lehman brothers financial service conference - credit … · lehman brothers financial services...

TRANSCRIPT

Lehman Brothers Financial Services Conference

New YorkSeptember 9, 2008

David Mathers, Head of Finance, Investment Banking

Lehman Brothers ConferenceSlide 2

Cautionary statement

Cautionary statement regarding forward-looking and non-GAAP information

This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995.

Forward-looking statements involve inherent risks and uncertainties, and we might not be able to achieve the predictions, forecasts, projections and other outcomes we describe or imply in forward-looking statements.

A number of important factors could cause results to differ materially from the plans, objectives, expectations, estimates and intentions we express in these forward-looking statements, including those we identify in "Risk Factors" in our Annual Report on Form 20-F for the fiscal year ended December 31, 2007 filed with the US Securities and Exchange Commission, and in other public filings and press releases.

We do not intend to update these forward-looking statements except as may be required by applicable laws.

This presentation contains non-GAAP financial information. Information needed to reconcile such non-GAAP financial information to the most directly comparable measures under GAAP can be found in Credit Suisse Group's second quarter report 2008.

Lehman Brothers ConferenceSlide 3

Financial Performance

Risk Reduction

Financial Markets

Key Competitive Advantages

Lehman Brothers ConferenceSlide 4

Private Banking continues to deliver good results

Solid results across most Investment Banking and Asset Management businesses

Credit Suisse has significant earnings power

Benefit from a diversified and integrated global business

Well-positioned to create long-term value and seize opportunities that arise from market dislocation

Lehman Brothers ConferenceSlide 5

All divisions profitable

Asset ManagementPre-tax income in CHF m

Investment BankingPrivate Banking

2,502

(3,460)

281 299

(468)

1671,381 1,324 1,220

2Q07 1Q08 2Q08

! Good results evidencing the strength of business

! Strong asset gathering and hiring trends across all regions

! Continue to implement international growth strategy

! 2Q08 operating earningsof CHF 650m 1)

! Most areas with good results! Immaterial net valuation

reductions of CHF 22m ! Significant progress in

reducing risk exposure

! Stable fee-based gross margin

! Strong inflows in alternative investments

! Reduced 'liftout' assets

1) Excluding a fair value adjustment on own debt of CHF (503)m and a net litigation credit of CHF 134m

Lehman Brothers ConferenceSlide 6

Continued momentum in Wealth Management

Good net asset inflows Gross margin on AuM at high level

1513

1012

1514

Net asset inflowsof CHF 50.2bn with

6.4% net growth rate

1Q08

86

30

Recurring

Transaction-based

CHF bn basis points

2Q081Q07 2Q07 3Q07 4Q07

117117 116112113118

1Q08 2Q081Q07 2Q07 3Q07 4Q07

Lehman Brothers ConferenceSlide 7

Fixed income trading with continued difficult market conditions; Strong equity trading resultFixed income trading net revenuesCHF m

6M07 6M08 2Q07 1Q08 2Q08

6,0543,282

(1,576)

320

(1,256)

! Increased revenues in RMBS, Europe high grade and life finance

! 2Q08 revenues benefit from substantial reductions in writedowns

! Reported revenues of CHF 320 m include writedowns of CHF 391m 1) and a fair value reduction on own debt of CHF 453m

1) Does not include offsetting gains of CHF 369m reported in debt underwriting and other revenues

6M07 6M08 2Q07 1Q08 2Q08

4,646

2,475

1,379

2,255

3,634

(9)%

(22)%

+64%

Equity trading net revenues

! Prime services generated near-record revenues with growing client balances and new mandates

! Near-record revenues in equity derivatives, driven by strength in all regions and products

! Strong result in the global cash business, driven by increased client flows and growth in AES

Lehman Brothers ConferenceSlide 8

Underwriting fees still adversely affected by market conditions

Underwriting feesCHF m

6M07 6M08 2Q07 1Q08 2Q08

1,438

713

136 216352

Advisory and other feesCHF m

6M07 6M08 2Q07 1Q08 2Q08

1,143632

396 364

760

724417 413 172 245

Debt underwriting

Equity underwriting

! Equity underwriting impacted by lower levels of industry-wide equity issuance, particularly in areas of historical strength for CS, and lower market share

! Credit environment has continued to impact high-yield and leveraged lending issuance

! High Grade performed well

! Solid advisory results as increase in strategic M&A partly compensated for decline in sponsor activity

! Global M&A volume down from strong 2Q07 ! #5 in announced M&A for 1H08 and #4 in

the Americas

Lehman Brothers ConferenceSlide 9

Financial Performance

Risk Reduction

Financial Markets

Key Competitive Advantages

Lehman Brothers ConferenceSlide 10

Significant progress in reducing risk positions

Leveraged finance Commercial mortgages

Residential mortgages 1) CDO trading 2)

3Q07 4Q07 1Q08 2Q08

59.2

35.1

UnfundedFunded

-76%Origination-based

(exposures shown gross)

Trading-based

(exposures shown net)

Net writedowns:2007 (0.8)1Q08 (1.7)2Q08 (0.1)

Exposures and writedowns in CHF bn

20.8

3Q07 4Q07 1Q08 2Q08

35.925.9

-58%

19.3

3Q07 4Q07 1Q08 2Q08

16.2

8.7

Other

Subprime

-67%

5.5

4Q07 1Q08 2Q08

4.6

1.9-76%

1.1

Net writedowns:2007 (0.6)1Q08 (0.8)2Q08 (0.5)

Net writedowns:2007 (0.5)1Q08 (0.1)2Q08 0.0

Net writedowns:2007 (1.3)1Q08 (2.7)2Q08 0.5

14.4 15.0

5.4

1) All non-agency business, including higher quality segments; global total; and year-end positions related to US subprime; total IB subprime is CHF 1.9bn (across RMBS & CDOs)

2) Exposures computed per 0% IDR methodology

Lehman Brothers ConferenceSlide 11

Financial Performance

Risk Reduction

Financial Markets

Key Competitive Advantages

Lehman Brothers ConferenceSlide 12

60

65

70

75

80

85

90

95

100

105

110

Jan-07 May-07 Aug-07 Dec-07 Apr-08 Aug-08

S&P 500 FTSE 100 MSCI World

0

5,000

10,000

15,000

20,000

25,000

30,000

Equity market performance

Market conditions continue to be difficult

Leveraged Finance spread trends

CMBS spread trends

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

Jan-07 May-07 Sep-07 Dec-07 Apr-08 Aug-08

AAA AA BBB

1,952

814

176

ABX priceEquity trading volume (NYSE and NASDAQ)

Trading volumeIndexed price change

-

100

200

300

400

500

600

700

800

900

Jan-07 May-07 Aug-07 Dec-07 Apr-08 Aug-08

CDX.NA.HY

iTraxx Europe Crossover

714

549

0

10

20

30

40

50

60

70

80

90

100

110

Jan-07 May-07 Aug-07 Dec-07 Apr-08 Aug-08

ABX HE AAA 06-02ABX HE BBB 06-02

66

5

Notes:1) All data through August 29, 2008

Lehman Brothers ConferenceSlide 13

Global announced M&A volumes

M&A less severely affected than underwriting

2005 2006 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08to

date

1) 3Q08 to date includes all of July and August 2) Source: Thomson / SDC3) Source: Standard & Poor's4) Leveraged loan volume as of August 21, 2008, High-yield volume includes all of July and August

Global CMBS origination volumesCommercial Mortgage Alert / Thomson

2005 2006 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08to

date

Thomson / SDC

1,4721,190

858730 836

Global ECM origination volumesDealogic / Equidesk

292

168

294

124

265

(USD bn)(USD bn)

(USD bn)

191149

1,7811,523

2005 2006 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08to

date

Leveraged finance origination volumesHigh-yield new issuance 2)

Leveraged loan volume 3)187

75

85

10

78

33466

4925

(USD bn)

47

120

75

30

Quarterly avg Quarterly avg

Quarterly avg2005 2006 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08

todate

Quarterly avg

5975

110

74

384

4)

81

60649

10 11

1)

0.5

1) 1)

Lehman Brothers ConferenceSlide 14

Financial Performance

Risk Reduction

Financial Markets

Key Competitive Advantages

Lehman Brothers ConferenceSlide 15

Credit Suisse�s competitive advantages

Diversified product offeringContinue build-out in key business areas, such as Derivatives and Prime Services

Emphasis on client-led businessesClient account management

�Integrated Bank� collaboration

Geographically diverseStrong presence across developed and

emerging markets

History of innovationStrong track record: AES, Life Finance

Continue to reinvent our business

Key competitive strengths of Credit Suisse Examples / Actions / Track Record

1/2

Lehman Brothers ConferenceSlide 16

Credit Suisse competitive advantages

Ability to adapt to weaker macro environment

Continued focus on efficiency,expense management

Diversified funding base, price credit correctly

Stable funding base; conservative liquidity management

Investment in people

Rebalance headcount between businesses

Momentum toward market-leading status

Key competitive strengths of Credit Suisse Examples / Actions / Track Record

2/2

Lehman Brothers ConferenceSlide 17

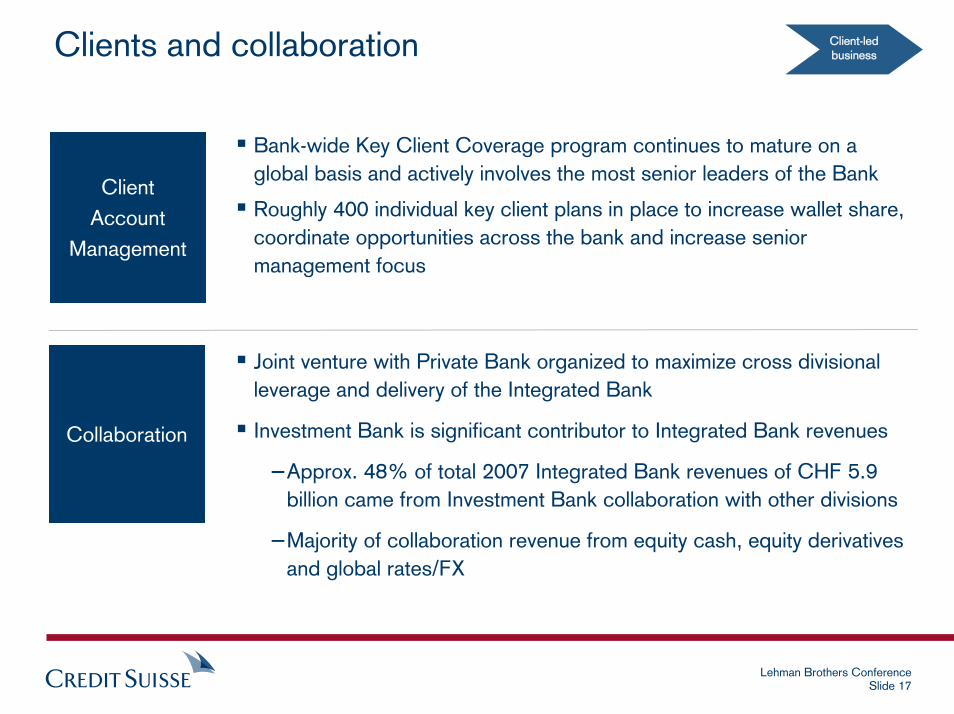

Clients and collaboration

ClientAccount

Management

! Bank-wide Key Client Coverage program continues to mature on a global basis and actively involves the most senior leaders of the Bank

! Roughly 400 individual key client plans in place to increase wallet share, coordinate opportunities across the bank and increase senior management focus

Collaboration

! Joint venture with Private Bank organized to maximize cross divisional leverage and delivery of the Integrated Bank

! Investment Bank is significant contributor to Integrated Bank revenues

�Approx. 48% of total 2007 Integrated Bank revenues of CHF 5.9 billion came from Investment Bank collaboration with other divisions

�Majority of collaboration revenue from equity cash, equity derivatives and global rates/FX

Client-led business

Lehman Brothers ConferenceSlide 18

Product innovation

! Revenues up over 50% vs. H107

! Recently registered first 1 billion share day in US AES (July 17)

! CrossFinder: #2 dark pool in US (more than160 million average daily shares crossed)

AES Quarterly Revenue Growth Life Finance Quarterly Revenue Growth

! Dominant market position in trading and distributing both longevity and mortality risk

! Trading in both physical (life settlements, premium finance) and synthetic (swaps, structured notes) forms

! Expanding internationally (Europe in 2008, Asia in 2009)

Innovation

47%

2Q07 1Q08 2Q084Q073Q07

201%

2Q07 1Q08 2Q084Q073Q07

Lehman Brothers ConferenceSlide 19

APAC = Asia / Pacific, EMEA = Europe, Middle East and Africa

Continued geographic diversification

Expansion of global footprint

In 2007 and 1H08, we strengthened our presence in the following countries:

Australia China Kazakhstan UkraineAustria India Panama United States Brazil Israel Turkey Pakistan

New York

Santiago

Bogotá

Buenos Aires

Monterrey

San FranciscoLos Angeles

Irvine Atlanta

LondonParis

Madrid

Zurich

Hong Kong

Pune

Singapore

Wroclaw

Montreal

Toronto

Milan

Russian Federation

Melbourne

SydneyPerth

Ukraine

Bangkok

Beijing

JakartaKuala Lumpur

DallasHouston

Mexico City

BostonChicago

MiamiNassau

MontevideoSão Paulo

Rio de Janeiro

Cayman Islands

Kazakhstan

U.A.E.

QatarNigeria

South Africa

Czech Republic

PhilippinesMalaysia

Tokyo

Geographically diverse

* Key IB offices in bold

+23%

+15%-19%

+16%

Credit Suisse 2007 net revenues by region

in CHF bn and up/down in % vs. 2006

4.0

10.410.4

11.5

Americas EMEA

APACSwitzerland

Lehman Brothers ConferenceSlide 20

Diversification into less correlated businesses

Prime Services Quarterly Revenue Growth

! Near-record revenue quarter for equity derivatives

! Record corporate and emerging markets activity

! Strong activity in US and EMEA flow derivatives

! Ongoing focus on infrastructure and efficiency

Diversified product offering

Equity Derivatives Quarterly Revenue Growth

! Near-record quarter with increased client balances and new client mandates

! CS viewed as a strong counterparty and a �safe haven� given strength and stability of funding and liquidity

! Well-positioned for �flight to quality,� with steady transfers of business from competitors boosting balances by over 15% in 1H08

68%

2Q07 1Q08 2Q084Q073Q07

7%

2Q07 1Q08 2Q084Q073Q07

Lehman Brothers ConferenceSlide 21

Disciplined cost management in Investment Banking

1) Excluding net litigation credit of CHF 134m in 2Q08

Macro environment

Other operating expenses (in CHF m)

! Other operating expenses1) decreased CHF 108m, or 5%, from 6M07, CHF 16m from 1Q08 and CHF 64m from 2Q07

! This reflects higher average headcount compared to 6M07, offset by cost reduction efforts, a stronger Swiss franc and, in 2Q08, lower commission spend

1)

1,097

2,178

1,0811)

6M07 6M08 3Q07 1Q08 2Q084Q07

1,232 1,300(11)%

2Q07

1,145

2,286

2,044

947

6M07 6M08 3Q07 1Q08 2Q084Q072Q07

172

149

175

184

145

153

168

G&A per head1) (in CHF 000�s)

(13)%

Lehman Brothers ConferenceSlide 22

Proactive reorientation of resources to capture growth

Headcount Change � 2Q 2007 to 2Q 2008

Investment in people

-50%

+50%

+100%

0%

Life Finance Commodities EQ Derivs. Prime Svcs. Lev Fin CMBS CDOs RMBS

Lehman Brothers ConferenceSlide 23

Conservative funding structure

Asset and liabilities by category, end of 2Q08

Assets Capital and liabilities

! Strong deposit base

! Long-term debt available to fund short-term trading book

! Benefited from 'flight to quality' during crisis, adding medium-term funding

! Integrated bank enables efficient access to retail funding and liquid markets globally

! All internal funding priced at market levels to ensure correct disciplines

CHF bn

Diversified funding base

1,230 1,230

Lehman Brothers ConferenceSlide 24

Well diversified unsecured funding mix

Unsecured funding by type / product

Retail &private banking

deposits 1)

50%Long-term

debt 2)

29%

Institutional deposits 3)

21%

! Well diversified funding distribution by client type and product

! Client deposits increased 15%, or CHF 37 bn, during 2007

! Centralized funding function covering both CDs and long-term borrowing ensures optimum efficiency in global market access

Total:CHF 541bn

1) Time, demand and saving deposits2) Structured notes, long-term bonds and subordinated debt3) Bank deposits, CDs, corporates

Diversified funding base

Lehman Brothers ConferenceSlide 25

Expense discipline

Recent market conditions validate Credit Suisse strategy

Benefits of integrated bank with a client focus

Importance of strong capital and liquidity position

Well-positioned to create long-term value and seize opportunities that arise from market dislocation

Innovative and diversified product offering

Geographic diversification

Efficient headcount management

Lehman Brothers ConferenceSlide 26