lakehead universityflash.lakeheadu.ca/~pgreg/assignments/bondvaluationn.pdf · bond valuation...

TRANSCRIPT

Bond Valuation

Lakehead University

Fall 2004

Outline of the Lecture

• Bonds and Bond Valuation

• Interest Rate Risk

• Duration

• The Call Provision

2

Bonds and Bond Valuation

A corporation’s long-term debt is usually involves interest-only

loans.

If, for example, a firm wants to borrow $1,000 for 30 years and

the actual interest rate on loans with similar risk characteristics is

12%, then the firm will pay a total of $120 in interest each year

for 30 years and repay the $1,000 loan after 30 years.

The security that guarantees these payments is called abond. A

bond may involve more than one interest payment during a year.

3

Bonds and Bond Valuation

In the above example, interest payments could be as follows:

• one payment of $120 per year;

• two payments of $60 per year;

• four payments of $30 per year;

• any arrangement such that a total of $120 in interest is paid

each year.

4

Bonds and Bond Valuation

With a single interest payment per year, the timing of cash flows

to the lender is as follows:

. . . -0 1 2 3 29 30Year

Interest

Principal

$120 $120 $120 $120 $120

$1,000

With semiannual payments, the timing is:

. . . -0 0.5 1 1.5 2 2.5 3 29 29.5 30Year

Interest

Principal

$60 $60 $60 $60 $60 $60 $60 $60 $60

$1,000

5

Bonds and Bond Valuation

A bond is characterized by the following items:

Face Value (F ): The amount of principal to be repaid at the

bond’s maturity date.

Coupon Rate (i): The fraction ofF paid in interest each year.

Maturity ( T ): The number of years until the face value is

repaid.

Number of Payments (m): Number of interest payments in a

year.

6

Bonds and Bond Valuation

Theannual coupon paymentof a bond is then

C = i×F.

If the bond makesm payments per year, each coupon payment is

Cm =Cm

=iFm

and there arem×T of these payments over the life of the bond.

7

Bonds and Bond Valuation

A bond is usually issuedat par, i.e. it sells for $F when issued.

If, for example, the face value of a bond is $1,000, an investor

pays $1,000 for the bond when issued.

As time evolves, the return required by buyers of bonds with

similar characteristics changes. This required return depends on

the market interest rates.

Market interest rates determine theyield to maturityof a bond,

which is the annual return to an individual buying the bond at its

market price and holding it until maturity.

8

Bonds and Bond Valuation

The yield to maturity of a bond is anAPR, not an EAR.

Let y denote the yield to maturity of a bond, which is also the

yield to maturity of bonds with similar risk characteristics.

The market interest rate of a bond between each coupon payment

is thenrm = y/m.

9

Bonds and Bond Valuation

What is the price of a bond with a face valueF = $1,000, a

coupon ratei = 12%and a time to maturityT = 30years if the

bond makes annual interest payments and the rate of return on

securities with similar characteristics (yield to maturity) is 10%?

. . . -0 1 2 3 29 30Year

Interest

Principal

$120 $120 $120 $120 $120

$1,000

10

Bonds and Bond Valuation

The price of this bond is

P =120.10

(1−

(1

1.10

)30)

+1,000

(1.10)30

= 120×9.4269 + 1,000×0.0573

= $1,188.53

11

Bonds and Bond Valuation

What if the bond makes semiannual coupon payments?

Each coupon payment is then120/2 = $60, the bond makes

2×30= 60coupon payments and the rate of return between

payments is10%/2 = 5%.

. . . -0 0.5 1 1.5 2 2.5 3 29 29.5 30Year

Interest

Principal

$60 $60 $60 $60 $60 $60 $60 $60 $60

$1,000

12

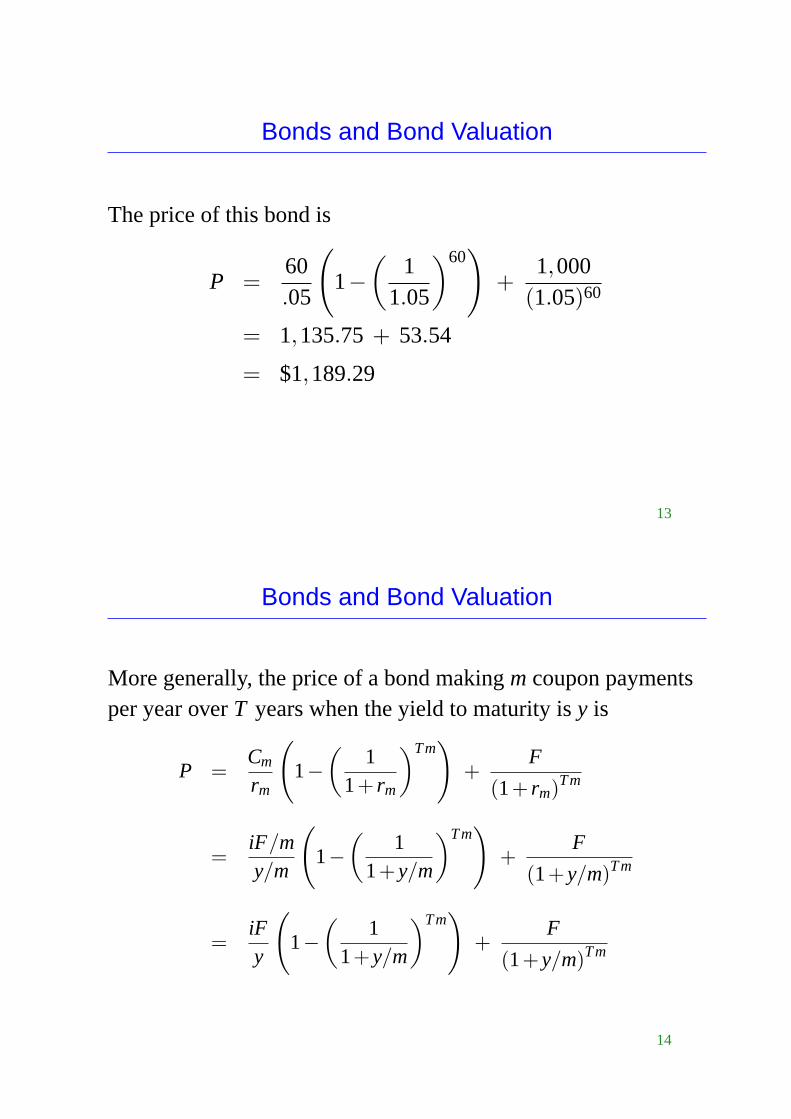

Bonds and Bond Valuation

The price of this bond is

P =60.05

(1−

(1

1.05

)60)

+1,000

(1.05)60

= 1,135.75 + 53.54

= $1,189.29

13

Bonds and Bond Valuation

More generally, the price of a bond makingm coupon paymentsper year overT years when the yield to maturity isy is

P =Cm

rm

(1−

(1

1+ rm

)Tm)

+F

(1+ rm)Tm

=iF/my/m

(1−

(1

1+y/m

)Tm)

+F

(1+y/m)Tm

=iFy

(1−

(1

1+y/m

)Tm)

+F

(1+y/m)Tm

14

Bonds and Bond Valuation

Note that

P

> F if i > y,

= F if i = y,

< F if i < y.

15

Bonds and Bond Valuation

A bond is said to

• sell at a premium whenP > F ;

• sell at par whenP = F ;

• sell at a discount whenP < F .

16

Bonds and Bond Valuation

Zero-Coupon Bonds

A zero-coupon bond is a bond that does not make coupon

payments, i.e. it is a bond with a 0% coupon rate.

The price of a zero-coupon bond with $1,000 face value and 22

years to maturity when the return on similar bonds is 6% is

P =1,000

(1.06)22 = $277.51.

Clearly, a zero-coupon bond always sells at a discount.

17

Bonds and Bond Valuation

A bond is normally issued at par, i.e. bonds with a coupon rate of

12% are issued when the yield to maturity of similar bonds is

12%.

If the face value of the bond is $1,000, its price at the time it is

issued is $1,000.

If, later on, the yield to maturity of similar bonds increases above

(decreases below) 12%, then the bond price will be less (more)

than $1,000.

18

Bonds and Bond Valuation

Knowing the face valueF , the coupon ratei, the time to maturity

T and the number of coupon payments per yearm, we can

computeP wheny is known and vice versa.

Most often, we know the price at which a bond trades and we use

the bond features (F , i andT) to determine its yield to maturity.

Most Canadian bonds make semiannual coupon payments.

19

Bonds and Bond Valuation

Bond prices are usually quoted as a percentage of face value.

If a bond with a face value of $5,000 is quoted at 97.02, this

means that the bond price is

97.02%×5,000 = $4,851.

If this bond has a coupon rate of 8%, makes semiannual

payments and has 21 years to maturity, can we find its yield to

maturity?

20

Bonds and Bond Valuation

The price of the bond is

4,851 =200y/2

(1−

(1

1+y/2

)42)

+5,000

(1+y/2)42.

What do we know abouty? It has to be more than 8% since the

bond is selling at a discount.

The yield is 8.29%.

21

Interest Rate Risk

A bond trader may be interested in two types of gains:

• Interest income

• Capital gain arising from an increase in the bond price

The risk associated with bond price changes arising from

changes in market interest rates is calledinterest rate risk.

22

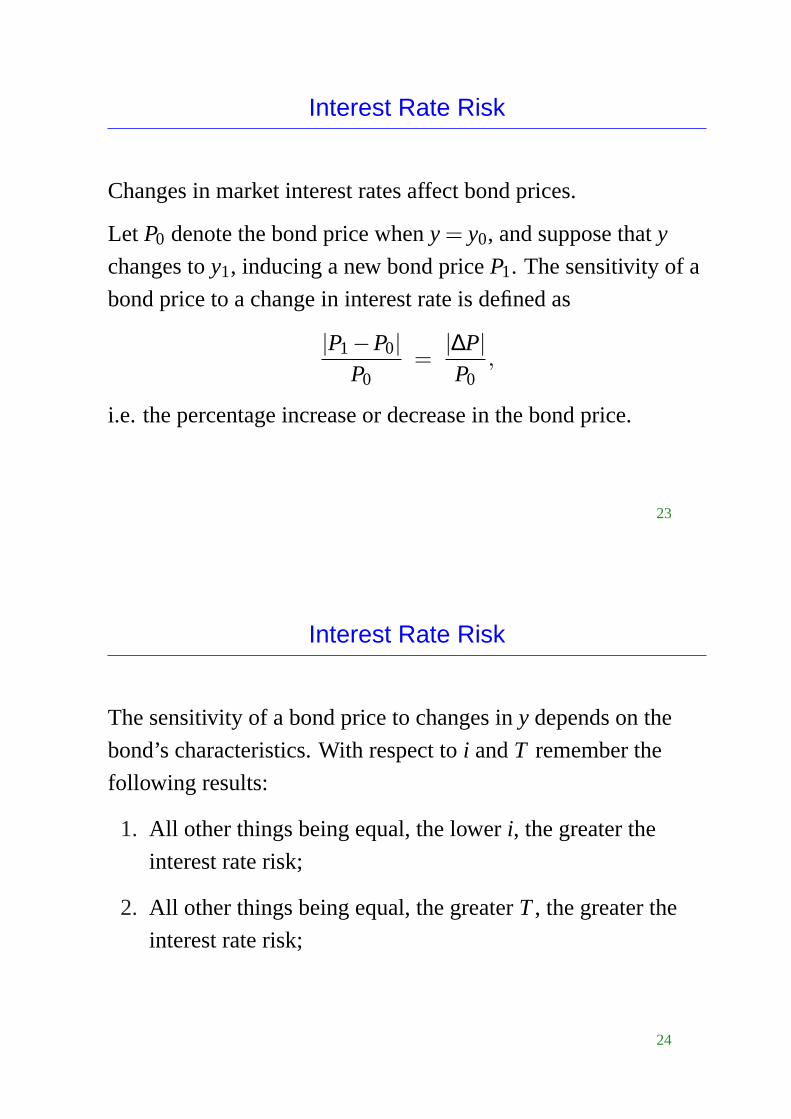

Interest Rate Risk

Changes in market interest rates affect bond prices.

Let P0 denote the bond price wheny = y0, and suppose thaty

changes toy1, inducing a new bond priceP1. The sensitivity of a

bond price to a change in interest rate is defined as

|P1−P0|P0

=|∆P|P0

,

i.e. the percentage increase or decrease in the bond price.

23

Interest Rate Risk

The sensitivity of a bond price to changes iny depends on the

bond’s characteristics. With respect toi andT remember the

following results:

1. All other things being equal, the loweri, the greater the

interest rate risk;

2. All other things being equal, the greaterT, the greater the

interest rate risk;

24

Interest Rate Risk

Take, for instance, a zero-coupon bond with a face valueF andT

years to maturity. The price of such a bond is

P =F

(1+y)T .

If y is initially y0 and then cahnges toy1, the relative change in

the bond price is (note that∆P > 0)

|∆P|P0

=

∣∣∣ F(1+y1)T − F

(1+y0)T

∣∣∣F

(1+y0)T

=

∣∣∣∣∣(

1+y0

1+y1

)T

− 1

∣∣∣∣∣ ,

25

Interest Rate Risk

If y1 < y0, then

|∆P|P0

=

∣∣∣∣∣(

1+y0

1+y1

)T

−1

∣∣∣∣∣ =(

1+y0

1+y1

)T

− 1,

which increases asT increases.

If y1 > y0, then

|∆P|P0

=

∣∣∣∣∣(

1+y0

1+y1

)T

−1

∣∣∣∣∣ = 1 −(

1+y0

1+y1

)T

,

which also increases asT increases.

26

Interest Rate Risk

Therefore,the greaterT, the greater the interest rate risk of a

zero-coupon bond.

Does this result hold with coupon bonds?

27

Interest Rate Risk

Consider two bonds, bond 1 and bond 2, withF = $1,000,

i = 10%andm= 1.

Bond 1 has 5 years to maturity while bond 2 has 10 years to

maturity.

If, initially y = 10%, then the price of each bond is $1,000.

28

Interest Rate Risk

Suppose thaty suddenly decreases to 5%.

Then the price of Bond 1 becomes $1,216, an increase of

1,216−1,0001,000

= 21.6%,

and the price of Bond 2 becomes $1,386, an increase of

1,386−1,0001,000

= 38.6%.

The percentage change is greater for the longer-term bond.

29

Interest Rate Risk

Suppose now thaty increases to 15%.

Then the price of Bond 1 becomes $832, a decrease of

1,000−8321,000

= 16.8%,

and the price of Bond 2 becomes $749, a decrease of

1,000−7491,000

= 25.1%.

Again, the percentage change is greater for the longer-term bond.

30

Interest Rate Risk

Consider now two bonds with the same characteristics except for

the coupon rates. More specifically,F = $1,000, T = 10and

m= 1 for both bonds, but Bond 1 has a 5% coupon rate while

Bond 2 has a 10% coupon rate.

If, initially y = 10%, then

• the price of Bond 1 is $693;

• the price of Bond 2 is $1,000.

31

Interest Rate Risk

Suppose thaty decreases to 5%.

Then the price of Bond 1 becomes $1,000, an increase of

1,000−693693

= 44.3%,

and the price of Bond 2 becomes $1,386, an increase of

1,386−1,0001,000

= 38.6%.

The percentage change is greater for the bond with a lower

coupon rate.

32

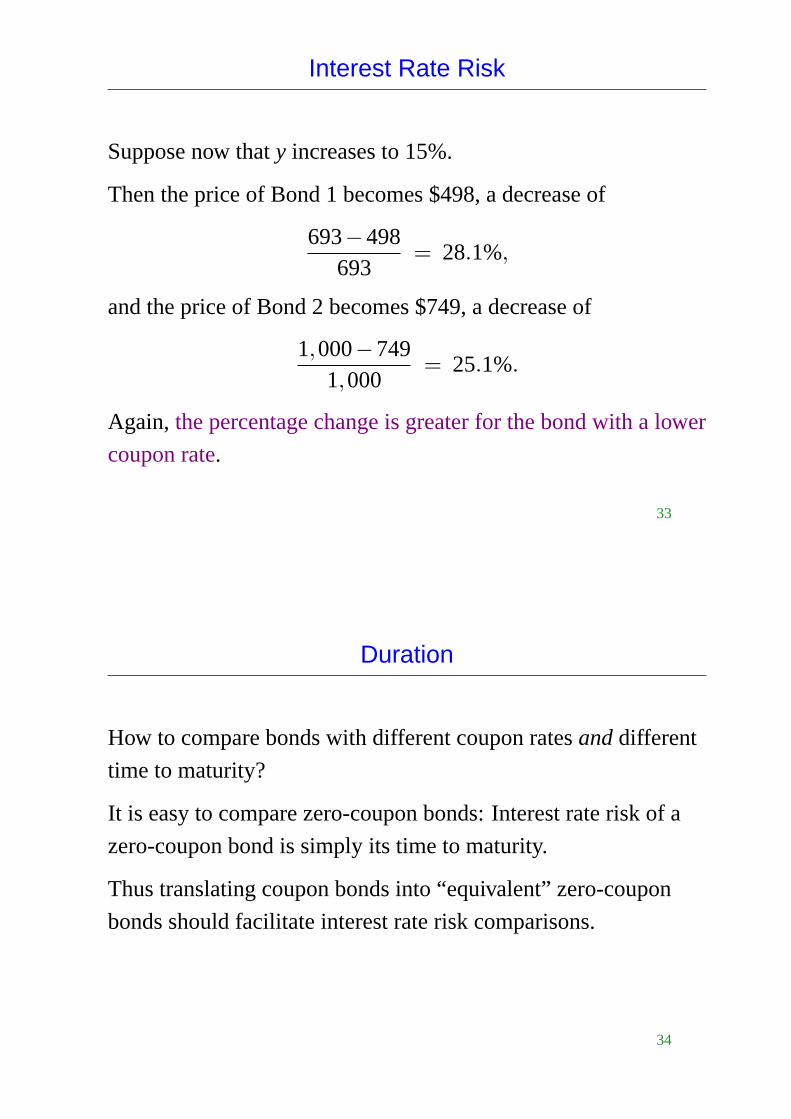

Interest Rate Risk

Suppose now thaty increases to 15%.

Then the price of Bond 1 becomes $498, a decrease of

693−498693

= 28.1%,

and the price of Bond 2 becomes $749, a decrease of

1,000−7491,000

= 25.1%.

Again, the percentage change is greater for the bond with a lower

coupon rate.

33

Duration

How to compare bonds with different coupon ratesanddifferent

time to maturity?

It is easy to compare zero-coupon bonds: Interest rate risk of a

zero-coupon bond is simply its time to maturity.

Thus translating coupon bonds into “equivalent” zero-coupon

bonds should facilitate interest rate risk comparisons.

34

Duration

Durationis a measure of the interest rate sensitivity of a bond’s

market price taking into consideration its coupon rate and time to

maturity.

The duration of a bond can be seen as the the time to maturity of

the bond’s equivalent zero-coupon bond.

Duration is measured in units of time.

35

Duration

How to calculate duration?

Take a 3-year bond with a 10% coupon rate,F = $1,000and

m= 1. This bond can be viewed as a set of three zero-coupon

bonds:

Bond z1; A zero-coupon bond paying $100 in one year;

Bond z2; A zero-coupon bond paying $100 in two years;

Bond z3; A zero-coupon bond paying $1,100 in three years.

36

Duration

If y = 8%, then the price of the coupon bond is

P =1001.08︸︷︷︸Pz1

+100

(1.08)2︸ ︷︷ ︸

Pz2

+1,100(1.08)3︸ ︷︷ ︸

Pz3

= $1,052,

i.e. the sum of its zero-coupon bond prices.

37

Duration

Duration,D, is the average time to maturity of all thezero-coupon bonds of a bond:

D =Pz1

P×1 +

Pz2

P×2 +

Pz3

P×3

=100/1.08

1,052×1 +

100/(1.08)2

1,052×2 +

1,100/(1.08)3

1,052×3

= 2.74years.

This is a weighted average, the weight on each payment time

being given by the present value of the payment divided by the

bond price.

38

Duration

More generally, a coupon bond can be viewed as a set ofTm

zero-coupon bonds:

• A zero-coupon bond payingiFm at time 1m (in years)

• A zero-coupon bond payingiFm at time 2m

...

• A zero-coupon bond payingF + iFm at timeT

39

Duration

The general equation for duration is

D =Tm

∑n=1

[Xn/(1+y/m)n

P× n

m

]

whereXn is the cash flow at timen, including the principal when

n = Tm.

Durationapproximatesinterest rate risk: The greater duration,

the greater interest rate riskshouldbe.

40

Duration

Note that

Tm

∑n=1

Xn/(1+y/m)n

P=

Tm

∑n=1

Xn

(1+y/m)n

P

=

Tm

∑n=1

Xn

(1+y/m)n

Tm

∑n=1

Xn

(1+y/m)n

= 1.

41

Duration

The duration of a zero-coupon bond is then

D =Tm

∑n=1

[Xn/(1+y/m)n

P× n

m

]=

F/(1+y)T

F/(1+y)T × T = T,

and the duration of a coupon bond is

D =Tm

∑n=1

[(iF/m)/(1+y/m)n

P× n

m

]+

F/(1+y/m)Tm

P× T.

42

Duration: Example 1

F = $1,000, i = 4%, T = 3, m= 2, y = 8%.

(1) (2) (3) (4) (5)

Year Cash Flow PV of Flow (PV of Flow)/P (1)×(4)

0.5 20 19.23 0.0215 0.0107

1.0 20 18.49 0.0207 0.0207

1.5 20 17.78 0.0199 0.0298

2.0 20 17.10 0.0191 0.0382

2.5 20 16.44 0.0184 0.0459

3.0 1,020 806.12 0.9005 2.7016

895.16 2.8469

43

Duration: Example 2

F = $1,000, i = 6%, T = 3, m= 2, y = 8%.

(1) (2) (3) (4) (5)

Year Cash Flow PV of Flow (PV of Flow)/P (1)×(4)

0.5 30 28.85 0.0304 0.0152

1.0 30 27.74 0.0293 0.0293

1.5 30 26.67 0.0281 0.0422

2.0 30 25.64 0.0271 0.0541

2.5 30 24.66 0.0260 0.0651

3.0 1,030 814.02 0.8591 2.5772

947.58 2.7831

44

Duration Hedging

A firm can hedge against interest rate risk by matching liabilities

with assets.

What do we match? Either

Duration ofassets

= Duration ofliabilities

or

Durationof assets

× Market valueof assets

= Durationof liabilities

× Market valueof liabilities

Using this procedure, a firm canimmunizeitself against interest

rate risk.

45

Duration Hedging

The IWG BankMarket Value Balance Sheet (in millions of $)

Assets Liabilities and Owners’ Equity

Value Duration Value Duration

Overnight money 35 0 C&S accounts 400 0

A/R-backed loans 500 3 months CD 300 1 year

Inventory loans 275 6 months LT financing 200 10 years

Industrial loans 40 2 years Equity 100

Mortgages 150 14.8 years

Total 1,000 Total 1,000

46

Duration Hedging

Duration of IWG’s assets:

35×0+500× 14 +275× 1

2 +40×2+150×14.8

1,000= 2.56years.

Duration of IWG’s liabilities:

400×0+300×1+200×10900

= 2.56years.

47

Duration Hedging

Is IWG immunized against interest rate risk?

2.56×1,000 > 2.56×900.

Both durations being equal, the percentage change in the value of

assets following a small change in interest rates is close to the

percentage change in the value of liabilities but, since there are

more assets than liabilities, the overall change in assets will be

greater than the overall change in liabilities.

48

Duration Hedging

What should the firm do?

1. Increase the duration of liabilities without changing the

duration of assets:

Duration ofliabilities

= 2.56× 1,000900

= 2.84years.

2. Decrease the duration of assets without changing the

duration of liabilities:

Duration ofassets

= 2.56× 9001,000

= 2.30years.

49

The Call Provision

A bond may be issued with a call provision.

That is, the issuer has the right to repurchase the bond issue

before its expiration.

The price at which the bonds can be repurchased is called thecall

price.

The call price is normally given by the bond’s face value plus a

call premium.

50

The Call Provision

Suppose, for example, that Company XYZ has a bond issue with

22 years until maturity, $1,000 face value and a coupon rate of

8%. The bonds make semiannual payments.

If the yield to maturity is 6%, the price of each of these bonds is

P =80.06

(1−

(1

1.03

)44)

+1,000

(1.03)44 = $1,242.54.

51

The Call Provision

If the firm had the right to repurchase the bonds for $1,150 each,

should it do it (bondholders would be obliged to sell at that

price)?

What if it had the right to repurchase each bond for $1,300?

A call provision on a bond is an option that gives the issuer (the

firm) the right to repurchase the issue at a pre-specified price (the

call price), usually after a pre-specified date. When the issuer

exercises its right, bondholders have the obligation to sell at the

pre-specified price. It is a contractual arrangement.

52

The Call Provision

Clearly, a call provision and the size of the call price on a bond

will affect its yield to maturity or the coupon rate needed for the

bond to be sold at par.

The idea behind a call provision is that, if interest rates fall in the

future, the issuer will be able take advantage of the low rates by

repurchasing its high-interest-rate bonds and replacing them with

low-rate bonds.

53

The Call Provision

Example

Company XYZ wants to raise $1M by issuing $1,000-bonds with

25 years to maturity. The current yield to maturity for similar

bonds is 10%. The bonds will make annual coupon payments.

Without a call provision, the coupon rate has to be 10% for these

bonds to be issued at par (i.e. $1,000 each).

54

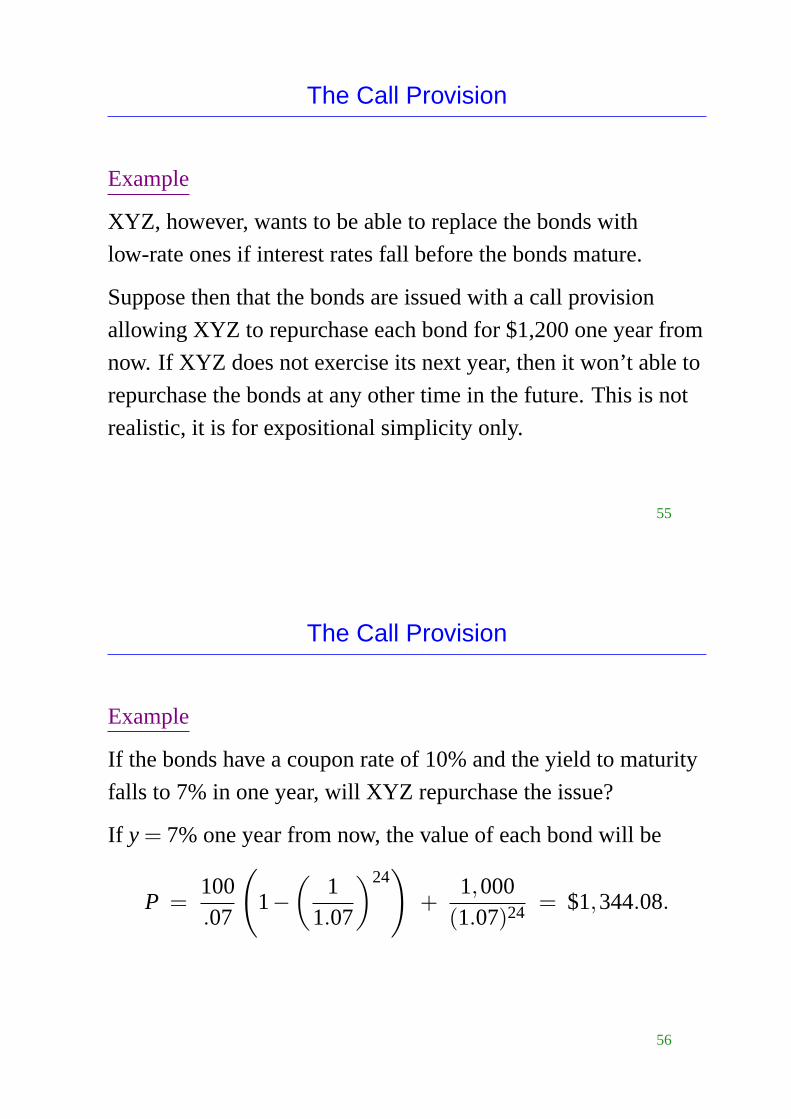

The Call Provision

Example

XYZ, however, wants to be able to replace the bonds with

low-rate ones if interest rates fall before the bonds mature.

Suppose then that the bonds are issued with a call provision

allowing XYZ to repurchase each bond for $1,200 one year from

now. If XYZ does not exercise its next year, then it won’t able to

repurchase the bonds at any other time in the future. This is not

realistic, it is for expositional simplicity only.

55

The Call Provision

Example

If the bonds have a coupon rate of 10% and the yield to maturity

falls to 7% in one year, will XYZ repurchase the issue?

If y = 7%one year from now, the value of each bond will be

P =100.07

(1−

(1

1.07

)24)

+1,000

(1.07)24 = $1,344.08.

56

The Call Provision

Example

If the firm repurchases each bond for $1,200, its profit per bond is

1,344.08 − 1,200.00 = $144.08

and thus it should do it.

57

The Call Provision

Example

Put differently, suppose that, if repurchasing the issue, XYZ

replaces it by a non-callable issue with a coupon rate equal to the

market rate.

If, for instance,y = 7%in one year, replacing the 10% callable

bonds with 7% non-callable bonds would save the company

100−70= $30per bond in interest each year.

58

The Call Provision

Example

The present value of the interest savings is

30.07

(1−

(1

1.07

)24)

= $344.08.

This $344.08 is thecash inflowfrom the repurchase.

59

The Call Provision

Example

Repurchasing the bonds, however, creates a cash outflow of

1,200−1,000= $200per bond.

That is, $1,200 has to be spent to repurchase an old bond and

each new bond provides $1,000.

The net cash flow from the operation is then

344.08 − 200.00 = $144.08.

60

The Call Provision

Example

How much would you pay for XYZ’s callable bond today if you

believed that next year’s yield to maturity had 50% chance to be

7% and 50% chance to be 13%? Today’s yield is 10%.

If y = 7%, XYZ repurchases the bond and you get $1,200.

If y = 13%XYZ does not repurchase and the bond is worth

100.13

(1−

(1

1.13

)24)

+1,000

(1.13)24 = $781.51.

In each case, you also receive $100 after one year.

61

The Call Provision

Example

What you would be willing to pay for a callable bond is the

present value of its expected cash flow in one year, which is

PV =.5×1,200.00+ .5×781.51+100.00

1.10= $991.60.

That is, you would pay less than $1,000 even though the coupon

rate is equal to the market rate.

Why? Because the call feature penalizes you: It prevents you

from receiving high interest payments when interest rates are low.

62

The Call Provision

Example

At what coupon rate would XYZ be able to issue its callable

bonds at par?

Assume that the yield to maturity one year from now has 50%

chance of being 7% and 50% chance of being 13% and each

bond can be repurchased at a call price of $1,200 one year from.

If not repurchased in one year, the bonds become regular bonds

(they cannot be repurchased at a later date).

63

The Call Provision

Example

Let C denote the coupon payment on XYZ’s callable bonds. Theexpected payoff (EP) of such a bond in one year, assuming it isrepurchased if the market rate falls to 7%, is

EP = .5×1,200 + .5×(

C.13

(1−

(1

1.13

)24)

+1,000

(1.13)24

)+ C

= 600 + 3.6414C + 26.6126 + C

= 626.6126 + 4.6414C.

64

The Call Provision

Example

If the market rate is currently 10%,C has to be such that

1,000 =626.6126 + 4.6414C

1.10⇒ C = 101.99,

which means a coupon rate of 10.199%.

65

The Call Provision

Example

To be issued at par, a callable bond’s coupon rate must be higher

than the actual return on non-callable bonds with similar

characteristics.

Purchasers of callable bonds have to be compensated for the

possible loss in interest payments.

66