july 20, 2012 orlando, florida · 7/20/2012 · hotel real estate cycle ... lake buena vista...

TRANSCRIPT

July 20, 2012 Orlando, Florida

1

John Lancet, MAI ◦ Director/Partner

◦ HVS Miami

2

Look back at past performance and where we stand in the hotel real estate cycle

Present our 5-year forecast of U.S. supply, demand,

occupancy, and average rate change

Present Metro Orlando performance forecasts Overview of recent national transaction trends and hotel

brand transaction trends Valuation parameters, discount rates, and cap rates

3

2009 represented a peak year for the increase in supply additions, registering a 2.8% increase over 2008, and adding a record131,000 rooms

This increase was on the heels of an increase in 108,000 rooms in 2008

Thus, during 2008 and 2009, over 5% supply growth was realized

From 2010 through 2011, total supply increased 2.2% representing another 104,000 rooms added during these 2 years

4

All time high in supply – over 4.8 million rooms in 2011

(000) A

vail

able

Ro

om

Nig

hts

5

Demand declined 2.5% in 2008 and another 6.2% in 2009

U.S. Lodging Industry experienced a rapid demand recovery in 2010 and 2011, increasing 7.3% and 4.9% respectively

Total Room nights sold in 2011 reached all time high (surpassing 2007 levels) at 2.897 million

6

7

◦ Occupancy in 2011: 60.1%

◦ Compares closely to 12 year average: 60.3%

8

9

◦ Average rate peaked in 2008 at

$107.40, before dropping 8.5% to just over $98 in 2009 ◦ Average rate remained at $98 in 2010

◦ Average rate increased 3.7% in 2011 to

just under $102 and roughly $6.00 off the prior peak

10

11

Average rate increased 3.7% in 2011

% C

han

ge

5.4%

-1.2% -1.2%

0.2%

4.2%

5.8% 7.5%

6.6%

2.9%

-8.5

3.7%

12

After a 16.7% decline in RevPAR in 2009, RevPAR increased 5.5% in 2010 and another 8.2% in 2011

RevPAR for 2011 at $61.07 approached the 2006 level $(61.76)

HVS forecasts National RevPAR to exceed 2007 high of $65.53 in 2013, reaching $69.77

13

14

15

HVS forecasts the following annual increases in room night supply:

2012 0.4%

2013 0.5%

2014 1.0%

2015 1.5%

2016 1.5%

Year end 2016 hotel supply estimated at 5.065 million rooms

16

(000)

17

HVS forecasts the following annual increases in room night demand:

2012 2.3% 2013 2.5% 2014 2.0% 2015 1.5% 2016 1.5%

Year end 2016 forecast to equal 3.191 million room nights sold

Thus the % increase in demand will be greater than the % increase in supply for 2012, 2013, 2014

National occupancy forecast at 63% from 2014 through 2016, at historical high levels

18

(000)

19

20

HVS forecasts the following annual increases in National ADR:

2012 4.75% 2013 5.00% 2014 4.75% 2015 4.00% 2016 3.00%

ADR forecast at $106.51 in 2012, about $1 less than 2008 record high of $107.40.

ADR will surpass previous peak and the $110 peak in 2013.

HVS forecast ADR increasing to $125.49 by year end 2016.

21

Average Rate to surpass previous peak and the $110 mark in 2013

22

HVS forecasts the following RevPAR increases: 2012 6.7% 2013 7.1% 2014 5.8% 2015 4.0% 2016 3.0%

RevPAR will hit $69.77 in 2013 and exceed the 2007

record

RevPAR growth will be healthy from 2012 to 2015

Year end 2016 RevPAR forecast at $79.06

23

24

2012: ◦ Supply additions minimal at 0.4%

◦ Demand expands by 2.3%

◦ Occupancy improves by 1.8% to end year at 61.2%

◦ Average Rate leads at 4.75% growth to end year at

$106.51

◦ RevPAR increase of 6.7% to end year at $65.16

25

Minimal to modest annual increases in supply ranging from 0.5% to 1.5%

Occupancies stay at 62.4% to 63.04% between 2013 and 2016

Respectable annual increase in ADR, ranging from 4% to 5%, from 2013 to 2016 will drive healthy annual increases in RevPAR of 4% to 7% between 2013 and 2016

Overall, 2013 through 2016 should be good performance years for the hotel industry

26

Orlando Regional Outlook

27

Orlando North: Altamonte Springs, Sanford, Winter Park, some North Orlando

Orlando Central: Downtown, from West Orlando (Winter Garden, Ocoee) to East Orlando (UCF) along State Road 50 (Colonial Drive)

Orlando South: South Orange Blossom Trail, Airport International (I-Drive): Universal Studios south to SeaWorld and

also includes Hilton Bonnet Creek/Waldorf-Astoria Lake Buena Vista (LBV): All LBV hotels, including Marriott World

Center, Hyatt Regency Grand Cypress and Caribe Royale; includes Walt Disney World Swan and Dolphin, but does not include all other Walt Disney World owned and operated hotel properties

Kissimmee West: Zip code 34747; South of Disney along I-4 and the western portion of U.S.192

Kissimmee East: All other zip codes in Osceola County, including the eastern portion of U.S. 192 Kissimmee and St. Cloud.

28 Source: Copyright 2012 Smith Travel Research, All Rights Reserved

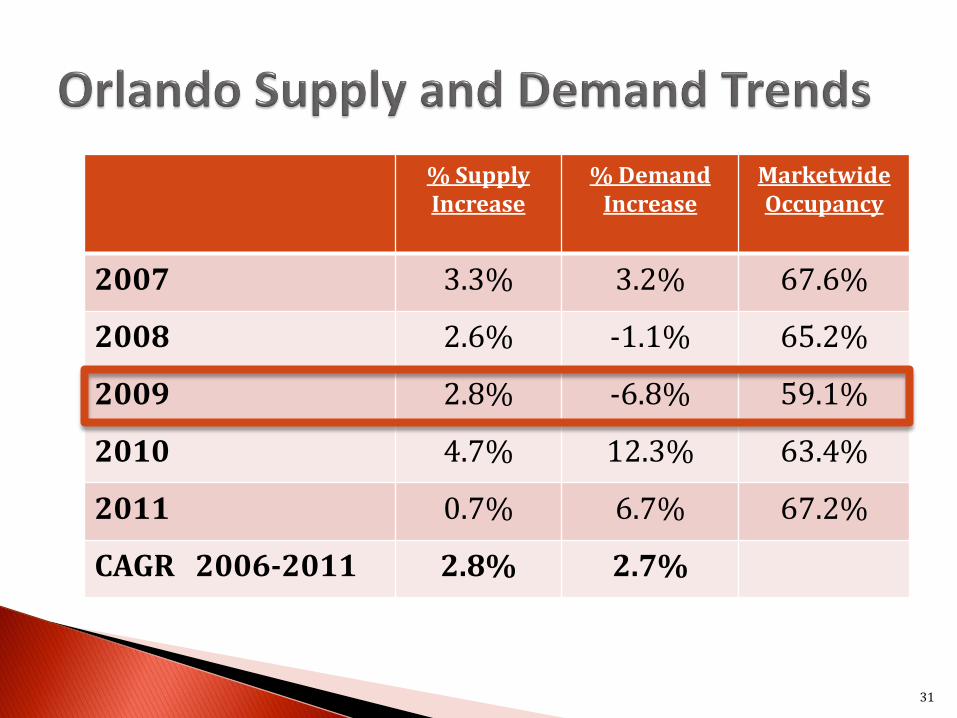

Excluding Disney, the Orlando hotel supply has grown from 67,000 rooms in 2006 to 77,000 rooms (current)

Disney has approximately 21,841 rooms but does not report performance metrics

Thus, total combined hotel supply for Orlando equals approximately 92,000 rooms

29

Orlando supply additions initiated during the boom years (06-08) resulted in the following annual increases in supply, which were not always aligned with the annual % change in demand

30

31

% Supply Increase

% Demand Increase

Marketwide Occupancy

2007 3.3% 3.2% 67.6%

2008 2.6% -1.1% 65.2%

2009 2.8% -6.8% 59.1%

2010 4.7% 12.3% 63.4%

2011 0.7% 6.7% 67.2%

CAGR 2006-2011 2.8% 2.7%

RevPAR for 2011 was $68.56 which is still below 2006 RevPAR of $73.98 and the peak RevPAR of $76.93 in 2007

2012 YTD (5 month) RevPAR of $81.71 is 5.3% above YTD 2011. Year end 2012 RevPAR is expected to be in the low $70’s

Year end 2012 ADR forecast at $105 to $106 which is still 7% to 8% less than the peak of $114 in 2008. Future % increases in ADR are not expected to exceed the national trend.

Return to peak occupancy levels had been fueled by the 2011 record of 55.1 million total visitors, with 56.4 million forecasted for 2012

32

33

40

45

50

55

60

65

70

75

80

2006 2007 2008 2009 2010 2011

Occupancy

Lake Buena Vista Orlando South International Drive

Orlando Central Orlando North Kissimmee West

Kissimmee East

34

50

55

60

65

70

75

80

85

May 2011 May 2012

Occupancy - Year to Date May

Lake Buena Vista Orlando South International Drive Orlando Central

Orlando North Kissimmee West Kissimmee East

35

$40

$50

$60

$70

$80

$90

$100

$110

$120

$130

2006 2007 2008 2009 2010 2011

Average Rate

Lake Buena Vista Orlando South International Drive Orlando Central

Orlando North Kissimmee West Kissimmee East

36

$40

$50

$60

$70

$80

$90

$100

$110

$120

$130

May 2011 May 2012

Average Rate - Year to Date May

Lake Buena Vista Orlando South International Drive Orlando Central

Orlando North Kissimmee West Kissimmee East

37

$20

$30

$40

$50

$60

$70

$80

$90

$100

2006 2007 2008 2009 2010 2011

RevPAR

Lake Buena Vista Orlando South International Drive

Orlando Central Orlando North Kissimmee West

Kissimmee East

38

$20

$30

$40

$50

$60

$70

$80

$90

$100

May 2011 May 2012

RevPAR- Year to Date May

Lake Buena Vista Orlando South International Drive Orlando Central

Orlando North Kissimmee West Kissimmee East

39

40

41

42

43

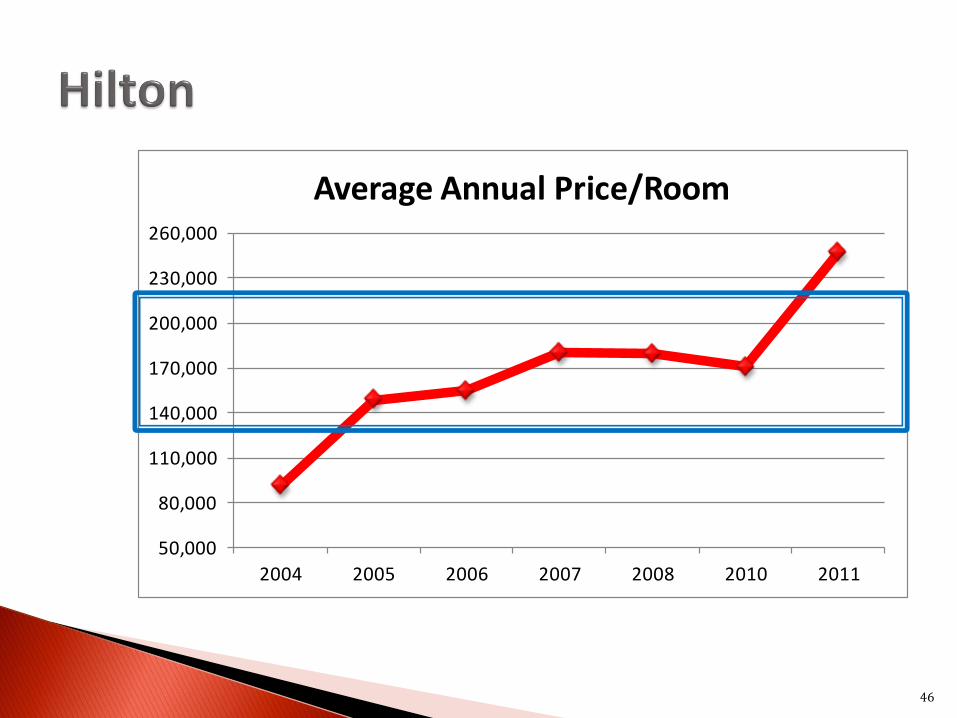

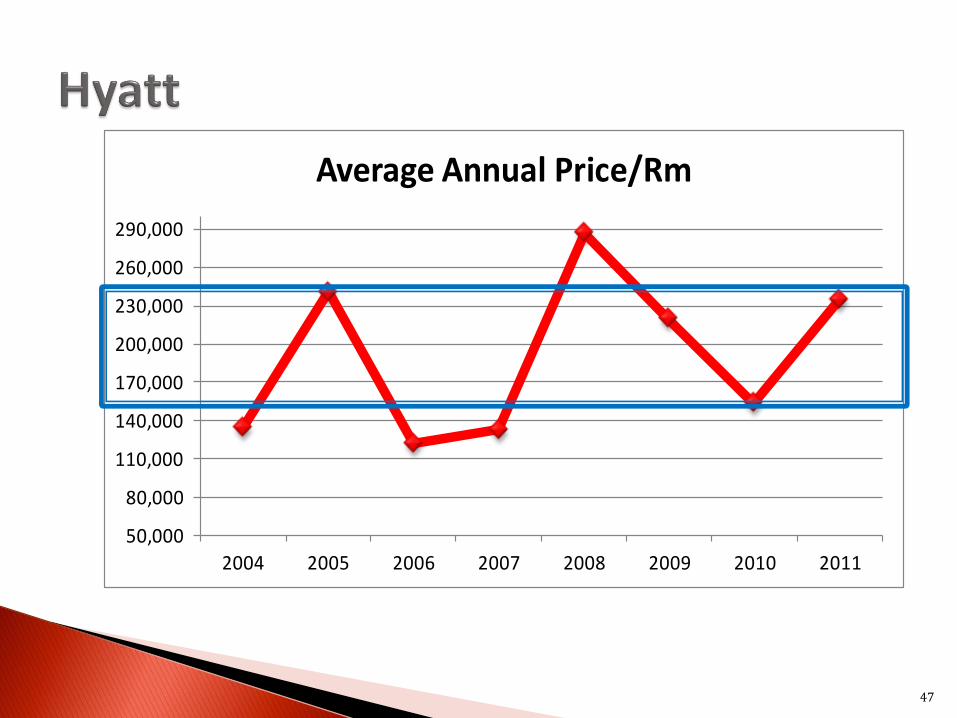

Hotel Transaction Trends by Brand

80,000

100,000

120,000

140,000

160,000

180,000

2004 2005 2006 2007 2008 2010 2011

Average Annual Price/Room

44

50,000

80,000

110,000

140,000

170,000

200,000

230,000

2004 2005 2006 2007 2008 2009 2010 2011

Average Annual Price/Room

45

46

50,000

80,000

110,000

140,000

170,000

200,000

230,000

260,000

2004 2005 2006 2007 2008 2010 2011

Average Annual Price/Room

47

50,000

80,000

110,000

140,000

170,000

200,000

230,000

260,000

290,000

2004 2005 2006 2007 2008 2009 2010 2011

Average Annual Price/Rm

48

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

2005 2006 2007 2008 2010 2011

Average Annual Price/Room

49

$122,523

$146,374 $150,800

$175,446

$234,182

$0

$50,000

$100,000

$150,000

$200,000

$250,000

Sheraton Hilton Marriott Hyatt Westin

Average Sale Price/Room 2004-2011

50

$50,000

$60,000

$70,000

$80,000

$90,000

$100,000

2004 2005 2006 2007 2008 2009 2010 2011

Average Annual Price Paid/Room

$50,000

$60,000

$70,000

$80,000

$90,000

$100,000

$110,000

$120,000

$130,000

2004 2005 2006 2007 2008 2009 2010 2011

Average Annual Price/Room

51

52

$50,000

$70,000

$90,000

$110,000

$130,000

$150,000

$170,000

$190,000

2004 2005 2006 2007 2008 2009 2010 2011

Average Annual Price/Room

53

$50,000

$70,000

$90,000

$110,000

$130,000

$150,000

$170,000

$190,000

2004 2005 2006 2007 2008 2009 2010 2011

Average Annual Price/Room

54

$80,449

$99,694

$127,430$135,944

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

Holiday Inn Express

Hampton Inn Courtyard Hilton Garden Inn

Average Sale Price/Room 2004-2011

55

11.4

15.9

5.4 6.3

12.3

18.3

7.0 8.0

13.6

21.2

7.5 9.1

0

5

10

15

20

25

Unlevered Discount Rate

Equity Yield Cap Rate Historical NOI

Cap Rate Projected Year One NOI

Full Service Select Service Limited Service

Source: HVS

Current U.S. lending parameters for hotels relative to senior debt position:

◦ LTV Ratios 55.0% - 65.0%

◦ Interest Rates 5.0% - 7.5%

◦ Debt Yield Ratio 11.0% - 12.0%

Assets Terminal Cap Overall

Property Yield Equity Yield

Highest Tier (higher barrier to entry- product type/location/quality – top 3% of assets) – TROPHY TYPE

7.0% - 8.0% 9.0% - 9.5% 13.0% - 15.0%

High Quality – not top 3% of hotel assets 8.0% - 9.0% 9.5% - 11.0% 15.0% - 17.0%

Middle Quality 9.0% - 11.0% 11.5% -13.0% 17.0% - 18.0%

Lower Quality 11.0% - 13.0% 13.5% - 16.0% 19.0% - 22.0%

58

59