j.p. morgan -tata steel ltd

DESCRIPTION

J.P. Morgan -Tata Steel LtdTRANSCRIPT

www.jpmorganmarkets.com

Asia Pacific Equity Research15 May 2014

Tata Steel LtdOverweightTISC.BO, TATA IN

Near-term hiccups (Odisha) aside, cyclical upturn in key markets (Europe, India) in place; remain OW and increase PT

▲

Price: Rs452.35

Price Target: Rs620.00Previous: Rs550.00

India

Metals & Mining

Pinakin Parekh, CFA AC

(91-22) 6157-3588

Bloomberg JPMA PAREKH <GO>

J.P. Morgan India Private Limited

Dinesh S. Harchandani, CFA

(91-22) 6157-3583

J.P. Morgan India Private Limited

Neha Manpuria

(91-22) 6157-3589

J.P. Morgan India Private Limited

Daniel Kang

(852) 2800 8570

J.P. Morgan Securities (Asia Pacific) Limited

YTD 1m 3m 12mAbs 6.2% 10.6% 22.0% 48.8%Rel -6.5% 4.7% 5.1% 28.0%

Tata Steel Ltd (Reuters: TISC.BO, Bloomberg: TATA IN)

Rs in bn, year-end Mar FY12A FY13A FY14E FY15E FY16ENet Sales (Rs bn) 1,329 1,347 1,387 1,473 1,615Net Profit (Rs bn) 52 (72) 32 59 78EPS (Rs) 51.45 (71.39) 31.17 57.96 76.85Net Profit growth (%) (41.9%) (238.7%) (143.7%) 85.9% 32.6%ROE 12.1% (17.4%) 8.3% 14.2% 16.6%P/E (x) 8.8 NM 14.5 7.8 5.9P/BV (x) 1.0 1.2 1.2 1.0 0.9EV/EBITDA (x) 7.5 8.2 6.9 5.9 4.9Source: Company data, Bloomberg, J.P. Morgan estimates.

Company Data52-week Range (Rs) 454.70-195.30Market Cap (Rs mn) 458,597Market Cap ($ mn) 7,686Price (Rs) 452.35Date Of Price 14 May 143M - Avg daily vol (mn) 6.333M - Avg daily val ($ mn) 40.5BSE30 2,3815.12Price Target (Rs) 620.00Price Target End Date 31-Mar-15

See page 13 for analyst certification and important disclosures, including non-US analyst disclosures.J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

150

250

350

450

Rs

May-13 Aug-13 Nov-13 Feb-14 May-14

Price Performance

TISC.BO share price (Rs)

BSE30 (rebased)

TATA reported another strong beat in Q4, this time driven by India. We roll forward our PT to FY16 estimates and remain OW with a revised March-15 PT of Rs620. Admittedly, near term there is the headwind of potential Odisha disruption(court order not yet out), but in our view with a new Government likely to be focused on economic growth, we do not see any disruption to be long lasting, as without Odisha iron ore, there is unlikely to be much steel available. TATA is well- positioned to benefit from demand improvement in both India and Europe with spare capacity available. Debt levels should come down post peak capex in FY15E. With steel spreads improving, we see upside risks to our Street-high EPS estimates. We would view any correction on negative news flow as a buying opportunity. Q4 wraps up a year of steadily improving earnings trend: Reported PAT

bear Rs10.2bn v/s cons at Rs9.4bn. Consol EBITDA stood at Rs50bn v/s cons at Rs45bn, driven by a large beat at India operations (EBITDA Rs41bn, and EBITDA/T at 7-quarter high of Rs17K/T). Implied TATA Europe EBITDA stood at ~$133mn and EBITDA/T at $33/t v/s JPMe at $43/t. We are not worried about the miss in EBITDA/T and would highlight the trend of reducing RM costs and stable steel prices point to further margin expansion ahead at Europe. TATA Europe FY14 EBITDA stood at ~Rs30bn

Odisha is an overhang but in our view any disruption should be short lived: The Supreme Court judgment is expected any day and admittedly there is increasing likelihood of some kind of disruption in Odisha (TATA sources ~75% of its iron ore from there). However, we believe it is likely to be short lived as: a) the key issue is of deemed extension which can be addressed by the Gov’t, and b) any prolonged disruption would sharply impact the broader economy, which the Govt would like to address

Cycle is improving in Europe, and should pick up in India; TATA well positioned given spare capacity: We expect the demand environment to pick up both in Europe and India. TATA Europe should continue to benefit from spread and volume expansion. JPM FY15E India EBITDA is at Rs14.9K/t(FY16E Rs13.9K/T) v/s Rs17K/T in Q4. TATA has capacity both in India (3MT expansion to flow through in FY16E) and Europe to benefit from cyclical demand pick up.

Net debt reduced q/q to Rs665bn v/s Rs693bn in Q3. FY14 capex stood at Rs165bn and TATA expects a similar amount in FY15 and reduce only in FY16.Key risks include a prolonged mining ban in India and slowdown in Europe.

2

Asia Pacific Equity Research15 May 2014

Pinakin Parekh, CFA(91-22) [email protected]

Key catalysts for the stock price: Upside risks to our view: Downside risks to our view:

• Continuing recovery in Europe demand• Stronger-than-expected Corus EBITDA/t• Ramp up of India EBITDA/t as it enters seasonally strong Q and price hikes flow through • Potential sale of non-core assets/investments

• Price hikes in Europe pushing EBITDA higher • India EBITDA/t better than expected from the new capacity • Limited capex, strong FCF at India to fund capex plans • INR depreciation, resulting in import substitution

and higher exports

• Muted domestic steel demand• Recovery in Europe appears short-lived • High leverage • Lower profitability of expansion given declining iron

ore linkage visibility

Key financial metrics FY13A FY14E FY15E FY16E Valuation and price target basis

Revenues (Rs Mn) 1,347,115 1,386,855 1,472,508 1,615,183 Our revised price target Mar-15 PT is Rs620, based on SOTP and we value the India operations at 5.7x, 5.0x for Asia and 6.0x for European operations FY16E EBITDA.

Revenue growth (%) 1% 3% 6% 10%EBITDA (Rs Mn) 123,212 160,167 190,756 218,101

EBITDA margin (%) 9% 12% 13% 14%Tax rate (%) 105% 51% 37% 32%

Net profit (Rs Mn) -72,375 31,602 58,756 77,909EPS (Rs) -71.4 31.2 58.0 76.8

EPS growth (%) 86% 33% TATA SOTP

DPS (Rs) 8.0 10.0 10.0 12.0

BVPS (Rs) 366.6 386.3 432.1 493.6Operating cash flow (Rs mn) 66,557 100,827 137,635 163,211

Free cash flow (Rs mn) -59,928 -54,150 -15,365 72,711Interest cover (X) 3.0 3.7 4.2 4.7

Net margin (%) -5% 2% 4% 5%Sales/assets (X) 0.9 0.9 0.9 0.9Debt/equity (%) 1.76 1.76 1.70 1.50

Net debt/equity (%) 1.47 1.65 1.54 1.23 ROE (%) 0% 8% 14% 17%

Key model assumptions FY13A FY14E FY15E FY16E

Domestic Volumes ('000 T) 7.5 8.5 9.2 10.7

Corus Volumes ('000 T) 13.0 13.8 14.5 15.5 Domestic EBITDA/t (Rs) 14,875 15,101 14,865 13,909

Corus EBITDA/t (USD) 13 35 54 62Source: J.P. Morgan estimates.

Source: Company and J.P. Morgan estimates.

Sensitivity analysis EBITDA EPS JPMe vs. consensus, change in estimates

Sensitivity to FY14E FY14E EPS FY14E FY15E

1% chg in India Volumes 0.4% 0.8% JPMe old 57.52 74.73

1% chg in Corus volumes 3.0% 7.0% JPMe new 58.0 76.81% chg in India ASP growth 1.3% 2.1% % chg 1% 3%

1% chg in Corus ASP growth 4.5% 13.1% Consensus 44.0 50.8

Source: J.P. Morgan estimates. Source: Bloomberg and J.P. Morgan estimates.

Rs bn Multiple FY15 EBITDA EVCorus 6.0 57.3 343.9India 5.7 148.8 848.0Asia 5.0 12.0 60.0Total EV 1,252Net Debt 617CWIP 34Pension Deficit 43Deriv ed Equity Value 626No of Shares (Mn) 1,014Target Price 620

3

Asia Pacific Equity Research15 May 2014

Pinakin Parekh, CFA(91-22) [email protected]

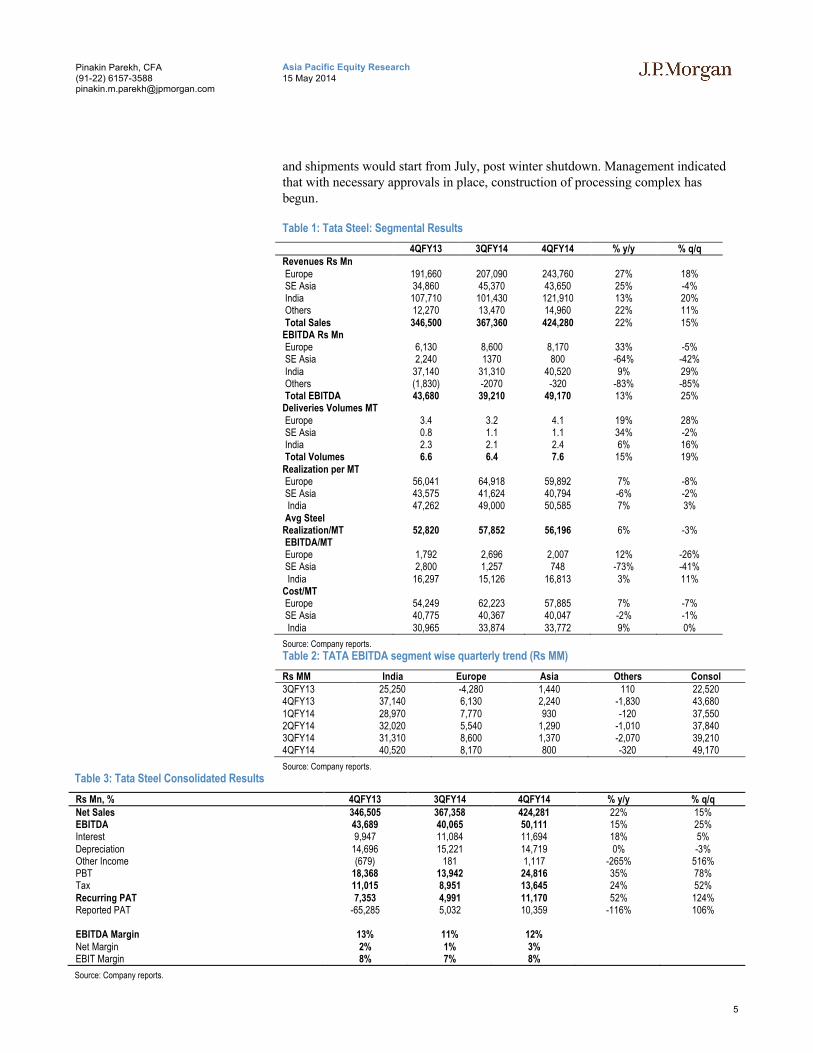

Q4 a strong beat driven by India as Europe misses slightly

TATA reported Q4 PAT (Rs10.2bn v/s consensus of Rs9.4bn) and EBITDA (Rs50bn v/s consensus of Rs45bn), which beat consensus estimates at the consolidated level, driven by large beat at India. Standalone EBITDA stood at Rs41bn and EBITDA/T stood at multi-quarter high of Rs17K/T. India volumes increased 6% y/y while ASP/T increased by ~3% q/q and implied cost/T declined. We are NOT building in Q4 India EBITDA to sustain in FY15, and our current forecast of EBITDA/T at Rs15K/t is significantly lower than Q4 levels.

TATA Europe was softer than expected, even as sales volumes were strong at 4.07Mt (+19% y/y). However, implied EBITDA/T stood at ~$33/T v/s JPMe at $43/T and 3QFY14 at $43/T. As a result, TATA Europe EBITDA at Rs8.17bn (-5% q/q) was lower than estimated. This was essentially driven by a sharp ~8% q/q decline in ASP/T, while implied costs/T declined ~7%. Some would view the miss in Europe as disappointing and question whether TATA is compromising in realizations in their quest for volumes. TATA highlighted that Q4 had some sale of semis, which impacted ASP/T and also highlighted that the impact of the lower raw material prices would flow through with a lag. We are not worried about the miss in Europe and would point to the trend of continuously improving operations in Europe with TATA able to sell higher volumes. TATA Europe reported EBITDA of ~Rs30bn in FY14, a multi-year high, and in our view with European demand improving and steel spreads holding out, we see the benefit of current steady steel prices and falling raw material costs to flow through in H1 FY15E in TATA Europe.

Asia operations were muted, but the EBITDA losses at the smaller units declined sharply.

FY14 capex stood at a multi-year high of Rs165bn (Rs95bn in India, Rs50bn at Europe, Rs17bn in mining projects) and TATA has guided to similar spending in FY15E with reduction in FY16E. From here, EBITDA should increase both at India and Europe, given a cyclical pick up while capex should reduce allowing for net debt reduction starting from FY16E.

The stock has run up sharply in sync with the broader markets and we would be buyers in corrections given the broadly improved economic outlook in Europe and expectations of a recovery in India.

Key Segment Highlights

India

India reported multi-quarter high EBITDA/t at Rs17K/t driven by: a) sharp increase in volumes (+19% y/y, +28% q/q) and improved realizations (+7% y/y, +3% q/). Management attributed the volume improvement (despite weak macroeconomic environment) to ramp up of 2.9mtpa expansion in 2HFY14. Improved product mix together with value-added products contributed to better realizations. Management

4

Asia Pacific Equity Research15 May 2014

Pinakin Parekh, CFA(91-22) [email protected]

noted that improved volumes have come mostly from domestic markets with exports making little contribution. Segment-wise, Autos & Special products sales increased 24% q/q and Industrial products sales increased 23% q/q. Branded Retail & Solution sales increased 10% q/q. For FY15, management guided to similar EBITDA/t as FY14’s average.

Europe

Despite reporting strong volume growth of 28% q/q, +19% y/y, Europe reported an EBITDA/t of $33/t vs. expectations of $43 and 3QFY14 at $43/t. Management attributed the lower sequential EBITDA/t to lower spreads during the quarter as well as higher sale of semis. Management noted that spreads had come down to $175 in 4Q vs. $190 in 3Q, with lower raw material prices impacting steel realizations. Management indicated that spreads should improve from current quarters as lower raw materials prices flow through. Realizations were down 7% q/q, 6% y/y. We are not worried about the miss in EBITDA/T and would highlight the trend of reducing RM costs and stable steel prices point to further margin expansion ahead at Europe. TATA Europe FY14 EBITDA stood at ~Rs30bn

SE Asia

SE Asia reported volumes of 1.07MT, increasing 34% y/y, a modest decline sequentially. EBITDA declined significantly to $13Mn, down 41% q/q and 69% y/y. Management noted the import pricing pressures in the region as well as political uncertainty in Thailand impacting operational performance. Management highlighted that key plant modernization and automation projects have been completed in Singapore. Together with restructuring of operations as well as optimization of variable costs at Thailand (through increased domestic scrap procurement), SE Asia should see improved operational performance going forward.

Debt

Net debt reduced q/q to Rs665bn v/s Rs693bn in Q3. FY14 capex stood at Rs165bn and TATA expects a similar amount in FY15. Management noted that debt should peak in FY15 as it incurs capex on its Kalinganagar project in Odisha. Post FY15, debt should come down. TATA also highlighted that they continue to evaluate non-core assets for monetization. Management also highlighted that major debt repayments are due at end of FY16. In order of preference, management noted that they prefer internal accruals, non-core asset sales and debt in that order.

Projects

KPO: Project work continues on track to commission by 4QFY15. TATA has so far spent Rs163.5bn on KPO, of which Rs80bn was spent in FY14. Management expects to incur most of the remaining ~Rs90bn capex in FY15. Management also indicated that they might invest in certain downstream projects in KPO plant to provide value-added products.

Benga Project, Mozambique: TATA noted that logistics issues and security concerns impacted production in 4QFY14. For FY14, 0.86MT of hard coking coal has been shipped with management targeting 1MT in FY15

Direct iron ore shipping project, Canada: Shipments of 240kt in FY14 with production of 1MT. Management noted that logistics infrastructure is now in place

5

Asia Pacific Equity Research15 May 2014

Pinakin Parekh, CFA(91-22) [email protected]

and shipments would start from July, post winter shutdown. Management indicated that with necessary approvals in place, construction of processing complex has begun.

Table 1: Tata Steel: Segmental Results

4QFY13 3QFY14 4QFY14 % y/y % q/qRevenues Rs MnEurope 191,660 207,090 243,760 27% 18%SE Asia 34,860 45,370 43,650 25% -4%India 107,710 101,430 121,910 13% 20%Others 12,270 13,470 14,960 22% 11%Total Sales 346,500 367,360 424,280 22% 15%

EBITDA Rs MnEurope 6,130 8,600 8,170 33% -5%SE Asia 2,240 1370 800 -64% -42%India 37,140 31,310 40,520 9% 29%Others (1,830) -2070 -320 -83% -85%Total EBITDA 43,680 39,210 49,170 13% 25%

Deliveries Volumes MTEurope 3.4 3.2 4.1 19% 28%SE Asia 0.8 1.1 1.1 34% -2%India 2.3 2.1 2.4 6% 16%Total Volumes 6.6 6.4 7.6 15% 19%

Realization per MTEurope 56,041 64,918 59,892 7% -8%SE Asia 43,575 41,624 40,794 -6% -2%

India 47,262 49,000 50,585 7% 3%Avg Steel

Realization/MT 52,820 57,852 56,196 6% -3%EBITDA/MT Europe 1,792 2,696 2,007 12% -26%SE Asia 2,800 1,257 748 -73% -41%

India 16,297 15,126 16,813 3% 11%Cost/MTEurope 54,249 62,223 57,885 7% -7%SE Asia 40,775 40,367 40,047 -2% -1%

India 30,965 33,874 33,772 9% 0%

Source: Company reports.

Table 2: TATA EBITDA segment wise quarterly trend (Rs MM)

Rs MM India Europe Asia Others Consol3QFY13 25,250 -4,280 1,440 110 22,5204QFY13 37,140 6,130 2,240 -1,830 43,6801QFY14 28,970 7,770 930 -120 37,5502QFY14 32,020 5,540 1,290 -1,010 37,8403QFY14 31,310 8,600 1,370 -2,070 39,2104QFY14 40,520 8,170 800 -320 49,170

Source: Company reports.

Table 3: Tata Steel Consolidated Results

Rs Mn, % 4QFY13 3QFY14 4QFY14 % y/y % q/qNet Sales 346,505 367,358 424,281 22% 15%EBITDA 43,689 40,065 50,111 15% 25%Interest 9,947 11,084 11,694 18% 5%Depreciation 14,696 15,221 14,719 0% -3%Other Income (679) 181 1,117 -265% 516%PBT 18,368 13,942 24,816 35% 78%Tax 11,015 8,951 13,645 24% 52%Recurring PAT 7,353 4,991 11,170 52% 124%Reported PAT -65,285 5,032 10,359 -116% 106%

EBITDA Margin 13% 11% 12%Net Margin 2% 1% 3%EBIT Margin 8% 7% 8%

Source: Company reports.

6

Asia Pacific Equity Research15 May 2014

Pinakin Parekh, CFA(91-22) [email protected]

Figure 1: TATA: Standalone 3QFY14 Results: QoQ Variation Figure 2: TATA: Consol 3QFY14 Results: QoQ Variation

Source: Company reports. Source: Company reports.

Figure 3: TATA's India Volume

Source: Company reports.

Figure 4: TATA's India EBITDA/MT (Rs/MT)

Source: Company reports.

Figure 5: TATA's Europe Volume

Source: Company reports.

Figure 6: TATA's Europe EBITDA/MT ($/MT)

Source: Company reports.

25%27%29%31%33%35%37%39%41%

15,000

20,000

25,000

30,000

35,000

40,000

45,000

India EBITDA (Rs MM) Margin

0%2%4%6%8%10%12%14%16%

0

10,000

20,000

30,000

40,000

50,000

60,000

Consol EBITDA (Rs MM) Margin

1.621.77

1.591.73

1.89

2.28

2.01 2.04 2.07

2.41

-5%0%5%10%15%20%25%30%35%

1.20

1.40

1.60

1.80

2.00

2.20

2.40

2.60

India Volume % Chg

16,218

16,92117,483

14,545

13,366

14,49814,136

14,40214,183

17,120

13,00013,50014,00014,50015,00015,50016,00016,50017,00017,50018,000

3QF

Y12

4QF

Y12

1QF

Y13

2QF

Y13

3QF

Y13

4QF

Y13

1QF

Y14

2QF

Y14

3QF

Y14

4QF

Y14

India (Rs/MT)

3.35

3.55

3.21

3.42

3.02

3.42

3.14

3.46

3.19

4.07

-20%-15%-10%-5%0%5%10%15%20%25%

3.00

3.20

3.40

3.60

3.80

4.00

4.20

Europe Volume % Chg

-44

8

35

-2

-26

3344

26

4333

-50-40-30-20-10

01020304050

3QF

Y12

4QF

Y12

1QF

Y13

2QF

Y13

3QF

Y13

4QF

Y13

1QF

Y14

2QF

Y14

3QF

Y14

4QF

Y14

Europe

7

Asia Pacific Equity Research15 May 2014

Pinakin Parekh, CFA(91-22) [email protected]

Figure 7: TATA's Consol Interest Expense and Int cover

Source: Company reports.

Figure 8: TATA's Overseas Interest Expense and Int cover

Source: Company reports.

Figure 9: Tata Steel India sales growth vs. India steel industry consumption growth

Source: Company reports, JPC India.

Figure 10: Tata Steel Consolidated tax rate trend (%)

Source: Company reports.

-1.00.01.02.03.04.05.06.07.08.0

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1QF

Y10

2QF

Y10

3QF

Y10

4QF

Y10

1QF

Y11

2QF

Y11

3QF

Y11

4QF

Y11

1QF

Y12

2QF

Y12

3QF

Y12

4QF

Y12

1QF

Y13

2QF

Y13

3QF

Y13

4QF

Y13

1QF

Y14

2QF

Y14

3QF

Y14

4QF

Y14

Consol Int Exp (Rs MM)- LHS Consol EBITDA/Int (x) - RHS

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

01,0002,0003,0004,0005,0006,0007,0008,000

1QF

Y10

2QF

Y10

3QF

Y10

4QF

Y10

1QF

Y11

2QF

Y11

3QF

Y11

4QF

Y11

1QF

Y12

2QF

Y12

3QF

Y12

4QF

Y12

1QF

Y13

2QF

Y13

3QF

Y13

4QF

Y13

1QF

Y14

2QF

Y14

3QF

Y14

4QF

Y14

Overseas Int (Rs MM) - LHS Overseas EBITDA/Int

-5%

0%

5%

10%

15%

20%

25%

30%

35%

3QFY12 4QFY12 1QFY13 2QFY13 3QFY13 4QFY13 1QFY14 2QFY14 3QFY14 4QFY14

TATA India Steel Consumption

27% 44%87%

0%83% 56%

-284%

60% 24% 32% 64% 55%

-400%

-300%

-200%

-100%

0%

100%

200%

300%

400%

Consol Tax rate

TATA has continued to grow

ahead of market in India over the

last seven quarters.

Consolidated tax rates continue to be volatile. 4Q tax rates were

impacted by an increase in tax in

TSI and reduction of deferred tax assets in TSE.

8

Asia Pacific Equity Research15 May 2014

Pinakin Parekh, CFA(91-22) [email protected]

Figure 11: Tata Europe Pension Surplus (GBP Mn)

Source: Company reports.

Figure 12: Tata Steel Consolidated Net Debt trend (Rsbn)

Source: Company reports.

Figure 13: Tata Steel FII and DII ownership trends

Source: BSE website

10690

211

38 34

78

283

428

242

301 298

0

50

100

150

200

250

300

350

400

450

Sep-11 Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14

Pension Surplus (GBP MM)

451

505477

540 552580

554

613643

701673

400

450

500

550

600

650

700

750

2QF

Y12

3QF

Y12

4QF

Y12

1QF

Y13

2QF

Y13

3QF

Y13

4QF

Y13

1QF

Y14

2QF

Y14

3QF

Y14

4QF

Y14

Net Debt Rsbn

20%

22%

24%

26%

28%

30%

10%

14%

18%

22%

Jun-

08

Sep

-08

Dec

-08

Mar

-09

Jun-

09

Sep

-09

Dec

-09

Mar

-10

Jun-

10

Sep

-10

Dec

-10

Mar

-11

Jun-

11

Sep

-11

Dec

-11

Mar

-12

Jun-

12

Sep

-12

Dec

-12

Mar

-13

Jun-

13

Sep

-13

Dec

-13

Mar

-14

FII - LHS DIIs - RHS

Pension surplus remained at

~GNP300MM

Net debt decreased during the

quarter despite additional borrowing of Rs41bn on account

of positive forex impact and

increase in cash.

Management expects debt to

peak in FY15 with its investment

in KPO and should decline from FY16 onwards.

9

Asia Pacific Equity Research15 May 2014

Pinakin Parekh, CFA(91-22) [email protected]

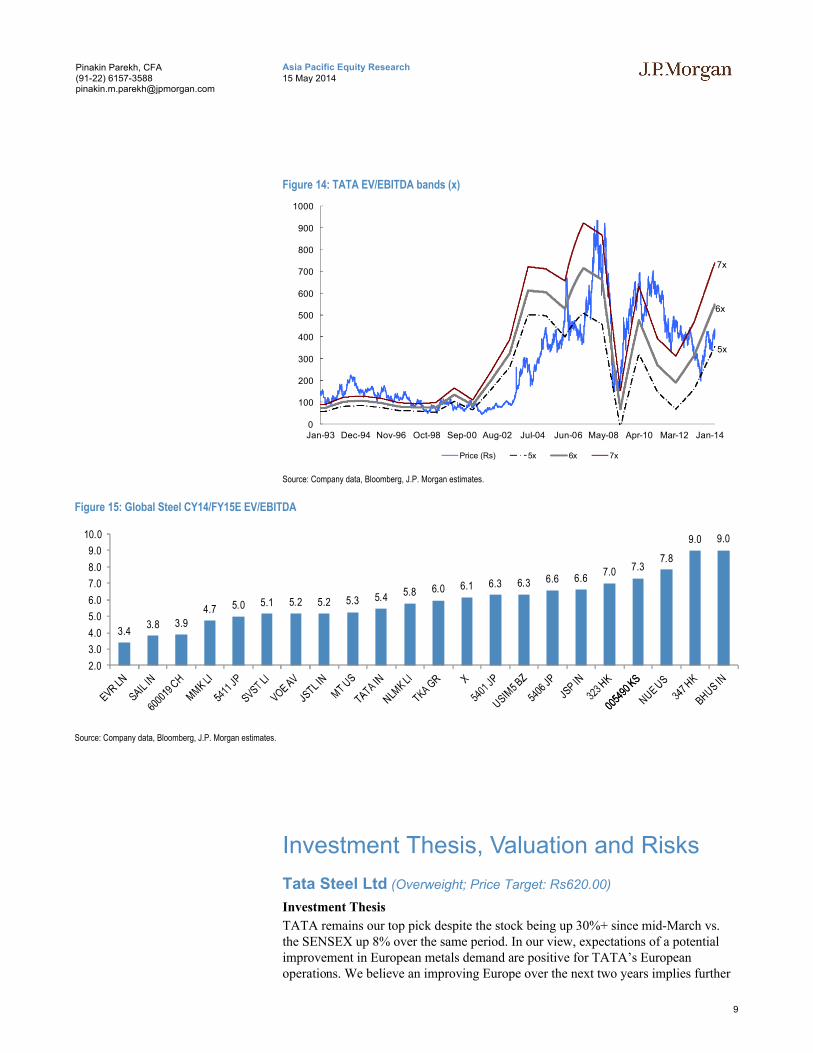

Figure 14: TATA EV/EBITDA bands (x)

Source: Company data, Bloomberg, J.P. Morgan estimates.

Figure 15: Global Steel CY14/FY15E EV/EBITDA

Source: Company data, Bloomberg, J.P. Morgan estimates.

Investment Thesis, Valuation and Risks

Tata Steel Ltd (Overweight; Price Target: Rs620.00)

Investment Thesis

TATA remains our top pick despite the stock being up 30%+ since mid-March vs. the SENSEX up 8% over the same period. In our view, expectations of a potential improvement in European metals demand are positive for TATA’s European operations. We believe an improving Europe over the next two years implies further

5x

6x

7x

0

100

200

300

400

500

600

700

800

900

1000

Jan-93 Dec-94 Nov-96 Oct-98 Sep-00 Aug-02 Jul-04 Jun-06 May-08 Apr-10 Mar-12 Jan-14

Price (Rs) 5x 6x 7x

3.43.8 3.9

4.7 5.0 5.1 5.2 5.2 5.3 5.4 5.8 6.0 6.1 6.3 6.3 6.6 6.67.0 7.3

7.8

9.0 9.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

10

Asia Pacific Equity Research15 May 2014

Pinakin Parekh, CFA(91-22) [email protected]

a re-rating of stock. In addition, we believe domestic demand should remain stable with limited new capacity addition from major players. Potential investment sales to de-lever could provide further upside.

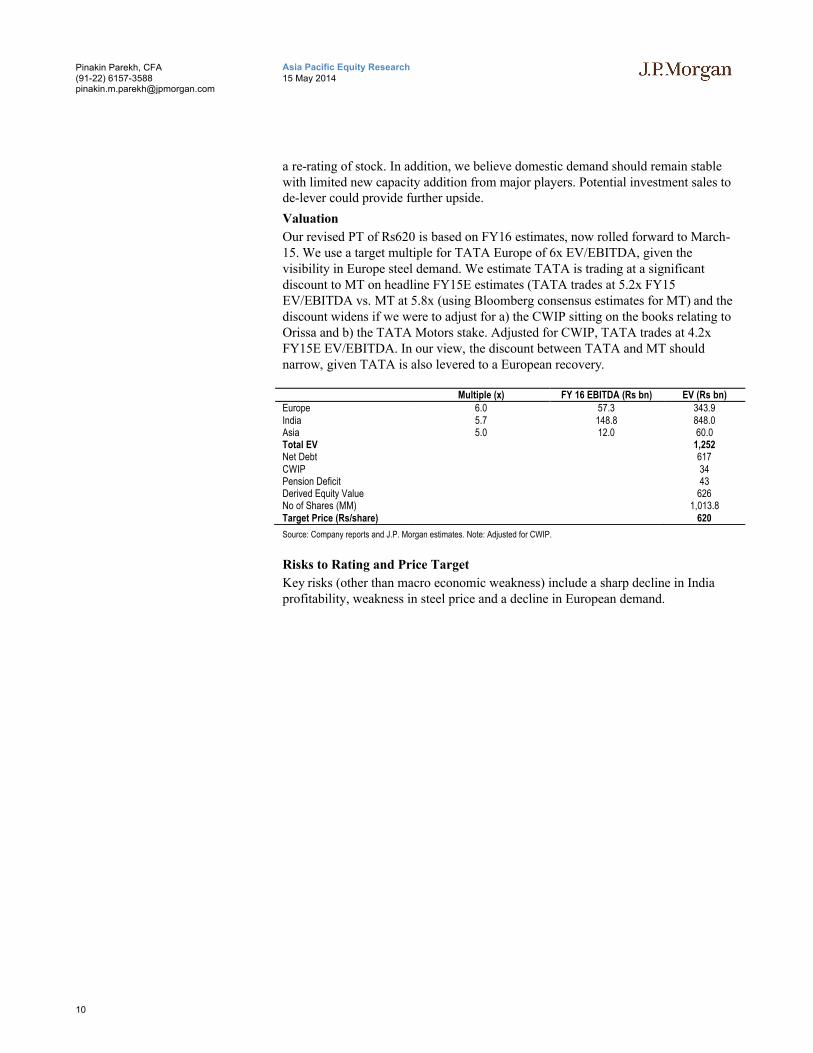

Valuation

Our revised PT of Rs620 is based on FY16 estimates, now rolled forward to March-15. We use a target multiple for TATA Europe of 6x EV/EBITDA, given the visibility in Europe steel demand. We estimate TATA is trading at a significant discount to MT on headline FY15E estimates (TATA trades at 5.2x FY15 EV/EBITDA vs. MT at 5.8x (using Bloomberg consensus estimates for MT) and the discount widens if we were to adjust for a) the CWIP sitting on the books relating to Orissa and b) the TATA Motors stake. Adjusted for CWIP, TATA trades at 4.2x FY15E EV/EBITDA. In our view, the discount between TATA and MT should narrow, given TATA is also levered to a European recovery.

Multiple (x) FY 16 EBITDA (Rs bn) EV (Rs bn)Europe 6.0 57.3 343.9India 5.7 148.8 848.0Asia 5.0 12.0 60.0Total EV 1,252Net Debt 617CWIP 34Pension Deficit 43Derived Equity Value 626No of Shares (MM) 1,013.8Target Price (Rs/share) 620

Source: Company reports and J.P. Morgan estimates. Note: Adjusted for CWIP.

Risks to Rating and Price Target

Key risks (other than macro economic weakness) include a sharp decline in India profitability, weakness in steel price and a decline in European demand.

11

Asia Pacific Equity Research15 May 2014

Pinakin Parekh, CFA(91-22) [email protected]

Tata Steel Ltd: Summary of FinancialsIncome Statement Cash flow statementRs in billions, year end Mar FY13 FY14E FY15E FY16E Rs in billions, year end Mar FY13 FY14E FY15E FY16E

Revenues 1,347 1,387 1,473 1,615 Net income (Pre exceptionals) (72) 32 59 78% change Y/Y 1.4% 2.9% 6.2% 9.7% Depr. & amortization 56 57 62 66

EBITDA 123 160 191 218 Change in working capital 9 12 17 19% change Y/Y (0.8%) 30.0% 19.1% 14.3% Cash flow from operations 67 101 138 163EBITDA margin 9.1% 11.5% 13.0% 13.5%

EBIT 67 103 129 152 Net Capex (126) (155) (153) (91)% change Y/Y (14.6%) 52.5% 25.0% 18.0% Free cash flow (60) (54) (15) 73

EBIT Margin 5.0% 7.4% 8.7% 9.4%Net Interest (37) (38) (35) (37) Equity raised/(repaid) (5) 0 0 0Earnings before tax 31 65 94 115 Debt raised/(repaid) 60 36 57 6

% change Y/Y (39.1%) 109.9% 44.8% 22.8% Other (52) (34) 0 0Tax (32) (33) (35) (37) Dividends paid (9) (12) (12) (16)

as % of EBT 105.0% 51.1% 37.2% 32.2% Beginning cash 108 99 35 64Net income (Pre exceptionals) (72) 32 59 78 Ending cash 99 35 64 127

% change Y/Y (238.7%) (143.7%) 85.9% 32.6% DPS 7.66 10.18 10.78 13.66Shares outstanding 1,014 1,014 1,014 1,014EPS (reported) (71.39) 31.17 57.96 76.85

% change Y/Y (238.7%) (143.7%) 85.9% 32.6%

Balance sheet Ratio AnalysisRs in billions, year end Mar FY13 FY14E FY15E FY16E Rs in billions, year end Mar FY13 FY14E FY15E FY16E

Cash and cash equivalents 99 35 64 127 EBITDA margin 9.1% 11.5% 13.0% 13.5%Short term investments 8 8 8 8 Operating margin 5.0% 7.4% 8.7% 9.4%Accounts receivable 140 86 91 98 Net margin (5.4%) 2.3% 4.0% 4.8%Inventories 241 290 283 296Others 55 55 55 55 Sales growth 1.4% 2.9% 6.2% 9.7%Current assets 542 473 500 583 Net profit growth (238.7%) (143.7%) 85.9% 32.6%

EPS growth (238.7%) (143.7%) 85.9% 32.6%Net fixed assets 692 790 881 905Total Assets 1,469 1,498 1,615 1,723 Interest coverage (x) 3.4 4.2 5.4 5.9

Net debt to total capital 58.5% 61.3% 59.7% 54.4%Liabilities Net debt to equity 147.1% 165.1% 153.9% 123.3%Short-term loans 191 191 191 191 Sales/assets 0.9 0.9 0.9 1.0Payables 218 269 281 317 Assets/equity 3.5 3.9 3.8 3.6Others 114 69 72 75 ROE (17.4%) 8.3% 14.2% 16.6%Total current liabilities 523 530 544 583 ROCE (0.3%) 4.8% 7.1% 8.4%Long-term debt 462 498 555 561Other liabilities 96 62 62 62Total Liabilities 1,081 1,089 1,161 1,206Shareholder's equity 372 392 438 500BVPS 366.56 386.28 432.10 493.58

Source: Company reports and J.P. Morgan estimates.

12

Asia Pacific Equity Research15 May 2014

Pinakin Parekh, CFA(91-22) [email protected]

JPM Q-ProfileTata Steel Limited (INDIA / Materials)As Of: 09-May-2014 [email protected]

Local Share Price Current: 399.95 12 Mth Forward EPS Current: 44.49

Earnings Yield (& local bond Yield) Current: 11% Implied Value Of Growth* Current: 19.27%

PE (1Yr Forward) Current: 9.0x Price/Book Value Current: 1.0x

ROE (Trailing) Current: -12.57 Dividend Yield (Trailing) Current: 2.00

Summary

Tata Steel Limited 6480.70 As Of:

INDIA 4.690946 SEDOL 6101156 Local Price: 399.95

Materials Metals & Mining EPS: 44.49

Latest Min Max Median Average 2 S.D.+ 2 S.D. - % to Min % to Max % to Med % to Avg12mth Forward PE 8.99x 1.77 15.39 7.93 7.98 12.44 3.52 -80% 71% -12% -11%P/BV (Trailing) 0.96x 0.38 5.01 1.89 2.01 4.16 -0.14 -60% 424% 98% 111%

Dividend Yield (Trailing) 2.00 1.18 10.40 2.66 2.94 5.90 -0.01 -41% 421% 33% 47%

ROE (Trailing) -12.57 -17.18 50.00 30.77 26.31 68.67 -16.06 -37% 498% 345% 309%

Implied Value of Growth 19.3% -3.46 0.57 0.03 -0.08 0.99 -1.14 -1895% 196% -84% -141%

Source: Bloomberg, Reuters Global Fundamentals, IBES CONSENSUS, J.P. Morgan Calcs * Implied Value Of Growth = (1 - EY/Cost of equity) where cost of equity =Bond Yield + 5.0% (ERP)

9-May-14

-60.00

-40.00

-20.00

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

Apr

/99

Nov

/99

Jun/

00

Jan/

01

Aug

/01

Mar

/02

Oct

/02

May

/03

Dec

/03

Jul/0

4

Feb

/05

Sep

/05

Apr

/06

Nov

/06

Jun/

07

Jan/

08

Aug

/08

Mar

/09

Oct

/09

May

/10

Dec

/10

Jul/1

1

Feb

/12

Sep

/12

Apr

/13

Nov

/13

0%

10%

20%

30%

40%

50%

60%

Apr

/99

Nov

/99

Jun/

00

Jan/

01

Aug

/01

Mar

/02

Oct

/02

May

/03

Dec

/03

Jul/0

4

Feb

/05

Sep

/05

Apr

/06

Nov

/06

Jun/

07

Jan/

08

Aug

/08

Mar

/09

Oct

/09

May

/10

Dec

/10

Jul/1

1

Feb

/12

Sep

/12

Apr

/13

Nov

/13

12Mth fwd EY India BY Proxy

0.00

100.00

200.00

300.00

400.00

500.00

600.00

700.00

800.00

900.00

1,000.00

Apr

/99

Nov

/99

Jun/

00

Jan/

01

Aug

/01

Mar

/02

Oct

/02

May

/03

Dec

/03

Jul/0

4

Feb

/05

Sep

/05

Apr

/06

Nov

/06

Jun/

07

Jan/

08

Aug

/08

Mar

/09

Oct

/09

May

/10

Dec

/10

Jul/1

1

Feb

/12

Sep

/12

Apr

/13

Nov

/13

-4.00

-3.50

-3.00

-2.50

-2.00

-1.50

-1.00

-0.50

0.00

0.50

1.00

1.50

Apr

/99

Nov

/99

Jun/

00

Jan/

01

Aug

/01

Mar

/02

Oct

/02

May

/03

Dec

/03

Jul/0

4

Feb

/05

Sep

/05

Apr

/06

Nov

/06

Jun/

07

Jan/

08

Aug

/08

Mar

/09

Oct

/09

May

/10

Dec

/10

Jul/1

1

Feb

/12

Sep

/12

Apr

/13

Nov

/13

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

18.0x

Apr

/99

Nov

/99

Jun/

00

Jan/

01

Aug

/01

Mar

/02

Oct

/02

May

/03

Dec

/03

Jul/0

4

Feb

/05

Sep

/05

Apr

/06

Nov

/06

Jun/

07

Jan/

08

Aug

/08

Mar

/09

Oct

/09

May

/10

Dec

/10

Jul/1

1

Feb

/12

Sep

/12

Apr

/13

Nov

/13

-1.0x

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

Apr

/99

Nov

/99

Jun/

00

Jan/

01

Aug

/01

Mar

/02

Oct

/02

May

/03

Dec

/03

Jul/0

4

Feb

/05

Sep

/05

Apr

/06

Nov

/06

Jun/

07

Jan/

08

Aug

/08

Mar

/09

Oct

/09

May

/10

Dec

/10

Jul/1

1

Feb

/12

Sep

/12

Apr

/13

Nov

/13

PBV hist PBV Forward

-30.00

-20.00

-10.00

0.00

10.00

20.00

30.00

40.00

50.00

60.00

Apr

/99

Nov

/99

Jun/

00

Jan/

01

Aug

/01

Mar

/02

Oct

/02

May

/03

Dec

/03

Jul/0

4

Feb

/05

Sep

/05

Apr

/06

Nov

/06

Jun/

07

Jan/

08

Aug

/08

Mar

/09

Oct

/09

May

/10

Dec

/10

Jul/1

1

Feb

/12

Sep

/12

Apr

/13

Nov

/13

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Apr

/99

Nov

/99

Jun/

00

Jan/

01

Aug

/01

Mar

/02

Oct

/02

May

/03

Dec

/03

Jul/0

4

Feb

/05

Sep

/05

Apr

/06

Nov

/06

Jun/

07

Jan/

08

Aug

/08

Mar

/09

Oct

/09

May

/10

Dec

/10

Jul/1

1

Feb

/12

Sep

/12

Apr

/13

Nov

/13

13

Asia Pacific Equity Research15 May 2014

Pinakin Parekh, CFA(91-22) [email protected]

Analyst Certification: The research analyst(s) denoted by an “AC” on the cover of this report certifies (or, where multiple research analysts are primarily responsible for this report, the research analyst denoted by an “AC” on the cover or within the document individually certifies, with respect to each security or issuer that the research analyst covers in this research) that: (1) all of the views expressed in this report accurately reflect his or her personal views about any and all of the subject securities or issuers; and (2) no part of any of the research analyst's compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed by the research analyst(s) in this report. For all Korea-based research analysts listed on the front cover, they also certify, as per KOFIA requirements, that their analysis was made in good faith and that the views reflect their own opinion, without undue influence or intervention.

Important Disclosures

Client: J.P. Morgan currently has, or had within the past 12 months, the following company(ies) as clients: Tata Steel Ltd.

Client/Non-Investment Banking, Securities-Related: J.P. Morgan currently has, or had within the past 12 months, the following company(ies) as clients, and the services provided were non-investment-banking, securities-related: Tata Steel Ltd.

Client/Non-Securities-Related: J.P. Morgan currently has, or had within the past 12 months, the following company(ies) as clients, and the services provided were non-securities-related: Tata Steel Ltd.

Investment Banking (next 3 months): J.P. Morgan expects to receive, or intends to seek, compensation for investment banking services in the next three months from Tata Steel Ltd.

Non-Investment Banking Compensation: J.P. Morgan has received compensation in the past 12 months for products or services other than investment banking from Tata Steel Ltd.

Company-Specific Disclosures: Important disclosures, including price charts, are available for compendium reports and all J.P. Morgan–covered companies by visiting https://jpmm.com/research/disclosures, calling 1-800-477-0406, or [email protected] with your request. J.P. Morgan’s Strategy, Technical, and Quantitative Research teams may screen companies not covered by J.P. Morgan. For important disclosures for these companies, please call 1-800-477-0406 or e-mail [email protected].

Date Rating Share Price (Rs)

Price Target (Rs)

21-Sep-07 N 654.72 740.00

15-May-08 N 881.90 800.00

11-Aug-08 N 651.20 740.00

29-Aug-08 N 600.35 690.00

17-Oct-08 N 269.75 290.00

03-Dec-08 N 164.70 155.00

29-Jun-09 N 397.15 415.00

03-Sep-09 N 416.45 425.00

30-Oct-09 N 467.65 475.00

15-Jan-10 N 645.15 605.00

14-Nov-10 N 606.95 665.00

14-Jan-11 OW 637.55 820.00

23-May-11 OW 559.40 785.00

09-Sep-11 OW 476.90 685.00

11-Nov-11 OW 429.85 630.00

03-Feb-12 OW 467.50 605.00

19-Jul-12 OW 411.65 590.00

14-Aug-12 OW 406.10 580.00

09-Nov-12 OW 390.55 530.00

14-Feb-13 OW 384.90 505.00

20-May-13 OW 315.35 530.00

16-Jul-13 OW 251.60 455.00

14-Aug-13 OW 241.40 500.00

14-Nov-13 OW 352.45 525.00

07-Feb-14 OW 361.25 550.00

0

254

508

762

1,016

1,270

1,524

Price(Rs)

Sep06

Mar08

Sep09

Mar11

Sep12

Mar14

Tata Steel Ltd (TISC.BO, TATA IN) Price Chart

N Rs690 N Rs475 OW Rs605OW Rs530OW Rs455OW Rs550

N Rs740N Rs155 N Rs425 OW Rs820OW Rs630OW Rs580OW Rs530OW Rs525

N Rs740N Rs800N Rs290 N Rs415N Rs605 N Rs665OW Rs785OW Rs685OW Rs590OW Rs505OW Rs500

Source: Bloomberg and J.P. Morgan; price data adjusted for stock splits and dividends.

Initiated coverage Sep 21, 2007.

14

Asia Pacific Equity Research15 May 2014

Pinakin Parekh, CFA(91-22) [email protected]

The chart(s) show J.P. Morgan's continuing coverage of the stocks; the current analysts may or may not have covered it over the entire period. J.P. Morgan ratings or designations: OW = Overweight, N= Neutral, UW = Underweight, NR = Not Rated

Explanation of Equity Research Ratings, Designations and Analyst(s) Coverage Universe: J.P. Morgan uses the following rating system: Overweight [Over the next six to twelve months, we expect this stock will outperform the average total return of the stocks in the analyst’s (or the analyst’s team’s) coverage universe.] Neutral [Over the next six to twelve months, we expect this stock will perform in line with the average total return of the stocks in the analyst’s (or the analyst’s team’s) coverage universe.] Underweight [Over the next six to twelve months, we expect this stock will underperform the average total return of the stocks in the analyst’s (or the analyst’s team’s) coverage universe.] Not Rated (NR): J.P. Morgan has removed the rating and, if applicable, the price target, for this stock because of either a lack of a sufficient fundamental basis or for legal, regulatory or policy reasons. The previous rating and, if applicable, the price target, no longer should be relied upon. An NR designation is not a recommendation or a rating. In our Asia (ex-Australia) and U.K. small- and mid-cap equity research, each stock’s expected total return is compared to the expected total return of a benchmark country market index, not to those analysts’ coverage universe. If it does not appear in the Important Disclosures section of this report, the certifying analyst’s coverage universe can be found on J.P. Morgan’s research website, www.jpmorganmarkets.com.

Coverage Universe: Parekh, Pinakin: ACC Limited (ACC.BO), Ambuja Cements Limited (ABUJ.BO), Coal India (COAL.BO), Grasim Industries Ltd (GRAS.BO), Hindalco Industries (HALC.BO), JSW Steel (JSTL.BO), NMDC (NMDC.NS), National Aluminium Co Ltd (NALU.BO), Sesa Sterlite (SESA.NS), Steel Authority of India Ltd (SAIL.BO), Tata Steel Ltd (TISC.BO), UltraTech Cement Ltd (ULTC.BO)

J.P. Morgan Equity Research Ratings Distribution, as of March 31, 2014

Overweight(buy)

Neutral(hold)

Underweight(sell)

J.P. Morgan Global Equity Research Coverage 44% 44% 11%IB clients* 58% 49% 40%

JPMS Equity Research Coverage 45% 48% 7%IB clients* 78% 67% 60%

*Percentage of investment banking clients in each rating category.For purposes only of FINRA/NYSE ratings distribution rules, our Overweight rating falls into a buy rating category; our Neutral rating falls into a hold rating category; and our Underweight rating falls into a sell rating category. Please note that stocks with an NR designation are not included in the table above.

Equity Valuation and Risks: For valuation methodology and risks associated with covered companies or price targets for covered companies, please see the most recent company-specific research report at http://www.jpmorganmarkets.com, contact the primary analyst or your J.P. Morgan representative, or email [email protected].

Equity Analysts' Compensation: The equity research analysts responsible for the preparation of this report receive compensation based upon various factors, including the quality and accuracy of research, client feedback, competitive factors, and overall firm revenues.

Registration of non-US Analysts: Unless otherwise noted, the non-US analysts listed on the front of this report are employees of non-US affiliates of JPMS, are not registered/qualified as research analysts under NASD/NYSE rules, may not be associated persons of JPMS, and may not be subject to FINRA Rule 2711 and NYSE Rule 472 restrictions on communications with covered companies, public appearances, and trading securities held by a research analyst account.

Other Disclosures

J.P. Morgan ("JPM") is the global brand name for J.P. Morgan Securities LLC ("JPMS") and its affiliates worldwide. J.P. Morgan Cazenove is a marketing name for the U.K. investment banking businesses and EMEA cash equities and equity research businesses of JPMorgan Chase & Co. and its subsidiaries.

All research reports made available to clients are simultaneously available on our client website, J.P. Morgan Markets. Not all research content is redistributed, e-mailed or made available to third-party aggregators. For all research reports available on a particular stock, please contact your sales representative.

Options related research: If the information contained herein regards options related research, such information is available only to persons who have received the proper option risk disclosure documents. For a copy of the Option Clearing Corporation's Characteristics and Risks of Standardized Options, please contact your J.P. Morgan Representative or visit the OCC's website at http://www.optionsclearing.com/publications/risks/riskstoc.pdf

Legal Entities Disclosures U.S.: JPMS is a member of NYSE, FINRA, SIPC and the NFA. JPMorgan Chase Bank, N.A. is a member of FDIC. U.K.: JPMorgan Chase N.A., London Branch, is authorised by the Prudential Regulation Authority and is subject to regulation by the Financial Conduct Authority and to limited regulation by the Prudential Regulation Authority. Details about the extent of our regulation by the Prudential Regulation Authority are available from J.P. Morgan on request. J.P. Morgan Securities plc (JPMS plc) is a member of the London Stock Exchange and is authorised by the Prudential Regulation Authority and

15

Asia Pacific Equity Research15 May 2014

Pinakin Parekh, CFA(91-22) [email protected]

regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Registered in England & Wales No. 2711006. Registered Office 25 Bank Street, London, E14 5JP. South Africa: J.P. Morgan Equities South Africa Proprietary Limited is a member of the Johannesburg Securities Exchange and is regulated by the Financial Services Board. Hong Kong: J.P. Morgan Securities (Asia Pacific) Limited (CE number AAJ321) is regulated by the Hong Kong Monetary Authority and the Securities and Futures Commission in Hong Kong and/or J.P. Morgan Broking (Hong Kong) Limited (CE number AAB027) is regulated by the Securities and Futures Commission in Hong Kong. Korea: J.P. Morgan Securities (Far East) Ltd, Seoul Branch, is regulated by the Korea Financial Supervisory Service. Australia: J.P. Morgan Australia Limited (JPMAL) (ABN 52 002 888 011/AFS Licence No: 238188) is regulated by ASIC and J.P. Morgan Securities Australia Limited (JPMSAL) (ABN 61 003 245 234/AFS Licence No: 238066) is regulated by ASIC and is a Market, Clearing and Settlement Participant of ASX Limited and CHI-X. Taiwan: J.P.Morgan Securities (Taiwan) Limited is a participant of the Taiwan Stock Exchange (company-type) and regulated by the Taiwan Securities and Futures Bureau. India: J.P. Morgan India Private Limited, having its registered office at J.P. Morgan Tower, Off. C.S.T. Road, Kalina, Santacruz East, Mumbai - 400098, is a member of the National Stock Exchange of India Limited (SEBI Registration Number - INB 230675231/INF 230675231/INE 230675231) and Bombay Stock Exchange Limited (SEBI Registration Number - INB 010675237/INF 010675237) and is regulated by Securities and Exchange Board of India. For non local research reports, thismaterial is not distributed in India by J.P. Morgan India Private Limited. Thailand: This material is issued and distributed in Thailand by JPMorgan Securities (Thailand) Ltd., which is a member of the Stock Exchange of Thailand and is regulated by the Ministry of Finance and the Securities and Exchange Commission and its registered address is 3rd Floor, 20 North Sathorn Road, Silom, Bangrak, Bangkok 10500. Indonesia: PT J.P. Morgan Securities Indonesia is a member of the Indonesia Stock Exchange and is regulated by the OJK a.k.a. BAPEPAM LK. Philippines: J.P. Morgan Securities Philippines Inc. is a Trading Participant of the Philippine Stock Exchange and a member of the Securities Clearing Corporation of the Philippines and the Securities Investor Protection Fund. It is regulated by the Securities and Exchange Commission. Brazil: Banco J.P. Morgan S.A. is regulated by the Comissao de Valores Mobiliarios (CVM) and by the Central Bank of Brazil. Mexico: J.P. Morgan Casa de Bolsa, S.A. de C.V., J.P. Morgan Grupo Financiero is a member of the Mexican Stock Exchange and authorized to act as a broker dealer by the National Banking and Securities Exchange Commission. Singapore: This material is issued and distributed in Singapore by or through J.P. Morgan Securities Singapore Private Limited (JPMSS)[MCI (P) 199/03/2014 and Co. Reg. No.: 199405335R] which is a member of the Singapore Exchange Securities Trading Limited and is regulated by the Monetary Authority of Singapore (MAS) and/or JPMorgan Chase Bank, N.A., Singapore branch (JPMCB Singapore) which is regulated by the MAS. This material is provided in Singapore only to accredited investors, expert investors and institutional investors, as defined in Section 4A of the Securities and Futures Act, Cap. 289. Recipients of this document are to contact JPMSS or JPMCB Singapore in respect of any matters arising from, or in connection with, the document. Japan: JPMorgan Securities Japan Co., Ltd. is regulated by the Financial Services Agency in Japan. Malaysia: This material is issued and distributed in Malaysia by JPMorgan Securities (Malaysia) Sdn Bhd (18146-X) which is a Participating Organization of Bursa Malaysia Berhad and a holder of Capital Markets Services License issued by the Securities Commission in Malaysia. Pakistan: J. P. Morgan Pakistan Broking (Pvt.) Ltd is a member of the Karachi Stock Exchange and regulated by the Securities and Exchange Commission of Pakistan. Saudi Arabia: J.P. Morgan Saudi Arabia Ltd. is authorized by the Capital Market Authority of the Kingdom of Saudi Arabia (CMA) to carry out dealing as an agent, arranging, advising and custody, with respect to securities business under licence number 35-07079 and its registered address is at 8th Floor, Al-Faisaliyah Tower, King Fahad Road, P.O. Box 51907, Riyadh 11553, Kingdom of Saudi Arabia. Dubai: JPMorgan Chase Bank, N.A., Dubai Branch is regulated by the Dubai Financial Services Authority (DFSA) and its registered address is Dubai International Financial Centre - Building 3, Level 7, PO Box 506551, Dubai, UAE.

Country and Region Specific Disclosures U.K. and European Economic Area (EEA): Unless specified to the contrary, issued and approved for distribution in the U.K. and the EEA by JPMS plc. Investment research issued by JPMS plc has been prepared in accordance with JPMS plc's policies for managing conflicts of interest arising as a result of publication and distribution of investment research. Many European regulators require a firm to establish, implement and maintain such a policy. This report has been issued in the U.K. only to persons of a kind described in Article 19 (5), 38, 47 and 49 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (all such persons being referred to as "relevant persons"). This document must not be acted on or relied on by persons who are not relevant persons. Any investment or investment activity to which this document relates is only available to relevant persons and will be engaged in only with relevant persons. In other EEA countries, the report has been issued to persons regarded as professional investors (or equivalent) in their home jurisdiction. Australia: This material is issued and distributed by JPMSAL in Australia to "wholesale clients" only. This material does not take into account the specific investment objectives, financial situation or particular needs of the recipient. The recipient of this material must not distribute it to any third party or outside Australia without the prior written consent of JPMSAL. For the purposes of this paragraph the term "wholesale client" has the meaning given in section 761G of the Corporations Act 2001. Germany: This material is distributed in Germany by J.P. Morgan Securities plc, Frankfurt Branch and J.P.Morgan Chase Bank, N.A., Frankfurt Branch which are regulated by the Bundesanstalt für Finanzdienstleistungsaufsicht. Hong Kong: The 1% ownership disclosure as of the previous month end satisfies the requirements under Paragraph 16.5(a) of the Hong Kong Code of Conduct for Persons Licensed by or Registered with the Securities and Futures Commission. (For research published within the first ten days of the month, the disclosure may be based on the month end data from two months prior.) J.P. Morgan Broking (Hong Kong) Limited is the liquidity provider/market maker for derivative warrants, callable bull bear contracts and stock options listed on the Stock Exchange of Hong Kong Limited. An updated list can be found on HKEx website: http://www.hkex.com.hk. Japan: There is a risk that a loss may occur due to a change in the price of the shares in the case of share trading, and that a loss may occur due to the exchange rate in the case of foreign share trading. In the case of share trading, JPMorgan Securities Japan Co., Ltd., will be receiving a brokerage fee and consumption tax (shouhizei) calculated by multiplying the executed price by the commission rate which was individually agreed between JPMorgan Securities Japan Co., Ltd., and the customer in advance. Financial Instruments Firms: JPMorgan Securities Japan Co., Ltd., Kanto Local Finance Bureau (kinsho) No. 82 Participating Association / Japan Securities Dealers Association, The Financial Futures Association of Japan, Type II Financial Instruments Firms Association and Japan Investment Advisers Association. Korea: This report may have been edited or contributed to from time to time by affiliates of J.P. Morgan Securities (Far East) Ltd, Seoul Branch. Singapore: JPMSS and/or its affiliates may have a holding in any of the securities discussed in this report; for securities where the holding is 1% or greater, the specific holding is disclosed in the Important Disclosures section above. India: For private circulation only, not for sale. Pakistan: For private circulation only, not for sale. New Zealand: This material is issued and distributed by JPMSAL in New Zealand only to persons whose principal business is the investment of money or who, in the course of and for the purposes of their business, habitually invest money. JPMSAL does not issue or distribute this material to members of "the public" as determined in accordance with section 3 of the Securities Act 1978. The recipient of this material must not distribute it to any third party or outside New Zealand without the prior written consent of JPMSAL. Canada: The information contained herein is not, and under no circumstances is to be construed as, a prospectus, an advertisement, a public offering, an offer to sell securities described herein, or solicitation of an offer to buy securities described herein, in Canada or any province or territory thereof. Any offer or sale of the securities described herein in Canada will be made only under an exemption from the requirements to file a prospectus with the relevant Canadian securities regulators and only by a dealer properly registered under applicable securities laws or, alternatively, pursuant to an exemption from the dealer registration requirement in the relevant province or territory of Canada in which such offer or sale is made. The

16

Asia Pacific Equity Research15 May 2014

Pinakin Parekh, CFA(91-22) [email protected]

information contained herein is under no circumstances to be construed as investment advice in any province or territory of Canada and is not tailored to the needs of the recipient. To the extent that the information contained herein references securities of an issuer incorporated, formed or created under the laws of Canada or a province or territory of Canada, any trades in such securities must be conducted through a dealer registered in Canada. No securities commission or similar regulatory authority in Canada has reviewed or in any way passed judgment upon these materials, the information contained herein or the merits of the securities described herein, and any representation to the contrary is an offence. Dubai: This report has been issued to persons regarded as professional clients as defined under the DFSA rules. Brazil: Ombudsman J.P. Morgan: 0800-7700847 / [email protected].

General: Additional information is available upon request. Information has been obtained from sources believed to be reliable but JPMorgan Chase & Co. or its affiliates and/or subsidiaries (collectively J.P. Morgan) do not warrant its completeness or accuracy except with respect to any disclosures relative to JPMS and/or its affiliates and the analyst's involvement with the issuer that is the subject of the research. All pricing is as of the close of market for the securities discussed, unless otherwise stated. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipient of this report must make its own independent decisions regarding any securities or financial instruments mentioned herein. JPMS distributes in the U.S. research published by non-U.S. affiliates and accepts responsibility for its contents. Periodic updates may be provided on companies/industries based on company specific developments or announcements, market conditions or any other publicly available information. Clients should contact analysts and execute transactions through a J.P. Morgan subsidiary or affiliate in their home jurisdiction unless governing law permits otherwise.

"Other Disclosures" last revised April 5, 2014.

Copyright 2014 JPMorgan Chase & Co. All rights reserved. This report or any portion hereof may not be reprinted, sold or redistributed without the written consent of J.P. Morgan. #$J&098$#*P