knowledge intensive service activities in innovation of ... · pdf fileknowledge-intensive...

TRANSCRIPT

http://aegis.uws.edu.au/KISA/main.html

M. Cristina Martinez-FernandezClaudine SoosayVenni Venkata Krishna

Knowledge Intensive Service Activities

in Innovation of the Tourism Industry in Australia

Phillip TonerTim TurpinMerete Bjorkli Kalika N. Doloswala

Knowledge-Intensive Service Activities (KISA)in Innovation of the Tourism Industry

in Australia

October 2005

AEGIS is a Research Centre of the University of Western Sydney.

M. Cristina Martinez-Fernandez Claudine Soosay

Venni Venkata KrishnaPhillip Toner

Tim TurpinMerete Bjorkli

Kalika N. DoloswalaMerete Bjorkli

2 KISA in Innovation of the Tourism Industry

AcknowledgementsThis report has been prepared by the Australian Expert Group in Industry Studies (AEGIS). AEGIS is a research centre of the University of Western Sydney. The team involved in this report includes Dr M. Cristina Martinez-Fernandez (Chief Investigator), Dr Claudine Soosay, Professor Venni Venkata Krishna, Dr Phillip Toner, Professor Tim Turpin, Merete Bjorkli and Kalika N. Doloswala.

The cover artwork is credited to Monty Chanthapanya.

We are grateful to the contribution of Professor Jane Marceau to the early developments of the KISA project.KISA project.KISA

The study is part of an ARC Linkage funded project (LP 0349167) in partnership with Australian Government Departments DITR and DCITA. The report also informs the OECD based KISA project.

DisclaimerThe views expressed in this report are solely those of the authors and should not be attributed to the Department of Industry Tourism and Resources or the Department of Communications, Information Technology and the Arts.

© Australian Expert Group in Industry Studies, 2005

ISBN 1 74108 107 6 print editionISBN 1 74108 108 4 web edition

Published by the University of Western Sydney, October 2005http://www.uws.edu.au

Martinez-Fernandez, M.C.; C. Soosay; V.V. Krishna; P. Toner; T. turpin; M. Bjorkli and K.N. Doloswala (2005) Knowledge Intensive Service Activities (KISA) in Innovation of the Tourism Industry in Australia, University of Western Sydney: Sydney.

For further information please contact:Dr Cristina Martinez-FernandezAEGISUniversity Western SydneyPO Box Q1287 QVB Post Offi ce NSW [email protected]: + 61 28255 6200Fax: +61 2 8255 6222

Or visit the project website: http://aegis.uws.edu.au/KISA/kisa_main.html

3AEGIS UWS

This report focuses on the role of knowledge intensive service activities in the tourism industry in Australia. The study is part of an ARC funded project1 on ‘Driving Innovation: Mixing, Matching and Transforming Knowledge-Intensive Services into Innovation.’ The study is also part of the OECD KISA project2.

Overview of the Industry

The Australian tourism industry has experienced a strong growth over the past 20 years. In 2002-2003, the tourism industry contributed 4.2 per cent to Australia’s gross domestic product. Four industries account for 80.1 percent of the output of the tourism. These industries are Transport and storage (27.6%); Accommodation, cafes and restaurants (20.9%) Manufacturing (16.9%) and Retail trade (14.7%).

The tourism sector draws on a wide range of industries supplying both services and goods. In 2002-03, 540,700 persons were employed. The majority of the jobs in the tourism industry are in retail trade, the accommodation sector and cafés and restaurants. There are over 350,000 tourism related businesses in Australia. Most businesses are small to medium sized, and 90 percent employ less than 20 staff. Tourism’s share of total employment (5.7%) is 50 percent larger than the industry’s share of national gross value added (3.8%). This implies that labour productivity, as measured by gross value added per employee in the tourism industry is lower than for the economy in general.

Tourism has less than half the number of Professionals (9.1% compared to 18.8%) and over 40 percent fewer Managers and Administrators (7.2% compared to 4.2%) than for all industries. Tourism’s share of Elementary Clerical, Sales & Service Workers is some 61 percent larger than for the economy as a whole. R&D expenditure on tourism as a share of the industry’s gross product is comparatively low. Tourism R&D was the equivalent of just 0.06 percent of tourism gross product in 2000-01. For the economy as a whole, R&D as a share of total gross domestic product was 1.53 percent in 2000-01. Although R&D as a share of tourism’s gross domestic product is 25 times less than R&D share of GDP, tourism fi rms do engage on research activities linked to innovation such as research on new markets.

Policies and Programs supporting the industry

A review of the tourism industry in Australia was undertaken as part of the development of the Tourism White Paper. The White Paper was subsequently released in November 2003 with an additional $235 million being put towards the tourism industry. A signifi cant change was the creation of a new body - Tourism Australia – that brings together the Australian Tourism Commission, See Australia, the Bureau of Tourism Research and the Tourism Forecasting Council.

Direct public tourism related expenditure accounted for AUD 140 million in 2002-3. Most of the expenditure covered activities by the Australian Tourist Commission, Export Market Development Grants, Regional Tourism Projects and Tourism Policy.

Executive Summary

4 KISA in Innovation of the Tourism Industry

Tourism fi rms are eligible for assistance under a range of generic industry programs offered by government but most tourism fi rms do not meet the criteria for those programs as they focus on innovation and research commercialisation.

Survey of Tourism Firms: Key Findings

The survey indicated that the fi rms in the tourism industry are quite innovative in terms of implementing product, process and organizational changes. Thirty-nine of the 44 fi rms (89%) made changes that involved a new product, a new process or other change such as a substantially changed accounting system or human resources management system. The innovation in these fi rms was mostly incremental (a series of small/gradual changes over time).

In relation to the use of inputs to KISA for the development and introduction of the above innovations, the most commonly used services were Research & Development, Marketing and Promotion, Accounting and Financial services and IT services. KISA-related services were used differently when mapped against the business life-cycle of the fi rm. Starting business did not use any service very often. Mature business used services regularly, especially IT services. Business in expansion used all services but specially marketing and IT. Firms identifi ed that they were most likely to access services intermittently (i.e. once or twice through the year).

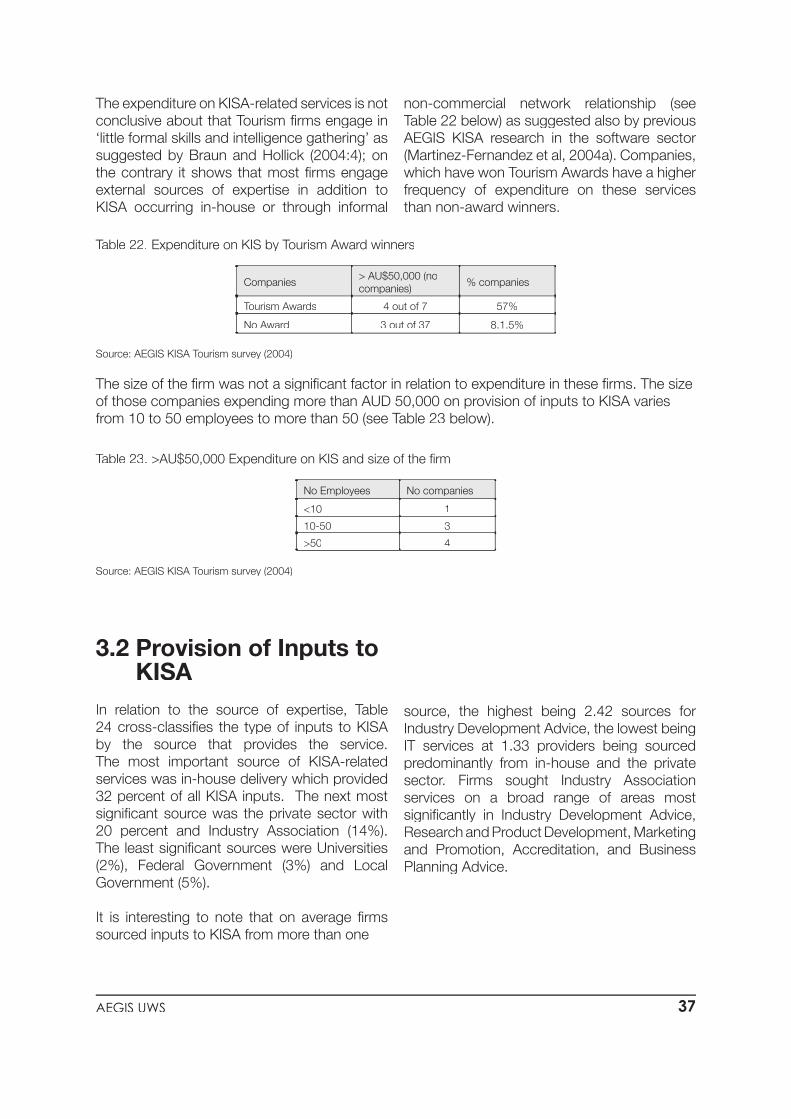

The most important source of KISA-related services was in-house delivery which provided 32 percent of all KISA inputs. The next most signifi cant source was the private sector with 20 percent and Industry Association (14%). The least signifi cant sources were Universities (2%), Federal Government (3%) and Local Government (5%).

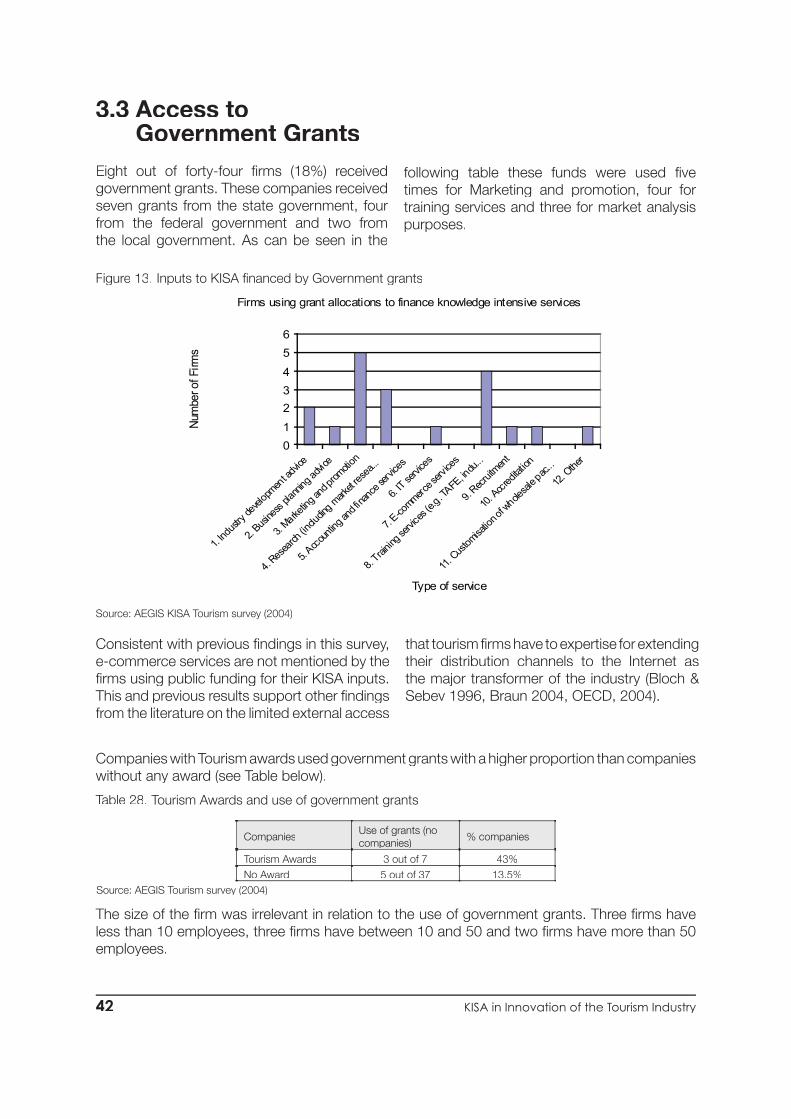

Expenditure on KISA related services was not very high. Sixty-four percent of respondents indicated that they spent less than AU$10,000 on KISA inputs. Eight of forty-four fi rms (18%) received government grants and these funds were used for Marketing and promotion, training services and research purposes.

Case studies: Key Findings

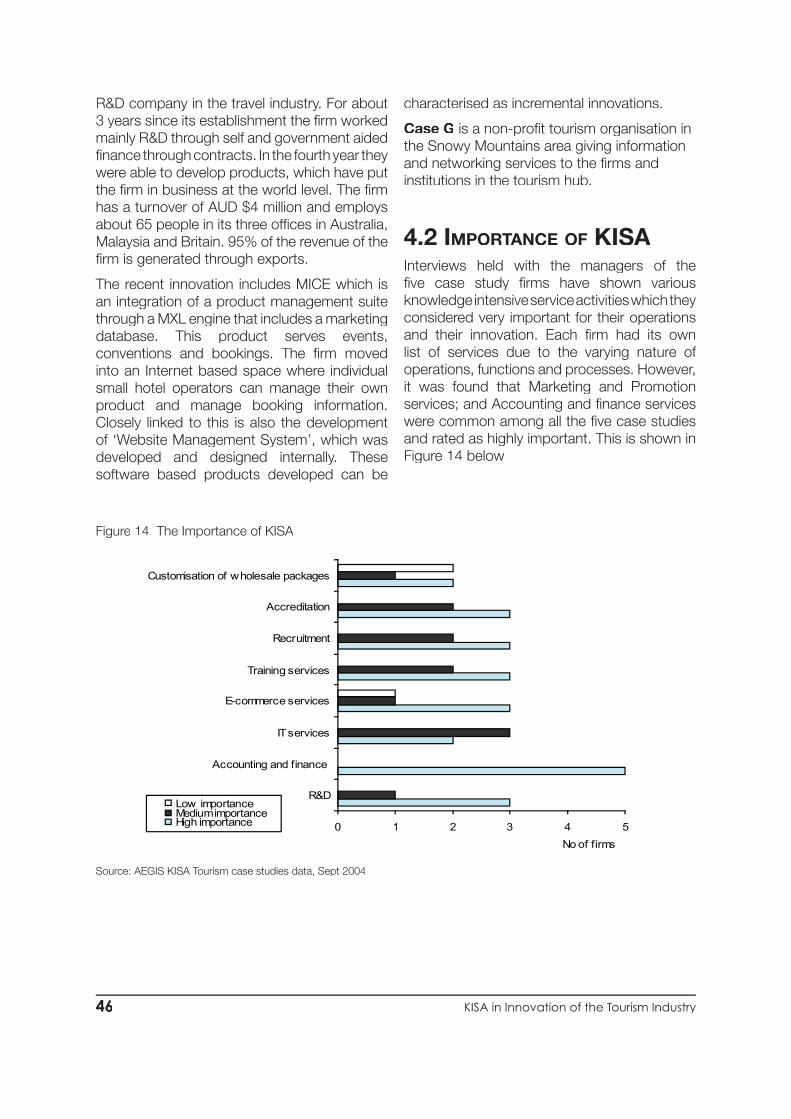

The six case studies interviewed depicted various knowledge intensive service activities they considered very important for their operations and their innovation. Marketing and promotion services, accounting and fi nance services were common among all the fi ve case studies and rated as highly important.

During the creation phase of a product, the main KISAs involved were industry development advice, the marketing and promotion, research and development, accounting and fi nance services and recruitment. The maturing phase involved business planning advice, IT services, e-commerce services and the customisation of wholesale packages. The standardisation phase involved marketing and promotion, accounting and fi nance services, training services, recruitment and accreditation. In relation to the fi rm life-cycle, the most used KISAs in the start up phase were industry development advice, business planning advice, R&D, recruitment and accreditation. At the entrepreneurial stage, the period after the initial 3 years have been survived, there was more emphasis on marketing and promoting their products, services and the business. At the professional management stage of the business life cycle, the main KISAs used were research and development, accounting and fi nance services, IT and E-commerce services. Firms in expansion tended to focus more on IT services, recruitment and the customisation of wholesale packages.

5AEGIS UWS

These cases show that external inputs to KISA contributes signifi cantly to the core competences of the fi rms in areas as critical as product development, process innovation, marketing innovation, the use of best practices and the awareness of opportunities conducting to grow. These fi rms show also a high specialisation of KISA inputs from their own employees. The value of these inputs was in the strong specialised knowledge of staff and their capacity to ‘customise’ it with innovative behaviour to the core operations of the company. This customization of knowledge includes the adaptation to particular regional characteristics and the pursuing of long-term relationships with customers.

In general it was found that, though based on a small sample, the case studies analysis supports the view that for success in innovation, market research is as important as institutional, organisational and marketing factors. Secondly, the in-house capabilities of fi rms (technical and non-technical) particularly the part played by managers of the fi rms (often being owners of small fi rms which dominated the survey sample) has come out as important factors for the generation of KISA and the innovation process. Thirdly, our case studies indicate the network space of ‘cluster based tourism destinations’ (such as Snowy Mountains and Gold Coast) playing an important part in catalysing the process of KISA in the tourism industry. Not withstanding the fi ndings of the survey results, the signifi cance of local, state and federal governments (tourism departments) is crucial to the development and in sustaining ‘cluster based tourism destinations’. Such network space and clusters are seen to provide an important source of KISA inputs for business development, marketing, and tourism related learning from others.

Emergent Policy Themes

• Government tourism departments have a role in raising the awareness of KISA and its impact on innovation through diffusion activities;

• As tourism activity is linked to geographic cluster-based destinations, cluster oriented policies and programs are important both for catalysing KISA and for strengthening the ‘destination innovation system’;

• Policies and programs are needed to increase the innovation capabilities of the professionals working in the tourism industry (specially in SMEs);

• Government programs are needed to target non-technical components of the industry such as Marketing;

• Policies and programs oriented to building networks, especially at the ‘destination’ level, would facilitate informal process of learning and building competences for innovation;

• There is a need for governments to collect statistics that better refl ect innovative KISA not usually collected in relation to innovation.

6 KISA in Innovation of the Tourism Industry

Table of contentsACKNOWLEDGEMENTS ...........................................................................................................................2EXECUTIVE SUMMARY ...........................................................................................................................EXECUTIVE SUMMARY ...........................................................................................................................EXECUTIVE SUMMARY 31. INTRODUCTION .................................................................................................................................8

1.1 Innovation and Importance of KISA .............................................................................1.1 Innovation and Importance of KISA .............................................................................1.1 Innovation and Importance of KISA 91.2 Knowledge-Intensive Service Activities (KISA) ............................................................121.3 The KISA Study .........................................................................................................141.4 Research Questions and Methods ............................................................................14 1.4.1 Survey and Case Studies .............................................................................14 1.4.2 Sample and Characteristics of Tourism fi rms ................................................15 1.4.3 Data Analysis ...............................................................................................18 1.4.4 Limitations of the study ................................................................................18

2. OVERVIEW OF THE TOURISM INDUSTRY ..............................................................................................RVIEW OF THE TOURISM INDUSTRY ..............................................................................................RVIEW OF THE TOURISM INDUSTRY 19

2.1 A statistical overview of Tourism ................................................................................19 2.1.1 Composition of the Industry .........................................................................20 2.1.2 The economic contribution of the Industry ....................................................21 2.1.3 Inputs to Tourism .........................................................................................22 2.1.4 Employment .................................................................................................23 2.1.5 Domestic Tourism ........................................................................................25 2.1.6 Tourism Exports ...........................................................................................25 2.1.7 Tourism Research and Development ............................................................37 2.1.8 Tourism in OECD countries ..........................................................................382.2 Government Policies and Programs for the Industry ..................................................302.3 Summary ..................................................................................................................32

3. SURVEY OF TOURISM FIRMS: KEY FINDINGS .......................................................................................33

3.1 Innovation and the Use of KISA .................................................................................333.2 Provision of inputs to KISA ........................................................................................473.3 Access to Government Grants ..................................................................................423.4 Summary of Findings ................................................................................................43

4. CASE STUDIES: KEY FINDINGS .........................................................................................................44

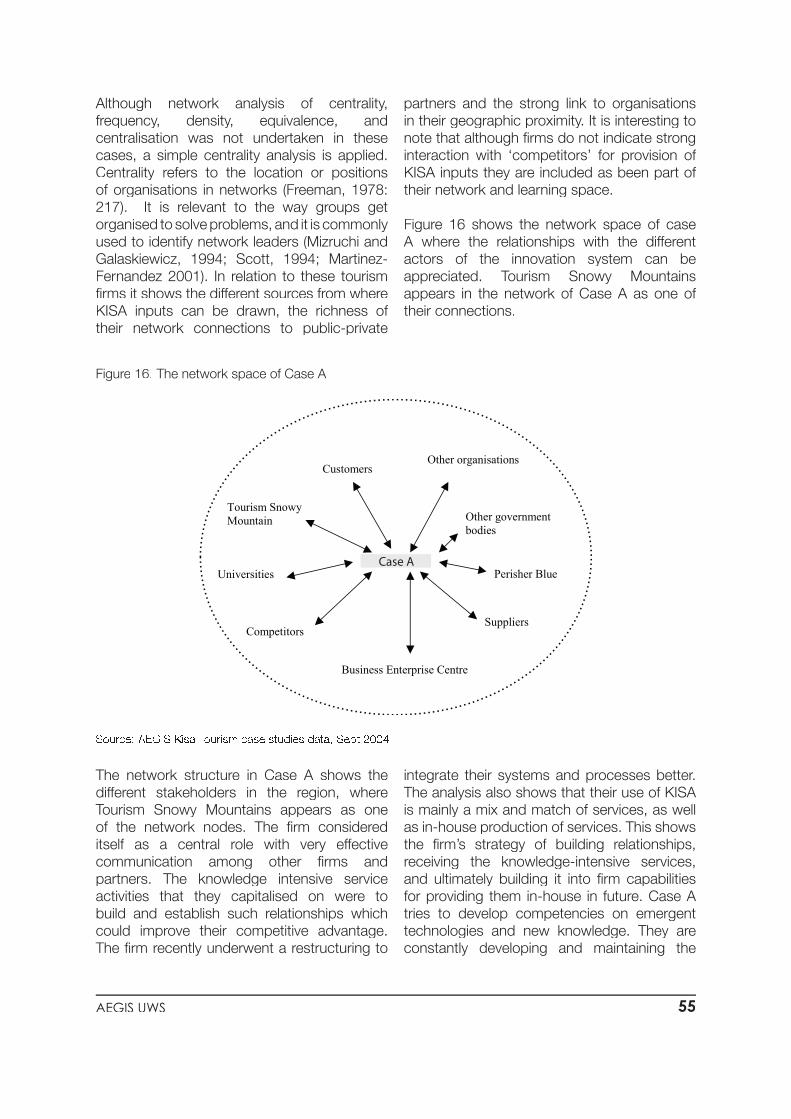

4.1 Background to the cases ..........................................................................................444.2 Importance of KISA ...................................................................................................46 4.2.1 Sources of inputs to KISA ............................................................................47 4.2.2 KISA in the product life cycle ........................................................................50 4.2.3 KISA in the business life cycle ......................................................................51 4.2.4 Network KISA ..............................................................................................524.3. Rationale for the use of KISA ....................................................................................59 4.3.1 Strategy for using externally produced inputs to KISA ..................................59 4.3.2 Strategy for using internally produced inputs to KISA ...................................614.4 KISA and fi rm capabilities ..........................................................................................62 4.4.1 External inputs to KISA and fi rm capabilities .................................................62 4.4.2 In-house KISA and fi rm capabilities ..............................................................63 4.4.3 KISA mix and match process: the integration of internal and external KISA ..644.5 Challenges to the innovation process ........................................................................654.6 Access to Government Programs .............................................................................664.7. Summary of fi ndings ................................................................................................67

5. CONCLUSIONS ................................................................................................................................69

5.1 KISA in the innovation process of Tourism Firms .......................................................695.2 Emergent policy themes ............................................................................................70

REFERENCES .....................................................................................................................................71APPENDIX A: CASE STUDY SUMMARIES ..................................................................................................74

7AEGIS UWS

LIST OF TABLES

Table 1: Educational qualifi cations (survey sample) ..........................................................................16Table 2: Business structure .............................................................................................................16Table 3: Profi le of case studies ........................................................................................................18Table 4 Number of businesses in the Tourism Industry in Australia ..................................................20Table 5 Number of management units by employment size for Tourism ..........................................20Table 6 Share of Tourism GDP (percent) ..........................................................................................21Table 7 Consumption of Domestically and Overseas Produced Tourism Goods and Services. 2002-03 (millions) ...............................................................................................................21Table 8 Tourism Industry Share of Total Gross Value Added (Percent) .............................................22Table 9 Short Term Arrivals and Departures (million) ........................................................................22Table 10 Inputs to the Tourism Industry. 2000-01 (Percent) .............................................................22Ta ble 11 Employed Persons in Tourism per Industry. 2002-03 .......................................................23Table 12 Occupational Structure of Total Employment and Tourist Industry. Australia. August 2003 .........................................................................................................................24Table 13 Proportion of Employment in ASCO Major Groups ...........................................................25Table 14: Exports of Tourism Goods and Services ..........................................................................26Table 15: Arrivals (1993-2012) ........................................................................................................27Table 16 Comparison with other OECD countries ...........................................................................28Table 17: Direct Tourism Related Spending (AUD $ million) by the Australian Government ..............31Table 18: Firms with Tourism Awards and radical innovation ...........................................................34Table 19: Use of KISA-related services ...........................................................................................34Table 20: Frequent use of KISA-related services by fi rm business cycle ..........................................35Table 21: Use of KISA-related services ...........................................................................................36Table 22: Expenditure on KIS by Tourism Award winners ................................................................37Table 23: >AU$50,000 Expenditure on KIS and size of the fi rm .......................................................37Table 24: Provision of KISA-related services ....................................................................................38Table 25: KISA mix of inputs ...........................................................................................................39Table 26: Importance of providers of inputs to KISA ........................................................................40Table 27: Preferred location for provision of KISA-related services ..................................................41Table 28: Tourism Awards and use of government grants ...............................................................42Table 29: Sources of knowledge-intensive service activities inputs in Australian tourism fi rms .........48Table 30 Frequency of knowledge/services provision ......................................................................49Table 31 KISAs mapped against product life cycle ..........................................................................50Table 32 KISAs mapped against fi rm life cycle ................................................................................51Table 33 Collaboration with partners ...............................................................................................58

LIST OF FIGURES

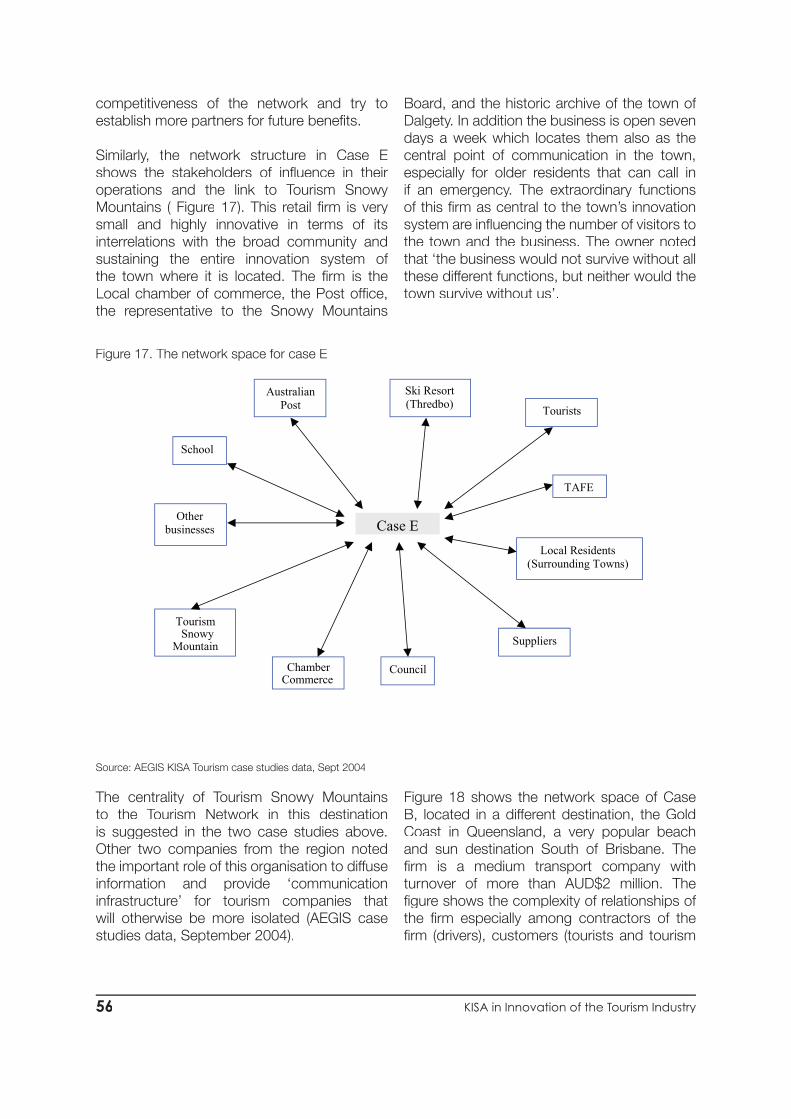

Figure 1: The Learning Space of Firm and Vectors in the C0-production of knowledge...................13Figure 2: Firm Size (survey sample) .................................................................................................15Figure 3: Years in operation ............................................................................................................16Figure 4: Average turnover ..............................................................................................................17Figure 5 Domestic Visitor Nights 2000-2012 ...................................................................................25Figure 6: International visitor arrivals December 1991–July 2003 .....................................................26Figure 7 International tourism: past and projected inbound tourism by region .................................29Figure 8 OECD International Tourism: Gross departure rate, trips per inhabitant ..............................30Figure 9: Change to products/services ...........................................................................................33Figure 10: Firm expenditure on KISA-related services .....................................................................36Figure 11: Provision of Services ......................................................................................................39Figure 12: Location of KISA-related providers .................................................................................41Figure 13: Inputs to KISA fi nanced by Government grants ..............................................................42Figure 14 The Importance of KISA ..................................................................................................46Figure 15: Snowy Mountains Tourism Development Network ..........................................................54Figure 16 The network space of Case A .........................................................................................55Figure 17 The network space of Case E .........................................................................................56Figure 18 The network space of Case B .........................................................................................57Figure 19 Challenges to the innovation process ..............................................................................65

8 KISA in Innovation of the Tourism Industry

Innovation is on the policy agenda in all OECD countries after two decades of research by the OECD itself and by researchers in many fi elds. In Australia the last few years have seen much increased government awareness of the major role in economic development played by innovation and the fi rms that carry it out. This awareness has been realised through the introduction of policies crossing many aspects of the innovative process and all sectors. Recognising that innovation is the key to sustained economic growth, governments in Australia now spend important amounts of money on a diverse range of innovation programs.

The international research-based literature clearly indicates the multiple dimensions of innovation and innovative activity by fi rms. From an initial focus on product innovation alone, understanding is now widespread that innovation encompasses not only radical and incremental product development but also new production methods and new organisational forms taken up by productive enterprises. It has become clear that all these aspects of change characterise innovative fi rms and infl uence competitive success.

It has also become clear that innovation, defi ned as novel activities of economic value to an enterprise, is a highly complex phenomenon and occurs differently in different industries, in relation to different products, in fi rms of different ages and size and at different stages of an industry or product cycle. Researchers in many countries have investigated most aspects of the innovation process and the operations of‘typical’ innovative fi rms but still there remain many areas where the processes involved and the ways in which fi rms go about changing their products, processes, markets, organisational shape and skill levels are still not

well understood. In the knowledge based ‘new economies’, a range of knowledge intensive service activities carried out by fi rms and aided by appropriate government policies that enable these fi rms to develop knowledge based capabilities and skills are seen as important as R&D itself in the overall success of innovation processes. It now seems likely that the mixed success of some policies designed to assist enterprises, especially small and medium fi rms, undertaking innovative activities results from both lack of clarity in understanding the processes and recognition of the impact on policy uptake of the factors mentioned above. In particular, it may be that many policies are designed with too little understanding of exactly how businesses using the programs offered mix and match knowledge-intensive services provided by public and private sources of expertise and assistance. In addition, limited understanding of the ways in which products and other innovative activities are developed in different industries often means that programs are insuffi ciently focused on the needs of particular client fi rms and industries.

The present report is an element of a broader project which aims to improve understanding of how fi rms use innovation services in different industries. The project is rooted in work AEGIS has been undertaking as part of an 9 countryOECD research project1 that will ultimately provide analysis of innovation-related policies or programs relating to specifi c industries and data on how fi rms in selected industries in the different countries use public programs and private sector sources of expertise available to them. The aim here is to provide policy makers with analytical and empirical insights to underpin the design and implementation of more effective industrial development strategies.

1. INTRODUCTION3. INTRODUCTION3. INTRODUCTION

9AEGIS UWS

KISA are defi ned as the production and integration of service activities (technical and non-technical) undertaken by fi rms in manufacturing or service sectors, in combination with manufactured outputs or as stand-alone services (OECD, 2003:2). KISA can be provided by private enterprises or public sector organisations. Typical examples include: Research and Development (R&D) services, management consulting, Information Technology (IT) services, human resource management services, legal services such as Intellectual Property (IP)-related issues, accounting, fi nancing, and marketing services.

The project has three main areas of research for government assistance in Australia’s innovation system. These are:

• Better understanding of how fi rms interact with external providers of innovation services in order to develop innovation capability;

• Better understanding of how fi rms mix and match their use of services at different ‘stages’ of their innovation project(s);

• Better understanding of both the ways in which and the reasons why such mixing and matching varies according to the sector where the fi rm operates.

Specifi cally, the study will investigate KISA in the Australian tourism industry to better identify its features, which are critical to innovation in Australian companies. The study of KISA is a sophistication of the defi nition of knowledge intensive services in the literature (Miles, 2003), as it focuses on the complexity of how and why knowledge-intensive services are sought and acquired in interaction with formal and informal knowledge providers.

1.1 INNOVATION AND IMPORTANCE OF KISARecent research on innovation undertaken by the OECD and EU suggests that there are three principal ‘lenses’ useful for analysing innovative activities in a nation. In summary, these ‘lenses’ focus attention on understanding particular patterns of innovative activity seen in an economy as a function of the characteristics of the major players (institutions and organisations public and private), and the ways in which these link public and private sectors together. The players may link in different ways at different spatial levels (national, regional or local), through activities such as R&D provided through public or private enterprises, through the development and use of management and other business-related skills and expertise – seen in the rise of knowledge-intensive business service fi rms (KIBS) who provide skills and expertise to other players in the system – or they may link through their entrepreneurial activities as suppliers and customers.

Recent decades have seen a vast amount of investigative work, both theoretical and empirical, on the different aspects of the study of players and their interactions. Many studies have developed understanding of the systemicnature of innovation and the importance of all elements of a nation’s innovation system – legal, scientifi c, training, business programs, for example – working well together. Much of the more recent work is summarised in OECD 1999, 2000, 2001a. (See also Edquist, 1997). The focus on national systems of innovation was national systems of innovation was nationalsubsequently complemented by recognition of the similar importance of regional and local innovation systems (eg Cooke, 2001). Work also progressed on sectoral or technological systems of innovation in specifi c industrial fi elds (Malerba, 2002; Marceau et al., 2001 and Marceau and Martinez, 2002) and more recently on the need to integrate the spatial elements of these systems (OECD, 2001b). There has also been important work on the

10 KISA in Innovation of the Tourism Industry

growth of the services sector and the separate systems of innovation operating there (see eg. Anderson et al., 2000; Howells, 1999; Metcalfe and Miles, 2000) and on linkages between manufacturing and services in fi rms’ competitive strategies (Marceau et al., 2001). Very recent work is bringing together theories about fi rms, institutions and organisations to provide a ‘systemic’ theory of innovation at fi rm level (Coriat and Weinstein, 2002).

Over the same period, the shift towards the ‘knowledge economy’ has seen the creation of KIBS as important private sector players in the innovation game (see eg. Miles et al., 1994; Gallouj and Weinstein, 1997. See also Muller, 2001 for interactions between KIBS and SMEs and Muller and Zenker, 2001) while public organisations, notably universities, have been encouraged to make their expertise widely available to business and community. The production and diffusion of knowledge via KIBS fi rms has become central to innovation systems in these countries. KIBS typically include legal and accounting but also, and more relevantly here, design and computer-related services, R&D consultancy, recruitment of skilled personnel, environmental services and technical and training services (Windrum and Tomlinson, 1999:393). KIBS play a twofold role in a country’s innovation system – as providers of knowledge services to other fi rms and as a means of introducing internal innovations (internal consultancy).

Private sector experts, however, are not the only players in innovation. On the one hand, innovation expertise is also provided to fi rms by public sector research organisations and, on the other hand, by a range of government programs aimed at encouraging innovation in the private sector. Driving fi rms and organisations towards packing an ever greater innovation punch through the use of the science and technology system and related policy instruments has become a major aim of government in Australia (see, for example, the series of measures gathered into ‘Backing Australia’s Ability’ 2001), as elsewhere in the OECD (OECD, 2002a).

In contrast to the wealth of understanding about what knowledge-intensive public and private organisations can do, as indicated above, two aspects of the national innovation effort remain understudied. The fi rst concerns the factors that trigger enterprises to decide on innovation per se. The second concerns how fi rms use the variety of sources of expertise available to innovating fi rms and companies and how they choose among several providers of similar services and seek different sources of assistance at different times and for different innovation project purposes. Nonaka and his colleagues, for example, have shown that innovating fi rms indeed draw on a range of providers of expertise (1995). Services available and used include R&D, testing, prototyping and other technical and engineering services, ICT, legal (especially IP-related), fi nancial, marketing and training.

However critical questions remain about how, when or why fi rms choose to use why fi rms choose to use why particular different kinds of government and publicly and privately provided innovation programs or services among the variety available, why they choose x and not y or x and y but not z, or how and why these choices vary according to whether the innovation concerned is radical or incremental. Even less is known about how fi rms transform the innovation services they receive from outside to build capability and hence permit sustained innovation at fi rm level. As a result, innovation-related policies are still poorly targeted and often less effective than had been thought.

One of the most important aspects of the latest phase of international work on innovation at fi rm level has begun focusing on fi rms’ development and use of the different sources of expertise available to them. Thus, for example, two projects funded by the European Union in recent years have focused on innovation in services and services for innovation. The fi rst of these, the IS4S project, focused on innovation in service industries and specifi cally the development of services to support innovation by others. The second, the RISE project, focused on mapping the transformation of

11AEGIS UWS

Research and Technology Organisations (RTOs) as they began to reach out more to private sector clients and to depend more on private sources of income (see Hales, 2001). The RISE project also began the investigation of how fi rms engage with external providers of innovation services, both public and private, at different stages of the innovation process and in different clusters (Hales, 2001; Hauknes, 2000; Preissl, 2001). In Australia, Marceau and Hyland, through their ARC Large Grant project, ARISE, are currently seeking to elucidate the shifting landscape of RTOs, with a particular focus on the public-private hybridisation of major scientifi c organisations, including universities.

Taken together these studies have shed considerable analytical light on many aspects of the fi eld. The fi rst results of the ARISE project, for example, have suggested strongly that three foci of research are now needed if government assistance for innovation in Australia is to be maximally effective. These are:

• better understanding of how fi rms interact with external providers of innovation services in order to develop innovation capability.

• better understanding of how fi rms mix and match their use of services at different ‘stages’ of their innovation project(s);

• better understanding of both the ways in which and the reasons why such mixing and matching varies according to the sector of principal activity of the fi rm.

The ARISE results thus suggest that what is missing now from innovation analysis is how fi rms seeking to innovate mix and match their use of publicly provided assistance programs and private sources of expertise including their own in order to transform different kinds of knowledge inputs into sustained innovation.

The Knowledge-Intensive-Service Activities (KISA) project, of which this report is a part, addresses precisely this issue. The study is

composed of several levels of analysis which provide the context for a fi rm-level analysis of innovation knowledge-seeking choices. The project involves detailed statistical description of the size and ‘shape’ of the industrial sectors selected for study and presentation of the policies available for fi rms in those sectors to use for innovation assistance. These two elements form the background for the empirical study of innovation at fi rm level. The results of this analysis for the tourism industry is presented in this report. The report also presents key fi ndings from an empirical study of tourism fi rms in Australia intended to show the choices among providers of innovation expertise made by fi rms in the tourism industry, to gain insights into the reasons for the choices made and to indicate how fi rms mix and match the knowledge-intensive services used.

12 KISA in Innovation of the Tourism Industry

1.2 KNOWLEDGE-INTENSIVE SERVICE ACTIVITIES (KISA)KISA are the knowledge-intensive service activities that fi rms undertake in conjunction with external or internal experts to build capability in the multiple areas needed for sustained innovative activity. A range of knowledge intensive service activities can be identifi ed as management and business service activities; consultancy services; legal; intellectual property and accounting services; recruitment and training activities; technology services such as IT; marketing services; research and development activities etc. There are generic KISA, such as those generated by software fi rms or engineering consultancy fi rms, for instance, and specifi c KISA which are sector or industry specifi c. The experts concerned may be from public or private sector or research organisations or they may have been developed inside innovating fi rms as part of a strategic package of actions designed to build long-term innovative capabilities. The ‘KISA’ project therefore focuses from a fi rm level view on how such expertise is accessed, adapted, incorporated, refi ned, added to and transformed into innovative products, processes and organisational forms and the innovation capability needed for the future. It is hoped that the analysis of what fi rms do in different industries will then enable us to connect to other work so as to build up industry (‘meso’) level analysis. It is this fi rm and then industry-level focus that distinguishes the KISA project from work on KIBS and innovation in service industries themselves and from most existing literature.

The particular and distinctive ways fi rms access, acquire, produce and integrate knowledge are the ‘KISA’ fi rms undertake in their learning and innovation processes. Learning processes can be internal and external to the fi rm as an outcome of engagement activities inside the fi rm or with external organisations. This engagement is produced through the acquisition of knowledge intensive services to internal

or external providers. The external providers are usually Knowledge Intensive Business Services (KIBS) but, increasingly, Research and Technology Organisations (RTOs) compete with KIBS as a result of changes in funding systems (Hales, 2001). Other important providers of expertise are competitors, customers and other organisations from the same or different industry sector and part of the network of fi rm. Inputs to KISA can come through networks and clusters via informal cooperation agreements.

The importance of the role of KIBS and RTOs might have been overestimated in the existing literature when we look in detail at how fi rms operate today within their learning space, especially in terms of their use of informal transactions for the co-production of knowledge. Figure 1 below illustrates the learning space of the software fi rm and the role of the three ‘vectors’ of knowledge providing inputs to KISA: KIBS, RTOs and other organisations in the network space of the fi rm. The fi gure also shows where KISA are taking place in the fi rm and in which way, i.e. as formal transactions (eg contractual) or informal (eg sharing information) or as internal to the fi rm. The arrows in the fi gure indicate the engagement function of KISA and its dependence on interaction for the co-production of knowledge.

13AEGIS UWS

The activities that provide for the integration of KISA are important to building and maintaining a fi rm’s innovation capability. For example, a fi rms sourcing providers in the marketplace to ensure that they get the optimum service. The fi rm engages in activities for sourcing, evaluating between service providers, assessing the services offered, the price, quality, and packages available. In this process the fi rm learns about the marketplace and acquires additional competences. Upon receipt of the service, there is further enhancement value to the fi rm as a result of the integration of the new service. Therefore the new service has added functionality and competence as well as providing new knowledge and learning abilities to the fi rm from the service provider’s input. The process of the fi rm sourcing, obtaining, mixing knowledge-intensive services are the activities accompanying the innovation process. This

innovation process is positively affected in both sides of the interaction: the fi rm and the provider of services (Muller & Zenker, 2001).

KISA can vary according to the fi rm’s own capabilities and innovation processes, the ‘process of engagement’ of the fi rm with external providers and the internal provision of knowledge intensive activities. Thus, KISA can be different in each fi rm and the activities that are more effective may indeed be the ones that differentiate a fi rm from its competitors. For example, company X, a manufacturing company focusing on advance metal products, might require the latest technology and know-how in the application of cutting-edge machinery to maintain its position in the market. This particular activity will require a combination of expert services sourced externally and undertaken internally by the fi rm.

KIBS RTOs*

NETWORK

Formal KISA

Informal KISA**

Customers / Suppliers Other firms / Organisations

Community

Internal KISA ������

*RTOs-Research and Technology Organisations. Includes Government Departments that provides services

such as research and development to fi rms/organisations.

KIBS-Knowledge Intensive Business Services.

**Although informal KISA can happen at any level they are more likely to appear while interacting with other

fi rms/organisations of the network space of the software fi rm.

Figure 1. The learning space of the Firm and vectors in the co-production of knowledge

14 KISA in Innovation of the Tourism Industry

Understanding these innovation-related knowledge-intensive service activities – KISA – is important for governments because it relates directly to a set of issues which lie at the heart of policymakers’ attempts to use public policy instruments to promote sustained innovation in all areas of the economy. KISA is also important for organisations providing innovation services so that a better understanding of how their services work in practice, what areas needs to be improved in the range of service provision and the ways in which their services may be accessed and used.

1.3 THE KISA STUDY

The Australian KISA study focuses on three industries – software, mining technology services and tourism. The industries selected provide a contrast in scale and spread. The fi rms in each sector are mostly small, providing information on the constraints on policy services uptake faced by SMEs.

Tourism was selected for the increasing relevance of this industry to the Australian economy. It is also a complex industry with inputs from many other industries and has not been studied in depth. There is a consequent lack of KISA-related literature.

1.4 RESEARCH QUESTIONS AND METHODS

The research questions refer to the analysis of the role of KISA in fi rm innovation processes:

• What does KISA mean?• What KISA are used by tourism fi rms?• When are KISA used?• Why is KISA used?• How does KISA relate to fi rms

capabilities? • Who provides inputs for KISA?• How are the different inputs to KISA

mixed and matched by the fi rm?• What are the policy implications of the

role of KISA in innovation?

The study of the Tourism industry is carried out in three steps. Firstly a review of recent literature and statistical analysis of the signifi cance of the sector; then a survey of tourism fi rms and fi nally case studies to better understand the role of KISA in tourism fi rms. The study has found that there is very limited KISA-related literature in the tourism industry and that surveys and in-depth company investigation will help to understand how fi rms access, use and integrate different sources of expertise (internal and external) to build their innovation capability. A statistical analysis of the tourism industry informs on its signifi cance and frames the target sample of companies to be used for the survey of fi rms and the selection of case studies.

1.4.1 Survey and Case StudiesThe survey targeted tourism business units. The themes investigated are, the use and importance of KISA in such fi rms and the access to government grants. The survey was conducted using the Australian Tourism Data Warehouse, a public website7 joint initiative of all states and territories that provides details of 13,000 companies. The sample of fi rms was extracted from the categories of ‘accommodation’, ‘transport’ and ‘tour operators’8. Companies were randomly contacted by phone from a sample of 137 companies across all Australian states. The survey of fi rms also included the 2003 Australian wide Tourism award winners fi rms. The survey was open for three weeks. A total of 44 responses were collected and analysed; 45.5 percent of responses were returned by fax, 25 percent by email, 18.2 percent by mail and 11.3 percent were collected over the phone. The survey instrument is found at Appendix A.

The survey questionnaire included questions concerning:

• Background data on fi rms such as size, turnover, business life-cycle;

• Information on innovation and the use of KISA related services;

• Importance of providers of inputs to KISA;• Use of government grants to fi nance

KISA-related services.

15AEGIS UWS

Six fi rms were further analysed in-depth covering the activities (KISA) undertaken by the fi rm – internal/ external – over the course of the decisions to seek, receive and integrate KISA inputs of different kinds, from different sources of expertise and at different stages of the product cycle and life-cycle of the fi rm. The aim of the case studies is to understand the nature of KISA and the complex web of factors affecting the co-production of knowledge within the tourism fi rm. The case studies extracted the ‘why’ questions to complement the survey i.e., why do the fi rms undertake certain activities, at certain times and from certain sources. Four fi rms were part of the ‘Snowy Mountains’ tourism hub and an interview was also conducted with the regional tourism organisation. One fi rm was from the Gold Coast. One fi rm specialised in corporate and government applications and R&D for the travel industry. Case studies summaries are found at Appendix A.

The selection of the six tourism fi rms for the case studies is based on several parameters which are identifi ed as:

• Market focus• Size• Ownership• Annual Turnover• Phase of Company Life Cycle• Innovation/Industry awards received• State location• Innovation Processes• Destination

The case studies discussion themes refer to:

• Background of the fi rm- Customers- Most recent innovation- Network KISA

• Importance and use of KISA- KISA within the fi rm

• Access and interaction with external providers- External inputs to KISA- Public inputs to KISA

• Integration of external and internal inputs to KISA- Integration of expertise- Knowledge management and KISA- KISA and innovation capabilities

• Challenges to the innovation process• Business Models and competitiveness

1.4.2 Sample and Characteristics of Tourism fi rmsThe sample frame consists of 137 fi rms. Forty-four fi rms participated in the survey. The 44 fi rms comprised of 24 tour fi rms (55%), 3 transport fi rms (7%), 15 accommodation fi rms (34%) and 2 retail fi rms (4.5%). Seven fi rms (16%) received National tourism awards in 2003. Surveyed fi rms were located at every state of Australia.

The average number of employees per fi rm in the sample was fi fty. Twenty-fi ve of 44 fi rms (57%) had between 1 and 6 employees. There was one employer with 1,200 employees (Figure 2).

12001306552362920119531

8

6

4

2

0

Number of firm employees

Number of employees

Num

ber o

f firm

s

Figure 2. Firm size (surveyed sample)

Source: AEGIS KISA Tourism survey (2004)

16 KISA in Innovation of the Tourism Industry

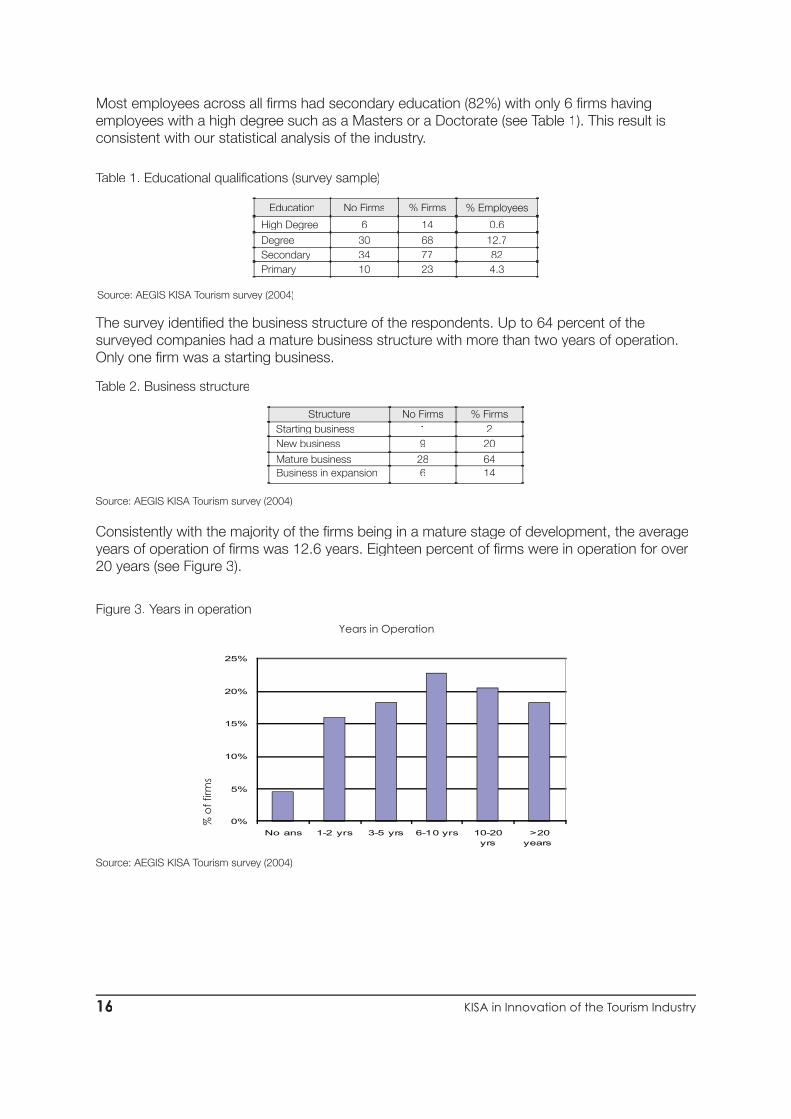

Most employees across all fi rms had secondary education (82%) with only 6 fi rms having employees with a high degree such as a Masters or a Doctorate (see Table 1). This result is consistent with our statistical analysis of the industry.

The survey identifi ed the business structure of the respondents. Up to 64 percent of the surveyed companies had a mature business structure with more than two years of operation. Only one fi rm was a starting business.

Consistently with the majority of the fi rms being in a mature stage of development, the average years of operation of fi rms was 12.6 years. Eighteen percent of fi rms were in operation for over 20 years (see Figure 3).

Figure 3. Years in operation

Source: AEGIS KISA Tourism survey (2004)

Table 1. Educational qualifi cations (survey sample)

Education No Firms % Firms % Employees

High Degree 6 14 0.6Degree 30 68 12.7Secondary 34 77 82Primary 10 23 4.3

Table 2. Business structure

Structure No Firms % FirmsStarting business 1 2New business 9 20Mature business 28 64Business in expansion 6 14

0%

5%

10%

15%

20%

25%

No ans 1-2 yrs 3-5 yrs 6-10 yrs 10-20yrs

>20years

% o

f firm

s

Years

Years in Operation

Source: AEGIS KISA Tourism survey (2004)

Source: AEGIS KISA Tourism survey (2004)

17AEGIS UWS

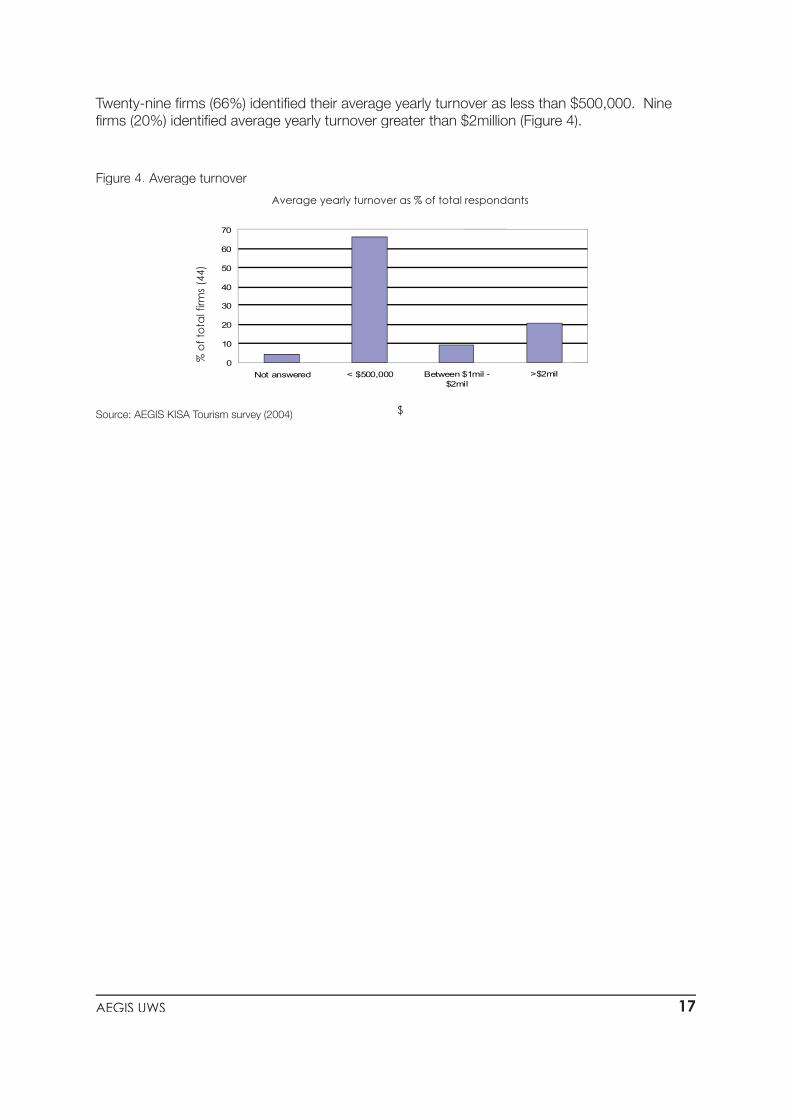

Twenty-nine fi rms (66%) identifi ed their average yearly turnover as less than $500,000. Nine fi rms (20%) identifi ed average yearly turnover greater than $2million (Figure 4).

Figure 4. Average turnover

Source: AEGIS KISA Tourism survey (2004)

0

10

20

30

40

50

60

70

Not answered < $500,000 Between $1mil -$2mil

>$2mil

Average yearly turnover as % of total respondants

$

% o

f tot

al fi

rms (

44)

18 KISA in Innovation of the Tourism Industry

1.4.4 Limitations of the studyThere are certain limitations to the analysis presented in this report. First, the number of respondents to the survey was not a statistically representative sample of the Australian Tourism Industry, so no claims can be made in regards to the representation of the whole industry. Second, the number of case studies was very small so it is not possible to draw conclusions about innovation across the Tourism industry as a whole. Nevertheless the analysis of the fi rms participating in the study contributes to an understanding of the role of KISA in Australian tourism fi rms.

This report gives an overview of the tourism industry in Australia, and then presents empirical results on the role of KISA from surveys and case studies.

1.4.3 Data AnalysisThe study relied on both quantitative and qualitative techniques of data collection and analysis. The survey conducted through a structured questionnaire involved simple statistical analysis9 of tabulating responses to various questions on KISA in percentages so descriptive statistics were applied. The case studies provided a more detail qualitative analysis of the KISA process. Case studies were recorded and transcripts generated for

writing the case studies and for presenting the results.

The case studies ranged from small family-owned businesses to large corporations. The table below summarises the profi le of these fi rms. The majority of the cases were medium and large companies with more than 15 years in operation and more than AUD$100,000 of yearly turnover.

Table 3. Profi le of case studies (fi rms)

Case Life cycle phase Annual turnover

Market Focus

Main products/services State Recent

InnovationInnovationprocessprocessprocess

Micro businesses (4 or less persons)

E Entrepreneurial (5 years)(5 years) < $100,000 Domestic Hospitality and

horticulture NSW incremental Small group improvementsimprovements

Small businesses (5 to 19 persons)

A Expansion (27 years) < $100,000 Domestic Ski school & ski

retail NSW incremental Small group improvements

Medium and large companies (20 or more persons)

B Expansion (29 years)(29 years)

$100,000 - $1mil$1mil International Transportation QLD radical External R&D

C Expansion (15 years)(15 years) >$1 mil International Accommodation NSW radical External R&D

DProfessional management (48 years)

>$1 mil Domestic Tourism resort NSW Incremental and radical External R&D

FProfessional management (9 years)

>$4 mil International Corporate applications NSW Incremental

Small group improvements (with CEO)

Source: AEGIS KISA Tourism case studies data, Sept 2004

19AEGIS UWS

2.1 A Statistical Overview of Tourism

The international system for defi ning and classifying industries and the local equivalent, the Australian and New Zealand Standard Industrial Classifi cation (ANZSIC) do not recognise tourism as a discrete ‘industry’ because ‘industries are classifi ed according to the goods and services they produce, whereas tourism depends on the status of the consumer’ (ABS 2004: 3). For the purpose of separating the consumption of tourists from non-tourists ‘tourism’ is defi ned as ‘activities ‘activities ‘of persons traveling to and staying in places outside their usual environment for not more than one consecutive year for leisure, business and other purposes not related to the exercise of an activity remunerated from within the place visited’ (ABS 2004: 48). This is adapted from the World Tourism Organisation (WTO) defi nition of Tourism10.

To provide data on the economic contribution of tourist activity to the economy, the Australian Bureau of Statistics applies a classifi cation system to identify the industries supplying inputs to tourist activities and how these inputs are consumed (OECD 2000). Each year since 1997-1978 to 2002-2003 data on the tourism industry has been presented in ‘satellite accounts’ to the standard national accounts. In the ABS, Australian National Accounts, tourism is defi ned according to these international standards to include visitors ‘whose primary purpose is private or government businesses, as well as more familiar tourism for leisure purposes’ (ABS, 2003a). It is therefore not only restricted to leisure activity, but also includes travel for business and other reasons, for example education. If the person stays longer than one year at a place, they are no longer regarded as a tourist.

2. Overview of the Tourism Industry

20 KISA in Innovation of the Tourism Industry

2.1.1 Composition of the Industry

Table 4 and Table 5 depict the nature of types of businesses in the tourism industry in Australia.

Table 4 above shows that there were 353,473 tourism related businesses in 1998; of these, 60,054 businesses were classifi ed as tourism characteristic and 293,419 businesses were tourism connected. They formed about 34 percent of total businesses in Australia.

Table 4. Number of businesses in the Tourism Industry in Australia

ANZSIC IndustryNo of

businessesbusinessesTotal

businessesbusinessesTourism characteristic industriesTravel agency and tour operator servicesTaxi transportAir and Water transportMotor vehicle hiringAccommodationCafes and restaurantsTakeaway food retailingTotal

5 3462 4722 168

9909 158

21 49318 427

60 054

ANZSIC IndustryNo of

businessesTotal

businessesTourism connected industriesClubs, pubs, taverns and barsOther road transportRail transportFood and beverage manufacturingTransport equipment and other manufacturingAutomotive fuel retailingOther retail tradeCasinos and other gambling servicesLibraries, museums and artsOther entertainment servicesEducationOwnership of dwellingsTotal

10 01827 8831 8065 061

58 3128 010

132 1562 7095 715

15 47422 4103 865

293 419Total tourism related businesses 353 473

Source: Australian Bureau of Statistics, 1998, ABS Business Register (unpublished data)

Table 5. Number of management units by employment size for Tourism

ANZSIC industryMicro

businesses11Small

businesses12Medium to large businesses13

Total businesses

Travel agency and tour operator services 3 100 848 123 4 071

Taxi transport 1 946 397 55 2 398Air and water transportAir and water transport 1 183 393 123 1 699Motor vehicle hiringMotor vehicle hiring 516 175 19 707Accommodation 4 429 2 610 701 7 740Cafes and restaurants 9 475 8 678 1 272 19 425Takeaway food retailingTakeaway food retailing 10 877 4 608 733 16 218Total tourism characteristic 31 523 17 709 3 026 52 258Clubs, pubs, taverns and barsClubs, pubs, taverns and bars 3 113 4 462 1 884 9 459Other road transportOther road transport 21 376 3 841 688 25 905Rail transportRail transport 20 8 14 42Food and beverage manufacturingFood and beverage manufacturing 1 636 1 617 1 001 4 254Transport equipment and other manufacturingTransport equipment and other manufacturing 29 033 17 561 6 199 52 793Automotive fuel retailingAutomotive fuel retailing 3 402 3 147 294 6 843Other retail trade 85 113 34 894 3 999 124 006Casinos and other gambling servicesCasinos and other gambling services 1 662 699 50 2 411Libraries, museums and artsLibraries, museums and arts 3 032 616 206 3 854Other entertainment services 9 056 3 079 1 037 13 172Education 5 776 3 070 1 469 10 315Ownership of dwellingsOwnership of dwellings 3 131 243 53 3 427Total tourism connected 166 350 73 237 16 894 256 481Total tourism related 197 873 90 946 19 920 308 739

Source: Australian Bureau of Statistics 1999, ABS Business Register (unpublished data)

21AEGIS UWS

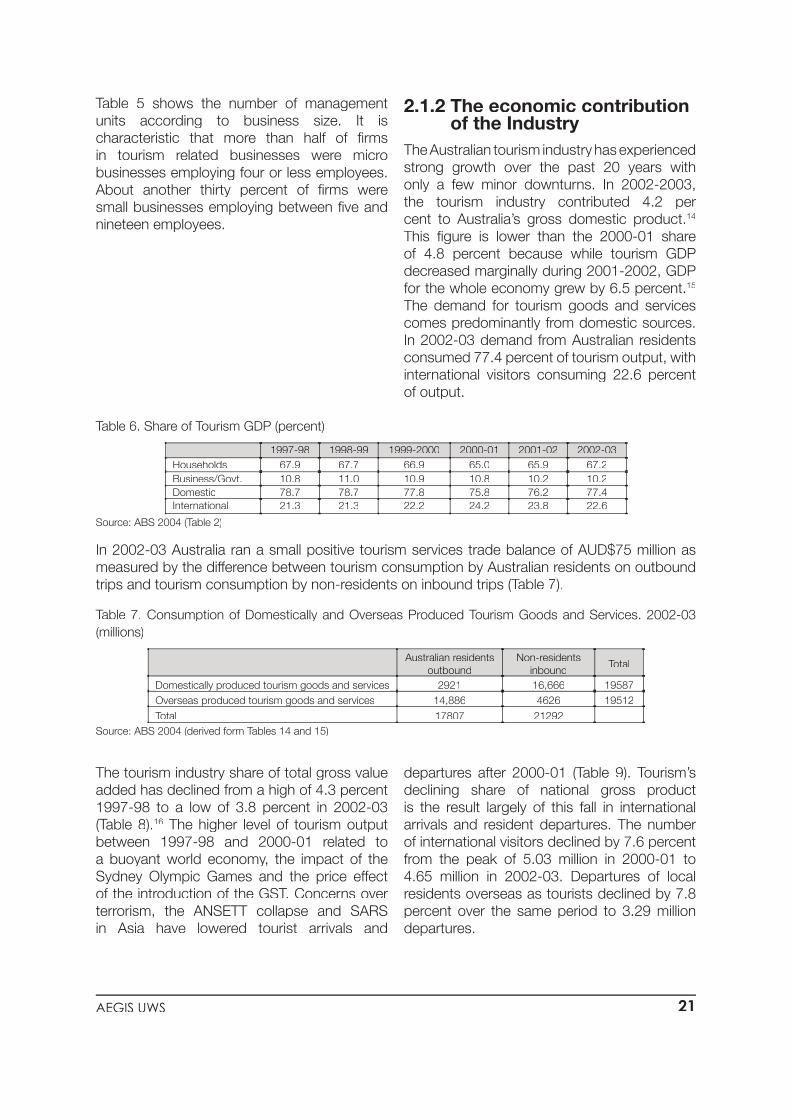

The tourism industry share of total gross value added has declined from a high of 4.3 percent 1997-98 to a low of 3.8 percent in 2002-03 (Table 8).16 The higher level of tourism output between 1997-98 and 2000-01 related to a buoyant world economy, the impact of the Sydney Olympic Games and the price effect of the introduction of the GST. Concerns over terrorism, the ANSETT collapse and SARS in Asia have lowered tourist arrivals and

departures after 2000-01 (Table 9). Tourism’s declining share of national gross product is the result largely of this fall in international arrivals and resident departures. The number of international visitors declined by 7.6 percent from the peak of 5.03 million in 2000-01 to 4.65 million in 2002-03. Departures of local residents overseas as tourists declined by 7.8 percent over the same period to 3.29 million departures.

Table 6. Share of Tourism GDP (percent)

1997-98 1998-99 1999-2000 2000-01 2001-02 2002-03Households 67.9 67.7 66.9 65.0 65.9 67.2Business/Govt. 10.8 11.0 10.9 10.8 10.2 10.2Domestic 78.7 78.7 77.8 75.8 76.2 77.4International 21.3 21.3 22.2 24.2 23.8 22.6

Source: ABS 2004 (Table 2)

Table 7. Consumption of Domestically and Overseas Produced Tourism Goods and Services. 2002-03 (millions)

Australian residents outbound

Non-residents inbound

Total

Domestically produced tourism goods and services Domestically produced tourism goods and services 2921 16,666 19587Overseas produced tourism goods and servicesOverseas produced tourism goods and services 14,886 4626 19512Total 17807 21292

Source: ABS 2004 (derived form Tables 14 and 15)

Table 5 shows the number of management units according to business size. It is characteristic that more than half of fi rms in tourism related businesses were micro businesses employing four or less employees. About another thirty percent of fi rms were small businesses employing between fi ve and nineteen employees.

2.1.2 The economic contribution of the IndustryThe Australian tourism industry has experienced strong growth over the past 20 years with only a few minor downturns. In 2002-2003, the tourism industry contributed 4.2 per cent to Australia’s gross domestic product.14

This fi gure is lower than the 2000-01 share of 4.8 percent because while tourism GDP decreased marginally during 2001-2002, GDP for the whole economy grew by 6.5 percent.15

The demand for tourism goods and services comes predominantly from domestic sources. In 2002-03 demand from Australian residents consumed 77.4 percent of tourism output, with international visitors consuming 22.6 percent of output.

In 2002-03 Australia ran a small positive tourism services trade balance of AUD$75 million as measured by the difference between tourism consumption by Australian residents on outbound trips and tourism consumption by non-residents on inbound trips (Table trips and tourism consumption by non-residents on inbound trips (Table trips and tourism consumption by non-residents on inbound trips ( 7).

22 KISA in Innovation of the Tourism Industry

2.1.3 Inputs to tourism

The value of tourism output is derived in the satellite accounts from the value of goods and services that are directly consumed by domestic and international tourists. The value of these goods and services from a wide range of industries can be conceived as inputs to the tourism industry. The share of these various inputs to the total value of tourism output is given in column 1 of Table 10. Just four industries account for 80.1 percent of the output of the tourism. These industries are Transport and storage (27.6 percent); Accommodation,

cafes and restaurants (20.9 percent) Manufacturing (16.9 percent) and Retail trade (14.7 percent). This indicates that the tourism industry draws on a wide range of industries supplying both services and goods.

Aside from identifying which industries supply inputs to tourism and how they contribute to total tourism output it is useful to examine the share of industries’ output going to the tourism industry. This data is given in column 2 of Table 10.

Table 9. Short Term Arrivals and Departures (million)

1997-98 1998-99 1999-2000 2000-01 2001-02 2002-03Arrivals (International Visitors) 4.22 4.28 4.65 5.03 4.76 4.65Departures (Australian Residents) 3.03 3.18 3.33 3.57 3.36 3.29

Source: ABS 2004 (Tables 17 and 18)

Table 8. Tourism Industry Share of Total Gross Value Added (Percent)

1997-98 1998-99 1999-2000 2000-01 2001-02 2002-034.3 4.2 4.2 4.1 3.9 3.8

Source: ABS 2004 (Table 1)

Despite this decline the tourism industry contributes more to national gross domestic product than other industries such as Cultural & Recreational Services 1.9 percent; Electricity Gas & Water 2.5 percent and Communication Services 2.9 percent.

Table 10. Inputs to the Tourism Industry. 2000-01 (Percent)

Contribution to Tourism Output From Industries

%

Tourism’s Share of Industries’ Gross Value Added

%Agric., forestry & fi shing 2.2 3.2Mining .01 0.1Manufacturing 16.9 3.6Electricity, gas & water Na naConstruction Na naWholesale trade 3.4 2.4Retail trade 14.7 9.6Accomm., cafes & rests. 20.9 36.1Transport and storage 27.6 16.5Communication servs. 1.4 2.2Finance and insurance Na naProperty & business servs. 1.6 naGovt. admin.& defence 0.03 0.3Education 2.1 3.9Health & community servs. 1.4 1.4Cultural and recreational servs. 4.0 10.4Personal and other servs. 0.2 0.5Ownership of dwellings 3.0 2.6Total 100 3.6

Source: ABS 2004 (Tables 7 and 6)

23AEGIS UWS

Whilst tourism derives its inputs from a wide range of industries, the tourism industry absorbs, in general, only a small proportion, of the value added of other industries. This is because the industry represents only 3.8 percent of national gross value added. Tourism absorbs more than 3.8 percent of the value of the output of the following industries: Accommodation, cafes and restaurants (36.1 percent); Transport and storage (16.5 percent); Cultural and recreational services (10.4 percent) and Retail trade (9.6 percent).

2.1.4 EmploymentThe tourism industry employed 540,700 persons in 2002-03, that is a 5.7% of National employment.17 The majority of the jobs in the tourism industry are in retail trade, the accommodation sector and cafés and restaurants. There are over 350,000 tourism related businesses in Australia. Most businesses are small to medium sized, and 90 percent employ less than 20 staff.18 In 2001-2002 the tourism industry stake of total employment decreased slightly to 5.9 percent after remaining at 6 percent since 1997 –1998.19

Estimates of employment in tourism are derived by the ABS by assuming that employment in each of the supplying industries is in proportion to the value added supplied to the tourism

industry (ABS 2004: 39). Tourism’s share of total employment (5.7 percent) is 50 percent larger than the industry’s share of national gross value added (3.8 percent) (Table gross value added (3.8 percent) (Table gross value added (3.8 percent) ( 11). This implies that labour productivity, as measured by gross value added per employee in the tourism industry is lower than for the economy in general. This result refl ects the lower level of labour productivity in the industries that supply the principal inputs to tourism, notably, accommodation, cafes and restaurants and retail who have a higher proportion of part time workers in these industries. Even adjusting for hours worked, these industries have substantially lower output per employee than for the economy as a whole (DITR 2004: 32).

Table 11. Employed Persons in Tourism per Industry. 2002-03

Industry ‘000Percent of Total

Employment in TourismTransport and storageTransport and storage 84.6 15.6Accommodation, cafes & restaurants 175.3 32.4ManufacturingManufacturing 45.8 8.5Retail trade 140.4 26.0Cultural and recreational services 28.5 5.3Education 24.6 4.5Total identifi ed industries 499.3 92.3Other 41.5 7.7Total tourist employment 540.7 100Total employmentTotal employment 9441.4

Tourism share of total employment 5.7

Source: ABS 2004 (derived from Table 16 by aggregating disaggregated industry data)

24 KISA in Innovation of the Tourism Industry

Applying the same method to deriving employment estimates by industry to cross tabulated data on industry and occupation, provides estimates of the occupational structure of the tourism industry (Table 12). This method assumes that the share of value added in a particular industry that is an input to tourism is the same as the share of all occupations in the industry that are employed in tourism (The value added data by industry was derived from ABS 2004: Table 8). Cross-tabulated data on the industry and occupational structure of all industries was derived from the ABS Labour Force (Cat. No. 6201.0), August 2003. The cross tabulated data consisted of Australian and New Zealand Standard Industrial Classifi cation (ANZSIC 1993 edition) Division and Australian Standard Classifi cation of Occupations (ASCO second edition) Major Group data. The total level of employment in tourism and its share of total employment differ from that reported in Table 12 largely because no employment

level could be assigned to the industry called ‘ownership of dwellings’ which provides value added inputs to tourism (ABS 2004: Table 8). The data represents 5.1 percent of total employment compared to 5.7 percent as reported in Table 12.

It is clear that the occupational structure of tourism is quite different from the occupational structure of total employment in the economy. Tourism has less than half the number of Professionals (9.1 percent compared to 18.8 percent) and over 40 percent fewer Managers and Administrators (7.2 percent compared to 4.2 percent). The higher proportion of Associate Professionals in tourism largely refl ects the fact that chefs are classifi ed to this occupational category and they work in tourism related industries. Tourism’s share of Elementary Clerical, Sales & Service Workers is some 61 percent larger than for the economy as a whole.

Table 12. Occupational Structure of Total Employment and Tourist Industry. Australia. August 2003

ASCO Major Group

Employed Total(‘000)

Occupation as a Share of Total

Employment(%)(%)

Employed in Tourism(‘000)

Occupation as a Share of Total Tourism

Employment

1 Managers & Administrators 680.9 7.2 21.4 4.2

2 Professionals 1762.7 18.8 46.5 9.1

3 Associate Professionals 1146.4 12.2 86.4 16.9

4 Tradespersons 1204.4 12.8 47.1 9.2

5 Advanced Clerical & Service Workers 377.1 4.0 11.7 2.3

6Intermediate Clerical, Sales & Service WorkersWorkers 1623.7 17.3 107.9 21.2

7Intermediate Production & Transport WorkersWorkers 794.8 8.5 53.6 10.5

8Elementary Clerical, Sales & Service WorkersWorkers 944.3 10.0 83.8 16.4

9 Labourers & Related Workers 862.4 9.2 52.0 10.2

Total 9396.7 100 510.4 100Source: ABS 2004 (derived from Table 6) and ABS (2003)

25AEGIS UWS

2.1.5 Domestic Tourism

The backbone of Australian tourism is domestic tourism. Up to three quarters of tourism consumption in Australia is domestic tourism, and it is a signifi cant contributor to regional Australia. It is the platform upon which inbound tourism is built. The domestic visitor share of tourism consumption was 77.3 percent in 2002-0320.

Over the forecast period, visitor nights are expected to grow by an average annual rate of 0.5 percent, from 298.7 million in 2002, to 314 million in 2012, as indicated by Figure 5.

Table 13. Proportion of Employment in ASCO Major Groups

Proportion of Total Employment in ASCO Groups

(Percent)

Proportion of Tourism Employment in ASCO Groups

(Percent)

ASCO Major Groups 1-5 (skilled)(skilled)

55 41.7

ASCO Major Groups 6-9 (less skilled)skilled)

45 58.3

Source: Derived from Table 12

Overall, tourism employs a smaller proportion of skilled workers (ASCO major groups 1-5) than the economy as a whole and a higher proportion of lesser skilled workers (ASCO major groups 6-9) (Table 13). These differences

in occupational structure between tourism and the economy as a whole, largely refl ect differences in industrial structure, the type of products produced and the tasks and skills required to produce them.

Figure 5. Domestic Visitor Nights 2000-2012

Source: Extracted from the Tourism White Paper, p. 16, National Visitor Survey and Tourism Forecasting Council, May 2003

200820072006200520042003200220012000 2009 2010 2011 2012

275

280285

290

295300

305

310

315320

('000s)Actual

Forecast

26 KISA in Innovation of the Tourism Industry

Visitors consumed a total of 73.3 billion worth of goods and services in 2002-2003, this was an increase of 26 percent of consumption in 1997-98. 23The international visitor share of tourism consumption was 22.7 percent in 2002-03, up from 22% in 1997-9824. There were 4,463, 000 inbound visitors into Australia in 2002. Their total expenditure in 2002, was AUD $11,377 million. The majority of the visitors came

from New Zealand, Japan, United Kingdom and USA.25 The Japanese inbound tourism industry is an example of the importance of the sector. In 2002, 668, 000 Japanese traveled to Australia. The growing economic benefi ts to Australia from the international tourist such as the Japanese are undeniable. Figure 6 shows the International visitor arrivals in December 1991- July 2003.

Table 14. Exports of Tourism Goods and Services

1997-98 1998-99 1999-00 2000-01 2001-02 2002-03

International visitor consumption (AUD $m)

12 792 13 446 14 611 17 140 17 080 16 700

Total Export (AUD $m) 113 744 112 025 126 034 153 511 152 357 NA

Tourism Share of Exports (%) 11.2 12.0 11.6 11.2 11.2 11.2

Growth in international visitor consumption (%)

5.1 8.7 17.3 -0.3 NA

Growth in total exports (%) -1.5 12.5 21.8 -0.8 NA

Source: ABS (2003) Australian National Accounts: Tourism Satellite Account 2001-2002, 5249.0, p. 8

2.1.6 Tourism ExportsTourism contributes signifi cantly to Australia’s export earnings. Tourism made more than AUD$16.6 billion in export earning in 2002-2003, through the direct sale of goods and services to international visitors. While tourism exports grew quite strongly between 1997–98 and 2000–01, so did exports of other goods and services. However both tourism exports

and total exports declined in 2001–02 (see Table 14).21 International visitors consumption was AUD $16.7 billion in 2002-2003. This is 11.2% of total exports. This is the same share as in 1997-98, but is down from its highest share of 12.0% in 1998-99.22

Iraq and SARS

September 11 and Ansett

Asian Economic Crises

Gulf War2000000

2500000

3000000

3500000

4000000

4500000

5000000

5500000

1991 1992 1993 1994 1994 1995 1996 1997 1997 1998 1999 2000 2000 2001 2002 2003

Num

ber o

f Vis

itors

Figure 6. International visitor arrivals December 1991–July 2003

Source: Extracted from the Tourism White Paper, p. 16, Australian Bureau of Statistics, Overseas Arrivals and Departures Catalogue No. 3401.0

27AEGIS UWS

Between 5 and 16 April 2004, the Australian Tourism Expert Council (ATEC) opened an on-line survey on the inbound sector. Those who were invited to respond were Inbound Tour Operator members of the Australian Tourism Export Council (ATEC) and international wholesalers. ATEC launched a unique International Tourism Index to estimate business confi dence within the tourism export industry and to identify trends in forward booking patterns, profi tability, turnover, competitive advantage and travel impediments.

The survey found that the majority of fi rms were confi dent about the growth prospects for their business; growth expectations were strongest from Japan, United Kingdom, Continental Europe and North America. Growth prospects were expected between up to fi ve percent. Operators also expected the profi tability of their businesses to grow. The majority of fi rms also expect employment to grow by more than one percent. Although these fi gures might suggest Australia will enjoy a greater comparative share of the inbound market, fi rms reported the negative effect of the strong Australian dollar on increased growth.26

2.1.7 Tourism Research and Development

In 2000-01 R&D expenditure with tourism as an objective totaled AUD 19.5 million, of which business supplied AUD 9.7 million; AUD AUD 8.7 million by universities and AUD 1.1 million by government (DITR 2004: 30). This represented only 0.2 percent of total R&D expenditure (ABS, 2002b: Table 1). This is signifi cantly less than tourism’s share of national gross product, which was 4.1 percent in 2000-01.

R&D expenditure on tourism as a share of the industry’s gross product is comparatively low. Tourism R&D was the equivalent of just 0.06 percent of tourism gross product in 2000-01 (derived from ABS 2002: Table 1 and ABS 2004: Table 1). For the economy as a whole R&D as a share of total gross domestic product was 1.53 percent in 2000-01 (ABS, 2002b: 3). R&D as a share of tourism’s gross domestic product is 25 times less than R&D share of GDP.

Table 15. Arrivals (1993-2012)

Year Arrivals Year Arrivals