leo p. grohowski files/leo - pittsburgh... · leo p. grohowski . chief investment officer, bny...

TRANSCRIPT

Leo P. Grohowski Chief Investment Officer, BNY Mellon Wealth Management

May 2015

Economic and Financial Market Outlook

2

1As of 3/31/15

The Investments Company for The World

• Top 10 U.S. wealth manager − Approximately $194 billion in private client assets1

− $15.2 billion in deposits and $11.6 billion in loans outstanding1 • Among nation’s largest family office providers and a leading

provider of charitable gift services

• Two centuries of experience and perspective − Oldest private bank in U.S. history

− Among first to create dedicated family office business • Offices in 18 states and 4 countries

BNY MELLON

BNY MELLON WEALTH

MANAGEMENT

• Leading global provider of securities services

−$28.5 trillion in assets under custody and administration1

• 7th largest global asset manager

−$1.7 trillion under management1 • 7th largest U.S. asset manager

3

4

Historical Bull Markets

As of 4/24/15. Source: StrategasRP.

S&P 500 Historical Bull Markets 1928 to Present

BU

LL M

AR

KE

T A

DVA

NC

E (%

)

BULL MARKET DURATION (MONTHS)

0

50

100

150

200

250

300

350

400

450

0 20 40 60 80 100 120

1966-68 1987-90

1970-73

1962-66 1957-61

1942-46

1932-37

1982-87

2002-07

1974-80

1949-56

1990-00

3/9/09 to Current, 72 Months, 213%

Average 57 Months, 165%

5

2015 Outlook and Strategy

• Further Equity Gains

• Improved Performance − Active vs. Passive − U.S. Small Cap vs. U.S. Large Cap − Non-U.S. vs. U.S.

• Normalization of Interest Rates

• Stronger U.S. Dollar

• Higher Volatility Environment – Diversifiers More Important

• Disciplined Rebalancing and Due Diligence Key to Alpha Generation and Downside Protection

1.9

3.7

1.7

9.2

10.2

1.2

3.8

0.0

2.3 2.6 1.9

0

3

6

9

12

LargeCap

MidCap

Small Cap

Dev. Emerg. Taxable HighYield

Treas. HedgeFunds

GlobalREITs

ManagedFutures

6

YTD Market Returns

As of 4/30/2015 unless noted otherwise. Indices used: Large Cap: S&P 500; Mid Cap: S&P MidCap 400; Small Cap: Russell 2000; Developed International: MSCI EAFE (Net); Emerging Markets: MSCI EMF; Taxable Fixed Income: Barclays Capital U.S. Aggregate; High Yield Fixed Income: Merrill Lynch HY Master II; Treasuries: U.S. 3 Month Treasury; Hedge: HFRX Global Hedge Index; Global Real Estate: FTSE EPRA/NAREIT; Managed Futures: HFRI Macro Index. Sources: Bloomberg L.P. and Morningstar. Past performance is not indicative of future performance.

U.S. Equities International Equities

Fixed Income Diversifiers

PE

RC

EN

T

7

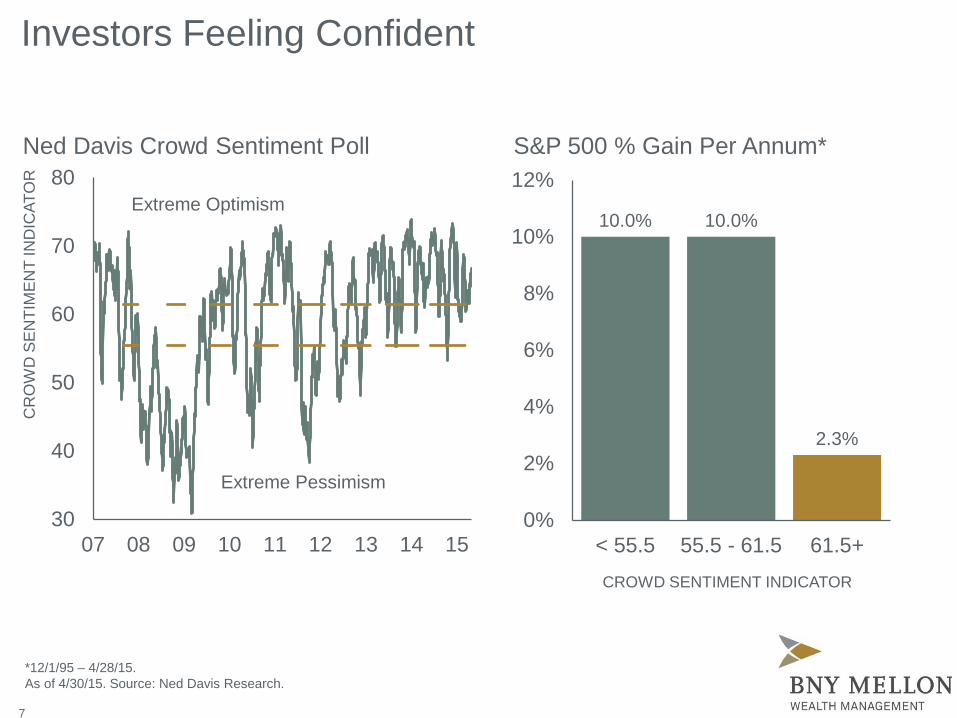

Ned Davis Crowd Sentiment Poll

Extreme Pessimism

Extreme Optimism

Investors Feeling Confident

S&P 500 % Gain Per Annum*

CROWD SENTIMENT INDICATOR

30

40

50

60

70

80

07 08 09 10 11 12 13 14 15

CR

OW

D S

EN

TIM

EN

T IN

DIC

ATO

R

10.0% 10.0%

2.3%

0%

2%

4%

6%

8%

10%

12%

< 55.5 55.5 - 61.5 61.5+

*12/1/95 – 4/28/15. As of 4/30/15. Source: Ned Davis Research.

Improving Confidence

78 82 86 90 94 98 02 06 10 1475

80

85

90

95

100

105

110

IND

EX

NFIB Index ofSmall Business Optimism*

8

71 76 81 86 91 96 00 05 10 1520

40

60

80

100

120

140

160

IND

EX

Conference Board'sConsumer Confidence Index**

*As of 4/30/15. Sources: National Federation of Independent Businesses and Ned Davis Research **As of 4/30/15. Shaded areas represent periods of U.S. recession. Source: The Conference Board

78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 143

6

9

12

15

18

PE

RC

EN

T

As of 4/30/15. Sources: Bureau of Labor Statistics and FactSet.*Includes officially unemployed, those who want a job but stopped looking, and those who need full-time jobs but can only find part-time work, measured as a percentage of the civilian labor force plus all the marginally attached workers.

Unemployment Rate, Seasonally-Adjusted

U.S. Civilian Unemployment Rate U.S. Broader Unemployment Rate*

9

Slow Improvement in Employment

10.8%

5.4%

10

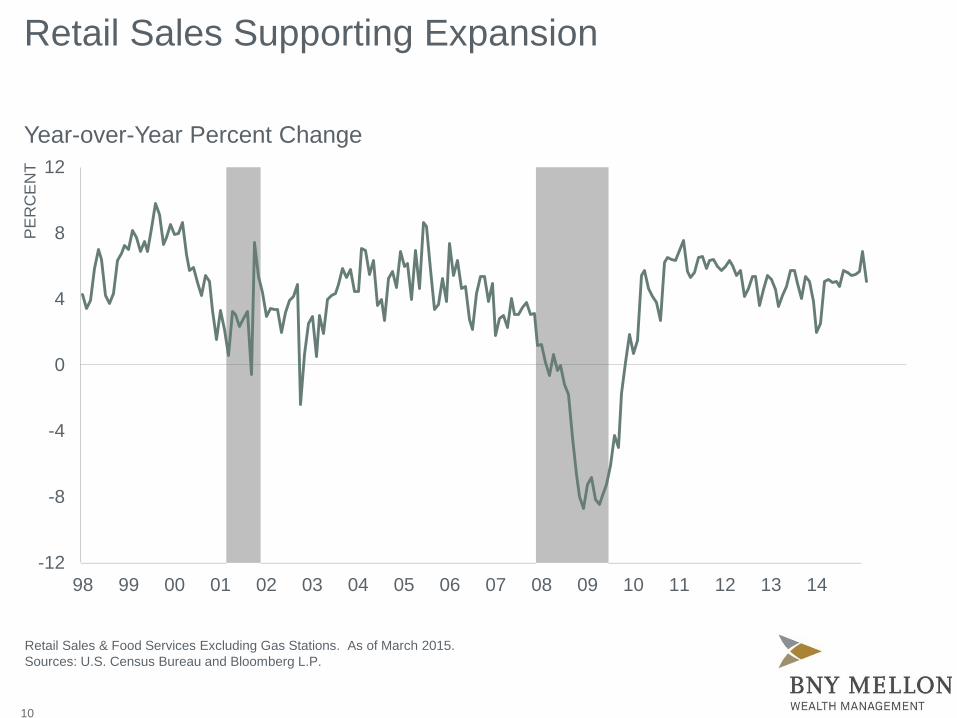

Retail Sales Supporting Expansion

Retail Sales & Food Services Excluding Gas Stations. As of March 2015. Sources: U.S. Census Bureau and Bloomberg L.P.

Year-over-Year Percent Change

-12

-8

-4

0

4

8

12

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

PE

RC

EN

T

60

70

80

90

100

110

120

130

81 85 89 93 97 01 05 09 13

Significant Reduction in Household Debt FORCED DELEVERAGING A PARTIAL CONTRIBUTOR

As of 12/31/14. Household debt includes home mortgage and consumer credit. Source: Department of Commerce and FactSet

Household Debt as Percentage of Disposable Personal Income

102.5%

11

3

6

9

12

99 02 05 08 11 14

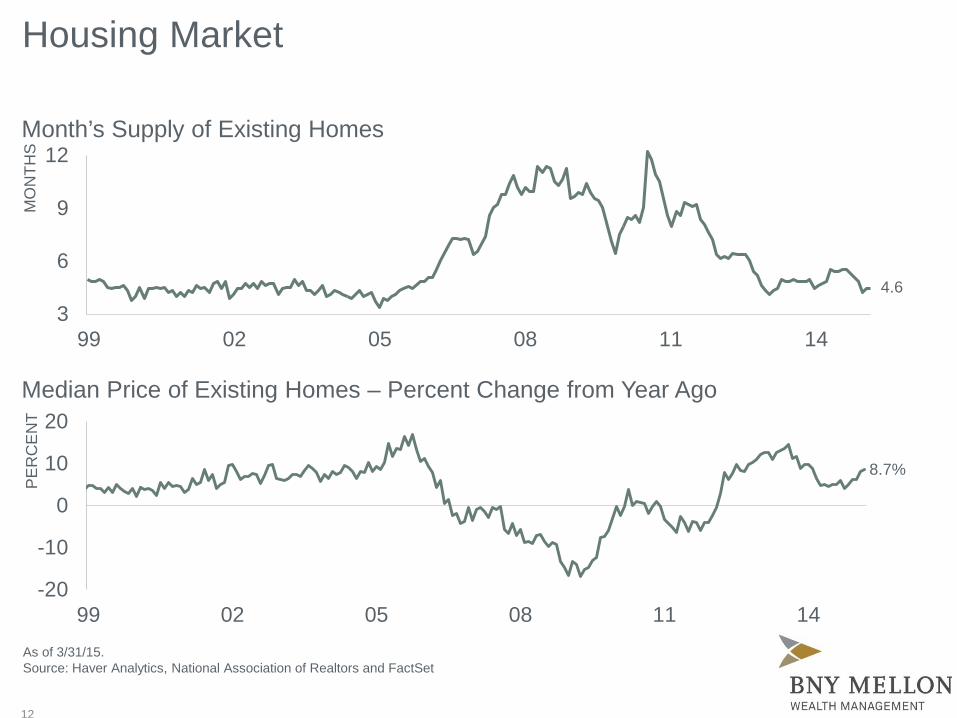

Housing Market

-20

-10

0

10

20

99 02 05 08 11 14

PE

RC

EN

T

As of 3/31/15. Source: Haver Analytics, National Association of Realtors and FactSet

Median Price of Existing Homes – Percent Change from Year Ago

Month’s Supply of Existing Homes

4.6

8.7%

MO

NTH

S

12

13

IND

EX

LEV

EL

U.S. Manufacturing Rebounding

30

40

50

60

70

95 97 99 01 03 05 07 09 11 13 15

ISM Purchasing Managers’ Index

As of 4/30/15. Source: Institute for Supply Management and FactSet

14

1.8

-0.3

-2.8

2.5 1.9

2.3 2.2 2.4 2.5

-4

-2

0

2

4

2007 2008 2009 2010 2011 2012 2013 2014 2015E

PE

RC

EN

T

Sources: 2007-2014: Bureau of Economic Analysis; 2015: BNY Mellon Wealth Management.

Moderate, but Improving U.S. Growth Expectations

BNY Mellon Wealth Management GDP Estimates

15

International Manufacturing

Eurozone vs. China Markit Manufacturing Purchasing Managers' Index

As of 4/30/15. Seasonally adjusted. Source: FactSet

IND

EX

LEV

EL

32

36

40

44

48

52

56

60

09 10 11 12 13 14 15

Eurozone

China

16

2.4 2.6

-0.1

7.4

0.9

2.4

1.3

3.1 2.7

1.0

6.8

1.5

2.7

0.9

-2

0

2

4

6

8

UnitedStates

UnitedKingdom

Japan China EuroArea

Middle Eastand

North Africa

LatinAmerica

PE

RC

EN

T

2014 2015E

Real Gross Domestic Product (GDP)

As of April 2015. Source: International Monetary Fund

Global Outlook

17

Central Banks Maintaining Accommodative Policies EXPECT GREATER DIVERGENCE IN 2015

Central Bank Rates

As of 4/30/15. Source: Bloomberg LP

0

2

4

6

8

10

12

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Bank of England U.S. Federal Funds Rate Bank of Japan European Central Bank

PE

RC

EN

T

18

70

80

90

100

110

Data represents the JP Morgan Trade-Weighted U.S. Dollar Index. As of 4/30/15. Source: Bloomberg L.P.

Avg = 90.4 Avg = 89.3

Avg = 85.9

Avg = 83.0

Avg = 87.3

Avg = 83.8

2005 2006 2007 2008 2009 2010

Avg = 79.5

2011 2012

Avg = 81.5

2013 2014

Avg = 83.6 Avg = 86.2

19

Avg = 96.1

2015

IND

EX

Trade-Weighted Dollar

The Dollar

U.S. Inflation Remains Contained

Year-over-Year Percent Change in Consumer Price Index

96 98 00 02 04 06 08 10 12 14YEAR

-3

-2

-1

0

1

2

3

4

5

6

PE

RC

EN

T

As of 03/31/15. Source: U.S. Bureau of Labor Statistics.

Core CPI Headline CPI

20

2.03 1.85

0.37 0.33

4.29 4.57

3.91

1.50

0

1

2

3

4

5

U.S. U.K. Germany Japan

As of 4/30/15. Source: FactSet.

Bond Yields Low by Historical Measures

Global Yields (Current vs. 20-year Average)

21

PE

RC

EN

T

Current 20-year Average

0

2

4

6

8

10

90 95 00 05 10 15

S&P 500 Operating Earnings Yield 10-Year Treasury Note

22

Stocks Attractive Relative to Bonds

Earnings yield is inverse of P/E for 4-quarter trailing operating earnings. As of 3/31/15. Sources: Standard & Poor’s Corp. and Bloomberg L.P.

Internet bubble: Earnings yield of 3.4 = P/E of 29

S&P 500 Earnings Yield vs. 10-Year Treasury Note

PE

RC

EN

T

As of 4/30/15. Indices used: U.S. Large Cap: S&P 500; Non-U.S. Developed: MSCI EAFE; Emerging Markets: MSCI EM. Source: Bloomberg and MSCI

Market Valuations (Forward P/E Ratio)

Global Equities Remain Attractively Valued

23

18.3x 18.5x

14.8x

19.4x 20.8x

15.4x

0

5

10

15

20

25

U.S.Large Cap

Non-U.S.Developed

EmergingMarkets

Current 1996-2015 Mean

P/E

RAT

IO

82.54

49.51 56.86

83.77 96.44 96.82

107.29 113.04

120-125

0

20

40

60

80

100

120

140

2007 2008 2009 2010 2011 2012 2013 2014 2015Estimate

24

S&P 500 Operating Earnings Estimates CONSISTENT WITH SLOW GROWTH SCENARIO

As of 3/31/15. Earnings represent trailing four-quarter earnings per share. Source: Standard & Poor’s and BNY Mellon Wealth Management.

S&P 500 Earnings and BNY Mellon Wealth Management Estimates

$ D

OLL

AR

S

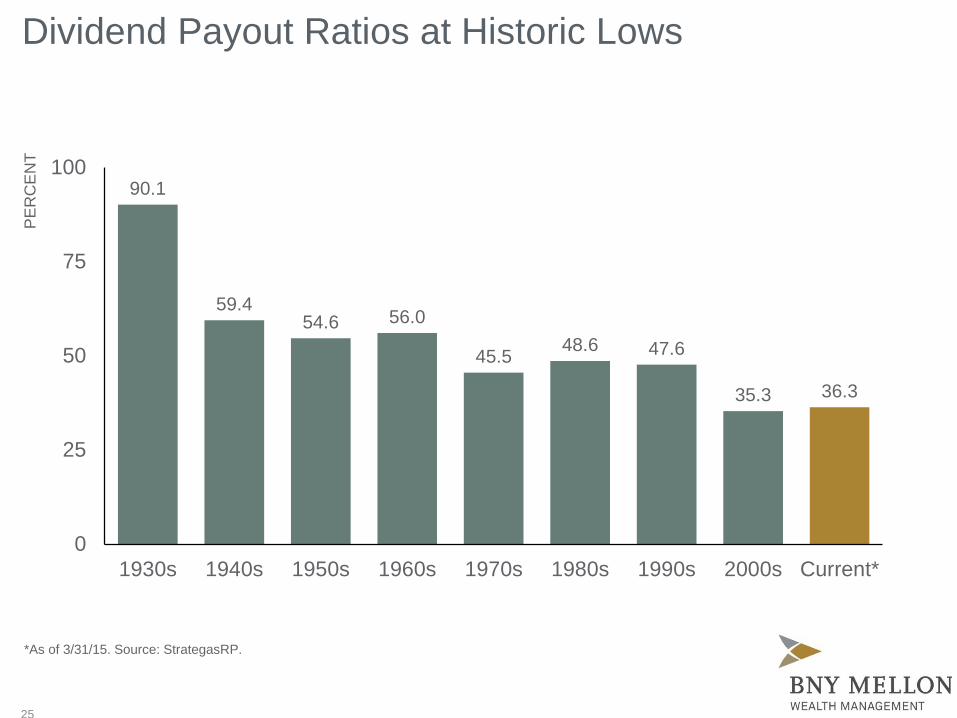

90.1

59.4 54.6 56.0

45.5 48.6 47.6

35.3 36.3

0

25

50

75

100

1930s 1940s 1950s 1960s 1970s 1980s 1990s 2000s Current*

Dividend Payout Ratios at Historic Lows

PE

RC

EN

T

*As of 3/31/15. Source: StrategasRP.

25

26

Number and Value of U.S. M&A Deals, Quarterly

050100150200250300350400450500

0

50

100

150

200

250

300

350

400

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Number of Deals (Left Axis) Value of Deals (Right Axis)

$ B

ILLI

ON

S

As of 3/31/15. Source: StrategasRP.

M&A Activity Improving

UNDERWEIGHT SMALL

UNDERWEIGHT NEUTRAL SMALL

OVERWEIGHT OVERWEIGHT

EQUITY Large Cap Mid Cap Small Cap International Developed Large Cap International Developed Small Cap Emerging Markets Private Equity Private Equity-Real Estate

FIXED INCOME Treasuries Investment-grade Corporate Tax-exempt High Yield Emerging Market Debt

DIVERSIFIERS Real Estate (REITs) Long/Short Hedge Absolute Return Hedge Managed Futures Commodities

Asset Class Positioning

As of 4/30/15.

-20%

-10%

0%

10%

20%

30%

40%

50%

Sha

ngha

i AM

SC

I Chi

naJa

pan

Taiw

anS

inga

pore HK

Asi

a x

JA

PA

C x

JK

orea

Mal

aysi

aA

ustra

liaIn

dia

Thai

land

New

Zeal

and

Phi

lippi

nes

Indo

nesi

a

0

5

10

15

20

25

Sha

ngha

i AM

SC

I Chi

naJa

pan

Taiw

anS

inga

pore HK

Asi

a x

JA

PA

C x

JK

orea

Mal

aysi

aA

ustra

liaIn

dia

Thai

land

New

Zeal

and

Phi

lippi

nes

Indo

nesi

a

28

P/E Ratio vs. Long-Term Average P/E Ratio Premium over Long-Term Avg.

12-month forward P/E ratios Source: Nomura

Some Large Markets Trading below Historical P/E Avg.

PE

RAT

IO

29

Earnings Expectations Rise as Euro Weakens

85

90

95

100

105-30-25-20-15-10

-505

101520

2009 2010 2011 2012 2013 2014 2015

PE

RC

EN

T

Euro Trade Weighted Index (Inverted, Right Axis)

Continental Europe: 13-Week Earnings Revisions Relative to Global (Left Axis)

IND

EX

As of 1/31/15. Source: Credit Suisse Research, Bloomberg, Thomson Reuters

Continental Europe Earnings Revisions vs. Euro Trade Weighted Index

30

Source: The Economist

31

Abe is Most Stable Government after Koizumi

0

1

2

3

4

5

6

KoizumiApr-'01

|Sep-'06

AbeSep-'06

|Sep-'07

FukudaSep-'07

|Sep-'08

AsoSep-'08

|Sep-'09

HatoyamaSep-'09

|Jun-'10

KanJun-'10

|Sep-'11

NodaSep-'11

|Dec-'12

AbeDec-'12

|Dec-'14

Potential for another 4 years after strong December lower-house election results

Life of Government for Each Prime Minister Since Koizumi

YEA

RS

Source: BNY Mellon Asset Management Japan

32

465,000

470,000

475,000

480,000

485,000

490,000

495,000

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

Pre-Abenomics Post-Abenomics

Steady Improvement in Japan’s Nominal GDP

Japan Nominal GDP, SAAR

YEN

BIL

LIO

N

As of 1/31/15. Source: Japan’s Cabinet Office, BNY Mellon Investment Management

-60

-40

-20

0

20

40

60

80

100

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

02 04 06 08 10 12 140

20

40

60

80

100

120

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

02 04 06 08 10 12 14

33

Is Good News Now in Price?

MSCI World vs. Trailing Weighted EPS TOPIX vs. Trailing Weighted EPS

IND

EX

IND

EX

EP

S

EP

S

As of 3/31/15 using 12-month trailing EPS. Source: Bloomberg LP TOPIX: Tokyo Stock Price Index

MSCI World (Left) MSCI EAFE Trailing EPS (Right)

TOPIX (Left Axis) TOPIX Trailing EPS (Right)

0

1

2

3

4

5

6

2007 2008 2009 2010 2011 2012 2013 2014 2015

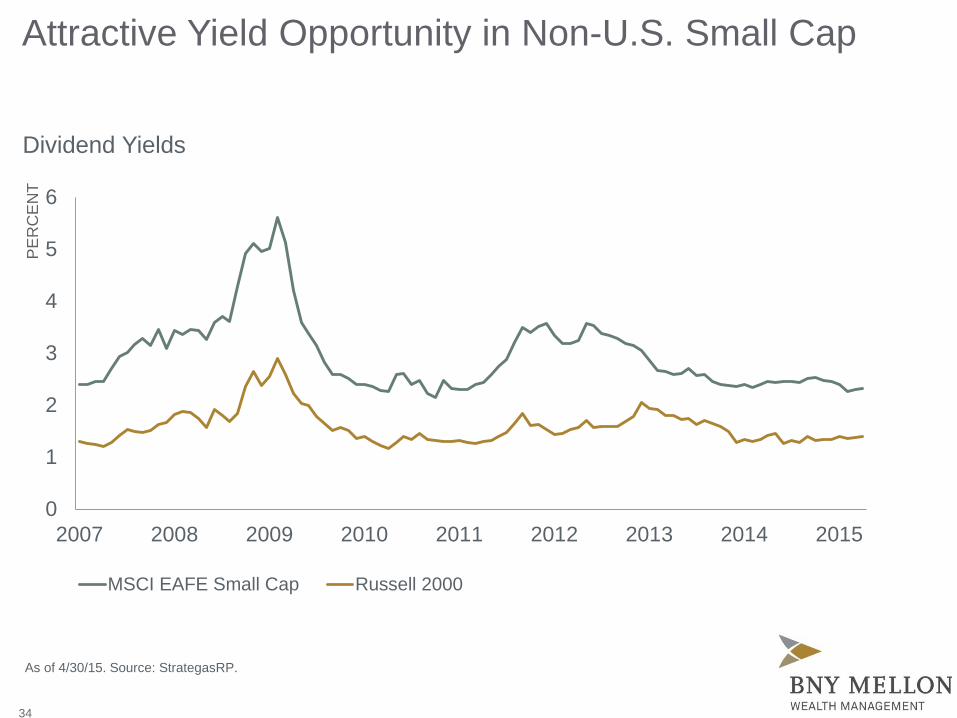

MSCI EAFE Small Cap Russell 2000

34

Attractive Yield Opportunity in Non-U.S. Small Cap

Dividend Yields

PE

RC

EN

T

As of 4/30/15. Source: StrategasRP.

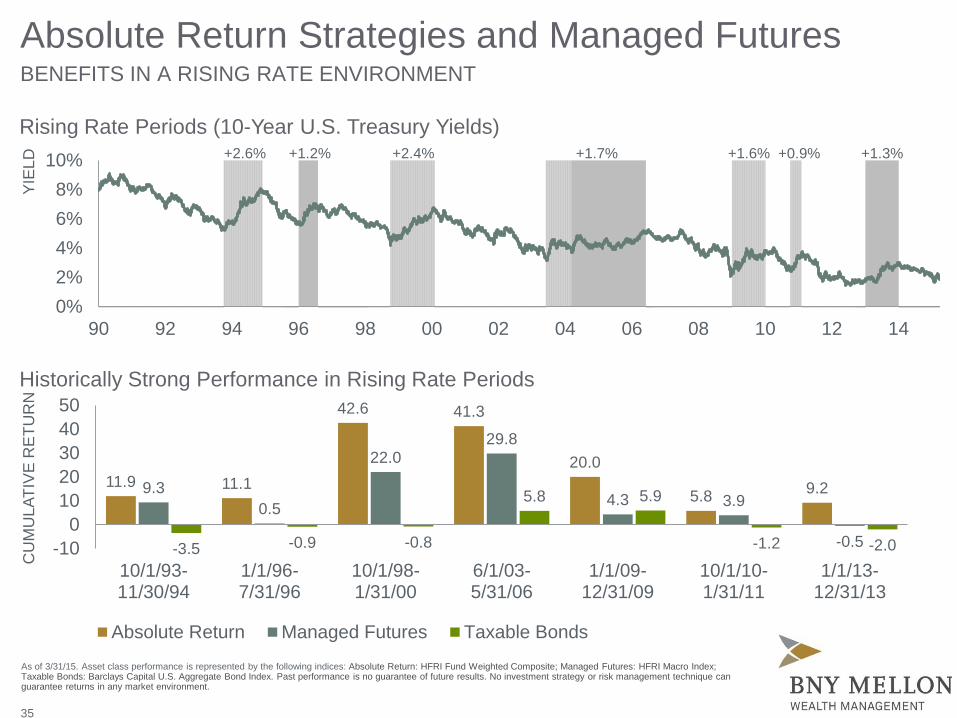

Absolute Return Strategies and Managed Futures BENEFITS IN A RISING RATE ENVIRONMENT

As of 3/31/15. Asset class performance is represented by the following indices: Absolute Return: HFRI Fund Weighted Composite; Managed Futures: HFRI Macro Index; Taxable Bonds: Barclays Capital U.S. Aggregate Bond Index. Past performance is no guarantee of future results. No investment strategy or risk management technique can guarantee returns in any market environment.

11.9 11.1

42.6 41.3

20.0

5.8 9.2 9.3 0.5

22.0 29.8

4.3 3.9

-0.5 -3.5 -0.9 -0.8

5.8 5.9

-1.2 -2.0 -100

1020304050

10/1/93-11/30/94

1/1/96-7/31/96

10/1/98-1/31/00

6/1/03-5/31/06

1/1/09-12/31/09

10/1/10-1/31/11

1/1/13-12/31/13

Absolute Return Managed Futures Taxable Bonds

Rising Rate Periods (10-Year U.S. Treasury Yields)

Historically Strong Performance in Rising Rate Periods

35

0%2%4%6%8%

10%

90 92 94 96 98 00 02 04 06 08 10 12 14

YIE

LD

CU

MU

LATI

VE

RE

TUR

N

+2.6% +1.2% +2.4% +1.7% +1.6% +0.9% +1.3%

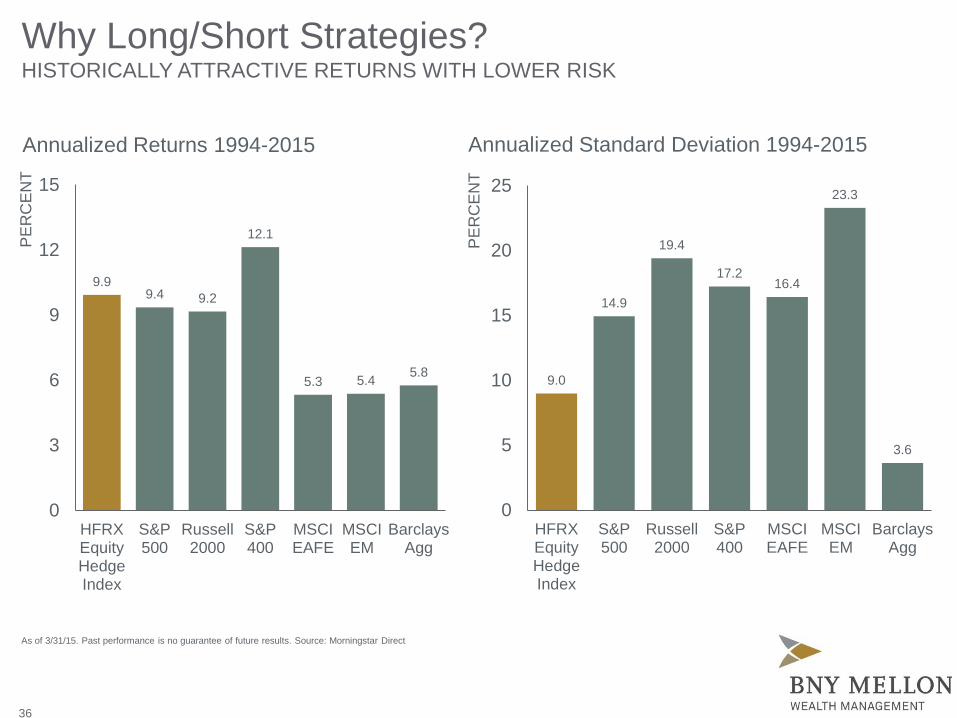

Why Long/Short Strategies? HISTORICALLY ATTRACTIVE RETURNS WITH LOWER RISK

9.9 9.4 9.2

12.1

5.3 5.4 5.8

0

3

6

9

12

15

HFRXEquityHedgeIndex

S&P500

Russell2000

S&P400

MSCIEAFE

MSCIEM

BarclaysAgg

As of 3/31/15. Past performance is no guarantee of future results. Source: Morningstar Direct

PE

RC

EN

T

9.0

14.9

19.4

17.2 16.4

23.3

3.6

0

5

10

15

20

25

HFRXEquityHedgeIndex

S&P500

Russell2000

S&P400

MSCIEAFE

MSCIEM

BarclaysAgg

PE

RC

EN

T

Annualized Returns 1994-2015 Annualized Standard Deviation 1994-2015

36

0

10

20

30

40

50

2009 2010 2011 2012 2013 2014 2015

37

As of 4/30/15. Source: FactSet

IND

EX

LEV

EL

20-YEAR MEAN

Expect Increased Volatility

CBOE Market Volatility Index (VIX)

Leo P. Grohowski Executive Vice President Chief Investment Officer BNY Mellon Wealth Management

Leo Grohowski is chief investment officer of BNY Mellon Wealth Management. He leads all investment strategy and investment management functions for the wealth management organization. Mr. Grohowski joined BNY Mellon in 2007 and has more than 30 years of industry experience. Previously, he was with US Trust, Bank of America, where he was chief investment officer, responsible for investment solutions and the end-to-end investment process, including portfolio management and investment strategy for Private Wealth Management clients. Prior to his role at US Trust, he was the chief investment officer for Deutsche Bank in the Americas, overseeing more than $250 billion in assets. From 1999 to 2002, Mr. Grohowski was chief investment officer of Deutsche Bank Private Banking, serving as chairman of the Global Markets Strategy Committee and Domestic Investment Strategy group, and head of Investment Products and Services for the DB Alex Brown unit. In 1996, Mr. Grohowski joined Bankers Trust where he served as a senior trust investment officer of the Private Bank and head of the U.S. Investment Strategy group. He was with HSBC Asset Management from 1988 to 1996 and was named chief investment officer in 1993, after heading the U.S. Equities group from 1988 to 1993.

Education

• Bachelor’s degree, Drew University • Master of Business Administration,

New York University’s Stern School of Business

Community Involvement • Board of Trustees and Investment Committee chair,

Drew University • Board Member and Vice Chair, Far Hills Country Day School

• Member, Investment Committee, Blair Academy

Executive Responsibilities • Member, BNY Mellon’s Operating Committee

• Benefits Investment Committee • Chair, Wealth Management Investment Policy Committee

• Member, Compliance, Ethics and Conflicts Committee • Member, Investment Ethics Council

38

39

Disclaimer

The information provided is for illustrative/educational purposes only. All investment strategies referenced come with investment risks, including loss of value and/or loss of anticipated income. This material is not intended to constitute investment advice. Effort has been made to ensure that the material presented herein is accurate at the time of publication. However, this material is not intended to be a full and exhaustive explanation of investments options available. The information discussed herein may not be applicable to or appropriate for every investor and should be used only after consultation with professionals who have reviewed your specific situation. ©2015 The Bank of New York Mellon Corporation. All rights reserved.