could adversely affect the housing market in flood-prone areas by stifling demand for high-risk homes. The loss of such subsidies could substantially affect a purchaser’s valuation of a property. For instance, Harrington (2013) notes one scenario in which a home could be sold, and the annual flood insurance premium could increase from $1,400 to $9,500—an increase of more than 6.5 times the original premium. With uncertainty surrounding the future of premium subsidies in the NFIP and the knowledge that flood insurance rates for many properties could increase substantially, the potential existed for property purchasers to demand lower real estate prices to account for an expected increase in annual flood insurance premiums.27

27. There is evidence linking risk of catastrophic damage to home value in prior literature.

Dumm, Sirmans, and Smersh (2011) find that homes in coastal regions of Florida sell for significantly higher values if the homes are built to withstand stronger natural disasters (e.g., hurricanes and windstorms).

Journal of Insurance Regulation

© 2014 National Association of Insurance Commissioners

While property-owners voiced concern regarding the potential rate increases, the uncertainty surrounding these increases could also directly affect insurers. Some consumers would likely attribute the imposition of the NFIP’s new rates that the Biggert-Waters Act mandated to the WYO insurers that issue and service the policies. Anticipated negative reactions resulting from dramatic rate increases may have induced some insurers to consider reducing their participation in the WYO program.28

Given the strong response from property owners and other stakeholders, many legislators pushed to have the Biggert-Waters Act repealed or delayed.29 As additional fallout, Mississippi filed a lawsuit against FEMA arguing that the rate increases were excessive and resulted from the use of inaccurate data. Several states—including Alabama, Florida, Louisiana, Massachusetts and South Carolina—supported the Mississippi suit through “friend of the court” briefs (Postal, 2013).

The Homeowner Flood Insurance Affordability Act of 2014

As a result of the concerns about the potential immediate impact that the

Biggert-Waters Act could have on property owners, Congress substantially modified the Biggert-Waters Act through the passage of the Homeowner Flood Insurance Affordability Act of 2014 (HFIA Act).30 Under the HFIA Act, the immediate premium increases that the Biggert-Waters Act required are ameliorated for some policyholders. For pre-FIRM primary residences receiving subsidies, annual premium increases are subject to a minimum of 5% and a maximum of 18%, as opposed to the 25% immediate annual increases that Biggert-Waters imposed. The changes to older pre-FIRM non-primary residences, business properties and severe repetitive loss properties are mostly unaffected by the HFIA Act; these properties will continue to experience potential dramatic premium increases (as required by the Biggert-Waters Act) until actuarially sound rates are achieved. Additionally, while the Biggert-Waters Act called for new policies to be charged the “full risk rate,” the HFIA Act repeals that provision and allows property owners to purchase new policies at the subsidized rates (Simpson, 2014b). These rates will continue while the NFIP develops new guidelines (FEMA, 2014c). To help support subsidies for high-risk properties, all policyholders in the NFIP will now pay a surcharge—$25 for primary residential properties and $250 for commercial or secondary residential properties—to a reserve fund (Simpson, 2014b). Each of the aforementioned components of the

28. We thank an anonymous reviewer for this insight. 29. This strong reaction from those with subsidized policies is consistent with the findings

of Landry and Jahan-Parvar (2011), who report that property owners with subsidized flood insurance coverages are much more sensitive to changes in the price of insurance.

30. The HFIA Act was signed into law by President Barack Obama on March 21, 2014 (Hofmann, 2014).

The State of the National Flood Insurance Program

© 2014 National Association of Insurance Commissioners

HFIA Act delays the rate increases that were initially intended to allow the NFIP to more directly address the financial problems that have plagued the program.

While the provisions noted above have been some of the most commonly discussed, several other important provisions that relate to the program’s rate structure are also found in the HFIA Act. For example, property-specific mitigation features that are not part of the insured structure are allowed to be considered when setting rates. The HFIA Act also encourages FEMA to offer coverage such that the premium is no greater than 1% of the total coverage, and FEMA must report to Congress those cases where the premium exceeds 1% of the coverage amount (Postal, 2014).31 In addition, the HFIA Act mandates new mapping and affordability studies (FEMA, 2014c). Finally, a provision for refunds to certain policyholders is created, where refunds apply to those paying the full-risk rate after July 6, 2012, and may apply to others who renewed their policies after the HFIA Act was enacted and experienced premium increases of greater than 18% (FEMA, 2014c). While the HFIA Act did not undo all of the changes to the NFIP that the Biggert-Waters Act initiated, it repealed the removal of premium subsidies for primary homeowners and the reduction in rate increases for many property-owners. Thus, the HFIA Act nullifies the largest (and arguably most significant) changes contained within the Biggert-Waters Act and represents a liability for taxpayers because the NFIP will revert to a subsidized and insufficient premium structure. However, the HFIA Act will help bolster real estate markets in coastal and flood-prone areas and likely provides immediate relief to the real estate market for pre-FIRM primary residences. Additionally, as a result of halting or delaying insurance premium increases, the HFIA Act may increase the value of coastal homes, leading to a larger property tax base for local communities.

In addition to legislative efforts to alter and repeal provisions found in the Biggert-Waters Act, several states have begun to discuss whether the federal flood insurance market is the most effective method to provide flood insurance to property owners or whether some other options beyond the federal market should be considered. For example, the West Virginia House of Representatives passed legislation to lessen the effects of the Biggert-Waters Act on property owners, creating a private market option to allow insureds to purchase coverage limits equal to their mortgage balance rather than replacement cost of the dwelling (Associated Press, 2014). The Florida Senate also recently passed a bill that attempts to encourage a private flood insurance market, and some insurers have begun selling flood insurance in Florida’s admitted market (Elmore, 2014).32 With more than 2 million NFIP policies in force, Florida represents the largest potential private insurance market for the flood risk.

While some legislators, property owners and special interest groups argued in favor of the repeal or delay of the provisions in the Biggert-Waters Act, insurers

31. For example, if a residential property has a NFIP policy with a $250,000 limit, the

annual premium should be no greater than $2,500. 32. At of the time of this writing, the Florida House of Representatives is considering a

companion bill.

Journal of Insurance Regulation

© 2014 National Association of Insurance Commissioners

appeared to favor the Biggert-Waters Act and the move to reduce and/or eliminate the subsidies that are provided to the highest risk properties. The HFIA Act allowed some, but not all, of the subsidies to remain in place, at least temporarily. As discussed previously, several major hurdles must be overcome before insurers are comfortable offering flood insurance and assuming the underwriting risk associated with the flood line of business. While the Biggert-Waters Act did not eliminate all of those hurdles, it did open the door for private insurers to eventually enter the market and offer coverage at an actuarially fair rate. The HFIA Act slows the implementation of the subsidy phase-out, but it continues a path for private insurers to enter the market. Without the removal of the subsidies that are currently available to high-risk property owners in the federal flood insurance program, private insurers are unlikely to enter the flood market to any significant degree.

Proposed Changes to the U.S. Flood Insurance Market

Given the recent pushback due to the passage of the Biggert-Waters Act,

several potential solutions to the issue of flood insurance in the U.S. have been offered, with some of the recommendations moving away from the federal program that has been in place over the past 50 years. Below we detail some of the recommendations that have been proposed.

Increased Involvement by the Private Insurance Market

One potential solution that legislators and insurance regulators have offered is increased involvement by the private insurance market. As mentioned previously, the federal government underwrites the majority of flood insurance policies, and most private insurers are only involved in the marketing and claims settlement process. It has been reported that the Florida Office of Insurance Regulation has been in discussions with private insurers to encourage them to write flood coverage outside of the NFIP system (Klas, 2013). However, this plan could be at risk; while some insurers have shown interest in entering the flood insurance market, a recent GAO report suggests that the rate increases associated with the Biggert-Waters Act are necessary for insurers to enter the market (Government Accountability Office, 2014). The report suggests that in addition to increased rates, private insurers would be more inclined to enter the market if the federal government provided coverage for those properties that the private market did not

The State of the National Flood Insurance Program

© 2014 National Association of Insurance Commissioners

want to insure and/or the federal government served a role as a reinsurer for flood-related losses.33

There is precedent for the government acting as a reinsurer to a private insurance market reluctant to sell catastrophic risks policies. At the federal level, the Terrorism Risk Insurance Act provides reinsurance against catastrophic loss from terrorism losses, allowing the private market to confidently continue to offer coverage (Kunreuther and Pauly, 2005). At the state level, Florida administers the Florida Hurricane Catastrophe Fund, which was established after Hurricane Andrew in 1993 to provide state-backed reinsurance to Florida property insurers (Harrington and Niehaus, 2001). Insurers have also indicated that regulators would need to provide insurers with flexibility in ratemaking. They argue that this flexibility would be necessary as there is not sufficient data to ensure that calculated rates are appropriate.

A private flood insurance market would help alleviate some of the federal government’s (and, ultimately, the taxpayers’) liability for future flood events by allowing insurers to charge risk-based premiums to high-risk homeowners. A private insurance market could also help homeowners with home values above the NFIP’s $250,000 coverage limit find single-insurer coverage, allow homeowners to insure their dwelling on a replacement cost rather than actual cash value basis, and increase the flexibility in flood insurance policy conditions (Browne and Halek, 2010).

Creation of a State Insurance Pool

Another option that legislators have mentioned as an alternative to federal flood insurance coverage is the creation of state insurance pools, which will act as insurers of last resort for property owners. This idea has been practiced in Florida through the Citizens Property Insurance Corporation. Originally, Citizens’ goal was that the state insurance pool would act as an insurer of last resort for those homeowners with the highest risk of hurricane damage. Similarly, state-run flood insurance pools could provide coverage at rates lower than those the NFIP provides (Bacchus, 2013). However, if it is believed that the NFIP’s rates are already below actuarially fair levels, the creation of an insurer that will offer even lower rates might only act to transfer future financial losses associated with underpricing from the federal government to the states. Some legislators question the validity of this concern, noting that over the past 20 years, Floridians paid

33. With the NFIP’s continued reliance on subsidized rates, one potential outcome is that

insurers could cherry-pick the lower-risk properties and then allow the high-risk properties to remain with the NFIP. Some argue that this is currently the case, and that those carriers that are currently writing private market flood coverage only write coverage for high-valued properties that face a low risk of flood loss (Jacobs, 2014). However, others argue that even if carriers were to try to cherry-pick in the flood market, it could prove difficult as property owners that face a low or moderate risk of flood loss may be less likely to demand coverage because they are less likely to face a loss (Friedman and Singh, 2014).

Journal of Insurance Regulation

© 2014 National Association of Insurance Commissioners

$16 billion in premiums to the NFIP but received less than $4 billion in claims payments (Klas, 2013).

Use of Long-Term Property Insurance Coverage

Another alternative that researchers have offered is the creation of long-term property insurance coverage tied to specific properties. Specifically, Jaffee, Kunreuther and Michel-Kerjan (2010) propose the use of long-term property insurance contracts that are attached to the property, and they directly address the role that long-term contracts could have in the flood insurance market. Under the arrangement that Jaffee et al. discussed (2010), the NFIP contract would either have a fixed premium for the entire policy term (with a term lasting between five and 20 years) or an adjustable premium where the policy is guaranteed renewable. The policy would be attached to the property, regardless of who the owner is. The authors also argue that the NFIP could offer a loan program that would be used to fund property mitigation projects, which would ultimately reduce flood losses in the future. The authors contend that this type of long-term arrangement would reduce insurance premium volatility and would also encourage property owners to invest in protection against flood losses for the property.

Maintain the Status Quo A final option that legislators across the U.S. have discussed is to simply

repeal (or partially repeal) the Biggert-Waters Act or delay the provisions found in the legislation. Given the recent passage of the HFIA Act, this option is clearly one preferred route for addressing the difficult issues associated with the NFIP. As noted previously, the passage of the HFIA Act effectively allows for some rate increases, but subsidies still remain in effect.34 The passage of the HFIA Act could have an adverse effect by inhibiting private insurer involvement in the flood insurance market, as many insurers have publicly stated they would be less inclined to enter the flood insurance market because the problems that have caused insurers to avoid the market would still remain. A recent GAO (2014) report acknowledged the potential effects of a delay or repeal of the Biggert-Waters Act by stating that such action “… may reinforce private insurers’ skepticism that they would ever be permitted to charge adequate rates and make their participation unlikely in the foreseeable future.” Although it was known that such an action would likely stall efforts to increase the level of private insurer involvement in the flood market and would do little to improve the NFIP’s current financial status, passage of the HFIA Act was largely viewed as politically wise for those legislators with constituents who are located in high-risk locations. This development indicates that the status quo is likely to remain, and it may be largely dependent on state government (rather than federal government) to take measures

34. The HFIA accounts for the subsidies by charging all property owners a $25 annual

assessment for primary residences and $250 for other properties (Simpson, 2014b).

The State of the National Flood Insurance Program

© 2014 National Association of Insurance Commissioners

necessary to increase the level of active involvement by the private insurance market.

Conclusion The private insurance market has long characterized the U.S. flood insurance

market as uninsurable. This long-held belief is primarily attributable to the relatively common frequency with which major flood events occur in the U.S., the presence of significant adverse selection in the market, moral hazard created and sustained by the financing function provided through the NFIP, and evidence that suggests that the most at-risk property owners are unwilling to pay an actuarially fair rate. Because of the absence of profit-making conditions, the private market has mostly been unwilling to enter the market, and the federal government has underwritten coverage for flood losses through the NFIP. While the NFIP has been effective in delivering flood insurance to those property owners that demand coverage, the last decade has proven to be difficult for the NFIP as budget deficits have reached record levels, while premiums remain artificially low and property development continues in flood-prone regions.

Given the financial and operational challenges that the NFIP has faced over the past decade, successful solutions will require an understanding of how the federal flood insurance market developed, how it currently operates, the problems that it currently faces, and the alternatives that have been proposed to make the program viable for the long-term. The evidence suggests that while the program has been operating for decades, the significant increase in catastrophic flood-inducing events and the continued property development in flood-prone areas make it incredibly difficult for the NFIP to remain viable in its current form. With the program currently more than $24 billion in debt, legislators will need to make difficult decisions regarding the overall financial structure of the program if it is to survive and operate without additional borrowing. While opinions vary with regards to the methods that should be used to improve the financial position of the NFIP, ultimately regulators, insurers and legislators must continue to work together to either fix the current program or develop new market-based solutions to ensure that property owners in the future will have access to this necessary coverage.

Journal of Insurance Regulation

© 2014 National Association of Insurance Commissioners

Appendix 2014 Write Your Own (WYO) Participants

A total of 84 insurers participated in the WYO program in 2014. WYO participant information for 2014 is obtained from the Federal Emergency Management Agency (www.fema.gov/wyo_company).

The State of the National Flood Insurance Program

© 2014 National Association of Insurance Commissioners

References Anderson, D.R., 1974. “The National Flood Insurance Program – Problems and

Potential,” Journal of Risk and Insurance, 41(4): 579–599. Associated Press, 2014. “W. Va. House OKs Private Flood Insurance Option,”

March 3, 2014. Bacchus, N., 2013. “Florida Looking for NFIP Alternatives,” Risk Management

Monitor, Oct. 14, 2013. Ballard, M., 2014. “House GOP Moves to Limit Flood Insurance Rate

Hikes,” The Advocate, accessed March 5, 2014, from http://theadvocate.com/home/8453786-125/house-gop-move-to-limit.

Browne, M. J. and R.E. Hoyt, 2000. “The Demand for Flood Insurance: Empirical Evidence,” Journal of Risk and Uncertainty, 20(3): 291–306.

Browne, M.J. and M. Halek, 2010. “Managing Flood Risk: The National Flood Insurance Program and Alternatives,” Public Insurance and Private Markets, American Enterprise Institute, Number 24900, Spring.

Carson, J.M., K.A. McCullough and D.M. Pooser, 2013. “Deciding Whether to Invest in Mitigation Measures: Evidence from Florida,” Journal of Risk and Insurance, 80(2): 309–327.

Dumm, R. E., G.S. Sirmans, and G. Smersh, 2011. “The Capitalization of Building Codes in House Prices,” Journal of Real Estate Finance and Economics, 42: 30-50.

Elmore, C., 2014. “State Lawmakers Pass Bill to Encourage Private Flood Insurance,” The Palm Beach Post, May 1, 2014.

Federal Emergency Management Agency (FEMA), 2011. “National Flood Insurance Program: Answers to Questions about the NFIP,” FEMA F-084/March 2011.

Federal Emergency Management Agency (FEMA), 2013a. “Biggert-Waters Flood Insurance Reform Act of 2013: Who Will Be Impacted by Rate Increases Nationally Under Section 205?”, accessed June 2, 2014 at www.fema.gov/media-library-data/20130726-1910-25045-4019/bw12_impact_fs_04092013_natl_508.pdf.

Federal Emergency Management Agency (FEMA). 2013b. “Changes to Flood Insurance Rates: What They Are and How to Explain Them,” accessed June 3, 2014, from www.fema.gov/media-library-data/1382115115666-0fba8b9a68fef69d546513c6da105bbe/BW12_AgentWhat_to_Know_Say_Sect205_Sept2013.pdf.

Federal Emergency Management Agency (FEMA), 2014a. “National Flood Insurance Program Summary of Coverage,” accessed March 3, 2014, at www.floodsmart.gov/toolkits/flood/downloads/NFIP-SummaryCoverage.pdf.

Federal Emergency Management Agency (FEMA), 2014b. “National Flood Insurance Program Summary of Coverage for Commercial Property,” accessed March 3, 2014, at www.floodsmart.gov/floodsmart/pdfs/NFIP_Summary_of_Coverage.pdf.

Journal of Insurance Regulation

© 2014 National Association of Insurance Commissioners

Federal Emergency Management Agency (FEMA), 2014c. “Homeowner Flood Insurance Affordability Act—Overview,” accessed June 2, 2014, at www.fema.gov/media-library-data/1396551935597-4048b68f6d695a6eb6e6e7118d3ce464/HFIAA_Overview_FINAL_03282014.pdf.

Frank, T., 2010. “Huge Losses Put Federal Flood Insurance Plan in the Red,” USA Today, Aug. 26, 2010.

Friedman, S.J. and A.U. Singh, 2014. “10 Models to Encourage Greater Private Market Participation in Flood Insurance,” Property Casualty 360°, April 18, 2014.

Garrison, T., 2014. “Flood Insurance Rate Hike Delay Passes House,” Housingwire, accessed March 6, 2014, from www.housingwire.com/articles/29186-what-will-happen-to-flood-insurance-reform-now.

Government Accountability Office (GAO), 2004. “National Flood Insurance Program: Actions to Address Repetitive Loss Properties,” GAO-04-401T.

Government Accountability Office (GAO), 2009. “Flood Insurance: Opportunities Exist to Improve Oversight of the WYO Program,” GAO-09-455.

Government Accountability Office (GAO), 2010. “National Flood Insurance Program: Continued Actions Needed to Address Financial and Operations Issues,” GAO-10-631T.

Government Accountability Office (GAO). 2013. “Flood Insurance: More Information Needed on Subsidized Properties,” GAO-13-607.

Government Accountability Office (GAO). 2014. “Flood Insurance: Strategies for Increasing Private Sector Involvement,” GAO-14-127.

Harrington, S.E. and G. Niehaus, 2001. “Government Insurance, Tax Policy, and the Affordability and Availability of Catastrophe Insurance,” Journal of Insurance Regulation, 19(4): 591–612.

Harrington, J., 2013. “Soaring Flood Insurance Rates Fuel Anxiety in Real Estate,” Tampa Bay Times, Sept. 10, 2013.

Hofmann, M.A., 2014. “Obama Signs Measure that Rolls Back Many 2012 Flood Insurance Reforms,” Business Insurance, March 21, 2014.

Insurance Journal, 2013. “Travelers to Exit NFIP’s Write-Your- Own Program,” accessed March 4, 2014, at www.insurancejournal.com/news/national/2013/08/23/302727.htm.

Jacobs, D., 2014. “Flood Fallout,” Greater Baton Rouge Business Report, accessed June 5, 2014, at http://businessreport.com/5142014/Flood-fallout.

Jaffee, D., H. Kunreuther, and E. Michel-Kerjan, 2010. “Long-Term Property Insurance,” Journal of Insurance Regulation, 167-187.

Kelly, M. and A.E. Kleffner, 2003. “Optimal Loss Mitigation and Contract Design,” Journal of Risk and Insurance, 70(1): 53–72.

King, R. O., 2005. “Federal Flood Insurance: The Repetitive Loss Problem,” Congressional Research Service, RL32972, June 30, 2005.

King, R. O., 2013. “The National Flood Insurance Program: Status and Remaining Issues for Congress,” Congressional Research Service, 7-5700, Feb. 6, 2013.

The State of the National Flood Insurance Program

© 2014 National Association of Insurance Commissioners

Klas, M.E., 2013. “State Looking into Alternatives to Federal Flood Insurance,” Miami Herald, Oct. 8, 2013.

Koba, M., 2014. “Flood Insurance Battle Reaching High-Water Mark,” CNBC, accessed March 5, 2014, at www.cnbc.com/id/101396047.

Kousky, C. and H. Kunreuther, 2013. “Addressing Affordability in the National Flood Insurance Program,” The Wharton School Working Paper # 2013-12.

Kriesel, W. and C. Landry, 2004. “Participation in the National Flood Insurance Program: An Empirical Analysis for Coastal Properties,” Journal of Risk and Insurance, 71(3): 405–420.

Kunreuther, H. and M. Pauly, 2005. “Terrorism Losses and All Perils Insurance,” Journal of Insurance Regulation, 23(4): 3–19.

Landry, C.E. and M. R. Jahan-Parvar, 2011. “Flood Insurance Coverage in the Coastal Zone,” Journal of Risk and Insurance, 78(2): 361–388.

Lehrer, E., 2013, “Strange Bedfellows: SmarterSafer.org and the Biggert-Waters Act of 2012,” Duke Environmental Law & Policy Forum, 23(2): 351–361.

Maloney, F. E., and D.C. Dambly, 1976. “The National Flood Insurance Program – A Model Ordinance for Implementation of its Land Management Criteria,” Natural Resources Journal, 16: 665–736.

Medders, L., K. McCullough, and V. Jager, 2011. “Tale of Two Regions: Natural Catastrophe Insurance and Regulation in the United States and the European Union,” Journal of Insurance Regulation, 171–196.

Michel-Kerjan, E.O., 2010. “Catastrophe Economics: The National Flood Insurance Program,” Journal of Economic Perspectives, 24(4): 399–422.

National Association of Insurance Commissioners, 2012. “Biggert-Waters Flood Insurance Reform and Modernization Act of 2012,” The Center for Insurance Policy and Research, accessed March 4, 2014, at www.naic.org/documents/cipr_overview_2012_flood_reauthorization.pdf.

Office of Inspector General, 2009. “FEMA’s Implementation of the Flood Insurance Reform Act of 2004,” OIG-09-45.

Pasterick, E.T., 1998. “The National Flood Insurance Program,” in Howard Kunreuther and Richard J. Roth, Sr. (eds.), Paying the Price: The Status and Role of Insurance Against Natural Disasters in the United States. Washington, DC: Joseph Henry Press.

Pettus, E.W., 2013. “Mississippi Insurance Chief Sues to Halt Flood Insurance Rates Hikes,” Insurance Journal, Sept. 19, 2013.

Postal, A.D., 2010. “State Farm Won’t Handle Claims for Flood Insurance Program,” Property Casualty 360°, June 7, 2010.

Postal, A.D., 2013. “Legal Paper Breaks Down Mississippi’s Arguments in NFIP Lawsuit,” Property Casualty 360°, Dec. 23, 2013.

Postal, A.D., 2014. “Senate Passes House NFIP Rate-Hike Delay; Bill Goes to President,” Property Casualty 360°, March 18, 2014.

Risk Management Solutions, 2007. “The 1927 Great Mississippi Flood: 80-Year Retrospective,” RMS Special Report.

Scales, A.F., 2006. “Nation of Policyholders: A Governmental and Market Failure in Flood Insurance,” Mississippi College Law Review, 26(3): 3–46.

Journal of Insurance Regulation

© 2014 National Association of Insurance Commissioners

Scism, L., 2014. “Private Insurers Start to Offer Flood Coverage,” The Wall Street Journal, Feb. 25, 2014.