large cap blend equity strategy jma large cap blend equity strategy performance june 30, 2004...

TRANSCRIPT

JMA

Large Cap Blend Equity Strategy

June 2004

JENNISON MANAGED ACCOUNTSA Division of Jennison Associates LLC

JMA

Investment Strategy & Process

2JMA

To outperform the S&P 500 Index over the long term by investing in a portfolio that has earnings growth greater than the index.

Large Cap Blend Investment Objective

3JMA

Utilize a bottom-up stock selection process to identify investment candidates from traditionally growth and value areas, as well as stocks exhibiting characteristics of both.

Growth Ideas: Seek Value in Growth

Reasonable valuations and relative expectations must accompany superior earnings and/or revenue growth.

Value Ideas: Seek Growth in Value

The potential for future earnings acceleration must accompany compelling valuations and sound fundamentals.

Core Ideas: Value + Growth

Companies exhibiting both Value and Growth characteristics that we believe will outperform the market, but may be viewed as “too expensive” by value managers or “too boring” by growth managers.

Large Cap Blend Investment Strategy

4JMA

Stock Selection Drives Investment Process

Bottom-up Stock Picking

Fundamental research is key to stock selection

The investment decision-making process is interactive

Daily morning meeting

Meetings and calls with company and external contacts

Large Cap Blend Investment Process

5JMA

Team of highly experienced analysts

Large Cap Blend universe of 900 companies

Regular meetings with company managements

Leverage insights from Wall Street

Portfolio Manager makes final investment decision, with benefit of input from all Equity Professionals

Fundamental Research Key to Stock Selection

6JMA

Bottom-up Approach

“Right Stock is the Most Important Factor”

Superior management

Strong market position

Unique marketing ability

Outstanding research & development

Global leadership

Large Cap Blend Buy Discipline

7JMA

GrowthGrowth

Qualitative Screening

Value Value

Favorable P/E ratio vs Projected

Growth Rates

Improving:Profitability &/or sales & earnings

growth

Low Price to Sales Significant

earnings stability

Low Price to Book Value

Above Average earnings & revenue

growth

Strong management teams

Unique Marketing Competence

Consistent track records

Strong research& development

Return on equity

Large Cap Blend

Stock Selection Criteria (Buy Discipline)

Financial Discipline

8JMA

Generally stocks may be sold or positions trimmed if we believe:

Company and/or industry fundamentals are deteriorating

Valuation becomes excessive

Security and/or sectors become too large relative to potential appreciation

Outlook no longer seems promising

A more attractive stock emerges

Large Cap Blend Sell Discipline

9JMA

Jeffrey P. SiegelExecutive Vice President, Portfolio Manager

19 Years of Experience

Joined Jennison in 1999

B.A., Rutgers University

Large Cap Blend Portfolio Manager

10JMA

Ted BrindisiPortfolio Advisor

35 Years of Experience

B.B.A. and M.B.A. Bernard Baruch College

Portfolio Advisors

Abhi KamerkarPortfolio Advisor

14 Years of Experience

B.A. (Economics) and M.B.A. (Finance) Rutgers University

11JMA

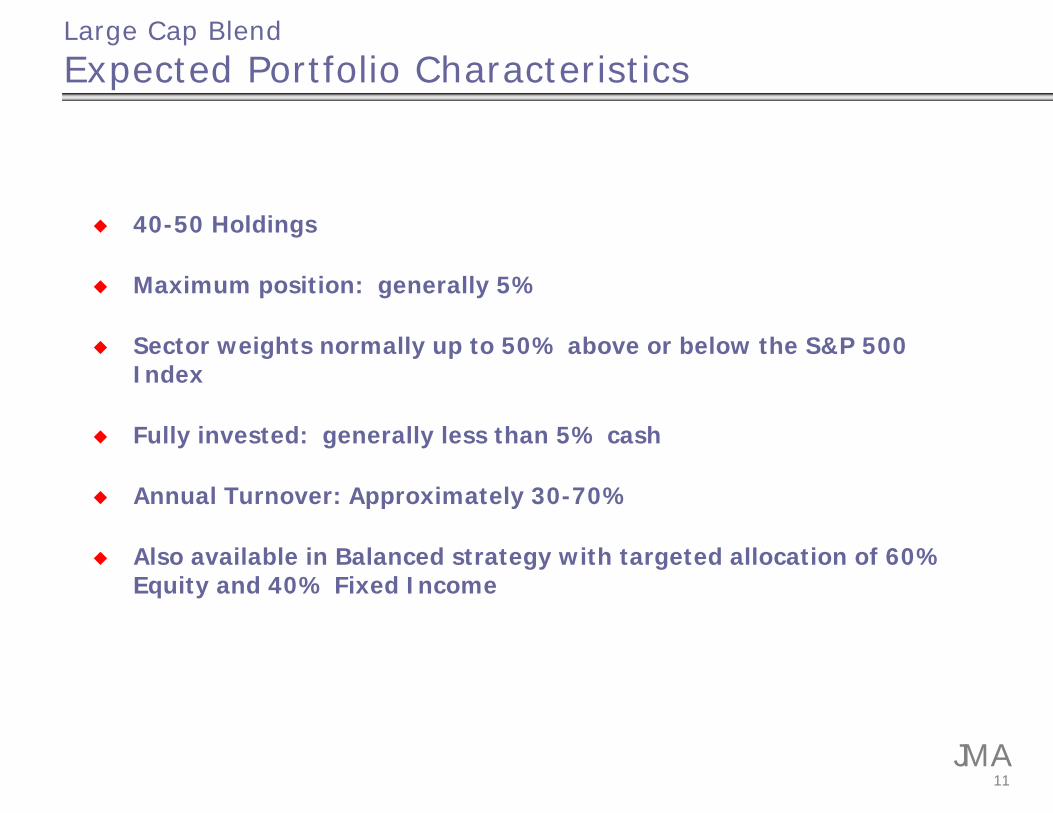

40-50 Holdings

Maximum position: generally 5%

Sector weights normally up to 50% above or below the S&P 500 Index

Fully invested: generally less than 5% cash

Annual Turnover: Approximately 30-70%

Also available in Balanced strategy with targeted allocation of 60% Equity and 40% Fixed Income

Large Cap Blend

Expected Portfolio Characteristics

12JMA

Balanced Option Lowers Total Portfolio Risk

Fixed Income target allocation is 40%35% to 45% range

High quality focus with U.S. government and agency securities (AAA Rated)

Strategic yield curve positioning to add incremental value

Maximum final maturity of all holdings is 10 years

JMA

Performance

14JMA

Large Cap Blend Equity Strategy PerformanceJune 30, 2004

*Inception date of Jennison’s portfolio management.Source for performance: Prudential Investments. Net performance reflects the deduction of actual program fees. Actual fees may vary depending on, among other things, the applicable fee schedule and portfolio size. Past performance does not guarantee future results. See Notes to Presentation 1 and 3.

2Q 2004 YTD 1 Year 3 Year Since

9/30/2000*

Gross 0.91% 1.60% 20.65% -2.42% -7.65%

Net 0.32 0.44 17.92 -4.73 -9.84

Russell® 1000 Index 1.40 3.33 19.48 -0.32 -4.65

S&P 500 Index 1.72 3.44 19.10 -0.69 -4.48

15JMA

Large Cap Blend Balanced Strategy PerformanceJune 30, 2004

*Inception date of Jennison’s portfolio management.Source for performance: Prudential Investments. Net performance reflects the deduction of actual program fees. Actual fees may vary depending on, among other things, the applicable fee schedule and portfolio size. Past performance does not guarantee future results. See Notes to Presentation 2 and 3.

2Q 2004 YTD 1 Year 3 Year Since

9/30/2000*

Gross -0.31% 0.95% 12.09% 1.89% -0.40%

Net -0.89 -0.24 9.46 -0.49 -2.71

60/40 Russell® 1000/LB Int. Gov. -0.08 1.94 11.27 2.72 0.37

60/40 S&P 500/LB Int. Gov. 0.11 2.01 11.06 2.48 0.46

JMA

Portfolio Characteristics

17JMA

%

19

6

17

13

23

6

9

5

0 0

3

11 1113

20

17

11

7

3 3 3

00

5

10

15

20

25

30

ConsumerDiscretion.

ConsumerStaples

Health Care Financials InformationTech.

Industrials Energy Materials Telecomm.Services

Utilities Cash

Portfolio Sector AllocationAs of June 30, 2004

See Notes to Presentation 4 and 5.

S&P 500 Index

Large Cap Blend Equity Strategy Model Portfolio

18JMA

Starbucks Corporation 3.5%Cisco Systems, Inc. 3.4Pfizer Inc. 3.3Yahoo! Inc. 3.2Intel Corporation Citigroup Inc. 3.0Merrill Lynch & Co., Inc. 3.0eBay Inc. 2.8Citigroup Inc. 2.7American Express Company 2.5Amgen Inc. 2.5

Total 29.9%

Largest Equity HoldingsAs of June 30, 2004

% of Model Portfolio

See Notes to Presentation 6.

19JMA

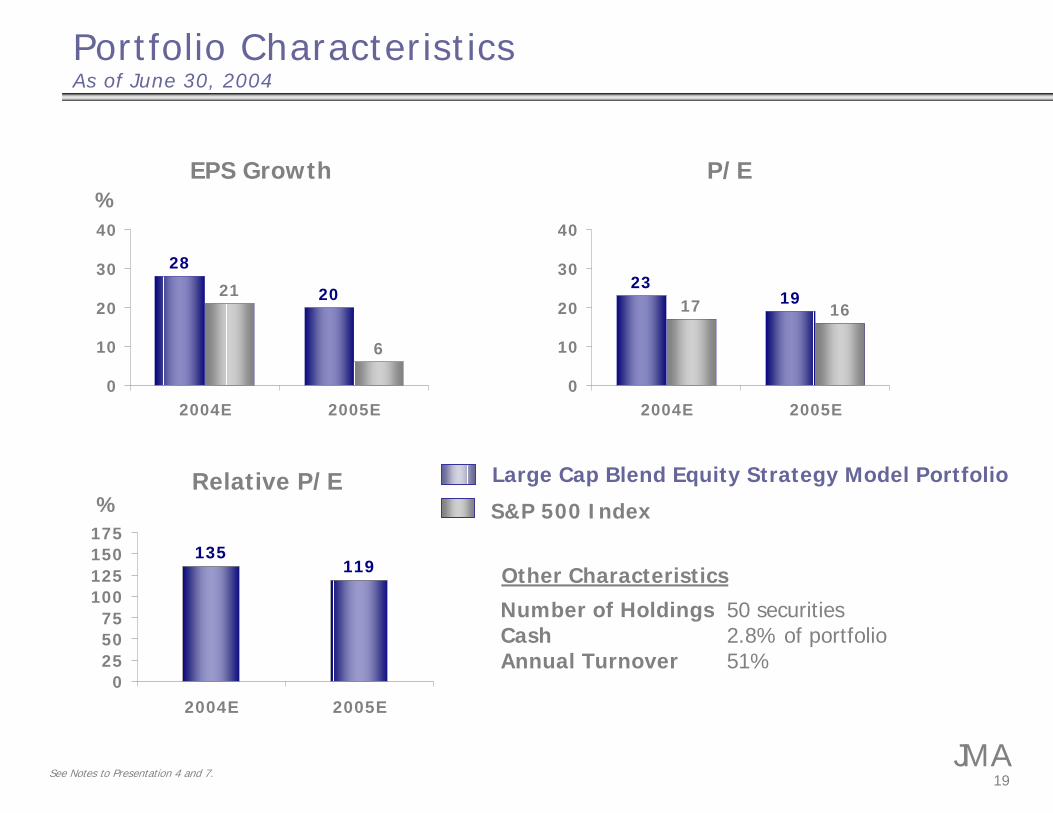

231917 16

0

10

20

30

40

2004E 2005E

See Notes to Presentation 4 and 7.

Portfolio CharacteristicsAs of June 30, 2004

EPS Growth P/E

Relative P/E

28

2021

6

0

10

20

30

40

2004E 2005E

%

S&P 500 Index

Large Cap Blend Equity Strategy Model Portfolio

135119

0255075

100125150175

2004E 2005E

%

Other Characteristics

Number of HoldingsCashAnnual Turnover

50 securities2.8% of portfolio51%

JMA

Summary

21JMA

“Growth In Value & Value In Growth”

Large Cap Blend Equity Strategy

22JMA

S&P Barra Value / S&P Barra Growth Relative Performance

1.0

1.2

1.4

1.6

1.8

2.0

74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04

VV VVVVVVGG GG GG

Value and Growth Perform in Cycles

Chart prepared by Jennison Associates LLC using information from Bloomberg. In order to construct the S&P 500 Barra Value and Growth Indices, companies are split into two groups based on price-to-book ratio to create growth and value indices. The Value index contains companies with lower price-to-book ratios, while the Growth index contains those with higher ratios. As of 6/30/04. See Notes to Presentation 4.

23JMA

-15%

-10%

-5%

0%

5%

10%

15%

20%

75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03

S&P BARRA Value minus Growth Quarterly Return Differences

Value Outperforms

Growth Outperforms

Value and Growth Performance Varies

Chart prepared by Jennison Associates LLC using information from Bloomberg. In order to construct the S&P 500 Barra Value and Growth Indices, companies are split into two groups based on price-to-book ratio to create growth and value indices. The Value Index contains companies with lower price-to-book ratios, while the Growth Index contains those with higher ratios. As of 6/30/04. See Notes to Presentation 4.

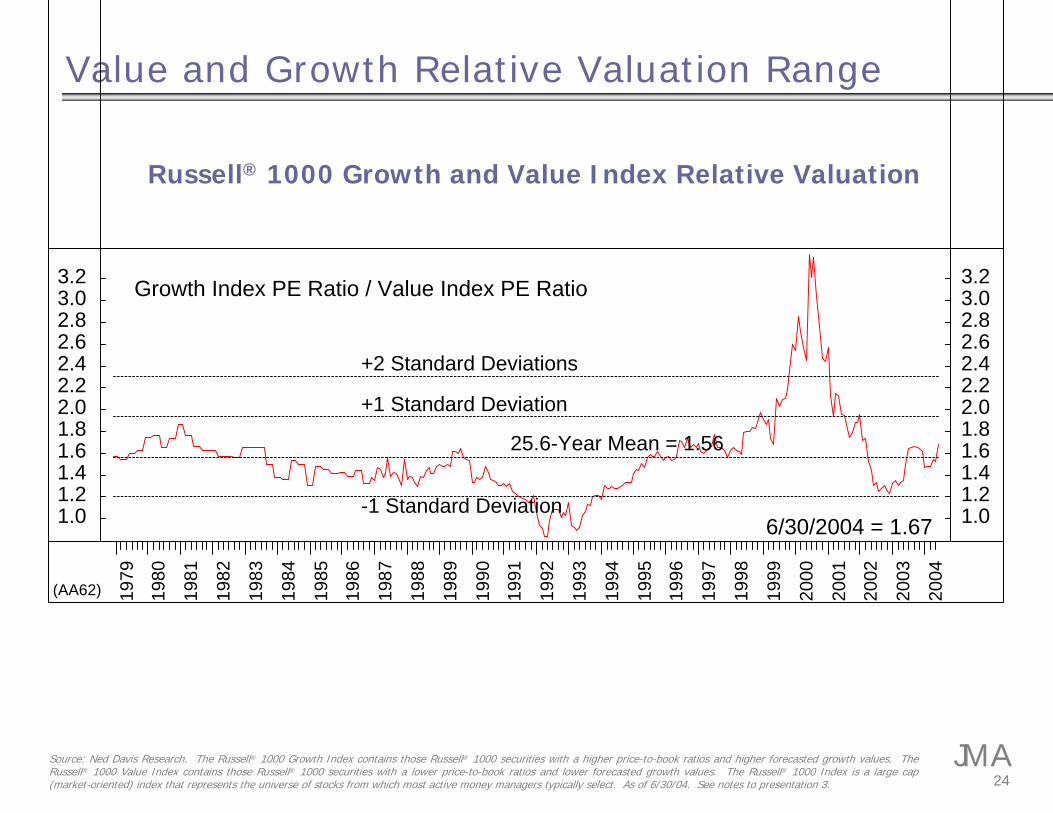

24JMASource: Ned Davis Research. The Russell® 1000 Growth Index contains those Russell® 1000 securities with a higher price-to-book ratios and higher forecasted growth values. The

Russell® 1000 Value Index contains those Russell® 1000 securities with a lower price-to-book ratios and lower forecasted growth values. The Russell® 1000 Index is a large cap (market-oriented) index that represents the universe of stocks from which most active money managers typically select. As of 6/30/04. See notes to presentation 3.

Value and Growth Relative Valuation Range

Russell® 1000 Growth and Value Index Relative Valuation

(AA62)

25.6-Year Mean = 1.56

+1 Standard Deviation

+2 Standard Deviations

-1 Standard Deviation

Growth Index PE Ratio / Value Index PE Ratio

6/30/2004 = 1.671.01.21.41.61.82.02.22.42.62.83.03.2

1.01.21.41.61.82.02.22.42.62.83.03.2

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

25JMA

Style diversification – Growth & Value

Access to attractive companies whose blend of growth and value characteristics may escape single-style managers

Access to experienced institutional portfolio management

Highly experienced, specialized blend equity team

Original Research

Selecting Jennison Large Cap Blend Equity

26JMA

Notes to Presentation1 The inception date of the Jennison Large Cap Blend strategy (formerly Prudential Investments Crossroads Equity) is July 1, 1995. Jennison became responsible for the portfolio management

of the Prudential Investments Large Cap Blend Strategy in September of 2000 pursuant to a transition of Prudential Financial's active public equity capabilities to Jennison. Performance forperiods since 9/30/2000 reflects returns generated solely by Jennison. The investment returns shown represent the historical performance of all fully discretionary accounts that have been managed under the Large Cap Blend strategy for at least one full calendar quarter. Returns for periods longer than one year are annualized. Some of the performance represented was achieved during a period of unprecedented returns in certain market sectors and may not be repeated. Past performance does not guarantee future results. The Russell® 1000 Index measures the performance of the 1,000 largest companies in the Russell® 3000 Index, which represents approximately 92% of the total market capitalization of the Russell® 3000 Index. The Standard & Poor’s 500 (S&P 500) Index is a market capitalization-weighted index of the common equity of 500 companies primarily traded on the NYSE. Investors cannot directly invest in an index.

2 The inception date of the Jennison Large Cap Blend Balanced strategy (formerly Prudential Investments Crossroads Balanced) is July 1, 1995. Jennison became responsible for the portfolio management of the equity portion of this strategy in September of 2000 pursuant to a transition of Prudential Financial's active public equity capabilities to Jennison. Performance for periods since 9/30/00 reflects returns generated by both Jennison and Prudential Investment Management (PIM). The investment returns shown represent the historical performance of all fully discretionary accounts that have been managed under the Large Cap Blend strategy for at least one full calendar quarter. Returns for periods longer than one year are annualized. Some of the performance represented was achieved during a period of unprecedented returns in certain market sectors and may not be repeated. Past performance does not guarantee future results. The 60/40 Russell® 1000 Index/Lehman Brothers Intermediate Government Bond Index is a blended index with 60% Russell® 1000 Index and 40% Lehman Brothers Intermediate Government Bond Index. The 60/40 S&P 500 Index/Lehman Brothers Intermediate Government Bond Index is a blended index with 60% S&P 500 Index and 40% Lehman Brothers Intermediate Government Bond Index. The Russell® 1000 Index measures the performance of the 1,000 largest companies in the Russell® 3000 Index, which represents approximately 92% of the total market capitalization of the Russell® 3000 Index. The Standard & Poor’s 500 (S&P 500) Index is a market capitalization-weighted index of 500 companies primarily traded on the NYSE. The Lehman Brothers Intermediate Government Index is an unmanaged index, and comprises U.S. Treasuries and agencies having 1- to 10-year maturities. Investors cannot directly invest in an index.

3 The Russell® Indicies are a trademark/service mark of the Frank Russell Company. Russell® is a trademark of the Frank Russell Company. The information in this presentation is confidential and further redistribution is prohibited.

4 Source for S&P 500 Index, S&P Barra Growth Index and S&P Barra Value Index: Bloomberg, Standard & Poor’s and FT Interactive Data Corporation. Jennison does not compile statistical or other data itself and relies on third-party vendors to provide such data. Although Jennison utilizes vendors that it believes are reliable, we can not guarantee the accuracy of such information as we do not control the methods used to compile such data.

5 Source for all data: Jennison Managed Accounts. Due to rounding, sector percentages may not sum to 100%. Sector classification of individual stocks is determined by Global Industry Classification standard developed by Standard & Poor’s in collaboration with Morgan Stanley Capital International. However, after periodic review, Jennison investment professionals may reclassify certain securities held in the portfolio. The cash percentage represents trade date cash and cash equivalents. It should not be assumed that future investments made on behalf of the Jennison Managed Accounts Large Cap Blend Equity Strategy Model Portfolio will be of comparable size in terms of percentage of the portfolio or will be as profitable or equal the performance of the securities currently held in the portfolio.

6 Source for all data: Jennison Managed Accounts. Due to rounding, percentages may not sum to total shown. These securities represent the largest positions held in the Jennison Managed Accounts Large Cap Blend Equity Strategy Model Portfolio as of 6/30/04 and do not represent all of the securities held in the model portfolio. Since accounts are individually managed actual holdings may vary from the holdings shown here and among other accounts. Neither the information contained herein nor any opinion expressed shall be construed to constitute an offer to sell or a solicitation to buy any securities mentioned herein. It should not be assumed that future investments made on behalf of the Jennison Managed Accounts Large Cap Blend Equity Strategy Model Portfolio will be of comparable size in terms of percentage of the portfolio or will be as profitable or equal the performance of the securities mentioned herein as well as those currently held in the portfolio. A list of all investments made on behalf of Jennison Managed Accounts throughout the past twelve months is available upon request.

7 Source for all data: Jennison Managed Accounts. The EPS Growth and P/E listed above are estimates determined by Jennison investment professionals. They are based on operating earnings per share and are subject to periodic change. Portfolio P/E is calculated using harmonic mean methodology. Certain securities for which earnings is not a primary basis for evaluation have been excluded from the calculation of EPS Growth and P/E. A list of those securities is available upon request. Relative P/E is the portfolio P/E divided by the Index P/E. The cash percentagerepresents trade date cash and cash equivalents. It should not be assumed that future investments made on behalf of the Jennison Managed Accounts Large Cap Blend Equity Strategy Model Portfolio will be of comparable size in terms of percentage of the portfolio or will be as profitable or equal the performance of the securities currently held in the portfolio. A list of allinvestments made on behalf of Jennison Managed Accounts throughout the past twelve months is available upon request.

27JMA

Why Core Mutual Funds?

Potential problems with separate growth and value funds:

Too much concentration in one sector and/or stock

Too much cash over market cycle

Core Fund Managers have the option to retain stocks that transition from value to growth or growth to value

The GOAL is Selecting and Keeping the Best Stocks

Growth Funds+

Value FundsCORE

TMahoney:

Use this additional slide?

TMahoney:

Use this additional slide?