kandil_sameh_ar50411_part 1 to 5

TRANSCRIPT

Please submit assignment via Moodle an upload the assignment cover sheet

SECTION 1: STUDENT TO COMPLETE

SECTION 2: TUTOR TO COMPLETE

1

2

3

4

5

Overall

Mark

TUTOR COMMENTS AND ADVICE TO STUDENT

In submitting this assignment, I confirm that I have read and understood the entry on Cheating & Plagiarism in the Department's current Programmes Handbook. I agree that all material I submit for assessment will be my

own work except where I have indicated using appropriate references or acknowledgements.

NOTE ABOUT YOUR ASSIGNMENT FEEDBACK: Your assignment grade and mark are provisional, subject to approval by the Faculty Board of Studies following the Board of Examiners meeting, where your overall module

result will be confirmed.

ASSIGNMENT COVER

SHEET

Student’s Name

Individual question marks

Assignment/ Case Study Name

Sustainable Business Practices

Sameh Kandil Mohammed Ibrahim

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 2 of 24

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 3 of 24

Contents

Chapter 1

1.0 Describtion of my Organization ................................................................................................5

2.0 Focus of my Case Study ............................................................................................................5

3.0 Aim of my Case Study ...............................................................................................................5

4.0 AECOM’s Understanding of SBP ..............................................................................................5

4.1 Ethics .......................................................................................................................................6

4.2 Community ...............................................................................................................................6

4.3 Environmental Protection ..........................................................................................................7

4.4 Employment Practices ..............................................................................................................7

Chapter 2

1.0 How SBP can attain Competitive Advantage for a Company ..................................................8

1.1 SBP and Competitive Advantage ..............................................................................................8

1.2 SBP (Employment Pratices) .....................................................................................................8

2.0 Reuse-Recycle-Reduce ..............................................................................................................8

2.1 Benefits of Recycling ................................................................................................................8

2.2 Cost of Recycling ......................................................................................................................9

3.0 Actions to Support SBP ........................................................................................................... 10

3.1 Organization Actions............................................................................................................... 10

3.2 Employees Actions ................................................................................................................. 10

4.0 True Cost of Waste .................................................................................................................. 10

5.0 Key Areas for RRR (Reuse-Reduce-Recycle) ......................................................................... 11

5.1 Reuse ..................................................................................................................................... 11

5.2 Reduce ................................................................................................................................... 11

5.3 Recycle................................................................................................................................... 11

6.0 Managers Resposnsibilties for SBP ...................................................................................... 11

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 4 of 24

Chapter 3

1.0 PEST Factors Definition .......................................................................................................... 13

2.0 SWOT Analysis of AECOM SBP’s Strategy ............................................................................ 13

2.1 AECOM’s Internal Strengths ................................................................................................... 13

2.2 AECOM’s Internal Weaknesses .............................................................................................. 13

2.3 AECOM’s External Opportunities ............................................................................................ 13

2.4 AECOM’s External Threats ..................................................................................................... 14

3.0 Minimize the Threats ................................................................................................................ 14

Chapter 4

1.0 Stakeholders and SBP Strategy .............................................................................................. 16

1.1 Stakeholders Definition ........................................................................................................... 16

1.2 Positive Effects of SBP Policy ................................................................................................. 16

1.3 Negative Effects of SBP Policy ............................................................................................... 16

2.0 Introducing SBP Policy’s Barriers .......................................................................................... 16

3.0 How to Overcome the Barriers of Implementation SBP Policy ............................................. 17

4.0 Effect of SBP Policy on the Rest of Supply Chain ................................................................. 17

Chapter 5

1.0 KPIs for Measuring SBP Perfrormance .................................................................................. 19

2.0 Achieveing KPIs and Customer Satisfaction ......................................................................... 19

3.0 Responsibility for Implementation of SBP ............................................................................. 20

4.0 Factors involved in the Process of SBP Implementation ...................................................... 20

5.0 SBP Policy and Addressing Stakeholders Requirements .................................................... 20

6.0 How to Report SBP Performance to Stakeholders and Public ............................................. 21

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 5 of 24

List of Figure Figure 1 AECOM’s Sustainability Business Practices ………………………………………………...……………………….5

Figure 2 SBP (Employment Practices) ……………………………...………………………………………………………….8 Figure 3 Jobs Opportunities (Landfilling vs Recycling)….......…………………………………..…………………….………9

Figure 4 Star Model Framework.……..…...…………………………………………………………………………...……….10

Figure 5 SWOT Analysis.……………………………………………………………………………………………...……….14

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 6 of 24

Chapter 1 Defining Context and Scope

------------------------------------------------------------------------------------------------------------------

1.0 Description of my Organization

AECOM is an infrastructure and support services firm, with a broad range of markets, including environmental, energy, water, high-rise buildings and transportation. AECOM is serving in more than 150 countries around the world with approximately 100,000 employees - including architects, engineers, designers, planners, scientists and construction services professionals. AECOM provides a blend of global reach, local knowledge, innovation and technical excellence in delivering solutions that create, enhance and sustain the world's built, natural, and social environments. AECOM ranked as the 1

st engineering design firm by revenue in the annual industry ranking of Engineering News-

Record magazine, AECOM official web site (2014:1).

2.0 Focus of my Case Study

My study is focusing on the existing sustainability strategy and practices inside AECOM. I will focus particularly on the design, legal and human resources departments.

3.0 Aim of my Case Study

The aim of my case study (focusing on AECOM’s strategy) is to highlight in section 4, AECOM’s current commitment towards employees, community and environment. However, there are still some areas that have to be improved by AECOM such as; diversity of employees in the level of senior management and plan for more effective employees development programs.

4.0 AECOM’s understanding of SBP

The heart of AECOM core values; ‘’to create, enhance and sustain the world’s built, natural and social environment’’.

AECOM’s Strategy is to provide stakeholders with innovative solutions that help them in achieving long-term and short-term goals in the most sustainable ways in order to shape a better tomorrow and reserve the planet for future generations.

The Sustainable Business Practices for AECOM are showing through;

Figure 1

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 7 of 24

4.1 Ethics

Committing to providing the client services ethically and in compliance with the law:

AECOM named by Ethisphere Institute as the World’s Most Ethical Companies in 2014 based on AECOM’s ethical behaviour and compliance with the laws and regulations beside the availability of the internal tools dedicated to maintaining integrity in its business dealings, Ethisphere (2014:1).

As advised by Epstein (2008:37), ‘’the ethical companies have to have a set of high standard of behaviour for all employees beside the availability of effective system for monitoring, evaluating and reporting on how the company does business’’. In the light of Epstein advice, AECOM have in place;

1. A Code of Conduct that addresses the professional, ethical, financial and social values of AECOM. Also it represents AECOM’s commitment to their clients, shareholders, partners and communities, AECOM

Sustainability Report (2009:53).

The said Code of Conduct addresses:

Compliance with applicable laws. Equal employment opportunity. Bribes and kickback prohibited. Corrupt practices abroad prohibited. Internal control.

2. According to AECOM’s code of conduct, all the employees are directed to report any concern/violation to one of the following: Direct supervisor, human resources director, AECOM chief ethics officer and AECOM hotline 1-888-299-9602, Corporate (2008:18).

4.2 Community

Creating jobs and improve the livelihood of local community:

AECOM contributed in creating nearly 5,000 jobs in the first 10 years of the operation of Strumosa Urban Agriculture and waste drop-off centre, AECOM Sustainability Report (2013:21). As a result of the loss of an eight months old girl, AECOM developed the Livvi’s place that is a playground designed to provide all children with a safe and comfortable place to play. Now more than 3,000 people are using Livvi’s place each week, AECOM Sustainability Report (2013:23).

Participating in charity programmes:

According to AECOM Sustainability Report (2013:15), AECOM exerted great efforts in charity through doing the followings;

1. A donation of US$ 5.1 million was given to charitable organization around the globe. 2. AECOM entered in strategic partnership with some organizations to maximize its effort in charity. 3. AECOM donated more than US$ 600,000 to help ‘’Water for People’’ to providing four million people with

access to clean water by 2018. 4. AECOM invested in supporting more than 30 universities worldwide.

Volunteering the time and effort of AECOM’s employees in community and charitable events:

According to AECOM Sustainability Report (2013:15) and Sustainability Report (2009:47):

1. AECOM donated in 2013 thousands of volunteers’ hours (AECOM Employees) in different charitable events. 2. Several staff from San Diego office donated their time to help in the Clean-Up efforts during the National

Lands Public Day.

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 8 of 24

4.3 Environment Protection

Reducing the carbon footprint by doing sustainable designs that have the least impact on the environment:

AECOM was selected a design consultant to provide a sustainable design and low carbon construction for Siemens headquarter in Masdar city - United Arab Emirates, AECOM Sustainability Report (2013:27). Through AECOM’s sustainable design the following achievements were possessed:

The first building in the United Arab Emirates certified LEED.

50% reduction in water demand.

46% reduction in electricity demand.

30% reduction in embodied carbon.

98% construction waste diversion from landfill.

Encouraging the conservation of energy and water in every AECOM office around the world:

AECOM embraced the best practices to reduce offices’ energy/water use through using; efficient office spaces, efficient lighting and electricity systems, water flushing systems and irrigation systems, AECOM Sustainability Report

(2013:17).

Embracing best practices in printing:

As mentioned in AECOM Sustainability Report (2013:17), AECOM embraced the best practices in printing to reduce using of papers, inks and toners. In order to achieve the said reduction, AECOM had a partnership with a ‘’Document Solution Company’’ in order to possess a new printing, guidelines and new printing/copying systems.

As a result of AECOM efforts, the North America offices had transitioned to 30% recycled papers; moreover, the new printing guidelines have been integrated into the company culture during 2013.

4.4 Employment Practices

Focusing on the health and safety issues for all AECOM’s employees:

As per AECOM Sustainability Report (2013:13), AECOM is committed to protect all its employees from the risks involved in the construction daily activities so that AECOM initiated ‘’Safety for Life’’ program that aims to prevent work-related injuries/illness. Also AECOM created ‘’9 Life-Preserving Principles’’ that will lead AECOM’s employees to commit to achieving these principles/goals.

As a result of AECOM continuous efforts as shown above, the rate of recordable injuries rate is improved by 22% during 2013.

Empowering the employees to take the right decisions:

AECOM believes in empowering its employees to take the right decisions through giving them the full responsibility over their work-related decisions without interfering from their direct supervisors, AECOM Sustainability Report (2013:6)

Committing to providing development trainings programs for AECOM’s employees:

AECOM is committed to develop the knowledge and skills of its employees around the globe through offering more than 40,000 learning opportunities through in-classroom teaching and online courses, AECOM Sustainability Report (2013:14).

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 9 of 24

Chapter 2 SBP and Competitive Advantage

------------------------------------------------------------------------------------------------------------------

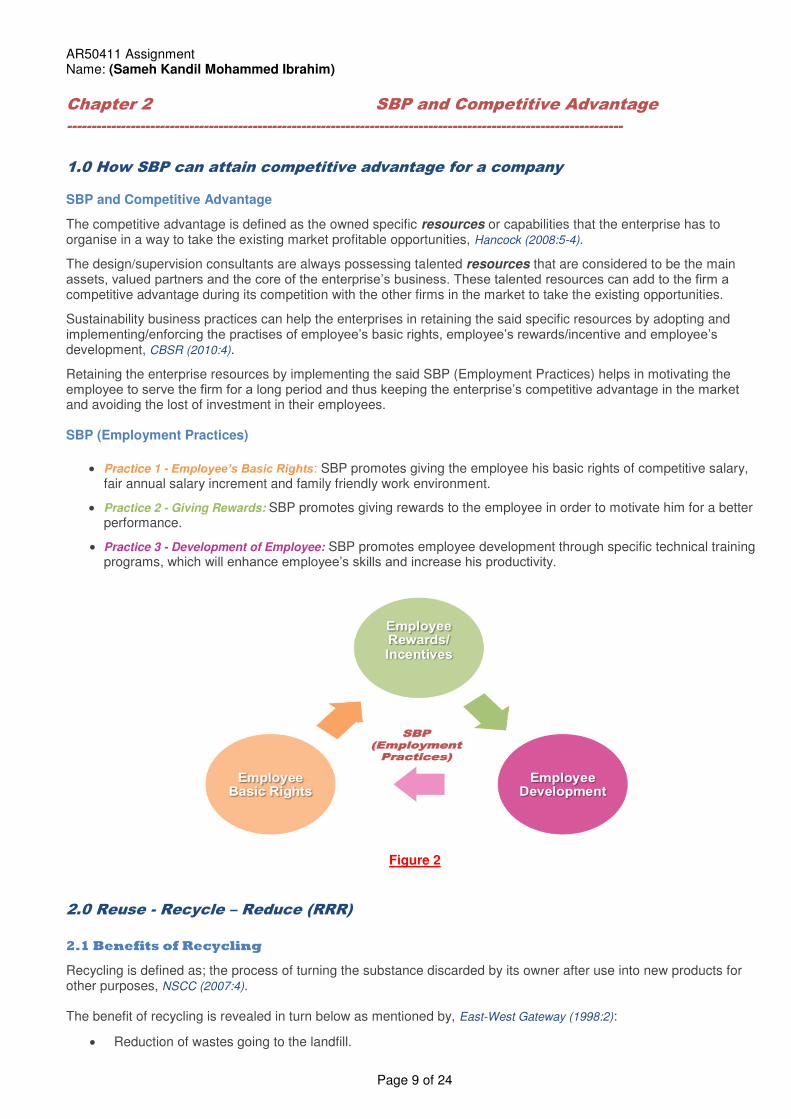

1.0 How SBP can attain competitive advantage for a company SBP and Competitive Advantage

The competitive advantage is defined as the owned specific resources or capabilities that the enterprise has to organise in a way to take the existing market profitable opportunities, Hancock (2008:5-4).

The design/supervision consultants are always possessing talented resources that are considered to be the main assets, valued partners and the core of the enterprise’s business. These talented resources can add to the firm a competitive advantage during its competition with the other firms in the market to take the existing opportunities.

Sustainability business practices can help the enterprises in retaining the said specific resources by adopting and implementing/enforcing the practises of employee’s basic rights, employee’s rewards/incentive and employee’s development, CBSR (2010:4).

Retaining the enterprise resources by implementing the said SBP (Employment Practices) helps in motivating the employee to serve the firm for a long period and thus keeping the enterprise’s competitive advantage in the market and avoiding the lost of investment in their employees. SBP (Employment Practices)

Practice 1 - Employee’s Basic Rights: SBP promotes giving the employee his basic rights of competitive salary, fair annual salary increment and family friendly work environment.

Practice 2 - Giving Rewards: SBP promotes giving rewards to the employee in order to motivate him for a better performance.

Practice 3 - Development of Employee: SBP promotes employee development through specific technical training programs, which will enhance employee’s skills and increase his productivity.

Figure 2

2.0 Reuse - Recycle – Reduce (RRR)

2.1 Benefits of Recycling

Recycling is defined as; the process of turning the substance discarded by its owner after use into new products for other purposes, NSCC (2007:4). The benefit of recycling is revealed in turn below as mentioned by, East-West Gateway (1998:2):

Reduction of wastes going to the landfill.

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 10 of 24

Decreasing the need to extract and process virgin materials from the earth.

Conservation of energy and reducing the pollution associated with extracting and process the virgin materials.

Creating and sustaining more job than the landfill. For every one job created in a landfill, there are 10 jobs in recycling process and 25 jobs in recycling based manufacturing, Eco. Cycle (2005:2).

Figure 3

Recycling produces an economic product as the recycling offsets the cost associated with extracting and

processing the virgin materials needed for production, Eco. Cycle (2005:2).

Avoid the cost of collection for landfill and the cost of landfill Covec (2007:16,17). 2.2 Cost of Recycling

The cost of recycling can be divided into 4 cost categories, as classified by Covec (2007:37 to 41):

Cost of collection

Cost of collection is built up from the following parts:

Trucks: cost of trucks that are used to collect the kerbside collections. Bins: cost of bins for each household. Labours: salaries of trucks’ drivers and runners. Fuel: cost of trucks fuel.

The total estimated cost is $168 per tonne in Auckland – New Zealand, Covec (2007:37).

Cost of sorting

Cost of sorting the materials collected from kerbside collection differs based on the waste stream. As per Covec

(2007:39), the cost per tonne for each stream is;

Plastics: $300 per tonne. Glass (bottle production): $8 per tonne. Glass (crushing): $5 per tonne. Paper: $40 per tonne. Steel: $15 per tonne. Aluminium: $20 per tonne.

Cost of processing (Recycling)

Recycling the materials needs a facility in which these materials can be recycled. This facility has a cost for establishment, operation and maintenance.

Cost of Transportation (Final Product)

The last cost category is the charges of transportation of the recycled materials to the end users.

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 11 of 24

3.0 Actions to support SPB Organization Actions

The organization can support the SPB through a framework called Star Model that developed by Professor Jay Galbraith, CBSR (2010:4). This framework is outlining the five elements that can an organization use to support the SPB. These elements are:

Figure 4

Strategy: Strategy determines the organization vision, goals, values and mission. A definition for sustainability has to be placed first and then it has to be integrated into the organization vision and linked to its goals and values.

Structure: Recruit SPB executive who report directly to the CEO. The SBP executive has to establish the SPB goals and embed these goals into the roles of employees; meanwhile, the CEO has to give the power and support to the SPB executive.

Process: Process is the horizontal and vertical flow of information across the organization. The SBP targets have to be communicated internally to the employees and externally to the organization’s stakeholders.

Rewards: To link the compensation to positive SPB performance which will motivate the employees to align their goals with the organization’s SBP goals.

People: The organization have to ensure first the availability of employees’ basic concerns like; pay, work-life balance, adequate work environment and incentives and then the SBP can be broaden into the employees goals to get their commitment and involvement.

Employees Actions

The employees have to adopt and embed the organization sustainability goals into their daily behaviour and work-related decisions in order to implement change. The employees of GlaxoSmithKline managed to achieve the organization’s target by reducing the Energy consumption by 11%, CBSR (2010:10).

4.0 Key Areas for RRR (Reuse, Reduce, Recycle)

As advised by, NSCC (2007: 8 to12):

4.1 Reuse

Reuse is about using the surplus materials in their original state on the same site or in another sites or liaising with the supplier in order to return back the unused materials.

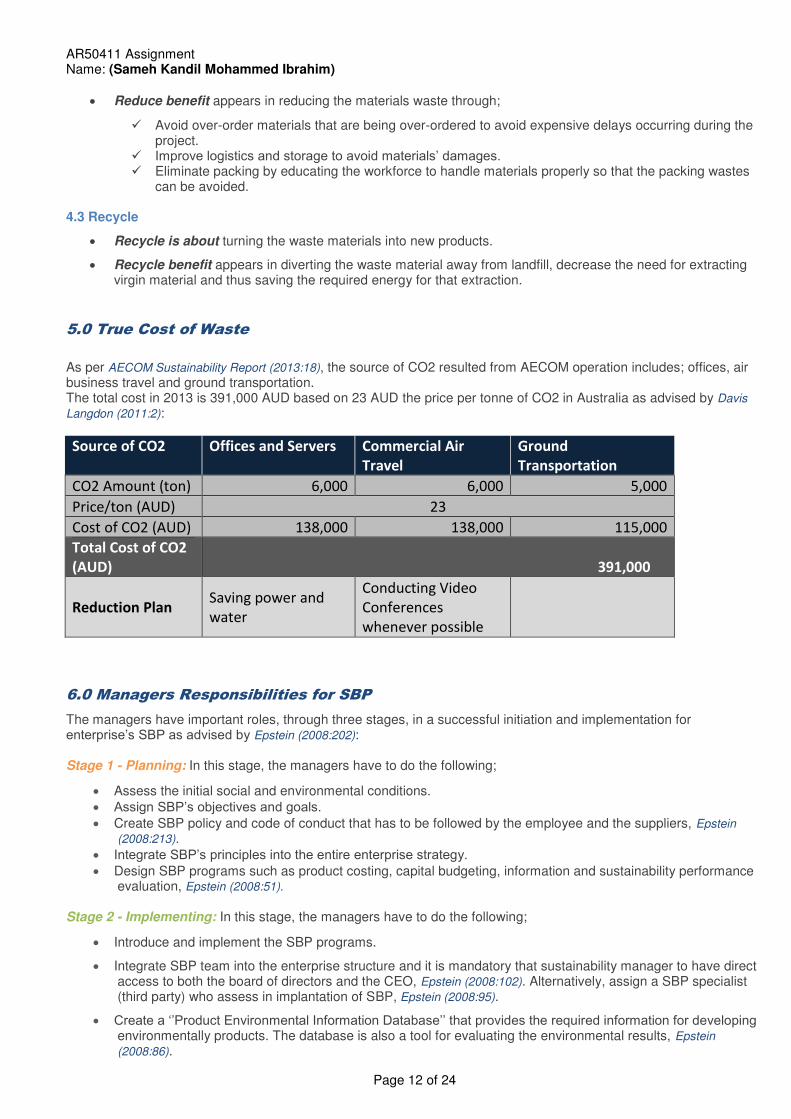

Reuse benefit appears in saving cost by declining the use of new materials that are required for any project. 4.2 Reduce

Reduce is about minimizing the waste of materials during construction.

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 12 of 24

Reduce benefit appears in reducing the materials waste through;

Avoid over-order materials that are being over-ordered to avoid expensive delays occurring during the project.

Improve logistics and storage to avoid materials’ damages. Eliminate packing by educating the workforce to handle materials properly so that the packing wastes

can be avoided.

4.3 Recycle

Recycle is about turning the waste materials into new products.

Recycle benefit appears in diverting the waste material away from landfill, decrease the need for extracting virgin material and thus saving the required energy for that extraction.

5.0 True Cost of Waste

As per AECOM Sustainability Report (2013:18), the source of CO2 resulted from AECOM operation includes; offices, air business travel and ground transportation. The total cost in 2013 is 391,000 AUD based on 23 AUD the price per tonne of CO2 in Australia as advised by Davis

Langdon (2011:2):

Source of CO2 Offices and Servers Commercial Air

Travel

Ground

Transportation

CO2 Amount (ton) 6,000 6,000 5,000

Price/ton (AUD) 23

Cost of CO2 (AUD) 138,000 138,000 115,000

Total Cost of CO2

(AUD) 391,000

Reduction Plan Saving power and

water

Conducting Video

Conferences

whenever possible

6.0 Managers Responsibilities for SBP

The managers have important roles, through three stages, in a successful initiation and implementation for enterprise’s SBP as advised by Epstein (2008:202): Stage 1 - Planning: In this stage, the managers have to do the following;

Assess the initial social and environmental conditions. Assign SBP’s objectives and goals. Create SBP policy and code of conduct that has to be followed by the employee and the suppliers, Epstein

(2008:213). Integrate SBP’s principles into the entire enterprise strategy. Design SBP programs such as product costing, capital budgeting, information and sustainability performance

evaluation, Epstein (2008:51). Stage 2 - Implementing: In this stage, the managers have to do the following;

Introduce and implement the SBP programs.

Integrate SBP team into the enterprise structure and it is mandatory that sustainability manager to have direct access to both the board of directors and the CEO, Epstein (2008:102). Alternatively, assign a SBP specialist (third party) who assess in implantation of SBP, Epstein (2008:95).

Create a ‘’Product Environmental Information Database’’ that provides the required information for developing environmentally products. The database is also a tool for evaluating the environmental results, Epstein

(2008:86).

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 13 of 24

Conduct SBP audit to ensure the minimum standards are met internally and externally (suppliers).

Monitor and measure SBP performance in order to help managers in setting the action plans and the schedule for reporting deficiencies, Epstein (2008:237).

Issue a regular sustainability report to provide an important feedback for decision-making and to help employees to see their contributions towards the successful performance of the company, Epstein (2008:218).

Stage 3 - Educating: In this stage, the managers have to do the following;

Provide SBP’s trainings for employees to make them aware about the social, environmental and financial impacts of the company business, Epstein (2008:203). Also the trainings are required to improve the employees’ performance in sustainability.

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 14 of 24

Chapter 3 SWOT Analysis

------------------------------------------------------------------------------------------------------------------

1.0 PEST Definition PEST is an analysis used to assess the external four factors that have an affect on the business. These factors are; political, economical, social and technological.

2.0 SWOT Analysis of AECOM SBP’s Strategy

2.1 Internal Strengths

There are internal strengths in AECOM that positively affect the enterprise’s Sustainability Business Practices:

Structure; SBP is supported in the enterprise through the availability of SPB executive who is creating SPB’s goals that to be embed into the employees roles, CBSR (2010:4) or sometimes by assigning a SBP specialist (third party) who assess in implementation of SBP, Epstein (2008:95).

Process; SBP is supported through the flow of SBP information (policy, targets and key performance indicators) internally among the employees and externally among the stakeholders, suppliers and publicity, CBSR (2010:11).

Leadership: the commitment to sustainability by the senior executives, who are knowledgeable enough about sustainability, is another internal factor that enforces the SBP implementation through AECOM, Epstein (2008:50).

People; AECOM’s commitment to provide the employees with a fair pay structure, work-life balance, an adequate work environment and skills development programs facilitates and enhances the employees commitment towards the AECOM’s sustainability goals, CBSR (2010:9).

Rewards; link the rewards to the employees performance in sustainability is considered to be another internal factor that guarantees the success of SBP implementation, as this link can ensure the alignment of employees goals with those of AECOM, CBSR (2010:10).

Systems: various management systems such as ‘’sustainability performance evaluation’’ drive effectively the sustainability strategy through AECOM as the sustainability performance evaluation system can help to gauge the sustainability performance of business units in order to take the proactive actions that impact and enhance sustainability performance, Epstein (2008:50).

2.2 Internal Weaknesses

There are internal Weaknesses in AECOM that negatively affect the enterprise’s Sustainability Business Practices:

Size of AECOM’s global business; the size of AECOM seizes its ability to control the quality standards which may impact adversely the quality of final product/services and thus affecting the corporate profitability and growth, IKEA (2009:79). Moreover, as a result of lack of product value, the customer satisfaction will be reduced, Epstein (2008:39).

Decentralization; AECOM that are operating in multiple geographic locations face more challenges, which always lead to adopting the principle of decentralization of enterprise structure. However, there are challenges associated with decentralization include the loss of scale economies that leads to increase of product/service cost and thus reduce the corporate profitability, Epstein (2008:86).

Difficulty of communication: due to the large scale of AECOM’s business and the geographical diversity of AECOM’s operation, AECOM face difficulty in communication with employees, customers, community activists, environmental groups and human right groups about the enterprise’s environmental activities. There are many companies where a lack of communication caused increased costs and thus affect the profitability, Epstein (2008:178).

2.3 External Opportunities

There are opportunities that arise from the external environment and will affect positively AECOM’s Sustainability Business Practices:

Growing Pressure for SBP: On the government level, there is growing interest worldwide in the development and implementation of proactive sustainability strategies. As informed by Hancock (2008:10-15), the EU seeks to

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 15 of 24

promote the concept of SBP (society, economic and environment) as a positive investment. Moreover, the EU suggested in the GRI report the inclusion of series of performance indicators that measures the success in implementation of SBP practices. These indicators are related to the human resources management, health and safety, environmental impact and use of natural resources and local communities.

Growing social and environmental awareness: On advocating groups level, there is awareness of the developments that have severe effects on environment and society so that, the advocating groups are forcing the companies to consider the environment and society while they are doing their business. In the UK, the construction companies have become familiar with the protesters reactions against the development that cause social, environmental or human rights concerns, Hancock (2008:10-17).

Media coverage: On media level, considering SBP will increase the positive media coverage and the company will be acknowledged for ‘’doing good’’ which will improve the reputation and future business opportunities, Hancock (2008:10-18).

2.4 External Threats

There are threats that arises from the external environment (sector/market) and will affect negatively AECOM’s Sustainability Business Practices:

Corruption in developing countries: In the developing countries, there is a high potential for corruption which creates difficulties for the enterprises when they are trying to follow their own code of conducts in doing ethical business overseas Epstein (2008:119).

Employee base: Doing a business in the remote areas especially in the case of mining and oil and gas industries where the workers are away from their families and communities, will expose them to the sexually transmitted diseases and increased drug and alcohol use, Epstein (2008:120). These passive consequences will increase the absenteeism rate due to illness and will cause a higher turn over due to HIV-related deaths plus more accidents due to intoxication by drugs and alcohol. As a result, the enterprise will encounter more costs coming from rehiring, loss of productivity and safety offences fines.

3.0 Minimize the Threats

Based on SWOT Analysis that has been done in ‘’section 1.0’’, the below chart is showing clearly the external threats that has to be overcome in order to effectively implement the SPB strategy, thus enhancing sustainability performance.

Figure 5

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 16 of 24

Corruption in developing countries: one possible solution is to refrain from doing a business in the countries where the corruption prevails, Unger (1998:4) otherwise the company has to follow one of the following approaches, Galang (2011:1);

If a company possess political influence in a country, they can use it to alter the regulations to reduce overall corruption.

In countries with limited regulations, the company can create self-regulating industry associations that will shift the power from the government to the industry and its stakeholders.

In strong centralized countries, no option rather than allying with the government, networking with powerful officials and establishing joint venture with local firms.

Employee Base: solutions to manage the challenges of doing business in remote areas might be as advised by Meredith et al (2014:4,5):

Considering a balanced work/family roster that enables the workers to be at home for extended time. Roster can be symmetrical (e.g., 2weeks on, 2 weeks off), asymmetrical (e.g., 2 weeks on, 1 week off), short (4/3 days) or long (6/1 days).

Managing workers who are experiencing excessive drug or alcohol use through allowing a limited leisure time, put restriction on the drinking inside the camp site and using of random breath tests.

Produce flexible workplace policies around leave options, ability to work from home during a family crisis and giving shorter roster cycles.

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 17 of 24

Chapter 4 Barriers to Change

------------------------------------------------------------------------------------------------------------------

1.0 Stakeholders and SBP Strategy

Stakeholders Definition

The stakeholders groups who are affected by the enterprise’s SBP policy are; employees, clients, suppliers, shareholders, community activists, environmental/human rights groups and industry safety associations, Epstein (2008:178).

Positive Effects of SBP Policy

There are positive effects for the SBP policy on each of the key stakeholders can be recorded as follows;

Employees: Enterprise’s employees are given by SBP policy the right for fair pay, incentives and rewards, developing program, employee engagement and a proper work environment.

Clients: Enterprise’s clients are given by SBP policy the right to be treated fairly and ethically.

Shareholders: Shareholders are given by SPB policy a more return on their investment as SBP policy plays a role in increasing employees productivity, reducing the rehiring cost. Besides avoiding the cost of bad reputation and non-compliance with the law and pollution fines, Rubin (2005:2).

Community Activists; SBP policy furnishes the community activists with what they are looking for, as the policy calls for the enterprise contribution in making the community a better place, providing employment, spreading literacy and doing donations, Chakraborty (2010:2).

Environmental Groups; again SBP policy provides the environmental groups with what they are looking for, as the policy calls for enhancing and protecting natural resources and model environmental sustainable practices such as planting and cleaning rivers AECOM (2014:1).

Human Rights Groups; SBP policy satisfies the human rights groups as the policy calls for eliminating the discrimination in respect of employment and occupation, Prandi (2005:188).

Safety Associations; SBP policy satisfies the safety associations, as the policy calls for promoting and protecting the health and safety of the employees and the communities through proactive programs, AECOM

(2014:1).

Negative Effects of SBP Policy

The negative effects of SBP policy might hit the shareholders and clients rather than the other stakeholders.

Shareholders: the only reason to do a business is to create a wealth with the interests of the shareholders and not for the interest of the other stakeholders, Heimann (2008:5,6). SBP policy can results in:

Investing money and resources to take care of the communities and thus reducing the company ability to pursuit the market opportunities comparing with the other companies who are retaining their money and resources for doing business only.

Minimising shares value if the SBP expenditures are greater than that which maximize the firm value, Rubin (2005:22).

Clients: SBP associated costs will be passed on to the clients, Heimann (2008:6).

2.0 Introducing SBP Policy’s Barriers

As mentioned by Collins (2007:6,7,8), there are some barriers to successful implementation of SBP policy as follow;

Internal Inertia: lack of pressure to change towards sustainable practices, because there is no pressure or support internally from the CEO and senior management.

Lack of Understanding and Shared Vision: lack of clear view of the SBP benefits or doubt that they can be realised, because there is a gap in the organization’s SBP knowledge.

Lack of Incentives: lack of incentive for the employees and suppliers to change and adopt new SBP standards.

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 18 of 24

Lack of Training: lack of training for the employees and suppliers due to the existed constraints of training budget or the limited/no access to external SBP specialist.

Lack of Clear Accountability: lack of a clear view around who will do or will be responsible for what. Also TSE (2001:177) added another barrier as follow:

Lack of clients support: lack of client support due to his perception around SBP. Some clients may see SBP, as it is an additional work or compliance burden with little value added.

3.0 How to Overcome the Barriers of Implementation SPB Policy

There are some means can be adopted by the organizations to overcome the barriers towards a successful implementation of SBP policy as follow;

Senior Management Support: CEO and senior managers have to be committed to the sustainability policy by making key decisions for sustainability strategy, Epstein (2008:60). The commitment of the senior managers encourages employees to comply with the sustainability policy, Epstein (2008:50).

Creating Awareness and Understanding: creating awareness can be done by senior managers who have to be knowledgeable about the sustainability practises benefits and challenges and then they have to communicate and share this knowledge alongside the company’s mission, vision, policy and strategy to the other organization’s members. The SBP knowledge can be communicated internally through memos, emails, formal presentation, company intranet and newsletter, Hancock (2008:10-20).

However, if the senior managers have a lack of knowledge about sustainability practices so a third party can be a provider for all the sustainability functions, Epstein (2008:65).

Building Commitment: building a commitment from the company’s employees and suppliers towards SBP policy is the way for a successful SBP implementation. This commitment can be gained as follow;

Employees: providing awards (incentives) to employees for exemplary sustainability performance. Awards will be an opportunity to gain their commitment towards the company sustainability policy, Epstein

(2008:132).

Suppliers: establishing company SBP’s policies. Non-compliance with these policies can lead those suppliers to lose their current contracts and will lead also to lose the potential business opportunity with the company in the future, Epstein (2008:213).

Provide Training Sessions: assigning a budget to provide the employees and suppliers with training sessions that aims to identify the sustainability and its practises, Epstein (2008:214).

Establish Clear Accountability: ensure assigning of SBP goals to the leaders of each business unit and also embed the SBP goals into the roles of employees, CBSR (2010:8).

Get Client Support: ensure client awareness about the benefit of developing their projects to the highest standard of energy efficiency, which could save a great deal of money for the client during the operation period, Forbes (2013:1).

4.0 Effect of SBP Policy on the rest of Supply Chain Introducing Sustainable Business Practice’s policy hasn’t an effect only on clients, employees, shareholders and different activists groups but it has also an effect on the other side of the company’s supply chain such as suppliers of goods/services and subcontractors.

As mentioned by Epstein (2008:213), company’s SBP policy is affecting the suppliers and subcontractors by imposing pressure on them to reduce the negative impacts of their products and services. Suppliers and subcontractors, who are seeking for doing business with company, must follow the company’s SBP policy.

Case Study

As per United Nations Global Compact (2014:1,2), Telenor group, a telecommunication company, has on board a Supply Chain Sustainability Program (SCS) that affected Telenor’s suppliers as follows;

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 19 of 24

SCS set out mandatory supplier requirements for minimum standard of their supplies (products), human rights and environmental protection. Furthermore, the suppliers are required to implement the SCS internally and to extend these requirements to their own supply chains.

More than 16,000 Telenor’s suppliers globally were monitored to make sure their compliance with the Supply Chain Sustainability (SCS) principles and standard. The result of non-compliance may lead to a termination of suppliers’ relationship with Telenor group.

Announced and unannounced inspections and audits are being carrying out at the supplier’s site worldwide.

Suppliers training sessions are carried out by Telenor Group on HSSE (health, safety, security & environment) to develop the suppliers’ awareness on HSSE, especially in Asia where HSSE awareness is lowest.

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 20 of 24

Chapter 5 Measuring and Reporting Performance

------------------------------------------------------------------------------------------------------------------

1.0 KPIs for Measuring SBP Performance

There are key performance indicators, as advised by Epstein (2008:170 to175), for each of the business sustainable practices as follow;

Environment Protection

Fresh water consumption. Percentage of materials recycled. Volume and cost of energy use. Packaging volume. Volume of emissions to air and water. Number and frequency of environmental reports. Number of employees participating in environmental programs.

Employment Practices

Salary gap between gender/races. Number of safety improvements projects. Percentage of women in senior position. Employees’ turn over. Employees’ satisfaction score. Percentage of bonuses earned. Percentage of sick leave used. Average work week hours. Average length of employment. Diversity of workforce.

Ethics Standards

Number of cases of bribery. Result of ethics audits. Number of trade violation. Number of suppliers with sustainability lawsuits.

Financial Return

Number of shareholders complaints. Increased market shares values.

Community Needs

Number of protests. Number of community complaints. Cost of fine and penalties. Community awards received. Local job created. Percentage of workforce in volunteer program. Noise level in community.

2.0 Achieving KPIs and Customer Satisfaction

The cost reduction to the final product’s price is the way for obtaining the customer satisfaction. The said cost reduction can result from achieving company’s KPI as follows;

Achieving Environmental KPIs; Using recycled materials, less packaging, lower energy consumption during the production process, reduced material storage and handling cost and reduced waste disposal can lead to cost reduction to the final product, Epstein (2008:176).

Achieving Community KPIs; Good performance on considering the community needs and expectations can protect the company from the cost of protests, the cost of fines/penalties and the cost of reputation damage. Avoiding the said costs can decline the final product price.

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 21 of 24

Achieving Employment KPIs; Cost savings from employee turnover reduction and expenses of work related accidents can lead to getting a cheaper product.

3.0 Responsibility for Implementation of SBP

The responsibility for ensuring implementation of SBP inside the company laid with the followings parties as advised by Epstein (2008:92 to102);

CEO: CEO commitment towards sustainability is the first step towards successfully implementation of established sustainability strategy. Beside the said commitment, the CEO has to communicate the importance of sustainability to the organization and establishes a culture for integrating sustainability into the daily decision-making, Epstein (2008:253).

Internal Team: an internally dedicated team for sustainability has an important role in functioning of established sustainability systems.

3rd

Party: a third party can assist in SBP strategy formulation and implementation.

NGOs: collaboration with NGOs can improve the sustainability and the financial performance.

4.0 Factors involved in the Process of SBP Implementation

There are some factors have to be involved in the process of SBP implementation as advised by Epstein (2008:253);

Strategy: Sustainability to be a central component of the company strategy.

Commitments: Commitments to be existed by CEO and senior management towards sustainability. The said commitment can be communicated internally by creating a strong mission statement that shows the company’s commitment to sustainability and it encourages the employees to consider sustainability in their daily decisions.

Formal and Informal Process: the formal process such as; performance measurement and rewards systems can be a support for successfully implementing sustainability. Performance management measures the company performance in sustainability and the rewards systems is an incentive tool to encourage the employees to view sustainability performance as critical to the long term financial success of the company. On the other hand, the informal process such as mission, vision and culture can conveys the company interest in sustainability.

5.0 SBP Policy and Addressing Stakeholders Requirements

The SBP policy should help the company to meet the requirements of its stakeholders.

To ensure the SBP policy address stakeholders’ requirement, the company have to have an internal auditing framework to record and evaluate its social and environmental performance, Epstein (2008:237). Among the types of audits are:

Compliance Audit: to assess the company compliance with government regulations, corporate goals and procedures and to monitor, evaluate and control company risks, Epstein (2008:238).

Pollution Prevention Audit: to assess the company ability in minimizing the waste at the source.

Product Audit: to assess whether more efforts should be done to make the company products socially and environmentally friendly.

Another way to ensure the SBP policy address stakeholders’ requirement is performing an external audit, which is considered to be an independent verification and attestation of progress toward improved social and environmental management and performance. 59% of stakeholders want sustainability reports to be verified by a professional body, Epstein (2008:240). The external audit should review the followings;

Company compliance with GRI reporting guidelines. Company performance in health, safety, environment, community investment and ethics. Company approach to stakeholder engagement.

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 22 of 24

6.0 How to Report SBP Performance to Stakeholders and Public

The company produces SBP reports that offer a brief overview of the company’s performance on key sustainability issues to provide basis for stakeholders and general public to assess the company’s sustainability performance and actions. This assessment is a basis for stakeholders before take a decision of making an investment. Also the assessment is a basis for general public to assess the company operation’s effect on their communities.

The SBP performance has to be reported as follows; Channel of Communication: the sustainability performance has to be communicated though different channels of communications such as; press conference, public news papers, media, formal documents and company web sites, Epstein (2008:232). Performance Indicators: the SBP performance indicators have to be provided as follows;

The SBP performance indicators have to be simple, easily collected and readily available.

The SBP performance indicators have to be financial and non-financial ones. Both types are basis for evaluating the company’s current and future performance. For instance: fines and penalties may be a leading indicator of corporate reputation, the amount of company’s toxic emission is a leading measure of future environmental costs and employee turn over is a leading measure of future recruitment and training cots, Epstein (2008:227).

The actual SBP performance indicators have to be provided in the report against the targets performance

indicators or benchmarks such as industry standards in order to enable stakeholders gauge performance by showing whether targets for each of theses indicators were met.

Report; the report of SBP performance should contain more comprehensive information about as advised by Epstein

(2008:228);

Human Rights.

Energy/eco-efficiency.

Health and safety.

Climate protection.

Environmental management of the production process.

Environmental policy.

Corporate governance.

Standards in developing countries.

Bribery and corruption.

Supply chain standards for social issue.

Social policy statements.

Education and Training.

Risk management.

Consumer protection.

Sources of energy used.

Research and development.

Quality management.

Basic business/ financial information.

*****Word Count: 5,940 (references included)

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 23 of 24

References

1- AECOM Official web site, 2014 (viewed 11-10-2014). ‘‘About ‘’ section (online). Available from;

http://www.aecom.com/About

2- AECOM Sustainability Report, 2009 (viewed 20-10-2014). Code of Conducts (online). Available from; http://www.exemplaryenvironments.com/volumeII_issue1/docs/PDDSustainabilityReport2009.pdf

3- AECOM Sustainability Report, 2013 (viewed 20-10-2014). Projects (online). Available from; http://www.aecom.com/deployedfiles/Internet/News/Sustainability/AECOM_2013_Sustainability_Report.pdf

4- AECOM, 2014 (viewed 31-10-2014). Corporate Social Responsibility (online). Available from; http://www.aecom.com/deployedfiles/Internet/About/Social%20Responsibility/CSR/CSR%20Sales%20Sheet_2014_final.pdf

5- Corporate, 2008 (viewed 20-10-2014). Code of Conducts (online). Available from; http://www.google.ae/url?url=http://phx.corporate-ir.net/External.File%3Fitem%3DUGFyZW50SUQ9MjY5NjV8Q2hpbGRJRD0tMXxUeXBlPTM%3D%26t%3D1&rct=j&q=&esrc=s&sa=U&ei=1eRJVP-SLKqV7Abc_IHYBg&ved=0CBIQFjAA&usg=AFQjCNEZFl5RyPE-B1zjym9_lsvQOgOOpA

6- CBSR, 2010 (viewed 25-10-2014). Embedding Sustainability in Organizational Culture (online). Available from; http://nbs.net/wp-content/uploads/CultureReport_v4_F2.pdf

7- Covec, 2007 (viewed 25-10-2014). Recycling: cost benefit analysis (online). Available from; http://91.74.184.67/videoplayer/recycling-cost-benefit-analysis-apr07.pdf?ich_u_r_i=d3c0f77ff080104d120e7c0578a85218&ich_s_t_a_r_t=0&ich_e_n_d=0&ich_k_e_y=1445108925750863502496&ich_t_y_p_e=1&ich_d_i_s_k_i_d=9&ich_u_n_i_t=1

8- Collins, Graham, 2007 (viewed 31-10-2014). Effective CSR Implementation (online). Available from; http://www.cips.org/Documents/Resources/Knowledge%20How%20To/Effective_CSR_v2.pdf

9- Chakraborty, Saheli, 2010 (viewed 31-10-2014). Corporate Social Responsibility and the Society. Business that cares (online).

Available from; http://businessthatcares.blogspot.ae/2010/08/corporate-social-responsibility-and.html

10- Davis Langdon, 2011 (viewed 25-10-2014). Carbon Price on Construction Costs (online). Available from;

http://www.aecom.com/deployedfiles/Internet/Geographies/Australia-New%20Zealand/PCC%20General%20content/Carbon%20Report.pdf

11- Eco. Cycle, 2005 (viewed 25-10-2014). Working to build zero waste communities (online). Available from; http://www.ecocycle.org/files/pdfs/why_recycle_%20brochure.pdf

12- East-West Gateway, 1998 (viewed 25-10-2014). Environmental Benefits of Recycling (online). Available from; http://swmd.net/documents/EnviroBenefitsBroch.pdf

13- Ethisphere, 2014 (viewed 20-10-2014). Engineering and Design (online). Available from; http://ethisphere.com/worlds-most-ethical/wme-honorees/

14- Epstein Marc J. (2008). Making Sustainability Work. 1st ed. UK: Greenleaf Publishing Limited. ISBN-13: 9781906093051.

15- Forbes, 2013 (viewed 31-10-2014). Why CSR? The Benefits Of Corporate Social Responsibility Will Move You To Act (online). Available from; http://supply-chain.unglobalcompact.org/site/article/124

16- Galang, Roberto Martin N, 2011 (viewed 25-10-2014). Doing Business in Corrupt Places (online). Journal of Management Studies. Available from; http://www.strategy-business.com/article/re00141?pg=0

17- Hancock, M. R. (2008). Unit6 – AR50126: Strategy in Construction. United Kingdom: Distance Learning Unit, University of Bath.

18- Heimann, Giles, 2008 (viewed 31-10-2014). Corporate Social Responsibility; Global Standards and Policies in Practice (online).

AR50411 Assignment Name: (Sameh Kandil Mohammed Ibrahim)

Page 24 of 24

Available from; http://www.sswm.info/sites/default/files/reference_attachments/HEIMANN%202008%20PPT%20CSR%20Standards%20and%20Policies%20in%20Practice.pdf

19- IKEA, 2009 (viewed 25-10-2014). SWOT Analysis and Sustainable Business Planning (online). Available from;

http://www.circleinternational.co.uk/circle/strategy_files/ikea%20mrktswot.pdf

20- Meredith Veronica, Rush Penelope, Robinson Elly, 2014 (viewed 25-10-2014). Fly-in Fly-out Workforce Practices in Australia; the effect on children and family relationships (online). Australia: CFCA. Journal of Management Studies. Available from; https://www3.aifs.gov.au/cfca/sites/default/files/cfca/pubs/papers/a146119/cfca19.pdf

21- NSCC, 2007 (viewed 25-10-2014). Reduce, Reuse, Recycle; Managing Your Waste (online). Available from; http://www.nscc.org.uk/docs/general/002fGuidanceonwaste.pdf

22- Prandi, Maria, 2005 (viewed 31-10-2014). Corporate Social Responsibility and Human Rights (online). Available from; http://escolapau.uab.cat/img/programas/derecho/corporate.pdf

23- Rubin, Amir, 2005 (viewed 31-10-2014). Corporate Social Responsibility as a conflict between owners (online). USA: University of California. Available from; http://community-wealth.org/_pdfs/articles-publications/sri/paper-barnes-rubin.pdf

24- TSE, Raymond Y.C. 2001. The Implementation of EMS in Construction Firms; Case Study in Hong Kong. Journal of Environmental

Assessment Policy and Management. 3 (2), 177-194.

25- Unger, Stephen H, 1998 (viewed 25-10-2014). Ethical Aspects of Bribing People in Other Countries (online). USA. Available from; http://www1.cs.columbia.edu/~unger/articles/bribery6-98.html

26- United Nations Global Compact, 2014 (viewed 31-10-2014). Supply Chain Sustainability (online). Available from; http://supply-chain.unglobalcompact.org/site/article/124