leasing in europe and beyond state of play and outlook 2015/leasing i… · form of bank lending....

TRANSCRIPT

Leasing in Europe and Beyond

State of Play and Outlook

Cascais, Portugal | 15 October

o Leasing in Europe & Beyond

o Growth in Europe

o Leased Assets & Customers

o State of the Industry

o Industry Performance

o Business Development

Agenda

Leasing in Europe &

Beyond

9.5%

9.9%

9.5%

European leasing market - new volume growth (% YoY)

Growth rates are calculated based on a homogenous sample of members reporting from year to year & are adjusted for exchange rate fluctuations 2007 onwards Source: Leaseurope Annual Surveys

Total volumes Real Estate Equipment incl

vehicles

€275.7 bil €15.4 bil €260.3 bil

New

Volumes

2014

Total outstandings:

(2013 vs 2014)

1.7%

Evolution of the European Leasing Market

Annual growth of new leasing volumes per country

Members not

reporting & non -

members

Leaseurope’s 2013 Annual Survey

Growth rates are adjusted for exchange rate fluctuations

European Leasing Market in 2013

2013/2012

0.7%

0 to 5%

5 to 10%

-5 to 0%

Under - 10%

-10 to -5%

Over 10%

0 to 5%

-5 to 0%

Under - 10%

-10 to -5%

Annual growth of new leasing volumes per country

Members not

reporting & non -

members

Leaseurope’s 2014 Annual Survey

Growth rates are adjusted for exchange rate fluctuations

2014/2013

9.5%

0 to 5%

5 to 10%

-5 to 0%

Under - 5%

10 to 20%

0 to 5%

-5 to 0%

Over 20%

European Leasing Market in 2014

Biannual growth of new leasing volumes per country

Members not

reporting & non -

members

0 to 9%

10 to 20%

-9% to 0

Under -20%

-10 to -20%

Over 20%

H1 2015/2014

9.1%

Source: Leaseurope Member Associations

25 Member Associations reporting; growth rates adjusted for exchange rate fluctuations

European Leasing Market in H1 2015

Leased Assets &

Customers

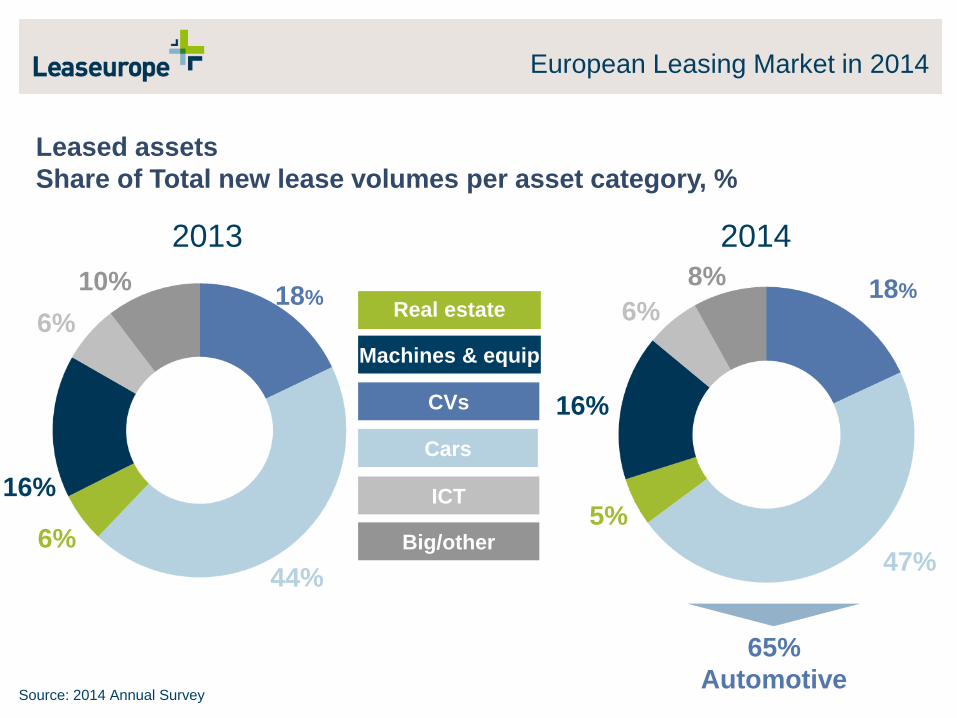

Leased assets

Share of Total new lease volumes per asset category, %

Source: 2014 Annual Survey

2013

65%

Automotive

Machines & equip

Cars

CVs

ICT

Big/other

Real estate

2014

6%

16%

6%

44%

18% 10% 18%

47%

5%

16%

6%

8%

European Leasing Market in 2014

-10%

-5%

0%

5%

10%

15%

20% Total

New lease volumes per asset type – % period on period

(2014/2013)

-15%

Real estate Movables

Growth rates are calculated based on a homogenous sample of members reporting from year to year & are adjusted for exchange rate fluctuations

Source: 2014 Annual Survey based on 33 members reporting

-10%

-5%

0%

5%

10%

15%

20%

-15%

9.5% 9.9% 9.5%

-5%

0%

5%

10%

15%

20%

25%

10.9%

0.9%

-10%

-15%

-20%

Machinery ICT CVs Cars Big Other

10.6%

14.6%

-21.9%

-0.2%

European Leasing Market in 2014

24%

NA

20% to 25%

25% to 30%

10% to 15%

15% to 20%

< 10 %

Lease penetration is the share of total investment financed by leasing calculated as new leasing volumes (excluding consumers)/ gross fixed capital formation in equipment Based on data from Leaseurope’s 2014 Annual Survey

Equipment

penetration

Share of equipment investment financed by leasing (2014)

> 30%

European Leasing Penetration

Evolution of leasing penetration in Europe

19 countries (1999-2014)

Lease penetration is the share of total investment (excluding residential real estate) financed by leasing calculated as new leasing volumes / gross fixed capital formation for the 19 associations reporting from ’99-’14 Source: Leaseurope, Eurostat and AMECO (GFCF)

European Leasing Penetration

10

30

50

70

90

110

130

150

170

190

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

No

rmali

sed

PR

1999 =

100

Total Equipment Real estate

Leasing clients

New movables leasing volumes by client sector

(2014)

Source: 2014 Annual Survey

European Leasing Market in 2014

Businesses

72%

Consumers

23%

Public sector

3%

Other

2%

% movable

leasing

volumes

Leasing is the most important external finance contributor to SME

investment spending

• SMEs financed 18.9% of their

total investment via leasing in

2013, more than any individual

form of bank lending.

• Bank loans of more than three

years accounted for 15.5% of

SME investment finance in

2013, with the proportion falling

as the bank loan duration

shortens.

• Leasing penetration rates

estimated to have grown in

2014, while cash/equity and all

forms of bank lending are to

decline.

18.9% 21.2%

30.5% 29.1%

7.3% 6.7%

10.0% 9.4%

15.5% 15.0%

17.8% 18.6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2013 2014

Leasing Cash/EquityShort-term credit Loan 1-3 yrsLoan >3 yrs Other debt

Investment finance in 2013-2014, all SMES

Proportion of investment financed by:

Source : Oxford Economics/EFG

Leasing to European SMEs

Source: "The Use of Leasing Amongst European SMEs", 2015

Percent of SME investment by finance type in 2013-2014

State of the Industry

2014 Ranking survey results • Value of total new contracts within Europe in 2014 (€ thousands)

*These companies also have operations outside Europe

Name Country EU

Countries

Value

2014

Value

2013

1 Société Générale Leasing Solutions (incl. ALD) * France 29 13,961,140 11,966,354

2 BNP Paribas Leasing Solutions (incl. Arval) * France 19 13,402,300 11,920,580

3 Volkswagen Leasing GmbH Germany 3 12,205,747 -

4 De Lage Landen International B.V. * Netherlands 21 10,036,511 9,735,033

5 Deutsche Leasing * Germany 19 7,436,400 7,386,827

6 UniCredit Leasing Italy 17 6,857,850 6,725,231

7 Nordea Finance Sweden 7 5,109,309 4,916,568

8 Alphabet International * Germany 13 4,780,000 4,190,000

9 LeasePlan Corporation N.V. * Netherlands 24 4,775,378 4,460,192

10 Crédit Agricole Leasing & Factoring * France 4 4,421,734 4,002,907

Characteristics of European Market Players

2014 Ranking survey results • Value of total new contracts within Europe in 2014 (€ thousands)

Name Country EU

Countries

Value

2014

Value

2013

11 CM-CIC BAIL France 7 3,577,095 3,540,810

12 DNB Finans Norway 3 3,076,198 2,949,638

13 LBBW Leasing * Germany 3 2,934,355 -

14 RCI Banque * France 36 2,901,783 2,843,589

15 ING Lease Netherlands 5 2,547,906 2,259,142

16 NATIXIS LEASE France 3 2,487,900 -

17 Siemens Financial Services GmbH * Germany 11 2,285,137 2,318,385

18 Raiffeisen Leasing * Austria 19 2,210,641 1,979,186

19 OJSC VEB Leasing * Russia 9 2,087,821 4,154,869

20 OJSC VTB Leasing Russia 4 1,777,099 1,342,517

*These companies also have operations outside Europe

Characteristics of European Market Players

Source: Leaseurope 2014 Ranking Survey of Top European Leasing Companies, BCS June 2015

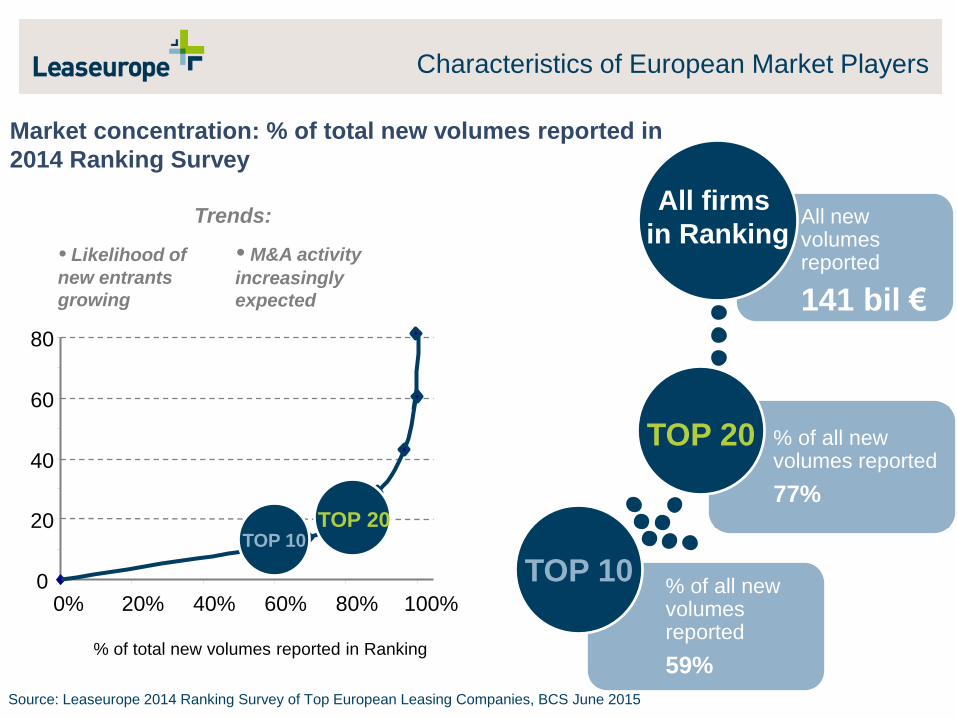

Market concentration: % of total new volumes reported in

2014 Ranking Survey

% of all new volumes reported

59%

% of all new volumes reported

77%

TOP 20

TOP 10

All new volumes reported

141 bil €

All firms

in Ranking Trends:

• Likelihood of

new entrants

growing

• M&A activity

increasingly

expected

% of total new volumes reported in Ranking

0

20

40

60

80

0% 20% 40% 60% 80% 100%

TOP 10 TOP 20

Characteristics of European Market Players

Source: Leaseurope 2014 Ranking Survey of Top European Leasing Firms

New Volumes granted

by TOP 20 (LHS) 2014

All firms

New volumes granted

by all firms (LHS)

Number of firms using

channel (RHS)

TOP 20 firms

2013

From 5% to 6% of

new volumes

From 32% to

31% of new

volumes

Distribution channels used by partaking firms in 2014 Ranking Survey

0

10

20

30

40

50

60

0

5

10

15

20

25

30

35

40

45

50

New

bu

sin

ess v

olu

me

s €

bill

0

2

4

6

8

10

12

14

16

18

20

0

5

10

15

20

25

30

35

40

45

50

New

bu

sin

ess v

olu

me

s €

bill

Characteristics of European Market Players

Industry Performance

Source: Leaseurope Index

The Leaseurope Index – median ratios (2013-Q2 2015)

Profitability ratio Cost / income ratio

Cost of risk ratio

Leaseurope Index

Source: Leaseurope Index

The Leaseurope Index – median ratios (2013-Q2 2015)

RoA RoE

Leaseurope Index

Leaseurope Index: Segment Survey 2014

• An annual supplement to the quarterly Index

• Financial ratios: profitability, cost/income, cost of risk and return on

assets

• Broken down by four asset types: equipment, real estate, passenger

cars and commercial vehicles

• The 2014 survey is the fourth edition of the project

Leaseurope Index

Profitability per asset segment, medians (2010-2014)

26.1%

32.5% 31.1% 34.0%

35.7%

39.6%

30.2%

5.3%

12.3%

24.8% 27.5%

34.8%

29.1% 32.1%

39.4%

31.3%

35.6%

31.9% 34.9%

29.1%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2010 2011 2012 2013 2014 2010 2011 2012 2013 2014 2010 2011 2012 2013 2014 2010 2011 2012 2013 2014

Equipment Real estate Passenger cars & LCVs Commercial vehicles

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Q12014

Q22014

Q32014

Q42014

Q12014

Q22014

Q32014

Q42014

Q12014

Q22014

Q32014

Q42014

Q12014

Q22014

Q32014

Q42014

Equipment Real estate Passenger cars & LCVs Commercial vehicles

Leaseurope Index

Cost/income per asset segment, medians (2010-2014)

39.2% 41.5%

43.2% 43.0%

35.7% 34.8%

39.2%

44.7% 45.3% 41.4% 41.6% 42.7%

50.9% 49.2%

45.3% 41.9%

36.4%

44.0%

49.0% 47.7%

0%

10%

20%

30%

40%

50%

60%

2010 2011 2012 2013 2014 2010 2011 2012 2013 2014 2010 2011 2012 2013 2014 2010 2011 2012 2013 2014

Equipment Real estate Passenger cars & LCVs Commercial vehicles

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Q12014

Q22014

Q32014

Q42014

Q12014

Q22014

Q32014

Q42014

Q12014

Q22014

Q32014

Q42014

Q12014

Q22014

Q32014

Q42014

Equipment Real estate Passenger cars & LCVs Commercial vehicles

Leaseurope Index

Cost of risk per asset segment, medians (2010-2014)

Leaseurope Index

1.0%

0.8% 0.8%

0.7%

0.5% 0.4%

0.3%

0.7% 0.7%

1.1%

0.6%

0.4%

0.3%

0.5%

0.3%

0.6%

0.4% 0.4%

0.6%

0.3%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

2010 2011 2012 2013 2014 2010 2011 2012 2013 2014 2010 2011 2012 2013 2014 2010 2011 2012 2013 2014

Equipment Real estate Passenger cars & LCVs Commercial vehicles

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Equipment Real estate Passenger cars & LCVs Commercial vehicles

RoA per asset segment, medians (2010-2014)

Leaseurope Index

0.7%

1.1% 1.0%

1.1% 1.2%

0.6%

0.3% 0.3% 0.2%

0.1%

1.0%

1.3% 1.3% 1.3%

1.9%

0.9% 1.0%

1.1%

0.8% 0.7%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

2.0%

2010 2011 2012 2013 2014 2010 2011 2012 2013 2014 2010 2011 2012 2013 2014 2010 2011 2012 2013 2014

Equipment Real estate Passenger cars & LCVs Commercial vehicles

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Q1 2014

Q2 2014

Q3 2014

Q4 2014

Q1 2014

Q2 2014

Q3 2014

Q4 2014

Q1 2014

Q2 2014

Q3 2014

Q4 2014

Q1 2014

Q2 2014

Q3 2014

Q4 2014

Equipment Real estate Passenger cars & LCVs Commercial vehicles

Business

Development

The European market is one of the largest leasing markets in the

world. Leasing plays a central role at the heart of the real economy.

Future trends

Develop services and solutions (mobility…)

Finance new markets (cloud, third platform, new energy…)

Foster innovation (big data…)

Asset focus and specialisation (new energy…)

Support customers and vendors globally

Looking ahead, the European leasing industry must be a at the

forefront of innovative financing solutions in order to take

advantage of the shift from “ownership” to “usage”

Concluding Remarks From 2014

Balance of expectations for business over next six months

Balance between respondents expressing positive and negative opinions of the outlook over the next six months

Source: Leaseurope/Invigors Business Confidence Survey June 2015

Margins

Bad Debt

Business Confidence Survey

Net Profit

New Business Volumes

Leasing in Europe and Beyond

State of Play and Outlook

Cascais, Portugal | 15 October