laws of kenya the income tax act chapter 470 470 - income tax act 2016... · laws of kenya the...

TRANSCRIPT

LLAAWWSS OOFF KKEENNYYAA

TTHHEE IINNCCOOMMEE TTAAXX AACCTT

CCHHAAPPTTEERR 447700

Note: This edition contains amendments to TheFinance Act 2016 dated 20 September2016

Disclaimer

While all reasonable care has been taken in the preparation andupdating of this Act, Ernst & Young LLP (EY), accepts noresponsibility for any errors it may contain, whether caused bynegligence or otherwise, or for any loss, however caused, orsustained by any person that relies on it.

CHAPTER 470 – THE INCOME TAX ACT ...................................................................................1

PART 1 – PRELIMINARY ................................................................................................................ 1

Section ......................................................................................................................................... 11. Short title and commencement 12. Interpretation 1

PART II – IMPOSITION OF INCOME TAX ....................................................................................... 143. Charge of tax 144. Income from businesses 154A Income from business where foreign exchange gain or loss is realized 164B Export processing zone enterprise 185. Income from employment, etc 186. Income from the use of property 286A. Imposition of residential rental Income Tax. 287. Income from dividends 287A Dividend Tax Account 298. Income from pensions, etc 319. Income of certain non resident persons deemed derived from Kenya 3510. Income from management or professional fees, royalties, interest and rents 3511. Trust income, etc., deemed income of trustee beneficiary, etc. 3712. Imposition of instalment tax 3812A Imposition of advance tax 3812B Imposition of fringe benefit tax 3912C Imposition of turnover tax 40

PART III – EXEMPTION FROM TAX ............................................................................................... 4113. Certain income exempt from tax, etc. 4114. Income on Government loans, etc., exempt from tax 41

PART IV – ASCERTAINMENT OF TOTAL INCOME ......................................................................... 4215. Deduction allowed 4216. Deduction not allowed 5117. Ascertainment of income of farmers in relation to stock 5417A Presumptive income on tax from certain farm produce 5618. Ascertainment of gains or profits of business in relation to certain non-resident persons. 5719. Ascertainment of income of insurance companies 5919A Co-operative societies 6320. Collective Investment Schemes 6521. Members’ clubs and trade associations 6522. Purchased annuities other than retirement annuities, etc. 6622A Deductions in respect of contributions to registered pension or provident funds 6822B Deductions in respect of registered individual retirement fund 7122C Registered home ownership savings plan 72

______

iii iii

23. Transactions designed to avoid liability of tax 7324. Avoidance of tax liability by non-distribution of dividends 7425. Income settled on children 7526. Income from certain settlements deemed to be income of settler 7827. Accounting periods not coinciding with year of income etc. 8028. Income and expenditure after cessation of business 81

PART V - PERSONAL RELIEF ...................................................................................................... 8229. General 8230. Personal relief 8331. Insurance relief 8332. Special single relief (repealed) 8433. Insurance relief (repealed) 84

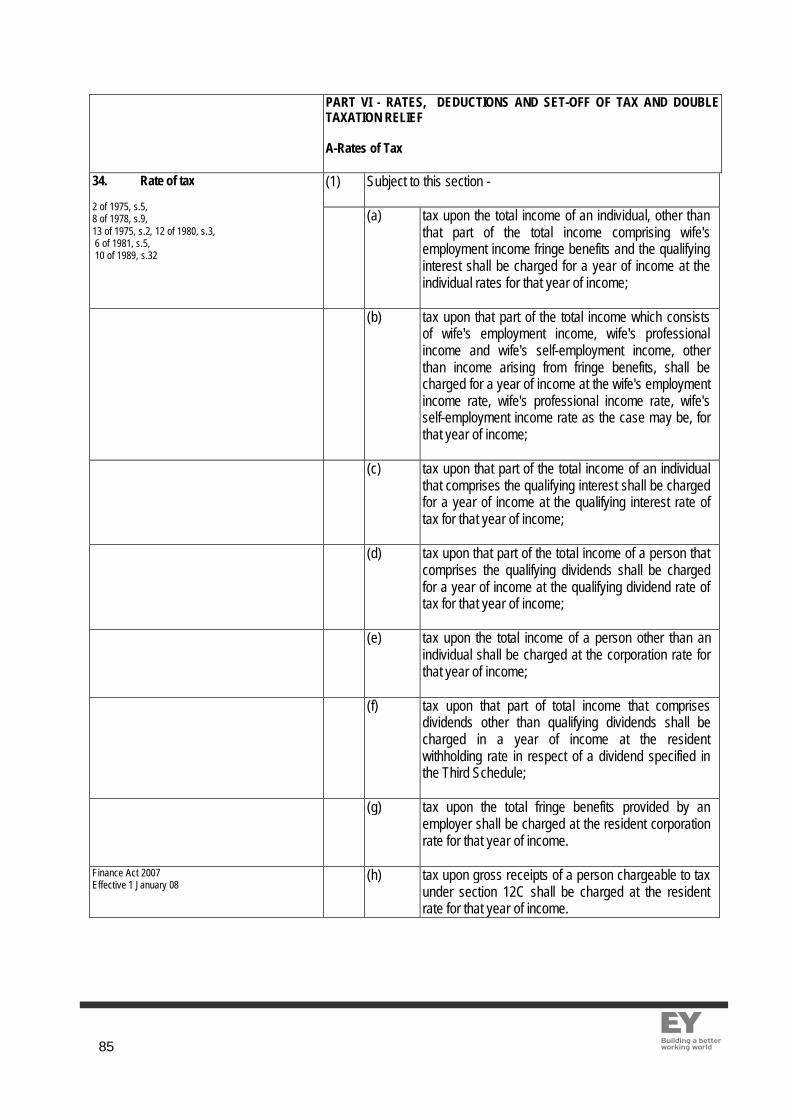

PART VI - RATES, DEDUCTIONS AND SET-OFF OF TAX AND DOUBLE TAXATION RELIEF............ 85

A-Rates of Tax ............................................................................................................................ 8534. Rate of tax 8534A Deduction in respect of certain rates of tax (Repealed) 88

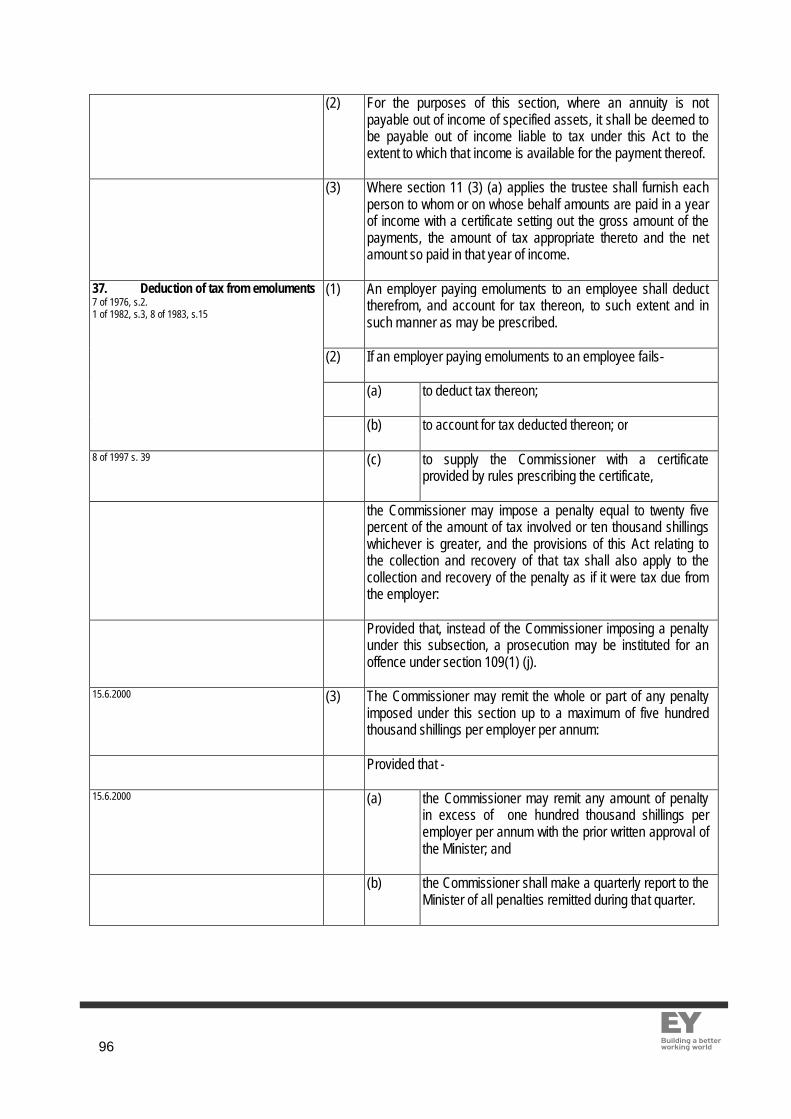

B-Deduction of Tax...................................................................................................................... 8835. Deduction of tax from certain income 8836. Deduction of tax from annuities etc paid under a will, etc. 9537. Deduction of tax from emoluments 9637A Penalty for failure to make deductions under section 35, 36 and 37 9838. Application to Government 98

C-set-off of Tax ........................................................................................................................... 9839. Set-off tax 9839A Set-off of import duty 99Cap 472 9939B Set-off tax rebate for apprenticeships 99

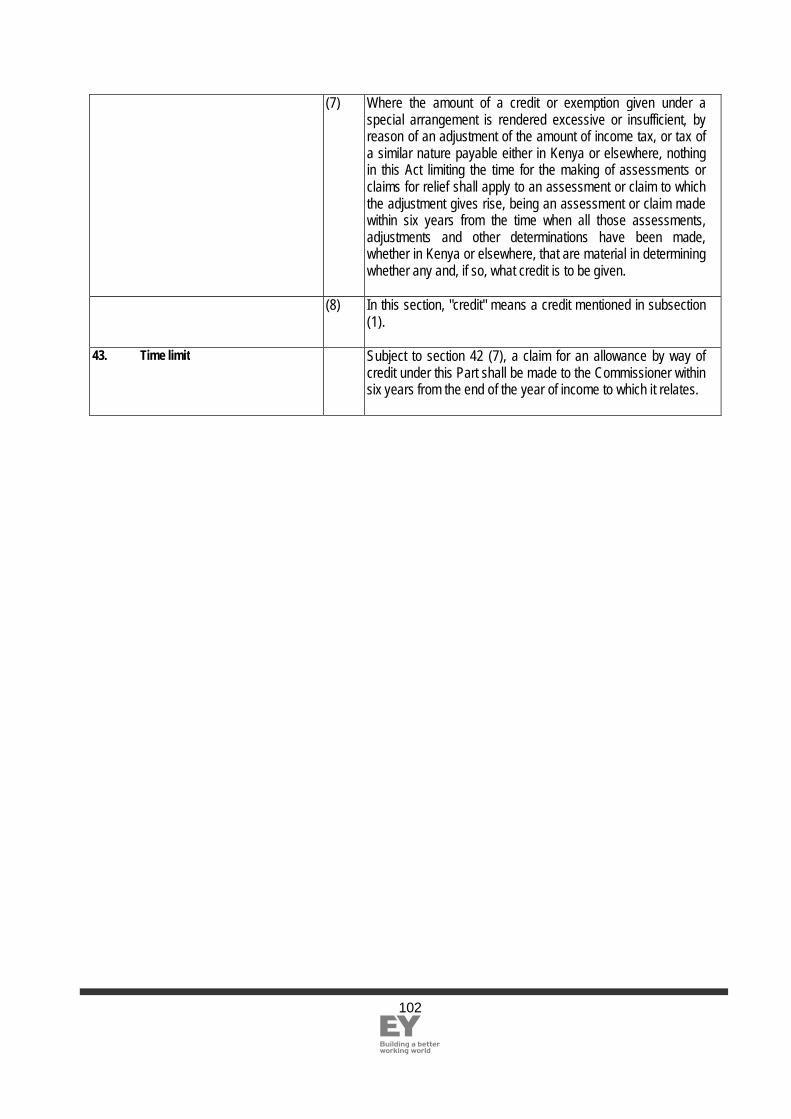

D-Double Taxation Relief ............................................................................................................. 9940. Relief in respect of inter-state tax (repealed) 9941. Special arrangements for relief from double taxation 9941A. Agreements for exchange of information 10042. Computation of Credits under special arrangement 10043. Time limit 102

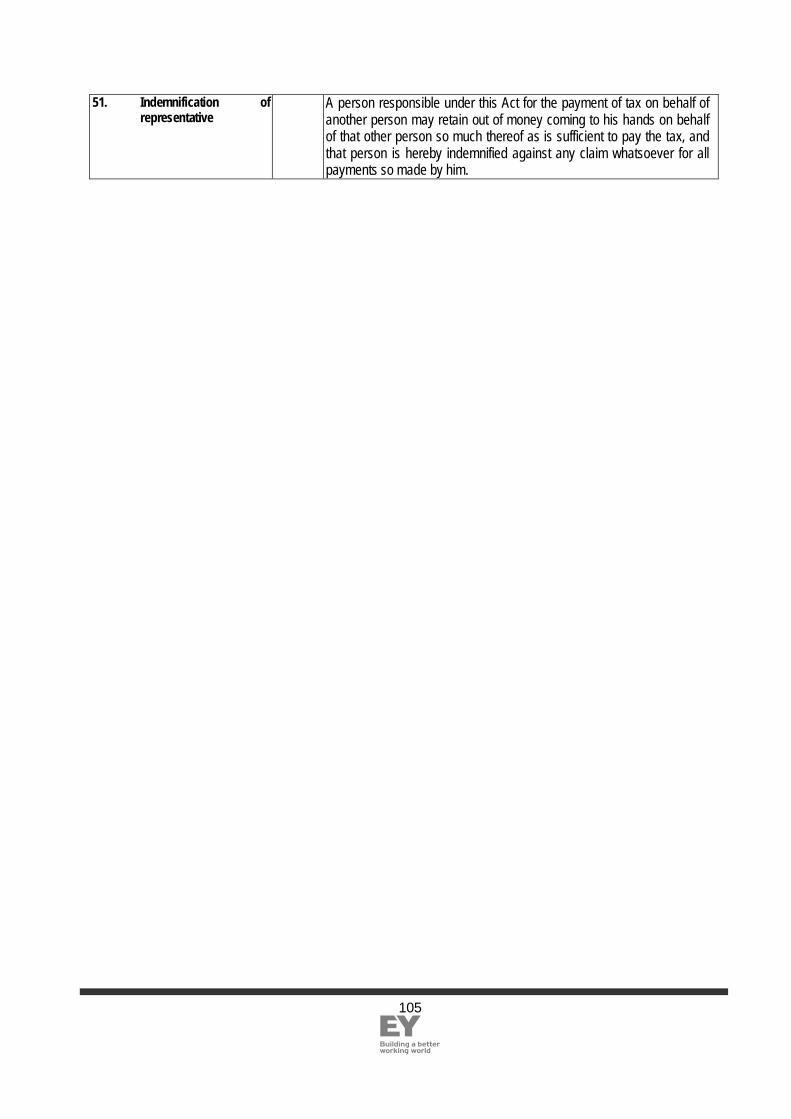

PART VII - PERSONS ASSESSABLE ........................................................................................... 10344. Income of a person assessed on him 10345. Wife’s income, etc 10346. Income of incapacitated person 10347. Income of non-resident person 10448. Income of deceased person etc. 10449. Liability of joint trustees 10450. Liability of person in whose name income of another person is assessed 10451. Indemnification of representative 105

______

iv iv

PART VIII - RETURNS AND NOTICES ......................................................................................... 10651A. Returns, records, etc to be in official languages 10652. Returns of income and notice of chargeability 10652A Return of income and notice of chargeability (repealed) 10752B Final return with self assessment 10753. Provisional returns 10854. Documents to be included in return of income 11054A Keeping of records of receipts, expenses, etc 11254B Supply of information upon change in particulars 11255. Books and accounts 11256. Production and preservation of books, attendance, etc. 11357. Returns of salaries pension, etc. 11458. Returns as to fees, commissions, royalties etc. 11459. Occupier’s return of rent 11560. Return of lodges and inmates 11561. Return of income received on account of other persons 11662. Return as to income exempt from tax 11663. Return in relation to settlements 11664. Return in relation to registered pension funds, etc. 11665. Return of annuity contract benefits 11766. Return of resident company dividends 11767. Return as to interest paid or credited by banks etc. 11768. Returns as to dividends paid by building societies. 11869. Access to official information 11870. Further returns and extension of time 11971. Return deemed to be furnished by due authority 11972. Additional tax in event of failure to furnish return or fraud in relation to a return. 11972A Offences in respect of failure to furnish return or fraud in relation to a return 12272B Penalty for the negligence of authorized tax agent 12272C Penalty on underpayment of instalment tax 12272D Penalty on unpaid tax 123

PART IX- ASSESSMENTS .......................................................................................................... 12473. Assessments 12474. Provisional assessments 12474A Instalment assessments 12574B Minimum additional tax or penalty. 12575. Assessment of person about to leave or having left Kenya 12575A Assessment in certain cases 12576. Assessment not to be made on certain employees 12576A Assessment not to be made on certain income. 12677. Additional Assessment 12678. Service of notice of assessment, etc 12679. Time limit for making assessments, etc. 12680. Assessment list 12781. Errors, etc in assessments or notices 127

PART X-OBJECTIONS, APPEALS AND RELIEF FOR MISTAKES .................................................. 129

______

v v

82. Local Committees 12983. The Tribunal 13084. Notice of objection to assessment 13185. Powers of Commissioner on receipt of objection 13286. Right of appeal from Commissioner’s determination of objection 13387. Procedure on appeal 13488. Finality of assessment 13589. Application of appeal procedure to other decisions etc, of the Commissioner 13690. Relief in respect of error or mistake. 13791. Rules for appeals to the court 13791A Appeals to court of appeal 138

PART XI – COLLECTION, RECOVERY AND REPAYMENT OF TAX ................................................ 13992. Time within which payment to be made 13992A Due date for payment of tax under self- assessment 14093. Payment of tax where notice of objection etc. 14194. Interest on unpaid tax 14295. Interest on underestimated tax 14395A Penalty in respect of instalment tax 14396. Appointment and duties of agent 14396A Preservation of funds 14597. Deceased persons 14698. Collection of tax from persons leaving or having left Kenya 14699. Exchange control income tax leaving or having left Kenya (repealed) 148100. Collection of tax from guarantor 149101. Collection of tax by suit 149102. Collection of tax by distraint 149103. Security on property for unpaid tax 150104. Collection of tax from shipowner, etc. 151105. Refund of tax overpaid 151106. Repayment of tax in respect of income accumulated under trusts 152

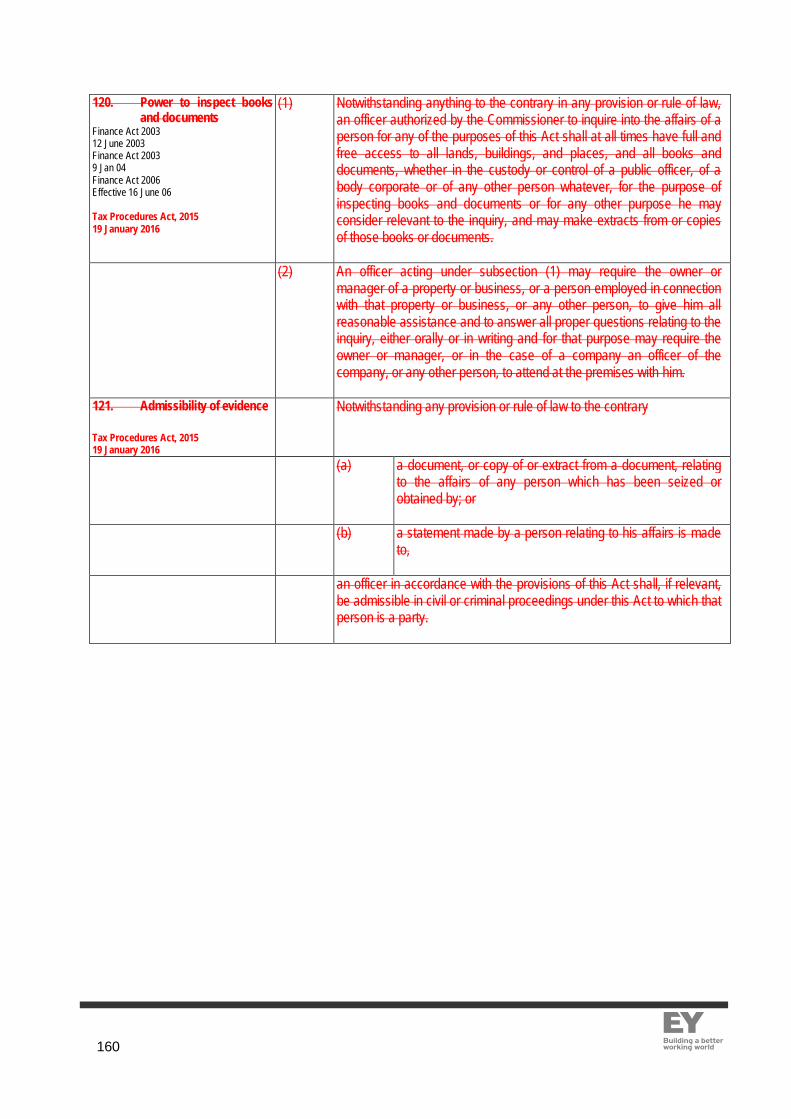

PART XII - OFFENCES AND PENALTIES ..................................................................................... 153107. General penalty 153108. Additional penalties 153109. Failure to comply with notice, etc. 153110. Incorrect returns, etc 154111. Fraudulent returns, etc. 154112. Obstruction of officer 156113. Evidence in cases of fraud, etc. 156114. Power of Commissioner to compound offences 156115. Place of trial 158116. Offences by corporate bodies 158117. Officer may appear on prosecution 158118. Tax charged to be payable notwithstanding prosecution 158119. Power to search and seize 158120. Power to inspect books and documents 160121. Admissibility of evidence 160

______

vi vi

PART XIII-ADMINISTRATION ...................................................................................................... 161122. Responsibility for administration, etc. 161123. Commissioners discretion to abandon or remit tax 161123A Amnesty for penalties and interest 161123B Commissioner to refrain from assessing tax in some cases. 162123C Commissioner to refrain from assessing or recovering tax in certain cases. 163124. Exercise of powers, etc. 163125. Official secrecy 163126. Offences by or in relation to officers, etc 165

PART XIV-MISCELLANEOUS PROVISIONS ................................................................................. 167127. Forms of notices, etc 167127A Application of information technology 167127B Users of the tax computerized system 167127C Cancellation of registration of registered user 167127D Unauthorized access to or improper use of tax computerized system 168127E Interference with tax computerized systems. 168128. Service of notices, etc. 169129. Liability of manager etc of corporate body 170130. Rules 170131. Exemption from stamp duty 170132. Personal identification numbers 170133. Repeals and transitional 171

SCHEDULES .................................................................................................................... 172

FIRST SCHEDULE - EXEMPTIONS .............................................................................................. 172PART I – Income accrued in, derived from or received in Kenya which is exempt from tax 172PART II-Securities, the interest on which is exempt from tax 179

SECOND SCHEDULE – DEDUCTIONS ........................................................................................ 181PART 1 – Deductions in respect of Capital Expenditure on certain buildings 181PART II- Deduction in respect of Capital Expenditure on Machinery 186PART III – Deductions in respect of Mining Operations 191PART IV-Deductions in respect of Capital Expenditure on Agricultural Land 194PART V-Investments Deductions 196PART VI - Miscellaneous Provisions 202

THIRD SCHEDULE – Rates of Personal Relief and Tax ................................................................ 207Head A – Resident Personal Relief 207Head B – Rates of Tax 207

FOURTH SCHEDULE - Financial Institutions ............................................................................. 216

FIFTH SCHEDULE – Scheduled Professions and Scheduled Qualifications .................................. 217

SIXTH SCHEDULE – Transitional Provisions ............................................................................... 218

______

vii vii

SEVENTH SCHEDULE ............................................................................................................... 221

EIGHTH SCHEDULE .................................................................................................................. 222

PART 1 Accrual and computation of gains from property other than investment shares transferred byindividuals ................................................................................................................................ 222PART II – Accrual and Computation of Gains from Investment Shares 229PART III –Reduction of chargeable gains in respect of property acquired 231before 1st Jan 1975, & transferred before 1st Jan 1985 231

NINTH SCHEDULE – Taxation of Petroleum Companies .............................................................. 233PART I – INTERPRETATION 233PART II – TAXATION OF PETROLEUM COMPANIES 234PART III-Taxation of Petroleum Services Subcontractors 238

NINTH SCHEDULE ..................................................................................................................... 241PART I – INTERPRETATION 241PART II – TAXATION OF MINING OPERATIONS 243PART III – PETROLEUM OPERATIONS 246PART IV — COMMON RULES APPLICABLE TO MINING AND PETROLEUM OPERATION 249

TENTH SCHEDULE - Agricultural Produce and Authorised Agents .............................................. 251

ELEVENTH SCHEDULE - Taxation of Export Processing Zone Enterprises.................................. 254

TWELFTH SCHEDULE - Provisions relating to Instalment Tax .................................................... 256

THIRTEENTH SCHEDULE – Transaction for which Personal Identification Number (PIN) will berequired .................................................................................................................................... 259

SUBSIDIARY LEGISLATION................................................................................................ 260

Declaration of Crops ................................................................................................................. 260

Specified Mineral....................................................................................................................... 260

Notices under sections 13 (2) and 14 (2) ..................................................................................... 261Notices under section 35 (7) 262Notices under section 41 263

Legal Notice No. 51 ................................................................................................................... 264

Income Tax Act – Exemptions .................................................................................................... 264

Legal Notice No. 53 – Prescribed Limit of Medical Benefit ........................................................... 264

Legal Notice No. 54– Declaration of Crops .................................................................................. 264

Legal Notice No. 82– Revocation of Exemption ........................................................................... 264

______

viii viii

Legal Notice No. 48 – Exemption: ............................................................................................... 265

Legal Notice No. 91 ................................................................................................................... 265

Legal Notice No. 165 .................................................................................................................. 265

Rules under Section 82 .............................................................................................................. 266The Income Tax (Local Committees) Rules 266

Rules under Section 83 .............................................................................................................. 270The Income Tax (Tribunal) Rules 270

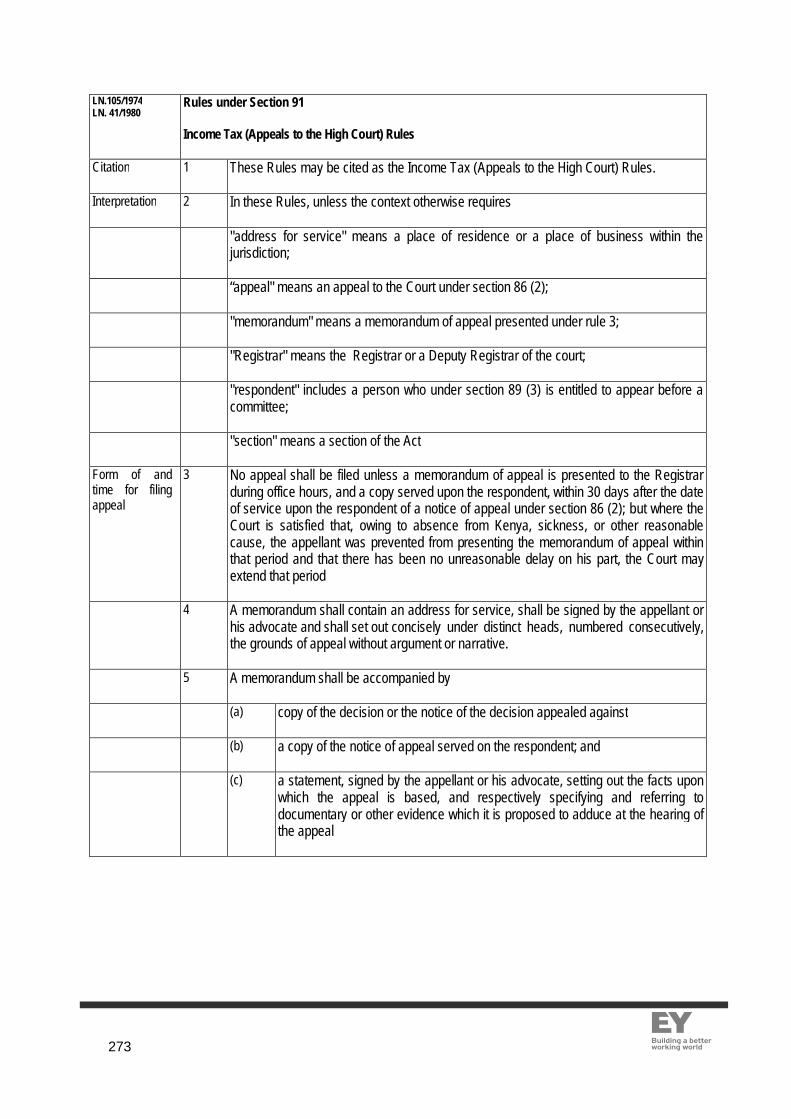

Rules under Section 91 .............................................................................................................. 273Income Tax (Appeals to the High Court) Rules 273

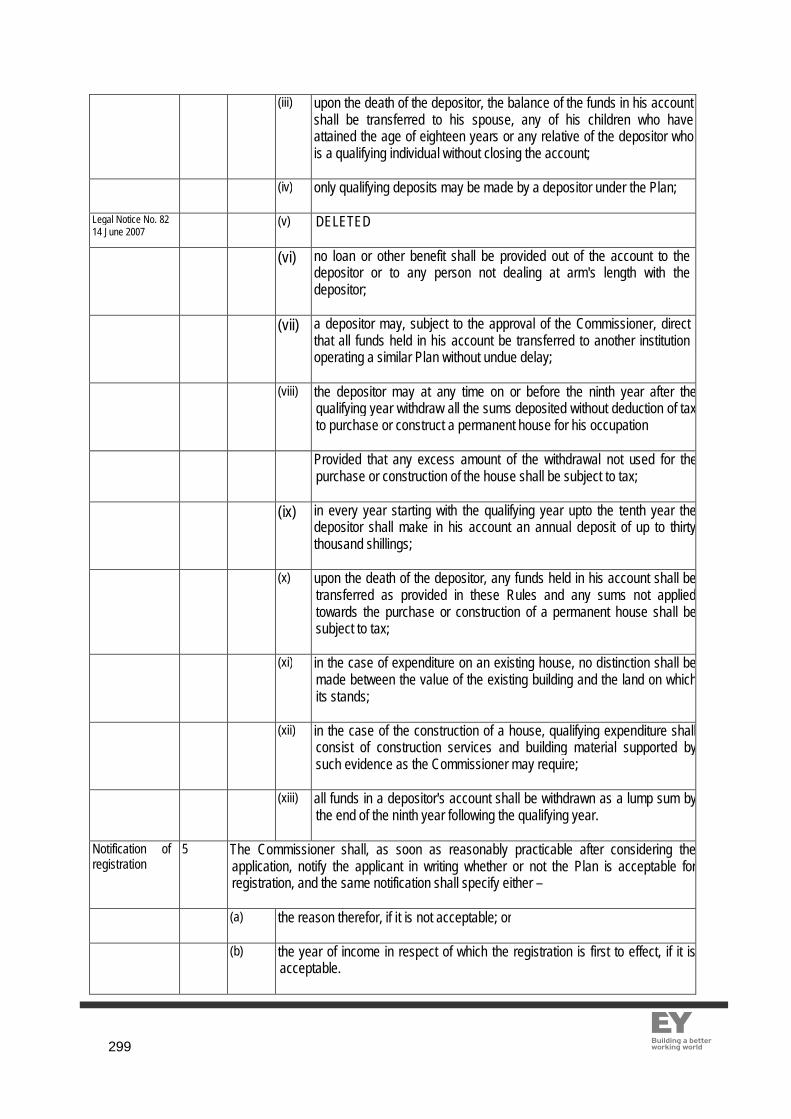

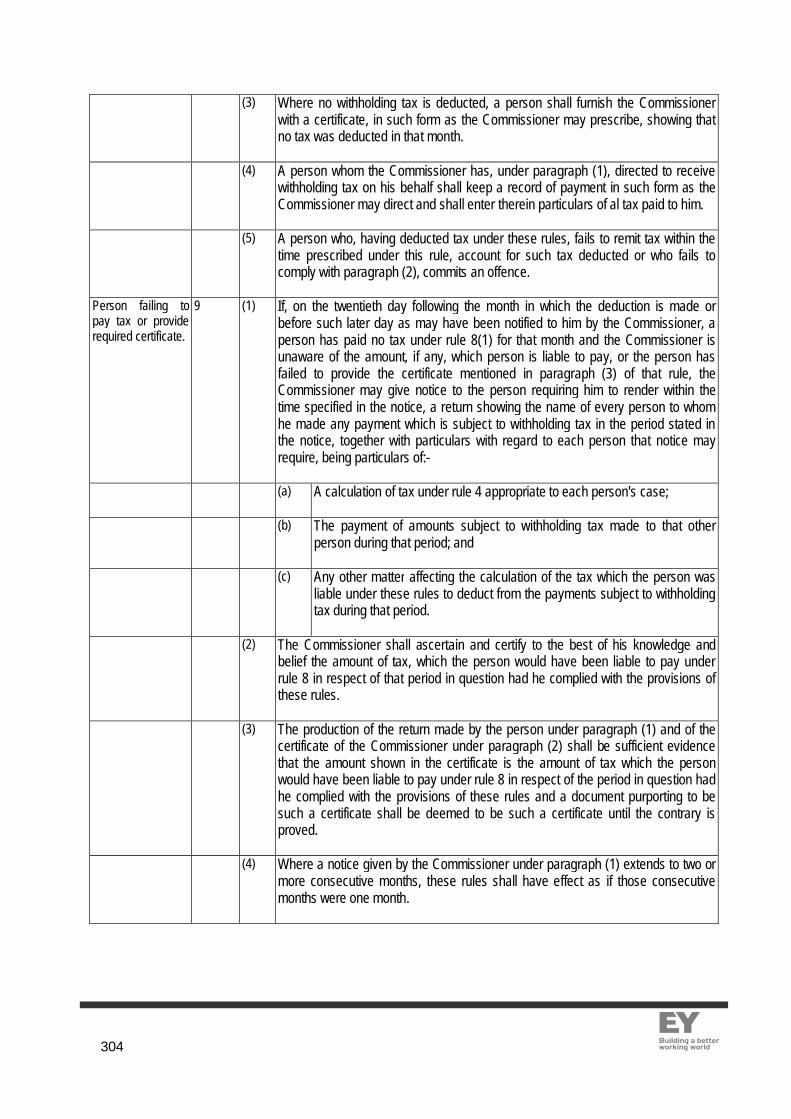

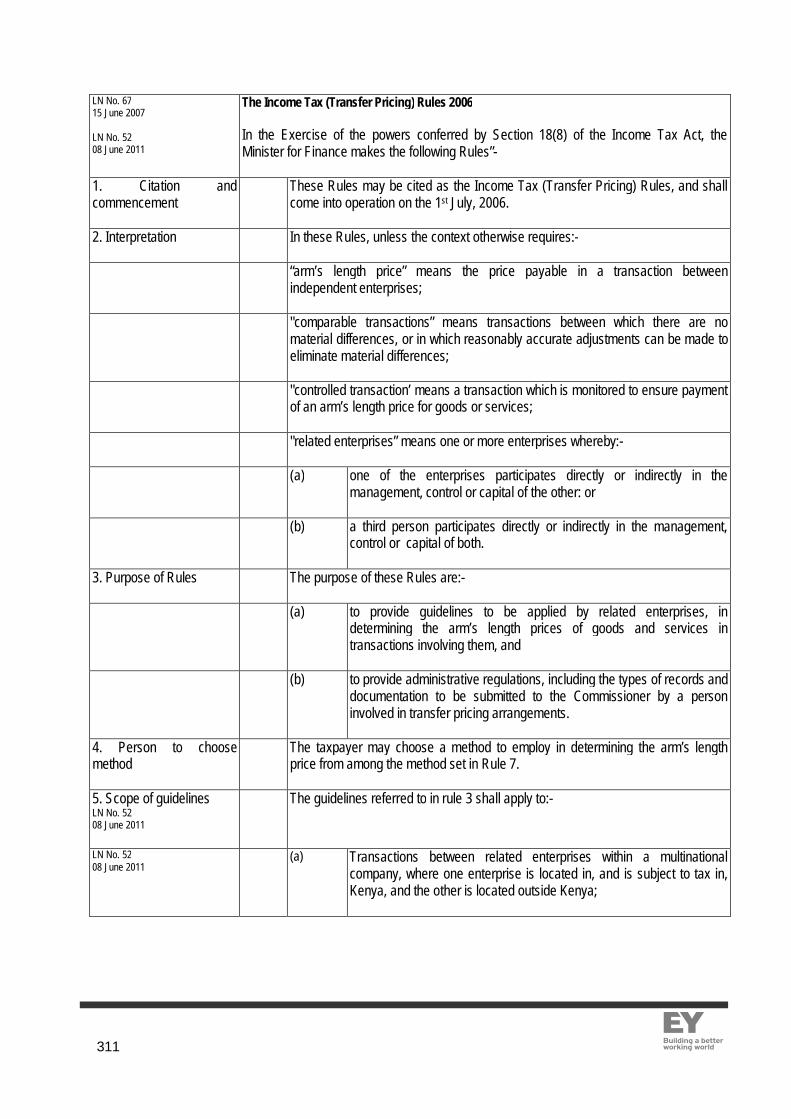

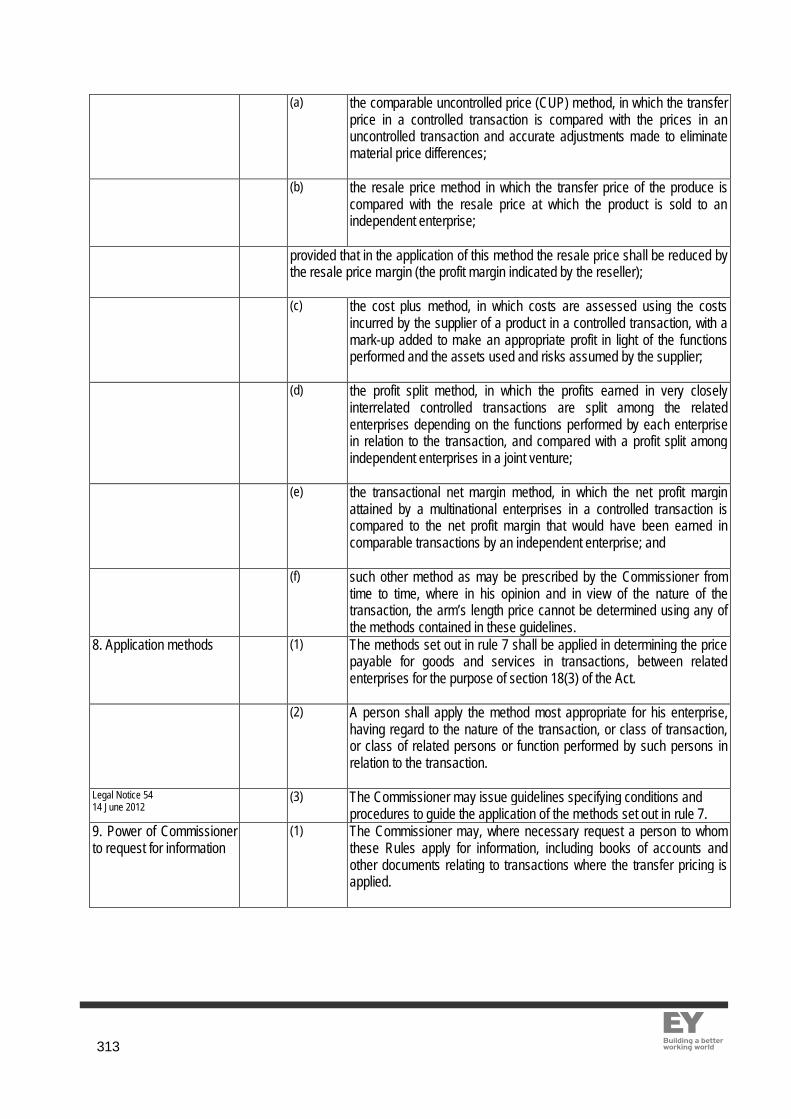

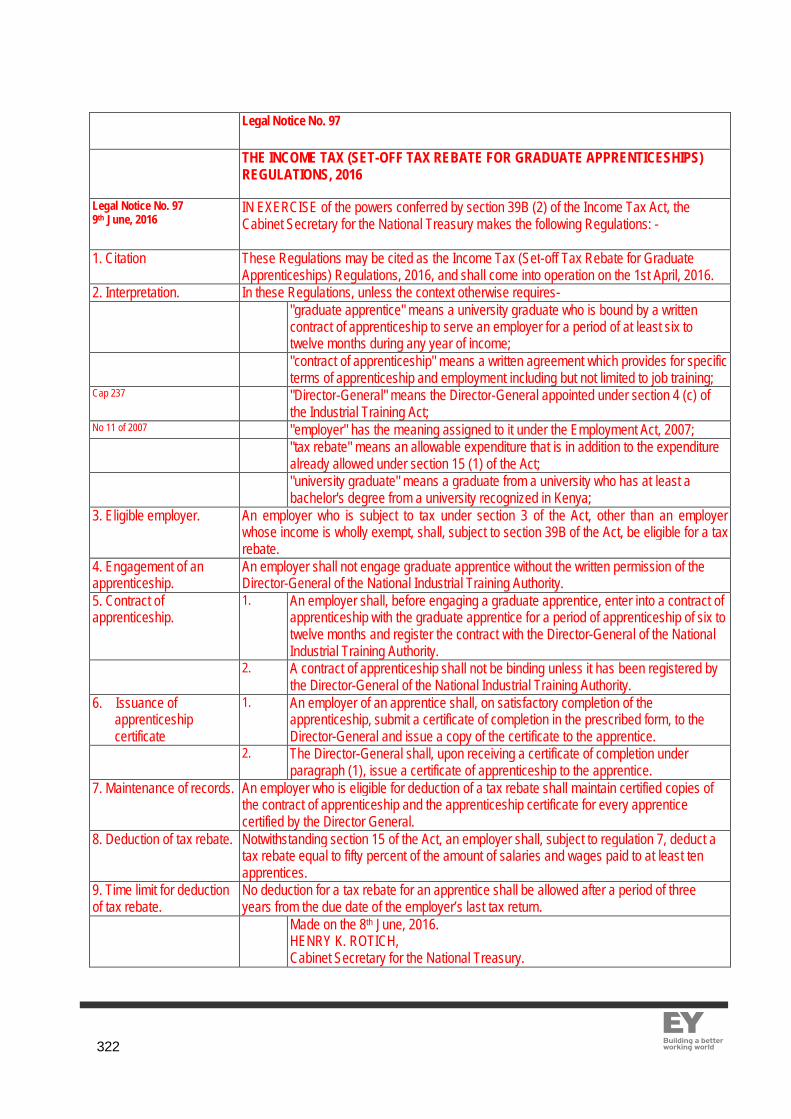

Rules under Section 130 ............................................................................................................ 277The Income Tax (P.A.Y.E) (Amendment) Rules, 2010 277The Income Tax (Distraint) (Amendment) Rules, 2008 283The Income Tax (Prescribed Dwelling-House) Rules 288The Income Tax (Retirement Benefit) (Amendment) Rules, 2008 289The Income Tax (Investment Duty Set Off) Rules – 1996 - Revoked 295The Income Tax (Venture Capital Enterprise) (Amendment) Rules, 2008 296The Income Tax (Registered Home Ownership Savings Plan) (Amendment) Rules, 1995 298The Income Tax (Registered Unit Trusts/Collective Investments Schemes) Rules, 2003 301The Income Tax (Withholding Tax) Rules, 2001 302The Income Tax (Leasing) (Amendment) Rules, 2009 308The Income Tax (Transfer Pricing) Rules 2006 311The Income Tax (Charitable Donations) Regulations, 2007 315The Income Tax (Turnover Tax) Rules, 2007 317Legal Notice No. 52 320The Income Tax (Advance Tax) (Conditions and Procedures) Rules, 2012 320Legal Notice No. 97 322

1_____________________________________________________________________________________________________

16 of 1973,2 of 1975,13 of 1975,7 of1976,11 of 1976,L.N. 1231of 1976,L.N.89 of1977, 12 of 1977, 16 of 1977

CHAPTER 470 – THE INCOME TAX ACT

Commencement: 1st January, 1974

PART 1 – PRELIMINARY

8 of 1978,13 of 1978,13 of 1979,18 of1979,10 of 1980,12 of 1980,6 of 1981,1 of1982,14 of 1982,8 of 1983,13 of 1984,18 of1984,8 of 1985,10 of 1986,10 of 1987,3 of1988,10 of 1988,9 of 1989,20 of 1989

An Act of Parliament to make provision for the charge, assessmentand collection of income tax; for the ascertainment of the income to becharged; for the administrative and general provisions relating thereto;and for matters incidental to and connected with the foregoing

Section

1. Short title andcommencement

This Act may be cited as the Income Tax Act and shall, subject tothe Sixth Schedule, come into operation on 1st January, 1974, andapply to assessments for the year of income 1974 and subsequentyears of income.

2. Interpretation (1) In this Act, unless the context otherwise requires -

7 of 1976 s. 2,12 of 1977, s. 5,8 of 1978, s. 9,12 of 1980, s.3,14 of 1982, s.16,10 of 1987, s.31,10 of 1988, s. 2813 of 1995 s 73.

1 July 2000

"accounting period", in relation to a person, means the period forwhich that person makes up the accounts of his business;

"actuary" means –

(a) a Fellow of the Institute of Actuaries in England; or of theFaculty of Actuaries in Scotland; or of the Society ofActuaries in the United States of America; or of theCanadian Institute of Actuaries; or

(b) such other person having actuarial knowledge as theCommissioner of Insurance may approve;

“agency fees” means payments made to a person for acting on behalfof any other person or group of persons, or on behalf of theGovernment and excludes any payments made by an agent on behalfof a principal when such payments are recoverable;

"annuity contract" means a contract providing for the payment to anindividual of a life annuity, and "registered annuity contract" meansone which has been registered with the Commissioner in such manneras may be prescribed;

Finance Act, 2014 effective 1st Jan 2015 "assessment" means an assessment, instalment assessment, self-assessment provisional assessment or additional assessment madeunder this Act;

"authorised tax agent" means any person who prepares or advisesfor remuneration, or who employs one or more persons to preparefor remuneration, any return, statement or other document, withrespect to a tax under this Act; and for the purposes of this Act, the

2_____________________________________________________________________________________________________

preparation of a substantial portion of a return, statement or otherdocument shall be deemed to be the preparation of the return,statement or other document;

"bank" means a bank or financial institution licensed under theBanking Act;

"bearer" means the person in possession of a bearer instrument;

“bearer instruments” includes a certificate of deposit, bond, note orany similar instrument payable to the bearer;

Cap 489 "building society" means a building society registered under theBuilding Societies Act;

"business" includes any trade, profession or vocation, and everymanufacture, adventure and concern in the nature of trade, butdoes not include employment;

Finance Act 200213 June 2002Cap 485A

“collective investment scheme” has the meaning assigned to it inSection 2 of the Capital Markets Act.

"commercial vehicle" means a road vehicle which theCommissioner is satisfied is -

(a) manufactured for the carriage of goods and so used inconnection with a trade or business; or

Cap 403 (b) a motor omnibus within the meaning of that term in theTraffic Act; or

(c) used for the carriage of members of the public for hire orreward;

Cap 469Finance Act 2004 Effective on 3 Jan 05Kenya Gazette

"Commissioner" means-

(a) the Commissioner – General appointed under section 11(1) of the Kenya Revenue Authority Act; or

(b) with respect to powers or functions that have beendelegated under section 11(4) of the Kenya RevenueAuthority Act to another Commissioner, that otherCommissioner.

"company" means a company incorporated or registered under anylaw in force in Kenya or elsewhere;

"compensating tax" means the addition to tax imposed undersection 7A;

1 July 2000 “consultancy fees” means payment made to any person for acting inan advisory capacity or providing services on a consultancy basis;

3_____________________________________________________________________________________________________

"contract of service" means an agreement, whether oral or inwriting, whether expressed or implied, to employ or to serve as anemployee for any period of time, and includes a contract ofapprenticeship or indentured learnership, under which the employerhas the power of selection and dismissal of the employee, pays hiswages or salary and exercises general or specific control over thework done by him; and for the purpose of this definition an officer inthe public service shall be deemed to be employed under a contractof service;

Finance Act 20011 July 2001

“contractual payments” Definition is deleted.

"corporation rate" means the corporation rate of tax specified inparagraph 2 of Head B of the Third Schedule;

"Court" means the High Court;

"current year of income", in relation to income charged to instalmenttax, means the year of income for which the instalment tax ispayable"

"debenture" includes debenture stock, a mortgage, mortgage stock,or any similar instrument acknowledging indebtedness, secured onthe assets of the person issuing the debenture; and, for thepurposes of paragraphs (d) and (e) of section 7 (1), includes a loanor loan stock, whether secured or unsecured;

Finance Act, 2016 effective 09 June 2016 “deemed interest” means an amount of interest equal to theaverage ninety-one day Treasury Bill rate, deemed to be payableby a resident person in respect of any outstanding loan providedor secured by the non-resident, where such loan is provided freeof interest."defined benefit provision", in respect of a registered fund, meansthe terms of the fund under which benefits in respect of eachmember of the fund are determined in any way other than thatdescribed in the definition of a "defined contribution provision";

"defined benefit registered fund" means a registered fund thatcontains a defined benefit provision, whether or not it also containsa defined contribution provision;

"defined contribution provision", in respect of a registered fund,means terms of the fund -

(a) which provide for a separate account to be maintained inrespect of each member, to which are creditedcontributions made to the fund by, or in respect of, themember and any other amounts allocated to themember, and to which are charged payments in respectof the member; and

4_____________________________________________________________________________________________________

(b) under which the only benefits in respect of a member arebenefits determined solely with reference to, andprovided by, the amount of the member's account;

"defined contribution registered fund" means a registered fundunder which the benefits of a member are determined by a definedcontribution provision, and does not contain a defined benefitprovision;

"director" means -

(a) in relation to a body corporate the affairs of which aremanaged by a board of directors or similar body, amember of that board or similar body;

(b) in relation to a body corporate the affairs of which aremanaged by a single director or similar person, thatdirector or person;

(c) in relation to a body corporate the affairs of which aremanaged by the members themselves, a member of thebody corporate,

and includes any person in accordance with whose directions andinstructions those persons are accustomed to act;

"discount" means interest measured by the difference between theamount received on the sale, final satisfaction or redemption of anydebt, bond, loan, claim, obligation or other evidence ofindebtedness, and the price paid on purchase or original issuanceof the bond or evidence of indebtedness or the sum originallyloaned upon the creation of the loan, claim or other obligation;

"dividend" means any distribution (whether in cash or property, andwhether made before or during a winding up) by a company to itsshareholders with respect to their equity interest in the company,other than distributions made in complete liquidation of thecompany of capital which was originally paid directly into thecompany in connection with the issuance of equity interest;

"due date" means the date on or before which tax is due andpayable under this Act or pursuant to a notice issued under this Act;

"employer" includes any resident person responsible for thepayment of, or on account of, emoluments to an employee, and anagent, manager or other representative so responsible in Kenya onbehalf of a non-resident employer;

"export processing zone enterprise" has the meaning assigned to itby the Export Processing Zones Act, 1990";

"farmer" means a person who carries on pastoral, agricultural or

5_____________________________________________________________________________________________________

other similar operations;

"foreign tax", in relation to income charged to tax in Kenya, meansincome tax or tax of a similar nature charged under any law in forcein any place with the government of which a special arrangementhas been made by the Government of Kenya and which is thesubject of that arrangement;

"incapacitated person" means a minor, or a person adjudged underany law, whether in Kenya or elsewhere, to be in a state ofunsoundness of mind (however described);

"individual" means a natural person;

"individual rates" means the individual rates of income tax specifiedin paragraph I of Head B of the Third Schedule;

"individual retirement fund" means a fund held in trust by a qualifiedinstitution for a resident individual for the purpose of receiving andinvesting funds in qualifying assets in order to provide pensionbenefits for such an individual or the surviving dependants of suchan individual subject to the Income Tax (Retirement Benefit) Rulesand "registered individual retirement fund" means an individualretirement fund where the trust deed for such a fund has beenregistered with the Commissioner;

Finance Act 2005 24 Nov 05Finance Act 2005Effective 8 June 05

“information technology” means any equipment or software for usein storing, retrieving, processing or disseminating information.

"interest" (other than interest charged to tax) means interestpayable in any manner in respect of a loan, deposit, debt, claim orother right or obligation, and includes a premium or discount by wayof interest and a commitment or service fee paid in respect of anyloan or credit;

Cap 312 "Kenya" includes the continental shelf and any installation thereonas defined in the Continental Shelf Act;

"local committee" means a local committee established undersection 82;

"loss", in relation to gains or profits, means a loss computed in thesame manner as gains or profits;

EA Cap 24 "Management Act" means the East African Income TaxManagement Act;

1 July 2000Finance Act 200213 June 200216 June 06

"management or professional fee" means a payment made to aperson, other than a payment made to an employee by hisemployer, as consideration for managerial, technical, agency,contractual, professional or consultancy services howevercalculated;

6_____________________________________________________________________________________________________

Finance Act, 2013 effective 1st Jan 2014 “Minister” means the Cabinet Secretary for the time beingresponsible for matters relating to finance;

Finance Act, 2014 effective 1st Jan 2015 “natural resource income” means -

(i) an amount including a premium or such other like amount paidas consideration for the right to take minerals or a living ornonliving resource from land or sea; or

(ii) an amount calculated in whole or in part by reference to thequantity or value of minerals or a living or non-living resourcetaken from land or sea.

Cap 258 "national Social Security Fund" means the National Social SecurityFund established under Section 3 of the National Social SecurityFund Act;

"non-resident rate" means a non-resident tax rate specified inparagraph 3 of Head B of the Third Schedule;

"notice of objection" means a valid notice of objection to anassessment given under section 84(1);

"number of full-year members", in respect of a registered fund,means the sum of the periods of service in the year under the fundof all members of the fund, where the periods are expressed asfractions of a year;

Cap 469Finance Act 2004 Effective on 3 Jan 05Kenya Gazette

"officer" means the Commissioner and any other member of staff ofthe Kenya Revenue Authority appointed under Section 13 of theKenya Revenue Authority Act.

Finance Act, 2013 effective 1st Jan 2014Finance Act, 2014 effective 1st Jan 2015

“oil company” means a petroleum company within the meaning ofthe Ninth Schedule;

"original issue discount" means the difference between the amountreceived on the final satisfaction or redemption of any debt, bond,loan, claim, obligation or other evidence of indebtedness, and theprice paid on original issuance of the bond or evidence ofindebtedness or the sum originally loaned upon creation of theobligation, loan, claim or other obligation;

"paid" includes distributed, credited, dealt with or deemed to havebeen paid in the interest or on behalf of a person;

"pension fund" means a fund for the payment of pensions or othersimilar benefits to employees on retirement, or to the dependants ofemployees on the death of those employees and "registeredpension fund" means one which has been registered with theCommissioner in such manner as may be prescribed;

"pensionable income" means

(a) in relation to a member of a registered pension or

7_____________________________________________________________________________________________________

provident fund or of an individual eligible to contribute toa registered individual retirement fund, the employmentincome specified in section 3(2)(a)(ii) subjected todeduction of tax under section 37;

(b) in the case of an individual eligible to contribute to aregistered individual retirement fund, the gains or profitsfrom business subject to tax under section 3(2)(a)(i)earned as the sole proprietor or as a partner of thebusiness:

Provided that where a loss from business is realised, the loss shallbe deemed to be zero;

Finance Act, 2014 effective 1st Jan 2015 "permanent establishment" in relation to a person means a fixedplace of business in which that person carries on business and forthe purposes of this definition, a building site, or a construction orassembly project, which has existed for six months or more shall bedeemed to be a fixed place of business;“permanent establishment” in relation to a person, means a fixed placeof business and includes a place of management, a branch, an office,a factory, a workshop, and a mine, an oil or gas well, a quarry or anyother place of extraction of natural resources, a building site, or aconstruction or installation project which has existed for six months ormore where that person wholly or partly carries on business:Provided that -(a) the permanent establishment of the person shall be deemed to

include the permanent establishment of the person’s dependentagent;

(b) in paragraph (a), the expression “dependent agent” means anagent of the person who acts on the person’s behalf and whohas, and habitually exercises, authority to conclude contracts inthe name of that person;

"permanent or semi-permanent crops" means those crops which theMinister may, by notice in the Gazette, declare to be permanent orsemi-permanent crops for the purposes of this Act

"personal relief" means:-

(a) the personal relief provided for under part V; and

(b) the relief mentioned in Section 30;

"preceding year assessment", in relation to instalment tax, meansthe tax assessed for the preceding tax year of income as of the datethe instalment tax is due without regard to subsequent additions to,amendments of, or subtractions from the assessment; and in theevent that as of the date the instalment tax is due no assessmentfor the preceding year of tax has, as yet, been made, means theamount of tax estimated by the person as assessable for thepreceding year of income;

8_____________________________________________________________________________________________________

"premises" means land, any improvement thereon, and any buildingor, where part of a building is occupied as a separatedwelling-house, that part;

"provident fund" includes a fund or scheme for the payment of lumpsums and other similar benefits, to employees when they leaveemployment or to the dependants of employees on the death ofthose employees but does not include a national provident fund ornational social security fund established by the Government;

"registered provident fund" means one which has been registeredwith the Commissioner in such manner as may be prescribed;

Finance Act, 2014 effective 1st Jan 2015 "provisional return of income" means a provisional return of incomefurnished by a person under section 53, together with anydocuments required to be furnished therewith;

"public pension scheme" means a pension scheme that payspensions or lump sums out of the Consolidated Fund

Finance Act 200213 June 2002

"qualifying assets", in respect of a registered individual retirementfund, means time deposits, treasury bills, treasury bonds, securitiestraded on any securities exchange approved under the CapitalMarkets Act and such other categories of assets as may beprescribed in the investment guidelines issued under the RetirementBenefits Act, 1997.

"qualifying dividend" means that part of the aggregate dividend thatis chargeable to tax under section 3(2)(b) and which has not beenotherwise exempted under any other provision of this Act, but shallnot include a dividend paid by a designated co-operative societysubject to tax under section 19A(2) or 19A(3);

"qualifying dividend rate of tax" means the resident withholding taxrate in respect of a qualifying dividend specified in the ThirdSchedule;

Finance Act 200213 June 2002

"qualified institution" means a bank licensed under the Banking Act,1989, or an insurer registered under the Insurance Act, or suchother financial institution as may be approved under the RetirementBenefits Act, 1997.

“qualifying interest" means the aggregate interest, discount ororiginal issue discount receivable by a resident individual in anyyear of income from -

Cap 488 (i) a bank or financial institution licensed under the BankingAct, or

Cap 489 (ii) a Building Society registered under the Building SocietiesAct which in the case of housing bonds has beenapproved by the Minister for the purposes of this Act, or

9_____________________________________________________________________________________________________

(iii) the Central Bank of Kenya:

1 July 1999 Provided that

(a) interest earned on an account held jointly by a husbandand wife shall be deemed to be qualifying interest; and

(b) in the case of housing bonds, the aggregate amount ofinterest shall not exceed three hundred thousandshillings;

"qualifying interest rate of tax" means the resident withholding taxrate in respect of interest specified in paragraph 5 of the ThirdSchedule;

Finance Act 201201 January 2012Cap. 485A

"real estate investment trust" shall have the meaning assigned to itin the Capital Markets Act;

"registered fund" means a registered pension fund or aregistered provident fund;

"registered home ownership savings plan" means a savings planestablished by an approved institution and registered with theCommissioner for receiving and holding funds in trust for depositorsfor the purpose of enabling individual depositors to purchase apermanent house;

"registered trust scheme" means a trust scheme for the provision ofretirement annuities which has been registered with theCommissioner in such manner as may be prescribed;

"registered unit trust" means a unit trust registered by theCommissioner in such manner as may be prescribed;

“registered venture capital company" means a venture capitalcompany registered by the Commissioner in such manner as maybe prescribed;

"resident", when applied in relation -

(a) to an individual, means –

(i) that he has a permanent home in Kenya andwas present in Kenya for any period in aparticular year of income under consideration; or

(ii) that he has no permanent home in Kenya but –

(A) was present in Kenya for a period orperiods amounting in the aggregate to

10_____________________________________________________________________________________________________

183 days or more in that year ofincome; or

(B) was present in Kenya in that year ofincome and in each of the twopreceding years of income for periodsaveraging more than 122 days in eachyear of income;

(b) to a body of persons, means –

(i) that the body is a company incorporated under alaw of Kenya; or

(ii) that the management and control of the affairs ofthe body was exercised in Kenya in a particularyear of income under consideration; or

(iii) that the body has been declared by the Minister,by notice in the Gazette, to be resident in Kenyafor any year of income;

"resident withholding rate" means a rate of resident withholding taxspecified in paragraph 5 of Head B of the Third Schedule;

Finance Act 200312 June 2003Finance Act 20039 Jan 04

"return of income" means a return of income furnished by a personconsequent upon a notice served by the Commissioner undersection 52, including a return of income together with a selfassessment of tax furnished to the Commissioner in accordancewith the provisions of section 52B, together with the documentsrequired to be furnished therewith;

"retirement annuity" means a retirement annuity payable under aregistered annuity contract;

Finance Act 200213 June 2002No. 3 of 1997

“Retirement Benefit Authority” means the authority by that nameestablished under the Retirement Benefits Act, 1997;

"royalty" means a payment made as a consideration for the use ofor the right to use -

(a) the copyright of a literary, artistic or scientific work; or

(b) a cinematograph film, including film or tape for radio ortelevision broadcasting; or

(c) a patent, trade mark, design or model, plan, formula orprocess; or

(d) any industrial, commercial or scientific equipment,

Cap 485A or for information concerning industrial, commercial or scientific

11_____________________________________________________________________________________________________

equipment or experience, and gains derived from the sale orexchange of any right or property giving rise to that royalty;

"securities exchange" has the meaning assigned to it in Section 2 ofthe Capital Markets Authority Act;

Finance Act, 2013 effective 1st Jan 2014 "special arrangement" means an arrangement for relief from doubletaxation having effect under section 41 or an arrangement for theexchange of tax information under section 41A;

Finance Act, 2014 effective 1st Jan 2015 "specified mineral" means a mineral which the Minister may, bynotice in the Gazette, declare to be a specified mineral for thepurposes of this Act;

"tax" means the income tax charged under this Act;

Finance Act 2005 24 Nov. 05Finance Act 2005Effective 8 June 05

“tax computerized system” means any software or hardware for usein storing, retrieving, processing or disseminating informationrelating to tax.

Finance Act 2009Effective 12 June 09Cap 411, No.2 of 1998.

“telecommunication operator” means a person licensed as suchunder the Kenya Information and Communications Act, 1998;

"total income" means, in relation to a person, the aggregate amountof his income, other than income exempt from tax under Part III,chargeable to tax under Part II, as ascertained under Part IV;

"trade association" means a body of persons which is anassociation of persons separately engaged in any business with themain object of safeguarding or promoting the business interests ofthose persons;

Finance Act 2008Effective 13 June 08Finance Act 2009Effective 12 June 09

“training fee” means a payment made in respect of a business oruser training services designed to improve the work practices andefficiency of an organization, and includes any payment in respectof incidental costs associated with the provision of such services.

Finance Act, 2015 effective 1st Jan 2016 Provided that training fee shall not include fees paid for educationalservices provided by—(a) a pre-primary, primary, or secondary school;(b) a technical college or university;(c) an institution established for the promotion of adult education,

vocational training or technical education."Tribunal" means the tribunal established under section 83;

"unit holder", in relation to a unit trust, means the owner of aninterest in the moneys, investments and other property which are forthe time being subject to the trusts governing the unit trust, thatinterest being expressed in the number of units of which he is theowner;

Finance Act 200213 June 2002Cap 485A

"unit trust" has the meaning assigned to it in Section 2 of the CapitalMarkets Act.;

12_____________________________________________________________________________________________________

Finance Act 2008Effective 13 June 08

"venture company" means a company incorporated in Kenya inwhich a venture company has invested and which at the time of firstinvestment by the venture company has assets with a market valueor annual turnover of less than five hundred million Kenya shillings;

"whole time service director" means a director of a company who isrequired to devote substantially the whole of his time to the serviceof that company in a managerial or technical capacity and is not thebeneficial owner of, or able, either directly or through the medium ofother companies or by any other means, to control more than fiveper cent of the share capital or voting power of that company;

"wife's employment income' means gains or profits fromemployment arising from a contract of service which is chargeableto tax under section 3(2)(a)(ii) and pensions, lumpsums andwithdrawals from a registered fund, public pension scheme orregistered individual retirement fund which are chargeable to taxunder section 3(2)(c), of a woman living with her husband,excepting income derived by her as a trustee or manager of asettlement created by her husband the income of which is deemedunder section 25 or 26 to be the income of the settler or incomederived by her as an employee of -

(a) a partnership in which her husband is a partner;

(b) her husband; or

(c) a company, the voting power of which is held to theextent of twelve and one-half per cent or more at anytime during the year of income by her or by her husbandor by both jointly, either directly or through nominees;

"wife's employment income rate" means the wife's employmentincome rate specified in paragraph I A of Head B of the ThirdSchedule;

"wife's professional income" means the gains or profits of a marriedwoman living with her husband derived from the exercise by her(but not as a partner of a partnership in which her husband is apartner) of one of the professions specified in the Fifth Schedulebeing also a person who has the qualifications specified in thatSchedule relevant to that profession;

"wife's professional income rate" means the wife's professionalincome rate specified in paragraph IA of Head B of the ThirdSchedule;

Finance Act 2008Effective 1 January 09

"wife's self-employment income" means gains or profits arising froma business of a married woman living with her husband which arechargeable to tax under section 3(2)(a)(i) and any incomechargeable under section 3(2) (a) (iii) or section 3(2) (b), but does

13_____________________________________________________________________________________________________

not include any income derived from the provision of goods orservices by her to a business, partnership or a company owned byor the voting power of which is held to the extent of twelve and onehalf percent, or more at any one time during the year of income byher or her husband either directly or through nominee;

"wife's self-employment income rate" means the wife's self-employment income rate specified in paragraph 1A of Head B of theThird Schedule;

Finance Act 201201 January 2012Cap. 131Finance Act 201209 January 2013

Finance Act, 2013 effective 1st Jan 2014CAP 131

“winnings” has the meaning assigned to it in the Betting, Lotteries andGaming Act;

Finance Act, 2015 effective 1st Jan 2016 Provided that this definition shall only apply in the case ofwinnings payable to punters (players) by bookmakers.

"year of income" means the period of twelve months commencingon 1st January in any year and ending on 31st December in thatyear.

Finance Act 200213 June 2002

1(A) Where under the provisions of this Act, any accounts, books ofaccounts or other records are required to be kept, such accountsbooks or other records may be kept in written form or on micro-film,magnetic tape or any other form of mechanical or electronic dataretrieval mechanism

Cap 415 2 In relation to any year of income in respect of which an orderrelating to tax or personal reliefs has been made under theProvisional Collection of Taxes and Duties Act reference in this Actto rates of tax and personal reliefs shall, so long as the orderremains in force, be construed as references to the rates or reliefsspecified in that order; and if, after the order has ceased to haveeffect, the rates of tax and of personal reliefs in relation to that yearof income as specified in this Act as amended are different fromthose referred to in the order, and assessments have already beenmade having regard to those rates in the order, then all necessaryadjustments shall be made to the assessments to give effect to therates of tax and of personal reliefs for that year of income asspecified in this Act as amended for that year of income.

__________________________

14

PART II – IMPOSITION OF INCOME TAX

3. Charge of tax

13 of 1975, s. .2, 8 of 1978, s.9 ,14 of 1982, s.17

(1) Subject to, and in accordance with, this Act, a tax to be knownas income tax shall be charged for each year of income uponall the income of a person, whether resident or non-resident,which accrued in, or was derived from Kenya.

(2) Subject to this Act, income upon which tax is chargeable underthis Act is income in respect of -

(a) gains or profits from –

(i) a business for whatever period of timecarried on;

(ii) employment or services rendered;

(iii) a right granted to another person for use oroccupation of property;

(b) dividends or interest;

(c) (i) a pension, charge or annuity; and

(ii) any withdrawals from, or payments out of,a registered pension fund or a registeredprovident fund or a registered individualretirement fund; and

(iii) any withdrawals from a registered homeownership savings plan.

(d) (Deleted by 14 of 1982, s. 17);

(e) an amount deemed to be the income of a personunder this Act or by rules made under this Act;

(f) gains accruing in the circumstances prescribed in,and computed in accordance with, the EighthSchedule.

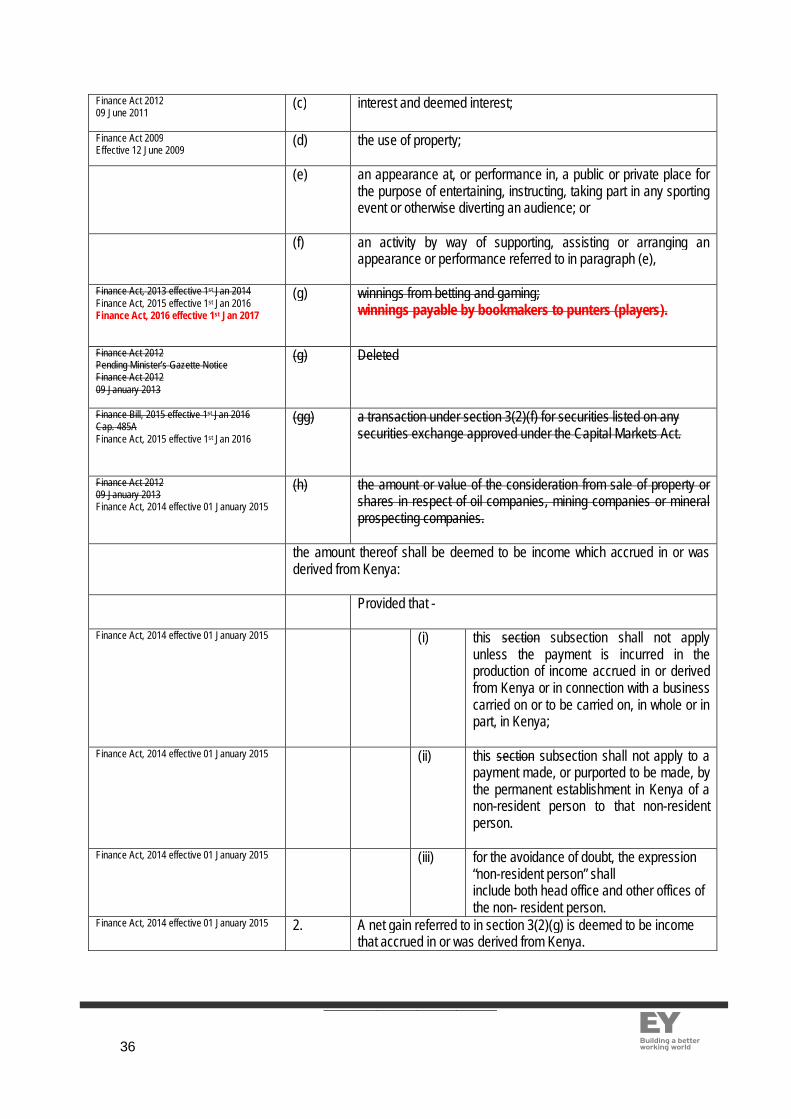

Finance Act 201209 January 2013Finance Act, 2014 effective 1st Jan 2015

(g)

(g)

the amount or value of the consideration from thesale of property or shares in respect of oilcompanies, mining companies or mineralprospecting companies.subject to section 15(5A), the net gain derived onthe disposal of an interest in a person, if the interestderives twenty per cent or more of its value, directlyor indirectly, from immovable property in Kenya; and

Finance Act, 2014 effective 1st Jan 2015 (h) a natural resource income.(3) For the purposes of this Section -

Finance Act, 2014 effective 1st Jan 2015 (a) "person" does not include a partnership; and

__________________________

15

(b) a bonus or interest paid by a designatedcooperative society, as defined under Section 19A,shall be deemed to be a dividend.

Finance Act 201209 January 2013Finance Act, 2014 effective 1st Jan 2015

(c) “sale of property or shares” includes the assignmentof rights, sale of companies and businesses, andtakeovers or any other non-inventory assets.for the purposes of subsection (2)(g) and section15(5A) –(i) “immovable property” means a mining right, an

interest in a petroleum agreement, mininginformation or petroleum information;

(ii) “net gain”, in relation to the disposal of aninterest in a person, means the consideration forthe disposal reduced by the cost of the interest;and

(iii) the terms “consideration”, “cost”, “disposal”,“interest in a person”, “mining information”,“mining right”, “person”, “petroleum agreement”,and “petroleum information” have the meaningassigned to them in the Ninth Schedule.

4. Income from businesses For the purposes of Section 3 (2) (a) (i)

18 of 1984 s.2 (a) where a business is carried on or exercised partly within andpartly outside Kenya by a resident person, the whole of thegains or profits from that business shall be deemed to haveaccrued in or to have been derived from Kenya;

(b) the gains or profits of a partner from a partnership shall be thesum of-

(i) remuneration payable to him by the partnershiptogether with interest on capital so payable, lessinterest on capital payable by him to the partnership;and

(ii) his share of the total income of the partnership,calculated after deducting the total of anyremuneration and interest on capital payable to anypartner by the partnership and after adding anyinterest on capital payable by any partner to thepartnership,

and where the partnership makes a loss, calculatedin the manner set out in subparagraph (ii), his gainsor profits shall be the excess, if any, of the amountset out in subparagraph (i) over his share of thatloss;

Finance Act 2009Effective 1 January 2010

“Provided that in computing the total income of apartnership, there shall be deducted the cost of

__________________________

16

medical expenses or medical insurance cover paidby the partnership for the benefit of any partner,subject to a limit of one million shillings per year.

Finance Act 201209 June 2011

(c) a sum received under an insurance against loss of profits, orreceived by way of damages or compensation for loss ofprofits, shall be deemed to be gains or profits of the year ofincome in which it is received;

(d) where in computing gains or profits for a year of income anyexpenditure or loss has been deducted, or a deduction inrespect of any reserve or provision to meet any liability hasbeen made, and in a later year of income the whole or part ofthat expenditure or loss is recovered, or the whole or part ofthat liability is released, or the retention in whole or in part ofthat reserve or provision has become unnecessary, then anysum so recovered or released or no longer required as areserve or provision shall be deemed to be gains or profits ofthe year of income in which it is recovered or released or nolonger required:

Provided that if the person so chargeable with tax in respect ofany such sum requests the Commissioner in writing to exercisehis power under this proviso, the Commissioner may divide thesum into as many equal portions, not exceeding six, as he mayconsider fit, and one such portion shall be taken into account incomputing the gains or profits of that person for the year ofincome in respect of which the sum is so deemed to be gains orprofits and for each of the previous years of incomecorresponding to the number of portions;

(e) where under the Second Schedule it is provided that abalancing charge shall be made, or a sum shall be treated as atrading receipt, for any year of income, the amount thereof shallbe deemed to be gains or profits of that year of income;

Finance Act, 2014 effective 1st Jan 2015 (f) in computing the gains or profits of a petroleum company or ofa petroleum service subcontractor, as those expressions aredefined in the Ninth Schedule, the provisions of that Scheduleshall apply.in computing the gains or profits of a “licensee”, “contractor” or“subcontractor” as defined in the Ninth Schedule, the provisions ofthat Schedule shall apply.

4A Income from business whereforeign exchange gain orloss is realized

10 of 1988 s.29

(1) A foreign exchange gain or loss realized on or after the 1stJanuary,1989 in a business carried on in Kenya shall be takeninto account as a trading receipt or deductible expenses incomputing the gains and profits of that business for the year ofincome in which that gain or loss was realized:

Provided that:-

(i) no foreign exchange gain or loss shall be taken intoaccount to the extent that taking that foreign

__________________________

17

exchange gain or loss into account would duplicatethe amounts of gain or loss accrued in any prioryear of income; and

(ii) the foreign exchange loss shall be deferred (and nottaken into account)–

Finance Act 2008Effective 13 June 08

(a) where the foreign exchange loss isrealized by a company with respect to aloan from a person who, alone ortogether with four or fewer other persons,is in control of that company and thehighest amount of all loans by thatcompany outstanding at any time duringthe year of income is more than threetimes the sum of the revenue reservesand the issued and paid up capital of allclasses of shares of the company; or

(b) to the extent of any foreign exchangegain that would be realized if all foreigncurrency assets and liabilities of thebusiness were disposed of or satisfied onthe last day of the year of income andany foreign exchange loss so deferredshall deemed realized in the nextsucceeding year of income.

Finance Act 2008Effective 13 June 08

(IA) For the avoidance of doubt, accumulated lossesshall be taken into account in computing the amountof revenue reserves.

(2) The amount of foreign exchange gain or loss shallbe calculated in accordance with the differencebetween (a times r1) and (a times r2) where-

A is the amount of foreign currency received,paid or otherwise computed with respect toa foreign currency asset or liability in thetransaction in which the foreign exchangegain or loss is realized;

r1 is the applicable rate of exchange for thatforeign currency ("a") at the date of thetransaction in which the foreign exchangegain or loss is realized;

r2 is the applicable rate of exchange for thatforeign currency ("a") at the date on whichthe foreign currency asset or liability wasobtained or established or on the 30thDecember, 1988, whichever date is thelater.

__________________________

18

(3) For the purposes of this section, no foreignexchange loss shall be deemed to be realizedwhere a foreign currency asset or liability isdisposed of or satisfied and within a period of sixtydays a substantially similar foreign currency asset orliability is obtained or established.

(4) For the purposes of this section -

“foreign currency asset or liability" means an assetor liability denominated in, or the amount of which isotherwise determined by reference to, a currencyother than the Kenya Shilling;

“control" shall have the meaning ascribed to it inparagraph 32 (1) of the Second Schedule;

Cap 488 “company" does not include a bank or a financialinstitution licensed under the Banking Act.

Finance Act 2009Effective 12 June 2009

“all loans” shall have the meaning assigned in section16(3).

4B Export processing zoneenterprise

Where a business is carried on by an export processing zoneenterprise, the provisions of the Eleventh Schedule shall apply.

5. Income from employment,etc

(1) For the purposes of section 3(2)(a)(ii), an amount paid to-

8 of 1978 s.913 of 1979 s.5 10 of 1987 s.32 9 of 1989s.17

(a) a person who is, or was at the time of theemployment or when the services were rendered, aresident person in respect of any employment orservices rendered by him in Kenya or outsideKenya; or

(b) a non-resident person in respect of any employmentwith or services rendered to an employer who isresident in Kenya or the permanent establishment inKenya of an employer who is not so resident,

shall be deemed to have accrued in or to have beenderived from Kenya.

(2) For the purposes of section 3(2)(a)(ii), "gains or profits"includes -

(a) wages, salary, leave pay, sick pay, payment in lieuof leave, fees, commission, bonus, gratuity, orsubsistence, traveling, entertainment or otherallowance received in respect of employment orservices rendered, and any amount so received inrespect of employment or services rendered in ayear of income other than the year of income in

__________________________

19

which it is received shall be deemed to be income inrespect of that other year of income:

Provided that -

(i) where such an amount is received inrespect of a year of income whichexpired earlier than four years prior to theyear of income in which it was received,or prior to the year of income in which theemployment or services ceased, ifearlier, it shall be deemed to be incomeof the year of income which expired fiveyears prior to the year of income in whichit was received, or prior to the year ofincome in which the employment orservices ceased; and

(ii) where the Commissioner is satisfied thatsubsistence, traveling, entertainment orother allowance represents solely thereimbursement to the recipient of anamount expended by him wholly andexclusively in the production of hisincome from the employment or servicesrendered then the calculation of the gainsor profits of the recipient shall excludethat allowance or expenditure;

Finance Act 2006Effective 16 June 06

(iii) Notwithstanding the provisions ofsubparagraph (ii), where such amount isreceived by an employee as payment ofsubsistence, travelling, entertainment orother allowance, in respect of a periodspent outside his usual place of workwhile on official duties, the first twothousand shillings per day expended byhim for the duration of that period shallbe deemed to be reimbursement of theamount so expended and shall beexcluded in the calculation of his gains orprofits.

Finance Act 20011 July 2001Finance Act 200312 .6.03Finance Act 20039 Jan 04Finance Act 2005Effective 9 Jun 05Finance Act 200524 Nov 05

(b) save as otherwise expressly provided in thissection, the value of a benefit, advantage, or facilityof whatsoever nature the aggregate value whereofis not less than thirty six thousand shillings grantedin respect of employment or services rendered;

(c ) an amount received as compensation for thetermination of a contract of employment or service,whether or not provision is made in the contract forthe payment of that compensation:

__________________________

20

Provided that, except in the case of a director, otherthan a whole time service director, of a company thedirectors whereof have a controlling interest therein-

Finance Act 20041 July 04 Kenya Gazette 3 Jan 05

(i) where the contact is for a specified term,any amount received as compensationon the termination of the contract shall bedeemed to have accrued evenly over theunexpired period of the contract;

(ii) where the contract is for an unspecifiedterm and provides for compensation onthe termination thereof, thecompensation shall be deemed to haveaccrued in the period immediatelyfollowing the termination at a rate equalto the rate per annum of the gains orprofits from the contract receivedimmediately prior to termination;

Finance Act 20041 July 04Kenya Gazette 3 Jan 05

(iii) where the contract is for an unspecifiedterm and does not provide for compensationon the termination thereof, anycompensation paid on the termination of thecontract shall be deemed to have accruedevenly in the three years immediatelyfollowing such termination.

(d) any balancing charge under Part II of the SecondSchedule;

(e) the value of premises provided by an employer foroccupation by his employee for residentialpurposes;

Finance Act 200213 June 2002

Deleted: under the Finance Act 2013,effective 1st Jan 2014

(f) an amount paid by an employer as a premium for aninsurance on the life of his employee and for thebenefit of that employee or any of his dependantsother than such an amount paid to a registered orunregistered pension scheme, pension fund,provident fund or individual retirement fund;

Finance Act, 2013 effective 1st Jan 2014 (f) an amount paid by an employer as a premium for aninsurance on the life of his employee and for thebenefit of that employee or any of his dependants:

Provided that this paragraph shall not apply wheresuch an amount is paid -(i) to a registered or unregistered pension

scheme, pension fund, or individualretirement fund; or

__________________________

21

(ii) for group life policy cover, unless sucha cover confers a benefit to theemployee or any of his dependants.

2(A) (a) Where an individual is a director or an employee oris a relative of a director or an employee and hasreceived a loan including a loan from anunregistered pension or provident fund by virtue ofhis position as director or his employment, or theemployment of the person to whom he is related, heshall be deemed to have received a benefit in thatyear of income equal to the greater of -

(i) the difference between the interest thatwould have been payable on the loanreceived if calculated at the prescribedrate of interest and the actual interestpaid on the loan; and

(ii) zero.

Provided that where the term of the loan extends fora period beyond the date of termination ofemployment, the provisions of this subsection shallcontinue to apply for as long as the loan remainsunpaid;

(b) For the purposes of this subsection -

"employee" means any person who is not abeneficial owner of or able either directly orindirectly or through the medium of other companiesor by any other means to control more than five percent of the share capital or voting power of thatcompany;

"market lending rates" means the average 91 daytreasury bill rate of interest for the previous quarter

"prescribed rate of interest" means the following -

(i) in the year of income commencing on the1st January, 1990, 6 per cent;

(ii) in the year of income commencing on the1st January, 1991, 8 per cent;

(iii) in the year of income commencing on the1st January, 1992, 10 per cent;

(iv) in the year of income commencing on the1st January 1993, 12 per cent;

__________________________

22

(v) in the year of income commencing on the1st January 1994, 15 per cent; and

(vi) in the year of income commencing on orafter the 1st January 1995, 15% or suchinterest rate based on the market lendingrates as the Commissioner may from timeto time prescribe, to cover a period of notless than six months but not more thanone year whichever is lower.

"relative of a director or an employee" means -

(i) his spouse;

(ii) his son, daughter, brother, sister, uncle,aunt, nephew, niece, step-father,step-mother, step-child, adopted child, orin the case of an adopted child hisadopter or adopters; or

(iii) the spouse of any such relativeas is mentioned in subparagraph(ii).

Motor Vehicle Benefit13 of 1995 s 75

Finance Act 2007Effective 1 January 08

2(B) Where an employee is provided with a motor vehicle by hisemployer, he shall be deemed to have received a benefit in thatyear of income equal to the higher of -

(a) Such value as the Commissioner may, from time totime, determine; and

(b) the prescribed rate of benefit.

Provided that –

(i) Where such vehicle is hired or leased from a thirdparty, the employee shall be deemed to havereceived a benefit in that year of income equal tothe cost of hiring or leasing; or

(ii) Where an employee has restricted use of suchmotor vehicle, the Commissioner shall, if satisfied ofthat fact upon proof by the employee, determine alower rate of benefit depending on the usage of themotor vehicle.

2(C) For the purposes of subsection 2(B) -

“prescribed rate of benefit" means the followingrates in respect of each month -

__________________________

23

(a) In the 1996 year of income, 1% of theinitial capital expenditure on the vehicleby the employer;

(b) In the 1997 year of income, 1.5% of theinitial capital expenditure on the vehicleby the employer; and

(c) In 1998 and subsequent years of income,2% of the initial expenditure on thevehicle by the employer.

13 of 1995 s 755 of 1998 s 30

(3) For the purposes of subsection (2)(e), the value of premisesexcluding the value of any furniture or other contents soprovided, shall be deemed to be-

Finance Act 2008Effective 13 June 08

(a) In the case of a director of a company, other than awhole time service director, an amount equal to thehigher of fifteen per centum of his total incomeexcluding the value of those premises and incomewhich is chargeable under section 3(2)(f), themarket rental value and the rent paid by theemployer.

Finance Act 2008Effective 13 June 08

(b) In the case of a whole time service director, anamount equal to the higher of fifteen per centum ofthe gains or profits from his employment, excludingthe value of those premises and income which ischargeable under section 3(2)(f), the market rentalvalue and the rent paid by the employer.

(c) in the case of an agricultural employee required bythe terms of employment to reside on a plantation orfarm an amount equal to ten per cent of the gains orprofits from his employment:

Provided that for the purposes of this paragraph -

(i) “plantation" shall not include a forest ortimber plantation; and

(ii) "agricultural employee" shall not include adirector other than a whole time servicedirector;

Finance Act 200213.6.02

(d) In the case of any other employee, an amount equalto fifteen per centum of the gains or profits from hisemployment, excluding the value of those premisesor the rent paid by the employer if paid under anagreement made at arm’s length with a third party,whichever is the higher.

Provided that -

__________________________

24

(i) where the premises are provided underan agreement with a third party which isnot at arm’s length, the value of thepremises determined under thissubsection shall be the fair market rentalvalue of the premises in that year, or therent paid by the employer, whichever isthe higher; or

(ii) where the premises are owned by theemployer, the fair market value of thepremises in that year.

Provided that –

(i) where a person occupiespremises for part only of a yearof income, the value ascertainedunder the foregoing provisionsshall be reduced by thatproportion which is just andreasonable having regard to theperiod of occupation and theyearly rate of gains or profitsfrom employment;

(ii) where the employee pays rent tohis employer for premises, thevalue ascertained under theforegoing provisions shall bereduced by the amount of therent;

(iii) where part only of any premisesis so provided, the Commissionermay reduce the value;ascertained under the foregoingprovisions, to the amount whichhe considers just andreasonable;

(iv) where the gains or profits from aperson's employment, excludingthe value of the premisesprovided by the employer,exceed six hundred thousandshillings in the year, the value ofthe premises determined underthis subsection shall be subjectto the limit of -

(a) The rent paid by the

__________________________

25

employer or the fairmarket rental value ofthe premises in that yearwhere the premises areprovided under anagreement with a thirdparty which is not atarm's length, whicheveris the higher; or

(b) The fair market rentalvalue of the premises inthat year where thepremises are owned bythe employer.

(4) Notwithstanding anything to the contrary in subsection (2)"gains or profits" do not include -

(a) the expenditure on passages between Kenya andany place outside Kenya borne by the employer:

Provided that this paragraph shall not apply toexpenditure other than expenditure on theprovision of passages for the benefit of anemployee recruited or engaged outside Kenya andwho is in Kenya solely for the purpose of servingthe employer and is not a citizen of Kenya;

Finance Act, 2014 effective 13 June 2014 (aa) expenditure on vacation trips to destinations in Kenyapaid by the employer on behalf of an employee:Provided that -

Finance Act, 2014 effective 13 June 2014 (i) this paragraph shall cease to apply on the 1stJuly, 2015;

Finance Act, 2014 effective 19 September2014

(ii) the period of vacation shall not exceed sevendays; and

Finance Act, 2014 effective 19 September2014

(iii) the term “employee” shall include theimmediate family members of the employee.

Finance Act 2005Effective 1 Jan 06Finance Act 200524 Nov. 05

Finance Act 2007Effective 1 January 08Finance Act 201209 June 2011

(b) in the case of a full-time employee or hisbeneficiaries (which expression includes a wholetime service director, or a director who controlsmore than five percent of the share capital orvoting power of a company) the value of anymedical services provided by the employer ormedical insurance provided by an insuranceprovider approved by the Commissioner ofInsurance and paid for by the employer on behalfof a full-time employee or his beneficiaries:

Provided that in the case of a director other than awhole time service director, the value of theservices shall be subject to such limit as theMinister may, from time to time prescribe.

__________________________

26

Finance Act 200213 June 02

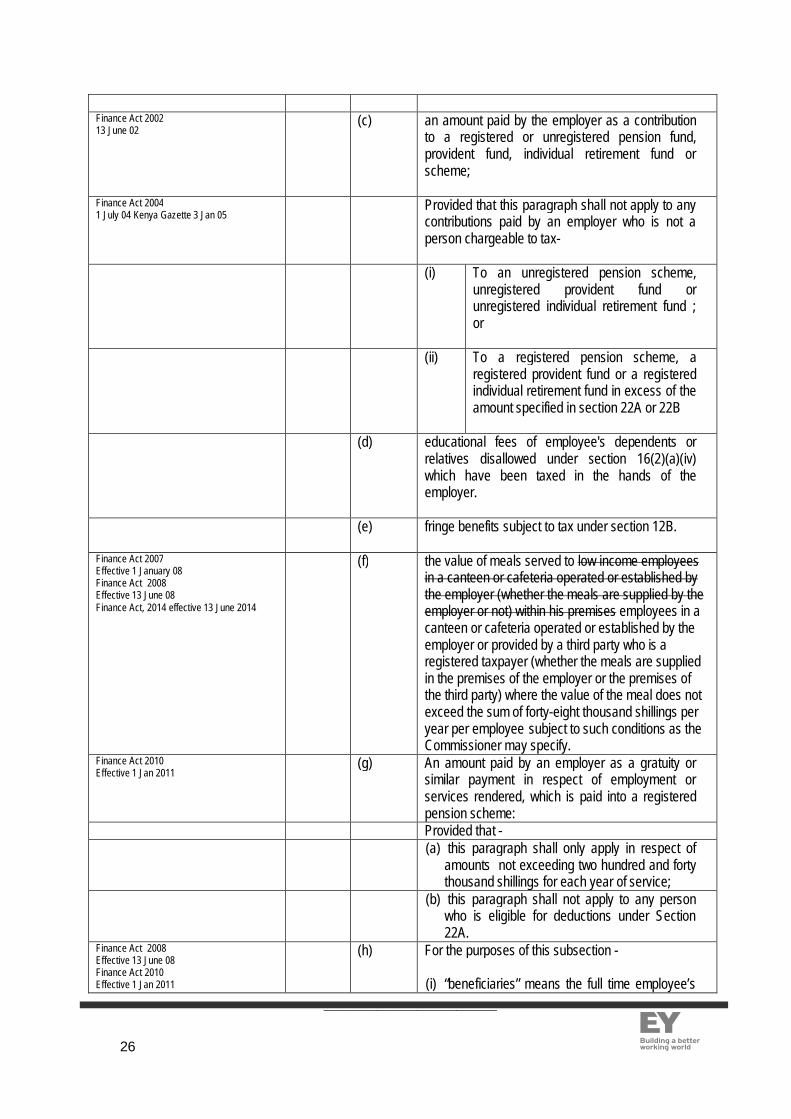

(c) an amount paid by the employer as a contributionto a registered or unregistered pension fund,provident fund, individual retirement fund orscheme;

Finance Act 20041 July 04 Kenya Gazette 3 Jan 05

Provided that this paragraph shall not apply to anycontributions paid by an employer who is not aperson chargeable to tax-

(i) To an unregistered pension scheme,unregistered provident fund orunregistered individual retirement fund ;or

(ii) To a registered pension scheme, aregistered provident fund or a registeredindividual retirement fund in excess of theamount specified in section 22A or 22B

(d) educational fees of employee's dependents orrelatives disallowed under section 16(2)(a)(iv)which have been taxed in the hands of theemployer.

(e) fringe benefits subject to tax under section 12B.

Finance Act 2007Effective 1 January 08Finance Act 2008Effective 13 June 08Finance Act, 2014 effective 13 June 2014

(f) the value of meals served to low income employeesin a canteen or cafeteria operated or established bythe employer (whether the meals are supplied by theemployer or not) within his premises employees in acanteen or cafeteria operated or established by theemployer or provided by a third party who is aregistered taxpayer (whether the meals are suppliedin the premises of the employer or the premises ofthe third party) where the value of the meal does notexceed the sum of forty-eight thousand shillings peryear per employee subject to such conditions as theCommissioner may specify.

Finance Act 2010Effective 1 Jan 2011

(g) An amount paid by an employer as a gratuity orsimilar payment in respect of employment orservices rendered, which is paid into a registeredpension scheme:Provided that -(a) this paragraph shall only apply in respect of

amounts not exceeding two hundred and fortythousand shillings for each year of service;

(b) this paragraph shall not apply to any personwho is eligible for deductions under Section22A.

Finance Act 2008Effective 13 June 08Finance Act 2010Effective 1 Jan 2011

(h) For the purposes of this subsection -

(i) “beneficiaries” means the full time employee’s

__________________________

27

Finance Act 201209 June 2011Finance Act, 2014 effective 13 June 2014

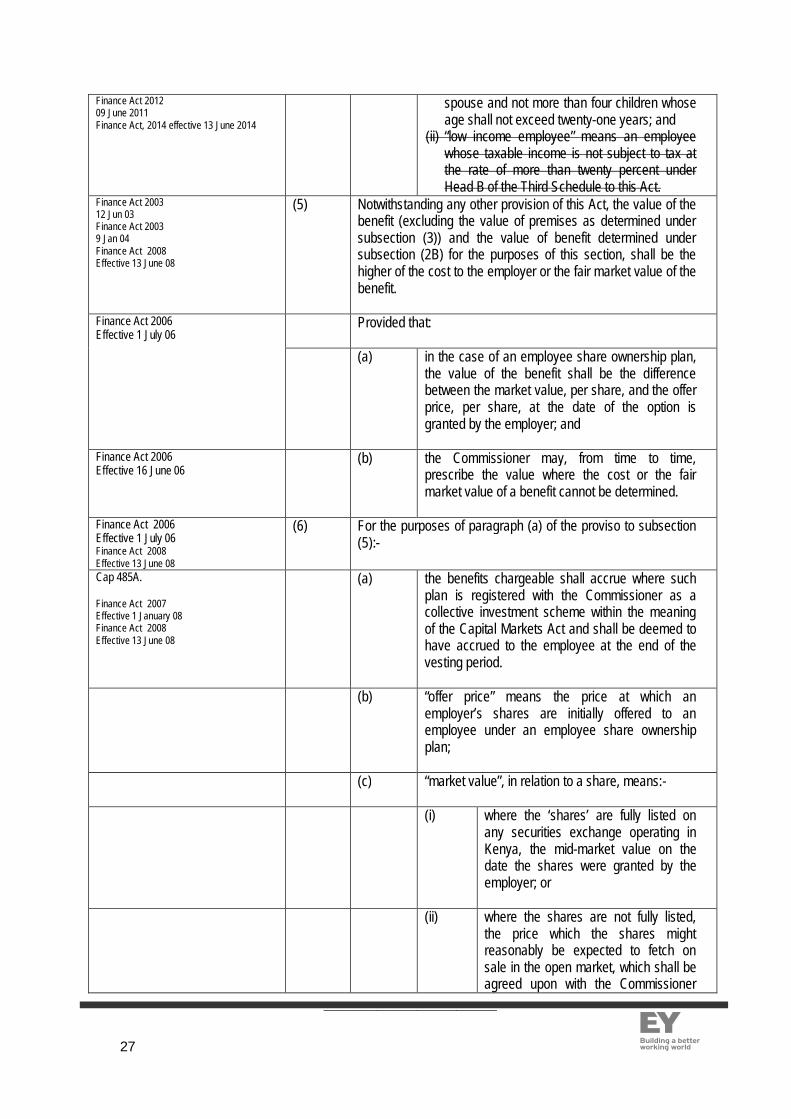

spouse and not more than four children whoseage shall not exceed twenty-one years; and

(ii) “low income employee” means an employeewhose taxable income is not subject to tax atthe rate of more than twenty percent underHead B of the Third Schedule to this Act.

Finance Act 200312 Jun 03Finance Act 20039 Jan 04Finance Act 2008Effective 13 June 08

(5) Notwithstanding any other provision of this Act, the value of thebenefit (excluding the value of premises as determined undersubsection (3)) and the value of benefit determined undersubsection (2B) for the purposes of this section, shall be thehigher of the cost to the employer or the fair market value of thebenefit.

Finance Act 2006Effective 1 July 06

Provided that:

(a) in the case of an employee share ownership plan,the value of the benefit shall be the differencebetween the market value, per share, and the offerprice, per share, at the date of the option isgranted by the employer; and

Finance Act 2006Effective 16 June 06

(b) the Commissioner may, from time to time,prescribe the value where the cost or the fairmarket value of a benefit cannot be determined.

Finance Act 2006Effective 1 July 06Finance Act 2008Effective 13 June 08

(6) For the purposes of paragraph (a) of the proviso to subsection(5):-

Cap 485A.

Finance Act 2007Effective 1 January 08Finance Act 2008Effective 13 June 08

(a) the benefits chargeable shall accrue where suchplan is registered with the Commissioner as acollective investment scheme within the meaningof the Capital Markets Act and shall be deemed tohave accrued to the employee at the end of thevesting period.

(b) “offer price” means the price at which anemployer’s shares are initially offered to anemployee under an employee share ownershipplan;

(c) “market value”, in relation to a share, means:-

(i) where the ‘shares’ are fully listed onany securities exchange operating inKenya, the mid-market value on thedate the shares were granted by theemployer; or

(ii) where the shares are not fully listed,the price which the shares mightreasonably be expected to fetch onsale in the open market, which shall beagreed upon with the Commissioner

__________________________

28

before the grant of the options;

(d) “share option” means the offer made by anemployer to an employee to purchase a fixednumber of shares at a fixed price, which may bepaid for at the end of the vesting period;

(e) “vesting period” means a fixed period of timebetween the date of offer by the employer and thedate after which the option to purchase can beexercised by the employee.

6. Income from the use ofproperty

(1) For the purposes of section 3 (2) (a) (iii), "gains or profits” includesroyalty, rent, premium or similar consideration received for the useor occupation of property.

(2) In the case of a lease or similar transaction, the income of a lessorshall be determined in accordance with such rules as may beprescribed under this Act.

6A. Imposition of residentialrental Income Tax.

Finance Act, 2015 effective 1st Jan 2016

Finance Act, 2016 effective 09 June 2016

(1) Notwithstanding any other provision of this Act, a tax to be knownas residential rental income tax shall be payable with effect fromthe 1st January, 2016 by any resident person from income whichis accrued in or derived from Kenya for the use or occupation ofresidential property, and which does not exceed is in excess ofone hundred and forty four thousand shillings but does notexceed ten million shillings during any year of income.Provided that this section shall not apply where a person whowould otherwise pay tax under this section, by notice in writingaddressed to the Commissioner, elects not to be subject toresidential rental income tax, in which case the other provisions ofthis Act shall apply to such a person.

(2) The Minister may, by notice in the Gazette, prescribe regulationsfor the better carrying out the provisions of this section.

7. Income from dividends2 of 1975, s, 5,