latino-owned businesses shining a light on national trends · latino business owners tend to rely...

TRANSCRIPT

A

LATINO-OWNED BUSINESSES

Shining a Light on National Trends

B

PUBLISHEDNovember 2018

AUTHORSClaire Kramer Mills, Ph.D. AVP, Federal Reserve Bank of New York

Jessica Battisto Senior Analyst, Federal Reserve Bank of New York

Scott Lieberman Senior Analyst, Federal Reserve Bank of New York

Marlene Orozco Lead Research Analyst, Stanford Latino Entrepreneurship Initiative

Iliana Perez, Ph.D. Research Analyst, Stanford Latino Entrepreneurship Initiative

Nancy S. Lee, Ph.D. Senior Manager, Research and Evaluation, Interise

The views and opinions expressed here are solely those of the authors and do not necessarily reflect those of the Federal Reserve Bank of New York or Federal Reserve System.

i

TABLE OF CONTENTS

TABLE OF CONTENTS

GLOSSARY AND DATA SOURCES iiGlossary of Terms iiData Sources and Focus on Employer Firms ii

EXECUTIVE SUMMARY ivKey Findings iv

INTRODUCTION vii

1 LATINO DEMOGRAPHICS 1

2 NATIONAL SMALL BUSINESS TRENDS 4Growth and Importance of Latino-owned Businesses 6Performance of Latino-owned Businesses 6Financial Challenges: Persistent Operating Expense and Credit Availability Issues 9

3 TOP TEN LATINO METROPOLITAN AREAS BY POPULATION 22Overview 22Latino Entrepreneurship Score 23Key Findings 24Discussion 34

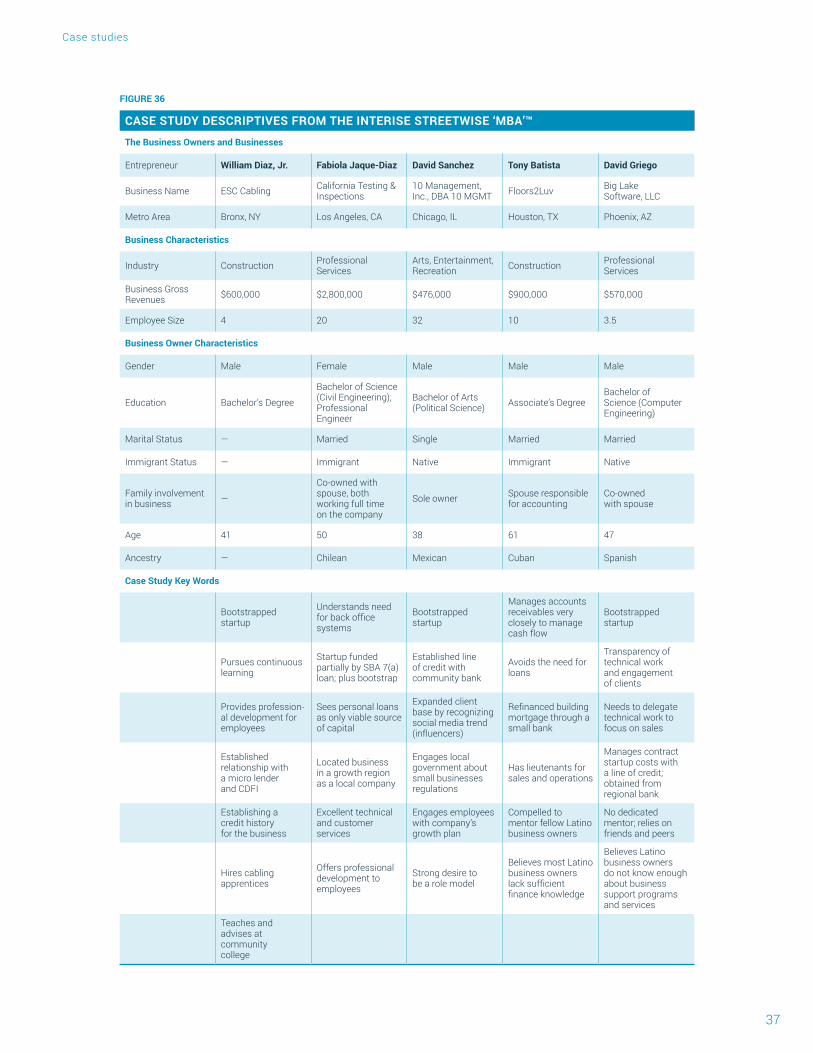

4 CASE STUDIES 35Overview 35Case Study Method 35Themes Among Scaled Firms 38Themes Among Unscaled Firms 38Overview of Cases 39

5 BEST PRACTICES FOR SCALING 46

6 KEY FINDINGS AND FUTURE RESEARCH 48Future Research 49

7 APPENDICES 52Appendix A: Survey Methodologies 52Appendix B: Top Ten Metro Area Characteristics 53Appendix C: About the Collaborating Organizations 56

ii

GLOSSARY AND DATA SOURCES

Glossary of Terms This report uses several terms repeatedly. In order to clarify the specific meanings used in this report, we define these terms below.

� Employer firm: A firm with part-time or full-time employees on payroll. These firms are poised to have the greatest impact on the economy and job creation compared to nonemployer firms.

� General chamber of commerce: A general chamber of commerce refers to any state, local, regional, or national business chamber of commerce that is not identity-specific (e.g. Hispanic chambers of commerce, black chambers of commerce, LGBT chambers of commerce).

� Metropolitan Statistical Area (MSA): A geographic region with a population density typically centered around a single, large city but expanding across a large region. MSAs are used by the Census Bureau and other agencies for statistical purposes and are defined by the U.S. Office of Management and Budget.

� Microbusiness: A business generating less than $100,000 in annual revenue.

� Nonemployer firm: A firm with no paid employees, annual business receipts of $1,000 or more ($1 or more in the construction industry), and subject to federal income taxes. These firms make up three-quarters of all U.S. businesses but account for only about three percent of business receipts, according to the Small Business Administration.

� Scale/scaling/scaled: A firm that is generating at least $1,000,000 in annual revenue.

� Unscaled: A firm that is not yet generating $1,000,000 in annual revenue.

Data Sources and Focus on Employer FirmsThis report draws on a variety of data sources, both quantitative and qualitative. A short descrip-tion of the range of sources referenced in this report, from Census data to surveys to detailed interviews with entrepreneurs, is found in the following paragraphs.

Timely and detailed data about small business growth potential, including the ability to access financing, is scarce. For national and state trends, researchers have relied heavily on two datasets from the U.S. Census Bureau: the Survey of Business Owners (SBO) and Annual Survey of Entre-preneurs (ASE). The SBO surveys both employer and nonemployer businesses and is conducted every five years (in years ending in two and seven), but contains limited financing questions. The ASE, which commenced in 2014, provides more frequent data (the first survey was released in 2016 and has been updated annually) but examines only employer firms. Beginning in 2017, the Census Bureau initiated a new survey called the Annual Business Survey (ABS) to replace the ASE and the SBO. The ABS will only survey employer firms and will contain more detailed questions on financing and credit market experiences, but limits public access to tabulations that provide sum-

iii

Glossary and data sources

mary statistics of business sales and receipts; annual payroll; employment broken out by firm size, age, and industry; and owner characteristics such as gender, race, ethnicity, and veteran status.1,2

While the ABS will be a critical source of small business information, data gaps remain, including detailed and accessible information on the performance and financing experiences of particular segments of firms (for example, the growing share of minority-owned firms). The Stanford Graduate School of Business’ Latino Entrepreneurship Initiative (SLEI) and the Federal Reserve Banks have launched surveys to help address these gaps: the SLEI Survey of U.S. Latino Business Owners and the Federal Reserve Banks’ Small Business Credit Survey (SBCS). The SLEI survey focuses exclusively on Latino-owned businesses,3 while the Fed’s survey draws upon a broader sample of business owners, including Latino-owned businesses, enabling comparisons between minority- and white-owned firms.4,5 To construct a more complete picture about the growth opportunities and challenges facing Latino-owned businesses, this report draws upon evidence from the Census Bureau, SLEI, Interise, and the Federal Reserve Banks.

The Federal Reserve Banks’ Small Business Credit Survey was developed as a complement to existing surveys in the wake of the Financial Crisis, with a specific emphasis on the financing needs and outcomes of small businesses nationwide. The survey dives far beyond demographics, including detailed questions about debt holdings, credit applications and outcomes, and financial challenges facing small businesses. These questions provide a unique lens to track the individual experiences of businesses that are not captured in aggregate demographic statistics.

Relatedly, the SLEI Survey of U.S. Latino Business Owners provides important information on the state and growth of Latino-owned businesses by asking in-depth questions about the business (e.g. regulatory impacts on profitability, export markets, operations, capital types, etc.) and the business owner’s characteristics (e.g. motivations, family history, year of immigration, etc.). Other similar data are often regional in nature and/or limited to small sample sizes. As a result, the implications are often limited to singular geographies and the data cannot be cut to look at specif-ic patterns by industry, gender, revenue, immigrant status, and region to better understand the heterogeneous experiences of Latino business owners.

In this report, we focus specifically on employer firms—those with part- or full-time employees on payroll in addition to the business owner—unless otherwise specified. Though these firms com-prise approximately 23.8 percent of small business establishments,6 they are responsible for a disproportionate share of revenue and job growth within the small business sector.7 Among Latinos, employer firms make up about nine percent of the business ecosystem.8

1 https://www.census.gov/programs-surveys/abs/about.html2 Additional sources of information include the U.S. Census Bureau’s County Business Patterns/Zipcode Business Patterns

(CBP/ZBP) and Nonemployer Statistics series. Both of these are available at the U.S. and state levels. Nonemployer Statistics are available for the 50 most populous MSAs. CBP/ZBP contains further geographic detail. However, both exclude detailed statistics by the race, ethnicity, and gender of owner. Statistics of U.S. Businesses is also available at the US, state, MSA, and county levels, but with minimal demographic information.

3 The SLEI survey defines Latino interchangeably with the ethnicity “Hispanic or Latino” reported on Census Bureau surveys. Non-Latino refers to the “Not Hispanic or Latino” ethnicity.

4 For detailed information about survey methodologies, please see Appendix A.5 The SBCS considers a business more than 50% owned by Hispanic or Latino owners as a Hispanic/Latino-owned business,

regardless of race. White-owned firms are firms where at least half of the business is owned by non-Hispanic white owners.6 Authors’ calculations based on County Business Patterns & Nonemployer Statistics. See also https://www.census.gov/library/

stories/2018/09/three-fourths-nations-businesses-do-not-have-paid-employees.html7 Mishel, L. and Wolfe, J. (2018). “Nonemployer establishments grew in 2016 but their real revenues were stable: This confirms other

data on self employment showing more activity, but little impact.” Economic Policy Institute. Available: https://www.epi.org/blog/ nonemployer-establishments-grew-in-2016-but-their-real-revenues-were-stable-confirming-other-data-on-self-employment- showing-more-activity-but-little-economic-impact/

8 Orozco, M., Oyer, P., & Porras, J. (2017). State of Latino Entrepreneurship 2017. Stanford Latino Entrepreneurship Initiative. Available: https://www.gsb.stanford.edu/sites/gsb/files/publication-pdf/report-slei-state-latino-entrepreneurship-2017.pdf

iviv

EXECUTIVE SUMMARY

9 U.S. Hispanic Chamber of Commerce10 Haltiwanger, J.C., Jarmin, R.S., & Miranda, J. (2012.) “Who Creates Jobs? Small vs. Large vs. Young.” NBER Working Paper No. 16300.

Available: https://www.nber.org/papers/w1630011 Ibid (8)12 Fairlie, R.; Morelix, A.; Reedy, E.J.; and Russell, J. (2015). “The Kauffman Index: Startup Activity, National Trends.” Ewing Marion

Kauffman Foundation.13 Haltiwanger, J.C., Jarmin, R.S., & Miranda, J. (2012.) “Who Creates Jobs? Small vs. Large vs. Young.” NBER Working Paper No. 16300.

Available: https://www.nber.org/papers/w16300; Alvarez, Sarah. (2017). Unleashing Latino-owned Business Potential: A Report of the Aspen Institute Forum on Latino Business Growth. The Aspen Institute Latinos & Society Program.

Latino-owned businesses are growing in number and importance to the American economy. Contributing more than $700 billion in sales to the economy annually,9 they are also an important source of employment as sole proprietors and as firms with employees on payroll. The 2012 U.S. Census Survey of Business Owners estimated that Latino-owned firms have 2.3 million employees on payroll, a number that by several counts has grown since the survey’s release. One in four new businesses, traditionally key sources of new jobs,10 is now Latino-owned. Quite simply, small business growth is tied to the fortunes of Latino-owned businesses.

Yet, research also shows that Latino-owned firms face significant growth barriers. Estimates from the Stanford Latino Entrepreneurship Initiative (SLEI) highlight that only three percent of Latino- owned businesses grow to $1,000,000 or more in annual revenues, compared to six percent of white-owned businesses.11 In short, despite impressive numbers of startups, Latino-owned firms tend to stay small.12

This report builds on earlier work from SLEI and the Aspen Institute13 to probe firm-level and environmental-level growth factors that influence Latino business performance. By comparing Latino-owned firms to non-Latino white-owned firms, unscaled Latino-owned firms to scaled firms, and metro areas of relatively strong Latino entrepreneurship to those with smaller shares of Latino-owned businesses, we are able to discern the most acute challenges and begin to highlight remedies to these challenges. This report’s goal is to focus attention on potential investments at the firm- and community-level that will advance Latino business growth. It draws on analysis of U.S. Census Bureau data, surveys from SLEI and the Federal Reserve Banks, interviews with the owners of scaled and unscaled Latino-owned firms as part of a research collaboration between Stanford Graduate School of Business, the Federal Reserve Bank of New York, and Interise.

Key Findings1. Latino business owners tend to rely on informal financing and are frequently averse

to taking on debt.

� Latino business owners tend to depend on personal savings and seed funding from friends and family to start their businesses.

� Latino entrepreneurs state they are averse to amassing debt to support the business, and that such financing is often not available at acceptable terms.

v

Executive summary

� Reliance on personal funds and loans from family/friends can cause a deterioration of personal credit and inhibit scaling.

2. Latino business owners bear greater personal financial risk, related to lower credit scores and limited credit histories.

� Latino business owners are more likely than non-Latino white business owners to use credit cards, factoring, and merchant cash advances—products that require less collateral and are associated with higher average interest rates.

� Latino-owned firms are also much more likely to use personal guarantees than business assets to secure financing (47 percent compared to 34 percent).

� Latino-owned businesses report being medium or high credit risk at higher rates than non-Latino white-owned firms: 49 percent compared to 29 percent. These patterns are consistent with the fact that a higher proportion of Latino-owned businesses are startups, but also suggest a limited ability to secure affordable growth capital.

3. Latino business owners face significant financial challenges compared to white business owners.

� Despite reporting comparable patterns of revenue growth, employment growth, and profitability as non-Latino white-owned businesses, Latino-owned businesses report acute operating expense and credit availability issues.

� These challenges are equally common among unscaled and scaled Latino-owned busi-nesses, with 44 percent of scaled firms stating that they have difficulties paying operating expenses and 35 percent reporting credit availability issues. In fact, scaled Latino-owned businesses are more likely to report credit availability issues than unscaled non-Latino white-owned businesses.

� Latino-owned businesses applied for financing in 2017 at slightly higher rates than non- Latino white-owned businesses—47 percent compared to 40 percent—but were much more likely to experience funding shortfalls: 28 percent received full funding, compared to 49 percent of non-Latino white-owned businesses. What’s more, the funding gaps are especially acute for the large share—97 percent—of Latino-owned businesses with $1,000,000 or less in annual revenues: 40 percent of loan and line of credit applicants received none of the financing applied for, compared to only 23 percent of non-Latino white-owned businesses.

4. Operational challenges differ for scaled and unscaled Latino-owned businesses.

� Scaled firms are facing talent shortages, citing smaller pools of skilled workers. These firms are considering ways to develop talent and create unique value propositions in order to set themselves apart.

� Unscaled firms cite difficulty accessing credit to help manage cash flow and to fund startup costs related to expansion and procurement.

vi

Executive summary

5. Metro areas with the highest concentrations of Latinos do not necessarily have the densest shares of Latino entrepreneurs.

� The external funding network (including availability of alternative lenders, e.g. CDFIs), local economic development that favors certain industries (e.g. construction), property values, state minimum wage laws, and local and state tax rates all play critical roles in supporting Latino entrepreneurs.

� Among areas with the densest Latino populations, only Miami and Chicago have commensurate entrepreneurship rates.

6. Latino-owned businesses have more success with relationship banking.

� The most common forms of capital that Latino-owned small businesses need are lines of credit, loans, and cash advances, like many small businesses.

� Latino business owners have more success working with small, local banks than large or national banks. Latino business owners in areas like Chicago and Houston use local banks at ten times and six times the rate of national banks, respectively.

� At small banks, there is greater opportunity for developing personal relationships with bankers and getting advice.

7. Latino-owned firms have opportunities to diversify and expand their revenue sources, including B2B and government sales.

� A majority of Latino-owned firms (64 percent) sell to individuals.

� Forty-two percent of Latino-owned businesses sell to other businesses, compared to 47 percent of non-Latino white-owned businesses.

� Despite incentives in state, local, and federal government procurement, only 16 percent of Latino-owned firms sell to state/local government and only 11 percent sell to the federal government. These percentages are identical to those of non-Latino white-owned businesses.

8. Density of existing business networks makes certain geographies more hospitable to Latino business growth, as do mentorship and capacity building programs.

� Latino business owners in the San Diego area participate in trade associations at nearly twice the rate of trade association participation among Latinos nationally (23 percent compared to 12 percent). There is also high trade association participation in Miami at 19 percent.

� Latino business owners in the Phoenix area participate in Hispanic chambers of commerce at nearly three times the rate of the national participation among Latinos (28 percent compared to ten percent).

� Experienced mentors help Latino business owners overcome business and environmental hurdles and can serve as models for success. Multiple business owners cited engaging mentors and participating in business organizations and executive education programs as ways to obtain information on new opportunities and further business support.

vii

INTRODUCTION

14 Passel J., Cohn D., & Lopez M. (2011). “Hispanics Account for More than Half of Nation’s Growth in Past Decade.” Pew Research Center. Available: http://www.pewhispanic.org/2011/03/24/hispanics-account-for-more-than-half-of-nations-growth-in-past-decade/

15 Alonzo, F. (2018). “Hispanic Heritage Month.” US Census Bureau https://www.census.gov/newsroom/facts-for-features/2018/hispanic-heritage-month.html

16 (2016). “Business Employment Dynamics: Entrepreneurship and the U.S. Economy.” US Bureau of Labor Statistics. https://www.bls.gov/bdm/entrepreneurship/entrepreneurship.htm

17 Pekkala Kerr, S. and W.R. Kerr. (2016). “Immigrants Play a Disproportionate Role in American Entrepreneurship.” Harvard Business Review. Available: https://hbr.org/2016/10/immigrants-play-a-disproportionate-role-in-american-entrepreneurship

18 US Census Bureau, Annual Survey of Entrepreneurs 2014, 2016.19 The collaboration began at a conference of the Aspen Institute’s Latinos & Society Program in June 2017.

Our thanks to Monica Lozano and Abigail Golden-Vazquez for their leadership in convening the group.

The Latino population in the United States has grown rapidly, accounting for more than half of the nation’s population growth from 2000 to 2010.14 As of 2017, Latinos comprised 18 percent of the total U.S. population and population projections suggest that figure will climb to 28 percent by 2060,15 which means one of every four residents in the U.S. will be Latino. Amid lagging business startup rates,16 immigrant and Latino business growth has bolstered the small business sector. One study found that, although immigrants constitute 15 percent of the U.S. workforce, they account for one quarter of U.S. entrepreneurs, and that share has grown over time.17 The growth of Latino-owned businesses has outpaced that of other demographic groups; specifically, the number of majority Latino-owned employer businesses increased more than 13 percent between 2014 and 2016, compared to less than three percent growth for non-Latino-owned businesses. In the same time period, employment among Latino-owned employer businesses increased by over 14 percent, more than twice the employment growth of non-Latino-owned businesses.18

Despite this rapid growth, the share of Latino employer firms relative to the Latino population remains low, a trend that the Stanford Latino Entrepreneurship Initiative (SLEI) calls the “Latino Entrepreneurship Gap.” As a share of the population, non-Latinos own employer firms at nearly three times the rate of Latinos. What are the circumstances that make it harder for Latinos to start businesses and for Latino-owned firms to thrive and scale? How are Latino entrepreneurs navigat-ing the complex task of running a business, and how might their experiences differ from other en-trepreneurs? This report, the result of collaboration between SLEI, Interise, and the New York Fed,19 aims to illuminate the challenges and opportunities facing Latino entrepreneurs. We utilize unique data assets, including the Federal Reserve Banks’ Small Business Credit Survey, SLEI’s Survey of U.S. Latino Business Owners, and interviews with Latino business owners conducted by SLEI and Interise to highlight opportunities for unleashing the potential of Latino-owned firms and creating a more equitable and successful business climate.

11

LATINO DEMOGRAPHICS

Census data, specifically the Annual Survey of Entrepreneurs (ASE), offer a unique look at the demographics of Latino-owned employer firms and entrepreneurs, compared to the rest of the U.S. business population. Overall, Latino-owned firms are smaller, younger, have younger manage-ment, and are slightly more concentrated in a few industry categories including transportation, construction, leisure & hospitality, and administrative services.

The following industry figure compares the types of businesses owned by Latinos and non-Latinos using the North American Industrial Classification System (NAICS). High concentrations of Latino- owned businesses are found in the Transportation and warehousing (NAICS 51) and Construction (NAICS 23) sectors, which are contained in the “Non-manufacturing goods production & associated services” category; these represent one in four Latino-owned firms. Latino-owned businesses are also more concentrated in the Leisure & hospitality category, specifically in the Accommodation & food services industries (NAICS 72), than non-Latino-owned businesses. There is also a large concen tration of Latino-owned businesses in the industry of Administrative and support and waste management and remediation services (NAICS 56) relative to non-Latino-owned businesses. In contrast, Latino-owned businesses are underrepresented in the Professional, scientific, and techni-cal services sector (NAICS 54).

1

FIGURE 1

Non-manufacturing goods production & associated services

Professional services, information, real estate & management of companies

Administrative support, waste management, and other services

Manufacturing

Retail trade

Leisure & hospitality

Finance & insurance

Education & healthcare

Latino-owned Non-Latino-

owned

INDUSTRY

Source: Annual Survey of Entrepreneurs, 2016.

22%26%

4%4%

12%11%

11%14%

4%3%

12%11%

22%15%

13%17%

2

Latino demographics

A second notable difference between Latino- and non-Latino-owned employer firms is the age of businesses. Nearly half of Latino-owned businesses were started less than six years ago, compared to 33 percent of non-Latino-owned firms. In the following figures, we compare the age distribution of firms with Latino ownership to those with non-Latino or equally Latino/non-Latino ownership. Latino-owned businesses tend to be younger, in aggregate, than non-Latino firms; only 19 percent of Latino-owned businesses are at least 16 years old, compared to 34 percent of non-Latino-owned businesses. While there is a dynamism to young firms, financial challenges are common, including the ability to secure loan financing, which often requires a minimum of two years of tax receipts.

Latino-owned businesses also tend to be a bit smaller, on average, than non-Latino-owned businesses. Non-Latino-owned businesses are nearly twice as likely to have 100 or more employ-ees compared to Latino-owned businesses, and more than twice as likely to have 500 or more employees. Latino-owned businesses are more likely to report having one to four employees than non-Latino-owned businesses.

AGE OF FIRM (Years in Business)

16 or more 11–15 6–10 4–5 2–3 Less than 2

Latino- owned

Non-Latino-owned

19%

13%

22%

13%

19%

14%

34%

14%

19%

10%

14%

9%

Source: Annual Survey of Entrepreneurs, 2016.

Latino- owned

Non-Latino-owned

NUMBER OF EMPLOYEES

50 or more 20–49 10–19 5–9 1–4 0

Source: Annual Survey of Entrepreneurs, 2016.

2%5%

11%

17%

55%

11%

3%

7%

11%

18%

52%

10%

FIGURE 2 FIGURE 3

3

Latino demographics

Demographically, the Latino population in the U.S. is younger than the non-Latino population— in 2017, the median age of the Latino population was 29, compared to the median age for the entire U.S. population of 38.20 Similarly, Latino business owners tend to be younger than non-Latino business owners—33 percent of Latino entrepreneurs are younger than 45, compared to just 22 percent of non-Latino entrepreneurs.

Finally, we look at the share of business owners born in the U.S., since immigrants are more likely to start businesses than non-immigrants. Among employer firms, fifty-one percent of Latino busi-ness owners were not born citizens of the U.S., compared with only fourteen percent of non-Latino business owners. This may be a factor in Latino business starts among employer firms, but it may also present challenges as immigrant business owners may lack established credit histories or financial and business networks that can help to accelerate growth.

20 US Census Bureau, 1-year American Community Survey, 2017.

AGE OF OWNER

65 or over 55–64 45–54 35–44 Under 35

Latino Non-Latino

10%

23%

34%

24%

9%

20%

31%

27%

16%

6%

Source: Annual Survey of Entrepreneurs, 2016.

FIGURE 4

4

NATIONAL SMALL BUSINESS TRENDS

21 A firm is classified as “Latino-owned” if more than half of the business is owned by a person/persons who is/are Hispanic.22 Battisto, J., deZeeuw, M., Kramer Mills, C., Lieberman, S., and Wiersch, A.M.(2017). Small Business Credit Survey: Report on Employer

Firms, Federal Reserve Banks. Available: https://www.fedsmallbusiness.org/medialibrary/fedsmallbusiness/files/2018/sbcs- employer-firms-report.pdf

23 Ibid (15)24 Ibid (10)25 Ibid (10)26 Rodriguez, N. (2017). 8 Facts about Latino-Owned Businesses. Stanford Latino Entrepreneurship Initiative. Available:

https://www.gsb.stanford.edu/sites/gsb/files/publication-pdf/academic-publication-slei-8-facts-latino-businesses.pdf27 Ibid (8)

This section describes how the business performance of Latino-owned small employer firms21 (in this section, referred to as “Latino-owned businesses”), their key financial challenges, and their financing experiences compare to those of non-Latino white-owned small employer firms (hereafter, referred to as “white-owned businesses”).

The economy for small business in the U.S. is strong and improving, but revenue and startup statistics alone do not tell the full story. In 2017, most small businesses exhibited growth, with 57 percent of small employer firms reporting profitability and 53 percent reporting increased revenue in the Federal Reserve Banks’ 2017 Small Business Credit Survey (SBCS).22 Expectations for future growth reflect a strong economic environment, with 72 percent of employer firms expecting that revenue will increase in the next year and 48 percent expecting to hire more employees in that same timeframe.23

Although small business revenues and profits are growing, firms are not reporting increased demand for new financing. In fact, the trends reflect the opposite. Forty percent of respondents to the 2017 SBCS reported applying for financing in the last year, down from 45 percent in 2016.24 Meanwhile, 64 percent of firms reported financial challenges for their business in the past year, with operating expenses (60 percent of respondents), credit availability (30 percent), and debt payments (25 percent) as the top three challenges. Most firms (67 percent) used personal funds to overcome these financing problems.25

The small business climate varies across demographic lines, including ethnicity, race, income, and gender. Between 2007 and 2012, the number of Latino-owned businesses increased by 47 percent, while the number of non-Latino-owned businesses decreased by two percent.26 Post-recession, the growth rate of Latino-owned businesses continues to outpace that of any other demographic group.27 However, the factors leading to business creation, challenges to growth, and performance of Latino-owned firms differ from their white and non-Latino counterparts.

Latino and black business owners may be more likely to begin their businesses out of necessity (referred to as necessity entrepreneurship) than non-Latino white and Asian business owners. The Kauffman Foundation defines necessity entrepreneurs as those who are unemployed before starting their business, possibly reflecting the higher unemployment rate of Latinos and black Americans (5.4 percent for Latinos and 8.4 percent for blacks as compared to 4.9 percent overall

2

5

National small business trends

in 2016).28 It should be noted that in addition to the motivations being racially and ethnically dis-tinct, patterns may also be gendered. Data from SLEI’s most recent survey show Latinas report more necessity-driven reasons for starting a business, such as greater work-life balance and flexible work arrangements, compared to men.29

The Kauffman Foundation study reports that non-Latino white and Asian business owners are more likely to begin their businesses out of opportunity (opportunity entrepreneurship).30 Revealing an emerging trend, SLEI’s most recent data show that opportunity-driven motivations are also primary drivers for Latino entrepreneurship overall. As such, differences in motivation do not suffi-ciently explain differences in outcomes.

Moreover, there is a disparity between Latinos and non-Latinos in access to financial capital from financial institutions. According to research compiled by SLEI, 69 percent of Latino-owned business-es use personal savings for financial capital, compared to 62 percent of non-Latinos. Furthermore, 12 percent of Latinos get financing from friends, as compared to only three percent of non-Latinos. Only six percent of Latinos access funding through commercial banks, compared to 11 percent of non-Latinos.31

The racial and ethnic wealth gap in the U.S. presents an added challenge for Latino entrepreneurs: Latinos have a median wealth of $13,730, which is about ten percent of the median wealth of white Americans.32 The pool of available financial capital for a group that largely draws from personal and friends’ savings is significantly smaller than groups that are more likely to draw from financial institutions. According to the Kauffman Foundation, small businesses with $5,000 or less in startup capital are 23 percent more likely to fail than those with $100,000 or more33 and $100,000 is more than seven times the average wealth of an American Latino. Access to capital presents a troubling challenge to specific demographics of business owners.

The wealth gap, along with access to education and family background, presents more challenges to the average Latino or black business owner than to the average white or Asian business owner in the U.S. For example, Asian and white Americans are more likely to have college degrees (50 percent and 29 percent, respectively) than black and Latino Americans (18 percent and 13 percent, respectively). However, it should be noted that these trends look different among the business owner population. For example, Latino business owners hold a college degree at more than twice the rate of the general Latino population.34 Still, entrepreneurs with college diplomas are more likely to have revenue over $100,000 and paid employees than those without.35

Evidence also suggests that people who know entrepreneurs are more likely to be successful entrepreneurs themselves.36 Presently, Latinos demonstrate a family history of entrepreneurship with 51 percent of entrepreneurs reporting a family history of entrepreneurship with a close family member currently or previously owning a business.37 However, because Latino-owned

28 Quittner, J. (2016) “It’s Hard to Tell Who’s Driving the Uptick in Minority Entrepreneurship.” Fortune. Available: http://fortune.com/ 2016/08/05/whos-driving-minority-entrepreneurship/

29 SLEI forthcoming report. 30 Fetsch, E. (2016). “Including People of Color in the Promise of Entrepreneurship.” Entrepreneurship Policy Digest. Kauffman Foundation.

Available: https://www.kauffman.org/what-we-do/resources/entrepreneurship-policy-digest/including-people-of-color-in-the-prom-ise-of-entrepreneurship

31 Ibid (18)32 Ibid (15)33 Ibid (15)34 Ibid (8)35 Ibid (15)36 Ibid (15)37 Ibid (8)

6

National small business trends

businesses tend to start small and stay small, the role modeling effect may not be as consequen-tial as previously thought, especially if the benefit of family entrepreneurship comes in the form of resource provision.

Despite the growth in number of Latino-owned businesses, ethnic and racial disparities are not necessarily lessening. There is still work to do to improve the small business climate for all types of entrepreneurs and business owners. The following section describes the business performance of Latino-owned employer firms, their key financial challenges, and their financing experiences compared to those of white-owned firms.

Growth and Importance of Latino-owned BusinessesTwo key facts underscore the economic importance of Latinos and Latino-owned businesses: 1) Latinos own an increasing number and share of businesses and 2) Latinos start approximately one in four new businesses in the U.S.—a critical source of new jobs in the economy.38

� Based upon Census data, Latinos owned 12 percent of all businesses in 2012, up from eight percent in 2007.39 Between 2007 and 2012, the number of total Latino-owned businesses grew by 46 percent compared a 0.2 percent decline in the number of non- Latino-owned businesses.40

� Between 1996 and 2016, the Latino share of new entrepreneurs rose from ten percent to 24 percent, consistent with longer-term rising rates of Latino entrepreneurship and their growing share of the U.S. population.41 During this same time period, the white share dropped from 77 percent to 56 percent.

Performance of Latino-owned Businesses

Concentration of Smaller FirmsGiven the growth in number and share of Latino-owned businesses, their performance and future growth is of increasing significance to the national economy and to the vitality of local communi-ties. Previous studies42 have examined various measures of performance, including the percentage of firms growing to scale—or having generated at least $1,000,000 in annual revenues. As detailed below from the 2017 SBCS data,43 Latino-owned businesses are generally smaller than white-owned businesses: 21 percent of Latino-owned employer firms reported revenues greater than $1,000,000 compared to 32 percent of white-owned employer firms. What’s more, Latino-owned employer firms are twice as likely as white-owned employer firms to be microenterprises, or firms with $100,000 or less in annual revenues (34 percent compared to 17 percent, respectively).

38 Haltiwanger, J., R.S. Jarmin, and J. Miranda. (2013). “Who Creates Jobs? Small Versus Large Versus Young.” The Review of Economics and Statistics 95, No. 2.

39 Bernstein, R. (2016). “Hispanic-Owned Businesses on the Upswing.” U.S. Census Bureau. Available: https://www.census.gov/ newsroom/blogs/random-samplings/2016/12/hispanic-owned_busin.html

40 Authors’ calculations from Survey of Business Owners.41 Morelix, A. Fairlie, R. and Tareque, I. (2017). Kaufman Index of Startup Activity. Ewing Marion Kauffman Foundation.42 Ibid (41)43 References to the Small Business Credit Survey refer to small businesses, defined as businesses with fewer than 500 employees.

7

National small business trends

Strong Revenue and Employment GrowthWhile Latino-owned employer firms may be smaller on average and the sector may have signifi-cant concentrations of microbusinesses, overall Latino-owned businesses reported comparable revenue and employment growth patterns to white-owned businesses. Data from the 2017 SBCS show nearly identical shares of growing firms as measured by changes in revenues and payroll additions of part- or full-time employees.

FIGURE 5

Categories have been simplified for readability. Actual categories are: $100K or less, $100,001-$1M, $1,000,001-$10M, More than $10M.Source: 2017 Small Business Credit Survey, Federal Reserve Banks

Latino-owned (N=502)

Non-Latino white-owned (N=6,332)

$100K or less $100K–$1M $1M–$10M More than $10M

17%

34%

51%45%

27%

18%

3% 5%

REVENUE SIZE OF FIRM

% of employer firms

FIGURE 6 FIGURE 7

Latino-owned (N=520) Non-Latino white-owned (N=6,446)

REVENUE CHANGE, Prior 12 Months

% of employer firms

Increased54%

52%

No change21%

23%

Decreased25%

25%

Source: 2017 Small Business Credit Survey, Federal Reserve Banks

Latino-owned (N=472) Non-Latino white-owned (N=6,254)

Source: 2017 Small Business Credit Survey, Federal Reserve Banks

EMPLOYMENT CHANGE, Prior 12 Months

% of employer firms

Increased34%

36%

No change50%

50%

Decreased16%

14%

8

National small business trends

Additionally, firms may be able to capitalize on this growth in a few ways. First, a sizeable share (50 percent) of Latino-owned businesses reports being certified minority-owned, which may help them access opportunities in corporate and government procurement. Second, diversifying sales targets by expanding into different revenue streams can provide additional growth opportunities. The 2017 SBCS indicated that Latino-owned businesses drew revenue from similar sources as white-owned businesses, with individuals being the most common source of revenue. Still, notable shares of Latino-owned firms sell to government entities, pointing to varied revenue streams.

Profitability According to the 2016 ASE, Latino-owned employer firms overall are also similar to white-owned businesses in profitability, with only slightly smaller shares of profitable firms, another key measure of economic success.

Latino-owned

White-owned

Reflects all employer firms. Other figures in this section (using the 2017 SBCS) reflect small employer firms.Source: U.S. Census Bureau, Annual Survey of Entrepreneurs, 2016.

Business had losses

Business broke even

Business had profits

Individuals Other businesses State/local government Federal government

Latino-owned (N=481)

Non-Latino white-owned (N=6,011)

10+% of revenue refers to a firm receiving at least 10 percent of its annual revenue from the source.Respondents could select multiple options.Source: 2017 Small Business Credit Survey, Federal Reserve Banks

FIGURE 8

SOURCE(S) OF 10+% OF REVENUE

% of employer firms

67%64%

47%42%

16%16%11%11%

FIGURE 9

PROFITABILITY

% of employer firms

65%17%18%

59%22%19%

9

National small business trends

Financial Challenges: Persistent Operating Expense and Credit Availability Issues Despite positive indicators of growth and bottom line performance, financial challenges are com-mon among small businesses, and even more common among Latino-owned businesses. The 2017 SBCS asked respondents whether they experienced a series of financial challenges during the 12 months prior to survey completion.44 First, Latino-owned businesses were more likely to state that they had financial difficulties—71 percent compared to 62 percent of white-owned businesses—and higher shares of Latino-owned businesses experienced each of the specific challenges than white-owned businesses. Second, difficulties paying operating expenses are a pervasive problem for small firms and are consistently reported as a top financial challenge. For Latino-owned businesses, credit availability challenges are equally acute as issues paying operating expenses. These credit-related issues are much more pronounced among Latino- owned businesses than white-owned businesses (41 percent versus 28 percent).

44 Approximately Q4 2016 through Q4 2017.

FIGURE 10

FINANCIAL CHALLENGES, Prior 12 Months

% of employer firms

Paying operating expenses

Credit availability

Making payments on debt

Purchasing inventory or supplies to fulfill contracts

Other financial challenge

Did not experience any financial challenges

Latino-owned (N=526)

Non-Latino white-owned (N=6,541)

40%41%

28%41%

24%29%

16%26%

12%10%

38%29%

Respondents could select multiple options.Prior 12 Months is approximately Q4 2016 through Q4 2017.Source: 2017 Small Business Credit Survey, Federal Reserve Banks.

10

Furthermore, challenges with paying operating expenses and credit availability are persistent, even among Latino-owned businesses that have grown to scale. Whereas scaled white-owned busi-nesses were much less likely to report difficulties meeting operating expenses than smaller firms (29 percent compared to 44 percent), these challenges are equally common among smaller and larger revenue Latino-owned businesses. In fact, almost half (44 percent) of scaled Latino-owned businesses reported operating expense issues.

Credit availability differences between Latino-owned businesses and white-owned businesses are also striking. Latino-owned businesses, both small and large, were much more likely to report ac-cess to credit issues than white-owned businesses. Notably, scaled Latino-owned businesses were slightly more likely to report credit availability challenges than non-scaled white-owned businesses.

National small business trends

Respondents could select multiple options.Source: 2017 Small Business Credit Survey, Federal Reserve Banks

44%

29%

42%44%

31%

22%

43%

35%

Latino-owned, >$1M (N=168)

Latino-owned, ≤$1M (N=333)

Non-Latino white-owned, >$1M (N=2,975)

Non-Latino white-owned, ≤$1M (N=3,304)

Paying operating expenses Credit availability

FIGURE 11

TOP FINANCIAL CHALLENGES, by Firm Revenue and Ethnicity

% of employer firms

11

National small business trends

These challenges are likely to have important implications for Latino business growth. When firms that applied for financing in the prior 12 months45 were surveyed about why they were seeking financing, a majority (61 percent) stated that they had applied for expansion funding. An inability to secure capital for expansion means deferred investment and growth.

Debt HoldingsOverall, more than two-thirds of both Latino- and white-owned businesses reported having outstanding debt.

45 Approximately Q4 2016 through Q4 2017.

Respondents could select multiple options.Source: 2017 Small Business Credit Survey, Federal Reserve Banks

Latino-owned (N=249)

Non-Latino white-owned (N=2,797)

59%61%

42%41%

25%22%

8%10%

Expand business, pursue new opportunity, or replace capital assets

Meet operating expenses

Refinance or pay down debt

Other reason

FIGURE 12

REASONS FOR APPLYING

% of applicants

Latino-owned (N=516)

Non-Latino white-owned (N=6,539)

Source: 2017 Small Business Credit Survey, Federal Reserve Banks

FIGURE 13

SHARE WITH PRIOR OUTSTANDING DEBT, At Time of Survey

% of employer firms

69%

69%

12

National small business trends

However, the debt holdings of Latino-owned businesses are smaller, consistent with higher shares of micro firms ($100,000 or less in annual revenues). Two-thirds of Latino-owned businesses with debt hold amounts of $100,000 or less, compared to 55 percent of white-owned businesses with debt.

The following figure details the type of debt holdings of Latino- and white-owned businesses, and illustrates that Latino-owned businesses are more likely to use credit cards, factoring, and merchant cash advances—products that require less collateral and that are also associated with higher average interest rates.

Categories have been simplified for readability. Actual categories are: ≤$25K, $25,001K–$100K, $100,001K–$250K, $250,001K–$1M, >$1M.Percentages may not sum to 100 due to rounding.Source: 2017 Small Business Credit Survey, Federal Reserve Banks

Latino-owned (N=351)

Non-Latino white-owned (N=4,554)

≤$25K $25K–$100K $100K–$250K $250K–$1M >$1M

22%

34% 33%32%

19%16%

18%14%

8%3%

FIGURE 14

AMOUNT OF DEBT

% of employer firms with debt

13

National small business trends

This observation about the types of financing products used is borne out in firms’ responses to questions about the collateral used to secure debt holdings. As seen in Figure 15, a higher share of Latino-owned businesses reported using products that require no collateral compared to white-owned businesses; among those that used collateral, more relied on a personal guarantee than business assets to secure the financing. There is a large gap between the 34 percent of Latino-owned businesses that use business assets to secure debt and the more than 51 percent of white-owned businesses that secure capital in this way.

Latino-owned (N=525)

Non-Latino white-owned (N=6,562)

Respondents could select multiple options.Source: 2017 Small Business Credit Survey, Federal Reserve Banks

Credit card

Factoring

Other

Business does not use external financing

Loan or line of credit

Trade credit

Leasing

Equity investment

Merchant cash advance

56%50%

51%54%

10%13%

10%11%

6%9%

7%4%

6%3%

3%2%

15%21%

FIGURE 15

EXTERNAL FINANCING HELD OR REGULARLY USED

% of employer firms

14

National small business trends

Financing NeedsDifferences in financing patterns are also present among firms that have recently applied for financing.46 Overall, Latino-owned businesses showed stronger demand for financing in 2017 than white-owned businesses, with nearly half of Latino-owned businesses applying for capital.

46 Applied for financing in the prior 12 months. Approximately Q4 2016 through Q4 2017.

Respondents could select multiple options.Source: 2017 Small Business Credit Survey, Federal Reserve Banks

FIGURE 16

COLLATERAL USED TO SECURE DEBT

% of employer firms with debt

Latino-owned (N=362)

Non-Latino white-owned (N=4,646)

Personal guarantee

Business assets

Personal assets

Portions of future sales

Other

None

56%47%

51%34%

33%25%

6%10%

14%21%

1%1%

Latino-owned (N=530)

Non-Latino white-owned (N=6,600)

Prior 12 Months is approximately Q4 2016 through Q4 2017.Source: 2017 Small Business Credit Survey, Federal Reserve Banks

FIGURE 17

SHARE THAT APPLIED FOR FINANCING, Prior 12 Months

% of employer firms

47%

40%

15

National small business trends

However, consistent with the smaller average revenue size of Latino-owned businesses, the financ-ing requests made by Latino-owned businesses tended to be smaller than those of white-owned businesses. Slightly more than two-thirds of Latino-owned businesses applied for $100,000 or less in capital, or what might be considered ‘micro loans.’ Differences in financing demand are also ap-parent among firms seeking amounts that are typically described as bank-friendly loans—amounts over $250,000—given origination costs and profitability concerns of financial institutions in lending smaller amounts of capital;47 the share of Latino-owned businesses applying for these amounts was 17 percent, compared to 26 percent of white-owned businesses.

47 Mills, K. and B. McCarthy. (2016). “The state of Small Business Lending: Innovation and Technology and the Implications for Regulation,” Harvard Business School Working Paper Series. Available: http://www.hbs.edu/faculty/Publication%20Files/ 17-042_30393d52-3c61-41cb-a78a-ebbe3e040e55.pdf

Percentages may not sum to 100 due to rounding.Source: 2017 Small Business Credit Survey, Federal Reserve Banks

Latino-owned (N=241)

Non-Latino white-owned (N=2,735)

≤$25K $25K–$100K $100K–$250K $250K–$1M >$1M

22%

27%

33%

40%

19%17% 18%

13%

8%4%

FIGURE 18

AMOUNT OF FINANCING APPLIED FOR

% of applicants

16

National small business trends

The products demanded are consistent across firms, with strong majorities of applicants—at least 80 percent—across the board seeking loans or lines of credit. In fact, the product demands of Latino and white applicants are similar, though Latino-owned firms apply at lower rates for loans and lines of credit and at higher rates for merchant cash advances.

Respondents could select multiple options.Source: 2017 Small Business Credit Survey, Federal Reserve Banks

FIGURE 19

FINANCING AND CREDIT PRODUCTS SOUGHT

% of applicants

Loan or line of credit

Factoring

Other

Credit card

Leasing

Trade credit

Equity investment

Merchant cash advance

Latino-owned (N=249)

Non-Latino white-owned (N=2,803)

86%80%

26%24%

10%12%

10%9%

8%9%

6%9%

4% 4%

6%5%

17

National small business trends

These differences persist when controlling for credit risk. Among low credit risk firms, 41 percent of white-owned businesses experienced a financing shortfall, compared to 53 percent of Latino-owned businesses. Moreover, while low credit risk Latino-owned businesses were more likely to receive all of the financing sought compared to medium/high credit risk Latino- owned businesses, about one-third of Latino-owned businesses received none of the financing sought, regardless of credit risk.

Credit risk is based on self-reported business credit score or personal credit score, depending on which is used to obtain financing for the business. If the firm uses both, the highest risk rating (lowest score) is used. ‘Low credit risk’ is an 80-100 business score or 720+ personal credit score. ‘Medium credit risk’ is a 50-79 business credit score or a 620-719 personal credit score. ‘High credit risk’ is a 1-49 business credit score or a <620 personal credit score.Source: 2017 Small Business Credit Survey, Federal Reserve Banks

Non-Latino white-owned, low credit risk (N=1,320)

Non-Latino white-owned, medium/high credit risk (N=634)

59%25%16%

26%44%30%

Latino-owned, low credit risk (N=75)

Latino-owned, medium/high credit risk (N=101)

47%19%34%

14%53%33%

Financing OutcomesWhile the expressed product needs of Latino-owned businesses and white-owned businesses are similar, their ability to secure financing differs markedly. The following figure shows the total amount of financing dollars approved by respondents. As seen in the figure below, nearly half of white-owned businesses received all of the financing they sought, whereas only 28 percent of Latino-owned businesses were approved for the full amount of financing. In fact, 71 percent of Latino-owned businesses experienced a financing shortfall in their applications, receiving less than the desired amount, compared to 51 percent of white-owned businesses.

Latino-owned (N=241)

Non-Latino white-owned (N=2,746)

Percentages may not sum to 100 due to rounding.Source: 2017 Small Business Credit Survey, Federal Reserve Banks

28%37%34%

49%31%20%

None Some All

FIGURE 20

FINANCING RECEIVED

% of applicants

FIGURE 21

FINANCING RECEIVED BY ETHNICITY & CREDIT RISK OF FIRM

% of employer firms

None Some All

18

National small business trends

A more detailed look at loan, line of credit, and cash advance applications shows higher financing success rates for these products than for financing amounts overall. Forty-five percent of Latino ap-plicants reported being fully approved for the loan, line of credit, or cash advance products that they applied for, compared to only 28 percent of applicants across all financing types. The same pattern holds among white applicants, with 62 percent of firms receiving the full amount requested for loans, lines of credit, and cash advances, compared to 49 percent success rates across all financing types.

Differences in success rates also vary by lending institution. The following figure depicts the success rates of loan/line of credit and cash advance applications at large and small banks for Latino-owned and white-owned businesses. While the data are limited and should be interpreted with caution, particularly among Latino-owned businesses, a consistent pattern holds; white-owned businesses reported higher approval rates. Moreover, small firms, irrespective of ethnicity, report greater success at small banks compared to large banks, and this pattern appears to be even more pronounced for Latino-owned businesses, with 60 percent of applicants reporting credit success at small banks, compared to 34 percent of applicants at large banks.

Latino-owned (N=180)

Non-Latino white-owned (N=2,129)

Percentages may not sum to 100 due to rounding.Source: 2017 Small Business Credit Survey, Federal Reserve Banks

FIGURE 23

LOAN, LINE OF CREDIT, AND CASH ADVANCE APPROVAL RATE BY SOURCE

% of loan/line of credit and cash advance applicants at each lender

Latino-owned (N=62–91)

Non-Latino white-owned (N=944–1,131)

Large bank Small bank

60%34%

70%56%

Source: 2017 Small Business Credit Survey, Federal Reserve Banks

FIGURE 22

LOAN, LINE OF CREDIT, AND CASH ADVANCE APPROVAL RATE

% of loan/line of credit and cash advance applicants

62%18%19%

45%21%34% None Some All

19

National small business trends

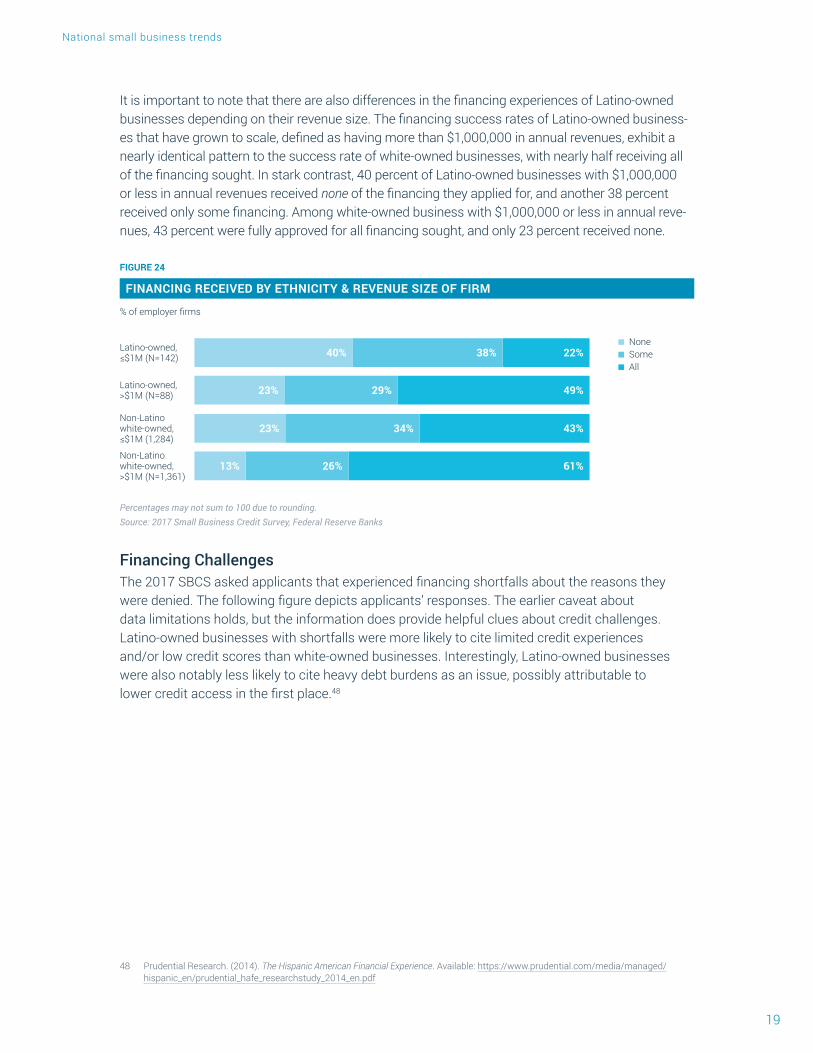

It is important to note that there are also differences in the financing experiences of Latino-owned businesses depending on their revenue size. The financing success rates of Latino-owned business-es that have grown to scale, defined as having more than $1,000,000 in annual revenues, exhibit a nearly identical pattern to the success rate of white-owned businesses, with nearly half receiving all of the financing sought. In stark contrast, 40 percent of Latino-owned businesses with $1,000,000 or less in annual revenues received none of the financing they applied for, and another 38 percent received only some financing. Among white-owned business with $1,000,000 or less in annual reve-nues, 43 percent were fully approved for all financing sought, and only 23 percent received none.

Financing ChallengesThe 2017 SBCS asked applicants that experienced financing shortfalls about the reasons they were denied. The following figure depicts applicants’ responses. The earlier caveat about data limitations holds, but the information does provide helpful clues about credit challenges. Latino-owned businesses with shortfalls were more likely to cite limited credit experiences and/or low credit scores than white-owned businesses. Interestingly, Latino-owned businesses were also notably less likely to cite heavy debt burdens as an issue, possibly attributable to lower credit access in the first place.48

48 Prudential Research. (2014). The Hispanic American Financial Experience. Available: https://www.prudential.com/media/managed/ hispanic_en/prudential_hafe_researchstudy_2014_en.pdf

43%34%23%

61%26%13%

Non-Latino white-owned, ≤$1M (1,284)

Non-Latino white-owned, >$1M (N=1,361)

22%38%40%

49%29%23%

Latino-owned, ≤$1M (N=142)

Latino-owned, >$1M (N=88)

Percentages may not sum to 100 due to rounding.Source: 2017 Small Business Credit Survey, Federal Reserve Banks

FIGURE 24

FINANCING RECEIVED BY ETHNICITY & REVENUE SIZE OF FIRM

% of employer firms

None Some All

20

National small business trends

An examination of self-reported credit scores offers further insight into these challenges. Across all respondents, including applicants and nonapplicants, Latino-owned businesses were more likely to report being medium or high credit risk than white-owned businesses: 49 percent compared to 29 percent. These patterns are consistent with the fact that a higher proportion of Latino-owned firms are startups.49

49 Fairlie, R.; Morelix, A.; Reedy, E.J.; and Russell, J. (2015). “The Kauffman Index: Startup Activity, National Trends.” Ewing Marion Kauffman Foundation.

FIGURE 25

Respondents could select multiple options.Source: 2017 Small Business Credit Survey, Federal Reserve Banks

Latino-owned (N=69)

Non-Latino white-owned (N=605)

Insufficient credit history

33%

45%

Low credit score

26%

37%

Insufficient collateral

34%35%

Too much debt already

31%

16%

Weak business performance

22%24%

Other

9%

REASONS FOR CREDIT DENIAL

% of applicants with financing shortfall

1%

FIGURE 26

Credit risk is based on self-reported business credit score or personal credit score, depending on which is used to obtain financing for the business. If the firm uses both, the highest risk rating (lowest score) is used. ‘Low credit risk’ is an 80-100 business score or 720+ personal credit score. ‘Medium credit risk’ is a 50-79 business credit score or a 620-719 personal credit score. ‘High credit risk’ is a 1-49 business credit score or a <620 personal credit score.Source: 2017 Small Business Credit Survey, Federal Reserve Banks

CREDIT RISK

Low credit risk

Medium credit risk

High credit risk

NON-LATINO WHITE-OWNED

(N=4,179)

71%5%

24%

LATINO- OWNED (N=372)

51%12%

37%

21

National small business trends

These credit risk patterns are also consistent with credit success rates and vary by firm size. Latino-owned businesses that have scaled reported similar credit score patterns to those of white-owned businesses, with more than two-thirds identifying as low credit risk. It is clear that, consistent with other indicators, firms with $1,000,000 or less in annual revenues face challenges in building credit histories and scores, which coincides with difficulty securing financing for their firms.

≤$1M (N=242)

>$1M (N=113)

Credit risk is based on self-reported business credit score or personal credit score, depending on which is used to obtain financing for the business. If the firm uses both, the highest risk rating (lowest score) is used. ‘Low credit risk’ is an 80-100 business score or 720+ personal credit score. ‘Medium credit risk’ is a 50-79 business credit score or a 620-719 personal credit score. ‘High credit risk’ is a 1-49 business credit score or a <620 personal credit score.Source: 2017 Small Business Credit Survey, Federal Reserve Banks

15%35%50%

5%30%65%

FIGURE 27

CREDIT RISK BY REVENUE SIZE OF FIRM

% of Latino-owned businesses

Low credit risk

Medium credit risk

High credit risk

2222

TOP TEN LATINO METROPOLITAN AREAS BY POPULATION

50 Morelix, A., Tareque, I., Orozco, M., Perez, I., Oyer, P., and Porras, J. The U.S. Latino Entrepreneurship Gap: A Comparative Measure of Latino Entrepreneurship Activity. Stanford Latino Entrepreneurship Initiative.

51 More information about methodology available in Appendix A.

OverviewDespite the progress and growth of Latino entrepreneurship, Latino business owners continue to face significant challenges, particularly in the realm of financing, which greatly affects the ability to scale. This is evident in the opportunity gap between employer versus nonemployer firms where non-Latinos own employer businesses at nearly three times the rate of Latinos.50 However, this gap is not evenly distributed across states or Metropolitan Statistical Areas (MSAs) and it is evident from the following figure that the share of the Latino population does not fully explain differences in the share of Latino-owned businesses. Differences in entrepreneurship rates and economic success may be due to personal characteristics of the entrepreneurs, such as gender, higher educational attainment, nativity, personal wealth, and social capital. Geographic characteristics, such as tax rates, cost of land, and local and state policies may also support or hinder business opportunity.

Using the nationally representative (at the MSA level) SLEI Survey of U.S. Latino Business Owners, employer and nonemployer, from 201751 (N=5,026), we have compiled a study of the ten largest metropolitan statistical areas (MSAs) by Latino population, as listed in Figure 28. This analysis uses demographic characteristics of Latino entrepreneurs in these MSAs, such as their average age, nativity, education, gender, and percent reporting a family history of entrepreneurship. Additionally, for each region we provide Latino business statistics on annual revenues, the share of industries among scaled (businesses generating at least $1,000,000 in annual revenue) and unscaled firms, and the greatest business challenges for growth. As an important contribution, we derive the Latino Entrepreneurship Scores of these metro areas, a measure of the gap in entrepreneurship rates between Latinos and non-Latinos.

3

23

Top ten latino metropolitan areas by population

FIGURE 28

TOP TEN METRO AREAS BY TOTAL LATINO POPULATION AND NUMBER OF LATINO-OWNED BUSINESSES (LOBs)

Metropolitan Area Latino Population Latino Share Number of LOBs LOB Share

Los Angeles, Long Beach, Anaheim 5,979,000 45.1 393,051 26.5

New York, Newark, Jersey City 4,780,000 23.9 339,415 15.4

Miami, Ft. Lauderdale, W. Palm Beach 2,554,000 43.3 423,163 47.0

Houston, The Woodlands, Sugar Land 2,335,000 36.4 164,923 27.2

Riverside, San Bernardino, Ontario 2,197,000 49.4 122,233 36.5

Chicago, Naperville, Elgin 2,070,000 21.8 89,523 9.9

Dallas, Fort Worth, Arlington 1,943,000 28.4 117,582 18.3

Phoenix, Mesa, Scottsdale 1,347,000 30.1 54,393 16.0

San Antonio, New Braunfels 1,259,000 55.7 81,126 43.3

San Diego, Carlsbad 1,084,000 33.3 62,753 21.4

Population and Origin in Select U.S. Metropolitan Areas, 2014Source: U.S. Census Survey of Business Owners, 2012 and Pew Research Center, Hispanic

Latino Entrepreneurship Score The Latino Entrepreneurship Score is a comparative measure of the entrepreneurship rates of Latinos and non-Latinos in the U.S. It is defined as the ratio of the employer business ownership rate—the number of entrepreneurs divided by the total population—for Latinos divided by the employer business ownership rate for non-Latinos.52 A score of one would indicate no discernable gap and a score of zero indicates a very large gap.53

As noted in The U.S. Latino Entrepreneurship Gap report, the five metropolitan statistical areas with the highest Latino Entrepreneurship Scores are:

1. Miami-Fort Lauderdale-West Palm Beach, FL2. Tampa-St. Petersburg-Clearwater, FL3. Washington-Arlington-Alexandria, DC-VA-MD-WV4. Orlando-Kissimmee-Sanford, FL5. Portland-Vancouver-Hillsboro, OR-WA

Among the ten MSAs with the largest Latino populations, only Miami makes the top five of the highest Latino Entrepreneurship Scores. Chicago makes the top ten list, ranked number seven with its Latino Entrepreneurship Score of 0.30. Figure 29 provides the rankings and scores of the other metro areas with the largest Latino populations. While we cannot prove the cause of these low entrepreneurship scores in the largest Latino metro areas, insights from Latino entrepreneurs in these regions, discussed in Section 4, shed light on possible factors. These factors include, but are not limited to, access to external funding, local economic development that favors certain indus-tries (e.g., construction), property values, state minimum wage laws, and local and state tax rates.

52 Number of entrepreneurs taken from the Census Bureau, 2015 Annual Survey of Entrepreneurs (ASE). Population data taken from 2011-2015 American Community Survey (5-year). We consider only employer firms, which are firms with at least one paid employee.

53 Ibid (51)

24

Top ten latino metropolitan areas by population

FIGURE 29

LATINO ENTREPRENEURSHIP SCORES FOR THE TEN MSAs WITH THE LARGEST LATINO POPULATIONS

Rank Metropolitan Area Latino Entrepreneurship Rate

Non-Latino Entrepreneurship Rate

Latino Entrepreneurship Score

1 Miami-Fort Lauderdale-West Palm Beach, FL 17.9 30.2 0.59

7 Chicago-Naperville-Elgin, IL-IN-WI 6.6 21.8 0.30

10 San Antonio-New Braunfels, TX 5.1 20.3 0.25

10 New York-Newark-Jersey City, NY-NJ-PA 6.8 27.3 0.25

11 San Diego-Carlsbad, CA 6.0 24.6 0.24

12 Houston-The Woodlands-Sugar Land, TX 4.3 20.0 0.22

13 Riverside-San Bernardino-Ontario, CA 3.7 17.7 0.21

14 Dallas-Fort Worth-Arlington, TX 3.9 19.2 0.20

15 Phoenix-Mesa-Scottsdale, AZ 3.3 18.5 0.18

16 Los Angeles-Long Beach-Anaheim, CA 5.0 33.3 0.15

Duplicate ranks are tied in the entrepreneurship score. Source: 2018 Stanford Latino Entrepreneurship Gap Report

Key Findings

RevenueAccording to the 2016 ASE, 20 percent of all Latino-owned employer firms are scaled, generating $1,000,000 or more in annual revenue, compared to 26 percent of non-Latino-owned employer firms. While Miami has historically been held as a central Latino entrepreneurship hub,54 greater success can be seen in other metro areas, as measured by the annual revenue of Latino-owned businesses. By this measure, shown in Figure 30, Phoenix is the metro leader with the greatest proportion (17 percent) of Latino-owned businesses surveyed in the scaled revenue bracket. New York comes in second with five percent of firms in the scaled bracket. The share of scaled firms in the other eight metro areas hovers around the national average share, among all Latino-owned businesses, of three percent.

54 Card, D. (1990). The Impact of the Mariel Boatlift on the Miami Labor Market. Industrial and Labor Relations Review, 43(2), 245–257.

25

Top ten latino metropolitan areas by population

Sources of CapitalData from the SLEI Survey of U.S. Latino Business Owners show that Latino-owned businesses primarily rely on personal savings and family/friends loans to start their businesses, not unlike that of other demographic groups. In addition, the data reveal nuances in the sources of external fund-ing that Latino entrepreneurs use to grow their businesses. These external sources include loans from commercial/national banks, local/regional banks, government agencies, private equity, angel funding, venture capital, and hard money. As noted in the previous section, these external sources of funding, such as national banks (large banks) and local banks (small banks), show different approval rates among Latino-owned businesses and white-owned businesses. These data are presented for those who had successful applications and do not account for those who attempted but did not receive funding from the different sources.

Similar to startup funding, the data show that personal savings and family/friends loans are commonly used in these ten MSAs for growth funding. Lines of credit also surface as a secondary source of capital for business growth. In fact, Latino employer firms use credit cards at higher rates than all other groups to grow their businesses and they also have the highest utilization rates of trade credit (buy now, pay later) according to the ASE, relative to other demographic groups. Similarly, Latino-owned businesses across the ten metro areas rely on hard money as the third most common and in some places, the second most common, source of external funding for growth. As noted in the 2017 State of Latino Entrepreneurship (SOLE) report, hard money is secured from private sources and is less regulated than more formal business loans. As well, the costs of hard money can be very high—interest rates often range from 12 to 18 percent—placing considerable pressure on businesses that use them for funding. Considering the primary sources of external funding, the data show that Latinos bear greater personal financial risk in starting and growing their businesses when compared to other groups.

FIGURE 30

Source: 2017 SLEI Survey of U.S. Latino Business Owners

>$1M $500K–$999K $100K–$499K $50K–$99K <$50K

Los Angeles (N=314)

New York (N=409)

Riverside (N=111)

Phoenix (N=76)

Miami (N=248)

Chicago (N=224)

San Antonio (N=70)

Houston (N=125)

Dallas (N=108)

San Diego

(N=62)

ANNUAL REVENUE FOR TOP TEN METRO AREAS

26

Top ten latino metropolitan areas by population

According to the 2016 ASE, Latino employer firms use bank loans the least to start businesses, relative to all other demographic groups. At the growth stage, Latino entrepreneurs rely more heavily on local bank loans as opposed to national bank funding. In Chicago and Houston, in par-ticular, local bank loans are accessed at higher rates than the national average among all Latino entrepreneurs surveyed.

FIGURE 31

Respondents could select multiple options.Source: 2017 SLEI Survey of U.S. Latino Business Owners

Hard Money Private Equity Angel Investor Venture Capital Loans from

a government agency

Loans from national/ commercial bank

Loans from local/regional bank

Lines of Credit Savings, Friends

and family

Los Angeles (N=314)

New York (N=409)

Riverside (N=111)

Phoenix (N=76)

Miami (N=248)

Chicago (N=224)

San Antonio (N=70)

Houston (N=125)

Dallas (N=108)

San Diego

(N=62)

Industry DistributionBased on SLEI’s 2017 Survey of U.S. Latino Business Owners, there is some variation across industries for scaled Latino-owned firms, which generally looks similar to other scaled non-Latino employer firms. Some notable differences among scaled employer firms include a higher concen-tration of Latino-owned businesses (19 percent) in the Construction (NAICS 23) sector, compared to 14 percent of non-Latino-owned businesses; a higher concentration of Latino-owned businesses in Accommodations and food services (NAICS 72) (14 percent), compared to nine percent of non-Latino-owned businesses; and a lower concentration of Latino-owned businesses (13 percent) in the Retail trade sector (NAICS 44-45), compared to 18 percent of non-Latino-owned businesses.55 In Figure 32, we see an overrepresentation in the Construction (NAICS 23) industry across all MSAs, except Chicago, which has a larger concentration of scaled businesses in Professional, sci-entific, technical services (NAICS 54) (65 percent) and Riverside, which has a larger representation of scaled businesses in the Information sector (NAICS 51) (31 percent). These results coincide with national trends for scaled Latino-owned firms, with 39 percent of scaled Latino-owned firms in the Construction (NAICS 23) sector and 23 percent in Professional, scientific, technical services (NAICS 54).56

55 Author’s calculations from 2016 ASE.56 Ibid

SOURCES OF CAPITAL FOR GROWTH FOR TOP TEN METRO AREAS

27

Top ten latino metropolitan areas by population

Employee CountsThe majority of Latino-owned businesses are nonemployer firms, firms that do not have any paid full- or part-time employees, as is shown in Figure 33 below. According to SLEI’s 2017 Survey of U.S. Latino Business Owners, among scaled Latino-owned firms in the ten MSAs with the largest Latino populations, the majority are employer firms, as is shown in Figure 34. Three MSAs are exceptions in having a higher proportion of scaled nonemployer firms, compared to the other MSAs: Chicago (59 percent), New York (73 percent), and Phoenix (97 percent).57

57 Some geographies have very small sample sizes. Data may not necessarily be representative at very small sample sizes.

FIGURE 33

Some geographies have very small sample sizes. Data may not necessarily be representative at very small sample sizes.Source: 2017 SLEI Survey of U.S. Latino Business Owners

Source: 2017 SLEI Survey of U.S. Latino Business Owners

50+ 10–49 1–9 0

Los Angeles (N=314)

New York (N=409)

Riverside (N=111)

Phoenix (N=76)

Miami (N=248)

Chicago (N=224)

San Antonio (N=70)

Houston (N=125)

Dallas (N=108)

San Diego

(N=62)

FIGURE 32

Trade/ Transportation/Utilities

Professional/Business Services

Other Services Natural

Resources/Marketing

Manufacturing Leisure/

Hospitality Information Financial

Activities Education/

Health Services

ConstructionLos Angeles (N=95)

New York (N=123)

Riverside (N=26)

Phoenix (N=12)

Miami (N=88)

Chicago (N=71)

San Antonio (N=11)

Houston (N=33)

Dallas (N=37)

San Diego

(N=28)

TOP INDUSTRIES AMONG SCALED LATINO-OWNED FIRMS ($1M+) FOR TOP TEN METRO AREAS

EMPLOYEE COUNTS AMONG ALL LATINO-OWNED FIRMS FOR TOP TEN METRO AREAS

28

Top ten latino metropolitan areas by population

Top Ten Metro Area SnapshotsThis section provides an overview of Latino-owned businesses, employer and nonemployer, across the top ten metro areas that includes business and business owner characteristics, utilization of capital for business growth, and participation in business organizations,58 based on data from SLEI’s 2017 Survey of U.S. Latino Business Owners.59 The top ten metros are discussed in order of their Latino entrepreneurship rank, based on the Latino entrepreneurship score. It should be noted that differences between MSAs are suggestive, rather than precise estimates. In addition to business and business owner characteristics, we include data on property and land value, wages and taxes at the metro and state levels.60 These data points begin to shed light on why some geographic areas may be doing better than others. For example, we see that metro areas in Texas benefit from lower land values and cost of labor, compared to all other metro areas discussed. Suburban metro areas in California, such as Riverside, also have a competitive advantage with lower land values across the state. We also see, according to the 2019 State Business Tax Climate Index,61 that Texas and Florida are states with some of the most business-friendly tax systems, which might attract new business and foment business growth. In this section, the trends in the metro areas are compared to the national averages among all Latino business owners surveyed (hereafter “national averages”).

58 See Table 1 in Appendix B for complete overview of the top ten metro area characteristics.59 The SLEI Survey of U.S. Latino Business Owners allows for comparisons of national Latino-owned businesses with Latino-owned busi-

nesses in the metro regions.60 See Table 2 in Appendix B for additional data about property value, wages, and taxes for the top ten metro areas.61 Walczak, J., Drenkard, S., & Bishop-Henchman, J. (2018) 2019 State Business Tax Climate Index. Tax Foundation.

https://files.taxfoundation.org/20180925174436/2019-State-Business-Tax-Climate-Index.pdf

FIGURE 34

Some geographies have very small sample sizes. Data may not necessarily be representative at very small sample sizes.Source: 2017 SLEI Survey of U.S. Latino Business Owners

50+ 10–49 1–9 0

Los Angeles (N=95)

New York (N=123)

Riverside (N=26)

Phoenix (N=12)

Miami (N=88)

Chicago (N=71)

San Antonio (N=11)

Houston (N=33)

Dallas (N=37)

San Diego

(N=28)

EMPLOYEE COUNTS AMONG SCALED FIRMS ($1M+) FOR TOP TEN METRO AREAS

29

Top ten latino metropolitan areas by population

MIAMI-FORT LAUDERDALE-WEST PALM BEACH, FL

62 Jiménez, A., Palmero-Cámara, C., González-Santos, M. J., González-Bernal, J., & Jiménez-Eguizábal, J. A. (2015). The impact of educational levels on formal and informal entrepreneurship. BRQ Business Research Quarterly, 18(3), 204-212.

Latino Entrepreneurship Rank:

1MSA Average Land Value:

$216,056State Minimum Wage:

$8.25State Corporate Income Tax:

5.5%Many Miami MSA Latino business owners have a strong family history of entrepreneurship (71 percent), which provides some evidence as to why it may have the highest Latino entrepreneurship gap score. There is also a high immigrant concentration (52 percent) compared to the national average of 27 percent and a much higher representation of females (56 percent), compared to the national average of 42 percent.