law firm perspective - jll | global commercial real … · average upon relocating in 2014, up from...

TRANSCRIPT

Law Firm Perspective

United States | 2014

2

Law firms will see real estate opportunities continue to shift away in the current expanding economic cycle. However, opportunity to optimize real estate costs will remain for firms that focus intently on maximizing the efficiency of their real estate footprint, while enhancing strategies around talent in fringe urban cores where Millennials live and ideally want to work.

JLL | United States | Law Firm Perspective | 2014

Table of contents

3

Key themes shaping the U.S. law firm market 4

2014 U.S. law firm office clock 9

Local U.S. law firm markets

Atlanta 11

Austin 12

Baltimore 13

Boston 14

Charlotte 15

Chicago 16

Cincinnati 17

Cleveland 18

Columbus 19

Dallas 20

Denver 21

Detroit 22

Fairfield County 23

Fort Lauderdale 24

Houston 25

Indianapolis 26

Long Island 27

Los Angeles 28

Miami 29

Minneapolis 30

New York 31

Oakland 32

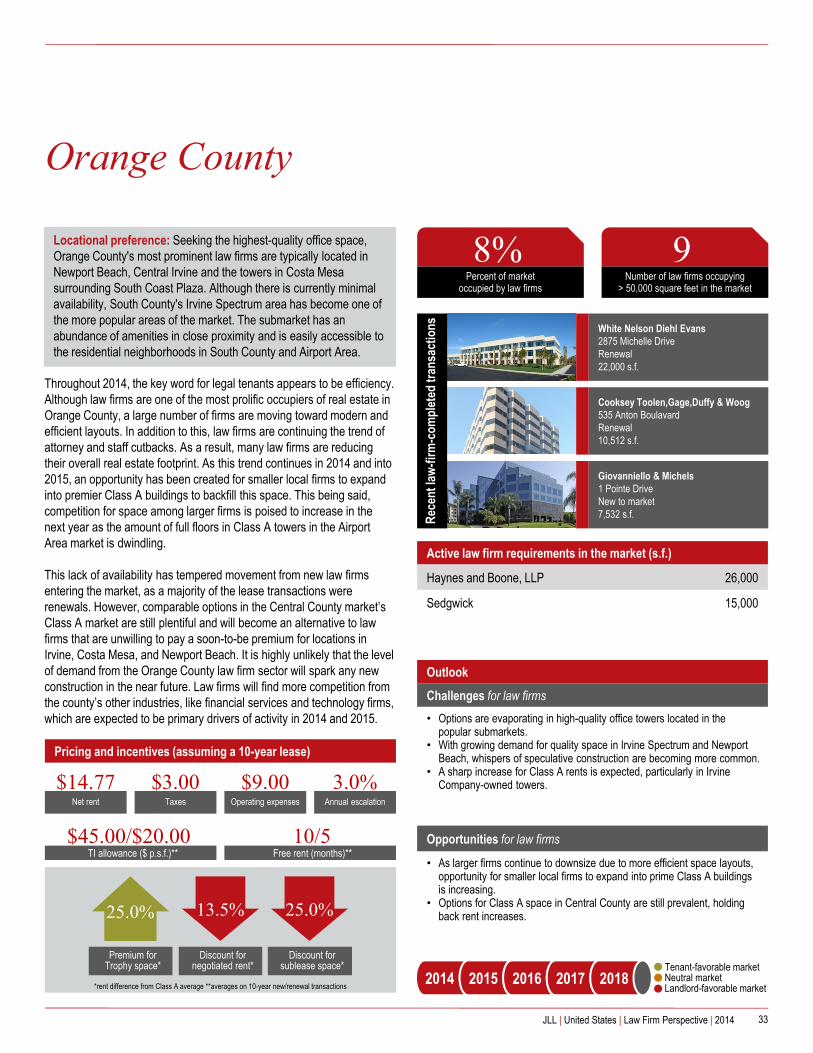

Orange County 33

Philadelphia 34

Phoenix 35

Pittsburgh 36

Portland 37

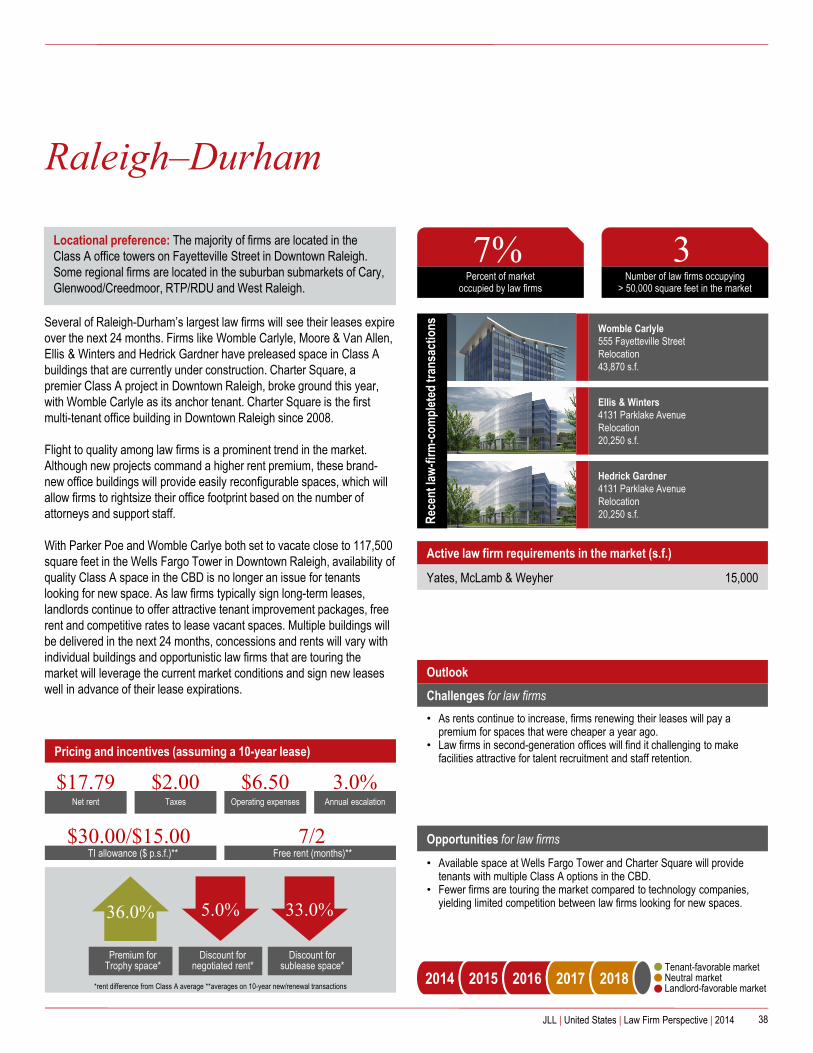

Raleigh-Durham 38

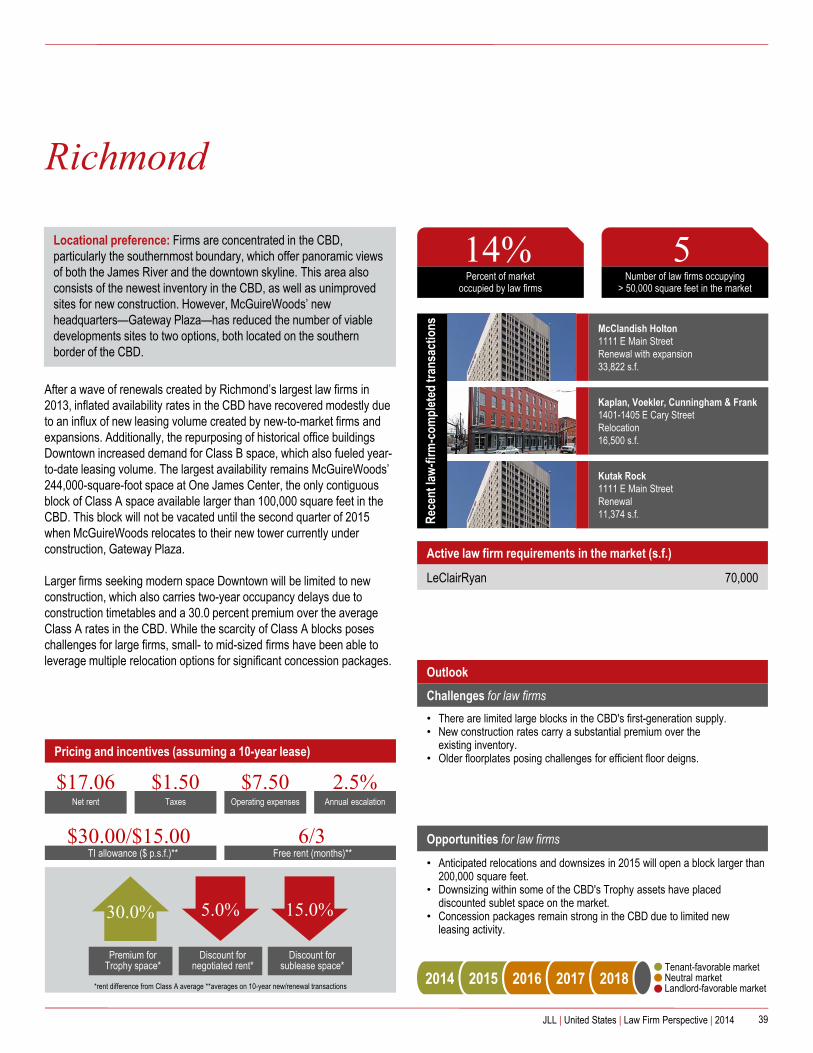

Richmond 39

Sacramento 40

San Diego 41

San Francisco 42

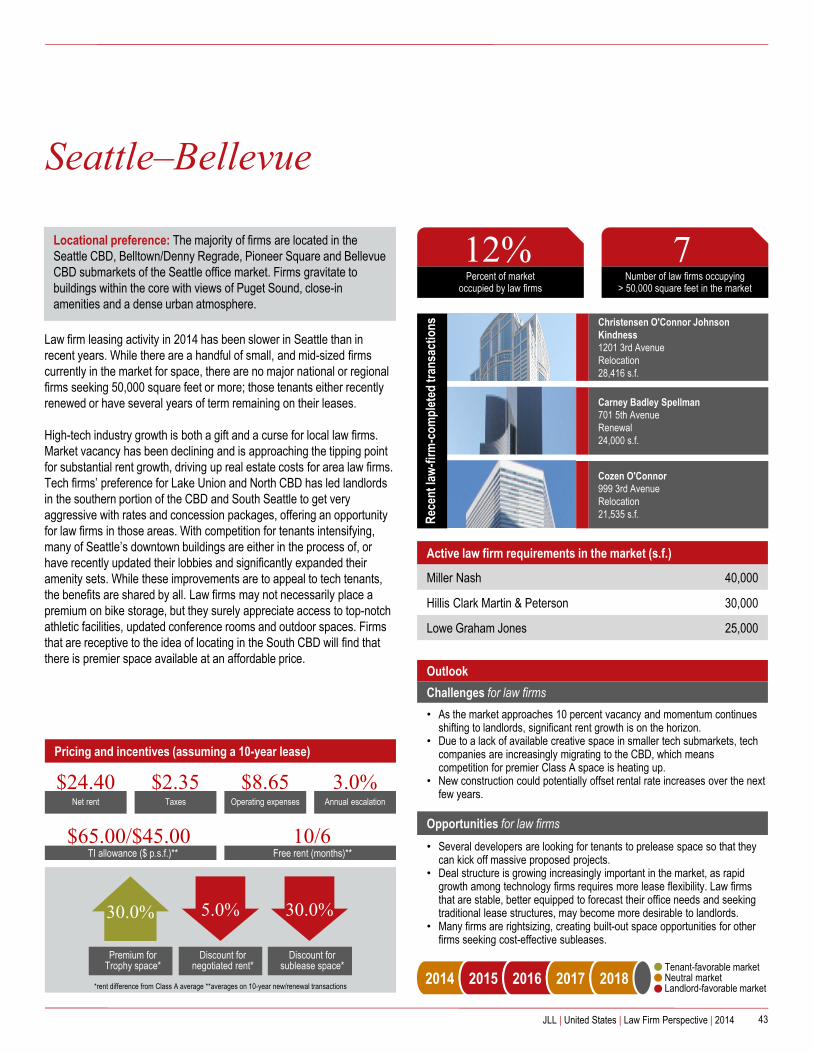

Seattle-Bellevue 43

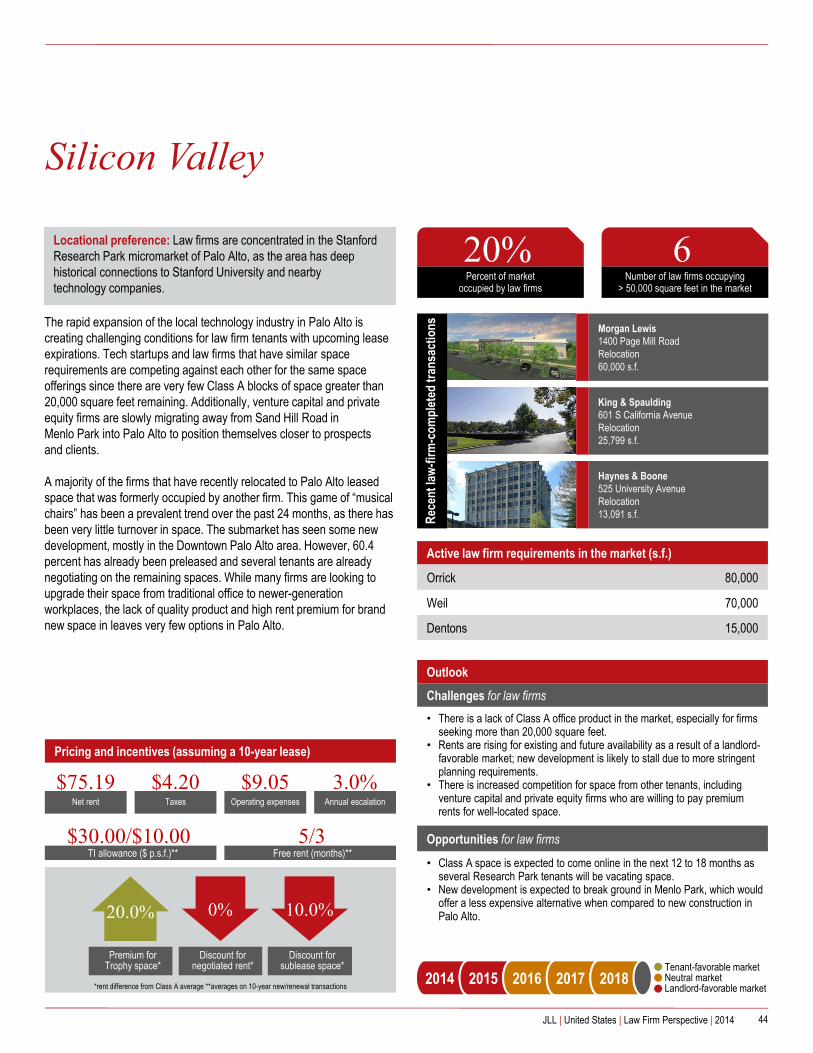

Silicon Valley 44

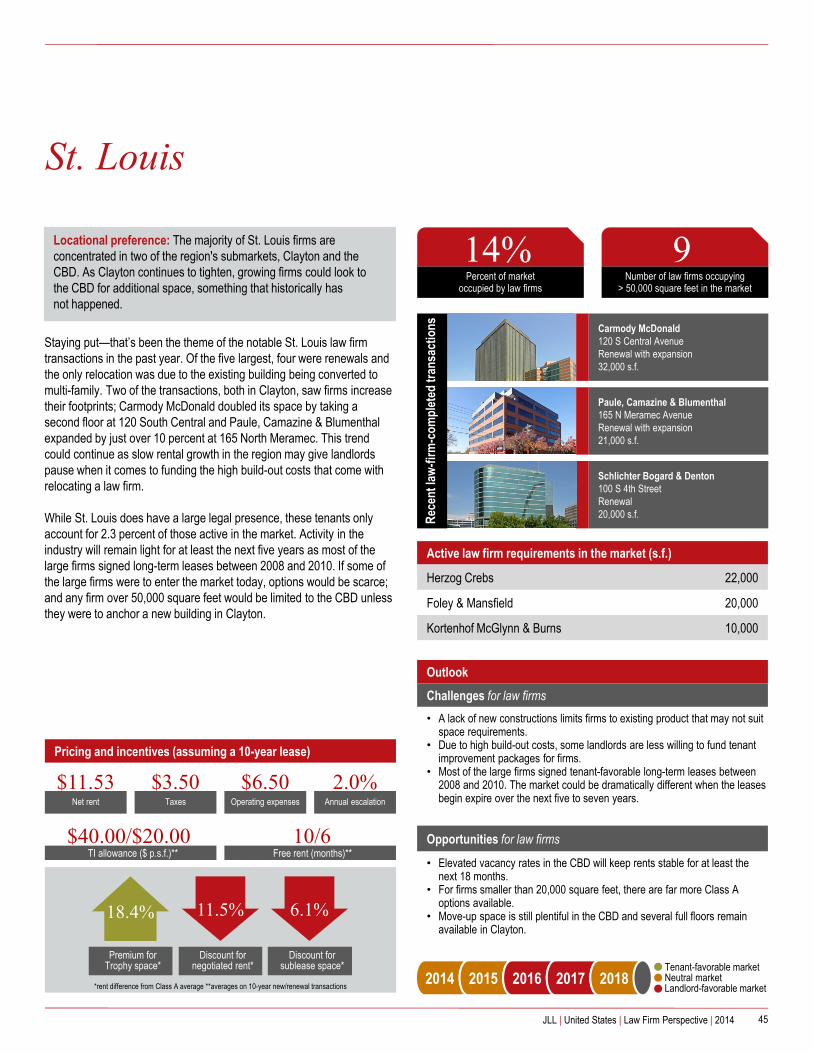

St. Louis 45

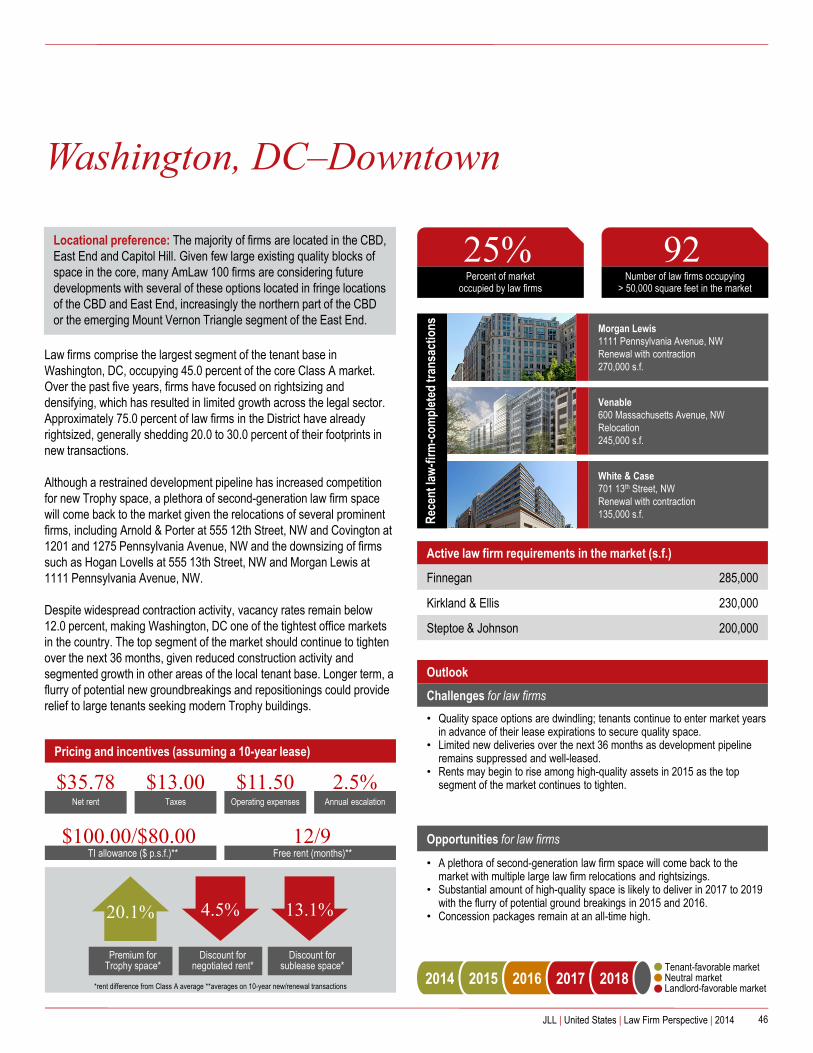

Washington, DC–Downtown 46

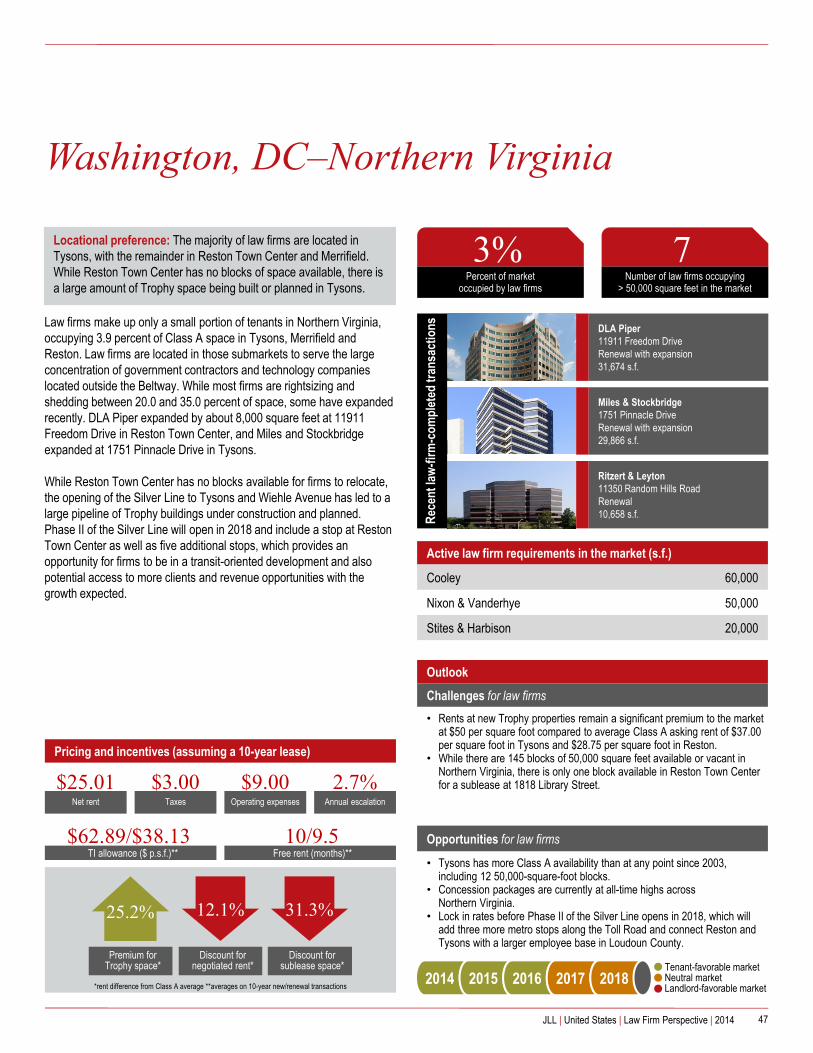

Washington, DC–Northern Virginia 47

Westchester County 48

Appendix 50

Contacts 54

JLL | United States | Law Firm Perspective | 2014

Mid- to large-sized law firms are still in contraction mode across U.S. markets, giving up roughly 17 percent of their space on average upon relocating in 2014, up from 14 percent in 2013 and 16 percent in 2012. However, over the past 12 months, the number of firms rightsizing is beginning to show signs of slowing. Markets across the U.S. have reported that anywhere from 55 percent to upward of 90 percent of law firms in primary and secondary markets have already devised substantial efficiency measures in new or restructured leases. For law firms with upcoming lease expirations, the current plateau of rightsizing could make market timing even more critical. Not only is new supply through the development pipeline limited, but second-generation options coming to the market could slow. Over the long term, more space will come back to the market as even firms that have already rightsized have more opportunity in front of them for cost savings and efficiencies. U.S. firms could take a page from their global counterparts and close the gap on efficiency measures and workplace layouts, even if those efficiencies are more conservative.

Key themes shaping the U.S. law firm market

4JLL | United States | Law Firm Perspective | 2014

The rightsizing wave is peaking, but will continue to evolve

5JLL | United States | Law Firm Perspective | 2014

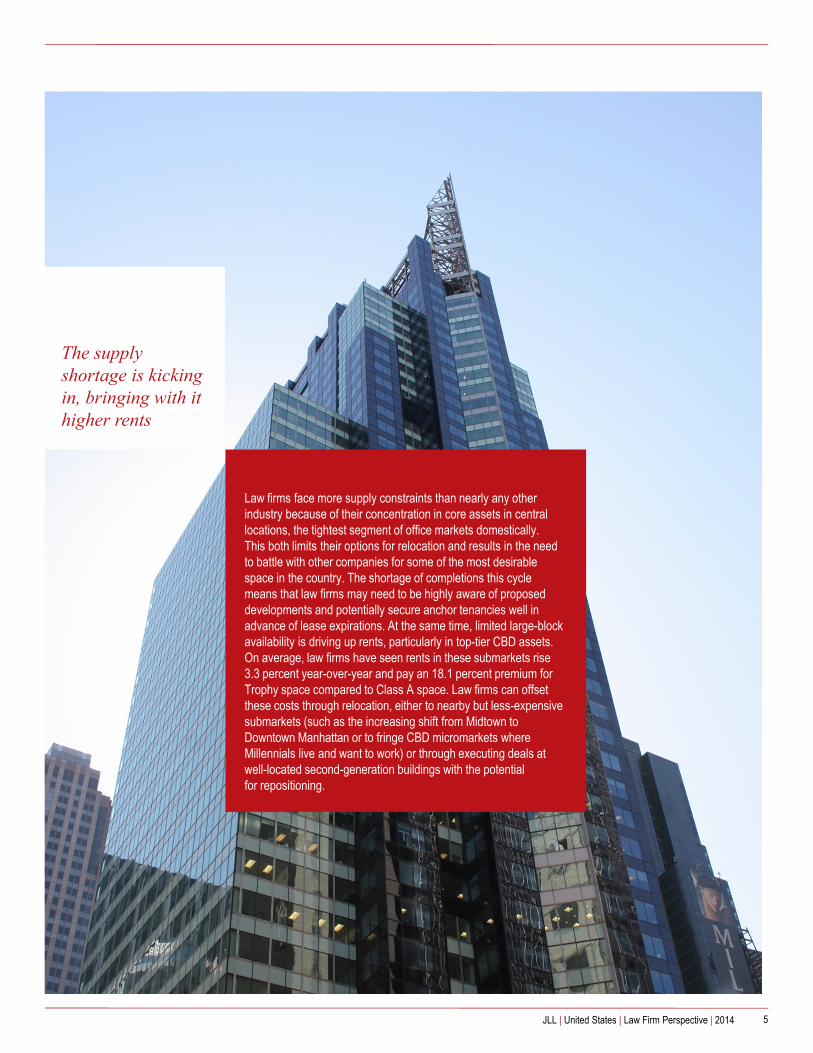

Law firms face more supply constraints than nearly any other industry because of their concentration in core assets in central locations, the tightest segment of office markets domestically. This both limits their options for relocation and results in the need to battle with other companies for some of the most desirable space in the country. The shortage of completions this cycle means that law firms may need to be highly aware of proposed developments and potentially secure anchor tenancies well in advance of lease expirations. At the same time, limited large-block availability is driving up rents, particularly in top-tier CBD assets. On average, law firms have seen rents in these submarkets rise 3.3 percent year-over-year and pay an 18.1 percent premium for Trophy space compared to Class A space. Law firms can offset these costs through relocation, either to nearby but less-expensive submarkets (such as the increasing shift from Midtown to Downtown Manhattan or to fringe CBD micromarkets where Millennials live and want to work) or through executing deals at well-located second-generation buildings with the potential for repositioning.

The supply shortage is kicking in, bringing with it higher rents

6JLL | United States | Law Firm Perspective | 2014

The law firm partner has always preferred locating their business in the heart of the business district, in close proximity to transit and clients. However, in recent years, fringe CBD and somewhat unorthodox locations to the typical law firm partner are becoming more and more desirable to associate-level and senior associate-level talent (the future of the firm), as these employees are increasingly opting to live in fringe CBD areas. Emerging micromarkets such as South Lake Union in Seattle, River West in Chicago, LoDo in Denver, the Mount Vernon Triangle in Washington, DC and Hudson Yards in Manhattan are some of the areas with evolving real estate characteristics that appeal to firms, but are closer to the favorable demographics and talented workforce that law firms need to thrive moving forward. This is happening even in the suburbs: Los Angeles-based firms specializing in media and entertainment law may find that the burgeoning tech and media scene in Playa Vista is more appealing than corporate-heavy Century City. Law firms should consider not just their current workforce, but also long-term talent acquisition and retention in potential relocations as competition for associates grows.

Talent, not a premier address, will increasingly influence site selection

7JLL | United States | Law Firm Perspective | 2014

About half of a typical law firm’s employees are not lawyers, but rather non-revenue administrative functions such as operations, finance, marketing and human resources. Furthermore, many firms still house contract attorneys, a lower-revenue source, in primary markets or high-priced real estate. With improved technology, headquartered firms in high-cost markets such as Boston, New York, Washington, DC and San Francisco are increasingly able to move these positions to lower-cost metro areas, including the Sun Belt, Midwest and Mountain West, or lower-priced buildings in primary cities, resulting in significant cost savings from rent and labor. This strategy keeps revenue producers in competitive products in core geographies and helps maximize profitability for firms by lowering labor costs and reducing redundancies across offices.

We don’t all have to sit together -firms relocating non-revenue functions

8JLL | United States | Law Firm Perspective | 2014

Despite changes in space utilization across industries, U.S. law firms on the whole remain somewhat hesitant to fully adapt to more contemporary, open-office plans compared to their global counterparts and other professional-and business-service industries. For instance, U.S. firms require more “me” than “we” space compared to other industries domestically as they spend more time on research and writing that requires personal space. In addition, American law firms have a lower partner-to-associate ratio compared to global counterparts and thus have a difficult time switching to non-office plans. In London and some cities in Asia, firms have more flexibility in terms of build-outs and workplace strategy due to the higher number of associates compared to partners. Further, the older office inventory found in U.S. CBDs favors traditional layouts. Despite some hesitation, even American law firms are demonstrating preferences for shared open-plan areas, interior glass-fronted offices, multipurpose collaborative space and lawyer lounges.

Despite moves toward efficiency, firms are still wary of aggressively reconfiguring offices

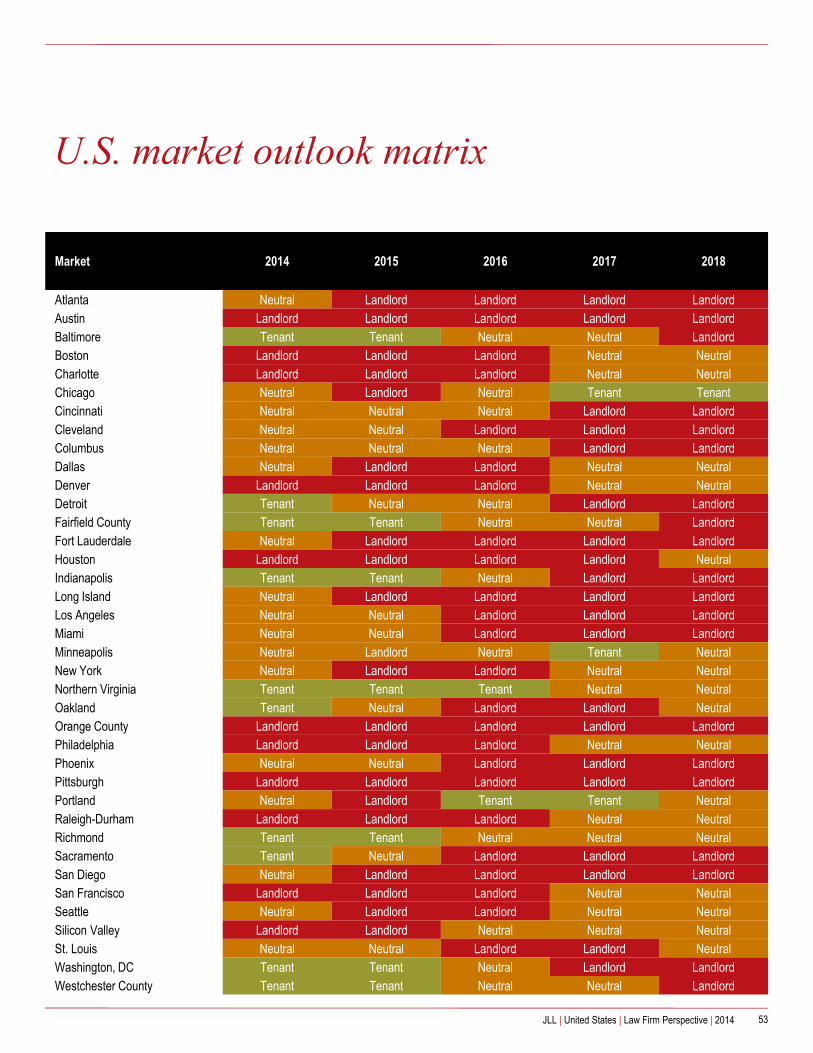

2014 U.S. law firm office clock

9JLL | United States | Law Firm Perspective | 2014

Peakingphase

Fallingphase

Risingphase

Bottomingphase

Source: JLL Research

Atlanta, PhiladelphiaBoston, New York (Midtown), United States

Seattle, Miami

Charlotte, Dallas, Fort Lauderdale,Los Angeles, Westchester County

Austin, Houston

Baltimore, Sacramento

New York (Downtown), Phoenix, Richmond

Fairfield County, Indianapolis, Minneapolis

Columbus, San Diego,Washington, DC

Pittsburgh, Portland

Chicago, Cleveland,Oakland CBD, Raleigh-Durham

San Francisco

Denver

Cincinnati, Detroit

St. Louis

Silicon Valley (Palo Alto)

Local U.S. law firm markets

10JLL | United States | Law Firm Perspective | 2014

Percent of market occupied by law firms

Number of law firms occupying> 50,000 square feet in the market

16% 27

Atlanta

11JLL | United States | Law Firm Perspective | 2014

Outlook

Challenges for law firms• Technology firms are beginning to drive demand in many of the Midtown

Trophy towers, competing for space options.• Delivery of new Class A inventory is still 12 to 18 months off and leasing

conditions are brisk; availability of premium contiguous options is increasingly scarce.

• Moderate rental rate appreciation may impact value-conscious firms as leasing conditions in the CBD become increasingly landlord-favorable.

Opportunities for law firms

• Planned towers are generally transit-oriented in terms of design and location, allowing for direct connectivity to the airport.

• Labor pool is expanding due to a robust population increase anticipated ahead.

• Rental rates remain discounted and attractive relative to gateway markets.

Atlanta-based firms made significant relocation and renewal plays in months following the recession, capitalizing on tenant-favorable leasing conditions and using the opportunity to streamline operations. Since then, however, real estate movement among industry participants has proven relatively sparse in Atlanta's urban submarkets. Only a handful of active requirements for space exist, suggesting leasing may continue to be slow through early 2015.

We do see opportunity on the horizon for smaller firms, which tend to serve local or regional clientele and are often highly specialized. These groups will likely see outsized benefit from continued improvement in the economy. As such, many Atlanta firms will grow quickly and find a need for more space. The question remains: Will they choose formal glass towers along the Peachtree corridor or gravitate to non-traditional converted warehouse-type product—once only reserved for the city's high-tech tenants. Regardless, we anticipate these nimble practices to be in the market first.

Mid- and large-sized firms are expected to eventually account for preleasing of much of the city's premium top-floor Trophy space as Atlanta's office development cycle matures. Asking rates for top elevator bank space will escalate into the low $40-per-square-foot range, drawing a sharp contrast against lease terms negotiated just following the recession..

Hunton & Williams600 Peachtree StreetRenewal43,000 s.f.

Bodker, Ramsey, Andrews, Winograd& Wildstein, P.C.3490 Piedmont RoadRenewal12,000 s.f.R

ecen

t law

-firm

-com

plet

ed tr

ansa

ctio

ns

Hollowell, Foster & Herring260 Peachtree StreetNew to market12,500 s.f.

2014 2015 2016 2017 2018Tenant-favorable marketNeutral marketLandlord-favorable market

Active law firm requirements in the market (s.f.)

Savell & Williams 25,000

Fish & Richardson 25,000

Kazmarek Mowrey Cloud Laseter 10,000

*rent difference from Class A average **averages on 10-year new/renewal transactions

Pricing and incentives (assuming a 10-year lease)

TI allowance ($ p.s.f.)** Free rent (months)**$45.00/$30.00 10/6

Net rent

$11.85Taxes

$3.40Operating expenses

$8.00Annual escalation

3.6%

20.0% 3.6% 25.0%

Premium for Trophy space*

Discount for negotiated rent*

Discount for sublease space*

Locational preference: The vast majority of Atlanta’s law firms choose to locate within the city’s urban submarkets of Buckhead, Midtown and Downtown. Central Perimeter has been urbanizing throughout the recovery. With a concentration of corporate occupiers nearby, transit options, and quality office inventory, the area often competes against Buckhead and Midtown. Proposed new towers in the area could threaten to lure firms from their traditional confines.

Percent of market occupied by law firms

25%

Austin

12JLL | United States | Law Firm Perspective | 2014

Outlook

Challenges for law firms• Heightened demand in Austin's CBD will continue to push rental

rates upward.• Few immediate near-term large blocks remain available.

Opportunities for law firms

• A new wave of development is likely on the way, which could offset rental rate increases over the next few years. Proposed buildings, Green Water and 5th & Colorado could deliver up to 670,000 square feet by 2016.

• Heated demand for expansion and growth opportunities among all tenants in the CBD creates an environment that is favorable to law firms looking to give back space as they seek to maximize efficiency.

The landscape of Austin’s CBD has undergone a transformation, and law firms no longer dominate the downtown office landscape. Heated competition for space, largely driven by demand from high-tech tenants, has left law firms with fewer options for high-quality office space in the city.

The majority of the significantly sized law firms in town have already rightsized and locked down space for the next 10 years. However, new construction downtown has attracted several firms away from their existing space. At Colorado Tower, set to deliver this year, law firms represent 22.0 percent of preleased space, with Scott, Douglass & McConnico; Dubois Bryant, and Munsch Hardt Kopf & Harr all signing significant deals there.

A new wave of development is likely on the way, which could offset rental rate increases over the next few years. Firms who sign deals today might be overpaying in the future. The proposed buildings, Green Water and 5th & Colorado, could deliver up to 670,000 square feet by 2016. The 19,000-square-foot floor plates at 5th & Colorado are ideal for the shrinking footprint of the modern law firm.

Scott, Douglass & McConnico303 Colorado StreetRelocation40,483 s.f.

Greenberg Traurig300 W 6th Street Renewal with expansion21,859 s.f.

DuBois, Bryant & Campbell303 Colorado StreetRelocation24,273 s.f.

2014 2015 2016 2017 2018Tenant-favorable marketNeutral marketLandlord-favorable market

Active law firm requirements in the market (s.f.)

Andrews Kurth LLP 35,000

Chamberlain McHaney 15,000

Gardere Wynne Sewell 15,000

*rent difference from Class A average **averages on 10-year new/renewal transactions

Pricing and incentives (assuming a 10-year lease)

TI allowance ($ p.s.f.)** Free rent (months)**$45.00/$20.00 2.5/2.6

Net rent

$27.07Taxes

$8.00Operating expenses

$8.07Annual escalation

$1.00

20.0% 10.0% 25.0%

Premium for Trophy space*

Discount for negotiated rent*

Discount for sublease space*

Number of law firms occupying> 50,000 square feet in the market

7Locational preference: The majority of law firms in Austin are located in the CBD, with proximity to the Capitol being a huge draw to the area. Due to high rents in Downtown Austin, some law firms, such as Vinson & Elkins, have opted to lease space in high-quality office projects in Southwest Austin or along the South MoPaccorridor. However, with construction finally commencing downtown, several firms are locking in deals at new developments.

Rec

ent l

aw-fi

rm-c

ompl

eted

tran

sact

ions

Locational preference: A handful of firms have relocated to Harbor East, but the majority of firms are located along Pratt and Charles Street in the CBD. Exelon's relocation to Harbor Point in 2016 will create a large block of Class A space at 750 E Pratt Street in addition to 50,000 square feet of speculative space that will deliver at Exelon's new headquarters. The two additional blocks will create opportunities for firms to continue their long-standing trend of migration south and east.

Percent of market occupied by law firms

9%

Baltimore

13JLL | United States | Law Firm Perspective | 2014

Outlook

Challenges for law firms• A long-standing trend of flight to quality and limited construction pipeline

has resulted in limited large blocks of Class A space.• The trend of conversions of Class B office space into residential has

accelerated in the past year and taken a total of over 800,000 square feet out of supply.

• Vacancy along Pratt Street and in Harbor East will fall well below 10 percent in the coming year, which will likely lead to increasing Class A and Trophy rents.

Opportunities for law firms

• Landlords are still focused on tenant retention, especially for locations off Pratt Street in the CBD, and are offering generous concession packages.

• Law firms will have a new relocation option in Harbor Point at Exelon's new headquarters, which is set to deliver in 2016 with approximately 50,000 square feet available.

• For tenants not requiring Class A space along Pratt Street or Harbor East, rents along Baltimore and Charles Street have continued a downward slide.

Compared to the major reshuffling in the downtown Baltimore law firm market in 2010 and 2011, activity remained relatively limited in 2014, with a handful of notable leasing transactions and limited sizeable tenants in the market. Law firms have followed the overall market in a steady migration to the south and east in a flight to quality that has left elevated vacancy along Baltimore and Charles Street in the CBD. The trend has left highly desirable Pratt Street with only three available Class A blocks larger than 30,000 square feet and none greater than 50,000 square feet. Off Pratt Street in the CBD, inventory has continued to dwindle as the trend of conversion of Class B office space into residential apartments has accelerated.

In late 2013, 10–12 N Calvert Street, a partially occupied 178,992-square-foot Class B building, traded to a developer with plans to convert the building into 180 apartment units. Consequently, numerous law firm tenants in the building, primarily under 5,000 square feet, have been forced into the market, which helped drive needed leasing velocity in the Charles Street Corridor as they sought to relocate in close proximity to the courthouses. While large blocks of Class A space are limited, landlords continue to be aggressive in concessions, especially off Pratt Street.

Peter T. Nicholl36 S Charles StreetRenewal42,708 s.f.

Womble Carlyle & Sandridge250 W Pratt StreetRenewal10,487 s.f.

Shapiro Sher250 W Pratt StreetRelocation15,000 s.f.

2014 2015 2016 2017 2018Tenant-favorable marketNeutral marketLandlord-favorable market

Active law firm requirements in the market (s.f.)

N/A

*rent difference from Class A average **averages on 10-year new/renewal transactions

Pricing and incentives (assuming a 10-year lease)

TI allowance ($ p.s.f.)** Free rent (months)**$17.00/$14.00 12/4

Net rent

$11.85Taxes

$2.50Operating expenses

$9.00Annual escalation

3.0%

40.0% 5.0% 20.0%

Premium for Trophy space*

Discount for negotiated rent*

Discount for sublease space*

Number of law firms occupying> 50,000 square feet in the market

8

Rec

ent l

aw-fi

rm-c

ompl

eted

tran

sact

ions

Percent of market occupied by law firms

10%

Boston

14JLL | United States | Law Firm Perspective | 2014

Outlook

Challenges for law firms• Strong employment growth and urbanization have created enhanced

demand for CBD space.• Competition for space from high-tech companies will continue to push

Class A low-rise and Class B rents upward.• Concession packages continue to tighten given the landlord-

favorable market.

Opportunities for law firms

• Remaining spaces within build-to-suit projects provide mid-sized law firms options to rightsize.

• Large blocks of space in Class A buildings in the Financial District and Back Bay will come on the market in the next few years.

• Firms specialized in the intellectual property and high-tech industries have the ability to relocate to buildings in close proximity to high-tech companies.

Legal employment in Massachusetts is still down nearly 2,600 jobs from pre-recession peaks. While Boston is the hub of the law firm market in New England, we have seen a modest decline in employment over the past year. However, Boston is experiencing stronger growth in the intellectual property and corporate law practices, spurred by the area’s rise in the high-tech and life sciences fields.

As area law firms are reconfiguring offices to be more in line with trends in the industries they serve, they are looking for flexible, more efficient spaces and many are considering moves from more traditional and suburban locations. As a result, the Seaport District, dubbed the Innovation District and home to a growing number of high-tech start-ups and the pharmaceutical giant Vertex, has attracted law firms from within and outside Boston looking to maximize proximity to potential clients. For example, Goodwin Procter signed a build-to-suit lease to occupy 360,000 square feet at Fan Pier, downsizing from 415,000 square feet in Financial District partly as a result of a more efficient building with greater window-line ratios. Gunderson Dettmer, a business law firm specializing in early stage companies and venture capital firms, also signed a 27,000-square-foot lease at Joseph Fallon’s One Marina Park Drive on Boston’s waterfront. The result of these relocations and other similar transactions will be larger blocks of tower space on the market beginning to impact both vacancy and rents. A few of the larger contiguous availabilities being marketed early to avoid significant vacancy include spaces that will be vacated by Goodwin Procter at 53 State Street, State Street Corporation at 200 Clarendon Street and Copley Place as well as PwC and Verizon at 125 High Street.

Skadden500 Boylston StreetRelocation47,722 s.f.

Gunderson Dettmer 1 Marina Park DriveRelocation27,692 s.f.

Hemenway & Barnes75 State StreetRelocation44,233 s.f.

2014 2015 2016 2017 2018Tenant-favorable marketNeutral marketLandlord-favorable market

Active law firm requirements in the market (s.f.)

Prince Lobel 55,000

Cetrullo 37,500

Fragomen 35,000

*rent difference from Class A average **averages on 10-year new/renewal transactions

Pricing and incentives (assuming a 10-year lease)

TI allowance ($ p.s.f.)** Free rent (months)**$55.00/$25.00 4/2

Net rent

$36.61Taxes

$8.00Operating expenses

$10.00Annual escalation

3.0%

20.0% 10.0% 30.0%

Premium for Trophy space*

Discount for negotiated rent*

Discount for sublease space*

Number of law firms occupying> 50,000 square feet in the market

28Locational preference: The city's premier law firms occupy space in the most prestigious office towers in Boston's Back Bay, Financial and Seaport Districts.

Rec

ent l

aw-fi

rm-c

ompl

eted

tran

sact

ions

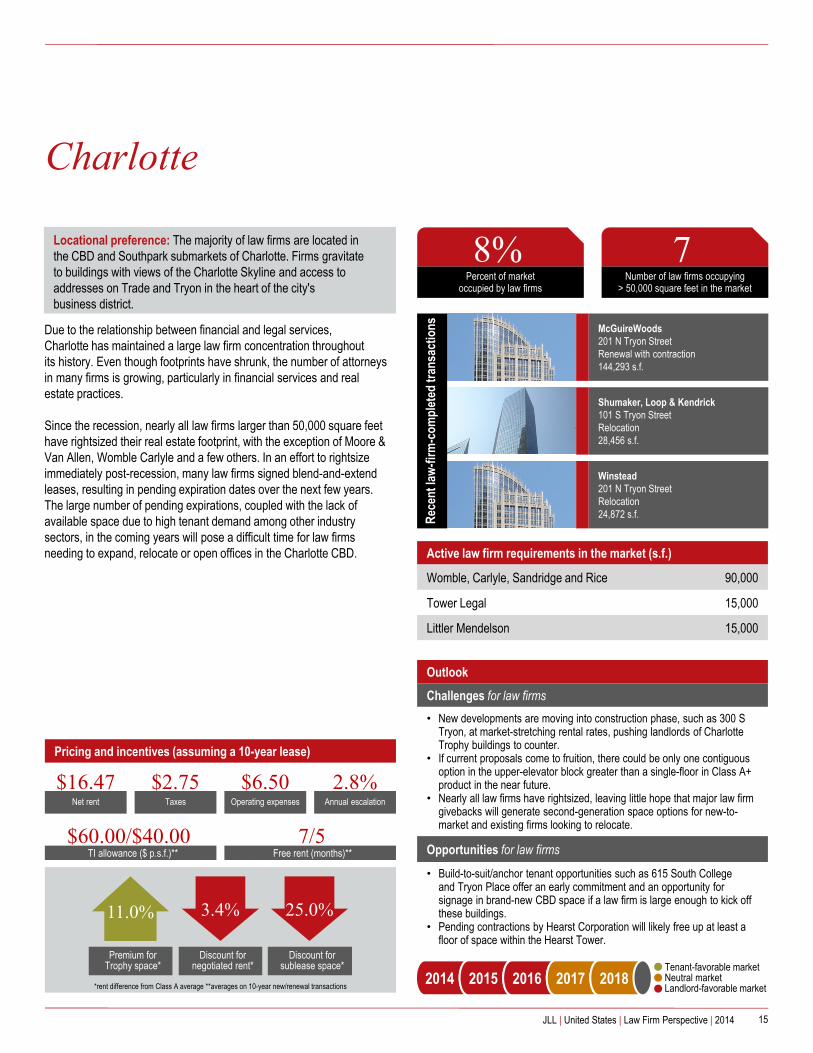

Locational preference: The majority of law firms are located in the CBD and Southpark submarkets of Charlotte. Firms gravitate to buildings with views of the Charlotte Skyline and access to addresses on Trade and Tryon in the heart of the city's business district.

Percent of market occupied by law firms

8%

Charlotte

15JLL | United States | Law Firm Perspective | 2014

Outlook

Challenges for law firms• New developments are moving into construction phase, such as 300 S

Tryon, at market-stretching rental rates, pushing landlords of Charlotte Trophy buildings to counter.

• If current proposals come to fruition, there could be only one contiguous option in the upper-elevator block greater than a single-floor in Class A+ product in the near future.

• Nearly all law firms have rightsized, leaving little hope that major law firm givebacks will generate second-generation space options for new-to-market and existing firms looking to relocate.

Opportunities for law firms

• Build-to-suit/anchor tenant opportunities such as 615 South College and Tryon Place offer an early commitment and an opportunity for signage in brand-new CBD space if a law firm is large enough to kick off these buildings.

• Pending contractions by Hearst Corporation will likely free up at least a floor of space within the Hearst Tower.

Due to the relationship between financial and legal services, Charlotte has maintained a large law firm concentration throughout its history. Even though footprints have shrunk, the number of attorneys in many firms is growing, particularly in financial services and real estate practices.

Since the recession, nearly all law firms larger than 50,000 square feet have rightsized their real estate footprint, with the exception of Moore & Van Allen, Womble Carlyle and a few others. In an effort to rightsizeimmediately post-recession, many law firms signed blend-and-extend leases, resulting in pending expiration dates over the next few years. The large number of pending expirations, coupled with the lack of available space due to high tenant demand among other industry sectors, in the coming years will pose a difficult time for law firms needing to expand, relocate or open offices in the Charlotte CBD.

McGuireWoods201 N Tryon StreetRenewal with contraction144,293 s.f.

Winstead201 N Tryon StreetRelocation24,872 s.f.

Shumaker, Loop & Kendrick101 S Tryon StreetRelocation28,456 s.f.

2014 2015 2016 2017 2018Tenant-favorable marketNeutral marketLandlord-favorable market

Active law firm requirements in the market (s.f.)

Womble, Carlyle, Sandridge and Rice 90,000

Tower Legal 15,000

Littler Mendelson 15,000

*rent difference from Class A average **averages on 10-year new/renewal transactions

Pricing and incentives (assuming a 10-year lease)

TI allowance ($ p.s.f.)** Free rent (months)**$60.00/$40.00 7/5

Net rent

$16.47Taxes

$2.75Operating expenses

$6.50Annual escalation

2.8%

11.0% 3.4% 25.0%

Premium for Trophy space*

Discount for negotiated rent*

Discount for sublease space*

Number of law firms occupying> 50,000 square feet in the market

7

Rec

ent l

aw-fi

rm-c

ompl

eted

tran

sact

ions

Percent of market occupied by law firms

10%

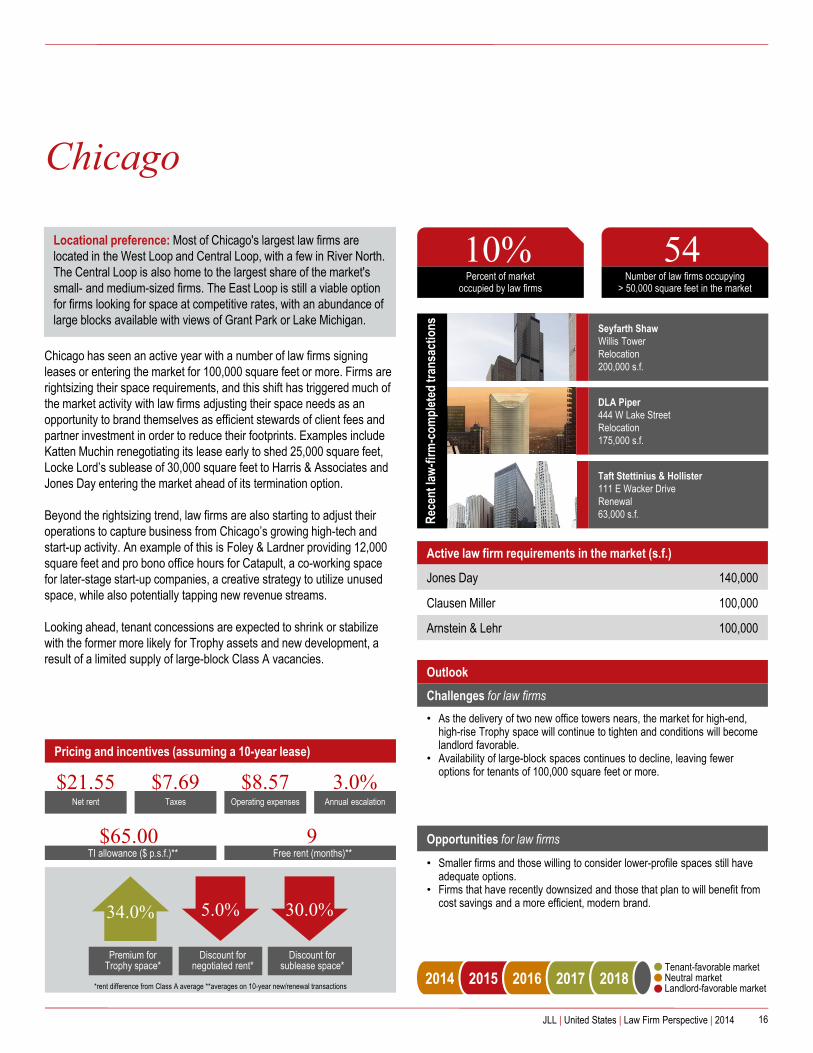

Chicago

16JLL | United States | Law Firm Perspective | 2014

Outlook

Challenges for law firms• As the delivery of two new office towers nears, the market for high-end,

high-rise Trophy space will continue to tighten and conditions will become landlord favorable.

• Availability of large-block spaces continues to decline, leaving fewer options for tenants of 100,000 square feet or more.

Opportunities for law firms

• Smaller firms and those willing to consider lower-profile spaces still have adequate options.

• Firms that have recently downsized and those that plan to will benefit from cost savings and a more efficient, modern brand.

Chicago has seen an active year with a number of law firms signing leases or entering the market for 100,000 square feet or more. Firms are rightsizing their space requirements, and this shift has triggered much of the market activity with law firms adjusting their space needs as an opportunity to brand themselves as efficient stewards of client fees and partner investment in order to reduce their footprints. Examples include Katten Muchin renegotiating its lease early to shed 25,000 square feet, Locke Lord’s sublease of 30,000 square feet to Harris & Associates and Jones Day entering the market ahead of its termination option.

Beyond the rightsizing trend, law firms are also starting to adjust their operations to capture business from Chicago’s growing high-tech and start-up activity. An example of this is Foley & Lardner providing 12,000 square feet and pro bono office hours for Catapult, a co-working space for later-stage start-up companies, a creative strategy to utilize unused space, while also potentially tapping new revenue streams.

Looking ahead, tenant concessions are expected to shrink or stabilize with the former more likely for Trophy assets and new development, a result of a limited supply of large-block Class A vacancies.

Seyfarth ShawWillis TowerRelocation 200,000 s.f.

Taft Stettinius & Hollister111 E Wacker DriveRenewal63,000 s.f.

DLA Piper444 W Lake StreetRelocation 175,000 s.f.

2014 2015 2016 2017 2018Tenant-favorable marketNeutral marketLandlord-favorable market

Active law firm requirements in the market (s.f.)

Jones Day 140,000

Clausen Miller 100,000

Arnstein & Lehr 100,000

*rent difference from Class A average **averages on 10-year new/renewal transactions

Pricing and incentives (assuming a 10-year lease)

TI allowance ($ p.s.f.)** Free rent (months)**$65.00 9

Net rent

$21.55Taxes

$7.69Operating expenses

$8.57Annual escalation

3.0%

34.0% 5.0% 30.0%

Premium for Trophy space*

Discount for negotiated rent*

Discount for sublease space*

Number of law firms occupying> 50,000 square feet in the market

54Locational preference: Most of Chicago's largest law firms are located in the West Loop and Central Loop, with a few in River North. The Central Loop is also home to the largest share of the market's small- and medium-sized firms. The East Loop is still a viable option for firms looking for space at competitive rates, with an abundance of large blocks available with views of Grant Park or Lake Michigan.

Rec

ent l

aw-fi

rm-c

ompl

eted

tran

sact

ions

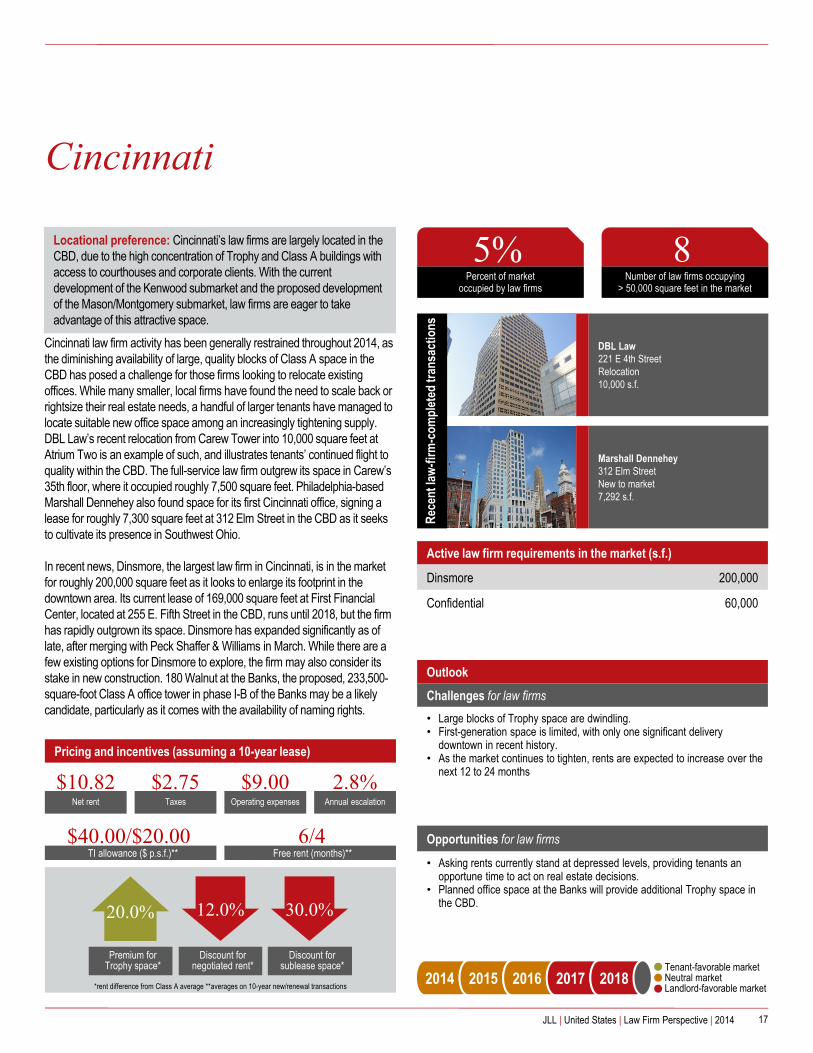

Locational preference: Cincinnati’s law firms are largely located in the CBD, due to the high concentration of Trophy and Class A buildings with access to courthouses and corporate clients. With the current development of the Kenwood submarket and the proposed development of the Mason/Montgomery submarket, law firms are eager to take advantage of this attractive space.

Percent of market occupied by law firms

5%

Cincinnati

17JLL | United States | Law Firm Perspective | 2014

Outlook

Challenges for law firms• Large blocks of Trophy space are dwindling.• First-generation space is limited, with only one significant delivery

downtown in recent history.• As the market continues to tighten, rents are expected to increase over the

next 12 to 24 months

Opportunities for law firms

• Asking rents currently stand at depressed levels, providing tenants an opportune time to act on real estate decisions.

• Planned office space at the Banks will provide additional Trophy space in the CBD.

Cincinnati law firm activity has been generally restrained throughout 2014, as the diminishing availability of large, quality blocks of Class A space in the CBD has posed a challenge for those firms looking to relocate existing offices. While many smaller, local firms have found the need to scale back or rightsize their real estate needs, a handful of larger tenants have managed to locate suitable new office space among an increasingly tightening supply. DBL Law’s recent relocation from Carew Tower into 10,000 square feet at Atrium Two is an example of such, and illustrates tenants’ continued flight to quality within the CBD. The full-service law firm outgrew its space in Carew’s 35th floor, where it occupied roughly 7,500 square feet. Philadelphia-based Marshall Dennehey also found space for its first Cincinnati office, signing a lease for roughly 7,300 square feet at 312 Elm Street in the CBD as it seeks to cultivate its presence in Southwest Ohio.

In recent news, Dinsmore, the largest law firm in Cincinnati, is in the market for roughly 200,000 square feet as it looks to enlarge its footprint in the downtown area. Its current lease of 169,000 square feet at First Financial Center, located at 255 E. Fifth Street in the CBD, runs until 2018, but the firm has rapidly outgrown its space. Dinsmore has expanded significantly as of late, after merging with Peck Shaffer & Williams in March. While there are a few existing options for Dinsmore to explore, the firm may also consider its stake in new construction. 180 Walnut at the Banks, the proposed, 233,500-square-foot Class A office tower in phase I-B of the Banks may be a likely candidate, particularly as it comes with the availability of naming rights.

DBL Law221 E 4th StreetRelocation10,000 s.f.

Marshall Dennehey312 Elm StreetNew to market7,292 s.f.

2014 2015 2016 2017 2018Tenant-favorable marketNeutral marketLandlord-favorable market

Active law firm requirements in the market (s.f.)

Dinsmore 200,000

Confidential 60,000

*rent difference from Class A average **averages on 10-year new/renewal transactions

Pricing and incentives (assuming a 10-year lease)

TI allowance ($ p.s.f.)** Free rent (months)**$40.00/$20.00 6/4

Net rent

$10.82Taxes

$2.75Operating expenses

$9.00Annual escalation

2.8%

20.0% 12.0% 30.0%

Premium for Trophy space*

Discount for negotiated rent*

Discount for sublease space*

Number of law firms occupying> 50,000 square feet in the market

8

Rec

ent l

aw-fi

rm-c

ompl

eted

tran

sact

ions

Percent of market occupied by law firms

17%

Cleveland

18JLL | United States | Law Firm Perspective | 2014

Outlook

Challenges for law firms• Rent increases are forecasted in prime assets over the next 12 months.• Concessions will begin to taper off as leverage transitions to landlords.• Limited large blocks will hinder law firm with active requirements of more

than 50,000 square feet.

Opportunities for law firms

• Additional office product is in the development pipeline downtown.• Law firms signing leases over the next 12 months will lock in historically

favorable lease rates.

Law firm tenant activity remained elevated through 2014, with lease signings totaling more than 250,000 square feet. The majority of transactions occurred downtown and involved relocations as tenants looked to upgrade offices. The largest law firm lease signed over the last year was by BakerHostetler. The law firm signed a lease for five floors at Key Tower in Downtown Cleveland, though the firm will not move into the city’s tallest office building until January 2016. BakerHostetler expects to move its Cleveland attorneys and office staff, a total of about 300 employees, to 115,000 square feet at Key Tower. The law firm signed a 15-year lease for floors 17 to 21 at Key Tower, absorbing much of the space given back by Key Bank when it signed a long-term renewal in mid-2013. BakerHostetler will move from the PNC Center downtown, where it currently leases roughly 165,000 square feet.

Other notable law firm transactions include Vorys, which leased 42,000 square feet at 200 Public Square, about as much space as it currently occupies at One Cleveland Center. Additionally, Cleveland-based law firm Mansour Gavin, which relocated in the second quarter from its longtime home at 55 Public Square to 21,000 square feet at North Point Tower. With the move, Mansour Gavin was able to upgrade to newer office space and gain future expansion rights. Finally, Zashin & Rich, leased the last full floor of the Ernst & Young Tower in the Flats East Bank project, relocating from 55 Public Square.

BakerHostetler127 Public SquareRelocation 115,000 s.f.

Mansour Gavin1001 Lakeside AvenueRelocation 21,000 s.f.

Vorys200 Public SquareRelocation 42,000 s.f.

2014 2015 2016 2017 2018Tenant-favorable marketNeutral marketLandlord-favorable market

Active law firm requirements in the market (s.f.)

Taft 50,000

Frantz Ward 40,000

Javitch Block 30,000

*rent difference from Class A average **averages on 10-year new/renewal transactions

Pricing and incentives (assuming a 10-year lease)

TI allowance ($ p.s.f.)** Free rent (months)**$50.00/$25.00 10/5

Net rent

$13.24Taxes

$3.00Operating expenses

$7.00Annual escalation

2.5%

20.0% 15.0% 25.0%

Premium for Trophy space*

Discount for negotiated rent*

Discount for sublease space*

Number of law firms occupying> 50,000 square feet in the market

13Locational preference: Cleveland's law firms are concentrated in the CBD, largely within the Financial and Public Square submarkets. Both areas are replete with a dense selection of Trophy and Class A assets offering convenient access to corporate clients as well as city, county and federal courthouses.

Rec

ent l

aw-fi

rm-c

ompl

eted

tran

sact

ions

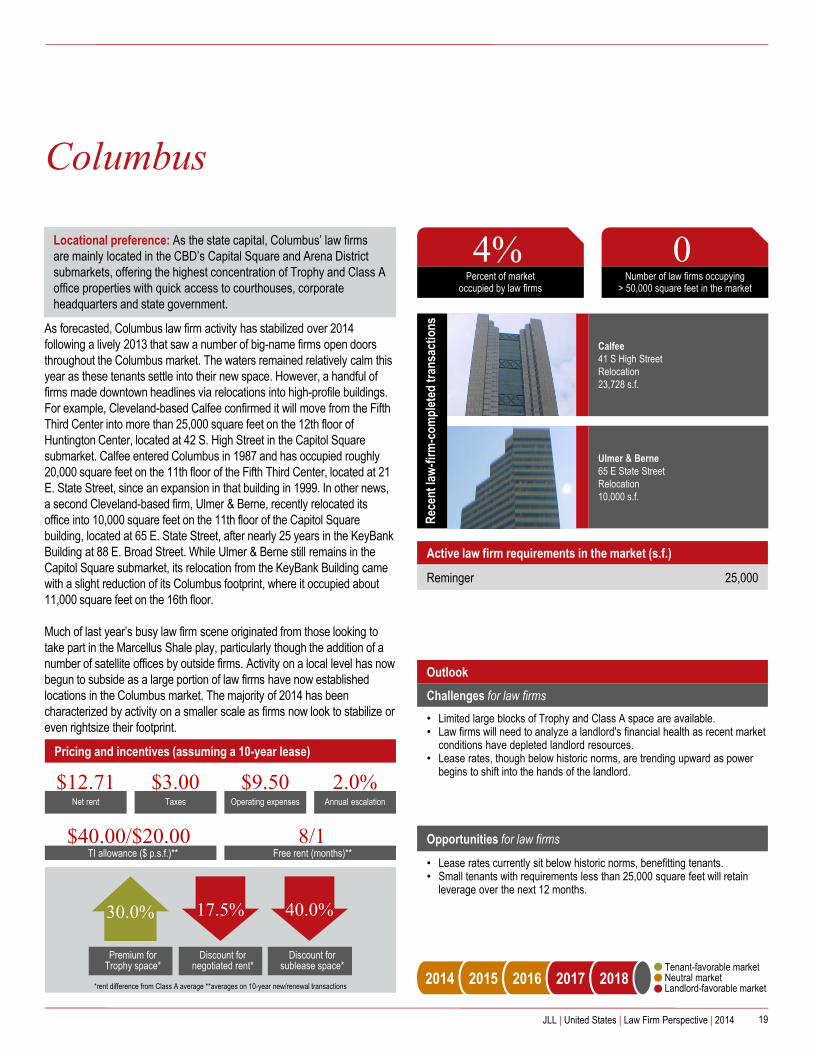

Locational preference: As the state capital, Columbus’ law firms are mainly located in the CBD’s Capital Square and Arena District submarkets, offering the highest concentration of Trophy and Class A office properties with quick access to courthouses, corporate headquarters and state government.

Percent of market occupied by law firms

4%

Columbus

19JLL | United States | Law Firm Perspective | 2014

Outlook

Challenges for law firms• Limited large blocks of Trophy and Class A space are available.• Law firms will need to analyze a landlord's financial health as recent market

conditions have depleted landlord resources.• Lease rates, though below historic norms, are trending upward as power

begins to shift into the hands of the landlord.

Opportunities for law firms

• Lease rates currently sit below historic norms, benefitting tenants.• Small tenants with requirements less than 25,000 square feet will retain

leverage over the next 12 months.

As forecasted, Columbus law firm activity has stabilized over 2014 following a lively 2013 that saw a number of big-name firms open doors throughout the Columbus market. The waters remained relatively calm this year as these tenants settle into their new space. However, a handful of firms made downtown headlines via relocations into high-profile buildings. For example, Cleveland-based Calfee confirmed it will move from the Fifth Third Center into more than 25,000 square feet on the 12th floor of Huntington Center, located at 42 S. High Street in the Capitol Square submarket. Calfee entered Columbus in 1987 and has occupied roughly 20,000 square feet on the 11th floor of the Fifth Third Center, located at 21 E. State Street, since an expansion in that building in 1999. In other news, a second Cleveland-based firm, Ulmer & Berne, recently relocated its office into 10,000 square feet on the 11th floor of the Capitol Square building, located at 65 E. State Street, after nearly 25 years in the KeyBank Building at 88 E. Broad Street. While Ulmer & Berne still remains in the Capitol Square submarket, its relocation from the KeyBank Building came with a slight reduction of its Columbus footprint, where it occupied about 11,000 square feet on the 16th floor.

Much of last year’s busy law firm scene originated from those looking to take part in the Marcellus Shale play, particularly though the addition of a number of satellite offices by outside firms. Activity on a local level has now begun to subside as a large portion of law firms have now established locations in the Columbus market. The majority of 2014 has been characterized by activity on a smaller scale as firms now look to stabilize or even rightsize their footprint.

Calfee41 S High StreetRelocation23,728 s.f.

Ulmer & Berne65 E State StreetRelocation10,000 s.f.

2014 2015 2016 2017 2018Tenant-favorable marketNeutral marketLandlord-favorable market

Active law firm requirements in the market (s.f.)

Reminger 25,000

*rent difference from Class A average **averages on 10-year new/renewal transactions

Pricing and incentives (assuming a 10-year lease)

TI allowance ($ p.s.f.)** Free rent (months)**$40.00/$20.00 8/1

Net rent

$12.71Taxes

$3.00Operating expenses

$9.50Annual escalation

2.0%

30.0% 17.5% 40.0%

Premium for Trophy space*

Discount for negotiated rent*

Discount for sublease space*

Number of law firms occupying> 50,000 square feet in the market

0

Rec

ent l

aw-fi

rm-c

ompl

eted

tran

sact

ions

Percent of market occupied by law firms

14%

Dallas

20JLL | United States | Law Firm Perspective | 2014

Outlook

Challenges for law firms• Uptown and the Arts District have tight vacancy and upward pressure on

rates, especially in the Trophy segment.• With several law firms expanding into the Dallas market, law firms are

facing new competition.

Opportunities for law firms

• Smaller firms have lots of available options, including backfilling excess space from other law firms.

• Two construction projects are currently under way, with a potential two or three additional developments breaking ground over the next year.

• Increase in institutional ownership in the CBD makes existing properties more attractive to law firms.

Law firm leasing activity has increased over last year for the Dallas market. While some firms have renewed and rightsized in their current locations, new and pending construction has lured a few of the larger firms from their established locations. Jackson Walker followed KPMG into the new KPMG Plaza at Hall Arts project in the CBD and GardereWynne Sewell and Sidley Austin are the first tenants to commit to Crescent’s new McKinney & Olive project in Uptown, scheduled to break ground in late 2014. Both of these projects are setting record asking rates, with full service gross rents in the $48.00- to $51.00-per-square-foot range. These rates are 15 to 20 percent higher than previous top rates.

Competition in the sector is also increasing locally due to the growth in energy and North Texas’ overall economic strength. In addition to consolidations, several national firms have opened Dallas offices in recent years. In early 2014, McGuireWoods, for example, opened an office at 2000 McKinney Avenue, starting with some former Patton Boggs partners. Perkins Coie (Ross Tower) and Holland & Knight (The Crescent), among others have also entered Dallas over the past few years.

Locke Lord2200 Ross AvenueRenewal176,057 s.f.

Jackson Walker2323 Ross AvenueRelocation 104,064 s.f.

Gardere2021 McKinney AvenueRelocation 109,000 s.f.

2014 2015 2016 2017 2018Tenant-favorable marketNeutral marketLandlord-favorable market

Active law firm requirements in the market (s.f.)

K&L Gates 65,000

Dentons 65,000

Strasburger & Price 60,000

*rent difference from Class A average **averages on 10-year new/renewal transactions

Pricing and incentives (assuming a 10-year lease)

TI allowance ($ p.s.f.)** Free rent (months)**$45.00/$20.00 10/6

Net rent

$19.50Taxes

$1.50Operating expenses

$9.00Annual escalation

2.5%

30.0% 12.0% 40.0%

Premium for Trophy space*

Discount for negotiated rent*

Discount for sublease space*

Number of law firms occupying> 50,000 square feet in the market

31Locational preference: The majority of firms are located within Trophy and Class A+ properties Downtown (the Dallas CBD) and Uptown. A firm’s potential move will parallel any new, high-end development delivered in these submarkets; both the CBD's and Uptown's latest spec developments are significantly occupied by law firms.

Rec

ent l

aw-fi

rm-c

ompl

eted

tran

sact

ions

Percent of market occupied by law firms

10%

Denver

21JLL | United States | Law Firm Perspective | 2014

Outlook

Challenges for law firms• Large blocks of space among well-located Trophy buildings continue to

decline due to oil and gas demand. • Credit enhancements are in greater demand as market tightens and

owners evaluate leasing options.• Owners of Trophy buildings have aggressively pushed rates based on

limited options, especially high-rise view space as well as space in LoDo.

Opportunities for law firms

• New construction is ramping up in the Denver CBD as three buildings remain under construction and at least three more will break ground within six months.

• Sublease dispositions have created additional space options for tenants, particularly in small to mid-size blocks.

Similar to many occupiers in the market, law firms are looking for opportunities to reduce real estate costs, while maintaining occupancy in view space in higher-quality buildings. Many firms are creating more efficient office layouts with smaller offices in hopes of avoiding construction costs when intra-office moves occur. Law firms are also reducing the number of sized offices from four to two, allowing for more offices and open space without expanding. Currently, most firms in the CBD are stable, with a few out in the market looking to expand their presence in Denver.

Denver has transitioned into an investor-heavy market, creating competition among building owners for tenants. Although the CBD is a landlord-favorable market, this competition has translated into higher tenant improvement and free rent packages. This has allowed tenants to create the aforementioned office space that will attract new talent and allow for more hires.

Holland & Hart555 17th StreetRenewal145,693 s.f.

BakerHostetler1801 California StreetRelocation 37,244 s.f.

Polsinelli1401 Lawrence StreetRelocation88,000 s.f.

2014 2015 2016 2017 2018Tenant-favorable marketNeutral marketLandlord-favorable market

Active law firm requirements in the market (s.f.)

Hogan Lovells 60,000

Moye White 45,000

Otten Johnson Robinson Neff & Ragonetti 30,000

*rent difference from Class A average **averages on 10-year new/renewal transactions

Pricing and incentives (assuming a 10-year lease)

TI allowance ($ p.s.f.)** Free rent (months)**$70.00/$50.00 10/8

Net rent

$20.10Taxes

$4.00Operating expenses

$8.00Annual escalation

3.0%

30.0% 8.0% 15.0%

Premium for Trophy space*

Discount for negotiated rent*

Discount for sublease space*

Number of law firms occupying> 50,000 square feet in the market

11Locational preference: Firms have historically been found on the eastern side of Downtown Denver in the Midtown CBD and Uptown/East Side micromarkets; however, development opportunities in LoDo could entice firms in the coming years.

Rec

ent l

aw-fi

rm-c

ompl

eted

tran

sact

ions

Locational preference: While many of Detroit’s largest firms are located in the CBD, a significant portion of small-to-medium-size firms have chosen to locate in the northern submarkets of Bloomfield, Southfield and Troy.

Percent of market occupied by law firms

11%

Detroit

22JLL | United States | Law Firm Perspective | 2014

Outlook

Challenges for law firms• Rent increases are forecasted in prime assets over the next 12 months.• Concessions will begin to taper off as leverage transitions away

from tenants.• New supply remains several years off given market fundamentals.

Opportunities for law firms

• Multiple redevelopment opportunities exist downtown.• Large blocks of space remain available across all size thresholds.

Real estate activity for Detroit area law firms was subdued this past year. The largest lease occurred downtown and involved a renewal of 53,000 square feet by the Kitch firm at One Woodward Avenue. The law firm has occupied a similar amount of space in the Class A property since 1988, although it relocated to higher floors in the tower in 2005. Meanwhile, just blocks away, significant renovations continued through the summer months at the offices of Miller Canfield. The law firm signed a long-term renewal for 70,000 square feet at 150 W Jefferson in March 2013.

In the suburbs, law firm activity over the last year was dominated by smaller firms, where the average lease size was just 11,000 square feet. Five law firm transactions were recorded over the last 12 months in the suburban submarkets, including three in Troy, one in Farmington Hills and one in Southfield. As with the recent lease signings downtown, size requirements in the suburbs have been stable over the last year, with the majority of law firms retaining a similar amount of space with their renewals or relocations, as technology has made legal space more efficient. Of the five transactions, three involved relocations as tenants looked to upgrade offices, while the other two transactions were renewals in top-quality assets.

Kitch1 WoodwardRenewal53,000 s.f.

Johnson Rosati Schultz Joppich27555 Executive Drive Relocation13,000 s.f.

Whiting Law 26300 Northwestern Renewal with expansion16,000 s.f.

2014 2015 2016 2017 2018Tenant-favorable marketNeutral marketLandlord-favorable market

Active law firm requirements in the market (s.f.)

N/A

*rent difference from Class A average **averages on 10-year new/renewal transactions

Pricing and incentives (assuming a 10-year lease)

TI allowance ($ p.s.f.)** Free rent (months)**$40.00/$20.00 10/10

Net rent

$12.05Taxes

$3.00Operating expenses

$7.00Annual escalation

2.5%

5.0% 10.0% 4.0%

Premium for Trophy space*

Discount for negotiated rent*

Discount for sublease space*

Number of law firms occupying> 50,000 square feet in the market

15

Rec

ent l

aw-fi

rm-c

ompl

eted

tran

sact

ions

Percent of market occupied by law firms

4%

Fairfield County

23JLL | United States | Law Firm Perspective | 2014

Outlook

Challenges for law firms• Continued leasing of UBS sublease space has driven net absorption of

200,000 square feet, reducing vacancy.• While transit center assets attract more tenant interest and broaden the

talent pool, this space commands a 20.0 percent rental premium.

Opportunities for law firms

• Many firms are downsizing and moving to New York City to be closer to the Millennial associate talent pool.

• Transportation options offer accessibility to New York City, but space remains at discounted rates.

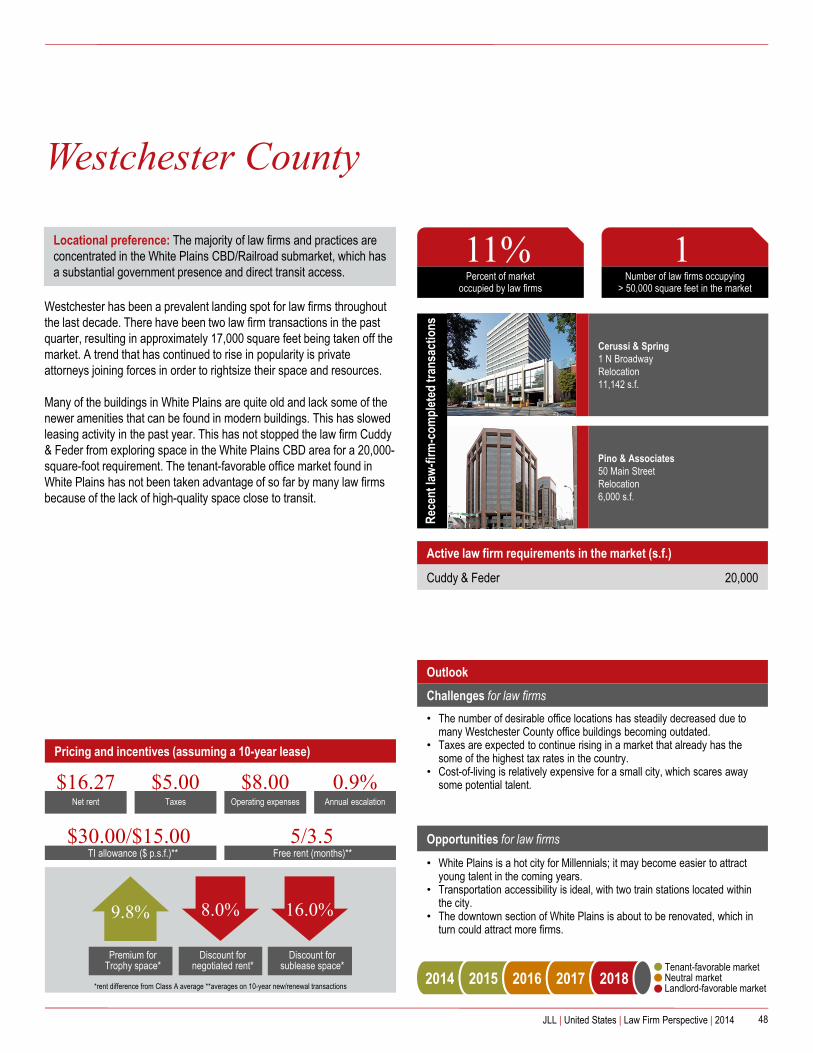

There has not been any law firm activity since the start of 2014 in the Stamford CBD. When rents bottomed back in 2011 and 2012, many law firms exercised early extension and renewal options, which has resulted in a dearth of activity related to near-term lease expirations. That said, law firms that have recently taken space and those that are currently in the market have been leaning toward relocations rather than renewals. Right now there are three major law firms looking for space in Stamford CBD, which is an encouraging sign for a stabling economy. The competition for space is limited, so asking rents have remained relatively low for Stamford CBD.

n/a

2014 2015 2016 2017 2018Tenant-favorable marketNeutral marketLandlord-favorable market

Active law firm requirements in the market (s.f.)

Kelly Drye 35,000

Finn Dixon 30,000

Murtha Cullina 20,000

*rent difference from Class A average **averages on 10-year new/renewal transactions

Pricing and incentives (assuming a 10-year lease)

TI allowance ($ p.s.f.)** Free rent (months)**$35.00/$25.00 6/6

Net rent

$32.31Taxes

$5.00Operating expenses

$10.00Annual escalation

1.0%

9.5% 7.8% 18.0%

Premium for Trophy space*

Discount for negotiated rent*

Discount for sublease space*

Number of law firms occupying> 50,000 square feet in the market

1Locational preference: The majority of law firms and practices are concentrated in the Stamford CBD/Railroad submarket, which has direct access to transit. Firms also dot the periphery of the CBD/Railroad in Stamford's other submarkets that are slightly farther from the transit hub, and offer more competitive pricing. The Greenwich CBD/Railroad is also a desired location for law firms as well, but space is priced at a premium.

Rec

ent l

aw-fi

rm-c

ompl

eted

tran

sact

ions

Percent of market occupied by law firms

32%

Fort Lauderdale

24JLL | United States | Law Firm Perspective | 2014

Outlook

Challenges for law firms• Larger law firms are finding limited options for high-quality space, as

only three Class A properties can accommodate full-floor users with desirable views.

• Rapid rent growth over the previous year, particularly along Las OlasBoulevard, has reversed the flight to quality trend seen in the wake of the recession.

• The lack of planned or proposed multitenant office construction in the CBD will accelerate rent growth.

Opportunities for law firms

• With limited space, more large law firms may look for built-to-suit opportunities to save costs, similar to the strategy used by Kopelowitz Law this year.

• As the market transitions to a landlord-favorable one, smaller law firms with less need for proximity to the courthouses may look to quality suburban space to lower overhead.

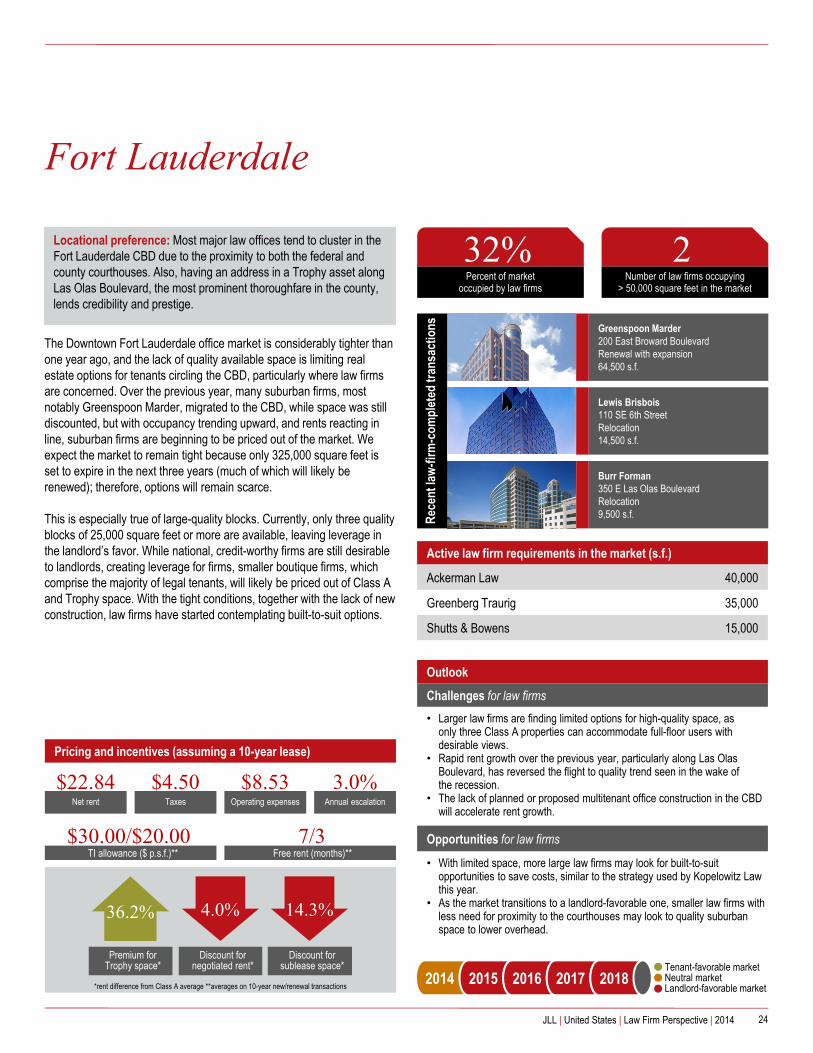

The Downtown Fort Lauderdale office market is considerably tighter than one year ago, and the lack of quality available space is limiting real estate options for tenants circling the CBD, particularly where law firms are concerned. Over the previous year, many suburban firms, most notably Greenspoon Marder, migrated to the CBD, while space was still discounted, but with occupancy trending upward, and rents reacting in line, suburban firms are beginning to be priced out of the market. We expect the market to remain tight because only 325,000 square feet is set to expire in the next three years (much of which will likely be renewed); therefore, options will remain scarce.

This is especially true of large-quality blocks. Currently, only three quality blocks of 25,000 square feet or more are available, leaving leverage in the landlord’s favor. While national, credit-worthy firms are still desirable to landlords, creating leverage for firms, smaller boutique firms, which comprise the majority of legal tenants, will likely be priced out of Class A and Trophy space. With the tight conditions, together with the lack of new construction, law firms have started contemplating built-to-suit options.

Greenspoon Marder200 East Broward BoulevardRenewal with expansion64,500 s.f.

Burr Forman350 E Las Olas BoulevardRelocation9,500 s.f.

Lewis Brisbois110 SE 6th StreetRelocation14,500 s.f.

2014 2015 2016 2017 2018Tenant-favorable marketNeutral marketLandlord-favorable market

Active law firm requirements in the market (s.f.)

Ackerman Law 40,000

Greenberg Traurig 35,000

Shutts & Bowens 15,000

*rent difference from Class A average **averages on 10-year new/renewal transactions

Pricing and incentives (assuming a 10-year lease)

TI allowance ($ p.s.f.)** Free rent (months)**$30.00/$20.00 7/3

Net rent

$22.84Taxes

$4.50Operating expenses

$8.53Annual escalation

3.0%

36.2% 4.0% 14.3%

Premium for Trophy space*

Discount for negotiated rent*

Discount for sublease space*

Number of law firms occupying> 50,000 square feet in the market

2Locational preference: Most major law offices tend to cluster in the Fort Lauderdale CBD due to the proximity to both the federal and county courthouses. Also, having an address in a Trophy asset along Las Olas Boulevard, the most prominent thoroughfare in the county, lends credibility and prestige.

Rec

ent l

aw-fi

rm-c

ompl

eted

tran

sact

ions

Percent of market occupied by law firms

6%

Houston

25JLL | United States | Law Firm Perspective | 2014

Outlook

Challenges for law firms• CBD Class A vacancy is very low and currently rests in the single digits, so

options are very limited.• The overall market is still very much landlord favorable, with rental rates on

the rise and minimal concessions.• Law firms must be, at the earliest, the second tenant into a new

development due to credit status.

Opportunities for law firms

• Large blocks of space will become available in CBD and the Galleria, with new and proposed developments coming online over the next few years.

• New office product could force the market toward neutrality over the next few years.

As 2014 progresses, Houston’s economy and office market benefit from energy’s overall economic growth as well as a STEM-based job uptick. The result of this economic and employment strength is a tightening office market, with peak rental rates especially within the CBD, Galleria, and Greenway submarkets.

The above-mentioned Inner Loop areas serve as homes for the majority of Houston’s major law firms. With vacancy rates in all three areas hovering around single-digits, law firms looking to renew or enter these submarkets remain focused on gaining efficiencies in their layout and maximizing their available space. While new Trophy and Class A buildings such as 609 Main, 6 Houston Center and 1885 St. James are currently under way and could offer law firms the efficiencies they desire, these new buildings (and additional spec buildings poised to being construction) in the Houston market will arrive with effective rents poised to be substantially higher than existing Class A space.

With large blocks of existing Trophy and Class A space in these areas at a premium, the submarkets are expected to remain landlord favorable in nature in the near term. With concessions being tight and rental rates continuing to rise, law firms in the Houston market must continue a balancing act in terms of space, location, and rates when contemplating their lease needs.

Gardere1000 Louisiana StreetRenewal with expansion75,000 s.f.

Arnold & Porter700 Louisiana StreetNew to market30,000 s.f.

Akin Gump1111 Louisiana StreetRenewal69,000 s.f.

2014 2015 2016 2017 2018Tenant-favorable marketNeutral marketLandlord-favorable market

Active law firm requirements in the market (s.f.)

Bracewell & Giuliani 200,000

Coats Rose 45,000

Skadden 20,000

*rent difference from Class A average **averages on 10-year new/renewal transactions

Pricing and incentives (assuming a 10-year lease)

TI allowance ($ p.s.f.)** Free rent (months)**$55.00/$35.00 4/2

Net rent

$24.97Taxes

$4.50Operating expenses

$12.75Annual escalation

3.0%

5.0% 0.0% 20.0%

Premium for Trophy space*

Discount for negotiated rent*

Discount for sublease space*

Number of law firms occupying> 50,000 square feet in the market

27Locational preference: Firms are found mostly in the CBD submarket. They are concentrated in Class A buildings with some of the most expensive rental rates in the city. Because of the lack of vacancy downtown, if national law firms were to move, they would consider moving to Midtown and the Galleria submarkets into new and proposed buildings.

Rec

ent l

aw-fi

rm-c

ompl

eted

tran

sact

ions

Percent of market occupied by law firms

13%

Indianapolis

26JLL | United States | Law Firm Perspective | 2014

Outlook

Challenges for law firms• The Class A and Trophy buildings are subject to branding competition, as

there are several law firms within the same building. • Rents are rising and forecasted to rise ahead.

Opportunities for law firms

• Employment growth in office-using sectors and a stronger economy will allow for the formation of new practice groups.

• Improvements in amenities such as new parking garages, redevelopment projects and new modes of transportation in the CBD submarket will offer firms a new lifestyle downtown.

Leasing activity for the largest Indianapolis law firms slowed as expected in 2014 as large firms such as Ice Miller and Bingham Greenebaum Doll had already signed their leases in the past two years for a total of 206,000 square feet in the Class A CBD locations of One American Tower and Market Tower, respectively. The combination of these large leases and no new construction places the CBD with a limited supply of available blocks of space.

Indianapolis’ law firm industry has historically been dominated by firms practicing state and county government in addition to real estate law. However, this is starting to change with the growth of high-tech companies, as local firms are placing a greater emphasis on intellectual property rights. Looking ahead, Indianapolis’ CBD will continue to be attractive to legal tenants due to area amenities, such as high walkability indexes to retail, entertainment and convenient housing options.

Quarles & Brady135 N Pennsylvania StreetRelocation19,000 s.f.

Alerding Castor47 S Pennsylvania StreetRelocation7,000 s.f.

Brannon Sowers & Cracraft1 N Pennsylvania StreetRelocation7,000 s.f.

2014 2015 2016 2017 2018Tenant-favorable marketNeutral marketLandlord-favorable market

Active law firm requirements in the market (s.f.)

Hall Render 65,000

Woodhard, Emhart, Moriarty, McNett & Henry 30,000

Wooden & McLaughlin 20,000

*rent difference from Class A average **averages on 10-year new/renewal transactions

Pricing and incentives (assuming a 10-year lease)

TI allowance ($ p.s.f.)** Free rent (months)**$35.00/$18.00 10/6

Net rent

$12.25Taxes

$4.25Operating expenses

$6.50Annual escalation

3.0%

20.0% 5.0% 40.0%

Premium for Trophy space*

Discount for negotiated rent*

Discount for sublease space*

Number of law firms occupying> 50,000 square feet in the market

8Locational preference: Indianapolis' law firms are primarily located in the CBD, with proximity to the Capitol, higher-quality amenities, and walkability being a huge draw to the area. However, there are some regional firms located in the Keystone submarket north of the CBD.

Rec

ent l

aw-fi

rm-c

ompl

eted

tran

sact

ions

Percent of market occupied by law firms

5%

Long Island

27JLL | United States | Law Firm Perspective | 2014

Outlook

Challenges for law firms• Blocks of Trophy and Class A assets are declining, causing rental

rate increases. • Demand from other industries, including healthcare and financial services,

will further decrease Class A availabilities.• The lack of new development creates consistent demand for new

construction with a rental premium.

Opportunities for law firms

• There is quality Class B space in Central Nassau, creating leverage for cost-conscious firms.

• Central Nassau offers value in comparison to New York City, especially for firms looking to in-source non-revenue functions.

Employment in legal services in Nassau County grew 5.0 percent year-over-year in 2013. Nassau County legal services employment reached 12,337 in December 2013, the highest since 2007, according to the Department of Labor. General practice law firms are growing in Central Nassau, and seeking to expand health care and real estate practices.

In Central Nassau, large blocks of Class A space are decreasing, thus more than half of law firm leases signed in the past year were renewals. In Central Nassau, specifically Garden City, firms are expanding and acquiring smaller practices. In Garden City, firms expanded by approximately 25.0 percent in the past year. Firms, meanwhile, are also renewing leases at Trophy RXR Plaza in Uniondale at a premium to comparable spaces in Central Nassau.

Moritt Hock & Hamroff400 Garden City PlazaRenewal with expansion25,600 s.f.

Bond, Schoenick & King 1010 Franklin AvenueRelocaton14,000 s.f.

Goldberg Segalla200 Garden City PlazaRelocation20,233 s.f.

2014 2015 2016 2017 2018Tenant-favorable marketNeutral marketLandlord-favorable market

Active law firm requirements in the market (s.f.)

Stein Wiener & Roth 10,000

Edelman, Krasin & Jaye 10,000

*rent difference from Class A average **averages on 10-year new/renewal transactions

Pricing and incentives (assuming a 10-year lease)

TI allowance ($ p.s.f.)** Free rent (months)**$25.33 5.6

Net rent

$15.00Taxes

$7.28Operating expenses

$8.84Annual escalation

3.0%

6.0% 10.0% 15.0%

Premium for Trophy space*

Discount for negotiated rent*

Discount for sublease space*

Number of law firms occupying> 50,000 square feet in the market

2Locational preference: Firms in Central Nassau are clustered on Franklin Avenue in Garden City, which is in close proximity to major highways, transit and the county seat. Firms are also located at Trophy buildings in Uniondale that command a premium to comparable spaces in Central Nassau. Limited new development may shift law firms to adjacent Jericho in Eastern Nassau.

Rec

ent l

aw-fi

rm-c

ompl

eted

tran

sact

ions

Locational preference: Los Angeles firms are concentrated in the Downtown CBD near the courthouses. Specialized practice groups, generally catering to media and entertainment companies, are located close to their clients on the Westside in Century City. Ahead, some firm tenants electing to be closer to tech and entertainment clients will migrate to more non-traditional low-rises in Santa Monica and Playa Vista.

Percent of market occupied by law firms

14%

Los Angeles

28JLL | United States | Law Firm Perspective | 2014

Outlook

Challenges for law firms• A diminishing number of Los Angeles-headquartered companies is

impacting demand for corporate litigation services.• There is reduced ownership competition as Downtown's top three landlords

control 58.0 percent of Class A availability.• There is identifying Downtown options with more efficient floor plates, given

a lack of new product.

Opportunities for law firms

• There are numerous options for tenants seeking large blocks of space in Class A Downtown assets.

• Delivery of the Wilshire Grand will offer a generational opportunity to be in a new Downtown Trophy asset with building-top signage rights.

• Return of construction on the Westside offers firms the opportunity to refresh their image with build-to-suit space.

The ongoing trend of corporate headquarters relocations from Southern California continues to negatively impact the growth of the law firm sector in Los Angeles. Nevertheless, the growing number of technology start-ups on the Westside, some of which will eventually become acquisition targets or pursue IPO strategies, will create additional demand for legal services. The growing interplay between technology and the entertainment industry is expected to boost practices specializing in digital rights management (DRM). Practice groups focused on international law will also see increased demand for services driven by Los Angeles’s growing linkage to Asia, thanks to expanded capital activity here. Downtown’s close proximity to the federal and state courts will continue to make the submarket a vital location for law firms specializing in complex litigation, although rightsizing has negatively impacted the vacancy levels in the CBD market.

In reviewing transaction trends of Los Angeles law firms, the average tenant occupies approximately 14,000 square feet and signs a 12-year deal. Within the next three years, 62.0 percent of LA law firm leases will expire, which will provide a potential shake-up in occupancy across law-firm-weighted markets. Although a majority of these tenants are anticipated to sign renewals (as recent trends would tend to indicate), some firms will commit the out-of-pocket capital costs necessary to relocate and move into more efficient facilities. With modest economic growth forecasted over the next few years, the Los Angeles office market is expected to turn landlord favorable in 2015, which may further drive firms to renew in place rather than opt for a costly relocation.

Hinshaw & Culbertson11601 Wilshire BoulevardRenewal20,060 s.f.

Dechert633 W 5th StreetRenewal17,094 s.f.

Anderson McPharlin707 Wilshire BoulevardRelocation18,525 s.f.

2014 2015 2016 2017 2018Tenant-favorable marketNeutral marketLandlord-favorable market

Active law firm requirements in the market (s.f.)

Munger & Tolles 160,000

Irell & Manella 100,000

O'Melveny 50,000

*rent difference from Class A average **averages on 10-year new/renewal transactions

Pricing and incentives (assuming a 10-year lease)

TI allowance ($ p.s.f.)** Free rent (months)**$70.00/$35.00 10/8

Net rent

$21.49Taxes

$3.00Operating expenses

$13.64Annual escalation

4.0%

5.2% 20.3% 30.0%

Premium for Trophy space*

Discount for negotiated rent*

Discount for sublease space*

Number of law firms occupying> 50,000 square feet in the market

36

Rec

ent l

aw-fi

rm-c

ompl

eted

tran

sact

ions

Percent of market occupied by law firms

17%

Miami

29JLL | United States | Law Firm Perspective | 2014

Outlook

Challenges for law firms• Contiguous Trophy space with prime views remains extremely limited.• Space properly designed to accommodate new workplace standards is in

demand, but lacking in availability.• Concessions are on the decline for both new deals and renewals.

Opportunities for law firms

• New construction is underway at Brickell City Centre.• New assets and upgrades from existing product offer greater efficiencies,

upgraded finishes and increased amenities.

Upholding its standing among the most prolific office users, CBD law firms led all industry sectors in leasing. Totaling 346,000 square feet, transactions involving law firms accounted for 41.0 percent of all CBD deals. These were among the largest occupiers, with two-thirds of this activity consisting of leases in excess of 20,000 square feet. Half of the top 10 transactions were executed by top-performing national AmLaw 100 and 200 firms. Miami’s top two active requirements, Ackerman Senterfitt and Hughes Hubbard, also rank among the same national giants.

CBD market conditions follow Miami’s overall fundamentals: declining vacancy with marginal sublets available thanks to new occupancy gains and leasing activity. This coincides with lower unemployment and higher job gains. Miami led all major U.S. markets with more than 20,000 people employed in legal services, growing 3.7 percent over the last 12 months, employing 22,500 people.

A challenge facing both tenants and landlords is that the leasing of premier CBD spaces has left relatively fewer options for high, full-floor offices with commanding, unobstructed views. Enticing tenants to less-attractive, view-challenged spaces is at the forefront of creative marketing efforts for Trophy landlords.

Shutts & Bowen200 S Biscayne BoulevardRelocation69,155 s.f.

GrayRobinson333 Avenue of the AmericasRelocation35,400 s.f.

White & Case200 S Biscayne BoulevardRenewal with contraction58,400 s.f.

2014 2015 2016 2017 2018Tenant-favorable marketNeutral marketLandlord-favorable market

Active law firm requirements in the market (s.f.)

Akerman Senterfitt 120,000

Hughes Hubbard 25,000

Broad and Cassel 20,000

*rent difference from Class A average **averages on 10-year new/renewal transactions

Pricing and incentives (assuming a 10-year lease)

TI allowance ($ p.s.f.)** Free rent (months)**$50.00/$50.00 5/5

Net rent

$22.23Taxes

$3.23Operating expenses

$15.63Annual escalation

3.0%

13.0% 5.1% 28.0%

Premium for Trophy space*

Discount for negotiated rent*

Discount for sublease space*

Number of law firms occupying> 50,000 square feet in the market

8Locational preference: Miami’s CBD is comprised of two submarkets, Brickell and Downtown. The vast majority of firms occupy space within the Downtown sector of the urban core.

Rec

ent l

aw-fi

rm-c

ompl

eted

tran

sact

ions

Locational preference: The Twin Cities' major firms are concentrated in the Minneapolis CBD, including the majority of firms occupying 50,000 square feet or more of. The CBD is home to the Hennepin County courthouse and is the business epicenter of the Twin Cities.

Percent of market occupied by law firms

11%

Minneapolis

30JLL | United States | Law Firm Perspective | 2014

Outlook

Challenges for law firms• Landlords continue to press on rents in high-profile Trophy properties.• Fit-out costs are increasing.

Opportunities for law firms

• A retreat to value, build-to-suits and rightsizing by some downtown tenants has resulted in an increase in large available Trophy blocks.

• Mid-tier Class A and Class B buildings with lower asking rates and some larger availabilities provide additional options for value-driven users.

• A decline in active requirements in the Minneapolis CBD reduces competition for space.

Leasing activity among law firms has been quite strong over the past year, with more than 650,000 square feet of lease transactions executed in the Minneapolis CBD. Current active requirements for law firms have been reduced considerably as a result, and while some sizeable requirements do remain, a decline in active office requirements for tenants across all industry types, not just legal tenants, is reducing the competition for space in the Minneapolis CBD. This is especially true when factoring in the increase of large available Class A blocks resulting from build-to-suit activity, rightsizing, and relocations by value-driven tenants to lower-cost options. Opportunities for large tenants remain more limited, however, in upper floors and in properties in close proximity to Nicollet Mall.

The local legal community has experienced significant merger and consolidation activity in the past few years as law firms look to fill gaps in practice areas, increase efficiencies and expand into new markets with strong economies and business opportunities. One of the more unique examples of consolidation is Boston-based Fish & Richardson’s recent decision to create a centralized, administrative hub in its Minneapolis office. Relatively affordable rents, a talented workforce and a high quality of life were factors in the decision to concentrate 80 positions to Minneapolis from multiple offices throughout the country.

Dorsey & Whitney50 S 6th StreetRenewal with contraction250,000 s.f.

Briggs & Morgan80 S 8th StreetRenewal with contraction116,827 s.f.

Robins, Kaplan, Miller & Ciresi800 LaSalle AvenueRenewal with contraction159,000 s.f.

2014 2015 2016 2017 2018Tenant-favorable marketNeutral marketLandlord-favorable market

Active law firm requirements in the market (s.f.)

Leonard, Street & Deinard 150,000

Lindquist & Vennum 100,000

Winthrop & Weinstine 90,000

*rent difference from Class A average **averages on 10-year new/renewal transactions

Pricing and incentives (assuming a 10-year lease)

TI allowance ($ p.s.f.)** Free rent (months)**$48.00/$27.00 7/4

Net rent

$17.24Taxes

$5.15Operating expenses

$7.59Annual escalation

2.0%

7.8% 10.0% 37.4%

Premium for Trophy space*

Discount for negotiated rent*

Discount for sublease space*

Number of law firms occupying> 50,000 square feet in the market

16

Rec

ent l

aw-fi

rm-c

ompl

eted

tran

sact

ions

Locational preference: The majority of firms in Manhattan are located in Grand Central and the Plaza District, where Grand Central Terminal and the Metro North Railroad are easily accessible. In an effort to find more efficient, lower-priced space, firms are relocating westward within Midtown to new construction and Downtown where pricing for Class A space is on par with Class B space in Midtown.

Percent of market occupied by law firms

11%

New York

31JLL | United States | Law Firm Perspective | 2014

Outlook

Challenges for law firms• Most new construction in Midtown will not be delivered until 2018 or later,

significantly limiting the supply of new, efficient space available to firms.• Landlords are beginning to push back, lowering concessions and

increasing rents as supply tightens.• If firms want new construction, they will have to move westward or

Downtown; the delay of the proposed Midtown East rezoning pushes off any new construction in the Grand Central corridor for the foreseeable future.

Opportunities for law firms

• Geographically diverse workforce opens opportunity for relocation outside traditional submarkets.

• Newer, lower-priced space on the west side and Downtown provide opportunities to reduce real estate footprints and costs.

• The Vanderbilt corridor rezoning provides the opportunity for new construction near Grand Central, including the proposed One Vanderbilt.

Leasing activity among major law firms year-to-date has resulted in three committing to a lease greater than 100,000 square feet, two relocations and one renewal—compared with four renewals larger than 100,000 square feet at this time last year. During the second quarter, White & Case signed the largest lease year-to-date, a 440,000-square-foot relocation four blocks north to 1221 Avenue of the Americas from 1155 Avenue of the Americas.