lbh 2.8% value 1 quantitative stock selection … · tfg 3.1% value avi 3.1% quality gln 3.0%...

TRANSCRIPT

09 March 2017

The disclaimer is available at the end of this document, and on our website: http://www.afrifocus.co.za

QUANTITATIVE STOCK SELECTION AND TOP 40 GUIDE

Afrifocus is a level 1 contributor with a BEE procurement level of 135%, and a registered member of JSE

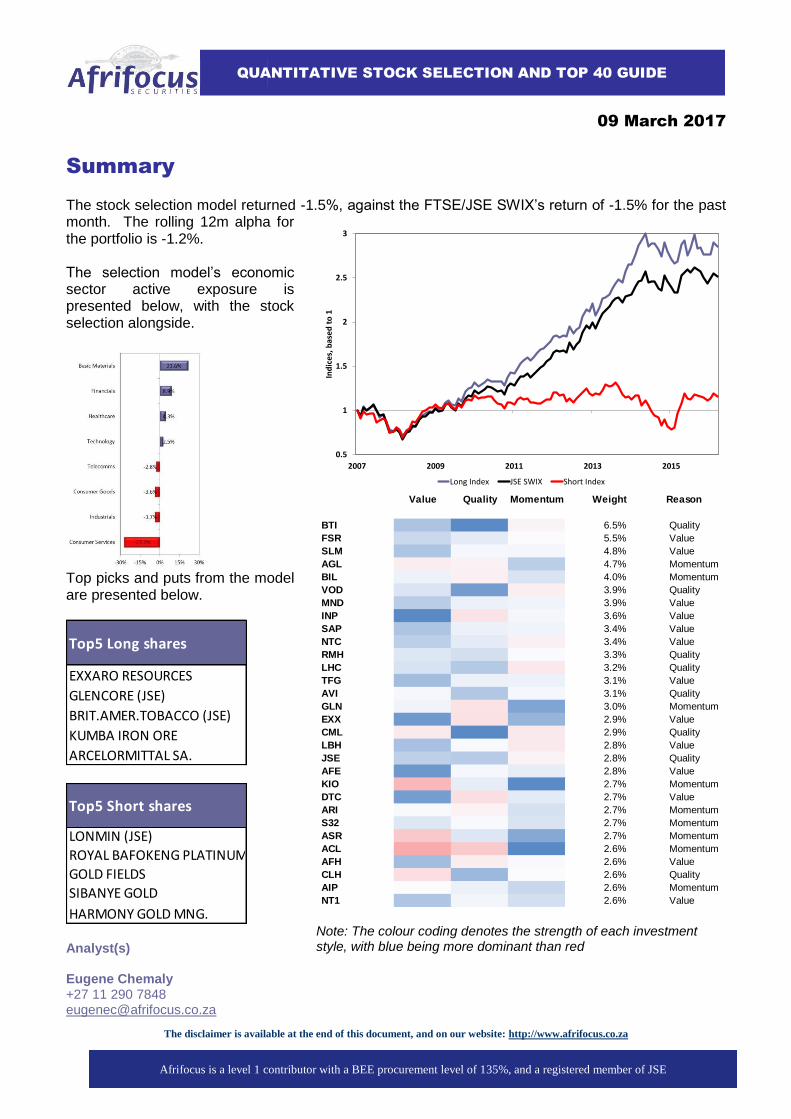

Note: The colour coding denotes the strength of each investment style, with blue being more dominant than red

0.5

1

1.5

2

2.5

3

2007 2009 2011 2013 2015

Ind

ice

s, b

ase

d t

o 1

Long Index JSE SWIX Short Index

Value Quality Momentum Weight Reason

BTI 6.5% Quality

FSR 5.5% Value

SLM 4.8% Value

AGL 4.7% Momentum

BIL 4.0% Momentum

VOD 3.9% Quality

MND 3.9% Value

INP 3.6% Value

SAP 3.4% Value

NTC 3.4% Value

RMH 3.3% Quality

LHC 3.2% Quality

TFG 3.1% Value

AVI 3.1% Quality

GLN 3.0% Momentum

EXX 2.9% Value

CML 2.9% Quality

LBH 2.8% Value

JSE 2.8% Quality

AFE 2.8% Value

KIO 2.7% Momentum

DTC 2.7% Value

ARI 2.7% Momentum

S32 2.7% Momentum

ASR 2.7% Momentum

ACL 2.6% Momentum

AFH 2.6% Value

CLH 2.6% Quality

AIP 2.6% Momentum

NT1 2.6% Value

Summary The stock selection model returned -1.5%, against the FTSE/JSE SWIX’s return of -1.5% for the past month. The rolling 12m alpha for the portfolio is -1.2%. The selection model’s economic sector active exposure is presented below, with the stock selection alongside.

Top picks and puts from the model are presented below.

Analyst(s) Eugene Chemaly +27 11 290 7848 [email protected]

Top5 Long shares

EXXARO RESOURCES

GLENCORE (JSE)

BRIT.AMER.TOBACCO (JSE)

KUMBA IRON ORE

ARCELORMITTAL SA.

Top5 Short shares

LONMIN (JSE)

ROYAL BAFOKENG PLATINUM

GOLD FIELDS

SIBANYE GOLD

HARMONY GOLD MNG.

1

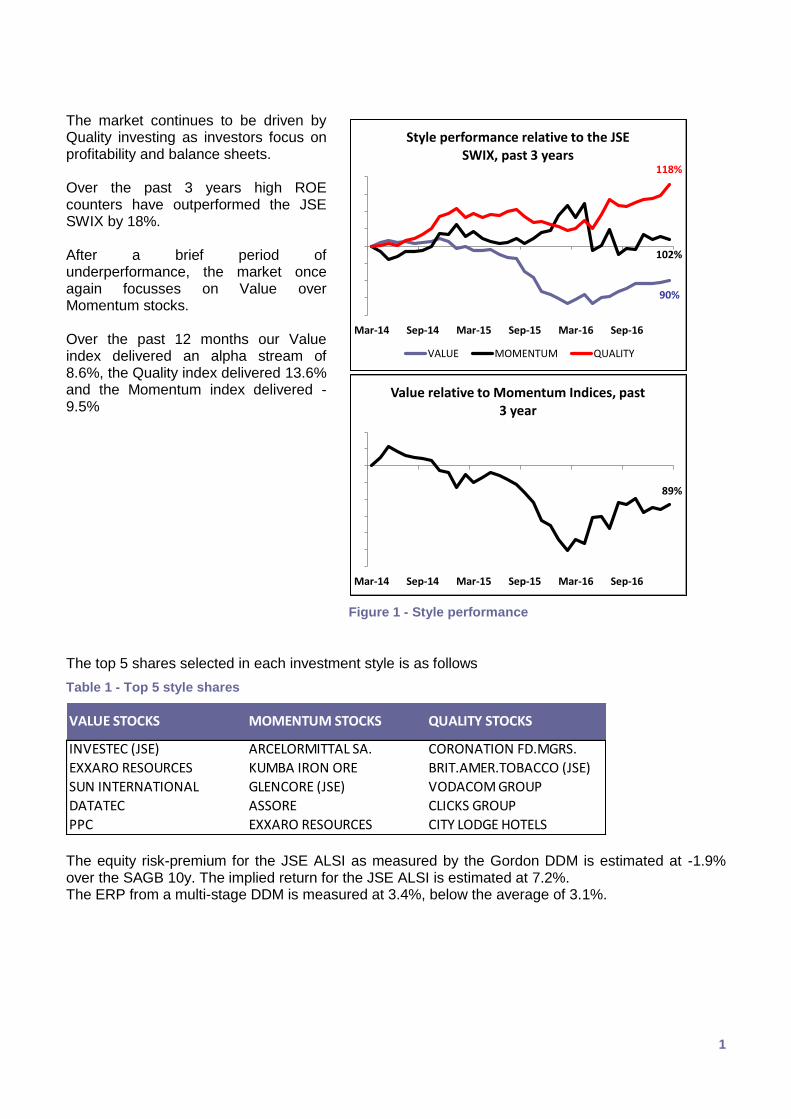

Figure 1 - Style performance

90%

102%

118%

Mar-14 Sep-14 Mar-15 Sep-15 Mar-16 Sep-16

Style performance relative to the JSE SWIX, past 3 years

VALUE MOMENTUM QUALITY

89%

Mar-14 Sep-14 Mar-15 Sep-15 Mar-16 Sep-16

Value relative to Momentum Indices, past 3 year

The market continues to be driven by Quality investing as investors focus on profitability and balance sheets. Over the past 3 years high ROE counters have outperformed the JSE SWIX by 18%. After a brief period of underperformance, the market once again focusses on Value over Momentum stocks. Over the past 12 months our Value index delivered an alpha stream of 8.6%, the Quality index delivered 13.6% and the Momentum index delivered -9.5%

The top 5 shares selected in each investment style is as follows

Table 1 - Top 5 style shares

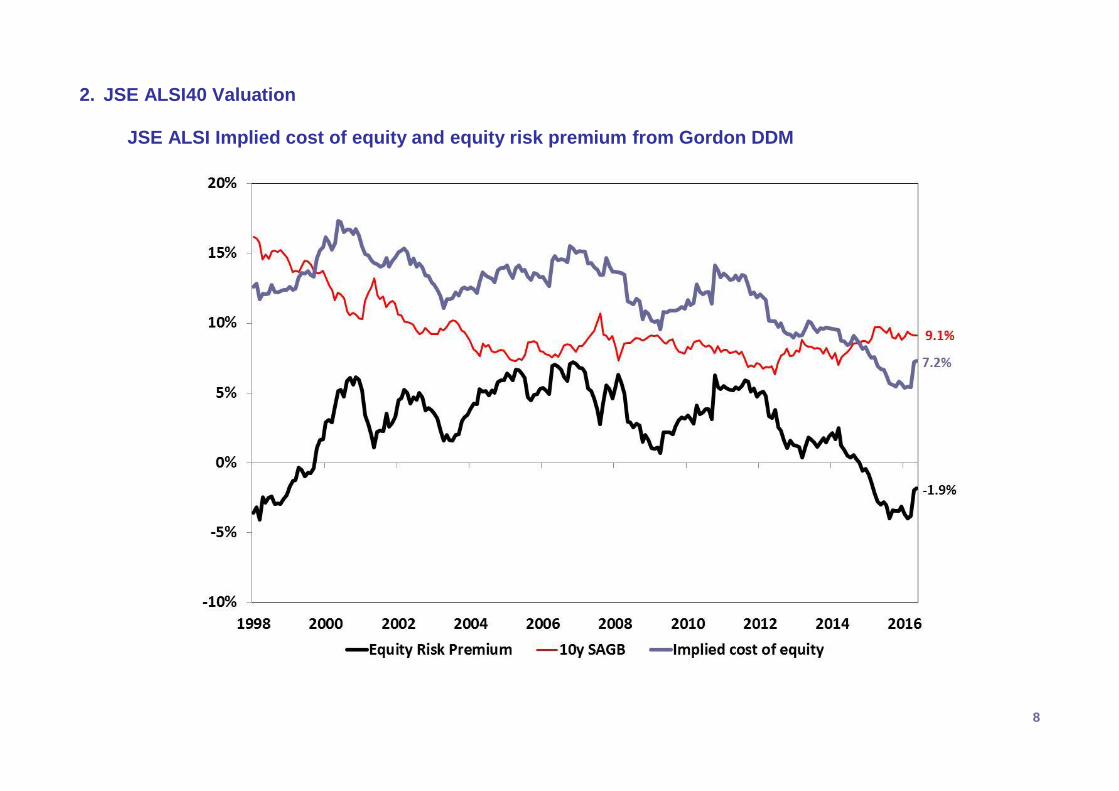

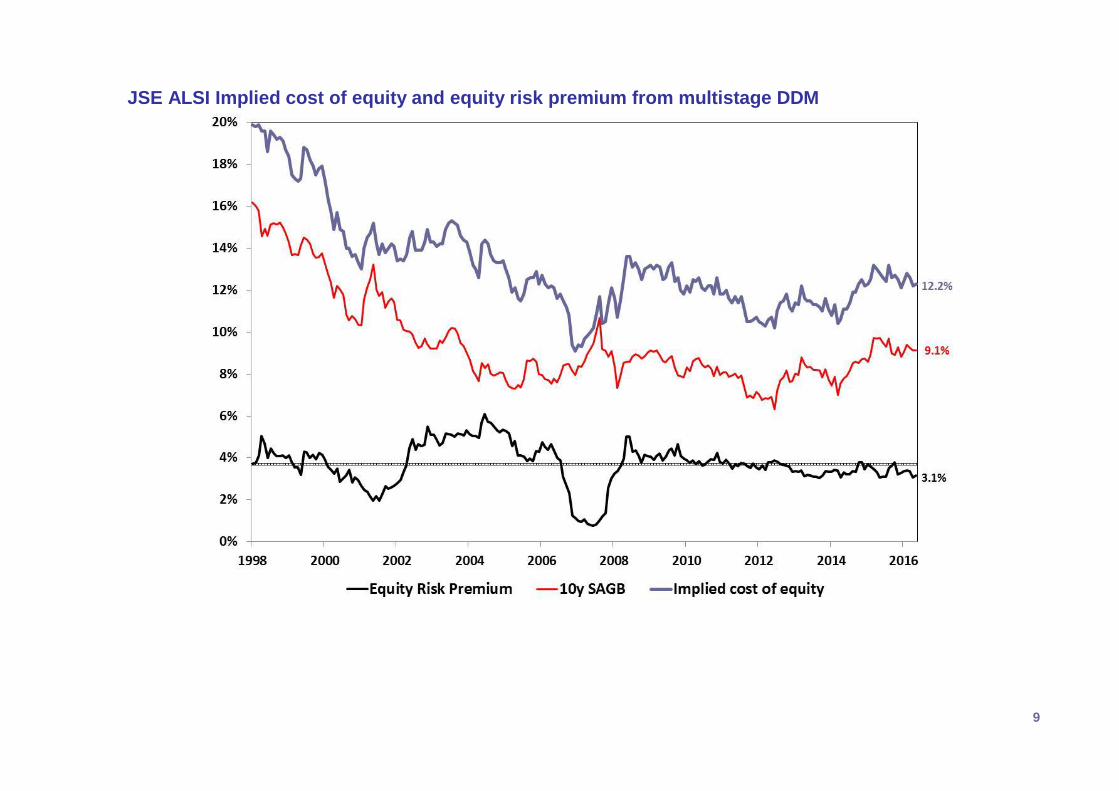

The equity risk-premium for the JSE ALSI as measured by the Gordon DDM is estimated at -1.9% over the SAGB 10y. The implied return for the JSE ALSI is estimated at 7.2%. The ERP from a multi-stage DDM is measured at 3.4%, below the average of 3.1%.

VALUE STOCKS MOMENTUM STOCKS QUALITY STOCKS

INVESTEC (JSE) ARCELORMITTAL SA. CORONATION FD.MGRS.

EXXARO RESOURCES KUMBA IRON ORE BRIT.AMER.TOBACCO (JSE)

SUN INTERNATIONAL GLENCORE (JSE) VODACOM GROUP

DATATEC ASSORE CLICKS GROUP

PPC EXXARO RESOURCES CITY LODGE HOTELS

2

Contents Page

1. Quantitative Stock Selection p.3

2. JSE ALSI40 Valuation p.8 JSE ALSI Implied cost of equity and equity risk premium P/NAV vs ROE plot PE vs 2year forecast EPS growth plot Dividend Yield vs 2year dividend growth plot Forward Ratings – PE, DYld, P/NAV, 2yCAGR, PEG Forward relative ratings – StdDev’s from mean

3. Top 40 Company Summary p.15

3

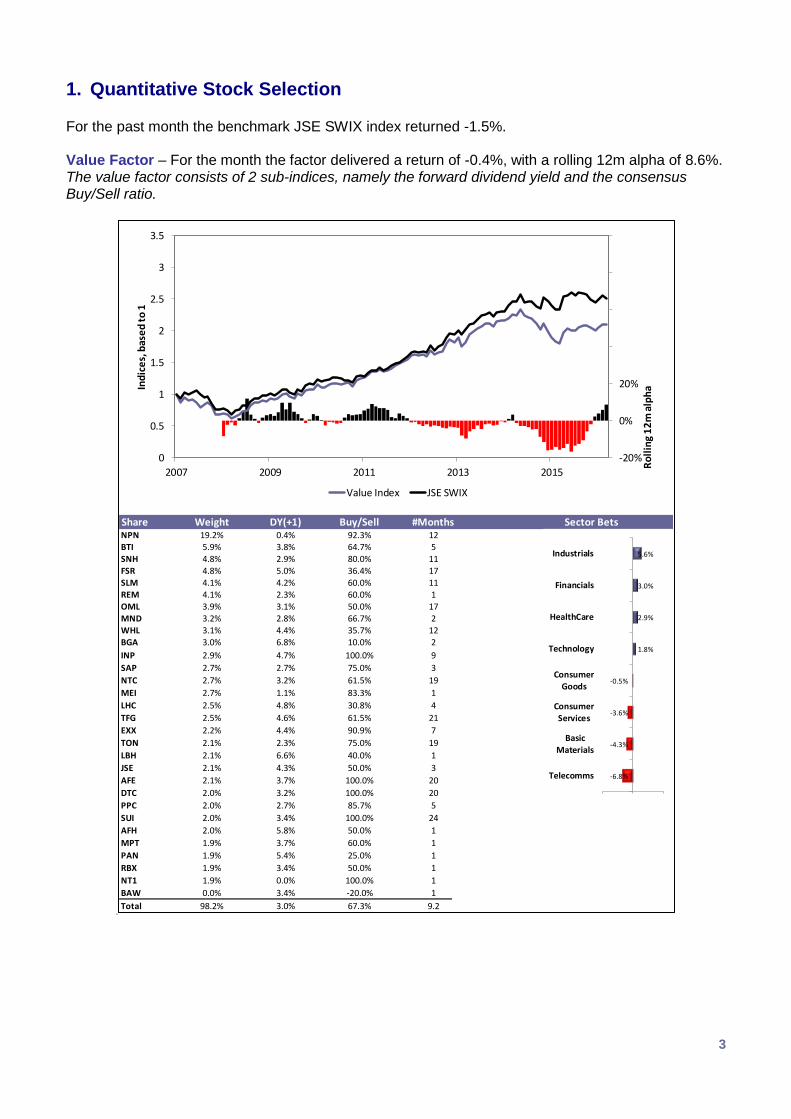

1. Quantitative Stock Selection For the past month the benchmark JSE SWIX index returned -1.5%. Value Factor – For the month the factor delivered a return of -0.4%, with a rolling 12m alpha of 8.6%. The value factor consists of 2 sub-indices, namely the forward dividend yield and the consensus Buy/Sell ratio.

Share Weight DY(+1) Buy/Sell #Months Sector BetsNPN 19.1% 0.4% 0.0% 11BTI 6.0% 3.8% 0.0% 4MTN 5.6% 6.3% 0.0% 78SNH 5.0% 3.3% 0.0% 10FSR 4.6% 5.0% 0.0% 16SLM 3.8% 4.3% 0.0% 10OML 3.8% 3.2% 0.0% 16MND 3.1% 2.9% 0.0% 1WHL 3.1% 4.5% 0.0% 11BGA 3.0% 6.7% 0.0% 1INP 2.9% 4.6% 0.0% 8NTC 2.7% 3.1% 0.0% 18SAP 2.6% 2.7% 0.0% 2RMH 2.6% 5.1% 0.0% 17LHC 2.4% 4.8% 0.0% 3TFG 2.4% 4.8% 0.0% 20EXX 2.1% 4.3% 0.0% 6TON 2.1% 2.9% 0.0% 18JSE 2.1% 4.5% 0.0% 2AFE 2.0% 3.8% NaN 19DTC 2.0% 3.4% 0.0% 19SUI 2.0% 3.1% 0.0% 23PPC 2.0% 2.3% 0.0% 4GND 1.9% 1.1% 0.0% 7AFH 1.9% 5.6% 0.0% 1MPT 1.9% 3.7% 0.0% 1RBX 1.9% 3.6% 0.0% 1GRF 1.8% 3.1% 0.0% 1NT1 1.8% 0.0% 0.0% 1PAN 0.0% 5.6% 0.0% 1Total 98.2% 3.2% 0.0% 13.2

-20%0%20%40%60%80%100%

00.511.522.533.5

2007 2009 2011 2013 2015 Rolling 12m alphaIndices, based to 1

Value Index JSE SWIX

-15% 0% 15%BasicMaterialsConsumerServicesTelecommsConsumerGoodsHealthCareTechnologyFinancialsIndustrials

Share Weight DY(+1) Buy/Sell #Months Sector BetsNPN 19.2% 0.4% 92.3% 12BTI 5.9% 3.8% 64.7% 5

SNH 4.8% 2.9% 80.0% 11FSR 4.8% 5.0% 36.4% 17

SLM 4.1% 4.2% 60.0% 11REM 4.1% 2.3% 60.0% 1

OML 3.9% 3.1% 50.0% 17MND 3.2% 2.8% 66.7% 2

WHL 3.1% 4.4% 35.7% 12BGA 3.0% 6.8% 10.0% 2

INP 2.9% 4.7% 100.0% 9

SAP 2.7% 2.7% 75.0% 3

NTC 2.7% 3.2% 61.5% 19

MEI 2.7% 1.1% 83.3% 1

LHC 2.5% 4.8% 30.8% 4

TFG 2.5% 4.6% 61.5% 21

EXX 2.2% 4.4% 90.9% 7

TON 2.1% 2.3% 75.0% 19

LBH 2.1% 6.6% 40.0% 1

JSE 2.1% 4.3% 50.0% 3

AFE 2.1% 3.7% 100.0% 20

DTC 2.0% 3.2% 100.0% 20

PPC 2.0% 2.7% 85.7% 5

SUI 2.0% 3.4% 100.0% 24

AFH 2.0% 5.8% 50.0% 1

MPT 1.9% 3.7% 60.0% 1

PAN 1.9% 5.4% 25.0% 1

RBX 1.9% 3.4% 50.0% 1

NT1 1.9% 0.0% 100.0% 1

BAW 0.0% 3.4% -20.0% 1

Total 98.2% 3.0% 67.3% 9.2

-20%

0%

20%

40%

60%

80%

100%

0

0.5

1

1.5

2

2.5

3

3.5

2007 2009 2011 2013 2015

Ro

llin

g 1

2m

alp

haIn

dic

es,

bas

ed

to

1

Value Index JSE SWIX

-6.8%

-4.3%

-3.6%

-0.5%

1.8%

2.9%

3.0%

5.6%

Telecomms

Basic

Materials

ConsumerServices

ConsumerGoods

Technology

HealthCare

Financials

Industrials

4

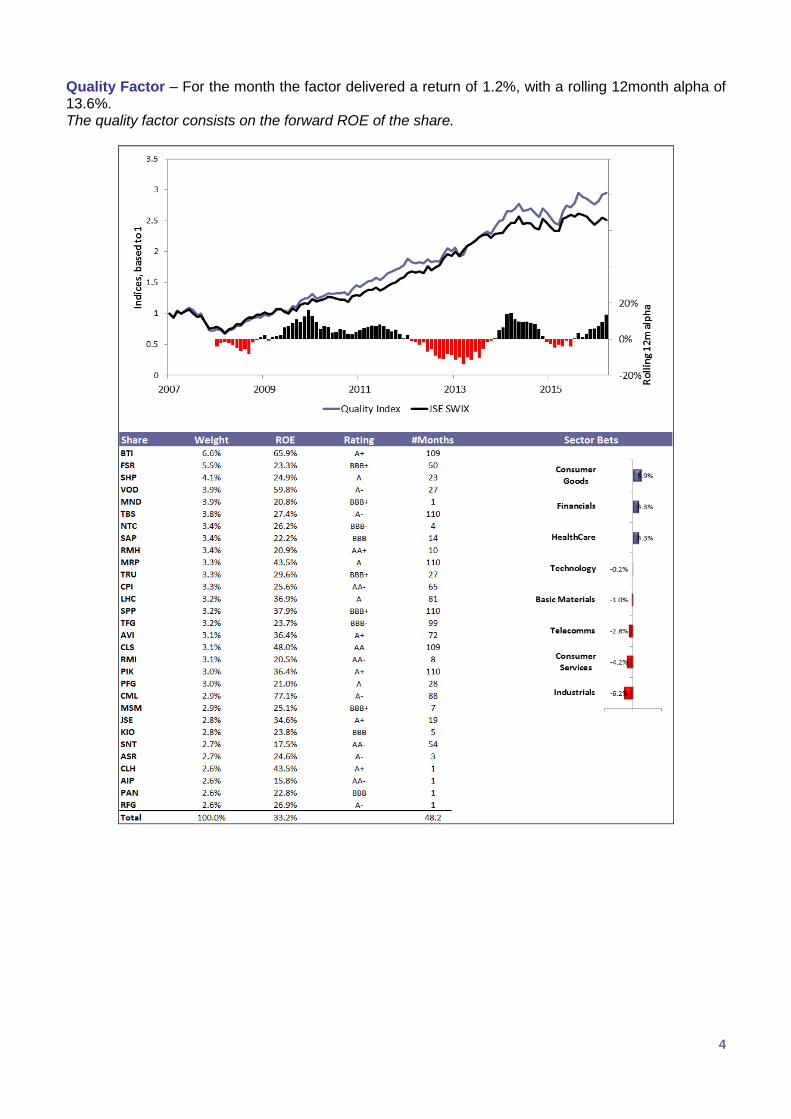

Quality Factor – For the month the factor delivered a return of 1.2%, with a rolling 12month alpha of 13.6%. The quality factor consists on the forward ROE of the share.

5

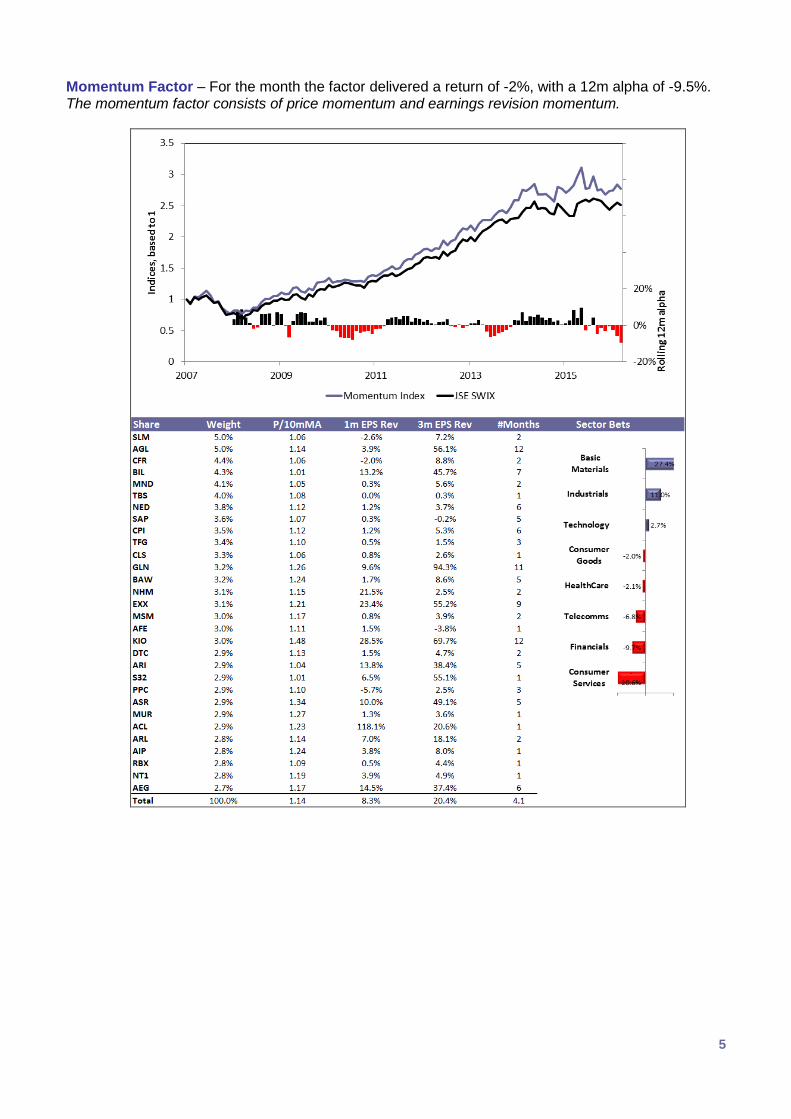

Momentum Factor – For the month the factor delivered a return of -2%, with a 12m alpha of -9.5%. The momentum factor consists of price momentum and earnings revision momentum.

6

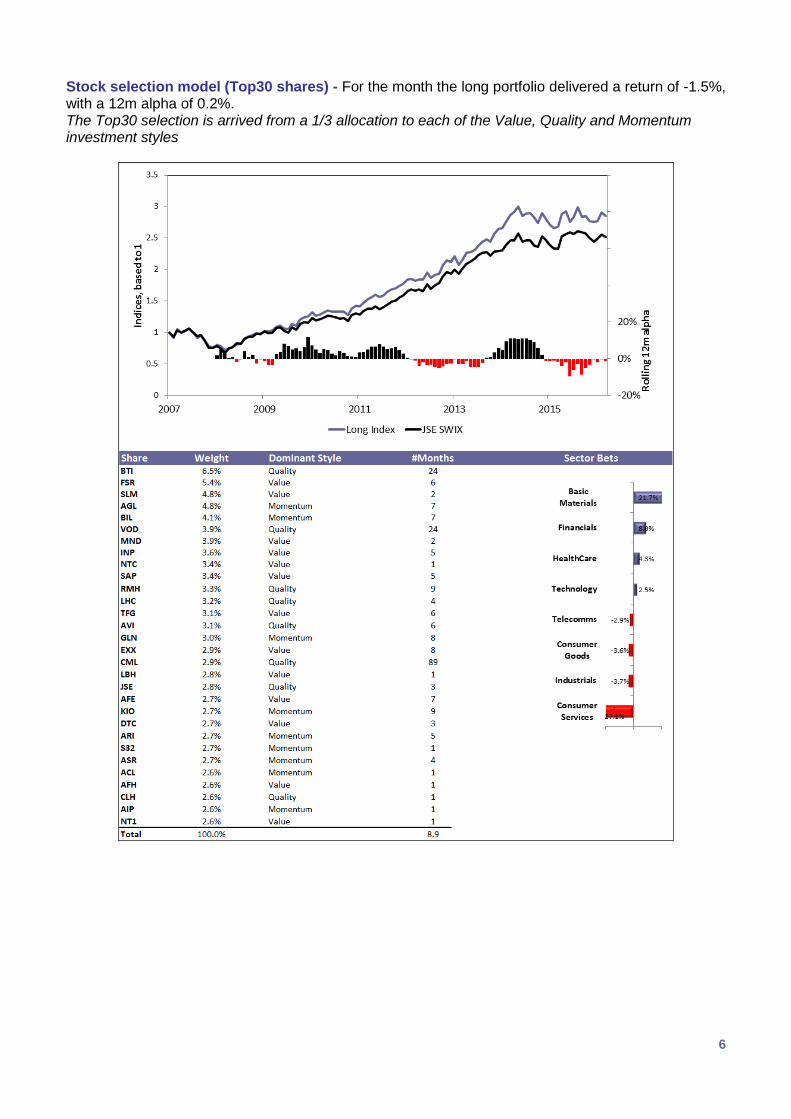

Stock selection model (Top30 shares) - For the month the long portfolio delivered a return of -1.5%, with a 12m alpha of 0.2%. The Top30 selection is arrived from a 1/3 allocation to each of the Value, Quality and Momentum investment styles

7

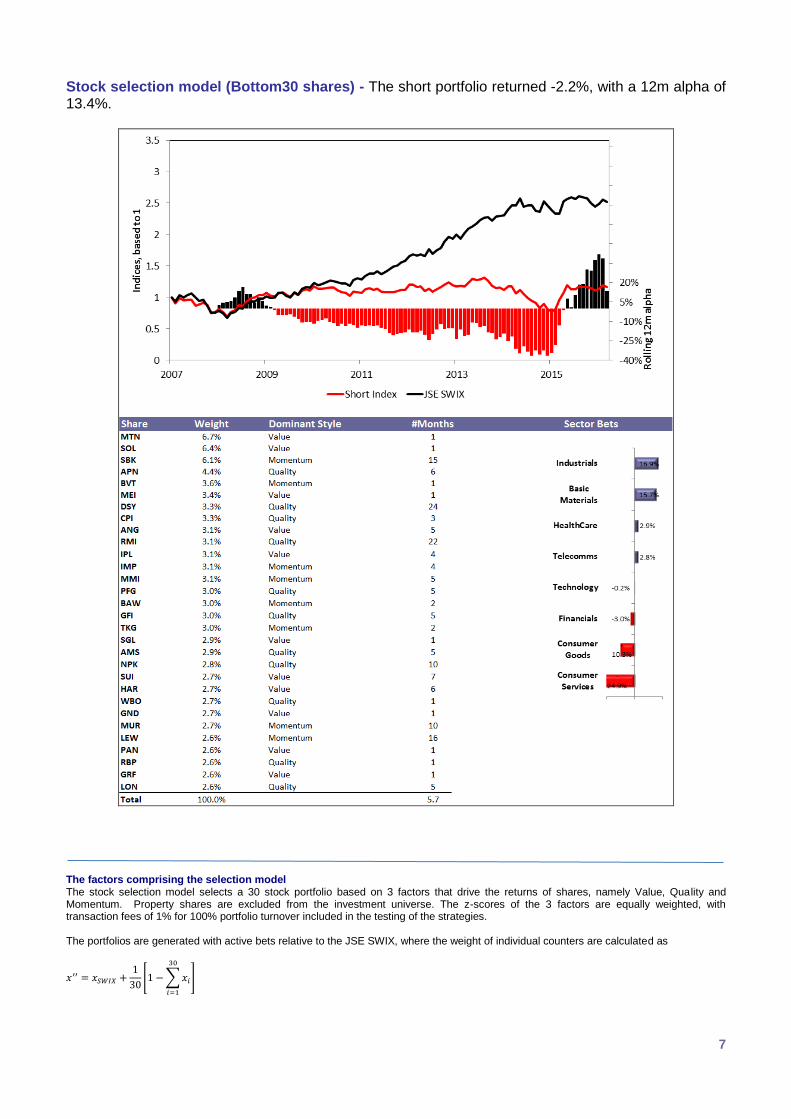

Stock selection model (Bottom30 shares) - The short portfolio returned -2.2%, with a 12m alpha of 13.4%.

The factors comprising the selection model The stock selection model selects a 30 stock portfolio based on 3 factors that drive the returns of shares, namely Value, Quality and Momentum. Property shares are excluded from the investment universe. The z-scores of the 3 factors are equally weighted, with transaction fees of 1% for 100% portfolio turnover included in the testing of the strategies. The portfolios are generated with active bets relative to the JSE SWIX, where the weight of individual counters are calculated as

𝑥′′ = 𝑥𝑆𝑊𝐼𝑋 +1

30[1 −∑𝑥𝑖

30

𝑖=1

]

8

2. JSE ALSI40 Valuation

JSE ALSI Implied cost of equity and equity risk premium from Gordon DDM

9

JSE ALSI Implied cost of equity and equity risk premium from multistage DDM

10

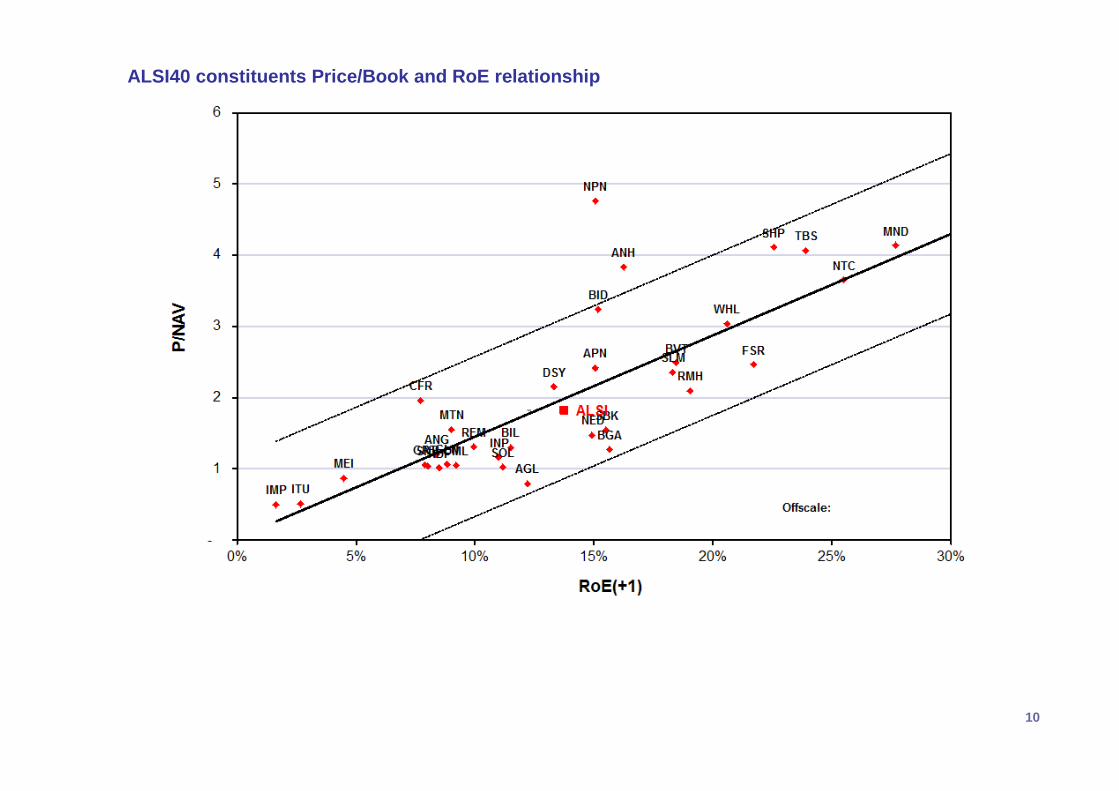

ALSI40 constituents Price/Book and RoE relationship

11

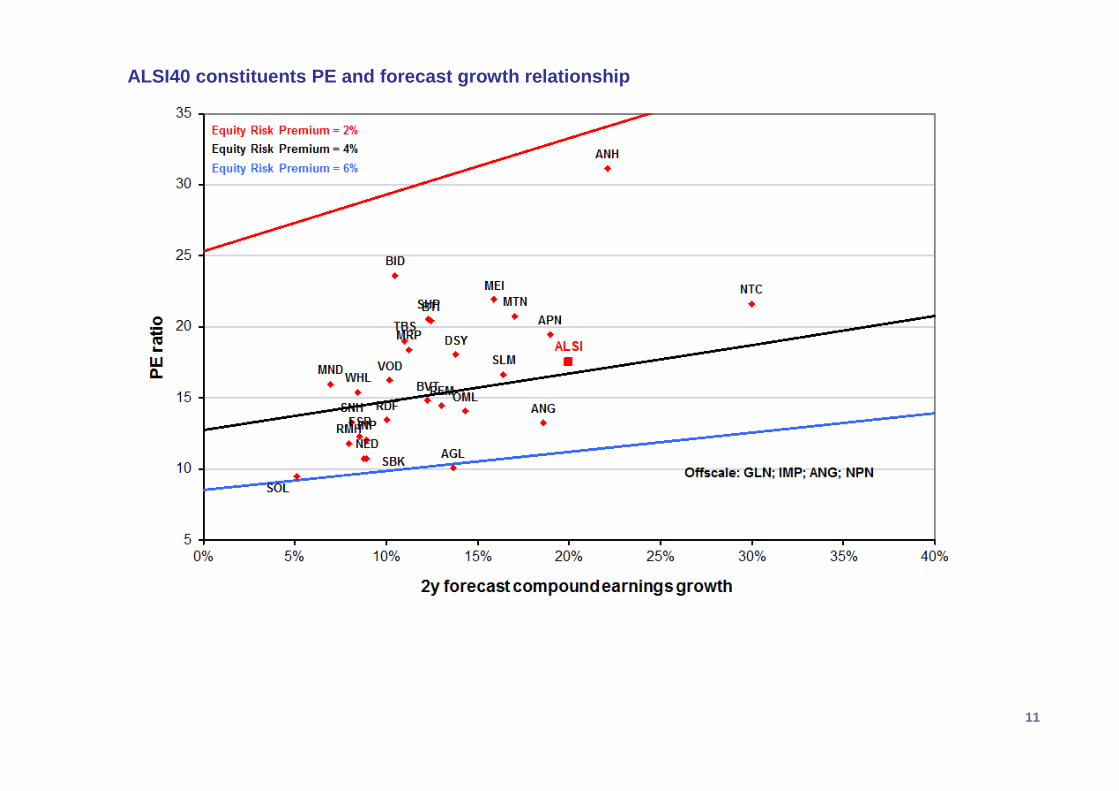

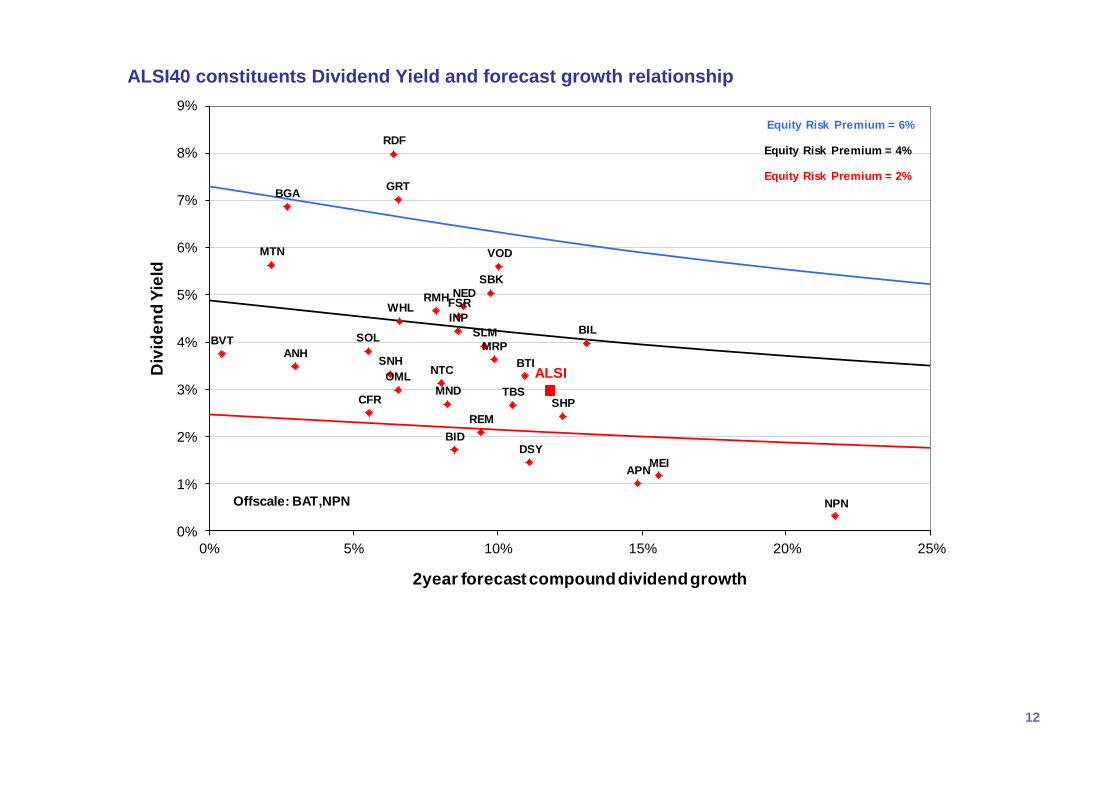

ALSI40 constituents PE and forecast growth relationship

12

ALSI40 constituents Dividend Yield and forecast growth relationship

ANH

APN

BGA

BID

BIL

BTI

BVT

CFR

DSY

FSR

GRT

INP

MEI

MND

MRP

MTN

NED

NPN

NTCOML

RDF

REM

RMH

SBK

SHP

SLM

SNH

SOL

TBS

VOD

WHL

ALSI

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

0% 5% 10% 15% 20% 25%

Div

ide

nd

Yie

ld

2year forecast compound dividend growth

Equity Risk Premium = 2%

Equity Risk Premium = 4%

Equity Risk Premium = 6%

Offscale: BAT,NPN

13

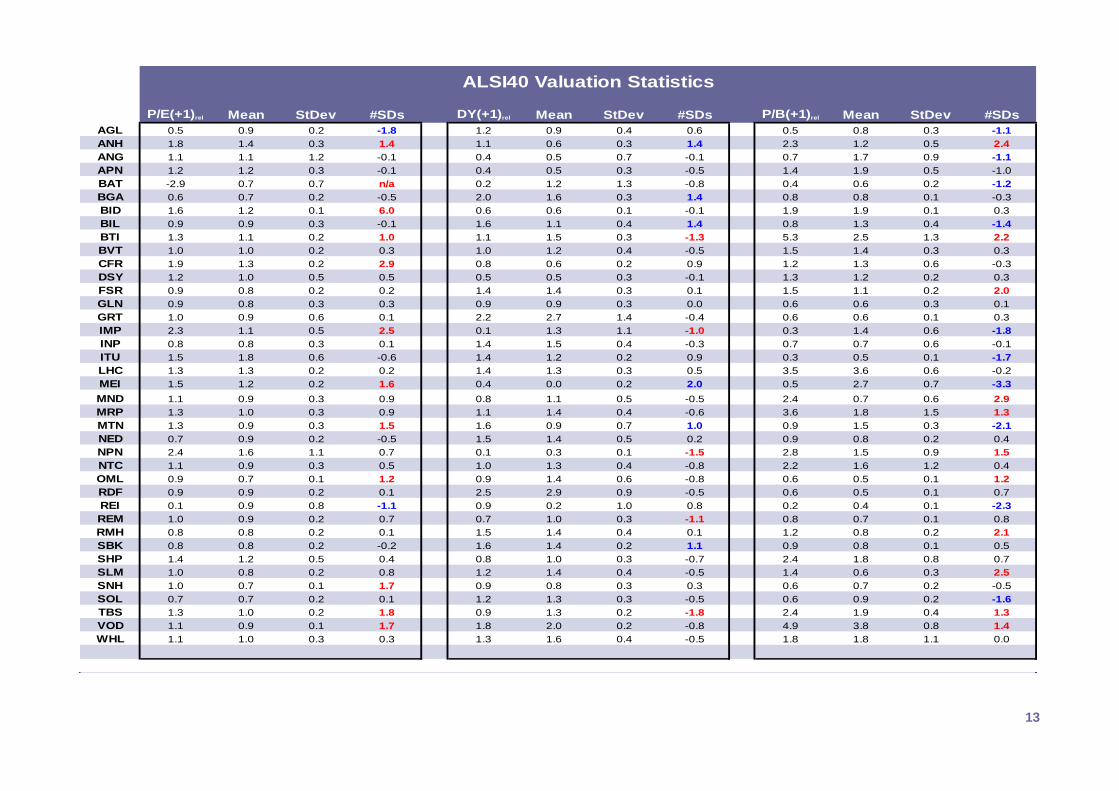

P/E(+1)rel Mean StDev #SDs DY(+1)rel Mean StDev #SDs P/B(+1)rel Mean StDev #SDs

AGL 0.5 0.9 0.2 -1.8 1.2 0.9 0.4 0.6 0.5 0.8 0.3 -1.1

ANH 1.8 1.4 0.3 1.4 1.1 0.6 0.3 1.4 2.3 1.2 0.5 2.4

ANG 1.1 1.1 1.2 -0.1 0.4 0.5 0.7 -0.1 0.7 1.7 0.9 -1.1

APN 1.2 1.2 0.3 -0.1 0.4 0.5 0.3 -0.5 1.4 1.9 0.5 -1.0

BAT -2.9 0.7 0.7 n/a 0.2 1.2 1.3 -0.8 0.4 0.6 0.2 -1.2

BGA 0.6 0.7 0.2 -0.5 2.0 1.6 0.3 1.4 0.8 0.8 0.1 -0.3

BID 1.6 1.2 0.1 6.0 0.6 0.6 0.1 -0.1 1.9 1.9 0.1 0.3

BIL 0.9 0.9 0.3 -0.1 1.6 1.1 0.4 1.4 0.8 1.3 0.4 -1.4

BTI 1.3 1.1 0.2 1.0 1.1 1.5 0.3 -1.3 5.3 2.5 1.3 2.2

BVT 1.0 1.0 0.2 0.3 1.0 1.2 0.4 -0.5 1.5 1.4 0.3 0.3

CFR 1.9 1.3 0.2 2.9 0.8 0.6 0.2 0.9 1.2 1.3 0.6 -0.3

DSY 1.2 1.0 0.5 0.5 0.5 0.5 0.3 -0.1 1.3 1.2 0.2 0.3

FSR 0.9 0.8 0.2 0.2 1.4 1.4 0.3 0.1 1.5 1.1 0.2 2.0

GLN 0.9 0.8 0.3 0.3 0.9 0.9 0.3 0.0 0.6 0.6 0.3 0.1

GRT 1.0 0.9 0.6 0.1 2.2 2.7 1.4 -0.4 0.6 0.6 0.1 0.3

IMP 2.3 1.1 0.5 2.5 0.1 1.3 1.1 -1.0 0.3 1.4 0.6 -1.8

INP 0.8 0.8 0.3 0.1 1.4 1.5 0.4 -0.3 0.7 0.7 0.6 -0.1

ITU 1.5 1.8 0.6 -0.6 1.4 1.2 0.2 0.9 0.3 0.5 0.1 -1.7

LHC 1.3 1.3 0.2 0.2 1.4 1.3 0.3 0.5 3.5 3.6 0.6 -0.2

MEI 1.5 1.2 0.2 1.6 0.4 0.0 0.2 2.0 0.5 2.7 0.7 -3.3

MND 1.1 0.9 0.3 0.9 0.8 1.1 0.5 -0.5 2.4 0.7 0.6 2.9

MRP 1.3 1.0 0.3 0.9 1.1 1.4 0.4 -0.6 3.6 1.8 1.5 1.3

MTN 1.3 0.9 0.3 1.5 1.6 0.9 0.7 1.0 0.9 1.5 0.3 -2.1

NED 0.7 0.9 0.2 -0.5 1.5 1.4 0.5 0.2 0.9 0.8 0.2 0.4

NPN 2.4 1.6 1.1 0.7 0.1 0.3 0.1 -1.5 2.8 1.5 0.9 1.5

NTC 1.1 0.9 0.3 0.5 1.0 1.3 0.4 -0.8 2.2 1.6 1.2 0.4

OML 0.9 0.7 0.1 1.2 0.9 1.4 0.6 -0.8 0.6 0.5 0.1 1.2

RDF 0.9 0.9 0.2 0.1 2.5 2.9 0.9 -0.5 0.6 0.5 0.1 0.7

REI 0.1 0.9 0.8 -1.1 0.9 0.2 1.0 0.8 0.2 0.4 0.1 -2.3

REM 1.0 0.9 0.2 0.7 0.7 1.0 0.3 -1.1 0.8 0.7 0.1 0.8

RMH 0.8 0.8 0.2 0.1 1.5 1.4 0.4 0.1 1.2 0.8 0.2 2.1

SBK 0.8 0.8 0.2 -0.2 1.6 1.4 0.2 1.1 0.9 0.8 0.1 0.5

SHP 1.4 1.2 0.5 0.4 0.8 1.0 0.3 -0.7 2.4 1.8 0.8 0.7

SLM 1.0 0.8 0.2 0.8 1.2 1.4 0.4 -0.5 1.4 0.6 0.3 2.5

SNH 1.0 0.7 0.1 1.7 0.9 0.8 0.3 0.3 0.6 0.7 0.2 -0.5

SOL 0.7 0.7 0.2 0.1 1.2 1.3 0.3 -0.5 0.6 0.9 0.2 -1.6

TBS 1.3 1.0 0.2 1.8 0.9 1.3 0.2 -1.8 2.4 1.9 0.4 1.3

VOD 1.1 0.9 0.1 1.7 1.8 2.0 0.2 -0.8 4.9 3.8 0.8 1.4

WHL 1.1 1.0 0.3 0.3 1.3 1.6 0.4 -0.5 1.8 1.8 1.1 0.0

ALSI40 Valuation Statistics

14

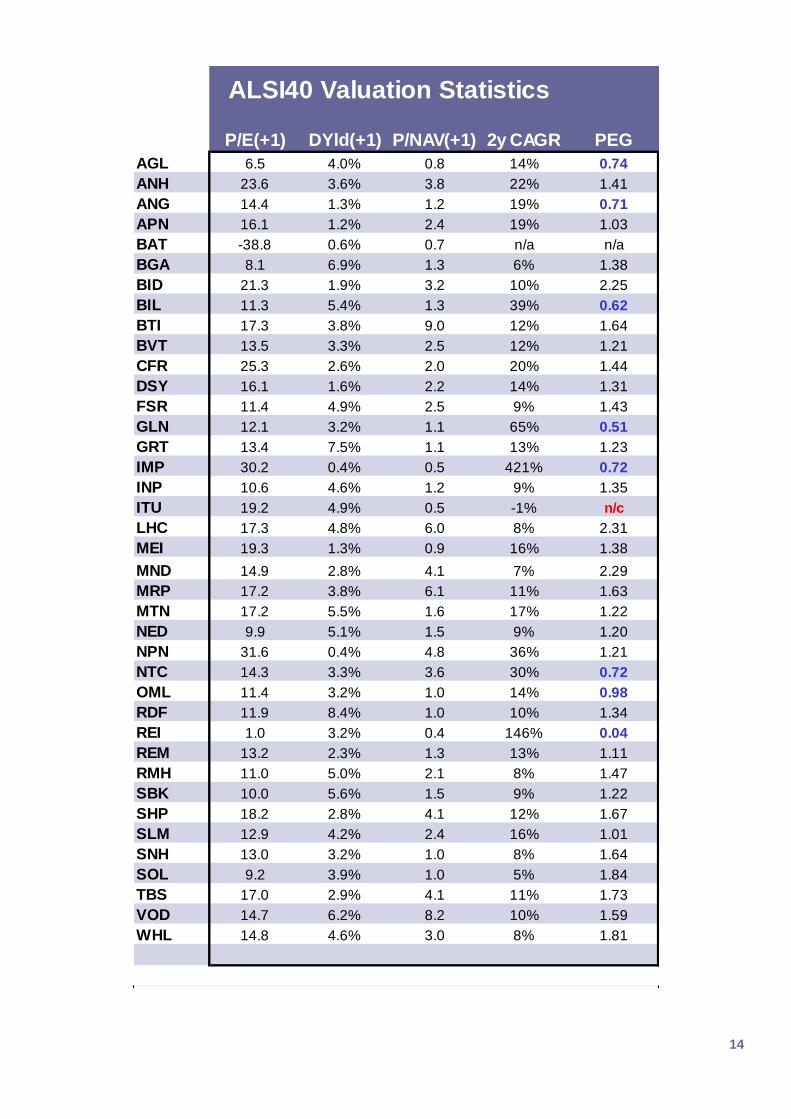

P/E(+1) DYld(+1) P/NAV(+1) 2y CAGR PEG

AGL 6.5 4.0% 0.8 14% 0.74

ANH 23.6 3.6% 3.8 22% 1.41

ANG 14.4 1.3% 1.2 19% 0.71

APN 16.1 1.2% 2.4 19% 1.03

BAT -38.8 0.6% 0.7 n/a n/a

BGA 8.1 6.9% 1.3 6% 1.38

BID 21.3 1.9% 3.2 10% 2.25

BIL 11.3 5.4% 1.3 39% 0.62

BTI 17.3 3.8% 9.0 12% 1.64

BVT 13.5 3.3% 2.5 12% 1.21

CFR 25.3 2.6% 2.0 20% 1.44

DSY 16.1 1.6% 2.2 14% 1.31

FSR 11.4 4.9% 2.5 9% 1.43

GLN 12.1 3.2% 1.1 65% 0.51

GRT 13.4 7.5% 1.1 13% 1.23

IMP 30.2 0.4% 0.5 421% 0.72

INP 10.6 4.6% 1.2 9% 1.35

ITU 19.2 4.9% 0.5 -1% n/c

LHC 17.3 4.8% 6.0 8% 2.31

MEI 19.3 1.3% 0.9 16% 1.38

MND 14.9 2.8% 4.1 7% 2.29

MRP 17.2 3.8% 6.1 11% 1.63

MTN 17.2 5.5% 1.6 17% 1.22

NED 9.9 5.1% 1.5 9% 1.20

NPN 31.6 0.4% 4.8 36% 1.21

NTC 14.3 3.3% 3.6 30% 0.72

OML 11.4 3.2% 1.0 14% 0.98

RDF 11.9 8.4% 1.0 10% 1.34

REI 1.0 3.2% 0.4 146% 0.04

REM 13.2 2.3% 1.3 13% 1.11

RMH 11.0 5.0% 2.1 8% 1.47

SBK 10.0 5.6% 1.5 9% 1.22

SHP 18.2 2.8% 4.1 12% 1.67

SLM 12.9 4.2% 2.4 16% 1.01

SNH 13.0 3.2% 1.0 8% 1.64

SOL 9.2 3.9% 1.0 5% 1.84

TBS 17.0 2.9% 4.1 11% 1.73

VOD 14.7 6.2% 8.2 10% 1.59

WHL 14.8 4.6% 3.0 8% 1.81

ALSI40 Valuation Statistics

15

3. Top 40 Company Summary

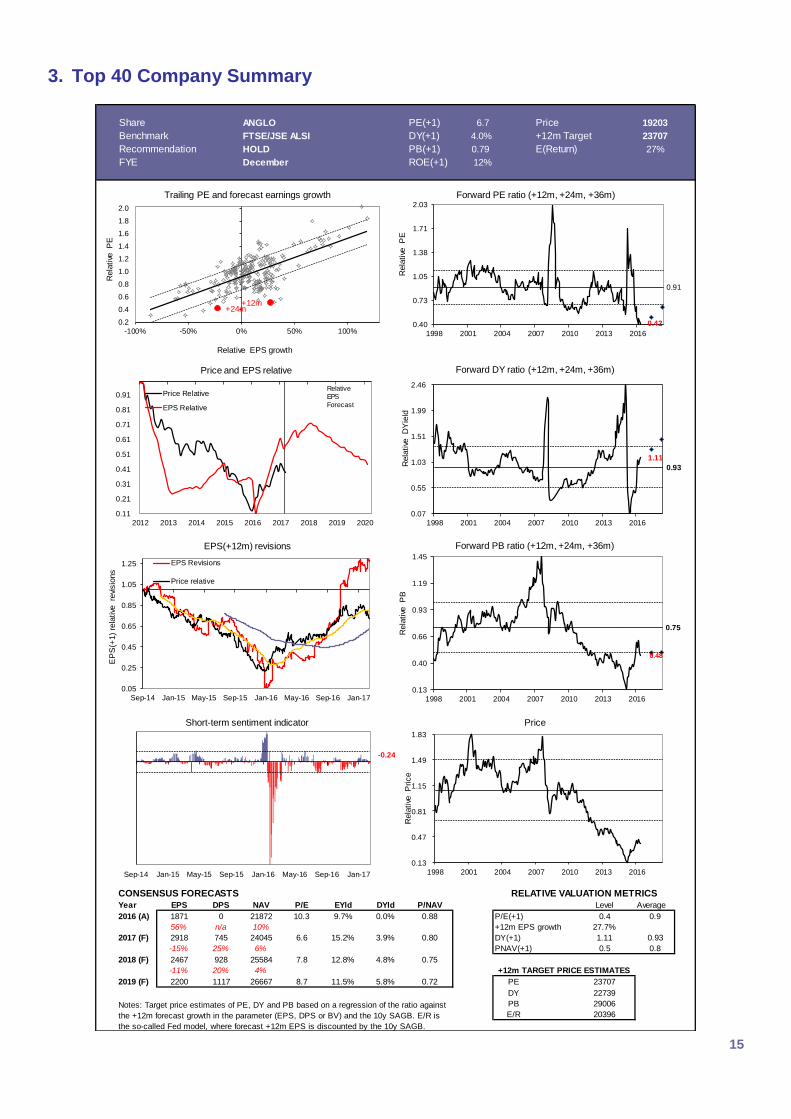

Share ANGLO PE(+1) 6.7 Price 19203

Benchmark FTSE/JSE ALSI DY(+1) 4.0% +12m Target 23707

Recommendation HOLD PB(+1) 0.79 E(Return) 27%

FYE December ROE(+1) 12% Buy/Sell ratio 41%

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 1871 0 21872 10.3 9.7% 0.0% 0.88 P/E(+1) 0.4 0.9

56% n/a 10% +12m EPS growth 27.7%

2017 (F) 2918 745 24045 6.6 15.2% 3.9% 0.80 DY(+1) 1.11 0.93

-15% 25% 6% PNAV(+1) 0.5 0.8

2018 (F) 2467 928 25584 7.8 12.8% 4.8% 0.75

-11% 20% 4%

2019 (F) 2200 1117 26667 8.7 11.5% 5.8% 0.72 PE 23707

DY 22739

PB 29006

E/R 20396Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

0.11

0.21

0.31

0.41

0.51

0.61

0.71

0.81

0.91

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m+24m

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

-100% -50% 0% 50% 100%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

0.42

0.91

0.40

0.73

1.05

1.38

1.71

2.03

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

1.11

0.93

0.07

0.55

1.03

1.51

1.99

2.46

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

0.48

0.75

0.13

0.40

0.66

0.93

1.19

1.45

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.05

0.25

0.45

0.65

0.85

1.05

1.25

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.13

0.47

0.81

1.15

1.49

1.83

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

-0.24

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

16

17

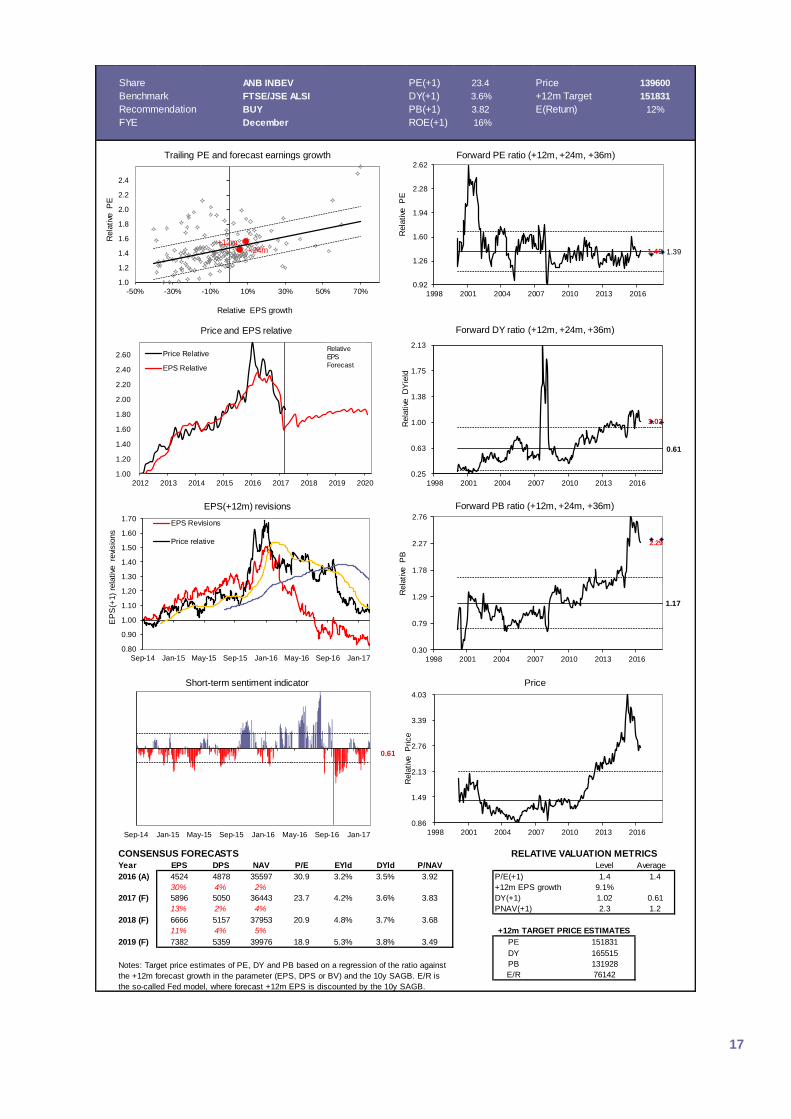

Share ANB INBEV PE(+1) 23.4 Price 139600

Benchmark FTSE/JSE ALSI DY(+1) 3.6% +12m Target 151831

Recommendation BUY PB(+1) 3.82 E(Return) 12%

FYE December ROE(+1) 16% Buy/Sell ratio #N/A

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 4524 4878 35597 30.9 3.2% 3.5% 3.92 P/E(+1) 1.4 1.4

30% 4% 2% +12m EPS growth 9.1%

2017 (F) 5896 5050 36443 23.7 4.2% 3.6% 3.83 DY(+1) 1.02 0.61

13% 2% 4% PNAV(+1) 2.3 1.2

2018 (F) 6666 5157 37953 20.9 4.8% 3.7% 3.68

11% 4% 5%

2019 (F) 7382 5359 39976 18.9 5.3% 3.8% 3.49 PE 151831

DY 165515

PB 131928

E/R 76142Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

2.60

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m+24m

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

-50% -30% -10% 10% 30% 50% 70%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

1.40 1.39

0.92

1.26

1.60

1.94

2.28

2.62

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

1.02

0.61

0.25

0.63

1.00

1.38

1.75

2.13

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

2.29

1.17

0.30

0.79

1.29

1.78

2.27

2.76

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.80

0.90

1.00

1.10

1.20

1.30

1.40

1.50

1.60

1.70

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.86

1.49

2.13

2.76

3.39

4.03

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

0.61

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

18

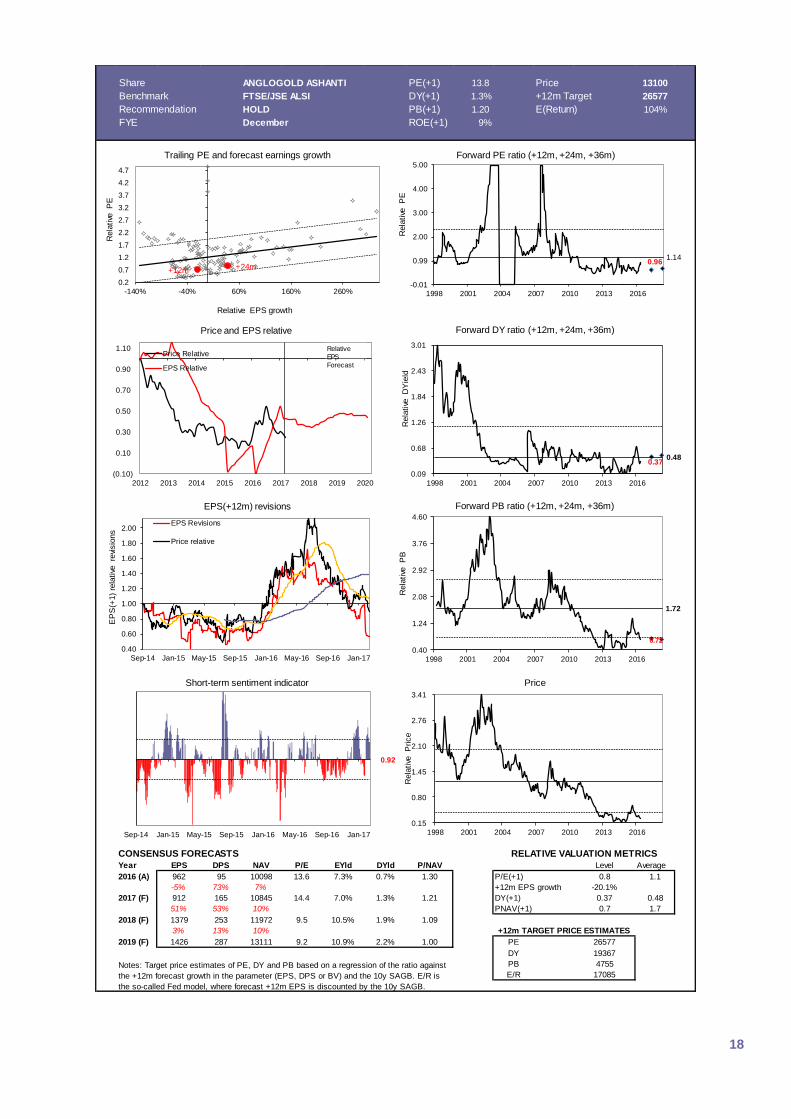

Share ANGLOGOLD ASHANTI PE(+1) 13.8 Price 13100

Benchmark FTSE/JSE ALSI DY(+1) 1.3% +12m Target 26577

Recommendation HOLD PB(+1) 1.20 E(Return) 104%

FYE December ROE(+1) 9% Buy/Sell ratio 25%

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 962 95 10098 13.6 7.3% 0.7% 1.30 P/E(+1) 0.8 1.1

-5% 73% 7% +12m EPS growth -20.1%

2017 (F) 912 165 10845 14.4 7.0% 1.3% 1.21 DY(+1) 0.37 0.48

51% 53% 10% PNAV(+1) 0.7 1.7

2018 (F) 1379 253 11972 9.5 10.5% 1.9% 1.09

3% 13% 10%

2019 (F) 1426 287 13111 9.2 10.9% 2.2% 1.00 PE 26577

DY 19367

PB 4755

E/R 17085Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

(0.10)

0.10

0.30

0.50

0.70

0.90

1.10

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m +24m

0.2

0.7

1.2

1.7

2.2

2.7

3.2

3.7

4.2

4.7

-140% -40% 60% 160% 260%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

0.961.14

-0.01

0.99

2.00

3.00

4.00

5.00

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

0.370.48

0.09

0.68

1.26

1.84

2.43

3.01

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

0.72

1.72

0.40

1.24

2.08

2.92

3.76

4.60

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.15

0.80

1.45

2.10

2.76

3.41

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

0.92

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

19

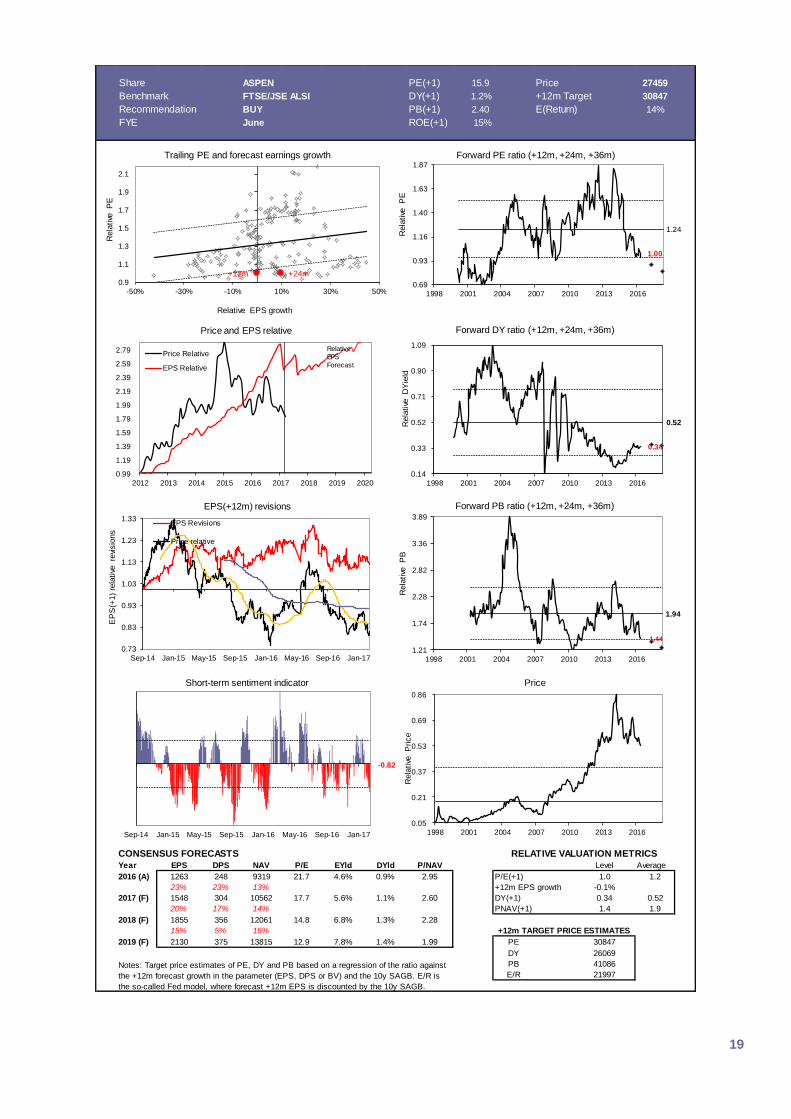

Share ASPEN PE(+1) 15.9 Price 27459

Benchmark FTSE/JSE ALSI DY(+1) 1.2% +12m Target 30847

Recommendation BUY PB(+1) 2.40 E(Return) 14%

FYE June ROE(+1) 15% Buy/Sell ratio 33%

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 1263 248 9319 21.7 4.6% 0.9% 2.95 P/E(+1) 1.0 1.2

23% 23% 13% +12m EPS growth -0.1%

2017 (F) 1548 304 10562 17.7 5.6% 1.1% 2.60 DY(+1) 0.34 0.52

20% 17% 14% PNAV(+1) 1.4 1.9

2018 (F) 1855 356 12061 14.8 6.8% 1.3% 2.28

15% 5% 15%

2019 (F) 2130 375 13815 12.9 7.8% 1.4% 1.99 PE 30847

DY 26069

PB 41086

E/R 21997Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

0.99

1.19

1.39

1.59

1.79

1.99

2.19

2.39

2.59

2.79

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m +24m0.9

1.1

1.3

1.5

1.7

1.9

2.1

-50% -30% -10% 10% 30% 50%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

1.00

1.24

0.69

0.93

1.16

1.40

1.63

1.87

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

0.34

0.52

0.14

0.33

0.52

0.71

0.90

1.09

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

1.44

1.94

1.21

1.74

2.28

2.82

3.36

3.89

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.73

0.83

0.93

1.03

1.13

1.23

1.33

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.05

0.21

0.37

0.53

0.69

0.86

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

-0.82

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

20

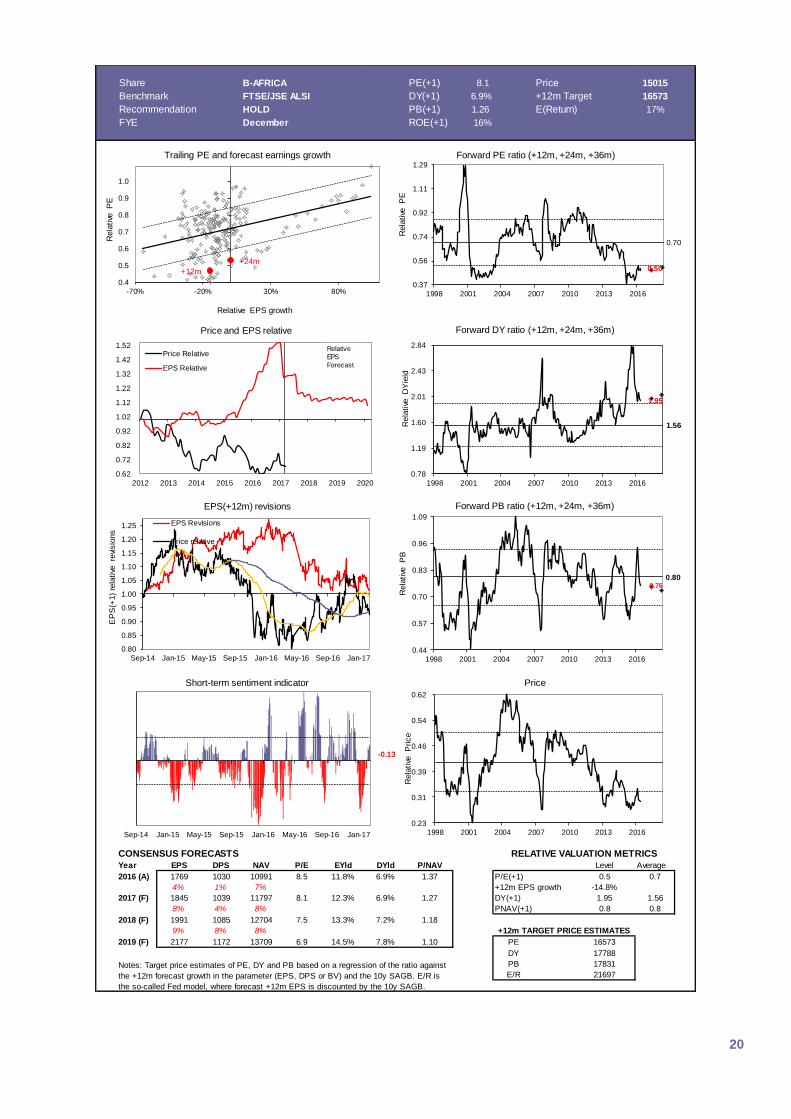

Share B-AFRICA PE(+1) 8.1 Price 15015

Benchmark FTSE/JSE ALSI DY(+1) 6.9% +12m Target 16573

Recommendation HOLD PB(+1) 1.26 E(Return) 17%

FYE December ROE(+1) 16% Buy/Sell ratio 73%

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 1769 1030 10991 8.5 11.8% 6.9% 1.37 P/E(+1) 0.5 0.7

4% 1% 7% +12m EPS growth -14.8%

2017 (F) 1845 1039 11797 8.1 12.3% 6.9% 1.27 DY(+1) 1.95 1.56

8% 4% 8% PNAV(+1) 0.8 0.8

2018 (F) 1991 1085 12704 7.5 13.3% 7.2% 1.18

9% 8% 8%

2019 (F) 2177 1172 13709 6.9 14.5% 7.8% 1.10 PE 16573

DY 17788

PB 17831

E/R 21697Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

0.62

0.72

0.82

0.92

1.02

1.12

1.22

1.32

1.42

1.52

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m

+24m

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-70% -20% 30% 80%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

0.50

0.70

0.37

0.56

0.74

0.92

1.11

1.29

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

1.95

1.56

0.78

1.19

1.60

2.01

2.43

2.84

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

0.76 0.80

0.44

0.57

0.70

0.83

0.96

1.09

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.23

0.31

0.39

0.46

0.54

0.62

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

-0.13

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

21

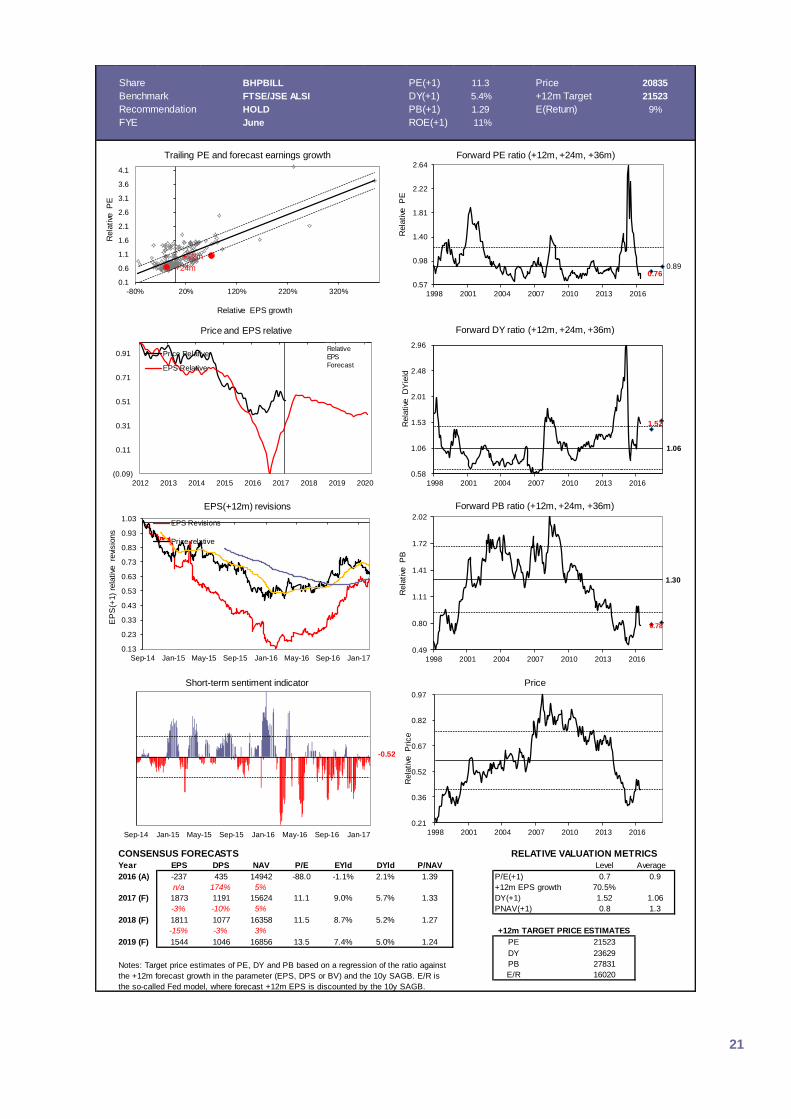

Share BHPBILL PE(+1) 11.3 Price 20835

Benchmark FTSE/JSE ALSI DY(+1) 5.4% +12m Target 21523

Recommendation HOLD PB(+1) 1.29 E(Return) 9%

FYE June ROE(+1) 11% Buy/Sell ratio 52%

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) -237 435 14942 -88.0 -1.1% 2.1% 1.39 P/E(+1) 0.7 0.9

n/a 174% 5% +12m EPS growth 70.5%

2017 (F) 1873 1191 15624 11.1 9.0% 5.7% 1.33 DY(+1) 1.52 1.06

-3% -10% 5% PNAV(+1) 0.8 1.3

2018 (F) 1811 1077 16358 11.5 8.7% 5.2% 1.27

-15% -3% 3%

2019 (F) 1544 1046 16856 13.5 7.4% 5.0% 1.24 PE 21523

DY 23629

PB 27831

E/R 16020Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

(0.09)

0.11

0.31

0.51

0.71

0.91

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m

+24m

0.1

0.6

1.1

1.6

2.1

2.6

3.1

3.6

4.1

-80% 20% 120% 220% 320%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

0.760.89

0.57

0.98

1.40

1.81

2.22

2.64

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

1.52

1.06

0.58

1.06

1.53

2.01

2.48

2.96

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

0.78

1.30

0.49

0.80

1.11

1.41

1.72

2.02

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.13

0.23

0.33

0.43

0.53

0.63

0.73

0.83

0.93

1.03

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.21

0.36

0.52

0.67

0.82

0.97

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

-0.52

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

22

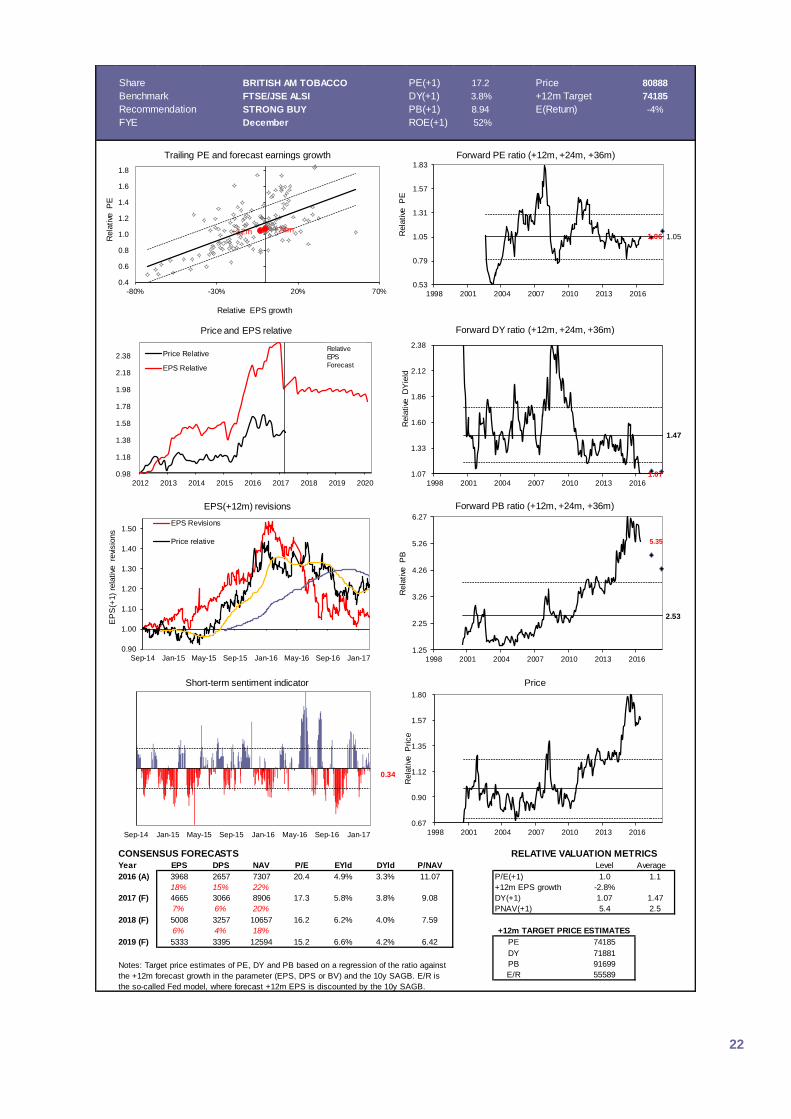

Share BRITISH AM TOBACCO PE(+1) 17.2 Price 80888

Benchmark FTSE/JSE ALSI DY(+1) 3.8% +12m Target 74185

Recommendation STRONG BUY PB(+1) 8.94 E(Return) -4%

FYE December ROE(+1) 52% Buy/Sell ratio 37%

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 3968 2657 7307 20.4 4.9% 3.3% 11.07 P/E(+1) 1.0 1.1

18% 15% 22% +12m EPS growth -2.8%

2017 (F) 4665 3066 8906 17.3 5.8% 3.8% 9.08 DY(+1) 1.07 1.47

7% 6% 20% PNAV(+1) 5.4 2.5

2018 (F) 5008 3257 10657 16.2 6.2% 4.0% 7.59

6% 4% 18%

2019 (F) 5333 3395 12594 15.2 6.6% 4.2% 6.42 PE 74185

DY 71881

PB 91699

E/R 55589Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

0.98

1.18

1.38

1.58

1.78

1.98

2.18

2.38

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m +24m

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

-80% -30% 20% 70%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

1.06 1.05

0.53

0.79

1.05

1.31

1.57

1.83

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

1.07

1.47

1.07

1.33

1.60

1.86

2.12

2.38

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

5.35

2.53

1.25

2.25

3.26

4.26

5.26

6.27

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.90

1.00

1.10

1.20

1.30

1.40

1.50

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.67

0.90

1.12

1.35

1.57

1.80

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

0.34

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

23

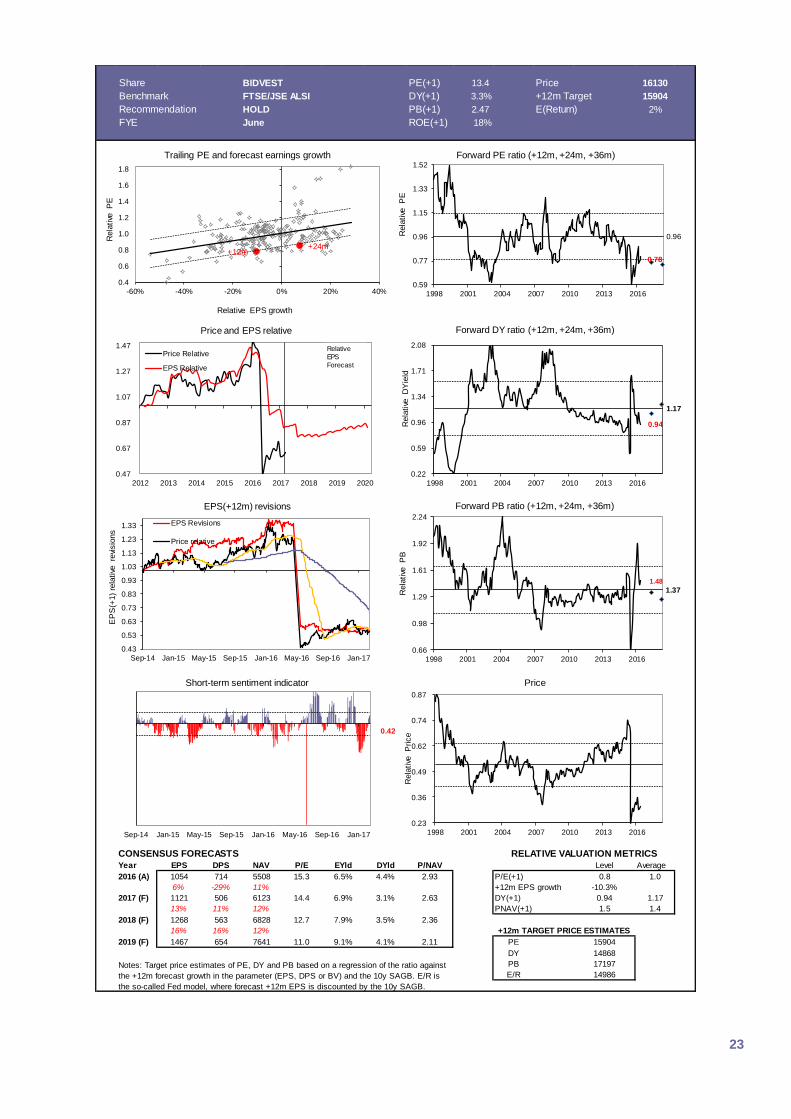

Share BIDVEST PE(+1) 13.4 Price 16130

Benchmark FTSE/JSE ALSI DY(+1) 3.3% +12m Target 15904

Recommendation HOLD PB(+1) 2.47 E(Return) 2%

FYE June ROE(+1) 18% Buy/Sell ratio 50%

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 1054 714 5508 15.3 6.5% 4.4% 2.93 P/E(+1) 0.8 1.0

6% -29% 11% +12m EPS growth -10.3%

2017 (F) 1121 506 6123 14.4 6.9% 3.1% 2.63 DY(+1) 0.94 1.17

13% 11% 12% PNAV(+1) 1.5 1.4

2018 (F) 1268 563 6828 12.7 7.9% 3.5% 2.36

16% 16% 12%

2019 (F) 1467 654 7641 11.0 9.1% 4.1% 2.11 PE 15904

DY 14868

PB 17197

E/R 14986Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

0.47

0.67

0.87

1.07

1.27

1.47

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m+24m

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

-60% -40% -20% 0% 20% 40%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

0.78

0.96

0.59

0.77

0.96

1.15

1.33

1.52

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

0.94

1.17

0.22

0.59

0.96

1.34

1.71

2.08

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

1.48

1.37

0.66

0.98

1.29

1.61

1.92

2.24

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.43

0.53

0.63

0.73

0.83

0.93

1.03

1.13

1.23

1.33

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.23

0.36

0.49

0.62

0.74

0.87

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

0.42

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

24

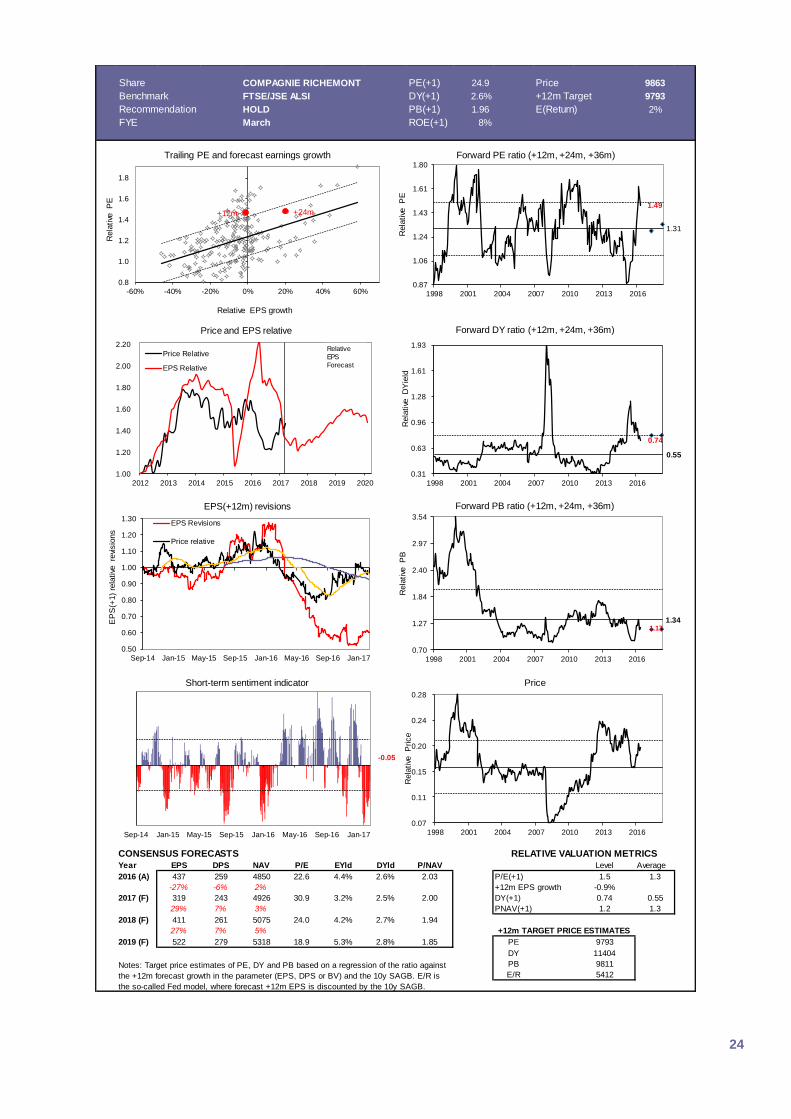

Share COMPAGNIE RICHEMONT PE(+1) 24.9 Price 9863

Benchmark FTSE/JSE ALSI DY(+1) 2.6% +12m Target 9793

Recommendation HOLD PB(+1) 1.96 E(Return) 2%

FYE March ROE(+1) 8% Buy/Sell ratio 48%

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 437 259 4850 22.6 4.4% 2.6% 2.03 P/E(+1) 1.5 1.3

-27% -6% 2% +12m EPS growth -0.9%

2017 (F) 319 243 4926 30.9 3.2% 2.5% 2.00 DY(+1) 0.74 0.55

29% 7% 3% PNAV(+1) 1.2 1.3

2018 (F) 411 261 5075 24.0 4.2% 2.7% 1.94

27% 7% 5%

2019 (F) 522 279 5318 18.9 5.3% 2.8% 1.85 PE 9793

DY 11404

PB 9811

E/R 5412Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m +24m

0.8

1.0

1.2

1.4

1.6

1.8

-60% -40% -20% 0% 20% 40% 60%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

1.49

1.31

0.87

1.06

1.24

1.43

1.61

1.80

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

0.74

0.55

0.31

0.63

0.96

1.28

1.61

1.93

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

1.17 1.34

0.70

1.27

1.84

2.40

2.97

3.54

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.07

0.11

0.15

0.20

0.24

0.28

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

-0.05

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

25

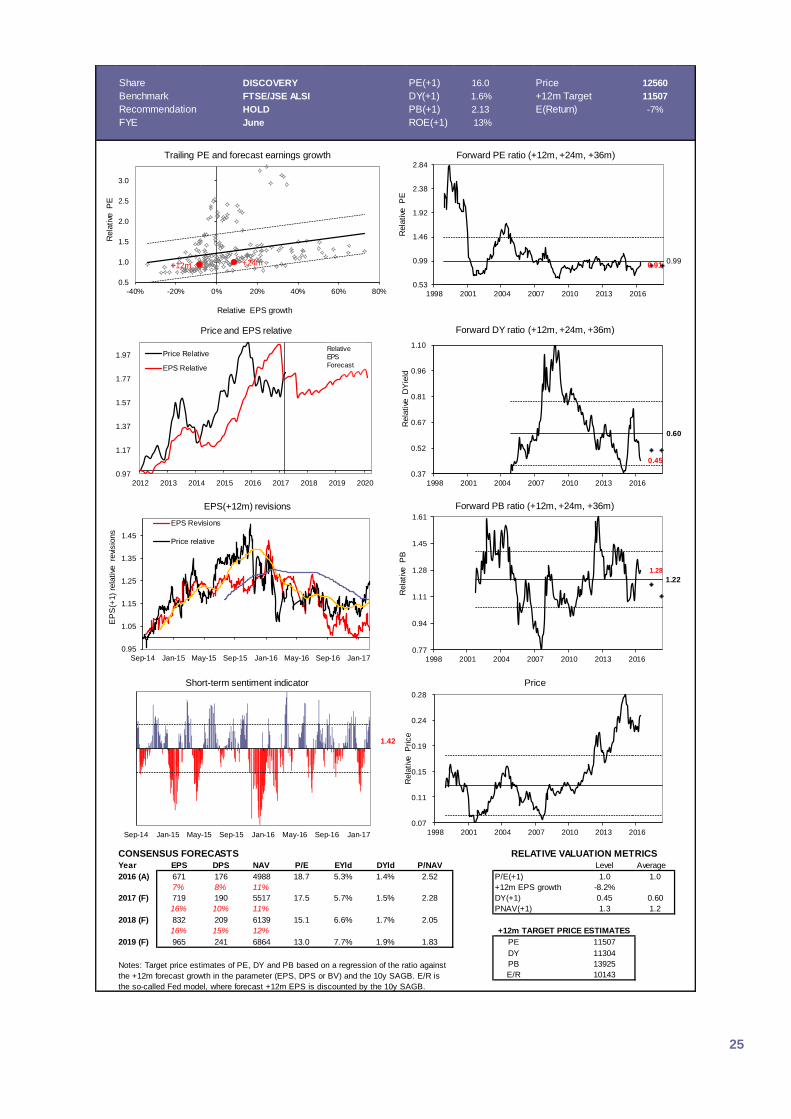

Share DISCOVERY PE(+1) 16.0 Price 12560

Benchmark FTSE/JSE ALSI DY(+1) 1.6% +12m Target 11507

Recommendation HOLD PB(+1) 2.13 E(Return) -7%

FYE June ROE(+1) 13% Buy/Sell ratio 40%

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 671 176 4988 18.7 5.3% 1.4% 2.52 P/E(+1) 1.0 1.0

7% 8% 11% +12m EPS growth -8.2%

2017 (F) 719 190 5517 17.5 5.7% 1.5% 2.28 DY(+1) 0.45 0.60

16% 10% 11% PNAV(+1) 1.3 1.2

2018 (F) 832 209 6139 15.1 6.6% 1.7% 2.05

16% 15% 12%

2019 (F) 965 241 6864 13.0 7.7% 1.9% 1.83 PE 11507

DY 11304

PB 13925

E/R 10143Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

0.97

1.17

1.37

1.57

1.77

1.97

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m +24m

0.5

1.0

1.5

2.0

2.5

3.0

-40% -20% 0% 20% 40% 60% 80%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

0.910.99

0.53

0.99

1.46

1.92

2.38

2.84

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

0.45

0.60

0.37

0.52

0.67

0.81

0.96

1.10

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

1.28

1.22

0.77

0.94

1.11

1.28

1.45

1.61

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.95

1.05

1.15

1.25

1.35

1.45

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.07

0.11

0.15

0.19

0.24

0.28

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

1.42

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

26

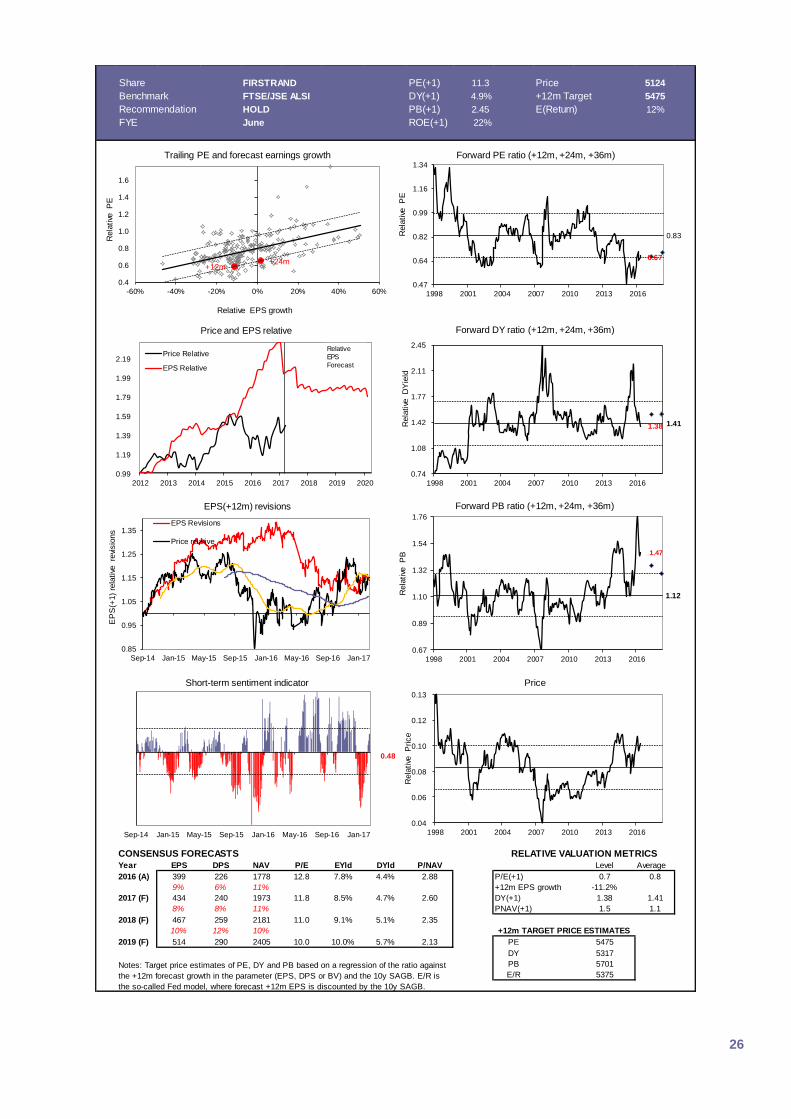

Share FIRSTRAND PE(+1) 11.3 Price 5124

Benchmark FTSE/JSE ALSI DY(+1) 4.9% +12m Target 5475

Recommendation HOLD PB(+1) 2.45 E(Return) 12%

FYE June ROE(+1) 22% Buy/Sell ratio 64%

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 399 226 1778 12.8 7.8% 4.4% 2.88 P/E(+1) 0.7 0.8

9% 6% 11% +12m EPS growth -11.2%

2017 (F) 434 240 1973 11.8 8.5% 4.7% 2.60 DY(+1) 1.38 1.41

8% 8% 11% PNAV(+1) 1.5 1.1

2018 (F) 467 259 2181 11.0 9.1% 5.1% 2.35

10% 12% 10%

2019 (F) 514 290 2405 10.0 10.0% 5.7% 2.13 PE 5475

DY 5317

PB 5701

E/R 5375Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

0.99

1.19

1.39

1.59

1.79

1.99

2.19

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m+24m

0.4

0.6

0.8

1.0

1.2

1.4

1.6

-60% -40% -20% 0% 20% 40% 60%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

0.67

0.83

0.47

0.64

0.82

0.99

1.16

1.34

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

1.38 1.41

0.74

1.08

1.42

1.77

2.11

2.45

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

1.47

1.12

0.67

0.89

1.10

1.32

1.54

1.76

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.85

0.95

1.05

1.15

1.25

1.35

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.04

0.06

0.08

0.10

0.12

0.13

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

0.48

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

27

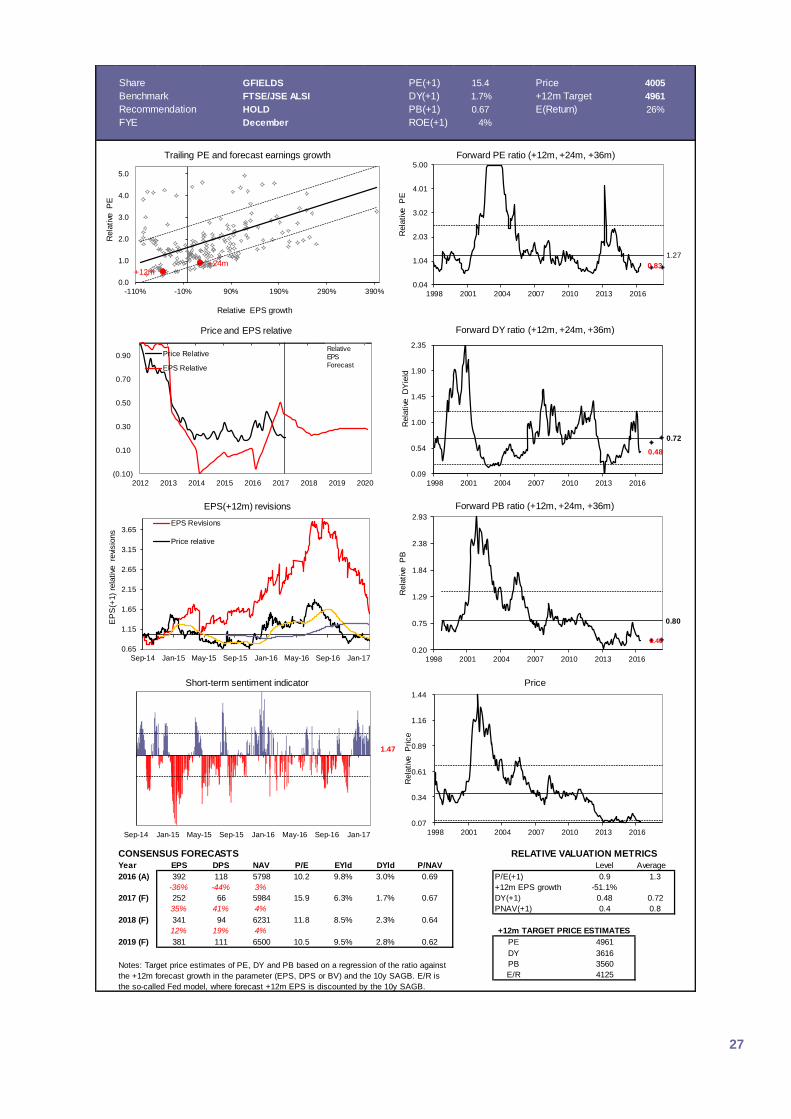

Share GFIELDS PE(+1) 15.4 Price 4005

Benchmark FTSE/JSE ALSI DY(+1) 1.7% +12m Target 4961

Recommendation HOLD PB(+1) 0.67 E(Return) 26%

FYE December ROE(+1) 4% Buy/Sell ratio 57%

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 392 118 5798 10.2 9.8% 3.0% 0.69 P/E(+1) 0.9 1.3

-36% -44% 3% +12m EPS growth -51.1%

2017 (F) 252 66 5984 15.9 6.3% 1.7% 0.67 DY(+1) 0.48 0.72

35% 41% 4% PNAV(+1) 0.4 0.8

2018 (F) 341 94 6231 11.8 8.5% 2.3% 0.64

12% 19% 4%

2019 (F) 381 111 6500 10.5 9.5% 2.8% 0.62 PE 4961

DY 3616

PB 3560

E/R 4125Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

(0.10)

0.10

0.30

0.50

0.70

0.90

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m+24m

0.0

1.0

2.0

3.0

4.0

5.0

-110% -10% 90% 190% 290% 390%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

0.83

1.27

0.04

1.04

2.03

3.02

4.01

5.00

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

0.48

0.72

0.09

0.54

1.00

1.45

1.90

2.35

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

0.40

0.80

0.20

0.75

1.29

1.84

2.38

2.93

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.65

1.15

1.65

2.15

2.65

3.15

3.65

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.07

0.34

0.61

0.89

1.16

1.44

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

1.47

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

28

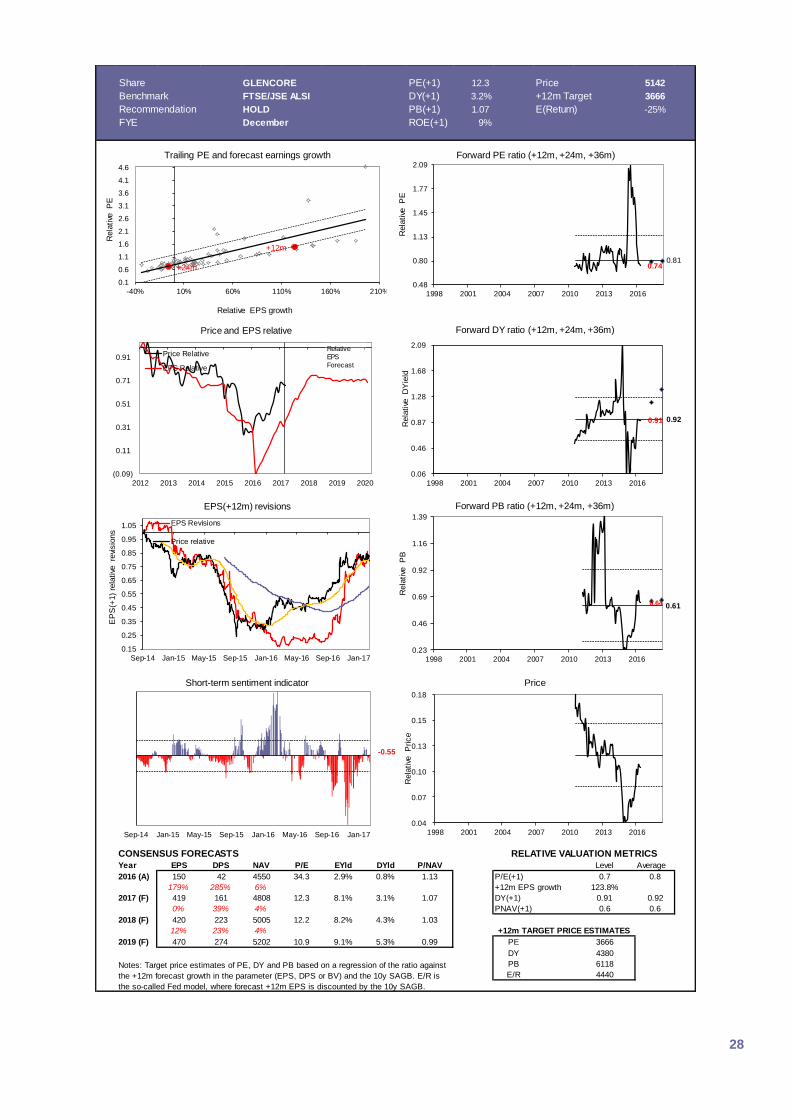

Share GLENCORE PE(+1) 12.3 Price 5142

Benchmark FTSE/JSE ALSI DY(+1) 3.2% +12m Target 3666

Recommendation HOLD PB(+1) 1.07 E(Return) -25%

FYE December ROE(+1) 9% Buy/Sell ratio 58%

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 150 42 4550 34.3 2.9% 0.8% 1.13 P/E(+1) 0.7 0.8

179% 285% 6% +12m EPS growth 123.8%

2017 (F) 419 161 4808 12.3 8.1% 3.1% 1.07 DY(+1) 0.91 0.92

0% 39% 4% PNAV(+1) 0.6 0.6

2018 (F) 420 223 5005 12.2 8.2% 4.3% 1.03

12% 23% 4%

2019 (F) 470 274 5202 10.9 9.1% 5.3% 0.99 PE 3666

DY 4380

PB 6118

E/R 4440Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

(0.09)

0.11

0.31

0.51

0.71

0.91

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m

+24m

0.1

0.6

1.1

1.6

2.1

2.6

3.1

3.6

4.1

4.6

-40% 10% 60% 110% 160% 210%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

0.740.81

0.48

0.80

1.13

1.45

1.77

2.09

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

0.91 0.92

0.06

0.46

0.87

1.28

1.68

2.09

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

0.64 0.61

0.23

0.46

0.69

0.92

1.16

1.39

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.15

0.25

0.35

0.45

0.55

0.65

0.75

0.85

0.95

1.05

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.04

0.07

0.10

0.13

0.15

0.18

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

-0.55

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

29

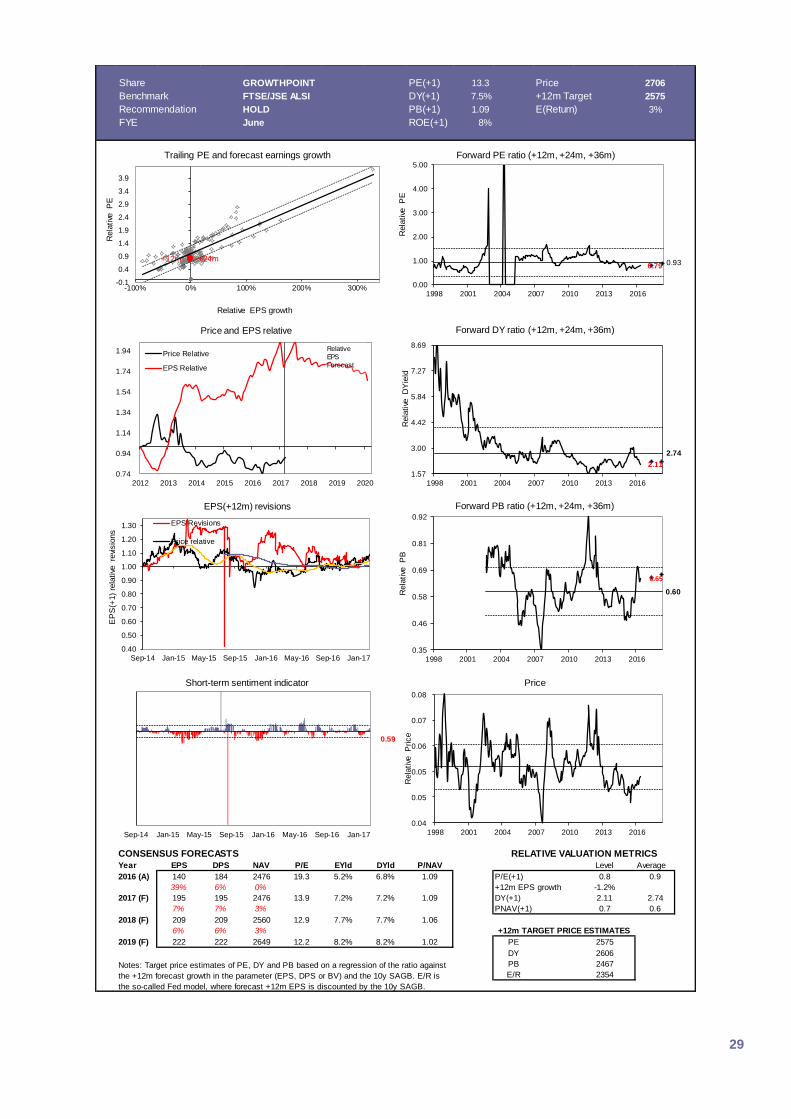

Share GROWTHPOINT PE(+1) 13.3 Price 2706

Benchmark FTSE/JSE ALSI DY(+1) 7.5% +12m Target 2575

Recommendation HOLD PB(+1) 1.09 E(Return) 3%

FYE June ROE(+1) 8% Buy/Sell ratio 80%

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 140 184 2476 19.3 5.2% 6.8% 1.09 P/E(+1) 0.8 0.9

39% 6% 0% +12m EPS growth -1.2%

2017 (F) 195 195 2476 13.9 7.2% 7.2% 1.09 DY(+1) 2.11 2.74

7% 7% 3% PNAV(+1) 0.7 0.6

2018 (F) 209 209 2560 12.9 7.7% 7.7% 1.06

6% 6% 3%

2019 (F) 222 222 2649 12.2 8.2% 8.2% 1.02 PE 2575

DY 2606

PB 2467

E/R 2354Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

0.74

0.94

1.14

1.34

1.54

1.74

1.94

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m +24m

-0.1

0.4

0.9

1.4

1.9

2.4

2.9

3.4

3.9

-100% 0% 100% 200% 300%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

0.79 0.93

0.00

1.00

2.00

3.00

4.00

5.00

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

2.11

2.74

1.57

3.00

4.42

5.84

7.27

8.69

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

0.65

0.60

0.35

0.46

0.58

0.69

0.81

0.92

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.04

0.05

0.05

0.06

0.07

0.08

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

0.59

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

30

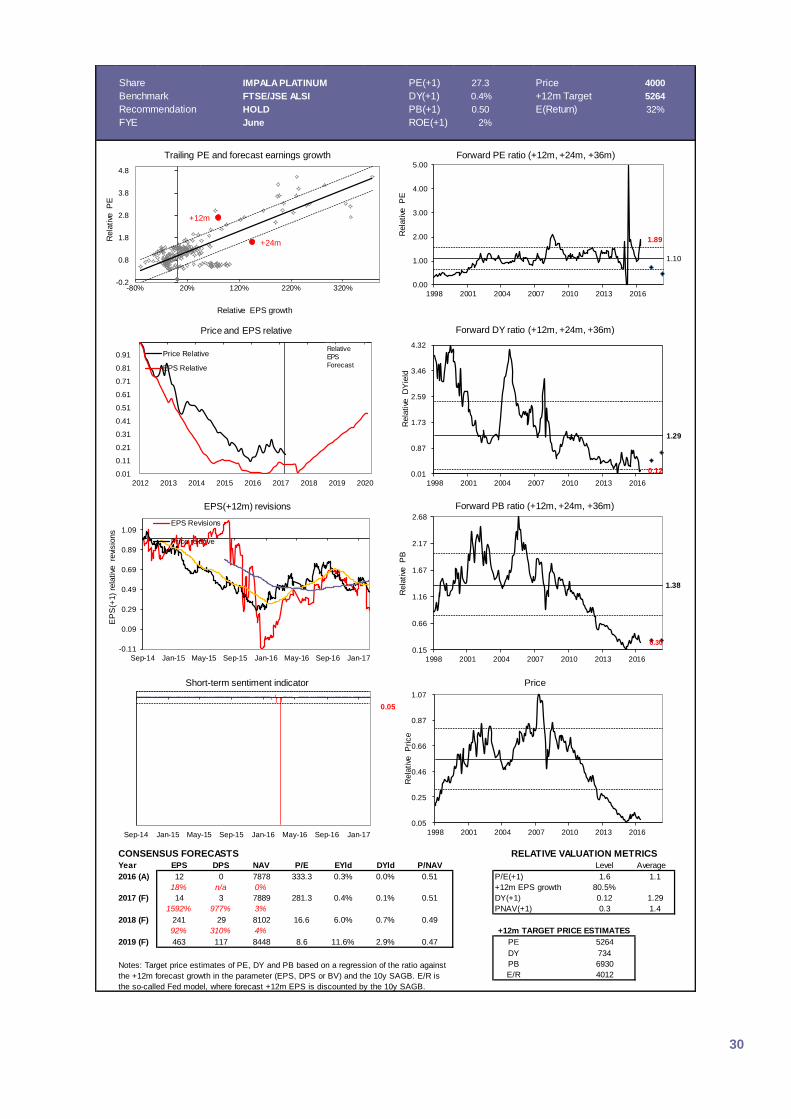

Share IMPALA PLATINUM PE(+1) 27.3 Price 4000

Benchmark FTSE/JSE ALSI DY(+1) 0.4% +12m Target 5264

Recommendation HOLD PB(+1) 0.50 E(Return) 32%

FYE June ROE(+1) 2% Buy/Sell ratio 46%

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 12 0 7878 333.3 0.3% 0.0% 0.51 P/E(+1) 1.6 1.1

18% n/a 0% +12m EPS growth 80.5%

2017 (F) 14 3 7889 281.3 0.4% 0.1% 0.51 DY(+1) 0.12 1.29

1592% 977% 3% PNAV(+1) 0.3 1.4

2018 (F) 241 29 8102 16.6 6.0% 0.7% 0.49

92% 310% 4%

2019 (F) 463 117 8448 8.6 11.6% 2.9% 0.47 PE 5264

DY 734

PB 6930

E/R 4012Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

0.01

0.11

0.21

0.31

0.41

0.51

0.61

0.71

0.81

0.91

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m

+24m

-0.2

0.8

1.8

2.8

3.8

4.8

-80% 20% 120% 220% 320%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

1.89

1.10

0.00

1.00

2.00

3.00

4.00

5.00

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

0.12

1.29

0.01

0.87

1.73

2.59

3.46

4.32

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

0.30

1.38

0.15

0.66

1.16

1.67

2.17

2.68

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

-0.11

0.09

0.29

0.49

0.69

0.89

1.09

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.05

0.25

0.46

0.66

0.87

1.07

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

0.05

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

31

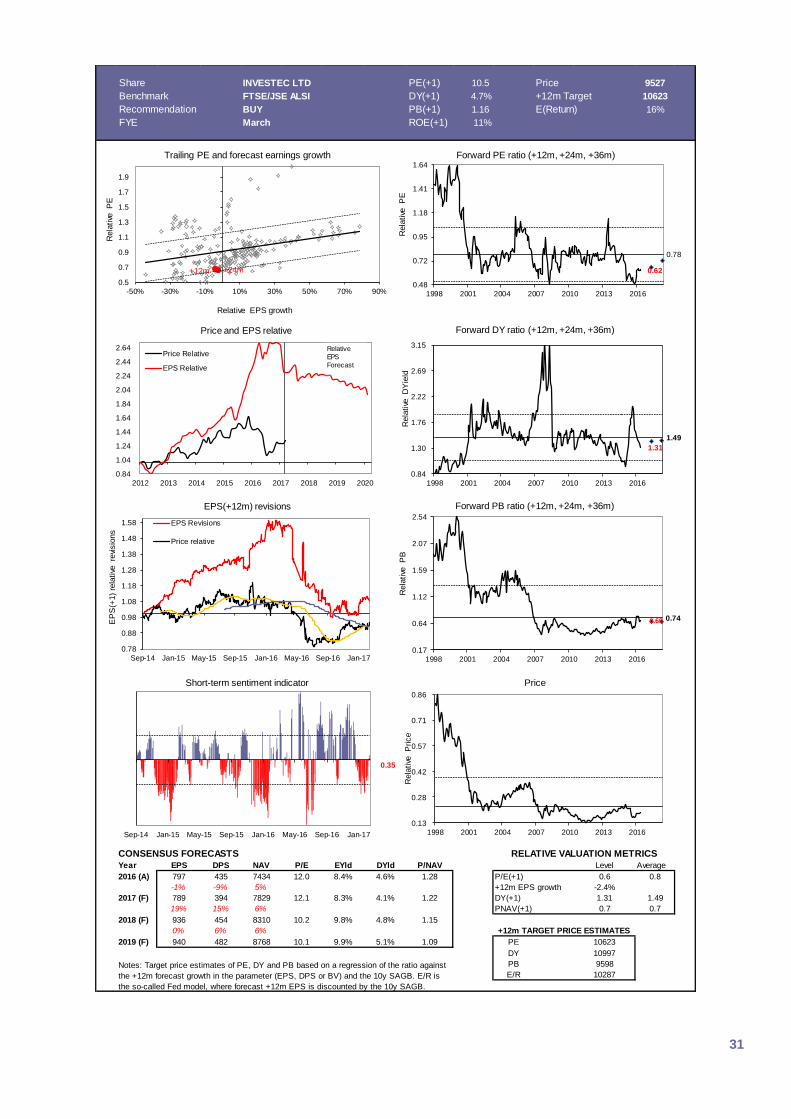

Share INVESTEC LTD PE(+1) 10.5 Price 9527

Benchmark FTSE/JSE ALSI DY(+1) 4.7% +12m Target 10623

Recommendation BUY PB(+1) 1.16 E(Return) 16%

FYE March ROE(+1) 11% Buy/Sell ratio 67%

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 797 435 7434 12.0 8.4% 4.6% 1.28 P/E(+1) 0.6 0.8

-1% -9% 5% +12m EPS growth -2.4%

2017 (F) 789 394 7829 12.1 8.3% 4.1% 1.22 DY(+1) 1.31 1.49

19% 15% 6% PNAV(+1) 0.7 0.7

2018 (F) 936 454 8310 10.2 9.8% 4.8% 1.15

0% 6% 6%

2019 (F) 940 482 8768 10.1 9.9% 5.1% 1.09 PE 10623

DY 10997

PB 9598

E/R 10287Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

0.84

1.04

1.24

1.44

1.64

1.84

2.04

2.24

2.44

2.64

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m +24m

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

-50% -30% -10% 10% 30% 50% 70% 90%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

0.62

0.78

0.48

0.72

0.95

1.18

1.41

1.64

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

1.31

1.49

0.84

1.30

1.76

2.22

2.69

3.15

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

0.69 0.74

0.17

0.64

1.12

1.59

2.07

2.54

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.78

0.88

0.98

1.08

1.18

1.28

1.38

1.48

1.58

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.13

0.28

0.42

0.57

0.71

0.86

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

0.35

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

32

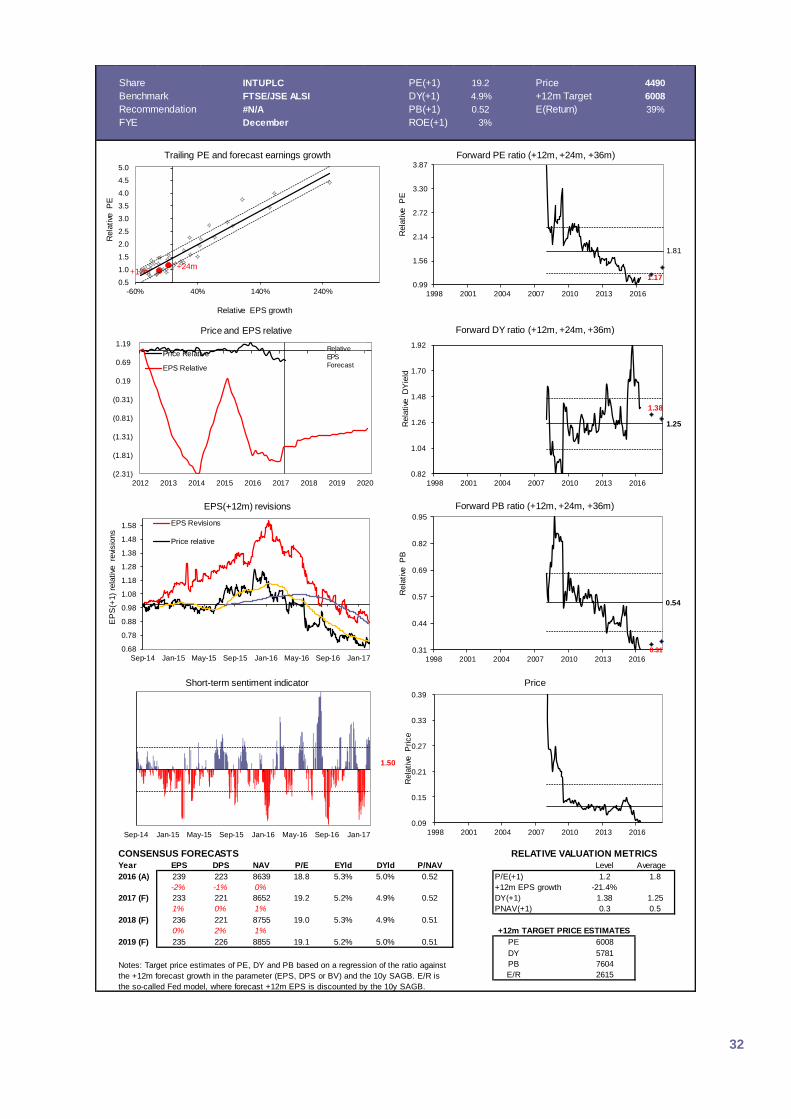

Share INTUPLC PE(+1) 19.2 Price 4490

Benchmark FTSE/JSE ALSI DY(+1) 4.9% +12m Target 6008

Recommendation #N/A PB(+1) 0.52 E(Return) 39%

FYE December ROE(+1) 3% Buy/Sell ratio n/a

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 239 223 8639 18.8 5.3% 5.0% 0.52 P/E(+1) 1.2 1.8

-2% -1% 0% +12m EPS growth -21.4%

2017 (F) 233 221 8652 19.2 5.2% 4.9% 0.52 DY(+1) 1.38 1.25

1% 0% 1% PNAV(+1) 0.3 0.5

2018 (F) 236 221 8755 19.0 5.3% 4.9% 0.51

0% 2% 1%

2019 (F) 235 226 8855 19.1 5.2% 5.0% 0.51 PE 6008

DY 5781

PB 7604

E/R 2615Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

(2.31)

(1.81)

(1.31)

(0.81)

(0.31)

0.19

0.69

1.19

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m+24m

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

-60% 40% 140% 240%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

1.17

1.81

0.99

1.56

2.14

2.72

3.30

3.87

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

1.38

1.25

0.82

1.04

1.26

1.48

1.70

1.92

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

0.31

0.54

0.31

0.44

0.57

0.69

0.82

0.95

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.68

0.78

0.88

0.98

1.08

1.18

1.28

1.38

1.48

1.58

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.09

0.15

0.21

0.27

0.33

0.39

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

1.50

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

33

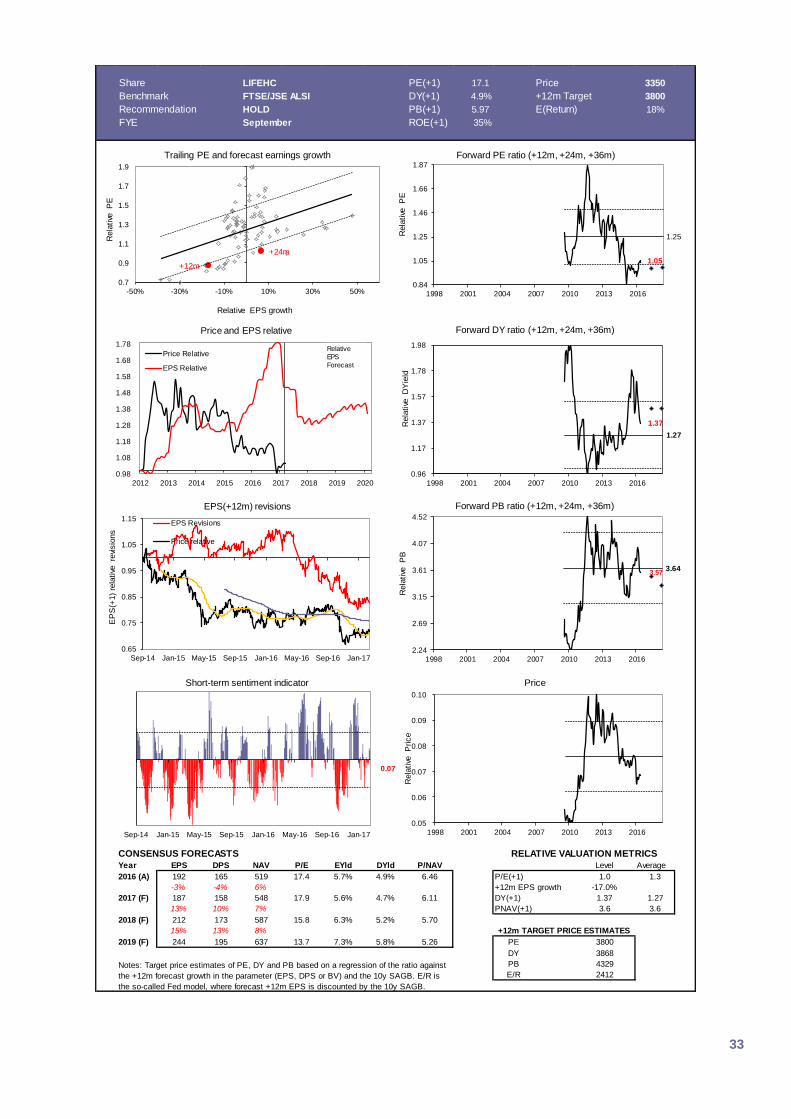

Share LIFEHC PE(+1) 17.1 Price 3350

Benchmark FTSE/JSE ALSI DY(+1) 4.9% +12m Target 3800

Recommendation HOLD PB(+1) 5.97 E(Return) 18%

FYE September ROE(+1) 35% Buy/Sell ratio 67%

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 192 165 519 17.4 5.7% 4.9% 6.46 P/E(+1) 1.0 1.3

-3% -4% 6% +12m EPS growth -17.0%

2017 (F) 187 158 548 17.9 5.6% 4.7% 6.11 DY(+1) 1.37 1.27

13% 10% 7% PNAV(+1) 3.6 3.6

2018 (F) 212 173 587 15.8 6.3% 5.2% 5.70

15% 13% 8%

2019 (F) 244 195 637 13.7 7.3% 5.8% 5.26 PE 3800

DY 3868

PB 4329

E/R 2412Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

0.98

1.08

1.18

1.28

1.38

1.48

1.58

1.68

1.78

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m

+24m

0.7

0.9

1.1

1.3

1.5

1.7

1.9

-50% -30% -10% 10% 30% 50%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

1.05

1.25

0.84

1.05

1.25

1.46

1.66

1.87

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

1.37

1.27

0.96

1.17

1.37

1.57

1.78

1.98

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

3.57 3.64

2.24

2.69

3.15

3.61

4.07

4.52

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.65

0.75

0.85

0.95

1.05

1.15

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.05

0.06

0.07

0.08

0.09

0.10

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

0.07

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

34

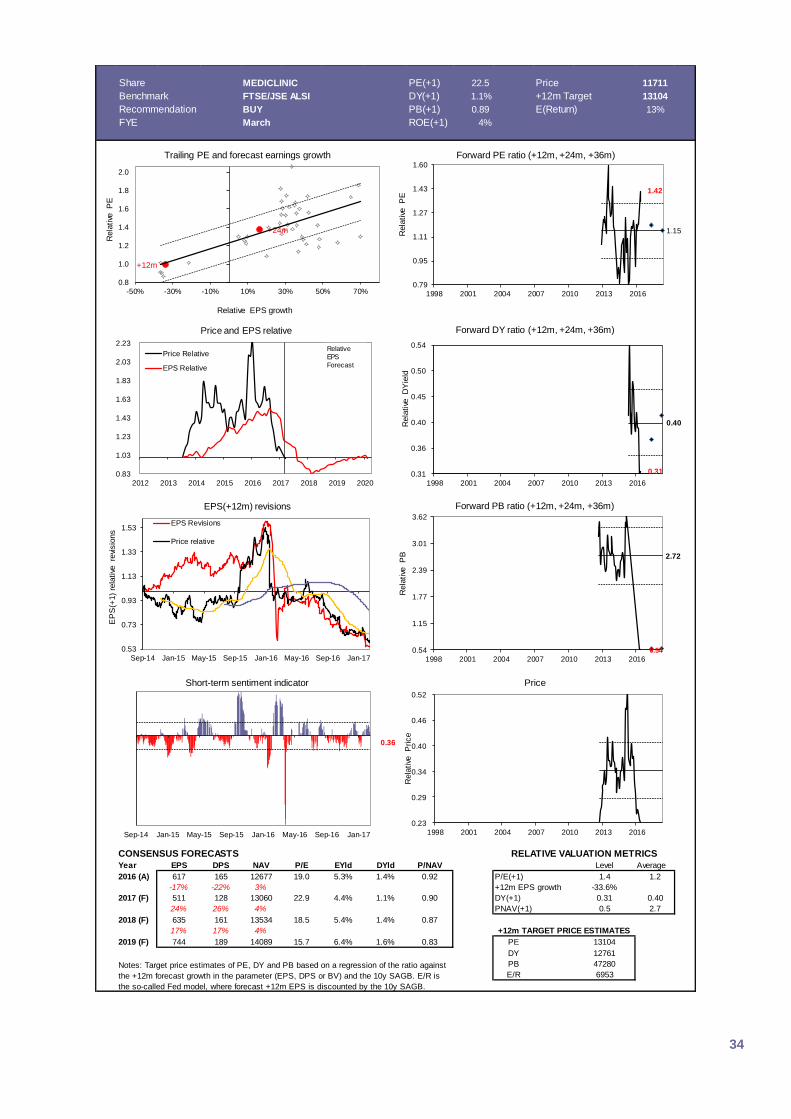

Share MEDICLINIC PE(+1) 22.5 Price 11711

Benchmark FTSE/JSE ALSI DY(+1) 1.1% +12m Target 13104

Recommendation BUY PB(+1) 0.89 E(Return) 13%

FYE March ROE(+1) 4% Buy/Sell ratio 50%

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 617 165 12677 19.0 5.3% 1.4% 0.92 P/E(+1) 1.4 1.2

-17% -22% 3% +12m EPS growth -33.6%

2017 (F) 511 128 13060 22.9 4.4% 1.1% 0.90 DY(+1) 0.31 0.40

24% 26% 4% PNAV(+1) 0.5 2.7

2018 (F) 635 161 13534 18.5 5.4% 1.4% 0.87

17% 17% 4%

2019 (F) 744 189 14089 15.7 6.4% 1.6% 0.83 PE 13104

DY 12761

PB 47280

E/R 6953Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

0.83

1.03

1.23

1.43

1.63

1.83

2.03

2.23

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m

+24m

0.8

1.0

1.2

1.4

1.6

1.8

2.0

-50% -30% -10% 10% 30% 50% 70%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

1.42

1.15

0.79

0.95

1.11

1.27

1.43

1.60

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

0.31

0.40

0.31

0.36

0.40

0.45

0.50

0.54

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

0.54

2.72

0.54

1.15

1.77

2.39

3.01

3.62

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.53

0.73

0.93

1.13

1.33

1.53

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.23

0.29

0.34

0.40

0.46

0.52

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

0.36

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

35

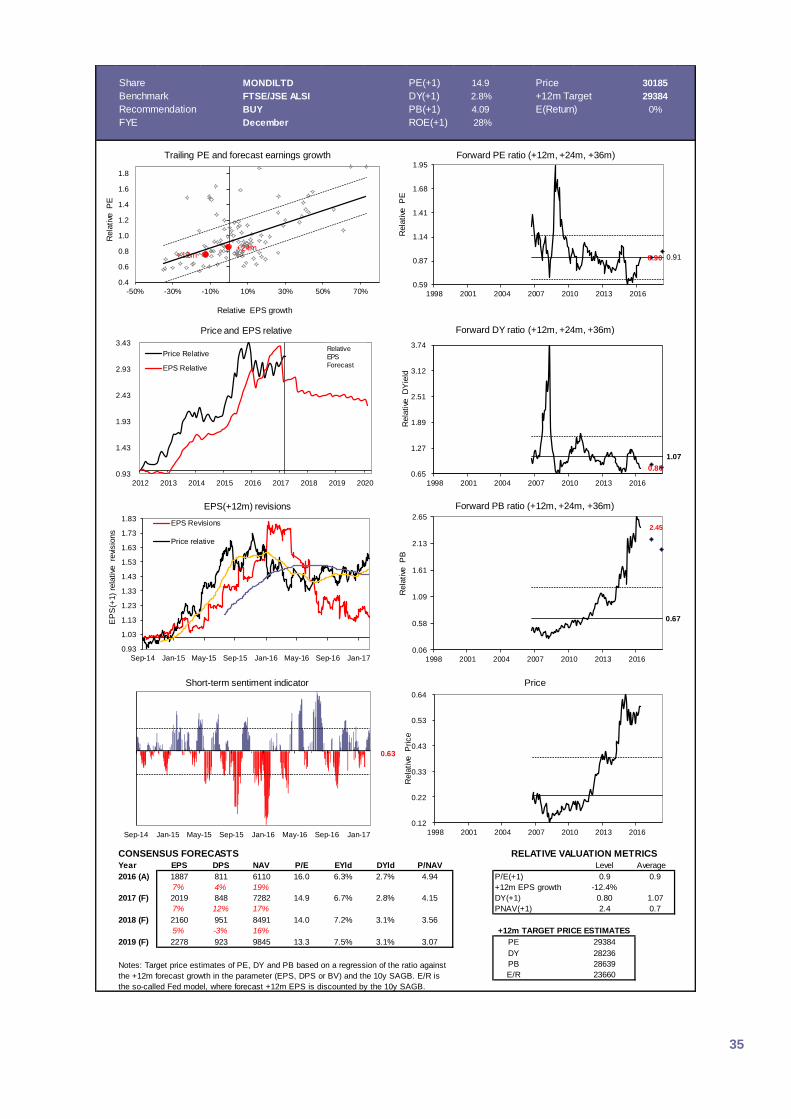

Share MONDILTD PE(+1) 14.9 Price 30185

Benchmark FTSE/JSE ALSI DY(+1) 2.8% +12m Target 29384

Recommendation BUY PB(+1) 4.09 E(Return) 0%

FYE December ROE(+1) 28% Buy/Sell ratio #N/A

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 1887 811 6110 16.0 6.3% 2.7% 4.94 P/E(+1) 0.9 0.9

7% 4% 19% +12m EPS growth -12.4%

2017 (F) 2019 848 7282 14.9 6.7% 2.8% 4.15 DY(+1) 0.80 1.07

7% 12% 17% PNAV(+1) 2.4 0.7

2018 (F) 2160 951 8491 14.0 7.2% 3.1% 3.56

5% -3% 16%

2019 (F) 2278 923 9845 13.3 7.5% 3.1% 3.07 PE 29384

DY 28236

PB 28639

E/R 23660Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

0.93

1.43

1.93

2.43

2.93

3.43

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m+24m

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

-50% -30% -10% 10% 30% 50% 70%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

0.90 0.91

0.59

0.87

1.14

1.41

1.68

1.95

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

0.80

1.07

0.65

1.27

1.89

2.51

3.12

3.74

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

2.45

0.67

0.06

0.58

1.09

1.61

2.13

2.65

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.93

1.03

1.13

1.23

1.33

1.43

1.53

1.63

1.73

1.83

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.12

0.22

0.33

0.43

0.53

0.64

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

0.63

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

36

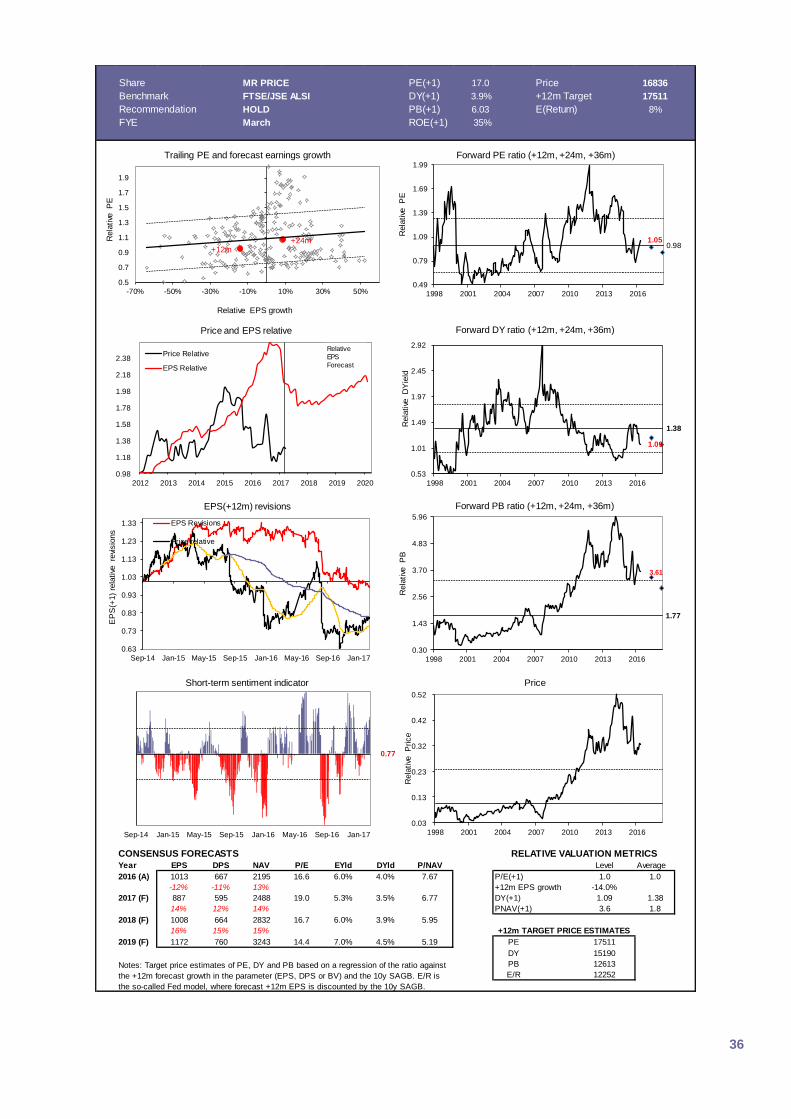

Share MR PRICE PE(+1) 17.0 Price 16836

Benchmark FTSE/JSE ALSI DY(+1) 3.9% +12m Target 17511

Recommendation HOLD PB(+1) 6.03 E(Return) 8%

FYE March ROE(+1) 35% Buy/Sell ratio 62%

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 1013 667 2195 16.6 6.0% 4.0% 7.67 P/E(+1) 1.0 1.0

-12% -11% 13% +12m EPS growth -14.0%

2017 (F) 887 595 2488 19.0 5.3% 3.5% 6.77 DY(+1) 1.09 1.38

14% 12% 14% PNAV(+1) 3.6 1.8

2018 (F) 1008 664 2832 16.7 6.0% 3.9% 5.95

16% 15% 15%

2019 (F) 1172 760 3243 14.4 7.0% 4.5% 5.19 PE 17511

DY 15190

PB 12613

E/R 12252Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

0.98

1.18

1.38

1.58

1.78

1.98

2.18

2.38

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m+24m

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

-70% -50% -30% -10% 10% 30% 50%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

1.050.98

0.49

0.79

1.09

1.39

1.69

1.99

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

1.09

1.38

0.53

1.01

1.49

1.97

2.45

2.92

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

3.61

1.77

0.30

1.43

2.56

3.70

4.83

5.96

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.63

0.73

0.83

0.93

1.03

1.13

1.23

1.33

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.03

0.13

0.23

0.32

0.42

0.52

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

0.77

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

37

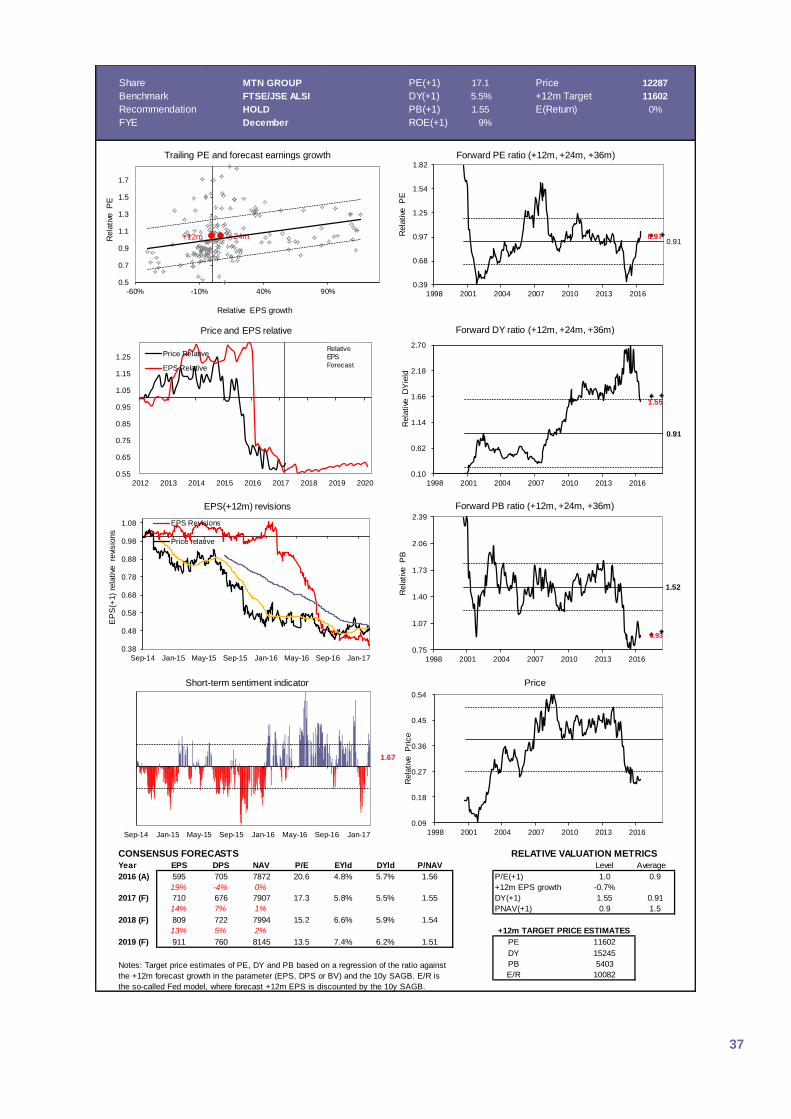

Share MTN GROUP PE(+1) 17.1 Price 12287

Benchmark FTSE/JSE ALSI DY(+1) 5.5% +12m Target 11602

Recommendation HOLD PB(+1) 1.55 E(Return) 0%

FYE December ROE(+1) 9% Buy/Sell ratio 31%

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 595 705 7872 20.6 4.8% 5.7% 1.56 P/E(+1) 1.0 0.9

19% -4% 0% +12m EPS growth -0.7%

2017 (F) 710 676 7907 17.3 5.8% 5.5% 1.55 DY(+1) 1.55 0.91

14% 7% 1% PNAV(+1) 0.9 1.5

2018 (F) 809 722 7994 15.2 6.6% 5.9% 1.54

13% 5% 2%

2019 (F) 911 760 8145 13.5 7.4% 6.2% 1.51 PE 11602

DY 15245

PB 5403

E/R 10082Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

0.55

0.65

0.75

0.85

0.95

1.05

1.15

1.25

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m +24m

0.5

0.7

0.9

1.1

1.3

1.5

1.7

-60% -10% 40% 90%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

0.970.91

0.39

0.68

0.97

1.25

1.54

1.82

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

1.55

0.91

0.10

0.62

1.14

1.66

2.18

2.70

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

0.93

1.52

0.75

1.07

1.40

1.73

2.06

2.39

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.38

0.48

0.58

0.68

0.78

0.88

0.98

1.08

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.09

0.18

0.27

0.36

0.45

0.54

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

1.67

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

38

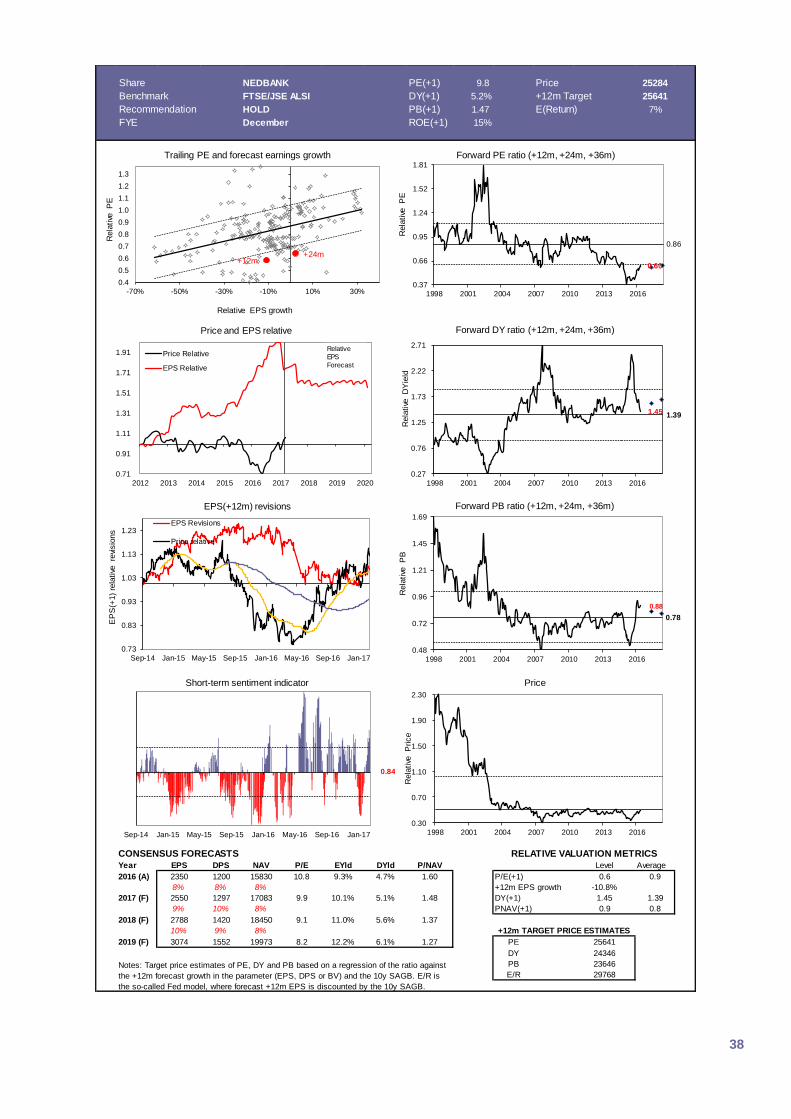

Share NEDBANK PE(+1) 9.8 Price 25284

Benchmark FTSE/JSE ALSI DY(+1) 5.2% +12m Target 25641

Recommendation HOLD PB(+1) 1.47 E(Return) 7%

FYE December ROE(+1) 15% Buy/Sell ratio 82%

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 2350 1200 15830 10.8 9.3% 4.7% 1.60 P/E(+1) 0.6 0.9

8% 8% 8% +12m EPS growth -10.8%

2017 (F) 2550 1297 17083 9.9 10.1% 5.1% 1.48 DY(+1) 1.45 1.39

9% 10% 8% PNAV(+1) 0.9 0.8

2018 (F) 2788 1420 18450 9.1 11.0% 5.6% 1.37

10% 9% 8%

2019 (F) 3074 1552 19973 8.2 12.2% 6.1% 1.27 PE 25641

DY 24346

PB 23646

E/R 29768Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

0.71

0.91

1.11

1.31

1.51

1.71

1.91

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m+24m

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

-70% -50% -30% -10% 10% 30%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

0.60

0.86

0.37

0.66

0.95

1.24

1.52

1.81

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

1.45 1.39

0.27

0.76

1.25

1.73

2.22

2.71

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

0.88

0.78

0.48

0.72

0.96

1.21

1.45

1.69

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.73

0.83

0.93

1.03

1.13

1.23

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.30

0.70

1.10

1.50

1.90

2.30

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

0.84

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

39

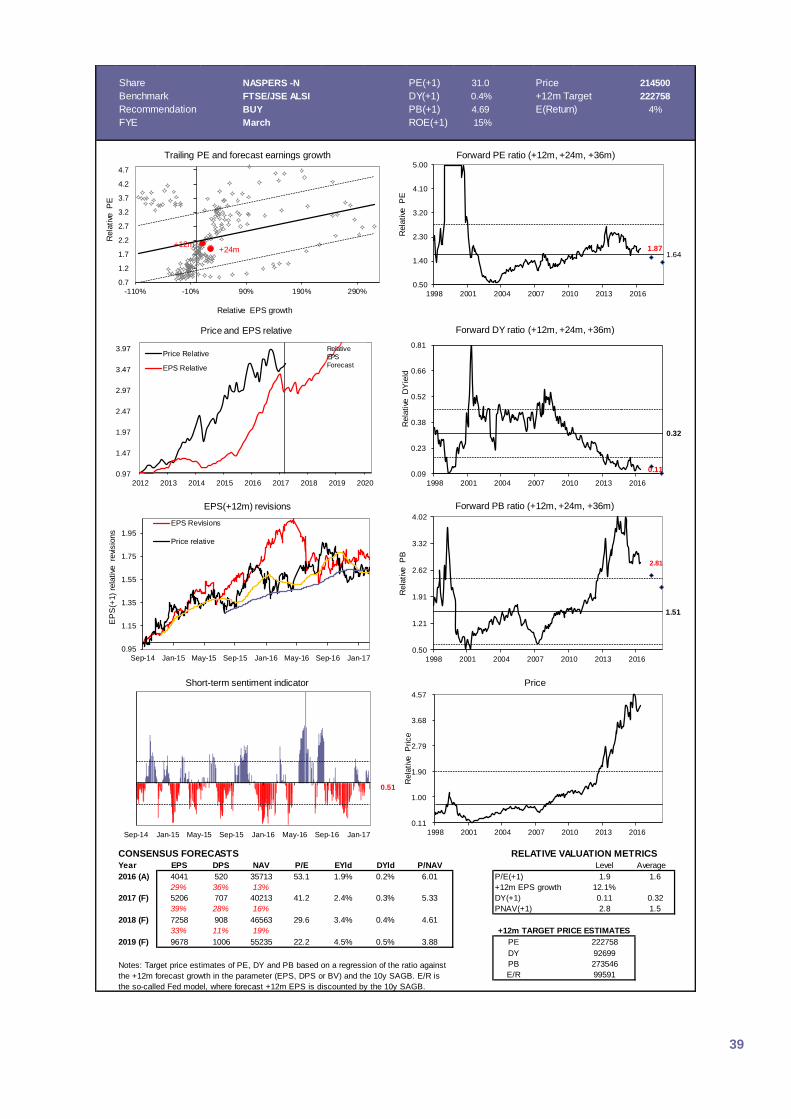

Share NASPERS -N PE(+1) 31.0 Price 214500

Benchmark FTSE/JSE ALSI DY(+1) 0.4% +12m Target 222758

Recommendation BUY PB(+1) 4.69 E(Return) 4%

FYE March ROE(+1) 15% Buy/Sell ratio 7%

CONSENSUS FORECASTS

Year EPS DPS NAV P/E EYld DYld P/NAV Level Average

2016 (A) 4041 520 35713 53.1 1.9% 0.2% 6.01 P/E(+1) 1.9 1.6

29% 36% 13% +12m EPS growth 12.1%

2017 (F) 5206 707 40213 41.2 2.4% 0.3% 5.33 DY(+1) 0.11 0.32

39% 28% 16% PNAV(+1) 2.8 1.5

2018 (F) 7258 908 46563 29.6 3.4% 0.4% 4.61

33% 11% 19%

2019 (F) 9678 1006 55235 22.2 4.5% 0.5% 3.88 PE 222758

DY 92699

PB 273546

E/R 99591Notes: Target price estimates of PE, DY and PB based on a regression of the ratio against

the +12m forecast growth in the parameter (EPS, DPS or BV) and the 10y SAGB. E/R is

the so-called Fed model, where forecast +12m EPS is discounted by the 10y SAGB.

+12m TARGET PRICE ESTIMATES

RELATIVE VALUATION METRICS

0.97

1.47

1.97

2.47

2.97

3.47

3.97

2012 2013 2014 2015 2016 2017 2018 2019 2020

Price and EPS relative

Price Relative

EPS Relative

+12m+24m

0.7

1.2

1.7

2.2

2.7

3.2

3.7

4.2

4.7

-110% -10% 90% 190% 290%

Rela

tive

P

E

Relative EPS growth

Trailing PE and forecast earnings growth

1.871.64

0.50

1.40

2.30

3.20

4.10

5.00

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

E

Forward PE ratio (+12m, +24m, +36m)

0.11

0.32

0.09

0.23

0.38

0.52

0.66

0.81

1998 2001 2004 2007 2010 2013 2016

Rela

tive

D

Yie

ld

Forward DY ratio (+12m, +24m, +36m)

Relative

EPS

Forecast

2.81

1.51

0.50

1.21

1.91

2.62

3.32

4.02

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

B

Forward PB ratio (+12m, +24m, +36m)

0.95

1.15

1.35

1.55

1.75

1.95

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

EP

S(+

1)

rela

tive

re

visio

ns

EPS(+12m) revisions

EPS Revisions

Price relative

0.11

1.00

1.90

2.79

3.68

4.57

1998 2001 2004 2007 2010 2013 2016

Rela

tive

P

rice

Price

0.51

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17

Short-term sentiment indicator

40

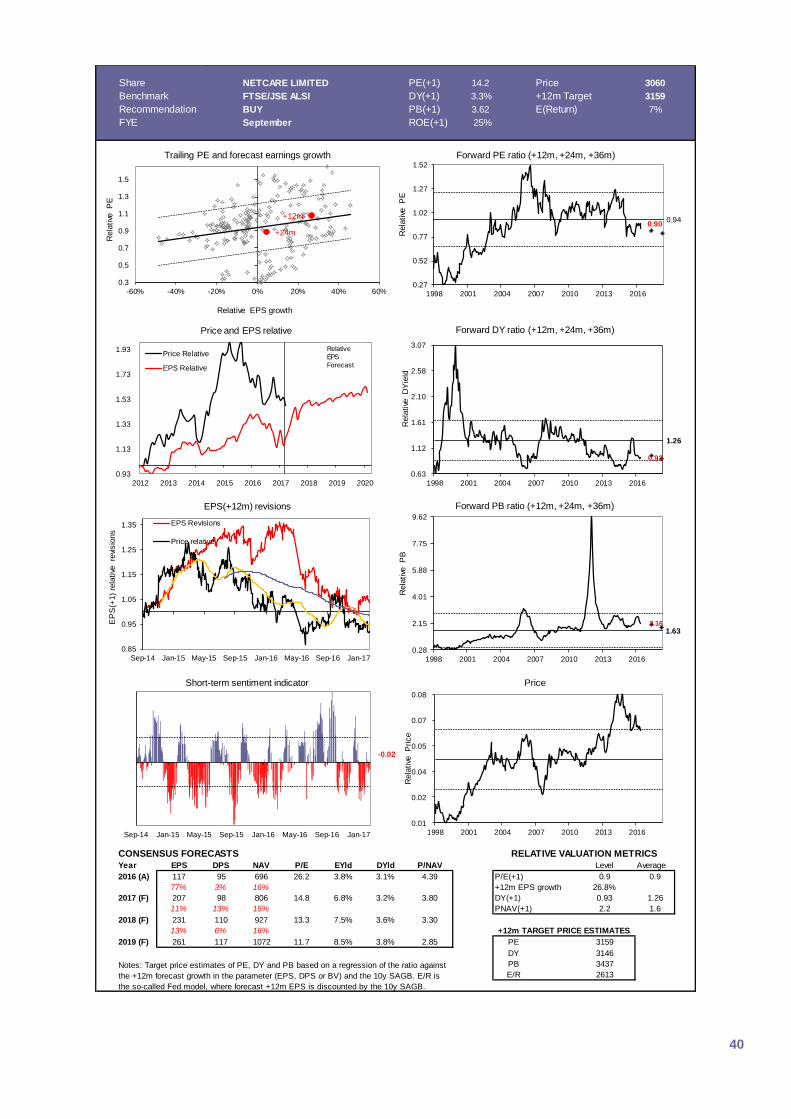

Share NETCARE LIMITED PE(+1) 14.2 Price 3060

Benchmark FTSE/JSE ALSI DY(+1) 3.3% +12m Target 3159

Recommendation BUY PB(+1) 3.62 E(Return) 7%