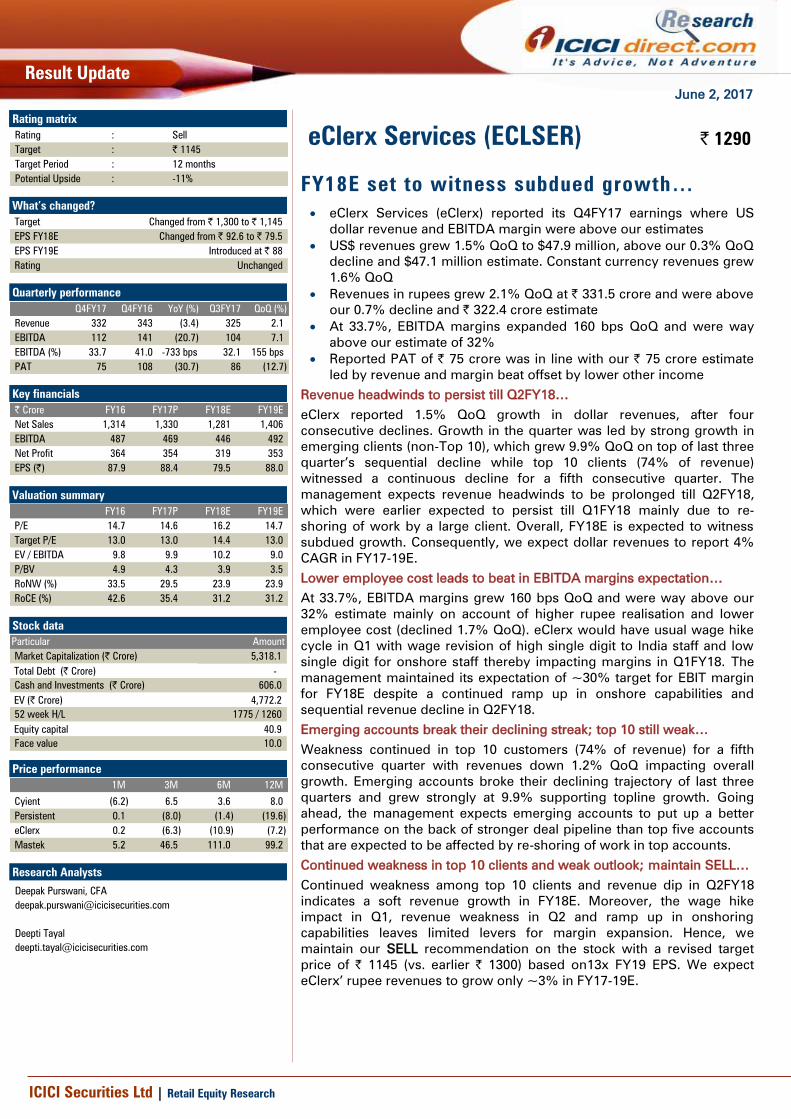

june 2, 2017 eclerx services (eclser) |...

TRANSCRIPT

June 2, 2017

ICICI Securities Ltd | Retail Equity Research

Result Update

FY18E set to witness subdued growth…

eClerx Services (eClerx) reported its Q4FY17 earnings where US

dollar revenue and EBITDA margin were above our estimates

US$ revenues grew 1.5% QoQ to $47.9 million, above our 0.3% QoQ

decline and $47.1 million estimate. Constant currency revenues grew

1.6% QoQ

Revenues in rupees grew 2.1% QoQ at | 331.5 crore and were above

our 0.7% decline and | 322.4 crore estimate

At 33.7%, EBITDA margins expanded 160 bps QoQ and were way

above our estimate of 32%

Reported PAT of | 75 crore was in line with our | 75 crore estimate

led by revenue and margin beat offset by lower other income

Revenue headwinds to persist till Q2FY18…

eClerx reported 1.5% QoQ growth in dollar revenues, after four

consecutive declines. Growth in the quarter was led by strong growth in

emerging clients (non-Top 10), which grew 9.9% QoQ on top of last three

quarter’s sequential decline while top 10 clients (74% of revenue)

witnessed a continuous decline for a fifth consecutive quarter. The

management expects revenue headwinds to be prolonged till Q2FY18,

which were earlier expected to persist till Q1FY18 mainly due to re-

shoring of work by a large client. Overall, FY18E is expected to witness

subdued growth. Consequently, we expect dollar revenues to report 4%

CAGR in FY17-19E.

Lower employee cost leads to beat in EBITDA margins expectation…

At 33.7%, EBITDA margins grew 160 bps QoQ and were way above our

32% estimate mainly on account of higher rupee realisation and lower

employee cost (declined 1.7% QoQ). eClerx would have usual wage hike

cycle in Q1 with wage revision of high single digit to India staff and low

single digit for onshore staff thereby impacting margins in Q1FY18. The

management maintained its expectation of ~30% target for EBIT margin

for FY18E despite a continued ramp up in onshore capabilities and

sequential revenue decline in Q2FY18.

Emerging accounts break their declining streak; top 10 still weak…

Weakness continued in top 10 customers (74% of revenue) for a fifth

consecutive quarter with revenues down 1.2% QoQ impacting overall

growth. Emerging accounts broke their declining trajectory of last three

quarters and grew strongly at 9.9% supporting topline growth. Going

ahead, the management expects emerging accounts to put up a better

performance on the back of stronger deal pipeline than top five accounts

that are expected to be affected by re-shoring of work in top accounts.

Continued weakness in top 10 clients and weak outlook; maintain SELL…

Continued weakness among top 10 clients and revenue dip in Q2FY18

indicates a soft revenue growth in FY18E. Moreover, the wage hike

impact in Q1, revenue weakness in Q2 and ramp up in onshoring

capabilities leaves limited levers for margin expansion. Hence, we

maintain our SELL recommendation on the stock with a revised target

price of | 1145 (vs. earlier | 1300) based on13x FY19 EPS. We expect

eClerx’ rupee revenues to grow only ~3% in FY17-19E.

eClerx Services (ECLSER) | 1290

Rating matrix

Rating : Sell

Target : | 1145

Target Period : 12 months

Potential Upside : -11%

What’s changed?

Target Changed from | 1,300 to | 1,145

EPS FY18E Changed from | 92.6 to | 79.5

EPS FY19E Introduced at | 88

Rating Unchanged

Quarterly performance

Q4FY17 Q4FY16 YoY (%) Q3FY17 QoQ (%)

Revenue 332 343 (3.4) 325 2.1

EBITDA 112 141 (20.7) 104 7.1

EBITDA (%) 33.7 41.0 -733 bps 32.1 155 bps

PAT 75 108 (30.7) 86 (12.7)

Key financials

| Crore FY16 FY17P FY18E FY19E

Net Sales 1,314 1,330 1,281 1,406

EBITDA 487 469 446 492

Net Profit 364 354 319 353

EPS (|) 87.9 88.4 79.5 88.0

Valuation summary

FY16 FY17P FY18E FY19E

P/E 14.7 14.6 16.2 14.7

Target P/E 13.0 13.0 14.4 13.0

EV / EBITDA 9.8 9.9 10.2 9.0

P/BV 4.9 4.3 3.9 3.5

RoNW (%) 33.5 29.5 23.9 23.9

RoCE (%) 42.6 35.4 31.2 31.2

Stock data

Particular Amount

Market Capitalization (| Crore) 5,318.1

Total Debt (| Crore) -

Cash and Investments (| Crore) 606.0

EV (| Crore) 4,772.2

52 week H/L 1775 / 1260

Equity capital 40.9

Face value 10.0

Price performance

1M 3M 6M 12M

Cyient (6.2) 6.5 3.6 8.0

Persistent 0.1 (8.0) (1.4) (19.6)

eClerx 0.2 (6.3) (10.9) (7.2)

Mastek 5.2 46.5 111.0 99.2

Research Analysts

Deepak Purswani, CFA

Deepti Tayal

ICICI Securities Ltd | Retail Equity Research Page 2

Variance analysis

Q4FY17 Q4FY17E Q4FY16 YoY (%) Q3FY17 QoQ (%) Comments

Revenue 331.5 322.4 343.2 -3.4 324.7 2.1 $ revenues grew 1.5% QoQ and were above our expectation

Employee expenses 131.6 133.8 118.9 10.7 133.9 -1.7

Gross Margin 199.9 188.6 224.3 -10.9 190.8 4.8

Gross margin (%) 60.3 58.5 65.4 -505 bps 58.8 155 bps

SG&A expenses 88.3 85.4 83.6 5.6 86.5 2.1

EBITDA 111.6 103.2 140.7 -20.7 104.3 7.1

EBITDA Margin (%) 33.7 32.0 41.0 -733 bps 32.1 155 bps EBITDA margins expanded 160 bps led by decline in employee cost

Depreciation & amortisation 13.7 6.5 13.8 -0.7 13.4 2.2

EBIT 97.9 96.6 126.9 -22.8 90.9 7.8

EBIT Margin (%) 29.5 30.0 37.0 -744 bps 28.0 155 bps

Other income (less interest) -7.2 0.7 9.0 -224.4 11.3 -163.5

PBT 90.7 97.4 135.8 -33.2 102.2 -11.2

Tax paid 15.9 22.4 27.6 -42.5 16.2 -2.0

PAT 75.0 75.0 108.2 -30.7 85.9 -12.7

PAT was in line with our expectations led by revenue and margin beat offset

by lower other income

Key Metrics

Closing employees 8,737 8,700 8,862 -1.4 8,648 1.0 Sequentially, headcount increased by 89

Attrition (%) 34.3 35.0 28.6 570 bps 33.1 120 bps Attrition grew QoQ and stands at elevated levels

Utilisation (%) 68.9 70.0 67.7 116 bps 68.9 0 bps

Average $/| 68.8 68.5 66.5 3.5 68.2 0.8

Source: Company, ICICIdirect.com Research

Change in estimates

FY18E FY19E

(| Crore) Old New % Change Introduced

Revenue 1,398 1,281 -8.4 1,406

EBITDA 510 446 -12.7 492

EBITDA Margin (%) 36.5 34.8 -171 bps 35.0

PAT 382 319 -16.6 353

EPS (|) 93 79 -14.2 88 Tweaked our estimates to incorporate management commentory for FY18E

Source: Company, ICICIdirect.com Research

Assumptions

Current Earlier Introduced

FY15 FY16 FY17P FY18E FY18E FY19E

Closing employees 8,100 8,862 8,737 8,837 8,848 9,244

Attrition (%) 28.3 33.1 34.8 35.0 30.0 35.0

Utilisation (%) 73.0 76.9 78.3 77.0 67.0 79.0

Average $/| 61.2 66.0 68.5 65.9 69.0 67.0

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 3

Conference call highlights…

FY18 revenue outlook – The management expects headwinds to

persist now till Q2FY18, which were earlier expected to persist till

Q1FY18 due to re-shoring of work by a large client. eClerx is

facing headwinds among top 10 clients since Q4FY16 and is

expected to be weak in FY18E. Overall, FY18E is expected to be a

soft year

Margins – The management maintained its expectation of ~30%

target for EBIT margin for FY18E despite near term headwinds

Employee update- Employee headcount is at 8737 (vs. 8862 in

FY16) at the end of FY17 with a net reduction of 125 employees.

Attrition for the fiscal was at 34.8%, up from 33.7% in FY16, which

drastically surged in Q2 owing to some mismatch of skills among

a few employees. Staff utilisation was at 78.3% in FY17, highest in

the last five years owing to economies of scale and automation

benefits, mostly in cable vertical. However, we foresee utilisation

being adversely impacted in FY18E due to Q2FY18 headwinds

Cash position – The company has cash & cash equivalent of | 606

crore. It has announced a token dividend of | 1/share. However, it

expects to maintain historical payout over the medium term

Capex - Capex declined to | 21.1 crore in FY17 vs. | 48.2 crore in

FY16. It expects capex to decline further in the coming year owing

to sufficient capacity at offshore centres

DSO days- DSO days were at 85 days at the year end (vs. 73 days

in FY16) due to one-off factors as indicated by the management

and expects it to be ~80 days, going ahead

Hedge position- Forward hedge book was at US$132.5 million

with average strike rate of | 72.1 and expects US$104 million to

convert into operating revenues by FY18E at | 72

ICICI Securities Ltd | Retail Equity Research Page 4

Company Analysis

eClerx reported 1.6% QoQ growth in constant currency (CC) revenues

while overall dollar revenues grew 1.5% QoQ led by strong growth in

emerging clients (non-top 10), which grew 9.9% QoQ offset by continued

weakness in top 10 clients (74% of revenue) declining sequentially by

1.2%. Revenue headwinds, which were earlier expected to persist till

Q1FY18, are now expected to be prolonged till Q2FY18 mainly due to re-

shoring of the work by a large client. Consequently, we expect dollar

revenues to report 4% CAGR in FY17-19E with subdued growth in FY18E.

Exhibit 1: Dollar revenues may grow at 4% CAGR during FY17-19E

76

97

122

138 154

46.4 50.2 51.8 50.8

199

50.2 48.947.2 47.9

194194

210

37.3

29.0

24.713.9

11.2

28.1

31.9 33.2

24.8

29.5

8.2

0.1

7.9

0

10

20

30

40

50

0

50

100

150

200

250

FY11

FY12

FY13

FY14

FY15

Q1FY16

Q2FY16

Q3FY16

Q4FY16

FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

FY17P

FY18E

FY19E

%

$ m

illion

Dollar revenue Growth, YoY

Source: Company, ICICIdirect.com Research

Exhibit 2: eClerx de-grows significantly in FY17 compared to industry growth of 9%

30.0

37.3

29.0

24.7

13.911.2

29.5

-2.5

5.5

18.716.5

10.213.0 13.0 13.0

9.0

-5

5

15

25

35

45

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17P

%

Growth, YoY NASSCOM guidance

Source: Company, ICICIdirect.com Research

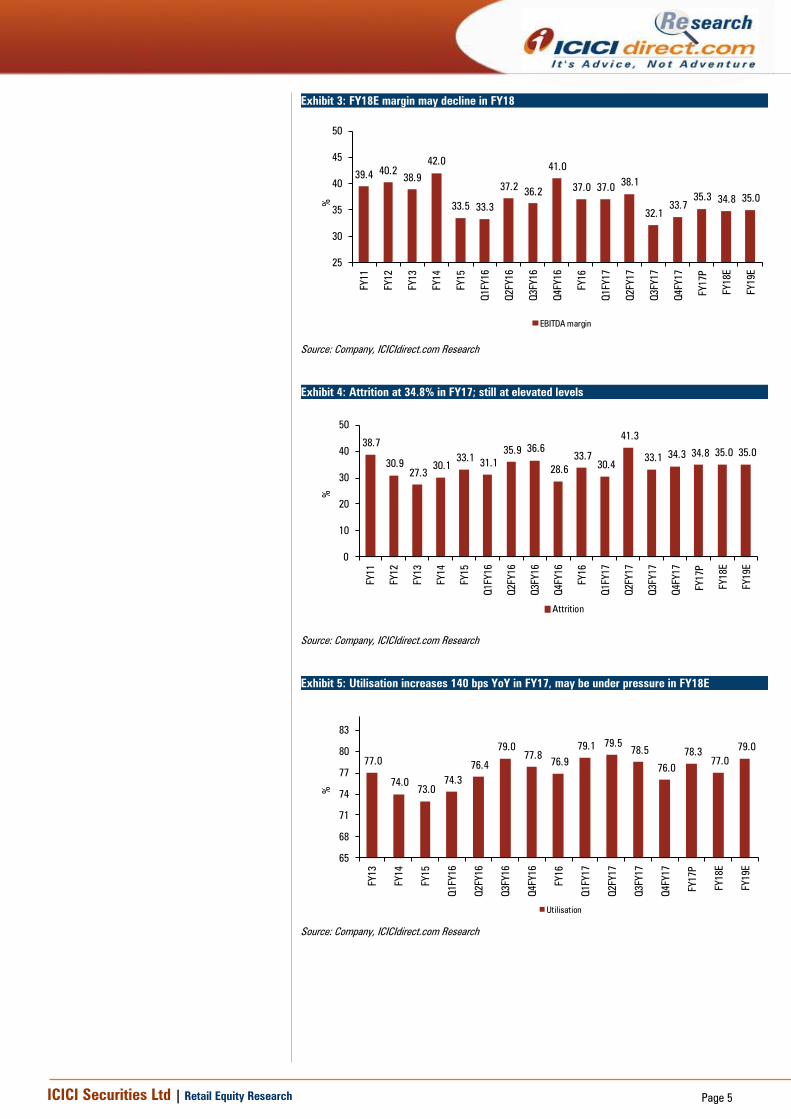

EBITDA margin beats expectations…

At 33.7%, EBITDA margins grew 160 bps QoQ and were way above our

32% estimate mainly on account of lower employee cost (declined 1.7%

QoQ). eClerx would have the usual wage hike cycle in Q1 with wage

revision of high single digit to India staff and low single digit for onshore

staff thereby impacting margins in Q1FY18. The management maintained

its expectation of ~30% target for EBIT margin for FY18E despite

continued ramp up in onshore capabilities and sequential revenue decline

in Q2FY18.

ICICI Securities Ltd | Retail Equity Research Page 5

Exhibit 3: FY18E margin may decline in FY18

39.440.2

38.9

42.0

33.5 33.3

37.236.2

41.0

37.0 37.038.1

32.1

33.7

35.3 34.8 35.0

25

30

35

40

45

50

FY11

FY12

FY13

FY14

FY15

Q1FY16

Q2FY16

Q3FY16

Q4FY16

FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

FY17P

FY18E

FY19E

%EBITDA margin

Source: Company, ICICIdirect.com Research

Exhibit 4: Attrition at 34.8% in FY17; still at elevated levels

38.7

30.9

27.3

30.1

33.1 31.1

35.9 36.6

28.6

33.7

30.4

41.3

33.1 34.3 34.8 35.0 35.0

0

10

20

30

40

50

FY11

FY12

FY13

FY14

FY15

Q1FY16

Q2FY16

Q3FY16

Q4FY16

FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

FY17P

FY18E

FY19E

%

Attrition

Source: Company, ICICIdirect.com Research

Exhibit 5: Utilisation increases 140 bps YoY in FY17, may be under pressure in FY18E

77.0

74.0 73.0

74.3

76.4

79.0

77.8 76.9

79.1 79.5 78.5

76.0

78.3

77.0

79.0

65

68

71

74

77

80

83

FY13

FY14

FY15

Q1FY16

Q2FY16

Q3FY16

Q4FY16

FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

FY17P

FY18E

FY19E

%

Utilisation

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 6

Clients contributing $0.5 million+ now at 38, down by two YoY…

In comparison to FY16, client count in FY17 declined by two to 14 in $0.5

million+ bucket due to certain projects getting completed in digital

verticals. Client contribution run rate increased and declined by one each

in $1 million+ bucket and US$5 million+ bucket to 18 and six,

respectively on the back of movement of a top 10 client to lower value

bucket. Weakness continued in top 10 customers (74% of revenue) for

fifth consecutive quarter with revenues declining 1.2% QoQ impacting

overall growth. Emerging accounts broke their declining trajectory of the

last three quarters and grew strongly at 9.9% supporting topline growth.

Exhibit 6: In FY17, clients contributing $0.5 million+ in revenues declined by two

56

7

9 9

16 16 16

18 18

1514 14

0

2

4

6

8

10

12

14

16

18

20

FY13

FY14

FY15

Q1FY16

Q2FY16

Q3FY16

Q4FY16

FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

FY17P

$0.5 million+ clients

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 7

Outlook and Valuation

eClerx reported Q4FY17 numbers, which were above our expectation on

the revenue front while margins also surprised on the upside. However,

for the year, consolidated dollar revenues declined 2.5% YoY and 1.5%

on a constant currency basis. The management expects headwinds to

persist till Q2FY18E with overall FY18E being a soft year.

Continued weakness among top 10 clients and revenue dip in Q2FY18

indicates a soft revenue growth in FY18E. Moreover, the wage hike

impact in Q1, revenue weakness in Q2 and ramp up in onshoring

capabilities leaves limited levers for margin expansion. Hence, we

maintain our SELL recommendation on the stock with a revised target

price of | 1145 (vs. earlier | 1300) based on 13x FY19 EPS. We expect

eClerx’ rupee revenues to grow only ~3% in FY17-19E.

Exhibit 7: One year forward rolling PE

0

360

720

1080

1440

1800

May-10

Nov-10

May-11

Nov-11

May-12

Nov-12

May-13

Nov-13

May-14

Nov-14

May-15

Nov-15

May-16

Nov-16

May-17

Price 16 13 10 7 4

Source: Company, ICICIdirect.com Research

Exhibit 8: Valuations

Sales Growth EPS Growth PE EV/EBITDA RoNW RoCE

(| cr) (%) (|) (%) (x) (x) (%) (%)

FY16 1,314 39.5 87.9 57.7 14.7 9.8 33.5 42.6

FY17P 1,330 1.2 88.4 0.6 14.6 9.9 29.5 35.4

FY18E 1,281 (3.7) 79.5 (10.0) 16.2 10.2 23.9 31.2

FY19E 1,406 9.8 88.0 10.8 14.7 9.0 23.9 31.2

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 8

Recommendation History vs. Consensus

0.0

10.0

20.0

30.0

40.0

50.0

60.0

200

500

800

1,100

1,400

1,700

2,000

May-17Mar-17Dec-16Oct-16Jul-16May-16Mar-16Dec-15Oct-15Jul-15May-15

(%

)(|)

Price Idirect target Consensus Target Mean % Consensus with SELL

Source: Bloomberg, Company, ICICIdirect.com Research

Key events

Date Event

Oct-12 Reports $29.8 million revenue (6% QoQ growth) and 32.5% EBIT margins for Q2FY13, below our $30.5 million and 34.1% estimate, respectively

Aug-13 Approves buyback of shares at maximum | 825 per share

Jul-14 Reports muted Q1FY15 revenue growth led by weakness in top 5 clients (cable and sales & marketing). Margins decline 600 bps

Jan-15 Q3FY15 was yet another disappointing quarter where dollar revenue growth and margins came below our estimates led by degrowth in top 5 clients

Mar-15 Acquires CLX Europe for €25 million. CLX had revenues of €19.4 million in CY14 with EBITDA of €4.5 million and PAT of €500,000

May-15 During Q4FY15, revenue growth came above our estimates led by emerging accounts while margins continue to decline sequentially

Jun-15

Reports steady Q1FY16 earnings as revenue growth was in line but margins were above our estimates. Growth was led by CLX integration and recovery in top 5

clients

Nov-15 Reports good set of Q2FY16 earnings as both revenue and margins were above our estimates. Growth was led by CLX and top 5 clients

Aug-16 Reports Q2FY17 numbers, which were marginally below our estimates

Oct-16 Eclerx finalises buyback price of | 2000 per share with final amount of buyback at | 234 crore

Nov-16 Eclerx to commence its | 234 crore buyback on November 28, 2016 and close on December 9, 2016

Dec-16

Eclerx step-down subsidiary Agilyst Inc US, to be merged with eclerx LLC US, its wholly-owned subsidiary for administrative convenience and to maintain a lean

organisational structure

Dec-16

eClerx completes buy-back programme worth | 234 crore. Buy-back undertaken on proportionate basis by way of tender offer for cash at | 2000 per equity shares

constituted 11,70,000 shares representing 2.87% of total paid-up equity share capital

Source: Company, ICICIdirect.com Research

Top 10 Shareholders Shareholding Pattern

Rank Name Latest Filing Date % O/S Position (m) Change (m)

1 Malik (Anjan) 31-Mar-17 25.1% 10.0 0.0

2 Mundhra (Priyadarshan) 31-Mar-17 25.1% 10.0 0.0

3 Matthews International Capital Management, L.L.C. 21-Dec-15 7.9% 3.2 -0.2

4 Fidelity Management & Research Company 31-Mar-16 4.5% 1.8 1.8

5 Franklin Templeton Asset Management (India) Pvt. Ltd. 31-Mar-16 3.3% 1.3 0.0

6 HDFC Asset Management Co., Ltd. 31-Mar-16 3.0% 1.2 0.0

7 UTI Asset Management Co. Ltd. 31-Mar-17 2.9% 1.2 0.7

8 PineBridge Investments Asia Limited 31-Mar-17 2.9% 1.2 0.1

9 SBI Funds Management Pvt. Ltd. 31-Mar-17 2.2% 0.9 0.0

10 IIFL Inc 31-Mar-17 1.6% 0.6 0.0

(in %) Sep-16 Dec-16 Mar-17

Promoter 50.25 50.44 50.28

Public 49.75 49.50 49.53

Others 0.00 0.06 0.19

Total 100.00 100.00 100.00

Source: Reuters, ICICIdirect.com Research

Recent Activity

Investor name Value Shares Investor name Value Shares

UTI Asset Management Co. Ltd. 16.0m 0.7m Goldman Sachs Asset Management International 5.9m 0.3m

PineBridge Investments Asia Limited 2.7m 0.1m ABN AMRO Investment Solutions (AAIS) 0.6m 0.0m

Norges Bank Investment Management (NBIM) 1.0m 0.0m L&T Investment Management Limited 0.5m 0.0m

Eclerx Employee Welfare Trust 0.7m 0.0m State Street Global Advisors (US) 0.3m 0.0m

Mirae Asset Global Investments Co., Ltd. 0.4m 0.0m Malik (Pawan) 0.3m 0.0m

Buys Sells

Source: Reuters, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 9

.

Financial summary

Profit and loss statement | Crore

FY16 FY17P FY18E FY19E

Total Revenues 1,314 1,330 1,281 1,406

Growth (%) 39.5 1.2 (3.7) 9.8

Employee expenses 501 525 506 555

Other Expenditure 327 337 329 359

EBITDA 487 469 446 492

Growth (%) 54.3 (3.7) (4.9) 10.4

Depreciation 51 52 50 55

Other Income 41 19 29 33

Interest expense - 0 - -

PBT before Exceptional Items 477 436 425 470

Growth (%) 60.1 (8.6) (2.6) 10.8

Tax 113 82 106 118

PAT before Exceptional Items 364 354 319 353

Exceptional items - - - -

PAT before MI 364 354 319 353

Minority Int & Pft. from associates 0 (0) - -

PAT 364 354 319 353

Growth (%) 58.3 (2.6) (10.0) 10.8

EPS 88 88 79 88

EPS (Growth %) 57.7 0.6 (10.0) 10.8

Source: Company, ICICIdirect.com Research

Cash flow statement | Crore

FY16 FY17P FY18E FY19E

Net profit before Tax 477 436 425 470

Depreciation 51 52 50 55

(inc)/dec in Current Assets (27) (5) (16) (21)

(inc)/dec in current Liabilities (113) (82) (106) (118)

CF from operations 426 441 308 359

Other Investments (63) - - -

Other income 41 19 29 -

(Purchase)/Sale of Fixed Assets (52) (75) (75) (75)

CF from investing Activities (172) (56) (46) (42)

Inc / (Dec) in Equity Capital 14 - - -

Dividend & Divendend tax (128) (5) (187) (207)

Interest Paid on Loans (0) - - -

CF from Financial Activities (165) (242) (187) (207)

Exchange rate differences (3) - - -

Opening cash balance 198 327 470 544

Other adjustments 43 - - -

Closing cash 327 470 544 654

Source: Company, ICICIdirect.com Research

Balance sheet | Crore

FY16 FY17P FY18E FY19E

Equity 41 40 40 40

Reserves & Surplus 1,045 1,162 1,293 1,439

Networth 1,086 1,202 1,333 1,479

Minority Interest 1 1 1 1

Loans - - - -

Other liabilities 33 29 29 29

Source of funds 1,119 1,230 1,363 1,508

Gross Block 264 339 414 489

Acc.dep 167 219 269 323

Net Block 97 120 145 165

CWIP - - - -

Investments 219 219 219 219

Goodwill 243 243 243 243

Debtors 186 154 174 186

Cash & Cash equivalents 327 470 544 654

Loans and advances 80 113 109 120

Other current assets 113 181 175 192

Trade payables 14 3 3 3

Current liabilities 50 27 13 14

Provisions 82 239 231 253

Application of funds 1,119 1,230 1,363 1,508

Source: Company, ICICIdirect.com Research

Key ratios

FY16 FY17P FY18E FY19E

Per share data (|)

EPS 87.9 88.4 79.5 88.0

Cash EPS 100.1 101.3 92.0 101.7

BV 262.5 299.9 332.7 369.0

DPS 1.0 1.0 39.7 44.0

Cash Per Share 79.0 117.2 135.8 163.2

Operating Ratios (%)EBITDA Margin 37.0 35.3 34.8 35.0

PAT Margin 27.7 26.6 24.9 25.1

Debtor days 52 42 49 48

Creditor days 4 1 1 1

Return Ratios (%)

RoE 33.5 29.5 23.9 23.9

RoCE 42.6 35.4 31.2 31.2

RoIC 132.1 139.3 111.1 111.6

Valuation Ratios (x)

P/E 14.7 14.6 16.2 14.7

EV / EBITDA 9.8 9.9 10.2 9.0

EV / Net Sales 3.6 3.5 3.6 3.2

Market Cap / Sales 4.0 4.0 4.2 3.8

Price to Book Value 4.9 4.3 3.9 3.5

Solvency Ratios

Debt/EBITDA - - - -

Debt / Equity - - - -

Current Ratio 2.6 1.7 1.9 1.8

Quick Ratio 2.6 1.7 1.9 1.8

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 10

ICICIdirect.com coverage universe (IT)

CMP M Cap EPS (|) P/E (x) RoCE (%) RoE(%)

(|) TP(|) Rating (| Cr) FY16 FY17P FY18E FY16 FY17P FY18E FY16 FY17P FY18E FY16 FY17P FY18E FY16 FY17P FY18E

Cyient (INFENT) 537 580 Hold 6,046 29.0 30.5 35.9 18.5 17.6 15.0 12.7 10.6 9.4 20.3 20.0 20.3 17.1 16.3 17.1

Eclerx (ECLSER) 1,290 1,145 Sell 5,318 87.9 88.4 79.5 14.7 14.6 16.2 9.8 9.9 10.2 42.6 35.4 31.2 33.5 29.5 23.9

Firstsource (FIRSOU) 39 45 Buy 2,582 3.8 4.1 4.4 10.2 9.4 8.9 7.7 6.7 6.0 11.7 12.1 12.1 12.9 11.5 11.0

HCL Tech (HCLTEC) 850 930 Buy 119,994 52.1 60.0 59.6 16.3 14.2 14.3 12.6 10.3 9.7 31.2 30.3 30.6 26.9 26.6 25.1

Infosys (INFTEC) 930 1,060 Buy 212,554 59.0 62.8 64.6 15.8 14.8 14.4 10.4 9.3 9.6 30.2 28.8 31.0 21.8 20.8 22.3

KPIT Tech (KPISYS) 128 140 Hold 2,547 14.1 10.6 11.0 9.1 12.0 11.6 5.4 7.0 6.6 23.7 16.3 16.3 20.4 15.4 12.8

Mindtree (MINCON) 442 485 Hold 7,422 35.9 24.9 29.1 12.3 17.7 15.2 8.4 9.1 8.2 31.1 21.1 23.9 25.2 16.0 18.0

NIIT Technologies (NIITEC) 496 520 Hold 1,777 45.8 43.2 45.3 10.8 10.5 11.0 2.9 2.5 2.2 30.5 29.9 28.1 17.6 14.9 14.1

Persistent (PSYS) 580 700 Buy 4,639 37.2 37.6 40.1 15.6 15.4 14.5 9.7 8.5 7.1 23.8 21.3 20.4 18.1 16.2 15.4

TCS (TCS) 2,290 2,400 Hold 448,542 122.9 133.4 135.0 18.6 17.2 16.9 13.7 12.6 12.4 42.2 38.0 40.9 33.1 29.7 32.2

Tech Mahindra (TECMAH) 429 490 Buy 42,158 31.7 31.8 33.9 13.5 13.5 12.7 8.8 8.7 7.8 25.5 21.9 20.6 21.7 17.2 16.2

Wipro (WIPRO) 494 500 Hold 121,676 36.1 35.2 34.1 13.7 14.0 14.5 9.9 8.7 8.7 19.6 17.3 15.9 19.1 15.7 14.1

Sector / Company

EV/EBITDA (x)

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 11

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns

ratings to its stocks according to their notional target price vs. current market price and then categorises them

as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless specified and the notional

target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

ICICI Securities Ltd | Retail Equity Research Page 12

ANALYST CERTIFICATION

We /I, Deepak Purswani, CFA MBA (Finance), Deepti Tayal, MBA, Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report

accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or

view(s) in this report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities

Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has

its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which

are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking

and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts

and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and

meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without

prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current.

Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended

temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this

company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This

report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their

receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific

circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment

objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate

the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any

loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the

risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to

change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment

in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in

respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned

in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any

compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts

and their relatives have any material conflict of interest at the time of publication of this report.

It is confirmed that Deepak Purswani, CFA MBA (Finance), Deepti Tayal, MBA, Research Analysts of this report have not received any compensation from the companies mentioned in the report in the

preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month

preceding the publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.

It is confirmed that Deepak Purswani, CFA MBA (Finance), Deepti Tayal, MBA, Research Analysts do not serve as an officer, director or employee of the companies mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,

publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities

described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and

to observe such restriction.