lease financing(suman bisht)

TRANSCRIPT

Presentation on “ Lease financing”Presentation on “ Lease financing”

In the partial fulfillment of the requirement for the award of degree, In the partial fulfillment of the requirement for the award of degree, Master of Commerce H.N.B.GARHWAL UNIVERSITYMaster of Commerce H.N.B.GARHWAL UNIVERSITY

Coordinator:Coordinator: Submitted bySubmitted by::Prof. R.C. DangwalProf. R.C. Dangwal Suman BishtSuman Bisht

M.Com IV SemM.Com IV Sem

SCHOOL OF COMMERCESCHOOL OF COMMERCEH.N.B.G.U (Central University)H.N.B.G.U (Central University)Srinagar GarhwalSrinagar Garhwal

(Session 2013-2015(Session 2013-2015))

Lease financing Lease financing

The evolution of lease financing is traced way back The evolution of lease financing is traced way back to the early 1950s when the United state started to the early 1950s when the United state started equipment leasing. It spread to all European equipment leasing. It spread to all European countries in the early 1960s and to the rest of the countries in the early 1960s and to the rest of the world during the 1970s. Land leasing has been world during the 1970s. Land leasing has been quite prevalent in India from old times.quite prevalent in India from old times.

However, leasing of capital equipment’s is of a However, leasing of capital equipment’s is of a recent origin in India. As per available records, recent origin in India. As per available records, lease financing started taking its roots in the Indian lease financing started taking its roots in the Indian soil since 1970s. The pioneer in this field was “ First soil since 1970s. The pioneer in this field was “ First leasing Company of India Ltd. (PLC)” based in leasing Company of India Ltd. (PLC)” based in Madras. The company started its business in 1973. Madras. The company started its business in 1973. Since then no. of leasing company came into Since then no. of leasing company came into existence. They are Mazda leasing, Twentieth existence. They are Mazda leasing, Twentieth Century , Ross Morarka leasing company, Pioneer Century , Ross Morarka leasing company, Pioneer Leasing and express leasing company etc.Leasing and express leasing company etc.

IntroductionIntroduction

Literature reviewLiterature review

Granof (1984)Granof (1984) - has discussed that a tax exempt lease is - has discussed that a tax exempt lease is an arrangement similar in economic substance to an an arrangement similar in economic substance to an installment purchase.installment purchase.

Srinivasan (2009)-Srinivasan (2009)- has discussed that leasing is an has discussed that leasing is an important source of funding for medium and small scale important source of funding for medium and small scale industries, which are key drivers of economic development industries, which are key drivers of economic development in developing countries.in developing countries.

Qian & Burritt (2011)-Qian & Burritt (2011)- discussed in their research paper discussed in their research paper that how leasing provide a more attractive option than that how leasing provide a more attractive option than selling and extend producer responsibility in helping to selling and extend producer responsibility in helping to close product life cycle loops , extend useful life of close product life cycle loops , extend useful life of products, an increase environmental benefitsproducts, an increase environmental benefits..

Objective of studyObjective of study

To focus on effect of lease financing on To focus on effect of lease financing on service market.service market.

To generate new knowledge about lease To generate new knowledge about lease financing.financing.

To know about its types and its product.To know about its types and its product. To know about its loopholes i.e. limitations or To know about its loopholes i.e. limitations or

its disadvantages.its disadvantages. To analyse the process of leasing.To analyse the process of leasing. To have a clear picture of understanding debt To have a clear picture of understanding debt

financing as it retakes to lease.financing as it retakes to lease.

Leasing is a contractual arrangement , where Leasing is a contractual arrangement , where

The owner (Lessor) of the Asset (Equipment)The owner (Lessor) of the Asset (Equipment) Transfers the possession / right to use the Asset Transfers the possession / right to use the Asset

(Equipment) to another (Lessee)(Equipment) to another (Lessee) For an agreed period of time in return for rental.For an agreed period of time in return for rental.

Lease - Definition

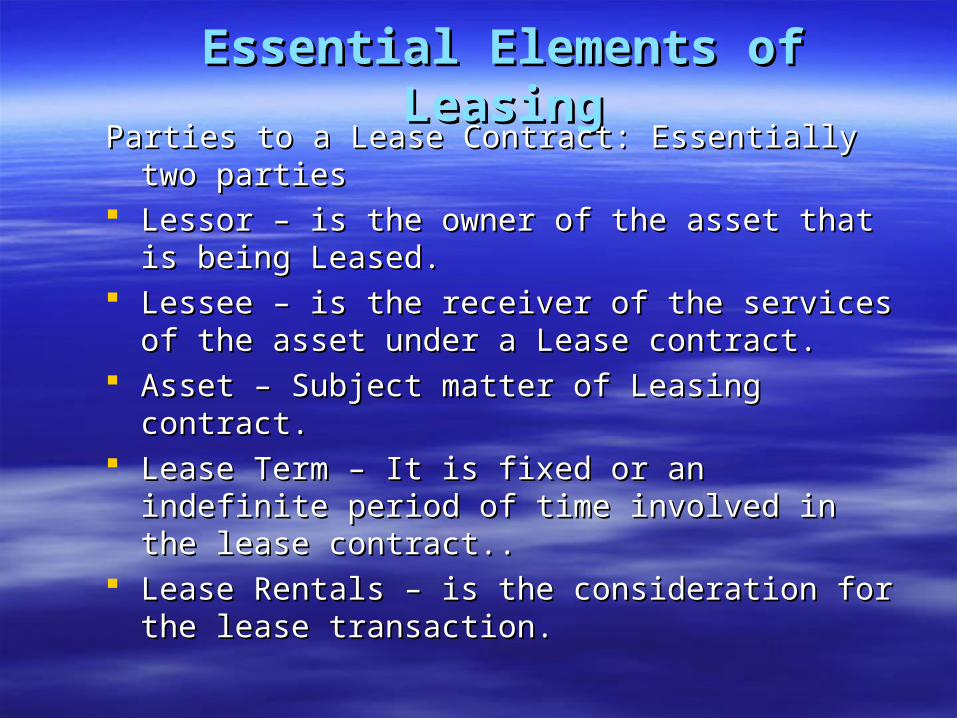

Essential Elements of Essential Elements of LeasingLeasing

Parties to a Lease Contract: Essentially two Parties to a Lease Contract: Essentially two parties parties

Lessor – is the owner of the asset that is being Lessor – is the owner of the asset that is being Leased.Leased.

Lessee – is the receiver of the services of the Lessee – is the receiver of the services of the asset under a Lease contract. asset under a Lease contract.

Asset – Subject matter of Leasing contract. Asset – Subject matter of Leasing contract. Lease Term – It is fixed or an indefinite period Lease Term – It is fixed or an indefinite period

of time involved in the lease contract..of time involved in the lease contract.. Lease Rentals – is the consideration for the Lease Rentals – is the consideration for the

lease transaction. lease transaction.

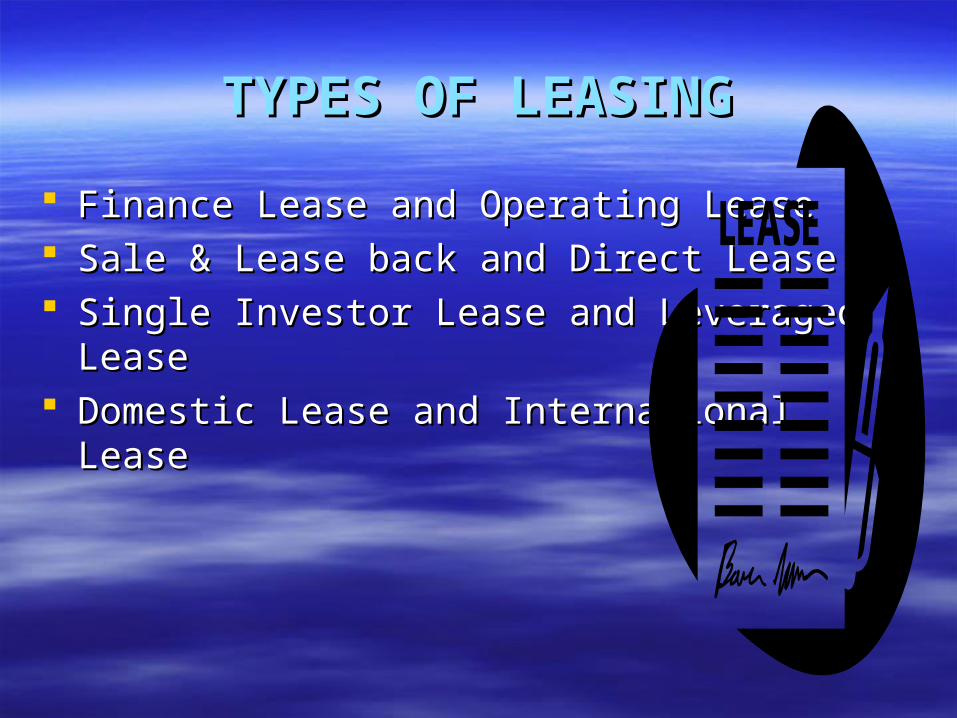

TYPES OF LEASINGTYPES OF LEASING

Finance Lease and Operating LeaseFinance Lease and Operating Lease Sale & Lease back and Direct LeaseSale & Lease back and Direct Lease Single Investor Lease and Leveraged LeaseSingle Investor Lease and Leveraged Lease Domestic Lease and International LeaseDomestic Lease and International Lease

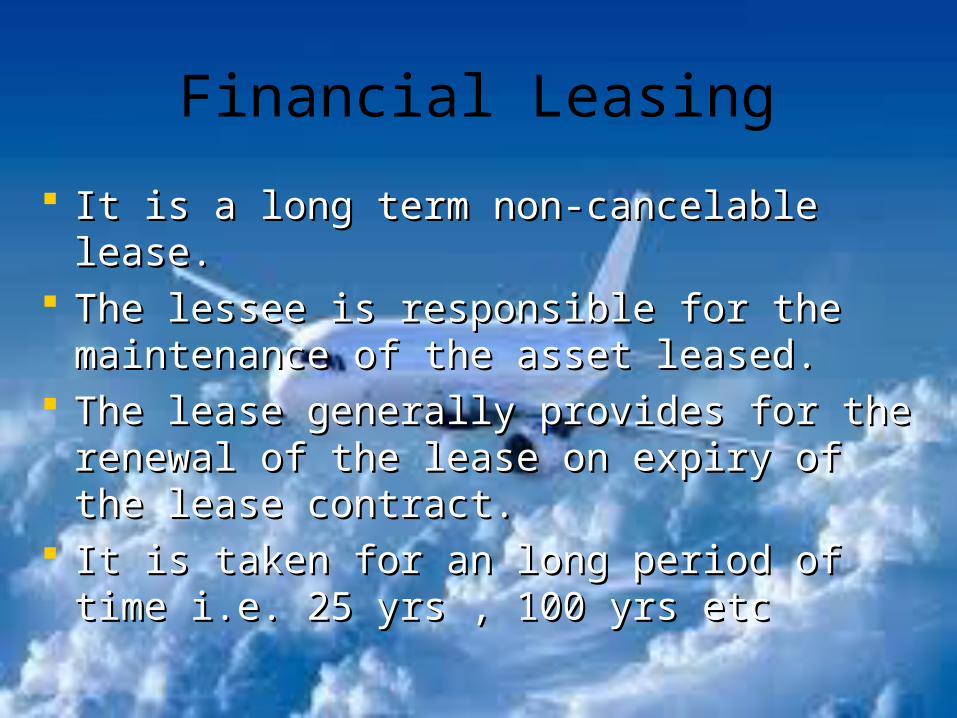

Financial Leasing

It is a long term non-cancelable lease.It is a long term non-cancelable lease. The lessee is responsible for the The lessee is responsible for the

maintenance of the asset leased.maintenance of the asset leased. The lease generally provides for the renewal The lease generally provides for the renewal

of the lease on expiry of the lease contract.of the lease on expiry of the lease contract. It is taken for an long period of time i.e. 25 It is taken for an long period of time i.e. 25

yrs , 100 yrs etc yrs , 100 yrs etc

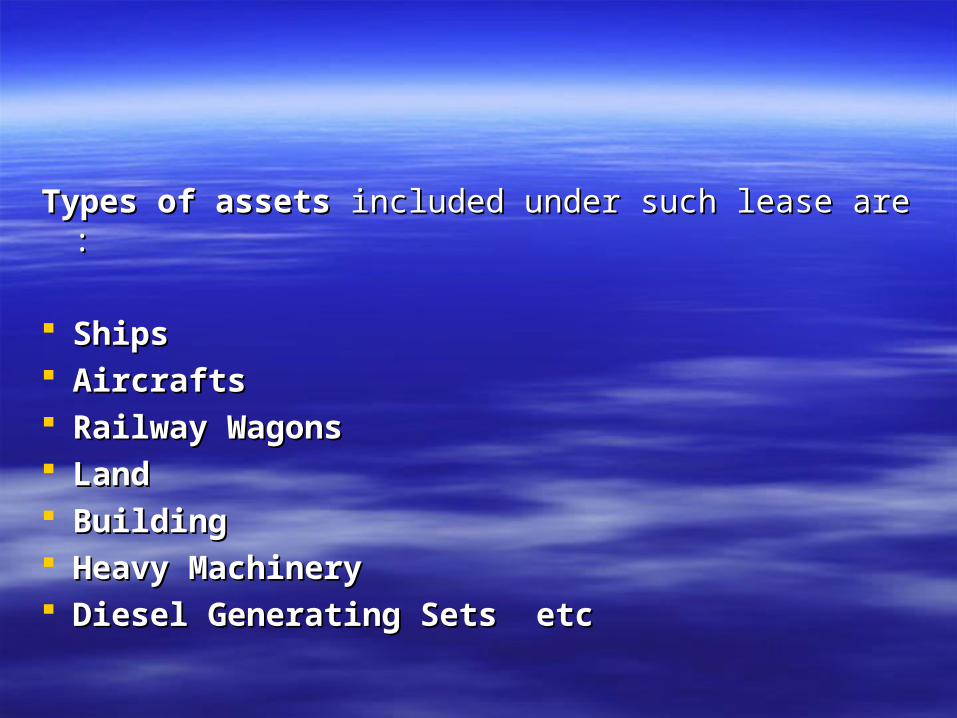

Types of assetsTypes of assets included under such lease are :included under such lease are :

ShipsShips AircraftsAircrafts Railway WagonsRailway Wagons LandLand BuildingBuilding Heavy MachineryHeavy Machinery Diesel Generating Sets etcDiesel Generating Sets etc

Operating Leasing

It is a short term cancelable lease.It is a short term cancelable lease. The lease is cancelable at short notice by the lessee. The lease is cancelable at short notice by the lessee. The Lease term is significantly less than the The Lease term is significantly less than the

economic life of the equipmenteconomic life of the equipment.. The lessee has the option of renewing the lease after The lessee has the option of renewing the lease after

the expiry of the lease periodthe expiry of the lease period Asset maintenance and insurance etc. is the Asset maintenance and insurance etc. is the

responsibility of the lessor and he charges for the responsibility of the lessor and he charges for the same.same.

It is a high risk lease to the lessor, as any time it may It is a high risk lease to the lessor, as any time it may be cancelled by the lessee.be cancelled by the lessee.

Operating leaseOperating lease is generally given for : is generally given for :

ComputersComputers Office equipmentsOffice equipments AutomobilesAutomobiles TrucksTrucks Other equipmentsOther equipments Telephones Telephones Walki - talkie Walki - talkie

Sale and Lease backSale and Lease back

In this, the lessee is already the owner of the In this, the lessee is already the owner of the asset. He, under the lease agreement, sells asset. He, under the lease agreement, sells assets to the buyer.assets to the buyer.

The buyer leases back the same asset to the The buyer leases back the same asset to the owner (now the lessee) in consideration of lease owner (now the lessee) in consideration of lease rentals.rentals.

Under the sale and lease back, the lessee not Under the sale and lease back, the lessee not only retains the use of the assets but also get only retains the use of the assets but also get funds from the sale of the assets to the lessor.funds from the sale of the assets to the lessor.

Two sets of cash flows occurTwo sets of cash flows occur::– The lessee receives cash today from the sale.The lessee receives cash today from the sale.– The lessee agrees to make periodic lease The lessee agrees to make periodic lease

payments, thereby retaining the use of the payments, thereby retaining the use of the asset.asset.

Leveraged LeaseLeveraged Lease

Arrangement for assets of huge outlay.Arrangement for assets of huge outlay. It is a 3 sided arrangement.It is a 3 sided arrangement. The lessor make an investment equal to, The lessor make an investment equal to,

say, 20% of the equipment’s original cost, say, 20% of the equipment’s original cost, and borrow the remaining 80% by lenders.and borrow the remaining 80% by lenders.

The lending company holds the title of The lending company holds the title of leased assets, while the lessor creates the leased assets, while the lessor creates the agreement with the lessee and collect the agreement with the lessee and collect the payment.payment.

If the lessee stops making the payment to If the lessee stops making the payment to the lessor, then the lessor stops making the lessor, then the lessor stops making payment to the financial institution (lender) .payment to the financial institution (lender) .

Direct LeaseDirect Lease Under direct leasing, a firm acquires the right to Under direct leasing, a firm acquires the right to

use an asset from the manufacturer directly. use an asset from the manufacturer directly. The ownership of the asset leased out remains The ownership of the asset leased out remains

with the manufacturer itself. with the manufacturer itself. Bipartite Lease – Equipment supplier-cum- Lessor Bipartite Lease – Equipment supplier-cum- Lessor

and Lessee.and Lessee. Tripartite Lease (Sales-aid-Lease) – Equipment Tripartite Lease (Sales-aid-Lease) – Equipment

supplier, Lessor and Lessee.supplier, Lessor and Lessee.

Single Investor LeaseSingle Investor Lease

• Only two parties – Lessor and Lessee. Only two parties – Lessor and Lessee.

• Leasing company (Lessor) funds the entire Leasing company (Lessor) funds the entire investment, having appropriate mix of Equity-cum-investment, having appropriate mix of Equity-cum-Debt.Debt.

• Finance raised by the Lessor, is Finance raised by the Lessor, is without recoursewithout recourse to to the Lessee.the Lessee.

When a lease agreement is made between citizen When a lease agreement is made between citizen of same countries, it is called Domestic leaseof same countries, it is called Domestic lease

When a lease agreement is made between citizen When a lease agreement is made between citizen of different countries, it is called International of different countries, it is called International leaselease

Domestic lease and International lease

Importance of lease financingImportance of lease financing

Leasing industry plays a very important role Leasing industry plays a very important role in the economic development of a country in the economic development of a country by providing money incentives to lessee by providing money incentives to lessee

The lessee does not have to pay the cost of The lessee does not have to pay the cost of asset at the time of signing the contract of asset at the time of signing the contract of lease lease

Advantages of LeasingAdvantages of Leasing

Provides full FinanceProvides full Finance FlexibleFlexible Saves from Recurring cost of financeSaves from Recurring cost of finance Absence of restrictionsAbsence of restrictions Tax BenefitsTax Benefits Useful in case of fast changing technologyUseful in case of fast changing technology Faster and Cheaper creditFaster and Cheaper credit

Limitations of LeasingLimitations of Leasing

No Benefit of Residual ValueNo Benefit of Residual Value High cost of leasingHigh cost of leasing No benefit of ownershipNo benefit of ownership Not FlexibleNot Flexible DisputesDisputes

Availability of cashAvailability of cash Effect on Borrowing CapacityEffect on Borrowing Capacity Shifting the Risk of ObsolescenceShifting the Risk of Obsolescence Convenient ArrangementConvenient Arrangement Less Restrictions on FirmLess Restrictions on Firm Salvage ValueSalvage Value Tax BenefitsTax Benefits Less ExpensesLess Expenses

Factors affecting Leasing Decisions Factors affecting Leasing Decisions

Institutions In the field of Institutions In the field of LeasingLeasing

All India Financial InstitutionsAll India Financial Institutions Leasing CompaniesLeasing Companies BanksBanks Financial CompaniesFinancial Companies Industrial Groups having Leasing CompaniesIndustrial Groups having Leasing Companies

Difficulties Faced by Leasing Difficulties Faced by Leasing Companies in IndiaCompanies in India

CompetitionCompetition Lack of Trained EmployeesLack of Trained Employees Proportion of Debt-Equity not maintainedProportion of Debt-Equity not maintained Lack of Provision for Depreciation Lack of Provision for Depreciation Low Investment of PromotersLow Investment of Promoters Shortage of FundsShortage of Funds Inefficiency of ManagementInefficiency of Management Government AttitudeGovernment Attitude

LEASING IN INDIALEASING IN INDIA

Leasing has grown by leaps and bounds in the Leasing has grown by leaps and bounds in the eighties but it is estimated that hardly 1% of the eighties but it is estimated that hardly 1% of the industrial investment in India is covered by the industrial investment in India is covered by the lease finance, as against 40% in USA and 30% lease finance, as against 40% in USA and 30% in UK and 10% in Japan.in UK and 10% in Japan.

Limitation of studyLimitation of study Although lots of care and efforts are made to Although lots of care and efforts are made to

ensure the fault free study but still there remains ensure the fault free study but still there remains certain limitations which possibly may occur.certain limitations which possibly may occur.

Lack of time acted as constraint in study.Lack of time acted as constraint in study. Researcher limitations in knowledge are also the Researcher limitations in knowledge are also the

limitation of study.limitation of study. The study is based on secondary data so any The study is based on secondary data so any

kind of discrepancy in that will cause same in the kind of discrepancy in that will cause same in the study.study.

DATA COLLECTIONDATA COLLECTION

Data source : SecondaryData source : Secondary

Secondary data was collected by using the Secondary data was collected by using the following techniques:following techniques:– BooksBooks

– WebsitesWebsites

ConclusionConclusion

The person who want to manufacture the The person who want to manufacture the

product needs an equipment to do it but not product needs an equipment to do it but not

the ownership of an equipment. The concept the ownership of an equipment. The concept

of lease finance says ‘of lease finance says ‘Eat the mangoes Eat the mangoes

rather than counting the treesrather than counting the trees OR OR why why

own a cow when milk is cheap? All you own a cow when milk is cheap? All you

need is milk and not the cow. need is milk and not the cow.

AnyAny

??