kibali site visit - randgold resources site... · kibali site visit january 2015 ... 19 x 777g...

TRANSCRIPT

1

Kibali site visitJanuary 2015

Randgold Central and East Africa structure…

MetManagerAndrews

Awini

KibaliFinancialManagerNortonKabeya

Eng.Manager

DriesMetrovich

GM Kibali MineCharles Wells

CEO RRLMark Bristow

COO C & E / AWillem Jacobs

Social &Sustainability.

ManagerCyrille

Mutombo

MineDirector

BruceFerreira

SupplyChainTeddy

Mbiyavanga

Camp Mngr +Regional Gov. LiasonJean Pierre

Mbuluyo

SafetyManagerEghardVoigt

HRManager

LucieKikadi

ExplorationManager

JustusKwibisa

MRMManagerGeorgeKondela

Kinshasa OfficeManager

RoyBondo

Country ManagerCyrille Mutombo

FINANCENaude van Eck

2

Kibali supply routes…

Kibali

Dar es Salaam

Mombasa

1 800 km

1 950 km

Overview of Kibali history in Randgold….

2006On site due diligence

by Randgold

Sep 2009Acquired

Moto Goldmines (70% Kibali) in JV with AGA in a public

international auction

Dec 2009JV acquired a further 20% in

Kibali from SOKIMO

Feasibility updated reserves

doubled to over 10Moz

Sep 2013

2010Formal notice to

illegal miners and alternate work

programme started

Mar 2010MOU signed with Catholic Church

Jul 2010

Aru-Doko road upgrade completed

Nov 2010Established Kokiza village

for resettlement

Feb 2011

Revisedfeasibility

Aug 2011 May 2012First Gold &

completion of RAP

Commissioning and ramp up of met facility and

associated infrastructure

completed

Pre-construction

started

Oct 2011 2014JV approves feasibility and vote capital

3

Kibali…project update to Dec 2014

Construction of the metallurgical facility completed and design parameters achieved

Construction related contractors in the metallurgical plant demobilised

Nzoro II hydropower station completed - all 4 turbines commissioned and a consistent power feed into the grid in line with design parameters

Vertical and decline shaft systems remain within budget and on schedule

Quarter on quarter improvement in throughput, recovery and gold production.

UG stoping commenced in Q4

RAP inclusive of Catholic Church Complex completed

Construction of the Ambarau hydro station started

Establishment of an elected community forum as the main platform for engagement with local communities

Award in excess of $600 million of business to companies with 50% or more Congolese shareholding since the inception of the project

Business Plan for 2015…

Gold production target 600 000 ounces

UG mine development on schedule

Commission Ambarau hydrostation

Continued nationalisation of management team

Secure more exploration permits in DRC

Collect TVA

Work with Government and industry to establish competitive mining code

Obtain ISO 14001 EMS certification

Establish large scale agribusiness venture

Improve working relationship with Provincial Government

4

Mineral resources and exploration

Congo Craton…

10km

N

N. MARA4.97 Moz

ADUMBI1.67 Moz

MAKAPELA1.16 Moz

KIBALI22.2 Moz ZANI KODO

2.97 Moz

MONGBWALU2.93 Moz

BUZWAGI3.43 Moz

GOLDEN PRIDE1.36 Moz

BULYANHULU15.63 Moz

GEITA10.67 Moz

KCD deposit

TWANGIZA6.3Moz

N

100km

Uganda

Tanzania

Kenya

DRC

5

Resource location

Mengu Hill

Megi

Mengu Hill

Reserve - 479KozResource outside reserve – 237Koz

Resource outside reserve – 287Koz (1.84g/t)

Megi

Gorumbwa

Resource outside reserve – 920Koz (3.66g/t)

KCD Dec 30th 2013

Mengu village

Resource outside reserve – 54Koz

Pakaka

Stockpile - 248Koz Open Pit Reserve – 1,415Koz (2.89g/t)Open pit resource outside reserve – 1,399Koz Underground Reserve – 8,009Koz (5.70g/t)Underground resource not in reserve –6,404Koz

Kombokolo

Reserve - 119KozResource outside reserve – 49Koz

Sessenge

Reserve – 274KozResource outside reserve – 368Koz

Pamao

Reserve - 268KozResource outside reserve – 448Koz

Resource outside reserve – 129Koz (1.4g/t)

Marakeke

Reserve - 751KozResource outside reserve – 530Koz

Kibali R.

Nzoro R.

Aru / Arua

WatsaDome

Reserve

Resources

Mofu

Gorumbwa

Mofu

Reserve – 24KozResource outside reserve – 7koz

3000 Lode 5000 Lode

9000 Lode

500m

KCD Resource halos and Project reserves

Type CategoryTonnes

(Mt)Grade (g/t)

Gold (Moz)

Stockpile Proven 3.2 2.3 0.2

Open PitsProven and

Probable42 2.5 3.4

Underground Probable 44 5.7 8.0

TotalProven and

Probable89 4.1 12

Reserves as at 31 Dec 2013Sessenge

6

NORTH

1

23

8

5White House

5105 HG

3000 lodeLow grade halo

5103 - HG

5110 - HG

Dispatch

9000 UG

3000 UG

DoleriteChert

Ironstone 3003

3005

3004

KCD…upside potential

Domain Au g/t Ounces

3003 1.8 397,574

3004 1.75 80,242

3005 0.89 7,663

67

Mofu and Gorumbwa deposits…

GRC09712m @ 4.51g/t (from 0m)

GRC10214m @ 3.04g/t (from 22m)

GRC10420m @ 5.72g/t (from 22m)

GDD09414m @ 7.73g/t from 126m

1001100210031004

1005100610071008

Ore domains

$1500 Pit

Nov.14

NORTHGorumbwa

historical pit

Gorumbwa Historical shaft

Gorumbwa Historical UG

depletion

7

Kalimva

Pakaka

KCD

Zambula

KCD

N

WatsaDome

35km KZ structure, terrain boundary hosting multiple plunging orebodies

Potential is open down dip and down plunge

Gaps in coverage along the structure being targeted at surface

Review and analysis of controls and mineralisation footprint in progress

10km

Kibali…world class potential over35km of strike

Plunging mineralised lode

Kalimva

Mofu

Mengu Hill

Mengu village

Marakeke

Megi

Pamao

Pakaka

AerodromeRhino

Agbarabo

KCD

Kombokolo

Gorumbwa

Sessenge

Kibali South

5850mRL

Gaps in drilling

5750mRL

2000m

KZ structure gap analysis…

250mMineralization Foot Print

“S2” structure

8

KZ structure…long section

Kanga SudKCD

1.7kmKibali Sud

Sessenge SW

Airborne EM conductivity

NESW

+150m

9000 lode

Kibali River Durba hill

500m

1000m

250m

1000m17.8 moz resource endowment

KZ structure…cross section…

500m

1000m

250m

Mengu Hill PakakaPamaoMegiMarakeke

Mengu village

0.9km0.8km

6 Km

716 Koz 1.28 moz716Koz287Koz129 Koz

Airborne EM conductivity

+150m

SENW

Sayi Gecamine

54 Koz

1000m3.1 moz resource endowment

“S2” structure

9

Kilo JV … 10km mineralized potential

10km

Gold target

ISIRO BELT

NGAYU BELT

10km

N

Yambenda

Bonzuzu

Mbese

Nepoko

30-4950-6970-99>100

Soil contoursAu ppb

3

5

7

~10km

Metallurgical facility

10

Metallurgical plant…

Twin Circuit metallurgical facility…

CIL F

lota

tion

CIL F

lota

tion

2

Flo

tatio

n1

Conc.

Oxide + Sulphide treatment Sulphide Only treatment

Conc.

UFG/Pump Cell UFG/Pump

Cell

Ball 2 Ball 1Ball 2Ball 1

11

Twin circuit processing strategy…

Material crushed through mineral sizer directly into ball mill 6.1m diam. x 9.5m

Gravity and flash float ahead of conventional CIL

CIL tails through detox to lined TSF

Circuit designed at 300ktpm or 3.6MTPA

Each Ball Mill capable of 300ktpm or 3.6MTPA (as per Tongon). CIL residence time capable of 358ktpm / 4.3MTPA

Conversion to sulphide processing through addition of a second bank of flotation cells to follow the gravity and flash float circuits (making it identical to the other sulphide circuit)

Oxide / transition Sulphide

Fresh Open Pit material crushed through primary jaw and secondary cone (with provision for tertiary cone if required) onto mill feed stockpile. Mill identical to oxide/trans at 6.1m diam. x 9.5m

Fresh underground material crushed through primary jaw crushers underground and conveyed to stockpile inside met plant ahead of secondary crushing

Gravity and flash float

Full flotation

Flotation tails (benign) direct to unlined TSF or backfill/paste plant

Circuit designed at 300ktpm or 3.6MTPA (single mill and flotation bank)

Mill capable of 300ktpm or 3.6MTPA . Oxide mill to be converted to sulphide mill increasing fresh material milling capability to 600ktpm or 7.2MTPA

Plant throughput and recovery…

5000

7000

9000

11000

13000

15000

17000

19000

21000

71

73

75

77

79

81

83

85

87

89

91

1-O

ct

8-O

ct

15-O

ct

22-O

ct

29-O

ct

5-N

ov

12-N

ov

19-N

ov

26-N

ov

3-D

ec

10-D

ec

17-D

ec

24-D

ec

31-D

ec

Th

rou

gh

pu

t 7d

ay a

vera

ge

[tp

d]

Ove

rall

reco

very

7d

ay a

vera

ge

[%

]

7 per. Mov. Avg. (Overall recovery) Linear (Overall recovery)

7 per. Mov. Avg. (Throughput [tpd]) Linear (Throughput [tpd])

87% Target 19000 tpd

12

Mining

A fully integrated mine design…

9000 lode5000 lode

Shaft

Boxcut

Open pit

Mine design

Haulage level

Crusher and Pumping stations

1km

13

Opencast mining…

Multiple pits to be mined over 10 years

KCD pit mining started in July 2012

Production achieved with trained local operators

3 x Liebher 9350 diggers , 1 x Liebher 984 digger and 19 x 777G dedicated to production and auxiliary equipment as support

The mine plan, including ore production and plant feed, was achieved for the year

Overview

Underground Mine Complex…Shaft

A 760m shaft, 8m diameter concrete lined

Shaft capacity Wet tonnes(includes 5% moisture) = 3.6Mt/yr.

Shaft capacity Dry tonnes = 3.43Mt/yr.

Average tonnage hoisted from the shaft on current schedule = 3Mt/yr.

Dedicated hoisting shaft but it will be equipped with a service cage for maintenance purposes

Material Handling and Orepass

Nine orepasses feeding onto a haulage drive

Automated loader feeding from orepasses to crusher

2 sets of crushers underground with 1000 t capacity for coarse and fine bin each.

Paste Plant

Paste plant with 192 m3/hr capacity

Full flexibility in throughput and binder content

Construction started and planned for commissioning in April 2015

14

Underground mining…vertical shaft

Shaft current depth 720m

83 days ahead of schedule

Development ongoing on last level close to main infrastructure

Target to finish sinking in Q3 2015 and equip in Q1 2016

Off shaft development will continue in 2016 together with equipment of main infrastructure

Shaft fully commissioned and hoisted Q3 2017

Shaft development progress…

Railway Haulage

Settlers

Trommels

Clear Water Dams

INTERFACE #1

1st MAIN SINK

-724.5

-682.0

-525.0

4m Vent ShaftVertical Shaft

2nd MAIN SINK

3rd MAIN SINK

4th MAIN SINK

-760.0

Temporary Ore

Pass

Fine Ore Silos

Crusher Station

Coarse Ore Silos

INTERFACE #4

INTERFACE #3

INTERFACE #2

Shaft Bottom

Main Pump Station

-293.4m 16Feb14

-7.0m 25Jan13

-14.8m 08Apr13

-28.0m 30Apr13

-525.0

PRE – SINK

(-25.0m to -102.4m)

Actual Start 26-Apr-13

Actual Finish 30-Jul-13

SLOW SINK

(-102.4m to -182.0m)Actual Start 26-Apr-

13Actual Finish to 30-

Jul-13Actual Start 25-

Dec-13

-182.0m 24Dec13

-257.0m 02Feb14

-335.5m 05Mar14

-158.0m 12Dec13

-419.5m 01Apr14

-485.5m 05May14

-525.0m 26-May-14

Plan Q1 2015Actual PTD – Dec 2014

15

Decline Development

Decline development started in Dec 2012 with Byrnecut as contractor

Byrnecut consistently achieving the development targets

Rate of advance has been materially better than planned in the feasibility

An average of 300m/month/jumbo was reached in development, with the decline contractor has now ramped up to 900m/month

A total of 12.1km was developed project to date of which 10km in the capital side and 2 km in opex

For 2014 a total of 8km was developed of which 6km in capital and 2 km in opex

Production started from the first stope in Dec 14

Target from stoping is 30Kt/month from Q1 to Q3

Stoping tonnes ramp up to 70Ktonnes/month in Q4

Completion ofB1_Decline

C_Decline

665L

OCT 2014

NOV 2014

DEC 2014

Actual YTD ending Q3 2014

630L595L560L

B1_Incline

620L_MRA_N

Quarter Quarter Quarter 9 months 9 monthsended ended ended ended ended30 Sep 30 Jun 30 Sep 30 Sep 30 Sep

2014 2014 2013 2014 2013Ore tonnes mined 2 843 - -Development metres 1 802 1 222 2 580

Decline development..Q4 plan

16

665 XC2 STOPE FIRING SEQUENCEID LEVEL Firing Grade (gr/t) Tonnages KG (ANFO) Orebody

1 665 SLOT RAISE (ready done Up to 10 m) 7.2 800 1524 5110

2 665 SLOT RAISE ( Up to 20 m) 7.2 800 1524 5110

3 665 R1‐2W & R1‐2E Up to 20m 7.2 1350 1684 5110

4 665 R3‐6W Up To 20m 7.2 850 873 5110

5 665 R3‐7E Up to 20 m 7.2 1650 2041 5110

6 665 SLOT RAISE + REMAINDER OF SLOT RINGS 7.2 2698.4 3530 5110

7 665 PRODUCTION RINGS 1 &2 3.7 10537.60 4436 5110

8 665 PRODUCTION RINGS 3 2.3 5738.60 2164 Waste Min.

9 665 PRODUCTION RINGS : R4, R5, R6, R7, R8 & R9 5.6 31528 11815 5103

TOTAL 5.1 55952.6 29591

First Stope MS-1…

Kibali Underground mining…Shaft Sinking

17

Hydropower

Our power strategy…

Supply concept is a hybrid arrangement

Peak power Deliver peak power on the available river schemes average flows

Dry season low flow powerMaximize the number of stations supplying to maximize the power available in the low flow periods.

Diesel back-up generationFor power load fluctuations of shaft winder and Met PlantInitially provide dry season make-up power from high speed diesel unitsSubstitute (diesel generation) with more hydro stations as overall power demand grows

18

Station Plan Min output (low flow

MW)

TargetOutput

(peak MW)

Completion

Nzoro 2 Operational 5 22 QTR2 2014

Kibali 1(Ambarau)

Under Construction 2.5 10QTR2 2016(1st power Q3 2015)

Kibali 2(Azambi)

Designed and planned for 2018

2.5 10 QTR3 2018

Total Main 10 42

Our plan…the supply of power via hydro

Nzoro ll hydropower plant construction…

4 turbines commissioned and 3 operational -currently generating 16,8MW

Synchronisation of power produced from Nzoro 2 with diesel power plant via Power Management System

View from canal of intake structure and control room

Views from canal of forebay structure and control room

Entrance ramp and cable rack for main power output cables

Turbine installations on lower level

Views of Nzoro river dammed up and diversion into Intake

19

Project Update

Investment phases…

Phase 2 capital programme is estimated at US$700m before escalation provisions and contingencies which will run concurrently with Phase 1 but will extend over a longer period, is focused primarily on the underground development and includes a twin decline and vertical shaft system as well as three hydropower stations. This is expected to bring the underground into first production by the end of 2014, with vertical shaft handover scheduled in 2017.

Phase 1 capital programme is estimated at US$1130m and will cover the metallurgical facility, one hydropower station and back-up thermal power facility, construction of the tailings storage facility, relocation of villages, open pit mining and all shared infrastructure. This is expected to be completed by December 2014.

20

Kibali…actual and forecast production

0

1

2

3

4

5

0

100

200

300

400

500

600

700

2013 2014 2015 2016 2017 2018 2019

Actual production Total cash cost/oz Capex Grade

Grade g/tTotal cash cost/oz

Capex $m

Gradeg/t

ProductionOz 000

Cash cost$/oz

Capex$m

Health and Safety

21

Kibali, health safety and environment…

113,14

70,2761,05

50,29

0

20

40

60

80

100

120

2011 2012 2013 2014

RA

TE

Malaria Incident Rate

2011-20146,14

2,49

0,59 0,37

0

1

2

3

4

5

6

7

2011 2012 2013 2014

RA

TE

LTIFR

Health and SafetyRecently passed 2 million LTI free hours

5 Accredited St John Trainers

Malaria incident rate decreasing (reduction +55% since start of project in 2011)

EBOLA PPE management plan in place

Environment

No major environmental incidents

ISO14001 preparations for accreditation in 2015

Biodiversity action plans in progress.

Community

22

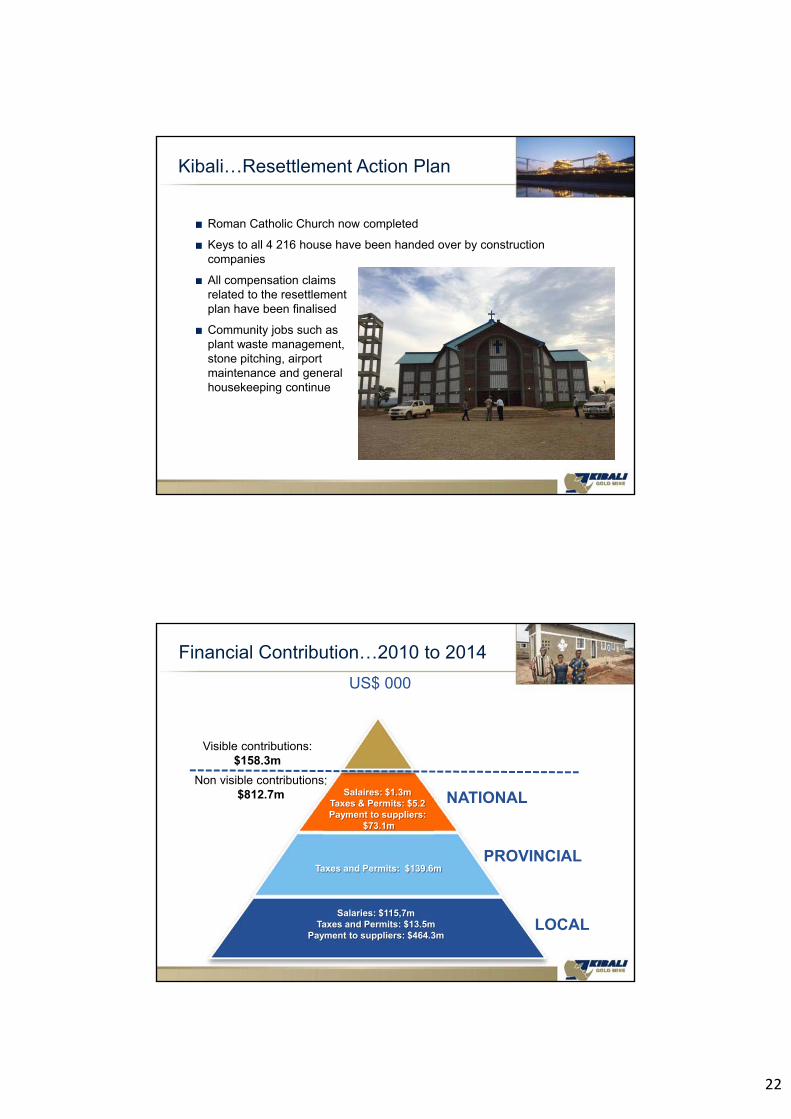

Kibali…Resettlement Action Plan

Roman Catholic Church now completed

Keys to all 4 216 house have been handed over by construction companies

All compensation claims related to the resettlement plan have been finalised

Community jobs such as plant waste management, stone pitching, airport maintenance and general housekeeping continue

Visible contributions:$158.3m

Non visible contributions:$812.7m Salaires: $1.3m

Taxes & Permits: $5.2Payment to suppliers:

$73.1m

Taxes and Permits: $139.6m

Salaries: $115,7mTaxes and Permits: $13.5m

Payment to suppliers: $464.3m

NATIONAL

PROVINCIAL

LOCAL

Financial Contribution…2010 to 2014

US$ 000

23

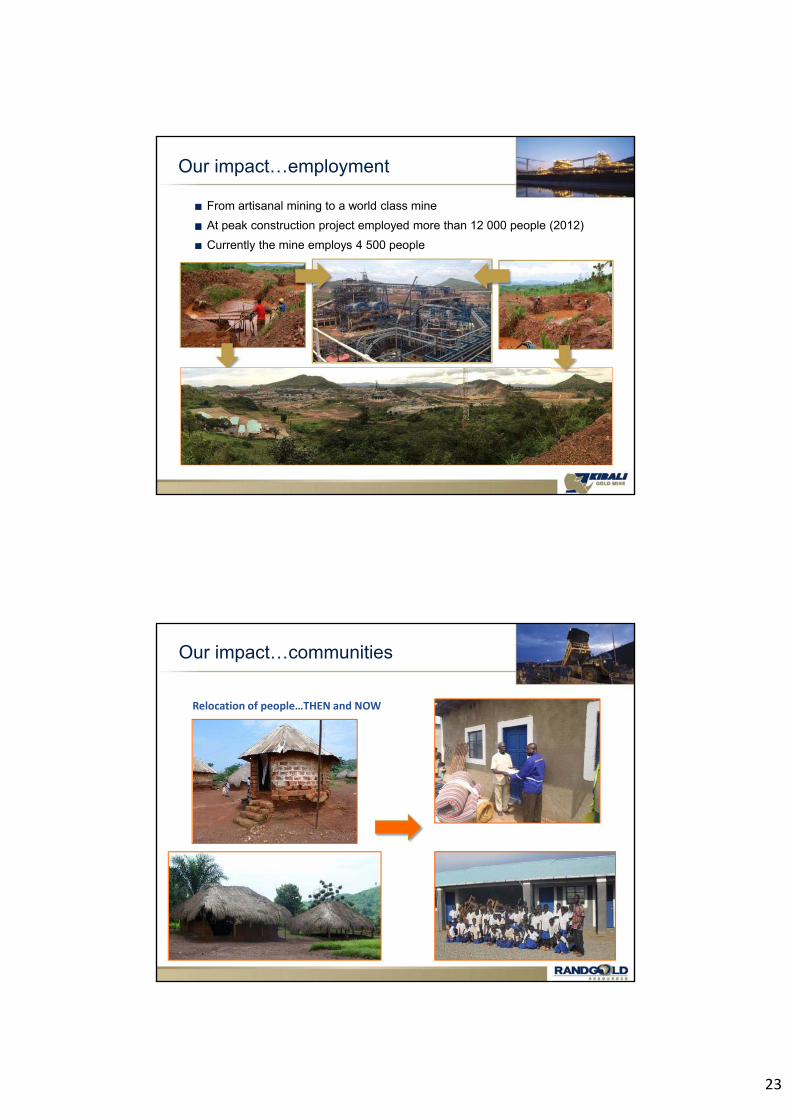

Our impact…employment

From artisanal mining to a world class mine

At peak construction project employed more than 12 000 people (2012)

Currently the mine employs 4 500 people

Our impact…communities

Relocation of people…THEN and NOW

24

Our impact…health

Handover of medical equipment - 2 containers in 2010, 2 in 2013 and 2 planned for 2014Durba mine clinic handed over to Provincial Health AuthoritiesWaste management initiative through an incentivised competition ‘ Pride of Ownership’ 5 clinics and health posts, part of the RAP

Public health

Handover of medical equipment Provincial Minister of Health receives keys for Centre Hospital Kibali

Our impact…education

15 schools build as part of the RAP project

3 schools built though community projects

Capacity building through funding a printing house

Stationaries distributed to more than 5,000 pupils in 2010

Support to orphanages through payment of school fees

Mosquito nets distributed to Adia Lemi boarding school

A tertiary institution built (Watsa ISP)

25

Durba…2006

Durba…2014

26

Our impact: infrastructures

Infrastructure: The road between Arua and the site (Doko) upgraded

Doko Aru: 180 km

Aru Ariwara: 45 km

Doko Watsa: 14 km

Doko Nzoro: 34 km

Kokiza: 90 km

Road network > 350 km

Roads…THEN and NOW

Disclaimer…

Randgold reports its mineral resources and mineral reserves in accordance with the JORC 2012 code. As suchnumbers are reported to the second significant digit. They are equivalent to National Instrument 43-101. Mineralresources are reported at a cut-off grade based on a gold price of US$1 500/oz.The reporting of mineral reserves is also in accordance with Industry Guide 7. Pit optimisations are carried out at agold price of US$1 000/oz, except for Morila which is reported at US$1 300/oz. Mineral reserves are reported at acut-off grade based on US$1 000/oz gold price within the pit designs. Underground reserves are also based on agold price of US$1 000/oz. Dilution and ore loss are incorporated into the calculation of reserves. Cautionary noteto US investors: The United States Securities and Exchange Commission (the SEC) permits mining companies, intheir filings with the SEC, to disclose only proven and probable ore reserves. Randgold uses certain terms in thisannual report such as ‘resources’, that the SEC does not recognise and strictly prohibits the company fromincluding in its filings with the SEC. Investors are cautioned not to assume that all or any parts of the company’sresources will ever be converted into reserves which qualify as ‘proven and probable reserves’ for the purposes ofthe SEC’s Industry Guide number 7.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS: Except for the historical informationcontained herein, the matters discussed in this presentation are forward-looking statements within the meaning ofSection 27A of the US Securities Act of 1933 and Section 21E of the US Securities Exchange Act of 1934, andapplicable Canadian securities legislation. Forward-looking statements include, but are not limited to, statementswith respect to the future price of gold, the estimation of mineral reserves and resources, the realisation of mineralreserve estimates, the timing and amount of estimated future production, costs of production, reservedetermination and reserve conversion rates. Generally, these forward-looking statements can be identified by theuse of forward-looking terminology such as ‘will’, ‘plans’, ‘expects’ or ‘does not expect’, ‘is expected’, ‘budget’,‘scheduled’, ‘estimates’, ‘forecasts’, ‘intends’, ‘anticipates’ or ‘does not anticipate’, or ‘believes’, or variations ofsuch words and phrases or state that certain actions, events or results ‘may’, ‘could’, ‘would’, ‘might’ or ‘will betaken’, ‘occur’ or ‘be achieved’. Assumptions upon which such forward-looking statements are based are in turnbased on factors and events that are not within the control of Randgold Resources Limited (‘Randgold’) and thereis no assurance they will prove to be correct. Forward-looking statements are subject to known and unknownrisks, uncertainties and other factors that may cause the actual results, level of activity, performance orachievements of Randgold to be materially different from those expressed or implied by such forward-lookingstatements, including but not limited to: risks related to mining operations, including political risks and instabilityand risks related to international operations, actual results of current exploration activities, conclusions ofeconomic evaluations, changes in project parameters as plans continue to be refined, as well as those factorsdiscussed in Randgold’s filings with the US Securities and Exchange Commission (the ‘SEC’). Although Randgoldhas attempted to identify important factors that could cause actual results to differ materially from those containedin forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated orintended. There can be no assurance that such statements will prove to be accurate, as actual results and futureevents could differ materially from those anticipated in such statements. Accordingly, readers should not placeundue reliance on forward-looking statements. Randgold does not undertake to update any forward-lookingstatements herein, except in accordance with applicable securities laws.CAUTIONARY NOTE TO US INVESTORS: The SEC permits companies, in their filings with the SEC, to discloseonly proven and probable ore reserves. We use certain terms in this release, such as ‘resources’, that the SECdoes not recognise and strictly prohibits us from including in our filings with the SEC. Investors are cautioned notto assume that all or any parts of our resources will ever be converted into reserves which qualify as ‘proven andprobable reserves’ for the purposes of the SEC’s Industry Guide number 7.