lecture 8 - quantitative easing - hec

TRANSCRIPT

Quantitative Easing

Macro-Economic Policy

University of Lausanne

Fall 2013

Macro-Economic Policy Quantitative Easing 1 / 31

What is Quantitative Easing?

Originally used to mean continued conventional open marketoperations at zero nominal bound.Now used to mean unconventional OMO at the ZLB, such as buyinglong-term government bonds, MBS, or other assets.

I Also known as Credit Easing

Macro-Economic Policy Quantitative Easing 2 / 31

Motivation - US Interest Rates

Macro-Economic Policy Quantitative Easing 3 / 31

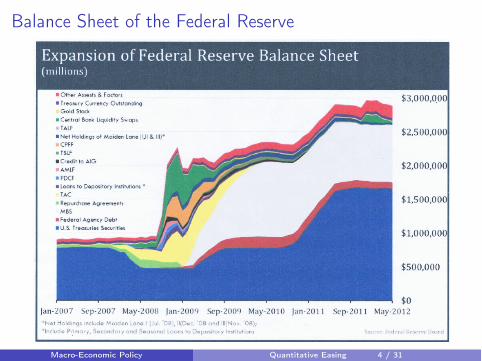

Balance Sheet of the Federal Reserve

Macro-Economic Policy Quantitative Easing 4 / 31

Quantitative versus Credit Easing

Macro-Economic Policy Quantitative Easing 5 / 31

Effects on Asset Returns

Time premiumI lower medium-term real interest rates

Inflation ExpectationsI Commitment mechanism for low nominal rates, future inflation

Macro-Economic Policy Quantitative Easing 6 / 31

Effects on Asset Returns

Cash Flow RiskI DefaultI Pre-payment

Market RiskI LiquidityI Duration and pre-payment clientele effects

Risk premiaI LiquidityI SafetyI DefaultI Pre-payment

Macro-Economic Policy Quantitative Easing 7 / 31

Channels (Two period example)

rLT = iST

+E [iST ] (Signaling)

+Term premium (safety, default, liquidity, pre-payment)

�E [⇡] (Inflation)

Macro-Economic Policy Quantitative Easing 8 / 31

Event Study Analysis

Krishnamurthy and Vissing-Jorgensen (2011)I Look at intra-day dataI Reaction of asset prices around statements by FOMCI Was there an effect?I Which were the main channels?

Macro-Economic Policy Quantitative Easing 9 / 31

Rounds of Quantitative Easing

QE1 (late 2008 and 2009)I Purchase on long-term treasuries and mortgage-backed securities

QE2 (late 2010 and beyond)I Exclusive purchase of long-term treasuries ($ 85 Billion per month)

QE3 (summer 2013 and beyond)I Exclusive purchase of mortgage backed securities ( $40 Billion per

month)

Macro-Economic Policy Quantitative Easing 10 / 31

Event Study Analysis - QE1

25/11/2008 - Fed announces intention to purchase $500B of Agencymortgage-backed securities and $100B of Agency debt.01/12/2008 - Speech by Bernanke16/12/2008 - FOMC Statement29/01/2009 - FOMC Statement: Fed may buy more agency debt,MBS, and Treasuries18/03/2009 - FOMC Statement: Increase agency debt purchases by$200B, agency MBS $1.25T, $300B long-term treasuries

Macro-Economic Policy Quantitative Easing 11 / 31

Event Study Analysis - QE2

10/08/2010 - FOMC Statement: The Committee announces that itwill keep constant the Federal Reserve’s holdings of securities at theircurrent level by reinvesting principal payments from agency debt andagency mortgage-backed securities in longer-term Treasury securities21/09/2010 - FOMC Statement: The committee maintains itsexisting policy of reinvesting principal payments and will monitordevelopments, it is prepared to provide additional accommodation ifneeded to support the economic recovery.03/11/2010 - Fed will continue its existing policy and purchase $600Bof additional treasury securities. This was widely expected and so hadlittle effect.

Macro-Economic Policy Quantitative Easing 12 / 31

QE1: 10-year Treasury Yields

Macro-Economic Policy Quantitative Easing 13 / 31

QE2: 10-year Treasury Yields

Macro-Economic Policy Quantitative Easing 14 / 31

How to identify the channels in action?

Study the effects of quantitative easing on securities that highlight aparticular channel

I Expected future short-term rates (signaling) - Federal Funds futurescontracts

I Default risk - Credit Default Swap SpreadsI Expected Inflation - Yield on nominal safe bonds minus TIPS yield (use

a nominal bond with a similar safety premium, e.g. CDS-adjusted Aaa)

Other channels are more complexI Duration risk - Differences in announcement effect between comparable

long and short-term assetsF However, safety channel confounds movements for treasuriesF Pre-payment risk channel confounds movements for MBSF Liquidity channel confounds movements for safe corporate bonds.F Use low grade corporate bonds! (deductive argument)

Macro-Economic Policy Quantitative Easing 15 / 31

How to identify the channels in action?

Pre-payment risk in MBS - Difference between fall in MBS yields andthe signaling effect (requires that the other channels do not affectMBS)

I Critique: Couldn’t this just be like saying that the duration risk channelonly applies to MBS?...

Safety channel - Agency bond yields: QE reduces supply, but does notaffect their liquidity, or default risk.Liquidity channel - Yield spread between Treasury and agency bonds:the spread should shrink.

Macro-Economic Policy Quantitative Easing 16 / 31

QE1 Channels

Present: Signaling, pre-payment risk, default risk, safety, liquidity,inflationAbsent: Duration risk

Macro-Economic Policy Quantitative Easing 17 / 31

QE2 Channels

Absent: pre-payment risk, default risk, liquidity, duration

Present: Signaling, safety, inflation

Since QE2 did not target MBS, seems reasonable the pre-payment riskchannel would be absent.What happened to the liquidity and default risk channels?

I Perhaps QE2 was taken as a negative signal for the economy -increases default risk premium

I No purchase of lower-grade bonds means there was no direct defaultrisk effect.

I Liquidity premia happened to be low in later 2010 - so removingliquidity had a negligible effect.

Macro-Economic Policy Quantitative Easing 18 / 31

Heterogeneous Effects on the Mortgage Market

Fuster Willen (2010) - Some facts about the effects of the FederalReserve’s mortgage market investments

I Interest rates on mortgages decreasedI Refinancing increased, but not new mortgages or searchesI Borrowers with high credit scores benefitted much more from the

intervention.F Perhaps this is a good thing!

I Did credit easing boost consumption?F Unlikely, since most of the benefits went to financially unconstrained

households

I Did credit easing increase house prices?F No evidence of an increase in households considering a purchase,

increasing loan amounts, or shifts in the composition of buyers.

Macro-Economic Policy Quantitative Easing 19 / 31

Fuster Willen (2010) Tables

Macro-Economic Policy Quantitative Easing 20 / 31

Macro-Economic Policy Quantitative Easing 21 / 31

Fuster Willen (2010) Figures

Macro-Economic Policy Quantitative Easing 22 / 31

Macro-Economic Policy Quantitative Easing 23 / 31

Macro-Economic Policy Quantitative Easing 24 / 31

Macro-Economic Policy Quantitative Easing 25 / 31

Macro-Economic Policy Quantitative Easing 26 / 31

Macro-Economic Policy Quantitative Easing 27 / 31

Macro-Economic Policy Quantitative Easing 28 / 31

Policy Critiques

Andrew Huszar (Nov 11, 2013 WSJ): Confessions of a QuantitativeEaser

I Quantitative easing is the greatest backdoor Wall Street bailout of alltime.

I Banks enjoyed huge capital gains on their securities, brokers collectedfees for the trades

I Banks did not issue more loans in response to quantitative easingI PIMCO analyst: $4Trillion investment for $40Billion return (0.25% of

GDP, 0.0001% return).

Macro-Economic Policy Quantitative Easing 29 / 31

A Third Way

Helicopter drops - direct delivery of cash into people’s handsNothing could be better to stimulate demand

I consumers feel relatively rich, so they spend moreI credit-constrained entrepreneurs can invest moreI demand for loans falls, interest rates fall.

Gains are spread around up-front, more politically popular.I The political attractiveness of this option is a major drawback!

Effective commitment to inflation by the central bankHard to get out. Once the money is in the system, how do you get itout?

I Implies major losses for the Fed. The treasury likes to receive adividend... political backlash.

What do you think?

Macro-Economic Policy Quantitative Easing 30 / 31

Summary

Two dimensions to unconventional monetary policy: quantitative andcredit easingPolicies succeeded in decreasing long-term interest rates

I which ones depends on which policy

Could think of other options...Should we be so concerned about ex-post policy making?

Macro-Economic Policy Quantitative Easing 31 / 31