kyrgyz republic - iuj.ac.jp · feliks kulov, entering the fray with a proposal to amend the...

TRANSCRIPT

Country Report

Kyrgyz Republic

November 2006

The Economist Intelligence Unit 26 Red Lion Square London WC1R 4HQ United Kingdom

The Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managing operations across national borders. For over 50 years it has been a source of information on business developments, economic and political trends, government regulations and corporate practice worldwide.

The Economist Intelligence Unit delivers its information in four ways: through its digital portfolio, where the latest analysis is updated daily; through printed subscription products ranging from newsletters to annual reference works; through research reports; and by organising seminars and presentations. The firm is a member of The Economist Group.

London The Economist Intelligence Unit 26 Red Lion Square London WC1R 4HQ United Kingdom Tel: (44.20) 7576 8000 Fax: (44.20) 7576 8500 E-mail: [email protected]

New York The Economist Intelligence Unit The Economist Building 111 West 57th Street New York NY 10019, US Tel: (1.212) 554 0600 Fax: (1.212) 586 0248 E-mail: [email protected]

Hong Kong The Economist Intelligence Unit 60/F, Central Plaza 18 Harbour Road Wanchai Hong Kong Tel: (852) 2585 3888 Fax: (852) 2802 7638 E-mail: [email protected]

Website: www.eiu.com

Electronic delivery This publication can be viewed by subscribing online at www.store.eiu.com

Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, online databases and as direct feeds to corporate intranets. For further information, please contact your nearest Economist Intelligence Unit office

Copyright © 2006 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author's and the publisher's ability. However, the Economist Intelligence Unit does not accept responsibility for any loss arising from reliance on it.

ISSN 1478-0399

Symbols for tables �n/a� means not available; ��� means not applicable

Printed and distributed by Patersons Dartford, Questor Trade Park, 151 Avery Way, Dartford, Kent DA1 1JS, UK.

Kyrgyz Republic 1

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Contents

Kyrgyz Republic

3 Summary

4 Political structure

5 Economic structure 5 Annual indicators 6 Quarterly indicators

7 Outlook for 2007-08 7 Political outlook 8 Economic policy outlook 9 Economic forecast

11 The political scene

15 Economic policy

20 The domestic economy 20 Output and demand 24 Sectoral trends

27 Foreign trade and payments

List of tables 9 International assumptions summary 10 Forecast summary 16 State budget, Jan-Aug 18 Sources of tax revenue, state budget 21 Main economic policy indicators 21 Basic data, Jan-Aug 24 Industrial production, Jan-Aug 26 Main macroeconomic indicators 30 Main external indicators

List of figures

11 Gross domestic product 11 Consumer price inflation 16 State budget 23 Monthly inflation 27 Trade statistics by country, Jan-May

Kyrgyz Republic 3

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Kyrgyz Republic November 2006

Summary

The political scene will continue to be plagued by instability, as a result of simmering popular discontent over persistent corruption and a lack of consensus over constitutional reform. Fiscal policy will remain reasonably prudent, constrained by the need to secure multilateral financing and support for debt relief. Annual real GDP growth should recover to just over 4% in 2007-08, once disputes in the gold sector are resolved and government measures to improve the business environment take some effect. Inflation will trend upwards but should remain manageable, as money demand will also rise. The current account will remain in deficit, largely because of increases in energy import prices.

Tensions between the president, Kurmanbek Bakiyev, and the Jogorku Kenesh (parliament) have remained high. The opposition "For Reforms" movement staged a rally in mid-September, and has pledged to hold another on November 2nd. The constitutional reform process has dragged on, with the prime minister, Feliks Kulov, entering the fray with a proposal to amend the existing constitution rather than writing a new one. Media freedoms have come under question, as several media outlets have returned to state control over the past year. Relations with Uzbekistan have continued to improve.

The state budget recorded a surplus of Som660m (US$16.4m) in January-August 2006, compared with one of Som381m in the same period of 2005. Revenue rose by 22% year on year, driven by an improvement in the collection of value-added tax (VAT).

Real GDP grew by 3.5% year on year in January-August, according to preliminary data from the National Statistical Committee (NSC). Excluding the Kumtor gold mine, which suffered a pit-wall movement in July, real GDP grew by 6.6% in this period. Inflation slowed during the middle of the year, bringing the government!s year-end target of 5.7% within reach. The som has continued to strengthen against the US dollar, partly as a result of rising remittances from abroad. Centerra Gold (Canada) has made downward revisions to its output projections for the Kumtor gold mine. Uzbekistan has announced that it will increase gas prices.

The Kyrgyz Republic!s current-account deficit widened to US$144m in the first half of 2006, largely because of rising energy and transport import costs.

Editors: Dafne Ter-Sakarian (editor); Anna Walker (consulting editor) Editorial closing date: November 13th 2006 All queries: Tel: (44.20) 7576 8000 E-mail: [email protected] Next report: Full schedule on www.eiu.com/schedule

Outlook for 2007-08

The political scene

Economic policy

The domestic economy

Foreign trade and payments

4 Kyrgyz Republic

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Political structure

Kyrgyz Republic

The Kyrgyz Soviet Socialist Republic declared its independence in August 1991 and changed its name to the Kyrgyz Republic. Its constitution was approved on May 5th 1993. The president!s powers were enhanced by a referendum held in February 1996. Further changes to the presidency were made in a referendum held in February 2003

The 313-member Jogorku Kenesh of the Soviet era was divided in 2000 into a 105-member bicameral parliament, elected for a five-year term and composed of the Legislative Assembly (the lower house, with 60 deputies) and the Assembly of People!s Representatives (the upper house, with 45 deputies). After the February 2005 parliamentary election, the Jogorku Kenesh became a unicameral chamber of 75 deputies, elected for a five-year term

February 27th and March 13th 2005 (parliamentary) and July 10th 2005 (presidential); next elections due in February 2010 (parliamentary) and July 2010 (presidential)

The president appoints a prime minister, who forms a government

Kurmanbek Bakiyev, taking over from Askar Akayev, who was president from October 1991 until March 2005, when he fled the country after protesters in the capital, Bishkek, stormed government buildings

Alga (Forward), Kyrgyzstan!; Adilet (Justice); Ar-Namys (Dignity); Asaba (Banner); Democratic Party of Women of Kyrgyzstan; Erkindik (Freedom); Mekenim (Fatherland) Kyrgyzstan movement; Moya Strana (My Country); Communist Party of Kyrgyzstan (KPK); Progressive-Democratic Party Erkin Kyrgyzstan (ErK); Party of Communists of Kyrgyzstan (PKK); Protection Party; Republican People�s Party; Social Democratic Party of Kyrgyzstan; Socialist Party Ata-Meken (Fatherland)

Prime minister Feliks Kulov First deputy prime minister Daniyar Usenov Deputy prime minister (acting) Tynychbek Tabyldiyev

Agriculture, water management & processing industry Azim Isabekov Culture Sultan Rayev Defence Ismail Isakov Economy & finance Akylbek Japarov Education, science & youth policy Dosbol Nur uulu Emergency situations Janysh Rustenbekov Foreign affairs Alikbek Jekshenkulov Health Shailoobek Niyazov Industry, trade & tourism Medetbek Kerimkulov Internal affairs Murat Sutalinov Justice Marat Kaypov Labour & social protection Yevgeny Semenenko Migration & employment committee Aygul Ryskulova Prime minister�s chief of staff Turuspek Koyenaliyev State property committee Tursun Turdumambetov Transport & communications Nurlan Sulaymanov

Elmurza Satybaldiyev (acting)

Kambaraly Kongantiyev

Marat Alapayev

Main political parties

National legislature

National elections

Prosecutor-general

National government

Head of state

Form of state

Head of National Security Service

Key ministers

Central bank chairman

Official name

Kyrgyz Republic 5

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

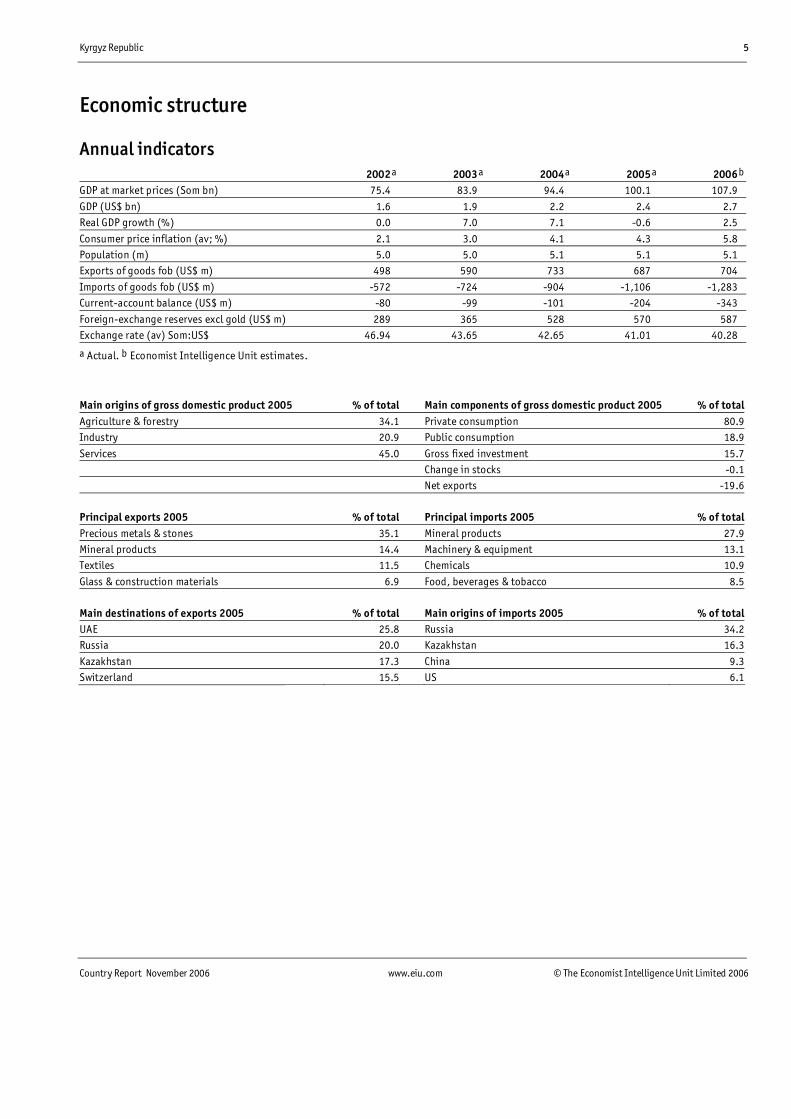

Economic structure

Annual indicators

2002a 2003a 2004 a 2005 a 2006b

GDP at market prices (Som bn) 75.4 83.9 94.4 100.1 107.9

GDP (US$ bn) 1.6 1.9 2.2 2.4 2.7

Real GDP growth (%) 0.0 7.0 7.1 -0.6 2.5

Consumer price inflation (av; %) 2.1 3.0 4.1 4.3 5.8

Population (m) 5.0 5.0 5.1 5.1 5.1

Exports of goods fob (US$ m) 498 590 733 687 704

Imports of goods fob (US$ m) -572 -724 -904 -1,106 -1,283

Current-account balance (US$ m) -80 -99 -101 -204 -343

Foreign-exchange reserves excl gold (US$ m) 289 365 528 570 587

Exchange rate (av) Som:US$ 46.94 43.65 42.65 41.01 40.28

a Actual. b Economist Intelligence Unit estimates.

Main origins of gross domestic product 2005 % of total Main components of gross domestic product 2005 % of totalAgriculture & forestry 34.1 Private consumption 80.9Industry 20.9 Public consumption 18.9

Services 45.0 Gross fixed investment 15.7 Change in stocks -0.1 Net exports -19.6

Principal exports 2005 % of total Principal imports 2005 % of totalPrecious metals & stones 35.1 Mineral products 27.9Mineral products 14.4 Machinery & equipment 13.1Textiles 11.5 Chemicals 10.9

Glass & construction materials 6.9 Food, beverages & tobacco 8.5 Main destinations of exports 2005 % of total Main origins of imports 2005 % of totalUAE 25.8 Russia 34.2Russia 20.0 Kazakhstan 16.3

Kazakhstan 17.3 China 9.3Switzerland 15.5 US 6.1

6 Kyrgyz Republic

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Quarterly indicators 2004 2005 2006 3 Qtr 4 Qtr 1 Qtr 2 Qtr 3 Qtr 4 Qtr 1 Qtr 2 QtrGovernment finance (Som bn) Revenue & grants 4.6 5.6 4.2 4.9 5.0 6.3 4.9 6.1Expenditure & net lending 4.4 6.8 3.6 5.0 5.0 6.6 4.2 6.2Balance 0.2 -1.2 0.6 -0.1 0.0 -0.4 0.7 -0.1Wages & prices Monthly earnings (Som) 2,202 2,502 2,276 2,466 2,589 2,931 2,659 2,911 % change, year on year 12.8 19.0 16.0 15.1 17.6 17.1 16.8 18.1Consumer prices (2000=100) 116.4 117.6 120.5 122.8 121.6 123.7 128.0 129.8 % change, year on year 5.6 2.6 2.6 5.0 4.5 5.2 6.2 5.8Producer prices (2000=100) 131.5 135.1 131.6 133.1 135.4 144.6 151.2 161.7 % change, year on year 9.2 5.9 1.0 1.3 3.0 7.0 14.9 21.5

Financial indicators Exchange rate Som:US$ (av) 42.45 41.64 41.01 41.10 40.94 41.00 41.38 40.71Exchange rate Som:US$ (end-period) 42.50 41.62 41.29 40.96 40.85 41.30 41.37 40.21Lending rate (av; %) 23.1 27.1 22.4 20.6 19.8 24.0 23.0 24.3Money market rate (av; %) 5.6 4.7 3.8 3.9 3.3 2.0 2.8 3.1M1 (end-period; Som m) 11.4 13.0 13.1 13.2 14.3 15.2 15.2 17.4 % change, year on year 26.6 22.9 18.8 17.2 24.9 16.4 16.1 31.3M2 (end-period; Som m) 16.7 19.4 19.8 21.0 23.1 21.4 21.6 24.1 % change, year on year 29.8 32.1 31.4 32.1 38.0 10.0 8.8 14.6

Sectoral trends, production Coal & lignite (�000 tonnes) 104 200 78 52 76 126 45 38Natural gas (m cu metres) 7.4 8.2 7.3 5.5 5.2 6.7 4.8 5.2Crude oil (b/d) 1,446 1,550 1,390 1,430 1,502 1,655 1,438 1,494Electricity (m kwh) 3.2 4.4 4.8 2.5 3.1 4.5 4.8 2.4Foreign trade (US$ m) Exports fob 185 196 164 158 165 184 175 202Imports cif 245 274 241 248 278 341 336 411Trade balance -60 -78 -77 -90 -113 -157 -161 -209

Balance of payments (US$ m) Merchandise trade balance fob-fob -48 -59 -57 -94 -125 -143 -133 -142Services balance -12 -8 -10 -14 -14 -13 -15 -5Income balance -15 -18 -19 -28 -17 -22 -20 -17Net transfer payments 59 61 63 77 94 101 75 112

Current-account balance -16 -24 -23 -58 -63 -77 -93 -52Reserves excl gold 496 528 527 505 534 570 557 601

Sources: IMF, International Financial Statistics; National Statistical Committee; National Bank of the Kyrgyz Republic.

Kyrgyz Republic 7

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Outlook for 2007-08

Political outlook

The outlook for the government that came to power after the ouster of the former president, Askar Akayev, is not very promising. The government is shackled by both internal divisions and external constraints, and its ability to implement consistent policies will remain severely limited until significant progress is made on two key issues: corruption and constitutional reform. Given these tensions, the current administration!s hold on power cannot be completely assured.

The widespread perception that the nepotism of the Akayev years has been replaced by a new but equally corrupt network"a perception fuelled by the appointment of several relatives of the president, Kurmanbek Bakiyev, to influential posts in the new administration"has created simmering popular discontent, manifested in repeated rallies and demonstrations. Political effectiveness is also hampered by tensions between Mr Bakiyev and his prime minister, Feliks Kulov, as well as by a drawn-out debate over constitutional reform.

Corruption is rife, not only because it flourished under Mr Akayev, but also because his ouster created a power vacuum that neither faction is strong enough to fill completely. It has therefore been especially easy for businessmen to seize assets and seek to gain political influence. This situation is unlikely to improve until either a working compromise is found or one political grouping prevails. However, even in conditions of greater political stability, corruption and criminalisation in business would not be easy to eradicate.

The current administration is fundamentally weak: it does not have full control over the bodies of law and order enforcement. Central authority over them was lost completely during the events of March 2005, and has not been regained. This has allowed pockets of lawlessness to emerge in various regions, most notably in Kara Keche; although the situation there appears to have been brought under some control, restoring order took long enough to raise the spectre of continued chaos and, in the most pessimistic prognoses, of civil war and national disintegration. The Economist Intelligence Unit does not think the Kyrgyz Republic will fragment, since, in the event of a serious threat to the geographic integrity of the country, regional security bodies would step in. Nonetheless, our central scenario does assume persistent political instability over the forecast period.

Mr Akayev!s successors will continue with the former president!s "multi-vectoral" foreign policy. Although earlier in the year Mr Bakiyev publicly stated that the US should set a timetable for the withdrawal of coalition troops from Central Asia, the base at Manas International Airport provides the Kyrgyz Republic with much-needed income. Consequently, a US withdrawal is unlikely to happen soon, as evidenced by the fact that the current agreement on the coalition forces� continued use of the base does not set a fixed date for their departure. The Kyrgyz Republic will continue to host the US military presence,

Domestic politics

International relations

8 Kyrgyz Republic

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

in addition to the permanent deployment of Russian troops at Kant, near the capital, Bishkek. Increasingly close military co-operation with China could add another dimension to the Kyrgyz Republic!s foreign relations, but this will be tempered by Kyrgyz mistrust of China�s territorial and political ambitions in the region.

Economic policy outlook

The IMF has favourably reviewed the Kyrgyz Republic!s progress under the three-year poverty reduction and growth facility (PRGF) signed in February 2005. Heavily reliant on multilateral funding, the Kyrgyz Republic has a strong incentive to maintain good relations with the IMF, but meeting the IMF criteria will have to be balanced against preventing a rise in social instability. This task will be eased by the IMF!s recognition of the difficult circumstances in the country reflected in the Fund!s October decision that the Kyrgyz Republic qualifies for the heavily indebted poor countries (HIPC) initiative. Nonetheless, the IMF has expressed grave concerns over corruption and the large quasi-fiscal deficits in the electricity sector. The government will therefore seek to make concrete progress in these spheres. The pace and depth of reform will be given an additional boost over the long term if the Kyrgyz Republic joins the HIPC initiative, as conditionality is stricter than under other multilateral programmes.

The government has pledged to make foreign direct investment (FDI) a priority, proposing far-reaching regulatory and tax reform. However, there is considerable uncertainty surrounding the ability of any government to pursue this approach, as domestic opposition to the sale of state assets is strong, and investors are wary because of the poor business environment and high levels of corruption. These factors will mean that, for the most part, only foreign investors familiar with the business environment in Central Asia"essentially Russian and Kazakh companies"will seek opportunities in the Kyrgyz Republic. The sale of assets to such firms is unlikely to attract controversy, owing to the long-standing historical links with these two countries.

The state budget posted a surplus of Som660m (US$16.4m) in the first eight months of 2006, as a result of continued improvements in revenue performance. The full-year budget targets a deficit ceiling of 2.1% of GDP, but on the basis of the solid performance thus far we expect the full-year deficit to come in below the government!s projection. Tax cuts will dampen revenue over the forecast period, but should spur some businesses to come out of the shadow economy. As a result, lost revenue per tax entity will be offset by greater compliance, allowing for a small deficit, of around 2% of GDP, in 2007, narrowing to less than 1.5% of GDP in 2008 as the economy continues to recover.

The National Bank of the Kyrgyz Republic (NBKR, the central bank) has been able to maintain its independence and pursue a relatively tight monetary policy"a stance that we expect it to adhere to throughout the forecast period. Nonetheless, the bank operates within significant constraints, since it has limited policy instruments with which to pursue financial deepening. Currently, the bank is helped by the fact that inflows of foreign exchange"related to financial

Policy trends

Fiscal policy

Monetary policy

Kyrgyz Republic 9

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

assistance and workers! remittances"are sterilised by the external deficit and do not exert significant pressures on the money supply.

Economic forecast

International assumptions summary (% unless otherwise indicated)

2005 2006 2007 2008

Real GDP growth World 5.0 5.3 4.7 4.7

OECD 2.6 3.1 2.2 2.4

EU25 1.7 2.6 2.1 2.2

Exchange rates Rb:US$ 28.3 27.5 27.4 28.5

US$:� 1.245 1.255 1.363 1.338

SDR:US$ 0.677 0.679 0.643 0.644

Financial indicators ¥ 2-month private bill rate 0.00 0.23 1.13 2.00

� 3-month interbank rate 2.15 3.06 3.86 3.90

Commodity prices Oil (Brent; US$/b) 54.7 69.3 69.3 66.0

Gold (US$/troy oz) 445.0 631.5 700.0 650.0

Food, feedstuffs & beverages (% change in US$ terms) -0.5 8.9 -4.5 0.7

Industrial raw materials (% change in US$ terms) 10.2 49.1 -3.7 -10.5

Note. Regional GDP growth rates weighted using purchasing power parity exchange rates.

Strong Russian demand, largely attributable to persistently high oil prices, is helping to support growth in the Commonwealth of Independent States (CIS). Although the rate of real GDP growth in Russia will trend downwards in 2007-08, Russian import demand growth will stay robust, ensuring that the country remains the Kyrgyz Republic!s most important destination for non-gold exports. The Kyrgyz Republic is also benefiting from vigorous growth in neighbouring Kazakhstan. Prices for gold, the Kyrgyz Republic!s main export commodity, are booming. Gold!s fundamentals remain supportive of its higher trading level, in addition to which shorter-term buying by funds and speculators will sustain investor interest in gold. This will keep prices high in the forecast period, despite a slight weakening in 2008.

The impact of an accident at the Kumtor gold mine in July has not been as severe as we had originally anticipated, with output in January-August growing by a respectable 3.5% year on year. As a result, we have revised upwards our full-year real GDP growth estimate for 2006 from 2% to 2.5%. Nonetheless, our forecast still assumes a deceleration of year-on-year growth in the second half of the year. Confusion over the licences to mine the Kyrgyz Republic!s two most promising gold deposits, Jerooy and Taldy-Bulak, as well as uncertainty over property rights, will prevent faster growth, but the eventual resolution of at least some of the current business disputes, as well as the effects of government measures to improve the investment climate, should allow real GDP growth to accelerate in 2007-08, to an annual average of slightly over 4%. The operator of the Kumtor gold mine, Centerra Gold (Canada), has revised

Economic growth

International assumptions

10 Kyrgyz Republic

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

downwards its 2007 output forecast; our 2007 real GDP growth forecast remains unchanged, however, because we had already factored in far more conservative estimates for gold output at the mine. Nevertheless, the downside risks to this relatively benign outlook are considerable, given the Kyrgyz Republic!s narrow economic base.

As the economy stabilises in 2007-08 and returns to growth, inflation will trend upwards, further boosted by rising inflows of workers! remittances. An increase in the price of gas imports from Uzbekistan will exert additional upward pressure on prices towards the end of 2006 and into the forecast period, although disinflation in the middle of the year has brought the official year-end target of 5.7% for 2006 within reach. Price increases over the forecast period will nonetheless remain manageable, as the economy has a low level of monetisation, of around 20% of GDP.

The NBKR will limit its interventions on the foreign-exchange market to the minimum required to smooth daily fluctuations and strengthen international reserves. However, political uncertainty raises risks to the conduct of exchange-rate policy, as further turmoil could weaken the exchange rate and force the bank to intervene more heavily. Reserves are unlikely to grow significantly over the forecast period, although US dollar sales by the NBKR will be offset by additional IMF disbursements and lower debt repayments resulting from the renegotiation of Paris Club debt. This should permit the central bank to cushion the som against political and seasonal pressures.

According to the NKBR, the current account posted a deficit of US$144.2m in the first half of 2006. This supports our estimate of a significant widening of the current-account deficit in 2006, owing to rising energy prices and slow growth in export revenue as a result of the fall in production at Kumtor. The govern-ment!s efforts to bring the deficit down will be helped somewhat in 2007-08 by steadily rising net transfers and the successful renegotiation of Paris Club debt, which will bring about a reduction in interest payments. Acceptance into the HIPC initiative will also ease the Kyrgyz Republic!s debt-servicing burden.

The current-account balance will nonetheless remain negative, in the light of rapidly rising imports of both goods and services. On the capital account, FDI will rise during the forecast period as a result of aggressive expansion by Russian and Kazakh companies, but levels will remain low"reflecting the Kyrgyz Republic�s paucity of attractive assets and an uncertain business climate.

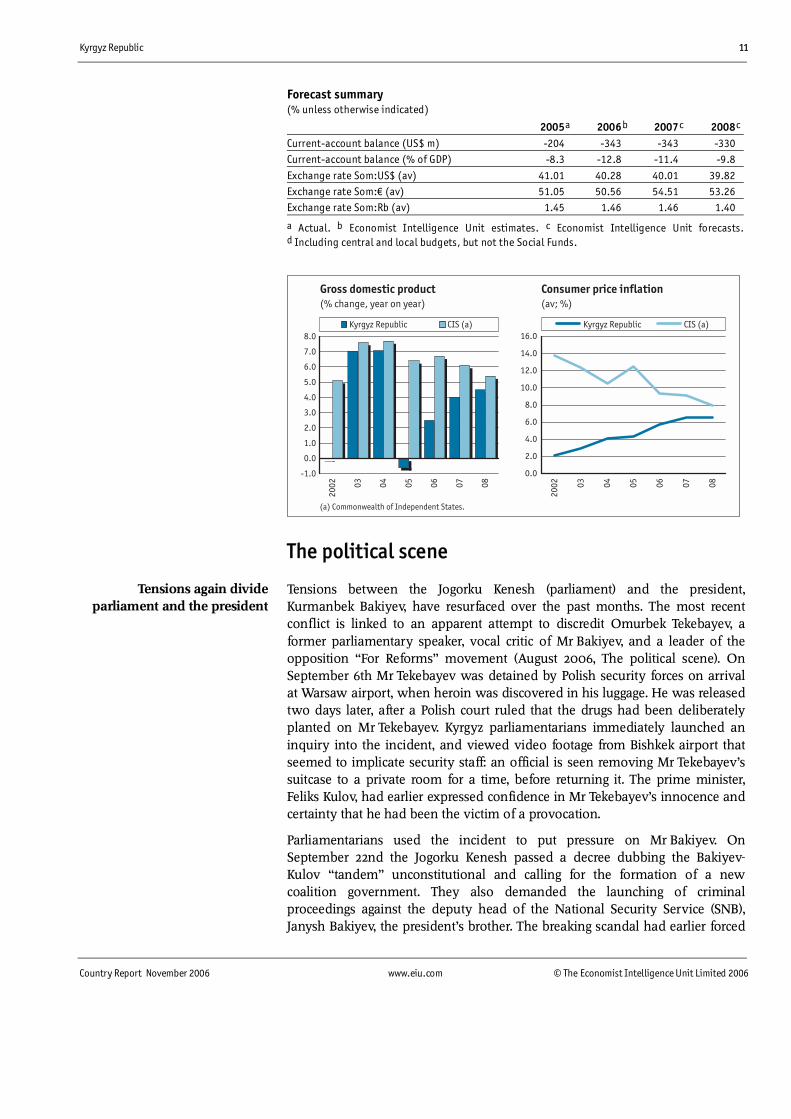

Forecast summary (% unless otherwise indicated)

2005 a 2006 b 2007c 2008c

Real GDP growth -0.6 2.5 4.0 4.5

Exports of gold ('000 kilograms) 16.6 10.0 13.4 14.1

Consumer price inflation (av) 4.3 5.8 6.5 6.6

Lending rate 21.7 19.0 17.5 19.0

Government balance (% of GDP)d 0.2 -1.8 -1.9 -1.4

Exports of goods fob (US$ m) 687 704 848 899

Imports of goods fob (US$ m) -1,106 -1,238 -1,472 -1,591

Exchange rates

External sector

Inflation

Kyrgyz Republic 11

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Forecast summary (% unless otherwise indicated)

2005 a 2006 b 2007c 2008c

Current-account balance (US$ m) -204 -343 -343 -330

Current-account balance (% of GDP) -8.3 -12.8 -11.4 -9.8

Exchange rate Som:US$ (av) 41.01 40.28 40.01 39.82

Exchange rate Som:� (av) 51.05 50.56 54.51 53.26

Exchange rate Som:Rb (av) 1.45 1.46 1.46 1.40

a Actual. b Economist Intelligence Unit estimates. c Economist Intelligence Unit forecasts. d Including central and local budgets, but not the Social Funds.

Kyrgyz Republic CIS (a)

Gross domestic product(% change, year on year)

Kyrgyz Republic CIS (a)

Consumer price inflation(av; %)

(a) Commonwealth of Independent States.

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.02

00

2

03

04

05

06

07

08

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

20

02

03

04

05

06

07

08

The political scene

Tensions between the Jogorku Kenesh (parliament) and the president, Kurmanbek Bakiyev, have resurfaced over the past months. The most recent conflict is linked to an apparent attempt to discredit Omurbek Tekebayev, a former parliamentary speaker, vocal critic of Mr Bakiyev, and a leader of the opposition �For Reforms� movement (August 2006, The political scene). On September 6th Mr Tekebayev was detained by Polish security forces on arrival at Warsaw airport, when heroin was discovered in his luggage. He was released two days later, after a Polish court ruled that the drugs had been deliberately planted on Mr Tekebayev. Kyrgyz parliamentarians immediately launched an inquiry into the incident, and viewed video footage from Bishkek airport that seemed to implicate security staff: an official is seen removing Mr Tekebayev�s suitcase to a private room for a time, before returning it. The prime minister, Feliks Kulov, had earlier expressed confidence in Mr Tekebayev�s innocence and certainty that he had been the victim of a provocation.

Parliamentarians used the incident to put pressure on Mr Bakiyev. On September 22nd the Jogorku Kenesh passed a decree dubbing the Bakiyev-Kulov �tandem� unconstitutional and calling for the formation of a new coalition government. They also demanded the launching of criminal proceedings against the deputy head of the National Security Service (SNB), Janysh Bakiyev, the president�s brother. The breaking scandal had earlier forced

Tensions again divide parliament and the president

12 Kyrgyz Republic

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

the president to dismiss his brother, and the head of the SNB, Busurmankul Tabaldiyev, also left his post. Charges that Janysh Bakiyev was implicated in planting the drugs on Mr Tekebayev also renewed controversy over the official positions occupied by the president�s family: two other brothers of the president have been appointed to diplomatic posts in overseas embassies. Opposition figures led calls for their dismissal, drawing parallels with the previous presidential administration led by Askar Akayev, which was tarnished by charges of nepotism"a key factor behind the popular demonstrations that led to Mr Akayev�s ouster in 2005.

The opposition, mainly led by Mr Tekebayev�s For Reforms movement and the Asaba (Banner) party of Azimbek Beknazarov, has been continuing its campaign for constitutional reforms and a crackdown on corruption. The scandal over Mr Tekebayev�s arrest might have been expected to boost the opposition cause, but visible popular support seems instead to be waning, compared with the well-attended demonstration in the capital, Bishkek, in April (August 2006, The political scene). In mid-September For Reforms and Asaba held a high-profile �people�s assembly� in the southern Aksy region, which is Mr Beknazarov�s home base.

However, contrary to the organisers� hopes, the assembly was sparsely attended. This raises doubts over the opposition movement�s ability to sustain popular support for its demands. For Reforms and Asaba have declared their intention to hold a large rally on November 2nd in Bishkek. Before previous demonstrations, tensions have been high over the possibility of an outbreak of violence. The opposition will thus be hampered in its attempts to stoke public discontent by the need to be seen to keep any protests peaceful, since some state-controlled media outlets have portrayed opposition leaders as intent on provoking civil breakdown. It will therefore be difficult to build greater momentum behind the protest movement while For Reforms struggles against a perception that it can do nothing more than offer Mr Bakiyev a �rolling deadline� to meet its demands.

Nevertheless, opposition pressure does seem to be having an effect in some areas. One of the demands that For Reforms issued in April was that the perpetrators of violence in Aksy in March 2002 be brought to justice. In that incident, a number of demonstrators protesting against the imprisonment of Mr Beknazarov were killed, which eventually led the entire government"at the time headed by Mr Bakiyev as prime minister"to resign. The investigation into the Aksy events was given renewed impetus following the ouster of Mr Akayev, but has since stalled. However, in September Kambaraly Kongantiyev, the prosecutor-general, said that the investigation would be finalised in December, following a public call from Mr Bakiyev for its rapid conclusion.

Opposition campaign continues

Some opposition demands may be bearing fruit

Kyrgyz Republic 13

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Mr Bakiyev has also reiterated his intention to hold a referendum on constitutional reform before the end of the year"another key demand of the opposition movement. The Jogorku Kenesh is currently studying the three drafts of the new constitution that were prepared by the Constitutional Conference under the leadership of Mr Beknazarov (August 2006, The political scene). There has been some confusion about the process of adopting a new constitution, with Mr Bakiyev seemingly ambivalent about whether the form of government enshrined in it should be decided by referendum or by parliament. However, in a television interview in late August, Mr Bakiyev said that a question on what form of government the Kyrgyz Republic should adopt"whether presidential, parliamentary or a mixture of the two"would be put to a referendum in late 2006.

A new constitution would be drafted in accordance with the response, and, following its approval by parliament, it would be put to the popular vote in a second referendum. Mr Bakiyev has also reiterated his opposition to a parliamentary form of government, stating that the party political system in the Kyrgyz Republic is too fragmented to ensure stable and coherent governance, should parliament wield executive power. Despite this, all three forms of the draft constitution before parliament stipulate that parliamentary elections will be run along party-list lines, rather than the current system of single-mandate constituencies.

Mr Kulov added to the already complex situation by submitting an alternative proposal to parliament on October 9th, consisting of a series of amendments to the current constitution. According to Mr Kulov, in the interests of political stability it would be preferable to retain the existing constitution, amending it according to his proposal, rather than to rewrite the text.

The turnout at the opposition people�s assembly in September may have been adversely affected by the media. The furore over Mr Tekebayev�s arrest"which might have been expected to boost public sympathy for the For Reforms movement"was downplayed by prominent TV stations and other media outlets, leading opposition figures to claim that press freedoms had been eroded since Mr Akayev�s ouster. Several media outlets have been involved in ownership disputes or have been returned to state control over the past year. Freedom House, a US-based non-governmental organisation (NGO), in its most recent annual report on worldwide civil liberties has said that the potential for significantly enhancing the media environment following the fall of the Akayev regime has not been fulfilled. Freedom House continues to class the Kyrgyz Republic as �not free� in terms of media freedoms, although its latest survey notes an improvement from �not free� to �partly free� in terms of overall political rights and civil liberties.

One independent Bishkek TV station, Pyramid TV, suffered a violent attack in September, when unknown assailants beat up staff and started a fire that damaged transmitter equipment. This forced the station off the air just as it began broadcasting again (Pyramid had been off the air for a month after a previous attack also damaged equipment). Senior journalists at the station also claim to have received threats and demands to change the tone of their

Media freedoms come under question

Constitutional reform process drags on

14 Kyrgyz Republic

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

coverage. In late 2005 Pyramid was caught up in an ownership dispute (February 2006, Economic policy); it is one of the For Reforms movement�s demands that Pyramid be returned to its previous owners and that �state pressure� on the station should cease.

Relations with the US have become more settled, following tensions earlier in the year"the Kyrgyz Republic dismissed two US diplomats in July, and long-standing negotiations over rent payments for the use of the Manas airbase had been fraught and occasionally bitter before an agreement was finally reached (August 2006, The political scene). In September the US donated four aircraft to the Kyrgyz Ministry of Defence, with a view to strengthening border control to combat terrorist threats and smuggling. One potential source of embarrassment surrounded the disappearance of a US officer based at Manas in early September. Jill Metzger disappeared while shopping in Bishkek; she was discovered by Kyrgyz police three days later, claiming to have been abducted, and has since been repatriated to the US. The circumstances around her disappearance remain opaque, but the incident does not seem to have had any serious diplomatic repercussions.

Despite the apparent rapprochement with the US, Kyrgyz foreign policy remains firmly directed towards maintaining close links with Russia and other members of the Shanghai Co-operation Organisation (SCO), including China. Kyrgyz forces are to carry out joint exercises with Russian troops in October in the south of the Kyrgyz Republic. Energy co-operation has also been a prominent feature of talks between SCO states recently, with other Central Asian countries and China keen to tap the Kyrgyz Republic�s hydroelectric power potential. Such moves have been seen as an attempt to thwart US desires to promote the Kyrgyz Republic as a power supplier for South Asian states such as Pakistan, rather than for China and the Russian-dominated Commonwealth of Independent States (CIS).

Relations with Uzbekistan, which foundered in 2005 over the status of refugees from Andijan, have improved markedly. The impetus for the reconciliation seems to have arisen from the Kyrgyz Republic�s increased emphasis on security concerns stemming from Islamist activity. The two countries stepped up their co-operation on border and security issues following a number of violent incidents that the Kyrgyz authorities blamed on Islamist militants (August 2006, The political scene). Some parliamentarians have questioned the motives behind this heightened security activity, and have suggested that the authorities are overplaying the threat from radical Islam.

Kyrgyz and Uzbek security forces carried out a controversial joint operation in early August, killing three men just outside the southern city of Osh. One of the men killed was a prominent imam, Muhammadrafik Kamalov, in the town of Kara Suu, which lies on the Uzbek-Kyrgyz border. The Kyrgyz authorities dubbed Mr Kalamov a terrorist, claiming that he had ties with the banned Islamic Movement of Uzbekistan (IMU), and that the two other men killed were IMU members. Friends and followers of Mr Kamalov denied this, although Mr Kamalov was known for tolerating the presence of members of Hizb ut-Tahrir (Party of Freedom) at his mosque, while disagreeing with their

International relations are calmer

Uzbek-Kyrgyz co-operation on terrorism continues

Kyrgyz Republic 15

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

views. Hizb ut-Tahrir advocates the establishment of a caliphate in Central Asia, and although it publicly eschews violence, it has long been conflated with the militant IMU by Uzbekistan; the Kyrgyz authorities now seem to have adopted the same view (August 2006, The political scene).

Several thousand turned out to protest against the killing of Mr Kamalov, and the Kyrgyz authorities partly retracted their earlier claims, suggesting that Mr Kamalov may have been killed accidentally. However, throughout August and September they continued to step up anti-terrorist activity, warning that the IMU was planning incursions in order to destabilise the south of the country. In August the trial began of six alleged Islamist militants suspected of being involved in the violent border incursions in May.

The recent confluence of views on the threat of Islamist extremism between the Kyrgyz Republic and Uzbekistan has alarmed NGOs and international human rights groups. In September four suspected members of an Uzbek-based Islamist group, Akramiya (an off-shoot of Hizb ut-Tahrir), were put on trial in Osh. The Uzbek authorities claim that the four were involved in planning violence in Andijan in May 2005, and the Kyrgyz authorities charged them with illegal possession of weapons and involvement in a terrorist plot. One of those charged was the daughter of Akram Yuldashev, the leader of Akramiya (from whom the group takes its name), who is currently serving a prison sentence in Uzbekistan. In a decision welcomed by local human rights groups, the four suspects were released only days later"two were exonerated of all charges, and two fined for possessing forged passports.

However, Uzbekistan enjoyed a diplomatic success in August, when the Kyrgyz authorities deported to Uzbekistan five refugees wanted in connection with the Andijan events. Four of the five had been granted asylum status by the UN High Commissioner for Refugees (UNHCR), and their extradition met with international condemnation"in 2005 local courts had overturned a decision to return two of the men to Uzbekistan (November 2005, The political scene). The UNHCR has also expressed concern about a number of other refugees from Andijan who have gone missing from their homes in Osh, and fears that they may have been forcibly repatriated to Uzbekistan.

Economic policy

In the first eight months of 2006 the state (consolidated) budget recorded a surplus of Som660m (US$16.4m), compared with one of Som381m in the first eight months of 2005. Overall revenue rose by 22% year on year, driven mainly by an improvement in collection of value-added tax (VAT), which makes up almost half of total tax revenue. VAT increased by over 28% year on year, an acceleration from the rate of 22% recorded in January-August. Customs revenue continues to perform well, rising by 77%. However, the rate of growth of revenue from income and profit tax has slowed compared with earlier in the year, and indeed profit tax receipts fell by 3.5% year on year. In January-May proceeds from profit tax had been rising by over 10% year on year, following an increase of almost 40% in 2005 as a whole.

Budget continues to record a surplus

Closer ties with Uzbekistan stoke human rights fears

16 Kyrgyz Republic

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

State budget(Som m)

Source: National Statistical Committee.

-1,000

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500BalanceRevenueExpenditure

JunAprFeb06

DecOctAugJunAprFeb05

DecOctAugJunAprFeb04

DecOctAugJun2003

Overall spending rose by 22% year on year, compared with a rise of only 12% in January-May. All categories of spending registered an acceleration. Among the more significant expenditure lines, particularly rapid growth was recorded in subsidies to the real sector, which went up by almost 30%. Subsidies to the transport and communications sector increased by nearly 60%, and those to the agricultural and related sectors by over 20%; together, these two items accounted for over four-fifths of total economic subsidies in the first eight months of 2006.

The �social� tenor of budget planning under the current government remained apparent in spending on education, health, housing and social welfare, which all rose by over 20% year on year"an acceleration since earlier in 2006, as well as compared with the growth of spending on these items in 2005 as a whole. Spending on administration, defence and internal security"still the most significant expenditure line, accounting for one-quarter of total spending"rose by less than 10%. However, as earlier in the year, the headline figure continues to mask varying trends within this category. Defence expenditure rose by only 4% year on year, and spending on general government services (largely state administration costs) by 5%. Outgoings on internal security, by contrast, rose by 25%, reflecting higher spending earlier in the year in response to the uncertain political and security situation (August 2006, Economic policy).

State budget, Jan-Aug (cumulative; Som m unless otherwise indicated)

2005 2006 % change, year on yearTotal revenue & grants 12,341 15,202 23.2Total revenue 12,341 15,002 21.6 Current revenue 12,306 14,967 21.6 Tax revenue 10,143 12,206 20.3 Income tax 1,107 1,147 3.6 Profit tax 839 810 -3.5 Value-added tax 4,271 5,474 28.2 Excise taxes 771 760 -1.4 Customs revenue 915 1,614 76.5 Non-tax revenue 2,163 2,762 27.7 Capital revenue 35 35 -1.9Grants 0 200 �

Kyrgyz Republic 17

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

State budget, Jan-Aug (cumulative; Som m unless otherwise indicated)

2005 2006 % change, year on yearExpenditure 11,960 14,542 21.6Administration, defence & internal security 3,608 3,963 9.9Education 2,871 3,625 26.3Healthcare 1,309 1,579 20.7Social insurance & security 1,825 2,210 21.1Housing & public utilities 662 883 33.5Leisure, cultural & religious activities 345 408 18.3Subsidies to economic sectors 1,001 1,275 27.3Budget balance 381 660 �Internal financing -21 505 �External financing 108 -102 �

Source: National Statistical Committee.

The draft budget for 2007 is currently being considered by the Jogorku Kenesh (parliament). The budget is premised on real GDP growth of 5.5%"taking nominal GDP to a planned Som122.2bn (US$3bn)"and on year-end inflation of 5%. The central budget targets revenue of Som22.9bn and expenditure of Som28.8bn. The expenditure figure includes grants pertaining to the state investment programme; when these are excluded, the central budget targets a deficit of Som4.1bn, equivalent to 3.3% of planned 2007 GDP. The consolidated budget targets a deficit of 2.8% of GDP, with both revenue and expenditure to increase by just over 12% in nominal terms.

The bulk of the planned increase in revenue to the state budget is to come from higher tax receipts. Tax revenue, at Som20.5bn, is projected to provide 80% of total state budget revenue. Overall state budget revenue is set to increase by 12% compared with the 2006 budget. Tax receipts, rising by a planned 16%, will drive much of the increase; non-tax revenue, by contrast, is set to expand by only 4%. This trend is even more marked with regard to the central budget, where tax revenue is targeted to rise by 21.5% and non-tax revenue by only 2%. However, the headline rates of growth for tax revenue mask divergent trends between direct and indirect taxation. Indirect taxation is set to continue to make a more significant contribution to the overall tax take. For example, revenue from VAT, when measured as a proportion of total tax revenue to the state budget, is targeted to increase to 48%, a rise of more than 1 percentage point in comparison with the 2006 budget plan, and of almost 5 percentage points compared with the 2005 budget outturn. A similar pattern emerges when VAT revenue is measured against GDP, with the VAT take set to rise from 7.1% of GDP in 2005 to 8% of GDP in the 2007 budget. Customs revenue follows the same trend, rising from just over 9% of total tax revenue in the 2006 budget to almost 12% in the 2007 plan, and from 1.5% to 2% of GDP over the same period.

This is in marked contrast to the trajectory for income and profit tax, revenue from which is planned to fall on both measures. From almost 11% of the total tax take in 2005, income tax is set to fall to just over 9% in 2007; the share of profit tax in the total similarly declines by over 2 percentage points. Income tax revenue is set to grow by just over 5%, similar to its performance so far in 2006, although much slower than the 20% increase registered in 2005. Part of

Draft budget for 2007 is before parliament

Revenue increase in 2007 is to be driven by tax revenue

18 Kyrgyz Republic

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

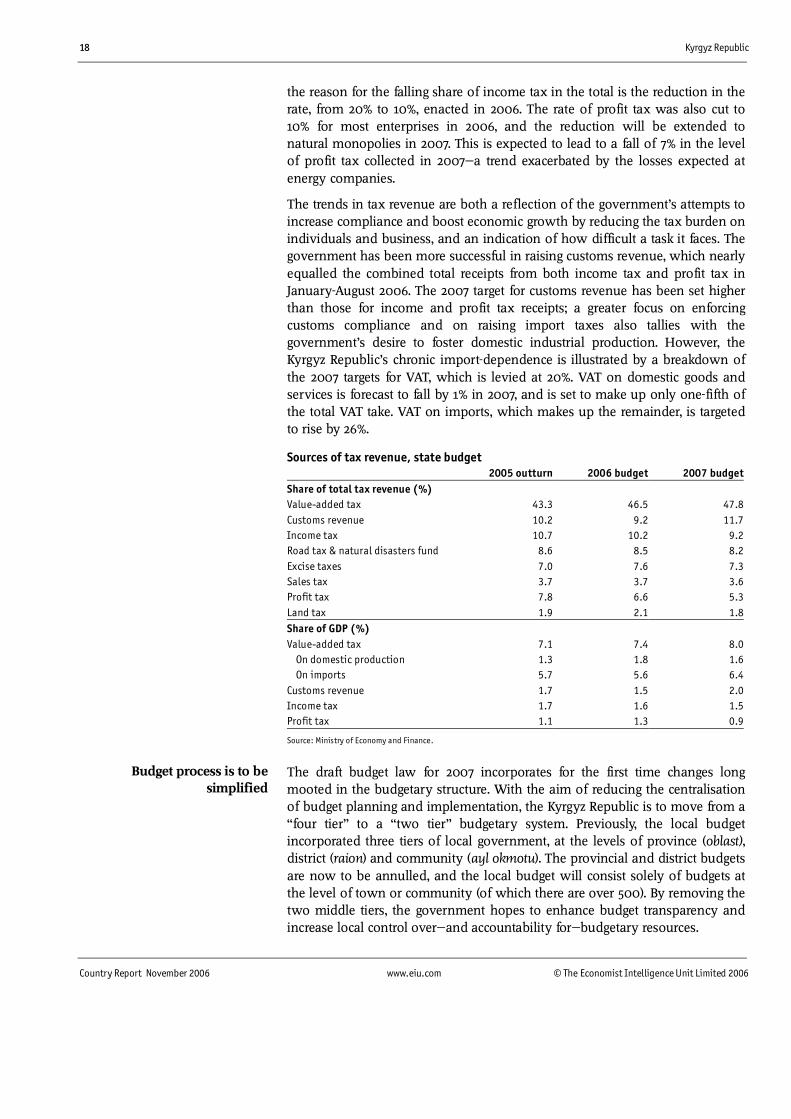

the reason for the falling share of income tax in the total is the reduction in the rate, from 20% to 10%, enacted in 2006. The rate of profit tax was also cut to 10% for most enterprises in 2006, and the reduction will be extended to natural monopolies in 2007. This is expected to lead to a fall of 7% in the level of profit tax collected in 2007"a trend exacerbated by the losses expected at energy companies.

The trends in tax revenue are both a reflection of the government�s attempts to increase compliance and boost economic growth by reducing the tax burden on individuals and business, and an indication of how difficult a task it faces. The government has been more successful in raising customs revenue, which nearly equalled the combined total receipts from both income tax and profit tax in January-August 2006. The 2007 target for customs revenue has been set higher than those for income and profit tax receipts; a greater focus on enforcing customs compliance and on raising import taxes also tallies with the government�s desire to foster domestic industrial production. However, the Kyrgyz Republic�s chronic import-dependence is illustrated by a breakdown of the 2007 targets for VAT, which is levied at 20%. VAT on domestic goods and services is forecast to fall by 1% in 2007, and is set to make up only one-fifth of the total VAT take. VAT on imports, which makes up the remainder, is targeted to rise by 26%.

Sources of tax revenue, state budget 2005 outturn 2006 budget 2007 budgetShare of total tax revenue (%) Value-added tax 43.3 46.5 47.8Customs revenue 10.2 9.2 11.7Income tax 10.7 10.2 9.2Road tax & natural disasters fund 8.6 8.5 8.2Excise taxes 7.0 7.6 7.3Sales tax 3.7 3.7 3.6Profit tax 7.8 6.6 5.3Land tax 1.9 2.1 1.8Share of GDP (%) Value-added tax 7.1 7.4 8.0 On domestic production 1.3 1.8 1.6 On imports 5.7 5.6 6.4Customs revenue 1.7 1.5 2.0Income tax 1.7 1.6 1.5Profit tax 1.1 1.3 0.9

Source: Ministry of Economy and Finance.

The draft budget law for 2007 incorporates for the first time changes long mooted in the budgetary structure. With the aim of reducing the centralisation of budget planning and implementation, the Kyrgyz Republic is to move from a �four tier� to a �two tier� budgetary system. Previously, the local budget incorporated three tiers of local government, at the levels of province (oblast), district (raion) and community (ayl okmotu). The provincial and district budgets are now to be annulled, and the local budget will consist solely of budgets at the level of town or community (of which there are over 500). By removing the two middle tiers, the government hopes to enhance budget transparency and increase local control over"and accountability for"budgetary resources.

Budget process is to be simplified

Kyrgyz Republic 19

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

In particular, the government hopes that the move will introduce more stable and predictable revenue sources for local government, and encourage greater efforts to broaden the tax base on the part of local authorities. To this end, it has specified a number of taxes that will accrue directly to local budgets, including the retail sales tax, the land tax (the rate of which is to be increased for non-agricultural land), a new property tax, the transport tax, and local taxes and levies. Excise taxes on domestic production will go entirely to the central budget, as will revenue from profit tax and tax on non-residents. Previously, these taxes had been shared, with 65% accruing to the central budget and 35% to local budgets. The government has justified its retention of the proceeds of profit tax by the fact that, aside from the difficulties inherent in predicting its level, which complicates budgetary planning, over 90% of the take on profit tax stems from activity in the capital, Bishkek, and in the surrounding Chui province. Local governments also have little influence over the levels of revenue accruing from excise tax on domestic production, given the state monopoly on alcohol production and vagaries arising from smuggling.

The government has also outlined its privatisation strategy for the next year. It still intends to privatise the Kyrgyz Agricultural Finance Corporation (KSFK; August 2006, Economic policy) by the end of 2006. Over the next year it also plans to set up a freight air carrier on the back of the struggling Altyn Air, which belongs to gold producer Kyrgyzaltyn, and to sell the state�s stake in Kyrgyztelecom by tender (May 2006, Economic policy). There are likely also to be further structural reforms in the electricity sector, with a reorganisation of power distributors on the agenda, followed by the possible privatisation of them, or at least the granting of concessions to outside investors.

Following the unification of electricity tariffs for domestic users earlier in 2006, the government has revealed its plans to push ahead with an overhaul of the tariff system. Towards the end of 2006 it will publish a medium-term electricity tariff policy for 2006-10, which will simplify tariff structures further, reduce the number of categories of power users, and attempt to reduce losses in the distribution system by forcing larger industrial enterprises to sign direct contracts with power generators rather than distributors. The government plans to introduce the new tariff structure in mid-2007; it hopes to bring the average tariff up to cost-recovery levels"estimated at 2.3 US cents/kwh, compared with the current average tariff of 1.45 US cents/kwh"by 2009.

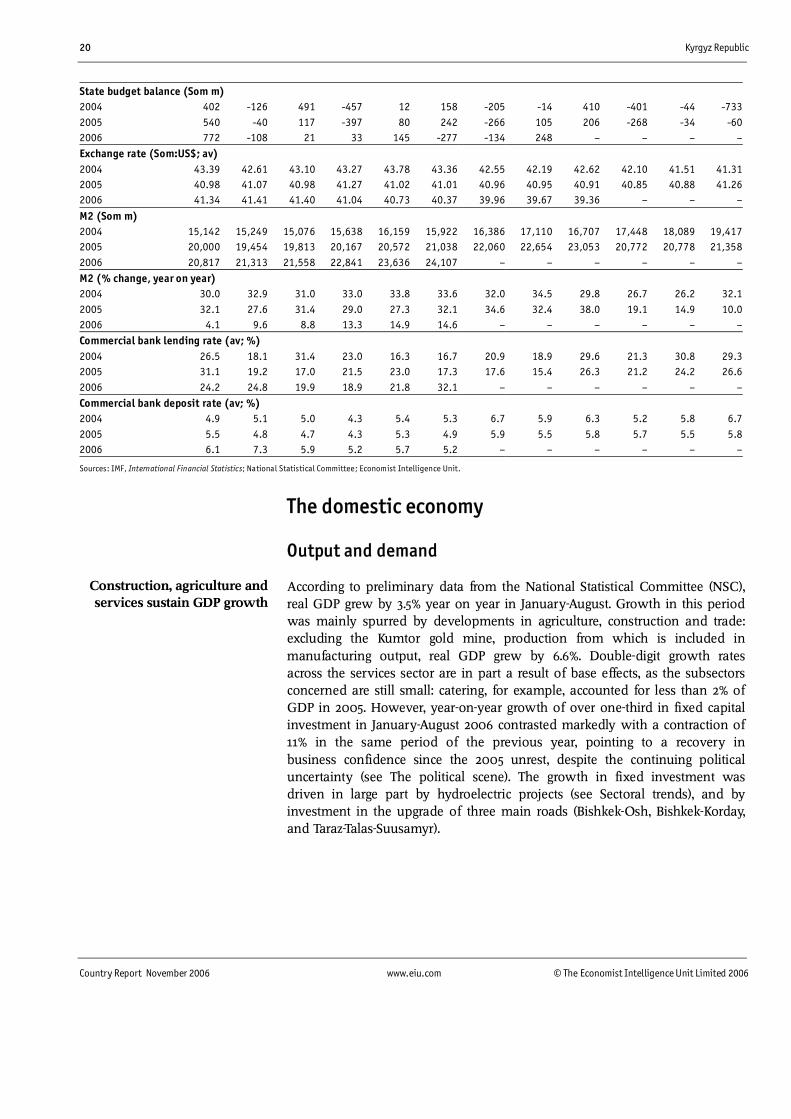

Main economic policy indicators Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecState budget revenue (Som m) 2004 1,003 1,121 1,644 1,545 1,335 1,541 1,428 1,393 1,739 1,735 1,641 2,2112005 1,376 1,462 1,374 1,653 1,672 1,569 1,562 1,673 1,770 2,025 1,901 2,3322006 1,550 1,526 1,785 2,170 1,944 1,970 1,954 2,300 � � � �State budget expenditure (Som m) 2004 601 1,247 1,154 2,002 1,323 1,383 1,632 1,408 1,329 2,136 1,685 2,9442005 837 1,502 1,257 2,050 1,591 1,328 1,828 1,568 1,564 2,293 1,935 2,3922006 778 1,634 1,764 2,137 1,800 2,247 2,088 2,052 � � � �

Further power sector reform is on the agenda

20 Kyrgyz Republic

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

State budget balance (Som m) 2004 402 -126 491 -457 12 158 -205 -14 410 -401 -44 -7332005 540 -40 117 -397 80 242 -266 105 206 -268 -34 -602006 772 -108 21 33 145 -277 -134 248 � � � �Exchange rate (Som:US$; av) 2004 43.39 42.61 43.10 43.27 43.78 43.36 42.55 42.19 42.62 42.10 41.51 41.312005 40.98 41.07 40.98 41.27 41.02 41.01 40.96 40.95 40.91 40.85 40.88 41.262006 41.34 41.41 41.40 41.04 40.73 40.37 39.96 39.67 39.36 � � �

M2 (Som m) 2004 15,142 15,249 15,076 15,638 16,159 15,922 16,386 17,110 16,707 17,448 18,089 19,4172005 20,000 19,454 19,813 20,167 20,572 21,038 22,060 22,654 23,053 20,772 20,778 21,3582006 20,817 21,313 21,558 22,841 23,636 24,107 � � � � � �M2 (% change, year on year) 2004 30.0 32.9 31.0 33.0 33.8 33.6 32.0 34.5 29.8 26.7 26.2 32.12005 32.1 27.6 31.4 29.0 27.3 32.1 34.6 32.4 38.0 19.1 14.9 10.02006 4.1 9.6 8.8 13.3 14.9 14.6 � � � � � �Commercial bank lending rate (av; %) 2004 26.5 18.1 31.4 23.0 16.3 16.7 20.9 18.9 29.6 21.3 30.8 29.32005 31.1 19.2 17.0 21.5 23.0 17.3 17.6 15.4 26.3 21.2 24.2 26.62006 24.2 24.8 19.9 18.9 21.8 32.1 � � � � � �Commercial bank deposit rate (av; %) 2004 4.9 5.1 5.0 4.3 5.4 5.3 6.7 5.9 6.3 5.2 5.8 6.72005 5.5 4.8 4.7 4.3 5.3 4.9 5.9 5.5 5.8 5.7 5.5 5.82006 6.1 7.3 5.9 5.2 5.7 5.2 � � � � � �

Sources: IMF, International Financial Statistics; National Statistical Committee; Economist Intelligence Unit.

The domestic economy

Output and demand

According to preliminary data from the National Statistical Committee (NSC), real GDP grew by 3.5% year on year in January-August. Growth in this period was mainly spurred by developments in agriculture, construction and trade: excluding the Kumtor gold mine, production from which is included in manufacturing output, real GDP grew by 6.6%. Double-digit growth rates across the services sector are in part a result of base effects, as the subsectors concerned are still small: catering, for example, accounted for less than 2% of GDP in 2005. However, year-on-year growth of over one-third in fixed capital investment in January-August 2006 contrasted markedly with a contraction of 11% in the same period of the previous year, pointing to a recovery in business confidence since the 2005 unrest, despite the continuing political uncertainty (see The political scene). The growth in fixed investment was driven in large part by hydroelectric projects (see Sectoral trends), and by investment in the upgrade of three main roads (Bishkek-Osh, Bishkek-Korday, and Taraz-Talas-Suusamyr).

Construction, agriculture and services sustain GDP growth

Kyrgyz Republic 21

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Basic data, Jan-Aug (% change, year on year)

2005 2006Agriculture -1.2 2.8Industrial production -7.8 -9.6 Excl Kumtor production 2.0 9.0Fixed capital investment -10.9 35.9 Construction -4.2 29.4

Trade & repairs 16.5 15.5 Retail trade 5.8 15.0Catering 9.6 19.0

Memorandum items GDP 0.1 3.5 Excl Kumtor production 2.4 6.6

Source: National Statistical Committee.

According to the World Bank�s Doing Business 2007, released in September, the Kyrgyz Republic is a more attractive place for doing business than countries such as Russia, China and Turkey. Nevertheless, substantial concerns remain about the Kyrgyz business environment. The results of a survey carried out by the International Business Council (IBC), a Kyrgyz business association comprising 54 enterprises from 15 different sectors, also showed an improve-ment in business confidence since the March 2005 riots. Although the respondents still scored the investment climate as negative overall, they considered the situation to be much better than in September 2005, and were more positive about the outlook than in any IBC survey since September 2004. Investors! main concerns, as expressed in the survey, were the tax environ-ment"against the backdrop of planned changes to the tax code (see Economic policy)"and the shortage of qualified personnel.

This last concern was aggravated by the announcement in early September of new regulations on foreign citizens and individuals without citizenship working in the Kyrgyz Republic. According to the regulations, individual foreign entrepreneurs will be allowed to stay in the Kyrgyz Republic for no longer than three years, and employment in the country will be limited for foreign workers, depending on their qualifications; the maximum term will be two years, applicable to qualified specialists. At the expiration of the relevant period, the foreign worker is to be replaced with a Kyrgyz counterpart"who, in theory, is to have received the necessary work experience for the job. The regulations have onerous implications for businesses, especially as they seem to bear the burden of training the local replacements.

Investors have also been made uneasy about the level of government protection for private property after Jerooyaltyn, a joint venture between the Austrian-registered Global Gold Holding and the state-owned gold company Kyrgyzaltyn, in September forcibly took control of the Jerooy gold deposit from the Talas Gold Mining Company, formerly a joint-venture between Oxus Gold (UK) and Kyrgyzaltyn. In July Jerooyaltyn received the licence to develop the deposit"a licence that had earlier been taken from Oxus�s subsidiary Norox

Business sentiment improves, but concerns remain

Investors are unsure about the safety of property rights

22 Kyrgyz Republic

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

(May 2006, The domestic economy; August 2006, The domestic economy: Sectoral trends).

The government!s disputes with Oxus and with another foreign company, Central Asia Gold Limited (Australia), have marked a change in the Kyrgyz business environment. Overall investor interest does not appear to have diminished as a result of these conflicts, but there has been a shift in the origins of foreign direct investment (FDI), as there are currently more Russian and Kazakh companies interested in the country than there are from Europe or the US. This in part seems to reflect the Kyrgyz Republic!s new foreign policy preferences, away from the West and towards of Russia. However, investors from the Commonwealth of Independent States (CIS) are not completely free from harassment. In September the Kazakh minister of energy and mineral resources, Baktykozha Izmukhambetov, said that a lack of protection for Kazakh businesses by the Kyrgyz government was hindering Kazakh investment in the country. According to Mr Izmukhambetov, Kazakh businessmen suffer from harassment by Kyrgyz officials, and there have also been attempts to seize Kazakh property. Kazakhstan invested US$28m into the Kyrgyz Republic in the first quarter of 2006 and US$163.2m in 2005.

On September 1st the number of people officially registered as unemployed in the Kyrgyz Republic was 74,500, according to the state migration and employment committee. However, preliminary data from a survey by the NSC published in September indicated that 300,000 people consider themselves to be unemployed. Given that the official unemployment rate, based on registered unemployment, was reported at 3.5% on September 1st"implying an econ-omically active population of around 2m people"the Economist Intelligence Unit estimates the real unemployment rate at around 14%. An assessment of the labour situation in the Kyrgyz Republic is complicated by shortcomings in the quality of the data. Official monthly labour data do not seem to capture the full working population, as the number of those employed is reported at just over 510,000"or only around 10% of the population. In its second (June 2006) review under the poverty reduction and growth facility (PRGF), the IMF noted that there are problems in the coverage and classification of employment data. The likelihood is that the official employment data do not adequately capture trends in the private sector.

Another problem that arises in the compilation of labour statistics is the high rate of emigration from the Kyrgyz Republic. In January-July 16,600 Kyrgyz citizens were reported to have emigrated, with only 2,000 returnees. These figures are likely to be conservative; the exact number of labour migrants leaving the country is difficult to estimate because many are leaving unofficially, and the real number of labour migrants is probably far higher.

The secular trend of emigration from the Kyrgyz Republic reflects the higher wages that can be earned elsewhere in the CIS. Monthly official wage data (which exclude wages in small businesses) show that real wages rose, on average, by around 11% year on year in January-July 2006, according to our calculations. In nominal terms, wages increased by an average of nearly 18% year on year in the first seven months. However, this rapid wage growth has

Real unemployment is much higher than the official rate

Wages are rising rapidly, but are low by regional standards

Kyrgyz Republic 23

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

not allowed Kyrgyz incomes to catch up with those in the more prosperous countries in the region, as wages are rising at double-digit rates throughout the CIS.

Seasonal factors helped to bring inflation down in the summer months, with cumulative inflation decelerating from 4.1% for the period between December 2005 and June 2006, to 1.8% in December-August. The main reason for rising inflation in May and June was seasonal, with food costs driving the increase in consumer prices. Some food prices continued to rise sharply in August: the price for sugar, for example, went up by 32%, and for meat, by 9%. Conversely, prices for fruit and vegetables fell by 9%, and for dairy products, by 12%. Inflation went up only modestly in September, by 0.5% month on month"a cumulative rate of 2.5%. In the same month food prices fell back, with only dairy prices posting a notable increase, of 2.7% month on month. The easing price trends in July-September have put the official year-end inflation target of 5.7% within reach.

Monthly inflation(% change, year on year)

Sources: IMF, International Financial Statistics; Economist Intelligence Unit.

-5.0

0.0

5.0

10.0

15.0

20.0

25.0Consumer pricesProducer prices

AugJulJunMayAprMarFebJan06

DecNovOctSepAugJulJunMayAprMarFebJan05

DecNovOctSepAugJul2004

In the third quarter of 2006 the Kyrgyz som continued to strengthen nominally against the US dollar, owing mainly to the weakening of the US dollar on international currency markets, and stood at Som39.47:US$1 on September 1st, compared with Som40.2:US$1 on July 1st. Over the course of January-August 2006 the US dollar weakened by 4.4% against the Kyrgyz som, compared with a 1.6% depreciation in the same period of 2005. Internal factors are also contributing to the strengthening of the Kyrgyz som"namely, the stabilisation of the country�s macroeconomic and political situation, the growth of business activity, and the rising level of remittances sent from abroad by labour migrants. Data from the Russian Central Bank (RCB) show that US$102m in remittances was sent from Russia to the Kyrgyz Republic in the second quarter of 2006, nearly half of the total of US$200m sent in 2005 as a whole, or around 8% of GDP. These figures include only funds sent through money transfers and the Russian postal system; the total figure for 2005 is estimated to have been as high as US$500m"around 20% of GDP.

Slowing inflation makes year-end target achievable

Som continues to strengthen against the US dollar

24 Kyrgyz Republic

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Sectoral trends

Industrial output fell by 9.6% year on year in January-August 2006, signalling a deepening slump in industry: total output fell year on year by 6.8% in January-June and by 8.9% in January-July. Kyrgyz industry is therefore the worst-performing in the Commonwealth of Independent States (CIS) so far this year. By contrast, oil-producing Azerbaijan saw industry grow by 41% year on year in the first eight months of 2006. A poor industrial performance in the first half of the year in the Kyrgyz Republic was aggravated considerably by a pit-wall movement at the Kumtor gold mine in July, which caused a year-on-year output contraction of 47% in the metals sector and resulted in an overall fall in industrial production of nearly 21% that month. The effects of the disruption in the mine were still being strongly felt in August, causing a further fall in industrial production of 16% on the back of a 55% drop in metals output.

Excluding the Kumtor mine, however, the Kyrgyz Republic!s industrial per-formance looks less dire, with non-Kumtor growth in January-August reaching 9% year on year. Given high world prices for sugar, a potentially promising development was the start of production at the new sugar refinery in Ak Suu. The plant had been at a standstill for the past 15 years, but a Kazakh food-processing company, Vita, refurbished the refinery at a cost of US$16m, and inaugurated it in July. The plant delivered its first sugar in August, and already produces 400 tonnes of sugar per day. Vita plans to have completed modernisation of the plant by 2008, investing a further US$65m in the refinery by 2010.

Industrial production, Jan-Aug (% change, year on year)

2005 2006Industrial production -7.8 -9.6 Excl Kumtor production 2.0 9.0 Mininga -19.0 4.3 Manufacturingb -10.1 -12.9 Utilities 2.8 1.9

a Comprises hydrocarbons and other minerals. b Includes gold output.

Source: National Statistical Committee.

The operator of the Kumtor gold mine, Centerra Gold (Canada), reported in September that the July pit-wall movement at the mine (August 2006, The domestic economy: Sectoral trends) will continue to dampen production in 2007. The company revised downwards its output target for 2007, from 533,000 troy oz to 440,000-475,000 troy oz, having earlier amended the production estimate for 2006 from 410,000-420,000 troy oz to 300,000 troy oz. The firm hopes to recover the production lost in 2006 and 2007 in subsequent years.

The accident at Kumtor had an adverse effect on output reported by the state-owned Kyrgyzaltyn, which is a shareholder in Centerra Gold and buys gold from the Kumtor deposit. In July 2006 the company produced gold bars worth Som504m (US$12.6m), compared with a targeted Som677.4m. This brought Kyrgyzaltyn!s January-July output to a total of Som5.61bn (US$140.25m). The

Industrial output contracts by nearly 10% year on year

Kumtor gold projection for 2007 revised downwards

Kyrgyz Republic 25

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

accident at Kumtor also led to a 37% contraction in gold export volumes in January-July 2006, causing a fall of 13% in earnings from sales of gold abroad.

In order for gold mining to remain an important sector, the Kyrgyz Republic needs to diversify production away from Kumtor, as the deposit is nearing the end of its life-span. However, the first deputy prime minister, Daniyar Usenov, said in September that only three gold deposits"out of a total of 158 in the country"are currently in exploitation. The government is looking for investors for all the other deposits.

Aside from possessing substantial gold deposits, the Kyrgyz Republic is rich in other rare metals, such as tungsten and molybdenum. In August 2006 Centrasia (Canada) agreed to acquire a 100% stake in the Turgeldy tungsten deposit from another Canadian-based company, Eurasian Minerals. Centrasia started to develop the deposit"located in the Tien Shan mountains in the south, some 110 km from the Kumtor mine"in September.

Another subsector that the government is hoping to revive is uranium-processing. The Kyrgyz Republic!s uranium deposits made it an important part of the Soviet Union!s nuclear industry, and a large complex for mining and milling uranium was built at Kara-Balta to process both local and Kazakh uranium concentrate ("yellowcake"). The Kyrgyz Republic has since exhausted its own uranium resources, and the government hopes to sell its stake of 72.28% in the Kara-Balta Ore Mining Combine.

With no local uranium resources, the combine!s main activity is to process uranium mined in Kazakhstan, and the government hopes that Kazakh investors will acquire the company. However, two tenders for it failed in quick succession when no applications for participation were received by either of the specified deadlines. The first two attempts to sell the complex failed because the government did not agree with investors� demands to secure a source of uranium for the plant; the complex had stopped activities in 2005 because of exhaustion of domestic deposits.

Kyrgyzgas announced in August that the price of gas imports from Uzbekistan will increase sharply as of January 2007, to approximately US$100 per 1,000 cu metres of natural gas. Currently, the country purchases Uzbek gas at around US$55 per 1,000 cu metres. The increase reflects rising prices for gas within the CIS, and Uzbekistan is following the example of Russia and Turkmenistan, both of which have negotiated higher prices with gas purchasers in 2006. The exact price that the Kyrgyz Republic will have to pay is to be negotiated in the fourth quarter of 2006. Higher gas prices are likely to widen further the Kyrgyz Republic�s already large trade deficit.

Meanwhile, Gazprom Neft Asia"a 100% subsidiary company of Russia�s Gazprom Neft based in the Kyrgyz capital, Bishkek"started operating in August in the Kyrgyz Republic!s wholesale and retail markets for oil products (petrol and diesel fuel), as well as in its liquefied gas market.

Agricultural output grew by 2.8% year on year in January-August 2006, reaching Som39.5bn (US$988m). Crop production accounted for nearly one-half of total

Government seeks investment in other metals sectors

Price for Uzbek gas to rise steeply

Agricultural output growing despite concerns over wheat

26 Kyrgyz Republic

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

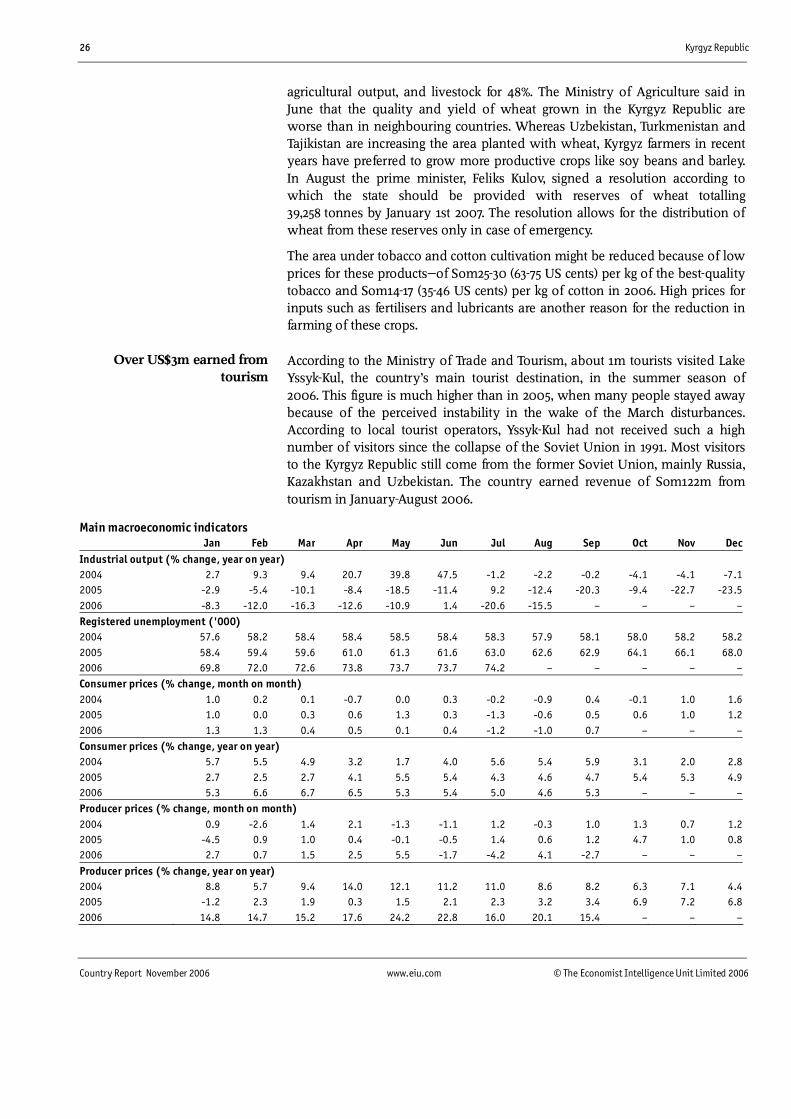

agricultural output, and livestock for 48%. The Ministry of Agriculture said in June that the quality and yield of wheat grown in the Kyrgyz Republic are worse than in neighbouring countries. Whereas Uzbekistan, Turkmenistan and Tajikistan are increasing the area planted with wheat, Kyrgyz farmers in recent years have preferred to grow more productive crops like soy beans and barley. In August the prime minister, Feliks Kulov, signed a resolution according to which the state should be provided with reserves of wheat totalling 39,258 tonnes by January 1st 2007. The resolution allows for the distribution of wheat from these reserves only in case of emergency.

The area under tobacco and cotton cultivation might be reduced because of low prices for these products"of Som25-30 (63-75 US cents) per kg of the best-quality tobacco and Som14-17 (35-46 US cents) per kg of cotton in 2006. High prices for inputs such as fertilisers and lubricants are another reason for the reduction in farming of these crops.

According to the Ministry of Trade and Tourism, about 1m tourists visited Lake Yssyk-Kul, the country�s main tourist destination, in the summer season of 2006. This figure is much higher than in 2005, when many people stayed away because of the perceived instability in the wake of the March disturbances. According to local tourist operators, Yssyk-Kul had not received such a high number of visitors since the collapse of the Soviet Union in 1991. Most visitors to the Kyrgyz Republic still come from the former Soviet Union, mainly Russia, Kazakhstan and Uzbekistan. The country earned revenue of Som122m from tourism in January-August 2006.

Main macroeconomic indicators Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecIndustrial output (% change, year on year) 2004 2.7 9.3 9.4 20.7 39.8 47.5 -1.2 -2.2 -0.2 -4.1 -4.1 -7.12005 -2.9 -5.4 -10.1 -8.4 -18.5 -11.4 9.2 -12.4 -20.3 -9.4 -22.7 -23.52006 -8.3 -12.0 -16.3 -12.6 -10.9 1.4 -20.6 -15.5 � � � �Registered unemployment ('000) 2004 57.6 58.2 58.4 58.4 58.5 58.4 58.3 57.9 58.1 58.0 58.2 58.22005 58.4 59.4 59.6 61.0 61.3 61.6 63.0 62.6 62.9 64.1 66.1 68.02006 69.8 72.0 72.6 73.8 73.7 73.7 74.2 � � � � �Consumer prices (% change, month on month) 2004 1.0 0.2 0.1 -0.7 0.0 0.3 -0.2 -0.9 0.4 -0.1 1.0 1.62005 1.0 0.0 0.3 0.6 1.3 0.3 -1.3 -0.6 0.5 0.6 1.0 1.22006 1.3 1.3 0.4 0.5 0.1 0.4 -1.2 -1.0 0.7 � � �Consumer prices (% change, year on year) 2004 5.7 5.5 4.9 3.2 1.7 4.0 5.6 5.4 5.9 3.1 2.0 2.82005 2.7 2.5 2.7 4.1 5.5 5.4 4.3 4.6 4.7 5.4 5.3 4.92006 5.3 6.6 6.7 6.5 5.3 5.4 5.0 4.6 5.3 � � �Producer prices (% change, month on month) 2004 0.9 -2.6 1.4 2.1 -1.3 -1.1 1.2 -0.3 1.0 1.3 0.7 1.22005 -4.5 0.9 1.0 0.4 -0.1 -0.5 1.4 0.6 1.2 4.7 1.0 0.82006 2.7 0.7 1.5 2.5 5.5 -1.7 -4.2 4.1 -2.7 � � �

Producer prices (% change, year on year) 2004 8.8 5.7 9.4 14.0 12.1 11.2 11.0 8.6 8.2 6.3 7.1 4.42005 -1.2 2.3 1.9 0.3 1.5 2.1 2.3 3.2 3.4 6.9 7.2 6.82006 14.8 14.7 15.2 17.6 24.2 22.8 16.0 20.1 15.4 � � �

Over US$3m earned from tourism

Kyrgyz Republic 27

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Main macroeconomic indicators Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecAverage gross monthly wagea (Som) 2004 1,872 1,948 2,067 2,050 2,072 2,307 2,249 2,102 2,255 2,211 2,261 3,0352005 2,159 2,208 2,460 2,358 2,442 2,597 2,573 2,556 2,636 2,620 2,648 3,5272006 2,557 2,550 2,869 2,818 2,808 3,107 3,060 � � � � �Average gross monthly wageb (real % change, year on year) 2004 n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a2005 15.4 13.4 19.0 15.1 17.9 12.6 14.4 21.6 16.9 18.5 17.1 16.22006 18.4 15.5 16.6 19.5 15.0 19.7 18.9 � � � � �Average gross monthly wageb (US$) 2004 43.13 45.70 47.96 47.37 47.33 53.19 52.84 49.81 52.91 52.52 54.48 73.472005 52.68 53.76 60.03 57.14 59.54 63.32 62.83 62.42 64.43 64.14 64.77 85.472006 61.85 61.57 69.29 68.68 68.94 76.97 76.56 � � � � �

a Monthly wage data exclude small businesses.

Sources: National Statistical Committee; Interstate Statistical Committee of the Commonwealth of Independent States; Economist Intelligence Unit.

Foreign trade and payments

The Kyrgyz Republic!s foreign trade turnover amounted to US$1.07bn in the first half of 2006, an increase of 32% year on year. Kyrgyz trade turnover with other members of the Commonwealth of Independent States (CIS) grew by 41%, and with other countries by 23%. Russia is the Kyrgyz Republic!s most important trade partner, accounting for over half of total turnover. Kyrgyz trade data are, however, skewed by exports of gold, since, because of the high price of the commodity, gold-trading countries accounting for a large share of exports. The most complete set of disaggregated data available, for January-May, put Switzerland as the Kyrgyz Republic!s largest export destination (accounting for 34% of export receipts), a position occupied by the UAE (33%) in the same period of 2005. If gold exports are excluded, Kazakhstan becomes the Kyrgyz Republic!s second-largest trade partner after Russia, accounting for around 37% of non-gold trade turnover in January-May 2006.

Trade statistics by country, Jan-May

(US$ m)

Exports Imports

Source: Interfax.

0

50

100

150

200

25020062005

South K

orea

US

Ukrain

e

Turk

ey

Germany

Uzbekist

anChin

a

Kazakhst

an

Russia

0

20

40

60

80

100

12020062005

UAE

Turk

ey

Uzbekist

an

Tajik

istan

China

Afghanist

an

Kazakhst

an

Russia

Switzerla

nd

China still accounts for a small share of Kyrgyz foreign trade turnover compared with Russia, but its importance is rising rapidly. Exports to China grew by 36%

Trade turnover reaches US$1bn in January-June 2006

28 Kyrgyz Republic

Country Report November 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006