lehman brothers 9th annual global healthcare conference march 8, 2006

DESCRIPTION

Lehman Brothers 9th Annual Global Healthcare Conference March 8, 2006. Forward-Looking Statements. - PowerPoint PPT PresentationTRANSCRIPT

Lehman Brothers9th Annual Global Healthcare

ConferenceMarch 8, 2006

2

Statements included in this presentation or in the oral comments made as part of this presentation may contain forward-looking statements, including but not limited to statements of the Company’s plans, objectives, expectations or intentions, that involve risk and uncertainties.

The Company’s actual results may differ significantly from those projected or suggested in any forward-looking statement due to a variety of factors, which are discussed in detail in the Company’s filings with the Securities and Exchange Commission.

Forward-Looking Statements

3

Today’s Challenging Environment:

Maintaining Access to Safe and Affordable Drugs

4

% Increase in Unmanaged PMPY Cost

11.311.211.612.011.810.6

15.5

18.5

0

4

8

12

16

20

2002 2003 2004 2005 2006 2007 2008 2009

Perc

ent

Rx's Cost

Unmanaged Prescription Drug Trend

Plan Sponsors Will Likely Increase the Use of PBM Tools to Manage Drug Spend

Source: 2004 Drug Trend Report

5

Our Value Proposition: Complete Alignment

To reduce pharmacy costs, without compromising health

outcomes, while maximizing patient satisfaction

6

Ability to

manage trend

2-tier

3-tier

Step Therapy

Exclusive Home Delivery

As Plan Sponsors Take Advantage of Our Tools

to Better Mange Trend, The Better We Perform

The Art of Trend Management -- Alignment

High Performance Formulary

Restricted Retail Network

Generic Utilization Programs

Specialty Pharmacy

Plan sponsor appetite for innovative clinical tools

7

1. Evaluate relative clinical value

Cost per prescription

Alignment - Building a Formulary

Drug A

Drug B

Drug C

$60$50 $70 $80

Rela

tive c

linic

al

valu

e

8

1. Evaluate relative clinical value

2. Determine net cost

Cost per prescription

Alignment - Building a Formulary

Drug A

Drug B

Drug C

$60$50 $70 $80

Rela

tive c

linic

al

valu

e

9

Cost per prescription

Drug A

Drug B

Drug C

Most cost effective

Rela

tive c

linic

al

valu

e

$50 $60 $70 $80

Alignment - Building a Formulary

1. Evaluate relative clinical value

2. Determine net cost

3. Account for market share

AA BB

CC

10

1. Evaluate relative clinical value

2. Determine net cost

3. Account for market share

4. Account for rebates

Cost per prescription

Rela

tive c

linic

al

valu

e

$50 $60 $70 $80

Drug A

Drug B

Drug C

Most cost effective

Alignment - Building a Formulary

AA BB

CC

AA BB

11

1. Evaluate relative clinical value

2. Determine net cost

3. Account for market share

4. Account for rebates

5. Select formulary products

Cost per prescription

Rela

tive c

linic

al

valu

e

$50 $60 $70 $80

Drug A

Drug B

Drug C

Most cost effective

Drug C

Drug ADrug B

Most cost effective

Alignment - Building a Formulary

Exceptions: * Market dynamics can trump net

cost* High Performance Formulary

AA BB

CC

12

More Number of Drugs Fewer

Ben

efi

t O

pti

on

s

Impact on Client

Impact on Patient

Impact on ESI

Lower drug cost

More choice

Lower co payment

More choice

Higher Profit/Rx

More Flexibility

Alignment – Formulary Management

Therapy Class

We Provide Flexible Formulary Management

1. Select number of drugs in therapy class 2. Determine formulary control 3. Drive towards lowest overall cost

# ofdrugs

# ofdrugs

# ofdrugs

Open

DifferentialCo-pay

ClosedLowestOverall

Cost

13

Alignment – Generic Utilization

Generic Utilization Rate

38%40%42%44%46%48%50%52%54%56%

Q1 0

2

Q2 0

2

Q3 0

2

Q4 0

2

Q1 0

3

Q2 0

3

Q3 0

3

Q4 0

3

Q1 0

4

Q2 0

4

Q3 0

4

Q4 0

4

Q1 0

5

Q2 0

5

Q3 0

5

Q4 0

5

ESI PBM B PBM CImpact on

ClientImpact on

PatientImpact on

ESI

Lowest drug cost

Lowest co payment

Highest profit/Rx

Source: From public filings

Express Scripts Leads in Generic Utilization

14

ESI Analysis

Our Clients and Members Will Benefit From a Growing Generic Opportunity

Alignment – Growing Generic Opportunity

15

Impact on Client

Impact on Patient

Impact on ESI

Lower drug cost

Lower co payment

Higher Profit/Rx

Alignment – Clinical Programs

0

2

4

6

8

10

12

14

16

Mil

lio

ns

Q1 2003 Q4 2004 2006E

Members in Step Therapy Programs

Clients using step therapy realize on average a

2 percentage point increase in generic utilization

Plan Designs Encourage Greater Use of

Generics and Preferred Low-cost Brands

16

Alignment – Specialty Pharmacy

Sources:IMS Data through November 2004Wall Street Equity Research, 2004CMS National Healthcare Expenditure Projection: 2003 – 2013Data on file: CuraScript.

2004 Total Outpatient Pharmacy Spend $190 Billion

2008 Projected Outpatient Pharmacy Spend $283 Billion

26%26%18%18%

Traditional SpendTraditional Spend$210 Billion$210 Billion

Specialty SpendSpecialty Spend$73 Billion$73 Billion

Specialty SpendSpecialty Spend$35 Billion$35 Billion

Traditional SpendTraditional Spend$155 Billion$155 Billion

Impact on Client

Impact on Patient

Impact on ESI

Lower drug cost

Lower co payment

Higher profit/Rx

Improved reporting

Improved quality of

care

Higher client

satisfaction

Clients are Seeking Solutions for High-cost

Specialty Drugs

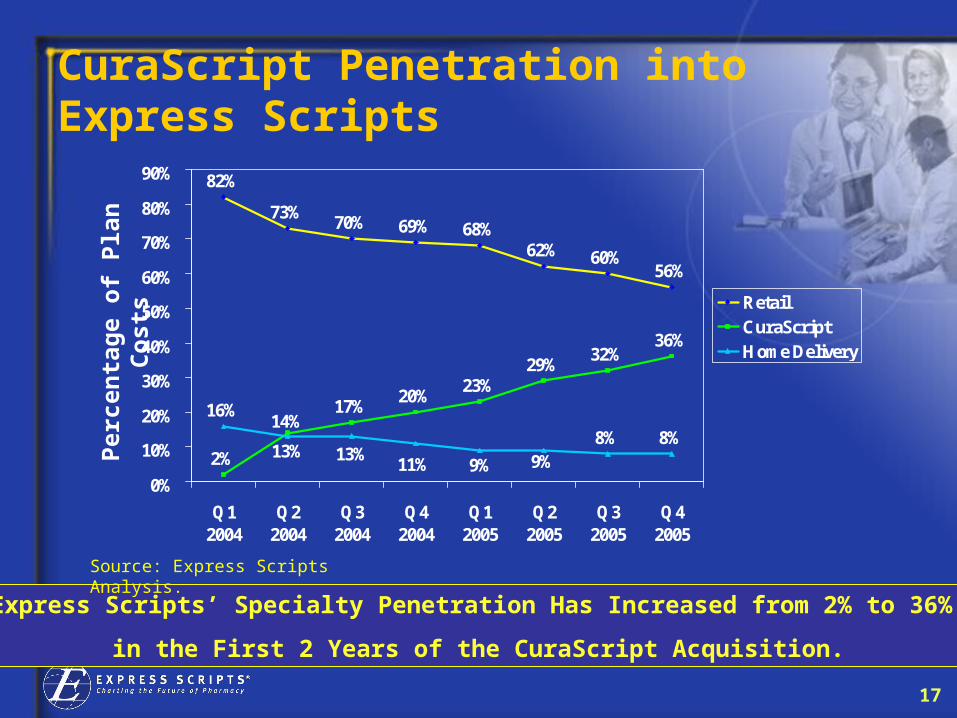

17

Express Scripts’ Specialty Penetration Has Increased from 2% to 36%

in the First 2 Years of the CuraScript Acquisition.

Per

cent

age

of P

lan

Cos

ts

Source: Express Scripts Analysis.

82%

73%70% 69% 68%

62% 60%56%

2%

17%20%

23%29%

32%36%

16%

8% 8%14%

9%9%11%13%13%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Q12004

Q22004

Q32004

Q42004

Q12005

Q22005

Q32005

Q42005

RetailCuraScriptHome Delivery

CuraScript Penetration intoExpress Scripts

18

Alignment – Home Delivery

Impact on Client

Impact on Patient

Impact on ESI

Lower drug cost

Choice

Lower co paymentChoice

Higher profit/Rx

We Offer Highly Efficient, Cost-effective

Home Delivery

19

16.4%

18.5%

21.6%

25%-26%

22.3%

20.2%

17.2%

13.8%12.6%

15.8%

13.1%

0

100

200

300

400

500

600

Ad

just

ed C

laim

s* (

mill

ion

s)

12.0%13.0%14.0%15.0%16.0%17.0%18.0%19.0%20.0%21.0%22.0%23.0%24.0%25.0%26.0%

% m

ail p

enet

ratio

n

Total Adjusted Claims Home Delivery Penetration

* Represents network claims plus 3 times home delivery claims –home delivery claims are 90 days vs. 30 days in the network.

D IVERSIFIED®

Increased home delivery penetration

Home Delivery Helps Manage the Cost of Maintenance Drugs

Alignment – Growing Demand for Home Delivery

Excludes UHC claims

20

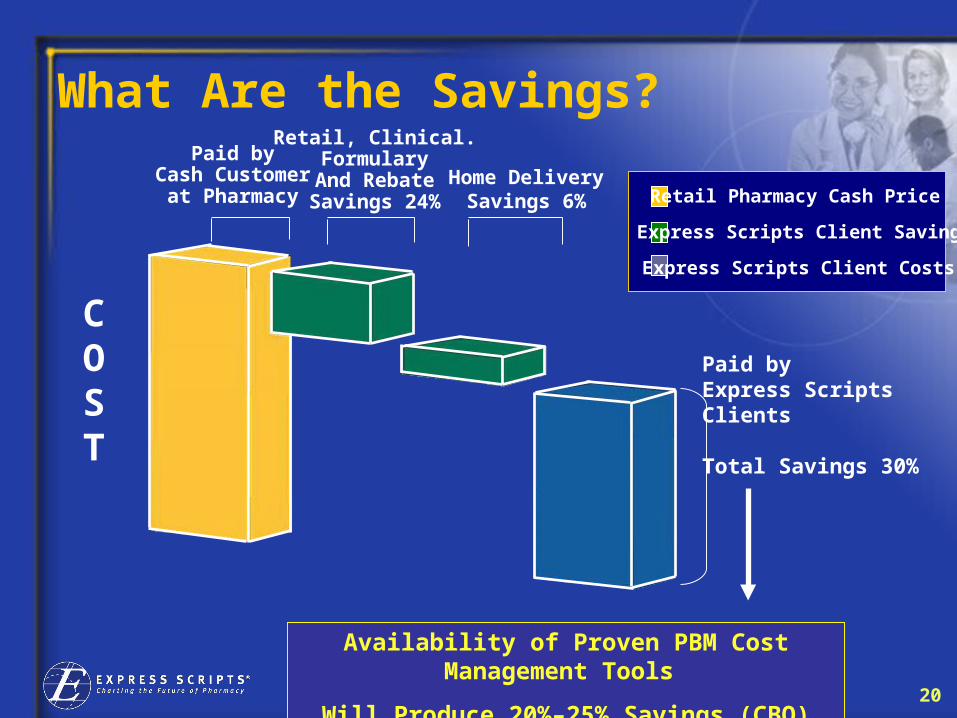

What Are the Savings?

Availability of Proven PBM Cost Management Tools

Will Produce 20%–25% Savings (CBO)

Paid byCash Customer

at Pharmacy

Retail, Clinical.Formulary

And RebateSavings 24%

Home Delivery

Savings 6%

Paid byExpress ScriptsClients

Total Savings 30%

COST

Retail Pharmacy Cash Price

Express Scripts Client Savings

Express Scripts Client Costs

21

Alignment – A Win-Win-Win Proposition

Retail Non-pref. Brand

Retail Pref.

BrandGenerics

Mail Pharma

cy

Increased Savings

Opportunities:

Client

Member

Increased

Profit

Opportunities:

Express Scripts

Moving to preferred brands, home delivery and generics

We Make Money by Saving Clients and Members Money

Moving to preferred brands, home delivery and generics

Moving to preferred brands, home delivery and generics

22

We Deliver Against Client and Patient Expectations:

To make the use of prescription drugs safer and

more affordable

23

Client/Patient Focus

Commercial24%

Canada12%

Managed Care40%

Public Sector24%

By membership

Health Plan Sponsors Recognize Express Scripts Single

Focus on Making Prescription Drugs More Affordable

Why Express Scripts?• Alignment With Clients• Trend management tools• Generics• Specialty

24

Client Satisfaction continues to improve..

Increases Were Recognized in All Categories With

Likelihood to Renew Showing the Largest Increase

78%80%82%84%86%88%90%92%94%96%98%

ESI Performance ExceedsExpectations

Likelihood toRecommend

2003 2004 2005

25

Our Financial Results

Express Scripts has demonstrated a proven track

record

26

Q4 2005 Highlights

– Adjusted EPS of $0.77*, up 45% from $0.53 last year

• For 2005, adjusted EPS of $2.60*, up 34% from 2004

– Cash flow from operations of $262 M vs. $193 M last year

• For 2005, cash flow of $793 M vs. $496M in 2004

– Gross profit of $364 million, up 38%• Gross profit per adjusted claim was $2.54, up 34%

– EBITDA of $220 M, up 42% • EBITDA per adjusted claim was $1.53, up 37%

* Reconciliation of reported EPS to adjusted EPS is included in Table 4 of the 4Q 2005 earnings release

27

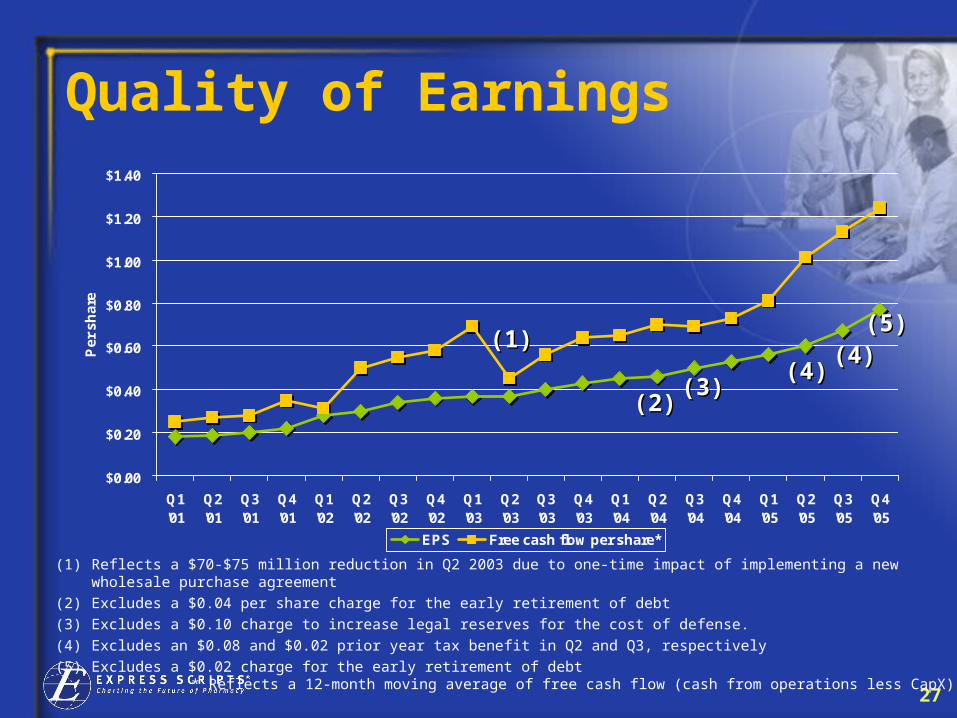

Quality of Earnings

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

Q1'01

Q2'01

Q3'01

Q4'01

Q1'02

Q2'02

Q3'02

Q4'02

Q1'03

Q2'03

Q3'03

Q4'03

Q1'04

Q2'04

Q3'04

Q4'04

Q1'05

Q2'05

Q3'05

Q4'05

Pe

r s

ha

re

EPS Free cash flow per share*

(1) Reflects a $70-$75 million reduction in Q2 2003 due to one-time impact of implementing a new wholesale purchase agreement

(2) Excludes a $0.04 per share charge for the early retirement of debt(3) Excludes a $0.10 charge to increase legal reserves for the cost of defense.(4) Excludes an $0.08 and $0.02 prior year tax benefit in Q2 and Q3, respectively(5) Excludes a $0.02 charge for the early retirement of debt

(1)(1)

(2)(2)

* Reflects a 12-month moving average of free cash flow (cash from operations less CapX)

(3)(3)(4)(4)

(4)(4)(5)(5)

28

Components Of EPS Growth

9% 10%5%

7%

15%

38%

5%

9%

2%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2004 2005 4Q 2005

Rx Growth EBITDA/ Rx Growth Cap Structure/ Other

29

-10%

-5%

0%

5%

10%

15%

20%

1999 2000 2001 2002 2003 2004 2005

Adju

sted C

laim

s G

row

th

ESI Medco Caremark

Major PBM Prescription Growth

Note: Rx growth for Medco, Caremark reflect as configured today

30

Claims Volume Vs. EPS Growth

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Q3 '04 Q4 '04 Q1 '05 Q2 '05 Q3 '05 Q4 '05

EPS growth Adj. claim growth

(1) Excludes a $0.10 charge to increase legal reserves (4) Reflects the June 1st anniversary of the DoD retail contract

(2) Excludes an $0.08 prior year tax benefit (5) Excludes a $0.02 charge for early retirement of debt(3) Excludes a $0.02 prior year tax benefit

(2)(2)(3)(3)

(1)(1)

Expanding Margins Supports Strong EPS Growth on More Modest Claims Growth

(4)(4)

(5)(5)

31

Profits Per Claim Growth

$1.32

$1.53

$1.13 $1.12

$1.05$1.03

$0.88$0.81

$1.19

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

2000 2001 2002 2003 2004** Q1 '05 Q2 '05 Q3 '05 Q4 '05

EBITDA* per adjusted claim

* A reconciliation of EBITDA to net income and to net cash provided by operating activities can be found in the Investor Relations

section of Express Scripts’ Web site, www.express-scripts.com under Presentations.

** Excluding $25 million charge to increase legal reserves for the cost of defense and $5.5 million termination payment received.

*** Based on 2005 average EBITDA per adjusted Rx of $1.29

Pricing can be lowered as clients tighten formulary compliance, increase home delivery, utilize generics and restrict retail networks. These changes result in lower prices to our clients and greater profits to Express Scripts.

10% CAGR***

32

Gross Profit* / SG&A* / EBITDA per Adj. Rx

Future EBITDA per Adj. Rx Must Come From Gross Profit per Adj. Rx

* Before depreciation and amortization** Excluding $25 million charge to increase legal reserves for the cost of defense and $5.5 million termination payment received. Source: Express Scripts Analysis.

$1.32$1.53

$2.20

$2.61

$0.78 $0.83 $0.90$0.80 $0.74 $0.82 $0.83 $0.88

$1.08

$1.13 $1.12$1.05$1.03

$0.88$0.81

$1.19

$1.59$1.71

$1.93 $1.85$1.87 $1.94

$2.02

$0.50$0.70$0.90$1.10$1.30$1.50$1.70$1.90$2.10$2.30$2.50$2.70

2000 2001 2002 2003 2004** Q1 2005 Q2 2005 Q3 2005 Q4 2005

EBITDA per Adj Rx Gross profit per Adj. Rx SGA per Adj Rx

``

33

Focus on Return on Invested Capital (ROIC)

Express Scripts ROIC*

0%2%

4%6%

8%10%

12%14%

16%18%

20%20

00

2001

2002

2003

2004

**

2005

ROIC is our Preferred Performance Metric

* Reflects operating income less tax divided by average invested capital, which consists of stockholder’s equity, plus interest

bearing liabilities plus long-term deferred income taxes, net. ** Excludes $25 million charge to increase legal reserves for the cost of defense and 5.5 million termination payment received

34

Peer Group Total Return - 2005

ESI’s 119% Return Was More than 3.5 Times Our Peer Group

41.2% 38.8%

3.0%

51.2%

15.9%

31.4%

17.9%

37.1% 34.1%

119.3%

0%

20%

40%

60%

80%

100%

120%

Peer group avg.

32.4%

35

S&P Total Return – 2005

41

142

179

84

35

114 4

0

25

50

75

100

125

150

175

200

Total Return

# of

Com

pani

es

Only 2 Companies in the S&P 500 Exceeded ESI’s

Total Return to Stockholders of 119% in 2005

Note: Returns reflect stock price increase plus dividend yield

36

Our Value Proposition Will Continue to Drive Growth

• Making the use of drugs safer and more affordable is more important than ever

• Plan sponsors will increasingly deploy our tools

• Express Scripts is well-positioned for sustainable growth

• Strong market fundamentals/new business opportunities • Increased use of home delivery and generic drugs• Growth in management of specialty pharmacy• Productivity and capital structure improvements

• We have taken a different approach• Alignment -- we make money by saving our clients money

• Strategic acquisitions have enhanced our value proposition