kevin jackson matt osborne head of risk

TRANSCRIPT

CLICK TO EDIT MASTER TITLE STYLE

Kevin JacksonLead Consultant

Matt OsborneHead of Risk

Robin PrestonSales Director

ENERGY PROCUREMENT

Understanding risk and how to manage it!

CLICK TO EDIT MASTER TITLE STYLE

UNDERSTANDING RISKAND HOW TO MANAGE IT. • What does risk

mean to you?

CLICK TO EDIT MASTER TITLE STYLEEVOLUTION OF THE ENERGY MARKET

1968 - Inenco

30.00

40.00

50.00

60.00

70.00

80.00

90.00

100.00

110.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

100.00

110.00

Oct

-200

5Ja

n-20

06A

pr-2

006

Jul-2

006

Oct

-200

6Ja

n-20

07A

pr-2

007

Jul-2

007

Oct

-200

7Ja

n-20

08A

pr-2

008

Jul-2

008

Oct

-200

8Ja

n-20

09A

pr-2

009

Jul-2

009

Oct

-200

9Ja

n-20

10A

pr-2

010

Jul-2

010

Oct

-201

0Ja

n-20

11A

pr-2

011

Jul-2

011

Oct

-201

1Ja

n-20

12A

pr-2

012

Jul-2

012

POWER PRICE £/MWh

GAS PRICE P/THERM

Gas and Power Forward Prices

GasPrices

1879 Edison’s lightbulb moment

2017 –Today

1986 – Gas Act

1st April 1990 – 1MW1800s - Volta / Franklin

1st April 1994 -100kW - HH

27th March 2001- NETA

1st April 1998 - Sub 100 - NHH

CLICK TO EDIT MASTER TITLE STYLEWHAT CAN YOU BUY, WHEN AND WHERE FROM?

Prebon Spectron

ICAP

GFI ICE

CLICK TO EDIT MASTER TITLE STYLETHE EVOLUTION OF THE ENERGY MARKET

0

20

40

60

80

100

120

140

160

180

£/M

Wh

Day Ahead (UKBaseload) (£/MWh)

Day Ahead (UKBaseload) (£/MWh)

THE PAST: BETTA

UK Energy markets begin liberalization in 2001-02 (NETA).Single GB market in 2005 (BETTA)Access to wholesale market participation widensControlling energy cost becomes a bumpy ride!!!!

Demand begins to outstrip supply (lack of import responsiveness & storage capacity) and commodities “super cycle” takes off

Global recession and the financial crisis brought an abrupt end to rising prices

Weak renewables andFrench nuclear

offline

Relative stability/gradual decline

Commodities “super cycle”peaks – oil touches $147/bbl

CLICK TO EDIT MASTER TITLE STYLE

FIXED PRICE

CAPPED/ LOCK/UNLOCK

TECHNICAL ANALYSIS

PROMPT TRADING

WHOLESALE

EVOLUTION OF TRADING

1990 2013+2003 2008

Risk

Man

agem

ent

High

UK Electricity Market Deregulated

April 2001NETA Introduced

Increased Volatility Gasand Power Prices Spike

Timeline

Further Developments in the Market

2001

CLICK TO EDIT MASTER TITLE STYLEYOUR BILL

What impacts what you pay

Taxes & Levies15 – 20%

Transportation & Distribution30 – 40%

Supplier Costs 5%

Commodity45% - 55%

CLICK TO EDIT MASTER TITLE STYLESO WHERE TO START

What isyour Goal?

What are youtrying to achieve?

CLICK TO EDIT MASTER TITLE STYLEBUYING ENERGYWHAT ARE YOU TRYING TO ACHIEVE

Budget Certainty?Best Price?

CLICK TO EDIT MASTER TITLE STYLEINENCO’S PROCUREMENT STRATEGY

‘Buying energy is all about knowing what you want to achieve and then managing the risk to secure the right balance between price and budget certainty for BOTH commodity and non commodity elements’

RISK LOWHIGHBEST PRICE BUDGETCERTAINTY

PromptYou take the risk

CappedShared Risk

FixedSupplier takes Risk

Pass ThroughYou take the risk

Partially FixShared Risk

Fully FixSupplier takes Risk

Commodity

Non-Commodity

CLICK TO EDIT MASTER TITLE STYLE

UNDERSTANDING THE ENERGY MARKET & STRATEGY DEVELOPMENTThe Energy Markets What gives

the market direction?

CLICK TO EDIT MASTER TITLE STYLE1. UNDERSTANDING THE MARKET : KEY TOOLS

CLICK TO EDIT MASTER TITLE STYLETHE RIGHT VIEW

Prebon Spectron ICAP GFI

We ensure we have full access to the wholesale market

Our bespoke trading system consolidates all broker screens so wecan identify truemarket value

ICE

CLICK TO EDIT MASTER TITLE STYLEASSESS THE MARKET

We combine technical & fundamental analysis

Technical

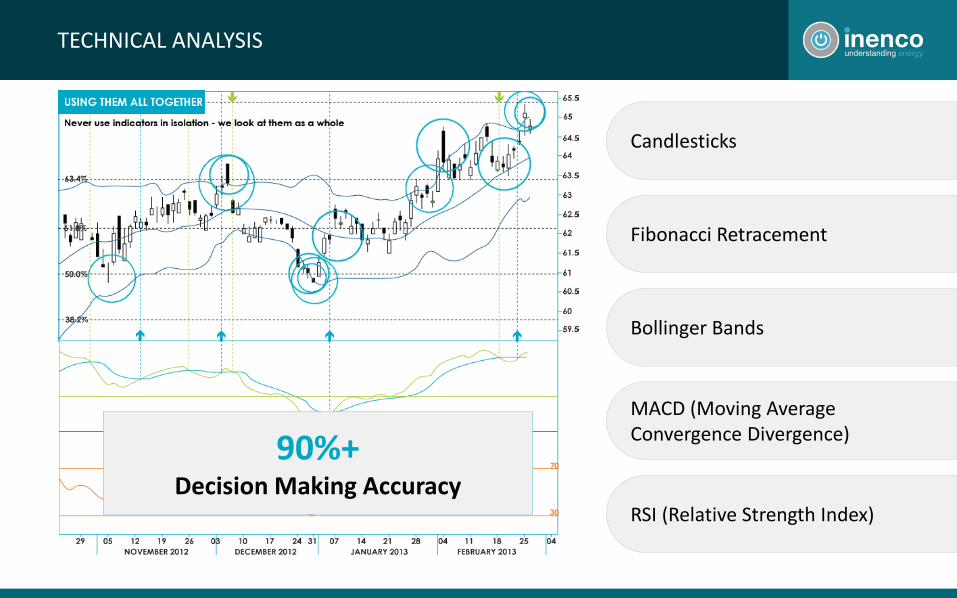

CLICK TO EDIT MASTER TITLE STYLETECHNICAL ANALYSIS

Candlesticks

Bollinger Bands

MACD (Moving Average Convergence Divergence)

RSI (Relative Strength Index)

Fibonacci Retracement

90%+Decision Making Accuracy

CLICK TO EDIT MASTER TITLE STYLE2. CURRENT MARKET DRIVERS

CLICK TO EDIT MASTER TITLE STYLECURRENT PRICE DRIVERS

MacroeconomicEU Zone debt Demand – EMBrexit Fundamentals

LNG - US/AUS Weather Margins & renewable outputStorage

GeopoliticsMiddle East OPEC vs Market UkraineN. Korea

Technical AnalysisMarket uptrend still intact?

Longer termLCPD/MCPDShale Development LNG – Asian Demand

CLICK TO EDIT MASTER TITLE STYLE

Bullish Bearish

CRUDE OIL

CLICK TO EDIT MASTER TITLE STYLEOIL

Brent touches $59/bbl as Turkey threatens to cut off the northern Iraq pipeline.

OPEC production cut compliance at c90%.

US refinery’s at c90% capacity following hurricanes Harvey and Irma.

EIA reports surprise fall in US stockpiles – 6m bbldrawdown vs forecast 0.5m bbl.

Recent $ strength could limit upside.

US production continues to increase (drilling technology & efficiency improvements.

Rig count remains high.

OPEC getting desperate? Calls for US shale producers to join production cuts.

CLICK TO EDIT MASTER TITLE STYLE

Bullish Bearish

GAS & POWER

£

CLICK TO EDIT MASTER TITLE STYLEAN EVOLVING GENERATION MIX

Source:National Grid Future Energy ScenariosInstalled generation by type –No Progression

CLICK TO EDIT MASTER TITLE STYLELNG – THE NEXT ENERGY BUBBLE?

Global LNG output to rise by c47% by 2020 & Demand insufficient to absorb the scale of new capacity

CLICK TO EDIT MASTER TITLE STYLESO WHERE NEXT FOR PRICES?

Technical Indication:

• Key resistance level continues to provide a ceiling for prices.

• Failure to break through has provided some near term bearish sentiment, which could test initial support levels.

Gas – Winter’18

CLICK TO EDIT MASTER TITLE STYLESO WHERE NEXT FOR PRICES?

Technical Indication:

• Recently broken through contract highs.

• Some softening but upward trend channel is still intact.

• Overall fundamentals indicate further bullish momentum, however OPEC production could change this outlook.

• Support and resistance levels in line with the trend lines.

Power – Winter’18

CLICK TO EDIT MASTER TITLE STYLEELECTRICITY PRICE FORECAST

Forward thinking is critical

Prices pose more upside risk than further downside potential

35

40

45

50

55

60

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

£/MWh Wholesale UK Power Price Forecast

High/Low Range Historical Normal

CLICK TO EDIT MASTER TITLE STYLE3. HOW TO MANAGE SUCH RISK : KEY STEPS

CLICK TO EDIT MASTER TITLE STYLEA) ESTABLISH A RISK MANAGEMENT STRATEGY IMPLEMENTATION PROCESS

MONITORRESULTS IDENTIFY &

ANALYSE EXPOSURES

EXAMINE RISK MANAGEMENT

TECHNIQUES

SELECT RISK MANAGEMENT

TECHNIQUE

IMPLEMENT TECHNIQUES

RISKMANAGEMENT

CLICK TO EDIT MASTER TITLE STYLEB) UNDERSTAND YOUR PRIORITIES

CERTAINTYAn exact price upfront

OPTIMISATIONChase the best price using risk management

PROTECTIONAn upper limit for budgeting

CLICK TO EDIT MASTER TITLE STYLEC) UNDERSTAND YOUR RISK-REWARD PROFILE

Performance

Risk

Prompt StrategyOptimise

Trend StrategyCapitalise

Fixed StrategyCertainty

Capped StrategyProtect

Use risk mapping & tolerance exercises to reach consensus!

CLICK TO EDIT MASTER TITLE STYLED) THINK ABOUT THE BIGGER PICTURE :BUDGETING – FULLY DELIVERED FORECASTING

Commodity Element 2015 2016 2017 2018 2019 2020 Key drivers/assumptionsLow 38 38.1 39.6 41 41.8 42.8 Low oil price forecast, declining power demand and low NBP price forecast

Base 40.1 40.9 43.2 44.6 45.2 46.2 Normal oil price forecast, static power demand and normal price forecast

High 50 52.3 52.7 53.9 55.3 56.3 High oil price forecast, increasing power demand and high NBP price forecast

Commodity Price Forecast (£/MWh) – illustrative only

Non-Commodity Element 2015 2016 2017 2018 2019 2020 Key drivers/assumptionsD and T Losses 0.33 0.33 0.33 0.33 0.33 0.33 Average across large section of supplies

BSUOS 0.21 0.22 0.23 0.24 0.25 0.26 Average across large section of supplies

DUOS 1.87 1.96 1.87 1.96 1.96 1.96 Average across large section of supplies

TNUOS (Triad) 0.72 0.81 0.95 1.09 1.22 1.37 Average across large section of supplies

CFD 0.00 0.00 0.00 0.00 0.00 0.00 Should remain fairly level during next few years

FIT 0.41 0.48 0.53 0.56 0.60 0.62 Uptake has slowed but the belief is that is will still rise faster than inflation

Capacity Market 0.00 0.00 0.00 0.00 0.00 0.00 Should remain fairly level during next few years

RO 1.29 1.37 1.40 1.40 1.40 1.40 Will rise for a couple of years before stagnating as no new renewable projects will be financed via this source

Other 0.024 0.02 0.02 0.02 0.02 0.02 Should remain fairly level during next few years

CCL 0.55 0.56 0.57 0.58 0.60 0.61 Subject to government legislation –should rise with inflation

Total (p/KWh) 2015 2016 2017 2018 2019 2020Low 5.53 6.13 6.43 7.34 7.94 8.70 (-3%)

Normal 5.70 6.32 6.62 7.57 8.19 8.98 As per assumptions above

High 5.99 6.63 6.96 7.95 8.60 9.42 (+5%)

Non Commodity Price Forecast (p/KWh) – illustrative only

Illustrative only

CLICK TO EDIT MASTER TITLE STYLEE) DEVELOP YOUR OVERARACHING APPROACH TO THE MARKET : BUYING ENERGY

Budget Certainty?Best Price?

FLEXIBLE? FIXED?

CLICK TO EDIT MASTER TITLE STYLE4. WHAT TOOLS ARE AVAILABLE & APPROPRIATE?

CLICK TO EDIT MASTER TITLE STYLEA) LOCK & UNLOCK

1 – Lock to limit exposure in rising market 2 – Unlock to expose volume in falling markets

CLICK TO EDIT MASTER TITLE STYLEB) SLEEVING

Go to

Trade

Offer(Buy @ £52.10/MWh)

Bid(Sell @ £50.75/MWh)

Trade at(£51.50/MWh)

SAVINGS (£0.60/MWh)On a 1MW clip of a season = £2,621

Go to Sleeving Counterparties

AddedValue 1%

What about access to green energy / asset specific generation : PPAs?

CLICK TO EDIT MASTER TITLE STYLEC) HEDGING ENVELOPE

Strategy requirements/objectives also help determine trading decisions: for example do we need a trading timetable to achieve a particular cash flow profile?

Risk Levels can act as trigger points:• Volatility

• Budget level

• CaR or CFaR

• Stop losses

• Cap & Collar

Season Current Season Bullish BearishFront Season Winter‘ 17 100% 60%

Front +1 Summer’ 18 80% 40%

Front +2 Winter‘ 18 80% 40%

Front +3 Summer‘ 19 60% 20%

Front +4 Winter‘ 19 60% 20%

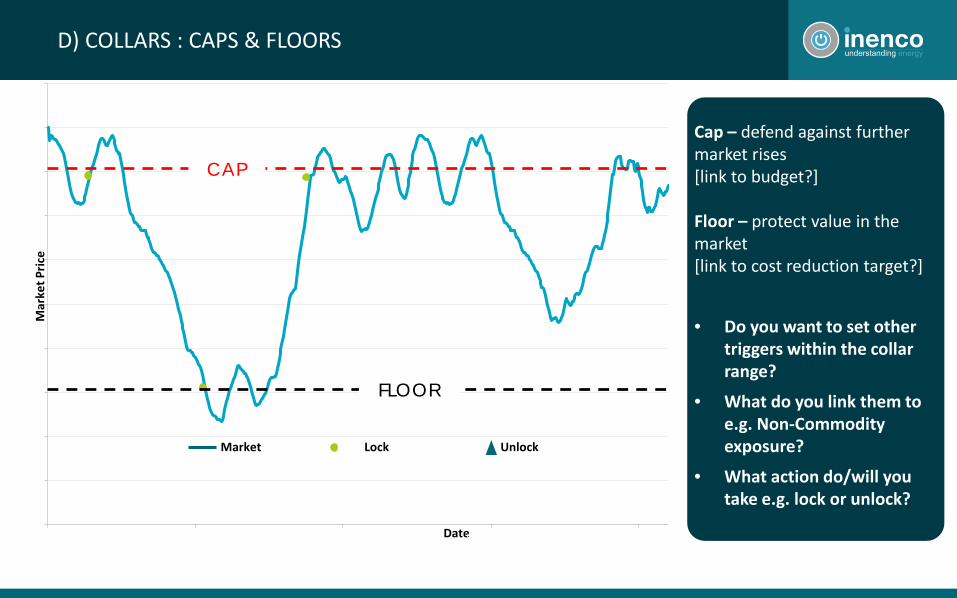

CLICK TO EDIT MASTER TITLE STYLED) COLLARS : CAPS & FLOORSM

arke

t Pric

e

Date

Good for securing your volume in a one time purchase 1 – Identifies likely low point in the market to purchase 100% of the volume in the portfolio a maximum of 12 months prior to the supply year

Cap – defend against further market rises[link to budget?]

Floor – protect value in the market[link to cost reduction target?]

• Do you want to set other triggers within the collar range?

• What do you link them to e.g. Non-Commodity exposure?

• What action do/will you take e.g. lock or unlock?

50

52

54

56

58

60

62

64

66

68

70

01/07/2010 01/12/2010 01/05/2011 01/10/2011 01/03/2012

Market Lock Unlock

CAP

FLOOR

CLICK TO EDIT MASTER TITLE STYLEE) NETTING

Buyer & Seller separately go to

Trade

Buyer Pays Offer Price(Buy @ £52.00/MWh)

Seller Gets Bid Price(Sell @ £51.00/MWh)

Both Trade at

(£51.50/MWh)

Instead trade internally with each other

AddedValue %

Net the two

positions

AddedValue %

CLICK TO EDIT MASTER TITLE STYLE5. COMBINE & BUILD INTO A COHERANT STRATEGYWHAT WILL IT LOOK LIKE?

CLICK TO EDIT MASTER TITLE STYLEFIXED STRATEGY

50

52

54

56

58

60

62

64

66

68

70

01/07/2010 01/12/2010 01/05/2011 01/10/2011 01/03/2012

CERTAINTY

Mar

ket P

rice

Date

Market Customer position Lock

1

Risk to Budget Medium/High

Performance Low

Overall Risk Rating Medium

Good for securing your volume in a one time purchase 1 – Identifies likely low point in the market to purchase 100% of the volume in the portfolio a maximum of 12 months prior to the supply year

• Places emphasis on budget certainty• Identifies likely low points in the market

to purchase 100% of the volume inthe portfolio

CLICK TO EDIT MASTER TITLE STYLECAPPED STRATEGYM

arke

t Pric

e

50

52

54

56

58

60

62

64

66

68

70

72

74

01/07/2010 01/12/2010 01/05/2011 01/10/2011 01/03/2012

Date

Optimises your price through risk management

Protection against rising market prices

Provides an upper level budgetary price

Capitalises on downward market movements

PROTECT

Cap Market Customer position Lock Unlock

Good for budget certainty

1 – CAP is set

2 – Volume locked out under cap protecting against rising market prices

3 – Unlock to re-expose volume to falling prices and capitalise on downward market movements

4 – Relock to take profit when downward market movements reverse

1

2

3

4

Risk to Budget Low

Performance Medium

Overall Risk Rating Low/Medium

CLICK TO EDIT MASTER TITLE STYLETREND STRATEGY

50

52

54

56

58

60

62

64

66

68

70

01/07/2010 01/10/2010 01/01/2011 01/04/2011 01/07/2011 01/10/2011 01/01/2012

Mar

ket P

rice

Date

CAPITALISE1

23

4

Risk to Budget Low/Medium

Performance Medium/High

Overall Risk Rating Medium

Cap Market Customer position Lock Unlock

Good for taking advantage of market volatility1 – Lock to limit exposure in rising market

2 – Unlock to expose volume in falling markets

3 – Unlocks more volume than the capped strategy to further optimise price

4 – Relock to take profit when downward market movements reverse

• Aims to optimise your price

• Uses technical analysis to identify and react to market trends and patterns

• Looks to reduce volume in rising markets and expose volume in falling markets

• Unlocks more volume than the capped strategy

CLICK TO EDIT MASTER TITLE STYLEPROMPT STRATEGY

50

52

54

56

58

60

62

64

66

68

70

01/07/2010 01/12/2010 01/05/2011 01/10/2011 01/03/2012 01/08/2012

Mar

ket P

rice

Date

Forward Market Prompt

OPTIMISE

Good for price optimisation if you can take the risk

1 – Buys volume within thedelivery period.

1

• Looks to buy volume within the delivery period

• Energy Trading Team will decide whether to buy Month-Ahead or Day-Ahead Market depending on the market conditions at the time

Risk to Budget High

Performance High

Overall Risk Rating High

Cap Market Customer position Lock Unlock

CLICK TO EDIT MASTER TITLE STYLEDOCUMENT YOUR STRATEGY POLICY

Key strategy parameters

Key contract parameters

Strategy exceptions

Process

Measuring value

Strategy review

Forecasting – consumption & budget

Agreement

CLICK TO EDIT MASTER TITLE STYLECONTINUE TO MONITOR & RE-ALIGN

FY16/17 £/MWh £

Mark 53.58 28,603,758.57

Inflated Mark 54.45 29,066,537.85

Market 33.78 18,239,973.77

Budget 53.19 28,394,157.11

Target/RecommendationForecasts remain bearish but excellent value. Scope for the market to fall further. Hold

0%

20%

40%

60%

80%

100%

Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16Exposed 0% 0% 0% 0% 0% 74% 100% 103% 102% 100% 94% 99%

Day Ahead Trade 74% 75% 74% 72% 73% 0% 0% 0% 0% 0% 0% 0%

Forward Trade 68% 92% 85% 95% 95% 77% 42% 43% 42% 0% 0% 0%

Hedged Position

Illustrative only

CLICK TO EDIT MASTER TITLE STYLEDON’T FORGET – A QUICK RECAP

MONITORRESULTS IDENTIFY &

ANALYSE EXPOSURES

EXAMINE RISK MANAGEMENT

TECHNIQUESSELECT RISK

MANAGEMENT TECHNIQUE

IMPLEMENT TECHNIQUES

RISKMANAGEMENT

Remember non-commodity costs!

Understand your options fully

Document the strategyKeep it simpleMake sure you understand it !

Are you best placed to do this?How quickly can you react?

Markets & business objectives change –keep strategy fit for purpose

CLICK TO EDIT MASTER TITLE STYLE

NON COMMODITY CHARGES What are they

and how to mitigate them

CLICK TO EDIT MASTER TITLE STYLENON COMMODITY COMPONENTS

Taxes & Levies15 – 20%

Transportation & Distribution30 – 40%

Supplier Costs 5%

Commodity45% - 55%

CLICK TO EDIT MASTER TITLE STYLENON COMMODITY COMPONENTS

Taxes & Levies15 – 20%

Transportation & Distribution30 – 40%

• Balancing & Settlement Use of System (BSUoS)

• Distribution Use of System (DUoS)

• Transmission Network Use of System (TNUoS)

• Line Loss Factors (LLF)

• AAHEDC - Assistance for Areas with high electricity distribution Costs

• Renewable Obligation (RO) Levy

• Feed in Tariff (FIT) Levy

• Contract for Difference Levy (CfD) Levy

• Climate Change Levy (CCL)

• Carbon Reduction Commitment (CRC)

• Capacity Market (CM)

Fixed Cost

per kWh

Vary on time and season

Vary on time and season

CLICK TO EDIT MASTER TITLE STYLENON COMMODITY - FIXED VS VARYING RATES

LLF(AAHEDC)

Renewable Obligations (RO) Levy

Feed in Tariff (FIT) Levy

Contract for Difference Levy (CfD) Levy

Climate Change Levy(CCL)

Carbon Reduction Commitment (CRC)

Capacity Market (CM)

Transmission Network Use of System (TNUoS)

Distribution Useof System (DUoS)

Balancing & Settlement Use of System (BSUoS)

CLICK TO EDIT MASTER TITLE STYLERENEWABLES NEED SUBSIDIES!

2012/13

£6.43/MWh

2017/18

£19.64/MWh

RO Demand levy

CLICK TO EDIT MASTER TITLE STYLETHERE IS SOME GOOD NEWS!

20 years

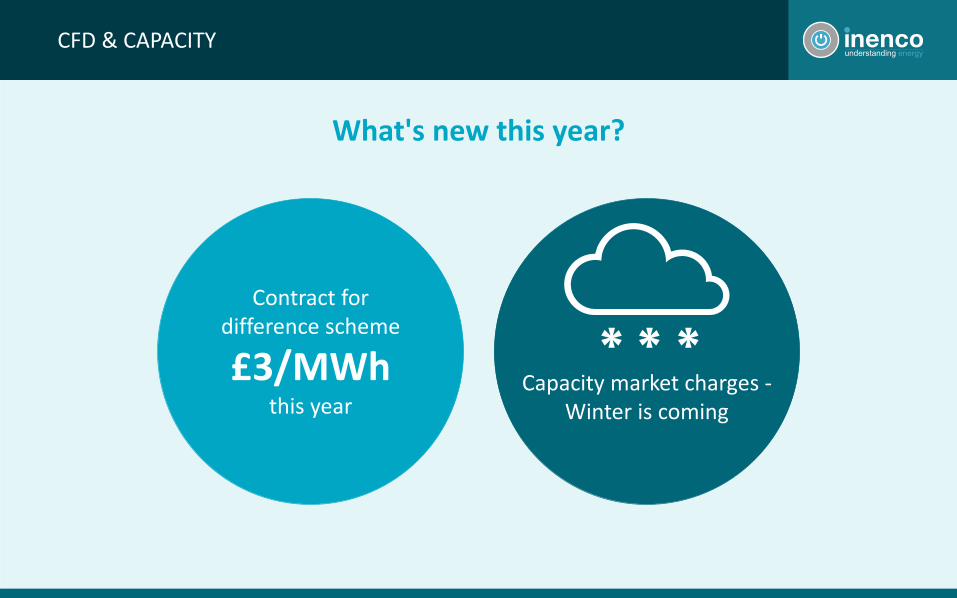

CLICK TO EDIT MASTER TITLE STYLECFD & CAPACITY

Capacity market charges -Winter is coming

Contract fordifference scheme

£3/MWhthis year

What's new this year?

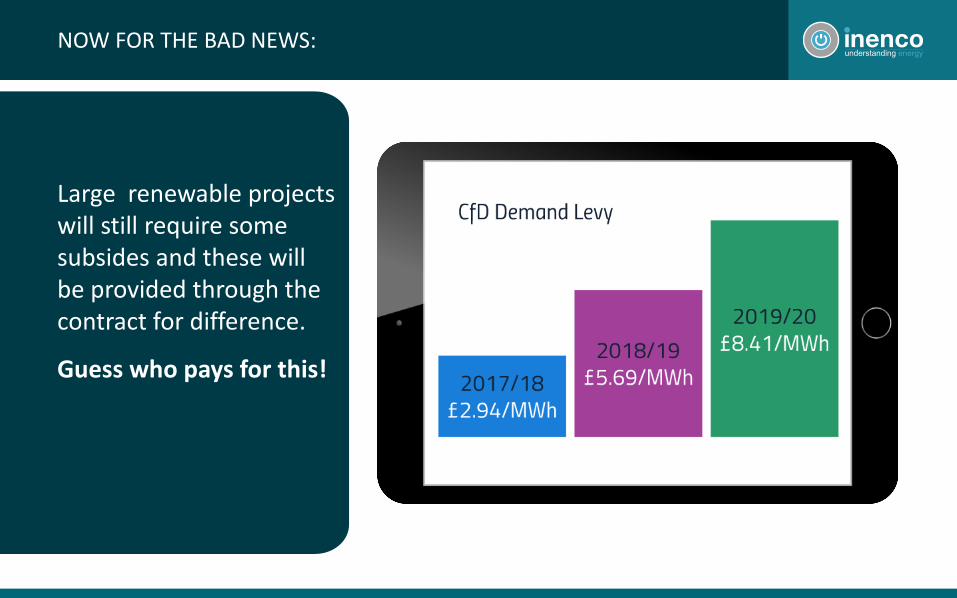

CLICK TO EDIT MASTER TITLE STYLENOW FOR THE BAD NEWS:

Large renewable projects will still require some subsides and these will be provided through the contract for difference.

Guess who pays for this!

CLICK TO EDIT MASTER TITLE STYLECAPACITY MARKET

The capacity market is a mechanism designed to control the rate of closure of power plants and to encourage new plants to be built.

The scheme will cost around £380m this year and almost £1bn in the following 2 years, but this rise considerably in the 2020’s when remaining coal plantsstart to close

£1bn

CLICK TO EDIT MASTER TITLE STYLECAPACITY MARKET

CLICK TO EDIT MASTER TITLE STYLETNUoS CHARGES

The Grid needs to be reconfigured.

Uncertainty of charges beyond 2019

It is impossible that we will move away from triads and have fixedcosts associated with connection capacity

CLICK TO EDIT MASTER TITLE STYLE

TNUoS costs will continue to rise quickly however much of the increase will be due to a programme to extend interconnector capacities

TNUoS CHARGES

CLICK TO EDIT MASTER TITLE STYLETRIAD NOTIFICATIONS

TRIAD NOTIFICATIONS - 2016/17

The 2016/17 Triad was

The winter of 2016/17 was relatively mild and consistent throughout the Triad season which was one reason there were no surprises at the Triad dates.

Wind speed also affects Triads – all three 2016/17 Triads occurred when speeds were below average.

TOTAL DEMAND OVER THE THREE TRIADS WAS AROUND 1% HIGHER THAN 2015/16+1%

The more businesses that participate in demand side management and shift load outside of peak periods, the less predictable Triads could be in future. Keep an eye on upcoming consultations from Ofgem. Triads may change from 2020.

Demand-Side Management may also be impacting Triads. More and more businesses are switching off loads or starting stand-by generators during Triad warnings in an attempt to reduce the Triad charges.

59

After the unusual Triad behaviour seen in Winter 15/16, the past winter produced Triad dates that were more consistent with previous years.

Since 2007/8 statistically the most common day for a Triad has been a Monday, followed by Thursday. Only one Triad has ever occurred on a Friday and never at the weekend. Over the last 10 years:

BACK TO NORMAL

5THDEC

23RDJAN

47%

27%

26%

27 of the previous 30 Triads occurred between

17:00 and 17:30 and 2 occurred between 17:30

and 18:00 and 1 occurred between 18:00 and 18:30.

This year all 3 Triads occurred between 17:00

and 17:30

Monday 5th December 201617:00pm – 17:30pm

50,163 MW chargeable

Thursday 5th January 201717:00pm – 17:30pm

48, 516 MW chargeable

Monday 23rd January 201717:00pm – 17:30pm

48,970 MW chargeable

SEVEN WEEKS APART

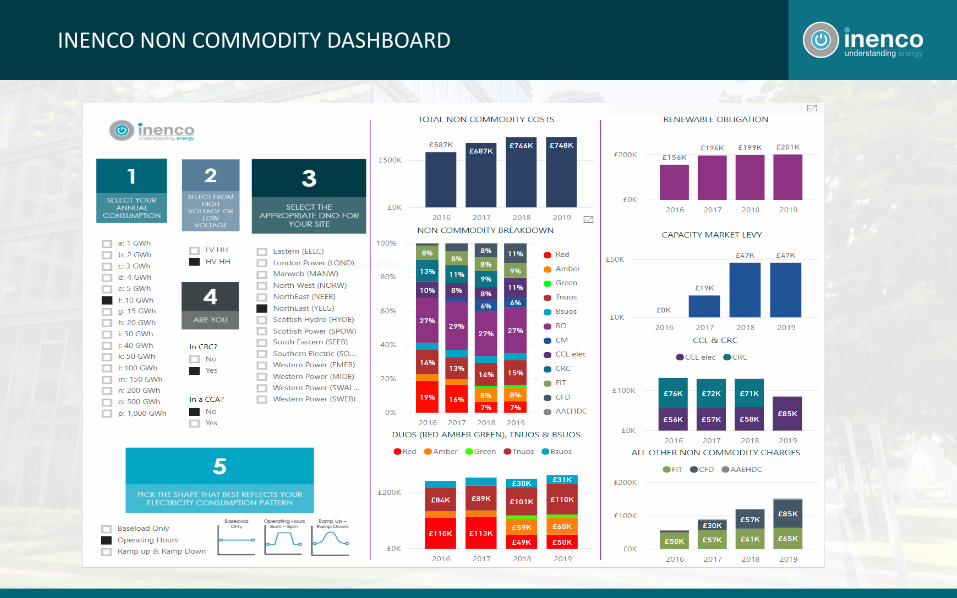

CLICK TO EDIT MASTER TITLE STYLEINENCO NON COMMODITY DASHBOARD

CLICK TO EDIT MASTER TITLE STYLE

REFRESHMENT BREAK

CLICK TO EDIT MASTER TITLE STYLE

INENCO TRADING GAMEPut what yourlearnings into action! • Could you be an

energy trader?

CLICK TO EDIT MASTER TITLE STYLEINENCO TRADING GAME

4th April End of Summer 17 Trading and Winter 17 and Summer 18 both look well supplied

11th April MET Office revise forecast average Winter temperatures up by 2 degrees after weaker El Nino

18th April Centrica announce that Rough storage is no longer viable and there will be no extractions this winter

25th April Dutch Government reduce withdrawals from Groningen Gas field down to 50% due to further tremors

2nd May Tension between US and North Korea increase after further nuclear and hydrogen missile testing

9th May US LNG production hits new highs

16th May Japan successfully re-start 3 nuclear power stations

23rd May LNG cargos to the UK are expected to increase by 25% over summer following Japanese news

30th May Generation capacity for offshore wind reaches record high

6th June Prices reach 3 year lows and attract buying interest

£33MWh£32MWh£31MWh£35MWh£37MWh£39MWh£35MWh£33MWh£32MWh£31MWh

CLICK TO EDIT MASTER TITLE STYLEINENCO TRADING GAME

13th June

Bullish hammer candle seen on chart after prices rise off 18th April lows

£32MWh

CLICK TO EDIT MASTER TITLE STYLEINENCO TRADING GAME

20th June

5 day moving average crosses above 21 day moving average

£34MWh

CLICK TO EDIT MASTER TITLE STYLEINENCO TRADING GAME

27th June

MACD crosses above its zero line

£36MWh

CLICK TO EDIT MASTER TITLE STYLEINENCO TRADING GAME

4th July

Evening star candle pattern

£37MWh

CLICK TO EDIT MASTER TITLE STYLEINENCO TRADING GAME

11th July

Bearish candle trades through central Bollinger band

£34MWh

CLICK TO EDIT MASTER TITLE STYLEINENCO TRADING GAME

18th July

Prices closed below previous support level of 31

31

£30MWh

CLICK TO EDIT MASTER TITLE STYLEINENCO TRADING GAME

25th July

Fails to break previous low and bounces off lower bollingerband

£28MWh

CLICK TO EDIT MASTER TITLE STYLEINENCO TRADING GAME

1st August

Stochastics rise above oversold line

£29MWh

CLICK TO EDIT MASTER TITLE STYLEINENCO TRADING GAME

8th August

Prices gap up, leaving a breakaway gap on the chart

£32MWh

CLICK TO EDIT MASTER TITLE STYLEINENCO TRADING GAME

15th August

Continuation candle pattern observed

£34MWh

CLICK TO EDIT MASTER TITLE STYLEINENCO TRADING GAME

22nd

Prices test 4th July level on strong volume

£37MWh

CLICK TO EDIT MASTER TITLE STYLEINENCO TRADING GAME

29th August

Prices reach 9th May highs

TOO LATE!!!!!

You should have bought earlier

£39MWh

CLICK TO EDIT MASTER TITLE STYLE

SESSION 3Improve your buyingfor the future

Putting together an integrated

energy strategy

CLICK TO EDIT MASTER TITLE STYLEPROCUREMENT STRATEGY SUMMARY

Choose the right supplier and the right contract type that enables you to implement your strategy

Execute your strategy to optimise your energy costs by purchasing from the wholesale market

Identify your goals and choose the appropriate strategy to match your appetite for risk

EnergyProcurement

Strategy & Risk

Management

Trading

CLICK TO EDIT MASTER TITLE STYLEHOW DO WE HELP YOU?

Delivery and benefits Delivery and benefits Delivery and benefits Delivery and benefits Delivery and benefits

Risk Scoping Session

Contract negotiation

Energy Trading Reporting & MI Optimisations

CLICK TO EDIT MASTER TITLE STYLEWHAT STRATEGY WOULD WORK BEST FOR YOU?

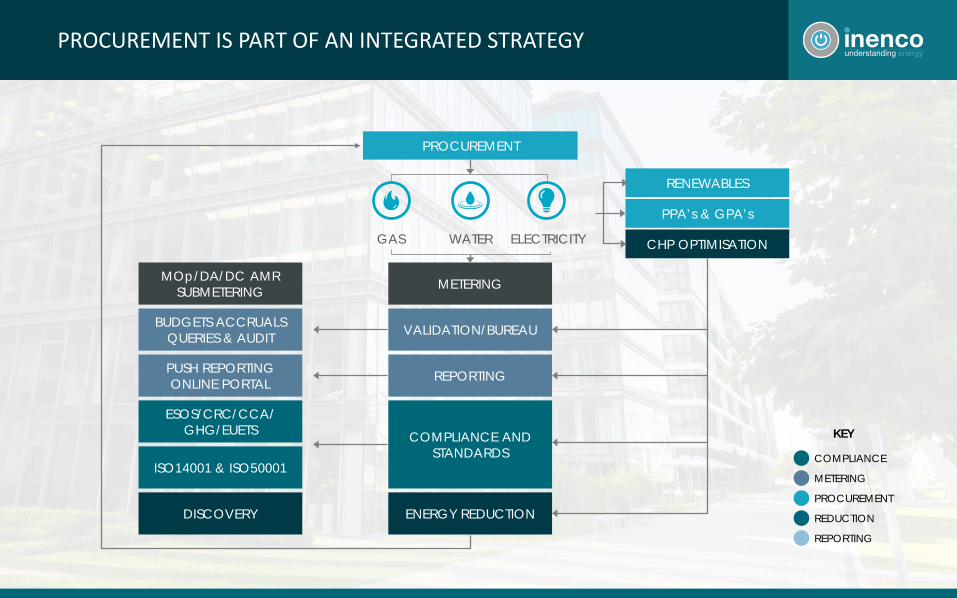

CLICK TO EDIT MASTER TITLE STYLEPROCUREMENT IS PART OF AN INTEGRATED STRATEGY

KEY

COMPLIANCE

RENEWABLES

CHP OPTIMISATION

PPA’s & GPA’s

ESOS/CRC/CCA/ GHG/EUETS

ISO14001 & ISO50001

DISCOVERY

MOp/DA/DC AMR SUBMETERING

BUDGETS ACCRUALS QUERIES & AUDIT

PUSH REPORTINGONLINE PORTAL

ENERGY REDUCTION

METERING

VALIDATION/BUREAU

COMPLIANCE AND STANDARDS

REPORTING

PROCUREMENT

GAS ELECTRICITYWATER

METERING

PROCUREMENT

REDUCTION

REPORTING

CLICK TO EDIT MASTER TITLE STYLEHOW TO BUILD AN ENERGY STRATEGY

REFRESH

GET A BOARD MANDATE 1

Review Your Existing

Situation

2

Set Your Targets

3

Review The Available

Alternatives

4

Challenge Your Review

5

Understand The

Implications

6

Prioritize Your Activities

7

Plan Your Next Steps

8

Implement Your Key

Tasks

9

Measure The Performance

10

CLICK TO EDIT MASTER TITLE STYLESOME INTERESTING MARKET FACTS

MARKETSOver 95% of

Inenco’s £3Bn energy portfolio is purchased via the wholesale energy market

CONSULTANTSSome 80% of all

companies use energy consultants for

support in buying energy

TECHNICAL ANALYSISTypically

averages over 90% decision

making accuracy

COMMODITYWholesale

commodity prices have gone up

40% since April 2016

BUYINGWINDOW

A three year procurement window

outperforms a one year window by

typically 15%

CLICK TO EDIT MASTER TITLE STYLEWHAT SHOULD YOU BE TELLING THE BOARD!

‘After a period of relative stability –prices are now going up due to both commodity and non commodity cost increases’

‘Markets are becoming more volatile with increases in intermittent renewable generation’

‘Flexible energy procurement helps manage risk’

‘Longer term integrated energy strategies are the way forward’

CLICK TO EDIT MASTER TITLE STYLE

• Established in 1968

• 250+ staff

• Procurement

• Bureau & Reporting

• Energy Optimisation

• Metering Management

• Legislative compliance

• Renewables & PPAs

• Water management

INENCO

SCALE

INENCO GROUP

Established 1983100+ staffFixed procurement SME focusedEnergy surveys

INENCO DIRECT

Lytham (Head Office)LiverpoolBudapest

OFFICES

£3bn£2bn worth of electricity

and £1bn gas procured for our clients annually

utility invoices processed and validated in our system

every year

~1,400,000

CLICK TO EDIT MASTER TITLE STYLEFCA ACCREDITATION

CLICK TO EDIT MASTER TITLE STYLEWHY USE INENCO?

As one of the largest TPIs in the UK, Inenco is playing a role in improving trust and transparency in the sector.

We have participated in the development of Ofgem’s Code of Practice over the past two years and in the absence of regulation, continue to voluntarily adhere to both the UIA and Microbusiness TPI Codes of Practice.

At Inenco we pride ourselves on being a trusted consumer champion.

We offer total transparency in what we do, and support our customers on minimising their costs for every element of their utility bills, through efficiencies, compliance or innovation.

Our sector based team have acquired specialist knowledge and as an agnostic but experienced consultancy we have the scale, heritage and breadth to advise you on every element of your utility strategy.”

CLICK TO EDIT MASTER TITLE STYLE

YOUR QUESTIONS

The image part with relationship ID rId2 was not found in the file.

CLICK TO EDIT MASTER TITLE STYLE