la polar - io - final · la polar 20 may 2013 page 3 investment highlights la polar, in our view,...

TRANSCRIPT

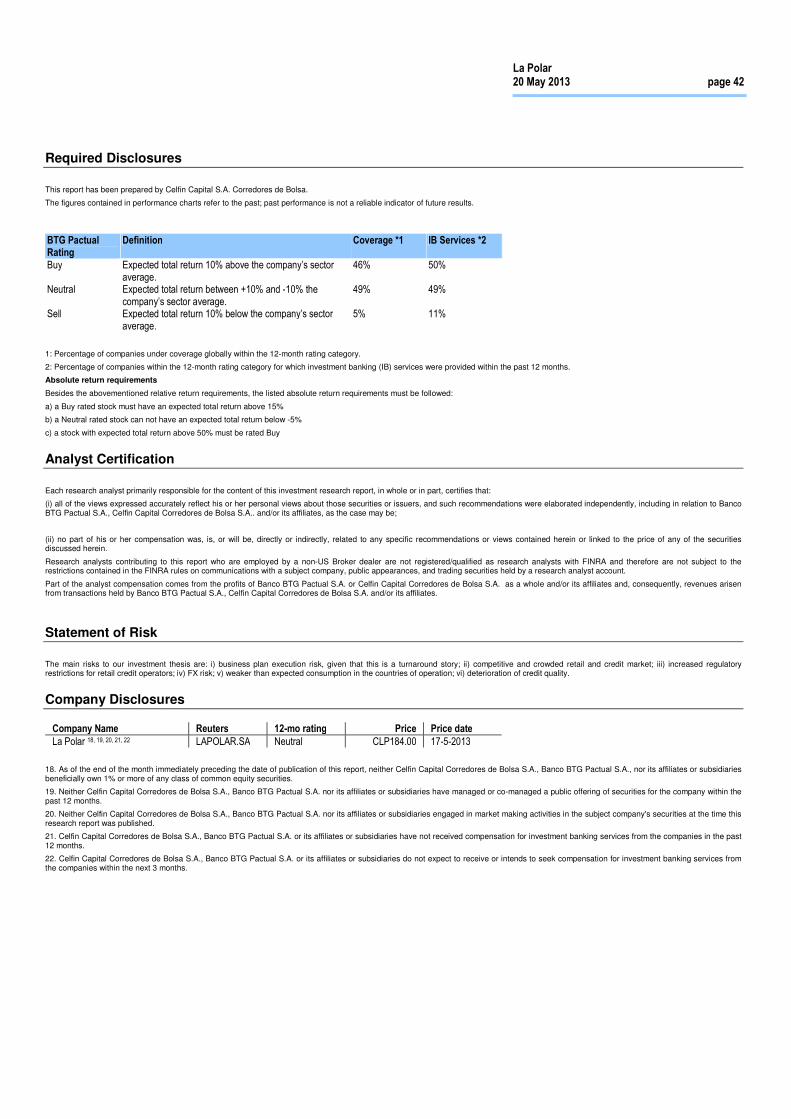

ANALYST CERTIFICATION AND REQUIRED DISCLOSURES BEGIN ON PAGE 42 Banco BTG Pactual S.A. does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

Equity Research

Rating Neutral

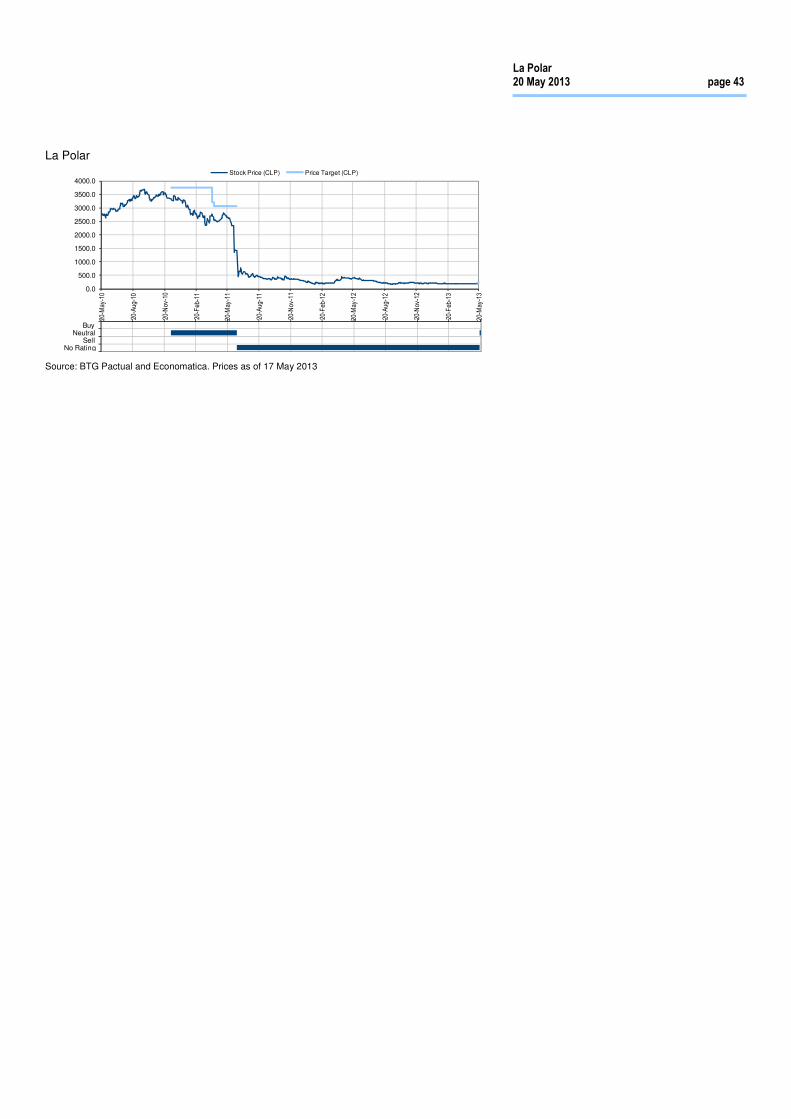

12m Price Target CLP218.00/US$0.45

Price CLP184.00/US$0.38

RIC: LAPOLAR.SA, BBG: NUEVAPOL CI Trading Data and Return Forecasts

52-wk range CLP416.15-165.04/US$0.82-0.35

Market cap. CLP184bn/US$382m

Shares o/s (m) 998.6

Free float 100%

Avg. daily volume('000 Shares) 1,953

Avg. daily value (CLP m) 369.5

Forecast price appreciation +18.5%

Forecast dividend yield 0.0%

Forecast stock return +18.5% Stock Performance (CLP)

Isabel Darrigrandi

Chile - BTG Pactual

+562 2490 5093

Alonso Aramburu

New York – BTG Pactual US Capital LLC

+1 646 924 2471

Fabio Monteiro

Brazil – Banco BTG Pactual S.A.

+55 11 3383 2006

0

30

60

90

120

150

0.0

500.0

1,000.0

1,500.0

2,000.0

2,500.0

3,000.0

3,500.0

4,000.0

20-M

ay-1

0

20-A

ug-1

0

20-N

ov-

10

20-F

eb-1

1

20-M

ay-1

1

20-A

ug-1

1

20-N

ov-

11

20-F

eb-1

2

20-M

ay-1

2

20-A

ug-1

2

20-N

ov-

12

20-F

eb-1

3

20-M

ay-1

3

Price Target (CLP) Stock Price (CLP) Rel. IPSA

Rising from the ashes: the new (& improved) La Polar

We are staying on the sidelines for now, initiating coverage with a neutral

We are initiating coverage on Chilean department store operator La Polar with a PT

of CLP218, which represents 19% upside to current levels. While La Polar is firmly

out of crisis mode, the retailer faces tough competition (Falabella, Paris, Ripley) and

an adverse regulatory environment. So, though we believe in the new management

team and the turnaround plan, execution risk is keeping us on the side lines, for now.

Out of bankruptcy and fully funded for growth

After a high profile credit card & accounting scandal nearly drove the company out of

business in mid-2011, La Polar’s new leadership i) raised US$280mn in equity to fund

its business plan; ii) restructured its debt (to less than half, in PV); and iii) reached an

agreement with the consumer protection agency to end its class action lawsuit.

Overhaul of proprietary brands should drive 15% SSS growth in 2013

La Polar’s new apparel & design team wasted no time in giving the retailer’s

proprietary brands a major (and much needed) face lift. Store renovations (US$40mn

in capex over two years) should also help get more customers through the door. As a

result, we expect 15% SSS growth in 2013.

New product mix & improved sourcing to boost retail gross margins by 300 bps

Management plans to improve the product mix to favor those with higher gross retail

margins: i.e. more apparel (30%-50% margins), and less electronics (15%). Within

apparel, more proprietary brands (50% margins) and less 3rd party brands (30%). La

Polar has also made mayor changes to its sourcing process, which has already

reduced direct costs for proprietary apparel brands by roughly 20%.

Quarterly results this year could be a catalyst for the stock

We value La Polar using a blended PT based on a DCF and multiples analysis.

Looking at the comps (Hites & Ripley), La Polar does not look cheap, but in our view

a 10 yr DCF better captures the full impact of the turnaround story. Execution will be

key, so hitting targets in quarterly results this year could be a catalyst for the stock.

Valuation 12/2011 12/2012 12/2013E 12/2014E 12/2015E RoIC (EBIT) % NM (10.6) (4.2) 6.8 11.8 EV/EBITDA NM (7.8) (95.0) 14.1 8.8 P/E NM 1.1 (11.5) 17.5 12.7 Net dividend yield % NM 0.0 0.0 0.0 2.6 Financials (CLPmn) 12/2011 12/2012 12/2013E 12/2014E 12/2015E Revenues NM 381,910 439,914 554,894 636,887 EBITDA NM (51,391) (3,952) 26,946 44,234 Net Income NM 187,528 (15,967) 10,520 14,442 EPS (CLP) NM 187.79 (15.99) 10.54 14.46 Net DPS (CLP) NM 0.00 0.00 0.00 4.82 Net (debt) / cash NM (193,460) (191,844) (196,782) (206,267)

Source: Company reports, Bovespa, BTG Pactual S.A. estimates. / Valuations: based on the last share price of the year; (E) based on a share price of CLP184.00, on 17 May 2013.

Chile

Retailers, Apparel

Company Note

20 May 2013

La Polar

La Polar 20 May 2013 page 2

Table of contents

Investment highlights 3

Retail sector valuation multiples 7

Investment thesis – pros 9

Investment thesis – cons 20

Valuation 23

Ownership structure 25

Company overview 26

Brief history 26

Appendix 35

The new board of directors 35

The new management team 36

Lawsuits 37

New brands 38

Example of a re-launched brand – Zibel 40

La Polar 20 May 2013 page 3

Investment highlights

La Polar, in our view, is well out of crisis mode and firmly positioned to continue

executing on its turnaround strategy. We estimate that in 2013, La Polar’s Chile

operation will once again be in positive Ebitda territory as we expect i) improvements

to the product offering and stores layouts to drive 15% SSS growth; ii) changes in the

sourcing process to increase retail gross margins by 300 bps; and iii) a gross loan

book which we expect will increase by over 25%, as the last restrictions to the credit

operation finally were lifted in late 2012. On a consolidated basis, including Colombia,

La Polar should be able to reach a 5% Ebitda margin by 2014.

When the company first went into bankruptcy in mid-2011, urgent steps needed to be

taken if La Polar was going to remain a going concern. One by one, these “to do’s”

have been checked off the list:

i) The board of directors was replaced and new management was hired;

ii) A viable business plan was developed;

iii) An agreement with creditors was reached to restructure the debt,

including a grace period to delay amortizations;

iv) Roughly US$280mn was raised in cash through a new equity offering to

finance the capex and working capital requirements in the turnaround

strategy;

v) An agreement with the Chilean consumer protection agency was

reached which capped the company’s legal liabilities, with regards to

the consumer class action lawsuit, at US$40mn.

Once the immediate crisis was addressed, La Polar was able to focus on reviving its

core business: retail sales. One of the first steps was to completely revamp the

apparel department. A professional, 25 person design team was hired, higher margin

proprietary brands were updated and reenergized, purchasing budgets were

reoriented to favor a better product mix. The sourcing process was also brought into

the 21st century, with industry standard best practices like using spec sheets, which

allows the company to not only receive comparable quotes from a larger number of

manufacturers, but also to hold the manufacturer accountable for the product

delivered.

The summer season (which just ended in March) was the first to fully capture all of

these, and other, changes. As a result, we expect La Polar to easily deliver double

digit same store sales growth in 1Q13.

Looking forward, La Polar still has a lot of low hanging fruit that it can easily pick, in

our view. Most of the company’s department stores were neglected for years under

the previous administration, so the investment plan includes roughly US$40mn to

renovate over 60% of the stores in Chile in the next two years. We think the

renovations will make a major difference in luring customers through the door. Also,

the company is no longer hamstrung by the loan caps and other restrictions the

La Polar 20 May 2013 page 4

regulators had placed on its credit card operation in Chile, so La Polar should be able

to take advantage of pent up demand from existing customers. La Polar also now has

sufficient cash, in our view, to grow its credit card customer base and loan book back

to the point where it is closer in line with the rest of the industry.

Given that La Polar is a turnaround story, the stock faces significant execution risk.

Chile has a crowded retail market with several large, world-class department store

players –including Falabella, Cencosud (Paris and Johnson) and Ripley– each with a

proven retail track record and an established credit card operation. Then there are

smaller players, such as Hites, that primarily target consumers in the lower to middle

income segments, not to mention competition from various specialty store chains, like

Forus. In the past, La Polar focused almost exclusively on low to mid income

customers. If La Polar is going to achieve the goals set forth in the “Aconcagua Plan”

(management’s target for 2014), the company needs to take at least some market

share away from these incumbent players.

Table 1: La Polar’s Chile operation – BTG Pactual forecast compared to the Aconcagua Plan

Source: La Polar. BTG Pactual.

An even bigger challenge, in our view, will be growing the credit card operation, given

the current adverse regulatory environment and the increasing competition from

banks. Most other department stores in Chile are seeing the percentage of retail

sales realized with their proprietary credit cards, contract. We do think that La Polar

has pent up demand that should fuel growth, at least initially. La Polar has the same

number of active credit cards as Hites, for example, even though La Polar has 40

stores compared to 14 for Hites.

While we do expect La Polar to grow its loan portfolio, we do not think it will likely

grow as fast as management’s plan. In fact, the biggest difference between our

forecast and the Aconcagua Plan is the credit card operation. We keep financial

revenue to roughly 20% of retail revenue while the Aconcagua Plan has financial

revenue ramping up to 30% of retail revenue by 2014. According to our estimates,

this would require more working capital (to increase credit card receivables) than

what La Polar could currently fund, unless it went back to the capital markets. If

management were to surprise to the upside on its retail operating metrics (sales

growth per square meter, retail gross margins), then the company may generate

BTG Pactual BTG Pactual Aconcagua

2012A 2013E 2014E 2014E

Retail revenue (CLP$bn) 294 338 400 437

Sales (UF)/sqm/month 6.7 7.5 8.6 10.0

Sales (USD$)/sqm/month 320 358 412 480

Retail gross margin 22% 25% 27% 30.0%

Financial revenues/retail revenues 20% 19% 19% 30.0%

(Retail + Credit SG&A)/retail revenue 40% 34% 31% 30%

Provision/gross loans 12% 12% 12% 12%

(Retail + Credit Ebitda) /retail revenue -13.7% 1.7% 8.5% 10.0%

La Polar 20 May 2013 page 5

more cash than what we are forecasting, which it could then be used to grow its loan

book more aggressively.

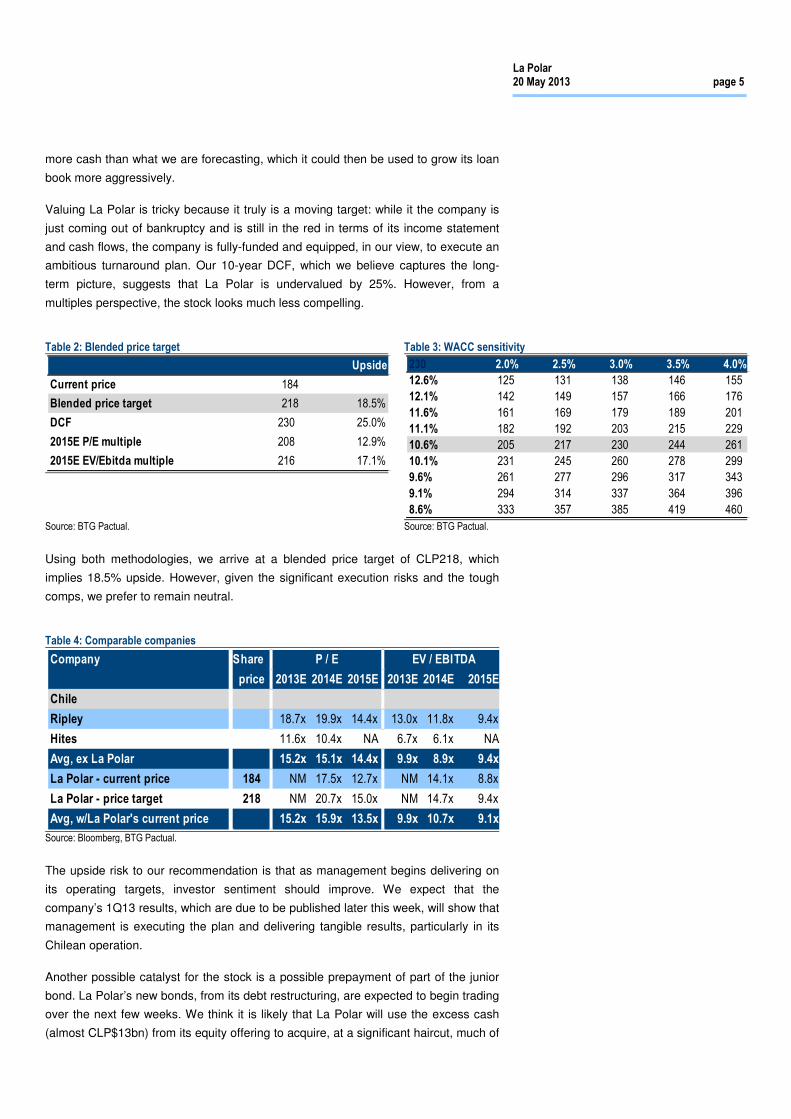

Valuing La Polar is tricky because it truly is a moving target: while it the company is

just coming out of bankruptcy and is still in the red in terms of its income statement

and cash flows, the company is fully-funded and equipped, in our view, to execute an

ambitious turnaround plan. Our 10-year DCF, which we believe captures the long-

term picture, suggests that La Polar is undervalued by 25%. However, from a

multiples perspective, the stock looks much less compelling.

Table 2: Blended price target

Table 3: WACC sensitivity

Source: BTG Pactual. Source: BTG Pactual.

Using both methodologies, we arrive at a blended price target of CLP218, which

implies 18.5% upside. However, given the significant execution risks and the tough

comps, we prefer to remain neutral.

Table 4: Comparable companies

Source: Bloomberg, BTG Pactual.

The upside risk to our recommendation is that as management begins delivering on

its operating targets, investor sentiment should improve. We expect that the

company’s 1Q13 results, which are due to be published later this week, will show that

management is executing the plan and delivering tangible results, particularly in its

Chilean operation.

Another possible catalyst for the stock is a possible prepayment of part of the junior

bond. La Polar’s new bonds, from its debt restructuring, are expected to begin trading

over the next few weeks. We think it is likely that La Polar will use the excess cash

(almost CLP$13bn) from its equity offering to acquire, at a significant haircut, much of

Upside

Current price 184

Blended price target 218 18.5%

DCF 230 25.0%

2015E P/E multiple 208 12.9%

2015E EV/Ebitda multiple 216 17.1%

230 2.0% 2.5% 3.0% 3.5% 4.0%

12.6% 125 131 138 146 155

12.1% 142 149 157 166 176

11.6% 161 169 179 189 201

11.1% 182 192 203 215 229

10.6% 205 217 230 244 261

10.1% 231 245 260 278 299

9.6% 261 277 296 317 343

9.1% 294 314 337 364 396

8.6% 333 357 385 419 460

Company Share P / E EV / EBITDA

price 2013E 2014E 2015E 2013E 2014E 2015E

Chile

Ripley 18.7x 19.9x 14.4x 13.0x 11.8x 9.4x

Hites 11.6x 10.4x NA 6.7x 6.1x NA

Avg, ex La Polar 15.2x 15.1x 14.4x 9.9x 8.9x 9.4x

La Polar - current price 184 NM 17.5x 12.7x NM 14.1x 8.8x

La Polar - price target 218 NM 20.7x 15.0x NM 14.7x 9.4x

Avg, w/La Polar's current price 15.2x 15.9x 13.5x 9.9x 10.7x 9.1x

La Polar 20 May 2013 page 6

its junior bond, reducing future financial (non-cash) expenses, improving the bottom

line and making the company more attractive from a P/E perspective, as well. Taking

out the junior bond would also make La Polar more attractive as a possible

acquisition target, given that any acquirer would have to value that debt at a much

lower discount rate.

Another possible catalyst for the stock is Colombia. Under La Polar current plan, the

Colombia operation –with only five stores— will not likely be cash flow positive for

another couple of years. A JV or partnership with a larger player could provide La

Polar with the means of reaching that goal much sooner (and free up cash for its

Chilean operation). We understand that La Polar is undergoing a search at this time.

La Polar 20 May 2013 page 7

Retail sector valuation multiples

Table 5: BTG Pactual Retail Comps – P/E

Source: Bloomberg, BTG Pactual.

Company Ticker Market Cap P / E Net Income Growth Dividend yield

(Local FX - mn) 2012E 2013E 2014E 2012E 2013E 2014E 2012E 2013E 2014E

Brazil

Lojas Renner LREN3.BZ 9,513 25.7x 21.5x 16.7x 9% 20% 28% 3% 3% 3%

Marisa AMAR3.BZ 5,571 26.7x 18.5x 14.3x 17% 45% 29% 1% 1% 1%

Hering HGTX3.BZ 6,856 21.3x 18.9x 16.4x 7% 12% 16% 4% 2% 4%

Le Lis Blanc LLIS3.BZ 1,572 31.5x 21.9x 17.3x -20% 44% 27% 1% 0% 1%

Arezzo ARZZ3.BZ 3,676 37.5x 31.0x 25.6x 7% 21% 21% 1% 1% 1%

Lojas Americanas LAME4.BZ 16,714 44.2x 32.2x 23.8x 14% 38% 35% 0% 1% 1%

Natura NATU3.BZ 21,674 23.9x 21.2x 18.5x 9% 13% 14% 5% 3% 4%

Hypermarcas HYPE3.BZ 10,572 33.6x 21.4x 17.1x >100% 57% 25% 0% 0% 1%

B2W BTOW3.BZ 1,698 NA NA NA NA NA NA 0% 0% 0%

Pao de Acucar PCAR4.BZ 28,947 29.1x 22.0x 18.3x 20% 27% 20% 1% 1% 1%

Magazine Luiza MGLU3.BZ 1,492 32.3x 11.4x 7.8x -7% NA 45% 0% 0% 0%

Raia Drogasil RADL3.BZ 7,368 47.9x 33.7x 25.0x 2% 42% 35% 0% 0% 1%

Brazil Pharma BPHA3.BZ 3,278 37.8x 22.3x 17.6x 3% 69% 27% 1% 1% 1%

IMC IMCH3.BZ 2,104 71.8x 25.8x 16.8x NA NA 54% 0% 0% 0%

Unicasa UCAS3.BZ 621 13.6x 13.9x 12.3x -26% 5% 13% 0% 2% 2%

Technos TECN3.BZ 1,782 24.0x 20.5x 16.6x 5% 17% 24% 2% 1% 1%

Brazilian Companies Average (ex-B2W) 33.4x 22.4x 17.6x 3% 32% 28% 1% 1% 2%

Mexico

Walmex WALMEXV.MM 644,593 27.7x 24.0x 21.0x -1% 25% 14% 0% 0% 0%

Soriana SORIANA.MM 90,504 25.1x 24.6x 25.8x 1% 11% -5% 1% 0% 0%

Chedraui CHDRAUIB.MM 45,179 30.1x 21.9x 19.1x -9% 49% 15% NM 0% 0%

Chile

Cencosud CENCOSUD.CI 7,351,831 24.3x 21.2x 17.1x -6% 32% 24% 1% 1% 1%

Falabella FALAB.CI 12,970,568 33.0x 24.6x 19.6x -7% 34% 25% 1% 1% 1%

Forus FORUS.CI 865,871 27.8x 24.6x 21.8x 10% 13% 13% 1% 1% 2%

Colombia

Almacenes Exito EXITO.CB 12,640,372 29.7x 26.0x 23.0x 12% 12% 13% -1% -1% -2%

Peru

InRetail INRETC1.PE 2,365 39.8x 33.0x 25.4x 30% 22% 30% 0% 0% 0%

LatAm (ex-Brazil) Companies Average 29.7x 25.0x 21.6x 4% 25% 16% NM 0% 0%

BTG Pactual Coverage Average 33.1x 23.4x 19.1x 3% 29% 24% NM 1% 1%

La Polar 20 May 2013 page 8

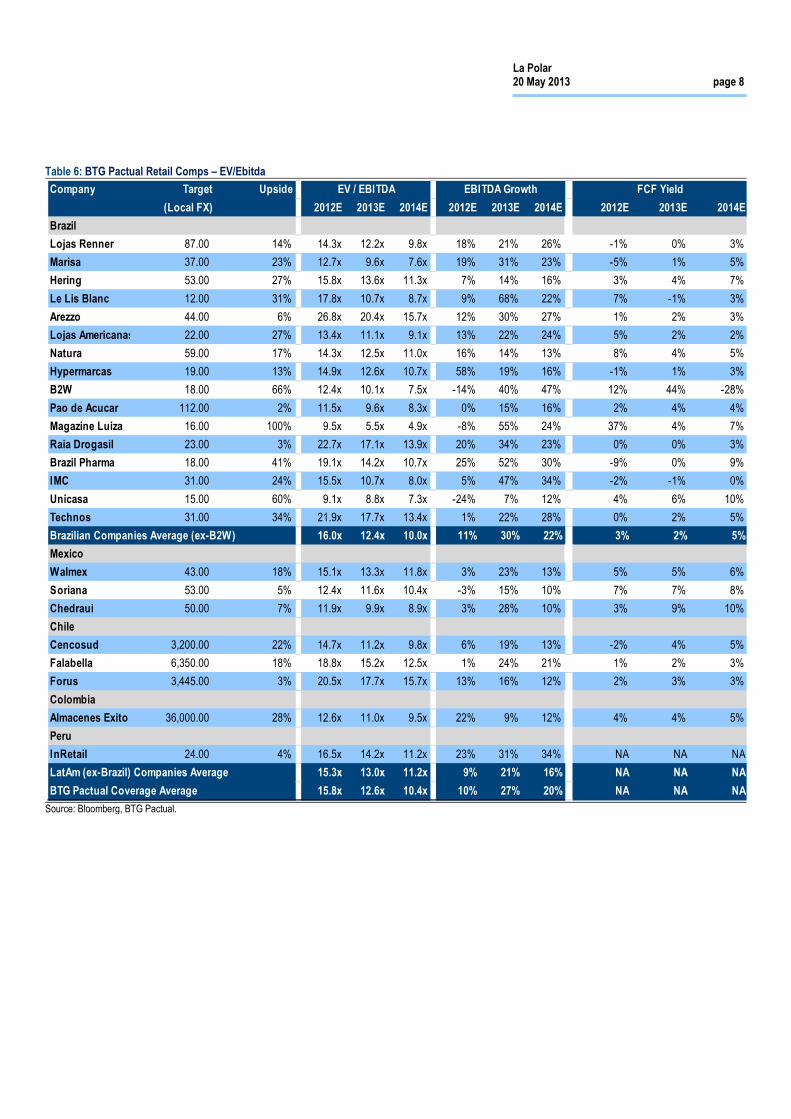

Table 6: BTG Pactual Retail Comps – EV/Ebitda

Source: Bloomberg, BTG Pactual.

Company Target Upside EV / EBITDA EBITDA Growth FCF Yield

(Local FX) 2012E 2013E 2014E 2012E 2013E 2014E 2012E 2013E 2014E

Brazil

Lojas Renner 87.00 14% 14.3x 12.2x 9.8x 18% 21% 26% -1% 0% 3%

Marisa 37.00 23% 12.7x 9.6x 7.6x 19% 31% 23% -5% 1% 5%

Hering 53.00 27% 15.8x 13.6x 11.3x 7% 14% 16% 3% 4% 7%

Le Lis Blanc 12.00 31% 17.8x 10.7x 8.7x 9% 68% 22% 7% -1% 3%

Arezzo 44.00 6% 26.8x 20.4x 15.7x 12% 30% 27% 1% 2% 3%

Lojas Americanas 22.00 27% 13.4x 11.1x 9.1x 13% 22% 24% 5% 2% 2%

Natura 59.00 17% 14.3x 12.5x 11.0x 16% 14% 13% 8% 4% 5%

Hypermarcas 19.00 13% 14.9x 12.6x 10.7x 58% 19% 16% -1% 1% 3%

B2W 18.00 66% 12.4x 10.1x 7.5x -14% 40% 47% 12% 44% -28%

Pao de Acucar 112.00 2% 11.5x 9.6x 8.3x 0% 15% 16% 2% 4% 4%

Magazine Luiza 16.00 100% 9.5x 5.5x 4.9x -8% 55% 24% 37% 4% 7%

Raia Drogasil 23.00 3% 22.7x 17.1x 13.9x 20% 34% 23% 0% 0% 3%

Brazil Pharma 18.00 41% 19.1x 14.2x 10.7x 25% 52% 30% -9% 0% 9%

IMC 31.00 24% 15.5x 10.7x 8.0x 5% 47% 34% -2% -1% 0%

Unicasa 15.00 60% 9.1x 8.8x 7.3x -24% 7% 12% 4% 6% 10%

Technos 31.00 34% 21.9x 17.7x 13.4x 1% 22% 28% 0% 2% 5%

Brazilian Companies Average (ex-B2W) 16.0x 12.4x 10.0x 11% 30% 22% 3% 2% 5%

Mexico

Walmex 43.00 18% 15.1x 13.3x 11.8x 3% 23% 13% 5% 5% 6%

Soriana 53.00 5% 12.4x 11.6x 10.4x -3% 15% 10% 7% 7% 8%

Chedraui 50.00 7% 11.9x 9.9x 8.9x 3% 28% 10% 3% 9% 10%

Chile

Cencosud 3,200.00 22% 14.7x 11.2x 9.8x 6% 19% 13% -2% 4% 5%

Falabella 6,350.00 18% 18.8x 15.2x 12.5x 1% 24% 21% 1% 2% 3%

Forus 3,445.00 3% 20.5x 17.7x 15.7x 13% 16% 12% 2% 3% 3%

Colombia

Almacenes Exito 36,000.00 28% 12.6x 11.0x 9.5x 22% 9% 12% 4% 4% 5%

Peru

InRetail 24.00 4% 16.5x 14.2x 11.2x 23% 31% 34% NA NA NA

LatAm (ex-Brazil) Companies Average 15.3x 13.0x 11.2x 9% 21% 16% NA NA NA

BTG Pactual Coverage Average 15.8x 12.6x 10.4x 10% 27% 20% NA NA NA

La Polar 20 May 2013 page 9

Investment thesis – pros

Corporate governance firmly in place

One of the first orders of business for La Polar’s new board of directors was to ensure

that a corporate governance structure was put into place to prevent a repeat of the

fraud that nearly brought down the company in 2011. The position of controller was

created with this goal in mind. The controller reports directly to the board, oversees

the transparency of internal reporting practices, and conducts the internal audit.

In the 2011 scandal, various board members claimed to not have known what was

going on with regards to the unilateral debt restructurings. La Polar’s new board

created various committees (retail, finance, audit, risk, Colombia and fraud

prevention) to make sure that in the future there would be no excuse for not being

informed. Each committee is composed of up to three board members and meets

with management on a regularly scheduled basis.

New, transparent provisioning methodology

La Polar’s new management introduced a new provisioning methodology for its loan

book based on widely accepted industry standards. The new methodology

establishes tranches, starting with non-delinquent loans, and then bases the groups

on length of delinquency (using 30-day intervals). As a loan passes from one tranche

to the next, provisions are increased accordingly. At 91 days, roughly 90% of the loan

has been provisioned. At 180 days, the entire loan and provision are written off as

bad debt.

Another important change is the greater transparency with regards to La Polar’s

receivables and provisioning practices. In its quarterly report, the company now

provides a clear and detailed breakdown of its loans and provisions by tranche so

that investors can monitor, quarter by quarter, the health of the loan book.

Healthy balance sheet should provide breathing room for turnaround

La Polar, which was insolvent just a few months ago, today has a healthy balance

sheet that in our view should give the company sufficient breathing room to execute

its turnaround strategy and return to positive cash flows. La Polar recently raised

CLP132.7bn (US$280mn) in cash in new equity and erased almost two thirds of its

debt (CLP296bn), when measured in present value, thanks to a major debt

restructuring. As a result, the company’s net debt to equity was 0.5x in 4Q12 with

CLP91bn in positive equity (US$190mn).

In our view, cash from the new equity should be sufficient to cover its working capital

and capex needs, as well as the client reimbursements agreed to in the class action

suit settlement. The new credit agreement provides a lenient amortization schedule

and low, nominal interest rate expenses in the first few years. A more detailed

account of the debt restructuring and the class action lawsuit settlement can be found

on pg. 31.

La Polar 20 May 2013 page 10

New, experienced management team and committed BOD

Given the extent and pervasiveness of the fraud and/or mismanagement, La Polar’s

board of directors decided early on to fire the entire top tier of executives at the

company. The new management team is comprised of experienced professionals,

primarily from the retail and finance industries. See appendix for details.

As already stated, La Polar’s board of directors meets with management on a regular

basis to monitor the company’s progress and to ensure that management follows the

regulations and policies established to protect the interests of shareholders and

clients. The BOD is made up of well-known business leaders and investors in Chile.

Back to the company’s roots: focus on the retail business

A central part of La Polar’s turnaround strategy is to make the retail business the

company’s core business once again. Under the previous management, La Polar’s

financial services division at one point came to represent roughly half of total

revenue. In 2012, revenue from credit cards represented 19% of retail revenue (16%

of total revenue). Management has stated that, going forward, financial services

revenue should reach, but not exceed, 30% of retail revenue (or 23% of total

revenue).

According to La Polar’s management, customers with the La Polar store credit card

purchase, on average, roughly four times more than customers without the card.

Management therefore views the credit card as important for customer loyalty. Today,

roughly 50% of La Polar’s retail sales are realized using the La Polar credit card.

Spotlight on “soft goods” should help gross retail margins

Like most department stores, La Polar’s products can be placed into two general

categories: i) “soft goods”, which at La Polar primarily include apparel, footwear,

accessories, cosmetics and toys; and ii) “hard goods”, which include home

appliances & décor, electronics and computing.

In Chile, retailers tend to sell home appliances and electronics (the bulk of the “hard

goods” category) at low prices and with thin gross retail margins (in the teens or lower

twenties, in the best cases). The retailers make up for the thin margins with the credit

card revenue that they generate by providing financing for those large-ticket items.

While a consumer may buy a flat screen TV in 12 installments, he or she is less likely

to do the same with the purchase of a T-shirt or a dress, so soft goods sales cannot

rely as much on credit card income. As a result, Chilean department store retailers do

not generally discount soft goods as deeply. Apparel, footwear and accessories,

therefore, generally have a gross retail margin in the range of 30% to 50%,

depending on whether or not the product is a non-exclusive, third-party brand or

proprietary brand.

In 2010, La Polar’s sales mix of soft and hard goods was approximately 51% and

49%. La Polar’s new management has already increased the share of soft goods

revenue to 55%, which has already improved the company’s overall gross margin

La Polar’s retail gross margins in Chile expected to improve, partly due to higher % of soft goods

2012A 2013E 2014E

Retail gross margin 22% 25% 27%

La Polar 20 May 2013 page 11

(and reduced its reliance on the riskier hard goods + financing business model).

Maintaining this mix should contribute to better margins in the future.

Chart 1: 2010 revenue mix

Chart 2: 2012 revenue mix

Source: La Polar, BTG Pactual. Source: La Polar, BTG Pactual.

Expect stronger growth and better margins from proprietary brands

As already mentioned, most department stores in Chile have a mix of i) proprietary

brands; ii) exclusively licensed brands; and ii) non-exclusive, third-party brands.

Within apparel/footwear/accessories, when we talk about “non-exclusive, third-party

brands” we refer to international staples, such as Nike or Levi’s, which are available

at most large department store chains. These brands are usually sourced locally,

either through a licensee, or directly through the local or regional branch of the

multinational brand. From the perspective of the department store chains, these

international brands generally provide the lowest direct gross retail margins.

Proprietary brands and exclusively licensed brands (depending on the terms of the

license) generally provide better retail gross margins.

In 2010, La Polar’s apparel revenue mix was roughly 43% proprietary/exclusive

brands and 57% non-exclusive, third-party brands. As already mentioned, for the

Chilean department store industry as a whole, proprietary brands have, on average,

higher retail gross margins (roughly 50%) than third-party brands (+/-30%). Retail

gross margins for La Polar’s proprietary brands in 2010 were roughly 40%, lower than

the industry standard.

La Polar’s strategy with its proprietary brands, therefore, has two components: i)

reverse the revenue mix so that proprietary brands represent 55% and non-exclusive

third-party brands, 45%, of apparel sales; and ii) increase its proprietary brands’

gross retail margins from 40% to 50%.

51%49%

soft goods hard goods

55%45%

soft goods hard goods

La Polar 20 May 2013 page 12

Chart 3: 2010 apparel revenue mix

Chart 4: Aconcagua plan - apparel revenue mix

Source: La Polar, BTG Pactual. Source: La Polar, BTG Pactual.

In order to improve sales for its proprietary brands, La Polar completely overhauled

its apparel department. To start with, La Polar’s in-house design team, under the prior

management, was made up of three people. Andres Molina, who was hired by

Lecaros as Apparel Manager in late 2011, beefed up the design team, hiring 25

experienced apparel designers poached from other Chilean retailers, and organized

them into four different groups: women’s, men, kids and home.

The next step was to take stock of the company’s brands. The first assessment was

that the company had too many brands and was prioritizing none of them. By

eliminating some lower-margin, underperforming brands, La Polar would be able to

focus its purchasing budget on fewer brands, better exhibit those brands on the retail

floor, and set up strategic advertising/marketing alliances with its top third-party brand

partners, all of which should improve sales.

Apart from the proprietary brands that La Polar had developed in-house over the

years, La Polar also had exclusive licenses with international brand owners. In some

cases, as with Soviet and Fiorucci, these licenses gave La Polar authority to use the

brand on products that La Polar designed and sourced directly, in exchange for a

royalty payment. Given the nature of these agreements, these brands had the

potential to deliver gross retail margins similar to those of proprietary brands (+/-

50%). The first brands that La Polar eliminated, therefore, were the international

brands that had the highest royalties, lowest margins and worst sales track record.

The company also eliminated several in-house brands that had little or no traction.

In parallel to this, La Polar’s new apparel department determined that many of the

company’s brands lacked a well-defined identity. As a result, the sourcing team had

been free to make interpretations, resulting in an inconsistent product offering. La

Polar’s new apparel team, therefore, put together a map of Chile’s three largest

department stores’ primary proprietary/exclusive brands, based on the gender, style,

budget and age group of each brand’s target customer. The brands were also

evaluated on a spectrum, with “fashion/trendy” at one end and “basics/perennial” at

the other.

43%57%

proprietary third party

55%45%

proprietary third party

Old design team: 3 people

New design team: 25 people

Old Polar: too many brands, prioritizing none of them

New Polar: focus purchasing budget on fewer brands, better exhibit those brands in the store, set up strategic alliances

Eliminate international brands with highest royalties and worst sales track record

Eliminate numerous in-house brands with little or no traction

Map out La Polar’s & competitors’ key brands

- Strategically define and re-launch existing brands

- Identify unattended segments and create brands to address those opportunities

La Polar 20 May 2013 page 13

The map helped La Polar determine i) how to best strategically position and re-launch

its top proprietary/licensed brands and ii) that the company needed to create a couple

of new brands to compete effectively with the country’s leading department stores.

With a clear view of the competitive landscape, La Polar’s design team went back

and precisely redefined each of the company’s key proprietary/licensed brands,

drawing up a manual for each one, with its identity, customer focus and strategy. The

brands were then grouped as either: i) low-to-mid-priced brands with more emphasis

on basics (Icono, Extralindas, Unanyme, Lisa, M&M, Chess and Ozono) or ii) mid-to-

high-priced brands with basics and fashion (Portman Club, Beverly Hills Polo Club,

Soviet, Fiorucci, Zibel, Lotto, Body Glove, Carven).

The company also launched two new brands. Alma was created to go head-to-head

with Tatienne, Umbrale and University Club, locally. Alma’s international “mirror”

brands include Free People, Rapsodia and Anthropologie. La Polar also created Mila

Jeans, a new brand inspired by international names such as Lucky Brand,

Abercrombie & Fitch, and American Eagle, on the international front, and was created

to compete against Lois and Robert Lewis, locally. See appendix for more on these

two brands.

The design cycle for each collection was also completely redefined, following industry

best practices that included sample trips to the U.S. and Europe, to make sure that

each of La Polar’s collections anticipates international trends that are relevant to the

brand. The commercial department, which is kept in the loop from the beginning of

the process, provides feedback to the design team for each collection.

La Polar 20 May 2013 page 14

Table 7: La Polar’s brand map – women’s wear

Source: La Polar, BTG Pactual. This brand map is not a comprehensive list of all of each store’s brands.

Women's Wear Falabella Paris Ripley La Polar

Basics & Fashion Basement Alaniz Marquis Zibel

Prices: Low/Medium Ziben Woman

Fashion Mango Zibel Woman

Prices: High Warehouse

Full figured women Stefano Cocci Viaressa Brigitte Naux Donna Erre

Stefano Cocci Woman VSS Woman Extra Lindas

Basics Newport Rainforest Aziz Unanyme

Prices: Low Regatta

Lifesty le University Club Greenfield Tatienne Alma

Prices: Medium/High Umbrale

Third-party , exclusivde brands Esprit Laura Ashley Dimensión Azul

Prices: High Elle Calv in Klein

Benetton Guess

Third-party , non-exclusive brands Wados Wados Fashion Wados

Prices: Medium/High Saville Row

Basics & Fashion Sybilla Opposite Index Icono

Prices: Low/Medium

Jeans Sybilla Foster Barbados Icono

Semi-basics & Fashion Americanino Fiorucci

Prices: Medium/High

Jeans Lee Lee Lee Lee

Third party , non-exclusive brands Ellus Ellus Ellus Ellus

Efesis Efesis Efesis Efesis

Wados Wados Wados Wados

Wrangler Wrangler Wrangler Wrangler

Levis Levis Lev is Lev is

Lifesty le - Fashion Mossimo Soviet

Prices: Medium/High

Lifesty le Lois Robert Lewis Mila

Semi-basics & Fashion

Prices: Medium/High

International, exclusivde brands Desigual Top Shop Pepe Jeans

Fashion Free People

Prices: High

Surf Doo Australia Aussie Body Glove

Billabong Rip Curl O'Neill

O'Neill Maui Girl

Roxy

Maui Girl

Contemporary

XL

Sportswear

Teens / Young Women

La Polar 20 May 2013 page 15

More basics in the mix should also improve retail sales and margins

The new apparel team also determined that La Polar’s apparel offering was too

heavily weighted towards fashion/trend products and too light on basics. The mix was

roughly 29% basics and 71% fashion, compared to 45% basics and 55% fashion for

the rest of the industry, according to their estimates.

The problem with this mix was twofold, according to La Polar’s new apparel manager,

Andres Molina. The fashion/trend product is generally a higher-cost item than a

“basic”. The apparel mix, therefore, contributed to La Polar’s higher-than-average

costs. The previous management tried to make up for this with higher initial price

points, which contributed to La Polar’s brands being less competitive compared to its

peers. Ultimately, La Polar’s apparel margins would suffer anyway when inventory

had to be liquidated at end-of-season sales.

The other problem was that La Polar’s basics did not offer enough “depth”, or number

of units per product, in a sufficient variety of sizes and colors. As a result, popular

basic items would sell out early, and the opportunity to realize additional sales was

lost.

In our view, La Polar’s apparel sales and margins should improve as the company

improves the mix with a deeper, more extensive offering of basics.

Better sourcing should boost gross retail margins

In the past, La Polar committed several errors when it came to its sourcing practices.

The company used to source at least part of its proprietary brands locally, using a

third-party trader who then outsourced the manufacturing to Asia. Also in the past,

the sourcing team did not put together comprehensive “spec sheets” for its designs,

which made it difficult to i) obtain quotes from more than a handful of manufacturers

and ii) compare the quotes once received. Spec sheets include the technical details

of the product (i.e. fabric weight, etc.). Even minor variations can have a significant

impact on the quality and cost of the product.

Today, La Polar sources 100% of its proprietary brands abroad, primarily in Asia. The

sourcing process now uses spec sheets, which allow the company to not only receive

comparable quotes from a larger number of manufacturers, but also to hold the

manufacturer accountable. La Polar can now more easily track whether specifications

are met during the production process before the final products are shipped. The

current management also introduced two primary seasons with three to four

collection purchasing windows per season, in order to more efficiently manage

inventories. The new sourcing strategy has already reduced La Polar’s direct costs by

20% for proprietary apparel brands.

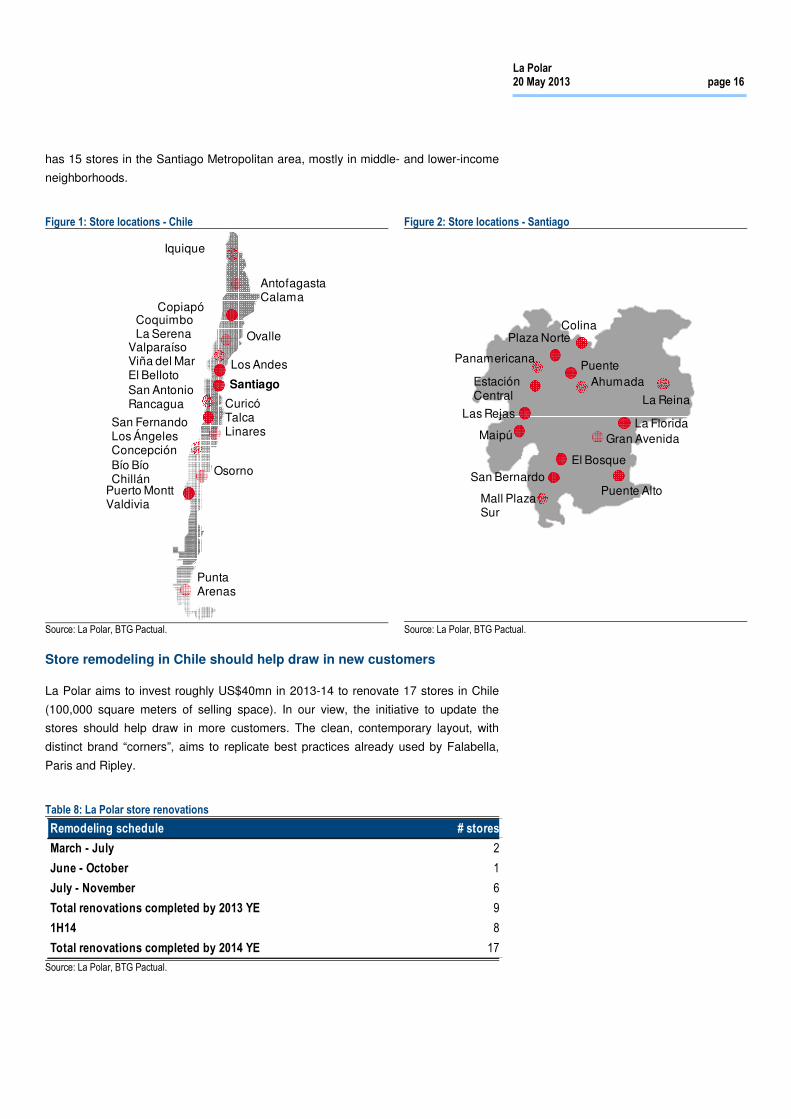

Established network of 40 stores, located throughout Chile

La Polar has 40 department stores, totaling roughly 161,000 square meters of selling

space, located throughout Chile. Of the total stores, 12 are located in shopping malls

and another eight are in power centers, next to a supermarket. The rest are mostly

located in or near the centers of the cities and towns, on high-traffic streets. La Polar

UNIQLO: example of “basics” with “depth”

The new sourcing strategy has already reduced

La Polar’s direct costs by 20% for proprietary

apparel brands.

La Polar 20 May 2013 page 16

has 15 stores in the Santiago Metropolitan area, mostly in middle- and lower-income

neighborhoods.

Figure 1: Store locations - Chile

Figure 2: Store locations - Santiago

Source: La Polar, BTG Pactual. Source: La Polar, BTG Pactual.

Store remodeling in Chile should help draw in new customers

La Polar aims to invest roughly US$40mn in 2013-14 to renovate 17 stores in Chile

(100,000 square meters of selling space). In our view, the initiative to update the

stores should help draw in more customers. The clean, contemporary layout, with

distinct brand “corners”, aims to replicate best practices already used by Falabella,

Paris and Ripley.

Table 8: La Polar store renovations

Source: La Polar, BTG Pactual.

Iquique

AntofagastaCalama

Punta Arenas

Copiapó

Osorno

Puerto MonttValdivia

CoquimboLa Serena Ovalle

ValparaísoViña del MarEl BellotoSan AntonioRancagua

Los Andes

Santiago

San FernandoLos ÁngelesConcepciónBío BíoChillán

CuricóTalcaLinares

ColinaPlaza Norte

EstaciónCentral

PuenteAhumada

Las Rejas

Maipú

Panamericana

La Reina

La FloridaGran Avenida

Puente AltoMall Plaza Sur

San BernardoEl Bosque

.

.

Remodeling schedule # stores

March - July 2

June - October 1

July - November 6

Total renovations completed by 2013 YE 9

1H14 8

Total renovations completed by 2014 YE 17

La Polar 20 May 2013 page 17

Figure 3: Estacion Central store before remodeling

Figure 4: Estacion Central store after remodeling

Source: La Polar, BTG Pactual. Source: La Polar, BTG Pactual.

Operating leverage from leases should help margins as sales increase

La Polar leases all of its stores. Shopping mall operators in Chile generally charge

their tenants the higher of i) a fixed fee in UF (the inflation adjusted currency linked to

the CLP) or ii) a variable fee based on a percentage of the store’s revenue. La Polar’s

stores currently pay a fixed lease in UF in all of the company’s shopping mall stores.

Given that this fixed amount was negotiated, for all of the stores, before the 2011

crisis, when La Polar had significantly higher sales per square meter, the delta with

regards to the variable lease should leave ample room for operating leverage as the

company increases its sales over the coming years.

Colombia, the new frontier

La Polar currently has five department stores in Colombia, with fully-funded plans to

open another nine by the end of 2015. La Polar is also evaluating another nine mall

development projects in Colombia that may present further growth opportunities.

When La Polar’s new management took over in mid-2011, the company had a

relatively clean slate in Colombia, given its short history and relatively few stores (four

at the time). The new administration, therefore, decided to directly target high-to-mid-

income customers going forward. La Polar hired Francisco Martinez, formerly

commercial director of Falabella Chile, to move to Colombia and lead the operation.

The first store that the new management opened was located in a posh neighborhood

in the city of Bucaramanga, in the Cacique mall. The Bucaramanga store was

designed with management’s new, more upscale and contemporary format.

La Polar 20 May 2013 page 18

Table 9: La Polar’s stores in Colombia

Table 10: Colombia store launch schedule

Source: La Polar, BTG Pactual. Source: La Polar, BTG Pactual.

La Polar’s current 3-year capex budget for Colombia is currently US$100mn, to

launch nine new stores and remodel the four stores that new management inherited

from the previous administration. Management estimates that the Colombia

subsidiary will breakeven with nine or ten stores in operation.

It is our understanding that La Polar has begun looking for a partner with financial

muscle, retail expertise, and local knowledge to accelerate its growth plans in

Colombia. We understand that an investment bank has been hired to facilitate the

search and evaluation process. Given that La Polar’s senior bond, to be issued in the

next few weeks, will be secured with shares of the Colombia subsidiary, La Polar

would likely have to initiate a capital increase at the subsidiary level for a new partner

to come in.

Figure 5: The Cacique mall

Figure 6: La Polar’s first store in Colombia designed by new management

Source: La Polar, BTG Pactual. Source: La Polar, BTG Pactual.

La Polar may repurchase part of its debt at a significant haircut

La Polar is evaluating the option of using up to CLP12.7bn from its equity increase to

repurchase part of the junior bond from its debt restructuring. In the equity offering

prospectus, La Polar stated that any cash raised in excess of CLP120bn could be

used for debt prepayment. The junior bond is expected to begin trading in the next

few weeks. The junior bond will be structured as a no-interest, inflation-adjusted bullet

Store City Date

Centro Mayor Bogota Oct-10

Carabobo Medellin Aug-11

Los Molinos Medellin Oct-11

Floresta Bogota Nov-11

Cacique Bucaramanga Nov-12

City Date

Yopal 4Q13

Palmira 4Q13

Cali 1Q14

Barranquilla 2Q14

Bogota 4Q14

Cali 4Q14

To be determined 2Q15

To be determined 4Q15

To be determined 4Q15

Colombia – locations of current and future stores

Barranquilla

Medellín

Cali

Yopal

BogotáBucaramanga

La Polar 20 May 2013 page 19

due in 2032 with a face value of CLP249bn. The present value of this bond is

estimated at roughly CLP18bn. Given IFRS accounting rules, La Polar must

recognize a financial expense for the junior bond that will increase each year as the

due date slowly approaches, even though there is no immediate cash outlay. Buying

back the bond would reduce La Polar’s financial expenses. In addition, the junior

bond, if left intact, would act as a poison pill for any would-be suitors, given that its

present value would likely increase if La Polar were acquired by a company with a

lower cost of capital. By eliminating the junior bond, La Polar is a more likely

acquisition target than if it is left in place, in our view. See page 31 for more details on

the debt restructuring.

Positive outlook for consumer should support retail sales

Our macroeconomics team has a generally positive midterm outlook for both Chile

and Colombia. Short-term, our macro team expects to see stronger GDP and private

consumption growth in Chile than in Colombia due to lower unemployment, higher

wage growth and consumer credit availability. Consumer confidence surveys in Chile

continue to score on the “optimistic” side of the scale.

Table 11: Real GDP growth, YoY

Table 12: Inflation (eop), YoY

Source: BTG Pactual. Source: BTG Pactual.

Private consumption in Colombia, on the other hand, is showing signs of a slowdown

in 2013, though our team expects growth to accelerate in 2014.

Table 13: Unemployment, %

Table 14: Private consumption growth, YoY

Source: BTG Pactual. Source: BTG Pactual.

2010 2011 2012 2013 2014

Chile 6.1% 6.0% 5.6% 5.4% 4.8%

Colombia 4.0% 6.6% 4.0% 3.9% 4.6%

2010 2011 2012 2013 2014

Chile 3.0% 4.4% 1.5% 2.4% 3.2%

Colombia 3.2% 3.7% 2.4% 2.4% 2.8%

2010 2011 2012 2013 2014

Chile 8.2% 7.1% 6.4% 6.5% 6.8%

Colombia 11.8% 10.9% 10.2% 10.3% 10.1%

2010 2011 2012 2013 2014

Chile 10.8% 8.9% 6.1% 6.4% 5.0%

Colombia 5.0% 5.9% 4.3% 3.7% 5.2%

La Polar 20 May 2013 page 20

Investment thesis – cons

La Polar faces tough competition from entrenched local players

La Polar’s business plan seeks to rebuild a company in what is an already crowded

and very competitive department store market (m2 per capita penetration in Chile is

the highest in Latam). La Polar is also targeting a higher-income customer (versus

the mid-to-low-income customer it targeted in the past) that is already served by

Falabella, Ripley and Paris (Cencosud), as well as local and international specialty

store retailers such as H&M, which opened its first store in Chile (at the Costanera

Center) this year.

While we believe that La Polar has ample space to improve its operating performance

in the initial stages of its turnaround strategy – driven by improved purchasing and

merchandising functions, a better product mix and store renovations – the longer-

term plan to achieve a strong competitive position and take market share away from

incumbent players involves significant execution risks, in our view. One of La Polar’s

main competitive strengths is the strategic location of its 40 stores in Chile. However,

many of those stores are also next to, or near, a Falabella, Paris or Ripley, even in

the mid-to-lower-income neighborhoods.

All three of these department store chains have proven business models that have

produced mostly consistent good results in recent years. These competitors are also

larger than La Polar, which translates into i) better economies of scale and ii) stronger

balance sheets. The cost of capital advantage can be particularly relevant in the

funding of the financial retail operation.

In addition, on the mid-to-lower-end of the spectrum, La Polar continues to face

competition from Hites and Johnson’s (Johnson’s was recently acquired by

Cencosud).

Chart 5: Department stores Chile – number of stores (2012)

Chart 6: Department stores Chile – square meters of selling space (2012)

Source: BTG Pactual. Source: BTG Pactual.

38

78

40 40

14

0

15

30

45

60

75

90

Falabella Paris + Johnson

Ripley La Polar Hites

253,595

377,190

252,042

161,000

86,994

0

100,000

200,000

300,000

400,000

Falabella Paris + Johnson

Ripley La Polar Hites

La Polar 20 May 2013 page 21

Chart 7: Department stores Chile – sqm/store (2012)

Chart 8: Department stores Chile – UF/sqm/month (2012)

Source: BTG Pactual. Source: BTG Pactual.

Chart 9: Department stores Chile – Retail revenue, CLPmn (2012)

Chart 10: Department stores Chile – Retail gross margin (2012)

Source: BTG Pactual. Source: BTG Pactual.

Chart 11: Department stores Chile – Active credit cards, millions (2012)

Chart 12: Department stores Chile – provisions/gross loans (2012)

Source: BTG Pactual. Source: BTG Pactual.

6,674

4,836

6,301

4,025

6,214

0

1,500

3,000

4,500

6,000

7,500

Falabella Paris + Johnson

Ripley La Polar Hites

16.1

8.7 9.9

6.7 7.0

0.0

3.0

6.0

9.0

12.0

15.0

18.0

Falabella Paris + Johnson

Ripley La Polar Hites

1,107,247

886,075

673,876

293,754

165,406

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

Falabella Paris + Johnson

Ripley La Polar Hites

29.0% 27.2% 26.4%22.1%

26.4%

0%

15%

30%

45%

Falabella Paris + Johnson

Ripley La Polar Hites

2.2

1.6

1.1

0.5 0.5

0.0

0.5

1.0

1.5

2.0

2.5

Falabella Paris + Johnson

Ripley La Polar Hites

4.6%

6.9%

12.0% 11.6%12.5%

0%

5%

10%

15%

Falabella Paris + Johnson

Ripley La Polar Hites

La Polar 20 May 2013 page 22

Challenging environment to grow retail credit card business

La Polar’s turnaround strategy aims to grow its credit card business by i) increasing

credit to existing customers with good credit histories and ii) issuing cards to new,

higher-income customers. As part of the fallout from the 2011 crisis, regulators

placed numerous restrictions on La Polar’s credit card operation. La Polar was

prohibited from issuing credit cards to new customers, and regulators set caps on

loans for existing customers, for example. The final restrictions were only lifted in late

2012, so we expect to see growth from pent-up demand in 2013. Additionally, La

Polar aims to launch a Visa or Mastercard branded card in 2013, which should help

reach more customers, especially within the mid-to-higher-income segments.

However, La Polar faces several challenges. The department store credit card market

is already crowded with large players: Falabella has 2.2mn active credit card

customers; Cencosud (Paris & Johnson) has 1.6mn; Ripley, 1.1mn. The retail credit

industry as a whole is also facing increasing competition from banks. In fact, usage of

store credit cards in department stores has been declining in recent years: from 62%

to 57% for Falabella and 55% to 51% for Paris between 2009 and 2012.

The regulatory environment has also become more difficult for retail credit card

operators, in large part due to the 2011 La Polar scandal. After news broke that La

Polar had unilaterally renegotiated loans, authorities passed the Ley Dicom, a “clean

slate” law that erased, on a one-time basis, the credit history of all the consumers in

Chile that had defaults of up to CLP2.5mn (roughly US$5,000). This perdonazo, or

“forgiveness” (which did not erase the debt, just the default credit history), was meant

to give consumers an opportunity to start afresh, since the Dicom credit bureau data

base can be accessed by anyone, including employers. However, the measure also

increased the credit risk for banks and retailers with credit businesses. As a result,

retailers were forced to tighten lending criteria.

Another challenge is the debate surrounding a new cap on interest rates. In Chile, the

government imposes a maximum rate that loan providers may charge. This maximum

interest rate depends on several factors, including the currency denomination, the

duration, and the size of the loan. Most of the consumer credit provided by the retail

industry is currently subject to a maximum interest rate of roughly 50% per year. The

government has stated that it intends to reduce this maximum rate to 35%, phased in

over time. The legislation regarding the interest rate caps has been modified a couple

of times already and may not go into effect until 2014. However, since retailers

charge, on average, higher interest rates than banks in Chile, it is highly likely, in our

view, that the retail sector will be more negatively impacted by the new legislation.

More recently, regulators have argued that it is illegal for department stores to

increase credit card fees without prior approval from the customer. Other regulatory

changes may be implemented in the coming months, such as a consolidated credit

database.

La Polar 20 May 2013 page 23

FX fluctuations could hurt margins

Given that virtually all of La Polar’s merchandise is imported in U.S. dollar

denominated purchases, a strong Chilean peso generally translates into better gross

margins. A weakening of the Chilean peso against the U.S. dollar, therefore, would

likely dampen gross margins.

Financial risk from credit card operation

While we think it is highly unlikely that La Polar will repeat the mistakes of its prior

management with regards to its loan book, external factors (such as a downturn in

the economy and a significant increase in unemployment) could result in higher

delinquency rates for the retail credit card industry overall. In such a scenario,

retailers with a higher percentage of lower income customers, like La Polar, may be

more exposed than department store operators with a greater share of high income

customers.

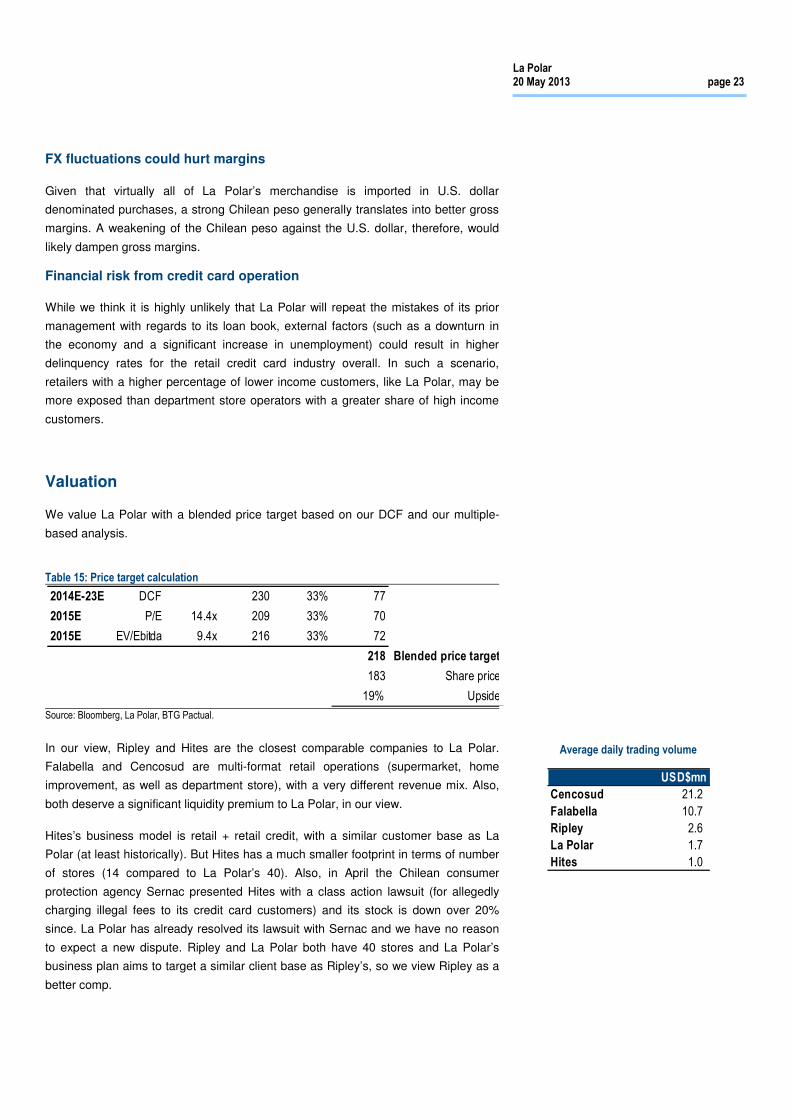

Valuation

We value La Polar with a blended price target based on our DCF and our multiple-

based analysis.

Table 15: Price target calculation

Source: Bloomberg, La Polar, BTG Pactual.

In our view, Ripley and Hites are the closest comparable companies to La Polar.

Falabella and Cencosud are multi-format retail operations (supermarket, home

improvement, as well as department store), with a very different revenue mix. Also,

both deserve a significant liquidity premium to La Polar, in our view.

Hites’s business model is retail + retail credit, with a similar customer base as La

Polar (at least historically). But Hites has a much smaller footprint in terms of number

of stores (14 compared to La Polar’s 40). Also, in April the Chilean consumer

protection agency Sernac presented Hites with a class action lawsuit (for allegedly

charging illegal fees to its credit card customers) and its stock is down over 20%

since. La Polar has already resolved its lawsuit with Sernac and we have no reason

to expect a new dispute. Ripley and La Polar both have 40 stores and La Polar’s

business plan aims to target a similar client base as Ripley’s, so we view Ripley as a

better comp.

2014E-23E DCF 230 33% 77

2015E P/E 14.4x 209 33% 70

2015E EV/Ebitda 9.4x 216 33% 72

218 Blended price target

183 Share price

19% Upside

Average daily trading volume

USD$mn

Cencosud 21.2

Falabella 10.7

Ripley 2.6

La Polar 1.7

Hites 1.0

La Polar 20 May 2013 page 24

Table 16: Comparable retail company multiples

Source: Bloomberg, BTG Pactual.

Our DCF is based on our forecast for the company’s consolidated operations in CLP.

We estimate a 10.6% WACC in CLP. Our pre tax cost of debt is based on the

weighted average discount rates used to value La Polar’s restructured debt.

Table 17: Free cash flow (CLPmn)

Table 18: WACC

Source: La Polar, BTG Pactual. Source: La Polar, BTG Pactual.

If La Polar successfully executes on its business plan, its WACC should decrease, in

our view, unlocking additional equity value.

Table 19: DCF valuation

Table 20: WACC sensitivity

Source: BTG Pactual. Source: BTG Pactual.

Company Share P / E EV / EBITDA

price 2013E 2014E 2015E 2013E 2014E 2015E

Chile

Ripley 18.7x 19.9x 14.4x 13.0x 11.8x 9.4x

Hites 11.6x 10.4x NA 6.7x 6.1x NA

Avg, ex La Polar 15.2x 15.1x 14.4x 9.9x 8.9x 9.4x

La Polar - current price 184 NM 17.5x 12.7x NM 14.1x 8.8x

La Polar - price target 218 NM 20.7x 15.0x NM 14.7x 9.4x

Avg, w/La Polar's current price 15.2x 15.9x 13.5x 9.9x 10.7x 9.1x

2012 2013 2014 2015

EBIT (58,516) (11,682) 18,796 34,511

(-) taxes - - - (6,902)

(+) depreciation 9,865 7,730 8,150 9,723

(-) capex (8,333) (23,348) (33,987) (16,667)

(+/-) change in WC 26,591 (60,497) (40,861) (25,316)

FCFF (30,393) (87,797) (47,901) (4,651)

Chile Colombia

Risk free rate 5.1% 5.5%

Expected return on the market 5.0% 5.0%

Beta 1.0 1.0

Cost of capital 10.3% 10.7%

Pretax cost of debt 13.8% 13.8%

Tax rate 20.0% 30.0%

Cost of debt 11.0% 9.7%

MV Equity 48.8% 48.8%

MV Debt 51.2% 51.2%

WACC per operation 10.7% 10.2%

2014-23 contribution 91.0% 9.0%

WACC - consolidated 10.6%

DCF - Perpetuity Based

NPV of cash flow 2014-2023 142,138

Perpetuity growth 3.0%

Perpetuity 211,315

EV @ 10.63% 353,453

Net Debt 2013E 124,243

Equity Value 229,210

Share Value (ChP/share) 230

Upside 25.4%

230 2.0% 2.5% 3.0% 3.5% 4.0%

12.6% 125 131 138 146 155

12.1% 142 149 157 166 176

11.6% 161 169 179 189 201

11.1% 182 192 203 215 229

10.6% 205 217 230 244 261

10.1% 231 245 260 278 299

9.6% 261 277 296 317 343

9.1% 294 314 337 364 396

8.6% 333 357 385 419 460

La Polar 20 May 2013 page 25

Ownership structure

La Polar does not have a controlling shareholder. In the 2012 equity raise, foreign

institutional investors acquired a roughly 25% stake in the company.

Chart 13: La Polar ownership structure, as of March 2013

Source: Superintendencia de Valores y Seguros (SVS), BTG Pactual. * Owned through CorpSeguros and CorpVida insurance companies.

25%

10%

7%5%3%

50%

Foreign institutional investors Alvaro Saieh *

AFP Habitat Moneda Asset Management

Sociedad de Rentas Massu Individual minority investors

La Polar 20 May 2013 page 26

Company overview

La Polar is the fourth largest department store operator in Chile, with 40 locations

totaling roughly 161,000 square meters of selling space. In addition, the company has

five department stores in Colombia. In both Chile and Colombia, La Polar provides

credit to customers through its credit card operation. In terms of department store

sales, the company has about a 9% market share in Chile.

Brief history

La Polar´s origins can be traced back to a tailor shop that opened for business circa

1920 near Santiago’s main railroad station. By the 1950’s, the company had evolved

into a general merchandise store, and by the 1980’s, the company began to adopt a

department store format and open new locations in Santiago. La Polar first began to

offer financing to customers, through a proprietary store credit card, in 1989. By

1990, the company had a dozen stores in Chile and 350,000 credit card holders.

In 1997, the company’s finances began to deteriorate. Chile suffered an economic

crisis, and La Polar, unable to navigate the turbulence, saw sales drop, credit card

default rates rise, and cash flow dry up. Unable to pay suppliers, the company’s

inventory levels plummeted, and by the end of 1998, sales were down by roughly

80% YoY, virtually paralyzing the operation.

In January 1999, with La Polar in bankruptcy court, the private equity firm Southern

Cross Group acquired 100% of the company’s fixed assets and brands, restructured

the debt, and re-launched the company as Comercial Siglo XXI S.A., while

maintaining the La Polar store brand. At the same time, Southern Cross replaced the

top management and recapitalized the company. Julian Moreno was the only top

executive from the prior administration that stayed on, reportedly due to his expertise

in consumer credit. Pablo Alcalde, who had worked in both the finance and retail

industries in Chile, was named CEO. By the end of August 1999, La Polar was back

up and running.

Between 2000 and 2003, La Polar’s sales, Ebitda, and net income grew at a CAGR

of 20%, 30% and 58%, respectively. In that period, the company opened 10 new

stores, more than doubling the square meters of selling space, for a total of 22 stores

(twelve in the Santiago Metropolitan area) with an average selling space of between

5,000 and 6,000 square meters each. La Polar doubled its share of Chile’s retail

market by year-end 2003, consolidating its position as the fourth largest department

store retail chain in Chile.

La Polar 20 May 2013 page 27

Table 21: Financial highlights (2000-03)

Table 22: Operating highlights (2000-03)

Source: La Polar, BTG Pactual. Source: La Polar, BTG Pactual.

During those first years under Southern Cross’ ownership, La Polar also expanded its

financial business. In late 2001, La Polar launched its first insurance products. The

next year, La Polar began to sign agreements with third-party shops and service

providers to extend the reach of its credit card. By the end of 2003, the company had

nearly 1.3mn credit card customers. The company launched its e-commerce website

in 2002.

In September 2003, La Polar went public, issuing 41,329,093 shares (20% of the

company’s equity) for CLP520 each on the Santiago Stock Exchange. The equity

offering raised a total of US32mn, which was to be used to expand operations in the

north of Chile, with the goal of reaching a total of 30 stores by 2006. The capital raise,

together with the company’s first (of many) securitized bond offering the year before,

significantly reduced leverage. By end-2003, Southern Cross’ stake in La Polar was

53.9%.

In the years that followed the IPO, La Polar continued to open stores, issue credit

cards to new clients, grow its financial and insurance businesses, and introduce new

brands. The company also continued to securitize a portion of its accounts

receivables through new bond offerings.

Table 23: Operating highlights (2004-10)

Source: La Polar, BTG Pactual.

2000-03

(CLPmn) 2000 2001 2002 2003 CAGR

Revenue 78,456 93,828 118,703 137,066 20%

YoY 53% 20% 27% 15%

Ebitda 7,320 9,575 13,809 16,145 30%

YoY 74% 31% 44% 17%

Ebitda mgn 9% 10% 12% 12%

Net income 2,139 3,586 5,238 8,407 58%

YoY 347% 68% 46% 61%

Net mgn 3% 4% 4% 6%

2000-03

2000 2001 2002 2003 CAGR

SQM 34,300 40,000 47,000 55,000 17%

YoY 31% 17% 18% 17%

Credit cards 485,000 660,000 1,014,000 1,273,000 38%

YoY 71% 36% 54% 26%

2004-10

2004 2005 2006 2007 2008 2009 2010 CAGR

Stores 24 26 33 35 40 40 43 10%

YoY 9% 8% 27% 6% 14% 0% 8%

SQM 70,000 81,000 110,750 130,000 153,000 153,000 154,100 14%

YoY 27% 16% 37% 17% 18% 0% 1%

Credit cards, issued (mn) 1.7 1.9 2.2 2.5 2.7 2.8 NA

YoY 34% 12% 16% 13% 8% 4% NA

Credit cards, active (mn) NA NA NA NA 1.6 1.7 1.7

YoY NA NA NA NA NA 1% 3%

La Polar 20 May 2013 page 28

Between 2004 and 2010, La Polar launched new proprietary brands, including a

brand aimed at teens called Icono (2005) and a brand for heavyset women called

Extra Lindas (2008). The company also received the exclusive license to sell several

international brands in Chile, including Body Glove, Beverly Hills Polo Club and

Soviet, among others.

In 2005, the company paid its first stock bonus to employees and inaugurated a new

58,500 square meter distribution center.

In October 2006, Southern Cross sold its controlling stake in La Polar through a

public auction in the Santiago Stock Exchange. Norberto Morita, a founding partner of

Southern Cross, stayed on as chairman of the board at La Polar, and Raul

Sotomayor, a partner at Southern Cross, also remained as a director.

In 2007, the company launched a new corporate logo and made significant

adjustments to its capital structure. La Polar successfully completed an offering of

15.9mn shares for US$70mn, with the purpose of financing the company’s future

growth and setting up a compensation plan (with 10% of the shares). That year, the

company also issued its fourth securitized bond, for a total of US$40mn, and its first

corporate bond, a 10-year note for UF7mn (US$250mn).

With the Chilean economy booming from 2004-07 (average annual real GDP growth

of 6.0%), La Polar reported sustained double-digit revenue, Ebitda, and net income

growth. Its net accounts receivables tripled in that four-year period, reflecting the

expansion of its credit card division.

Table 24: Financial highlights (2004-10)

Source: La Polar, BTG Pactual. Financials stated in Chilean GAAP up to 2009. In 2010 LaPolar begins to report in IFRS (and restates 2009).

But as the global subprime credit crisis gained momentum in the second half of 2008,

Chile’s economy began to feel the repercussions. Real GDP growth slowed from

5.2% the year before to 3.3%, average inflation for 2008 was nearly 9%, the CLP

depreciated 22% against the USD by year-end, and unemployment began to rise. In

2008, La Polar’s top line and net income decelerated sharply, but on the balance

sheet, net accounts receivable grew by over 55% YoY for the second year in a row.

After significantly outperforming the IPSA index from 2005-07, La Polar’s stock

underperformed in 2008.

Chilean GAAP IFRS 2004-10

(CLPmn) 2004 2005 2006 2007 2008 2009 2009 2010 CAGR

Revenue 180,807 240,210 303,071 379,386 445,534 440,876 472,541 540,190 20%

YoY 32% 33% 26% 25% 17% -1% 6% 14%

Ebitda 23,570 33,516 44,541 64,118 89,956 71,268 83,750 69,445 20%

YoY 46% 42% 33% 44% 40% -21% -7% -17%

Ebitda mgn 13% 14% 15% 17% 20% 16% 18% 13%

Net income 13,784 19,209 27,055 33,573 37,556 45,744 48,148 29,767 14%

YoY 64% 39% 41% 24% 12% 22% 28% -38%

Net mgn 8% 8% 9% 9% 8% 10% 10% 6%

La Polar 20 May 2013 page 29

Chart 14: La Polar historical stock performance

Chart 15: La Polar’s stock price compared to the IPSA Index

Source: Bloomberg, BTG Pactual. Source: Bloomberg, BTG Pactual.

In 2009, Chile’s macro environment deteriorated even further. The economy

contracted by 1% in real terms, the specter of deflation raised its head, and

unemployment averaged 9.7% for the year. For the first time in a decade, La Polar’s

top line and Ebitda contracted. The stock, however, resumed its upward trend, as

investors likely anticipated a quick recovery in Chile’s economy, which would favor

cyclical names like La Polar.

That same year, the company issued its first commercial paper for CLP30bn and

issued its fifth securitized bond for CLP34.5bn. In November of that year, the

company raised CLP67.4bn in another share offering and announced plans to enter

Colombia in 2010, with six stores in three years.

Also in 2009, Norberto Morita and Raul Sotomayor, of Southern Cross, stepped down

from the board of directors. Pablo Alcalde, CEO of La Polar since 1999, resigned in

order to replace Morita as chairman of the board. Nicolas Ramirez, the commercial

director, was promoted from the ranks to replace Alcalde as the new CEO.

In 2010, the company issued a second corporate bond, a 21-year note for UF5mn,

classified as A- by Feller Rate and A by Fitch Ratings. The funds were used to

restructure debt. The company also issued CLP30bn in commercial paper.

The fraud that triggered the 2011 La Polar crisis

On January 19, Ramirez resigned his post as CEO, citing “health issues”. He was

replaced by interim CEO Martin Gonzalez, who, until then, was the commercial

director at La Polar. On April 29, La Polar elected new members to its board of

directors, including Fernando Tisne, one of the founders and partners of Moneda

Asset Management.

In late May 2011, Chile’s Consumer Protection Agency (Sernac) presented a class

action lawsuit that alleged that La Polar’s clients had been victims of unilateral debt

restructurings. According to the press, immediately after learning about the Sernac

lawsuit, Tisne reportedly asked Alcalde to call an extraordinary meeting of the BOD.

After several meetings and conferring with management, on June 9 La Polar’s BOD

informed the Chilean securities regulatory authority (Superintendencia de Valores y

0

50

100

150

200

250

300

0

1,000

2,000

3,000

4,000

Dec

-05

Jun-

06

Dec

-06

Jun-

07

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

Share price - CLP (LHS) Share count - mns (RHS)

-50%

0%

50%

100%

150%

200%

250%

Dec

-05

Jun-

06

Dec

-06

Jun-

07

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

La Polar IPSA Index

La Polar 20 May 2013 page 30

Seguros, SVS) and the market that management had engaged, without the board’s

approval or knowledge, in credit practices that violated the company’s policies.

The credit practices in question consisted of taking past-due consumer loans and

credit card debt, applying penalties and commissions that the client had not agreed

to, and restating those loans as brand new loans. Again, all of this was done without

the client’s consent. The unilaterally “renegotiated” loans would then appear on La

Polar’s balance sheet as new, larger loans. The alleged practice would have

generated non-cash credit card revenue, inflated net receivables, and hidden losses

given that these loans, in reality, should have been recognized as delinquent. Many

of these credit card loans were unilaterally renegotiated more than once.

When the news hit the ticker, La Polar’s stock lost over 70% of its value in one day,

with further declines in the following days and months. Alcalde resigned as chairman

on June 10 (and later stepped down as a director in July). Over the next few days, La

Polar’s board hired new auditors to determine the true state of the loan book, among

other measures.

Chart 16: La Polar’s stock price and share count

Source: Bloomberg, BTG Pactual.

On June 17, the board informed the SVS that, according to revised estimates, La

Polar’s provision for bad debt for CLP118bn should be increased to CLP538bn in

order to properly reflect the true standing of the loan book. Recognizing a CLP420bn

loss would, in effect, push the company into bankruptcy.

The first steps toward a turnaround

On June 19, La Polar’s shareholders and creditors agreed to ask Cesar Barros, a

Stanford Ph.D. in Economics, with years of experience in banking and finance, to

step in as the new chairman of the board. Barros had previous experience with large-

scale turnarounds. When the ISA virus devastated salmon fisheries in the south of

Chile, Barros was appointed president of the Chilean Salmon Industry Association

0

200

400

600

800

1,000

1,200

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Share price - CLP (LHS) Shares outstanding- mns (RHS)

La Polar 20 May 2013 page 31

(SalmonChile), and he successfully helped the group restructure its debts and return

to profitability.

On July 8, La Polar’s shareholders elected a new board of directors, keeping Barros

as chairman. Tisne, who reportedly played a major role in uncovering the fraud, was

asked to say on as a director, at least for the transition period.

At the same shareholders’ meeting, Barros informed that the following measures had

been taken: i) 15 top executives had been fired; ii) the company had hired a law firm

to file civil lawsuits against six former executives on behalf of shareholders; iii) the

company was in discussions with the consumer protection agency to find a solution to

the class action lawsuit; iv) the company was actively collaborating with investigators

from the securities authority; v) Deloitte had been hired to determine the true value of

the loan book; and vi) Ernst & Young was hired to conduct an extensive audit of the

company’s financial statements.

On July 28, the board announced that it had entered into formal negotiations with its

creditors, which primarily included local banks and pension funds, in order to

restructure the company’s debt. La Polar’s restructuring proposal was accepted by its

creditors in November. Liquidation of La Polar’s assets would have only recovered

roughly 7% of the debt owed by La Polar to its creditors, so keeping the company a

going concern was a strong argument in La Polar’s favor.

On July 29, respected retail industry veteran Patricio Lecaros was named CEO.

Lecaros worked at Ripley for 14 years, rising up to the rank of commercial vice

president. Among many other accomplishments, Lecaros led the initiative to launch

Ripley’s operations in Peru. Lecaros was CEO of Ripley Peru for five years.

In the following months, La Polar also hired an external consultant and Ph.D. in

Finance, Eduardo Walker, to study the impact on customers of the company’s

irregular credit practices. Walker’s investigation concluded that, of the over one

million customers whose debt was unilaterally restructured, roughly 80% of those

clients had not paid enough to cover the initial purchase. In other words, those clients

had not made excess payments with regards to penalties and commissions. The

investigation concluded that roughly 140,000 clients had overpaid as a result of the

unilateral restructurings.

Accomplishments since the early days of the crisis

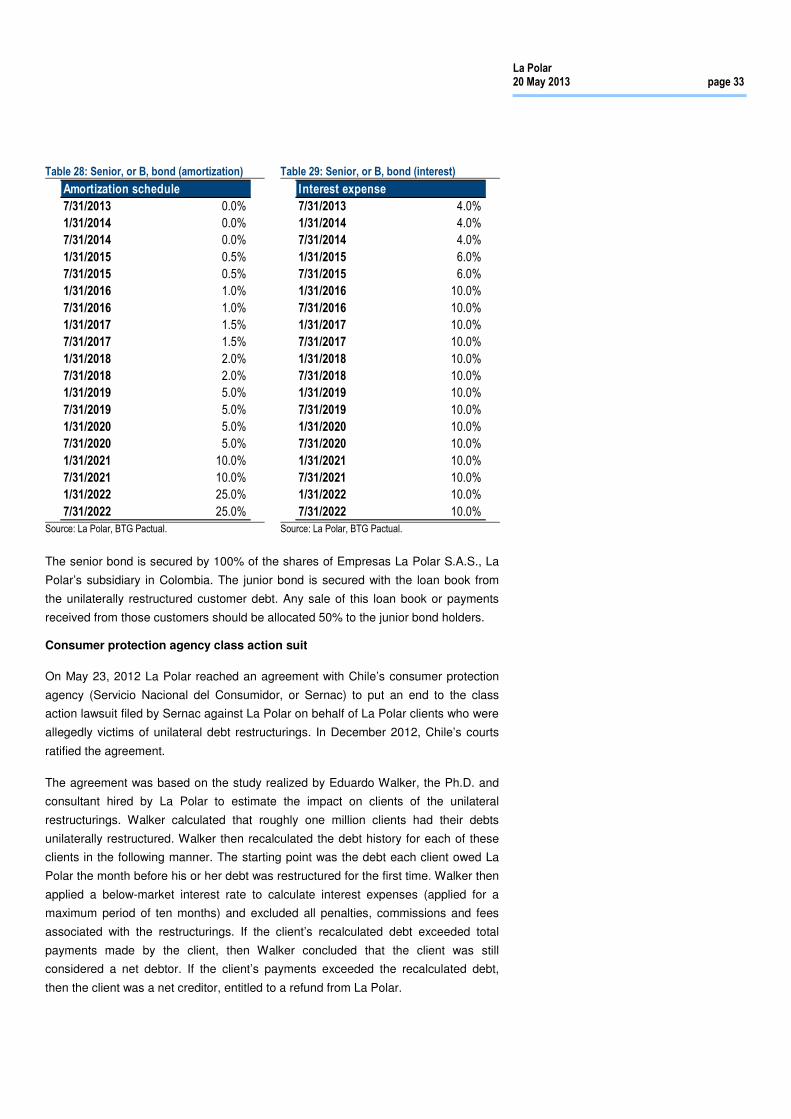

Debt restructuring

On November 7, 2011, La Polar reached an agreement with its creditors to

restructure the company’s debt. The agreement was contingent on La Polar raising at

least CLP120bn (US$250mn) in cash in new equity.

In the creditors’ agreement, all of the outstanding unsecured debt (bank debt,

commercial paper & corporate bonds) would be combined and reissued as a senior

bond and a junior bond. The senior, or A bond, would represent 44% of the

unsecured debt, and the junior, or B bond, would represent the other 56%. The

securitized bonds (Patrimonio Separado 27, or PS 27) would be kept apart, given that

they had been secured with a portion of La Polar’s receivables.

La Polar 20 May 2013 page 32

The goal of the creditors’ agreement was to not overburden La Polar with large

amortization or interest expense payments in the first years of its turnaround.

Therefore, the senior bond was structured as a 10-year note (due in 2022),

denominated in Chilean pesos, with amortization of the principal beginning on

January 31, 2015. Interest expense payments would begin on July 31, 2013. The

junior bond was structured as a 20-year, no-interest bullet (due in 2032),

denominated in UF, an inflation-adjusted currency based on the Chilean peso.

The PS 27’s amortization payments are set to begin on January 31, 2018. The

interest expense payments are scheduled to start on July 31, 2013. The interest

expense rate will be the Chilean Central Bank 10-year note (BCP 10) plus 1%.

Given Chile’s IFRS accounting rules, La Polar’s restructured debt needed to be

accounted for at present value in 4Q12. The debt restructuring, therefore, generated

CLP296bn in non-operating, non-recurring, non-cash financial income in that period,

mostly from the reduction in value of the junior bond.

Table 25: Debt pre-restructuring (CLPbn)

Table 26: Debt post-restructuring (CLPbn)

Table 27: PV of restructured debt (CLPbn)

Source: La Polar, BTG Pactual. Source: La Polar, BTG Pactual. Source: La Polar, BTG Pactual.

La Polar estimated a discount rate for the senior and junior bonds by compiling a

sample of bonds in the U.S. with similar characteristics (credit rating, amortization

schedule, covenants), estimating their average spread over the U.S. 10-year

Treasury, and applying that spread to the Chilean 10-year Central Bank note (BCP

10).

Bank debt

Commercial paper