leveraging quandl

TRANSCRIPT

Presenters: Tammer Kamel (CEO)

Brian Risk (head of marketing)

Data is everywhere…

Data is Everywhere

• Difficult to find (all over the web, hard to find on a site even if you know the site)

• Non-standard download formats, random filenames, variable data formatting

• Typically no API support

(BUT THAT’S THE PROBLEM)

One Access Point

12 Million Data Sets

Over 500 Data sources

Gold, oil, GDP, Gini index, splits, dividends, literacy rates, earnings surprises, China core fundamentals, home values,

continuous futures, FOREX rates, diabetes rates, twitter account sats, Bitcoin, coal, natural gas, energy consumption,

global yield curves, population data, stock fundamentals, Shanghai futures, options volatilities, oil production by

country, iridium prices, federal reserve economic data, corn, startup valuations, venture capital, dry bulk freight forward agreements, industrial metals, cereals, sports, alexa ranking

Futures, Stocks, Options, Global !Economics, Housing, Education, Health!

All Quandl Data is

• Accessible in the format that works best for you

• Accessible with the tools that work for you

• Easily findable

• Verifiably Sourced

Getting Data as easily as possible

API

A Host of Libraries

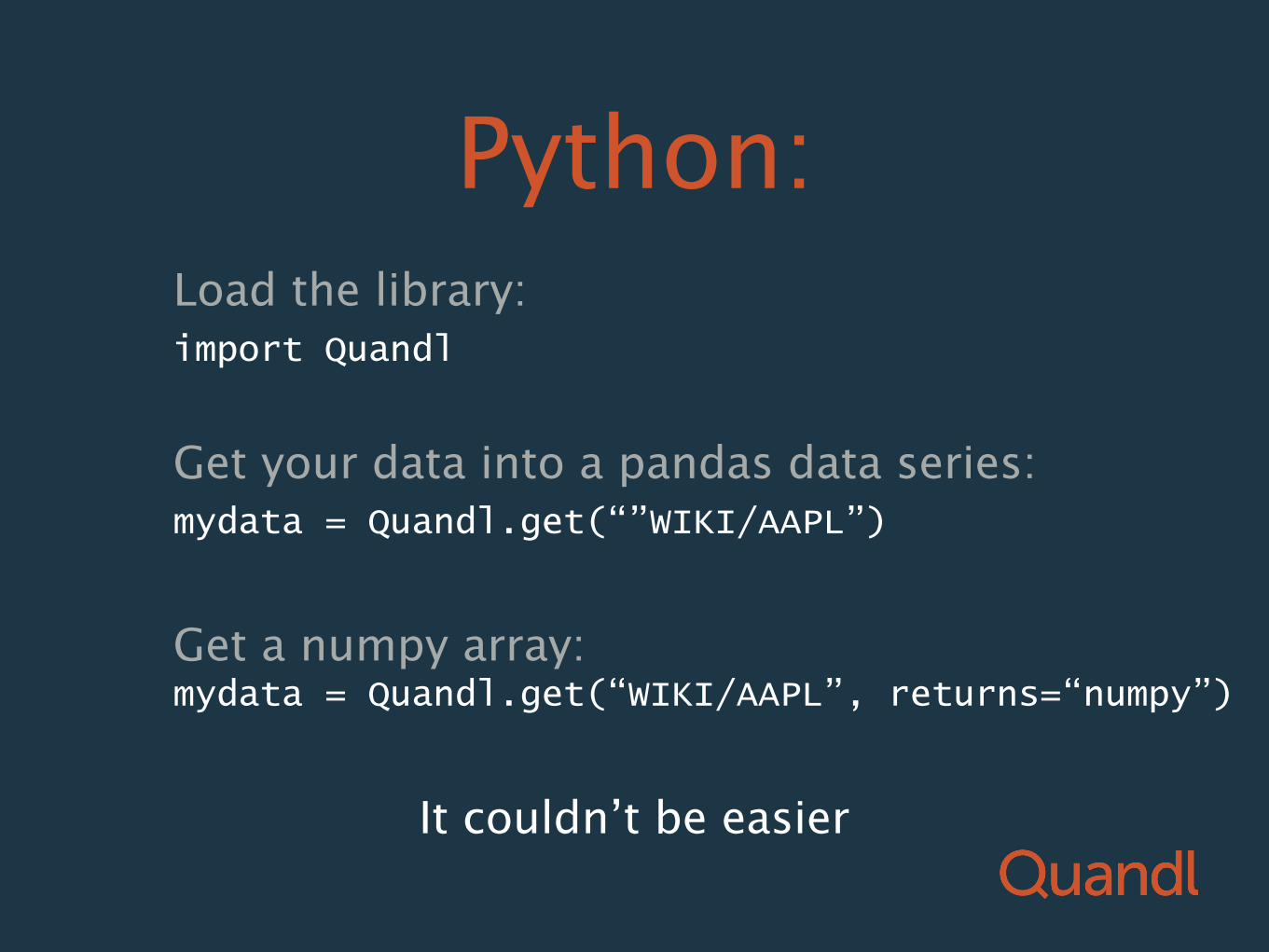

Python:

Get your data into a pandas data series:

Get a numpy array:

Load the library:

It couldn’t be easier

import Quandl

mydata = Quandl.get(“”WIKI/AAPL”)

mydata = Quandl.get(“WIKI/AAPL”, returns=“numpy”)

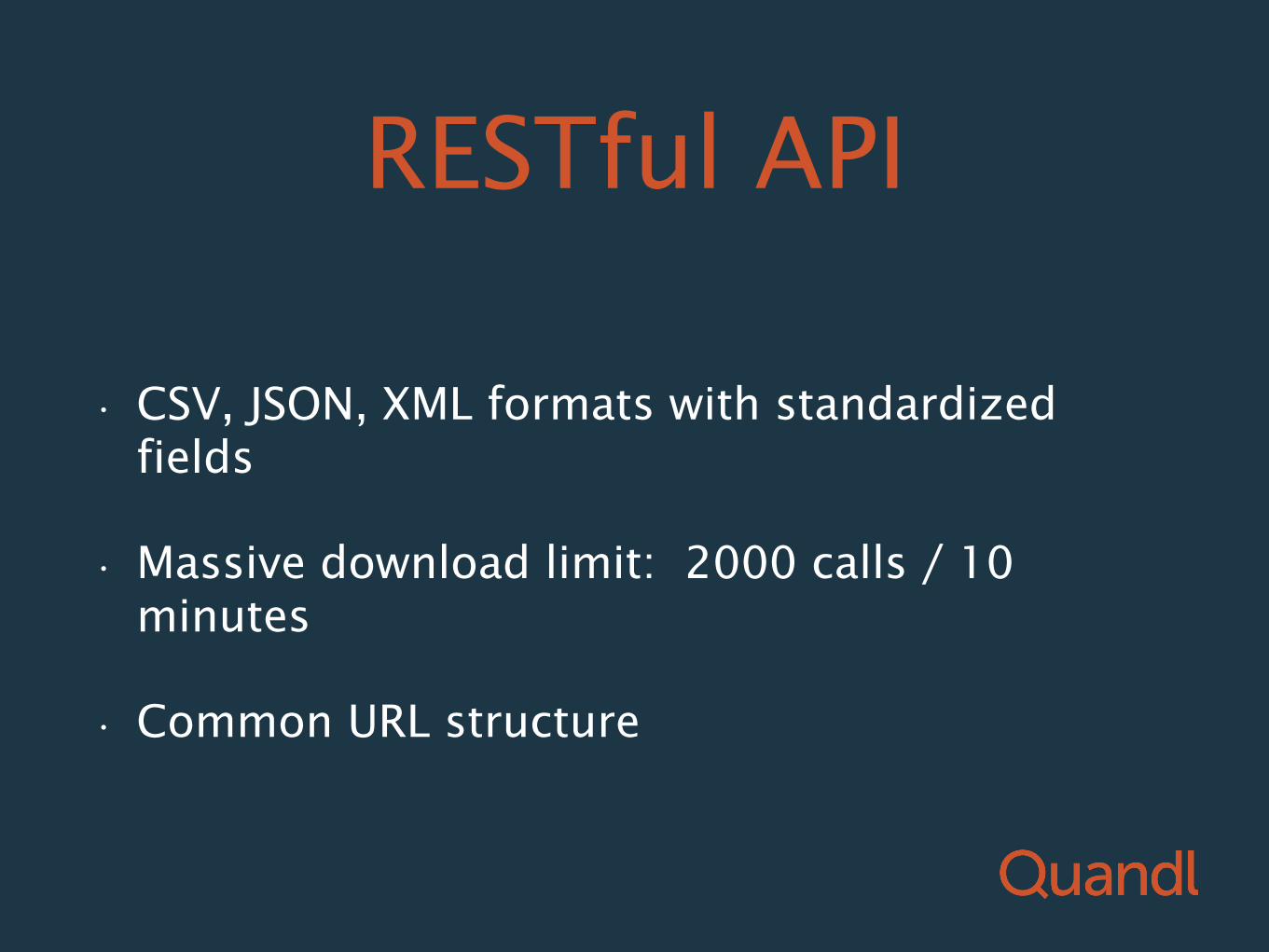

RESTful API

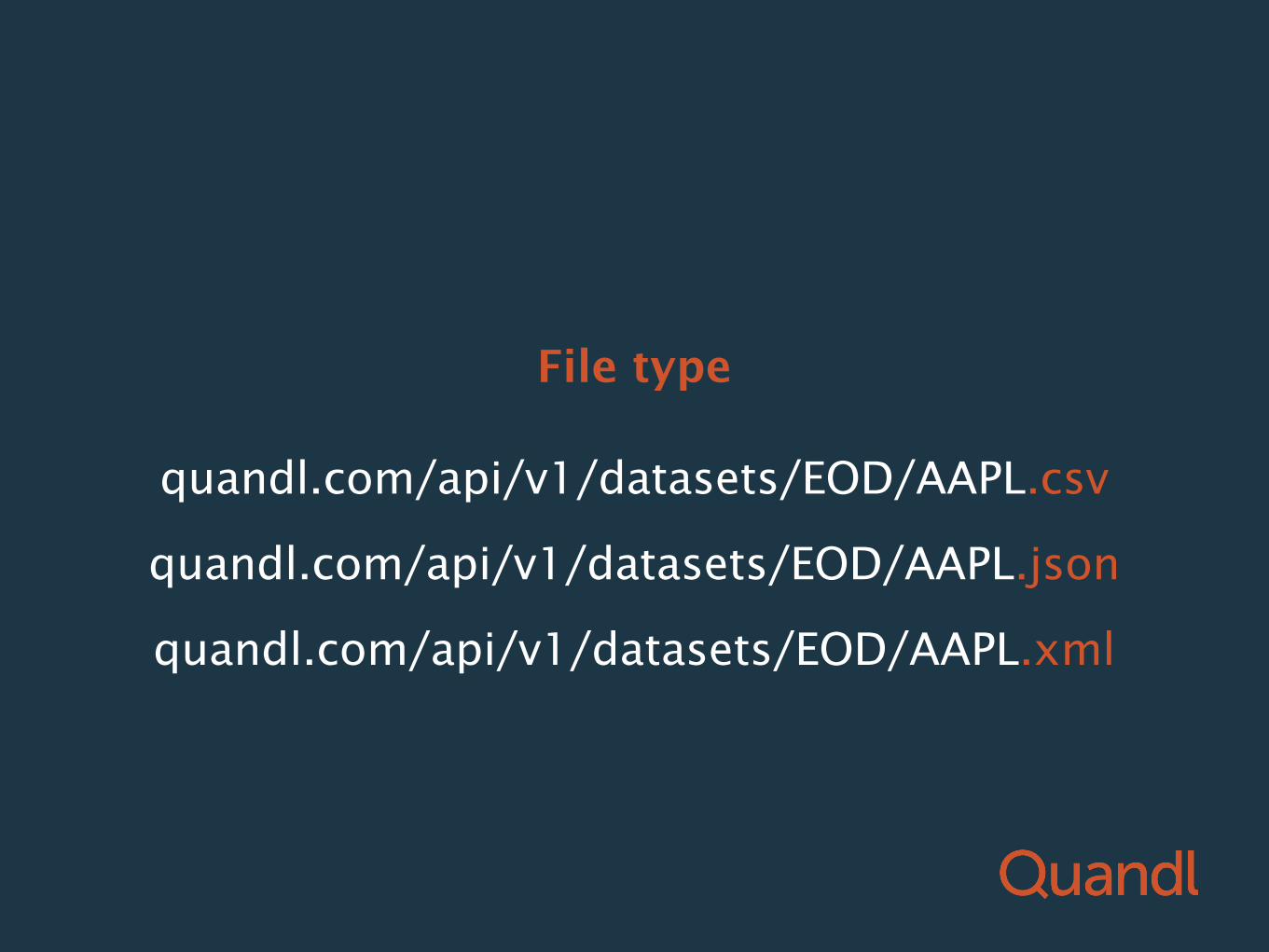

• CSV, JSON, XML formats with standardized fields

• Massive download limit: 2000 calls / 10 minutes

• Common URL structure

URL structure

quandl.com/data/UNDATA/GEN_LITR_SRB

Literacy rates in Serbia:

quandl.com/data/ZILLOW/METRO_2BEDROOM_NEWYORKNY

Price of 2 Bedroom homes in NYC:

quandl.com/data/LBMA/GOLD

London gold price:

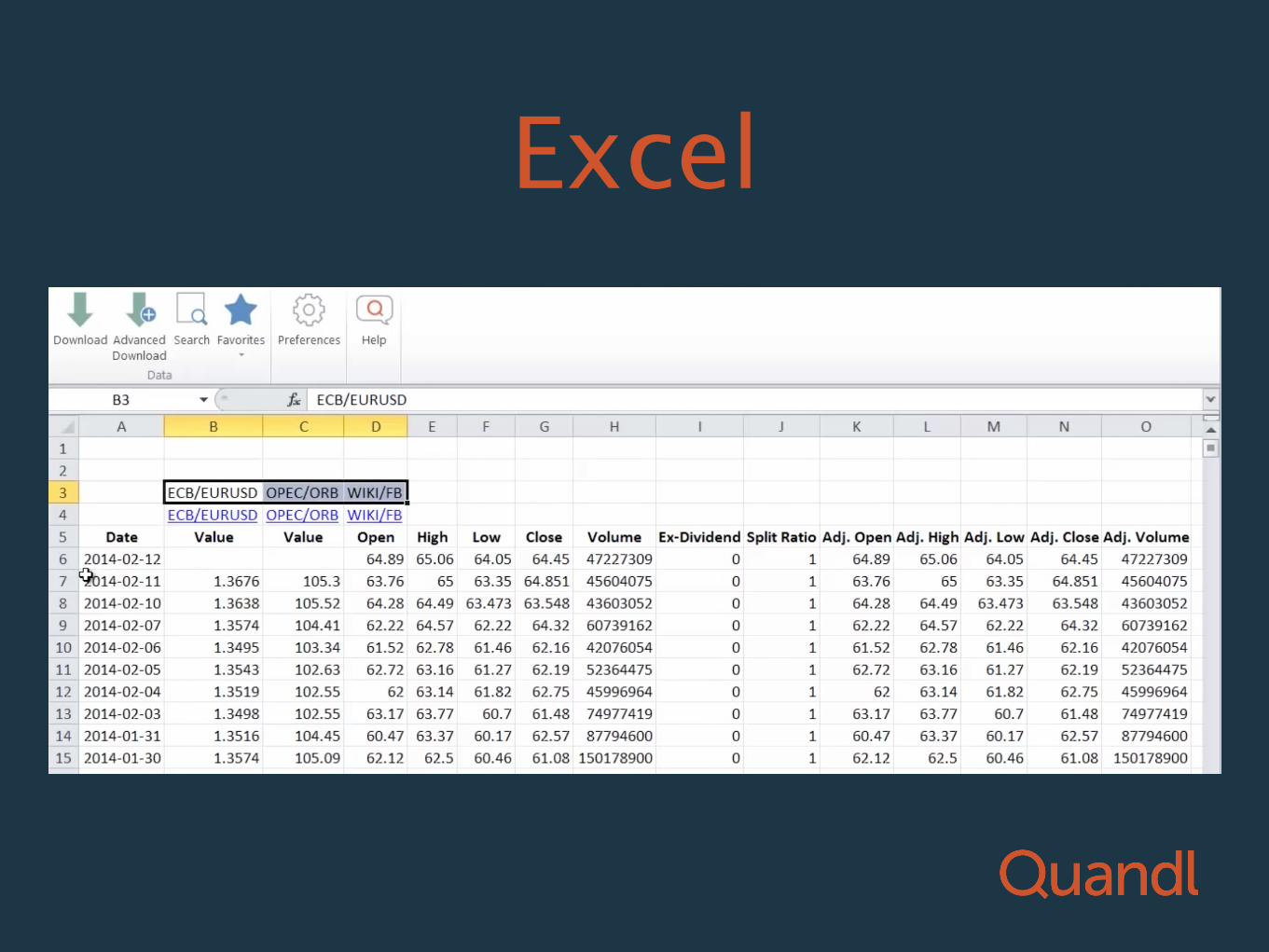

Excel

Bulk Downloads

• Full database all at once.

• Accessible via API or download link

• Available for all premium data sets

Premium Data

Premium Data

• 5 million professional grade financial data sets

• valuable, high-alpha data

• Free previews for logged in users

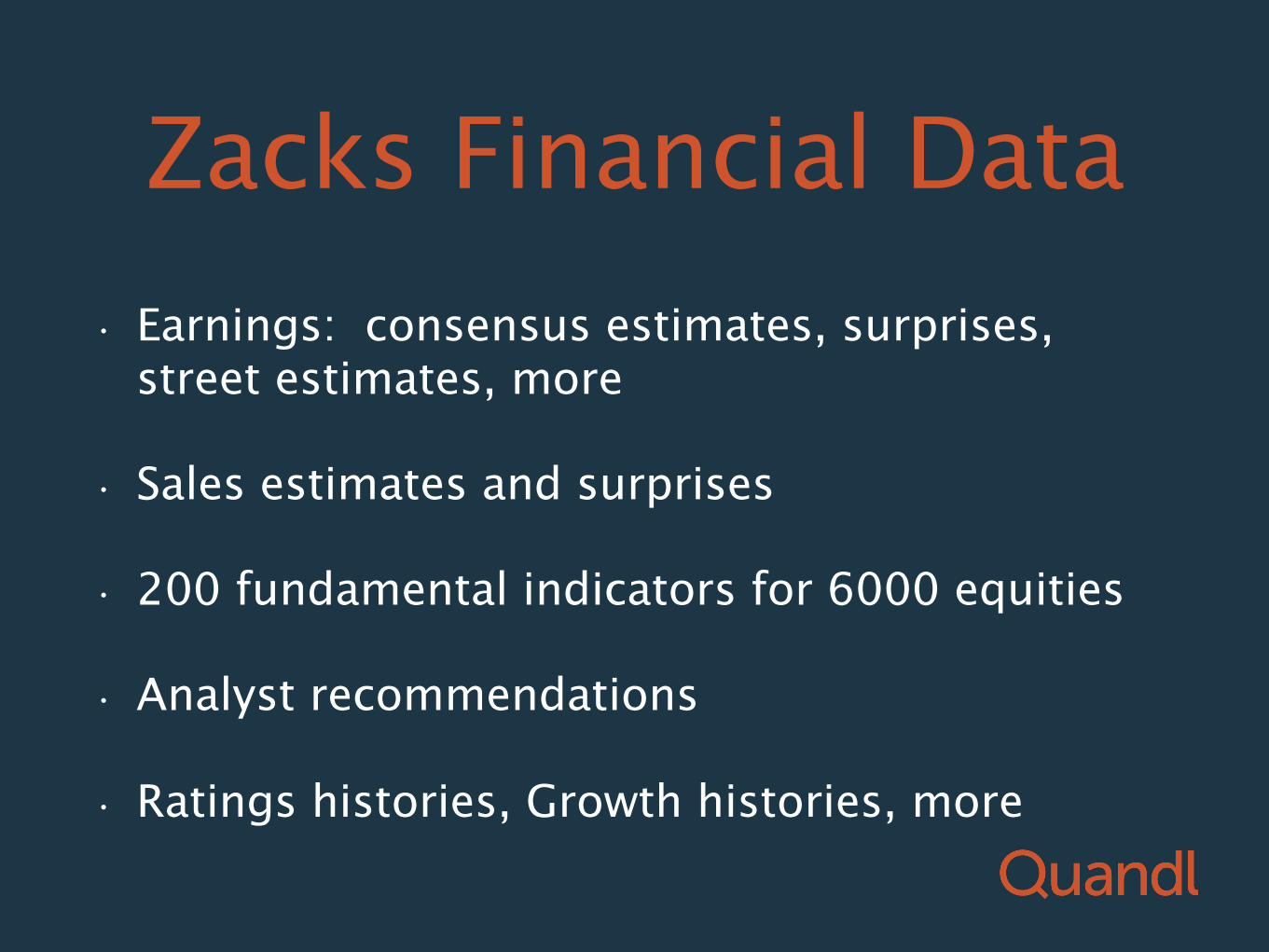

Zacks Financial Data

• Earnings: consensus estimates, surprises, street estimates, more

• Sales estimates and surprises

• 200 fundamental indicators for 6000 equities

• Analyst recommendations

• Ratings histories, Growth histories, more

Using Quandl

with Quantopian

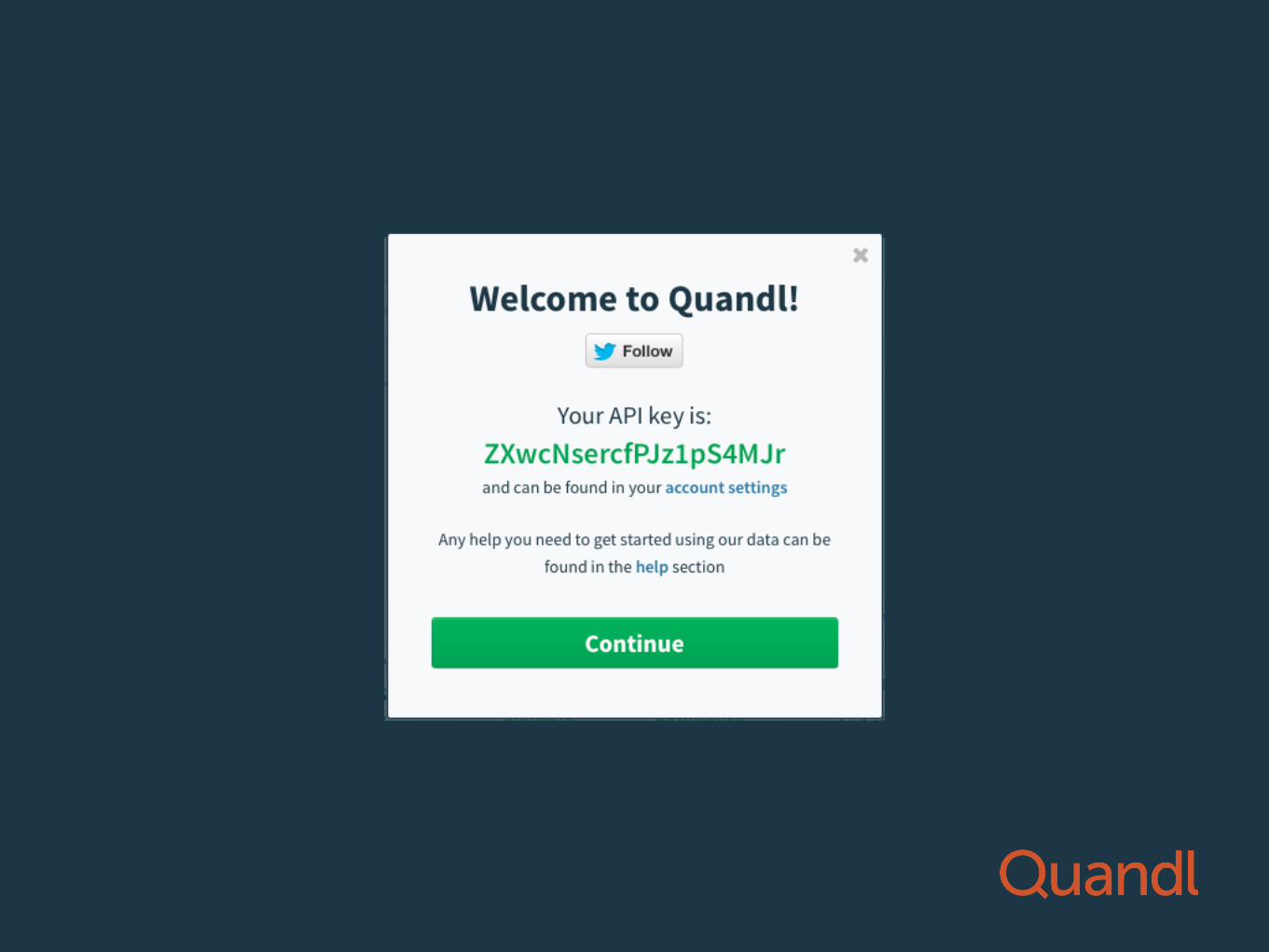

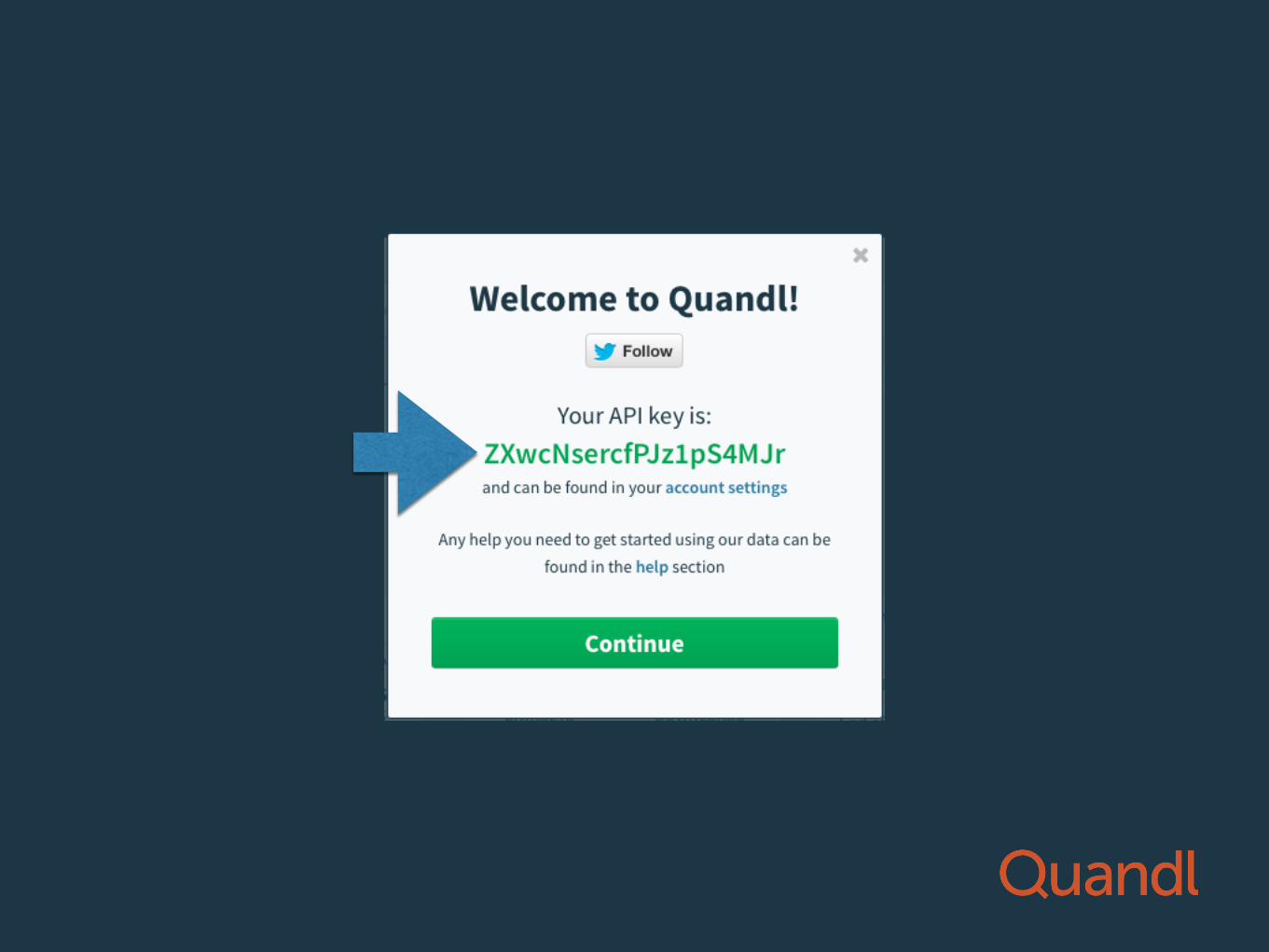

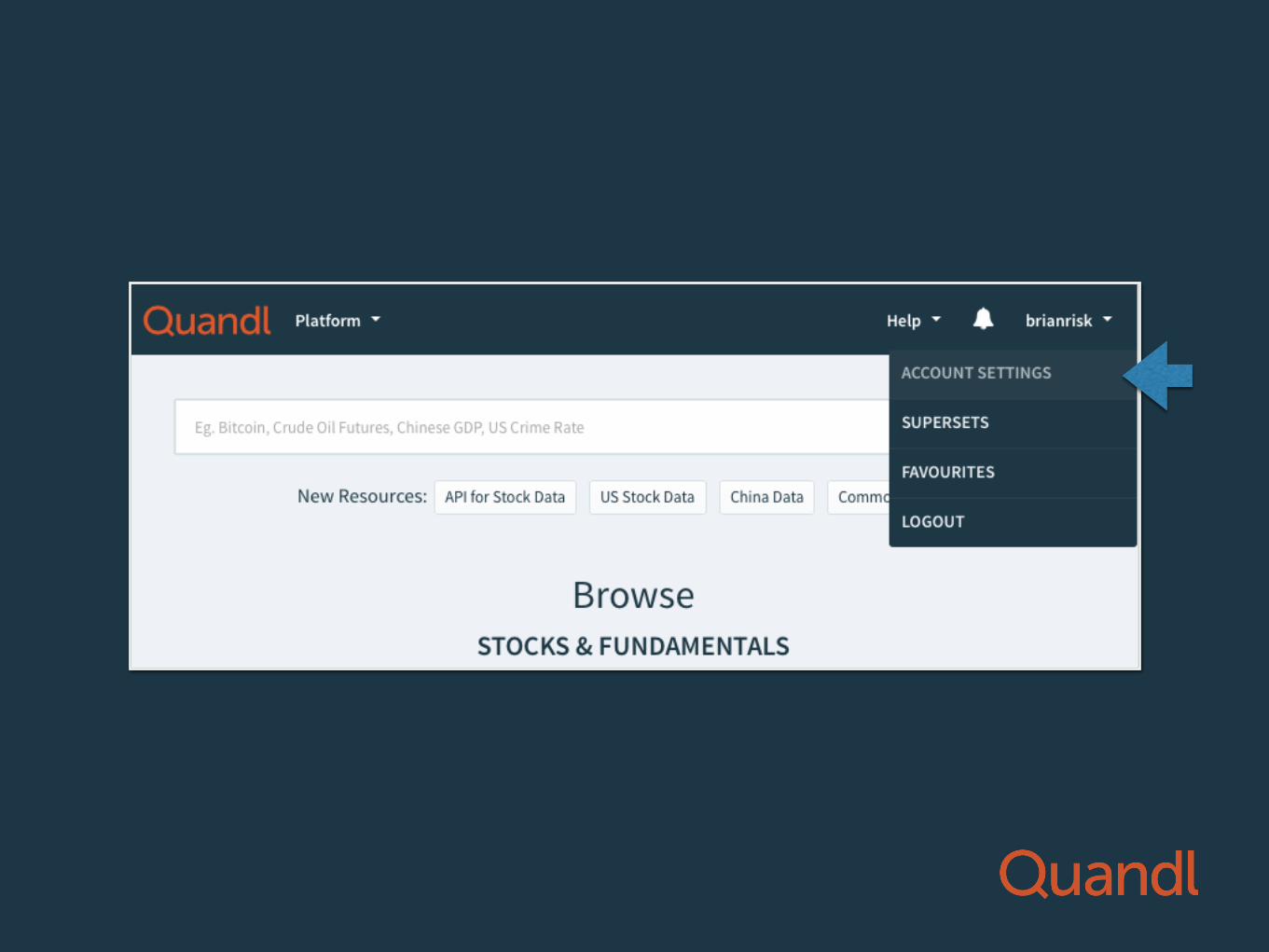

STEP #1 GET YOUR API KEY

Getting your API key

• FREE

• 2000 API calls / 10 minutes

• Free previews and downloads of premium data

go to: quandl.com

Click here

Getting the data

Downloading by URL

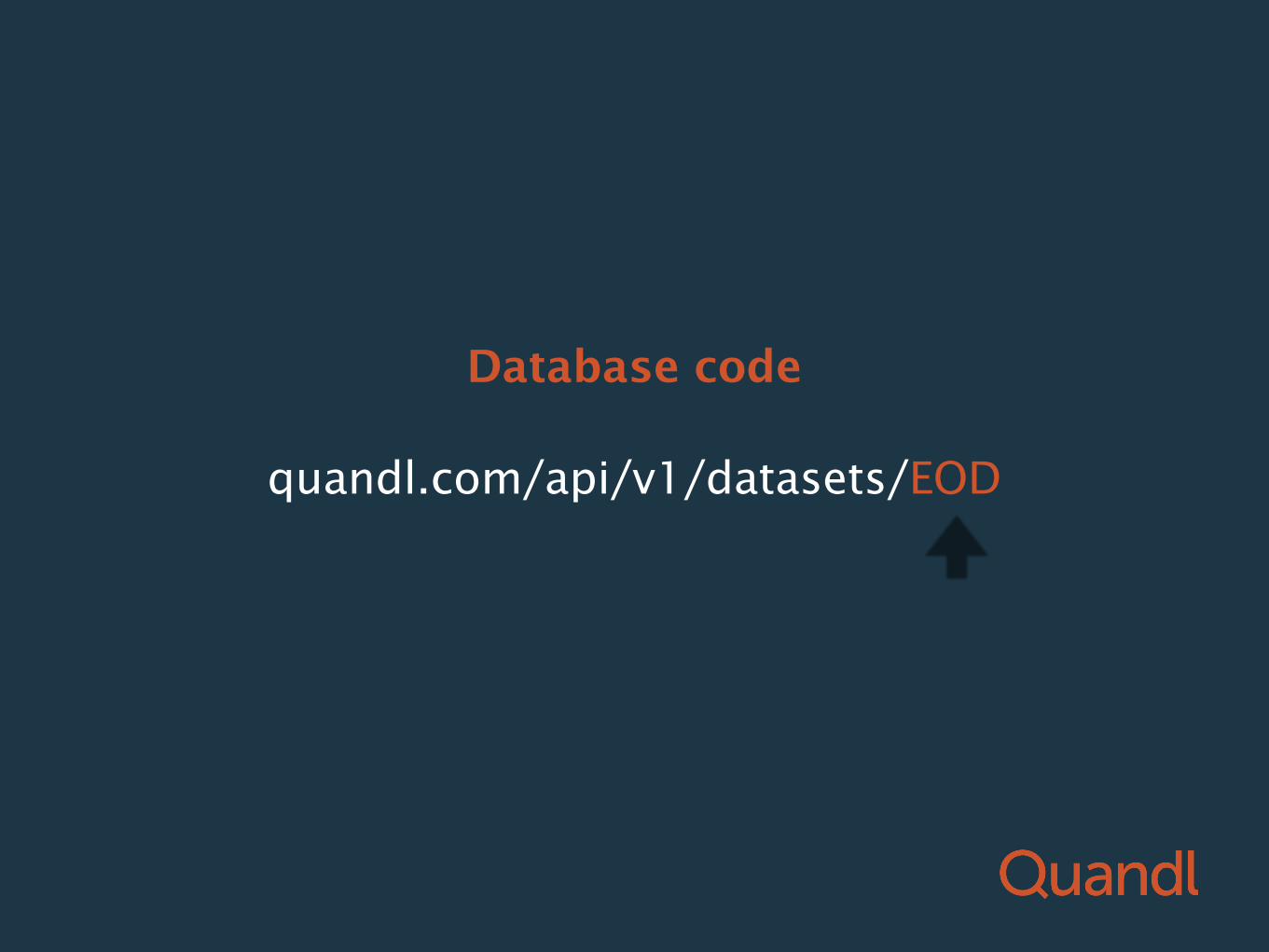

quandl.com/api/v1/datasets/

Standard beginning part

quandl.com/api/v1/datasets/EOD

Database code

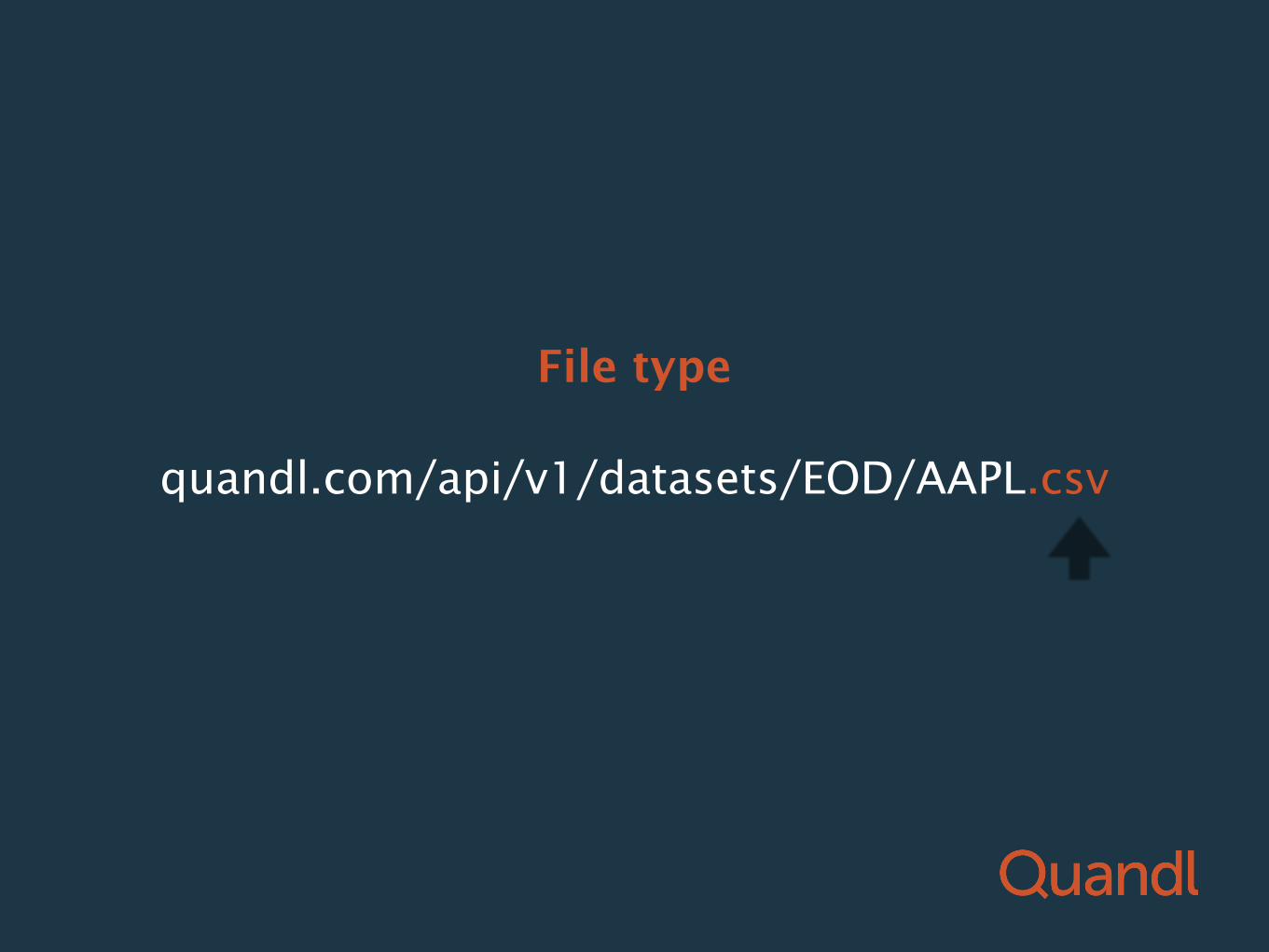

quandl.com/api/v1/datasets/EOD/AAPL

Data set code

quandl.com/api/v1/datasets/EOD/AAPL.csv

File type

quandl.com/api/v1/datasets/EOD/AAPL.csv

File type

quandl.com/api/v1/datasets/EOD/AAPL.json

quandl.com/api/v1/datasets/EOD/AAPL.xml

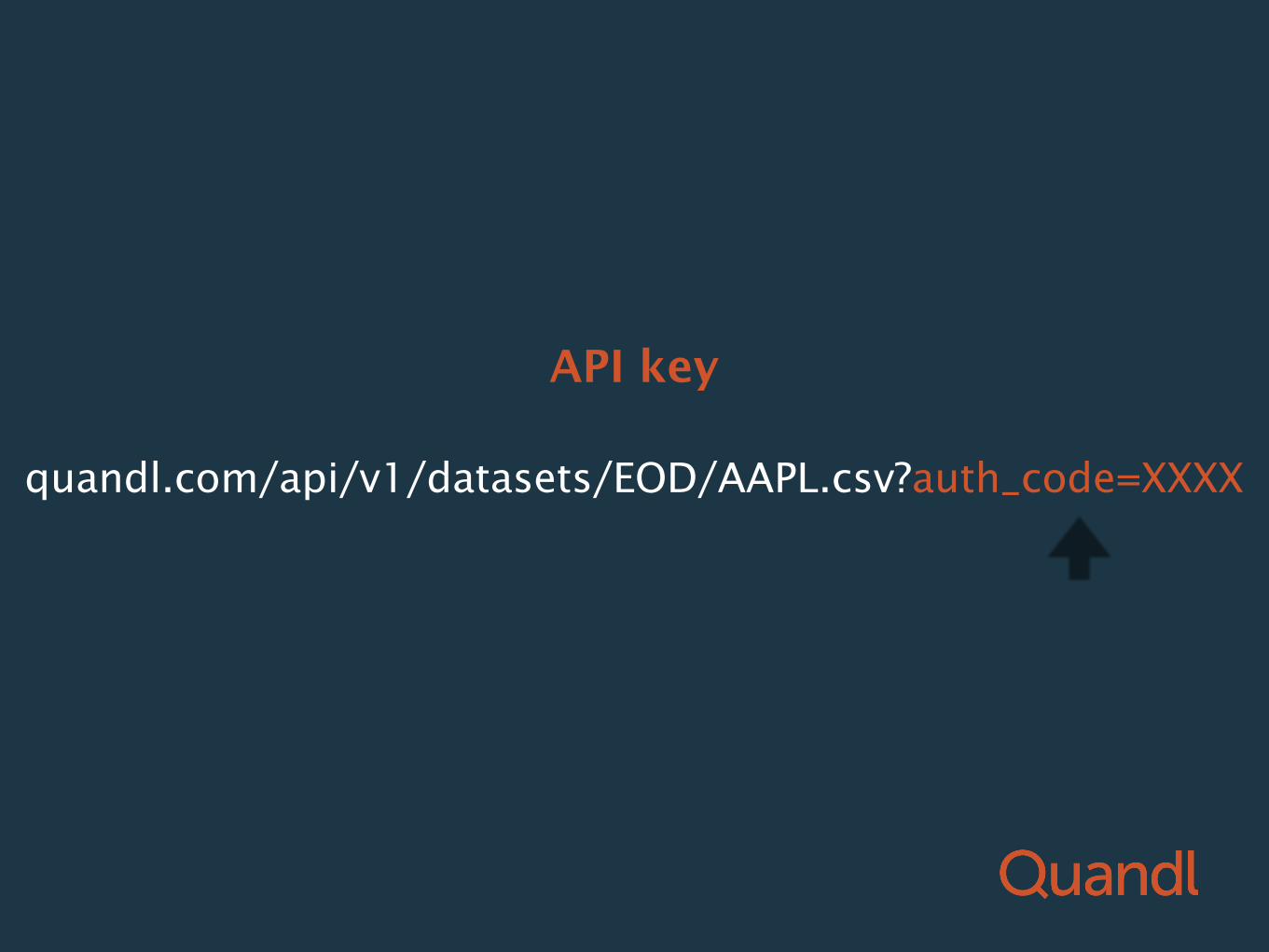

quandl.com/api/v1/datasets/EOD/AAPL.csv?auth_code=XXXX

API key

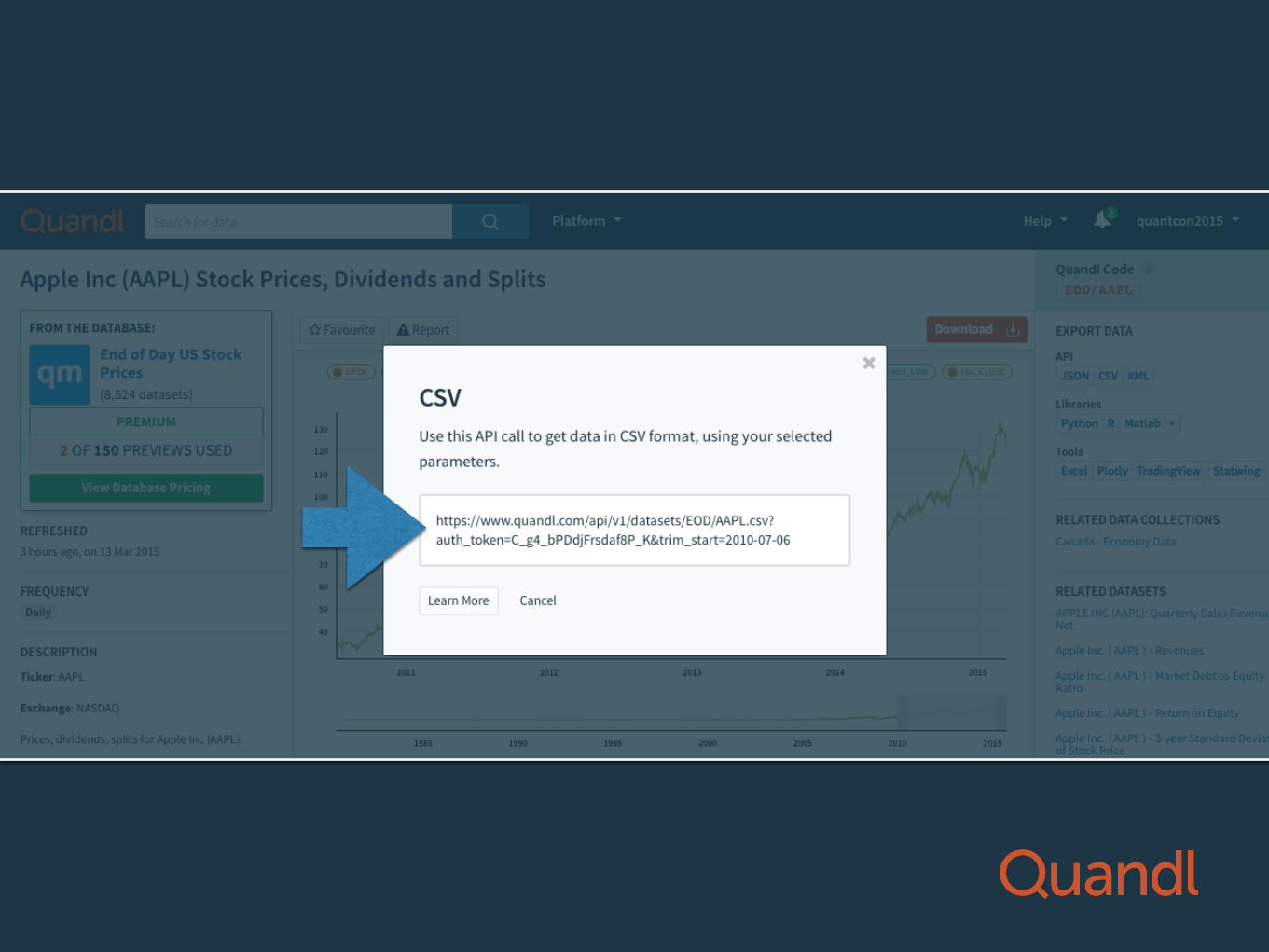

Too hard?

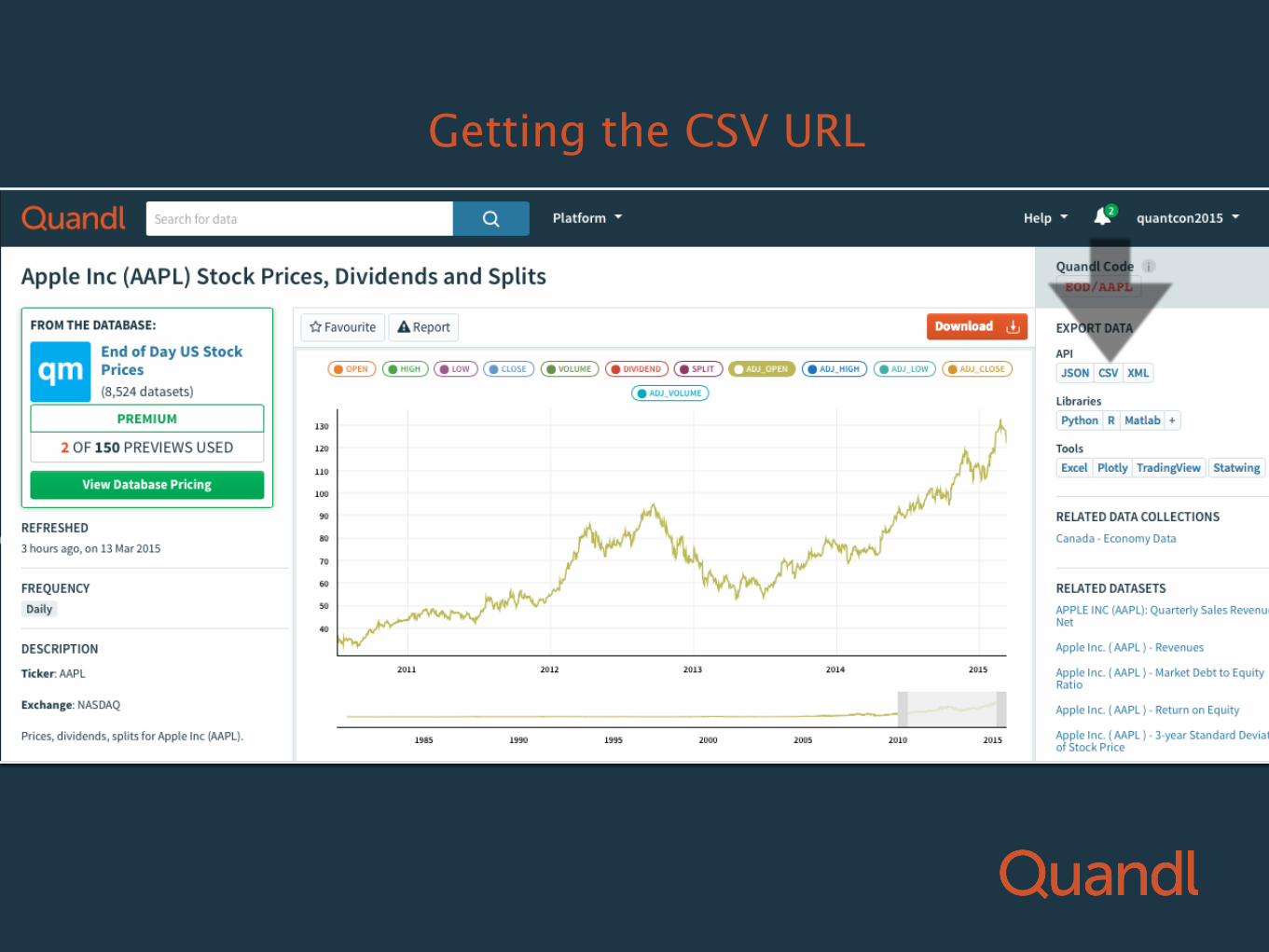

Getting the CSV URL

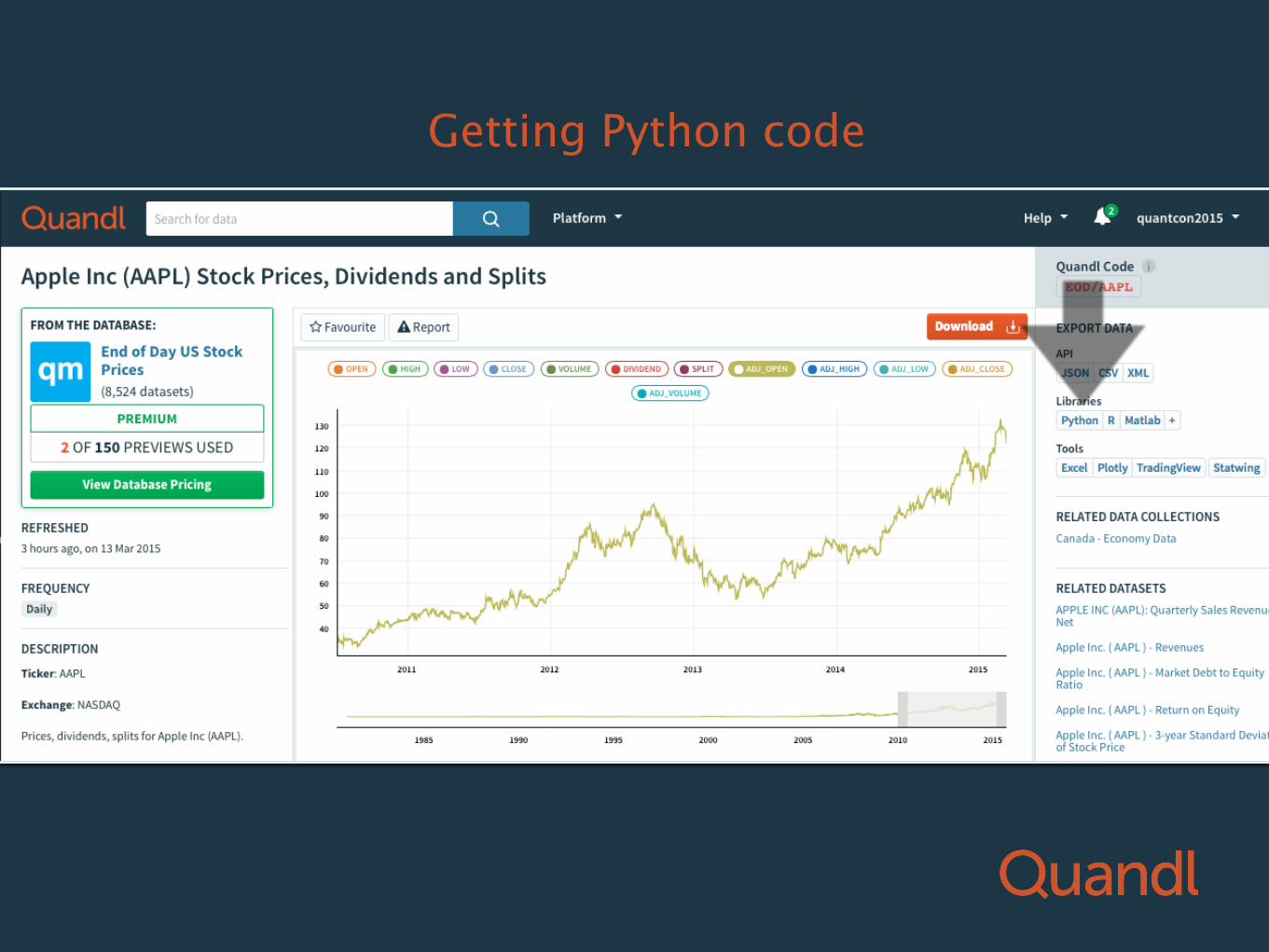

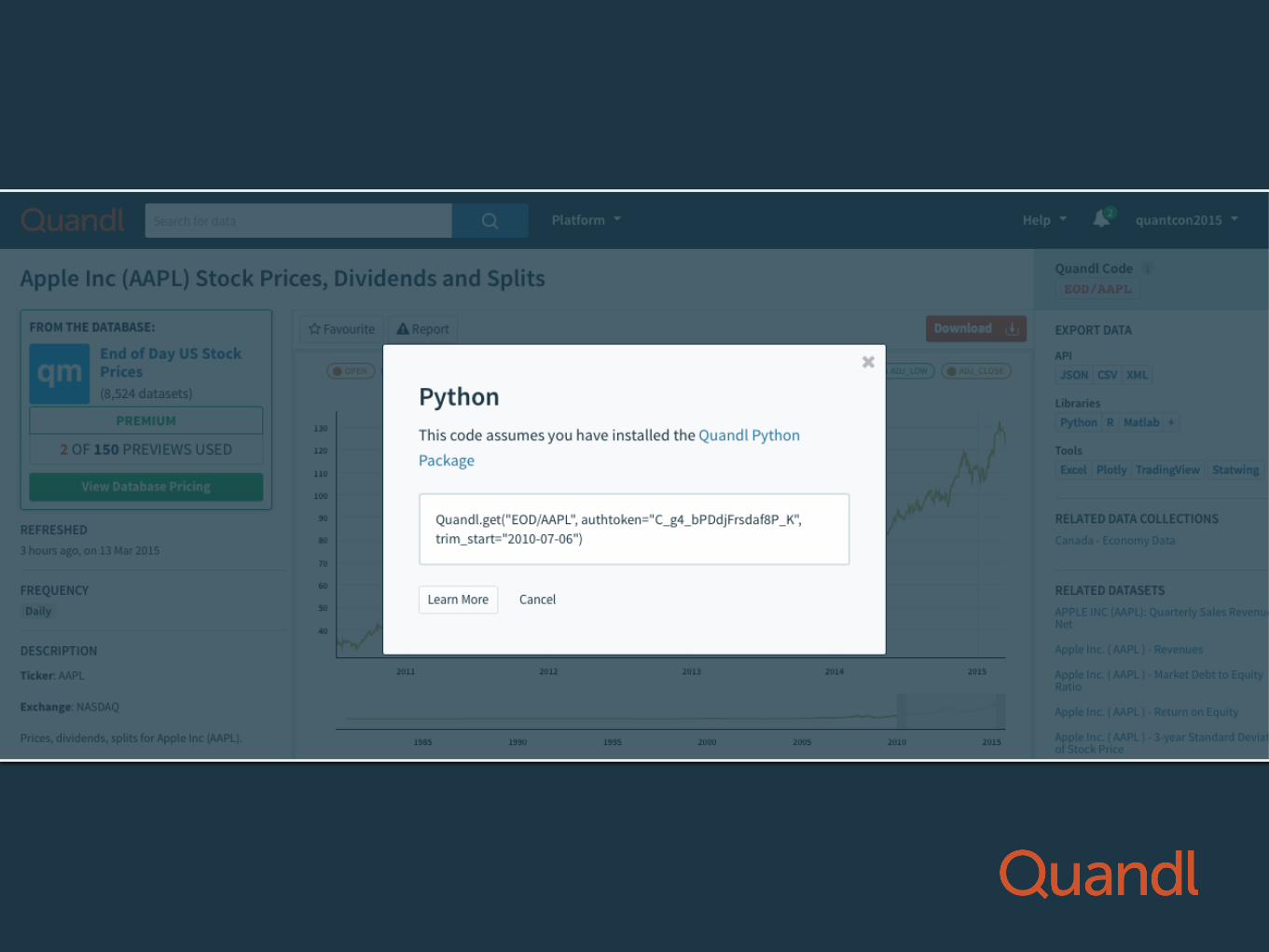

Getting Python code

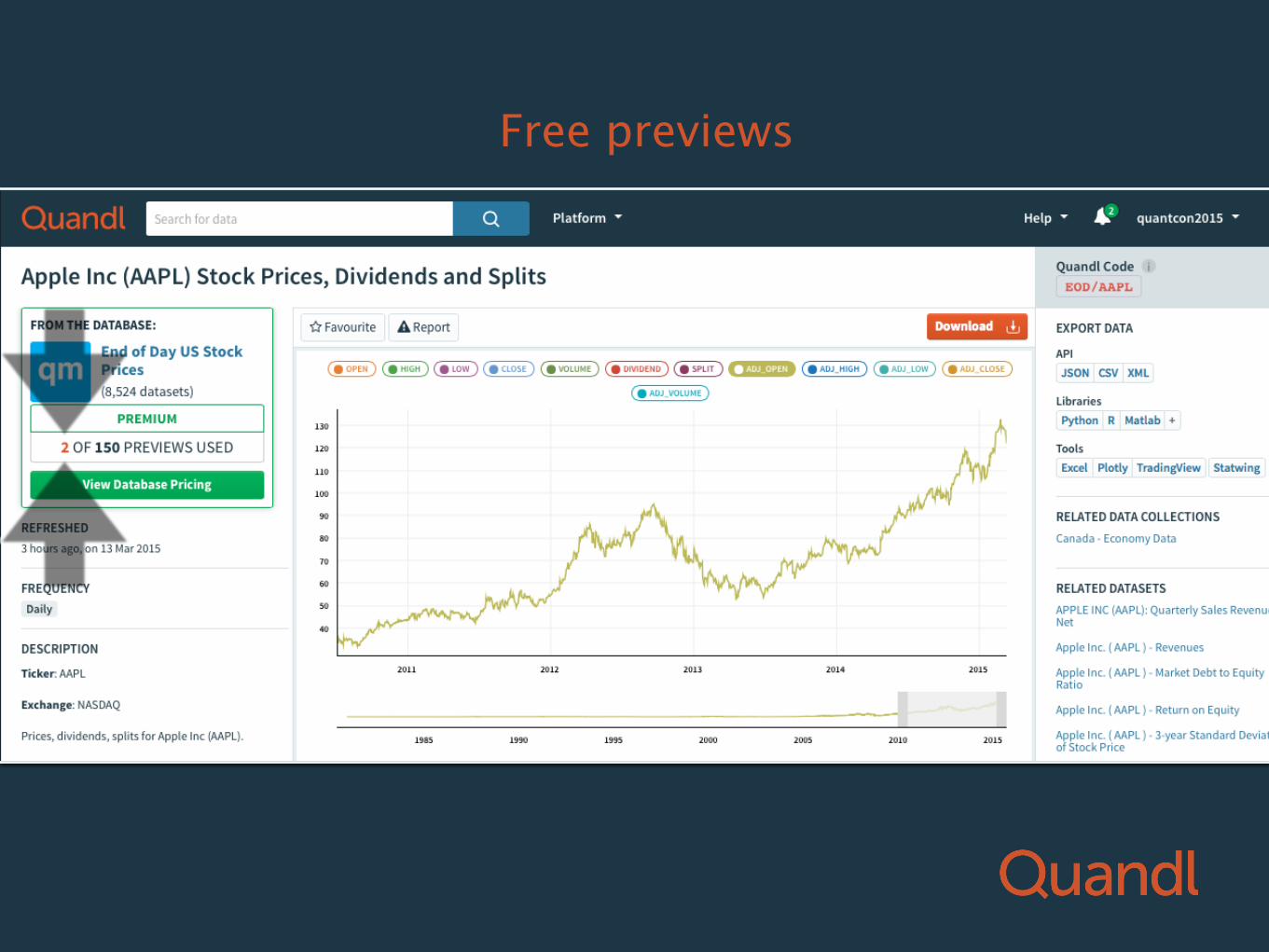

Free previews

Free previews

Hackathon

Zacks Data quandl.com/vendors/zacks

Zacks Data quandl.com/vendors/zacks

consensus earnings estimates

ratings history

long term growth history

earnings estimates history

analyst recommendations

street earnings estimates

sales surprises

earnings estimates

sales estimates

earnings announcements earnings surprises

dividends

Zacks Data quandl.com/vendors/zacks

consensus earnings estimates

ratings history

long term growth history

earnings estimates history

analyst recommendations

street earnings estimates

sales surprises

earnings estimates

sales estimates

earnings announcements earnings surprises

dividends

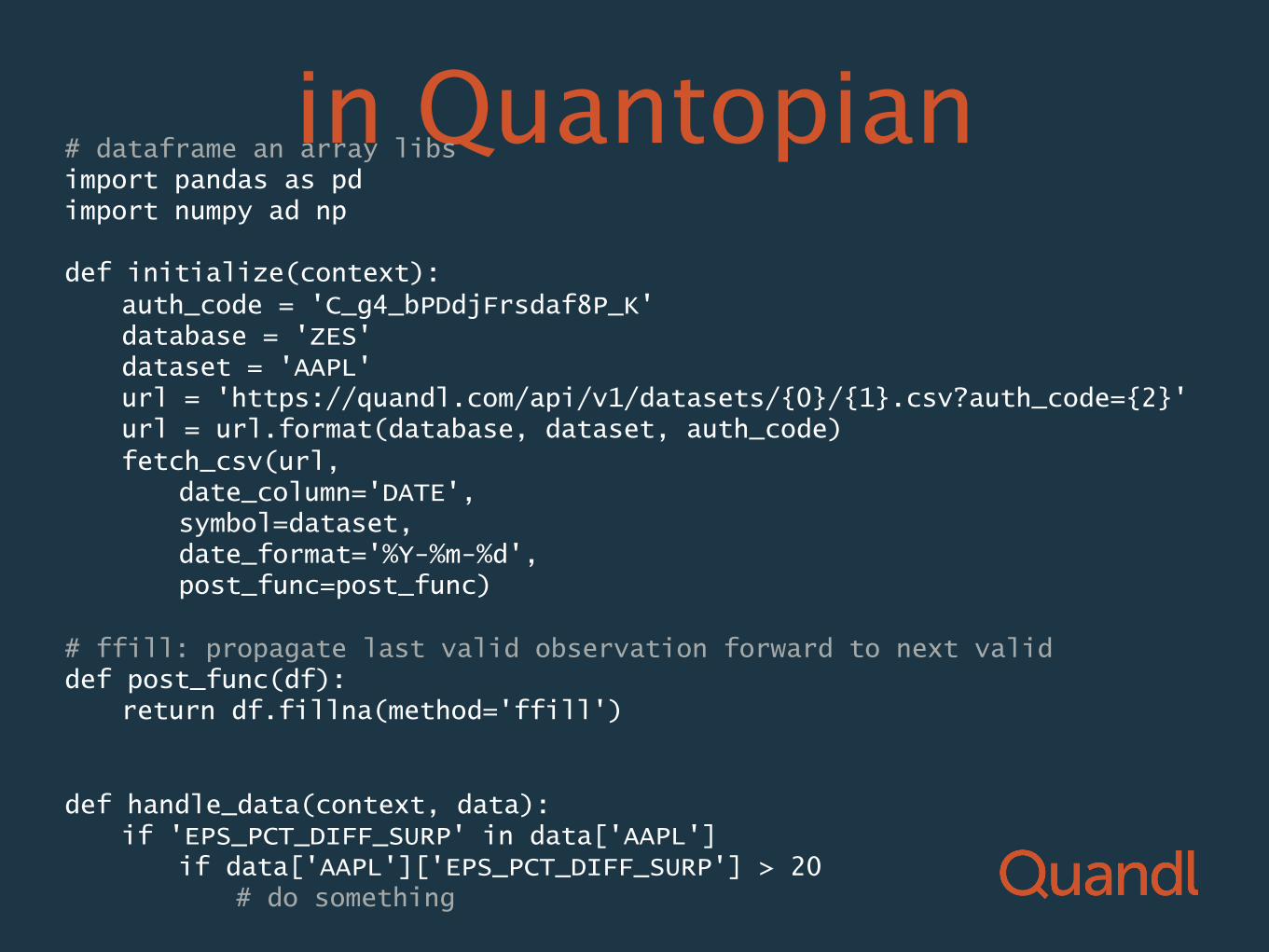

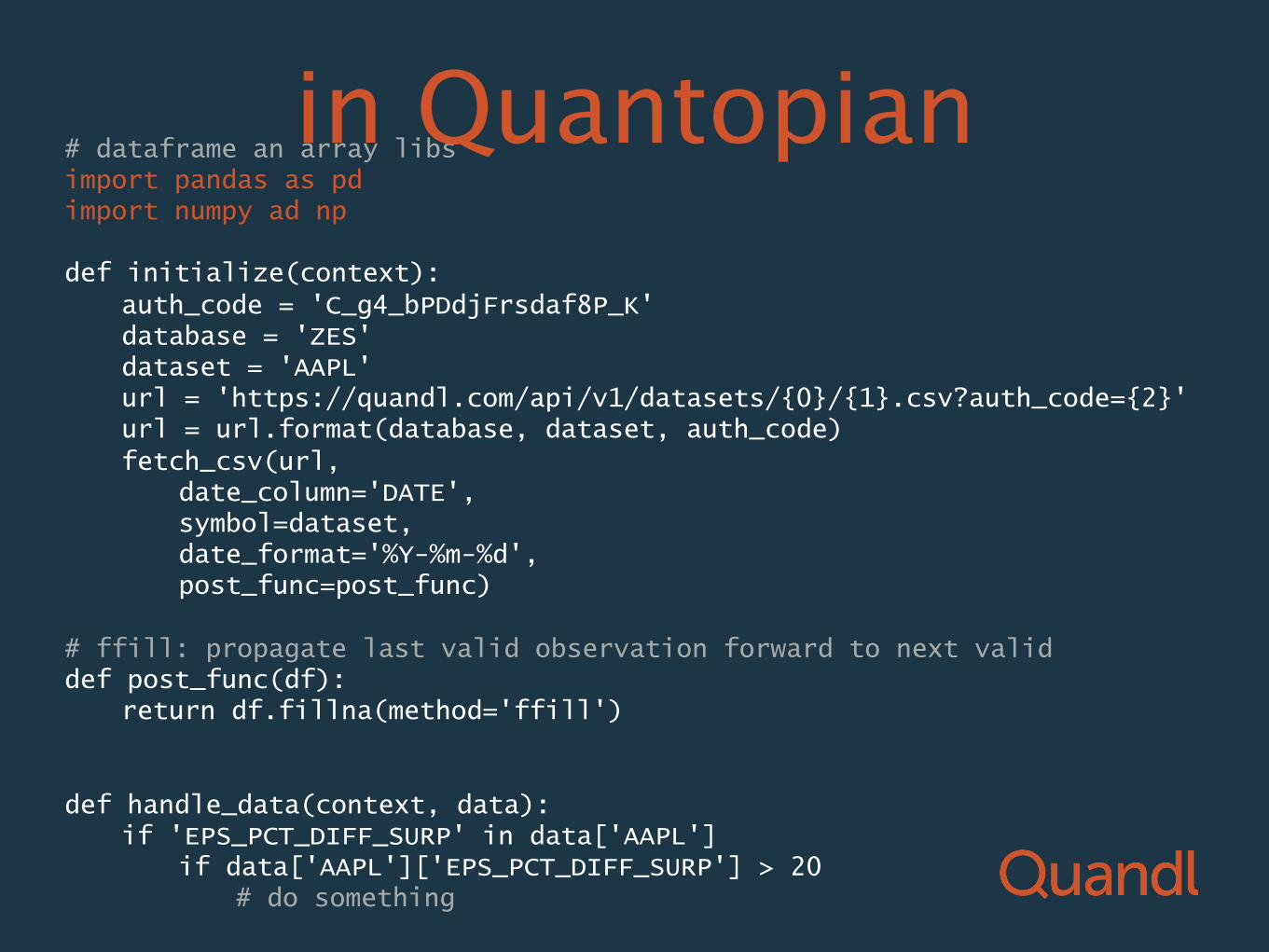

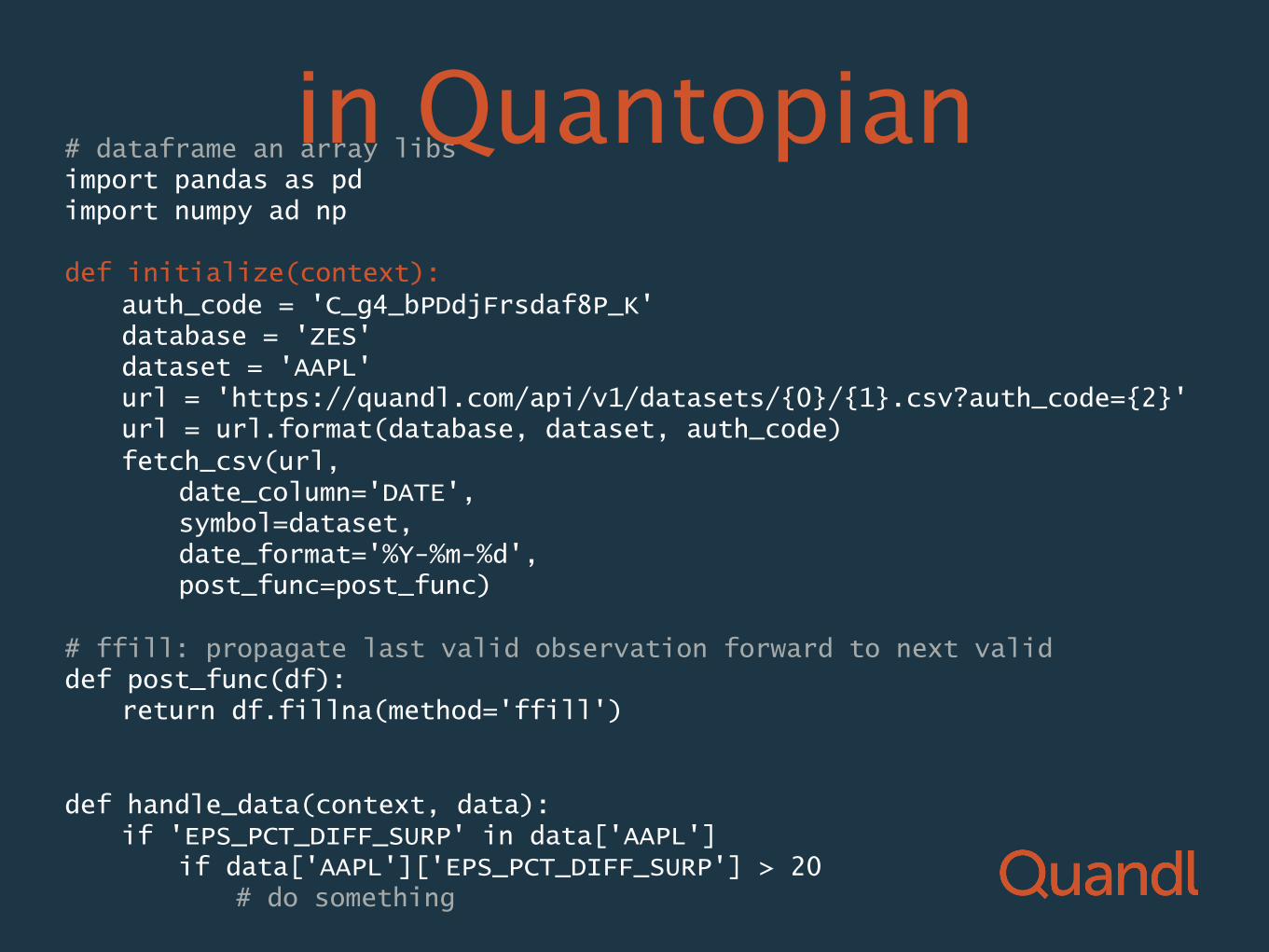

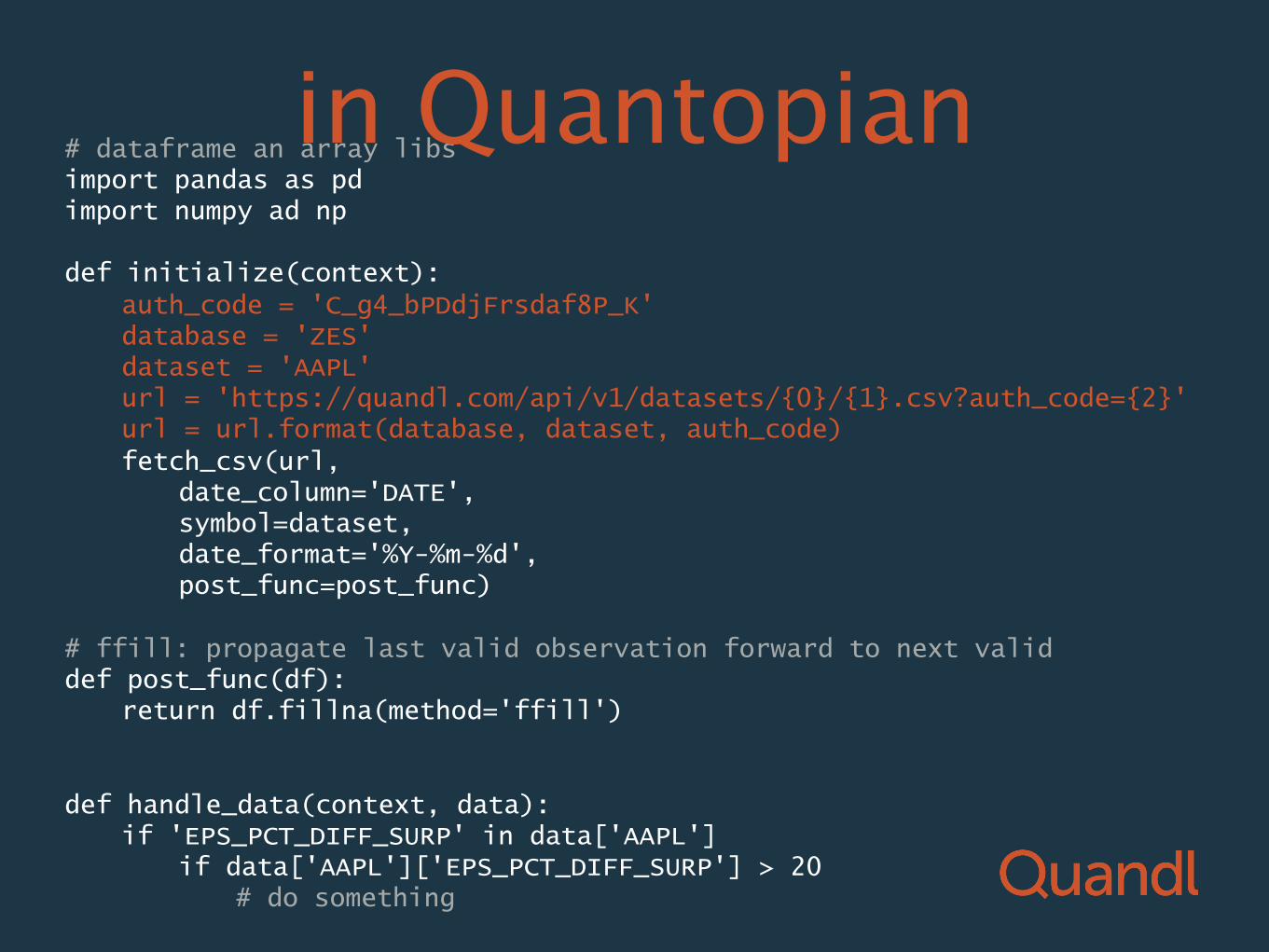

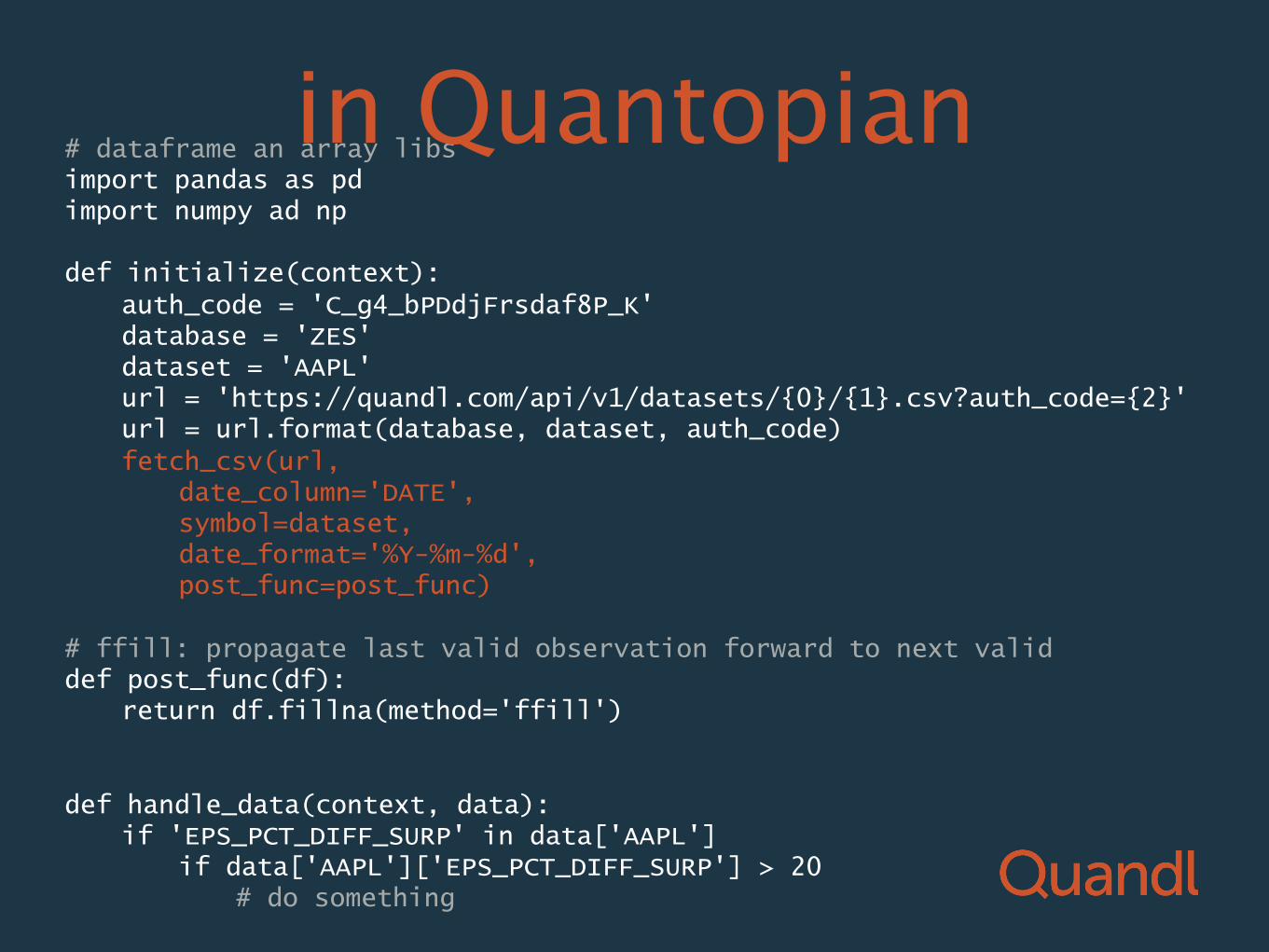

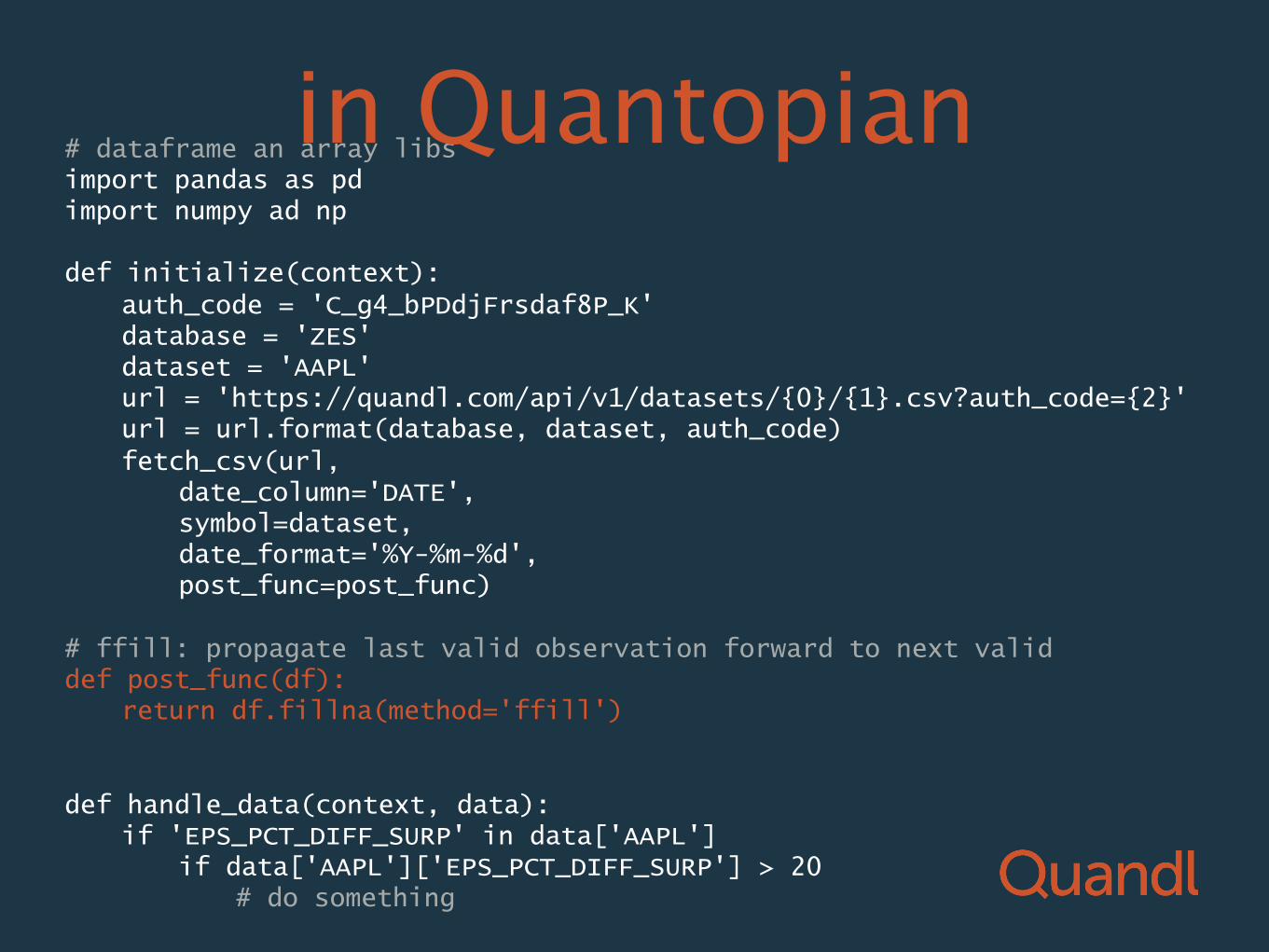

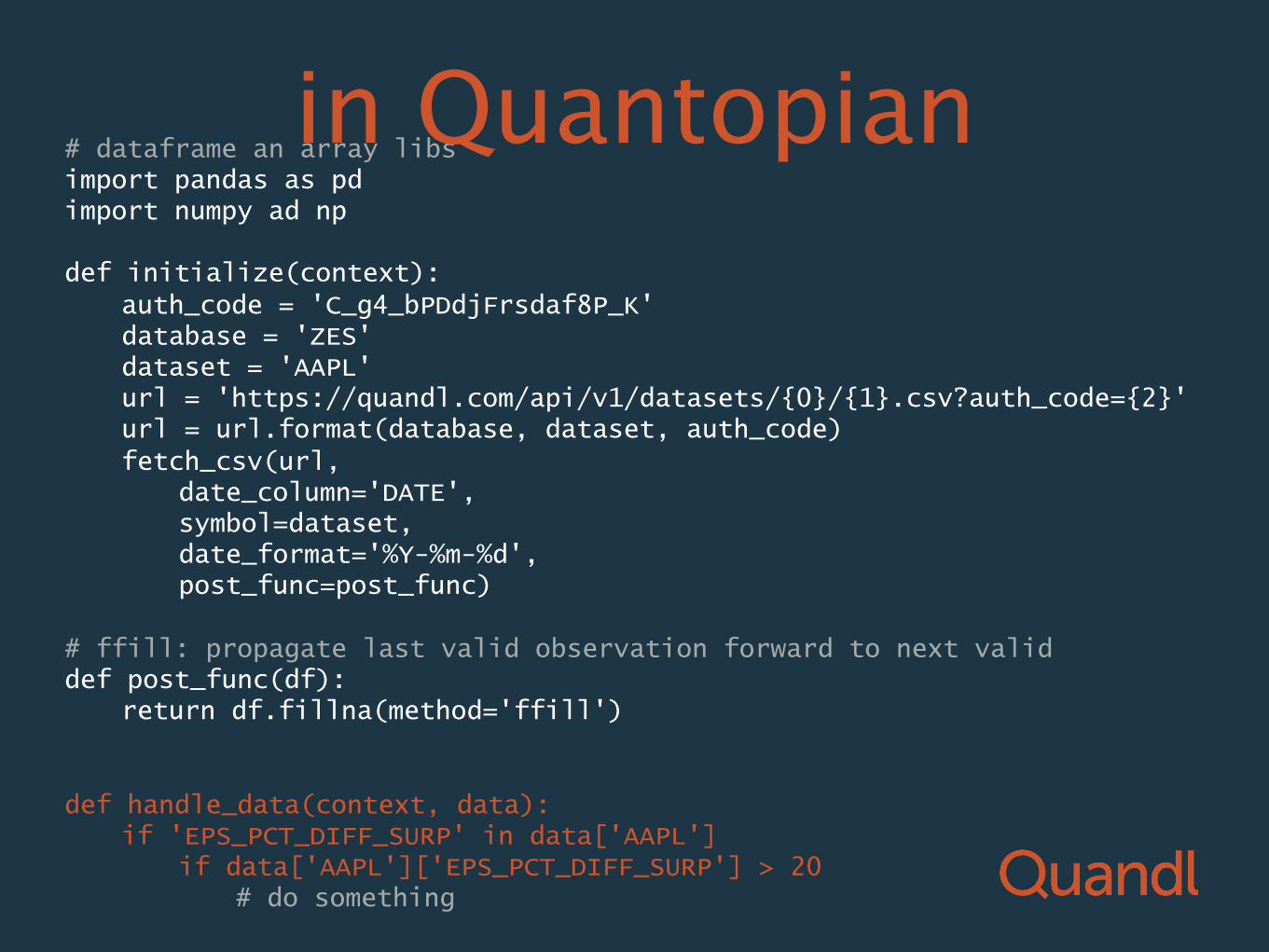

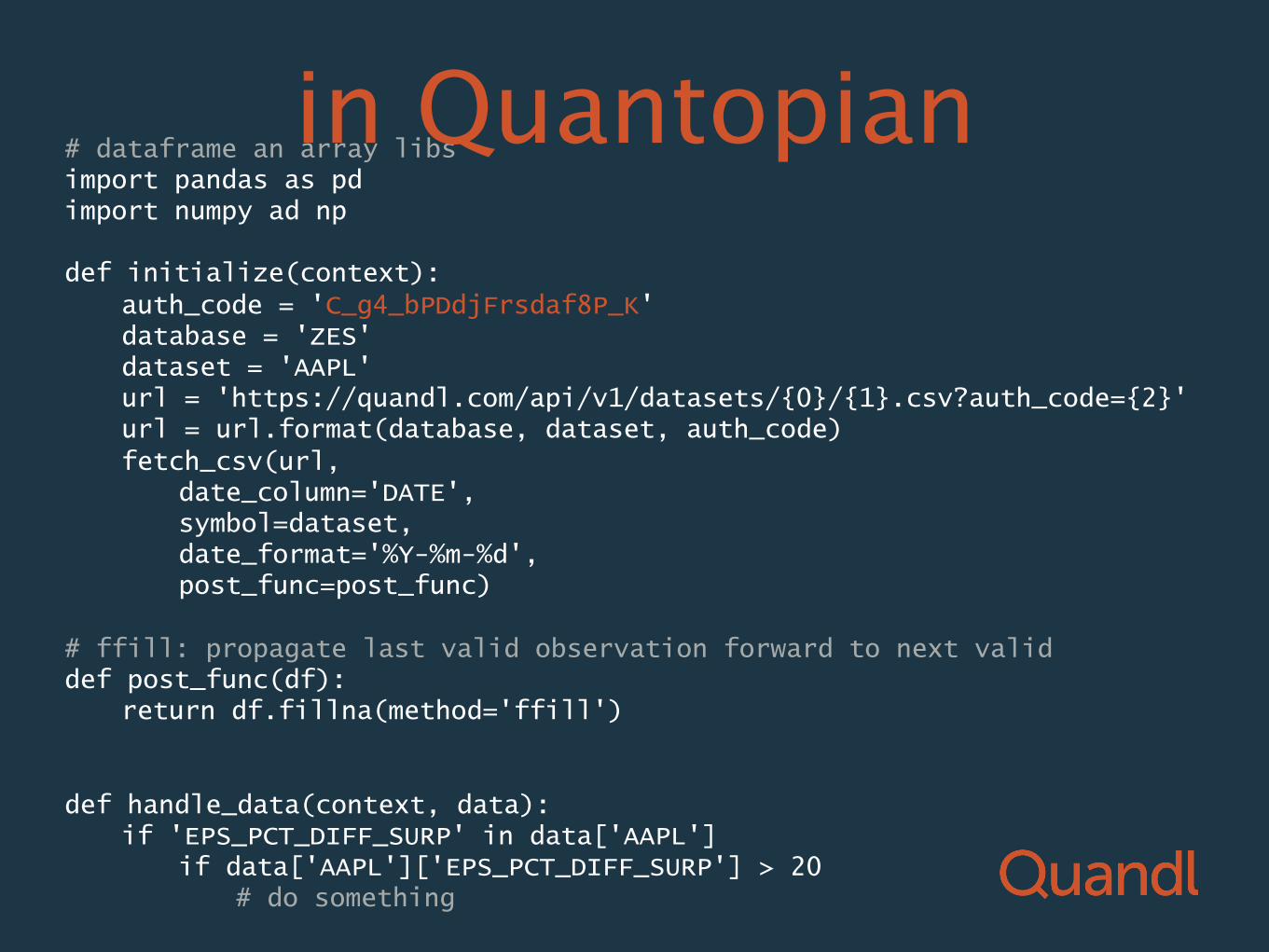

in Quantopian # dataframe an array libs import pandas as pd import numpy ad np def initialize(context):

auth_code = 'C_g4_bPDdjFrsdaf8P_K' database = 'ZES' dataset = 'AAPL' url = 'https://quandl.com/api/v1/datasets/{0}/{1}.csv?auth_code={2}' url = url.format(database, dataset, auth_code) fetch_csv(url, date_column='DATE', symbol=dataset, date_format='%Y-%m-%d', post_func=post_func)

# ffill: propagate last valid observation forward to next valid def post_func(df):

return df.fillna(method='ffill')

def handle_data(context, data): if 'EPS_PCT_DIFF_SURP' in data['AAPL'] if data['AAPL']['EPS_PCT_DIFF_SURP'] > 20 # do something

# dataframe an array libs import pandas as pd import numpy ad np def initialize(context):

auth_code = 'C_g4_bPDdjFrsdaf8P_K' database = 'ZES' dataset = 'AAPL' url = 'https://quandl.com/api/v1/datasets/{0}/{1}.csv?auth_code={2}' url = url.format(database, dataset, auth_code) fetch_csv(url, date_column='DATE', symbol=dataset, date_format='%Y-%m-%d', post_func=post_func)

# ffill: propagate last valid observation forward to next valid def post_func(df):

return df.fillna(method='ffill')

def handle_data(context, data): if 'EPS_PCT_DIFF_SURP' in data['AAPL'] if data['AAPL']['EPS_PCT_DIFF_SURP'] > 20 # do something

in Quantopian

# dataframe an array libs import pandas as pd import numpy ad np def initialize(context):

auth_code = 'C_g4_bPDdjFrsdaf8P_K' database = 'ZES' dataset = 'AAPL' url = 'https://quandl.com/api/v1/datasets/{0}/{1}.csv?auth_code={2}' url = url.format(database, dataset, auth_code) fetch_csv(url, date_column='DATE', symbol=dataset, date_format='%Y-%m-%d', post_func=post_func)

# ffill: propagate last valid observation forward to next valid def post_func(df):

return df.fillna(method='ffill')

def handle_data(context, data): if 'EPS_PCT_DIFF_SURP' in data['AAPL'] if data['AAPL']['EPS_PCT_DIFF_SURP'] > 20 # do something

in Quantopian

# dataframe an array libs import pandas as pd import numpy ad np def initialize(context):

auth_code = 'C_g4_bPDdjFrsdaf8P_K' database = 'ZES' dataset = 'AAPL' url = 'https://quandl.com/api/v1/datasets/{0}/{1}.csv?auth_code={2}' url = url.format(database, dataset, auth_code) fetch_csv(url, date_column='DATE', symbol=dataset, date_format='%Y-%m-%d', post_func=post_func)

# ffill: propagate last valid observation forward to next valid def post_func(df):

return df.fillna(method='ffill')

def handle_data(context, data): if 'EPS_PCT_DIFF_SURP' in data['AAPL'] if data['AAPL']['EPS_PCT_DIFF_SURP'] > 20 # do something

in Quantopian

# dataframe an array libs import pandas as pd import numpy ad np def initialize(context):

auth_code = 'C_g4_bPDdjFrsdaf8P_K' database = 'ZES' dataset = 'AAPL' url = 'https://quandl.com/api/v1/datasets/{0}/{1}.csv?auth_code={2}' url = url.format(database, dataset, auth_code) fetch_csv(url, date_column='DATE', symbol=dataset, date_format='%Y-%m-%d', post_func=post_func)

# ffill: propagate last valid observation forward to next valid def post_func(df):

return df.fillna(method='ffill')

def handle_data(context, data): if 'EPS_PCT_DIFF_SURP' in data['AAPL'] if data['AAPL']['EPS_PCT_DIFF_SURP'] > 20 # do something

in Quantopian

# dataframe an array libs import pandas as pd import numpy ad np def initialize(context):

auth_code = 'C_g4_bPDdjFrsdaf8P_K' database = 'ZES' dataset = 'AAPL' url = 'https://quandl.com/api/v1/datasets/{0}/{1}.csv?auth_code={2}' url = url.format(database, dataset, auth_code) fetch_csv(url, date_column='DATE', symbol=dataset, date_format='%Y-%m-%d', post_func=post_func)

# ffill: propagate last valid observation forward to next valid def post_func(df):

return df.fillna(method='ffill')

def handle_data(context, data): if 'EPS_PCT_DIFF_SURP' in data['AAPL'] if data['AAPL']['EPS_PCT_DIFF_SURP'] > 20 # do something

in Quantopian

# dataframe an array libs import pandas as pd import numpy ad np def initialize(context):

auth_code = 'C_g4_bPDdjFrsdaf8P_K' database = 'ZES' dataset = 'AAPL' url = 'https://quandl.com/api/v1/datasets/{0}/{1}.csv?auth_code={2}' url = url.format(database, dataset, auth_code) fetch_csv(url, date_column='DATE', symbol=dataset, date_format='%Y-%m-%d', post_func=post_func)

# ffill: propagate last valid observation forward to next valid def post_func(df):

return df.fillna(method='ffill')

def handle_data(context, data): if 'EPS_PCT_DIFF_SURP' in data['AAPL'] if data['AAPL']['EPS_PCT_DIFF_SURP'] > 20 # do something

in Quantopian

# dataframe an array libs import pandas as pd import numpy ad np def initialize(context):

auth_code = 'C_g4_bPDdjFrsdaf8P_K' database = 'ZES' dataset = 'AAPL' url = 'https://quandl.com/api/v1/datasets/{0}/{1}.csv?auth_code={2}' url = url.format(database, dataset, auth_code) fetch_csv(url, date_column='DATE', symbol=dataset, date_format='%Y-%m-%d', post_func=post_func)

# ffill: propagate last valid observation forward to next valid def post_func(df):

return df.fillna(method='ffill')

def handle_data(context, data): if 'EPS_PCT_DIFF_SURP' in data['AAPL'] if data['AAPL']['EPS_PCT_DIFF_SURP'] > 20 # do something

in Quantopian

user: QuantCon2015 pass: bbbbbbbb

Useful Docs: quandl.com/help/python

quandl.com/help/quantopian

Example Application

Goals

• Take advantage of the very easy, very powerful backtesting of Quantopian

• Take advantage of the huge amounts of data in Quandl

• Write up the process using Quantopian’s new research notebook

Zacks Fundamentals B

• 200+ indicators

• over 7000 US equities

• How to take advantage of all 200 indicators?

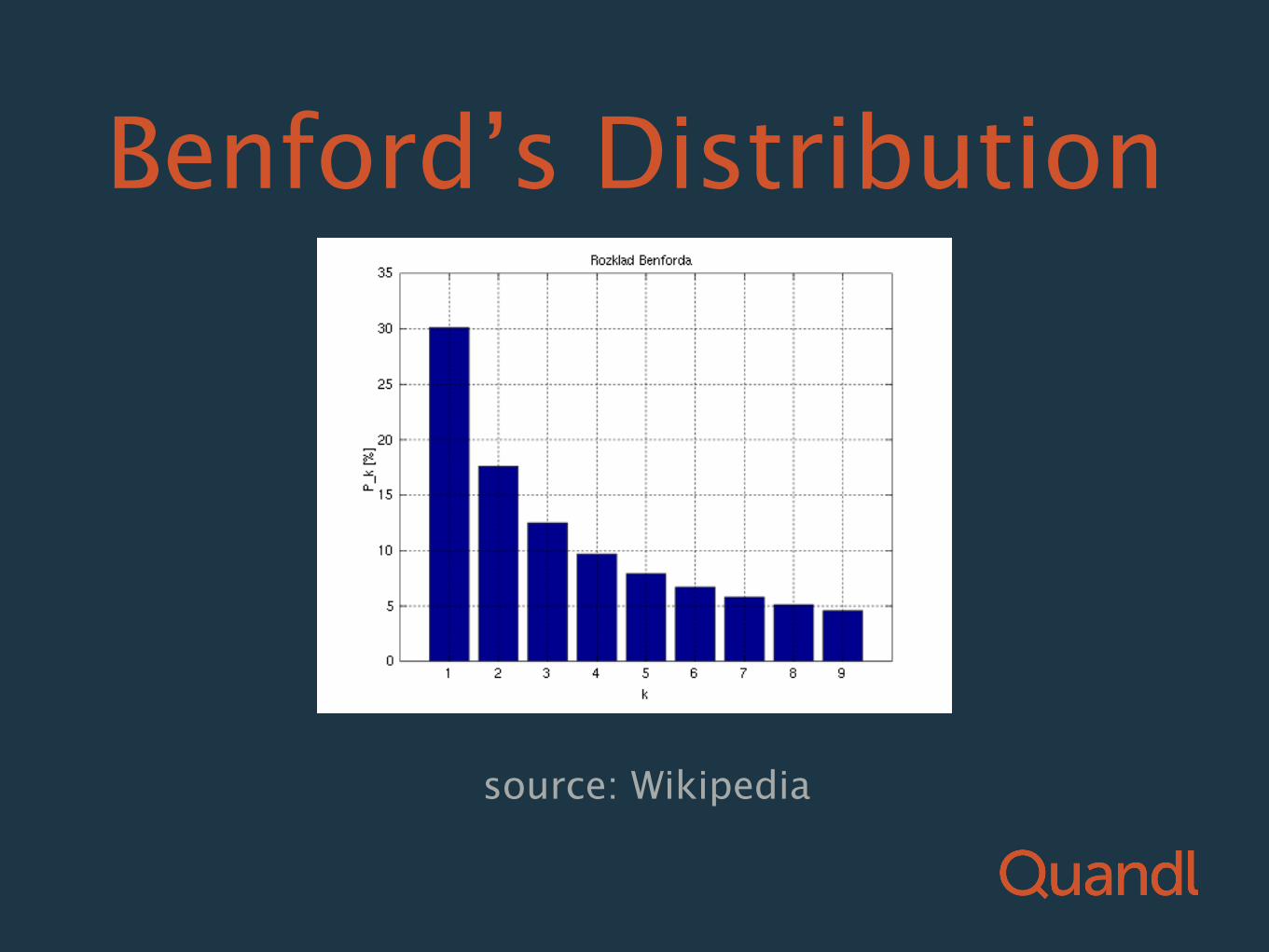

Benford’s Law Example algorithm:

The most common first number is 1

source: Wikipedia

Benford’s Distribution

Summary

• using goodness-of-fit score for the distribution of sig-figs for all 200 indicators for each filing

• finding the top 0.1% best-fit filings

• investing in those companies for that quarter

• Followed Karin Rubin’s “Investing in Women-led Companies” as a template

Results

Results

#QuandlApps

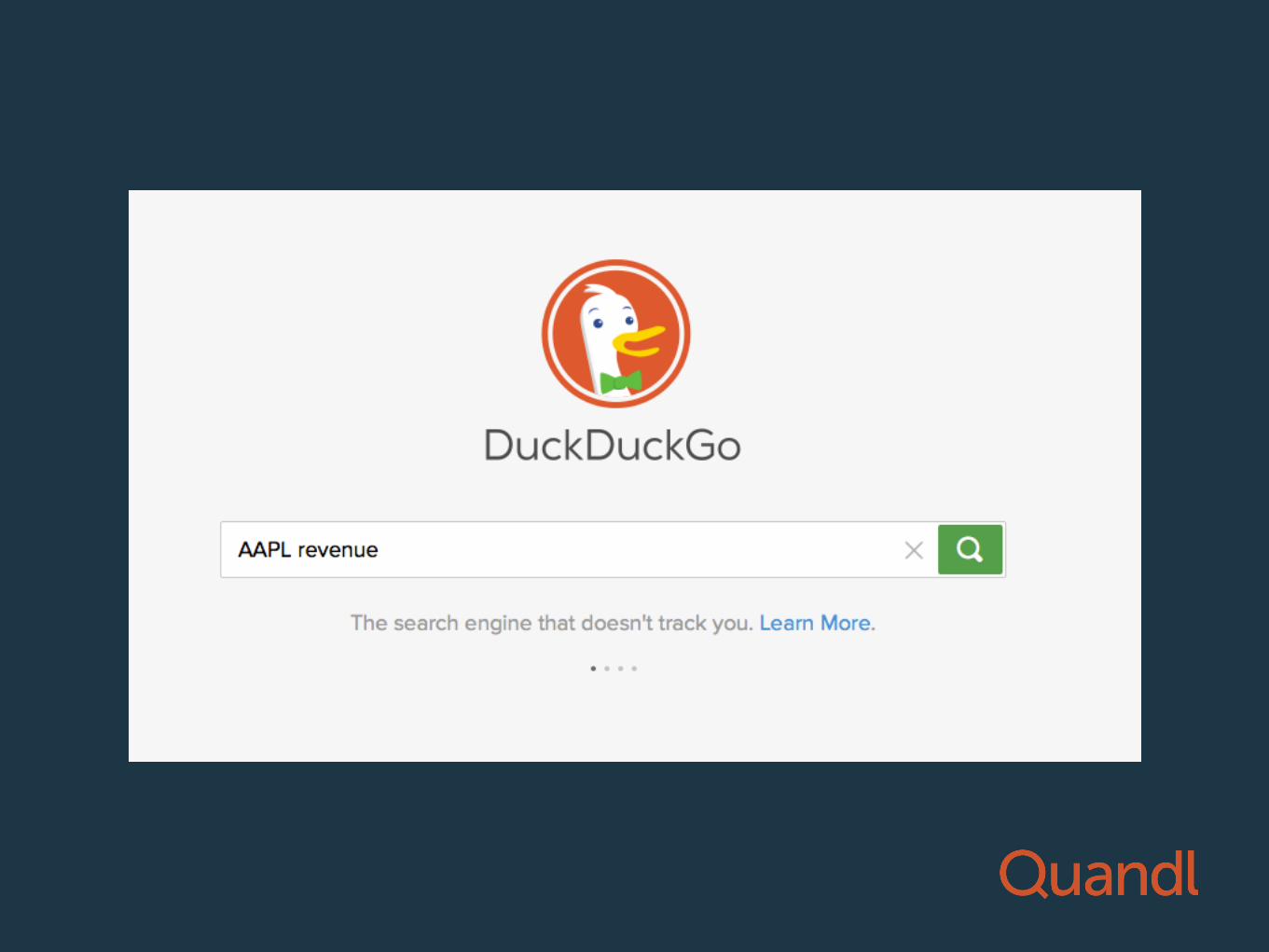

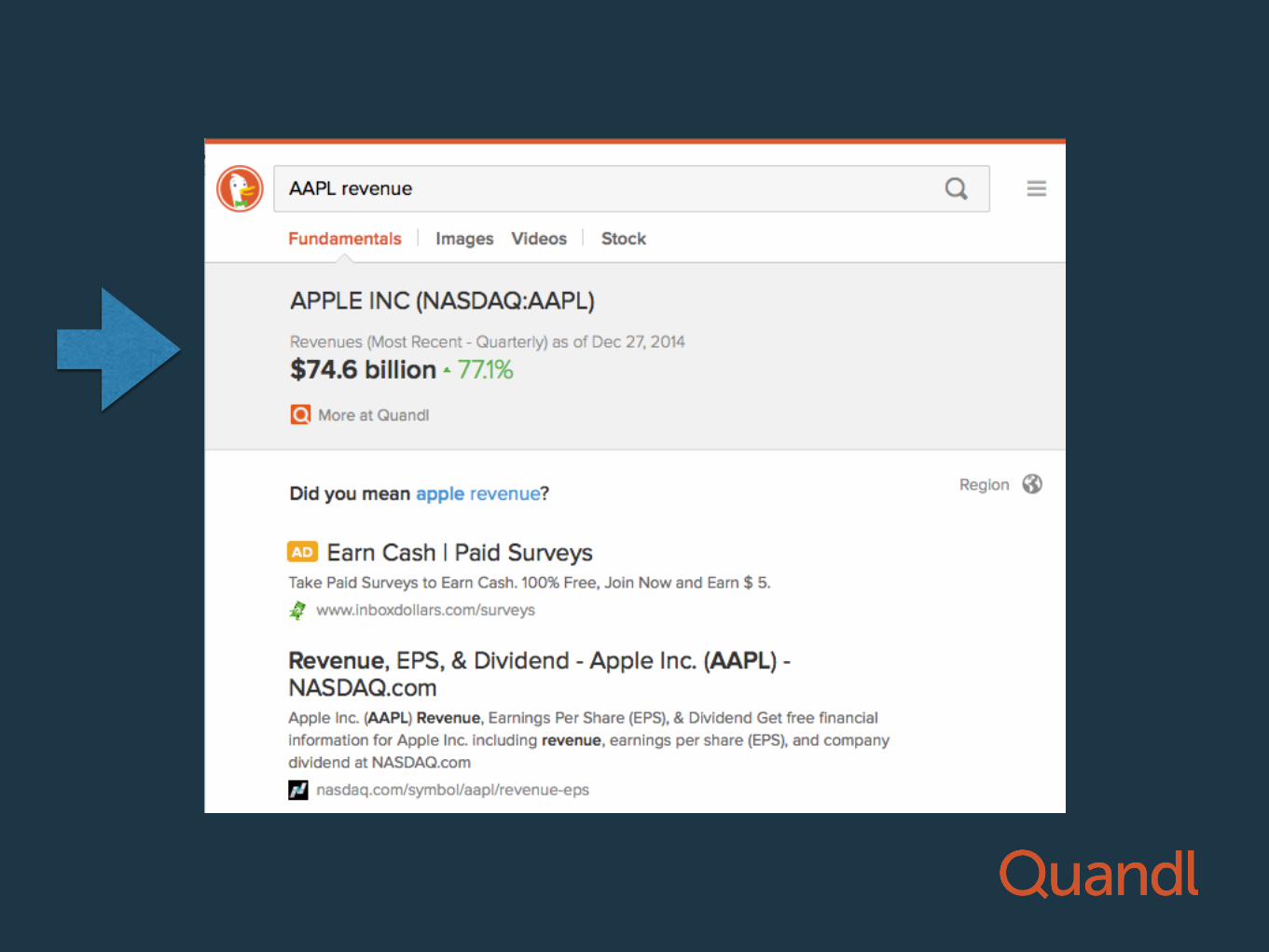

DuckDuckGo

DuckDuckGo

DuckDuckGo

• Does not track your history

• Allows open-source development of “instant answer” modules

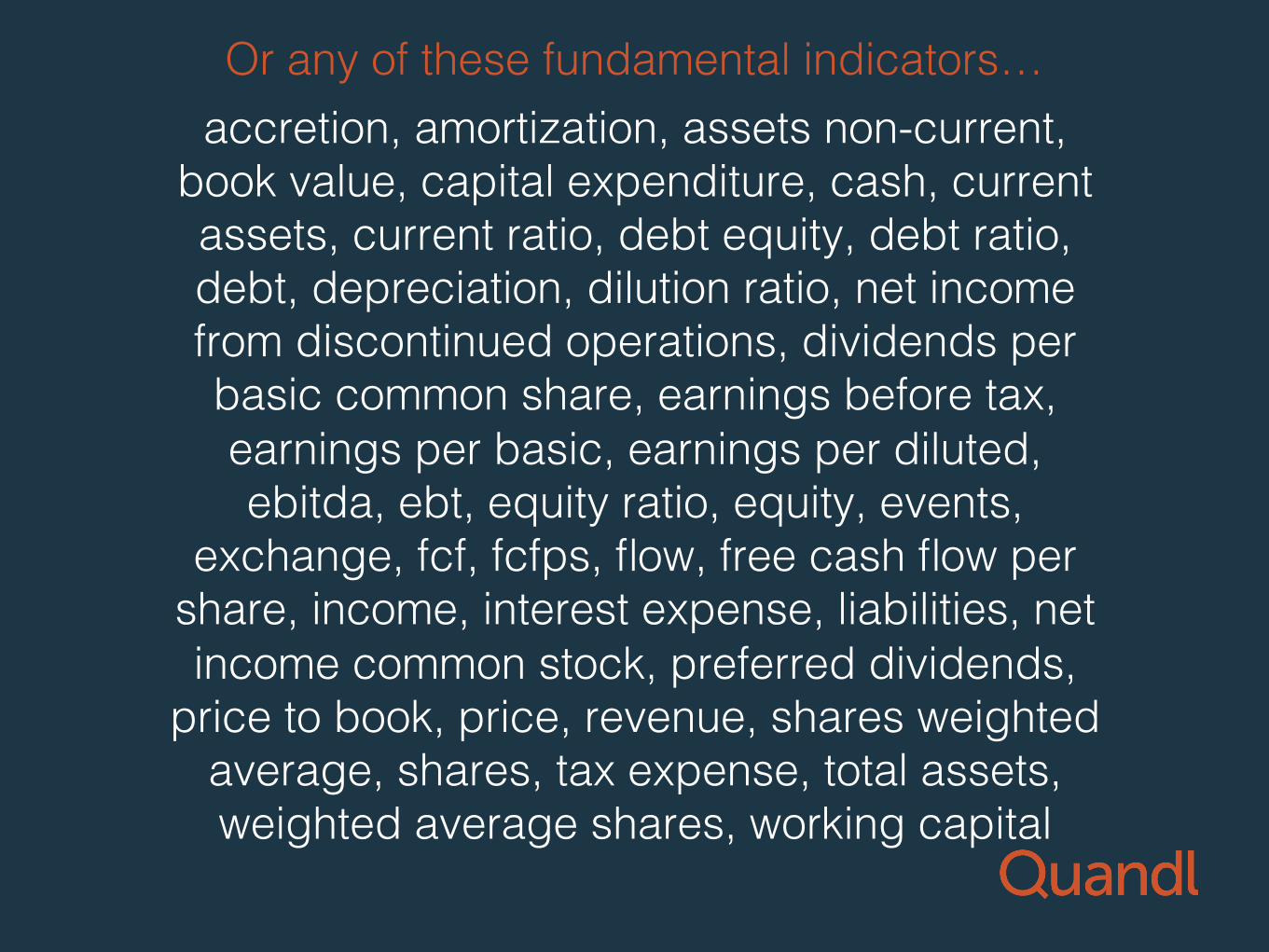

accretion, amortization, assets non-current, book value, capital expenditure, cash, current assets, current ratio, debt equity, debt ratio, debt, depreciation, dilution ratio, net income from discontinued operations, dividends per basic common share, earnings before tax, earnings per basic, earnings per diluted, ebitda, ebt, equity ratio, equity, events,

exchange, fcf, fcfps, flow, free cash flow per share, income, interest expense, liabilities, net income common stock, preferred dividends,

price to book, price, revenue, shares weighted average, shares, tax expense, total assets, weighted average shares, working capital!

Or any of these fundamental indicators…!

Useful Docs: quandl.com/help/python

quandl.com/help/quantopian

Hackathon data: user: QuantCon2015

pass: bbbbbbbb (8 b’s)