leave nostone unturned. -...

TRANSCRIPT

Compiled for the Coachella Valley Economic Partnership by John E. Husing, Ph.D., Economics & Politics, Inc.

The Coachella Valley Economic Report. 2008

Leaveno stone

unturned.

CVEP, AS AN ORGANIZATION, was formed

approximately 12 years ago as primarily

a business-driven economic development

organization with an important, albeit

limited, role for local government. For

over a decade now our private sector has

done a remarkable job of attracting new

wealth, jobs and opportunity to our com-

munity. It was also during that decade

that our country, and Riverside County in

particular, had unprecedented economic

growth. Over the recent two years, as our

economic markets have gone through a

period of adjustment and budgets became

increasingly tight, funding for CVEP lev-

eled off to a point where our resources

could not keep pace with our success.

As a result, this past year we made a

concerted effort to provide greater

involvement for our regional govern-

mental entities and Native American

tribes – and they have stepped up in a big

way. We have roughly doubled the fund-

ing for the organization and financially

positioned it to move to the next level on

behalf of the entire Coachella Valley.

This level of commitment by our public

sector leaders is a testament to the vision,

entrepreneurship and leadership in our

valley. After all, economic development

is not just about creating jobs: it’s about

inculcating, molding and shaping our

future for decades to come. We are all

pulling the same oar. Nowhere has this

been better demonstrated than in the

increased contributions of our partners

this year. For example, at a time when

earnestly seeking to expand its desert

campus, UCR gave the first $50,000

towards our expansion effort. Desert Hot

Springs was next with a contribution of

$50,000, followed by Eisenhower Medical

Center. The list goes on and on, but I men-

tion these three organizations in particu-

lar because all of them are in the midst of

their own significant financial challenges,

yet they saw it fit and appropriate tomake

an investment in the future of our valley.

They realized that their success potential

is greatly enhanced by CVEP’s success

and that requires a cohesive, well-funded,

regional economic effort.

Palm Desert and Indian Wells each con-

tributed $50,000 and every other valley

city nearly tripled their previous contri-

butions to CVEP. Additionally, Imperial

Irrigation District has committed $100,000

per year over the next three years, making

them CVEP’s largest single contributor.

Simply put, we all pulled together toward

this one common goal. Congratulations.

This coming year, thanks to your increased

support, CVEPwill be proactively develop-

ing a new regional economic model and

restructuring our organization to better

reflect all of the stakeholders in our valley.

Together we can and will shape our

tomorrow with a renewed vigor.

Thank you for your support of the

Coachella Valley Economic Partnership.

A MESSAGE FROM THE CHAIRMAN

Jim Ferguson

Chairman of the Board

3

TOP IC PAGE

A Letter from Jim Ferguson, Chairman of the Board 1

Executive Committee and Board of Directors 2007-2008 4

A Message from John Soulliere, President/CEO 6

PENTA: Building a Foundation for Success 10

Career Pathways for a 21st Century Workforce 13

Coachella Valley Economy: Brief Analysis 14

Exhibit List 21

Demographics 24

Employment 32

Housing 44

Taxable Sales 50

Banking 54

Assessed Valuation 58

Crime Rates 62

Education 64

Colleges and Universities 66

Appendix (Employment & Payroll Detailed Tables) 68

Coachella Valley Economic Report, 2008

TABLE OF CONTENTS

PLAT INUM SPONSORS

GOLD SPONSORS

MED IA SPONSORS

MORNING KEYNOTE SPEAKER SPONSOR

BUILDING INDUSTRY ASSOCIATION - DESERT CHAPTER

SILVER SPONSORS

A.A. WEBB AND ASSOCIATES • AGUA CALIENTE CASINO RESORT SPA • CANYON NATIONAL BANKCITIBANK • CITY OF PALM SPRINGS • ORR BUILDERS • PETERSON SLATER & OSBORNERIVERSIDE COUNTY EDA • SOUTHERN CALIFORNIA EDISON • VERIZON FOUNDATION

NEW MEMBER SPONSOR HOSPITALITY SPONSOR

THE PENTA BUILDING GROUP THE CHANK GROUP

CITY SPONSORS

City of Cathedral City • City of Coachella • City of Desert Hot Springs • City of IndianWellsCity of Indio • City of La Quinta • City of Palm Desert • Town of Yucca Valley

PRESENTED BY

4

Coachella Valley Economic Partnership

EXECUT IVE COMMITTEE

2007-2008

Thank you to the following individuals and the organizations they represent, for

their dedication and commitment to CVEP this past year:

Chairman: Jim Ferguson, Ferguson Law Firm

Immediate Past Chair: Bob Marra, Wheeler’s Market Intelligence

Vice Chairperson: Michelle Krans, The Desert Sun

Secretary: Kevin McGuire, Palm Desert National Bank

Treasurer: Aubry Serfling, Eisenhower Medical Center

Member-at-Large: Ben Scholten, Rabobank

Member-at-Large: Lee Morcus, Kaiser Restaurant Group

Member-at-Large: Steve Pougnet

Member-at-Large: Kathy DeRosa, City of Cathedral City

Public (West): Agua Calliente Band of Cahuilla Indians

Public (East): City of La Quinta

EXECUTIVE LEVEL MEMBERS

City of Desert Hot Springs

City of Indian Wells

City of Palm Desert

Economic Development Agency of Riverside County

IID Energy

University of California Riverside/Palm Desert Campus

BOARD LEVEL MEMBERS

Agua Caliente Band of Cahuilla Indians Albert A. Webb Associates

Best Best & Krieger LLP Blytheco, LLC

Burrtec Waste & Recycling Services Citibank

City of Cathedral City City of Coachella

City of Indio City of La Quinta

City of Palm Springs City of Rancho Mirage

Delfino Palm Desert Desert Regional Medical Center

Eisenhower Medical Center Granite Construction

Integrated Wealth Management Kaiser Restaurant Group

Kaiser Permanente Pacific Western Bank

Palm Desert National Bank Rabobank

Southern California Edison Southern California Gas Company

Spotlight 29 Casino Sunline Transit Agency

The Desert Sun Time Warner Cable

Verizon Communications

A M E S S A G E F R OM

J O HN S O U L L I E R E , P R E S I D E N T / C E O

Leaveno stone

unturned.

I M A G I N E .

Envision what our future can be.

INSP IRE .Instill vision and motivate others towards action.

C O L L A B O R A T E .Lock arms and press toward our defined goals.

A C H I E V E .The outcomes of our hopes and dreams begin to appear.

8

Most of us have heard the expression

“the Devil is in the details.” No doubt

many of us have experienced the reality

of that phrase when some theoretically

“great” idea failed due to overlooking a

seemingly insignificant detail. Maybe a

lesser known fact is that this phrase is

believed to be a variation of “God is in

the details.” Whether you approach it

from a positive or negative perspective

the point is clear — details matter!

When it comes to the economy of the

Coachella Valley, the Coachella Valley

Economic Partnership (CVEP) has been

committed to working with its partners

to better understand those details in the

hope of moving our region towards a

sustainable, prosperous future.

Even as the country is facing

extraordinary economic chal-

lenges, we (CVEP and the

greater Coachella Valley

community) cannot afford to

be paralyzed by fears of what

may come. Wemust take control

of our destiny through utilizing this

down cycle to plan for eventual recov-

ery. Readiness will be a key to our suc-

cess as an organization and as a region in

the future. We will either uncover the

opportunities of change or allow “fate”

to take us forward to a destination that

may or may not be something we want.

The theme of CVEP’s expanded 2008

Economic Summit is “Leave No Stone

Unturned.” The phrase originates from a

Greek legend about a lost treasure. When

asked where to find this great prize, the

Oracle responded, “leave not one stone

unturned.”

For our purposes, the phrase suggests

that if we are to uncover the yet-to-be-

discovered treasures of the Coachella

Valley’s economic potential, we must

investigate every possibility, sparing no

effort. Moreover, we propose that there

are four great “stones” that must be

turned over to lead us to

our prize. These

stones are called

imagine, inspire,

collaborate, and

achieve.

I M A G I N E

We can only begin to

discover the economic potential of

our region by first daring to imagine

what it can be. The great sculptor

Michelangelo is reputed as having said,

“In every block of marble I see a statue as

plain as though it stood before me …. I

John Soulliere

9

have only to hew away the rough walls

that imprison the lovely apparition to

reveal it to other eyes

as mine see it.” To

imagine is to

envision.

I N S P I R E

Inspire is

comprised of

instilling vision and motivating others

towards action. Once we

imagine what we can

be, we are compelled to

ignite that vision in the

minds of others. When we

look at the Coachella Valley,

are we able to identify a com-

mon vision for an economically

sustainable future?

C O L L A B O R A T E

To collaborate is to lock arms and press

toward our defined goals. The most criti-

cal components of this idea are agree-

ment and resource allocation. If we agree

upon the goal and understand its impor-

tance, we focus our resources to both

develop and implement a strategy to

achieve it. Remember, after the planning

the real work begins.

A C H I E V E

Finally, we achieve. The outcomes of our

hopes and dreams begin to appear on

the horizon. More importantly, we

have been responsible at this

point in our regional

history to create

and pass on a

working model to the

next generation.

For 2008-09, CVEP has

been pledged financial

support to spearhead a

comprehensive

and candid

look at the

economic

potential of

the Coachella

Valley— its

strengths and weaknesses, its opportuni-

ties and threats. This analysis will create

a foundation from which a regional

“Blueprint for Economic Success” will be

developed. This Blueprint will enable

CVEP to focus its efforts on aggressive

business attraction while continuing to

influence development of community

amenities that will increase the region’s

draw to industry and higher wage jobs.

Regional economic development must

be approached holistically, taking into

account every asset of the

broader community and

presenting it to indus-

try decision makers as

a complete Coachella

Valley package.

I am honored to have served

with the Board of Directors, Executive

Committee and general members

throughout this, my first year with CVEP.

Special thanks go out to those organiza-

tions and individuals who determined

that continued and increased financial

support of CVEP in the face of these most

challenging times is an investment in

the future of the entire region.

Additionally, thanks to those who have

become partners this past year. Your

investment will help build a more effec-

tive organization to the benefit of our

Coachella Valley.

This Blueprint will enable CVEP to focus its efforts on aggressive

business attraction while continuing to influence development

of community amenities that will increase the region’s draw to

industry and higher wage jobs.

10

The PENTA Building Group has played a

role in the growth and development of

the Coachella Valley since 2002. With its

ongoing presence over the last 6 years,

PENTA officially opened its most recent

office in Palm Desert, California in 2008,

where they now have a staff in excess of

20 full-time professional employees.

Their experienced team, led by the owners

and senior management, is committed

to a shared responsibility of value, reliabil-

ity, integrity, quality and results. PENTA

prides itself on providing a personalized

approach toall general contracting services.

PENTA is headquartered in Las Vegas,

with offices in Palm Desert, CA and Reno,

NV. From their inception in 2000, PENTA

has strived to gather the best team in the

business, providing the foundation for

well managed expansion.

As a testament to the leadership and ded-

ication of the founding principals, the

PENTA team has reached revenue levels

in excess of $600 million per year and

has quickly established itself as one of

the leading private commercial general

contractors in the nation. Recently,

PENTA was ranked among the top 400

general contracting firms nationally

by Engineering News Record, currently

103rd in the nation (2008).

The success and experience of PENTA

spans a wide variety of market segments

including gaming, hotel and timeshare

resorts, convention/meeting facilities,

restaurants and related venues, educa-

tional and other institutional facilities,

retail, industrial/distribution and park-

ing garages.

PENTA’s projects range in size from

$200,000 to in excess of $300,000,000.

Some of their more notable recent large

projects include World Market Center

Building 3 and Aliante Hotel Casino, both

located in Las Vegas.

However, in addition to doing the “ground

up” construction of new projects, they

have extensive experience and capabili-

ties in small renovations, remodels, and

tenant improvement build-outs, as well

as expansions, small and large, of exist-

ing facilities. A significant, continuous

portion of their backlog consists of these

types of projects.

They can provide their services on a

Construction Manager at Risk basis, with

preconstruction services (budgeting,

scheduling, constructability review, etc.)

commencing early in the design phase,

under a traditional general contractor

arrangement, or on a Design-Build basis.

PENTA Palm Desert is proud to have been

a part of some of the most exciting and

challenging projects in the Coachella

Valley, including The Spa Resort Casino

in downtown Palm Springs, Desert Water

Agency, Agua Caliente Casino Renovation,

Tribal Administration Plaza, Agua Caliente

Casino Headliner Room and the Gaming

Commission Renovation.

PENTA is privately held, and possesses

a very impressive financial statement,

bonding capacity, and a commendable

safety record.

For more information about The PENTA

Building Group and the services they

offer, call 760.776.6111 or visit their web-

site at www.pentabldggroup.com.

PENTA: Building a Foundation for Success

11

12

13

Imagine a region that brings together all

systems of education, K to University, in

a collaborative effort with business to

create career pathways strategies for its

future economy. Then imagine this same

regional collaboration launching a $10

million scholarship and student support

system to move more students into and

through college in fields of study related

to the new economy.

The Coachella Valley, under the leadership

of CVEP, has done exactly that by creating

the Career Pathways Initiative and the

Pathways to Success scholarship support

program. With support from major foun-

dations and local partners, CVEP has

transformed the region’s understanding

of economic development in order to

achieve a workforce that is technically

competent and educated to meet the

needs of new industry.

CVEP has inspired the region to link

business, education, local governance

and social support systems in an all out

effort to make education relevant to the

world of business and to put educators

and business leaders into new relation-

ships through industry councils and col-

laborative relationships that change the

way we teach our students.

The models that are evolving in the

Coachella Valley have been widely rec-

ognized by organizations such as The

Ford Motor Company Fund, James

Irvine Foundation and the College

Access Foundation, to name a few. These

organizations recognize the work of

CVEP and its business and education

partners throughout the Coachella

Valley as the wave of the future for

developing a qualified, well educated

and prepared workforce.

Career Pathways for a 21st Century WorkforceLinked to a Regional Higher Education Scholarship and Student Support Strategy

We invite your business to join our team.

A commitment to the Coachella Valley

and CVEP assures direct linkages to the

educational innovations of the region

and access to a transformative approach

to economic development.

Join us as we explore and implement

these innovative new strategies. For

more information, refer to our website:

www.cvep.com.

14

Coachella Valley Economy: BR I EF ANALYS I S

John E. Husing, Ph.D.

15

In 2008, the Coachella Valley’s economy is caught up in the difficulties unleashed

by the excesses of the recent housing boom in Southern California. The current

situation began because Southern California’s home construction has not kept up

with its population growth over the past twenty years. As a result, once the

post-Cold War recession ended, home prices began rising primarily to chase away buyers

since there were not enough houses to fill all of the demand. In roughly 2004, speculators

began noticing how fast home prices had been rising and entered the market with a

vengeance. Sub-prime and alt-A financing also entered the picture that year. Together, they

helpedpower an existinghomeprice gain of 30.8% in theCoachella Valley in 2004. The jump

was 22.6% in 2005. Those high increases caused sales to slow, but prices continued upward

rising by 6.6% in 2006 and 1.6% in 2007 before the collapse of –21.3% through 2nd quarter

2008. That drop took the median price back to roughly its $365,000 level of 2004, leaving

many buyers who purchased from 2004-2007 upside down on their mortgages.

Home sales were affected by this pricing pattern. From

late 2001 until second quarter 2004, the Coachella

Valley’s seasonally adjusted existing home sales soared

98.4% to 2,061 quarterly units. However, as prices rose

rapidly through 2004-2007, volumes began falling, even-

tually reaching a modern low of 948 units by 4th quar-

ter 2007. Sales have since jumped 35.1% to 1,280 units as

foreclosure sales have shown that there is significant

demand at 2004 prices.

As the data in this report show, the decline in home

sales has led to difficulties in numerous aspects of the

Coachella Valley’s economy. Construction jobs and pay-

roll have decreased, hurting a crucial employment sec-

tor for the valley’s many blue collar workers. Retail

sales have fallen as people are not buying furniture,

appliances and home improvement supplies. High gaso-

line prices have contributed to the retail sales difficulty

as they have reduced vehicle purchases as well as the

retail spending of lower income consumers. As the

sales tax is the primary source of discretionary funding

for municipal governments, their budgets are being

commensurately hurt. Assessed valuation was not down

in 2008 but will be in 2009, adding to this difficulty.

Meanwhile, bank deposits are off, including on a per

capita basis, indicating the economic downturn is direct-

ly affecting household incomes.

Looking ahead, a return to economic prosperity will

take a housing market recovery. Here, the key is the sig-

nificant increase in home sales that has occurred in

2008 now that prices have returned to 2004 levels. This

is a sign that there remains a pent-up demand for

homes. Importantly, realtors report multiple offers

from families wanting to buy the repossessed homes

being offered at these prices. It indicates that this is

likely the level of pricing that will emerge once the

flow of foreclosures has halted. This situation gives the

Coachella Valley three short-term challenges:

� It needs to take advantage of recent federal legislation

to reduce the number of foreclosures as fast as possible.

Until that flow is significantly diminished, the current

economic difficulties will persist.

� It needs to find ways to ensure that home builders

can produce homes at 2004 prices. This is a challenge,

given the increases in fees, material and labor cost

since 2004. It will require adjustments in the sizes of

homes, sizes of lots, types of products built and the fees

charged to build homes.

� It needs to ensure that foreclosed homes that cannot

be easily inhabited are retrofitted and sold to families,

not sold “as is” at auction to landlord investors who

can upset the nature of single family neighborhoods by

injecting large numbers of renters into them.

Looking longer term, the data in this report show that

apart from the housing cycle, the Coachella Valley’s

16

The skills required to work in these sectors often do

not require well-educated workers. The major excep-

tion to this fact is the valley’s large health care sector.

� The Coachella Valley’s agricultural heritage has meant

that, historically, a significant blue collar population has

always lived in it. Though agriculture is now less of a

growth force, many people from these families consti-

tute a significant share of the local labor force. This

working population has tended to live in Indio,

Coachella, Desert Hot Springs and Cathedral City, while

their jobs have often been in the other five cities. Though

recent housing trends have tended to breakdown some

of this separation, the valley still has a significant divi-

sion between cities with high income people needing

services and cities with modest income residents

who provide them.

These facts about the economic life of the Coachella

Valley, today, present the area with its long-term eco-

nomic challenges:

� How to broaden the economy away from the exag-

gerated influence of the ebbs and flows of U.S. discre-

tionary income to even out the levels of its peaks

and valleys.

� How to plan for an economy with a much larger full-

time retirement population and use that emerging

trend to help stabilize the valley’s ebbs and flows.

� How to take advantage of the migration of the edge

of urbanized Southern California into the portions of

the valley closest to San Gorgonio Pass to help diversi-

fy the economy.

� How to develop industries that will employ well-edu-

cated and higher paid workers and help raise the

incomes of local workers.

� How to raise the educational aspirations and achieve-

ment of the region’s school children as well as its adult

workforce, given that higher paying jobs tend to require

greater levels of education and/or skill.

Dealing with these broad issues requires the develop-

ment and execution of economic strategies. This has

economy can still be thought of as a relatively isolated

economy operating according to dynamics that, while

related to the Inland Empire and Southern California,

have distinctive rhythms and elements. This is the case

for five reasons:

� The area is a national destination for tourists and

conventions plus people with seasonal second homes.

As the flow of these people to the Coachella Valley is

heavily dependent upon U.S. discretionary income, the

Coachella Valley’s economy has tended to have an

exaggerated business cycle: soaring in good times and

plunging in bad times. That said, in the past four years,

that fact has not been in evidence, with the valley actu-

ally fluctuating less than the surrounding Inland

Empire. This is likely the result of the Coachella Valley’s

growing a full time resident population.

� The region has grown up as an important Southern

California and national retirement center. As a result,

an important portion of its economy is devoted to pro-

viding services to an aging population. This is seen in

its health care industry as well as its retail, restaurant

and entertainment (including golf courses and tennis

clubs) sectors. With the baby boomer generation now

at 62 years old, residential construction has been added

as a major economic force. Meanwhile, the number of

full time residents of the area is growing as retirees,

many from Southern California, make the decision to

migrate to the valley.

� The expanding frontier of Southern California’s

urban economy has not yet reached the valley. Thus,

the jobs within the region tend to be filled by local res-

idents while relatively few local residents tend to be

commuters to jobs outside of it. This fact means that

the economy can be thought of as one that ebbs and

flows according to the volume of dollars flowing into it

from any location outside of it. That isolation will like-

ly break down now that the edge of the urban region is

in Beaumont and heading east along the I-10 freeway.

� An economy that evolves based upon providing

services to tourists, conventions, seasonal second

homeowners and a growing base of retirees is one in

which a significant share of the job base is in retailing,

consumer services, hotels, amusement and construction.

17

become the essential mission of the Coachella Valley

Economic Partnership. Some comments on the directions

which their work can and/or is taking are thus in order:

� Certainly, the valley will continue to welcome the

influx of spending by national tourists, conventions

and seasonal residents. These outside flows of dollars

are a key portion of the region’s prosperity, because as

this money changes hands locally, it has a multiplied

impact on the area’s economy. The issue is not how to

lower these flows of outside funds, but rather to broad-

en the economy with other sources of funds that are

not subject to the seasonal and national business cycle

fluctuations inherent in an economy heavily based on

this form of spending.

� One way to broaden and stabilize the Coachella

Valley’s economy is being naturally presented to it by

the aging of the baby-boomer population. Already,

numerous members of this generation are beginning

to eye the valley as their full-time retirement home.

Many of the couples making these decisions are

Southern Californians and are not afraid of the heat

that impacts desert areas in the summer. Their retire-

ment incomes will provide the region with a year-

round source of outside dollars that will serve to blunt

the Coachella Valley’s seasonal cycle. And, as pension

incomes are relatively stable, they will also have the

desired impact of blunting the ebbs and flows that

hit the local economy when the U.S.

economy goes through its business

cycles. In effect, this flow of

retirees is a trend that should be

encouraged by the valley’s leaders.

� Like it or not, the edge of urban

Southern California is now quite close to the Coachella

Valley. The outward migration of residential construc-

tion for a commuter population has now reached

Beaumont along the I-10 freeway. While the recent

building cycle has come to a difficult end, the shortage

of housing in Southern California makes the next up-

tick inevitable. When it occurs, Banning will be the

next city caught up in a building boom, followed by

north Palm Springs and Desert Hot Springs. This will

put added pressure on the valley’s I-10 linkage to the

balance of Southern California as many of these new

residents will be commuters. This pattern has already

emerged in the Victor Valley and its issues can be

instructive for leaders in the Coachella Valley.

The incomes brought home by these commuters will

have a stabilizing impact on the region’s economy as

they will ebb and flowwith Southern California’s econ-

omywhich often has beenmore stable than the nation-

al economy. There have been two exceptions to that

fact. The first was the aerospace/defense bust at the

end of the Cold War. The second is occurring nowwith

the exaggerated downturn in construction due to the

excesses of the most recent home building cycle.

� Meanwhile, the disappearance of industrial land in

the urbanized portion of the Inland Empire, combined

with the rapid rise of imports through the ports of Los

Angeles and Long Beach will likely open a new source

of jobs in the Coachella Valley in the next decade. These

will be in the logistics sector. In 2007, 43.2% of all con-

tainers entering the

country passed

through

Southern California’s

ports. There is a crying need for

facilities where the goods in these containers can be

unloaded, stored, managed and shipped as needed. The

Coachella Valley is the next place along the I-10 truck

route and UP Railroad mainline that will be asked by

the development community to host these facilities

once the San Bernardino-Redlands area runs out of

room. Already, large buildings are going up in San

Gorgonio Pass and UP Railroad is seeking a site for a

new intermodal yard along its mainline, a key piece of

18

logistics infrastructure since it is where containers

move between trucks and trains. Of late, the high price

of diesel fuel has slowed the outward move of build-

ings. That will be overcome once the available space in

area’s like Ontario is completely absorbed.

As the data following show, distribution is the blue collar

sector that pays more than either construction or manu-

facturing both in the Coachella Valley and in Southern

California. It can thus serve to provide a source of higher

pay to workers who do

not have good educations

and need a career path

based via on-the-job learn-

ing to reach the middle

class. It is also a sector

that can broaden the val-

ley’s economy and make

it less dependent upon

the flow of funds that are

seasonal or follow the U.S.

business cycle. However,

this sector brings impor-

tant issues. It will put

pressure on the I-10 free-

way. Unless its air quality

issues are addressed, it

will impact the levels of

diesel emissions. For the

Coachella Valley, it will

also provide higher wage

competition for the kinds

of workers now earning

less in the consumer serv-

ice sectors. Like com-

muter-based residents, the flow of this activity into the

valley is likely inevitable and leaders need to be planning

for it.

� Another way to raise the incomes of workers in the

Coachella Valley is to attempt to stimulate sectors that

pay better. The Coachella Valley Economic Partnership

has targeted five such parts of the economy: health

care, multi-media, advanced technology, education and

recreation.

� The health care sector is a natural for the valley

since it is already awell-defined cluster including hos-

pitals, out-patient care, rehabilitation, dentists and

related work. In addition, the valley has a national

reputation in these areas. What is lacking is a labor

force that can keep up with the expansion of the sec-

tor, given the educational and skill levels needed to

work within it. In addition, the maturity of the sector

plus the anticipated growth in base of local full-time

retirees, opens the possibility of research and devel-

opment on techniques and products needed by what

will be a growing segment of America’s population.

� The multi-media cluster is another natural for the

valley. Traditionally, it

has been home to the

stars of radio, television

and the cinema. It is

often the location for

major production shoots.

There are annual film

and music festivals that

are growing in industry

recognition. Today, many

of the technicians and

the artists who operate

within the sector are

relocating to the area.

This gives the region a

base of activity and

knowledge from which

to build. In addition, in

the virtual world, many

of the activities that can

drive this sector can be

located anywhere. Here,

an example is the remote

location of George Lucas’s

Industrial Light andMagic

in Marin County.

� One just has to drive by the windmill farms at the

entrance to the Coachella Valley or read about the

solar energy farms in Southern California’s deserts to

realize that alternative energy production is already

showing up in these areas. In addition, as a desert

region, the valley has long had to be aware of the

need for advanced water technology, a fact now

heightened by the need to preserve the Salton Sea.

With petroleum prices soaring, global warming and

energy independence emerging as issues, plus popu-

lation straining our water and electrical resources,

there is and will be a rising worldwide demand for

alternative energy and water solutions. Again, the

19

valley has an important base of knowledge and

activity from which to develop these sectors.

� There is no such thing as a poor, well-educated

region, unfortunately the opposite is also true. That is

why CVEP’s economic development strategy seeks to

tackle the relatively low educational level of the

area’s adult workforce as well as the marginal per-

formance of toomany of its school children. Strategies

for doing so must be partially driven from the busi-

ness community, given

its increasing under-

standing of the types

of workers it will need.

In addition, the devel-

opment of the strate-

gies just mentioned

has also involved the

framing of educational

strategies as they can-

not succeed without

them. Similarly, the

expansion of the logis-

tics sector will require

local access to work-

force training.

� A good sign is the

fact that test scores in

the area have been ris-

ing in all three local

school districts, with

particular success in

the Desert Sands dis-

trict. Meanwhile, each

of the three districts is in various stages of adding

facilities and a new Catholic high school has been

sited. Noteworthy is the interest and willingness of

College of the Desert to participate in working to

increase the skills of the adult workforce. The cam-

pus is expanding at its current site and at two addi-

tional locations.

� Ultimately, the expansion of the Cal State San

Bernardino campus aswell as UCR’s nearby Heckmann

Center for Entrepreneurial Studies will also be of

great significance in helping the Coachella Valley to

both hold its best students and boost its economy.

This year, Cal State will break ground on its third

building, a Health Sciences facility. It will provide

training in one of CVEP’s key target sectors. In addi-

tion, UCR has launched an MBA program plus an MFA

in Screenwriting. The second of these will be on point

to another of CVEP’s targeted sectors. UCR campus is

also assisting in the formation of an Angel Network to

assist entrepreneurs in acquiring funding.

� Recreation is CVEP’s other targeted sector. This is in

keeping with the Coachella Valley’s obvious strength

in serving retirees, tourists, conventioneers and

others wanting to enjoy

golf, tennis, gaming, bik-

ing and hiking, as well as

rock climbing in nearby

Joshua Tree National Park.

This sector already brings

huge amounts of tourists

dollars to the region. The

Indian gaming sector has

added a new element

that pays above average

for the sector group.

Affiliatedwith these activ-

ities is the possibility for

expanded design and

manufacturing of the

equipment associated

with these activities such

as the alternative energy

vehicles related to golf

carts and the specialized

equipment used in rock

climbing.

Today, the Coachella Valley

has an economy that is facing the short-term issues

from a housing cycle gone bad. Clearly, its leaders need

to deal with lowering the flow of foreclosure sales,

defending neighborhoods with a large number of

potential problem homes, and ensuring that builders

can succeed in the next housing cycle. Looking farther

ahead, the Coachella Valley’s underlying economy has

gained considerable strength. Over the long haul, its

leaders need to deal with the fact its composition has

historically made its business cycle unusually volatile

and the fact that a disproportionately large share of its

work is concentrated in modest paying sectors. Here,

conditions are developing in ways that could well

allow the region’s leaders to improve upon both of

these situations.

Over the long haul,

Coachella Valley leaders

need to deal with the fact

that its composition has

historically made its

business cycle unusually

volatile and the fact that

a disproportionately

large share of its work is

concentrated in modest

paying sectors.

20

21

NUMBER TOP IC PAGE

DEMOGRAPH ICS

1 Population Growth, Coachella Valley, 1990-2008 24

2 Population Growth Rates, Coachella Valley & Other Major Areas, 2000-2008 25

3 Population By City, Coachella Valley Communities, 2008 25

4 Population Growth By City, Coachella Valley Communities, 2000-2008 25

5 Age Distribution, Coachella Valley & Inland Empire, 2007 26

6 Adult Educational Level, Coachella Valley & So. California Counties, 2007 26

7 Ethnic Composition, Coachella Valley Cities, 2007 29

8 Income Estimates, Coachella Valley & Inland Empire, 2007 29

9 Median Income By City, Coachella Valley, 2007 30

10 Total Income By City, Coachella Valley, 2007 30

EMPLOYMENT

11 Employment, Coachella Valley, 1991-2007 32

12 Employment Gain By Sector, Coachella Valley, 2000-2007 32

13 Employment Growth Rates, Coachella Valley & Inland Empire, 1991-2007 33

14 Employment Distribution By Sector, Coachella Valley, 2007 34

15 Employment Distribution By Sector, Coachella Valley, 2000 34

16 Payroll, Coachella Valley, 1991-2007 34

17 Payroll Growth, Allowing for Inflation, Coachella Valley, 2000-2007 35

18 Payroll Gain By Sector, Coachella Valley, 2000-2007 36

19 Payroll Per Job, Coachella Valley, 1991-2007 36

20 Growth in Average Pay Per Job, Allowing for Inflation, Coachella Valley, 2000-2007 39

21 Average Pay Per Job By Sector, Coachella Valley, 2007 39

22 Number of Firms, Coachella Valley, 1991-2007 40

23 Change in Number of Firms, Coachella Valley, 2000-2007 40

24 Distribution of Firms By Sector, Coachella Valley, 2007 41

25 Average Workers per Firm, Coachella Valley, 1991-2007 41

26 Employment of Residents, By Sector, Coachella Valley, 2006 42

27 Employment of Residents, by Occupation, Coachella Valley & Inland Empire, 2006 42

HOUS ING

28 Existing Home Sales, Coachella Valley, Seasonally Adjusted, By Quarter, 1988-2008 44

29 Existing Home Sales, Coachella Valley Cities, 2007 v. 2008 44

30 New Home Sales, Coachella Valley, Annual, 1988-2008 45

31 New Home Sales, Coachella Valley Cities, 2007 v. 2008 45

32 Existing Home Price Trend, Coachella Valley, 1998-2008 2nd Qtr. 46

33 Existing Home Prices, 2008 2nd Qtr., Coachella Valley & So. Calif. Counties 47

34 New Home Price Trend, Coachella Valley, 1988-2008 2nd Qtr. 48

35 New Home Prices, 2008 2nd Qtr., Coachella Valley & So. Calif. Counties 49

36 Apartment Rental Rate, Investment Grade Units, Inland Empire Markets & Coastal Counties, 1st Qtr., 2008 49

Coachella Valley Economic Report, 2008

Exhibit List

22

NUMBER TOP IC PAGE

TAXABLE SALES

37 Taxable Retail Sales, Coachella Valley, 1990-2007 50

38 Taxable Sales Growth, Coachella Valley vs. Inland Empire, 1990-2007 50

39 Retail Sales By City, Coachella Valley, 2007 51

40 Retail Sales Growth & Growth Rates, By City, Coachella Valley, 2006-2007 51

41 Retail Sales Per Capita, Coachella Valley & Inland Empire, 1990-2007 52

42 Retail Sales Per Capita, Coachella Valley & Major Inland Cities, 2007 52

43 Retail Trade by Sector, Coachella Valley, 2007 53

BANK ING

44 Bank Deposits, Coachella Valley, 1992-2007 54

45 Bank Deposits by City, Coachella Valley Cities & Highest Inland Cities, 2007 54

46 Per Capita Bank Deposits, Coachella Valley, 1992-2007 55

47 Per Capita Bank Deposits, Coachella Valley Cities & Highest Inland Cities, 2007 55

48 Bank Deposits By Bank, Coachella Valley, 2007 56

ASSESSED VALUAT ION

49 Assessed Valuation, Coachella Valley Cities, 1990-2008 58

50 Assessed Valuation Growth, Coachella Valley & Riverside County, 1990-2007 58

51 Assessed Valuation by City, Coachella Valley, Fiscal year 2008-2009 59

52 Per Capita Assessed Valuation, Coachella Valley, 1990-2008 59

53 Assessed Valuation Per Capita, Riverside County Cities, FY 2008-2009 60

CR IME RATES

54 Reported Crime Rate Per 1,000 Residents, Coachella Valley, 1994-2006 62

55 Total Crime Report per 1,000 Residents, Coachella Valley Cities, 2006 62

56 Violent Crime Reported Per 1,000 Residents, Coachella Valley Cities, 2006 63

57 Property Crime Reported Per 1,000 Residents, Coachella Valley Cities, 2006 63

58 Types of Crime Reported, Coachella Valley Cities, 2006 63

EDUCAT ION

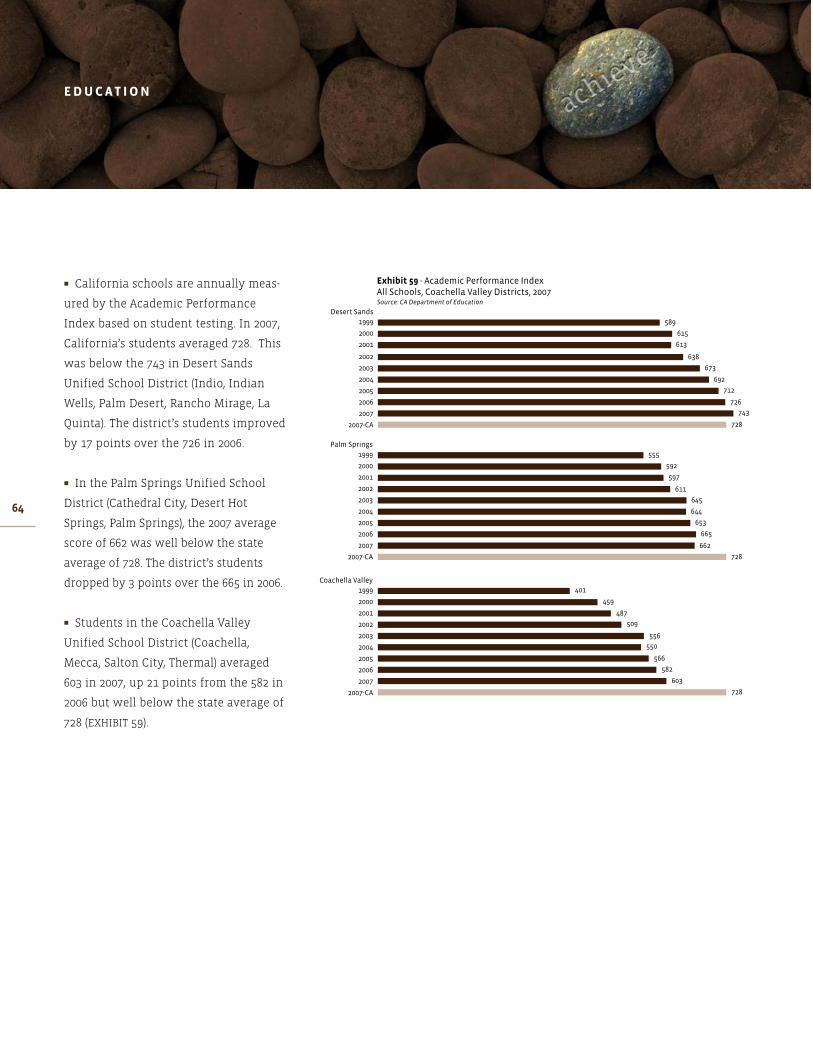

59 Academic Performance Index, All Schools, Coachella Valley School Districts, 2007 64

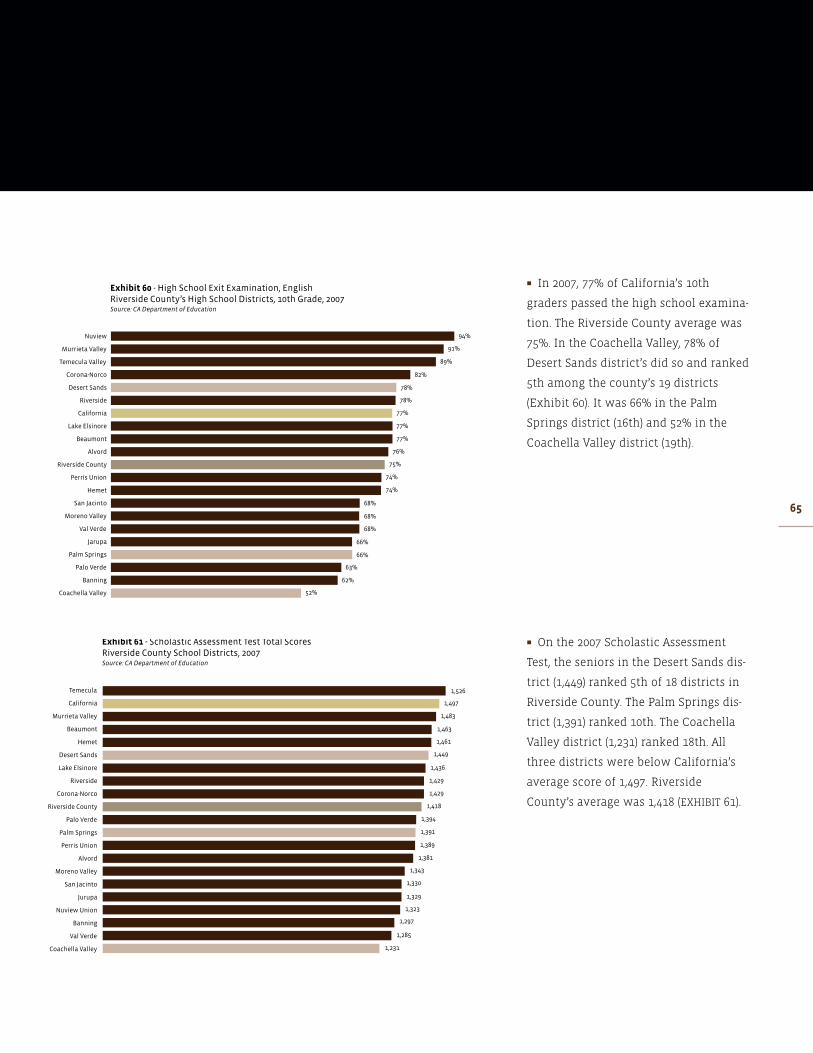

60 High School Exit Examination, Riverside County High School Districts, English, 10th Grade, 2007 65

61 Scholastic Assessment Test, Total Scores, Riverside County High School Districts, 2007 65

Colleges & Universities 66

APPEND IX : EMPLOYMENT & PAYROLL DETA I LS

62 Employment By Sector, Coachella Valley, 1991-2007 68

63 Payroll By Sector, Coachella Valley, 1991-2007 69

64 Average Pay Per Job, Coachella Valley, By Sector, 1991-2007 71

Environmental stewardship and conservation have long been a focus of the Imperial Irrigation District. Founded in 1911, IID’s commitment to the environment, conservation and protection of resources is part of the organization’s charter and mission.

This commitment lives on today as IID promotes green practices in our community. To help our customers, cities and businesses become greener IID offers several programs designed to promote smarter and more efficient uses of energy.

New Construction Energy Efficiency This program combines an integrated design process with financial incentives for all new construction and renovation projects. It is geared toward assisting customers in moving beyond initial cost considerations and toward the realization of long-term energy cost savings as well as avoiding lost opportunities as new buildings are designed and constructed.

Energy Management Program IID works with cities to develop energy-saving solutions that will create a greener and more efficient community. IID has assigned an energy management expert to each participating city in which we do business.

Energy Swing Shift New in 2008, the IID Energy Swing Shift program makes it easy for customers to help cut energy costs and maintain reliability by reducing the amount of electricity needed at critical times when high demand for power

strains the system. This reduces the need to generate additional peak-time power, which, in turn, helps reduce environmental impacts.

Agricultural Energy Efficiency This program is designed for irrigation, golf course and municipal water pumping needs. It promotes state-of-the-art methods for improving pump efficiency.

On-site Energy Efficiency Analysis We are the experts, therefore it’s important that we offer customers the technical expertise to identify energy efficiency and savings opportunities in their businesses. As a part of this program, customers are eligible for financial assistance for detailed project analysis and for the implementation of energy conservation projects.

Inspector Energy When residential customers need advice about energy efficiency they can turn to Inspector Energy. We’ll send a conservation specialist to your home to evaluate your current usage and give you suggested ways to save even more.

ENERGY STAR® Rebates Appliances have two costs, the price to take them home and the cost to run them each month. IID offers rebates on ENERGY STAR qualified appliances that use 10–50 percent less energy and water than standard models.

These are just a few of the energy efficiency programs IID offers its customers. For more information about our efficiency programs, visit www.iid.com.

23

24

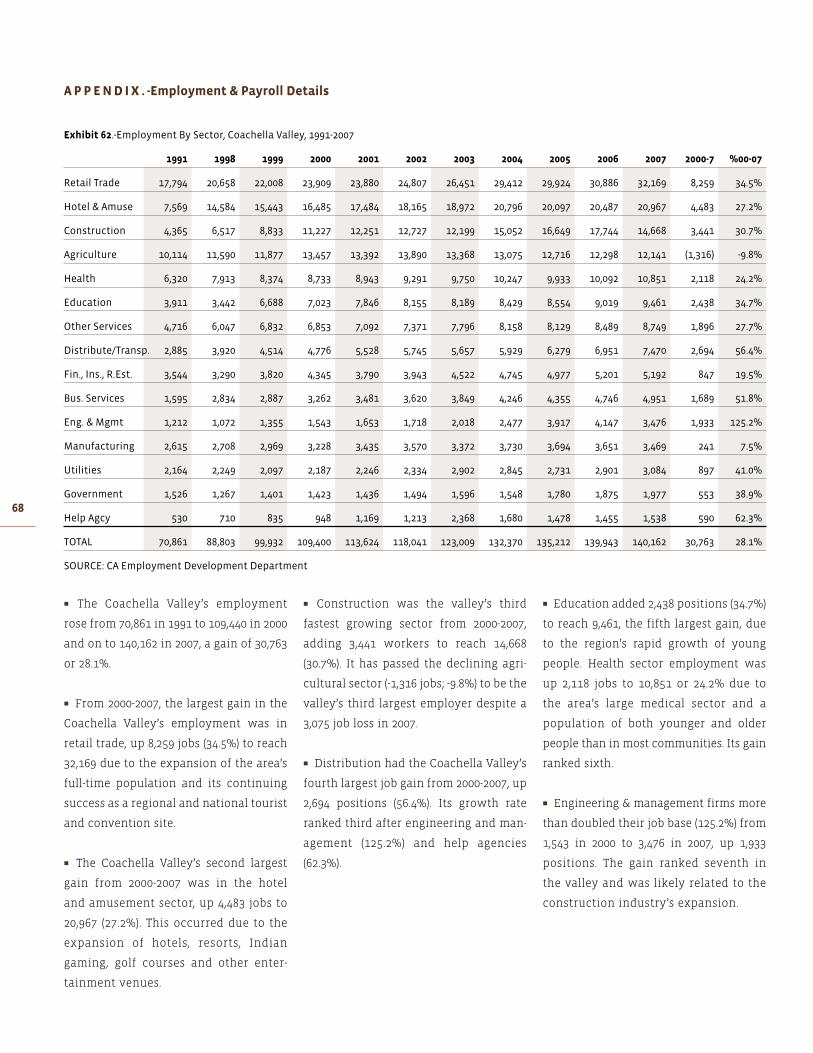

� From 2000-2008, the Coachella Valley’s

population grew from 309,530 to 437,655.

That was a gain of 128,125 people in just

eight years (41.4%) (EXHIBIT 1).

DEMOGRAPH ICS

25� In 2008, the Coachella Valley’s cities

ranged in size from Indio with 81,512

people to Indian Wells with 5,025. Three

additional cities had over 45,000 people:

Cathedral City (52,465), Palm Desert

(50,907) and Palm Springs (47,251)

(EXHIBIT 3).

� From 2000-2008, Indio’s growth led the

Coachella Valley, up by 32,396 people

(EXHIBIT 4). La Quinta was second (19,264),

followed by Coachella (17,793). Each of

these cities had land to develop.

Cathedral City (9,818), Palm Desert (9,752)

and Desert Hot Springs (9,486) had modest

increases. The fewest people were added

by Palm Springs (4,446), Rancho Mirage

(3,808) and Indian Wells (1,209).

� The Coachella Valley’s 41.4% increase

in population from 2000-2008 was much

faster than the surrounding Inland

Empire (27.3%), California (12.3%) or

the U.S. (8.2%) (EXHIBIT 2).

26

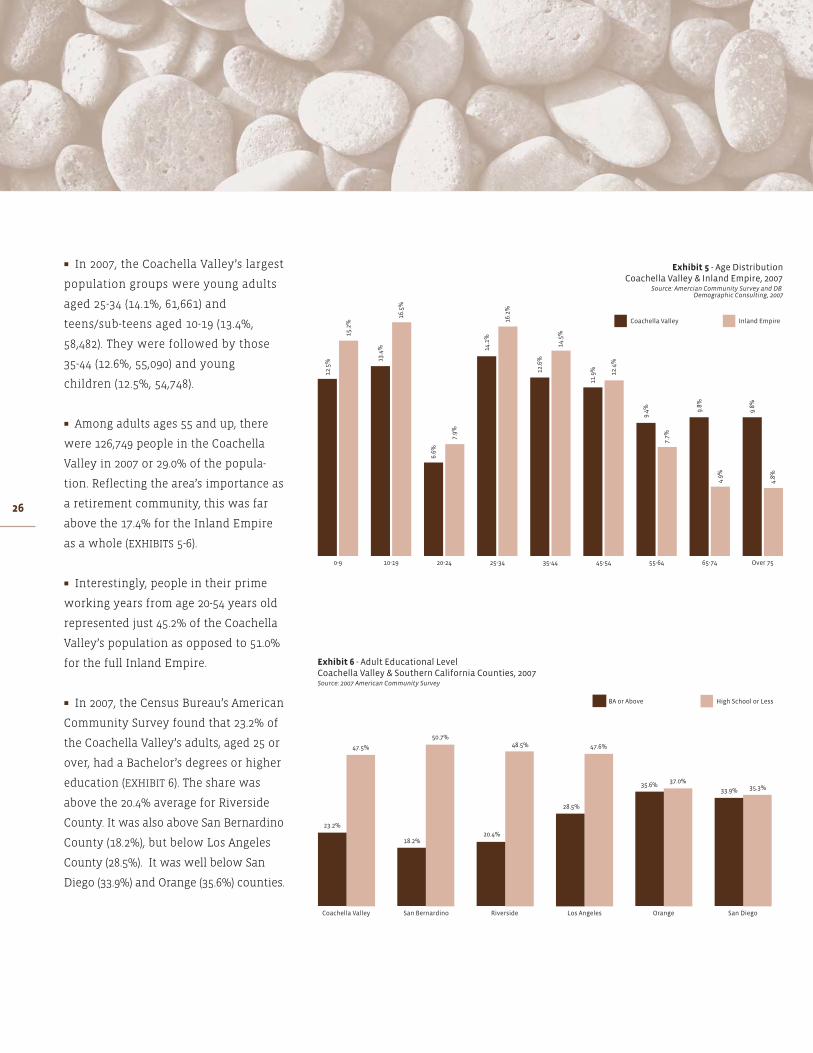

� In 2007, the Coachella Valley’s largest

population groups were young adults

aged 25-34 (14.1%, 61,661) and

teens/sub-teens aged 10-19 (13.4%,

58,482). They were followed by those

35-44 (12.6%, 55,090) and young

children (12.5%, 54,748).

� Among adults ages 55 and up, there

were 126,749 people in the Coachella

Valley in 2007 or 29.0% of the popula-

tion. Reflecting the area’s importance as

a retirement community, this was far

above the 17.4% for the Inland Empire

as a whole (EXHIBITS 5-6).

� Interestingly, people in their prime

working years from age 20-54 years old

represented just 45.2% of the Coachella

Valley’s population as opposed to 51.0%

for the full Inland Empire.

� In 2007, the Census Bureau’s American

Community Survey found that 23.2% of

the Coachella Valley’s adults, aged 25 or

over, had a Bachelor’s degrees or higher

education (EXHIBIT 6). The share was

above the 20.4% average for Riverside

County. It was also above San Bernardino

County (18.2%), but below Los Angeles

County (28.5%). It was well below San

Diego (33.9%) and Orange (35.6%) counties.

Leavingno stone

unturned.

I M A G I N E .

Envision what our future can be.

I N S P I R E .

Instill vision and motivate others towards action.

C O L L A B O R A T E .

Lock arms and press toward our defined goals.

A C H I E V E .

The outcomes of our hopes and dreams begin to appear.

Coachella Valley Economic Partnership

73-710 Fred Waring Drive, Suite 106

Palm Desert, California 92260

Phone: 760.340.1575 or 1.888.318.CVEP

Fax: 760.340.9212

www.cvep.com

28

29

� In 2007, the share of the valley’s adults with just a high school or less education

(47.5%) was nearly the same as Los Angeles County (47.6%). It was lower than

Riverside (48.5%) and San Bernardino (50.7%) counties but well over San Diego

(35.3%) and Orange (37.0%) counties.

� In 2007, the share of population in Coachella Valley cities that was White was

43.2% compared to 43.0% for all of Riverside County (EXHIBIT 7). Hispanics were

43.4% in the valley and 42.2% for the full county.

� In 2007, the 2007 American

Community Survey indicated that the

Coachella Valley’s total income was

$12.1 billion. That was 12.7% of the $95.0

billion in total income for the Inland

Empire (EXHIBIT 8).

� The Coachella Valley’s average house-

hold income of $77,058 was about $5,500

higher than the Inland Empire’s $72,546.

Its per capita income of $30,076 was

roughly $6,000 above the region’s $23,273.

However, Coachella Valley’s median

income of $51,915 (half above & below)

was lower than the regional figure as

medians are not pulled up by very

high incomes.

30

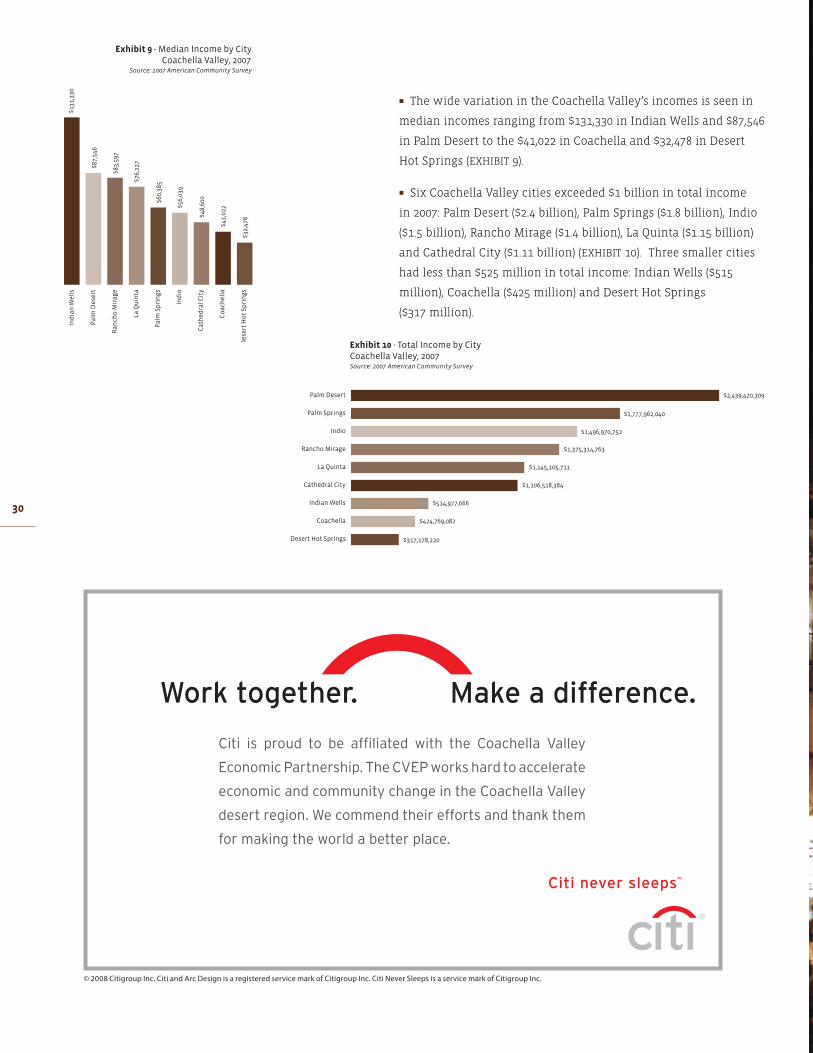

� The wide variation in the Coachella Valley’s incomes is seen in

median incomes ranging from $131,330 in Indian Wells and $87,546

in Palm Desert to the $41,022 in Coachella and $32,478 in Desert

Hot Springs (EXHIBIT 9).

� Six Coachella Valley cities exceeded $1 billion in total income

in 2007: Palm Desert ($2.4 billion), Palm Springs ($1.8 billion), Indio

($1.5 billion), Rancho Mirage ($1.4 billion), La Quinta ($1.15 billion)

and Cathedral City ($1.11 billion) (EXHIBIT 10). Three smaller cities

had less than $525 million in total income: Indian Wells ($515

million), Coachella ($425 million) and Desert Hot Springs

($317 million).

32

� From 2000-2007, the Coachella Valley’s

employment went from 109,400 to

140,162 a gain of 30,763 jobs or 28.1%

(EXHIBIT 11). In this period, the Inland

Empire was up 27.3%.

� The region’s economy grew because its

full time population has grown as has its

convention, tourism, health and retire-

ment activities expanded through this

period. Also, until 2007, its construction

industry had thrived. It has faltered with

the housing crisis.

� From 2000-2007, the Coachella Valley’s

retail trade added 8,259 jobs or 26.8% of

its 30,763 new positions due to growth

in both population and tourism (EXHIBIT

12). The hotel and amusement sectors

including casinos added 4,483 jobs or a

14.6% share. Construction was up 3,441

jobs or 11.2% of the job growth, despite

a loss of 3,075 positions in 2007. Distribu-

tion added 2,694 or 8.8%. This is important

as the region seeks to diversify its eco-

nomic base. The four sectors were 61.4%

of the area’s growth.

� Ultimately, distributors will likely

locate large facilities along the Union

Pacific Railroad’s right of way through

the valley to handle goods entering

Southern California through the ports

of Los Angeles and Long Beach.

EMPLOYMENT

33

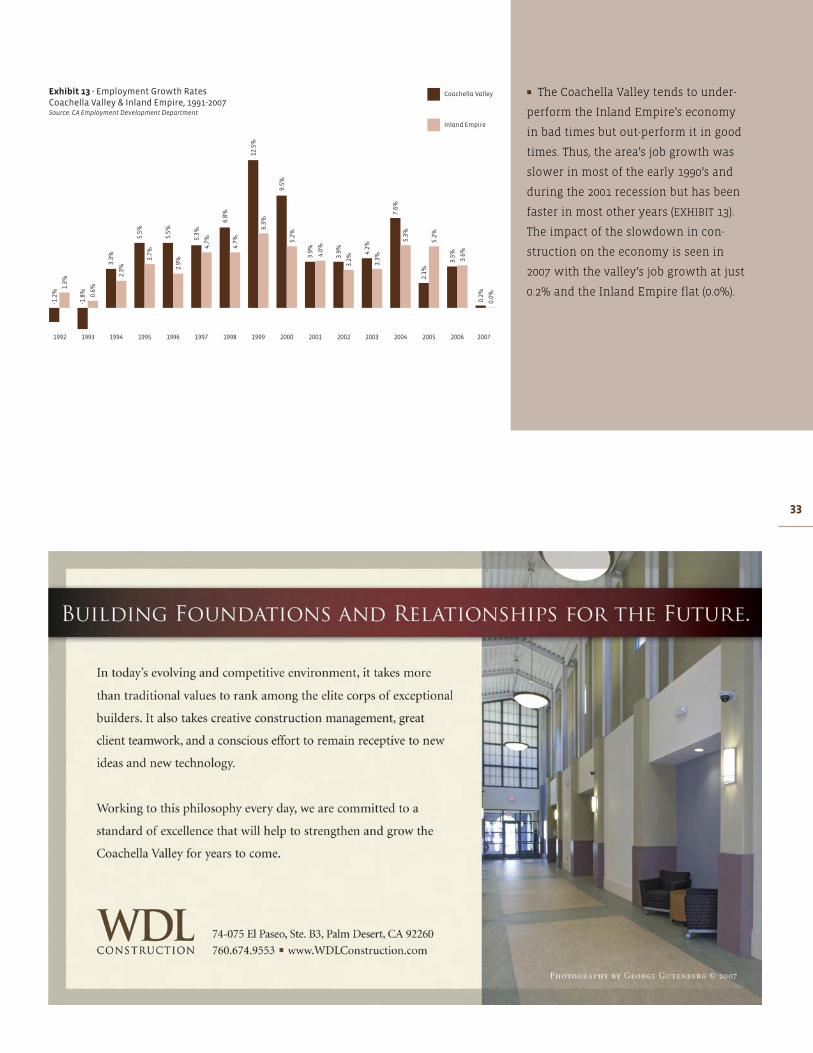

� The Coachella Valley tends to under-

perform the Inland Empire’s economy

in bad times but out-perform it in good

times. Thus, the area’s job growth was

slower in most of the early 1990’s and

during the 2001 recession but has been

faster in most other years (EXHIBIT 13).

The impact of the slowdown in con-

struction on the economy is seen in

2007 with the valley’s job growth at just

0.2% and the Inland Empire flat (0.0%).

34

� With the general expansion and diver-

sification of the Coachella Valley’s job

base from 2000-2007, its large and grow-

ing retail sector went from to 21.9% to

23.0% of employment (EXHIBITS 14-15). The

second largest sector, hotel and amuse-

ment (including casinos), saw its share

essentially unchanged, going from 15.1%

to 15.0%. Meanwhile, the recent decline in

construction projects meant that con-

struction employment, which had

reached 12.7% in 2007, only rose slightly

from 10.3% in 2000 to 10.5% in 2007.

� Increased urbanization and rising

costs caused agriculture to fall from

12.3% to 8.7% and drop from third to

fourth largest. Health care lost some

share from 2000 to 2007 going from 8.0%

to 7.7%. Education jumped up slightly

from 6.4% to 6.8%. Indicating some

increase in the valley’s diversification,

the smaller sectors combined went

from 11.5%t o 13.2%.

� From 2000-2007, the total payroll

released by the Coachella Valley’s firms

and agencies grew by $2.07 billion from

$2.8 billion to $4.9 billion or 73.8%

(EXHIBIT 16).

35

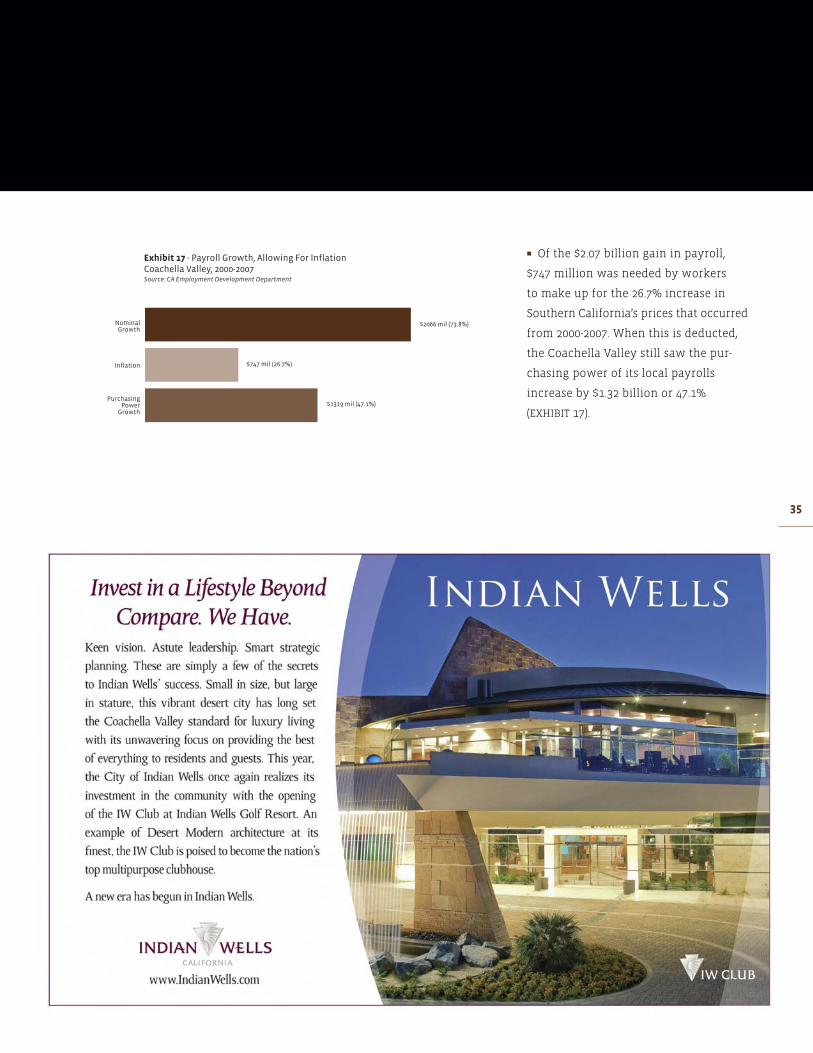

� Of the $2.07 billion gain in payroll,

$747 million was needed by workers

to make up for the 26.7% increase in

Southern California’s prices that occurred

from 2000-2007. When this is deducted,

the Coachella Valley still saw the pur-

chasing power of its local payrolls

increase by $1.32 billion or 47.1%

(EXHIBIT 17).

36

� From 2000-2007, the largest share

of the $2.07 billion increase in the

Coachella Valley’s payrolls (14.8%) was

from the $305.5 million gain in the retail

trade sector. Next was construction,

which was responsible for $262.4 mil-

lion (12.7%) of the increase, despite an

$85.1 million decline from 2007-2007

(EXHIBIT 18).

� The hotel and amusement sector

ranked third in payroll growth account-

ing for $249.2 million (12.1%). The health

services sector ranked fourth, up $223.9

million (10.8%). These four sectors

accounted for 50.4% of the Coachella

Valley’s payroll expansion.

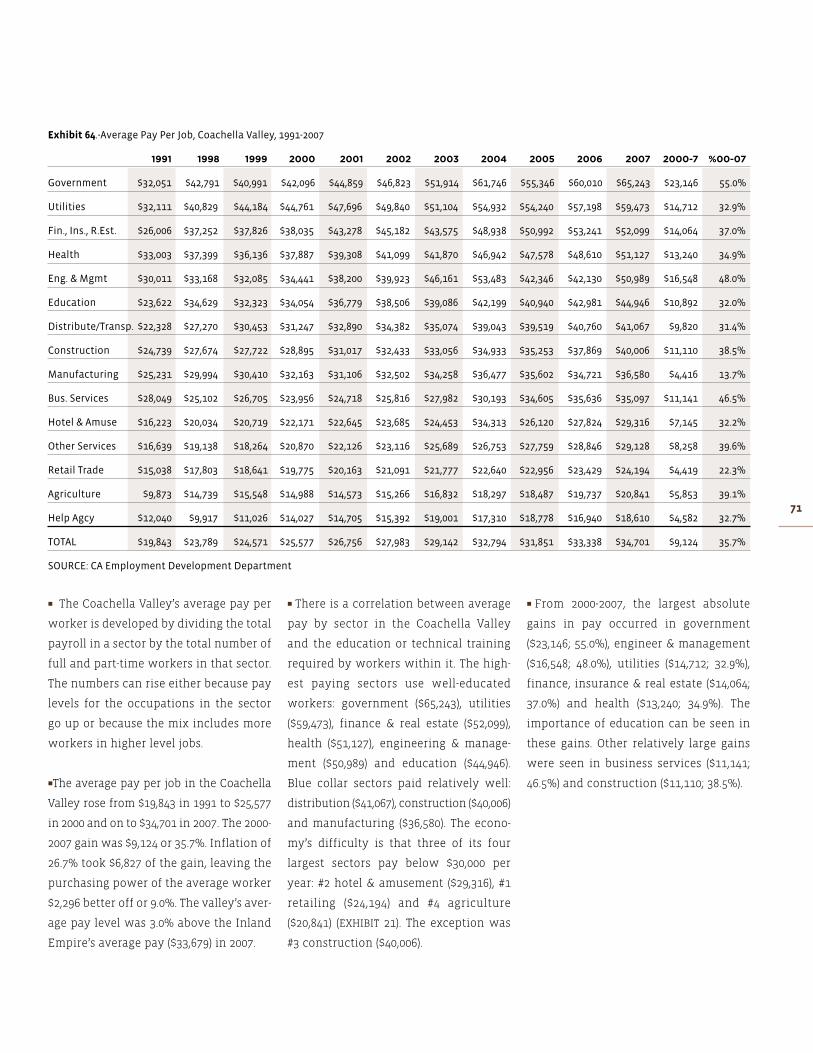

� In 1991, the average pay per worker

in the Coachella Valley was $19,843. By

2000, this had reached $25,577. It then

moved on to $34,701 by 2007. That was

3.0% above the $33,679 for all Inland

Empire firms (EXHIBIT 19).

37

38

39

� The Coachella Valley’s average pay

per job increased by $9,124 (35.7%) from

2000-2007. Of this, $6,827 was needed to

keep up with the 26.7% gain in Southern

California’s prices. As a result, the average

worker’s purchasing power rose $2,296

or 9.0% (EXHIBIT 20).

� There is a correlation between

average pay by sector in the Coachella

Valley and the education or technical

training required by workers within it.

The highest paying sectors use well-edu-

cated or skilled workers: government

($65,243), utilities ($59,473), finance &

real estate ($52,099), health ($51,127),

engineering & management ($50,989)

and education ($44,346).

� Blue collar sectors paid relatively

well: distribution ($41,067), construction

($40,006) and manufacturing ($36,580).

The economy’s difficulty is that three

of its four largest sectors pay below

$30,000 per year: #2 hotel & amusement

($29,316), #1 retailing ($24,194) and #4

agriculture ($20,841) (EXHIBIT 21). The

exception was #3 construction ($40,006).

40

� The number of firms in the Coachella

Valley has risen from 5,384 in 1991 to

6,236 by 2000, and 7,846 by 2007. The

gain from 2000-2007 was 1,610 firms

or 25.8% (EXHIBIT 22).

� These numbers should be viewed as a

long-term “general trend” not “exact”

data as they do not include entrepre-

neurs with no payroll. For this reason,

upward or downward fluctuations from

year to year are not as significant as

they may appear as they generally

involve very small firms switching from

pure entrepreneurs to employers with

one or two workers.

� From 2000-2007, the largest number of

firms was added in construction (405). The

next largest gain was in engineering and

management (228). These were followed

by distribution (204), health services (198)

and finance and insurance (191). Only two

sectors lost jobs: agriculture (-4) and other

services (-2) (EXHIBIT 23).

41

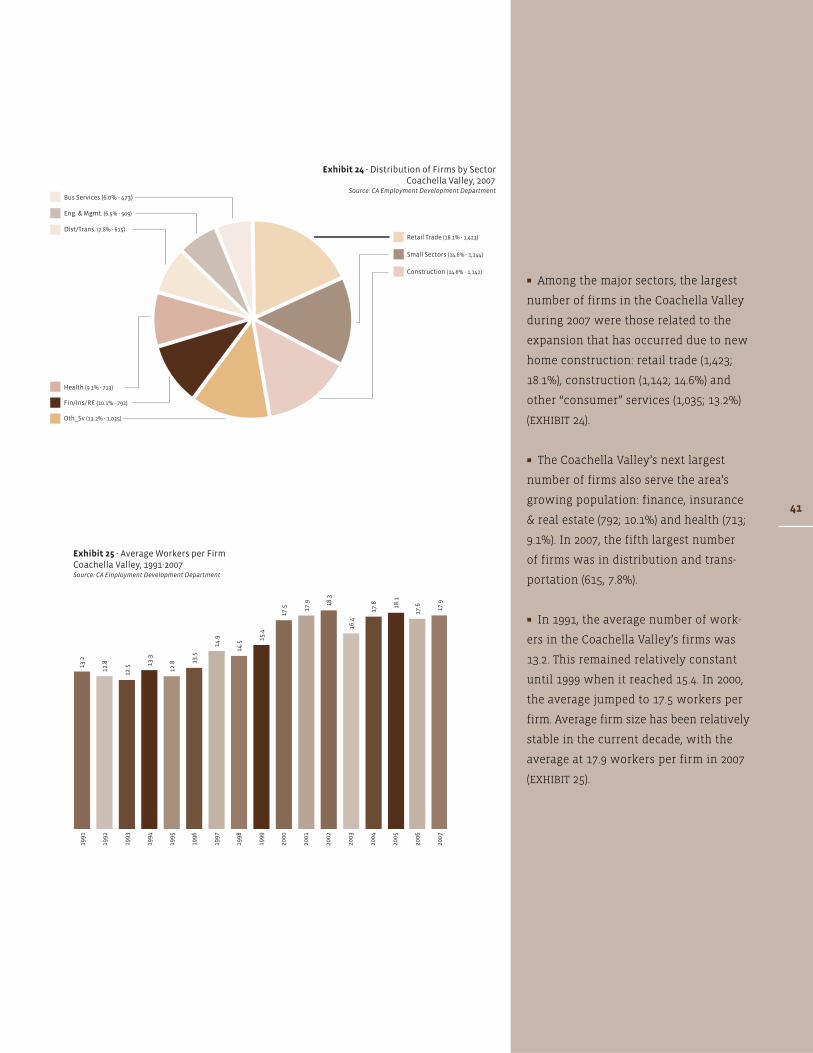

� Among the major sectors, the largest

number of firms in the Coachella Valley

during 2007 were those related to the

expansion that has occurred due to new

home construction: retail trade (1,423;

18.1%), construction (1,142; 14.6%) and

other “consumer” services (1,035; 13.2%)

(EXHIBIT 24).

� The Coachella Valley’s next largest

number of firms also serve the area’s

growing population: finance, insurance

& real estate (792; 10.1%) and health (713;

9.1%). In 2007, the fifth largest number

of firms was in distribution and trans-

portation (615, 7.8%).

� In 1991, the average number of work-

ers in the Coachella Valley’s firms was

13.2. This remained relatively constant

until 1999 when it reached 15.4. In 2000,

the average jumped to 17.5 workers per

firm. Average firm size has been relatively

stable in the current decade, with the

average at 17.9 workers per firm in 2007

(EXHIBIT 25).

42

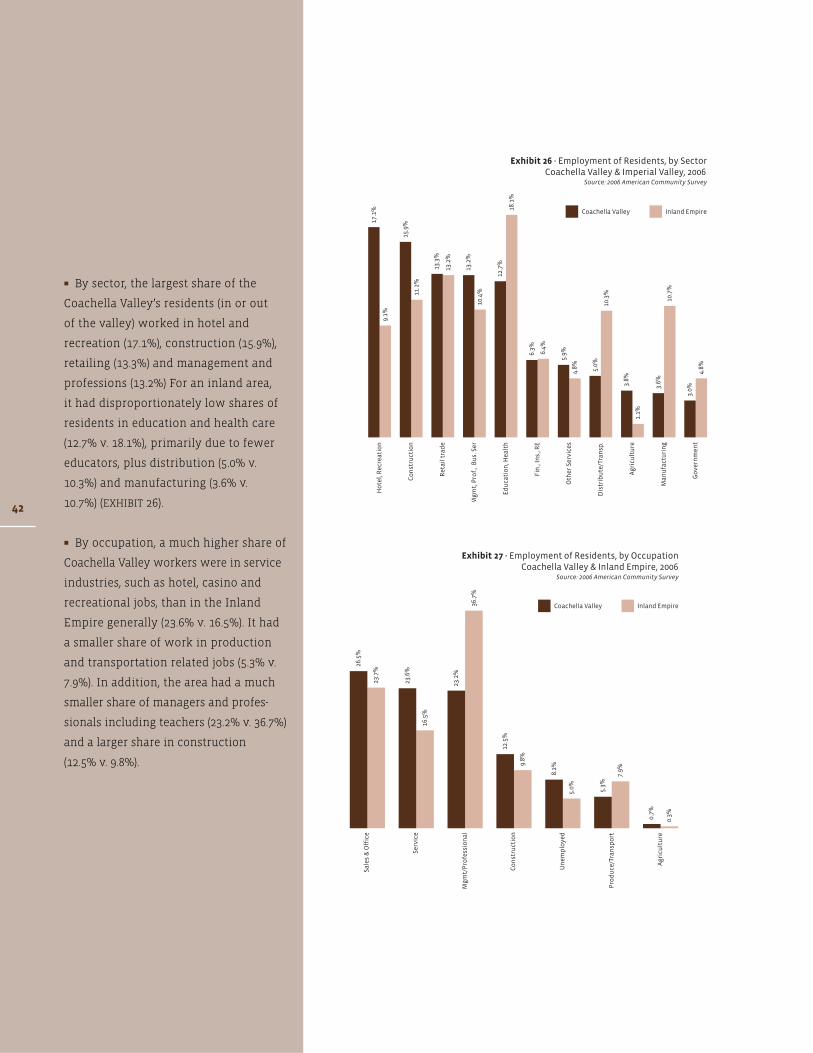

� By sector, the largest share of the

Coachella Valley’s residents (in or out

of the valley) worked in hotel and

recreation (17.1%), construction (15.9%),

retailing (13.3%) and management and

professions (13.2%) For an inland area,

it had disproportionately low shares of

residents in education and health care

(12.7% v. 18.1%), primarily due to fewer

educators, plus distribution (5.0% v.

10.3%) and manufacturing (3.6% v.

10.7%) (EXHIBIT 26).

� By occupation, a much higher share of

Coachella Valley workers were in service

industries, such as hotel, casino and

recreational jobs, than in the Inland

Empire generally (23.6% v. 16.5%). It had

a smaller share of work in production

and transportation related jobs (5.3% v.

7.9%). In addition, the area had a much

smaller share of managers and profes-

sionals including teachers (23.2% v. 36.7%)

and a larger share in construction

(12.5% v. 9.8%).

43

44

� From late 2001 until second quarter

2004, the Coachella Valley’s existing

homes sales soared. On a seasonally

adjusted basis, they reached 2,061

quarterly sales. With prices reaching

very high levels, due to speculators and

sub-prime financing, demand then

began to fall. It plunged starting in late

2007, ultimately causing prices to drop

as well. The valley’s existing home

market fell to a modern low of 948

quarterly sales in fourth quarter 2007.

Volume has since jumped 35.1% to 1,280

units as foreclosure sales have shown

that there is significant demand at

early 2004 prices.

� By city, the Coachella Valley’s estimat-

ed 2008 existing home sales are being

led by Indio (1,010) and La Quinta (858).

The cities of Palm Desert (680), Palm

Springs (539), and Cathedral City (489) are

next. The lowest volumes are occurring

in Desert Hot Springs (469), Rancho

Mirage (311), Coachella (220) and Indian

Wells (118) (EXHIBIT 29).

HOUS ING

45

� New home sales reached post-Cold

War recession lows of under 800 units in

the mid-1990s. Increasing demand then

sent sales to a modern record of 2,255

units in 1999. Sales stayed close to 2,000

units until they exploded to 4,065 in

2003, 5,535 in 2004 and a record 5,490 in

2005 (Exhibit 30). In 2007, the new home

market began to falter (4,913) as buyers

started to rebel against very high prices.

Production and prices plunged in 2007

with sales down to 2,771 units. Through

June 2008, volume was running at an

annual rate of just 1,366 units.

� By city, new home volume slowed

significantly throughout the Coachella

Valley from 2007 to its annualized 2008

rates (EXHIBIT 31). The highest volumes

are still occurring in Indio (1,018) and La

Quinta (512), two cities with significant

available land. Next is Coachella (341),

followed by Palm Springs (332) and

Desert Hot Springs (231). The valley’s

more developed cities added fewer

new homes: Palm Desert (162), Cathedral

City (90), as did its most expensive

communities: Rancho Mirage (68) and

Indian Wells (17).

46

� During this decade, the Coachella Valley’s median existing home price soared

from 2000-2007, rising at a compound annual rate of 18.4% from $170,756 to $470,191.

In 2007, as demand faltered, the price increase slowed to just 1.6% ($477,672). By 2nd

quarter 2008, demand had evaporated except for homes being sold at much lower

prices, often through the foreclosure process. The median price fell $104,313 or

–30.7% to just $376,045 (EXHIBIT 32).

47

� In 2nd quarter 2008, median existing home prices in Indian Wells ($890,000) and Rancho Mirage ($705,000) were still above

all of Southern California’s counties (Exhibit 33). La Quinta ($485,500) was below Orange County ($549,000) and Palm Springs

($445,090) was above Los Angeles County ($435,000) and San Diego ($417,500) counties. It was followed by Palm Desert ($405,455).

Indio ($243,509) and Cathedral City ($235,000) were below Riverside County ($270,000) and above San Bernardino County

($234,000). Coachella ($215,000) and Desert Hot Springs ($145,161) are among the Southland’s more affordable markets. So

was nearby Yucca Valley ($155,000), home to many commuters to the valley.

48

� From 2003-2007, the Coachella Valley’s new home median price jumped from $309,570 to a record $462,760, a compound annual

increase of 14.3%. In 2007, slowing demand plus the importance of more affordable markets like Indio and Coachella caused the

median price to fall –9.4% to $419,452. By second quarter 2008, the drop in housing demand and competition from existing

home prices hit by a glut of foreclosures sent the valley’s median new home price to $375,175, down another –10.6% to roughly

the 2004 level (EXHIBIT 34).

49

� Among cities, new homes in Rancho

Mirage ($827,000), Indian Wells ($740,500)

and La Quinta ($600,000) were more

expensive than San Diego ($472,500) or

Orange ($468,000) counties. Palm Springs

($457,672) was next, above Los Angeles

County ($435,000), while Cathedral City

($410,000) was well above Riverside

County ($338,500). Palm Desert ($323,615)

was just above San Bernardino County

($315,000). Indio ($313,127), Coachella

($250,000) and Desert Hot Springs

($192,912) were the most affordable new

home prices as was nearby Yucca Valley

($240,000) (EXHIBIT 35).

� The Coachella Valley’s class “A”

apartments are relatively affordable by

Inland Empire standards. The average

rental rate in 1st quarter 2008 was $958,

up 3.2% from 2007 and well below the

inland region’s $1,154 average (EXHIBIT

36). The market had a 5.6% vacancy

rate, matching 2007. Its price was far

below those in Southern California’s

coastal markets.

50

� With a growing population and its

continuing role as a regional and national

tourist and convention destination, the

Coachella Valley’s retail sales have soared.

In 2007, taxable sales in its nine cities

reached a record $5.98 billion. With the

housing market’s slowdown, sales fell to

$5.89 billion in 2007 (-0.9%). From 2000-

2007, sales growth was still $2.01 billion

or 51.9%, far above the 26.7% inflation

rate indicating that the underlying

volume of goods grew substantially

in this period (EXHIBIT 37).

TAXABLE SALES

� The Coachella Valley’s taxable sales are generally more volatile than the surrounding Inland Empire (EXHIBIT 38). In good times,

the valley’s sales have tended to grow faster than the region as in 1997-2000. In poor times, they tend to grow slower, as in 2001-2002

(3% vs. 6%). However, from 2004-2007, this pattern did not show up. The valley’s growth was slower in the good times of 2004

(14% v. 16%) and 2005 (9% v. 13%). With the housing crisis, it has essentially matched that of the region in 2006 (4.7% v. 5.4%)

and 2007 (-1.6% v. –1.8%).

51

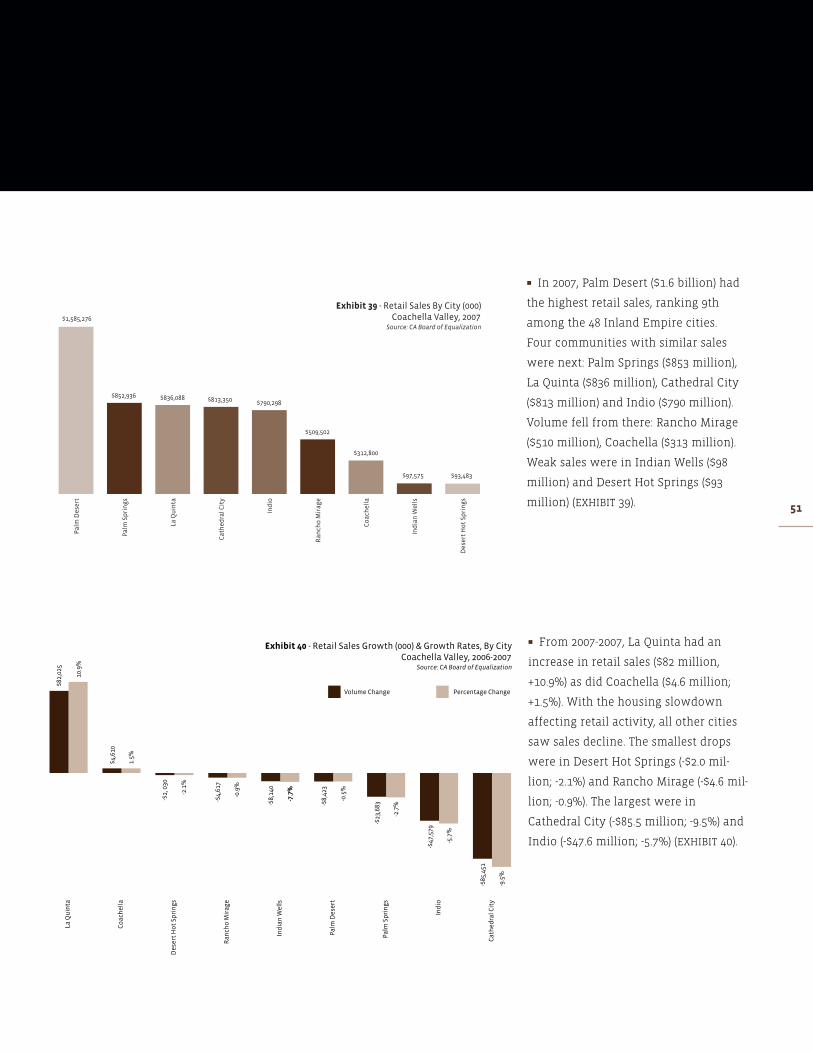

� In 2007, Palm Desert ($1.6 billion) had

the highest retail sales, ranking 9th

among the 48 Inland Empire cities.

Four communities with similar sales

were next: Palm Springs ($853 million),

La Quinta ($836 million), Cathedral City

($813 million) and Indio ($790 million).

Volume fell from there: Rancho Mirage

($510 million), Coachella ($313 million).

Weak sales were in Indian Wells ($98

million) and Desert Hot Springs ($93

million) (EXHIBIT 39).

� From 2007-2007, La Quinta had an

increase in retail sales ($82 million,

+10.9%) as did Coachella ($4.6 million;

+1.5%). With the housing slowdown

affecting retail activity, all other cities

saw sales decline. The smallest drops

were in Desert Hot Springs (-$2.0 mil-

lion; -2.1%) and Rancho Mirage (-$4.6 mil-

lion; -0.9%). The largest were in

Cathedral City (-$85.5 million; -9.5%) and

Indio (-$47.6 million; -5.7%) (EXHIBIT 40).

52

� Given the importance of retail sales

to city finances, sales per capita is a key

measure of a municipality’s ability to

provide services to its population. It

gives an estimate of the purchasing

power per resident that this tax supplies

to the city’s services. From 2000-2007, the

Coachella Valley’s per capita sales went

from $14,922 to $16,650, up $1,728 or 11.6%.

This left the valley with more sales per

person than the Inland Empire ($14,631).

That said, inflation grew 26.7% in the

seven year period, indicating that the

volume of trade per person actually fell,

as did the purchasing power of local

sales taxes per person based on this

activity. Note: with the housing crisis,

the Coachella Valley’s 2007 per capita

sales ($16,650) were down –5.8% from

the 2006 record of $17,522 (EXHIBIT 41).

� Of the Inland Empire’s major cities,

Palm Desert ($31,654) ranked third to

Montclair ($32,885) and Ontario ($32,128)

in per capita sales in 2007. Rancho

Mirage ($30,230) ranked fourth ahead of

Temecula ($26,114). Compared to other

major cities, Indian Wells ($21,207) was

next behind Corona ($24,099) Palm

Springs ($18,623), La Quinta ($17,936) and

Cathedral City ($17,183) ranked above

Riverside. Indio ($10,558) was below

Fontana ($13,013) (EXHIBIT 42).

53

� In 2007, the Coachella Valley’s $5.89

billion in retail sales were led by non-

retail outlets $942 million. That group

includes manufacturers, distributors,

builders and professionals selling direct

to consumers. Next was automotive

sales at $891 million. General merchan-

disers ($869 million) was third, followed

by restaurants ($636 million) and other

“specialty” retailers ($610 million)

(EXHIBIT 43).

54

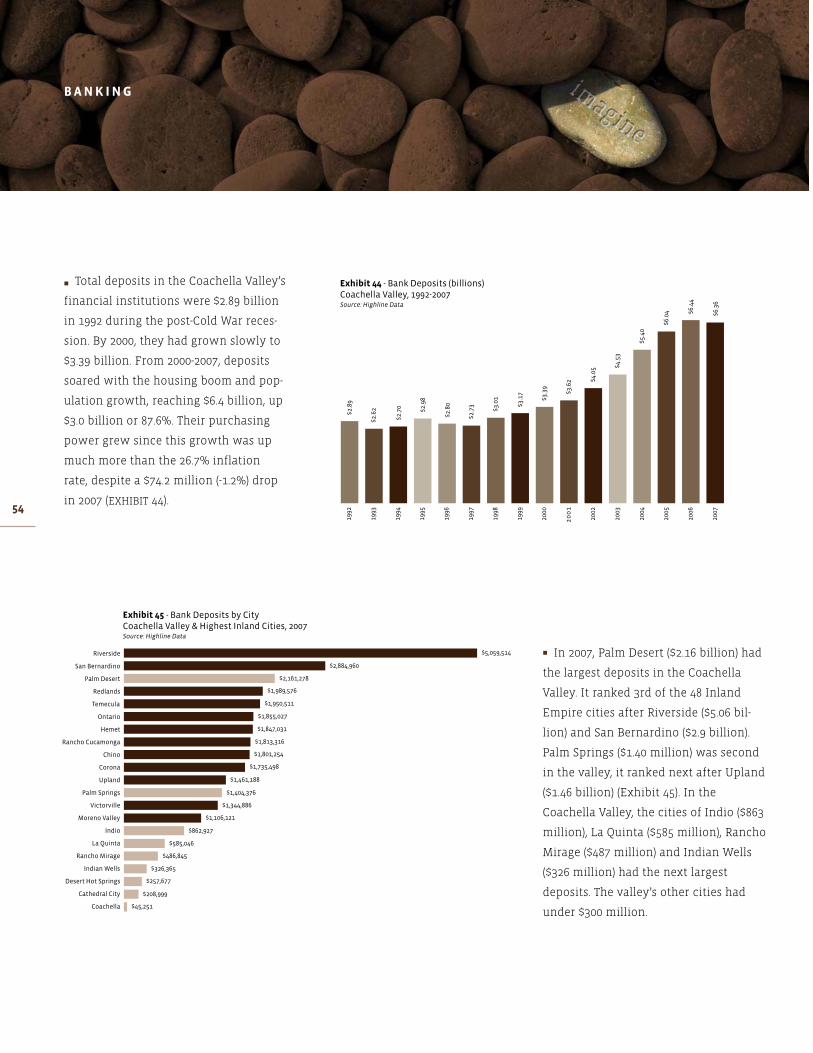

� Total deposits in the Coachella Valley’s

financial institutions were $2.89 billion

in 1992 during the post-Cold War reces-

sion. By 2000, they had grown slowly to

$3.39 billion. From 2000-2007, deposits

soared with the housing boom and pop-

ulation growth, reaching $6.4 billion, up

$3.0 billion or 87.6%. Their purchasing

power grew since this growth was up

much more than the 26.7% inflation

rate, despite a $74.2 million (-1.2%) drop

in 2007 (EXHIBIT 44).

BANK ING

� In 2007, Palm Desert ($2.16 billion) had

the largest deposits in the Coachella

Valley. It ranked 3rd of the 48 Inland

Empire cities after Riverside ($5.06 bil-

lion) and San Bernardino ($2.9 billion).

Palm Springs ($1.40 million) was second

in the valley, it ranked next after Upland

($1.46 billion) (Exhibit 45). In the

Coachella Valley, the cities of Indio ($863

million), La Quinta ($585 million), Rancho

Mirage ($487 million) and Indian Wells

($326 million) had the next largest

deposits. The valley’s other cities had

under $300 million.

55

� Deposits per capita in the Coachella

Valley rose consistently from a post-Cold

War recession low of $9,649 in 1997 to a

high of $15,402 in 2007 (EXHIBIT 46). Per

capita deposits dropped $664 to $14,738

(-4.3%) in 2007 with the economic slow-

down associated with the housing cri-

sis. For the full 2000-2007 period, per

capita deposits went from $10,759 to

$14,738, up $3,979 or 37.0%. The purchas-

ing power of deposits per person rose as

the inflation rate was only 26.7%.

� In 2007, Indian Wells ($66,732) and

Palm Desert ($43,912) ranked 1st and 2nd

in per capita deposits among the Inland

Empire’s 48 cities, ahead of Big Bear

Lake ($37,297). Palm Springs ($32,619) and

Rancho Mirage ($27,318) ranked 4th and

6th. Nearby, Yucca Valley ($24,832)

ranked 9th in the region. The valley’s

other cities, starting with La Quinta

($15,058), were below 14th ranked

Banning ($15,715) (EXHIBIT 47).

56

� In the Coachella Valley, three of

California’s mega-banks had the most

deposits in 2007. Bank of America led

with $1.13 billion in deposits for a 17.8%

share, down from 17.9% in 2007. Wells

Fargo was second with $763 million, a

12.0 % share, up from 11.9% in 2007.

Third was Washington Mutual with $717

million in deposits and a 11.3% share;

down from 11.5% in 2007. The merger of

Wachovia with World Savings Bank gave

it $486 million in deposits and a fourth

ranked 7.6% share; up from 5.9% in 2007.

� Several regional banks also had large

shares: #5 La Jolla Bank (5.7%), #6

Downey S&L (5.7%), #8 PFF Bank (4.3%)

and #9 First Bank (3.6%) (EXHIBIT 48).

� Palm Desert National Bank ($291

million), a local financial institution,

moved from ninth ranked in 2007 to

seventh ranked in 2007 as its deposits

rose 5.7% and its share market

increased from 4.2% to 4.6%.

Exhibit 48 Bank Deposits By Bank, Coachella Valley, 2007 (000)

Financial Institution 2007 Deposits (000) Market Share

Bank of America NA $1,131,838 17.8%

Wells Fargo Bk NA $763,170 12.0%

Washington Mutual Bank $717,064 11.3%

Wachovia Mortgage, FSB $484,553 7.6%

LA Jolla Bk FSB $365,346 5.7%

Downey S&LA FA $362,320 5.7%

Palm Desert NB $290,698 4.6%

PFF B&T $286,269 4.5%

Firstbank $231,801 3.6%

Canyon NB $231,277 3.6%

Union Bk of CA NA $219,946 3.5%

Rabobank, NA $219,741 3.5%

Pacific Western NB $195,492 3.1%

Guaranty Bk $167,890 2.6%

Citibank (West), FSB $164,441 2.6%

Frontier Bk FSB $128,859 2.0%

Provident Svgs Bk FSB $91,884 1.4%

Desert Commercial Bk $89,534 1.4%

California B&TC $74,783 1.2%

Other: Under 1% Each $144,064 2.3%

Total $6,360,970 100.0%

SOURCE : Highline Data

57

58

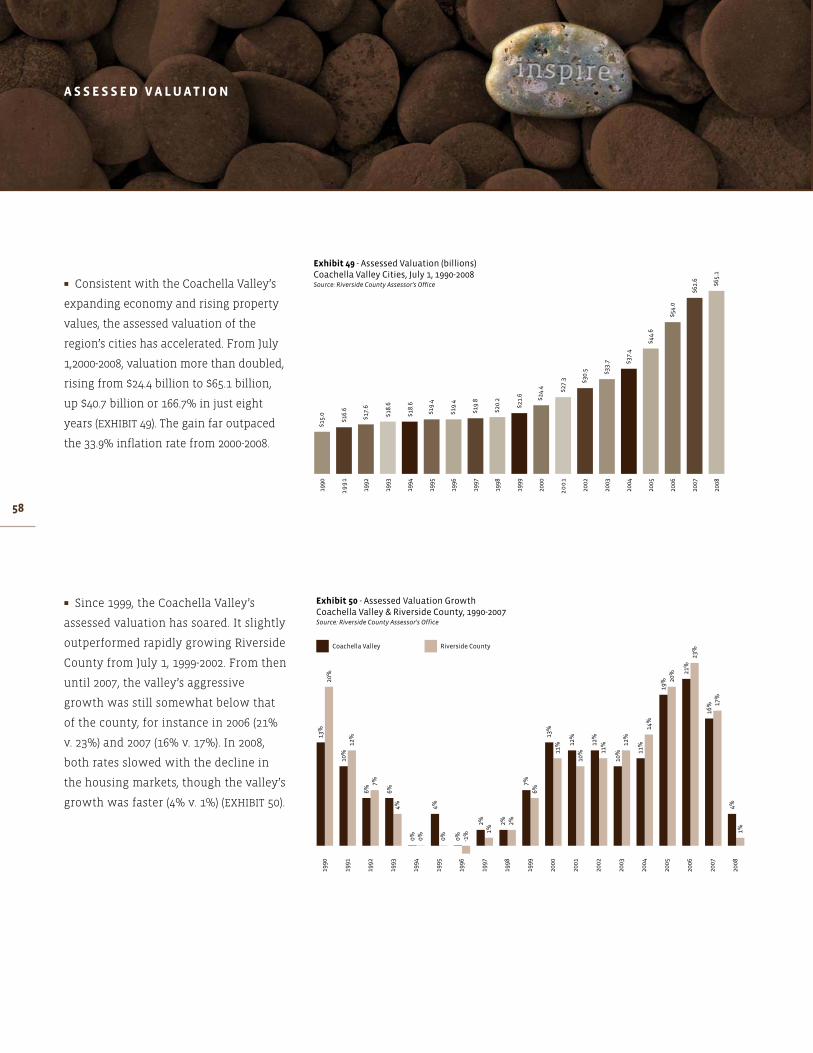

� Consistent with the Coachella Valley’s

expanding economy and rising property

values, the assessed valuation of the

region’s cities has accelerated. From July

1,2000-2008, valuation more than doubled,

rising from $24.4 billion to $65.1 billion,

up $40.7 billion or 166.7% in just eight

years (EXHIBIT 49). The gain far outpaced

the 33.9% inflation rate from 2000-2008.

� Since 1999, the Coachella Valley’s

assessed valuation has soared. It slightly

outperformed rapidly growing Riverside

County from July 1, 1999-2002. From then

until 2007, the valley’s aggressive

growth was still somewhat below that

of the county, for instance in 2006 (21%

v. 23%) and 2007 (16% v. 17%). In 2008,

both rates slowed with the decline in

the housing markets, though the valley’s

growth was faster (4% v. 1%) (EXHIBIT 50).

ASSESSED VALUAT ION

59

� In FY 2008-2009, Palm Desert ($13.8

billion) had the Coachella Valley’s

highest assessed valuation, followed

by La Quinta ($12.4 billion). Palm Springs

($10.1 billion) was third followed by

Rancho Mirage ($8.1) and Indio ($7.4

billion) (EXHIBIT 51).

� Indian Wells ($5.1 billion) was followed

by Cathedral City ($4.3 billion). The small-

est assessed valuations were in Desert

Hot Springs ($2.0 billion) and Coachella

($2.0 billion).

� Assessed valuation per capita is

another measure of a community’s

ability to finance governmental services

for each resident. This measure rose in

the Coachella Valley from $92,407 in 2000

to $173,615 in 2008, a gain of $81,208 per

person or 87.9% in just eight years

(EXHIBIT 52).

� As inflation was just 33.9% from 2000-

2008, there was a significant gain in the

purchasing power of the property taxes

collected per person due to this gain

in valuation.

60

� On July 1, 2008, five Coachella Valley

cities had the highest per capita

assessed valuations among Riverside

County’s 24 cities (EXHIBIT 53). Indian

Wells ($1,006,183) led, followed by

Rancho Mirage ($473,189), La Quinta

($289,027), Palm Desert ($270,170) and

Palm Springs ($213,930). They ranked

above Canyon Lake ($149,626) and

Temecula ($131,817).

� Per capita valuation in the valley’s

other cities were: Indio ($90,390),

Cathedral City ($82,653), Desert Hot

Springs ($77,929), and Coachella ($48,617).

The latter ranked 23rd of the county’s

24 cities above Blythe ($21,744).

61

62

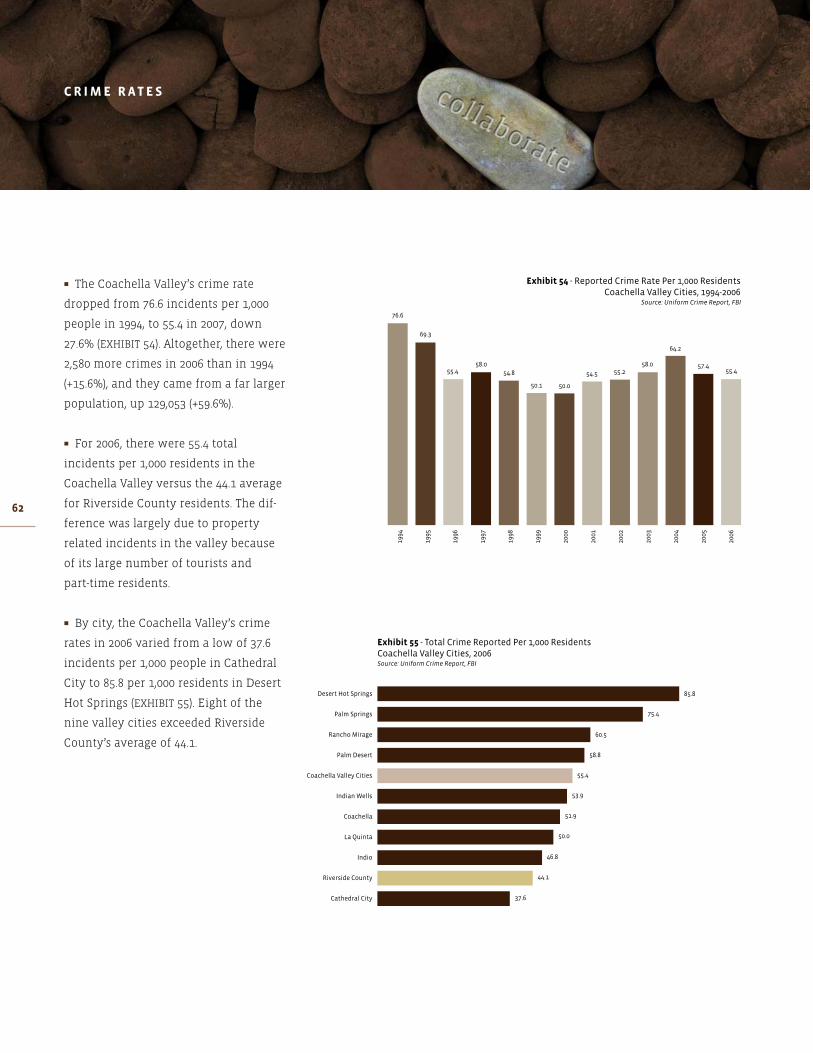

� The Coachella Valley’s crime rate

dropped from 76.6 incidents per 1,000

people in 1994, to 55.4 in 2007, down

27.6% (EXHIBIT 54). Altogether, there were

2,580 more crimes in 2006 than in 1994

(+15.6%), and they came from a far larger

population, up 129,053 (+59.6%).

� For 2006, there were 55.4 total

incidents per 1,000 residents in the

Coachella Valley versus the 44.1 average

for Riverside County residents. The dif-

ference was largely due to property

related incidents in the valley because

of its large number of tourists and

part-time residents.

� By city, the Coachella Valley’s crime

rates in 2006 varied from a low of 37.6

incidents per 1,000 people in Cathedral

City to 85.8 per 1,000 residents in Desert

Hot Springs (EXHIBIT 55). Eight of the

nine valley cities exceeded Riverside

County’s average of 44.1.

CR IME RATES

63

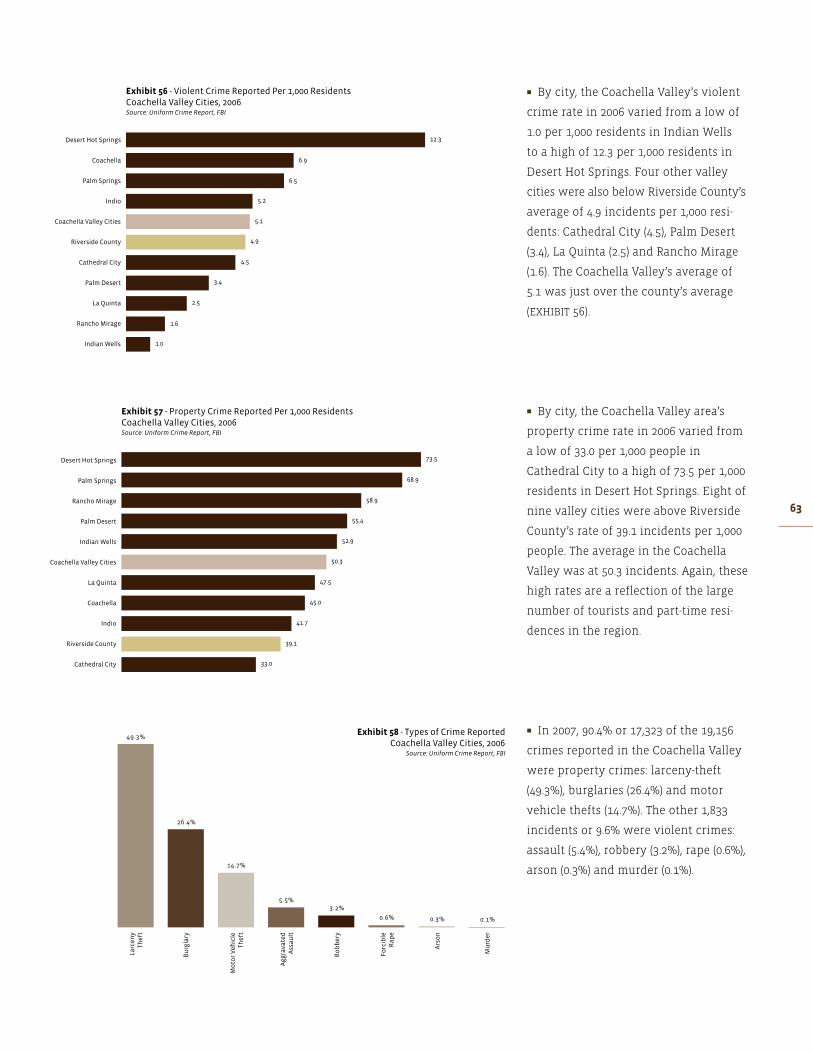

� By city, the Coachella Valley’s violent

crime rate in 2006 varied from a low of

1.0 per 1,000 residents in Indian Wells