l6-8: revolutionary changes in economic life: capitalism agenda objective: to understand 1.the main...

TRANSCRIPT

L6-8: Revolutionary Changes in Economic Life: Capitalism

AgendaObjective:To understand1. The main ideas and

principles of capitalism.2. The implications of

capitalism for life in the modern world.

Schedule: 1. Mini-Lesson on Footnotes2. Principles of Capitalism3. Capitalism Discussion

Homework: 1.Consult unit

schedule. No modifications to assignments at this time.

REMINDER: Next Pre-Writing Check Due Mon 9/24

Lesson on Footnotes

Footnotes: Introduction• For ALL of your papers you need to reference

specific ideas/facts/arguments from class discussion and/or course readings.

• These references must be cited – Give credit to your sources.

• The method you will use to cite these references is footnotes.• You will also include a bibliography listing all of the resources you used at the end of the paper. QuickTime™ and a

decompressorare needed to see this picture.

Footnotes: What Are They?• Citations to credit sources.

• Footnotes are indexed within the text using a superscripted numeral that refers to an expanded note presented at the bottom of the text which gives the full citation information for a source.

• Footnotes should go at the end (after the period) of the sentence(s) to which a reference is made.

• Sample…

QuickTime™ and a

decompressorare needed to see this picture.

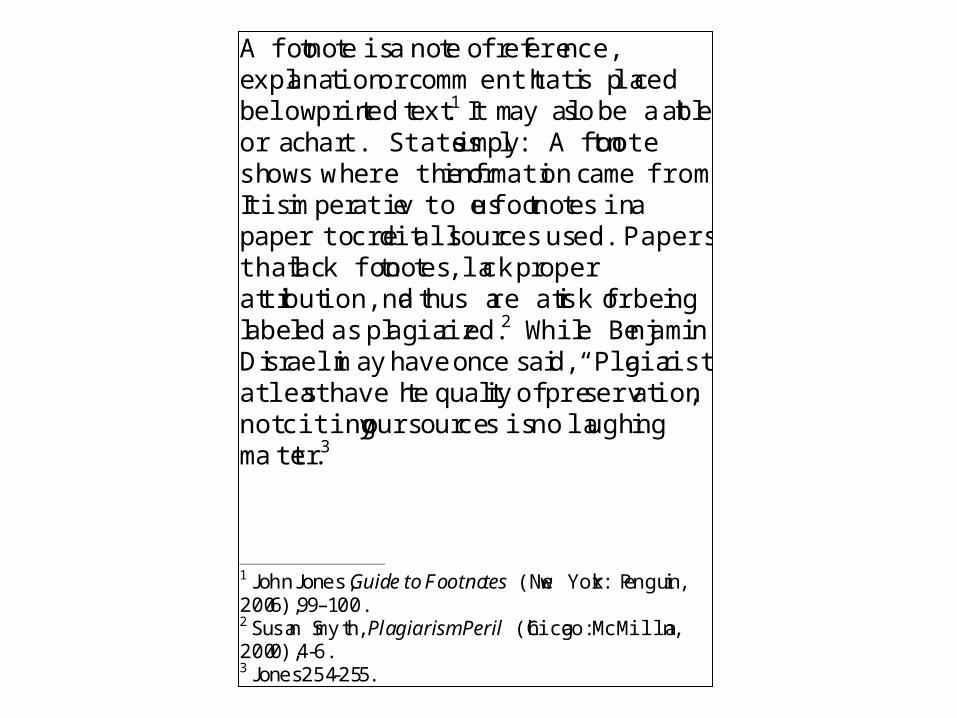

A footnote is a note of reference, explanation or comment that is placed below printed text.1 It may also be a table or a chart. States simply: A footnote shows where the information came from. It is imperative to use footnotes in a paper to credit all sources used. Papers that lack footnotes, lack proper attribution, and thus are at risk for being labeled as plagiarized.2 While Benjamin Disraeli may have once said, “Plagiarists at least have the quality of preservation,” not citing your sources is no laughing matter.3

1 John Jones, Guide to Footnotes (New Yor k: Penguin, 2006), 99–100. 2 Susan Smyth, Plagiarism Peril (Chicago: McMillan, 2000), 4-6. 3 Jones 254-255.

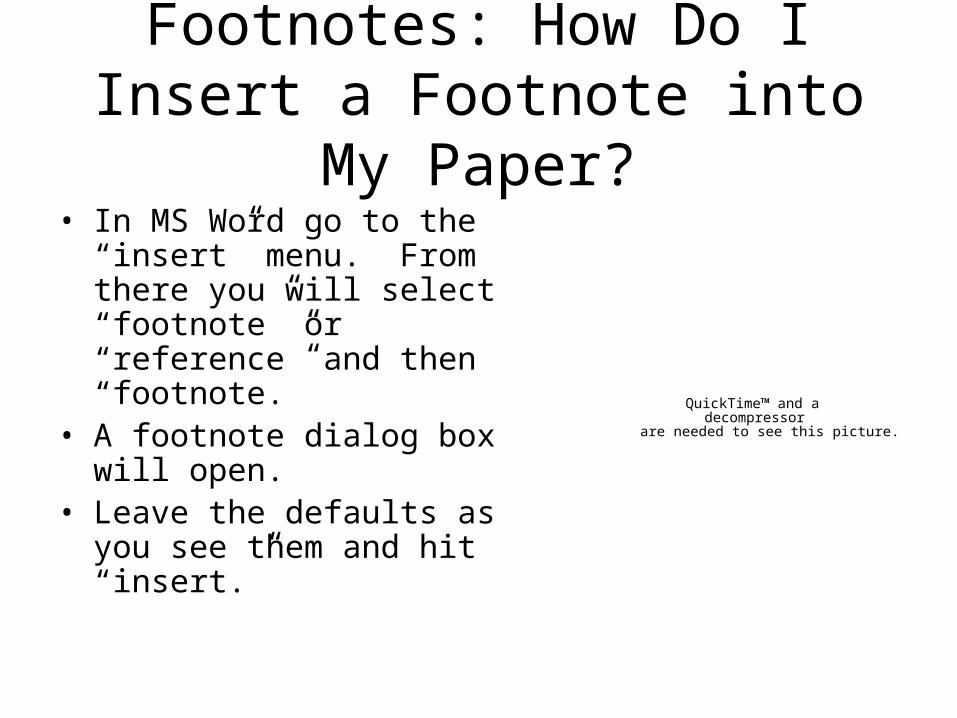

Footnotes: How Do I Insert a Footnote into My Paper?

• In MS Word go to the “insert” menu. From there you will select “footnote” or “reference” and then “footnote.”

• A footnote dialog box will open.

• Leave the defaults as you see them and hit “insert.”

QuickTime™ and a decompressor

are needed to see this picture.

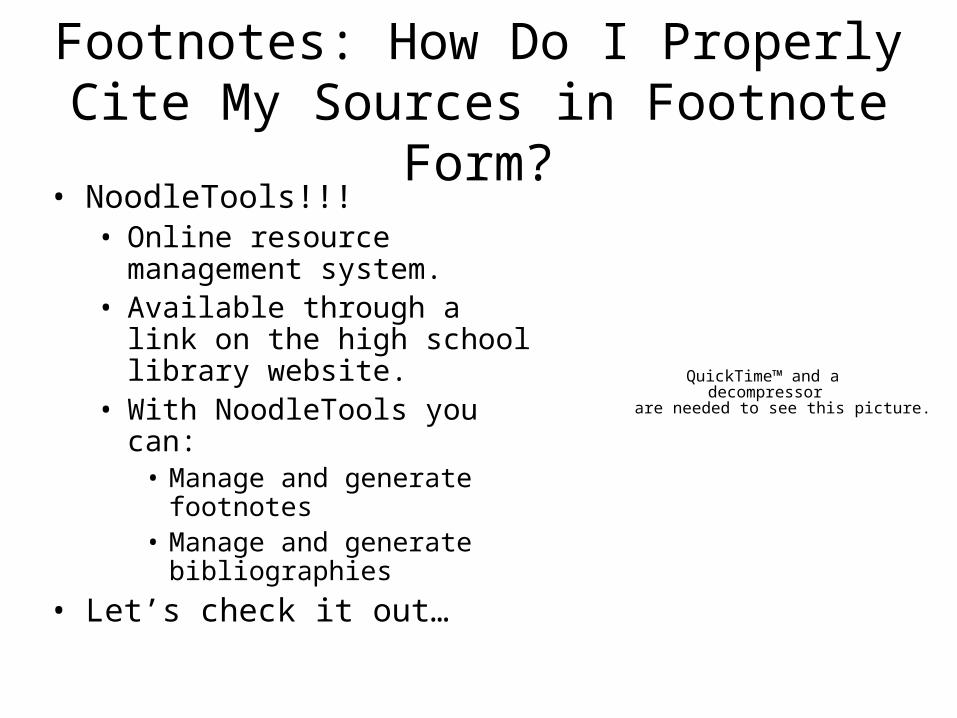

Footnotes: How Do I Properly Cite My Sources in Footnote Form?

• NoodleTools!!!• Online resource

management system.• Available through a link on

the high school library website.

• With NoodleTools you can:• Manage and generate

footnotes• Manage and generate

bibliographies

• Let’s check it out…

QuickTime™ and a decompressor

are needed to see this picture.

The Subject Matter at Hand…

Capitalism

Dual Revolutions Brings Economic Changes

• Just as the Industrial Revolution and French Revolution brought changes to social life, they also brought changes to economic life.

• In particular, the Industrial Revolution, through the development of the factory system, ushered in a new economic system: capitalism.

• Our goals are to study:– The principles of capitalism– The effects of capitalism

QuickTime™ and a decompressor

are needed to see this picture.

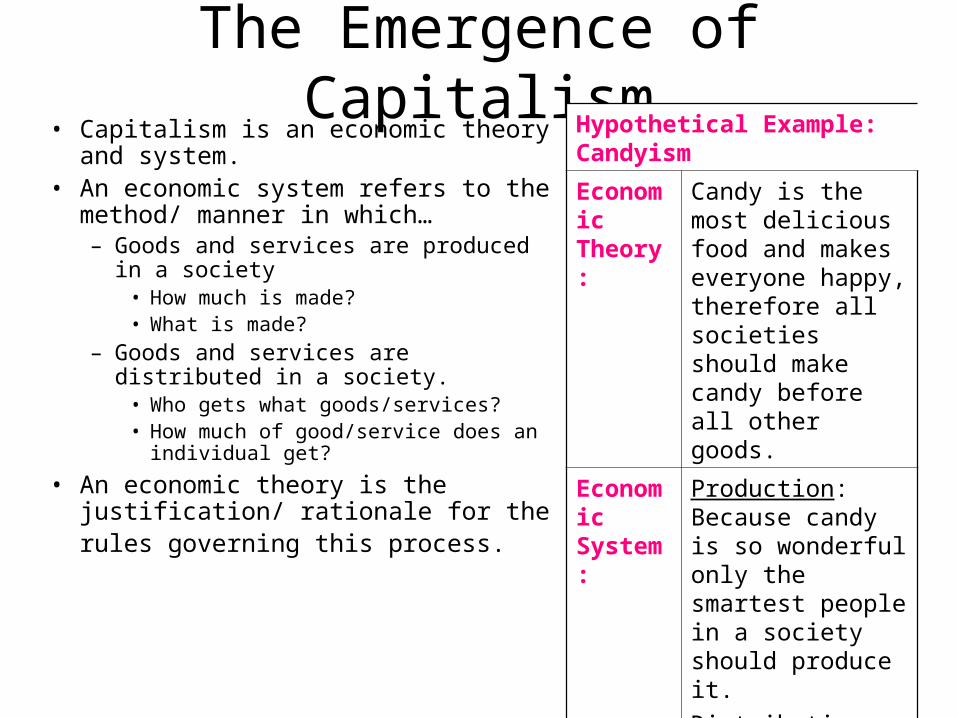

The Emergence of Capitalism

• Capitalism is an economic theory and system.

• An economic system refers to the method/ manner in which… – Goods and services are produced in

a society• How much is made? • What is made?

– Goods and services are distributed in a society.

• Who gets what goods/services?• How much of good/service does an

individual get?

• An economic theory is the justification/ rationale for the rules governing this process.

Hypothetical Example: Candyism

Economic Theory:

Candy is the most delicious food and makes everyone happy, therefore all societies should make candy before all other goods.

Economic System:

Production: Because candy is so wonderful only the smartest people in a society should produce it.Distribution: Everyone should get equal amounts of candy to share in its joy.

At the Beginning of the IR, Europe had a

Mercantilism Economic Theory/System

• Mercantilism is an economic theory that holds that the wealth of a nation is dependent upon how much gold and silver it has. – The more gold or silver a nation has the wealthier it is.

• Therefore, in order to increase the amount of gold and silver it has, nations must pursue a positive balance of trade (exports must be greater than imports) with other nations.

• The state should therefore play an active role in the economy by encouraging exports and discouraging

imports through the use of tariffs and subsidies.

Mercantilist Assumptions• Increasing the stock of gold and silver makes everyone

richer.– If a nation were to increase its stocks of gold and silver, everyone

in the nation would benefit. There would be more gold and silver to go around and everyone would be wealthier.

• Gold and silver have inherent value.• The wealth of the world is fixed.

– Wealth is determined by gold or silver. The amount of gold and silver in the world is finite (we can’t create more) therefore wealth is fixed. Therefore nations need to do all in their power to accumulate as much gold and silver as possible to get the largest share of the pie.

• International trade is a zero-sum game.– If the amount of wealth in the world is fixed, then international

trade is a zero-sum game: In order for Nation A to get richer, Nation B must get poorer. Both nations cannot benefit from a trade agreement.

Flaws in Mercantilist Thinking • Increasing the stock in gold and silver won’t make everyone

richer.– As the supply of gold and silver increased its value would actually decrease

(the more of something you have the less valuable it is). – Moreover, prices would increase (the more money people have the higher

the price you can command for a good). – The result is that everyone would need even more money just to make ends

meet, no one would be getting richer.

• Gold and silver do not have inherent value– These goods are only valuable because:

• We ascribe them value (value is a social construct)• They are scarce

• International trade is not a zero-sum game (Theory of Comparative Advantage, David Ricardo 1817)– Suppose Portugal was a more efficient producer wine rather than cloth, yet

in England it was cheaper to produce cloth compared to wine. If Portugal specialized in wine and England in cloth, both nations would end up better of if they traded. If both nations produce and trade in goods for which they have a comparative advantage, they will both be better off.

Mercantilism is Replaced with Capitalism

• In 1776, Adam Smith develops a new economic theory in his book, The Wealth of Nations: capitalism.

• With the introduction of capitalism Britain would have a theory that would help create an incredibly profitable Industrial Revolution.

Adam Smith• 1720-1790• Scottish philosopher

and economist.• Famous works include:

Theory of Moral Sentiments and An Inquiry into the Nature and Causes of the Wealth of Nations

• Considered the founder of capitalist thought.

QuickTime™ and a decompressor

are needed to see this picture.

Understanding Smith’s Ideas

• Task…– We will read excerpts from Smith’s The

Wealth of Nations and answer a series of questions on the reading to better understand the economic theory of capitalism that Smith lays out in 1776.

Smith Rejects Mercantilism• Smith rejects mercantilism

on the grounds that it allows the government to direct the economy which actually hurts, rather than helps the economy.

• Instead, her proposes that England should adopt his economic system, known as capitalism.

• What is capitalism? (Your definitions)

QuickTime™ and a decompressor

are needed to see this picture.

Capitalism • Definition: an economic system in which:

– Supply, demand, price, and distribution are determined by the invisible hand of the free market in the absence of government intervention;

– The means of production are privately owned;– Goods and services are created for profit which is

retained by the producer.

• Key Ideas:– Private Ownership of the Means of Production – Uneven Distribution of Wealth– Homo Economicus– Invisible Hand– Laissez-Faire

Private Ownership of the Means of Production

• Means of production: physical inputs used in the production process such as tools, machines, factories, money, etc. (The stuff needed to make more stuff.)

• In a capitalist system all of the means of production are owned and controlled privately.– Individuals/businesses own the inputs needed

to produce and dictate their use not the government.

• Not only do individuals/businesses own the means of production, but as a result they have the right to enjoy the economic rewards that result.– Profits are retained by individuals/businesses.– Losses are assumed by individuals/businesses.

• Why do you think Smith advocates private ownership of the means of production?

QuickTime™ and a decompressor

are needed to see this picture.

Wealth is Unevenly Distributed

• If property is privately held, then it is permissible for some individuals to own more or less than others.

• The result is that in capitalist societies wealth is unevenly distributed - some people have more than others.

QuickTime™ and a decompressor

are needed to see this picture.

Homo Economicus• Assumption is that humans are

rational and self-interested actors who have the ability to gather perfect information and make reasoned judgments for themselves about their economic actions.

QuickTime™ and a decompressor

are needed to see this picture.

The Invisible Hand

QuickTime™ and a decompressor

are needed to see this picture.

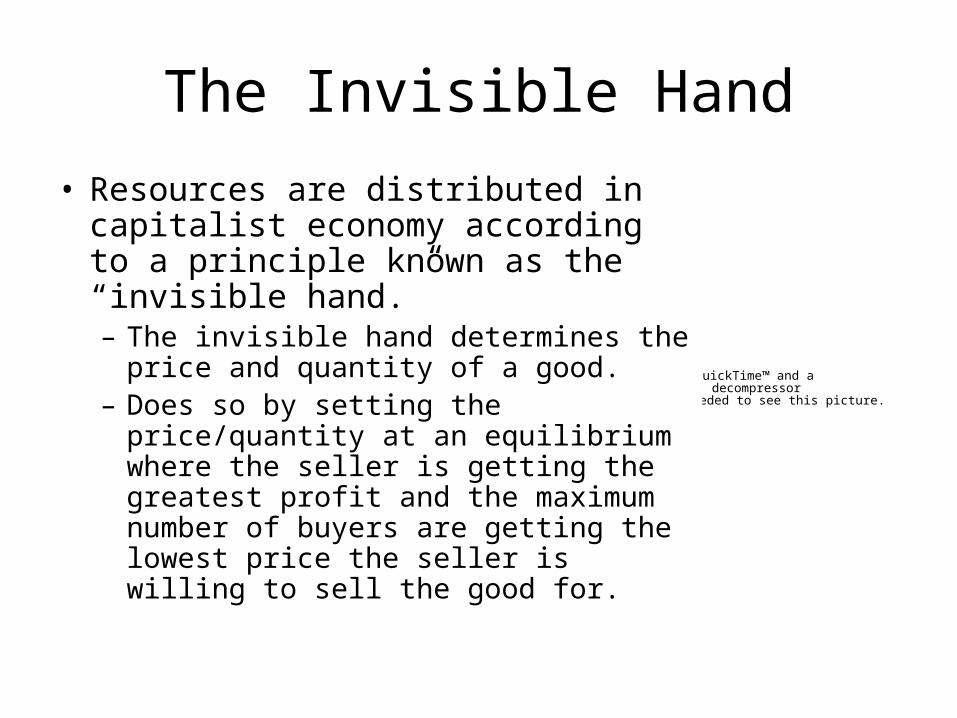

• Resources are distributed in capitalist economy according to a principle known as the “invisible hand.”– The invisible hand determines the

price and quantity of a good.– Does so by setting the

price/quantity at an equilibrium where the seller is getting the greatest profit and the maximum number of buyers are getting the lowest price the seller is willing to sell the good for.

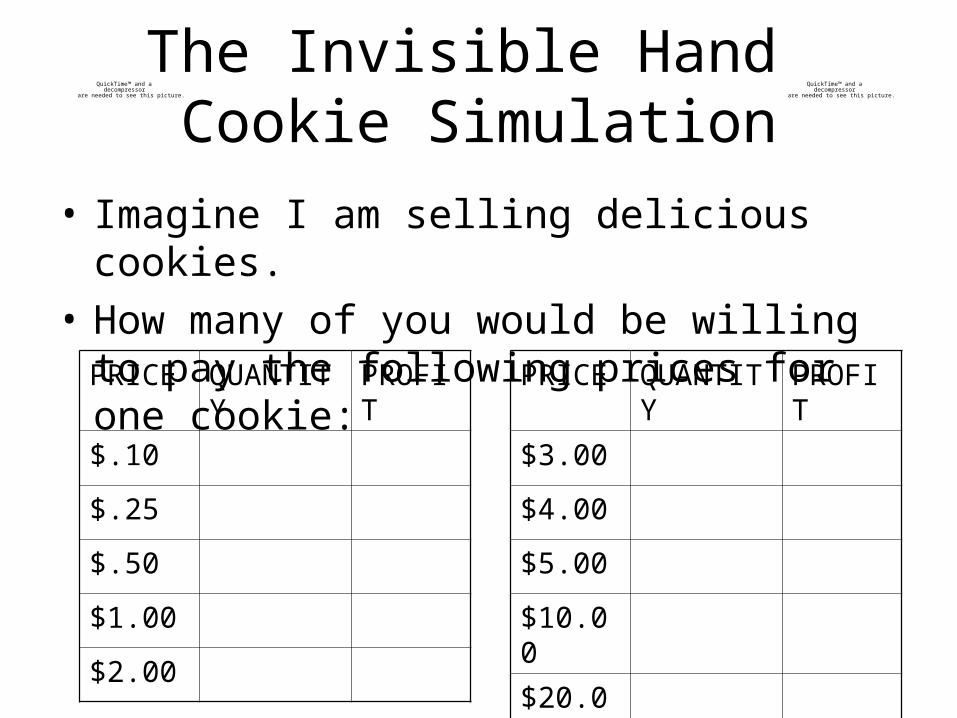

The Invisible Hand Cookie Simulation

• Imagine I am selling delicious cookies. • How many of you would be willing to

pay the following prices for one cookie:PRICE QUANTITY PROFIT

$.10

$.25

$.50

$1.00

$2.00

QuickTime™ and a decompressor

are needed to see this picture.

QuickTime™ and a decompressor

are needed to see this picture.

PRICE QUANTITY PROFIT

$3.00

$4.00

$5.00

$10.00

$20.00

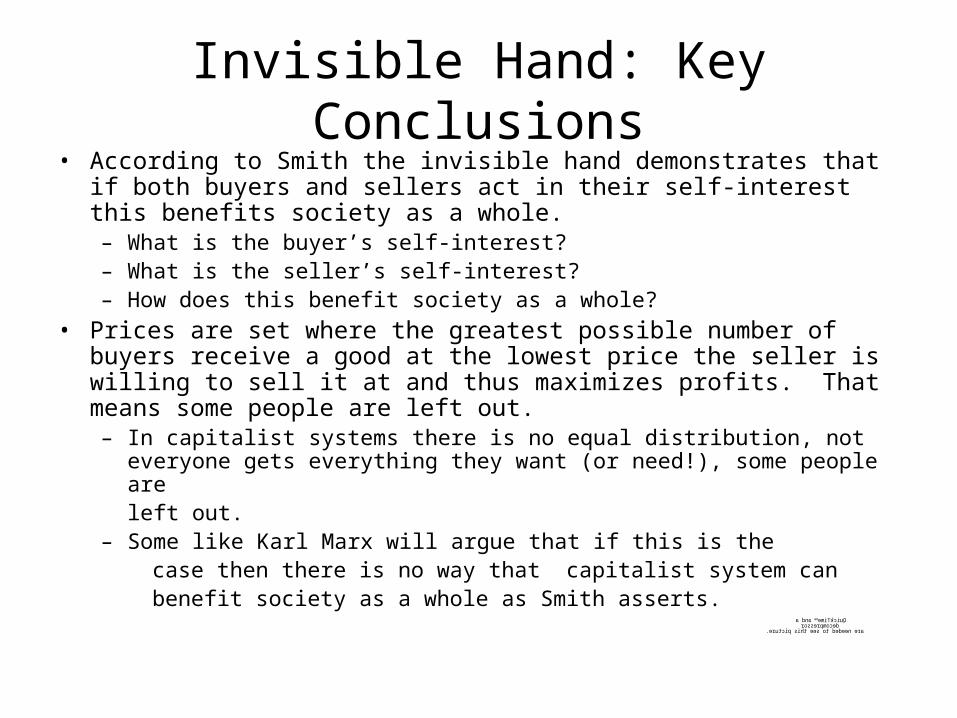

Invisible Hand: Key Conclusions• According to Smith the invisible hand demonstrates that if

both buyers and sellers act in their self-interest this benefits society as a whole.– What is the buyer’s self-interest?– What is the seller’s self-interest?– How does this benefit society as a whole?

• Prices are set where the greatest possible number of buyers receive a good at the lowest price the seller is willing to sell it at and thus maximizes profits. That means some people are left out.– In capitalist systems there is no equal distribution, not everyone

gets everything they want (or need!), some people are left out.

– Some like Karl Marx will argue that if this is the case then there is no way that capitalist system can benefit society as a whole as Smith asserts.

Invisible HandWage Simulation

• The invisible hand not only sets the prices of goods, but also determines wages.

• I live on a 100 acre estate and need at least 10 of you to come over and do yard work.

• How many of you would be willing to work for the following wages:

WAGE/HOUR WORKERS

$1

$5

$10

$25

$50

$100

$150

$200

QuickTime™ and a decompressor

are needed to see this picture.

QuickTime™ and a decompressor

are needed to see this picture.

Laissez-Faire• Because Smith believed that the invisible hand was

the most efficient way to distribute goods he believed that government should not interfere in the market.– Efficiency = (distributed in a way that the

greatest number of buyers get the good for the lowest price the seller is willing to sell while still maximizing profits).

• He argued that if the government got involved in the buying/selling goods or in setting wages it would create distortions in the market that would prevent them from reaching the most efficient equilibrium.

• Laissez-Faire = government stays out of the economy! (Hands off!)

QuickTime™ and a decompressor

are needed to see this picture.

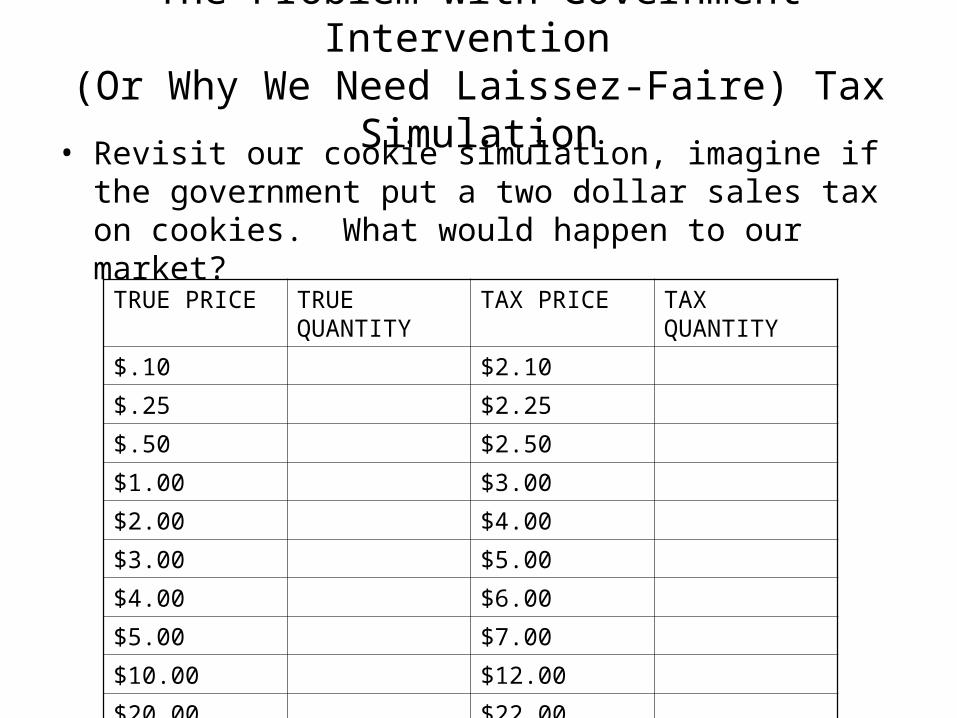

The Problem with Government Intervention (Or Why We Need Laissez-Faire) Tax

Simulation• Revisit our cookie simulation, imagine if the

government put a two dollar sales tax on cookies. What would happen to our market?

TRUE PRICE TRUE QUANTITY TAX PRICE TAX QUANTITY

$.10 $2.10

$.25 $2.25

$.50 $2.50

$1.00 $3.00

$2.00 $4.00

$3.00 $5.00

$4.00 $6.00

$5.00 $7.00

$10.00 $12.00

$20.00 $22.00

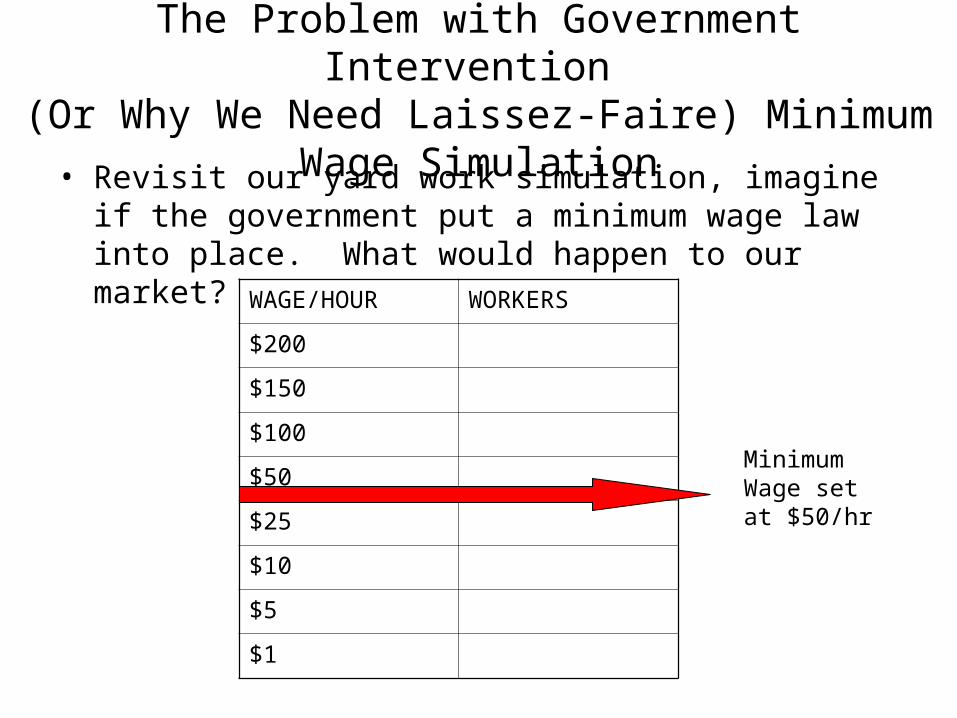

The Problem with Government Intervention (Or Why We Need Laissez-Faire) Minimum

Wage Simulation• Revisit our yard work simulation, imagine if the

government put a minimum wage law into place. What would happen to our market?

WAGE/HOUR WORKERS

$200

$150

$100

$50

$25

$10

$5

$1

Minimum Wage set at $50/hr

Quick Assessment

• Assess your understanding of capitalism by completing the Capitalism Quiz!

• Your responses will not be graded.

Other Capitalist Thinkers

• Writing shortly after Smith were two other capitalist thinkers who offered extensions of Smith’s ideas:– Thomas Malthus

and Malthusian Population Theory

– David Ricardo and the Iron Law of Wages

QuickTime™ and a decompressor

are needed to see this picture.

QuickTime™ and a decompressor

are needed to see this picture.

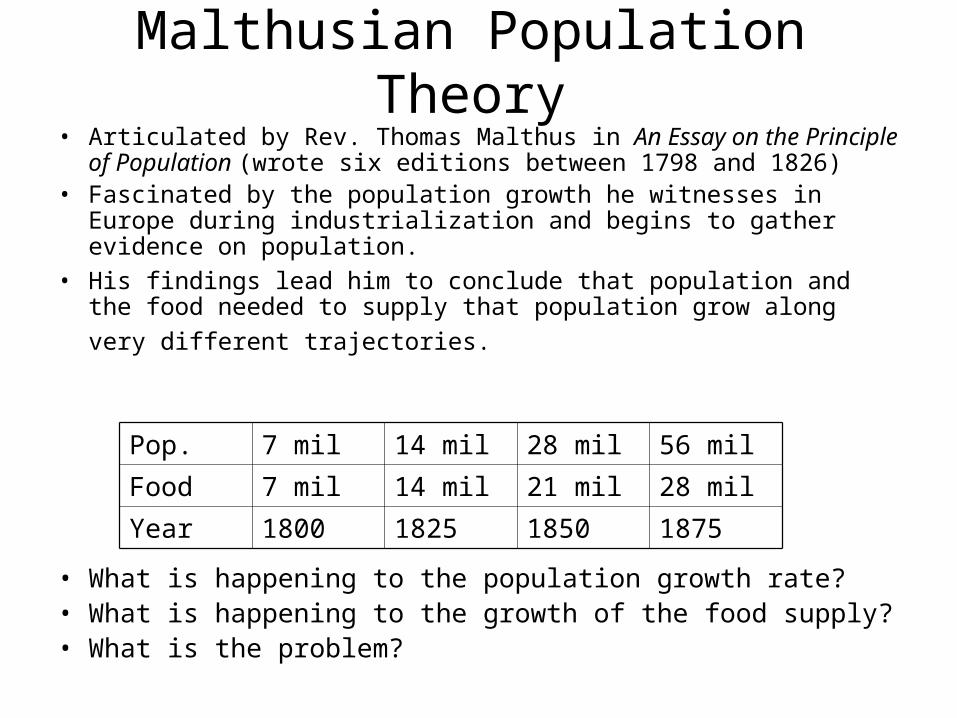

Malthusian Population Theory• Articulated by Rev. Thomas Malthus in An Essay on the

Principle of Population (wrote six editions between 1798 and 1826)

• Fascinated by the population growth he witnesses in Europe during industrialization and begins to gather evidence on population.

• His findings lead him to conclude that population and the food needed to supply that population grow along very different trajectories.

• What is happening to the population growth rate?• What is happening to the growth of the food supply?• What is the problem?

Pop. 7 mil 14 mil 28 mil 56 mil

Food 7 mil 14 mil 21 mil 28 mil

Year 1800 1825 1850 1875

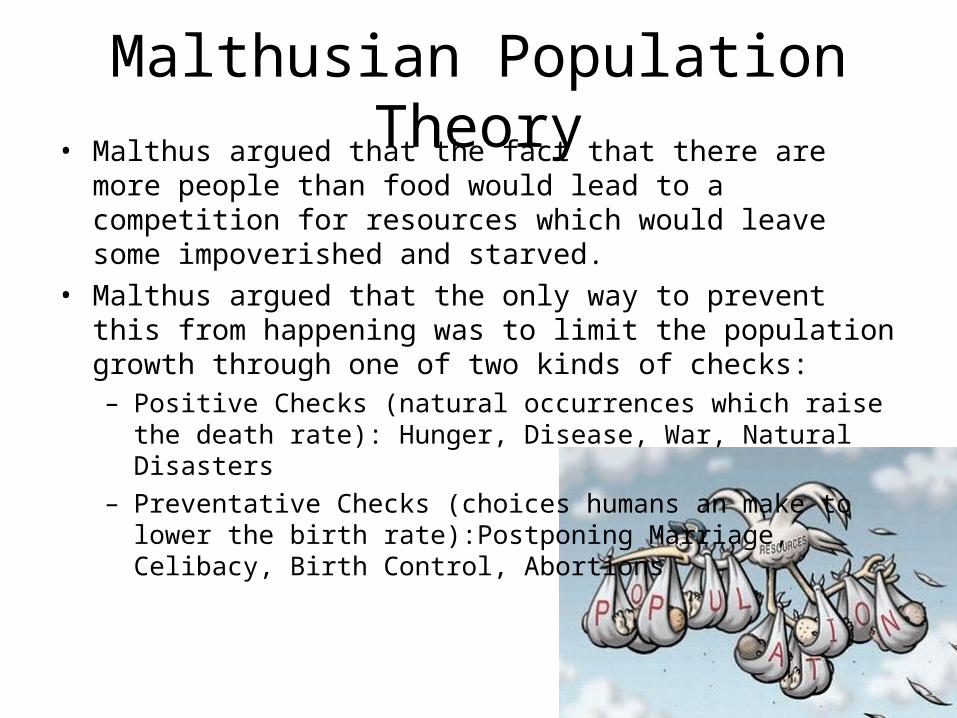

Malthusian Population Theory• Malthus argued that the fact that there are more

people than food would lead to a competition for resources which would leave some impoverished and starved.

• Malthus argued that the only way to prevent this from happening was to limit the population growth through one of two kinds of checks:– Positive Checks (natural occurrences which raise the

death rate): Hunger, Disease, War, Natural Disasters– Preventative Checks (choices humans an make to lower

the birth rate):Postponing Marriage, Celibacy, Birth Control, Abortions

Malthusian Population Theory

• Malthus also argued that in order to limit population growth, poor laws had to be abolished.

• He reasoned that by giving the poor money, homes, and/or jobs all society was doing was facilitating their survival and reproduction.

• Society would be better off if these people died and never reproduced.

QuickTime™ and a decompressor

are needed to see this picture.

Iron Law of Wages• Wage theory articulated by David

Ricardo in The Principles of Political Economy and Taxation (1821)

• Iron Law of Wages: Because of increased population growth the supply of labor will always exceed the demand, thus causing wages to sink to subsistence level.

• Building on Malthus, Ricardo argues that so long as population continues to grow, wages will continue to drop.

• Workers were condemned to low wages and a life of poverty.

• Modern economics rejects the iron law of wages.

QuickTime™ and a decompressor

are needed to see this picture.

Capitalism Discussion1. Is capitalism a utopian idea? Does it try to

achieve a better/ideal society? Do you think it achieves this in practice?

2. What do you see as the strengths/weaknesses of capitalism?

3. Given what you know about the world in the 1700s from last year, why do you think capitalism emerged when it did?

4. Smith says that all of society benefits from a capitalist economy. Do you agree? Do you think that some people are more likely to be winners or losers, who are these different groups?