kbank investor presentation 4q13 jan2014 final · for further information, please contact the...

TRANSCRIPT

1

KASIKORNBANK

For further information, please contact the Investor Relations Unit or visit our website at www.kasikornbankgroup.com or www.kasikornbank.com

Investor Presentation as of 4Q13

January 2014

2

Consolidated (as of December 2013)Assets Bt2,290bn (USD69.8bn) Ranked #4 with 14.8% market share** Loans* Bt1,439bn (USD43.9bn) Ranked #4 with 14.5% market share** Deposits Bt1,530bn (USD46.6bn) Ranked #4 with 15.0% market share** CAR 15.78% ***ROE 20.45%ROA 1.89%Number of Branches 965Number of ATMs 8,740Number of Employees 19,303

KASIKORNBANK at a Glance

Share InformationSET SymbolShare Capital: Authorized Bt30.5bn (USD0.9bn) Issued and Paid-up Bt23.9bn (USD0.7bn)Number of Shares 2.4bn sharesMarket Capitalization Bt373bn (USD11.4bn) Ranked #2 in Thai banking sector 4Q13 Avg. Share Price: KBANK Bt177.20 (USD5.40) KBANK-F Bt179.52 (USD5.47)EPS Bt17.27 (USD0.53)BVPS Bt91.60 (USD2.79)

KBANK, KBANK-F

Established on June 8, 1945 with registered capital of Bt5mn (USD 0.15mn)Listed on the Stock Exchange of Thailand (SET) since 1976

Notes: * Loans = Loans to customers less Deferred revenue** Assets, loans and deposits market share is based on C.B.1.1 (Monthly statement of assets and liabilities) as of December 2013*** Capital Adequacy Ratio (CAR) has been reported in accordance with Basel III Capital Requirement from 1 January 2013 onwards.

CAR is based on KASIKORNBANK FINANCIAL CONGLOMERATE. KASIKORNBANK FINANCIAL CONGLOMERATE means the company under the Notification of the Bank of Thailand re: Consolidated Supervision, consisted of KBank, K Companies and subsidiaries operating in supporting KBank, Phethai Asset Management Co., Ltd. and other subsidiaries within the permitted scope from the BOT’s to be financial conglomerate

Exchange rate at the end of December 2013 (Mid Rate) was Bt32.81 per USD (Source: Bank of Thailand)

3

Table of ContentsTopic Slide Page

Operating Environment 5 - 6

2014 Financial Targets 7

Composition of Growth 8 - 11

The K-Strategy 12 - 13

Capital and Dividend 14 - 15

Summary 16

Appendix 17 - 125

4

Topic Slide PageKBank

Segment HighlightsStrategyRisk and Credit Management Financial Performance

18-2425-3536-4041-63

• 2013 Highlights• Net Interest Margin• Interest Income - net• Non-interest Income• Net Fee Income• Net Premium Earned - net• Other Operating Expenses• Loan• Asset Quality• Investment in Securities and Funding Structure

42-45464748

49-505152

53-5657-5960-63

The wholly-owned subsidiaries of KBankMuang Thai Life Assurance (MTL)Other Information

64-7172-7980-86

Banking System and Regulation Update 87-94

Government Policy 95-105

Thai Economic Figures 106-123

IR Contact Information and Disclaimer 124-125

Appendix

5

Key Points:

6.52.7 3.0

-5.0-2.01.04.07.0

10.0

2012 2013F 2014F

% Y

oY

Risk Factors:

Source: KResearch (as of January 20, 2014) and **KBank Capital Markets Research (as of January 22, 2014)

Operating Environment: Economic Outlook for 2014 Key GDP Forecasts and Assumptions

Uncertainties in domestic politics

Capital volatility and monetary policy management

Geo-political risks

Due to the current political strife, the 2014 GDP forecast was revised down to 3.0%, with a range of 2.2-3.7%

The ongoing political stalemate will likely shelve a large portion of public investment projects; the private sector is also likely to put its investments on hold

Mounting household debt and eroding confidence may put pressure on private consumption growth in 2014

Nevertheless, recovery in the export sector is expected to be the main economic driving force in 2014, in line with G4 sustained economic improvement

% YoY

Forecast Range

Base Case

GDP 6.5 2.7 2.2-3.7 3.0

Private Consumption 6.7 0.6 0.5-1.8 1.4

Total Investment 13.2 -0.9 1.3-3.3 2.2

Gov't Budget Deficit (% of GDP)* -2.8 -2.4 -1.7 to -2.6 -2.2

Exports 3.1 -0.3 3.0-7.0 5.0

Imports 8.8 -0.9 0.0-4.0 2.0

Current Account (USD bn) -1.5 -4.0 0.4-3.0 1.7

Headline Inflation 3.0 2.2 2.2-2.6 2.4

Policy Interest Rate* 2.75 2.25 2.50-2.75 2.75

2014F2013F2012

6

Government Stimulus Plan (App. pages 95-105)Due to the current political uncertainty, government investment in infrastructure projects, along with other public investment projects, may experience severe delays

Outlook on Europe, the US, China, and ASEAN The global economy is expected to gradually recover and become more stabilized in 2014

Eurozone: already bottomed-out and will modestly recover; structural reforms are yielding positive results, but fragmentation in the Eurozone financial system remains a challengeUS: economic recovery remains resilient. Political settlement regarding the fiscal deal provides optimism toward US economic prospects amid QE taperingChina: substantial economic growth is expected, but may not be as high as during the historic reform period; some uncertainties remainregarding the fragile banking system; however, ongoing reform will likely help sustain the Chinese economy in the longer-term ASEAN economies: recovery will be partly spurred by the regional economic integration. However, QE tapering may pose downside risks to countries with weak external balance, leading to large capital outflows

Outlook on Inflation (App. pages 108 and 110)Headline inflation remains benign in 2014, despite some increased pressure from higher living costs that will be affected by authorities’ plans, such as energy price restructuring

Outlook on Exports and Tourism (App. pages 109 and 111-112)Exports will likely rebound, due to a low base effect and better global economic prospectsRevenue from tourism is likely to cool, in light of a base effect and impacts from domestic political issues

Outlook on CAPEX cycle (App. page 113)A massive investment cycle is not expected until there is a robust recovery in exports; however, there might be new investment in some BOI-promoted industries, i.e. automobile and utility sectors

Impacts from QE tapering (App. page 117-118)Impacts on the Thai economy should be rather modest, given ample domestic liquidity as well as strong external balances e.g. high international reserves and low external debts

Baht (App. page 107)QE tapering began in Jan-14 and will result in a higher premium on the USD and re-pricing of other assets; capital outflows are expected to pick up, pressuring THB sentiment

Operating Environment: Economic Outlook for 2014

Source: KResearch and KBank Capital Markets Research (as of January 22, 2014)

7

Consolidated 2013 Actual 2014 Targets Notes

ROE 20.45% N/A

ROA 1.89% N/A

NIM 3.55% 3.4-3.6% Ranking maintained among large commercial banks (Page 46)

Loan Growth 8.46% YoY 9-11% Decent and sustainable loan growth; in line with economic growth (Page 8 and 53-56)

Non-Interest Income Growth* 18.24% YoY Up to mid-teens Mainly driven by fee income and insurance business (Page 9 and 48-51)

Cost to Income Ratio** 43.74% Mid-40sCost to income ratio continues to range in the mid-40s; seasonally higher in 2H (Page 11)

Credit Cost per year (bps) 85 bps Mid-80s Prudent and aligned with global market environment (Page 10 and 58)

NPL Ratio (Gross)*** 2.11% Below 2.2% Manageable with lingering global economic environment (Page 10 and 57)

2014 Financial Targets

Note: * Non-Interest Income includes Net Premium Earned - net (Net Premium Earned less Underwriting Expenses) from Muang Thai Life Assurance PCL (MTL); KBank has a 38.25% economic interest in MTL; on the

consolidated basis, Bancassurance fees are not included in net fee income, due to the elimination of inter-company transactions (the accounting treatment from the Muangthai Group Holding consolidation); Non-Interest Income = Total operating income – net less Interest income – net

** Cost to Income Ratio = Total Other Operating Expenses to Total Operating Income – net (Total Operating income less Underwriting Expenses)*** NPL Ratio (Gross) = NPL (gross) to total loans; NPL (gross ) used in calculation are loans to general customers and loans to financial institutions of non-performing loans; total loans used in calculation

are loans to general customers and loans to financial institutions

8

31%31%

36%36%

26%26%

7%7%

0

500

1,000

1,500

2012 2013

Other Loans

Retail Loans

SME Loans

Corporate Loans

1,3271,439

Composition of Growth: Loans by Business

Loan Portfolio Loan Portfolio Structure

Note: Since 1Q13, as per the Bank of Thailand’s requirement, the Bank has complied with TFRS 8 (Operating Segments) to present operating results for each key segment in financial reports

(Bt bn)

2013 2014 Outlook

Corporate Loans

Mainly from short-term domestic and trade finance credit with seasonal working capital loan demands with some loan repayment; loans drawn from the real estate, construction, and utilities industries

Growth target on long-term investment and high capacity utilizationindustries with a focus on international trade customers

Focused industries: construction materials, hardware, and automotive & parts

SME

LoansMainly from long-term and short-term credit, and seasonal working capital loan demands, especially from agriculture industry

Growth target reflects demand from domestic consumption andinternational trade benefits from the FTA and AECFocused industries: commerce, construction materials, and hardware

Retail

Loans

Mainly from mortgage loans and credit cards, growth in line withindustry; continued loan growth in all areas, driven by year-end seasonal growth

Conservative growth target, in line with industry

Focus on high yield products (K-Credit Card and K-Express Cash) with effective risk management

Loan growth continues to be decent, sustainable, and in line with economic growth

Loan Definition (more details on loans can be found in App. page 54-55)Corporate Loans: Loans of KBank and KBank’s Subsidiaries in Corporate Segments (Annual sales turnover > Bt400mn)SME Loans: Loans of KBank and KBank’s Subsidiaries in SME Segments (Annual sales turnover ≤ Bt400mn)Retail Loans: Loans of KBank and KBank’s Subsidiaries in Retail SegmentsOther Loans: Loans in Enterprise Risk Management Division (NPL + Performing Restructured Loans), and other loan types

Consolidated %YoY % Yield Loan Growth Dec12 Dec 13 Growth Range Target (Y2014)

2013 2013

Corporate Loans 416 443 6.7% 4-6% 6-8% SME Loans 469 521 10.9% 7-8% 9-11% Retail Loans 347 382 10.3% 6-7% 10-13% Other Loans 95 93 (2.9%) Total Loans 1,327 1,439 8.5% 6.4% 9-11%

Amount (Bt bn)

9

15%

2%0.04%2%

18%16%

60%61%

0

10

20

30

40

50

2010 2011 2012 2013

Other Operating Income

Fee and Service Income - net

Net Premium Earned - net*

Dividend Income

Share of Profit from Investmentson Equity Method

Gain on Investment

Gain on Trading and FXtransactions

4%

2%

64%

0.02%2%

14%

12%

2%

2%

20%

61%

0.4%

16%

2%

14%

3%

2%

0.05%3%

2%

Note:

Non-interest income growth continues to be main driver to help achieving the long-term sustainable profitability; mainly from net fee income and life insurance premiums as a result of customer-centric strategy

2013 non-interest income accounted for 40% of total net operating income and net fee income accounted for 24%; Net fee income in 2013 rose mainly through card business and fees from mutual fund and brokerage businesses

2014 non-interest income growth will be up to mid-teens, mainly driven by net fee income and life insurance premiums

Composition of Growth: Net Fees and Non-interest Income

29.44

20.6418.23

24.47

0

10

20

30

2010 2011 2012 2013

(Bt bn)

60%61%62%

62%

40%

38%38%

39%

0

40

80

120

2010 2011 2012 2013

Net Interest Income Non-interest Income

(Bt bn)40%39%38%38%

24%23%23%24%

0

10

20

30

40

50

2010 2011 2012 2013

Non-interest Income Ratio Net Fee Income Ratio

December 2013 (Consolidated)

Total Operating Income - net

Non-interest Income

(Bt bn)

28.40

34.02

40.72

Net Fee Income

(+13%)

(+19%)

Non-interest Income Ratio and Net Fee Income Ratio

75.1490.51

104.31

(+20%)(+15%)

(+22%)

(+14%)(+31%)

(+20%)

(+20%)

- Non-interest Income Ratio = Non-interest Income/Total Operating Income - net - Net Fee Income Ratio = Net Fee Income / Total Operating Income – net- Net Premium Earned - net = Net Premium Earned less Underwriting Expense

(%)120.95(+16%)

48.15(+18%)

(+20%)

10

December 2013 (Consolidated)

(Bt bn)

Coverage Ratio(%)

Asset Quality and Impairment Loss of Loans and Debt Securities (Provision)

(bps)(%)

Provision

NPL Ratio and Credit Cost

Asset quality remains stable and manageable

2013 NPL was at 2.11% with a coverage ratio of 134.52%

2013 credit cost is 85bps, to reflect a countercyclical provision policy

2014 asset quality is expected to remain stable with credit cost to be in the mid-80s bps

3.75.4 5.9

7.89.4

6.7 7.38.4

11.7

0

4

8

12

2005 2006 2007 2008 2009 2010 2011 2012 2013

131.83 134.52127.12

111.0291.64

88.38

73.9070.9666.60

0

50

100

150

2005 2006 2007 2008 2009 2010 2011 2012 2013

85

6083 82

93 102

66 64 66

6.85

8.88

2.162.453.76

3.09

4.44

2.912.11

0

2

4

6

8

10

2005 2006 2007 2008 2009 2010 2011 2012 2013

0

50

100

150

200

Credit Cost

NPL ratio

11

2.422.472.632.61

0

2

4

6

2010 2011 2012 2013

43.7445.0050.5750.9247.53

0

10

20

30

40

50

60

70

2009 2010 2011 2012 2013

Cost to Income Ratio

(%)

Cost to Income Ratio Cost to Average Assets Ratio

(%)

2009 2010 2011 2012 2013 1Q13 2Q13 3Q13 4Q13Cost to Income Ratio (%) 50.92 50.57 47.53 45.00 43.74 40.02 42.65 43.63 48.40

Cost to Average Assets Ratio (%) n.a. 2.61 2.63 2.47 2.42 2.19 2.41 2.42 2.63

December 2013 (Consolidated)

Cost to income ratio continues to range in the mid-40s; seasonally higher in 2H

2013 cost to income ratio was 43.74% as the Bank carefully monitored spending in response to economic uncertainty

2014 cost to income ratio will be stable in the mid-40s

12

The K-Strategy

Strategic Capabilities

PRODUCT & SOLUTIONInnovate & be responsive

PRODUCT & SOLUTIONInnovate & be responsive

SERVICE QUALITYExcellent customer experience

at all channels

SERVICE QUALITYExcellent customer experience

at all channels

BRANDING & MARKETINGClear & consistent communication

BRANDING & MARKETINGClear & consistent communication

Customer Centricity

Customer Strategy

4 Product Domains8 Customer Segments*

The Way We Work

Long-Term Risk-Adjusted Sustainable Profitability

TO BE CUSTOMER’S MAIN BANK

Innovative & Managing Products

Understanding Customer Needs

Sales & Service Excellence

Proactive Risk Management

KASIKORNBANK, its wholly-owned subsidiaries, and its strategic partner

I N T E G R A T I O N

Note: * The definition of the eight customer segments can be found in App. page 26

+

13

2.82

1.69

2.80

2.15

2.632.78 2.81

2.71

1

2

3

2007 2008 2009 2010 2011 2011(New)

2012(New)

9M13(New)

26%

18%

25%24%

17%23%

24%

27% 27%28% 29%

14%

12%11%10%

5%

10%

15%

20%

25%

30%

2008 2009 2010 2011 2012

Segment Performance Highlights

Average Product Holdings per CustomerMain Bank Status*

** In 2012, the Average Product Holding calculation is adjusted in all eight customer segments to align with our better understanding of customer behavior; 2011 numbers were restated for comparison purposes

Old Definition New Definition**

(Overall)

(By Business Division)

Corporate Business

SME Business

Retail Business

Main Bank Status and Market Penetration increased on track with our customer segment aspirations

Overall Customer Satisfaction

Overall Customer Satisfaction****

*** Customers in Retail Business Division (RBS) account for 97%, SME Business Division (SME) 3%, and Corporate Business Division (CBS) less than 1% of customer portfolio

**** Customer Satisfaction Index are calculated using the weighted average of customer satisfaction index from our eight customer segments; our retail customer satisfaction exceed the World Finance Industry Norm

No. of Customers (mn)***

* Main Bank Status = % of customers in the market who use KBank and its wholly-owned subsidiaries as their main operating bank and/or main saving and investing bank and/or main borrowing bank

Performance improvement driven by the success of our customer-centric strategy and new IT capabilities

Average product holdings per customer increasing as a result of enhanced cross-selling capabilities

Overall average rose to 2.82 in 9M13, from 2.71 in 2011

No. of customers grew 66% since 2007

No. of customers grew 5% YTD in 9M13

Overall Customer Satisfaction was at 85 in 2012

6.9 7.5 8.0 9.0 10.0

10.911.5

83 85 85 86 86 85

0

20

40

60

80

100

0

5

10

15

2007 2008 2009 2010 2011 2012 9M13

No. of Customers (mn) Overall Customer Satisfaction

2.172.66 2.82 2.862.67

3.12 3.11 3.30 3.54

4.55

2.812.722.78

1.71

2.963.05

2.562.142.122.101.831.44

4.41 4.59

0

5

10

2007 2008 2009 2010 2011 2011(New)

2012(New)

9M13(New)

Retail Business SME Business Corporate Business

14

Bank only KASIKORNBANK FINANCIAL CONGLOMERATE*

Capital (Reported Number: Excluding Net Profit of Each Period)

Capital adequacy remains sufficient to support business growth; maintained adequate Tier 1 ratio, as required under the Basel III

December 2013

Under Bank of Thailand regulations, net profit in the first half of the year is to be counted as capital after approval by the Board of Directors as per the Bank’s regulations. Net profit in the second half of the year is also counted as capital after approval of the General Meeting of Shareholders. However, whenever a net loss occurs, the capital must be immediately reduced accordingly.

Note: * KASIKORNBANK FINANCIAL CONGLOMERATE means the company under the Notification of the Bank of Thailand re: Consolidated Supervision, consisted of KBank, K Companies and subsidiaries operating in supporting KBank, Phethai Asset Management Co., Ltd. and other subsidiaries within the permitted scope from the BOT’s to be financial conglomerate.

** The details on Basel III regulations can be found in App. Page 90-91

12.579.13 9.57 10.44

5.20

3.844.27

0

3

6

9

12

15

18

2010 2011 2012 2013Tier1 Tier2

(%)

13.40 13.41

15.6415.78

3.21

12.029.37 9.63 10.43

5.554.184.59

0

3

6

9

12

15

18

2010 2011 2012 2013Tier1 Tier2

(%)

13.96 13.81

15.98

3.23

15.25

Basel II Basel III Basel II Basel III

Basel III2010 2011 2012 2013 1Q13 2Q13 3Q13 4Q13

Bank onlyCAR (%), excluding net profit of each period 13.96 13.81 15.98 15.25 15.44 15.71 16.72 15.25Tier 1 (%), excluding net profit of each period 9.37 9.63 10.43 12.02 11.08 11.44 12.50 12.02

KASIKORNBANK FINANCIAL CONGLOMERATE

CAR (%), excluding net profit of each period 13.40 13.41 15.64 15.78 15.79 16.20 17.31 15.78Tier 1 (%), excluding net profit of each period 9.13 9.57 10.44 12.57 11.47 11.97 13.13 12.57

Basel IIIBasel II

15

Dividend

2004 2005 2006 2007 2008 2009 2010 2011 2012 1H13Dividend Per Share (Bt) 1.00 1.25 1.75 2.00 2.00 2.50 2.50 2.50 3.00 0.50

Dividend Payout Ratio (%) 15.45 21.36 30.55 31.88 32.33 42.49 32.14 27.00 22.12

Dividend policy: both operating results and long-term returns to shareholders are taken into consideration in determining dividend paymentsDividend payout ratio ranges 20-25%, in order to ensure a sustainable and adequate capital level through the changing economic environment and the ongoing adoption of Basel III

22.1227.00

32.14

15.4521.36

30.55 31.88 32.33

42.49

0

10

20

30

40

50

2004 2005 2006 2007 2008 2009 2010 2011 2012

(%)

Dividend Payout RatioDividend Per Share

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2004 2005 2006 2007 2008 2009 2010 2011 2012 1H13

(Bt)

1.001.25

1.752.00 2.00

2.50

Interim Dividend

2.50 2.50

3.00

Interim Dividend

0.50

16

Summary

Customer-centric strategy effectively executed: the data-mining, analytic campaign management, and multi-channel sales and services platform have enhanced our capability to quickly acquire new customers; the result is a top-notch total customer experience and strong market position

Balanced growth: loans to grow carefully in line with economic condition; appropriate liquidity maintained; asset quality sustained; appropriate loan loss reserves; strong non-interest income growth; stable cost to income ratio; strong ROE maintained

Adequate capital: maintained adequate Tier 1 ratio, as required under the Basel III

17

Appendix

18

KBank: Segment Highlights

19

Performance and Market PositionMain Bank Status: maintained #1 ranking

Trusted Partner Bank: aim to be #1 through comprehensive fund raising solutions, integrated cash management solutions, and value chain solutions

Outright Trading Volume of Corporate Bonds: ranked #1 with 27% market share in 2013

Corporate Bond Underwriting: ranked #4 with 11% market share in 2013

Syndicated Loan Arranging: leading position with acclaimed expertise in power and petrochemical sectors

Transaction Services: a top player in transactional banking services

Security Services (MFS): 39% market share in November 2013

Cash Management Services: 24% market share in 2013

Trade Finance: 31% market share in 2013

Industrial Expertise: leverage capability in utility, real estate, transportation, and commerce, etc; in 2012 our executives were invited to speak at seminars

on green business and urbanization

Knowledge-based Organization: strive to be a knowledge-based organization for family business (KFAM Club, and Family Business Open Up)

23%

19%21%

23% 24%

0%

10%

20%

30%

2009 2010 2011 2012 2013

25%23% 24%26% 26%

0%

10%

20%

30%

2009 2010 2011 2012 2013

14%18%

15%17%

11%

0%

10%

20%

30%

2009 2010 2011 2012 2013

Corporate Business: Performance and Market PositionMulti-Corporate

BusinessLarge Corporate

BusinessMedium Business

Small and Micro Business

High Net WorthIndividual

MiddleIncome

Mass

Corporate Bond Underwriting

Affluent

Source: ThaiBMA

Main Bank Status

Source: KBank Customer Survey

Cash Management Services

Source: KBank Customer Survey

Note: Main Bank Status = % of customers in the market who use KBank and its wholly-owned subsidiaries as their main operating bank and/or main savings and investing bank and/or main borrowing bank

(#1) (#1) (#1) (#1)(#2) (#2) (#3) (#2)

(#2) (#2) (#2) (#2)

(#4)

(#1)(#2)

20

30%27% 29%

30%

0%

10%

20%

30%

2009 2010 2011 2012

28%27% 27%29%

0%

10%

20%

30%

2009 2010 2011 2012

Multi-Corporate Business

Large Corporate Business

Medium Business

Small and Micro Business

High Net WorthIndividual

MiddleIncome

MassAffluent

SME Business: Performance and Market Position

Performance and Market PositionMain Bank Status: strengthened #1 position by acquiring new trade credit customers and offering effective cross-selling cash management solutions and packages

Market Share: maintained at 30% in 2012; improved from 29% in 2010 to 30% in 2011

Market Position: strengthened #1 position in SME market – “Bank for SMEs”; targeted to be SME market leader in all areas

Improved capital usage efficiency by increasing total income to loan ratio

Only bank to offer a 2-day credit approval process for small and micro SMEs, with receipt of funds within 5 days

Only bank to offer comprehensive solutions to SMEs through K SME Care program (launched in 2006, with a total of 19 classes and about 10,000 participants so far) and K SME Care Knowledge Center (established in 2009)

#1 in Market Share by Value #1 in Main Bank Status

Source: KBank Customer Survey (updated annually)

(#1)

Source: KBank Customer Survey (updated annually)

(#1)(#1)(#1) (#1)

(#1)(#1)(#1)

Note: - SME Business in Thailand accounts for 37.0% of Thailand’s GDP, or Bt4.2trn; 2.73 million SME customers with 0.66 million registered as legal entities (as of December 2012);supported by the government to become a key factor in economic and social growth (Source: The Office of Small and Medium Enterprises Promotion or OSMEP)

- Market Share by Value = share of revenue (derived from both credit and non-credit products) that each bank gains from the market - Main Bank Status = % of customers in the market who use KBank and its wholly-owned subsidiaries as their main operating bank and/or main savings and investment bank and/or

main borrowing bank

21

9.2%9.4%8.8%

7.7%9.6%

0%

5%

10%

15%

2009 2010 2011 2012 9M13

25.7%23.5%

20.5%15.8%

25.0%23.9%

19.2%

16.1%

22.1% 22.3%

0%

5%

10%

15%

20%

25%

30%

2009 2010 2011 2012 9M13

NewBusiness

TotalPremium

23.1%24.3%23.7%

20.8%

25.5%

0%

10%

20%

30%

2009 2010 2011 2012 2013

#1 in Mutual Fund (KAsset)

Multi-Corporate Business

Large Corporate Business

Medium Business

Small and Micro Business

High Net WorthIndividual

MiddleIncome

Mass

Mortgage Loan

Affluent

Retail Business: Performance and Market Position

(% Market Share) (% Market Share) (% Market Share)

#1 in Bancassurance*(Total Premium and New Business Premium)

Performance and Market PositionMarket Penetration: strong market penetration to affluent customers, with 81% penetration in Nov13 (continual increase from 40% in 2010)Bancassurance: MTL held #1 position in Bancassurance total premium with 23.9% market share, and Bancassurance new business premium with 25.7% market share in 9M13; MTL also held #1 position for new business premium of life insurance industry with 18.7% market share in 9M13Fund Management Service:

Mutual Funds: KAsset maintains #1 position, with Gold Winner Award from Reader’s Digest Most Trusted Brand for 6th consecutive year and two Best Mutual Fund of the Year 2013 Awards by Money & Banking magazineMutual Funds + Private Funds + Provident Funds: maintains #1 position, with highest total AUM for the 5th consecutive year

Mortgage Loans: ranked in top 3, with 9.2% market share in 9M13; conservative growth (in line with industry) and maintaining a good quality portfolioCredit Cards:

Total spending: ranked #1 , with highest spending volume of Bt234bn or 20.8% market share in 11M13Number of cards: ranked #2, with 3.02mn cards in November 2013 Card-accepting merchant services (such as EDC, payment gateway, etc.): ranked #1, with 34.9% market share by volume in 11M13

Debit Cards: Maintain leader position to match customer lifestyles, with the launch of Character Card (latest offering with LINE Sticker Set) and Provincial Debit CardHighest debit card spending in the industry, at Bt7,000/active card/month

Digital Banking: Market leader, with 33% market share of Thailand Digital Banking users (Bank of Thailand report, Sep 2013) #1 Digital Banking top of mind Brand perception rating (Nielsen, 2012)

(#2)

(#1) (#2)(#1)

(#2)(#2)

(#2)

(#2)(#1)(#1)

Ranked # 1 in both total and new business premium

Ranked #1 in Mutual Fund AUM (KAsset)

(#2)

(#1)(#1)(#1) ( #1)

(#3) (#3)(#2) (#3)

(#3)

Maintaining good quality portfolio with lowest %NPL ratio among leading commercial banks

Note: * Total Premium = New Business Premium (NBP) + Renewal Premium; New Business Premium = First Year Premium (FYP) + Single Premium (SP)

22

34

262321 24

0

20

40

2009 2010 2011 2012 2013

145117

9587114

0

50

100

150

200

2009 2010 2011 2012 2013

866

12

8

0

5

10

15

20

2009 2010 2011 2012 2013

63636160 62

0

15

30

45

60

75

90

2009 2010 2011 2012 2013

Corporate & SME Service Centers

Channels: Corporate and SME Business

Corporate Business Centers* SME Business Center**

Cheque Direct Service Office

Customer facilitation in areas with good potential, via the opening of financial service centers and cheque points

* Reduction in the number of centers was a result of consolidation of some centers** Excluding Corporate & SME Service Centers; in one branch, there could be more than one SME Business Centers

Note:

23

8,7407,6037,4716,955 7,366

9,394

0

1,500

3,000

4,500

6,000

7,500

9,000

10,500

2009 2010 2011 2012 2013 2014F

835869 883

3096

262

400

600

800

1,000

1,200

2009 2010 2011 2012 2013 2014F

Branch ATM

(+11)

Channels: Retail Business

(+120) (+23)

(+1,853)(+516)

185

126

9977

103

252

0

40

80

120

160

200

240

280

2009 2010 2011 2012 2013 2014F

K-Lobby ***

(+33)(+22)

(-105**)

* “New Branch Model” is a new modern-lifestyle branch model aiming to provide more convenience to targeted customers. This type of branch is designed to be smaller in size and equipped with an electronic banking machine and a small staff; hence, it is cost efficient to operate

(+4)

(+237)

(+23)

782 805 816865

(+34)

965(+1,137)

(+59)

(+66)

New Branch Model*

*** K-Lobby is an electronic banking service with multiple functions such as K-ATM, K-CDM (Cash Deposit Machines), and K-PUM (Passbook Update Machine). K-Lobby is available to serve customers both outside of branch offices and as stand-alone machines in areas without branches

(+100)

Note:

(+19)

(+30)

2009 2010 2011 2012 2013Branch 782 805 816 865 965 - Bangkok and Metro 46% 46% 46% 45% 42% - Upcountry 54% 54% 54% 55% 58%ATM 6,955 7,471 7,366 7,603 8,740 - Bangkok and Metro 52% 51% 52% 51% 48% - Upcountry 48% 49% 48% 49% 52%xxCDM 973 1,014 1,067 1,398 2,195 - CDM (Deposit) 973 1,014 1,016 1,066 1,138 - CDM (Deposit & Withdraw) 51 332 1,057K-Lobby 77 99 103 126 185

The WISDOM Centers and Corners 31 36 75

** A drop in the number of ATMs reflected a relocation plan

1,145(+180)

(+654)(+67)

(+14)

(+166)(+49)

Key Strategies in Channel ExpansionBranch: provide customer service

Increase number of branches to 1,145 by year-end 2014 (including “new branch model”)

Expand branch and “new branch model” to potential areas for high competitiveness

Expand branch size in high traffic/strategic areas to better serve customers

Relocate low use branches to more convenient areas

E-Channel: provide customer convenience

#1 in number of Cash Deposit Machines (CDMs) in Thailand; utilize duo-function CDMs(deposits & withdrawals) to increase efficiency, enhance service coverage and improve customer convenience

#1 in number of K-Lobby in Thailand; increase number of K-Lobby to 252 in 2014

Relocate ATMs to provide more convenient service to customers

24

Branch

Sample of Channels

K-Lobby

A new modern-lifestyle branch model aiming to provide more convenience to targeted customers. This type of branch is designed to be smaller in size and equipped with an electronic banking machine and a small staff; hence, it is cost efficient to operate

An electronic banking service with multiple functions such as K-ATM, K-CDM (Cash Deposit Machines), and K-PUM (Passbook Update Machine). K-Lobby is available to serve customers both outside of branch offices and as stand-alone machines in areas without branches

New Branch Model

THE WISDOM Center and Corner

An exclusive center providing a full range of services and facilities to the High Net Worth Individual and Affluent segments

Digital Banking

Sample of Digital Banking

• K-Mobile Banking

• K-Cyber Service (K-Cyber Banking, K-Cyber Trade and K-Cyber Invest)

• K-Payment Gateway

• K-PowerP@y (mPOS)

THE WISDOM Lounge @ Sofitel So Bangkok

Branch @ Department Stores Mini Branch @ BTS

25

KBank: Strategy

26

Eight Customer Segments Multi-Corporate Business

Large Corporate Business

Medium Business

Small & Micro Business

High Net Worth Individual

Co

rpo

rate

B

usi

nes

sS

ME

B

usi

nes

sR

etai

l Bu

sin

ess

Ret

ail

Bu

sin

ess

Company with annual sales >Bt5,000mn

Company with annual sales >Bt400mn to Bt5,000mn

Individual or company with annual sales >Bt50mn to Bt400mn

Individual or company with annual sales ≤ Bt50mn, and with commercial credit limit ≤ Bt15mn

Individual wealth with KBank and its wholly-owned subsidiaries* ≥ Bt50mn

Individual wealth with KBank and its wholly-owned subsidiaries* ≥ Bt15,000 to < Bt10mn

Individual wealth with KBank and its wholly-owned subsidiaries* < Bt15,000

Note: * Wealth with KBank and its wholly-owned subsidiaries is defined as savings and investments, such as deposit products with KBank, mutual funds with KAsset; or the monthly income of an individual customer

Affluent

Middle Income

Mass

Individual wealth with KBank and its wholly-owned subsidiaries* ≥ Bt10mn to < Bt50mn

Customer-centric strategy: offering a full array of financial solutions and a satisfying experience to our customers

Synergistic portfolio management by monitoring eight customer segments Offer financial solutions from among KBank, its wholly-owned subsidiaries, and the insurance companyMake significant progress towards long-term aspirations; performance on track

27

Revenue by Eight Customer Segments

Note: Loan portion and loan yield of each customer segment includes loans from the Enterprise Risk Management Division (NPL + Performing Restructured Loans); figures are not comparable with loan data in other pages

Non-interest income *

0.5%

22.7%

3.5%0.3%

18.2%

21.8%

16.9%

16.1%

Loan

Portion

Average

Loan Yield (%)

High Network

4%

Multi-Corporate Business

13%

Small & Micro

Business 15%

Medium Business

12%

Large Corporate Business

9%

Mass10%

Middle Income

28%

Affluent9%

* Non-interest income excludes capital market business, treasury business and others

4.4%

6.5%

7.1%

9.4%

4.5%

9.6%

4.5% 5.5%

Large Corporate Business

Medium Business

Small & Micro Business

High Net Worth Individual

Affluent

Middle Income

Mass

Multi-Corporate Business

December 2013

28

K-Transformation Foundation Capabilities

Information Technology

Capital (ITC)

Financial Information

System (FIS)

Know Our Customers

(KOC)

Multi-channel

Sales And Services

(MSS)

K-Transformation Supporting Solution (KSS)

Innovative & Managing Products

Understanding Customer Needs

Sales & Service Excellence

Strategic Capabilities

Proactive Risk Management

K-Transformation Project

Implementing: completion expected by

2015

Implemented

29

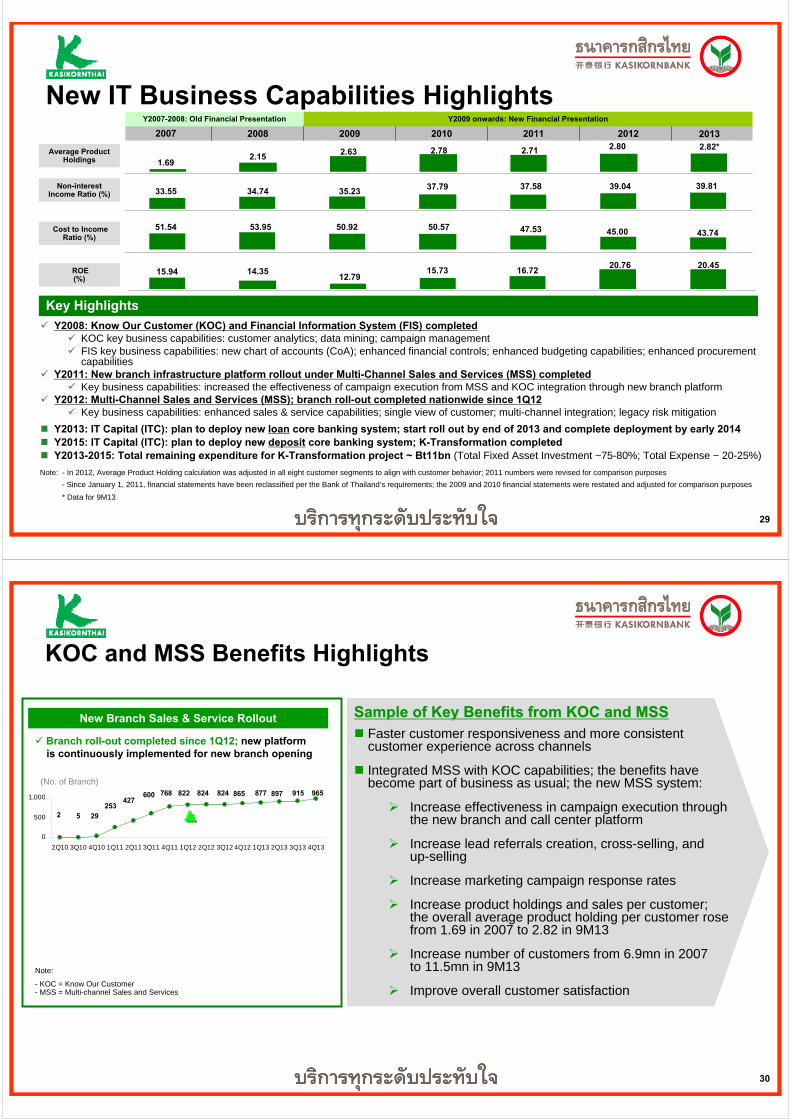

2007 2008 2009 2010 2011 2012

- In 2012, Average Product Holding calculation was adjusted in all eight customer segments to align with customer behavior; 2011 numbers were revised for comparison purposes

- Since January 1, 2011, financial statements have been reclassified per the Bank of Thailand’s requirements; the 2009 and 2010 financial statements were restated and adjusted for comparison purposes

1.692.15

2.71

51.54

2.782.63

47.5350.5750.9253.95

39.0435.23

39.8134.7433.55

Average Product Holdings

Non-interest Income Ratio (%)

Cost to Income Ratio (%)

14.3512.79

15.7315.94 16.72ROE (%)

2.80

37.58

45.00

20.76

Y2007-2008: Old Financial Presentation Y2009 onwards: New Financial Presentation

Note:

37.79

43.74

20.45

2013

Key Highlights

Y2008: Know Our Customer (KOC) and Financial Information System (FIS) completedKOC key business capabilities: customer analytics; data mining; campaign managementFIS key business capabilities: new chart of accounts (CoA); enhanced financial controls; enhanced budgeting capabilities; enhanced procurement capabilities

Y2011: New branch infrastructure platform rollout under Multi-Channel Sales and Services (MSS) completedKey business capabilities: increased the effectiveness of campaign execution from MSS and KOC integration through new branch platform

Y2012: Multi-Channel Sales and Services (MSS); branch roll-out completed nationwide since 1Q12Key business capabilities: enhanced sales & service capabilities; single view of customer; multi-channel integration; legacy risk mitigation

New IT Business Capabilities Highlights

2.82*

* Data for 9M13

Y2013: IT Capital (ITC): plan to deploy new loan core banking system; start roll out by end of 2013 and complete deployment by early 2014Y2015: IT Capital (ITC): plan to deploy new deposit core banking system; K-Transformation completedY2013-2015: Total remaining expenditure for K-Transformation project ~ Bt11bn (Total Fixed Asset Investment ~75-80%; Total Expense ~ 20-25%)

30

KOC and MSS Benefits Highlights

Faster customer responsiveness and more consistent customer experience across channels

Integrated MSS with KOC capabilities; the benefits have become part of business as usual; the new MSS system:

Increase effectiveness in campaign execution through the new branch and call center platform

Increase lead referrals creation, cross-selling, and up-selling

Increase marketing campaign response rates

Increase product holdings and sales per customer; the overall average product holding per customer rose from 1.69 in 2007 to 2.82 in 9M13

Increase number of customers from 6.9mn in 2007 to 11.5mn in 9M13

Improve overall customer satisfaction

Sample of Key Benefits from KOC and MSSSample of Key Benefits from KOC and MSS

965915897824824822768600427

2532952

865 877

0

500

1,000

2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13

(No. of Branch)

New Branch Sales & Service Rollout

Branch roll-out completed since 1Q12; new platform is continuously implemented for new branch opening

Note:

- KOC = Know Our Customer- MSS = Multi-channel Sales and Services

31

New IT Business Capabilities

New Core Banking System on Loans- Open possibilities to capture new business

opportunities- Help shorten product development time - Enhance product innovation capability

New Branch Sales & Service and Call Center System Enhancement- Create unique and consistent customer

experience across channels including new infrastructure

- Enhance cross selling capability via diverse sales and service channels

New Core Banking System on Deposits - Start to deploy legacy system in multiple

groups to mitigate risk of big bang deployment

Key Deliverables and Benefits in 2013Key Deliverables and Benefits in 2013--20142014

Develop a constructive and harmonious corporate culture; new IT platform to provide unique tools to support our customer-centric strategy; overcoming IT obstacles makes KBank a leader among peers

LongLong--term Strategic Positioningterm Strategic PositioningThe K-Transformation project is expected to be completed by 2015

A new core banking system, the last capability enhancement under the K-Transformation project, consists of new loan and deposit core banking systems

New capabilities will help enhance new product development capability, shorten product development time, and significantly reduce maintenance costs in the long-term; as well as open possibilities to capture new business opportunities

Gradual deployment of the K-Transformation project will make the project KBank’s new standard business system platform; the project budget will be included as a part of KBank’s regular annual IT budget

KBank’s cost to income ratio will range in the mid-40s

June 2013: changes to some parts of deposit core banking system development

New deposit core banking vendor provides more benefits in the long-term, including faster data processing, mitigated risk concerning for staff competence in maintaining system stability, and reduction in maintenance costs

New capabilities will help enhance new product development capability, shorten product development time, and significantly reduce maintenance cost in the long term

End 2013 to early 2014: Plan to deploy on new loan accounts, with gradual deployment to mitigate new technology system risk; deployment for all loan accounts will be completed by early 2014

End 2015: Plan to deploy new deposit core banking system to complete the K-Transformation project

32

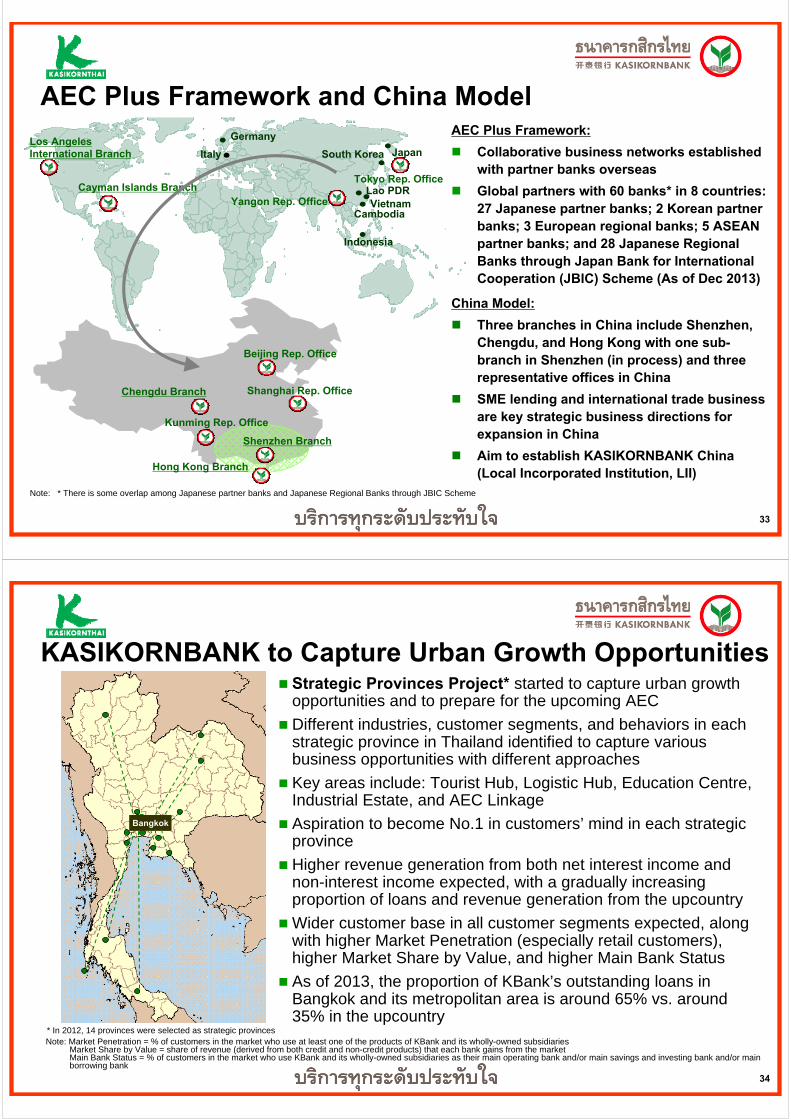

KASIKORNBANK to Capture AEC Opportunities

Note: 1. Size of economy for 2013 from IMF and compiled by KResearch (as of October 15, 2013)2. 2014 GDP forecast is projected by KResearch (as of January 20, 2014) 3. ASEAN economic growth are averaged growth among ASEAN member countries in national currencies4. Greater Bangkok includes Nonthaburi, Samut Prakarn, Nakorn Pathom, Samut Sakhon, and Patumthani

GDP Thailand ASEAN

Size of Economy (GDP) in USD Trillion for 2013 0.38 3.30

2014 GDP Forecast 3.0% 5.5%

Contribution to GDP (by NESDB) 2012 Y2015F

Greater Bangkok : Provinces 44 : 56 42 : 58

KBank has 5 international branches (Los Angeles, Cayman Islands, Hong Kong, Shenzhen, and Chengdu), and 5 representative offices (Beijing, Shanghai, Kunming, Tokyo, and Yangon)

ASEAN Economic Community (AEC): ASEAN member countries to become a single market by 2015; free flow of goods & services and non tariff barrier among 10 member nationsGreater opportunities available through ASEAN + 3 (China, Japan, and South Korea)To capture AEC opportunities, KBank continues to enhance business in

International TradeBorder TradeCross Border Investment Retail Customer (Tourist / Expatriate / Transit)Host Country Business

Higher revenue generation and expansion of customer base“AEC Plus” framework is established to cover ASEAN, China, Japan, and Korea through our presence and collaborative business networks with partner banksChina model developed to ensure KBank’s presence in China

33

AEC Plus Framework and China ModelGermany

Italy

Indonesia

Japan South Korea

VietnamLao PDR

Cambodia

Beijing Rep. Office

Kunming Rep. Office

Shenzhen Branch

Chengdu Branch Shanghai Rep. Office

Hong Kong Branch

Los Angeles International Branch

Yangon Rep. Office

Tokyo Rep. OfficeCayman Islands Branch

Note: * There is some overlap among Japanese partner banks and Japanese Regional Banks through JBIC Scheme

AEC Plus Framework:

Collaborative business networks established with partner banks overseas

Global partners with 60 banks* in 8 countries: 27 Japanese partner banks; 2 Korean partner banks; 3 European regional banks; 5 ASEAN partner banks; and 28 Japanese Regional Banks through Japan Bank for International Cooperation (JBIC) Scheme (As of Dec 2013)

China Model:

Three branches in China include Shenzhen, Chengdu, and Hong Kong with one sub-branch in Shenzhen (in process) and three representative offices in China

SME lending and international trade business are key strategic business directions for expansion in China

Aim to establish KASIKORNBANK China (Local Incorporated Institution, LII)

34

KASIKORNBANK to Capture Urban Growth Opportunities

Bangkok

Note: Market Penetration = % of customers in the market who use at least one of the products of KBank and its wholly-owned subsidiaries Market Share by Value = share of revenue (derived from both credit and non-credit products) that each bank gains from the market Main Bank Status = % of customers in the market who use KBank and its wholly-owned subsidiaries as their main operating bank and/or main savings and investing bank and/or main borrowing bank

* In 2012, 14 provinces were selected as strategic provinces

Strategic Provinces Project* started to capture urban growth opportunities and to prepare for the upcoming AEC

Different industries, customer segments, and behaviors in each strategic province in Thailand identified to capture various business opportunities with different approaches

Key areas include: Tourist Hub, Logistic Hub, Education Centre, Industrial Estate, and AEC Linkage

Aspiration to become No.1 in customers’ mind in each strategic province

Higher revenue generation from both net interest income and non-interest income expected, with a gradually increasing proportion of loans and revenue generation from the upcountry

Wider customer base in all customer segments expected, along with higher Market Penetration (especially retail customers), higher Market Share by Value, and higher Main Bank Status

As of 2013, the proportion of KBank’s outstanding loans in Bangkok and its metropolitan area is around 65% vs. around 35% in the upcountry

35

Strategic Provinces Project: Highlights in 2013*

Corporate Business Total income earned from corporate customers in strategic provinces increased 12% YoY in 10M13Successfully launched events to keep a strong relationship with Big Family (Phuket) Created Marketing Activities for corporate customers such as Professional Family Business Management and Business Matching Activities

SM

E

Bu

sin

ess

SME BusinessTotal income earned from SME customers in strategic provinces increased 9% YoY in 10M13Opened six SME hubs in strategic provincesBuilt K-SME brand awarenessLaunched localized marketing campaigns, including brand selling and retention programs, to serve customer needs in each strategic province

Co

rpo

rate

B

usi

nes

s

KBank, its wholly-owned subsidiaries, and Muang Thai Life Assurance (MTL) aim to offer a full range of financial solutions based on customer-centric strategy to capture business in strategic provinces

Ret

ail

Bu

sin

ess

Note: * In 2013, 15 provinces were selected as strategic provinces for corporate and SME customers; 19 provinces were selected as strategic provinces for retail business

Retail BusinessSince launching the strategic province project, the number of retail customers has grown continuously by a total of 23% in 2013, with significant growth particularly in High Net Worth Individual and Affluent segmentsStrengthen KBank infrastructure through new branches and THE WISDOM lounge opening in strategic provinces Massive acquisition and customer engagement with effective marketing communication by launching localized offerings, events, campaigns, and privileges to match customer lifestyles and needs such as Joyful Festival, Provincial Debit Card, Localized Privileges, and Exclusive Experience Activities for high value customers

36

KBank: Risk and Credit Management

37

KBank Risk Management StructureThe Bank’s organization is structured to facilitate all aspects of risk management; each business unit’s responsibilities and segregation of duties are clearly identified in accordance with good internal-control practices

Board of DirectorsBoard of Directors

Audit CommitteeAudit Committee

Risk Management Committee

Sub-committeeCredit Policy and Risk Management Sub-committee

Credit Process Management Sub-committeeMarket Risk Management Sub-committee

Asset and Liabilities Management Sub-committeeOperational Risk Management Sub-committee

Capital Management Sub-committee

Business FunctionsCBS/ RBS/

SME/ CMB/ CSP

Risk FunctionsERM

Approve risk appetite and all risk management policies and guidelinesEnsure the adequacy and effectiveness of risk management system and internal controls

Approve risk limits according to the risk appetite approved by the Bank’s Board of DirectorsOversee and monitor risk management policies and overall risk profile under the policies and guidelines approved by the Bank’s Board of Directors

Risk functions are responsible for risk management policies, methodologies, and processes in order to effectively measure, monitor, and control all related risks

Business functions are accountable for managing all risks inherent in their day-to-day activities

CBS = Corporate Business Division, RBS = Retail Business Division, SME = SME Business Division, CMB = Capital Market Business Division, CSP = Corporate and SME Products Division, ERM = Enterprise Risk Management Division

38

KBank Credit Risk Management Process

Monitor customer behavior and detect early warning signsEnsure credit condition compliance (e.g. insurance, capital injection, project progress) Take prompt action to prevent credit deterioration

Efficient collection and follow-up of customers with late paymentsRestructure viable customers to prevent NPLsForeclose pledged assets to recover loan loss

Enhance decision making/supporting tools for more efficient return and risk evaluationSetup specific prescreening criteria for potential industriesEnhance customer income validation process

MonitoringMonitoringMonitoring Collection & RecoveryCollection & RecoveryCollection & RecoveryOriginationOriginationOrigination

Portfolio ManagementPortfolio ManagementPortfolio Management

Determine portfolio-by-design i.e., portfolio target setting by key credit concentration dimensions (Country, Industry, Large Customer Group) and other sub portfolio dimensions based on value-based analysis

Manage portfolio according to the Bank’s risk appetite and concentration

Perform stress testing to identify portfolio weaknesses and proactively prepare appropriate management actions

The Bank continues to enhance credit risk management processes to promote risk strategies with justified risk-return tradeoff within the rapidly changing economic environment

39

• Automated collection system• Efficiently utilize available behavior scoring and collection tools i.e. SMS, automated letter

generation, phone

Unsecured Credit Product Operation Dept.

Credit Card/Unsecured Consumer

Housing Loan/ Secured Consumer

SM≤ Bt50mn

MB> Bt5,000mn

ME> Bt50 – 400mn

CB> Bt400 - 5,000mn

Policy Lending

• Sufficiency of cash flow• Growth trends and ability to compete• Management experience and depth• Leverage, Liquidity, and asset quality• Credit Risk Mitigation• Facilities Structure

Formula Lending

Corporate SME Retail

Po

st A

pp

rova

l

• Legal document• Limit set up

Credit Processing Dept.

Bank-wide Risk Asset Review

• Customer Review by Relationship Manager (RM)• Credit Portfolio Monitoring Unit to facilitate RM in

customer monitoring• Credit Clinic

Retail and SME Business Collection and Recovery Dept.

Ap

pro

val P

roce

ssA

nn

ual

Sal

e s

• Legal document• Limit set up

• Application Score• FICO Score• Bureau information/Credit

history• Debt service capacity• LTV

Unsecured Credit Product Operation Dept.

KBank Credit Approval Process

Note: MB = Multi-Corporate Business, CB = Large Corporate Business, ME = Medium Business, SM = Small & Micro Business , FICO = Fair Isaac Corporation

Formula Lending

• Application Score• FICO Score• Bureau information/Credit history• Debt service capacity (except Credit Card)• LTV (only housing loan/secured consumer)

SME Credit and Housing Loan Approval Processing Dept.Credit Underwriting Dept.

40

Credit Bureau Summary

Two Types of Credit Reports Offered by NCB:

Consumer credit report for individuals

Commercial credit report for businesses

Credit report (monthly reported by members)

Customer information (Name, address, identification number, birth date, occupation, etc.)

Credit information (History of application, approval history, loan payment history, etc.)

Data Record of Credit Report

Individuals: Credit report remains on file for 3 years

Businesses: Credit report remains on file for 5 years

Members: Financial institutions including commercial banks, specialized financial institutions (SFIs), non-bank financial institutions, finance companies, securities companies, insurance companies, etc.

KBank PracticeNational Credit Bureau (NCB)*

Note: * The concept of a credit bureau started in 1961 and central credit registration started in 1964. The Central Information Service was established in 1999 and its name was changed to Central Credit Information Service in 2000 and to the National Credit Bureau in 2005

KBank’s customers applying for loans

Corporate Business

Multi-Corporate Business

Large Corporate Business

Required to

4 Customer Segment in Retail (HN, AF, MI and MA)

Retail Business

Reject application

Sign agreement to allow the Bank to get credit report from NCB

Good credit

Small & Micro

Business

Medium Business

SME

Reject application

Required to (Large companies normally have reliable financial statements)

Optional to

Poor credit Good credit Poor credit

KBank’s Policy

Lending

KBank’s Credit

Scoring

41

KBank: Financial Performance

42

Consolidated 2012 1Q13 2Q13 3Q13 4Q13 2013

Net Profit (Bt bn) 35.26 10.11 10.98 10.71 9.53 41.33Profitability

- NIM 3.58% 3.49% 3.52% 3.52% 3.60% 3.55%

- ROE 20.76% 21.23% 22.17% 20.94% 17.80% 20.45%

- ROA 1.86% 1.93% 2.03% 1.92% 1.68% 1.89%

- YTD Loan growth 9.57% 2.19% 4.78% 6.51% 8.46% 8.46%

- YoY Loan growth 9.57% 11.12% 10.67% 9.77% 8.46% 8.46%

- YoY net fee income growth 18.56% 29.52% 23.63% 20.64% 9.67% 20.34%

- YoY non-interest income growth 19.72% 16.72% 21.39% 20.09% 14.61% 18.24%

Cost control

- Cost to income 45.00% 40.02% 42.65% 43.63% 48.40% 43.74%

Asset quality

- NPL ratio 2.16% 2.09% 2.13% 2.13% 2.11% 2.11%

- Coverage ratio 131.83% 138.62% 133.93% 132.85% 134.52% 134.52%

Loans to Deposits 95.35% 94.92% 94.76% 91.03% 94.06% 94.06%

Tier 1 Ratio (Bank Only)** 10.43% 11.08%** 11.44%** 12.51%** 12.02%** 12.02%**

CAR (Bank Only)** 15.98% 15.44%** 15.71%** 16.72%** 15.25%** 15.25%**

2013 Performance Highlights2013 net profit rose 17.20% YoY, driven by both net interest income and non-interest income

Loans grew 8.46% YoY from all business segments: Corporate, SME, and Retail

High NIM maintained; focus on high yield lending markets

Net fee income continued to grow due to customer-centric strategy; growth entails strengthening acquisition, retention, and cross-selling capabilities

2013 cost to income ratio was at 43.74%; cost to income ratio in 2014 will range in the mid-40s

Manageable NPLs, with high coverage ratio maintained

Strong capital base maintained

Note: * Under Bank of Thailand regulations, net profit in the first half of the year is counted as capital after approval by the Board of Directors as per Bank regulations. Net profit in the second half of the year is counted as capital after approval of the GeneralMeeting of Shareholders. However, when a net loss occurs, the capital must be reduced immediately.

** Capital Adequacy Ratio (CAR) has been reported in accordance with Basel III Capital Requirement from 1 January 2013 onwards.For KASIKORNBANK FINANCIAL CONGLOMERATE, as of 2013, Tier 1 = 12.57%, Tier 2 = 3.21%, and CAR = 15.78%.

KASIKORNBANK FINANCIAL CONGLOMERATE means the company under the Notification of the Bank of Thailand re: Consolidated Supervision, consisting of KBank, K Companies and subsidiaries operating in supporting KBank, Phethai Asset Management Co., Ltd. and other subsidiaries within the permitted scope of the BOT’s to be a financial conglomerate

43

Consolidated Financial Statements

KBank acquired additional ordinary shares in MTGH, to hold a 51% stake valued at Bt7,529mn; the MTGH Acquisition was completed on November 30, 2009. As the MTGH acquisition was completed on November 30, 2009, the Bank’s consolidated financial statements from 2010 include the performance of companies in the MTGH Group for the whole year.

Statements of Comprehensiv e Income (Bt mn)

2011* 2012 1Q13 2Q13 3Q13 4Q13 2013

Interest income 83,693 96,174 25,088 26,053 27,158 27,927 106,226

Interest expenses 27,202 32,593 7,883 8,121 8,641 8,783 33,428

Interest income - net 56,491 63,581 17,205 17,931 18,517 19,144 72,797Fee and service income 26,072 31,429 9,037 9,241 9,419 9,549 37,246

Fee and service expenses 5,435 6,961 1,901 1,867 1,899 2,136 7,803

Fee and serv ice income - net 20,637 24,467 7,136 7,374 7,519 7,413 29,443

Total operating income 122,216 144,495 40,575 42,541 43,295 43,224 169,635Underwriting expenses 31,707 40,190 11,872 11,971 12,396 12,446 48,685

Total operating income - net 90,508 104,305 28,703 30,569 30,899 30,779 120,950

Total other operating expenses 43,019 46,934 11,488 13,037 13,482 14,896 52,903Impairment loss of loans and debt securities 7,346 8,390 3,525 2,200 2,983 3,035 11,743

Operating profit before income tax expenses 40,144 48,981 13,690 15,332 14,433 12,848 56,303Income tax expenses 13,962 11,136 2,743 3,335 2,778 2,601 11,457

Net profit attributable:

Equity holders of the Bank 24,226 35,260 10,106 10,979 10,713 9,527 41,325 Non-controlling interest 1,957 2,585 842 1,018 942 720 3,522

Statements of Financial Position (Bt mn)2011 2012 1Q13 2Q13 3Q13 4Q13 2013

Loans to customers (less deferred revenue) 1,210,834 1,326,732 1,355,747 1,390,135 1,413,050 1,438,978 1,438,978Total Assets 1,722,940 2,077,442 2,109,967 2,225,152 2,240,034 2,290,045 2,290,045Deposits 1,242,229 1,391,380 1,428,318 1,467,058 1,552,217 1,529,835 1,529,835Total Liabilities 1,555,974 1,876,621 1,896,632 2,007,654 2,013,315 2,053,038 2,053,038Total Equity attributable to equity holders of the Bank 154,799 184,946 195,877 200,250 209,058 219,232 219,232

Notes:

* In accordance with the corporate income tax rate reduction from 30% of taxable profit to 23% in 2012 and 20% in 2013, KBank recognized a one-time Bt1.9bn impact to the 4Q11 income statement due to deferred tax item adjustments; there was no affect on the business undertakings, profitability, or capital fund of the Bank and its subsidiaries

44

Earnings Before Provision and Tax (EBPT) and Net Profit

37.1430.20

47.49

57.37

68.05

0

10

20

30

40

50

60

70

2009 2010 2011 2012 2013

(Bt bn)

December 2013 (Consolidated)

EBPT Net Profit

2009 2010 2011* 2012 2013 1Q13 2Q13 3Q13 4Q13

EBPT (Bt bn) 30.20 37.14 47.49 57.37 68.05 17.22 17.53 17.42 15.88

EBPT Growth (% YoY) n.a. 22.97% 27.86% 20.81% 18.61% 18.65% 21.32% 16.34% 18.17%

Net Profit (Bt bn) 14.73 20.05 24.23 35.26 41.33 10.11 10.98 10.71 9.53

Net Profit Growth (% YoY) n.a. 36.07% 20.85% 45.55% 17.20% 12.44% 17.21% 16.29% 23.85%

* In accordance with the corporate income tax rate reduction from 30% of taxable profit to 23% in 2012 and 20% in 2013, KBank recognized a one-time Bt1.9bn impact to the 4Q11 income statement due to deferredtax items adjustment; there was no affect on the business undertakings, profitability, or capital fund of the Bank and its subsidiaries

Note:

**

EBPT and net profit in 2013 grew 18.6% and 17.2% YoY, respectively

20.0514.73

24.23

35.26

41.33

0

10

20

30

40

50

2009 2010 2011 2012 2013

(Bt bn)

45

12.7915.73 16.72

20.4520.76

0

4

8

12

16

20

24

2009 2010 2011 2012 2013

(%)

1.101.38 1.48

1.891.86

0.00

0.50

1.00

1.50

2.00

2.50

2009 2010 2011 2012 2013

(%)

2009 2010 2011* 2012 2013 1Q13 2Q13 3Q13 4Q13

ROA (%) 1.10 1.38 1.48 1.86 1.89 1.93 2.03 1.92 1.68

ROE (%) 12.79 15.73 16.72 20.76 20.45 21.23 22.17 20.94 17.80

Note:

ROA and ROE

ROA ROE

December 2013 (Consolidated)

* In accordance with the corporate income tax rate reduction from 30% of taxable profit to 23% in 2012 and 20% in 2013, KBank recognized a one-time Bt1.9bn impact to the 4Q11 income statement due to deferredtax items adjustment; there was no affect on the business undertakings, profitability, or capital fund of the Bank and its subsidiaries

**

46

Net Interest Margin

3.23 3.48 3.553.583.75

0

1

2

3

4

5

2009 2010 2011 2012 2013

(%) (%)

NIM

December 2013 (Consolidated)

Note: * Cost of deposits including contributions to the Financial Institutions Development Fund (FIDF) and Deposit Protection Agency (DPA)

Yield on Loans

Yield on Earnings Assets

Cost of Fund

Cost of Deposit*

Yield on Earnings Assets and Cost of Fund

NIM was 3.55% in 2013, remaining the highest level among large commercial banksNIM position will be maintained, focusing on the high-yield lending market; pressure from rising competition will remain

5.185.424.63

5.55

5.245.94

6.24 6.37

1.932.142.08

1.321.891.991.70

1.050

2

4

6

8

2010 2011 2012 2013

2009 2010 2011 2012 2013 1Q13 2Q13 3Q13 4Q13

NIM (%) 3.23 3.48 3.75 3.58 3.55 3.49 3.52 3.52 3.60

Yield on Earnings Assets (%) n.a. 4.63 5.55 5.42 5.18 5.09 5.11 5.16 5.24Yield on Loans (%) n.a. 5.24 5.94 6.24 6.37 6.26 6.29 6.44 6.46

Cost of Fund (%) n.a. 1.32 2.08 2.14 1.93 1.89 1.89 1.95 1.97

Cost of Deposit (%), incl DPA n.a. 1.05 1.70 1.99 1.89 1.81 1.82 1.92 1.93

47

72.80

63.5856.49

39.8646.74

0

20

40

60

80

2009 2010 2011 2012 2013

Interest Income - net

(Bt bn)106.23

96.17

62.27

83.69

15.5327.20

32.59 33.43

0

20

40

60

80

100

120

2010 2011 2012 2013Interest Income Interest Expenses

(Bt bn)

Interest Income - net

Interest Income and Interest Expenses Interest Income- net

December 2013 (Consolidated)

Note: KBank acquired additional ordinary shares in MTGH, to hold a 51% stake valued at Bt7,529mn; the MTGH Acquisition was completed on November 30, 2009. As the MTGH acquisition was completed on November 30, 2009, the Bank’s consolidated financial statements from 2010 include the performance of companies in the MTGH Group for the whole year.

2013 net interest income grew 14.50% YoY

2009 2010 2011 2012 2013 1Q13 2Q13 3Q13 4Q13

Interest Income (Bt bn) n.a. 62.27 83.69 96.17 106.23 25.09 26.05 27.16 27.93

Interest Expenses (Bt bn) n.a. 15.53 27.20 32.59 33.43 7.88 8.12 8.64 8.78

Interest Income - net (Bt bn) 39.86 46.74 56.49 63.58 72.80 17.21 17.93 18.52 19.14

Interest Income - net (% Growth YoY) n.a. 17.28% 20.85% 12.55% 14.50% 15.33% 15.95% 14.27% 12.65%

48

15%

2%0.04%2%

18%16%

60%61%

0

10

20

30

40

50

2010 2011 2012 2013

Other Operating Income

Fee and Service Income - net

Net Premium Earned - net*

Dividend Income

Share of Profit from Investmentson Equity Method

Gain on Investment

Gain on Trading and FXtransactions

4%

2%

64%

0.02%2%

14%

12%2%

2%

20%

61%

0.4%

16%

2%

14%

3%

2%

0.05%

3%

2%

1.621.95 2.08 2.14 2.21

0

1

2

3

4

2009 2010 2011 2012 2013

(%)

4039383835

0

10

20

30

40

50

60

2009 2010 2011 2012 2013

(%)

Non-interest Income and StructureNon-interest Income to Average Assets

Non-interest Income Ratio**

Non-interest Income Structure

2009 2010 2011 2012 2013 1Q13 2Q13 3Q13 4Q13Non-interest Income (Bt bn) 21.68 28.40 34.02 40.72 48.15 11.50 12.64 12.38 11.64

Non- interest Income Growth (%YoY) n.a. 30.97 19.78 19.72 18.24 16.72 21.39 20.09 14.61

Non- interest Income Ratio (%) 35.23 37.79 37.58 39.04 39.81 40.06 41.34 40.07 37.80

December 2013 (Consolidated)

Note: * Net Premium Earned - net = Net Premium Earned less Underwriting expense** Non-interest income ratio = Non-interest income / Total operating income-net

(Bt bn)

28.40

34.02

Non-interest income continued to grow, mainly from net fee income and life insurance earned premium

40.72

48.15

49

24%23%23%24%

26%

0

10

20

30

2009 2010 2011 2012 2013

(%)29.44

24.47

18.2315.94

20.64

0

10

20

30

2009 2010 2011 2012 2013

(Bt bn)

Net Fee IncomeDecember 2013 (Consolidated)

Net Fee Income to Net Total Operating IncomeNet Fee Income

2009 2010 2011 2012 2013 1Q13 2Q13 3Q13 4Q13Fee Income (Bt bn) 19.54 22.82 26.07 31.43 37.25 9.04 9.24 9.42 9.55Fee Income-net (Bt bn) 15.94 18.23 20.64 24.47 29.44 7.14 7.37 7.52 7.41

Fee Income Growth (%YoY) n.a. 16.77 14.25 20.55 18.51 26.19 20.53 18.73 10.18Net Fee Income Growth (%YoY) n.a. 14.36 13.22 18.56 20.34 29.52 23.63 20.64 9.67

Net Fee Income to Net Operating Income (%) 25.90 24.26 22.80 23.46 24.34 24.86 24.12 24.34 24.09

2013 net fee income grew 20.34% YoY, driven by a rise in card business, mutual fund business and brokerage business in line with market growthNet fee income growth will continue to be helped by the cross-selling capabilities of our customer-centric strategyNet fee income to net total operating income was 24% in 2013Consolidated net fee income reflects the accounting treatment following the MTGH consolidation; Bancassurance fees were not included

50

Others10%

Bancassurance16%

Trade Finance6%

Cash Management

5%

Commercial Credit24%

Transaction Services

24%

Credit Card Business

15%

Credit Card Business

Transaction Services

Commercial Credit

Cash Management

Trade Finance

Bancassurance

Others

Net Fee Income Structure (Bank only)

Net Fee Income by Product

Loan Related and Non-loan Related Fees - net

Loan related24%

Non-loan related76%

(mainly from credit card merchant fees)

(such as ATM & debit cards, bill payments, money transfers, etc.)

(such as mutual funds, securities services, capital market business, etc.)

(mainly from commercial credit related fees)

(such as fees from payroll accounts)

(fee income obtained from selling Bancassurance products)

Note: - On the consolidated basis, Bancassurance fees are not

included, due to the elimination of inter-company transactions (the accounting treatment from the Muangthai Group Holding consolidation)

- On the consolidated basis, Net Premium Earned - net (Net Premium Earned Less Underwriting Expenses) from Muang Thai Life Assurance (MTL) is reported as a part of non-Interest Income; KBank has a 38.25% economic interest in MTL

December 2013

51

9.73

7.33

5.41

0.26

3.87

0

5

10

15

20

2009 2010 2011 2012 2013

Net Premium Earned - net

(Bt bn)58.41

47.52

37.12

2.20

29.09

1.94

25.22

31.71

40.19

48.69

0

20

40

60

2009 2010 2011 2012 2013

Net Premium Earned Underwriting Expenses

(Bt bn)

Net Premium Earned - net

Net Premium Earned and Underwriting Expenses Net Premium Earned – net

December 2013 (Consolidated)

Note: KBank acquired additional ordinary shares in MTGH, to hold a 51% stake valued at Bt7,529mn; the MTGH Acquisition was completed on November 30, 2009. As the MTGH acquisition was completed on November 30, 2009, the Bank’s consolidated financial statements from 2010 include the performance of companies in the MTGH Group for the whole year.

2009 2010 2011 2012 2013 1Q13 2Q13 3Q13 4Q13

Net Premium Earned (Bt bn) 2.20 29.09 37.12 47.52 58.41 14.10 14.82 14.98 14.51

Underwriting Expenses (Bt bn) 1.94 25.22 31.71 40.19 48.69 11.87 11.97 12.40 12.45

Net Premium Earned - net (Bt bn) 0.26 3.87 5.41 7.33 9.73 2.23 2.85 2.59 2.07

Net Premium Earned - net (% Growth YoY) n.a. n.a. 39.84 35.41 32.79 22.17 47.24 27.88 33.70

Net Premium Earned - net = Net Premium Earned less Underwriting Expense

52

Other Operating ExpensesOther Operating Expenses Structure

December 2013 (Consolidated)

46%46%43%

21%22%

23%

8%7%

7%0.3%

0.2%0.2%

25%

25%27%

3%

0

10

20

30

40

50

60

2010 2011 2012 2013

Impairment on ApplicationSoftware & Related Expenses

Others

Directors' remuneration

Taxes & Duties

Premises & Equipment

Employee's expenses

44%

20%

7%

25%

0.2%38.00

43.0246.93

(Bt bn) 52.90

2013 other operating expenses rose 12.72% YoY, the majority came from other promotion, advertising and marketing expenses, and employee expensesIn 2Q13, the Bank set the allowance for impairment on application software and related expenses at Bt1.6bn as a result of changes to some parts of the deposit core banking development under the K-Transformation Strategic Project; in addition, the Bank has made a reversal of estimate for loss sharing for asset management amounting to Bt1.1bn by Thai Asset Management Corporation (TAMC)

2009 2010 2011 2012 2013 1Q13 2Q13 3Q13 4Q13Other Operating Expenses (Bt bn) 31.34 38.00 43.02 46.93 52.90 11.49 13.04 13.48 14.90

% Growth (YoY) n.a. 21.27 13.20 9.10 12.72 11.97 14.10 16.79 8.69

53

14.4312.43

9.578.46

0

5

10

15

20

2010 2011 2012 2013

(%)

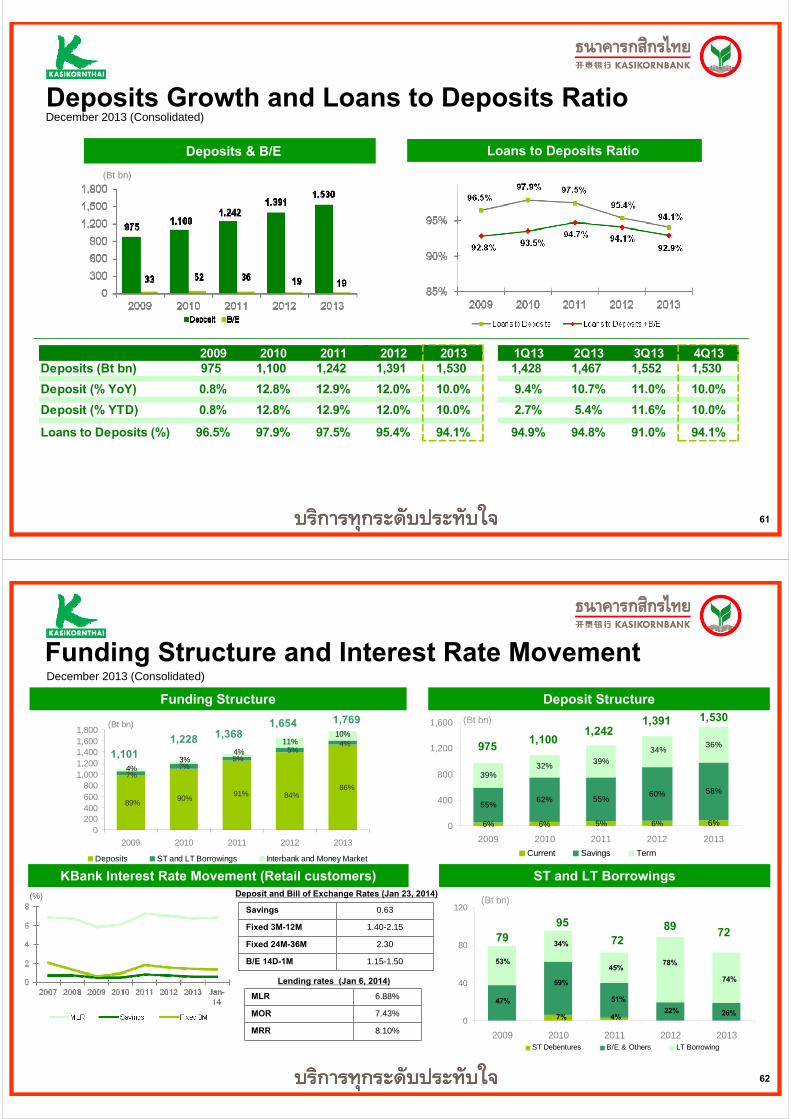

Loan Growth December 2013 (Consolidated)

Loans grew sensibly at 8.46% YoY from all business segments: Corporate, SME, and Retail

Loan Growth (% YoY)

2010 2011 2012 2013 1Q13 2Q13 3Q13 4Q13Loans (Bt bn) 1,077 1,211 1,327 1,439 1,356 1,390 1,413 1,439

Loan Growth (% YoY) 14.43 12.43 9.57 8.46 11.12 10.67 9.77 8.46

Loan Growth (% YTD) 14.43 12.43 9.57 8.46 2.19 4.78 6.51 8.46

54

31%31%

36%36%

26%26%

7%7%

0

500

1,000

1,500

2012 2013

Corporate Loans SME Loans Retail Loans Other Loans

(Bt bn)1,327 1,439

Loan Structure and Loan Growth Targets

(Amount in Bt bn) Dec 12** Y2012 Dec 13 Y2013 2013 Y2014Loan Loan Yield Loan Growth

Growth Growth Range Target (%)(%) (%) (%)

1) Corporate 416 5.5 443 6.7 4-6 6-8Multi-Corporate Business 203 5.2 220 8.3Large Corporate Business 212 5.8 223 5.2

2) SME 469 8.7 521 10.9 7-8 9-11Medium Business 260 1.9 277 6.6Small and Micro Business 207 18.5 241 16.9

3) Retail 347 16.0 382 10.3 6-7 10-134) Others 95 10.8 93 (2.9)Total Loans 1,327 9.6 1,439 8.5 6.4 9-11

December 2013 (Consolidated, TFRS 8: Operating Segments*)

Loan Portfolio Structure Loan Structure, Loan Yield and Loan Growth Targets

** December 2012 loan base is not comparable with previous reports, due to customer migration to larger segments and changes to comply with TFRS 8

Loan Definition (TFRS 8: Operating Segments)Corporate Loans: Loans of KBank and KBank’s Subsidiaries in Corporate Segments (Annual sales turnover > Bt400mn)SME Loans: Loans of KBank and KBank’s Subsidiaries in SME Segments (Annual sales turnover ≤ Bt400mn)Retail Loans: Loans of KBank and KBank’s Subsidiaries in Retail SegmentsOther Loans: Loans in Enterprise Risk Management Division (NPL + Performing Restructured Loans), and other loan types

Note: * Since 1Q13, as per the Bank of Thailand’s requirement, the Bank has complied with TFRS 8 (Operating Segments) to present operating results for each key segment in financial reports

55

Loan by Retail Products December 2013 (Consolidated, TFRS 8: Operating Segments*)

Loan Definition (TFRS 8: Operating Segments)Housing Loans: KBank’s housing loans to retail customer segmentsCredit Cards: KBank’s credit card loans to all eight customer segmentsConsumer Loans: KBank’s consumer loans to retail customer segmentsKLeasing: KLeasing’s loans to all eight customer segments

(Amount in Bt bn) Dec 12** Y2012 Dec 13 Y2013 % Portion

Loan Loan to

Growth Growth Total Loan(%) (%)

Housing Loans 203 10.1 215 5.5 14.9Credit Cards 54 27.7 66 21.8 4.6Consumer Loans 37 38.7 44 17.8 3.1KLeasing 83 29.8 89 7.7 6.2

Note: * Since 1Q13, as per the Bank of Thailand’s requirement, the Bank has complied with TFRS 8 (Operating Segments) to present operating results for each key segment in financial reports

Loan by Retail Products

** December 2012 loan base is not comparable with previous reports, due to customer migration to larger segments and changes to comply with TFRS 8

56

6 months and over16.0%

Immediate Repricing61.0%

< 6 months11.5%

Other11.5%

48.4%48.9%51.2%54.3%55.4%

6.5%6.5%6.2%5.7%

6.3%10.8%

13.1%13.0%12.4%

10.7%

15.7%16.0%16.0%

15.5%14.0%

13.9%13.1%

11.6%

11.4%

10.9%

0

200

400

600

800

1,000

1,200

1,400

1,600

2009 2010 2011 2012 1H13

OthersHousing LoansUtilities & ServicesReal Estate & Construction

Manufacturing & commerceAgricultural and mining

(Bt bn)

2.7% 2.5%

942

1,077

2.5%

1,211

2.4%

1,327

2.3%

1,390

Loan Portfolio Breakdown by Industry, Currencies, and Interest Rate Consolidated

Loan Portfolio by Industry (June 2013)*

Definition of Loans1) by industry = Gross loans = Loans to customers less deferred revenue2) by top 20 borrowers = Loans excluding the wholly-owned subsidiaries of KBank and Phethai Asset

Management Company 3) by currency = Loans to customers and AIR - net4) by maturity of interest repricing = Loans to customers less deferred revenue

By Maturity of Interest Repricing (June 2013)*

By Currencies (June 2013)*

Note:

Thai Baht92.46%

US Dollar6.60%

Other Currencies0.94%

* The data as of December 2013 is not available until the release of the audited financial statements** The information on loans breakdown by currencies and maturity of interest repricing are disclosed on half year basis

57

134.52131.83127.12111.02

91.64

0

50

100

150

2009 2010 2011 2012 2013

3.762.91

2.45 2.16 2.11

0

2

4

6

8

2009 2010 2011 2012 2013

Asset QualityDecember 2013 (Consolidated)

NPL Ratio(%)

Coverage Ratio(%)

2009 2010 2011 2012 2013 1Q13 2Q13 3Q13 4Q13

NPL Ratio (%) 3.76 2.91 2.45 2.16 2.11 2.09 2.13 2.13 2.11