lender effects on gains from mergers and acquisitions

TRANSCRIPT

Lender Effects on Gains from Mergers and Acquisitions

Abstract

This paper employs a new approach to identify merger and acquisition (M&A) transactions

financed by syndicated loans and provides evidence that acquirer announcement returns are higher

in loan-financed M&A deals than in other deals. Utilizing an instrumental variable approach and

a quasi-natural experiment, we provide evidence that lenders contribute to the higher acquirer

announcement returns in loan-financed M&A deals. Lenders’ performance in M&A financing is

persistent over time. Lenders’ participation in the M&A market can resolve uncertainty about

M&A deal quality, improve corporate governance by preventing value-destroying M&A

transactions, and provide long-term monitoring benefits to acquirer shareholders.

Keywords: M&As, syndicated loan, corporate governance, lending relationship, uncertainty

resolution, lender ability, FAS 166/167

JEL Classifications: G14, G34, G21, D82

1

1. INTRODUCTION

When companies undertake mergers and acquisitions (M&As), the impact of the payment

method on acquiring shareholders’ gains is a key consideration and has been investigated

extensively in the M&A literature. However, prior research has primarily focused on differences

between stock and cash payments without differentiating sources of cash.1 A few studies have

examined the relationships between debt financing and M&A outcomes and found mixed results

(Bharadwaj and Shivadasani, 2003; Schlingemann, 2004; Martynova and Renneboog, 2009;

Vladimirov, 2015).2

Two empirical challenges impede complete understanding of the relationship between debt

financing and acquirer gains. First, the difficulty in accurately identifying the sources of cash used

to finance M&A transactions has hindered research on this important topic. Schlingemann (2004),

for example, relies on acquirers’ available financing sources (excess cash, new equity and debt

issuances) before an M&A to infer the source of financing used for the deal.3 Second, any effect

of debt financing on acquirer gains from M&A investments could be attributed to either borrower-

side or lender-side factors. On the borrower side, finance theories suggest that firms might choose

debt financing when managers have favorable private information (Myers and Majluf, 1984) or to

commit themselves to making more efficient investments (Stulz, 1990; Barclay, Smith, and Watts,

1997), which can cause a positive relation between debt financing and acquirer gains. On the lender

1 See Travlos (1987); Franks, Harris and Mayer (1988); Loughran and Vijh (1997); Chang (1998); Shleifer and Vishny

(2003); Bradley and Sundaram (2006); Betton, Eckbo, and Thorburn (2008); and Officer, Poulsen, and Stegemoller

(2009). 2 Bharadwaj and Shivadasani (2003), examine a sample of 115 tender offers and find the announcement return is

higher for deals financed by bank loans. Schlingemann (2004) and Martynova and Renneboog (2009) examine broader

samples of M&As and find an insignificant relation between debt financing and acquirers’ announcement returns.

Vladimirov (2015), on the other hand, finds that deals not financed with debts generate lower acquirers’ announcement

returns than deals financed at least partially with debts. 3 Schlingemann (2004, p. 684) acknowledges a potential issue with this approach: “[u]nfortunately, there is no way to

establish a precise correspondence between a dollar raised in time t and a dollar spent on a takeover in time t+.”

2

side, private lenders can play an important role in monitoring and generating proprietary

information about borrowing firms (Diamond, 1984, 1991; Fama, 1985; Boyd and Prescott, 1986),

which can also result in higher acquirer gains in M&A deals financed with debts. Thus, delineating

the roles of lender- and borrow-side factors is important for a complete understanding of the effects

of debt financing on acquirer gains from M&As.

The extant empirical M&A literature generally treats debt financing as a choice made by

acquirers and focuses on acquirer-side factors. The impacts of lenders on M&A deal outcomes are

largely ignored. We argue that M&As are among the largest and most complex investments for

firms, potential losses caused by value-destroying M&As can be substantial (Loughran & Vijh,

1997; Moeller et al., 2004, 2005). Therefore, the outcome of an M&A often has a significant, long-

term impact on the acquirer’s financial performance and solvency.4 This, in turn, can have a

substantial impact on the lender that provides financing for the deal.5 Accordingly, lenders should

have strong incentives to assess the M&A deal quality before deciding whether to provide

financing and, conditional on providing loans, to monitor the acquirer’s financial condition over

the loan term. The extant literature, however, lacks empirical evidence on (1) whether and (2) the

channels through which lenders impact acquirer gains. This study aims to provide empirical

evidence on these two important open questions.

We primarily focus on the impact of syndicated loan financing on acquirer gains, because

this type of debt is the most significant source of corporate funding. Moreover, the ownership of

private debts including syndicated loans is relatively more concentrated (Amihud, Garbade, and

Kahan, 1999), and private lenders – including banks – play a more important role in information

4 Our untabulated statistics shows that 28% of acquirers in our M&A sample experience a credit rating downgrade

within five years after the M&A deal completion (source: Capital IQ S&P Credit Ratings). 5 The average size of syndicated loans for M&A financing in our sample is $797 million, equivalent to 67% of the

M&A deal value.

3

generation and monitoring (Diamond, 1984, 1991; Fama, 1985; Boyd and Prescott, 1986) than

public bondholders. Therefore, lender effects, if any, are likely to be stronger in M&As financed

by syndicated loans than in M&As financed by public debts.

As discussed above, identifying sources of financing for M&A investments is difficult. This

study uses a new approach that allows us to accurately identify M&A deals that are financed with

syndicated loans. For an M&A sample from the SDC Platinum database, we first identify deals in

which the acquirer initiates syndicated loans with the purpose of financing an acquisition during

the period from 90 days before to 180 days after the M&A announcement or to the deal completion

date, whichever comes first. Then, we read the M&A announcements for those identified deals to

verify whether the acquirer explicitly states that the M&A deal is financed with syndicated

loan(s).6 As an example, on November 26, 2012, ConAgra Foods Inc. (listed on NASDAQ: CAG)

announced its acquisition of Ralcorp Holdings Inc. In the acquisition announcement, CAG stated

explicitly that $1.5 billion (30% of deal value) would be financed by a new senior unsecured term

loan from Bank of America and JPMorgan Chase Bank. This M&A deal is therefore recorded as

a loan-financed M&A in our sample.

Using this new approach, for the period from January 1990 to December 2015 for the US

takeover market, we identify 745 M&A deals that were financed by newly issued syndicated loans

out of 7,681 M&A deals paid for with cash or a mix of stock and cash. Our univariate tests show

that, on average, acquirers’ 3-day cumulative abnormal returns around M&A announcements

(acquirer CAR) is 1.1% higher for M&A deals financed with syndicated loans than for other M&A

deals in our sample, and this difference is both economically and statistically significant. This

6 We obtain M&A announcements using Factiva and SEC filings (form 8-K). We acknowledge that our approach

might still misclassify some loan-financed M&As as non-loan-financed M&As if the loans were initiated outside the

aforementioned [-90, +180] window.

4

result remains intact when we restrict the sample to cash-only M&A deals or a matched sample

formed using a propensity score matching method. To provide preliminary evidence of lender-side

effects on acquirers’ gains, we conduct multivariate regression tests that control for various

acquirer-side factors, M&A deal characteristics and target credit risk, and find similar results.

Next, we use three methods to provide direct evidence on lenders’ role in explaining

acquirer CAR. We first use an instrumental variable (IV) method. Since lenders’ activities tend to

concentrate in their local captive markets (Guiso, Sapienza, and Zingales, 2004; Degryse and

Ongena, 2005) and the degree of bank competition affects firms’ access to bank credit (Cetorelli

and Strahan, 2006), the likelihood that an acquirer receives loans to finance an M&A should

increase with the degree of competition among local banks. Thus, we use Bank Density, the number

of local banks scaled by the number of local public firms (excluding the acquirer), as the

instrument. We find that the relation between loan financing and acquirer CAR remains

statistically significant in the IV analysis.

Second, we use a change in accounting standards that affects banks’ lending behaviors as

a quasi-natural experiment and examine how this shock on the lender side influences the

relationship between loan financing and acquirer CAR. Specifically, the adoption of Financial

Accounting Standards (FAS) 166 and 167 in 2010 caused banks to recognize a large amount of

securitized assets on their balance sheets, which forced them to tighten lending standards and

reduce credit supply (Dou, Ryan, and Xie, 2018). We expect that the lender-side effect of loan

financing strengthens after FAS 166/167. Consistent with this expectation, we find that the positive

association between loan financing and acquirer CAR becomes stronger after this regulatory

shock.

5

The third piece of evidence on lenders’ role in explaining acquirer CAR is the persistence

in lead lender’s performance in M&A lending. Private lenders differ in their ability or skills in

screening and monitoring borrowing firms (Fama, 1985; Chemmanur and Fulghieri, 1994). If

lenders’ skills contribute to the higher acquirer CAR in loan-financed M&As, we should observe

that lender performance in M&A lending is persistent over time. We measure a lead lender’s past

(future) performance as the average acquirer CAR of M&A deals financed by the same lead lender

over one, two and three years in the past (future). We find that lead lenders with high M&A lending

performance in the past tend to also have high M&A lending performance in the future.

The results from our previous tests suggest that lenders contribute to higher acquirer CAR

in loan-financed M&As. Our subsequent tests explore possible channels through which lenders

affect M&A announcement returns and create value for acquirer shareholders. First, a private

lender’s decision to finance an M&A could be viewed by investors as a positive signal of the

acquirer’s stand-alone value (Barraclough et al., 2013; Wang, 2016), thus leading to a higher

acquirer CAR (the acquirer revaluation effect). Our test results, however, suggest that the relation

between loan financing and acquirer CAR is not driven by the acquirer revaluation effect.

Specifically, we find that the association between loan financing and acquirer CAR is not stronger

when there is a higher degree of uncertainty about the acquirer’s stand-alone value (as proxied by

acquirer stock return volatility and the dispersion of financial analysts’ earnings forecasts), or

when the lead lender has a prior lending relationship with the acquirer. We also find no evidence

that association between loan financing and acquirer CAR is weaker when the acquirer has already

had outstanding loans at the time of M&A announcement, which diminishes the acquirer

revaluation effect of new loans.

6

Second, a private lender’s decision to finance an M&A deal might reduce the uncertainty

about the M&A deal quality faced by external investors, causing higher acquirer CAR (the deal

quality certification channel). The deal quality certification channel implies that the association

between loan financing and acquirer CAR should be stronger when uncertainty about the M&A

deal quality is higher and weaker when other signals about the M&A deal quality already exist.

M&A deal quality, from acquirer shareholders’ perspective, depends on both expected synergy

and target stand-alone value. We argue that both expected synergy and target stand-alone value

are more difficult to assess in deals with private targets than in deals with public targets since the

former tend to have lower financial reporting quality (Hope, Thomas, and Vyas, 2013).

Additionally, the presence of multiple bidders sends an alternative positive signal of the target’s

stand-alone value. Therefore, we expect the relationship between loan financing and acquirer CAR

to be weaker for deals with public targets and for deals with multiple bidders. On the other hand,

lead lenders that have a prior lending relationship with the M&A target likely have informational

advantages that allow more accurate assessment of the M&A deal quality. We therefore expect the

deal quality certification effect of loan financing to be stronger when the lead lender has a prior

lending relationship with the target. We find that the association between loan financing and

acquirer CAR is significantly weaker when there are multiple bidders, and significantly stronger

when the lead lender has a prior lending relationship with the target firm. Our results generally

support the deal quality certification channel.

Third, a lender’s decision not to finance a low-quality M&A deal might help prevent a

value-destroying M&A (the ex-ante monitoring channel). The ex-ante monitoring channel is

difficult to verify directly, because we do not observe declined loan applications by acquirers.

However, we find some indirect evidence of this channel by examining boundary conditions that

7

attenuate or strengthen lenders’ role in preventing value-destroying M&A deals. Specifically,

lenders’ ability to deter value-destroying acquisitions should be less important when the acquirer

already has strong corporate governance. We focus on two sources of corporate governance: the

market for corporate control (Masuli, Wang, and Xie, 2007) and dedicated institutional investors

(Chen, Harford, and Li, 2007). We find that the relationship between acquirer CAR and loan

financing is significantly stronger when the acquirer has weaker corporate governance (having

more anti-takeover provisions or lower dedicated institutional ownership).

Fourth, once a bank has financed an M&A, it will monitor the acquirer over the term of the

loan ex post. This can create a positive spillover to the acquirer’s shareholders (the ex-post

monitoring channel). We argue that the benefit of lenders’ ex-post monitoring should be larger if

lenders monitor the acquirer for a longer period. Indeed, we find that the relationship between loan

financing and acquirer CAR is most prominent when the loans used to finance the M&A have the

longest terms to maturity.7 Additionally, we find a positive and marginally statistically significant

relationship between loan financing and acquirer 3-year buy-and-hold abnormal returns.8 These

findings together provide some support for the ex-post monitoring channel.

This paper makes several contributions to the literature. First, we provide evidence on the

direct link between acquirer gains and syndicated loan financing in a general M&A setting.

Schlingemann (2004), Martynova and Renneboog (2009), and Vladimirov (2015) examine the role

of debt financing in general without differentiating types of debts. Bharadwaj and Shivadasani

(2003) examine the effects of bank financing for tender offers, which account for only a small

fraction of M&As.9 Our approach allows us to accurately identify loan-financed M&As and study

7We acknowledge that there are alternative explanations for this finding. For example, it is possible that lenders are

willing to accept a longer loan term when the perceived M&A deal quality is higher. 8 This finding can be interpreted as the market underreacting to the benefit of private lenders’ ex-post monitoring. 9 In our sample, for example, tender offers only account for 8% of all M&A deals.

8

the roles of lenders in determining acquirer gains in a more general M&A setting. More

importantly, prior studies either only consider acquirer-side factors (Schlingemann, 2004;

Martynova and Renneboog, 2009; Vladimirov 2015) or provide results that can be attributed to

either acquirer or lender-side factors (Bharadwaj and Shivadasani, 2003). In contrast, our study

provides direct evidence of lender-side effects on acquirer gains and the channels through which

lenders impact acquirer shareholders’ value.

Our findings also complement the literature on the impacts of stock versus cash payment

methods on acquirer gains (e.g. Travlos, 1987; Amihud, Lev, and Travlos, 1990; Martin, 1996;

Loughran and Vijh, 1997; Akbulut, 2013). This strand of literature generally finds that acquirer

gains are higher in cash deals and attributes this result to the signaling effect of payment methods

(i.e. acquirers use their overvalued stocks to pay target shareholders). Our study suggests that

lenders contribute to the higher acquirer gains in cash deals. Finally, to the best of our knowledge,

our study is the first that shows the interplay between lenders and other corporate governance

mechanisms in determining M&A gains.

The remainder of this paper proceeds as follows. In section 2, we describe the sample and

main variables. Section 3 presents our methodology and the baseline empirical results. Section 4

presents evidence of lender-side effects on acquirer gains. In section 5 we explore some channels

through which lenders can benefit acquirer shareholders. Section 6 concludes the paper.

2. DATA AND RESEARCH DESIGN

2.1. M&A sample construction

Our initial sample includes all M&A deals from the SDC Platinum Database over 1990–

2015 that satisfy the following criteria: (1) both the acquirer and the target are U.S. firms; (2) the

acquirer is a public firm; (3) the deal is classified as a merger, acquisition or acquisition of major

9

interest; (4) M&A deal value is non-missing; and (5) the acquirer owns less than 50% of the

target’s shares before the deal announcement and seeks to own 100% of the target’s shares after

the deal. We merge this initial sample with CRSP and Compustat to obtain stock returns and

financial data, respectively. To focus on economically meaningful transactions, we drop deals

smaller than 1% of the acquirer’s market value of equity measured at the end of the most recent

fiscal year before the acquisition announcement. Finally, we exclude pure stock-for-stock

acquisitions, since loan financing is not an option in those transactions.10 Our final sample includes

7,681 M&As. Panels A and B of Table 1 present our sample distribution over time and by Fama–

French’s 30 industry categories, respectively. Overall our sample is well represented across time

and industry.

<Insert Table 1 here>

2.2. Identification of M&A transactions financed with syndicated loans and bonds

We use a two-step process to identify M&A transactions that are financed with syndicated

loans. First, starting with the sample of M&As described earlier, we use information from the

DealScan syndicated loan database to identify acquirers that initiate loans with “Takeover” or

“Acquisition Line” being the primary or secondary purpose during the period from 90 days before

to 180 days after the M&A announcement (or to the M&A completion date if it comes first).11 We

only consider term loans and revolving facilities. In our sample, there are 985 M&A deals in which

the acquirer initiates syndicated loan(s) for M&A purposes during the aforementioned window.

Second, for these 985 potentially loan-financed M&A deals identified in the first step, we search

for M&A announcements using Factiva and SEC filings (form 8-K) and read the announcements

10 The main results of this study remain intact if we also include pure stock-for-stock acquisitions. 11 We merge our SDC/CRSP/Compustat sample with DealScan using the Compustat/Dealscan link table provided by

Chava and Roberts (2008).

10

to verify sources of financing. An M&A deal is categorized as being financed with syndicated

loans only if the acquirer explicitly states so in the M&A announcement. Our two-step approach

identifies 745 loan-financed M&A deals out of 7,681 deals in our sample. We construct a dummy

variable (Loan Finance) equal to one for the 745 syndicated-loan-financed M&A deals and zero

otherwise, and a continuous variable (Loan Finance Ratio) equal to the amount of loan(s)

borrowed to finance the M&A scaled by the M&A deal value. These are two key independent

variables in our analyses.

We identify M&A transactions financed with bond issuances using a similar approach. First,

we use the Mergent FISD bond issuance database to identify acquirers that issue bonds during the

period from 90 days before to 180 days after the M&A announcement (or to the M&A competition

date if it comes first). For M&A deals identified as potential bond-financed deals in the first step,

we then read acquisition announcements, obtained from Factiva and SEC filings (form 8-K), to

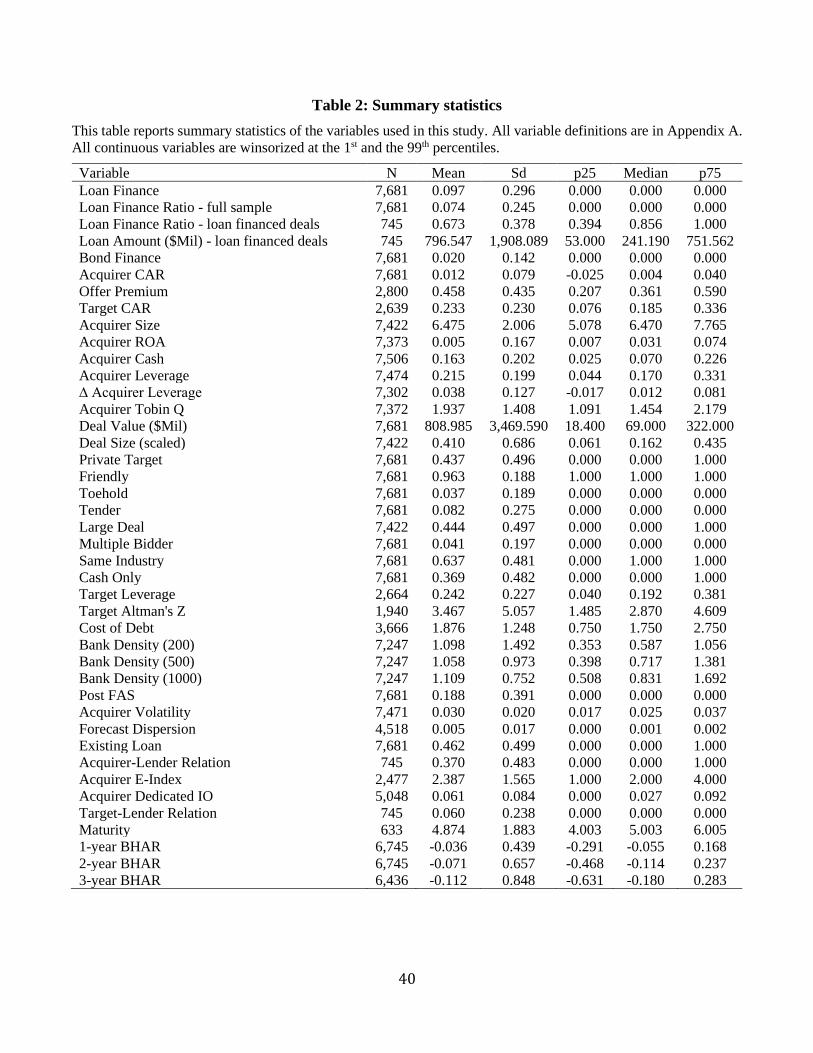

verify if they are indeed financed with proceeds from new bond issuances. Table 2 presents

summary statistics for the variables used in this study. On average, 9.7% of the M&A transactions

in our sample are financed with newly borrowed syndicated loans, while 2% of the M&A

transactions are financed with newly issued bonds. Figure 1 plots the average ratio of loan amount

to M&A deal value by year.

<Insert Table 2 here>

<Insert Figure 1 here>

2.3. Measure of acquirer gains

Following previous studies (e.g., Moeller et al. 2005), we use acquirers’ CAR over a 3-day

window centered on the acquisition announcement date (Acquirer CAR) as the measure of gains

to acquirer shareholders. Abnormal stock returns are estimated using a Carhart’s 4-factor model

11

(Carhart, 1997).12 The model is estimated for individual firms over the period from the 273rd

trading day to the 21st trading day prior to the M&A announcement. Firms with fewer than 60

trading days available over the estimation window are excluded. As shown in Table 2, the mean

and median of Acquirer CAR are 1.2% and 0.4%, respectively.

2.4. Control variables

Myers and Majluf’s (1984) pecking order theory suggests that, in the presence of information

asymmetry, firms should rely on their cash on hand first and prefer debt to equity if external

financing is needed. Additionally, firms with inadequate financial slack and limited access to debt

financing might refuse to issue equity and forgo some investment opportunities. To control for

these borrower-side factors, we construct Acquirer Cash (acquirer’s cash scaled by total assets)

and Acquirer Leverage (acquirer’s total long-term and short-term debts scaled by total assets) as

proxies for acquirers’ financial slack, and Acquirer Tobin Q (the sum of market value of equity

and book value of liabilities scaled by total assets) as a proxy for acquirers’ growth opportunities.

We also construct other common control variables used in the M&A literature, including

acquirers’ market capitalization (Acquirer Size) and profitability (Acquirer ROA), M&A deal value

scaled by the acquirer’s market value of equity (Deal Size), whether the target is a private firm

(Private Target), whether the takeover is friendly (Friendly), whether the takeover is a tender offer

(Tender), whether there are multiple bidders involved (Multiple Bidder), whether the acquirer and

the target are in the same industry based on two-digit SIC codes (Same Industry), whether the

acquirer already owns some shares of the target before the deal announcement (Toehold), and

whether the deal payment is fully in cash (Cash Only). Additionally, Fu, Guay, and Zhang (2016)

show that bidders have incentives to construct M&A deals to maintain new equity issues at slightly

12 Our results remain robust if we use alternatives models including CAPM and Fama-French 3 factor model (Fama

and French, 1993) or a (-2, +2) event window using the 4-factor model

12

less than 20% to avoid triggering shareholder approval. We construct a dummy variable indicating

whether the deal value is at least 20% of the acquirer’s market value (Large Deal), since deal size

beyond this threshold might have an impact on bidders’ financing choice. All acquirer

characteristics are measured using data for the most recent fiscal year before the M&A

announcement. The complete definitions of all variables are in Appendix A.

3. LOAN FINANCING AND ACQUIRER CAR

3.1. Univariate analysis

Our main objective in this section is to compare the mean and median of the Acquirer CAR

for the treatment group (M&A deals financed with syndicated loans) and the control group (other

M&A deals). Since prior literature finds that acquirer announcement return tends to be higher for

cash deals than for stock and mixed deals (Travlos, 1987; Loughran and Vijh, 1997), we also

conduct univariate tests on a restricted sample that includes cash-only M&A deals. Additionally,

we use a propensity score matching approach to select, for each loan-financed M&A deal, a

matched M&A deal that has similar acquirer and M&A deal characteristics but is not financed

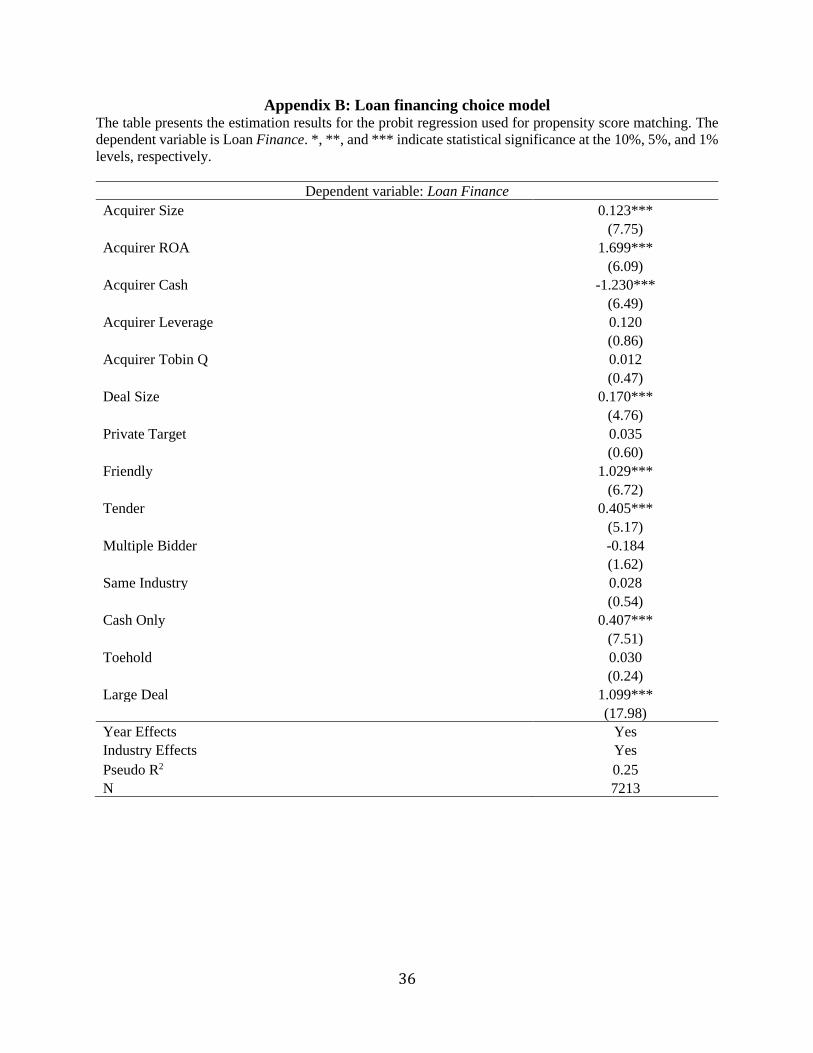

with loans. Propensity scores are estimated using a probit regression (the estimation result is

reported in Appendix B). We then test if there is a difference in Acquirer CAR between M&A

deals financed with loans and other deals within this matched sample.

The univariate test results for the full sample, cash-only sample and matched sample are

presented in Table 3. We find that the mean and median Acquirer CAR are significantly higher for

loan-financed M&A deals than for other deals. Specifically, for the full sample, the mean Acquirer

CAR for loan-financed M&A deals is 2.2%, while it is only 1.1% for other deals. The difference

in Acquirer CAR between the two groups is statistically significant at the 1% level and

economically significant (for comparison, the mean Acquirer CAR for our full sample is 1.2%).

13

The results are qualitatively similar for the of cash-only M&A sample and the propensity score

matched sample.

<Insert Table 3 here>

3.2. Multivariate analysis

To formally test the relationship between loan financing and acquirer gains, we estimate the

following baseline multivariate regression model:

𝐴𝑐𝑞𝑢𝑖𝑟𝑒𝑟 𝐶𝐴𝑅 = 𝛽0 + 𝛽1𝐿𝑜𝑎𝑛 𝐹𝑖𝑛𝑎𝑛𝑐𝑒 (𝐿𝑜𝑎𝑛 𝐹𝑖𝑛𝑎𝑛𝑐𝑒 𝑅𝑎𝑡𝑖𝑜) + 𝛽2𝐴𝑐𝑞𝑢𝑖𝑟𝑒𝑟 𝑆𝑖𝑧𝑒

+ 𝛽3𝐴𝑐𝑞𝑢𝑖𝑟𝑒𝑟 𝑅𝑂𝐴 + 𝛽4𝐴𝑐𝑞𝑢𝑖𝑟𝑒𝑟 𝐶𝑎𝑠ℎ + 𝛽5𝐴𝑐𝑞𝑢𝑖𝑟𝑒𝑟 𝐿𝑒𝑣𝑒𝑟𝑎𝑔𝑒

+ 𝛽6𝐴𝑐𝑞𝑢𝑖𝑟𝑒𝑟 𝑇𝑜𝑏𝑖𝑛′𝑠 𝑄 + 𝛽7𝐷𝑒𝑎𝑙 𝑆𝑖𝑧𝑒 + 𝛽8𝑃𝑟𝑖𝑣𝑎𝑡𝑒 𝑇𝑎𝑟𝑔𝑒𝑡 + 𝛽9𝐹𝑟𝑖𝑒𝑛𝑑𝑙𝑦

+ 𝛽10𝑇𝑒𝑛𝑑𝑒𝑟 + 𝛽11𝑀𝑢𝑙𝑡𝑖𝑝𝑙𝑒 𝐵𝑖𝑑𝑑𝑒𝑟 + 𝛽12𝑆𝑎𝑚𝑒 𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦 + 𝛽13𝑇𝑜𝑒ℎ𝑜𝑙𝑑

+ 𝛽14𝐿𝑎𝑟𝑔𝑒 𝐷𝑒𝑎𝑙 + 𝛽15𝐶𝑎𝑠ℎ 𝑂𝑛𝑙𝑦 + 𝜀 (1)

The dependent variable is Acquirer CAR. The main explanatory variable of interest is alternatively

Loan Finance dummy and Loan Finance Ratio. The baseline regression model controls for

borrower-side factors, deal characteristics and industry and year fixed effects.13 Standard errors

are clustered by industry.

The results of our multivariate analyses are reported in Table 4. In Panel A our key

explanatory variable is the Loan Finance dummy. Column (1) presents the regression results for a

reduced form of the baseline regression that includes only Loan Finance and year and industry

dummies. Column (2) presents the results for the baseline regression estimated on the full sample.

Column (3) presents the baseline regression results estimated on cash-only M&A deals. Overall,

the coefficient on Loan Finance is positive and statistically significant at the 5% level or lower in

all regressions. The magnitude of the coefficient is economically significant. For example, in the

13 Industries are defined based on Fama–French’s 30 industry categories.

14

baseline regression for the full sample, the coefficient on Loan Finance is 0.013, suggesting that

Acquirer CAR is 1.3% higher for M&As financed with syndicated loans than for deals not financed

with syndicated loans. Moreover, given that the coefficient on Loan Finance remains statistically

significant even in the subsample of cash-only M&A deals, our results are unlikely to be driven

by the impact of payment method.

Table 4, Panel B presents regression results when the key explanatory variable is Loan

Finance Ratio.14 The coefficient on Loan Finance Ratio is positive and statistically significant at

the 5% level or lower. Overall, the estimation results in Panels A and B of Table 4 confirm that

acquirer CAR is significantly higher in M&A deals financed with syndicated loans than in M&A

deals not financed with syndicated loans.

<Insert Table 4 here>

3.3. Alternative explanations for the association between loan financing and acquirer CAR

In this section we conduct additional tests to rule out alternative explanations for a positive

relation between acquirer’s use of loan financing and announcement returns (other than lender

effects). First, the pecking order theory of Myers and Majluf (1984) suggests that debt financing

is viewed by external investors as a signal that managers have favorable private information about

the firm’s investments. If this explains the higher acquirer CAR in loan-financed M&A deals, we

would expect to observe similar result for M&A loans financed with public debts (bond issuances).

Lender-side factors, however, suggest that the same effect is unlikely to hold for public debt

financing. This is because private lenders generally play a more important role in monitoring and

information generation (Diamond, 1984, 1991; Fama, 1985; Boyd and Prescott, 1986) than public

debt holders. To examine whether the results also hold for M&A deals financed with public debts,

14 Loan Finance Ratio equals zero for deals that are not financed with loans.

15

we add to regression model (1) a dummy variable indicating whether the acquirer issues bonds to

finance the M&A deal (Bond Finance) and report the estimation results in column (1) of Table 5,

Panel A. The coefficient on Bond Finance is not statistically different from zero, whereas that on

Loan Finance remains statistically significant. This finding suggests that the higher Acquirer CAR

in loan-financed M&As is not driven by the market inferring positive managerial private

information when loans are used as a financing source.

Second, Yook (2003) argues that an increase in financial leverage might be associated with

greater acquirer CAR because acquirers with higher leverage should be more diligent in choosing

their target firms and structuring M&A deals, leading to more profitable deals. To control for this

disciplinary effect of debts, we add the change in leverage from the year before the M&A

announcement to the year after the M&A completion (∆ Acquirer Leverage) to model (1) and

present the estimation results in column (2) of Table 5, Panel A. We find that the positive

association between Loan Finance and Acquirer CAR remains statistically significant with a

similar economic magnitude, suggesting that our previous results are not driven by the disciplinary

effect of leverage. In column (3) of the same table, we add both Bond Finance and ∆ Acquirer

Leverage to the baseline regression, and the statistical and economic significances of the

coefficient on Loan Finance remain intact.

<Insert Table 5 here>

Third, Ivashina et al. (2009) show that lenders might have an incentive to get rid of

borrowers with bad credit quality through M&A transactions. To investigate whether our results

are driven by M&A deals in which the target has poor credit quality, we add to our regression

model two additional variables: Target Leverage and Target Altman’s Z score. The estimation

results are reported in Table 5, Panel B. Since these two measures are only available for public

16

targets, our sample size reduces by more than two thirds. The coefficient on the Loan Finance

dummy, however, remains statistically significant, suggesting that our results are unlikely to be

driven by lenders’ incentive to turn risky borrowers into M&A targets.

Last, the model in Vladimirov (2015) suggests that, in bidding contests, acquiring firms

with lower cost of debt can offer higher premiums to the target and enjoy greater gains from M&A

investments. To test if our results are driven by differences in cost of debt financing, we construct

Cost of Debt as the average of interest rate spread (all-in-spread-drawn) of all syndicated loans

borrowed by the acquirer over the past five years before the M&A announcement and include it as

a control variable in model (1). The results are reported in Table 5, Panel C. Even though the

sample size reduces by more than one half due to the unavailability of cost of debt data, the

coefficient on Loan Finance dummy remains statistically significant. Cost of Debt, on the other

hand, is not significantly related to Acquirer CAR. In column (2) of Table 5, Panel C, we further

add the interaction term Loan Finance × Cost of Debt. If the effect of loan financing is driven by

firms with low cost of debt, the coefficient on the interaction term should be negative. We find

that the coefficient on the interaction term is significantly positive, suggesting that cost of debt

does not explain our main findings.

Vladimirov’s model (2015) also implies that target announcement returns should be higher

for debt-financed M&A deals, since acquirers with a cost advantage in debt financing should pay

a higher offer premium to the target in order to win the bidding contest. Although it is not our

focus, we also examine the relationship between loan financing and Offer Premium and Target

CAR. The results are reported in Table 5, Panel D. We find that Loan Finance has statistically

insignificant relationships with Target CAR and Offer Premium. These results are again

inconsistent with Vladimirov’s (2015) prediction.

17

4. DIRECT EVIDENCE OF LENDER-SIDE FACTORS

4.1 Instrumental variable (IV) analysis

In this section, we use an IV approach to provide direct evidence of lender-side effects on

acquirer CAR. Given our purpose, the instrument needs to be a lender-side variable that (1) affects

the likelihood that an M&A deal is financed with syndicated loans (the relevance condition) and

(2) does not directly affect M&A announcement returns (the exclusion restriction).

Prior banking literature suggests that private lenders such as banks tend to concentrate their

lending activities in their local captive markets (Guiso et al., 2004; Degryse and Ongena, 2005).

This is because lenders’ ability to obtain borrower-specific information decreases with lender-

borrower distance (e.g. Almazan, 2002; Agarwal and Hauswald, 2010; Knyazeva and Knyazeva,

2012; Hollander and Verriest, 2016). Additionally, Cetorelli and Strahan (2006) suggest that the

degree of bank competition affects firms’ access to bank credit. Accordingly, the likelihood that

an acquirer receives syndicated loans to finance an M&A deal should increase with the degree of

competition among local banks. Therefore, we use Bank Density, defined as the number of local

banks divided by the number of local public firms (excluding the acquirer), as our instrument. We

obtain bank location from Reports of Condition and Income (Call Reports), which contain all US

commercial banks registered with the Federal Deposit Insurance Corporation.15 We obtain public

firms’ headquarters location from the Compustat database.16 For each acquirer in the sample, we

compute the ratio of the numbers of banks to the number of public firms (excluding the acquirer)

located within 200, 500 and 1000 kilometers from the acquirer’s headquarters in the fiscal year

prior to the M&A announcement17.

15 We do not use lender location in the Dealscan database because most ZIP codes in Dealscan are missing. 16 Note that the location of a firm’s headquarters is not necessarily where the firm is incorporated. 17 The spherical distance between two places, X and Y, is calculated as follows: Distance =

6,371×Arcos[Sin(LatitudeX)*Sin(LatitudeY) + Cos(LatitudeX)*Cos(LatitudeY)*Cos(LongitudeX-LongitudeY)].

18

Since our endogenous regressor, Loan Finance, is a binary variable, we follow the

approach suggested by Wooldridge (2002) in conducting our instrumental analysis. This approach

has been implemented in prior empirical studies, such as Faulkender and Peterson (2006) and

Bharath et al. (2011). Specifically, in the first stage we estimate a probit regression with Loan

Finance as the dependent variable. The independent variables are Bank Density and all other

control variables from model (1). We then use the predicted probability from the first-stage

regression as an instrumental variable in the second stage of analysis. The results for this test are

presented in Table 6, Panels A and B. Panel A presents the estimation results for the first-stage

regression. The coefficient on Bank Density has the predicted signs and is statistically significant.

The first-stage F-statistic shows that the instrument is a significant explanatory variable of Loan

Finance, suggesting that the relevance condition is satisfied. Results for the second-stage

regression are presented in Panel B, confirming a positive relationship between Loan Finance and

Acquirer CAR. Overall, the results in Table 6 provide direct evidence that the relationship between

loan financing and acquirer CAR is at least partially attributable to lender-side factors.

<Insert Table 6 here>

4.2. FAS 166/167 and the relationship between loan financing and acquirer CAR

FAS 166/167, which became effective at the beginning of 2010, requires banks to

consolidate a large number of variable interest entities that had previously been kept off banks’

balance sheet. This regulatory change led to a significant increase in banks’ assets and hence

effectively increased their regulatory capital requirement.18 Prior studies find that on average

banks tighten lending standard and increase loan quality after FAS 166/167 (Tian and Zhang, 2016;

Dou, 2017; Dou, Ryan, and Xie, 2018). Therefore, we use FAS 166/167 as a quasi-natural

18 Banks can respond to an increase in regulatory capital by either reducing assets or raising more capital. It is likely

that they employ both solutions.

19

experiment to examine the impact of lender monitoring and screening effects on acquirer gains. If

lenders’ monitoring and screening explain the association between loan financing and Acquirer

CAR, then this association should become stronger after FAS 166/167.

To provide evidence on this prediction, we add Post FAS and its interaction with Loan

Finance into the baseline regression (1). Post FAS is a dummy variable that equals one for

acquisitions announced in 2010 or later and zero otherwise. We expect the coefficient on the

interaction term Loan Finance × Post FAS to be positive, consistent with the relationship between

loan financing and acquirer gains becoming stronger after FAS 166/167. The estimation results

are presented in Table 7, Panel A. The first column presents the estimation results using the full

sample period. As predicted, the coefficient on the interaction term Loan Finance × Post FAS is

positive and statistically significant at the 5-percent level, suggesting that the association between

Loan Finance and Acquirer CAR is more positive when lenders have incentives to tighten lending

standards.

<Insert Table 7 here>

Since the implementation of FAS 166/167 in 2010 was adjacent to the 2007–08 GFC, to

mitigate the concern that the regression results for the full sample are confounded by the unusual

market conditions around the GFC, we exclude M&As announced in 2007 and 2008 and re-

estimate the regression. The coefficient on the interaction term remains significantly positive (see

the second column in Table 7, Panel A). In the last column in Table 7 (Panel A), we present the

estimation results using only M&As announced in 2009–10 (the two years immediately before and

after FAS 166/167); the sample size drops to only 342 observations after this restriction. However,

the coefficient on the interaction term Loan Finance × Post FAS remains positive and statistically

20

significant at the 5-percent level. Since our results still hold in this much smaller subsample of

only two years surrounding FAS 166/167, they are unlikely to be driven by trend effects.

To further rule out the possibility that our previous results were driven by trend effects, we

conduct two placebo tests. Specifically, we define two placebo regulatory changes, one before and

one after FAS 166/167 became effective, and repeat our analysis using these placebo changes. In

the first test, the placebo regulatory change is defined as the beginning of 2012 and we restrict the

sample to the 2011–12 period. We present the results in the first column of Table 7, Panel B. The

coefficient on the interaction of the term Loan Finance ×Post FAS dummy becomes statistically

insignificant. In the second test, the placebo regulatory change is defined as the beginning of 2006

and we restrict the sample to the 2005–06 period.19 The coefficient on the interaction term remains

statistically insignificant (see the second column in Table 7, Panel B). These placebo tests provide

more confidence that our results in Table 7, Panel A are driven by the shock in lenders’ monitoring

and screening incentives caused by FAS 166/167.

4.3. Persistence in lead lender’s M&A lending performance

Fama (1985) and Chemmanur and Fulghieri (1994) suggest that lenders differ in their skills

in screening and monitoring borrowers. Assuming that lenders indeed vary in their skills and lender

skills are persistent, we expect that lenders that perform well in the past, on average, will continue

to perform well in the future. We follow an approach similar to Bao and Edmans (2011) and

Golubov and Zhang (2015) to test this prediction. Specifically, we first identify 122 lead lenders20

that have provided financing to at least two M&A deals in our sample. We calculate the mean

acquirer CAR for M&A deals financed by each lead lender at the beginning of each year over one,

19 We choose the beginning of 2006 as the second placebo regulatory change to make sure the sample period for our

second placebo test does not overlap with the 2007–08 GFC. 20 We use lender company ID provided by the DealScan database to define lenders.

21

two and three years in the past (past performance) and over one, two and three years in the future

(future performance). As discussed before, we expect a positive relation between lenders’ past

performance and future performance.

We sort the lender-year observations in our sample into quartiles based on historical

performance and compare the average future performance for each quartile. Table 8, Panels A, B

and C present the results when past performance is calculated over one year, two years, and three

years, respectively. In general, we find that lead lenders’ performance is indeed persistent. In Panel

A, for example, when lender-year observations are sorted on one-year past performance, the

average Acquirer CAR over two years in the future in the top quartile is 4.4%, while that of the

bottom quartile is only 1.5%. The difference in Acquirer CAR between the two groups (2.9%) is

statistically significant at the 5-percent level. The results in Panels B and C again suggest that

lender performance is persistent. This finding provides additional evidence that the higher acquirer

CAR of loan-financed M&A deals can be attributed to lender-side factors.

<Insert Table 8 here>

5. CHANNELS THROUGH WHICH LENDERS AFFECT ACQUIRER

ANNOUNCEMENT RETURNS

Our previous analyses establish that syndicated loan lenders contribute to the higher

acquirer CAR in loan-financed M&A deals. In this section we explore possible channels through

which lenders affect acquirer CAR.

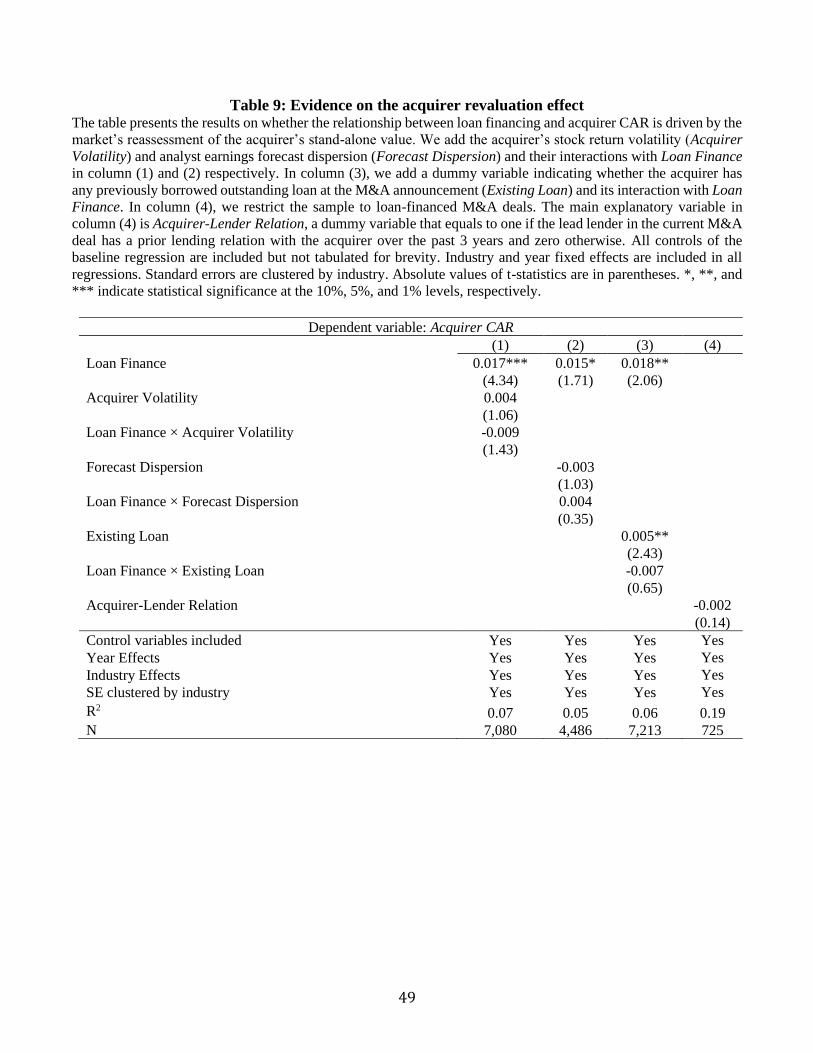

5.1. The acquirer revaluation effect

M&A announcement may induce external investors to reassess the acquirer and the target’s

stand-alone values (e.g. Barraclough et al., 2013; Wang, 2016). Therefore, the higher acquirer

CAR in loan-financed M&A deals may also reflect the market’s updated assessment of the

22

acquirer’s stand-alone value (the acquirer revaluation effect). In the context of this study, a private

lender’s decision to provide a loan to finance an M&A could be viewed as a favorable signal of

the stand-alone value of the borrower (Diamond, 1984; Ramakrishnan and Thakor, 1984; Fama,

1985) rather than the quality of the M&A deal, therefore leading to higher acquirer announcement

returns. Thus, we conduct several tests to examine whether our results are driven by the acquirer

revaluation effect.

First, the acquirer revaluation effect implies that the association between Loan Finance and

Acquirer CAR results should be stronger when the information asymmetry or uncertainty about

the acquirer’s stand-alone value is higher. We utilize two measures of the acquirer’s information

asymmetry: the acquirer’s stock return volatility measured prior to M&A announcement and

financial analysts’ earnings forecast dispersion. Higher acquirer stock volatility or analyst forecast

dispersion indicates higher information asymmetry between the acquirer and external investors.

We add these two alternative measures of acquirer information asymmetry and their interactions

with Loan Finance into the baseline regression. The estimation results, reported in columns (1)

and (2) of Table 9, show that the coefficients on the two interaction terms are statistically

indistinguishable from zero. These results are inconsistent with the acquirer revaluation effect.

<Insert Table 9 here>

Second, we argue that the acquirer revaluation effect of loan financing in M&A deals should

be weaker if other indicators of acquirers’ stand-alone value already exist. The presence of the

acquirer’s previously borrowed outstanding loans (other than the loan used to finance the focal

M&A deal) is one such alternative indicator. To test this conjecture, we construct Existing Loan,

a dummy variable equal to one if an acquirer has at least one previously borrowed outstanding

loan at the time of the M&A announcement. In column (3) of Table 9, we add Existing Loan and

23

its interaction with Loan Finance into the baseline regression. If the acquirer revaluation effect

drives the relation between loan financing and acquirer CAR, we expect the coefficient on the

interaction term to be significantly negative. However, we find that the coefficient is statistically

indistinguishable from zero, again inconsistent with the acquirer revaluation effect.

Third, prior studies such as Boot (2000) and Bharath et al. (2011) suggest that banks can

gain reusable proprietary information about a borrower through a repeated lending relationship.

Lenders that have a prior lending relationship with the acquirer likely have access to more

proprietary information about the acquirer’s stand-alone value. The revaluation effect, if any,

should be stronger in such cases. To test this prediction, we construct Acquirer-Lender Relation

as a dummy variable equal to one if the lead lender(s) had lent any loan to the acquirer over the

three years before the M&A. In column (4) of Table 9, we restrict the sample to loan-financed

M&A deals only and test the relation between Acquirer-Lender Relation and acquirer CAR. The

coefficient on Acquirer-Lender Relation is negative and statistically insignificant. In sum, all the

results presented in Table 9 are inconsistent with the hypothesis that the higher acquirer CAR in

loan-financed M&As is driven by the acquirer revaluation effect.

5.2 The deal quality certification effect

Uncertainty about the M&A deal quality may cause external investors to apply a higher

discount rate when valuing an M&A transaction, leading to a value loss for acquirer shareholders.

Since syndicated loan lenders likely have access to private information about the acquirer and the

M&A deal, lenders’ decision to finance an M&A deal may help reduce the uncertainty about the

M&A deal quality faced by external investors and, therefore, at least partially unlocks the lost

value (the deal quality certification effect). This deal quality certification effect suggests that the

association between loan financing and acquirer gains should be stronger if information

24

asymmetry or uncertainty about the M&A deal quality is higher and weaker if other indicators of

the M&A deal quality already exist.21

To examine the deal quality certification effect, we construct several measures of

information asymmetry with regard to the M&A deal quality. From the acquirer shareholders’

perspective, M&A deal quality depends on multiple factors including potential synergy and the

target stand-alone value. We argue that both potential synergy and target stand-alone value are

more difficult to assess for deals with private targets than deals with public targets due to less

stringent disclosure requirements for private firms (Officer, Poulsen, and Stegemoller, 2009). The

presence of multiple bidders, on the other hand, could serve as a positive indicator of the target’s

stand-alone value. Also, bidding contests that involve multiple bidders can reveal more

information about the potential synergy to external investors, thereby reducing the uncertainty

about the perceived M&A deal quality. Accordingly, we expect the effect of loan financing on

acquirer CAR to be stronger for deals with private targets and weaker for deals with multiple

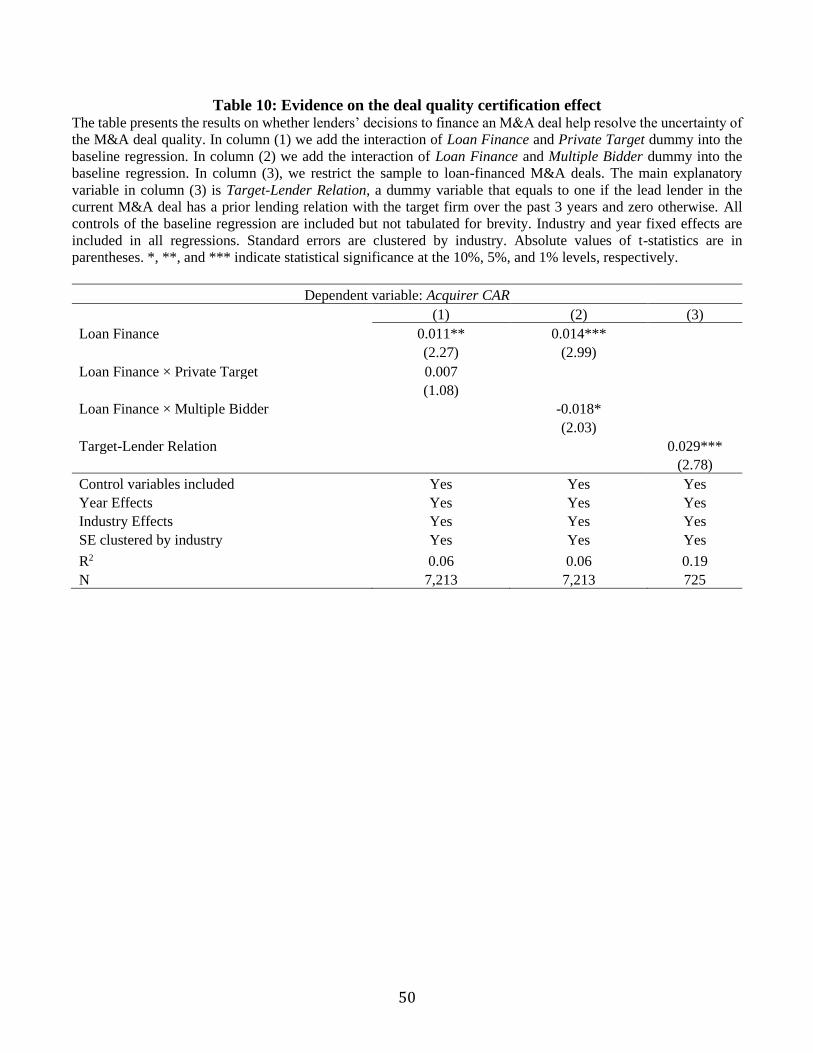

bidders. In column (1) and (2) of Table 10, we add the interaction terms of Loan Finance with

Private Target and Multiple Bidder, respectively. The coefficient on the interaction term of Loan

Finance and Private Target is positive but insignificant, while the coefficient on the interaction

term between Loan Finance and Multiple Bidder is significantly negative.22 Thus, we find some

evidence consistent with the deal quality certification effect.

<Insert Table 10 here>

21 It is possible that both lenders and external investors rely on the same source of information to assess the M&A

deal quality. In this case, lenders do not create value for acquiring shareholders even though loan-financed M&As are

associated with higher acquirer CAR. Under this scenario, the relationship between loan financing and acquirer CAR

should not be affected by information asymmetry or uncertainty about the M&A deal quality. 22 The coefficient on the interaction term of Loan Finance and Private Target is significantly positive when we restrict

the sample to cash-only M&A deals.

25

Finally, if the lead lender that provides loan financing to the acquirer also has a prior lending

relationship with the target, it can gain access to proprietary information on the target side. Under

such a scenario, the lead lender should have a better ability to assess the target’s stand-alone value

and the potential synergy gains from the M&A deal. In this case, lenders’ decision to loan money

to finance an M&A deal helps reduce uncertainty about the deal quality, thus leading to a higher

acquirer CAR. To test this conjecture, we construct Target-Lender Relation based on whether the

lead lender that finances the M&A deal has lent any loan to the M&A target over the three years

before the M&A announcement. In column (3) of Table 10, we restrict the sample to syndicated

loan-financed M&A deals, with the Target-Lender Relation dummy as the explanatory variable of

interest. We find that acquirer CAR is significantly higher when the lead lender has a prior

relationship with the target (p<0.01). In sum, these findings are generally consistent with the deal

quality certification effect of loan financing in M&As.

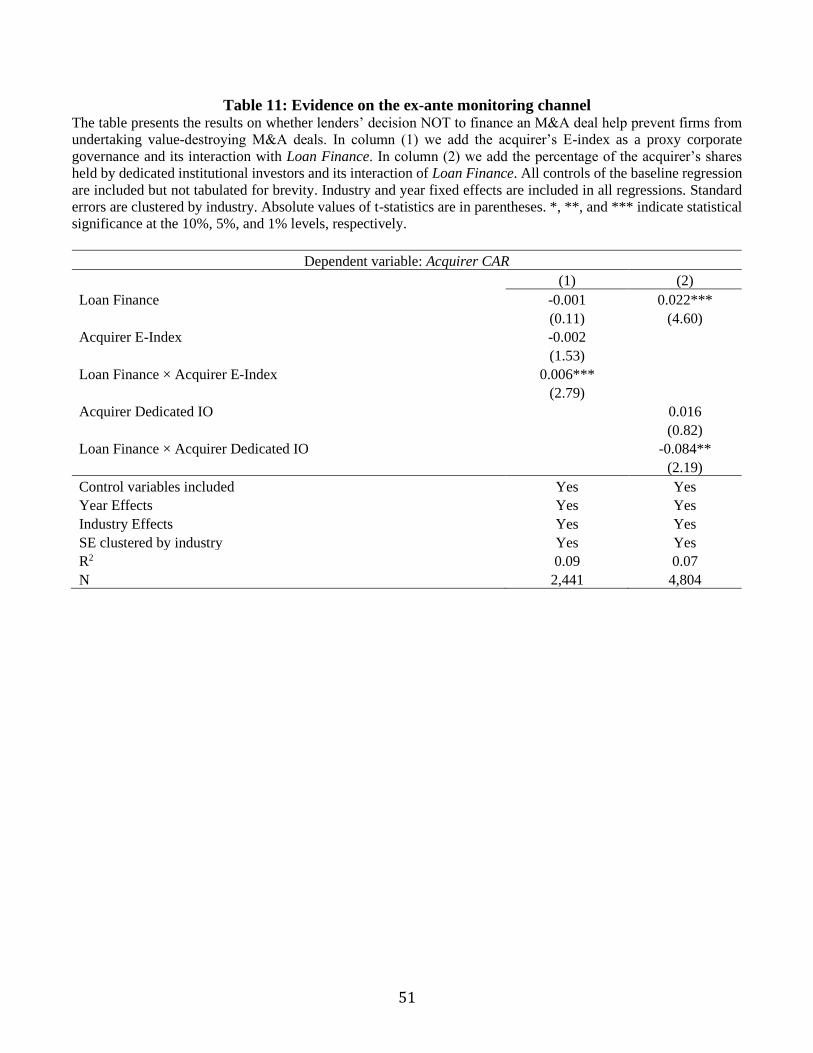

5.3 The ex-ante monitoring effect

Assuming lenders have informational advantages that allow them to better assess M&A

deal quality relative to shareholders, by refusing to provide financing to value-destroying M&As

lenders can prevent at least some of those bad M&As from happening, thus preserving shareholder

value (the ex-ante monitoring channel). This ex-ante channel is difficult to verify directly, because

we do not observe cases where the acquirer requests a loan but is declined by the lender. Therefore,

we attempt to provide indirect evidence of the ex-ante monitoring channel by exploring the

boundary conditions where private lenders’ role in preventing value-destroying M&A deals are

potentially more prominent. Specifically, we argue that the role of private lenders in preventing

value-destroying M&A deals should be less significant for acquirers that already have strong

26

corporate governance in place. Thus, we expect that the relationship between loan financing and

acquirer CAR is attenuated by alternative corporate mechanisms.

Following Bebchuk, Cohen, and Ferrell (2009) and Masulis et al. (2007), we create an

acquirer management entrenchment index (Acquirer E-index) based on the six most important anti-

takeover provisions, using the ISS Governance database.23 A greater Acquirer E-index indicates

weaker acquirer corporate governance from the market for corporate control (Masulis et al., 2007);

therefore, we expect the coefficient on the interaction of Loan Finance and Acquirer E-index to be

positive. Additionally, we follow the approach in Bushee and Noe (2000) and Bushee (2001) to

construct the percentage of shares outstanding held by dedicated institutional shareholders

(Acquirer Dedicated IO) and use it as a proxy for shareholder monitoring. We expect the

coefficient on the interaction of Loan Finance and Acquirer Dedicated IO to be negative, since a

high percentage of dedicated institutional holding indicates that the acquirer already has strong

corporate governance in place (Chen et al., 2007). The estimation results are reported in Table 11.

We find that the relationship between Loan Finance and Acquirer CAR is significantly stronger

for acquirers that have higher management entrenchment index (i.e., weaker governance) and

significantly weaker for acquirers that have higher dedicated institutional ownership (i.e., stronger

governance). Thus, the results presented in Table 11 provide evidence consistent with the ex-ante

monitoring channel.

<Insert Table 11 here>

5.4 The ex-post monitoring effect

23 An alternative corporate governance measure is the G-index based on 24 antitakeover provisions developed by

Gompers, Ishii, and Metrick (2003). However, the G-index data is unavailable for the period after 2006. As a result,

we use the E-index instead because it is available for most of our sample period.

27

The fourth possible channel through which syndicated loan financing benefits acquirer

shareholders is ex-post monitoring. Specifically, once private lenders have loaned money to

finance an M&A deal, they will monitor the acquirer over the term of the loan ex post. Lenders’

ex-post monitoring activities can create a positive spillover effect for acquirer shareholders. We

reason that the ex-post monitoring effect should be stronger if lenders monitor the acquirer for a

longer period. To test this prediction, we sort the loan-financed M&A deals into three groups

(short, medium and long maturity) based on the term to maturity of loans used for M&A

financing24. We then re-estimate model (1) replacing the key explanatory variable Loan Finance

with three dummies variables corresponding to the three term-to-maturity groups and report the

results in Table 12, Panel A. Consistent with the ex-post monitoring channel, we find that the effect

of loan financing is strongest for the group with the longest terms to maturity. We acknowledge

that there might be alternative explanations for this finding; for example, private lenders are willing

to offer loans with longer terms to maturity if the perceived M&A deal quality is higher.

<Insert Table 12 here>

In addition to acquirer CAR around the M&A announcement, we examine acquirer post-

merger long-run stock performance. If the ex-post monitoring effect is gradually realized by the

market over time, we might observe a positive relation between loan financing and acquirers’ long-

run stock performance. We adopt the method in Barber and Lyon (1997) and Mitchell and Stafford

(2000) to construct buy-and-hold long-run abnormal returns (BHAR) for acquirers. More

specifically, we first merge the CRSP monthly stock return universe with Compustat to acquire

firms’ book value of equity. Then, for the merged CRSP/Compustat universe we create 5-by-5

portfolios formed by firm size (as measured by market value of equity at the end of June) and

24 If an M&A deal is financed by more than one loan facility, we choose the longest term to maturity.

28

book-to-market quintiles using NYSE breakpoints. Each acquirer is assigned to a portfolio, and

we use the equal-weighted buy-and-hold return with monthly rebalancing of the corresponding

portfolio as the performance benchmark for the acquirer. Acquirer BHAR is the difference between

the acquirer’s post-acquisition buy-and-hold return and the benchmark portfolio’s buy-and-hold

return over one, two, and three years after the acquisition announcement month. If a stock in the

M&A sample is delisted during the holding period, we include the delisting return in the delisting

month and replace the missing stock returns in the subsequent months with the benchmark

portfolio’s returns. In Table 12, Panel B, we estimate a modified version of the regression model

(1) with 1-year, 2-year and 3-year BHAR as the dependent variables. We find a positive and

marginally significant relationship between Loan Finance and 3-year BHAR. Loan Finance, on

the other hand, does not have a statistically significant relation with 1-year or 2-year BHAR. In

sum, our results provide some support for the ex-post monitoring channel.

6. CONCLUSION

This paper makes four main contributions to the M&A literature. First, we employ a new

approach to identify M&A transactions financed by syndicated loans and provide evidence that

acquirer gains are higher in loan-financed M&A deals than in other deals. Most prior studies rely

on firms’ financing sources that exist before the M&A announcement date without being able to

verify that those existing sources are actually used to finance the M&A deal. To address this

limitation, we use a two-step approach that involves manually checking M&A announcements to

correctly identify M&A deals financed with syndicated loans.

Second, this study provides direct evidence of lender-side effects on acquirer gains, which

are largely ignored in prior literature. In particular, we use two identification strategies including

an instrumental variable approach and a quasi-natural experiment to accentuate the lender-side

29

factors while controlling for acquirer-side factors. Additionally, we demonstrate that lender

performance in M&A lending is persistent over time.

Third, we establish the channels through which syndicated loan financing can affect

acquirer shareholders’ value. Specifically, we show that lenders’ participation in the M&A market

can resolve uncertainty about the M&A deal quality, prevent acquirers from undertaking value-

destroying M&A transactions, and provide long-term monitoring that is beneficial to acquirer

shareholders. Our study also examines the interplay between lenders and other corporate

governance mechanisms.

Fourth, our study complements the empirical literature on the impacts of payment methods

on acquirer gains. In addition to the signaling effects of payment methods documented in prior

M&A studies, our results suggest that lenders’ participation in M&A deals also contributes to

higher acquirer gains in cash deals.

30

REFERENCES

Agarwal, S., Hauswald, I., 2010. Distance and private information in lending. Review of Financial Studies

23 (7), 2757-2788.

Akbulut, M. 2013. Do overvaluation-driven stock acquisitions really benefit acquirer shareholders? The

Journal of Financial and Quantitative Analysis 48(4), 1025-1055.

Almazan, A., 2002. A model of competition in banking: bank capital versus expertise. Journal of Financial

Intermediation 11(1), 87–121.

Amihud, Y., Garbade, K., Kahan, M., 1999. A new governance structure for corporate bonds. Stanford Law

Review 51(3), 447–492.

Amihud, Y., Lev, B., Travlos, N.G., 1990. Corporate control and the choice of investment financing: the

case of corporate acquisitions. Journal of Finance 45(2), 603-616.

Bao, J., Edmans, A., 2011. Do investment banks matter for M&A returns? The Review of Financial Studies

24(7), 2286-2315.

Barclay, M.J., Smith, C.W., Watts, R.L., 1997. The determinants of corporate leverage and dividend

policies. Journal of Financial Education 23, 1-15.

Barber, B.M., Lyon, J.D., 1997. Detecting long-run abnormal stock returns: The empirical power and

specification of test statistics. Journal of Financial Economics 43(3), 341-372.

Barraclough, K., Robinson, D.T., Smith, T., Whaley, R.E., 2013. Using option prices to infer overpayments

and synergies in M&A transactions. Review of Financial Studies 26(3), 695-722.

Bebchuk, L., Cohen. A., Ferrell A., 2009. What matters in corporate governance? The Review of Financial

Studies 22(2),783–827.

Betton, S., Eckbo, B.E., Thorburn, K.S., 2008. Corporate takeovers. In Eckbo, B.E. (Ed.), Handbook of

Corporate Finance: Empirical Corporate Finance. Elsevier/North-Holland, Amsterdam, pp. 291-430.

Bharadwaj, A., Shivadasani, A., 2003. Valuation effects of bank financing in acquisitions. Journal of

Financial Economics 67(1), 113-148

Bharath, S.T., Dahiya, S., Saunders, A., Srinivasan, A., 2011. Lending relationships and loan contract terms.

The Review of Financial Studies 24(4), 1141–1203.

Boot, A., 2000. Relationship banking: what do we know? Journal of Financial Intermediation 9(1), 7-25.

Boyd, J.H., Prescott, E.C., 1986. Financial intermediary-coalitions. Journal of Economic Theory 38(2),

211–232.

Bradley, M., Sundaram, A., 2006. Acquisitions and performance: a reassessment of the evidence. Working

Paper, Duke University, Durham NC.

Bushee, B.J., 2001. Do institutional investors prefer tear-term earnings over long-run value? Contemporary

Accounting Research 18(2): 207-246.

31

Bushee, B.J., Noe, C.F., 2000. Corporate disclosure practices, institutional investors, and stock return

volatility. Journal of Accounting Research 38, 171-202.

Carhart, M., 1997. On persistence in mutual fund performance. Journal of Finance 52(1), 57-82.

Cetorelli, N., Strahan, P.E., 2006. Finance as a barrier to entry: bank competition and industry structure in

local U.S. markets. The Journal of Finance 61(1), 437-461.

Chang, S., 1998. Takeovers of privately held targets, method of payment, and bidder returns. Journal of

Finance 53(2), 773-784.

Chava, S., Roberts, M.R., 2008. How does financing impact investment? The role of debt covenants.

Journal of Finance 63(5), 2085-2121.

Chemmanur, T.J., Fulghieri, P., 1994. Reputation, renegotiation, and the choice between bank loans and

publicly traded debt. The Review of Financial Studies 7(3), 475-506.

Chen, X., Harford, J., Li, K., 2007. Monitoring: which institutions matter. Journal of Financial Economics

86(2), 279–305.

Degryse, H., Ongena, S., 2005. Distance, lending relationship, and competition. The Journal of Finance

60(1), 231-266.

Diamond, D.W., 1984. Financial intermediation and delegated monitoring. The Review of Economic

Studies 51(3), 393-414.

———. 1991. Monitoring and reputation: The choice between bank loans and directly placed debt. Journal

of Political Economy 99(4), 689–721.

Dou, Y., 2017. The spillover effect of consolidating securitization entities on small business lending.

Working Paper, New York University, New York NY.

Dou, Y., Ryan, S.G., Xie, B., 2018. The real effects of FAS 166/167 on banks’ mortgage approval and sale

decisions. Journal of Accounting Research 56(3), 843-882.

Fama, E., 1985. What’s different about banks? Journal of Monetary Economics 15(1), 29-39.

Fama, E., French, K., 1993. Common risk factors in the returns on bonds and stocks. Journal of Financial

Economics 33(1), 3-53.

Faulkender, M., Petersen, M., 2006. Does the source of capital affect capital structure? Review of Financial

Studies 19(1), 45-79.

Franks, J.R., Harris, R.S., Mayer, C., 1988. Means of payment in takeovers: results for the U.K. and the

U.S. In Auerbach, A. (Ed.), Corporate Takeovers, University of Chicago Press, Chicago IL

Fu, F., Guay, W.R., Zhang, W., 2016. Costly corporate governance: evidence from shareholder approval in

mergers and acquisitions. SSRN working paper.

Golubov, A., Zhang, H., 2015. Extraordinary acquirers. Journal of Financial Economics 116(2), 314-330.

32

Gompers, P.A., Ishii, J.L., Metrick, A., 2003. Corporate governance and equity prices. Quarterly Journal of

Economics 118(1), 107–55.

Guiso, L., Sapienza, P., Zingales, L., 2004. Does local financial development matter? Quarterly Journal of

Economics 119(3), 929-969.

Hollander, S., Verriest, A., 2016. Bridging the gap: the design of bank loan contracts and distance. Journal

of Financial Economics 119(2), 399-419.

Hope, O.K., Thomas, W., Vyas, D. 2013. Financial reporting quality of U.S. private and public firms. The

Accounting Review 88(5), 1715-1742.

Ivashina, V., Nair, V.B., Saunders, A., Massoud, N., 2009. Bank debt and corporate governance. The

Review of Financial Studies 22(1), 41-77.

Knyazeva, A., Knyazeva, D., 2012. Does being your bank’s neighbor matter? Journal of Banking & Finance

36(4), 1194-209.

Loughran, T., Vijh, A.M., 1997. Do long-term shareholders benefit from corporate acquisitions? Journal of

Finance 52(5), 1765-1790.

Martin, K.J., 1996. The method of payment in corporate acquisitions, investment opportunities, and

management ownership. Journal of Finance 51(4), 1227-1246.

Masulis, R.W., Wang, C., Xie, F., 2007. Corporate governance and acquirer returns. The Journal of Finance

62(4), 1851-1889.

Martynova, M., Renneboog, L., 2009. What determines the financing decision in corporate takeovers: Cost

of capital, agency problems, or the means of payment? Journal of Corporate Finance 15(3), 290-

315.

Mitchell, M.L., Stafford, E., 2000. Managerial decisions and long-term stock price performance. Journal of

Business 73(3), 287-329.

Moeller, S.B., Schlingemann, F.P., Stulz, R.M., 2004. Firm size and the gains from acquisitions. Journal of

Financial Economics 73(2), 201-228.

———., 2005. Wealth destruction on a massive scale? A study of acquiring firm returns in the recent

merger wave. Journal of Finance 60(2), 757–782.

Myers, S., Majluf, N., 1984. Corporate financing and investment decisions when firms have information

that investors do not have. Journal of Financial Economics 13(2), 187-221.

Officer M.S., Poulsen, A.B., Stegemoller, M., 2009. Target-firm information asymmetry and acquirer

returns. Review of Finance 13(3), 467–493.

Ramakrishnan, R.T.S., Thakor, A.V., 1984. Information reliability and a theory of financial intermediation.

Review of Economic Studies 51(3), 415-432.

33

Schenone, C., 2010. Lending relationships and information rents: Do banks exploit their information

advantages? The Review of Financial Studies 23(3), 1149-1199.

Schlingemann, F.P., 2004. Financing decisions and acquirer gains. Journal of Corporate Finance 10(5),

683-701.

Shleifer, A. Vishny, R.W., 2003. Stock market driven acquisitions. Journal of Financial Economics 70(3),

295-311.

Stulz, R.M., 1990. Managerial discretion and optimal financing policies. Journal of Financial Economics

26(1), 3– 27.

Tian, X., Zhang, H., 2016. Impact of FAS 166/167 on credit card securitization. Working Paper, Ohio

State University, Columbus OH.

Travlos, N.G., 1987. Corporate takeover bids, method of payment, and bidding firms’ stock returns.

Journal of Finance 42(4), 943-963.

Vladimirov, V., 2015. Financing acquirers in takeover contests. Journal of Financial Economics 117(3),

534-557.

Wang, W., 2018. Bid anticipation, information revelation, and merger gains. Journal of Financial

Economics 128 (2), 320-343.

Wooldridge, J.M., 2002. Econometric analysis of cross section and panel data. The MIT Press, Cambridge

MA.

Yook, K.C., 2003. Larger returns to cash acquisitions: Signaling effect or leverage effect? Journal of

Business 76(3), 477–498.

34

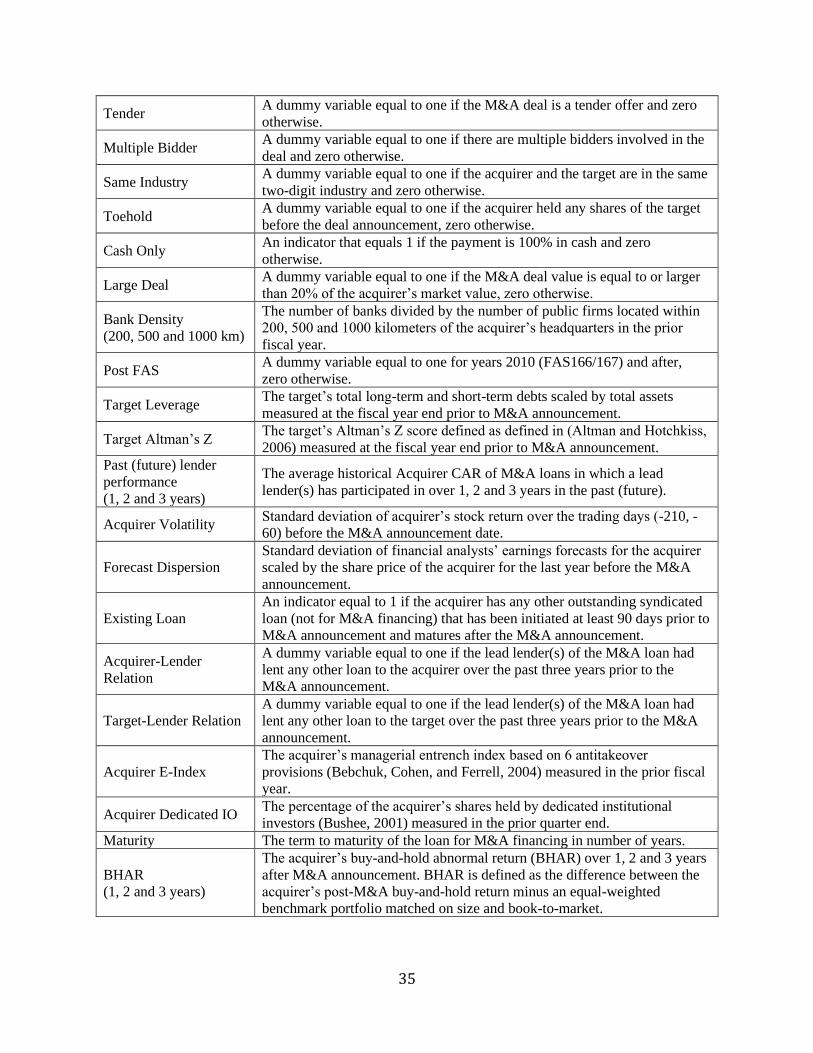

Appendix A: Variable definitions Variable Definition

Loan Finance An indicator that equals one if an M&A deal is financed by syndicated

loan(s) and zero otherwise. To identify loan-financed M&A deals, we first

identify M&A deals in which the acquirer has borrowed any loans with

“Acquisition line” or “Takeover” as the primary or secondary purpose

initiated during the periods from 90 days prior to the M&A announcement

to 180 days following the announcement, or the completion date of the deal

if this comes first. For potential loan-financed M&As, we manually search

the M&A announcement through Factiva, and SEC filings (form 8-K) to

verify whether the acquirer explicitly states that the M&A deal is financed

with bank loans.

Loan Finance Ratio The amount of M&A loan(s) scaled by the M&A deal value. If an M&A

deal is not financed with loans, then the value of this variable is zero.

Bond Finance

A dummy variable that equals 1 if an M&A deal is financed by a new bond

issuance. We first check whether the acquirer of an M&A deal has issued

any new bond issued during the periods from 90 days prior to the M&A

announcement to 180 days following the announcement, or the completion

date of the deal if this comes first. For potential bond-financed M&As, we

manually search the M&A announcement through Factiva and SEC filings

(form 8-K) to verify whether the acquirer explicitly states that the M&A

deal is financed with a new bond issuance.

Acquirer CAR

The three-day CAR to the acquirer’s stock over the three-day window (-1,

+1) around the M&A announcement date. Abnormal stock returns are

estimated using Fama-French-Carhart 4-factor model over the trading days

(-272, -21) before the deal announcement. Firms with less than 60 trading

days available to estimate the model are excluded.

Offer Premium The premium of the offer price over the target share price 4 weeks prior to

M&A announcement.

Target CAR The CAR to the target’s stock over window (-1, +1). Abnormal returns are

estimated using the same method as for the acquirer.

Acquirer Size The natural logarithm of the acquirer’s market value of equity in million

dollars measured at the fiscal year end prior to M&A announcement.

Acquirer ROA The acquirer’s return on assets for the last fiscal year prior to M&A

announcement.

Acquirer Cash The acquirer’s cash holding scaled by total assets measured at the fiscal year

end prior to M&A announcement.

Acquirer Leverage The acquirer’s total long-term and short-term debts scaled by total assets

measured at the fiscal year end prior to M&A announcement.

∆ Acquirer Leverage

Change in acquirer’s leverage ratio from the last year before the deal

announcement to the first year after the deal completion.

Acquirer Tobin Q

The acquirer’s Tobin’s Q, which is defined as the sum of market value of

equity and book value of liabilities scaled by book value of total assets at

the most recent fiscal year end prior to M&A announcement.

Deal Size The M&A transaction value scaled by acquirer’s market value of equity.

Private Target A dummy variable equal to one if the target is a private company and zero

otherwise.

Friendly A dummy variable equal to one if the M&A deal is a friendly takeover and

zero otherwise.

35

Tender A dummy variable equal to one if the M&A deal is a tender offer and zero

otherwise.

Multiple Bidder A dummy variable equal to one if there are multiple bidders involved in the

deal and zero otherwise.

Same Industry A dummy variable equal to one if the acquirer and the target are in the same

two-digit industry and zero otherwise.

Toehold A dummy variable equal to one if the acquirer held any shares of the target

before the deal announcement, zero otherwise.

Cash Only An indicator that equals 1 if the payment is 100% in cash and zero

otherwise.

Large Deal A dummy variable equal to one if the M&A deal value is equal to or larger

than 20% of the acquirer’s market value, zero otherwise.

Bank Density

(200, 500 and 1000 km)

The number of banks divided by the number of public firms located within

200, 500 and 1000 kilometers of the acquirer’s headquarters in the prior

fiscal year.

Post FAS A dummy variable equal to one for years 2010 (FAS166/167) and after,

zero otherwise.

Target Leverage The target’s total long-term and short-term debts scaled by total assets

measured at the fiscal year end prior to M&A announcement.

Target Altman’s Z The target’s Altman’s Z score defined as defined in (Altman and Hotchkiss,

2006) measured at the fiscal year end prior to M&A announcement.

Past (future) lender

performance

(1, 2 and 3 years)

The average historical Acquirer CAR of M&A loans in which a lead

lender(s) has participated in over 1, 2 and 3 years in the past (future).

Acquirer Volatility Standard deviation of acquirer’s stock return over the trading days (-210, -

60) before the M&A announcement date.

Forecast Dispersion

Standard deviation of financial analysts’ earnings forecasts for the acquirer

scaled by the share price of the acquirer for the last year before the M&A

announcement.

Existing Loan

An indicator equal to 1 if the acquirer has any other outstanding syndicated

loan (not for M&A financing) that has been initiated at least 90 days prior to

M&A announcement and matures after the M&A announcement.

Acquirer-Lender

Relation

A dummy variable equal to one if the lead lender(s) of the M&A loan had

lent any other loan to the acquirer over the past three years prior to the

M&A announcement.

Target-Lender Relation

A dummy variable equal to one if the lead lender(s) of the M&A loan had

lent any other loan to the target over the past three years prior to the M&A

announcement.

Acquirer E-Index

The acquirer’s managerial entrench index based on 6 antitakeover

provisions (Bebchuk, Cohen, and Ferrell, 2004) measured in the prior fiscal

year.

Acquirer Dedicated IO The percentage of the acquirer’s shares held by dedicated institutional

investors (Bushee, 2001) measured in the prior quarter end.

Maturity The term to maturity of the loan for M&A financing in number of years.

BHAR

(1, 2 and 3 years)