leveraging remittance flows: an introduction to future flow transactions

DESCRIPTION

Presented by: 1. Stefan Hruschka, Asian Development Bank2. Wan Ning Lie, Standard Chartered Bank3. Jim Patti, Mayer Brown LLPTRANSCRIPT

Mayer Brown is a global legal services provider comprising legal practices that are separate entities (the "Mayer Brown Practices"). The Mayer Brown Practices are: Mayer Brown LLP and Mayer Brown Europe – Brussels LLP both limited liability partnerships established in Illinois USA; Mayer Brown International LLP, a limited liability partnership incorporated in England and Wales (authorized and regulated by the Solicitors Regulation Authority and registered in England and Wales number OC 303359); Mayer Brown, a SELAS established in France; Mayer Brown JSM, a Hong Kong partnership and its associated entities in Asia; and Tauil & Chequer Advogados, a Brazilian law partnership with which Mayer Brown is associated. "Mayer Brown" and the Mayer Brown logo are the trademarks of the Mayer Brown Practices in their respective jurisdictions.

LEVERAGING REMITTANCE FLOWS: An Introduction to Future Flow Transactions

Asian Development BankManila, PhilippinesMarch 2015By: Stefan Hruschka, Asian Development Bank

Wan Ning Lie, Standard Chartered BankJim Patti, Mayer Brown LLP

2

Welcome!

What is our goal for today?OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

3

Welcome!

What is our goal for today?• To describe techniques for using international remittances

to finance a nation’s development, people and companies.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

4

Welcome!

What is our goal for today?• To describe techniques for using international remittances

to finance a nation’s development, people and companies.• To describe these remittances from a legal perspective.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

5

Welcome!

What is our goal for today?• To describe techniques for using international remittances

to finance a nation’s development, people and companies.• To describe these remittances from a legal perspective.• To discuss potential investor interest in remittance-backed

financings.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

6

Welcome!

What is our goal for today?• To describe techniques for using international remittances

to finance a nation’s development, people and companies.• To describe these remittances from a legal perspective.• To discuss potential investor interest in remittance-backed

financings.• To describe the important role that governments can play

in facilitating these transactions and enabling their populations to benefit from these financing alternatives.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

7

Why is this topic of interest?

Because remittance-backed financings can:OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

8

Why is this topic of interest?

Because remittance-backed financings can:• Be a source of medium-/long-term international funding

(five or more years),

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

9

Why is this topic of interest?

Because remittance-backed financings can:• Be a source of medium-/long-term international funding

(five or more years),• Promote developmental funding, including from DFIs,

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

10

Why is this topic of interest?

Because remittance-backed financings can:• Be a source of medium-/long-term international funding

(five or more years),• Promote developmental funding, including from DFIs,• Establish relationships with new investors, including

potential for “AAA” investors if a guaranty is used,

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

11

Why is this topic of interest?

Because remittance-backed financings can:• Be a source of medium-/long-term international funding

(five or more years),• Promote developmental funding, including from DFIs,• Establish relationships with new investors, including

potential for “AAA” investors if a guaranty is used,• Assist in the development of a domestic framework and

experience for international financings,

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

12

Why is this topic of interest?

Because remittance-backed financings can:• Be a source of medium-/long-term international funding

(five or more years),• Promote developmental funding, including from DFIs,• Establish relationships with new investors, including

potential for “AAA” investors if a guaranty is used,• Assist in the development of a domestic framework and

experience for international financings,• Encourage local banks to seek additional retail customers

(e.g., the unbanked),

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

13

Why is this topic of interest?

Because remittance-backed financings can:• Be a source of medium-/long-term international funding

(five or more years),• Promote developmental funding, including from DFIs,• Establish relationships with new investors, including

potential for “AAA” investors if a guaranty is used,• Assist in the development of a domestic framework and

experience for international financings,• Encourage local banks to seek additional retail customers

(e.g., the unbanked),• Offer attractive pricing compared to unsecured debt, and

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

14

Why is this topic of interest?

Because remittance-backed financings can:• Be a source of medium-/long-term international funding

(five or more years),• Promote developmental funding, including from DFIs,• Establish relationships with new investors, including

potential for “AAA” investors if a guaranty is used,• Assist in the development of a domestic framework and

experience for international financings,• Encourage local banks to seek additional retail customers

(e.g., the unbanked),• Offer attractive pricing compared to unsecured debt, and• Achieve a rating higher than a country’s current foreign

currency sovereign rating (often as high as the originator’s domestic or “survivability” rating).

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

15

Asset Classes

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

16

Asset Classes

Remittance Flows• Worker remittances through banks• Western Union/MoneyGram payments• Credit card/mobile phone transfers

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

17

Asset Classes

Remittance Flows• Worker remittances through banks• Western Union/MoneyGram payments• Credit card/mobile phone transfers

Commerce-related Flows• Export collections• Foreign direct investment (FDI)

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

18

Asset Classes

Remittance Flows• Worker remittances through banks• Western Union/MoneyGram payments• Credit card/mobile phone transfers

Commerce-related Flows• Export collections• Foreign direct investment (FDI)

Tourism-related Flows• Credit card net settlement payments• Check/Travellers cheque payments• Airline/airport receivables

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

19

Asset Classes

Remittance Flows• Worker remittances through banks• Western Union/MoneyGram payments• Credit card/mobile phone transfers

Commerce-related Flows• Export collections• Foreign direct investment (FDI)

Tourism-related Flows• Credit card net settlement payments• Check/Travellers cheque payments• Airline/airport receivables

Other Flows• International calling payments

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

20

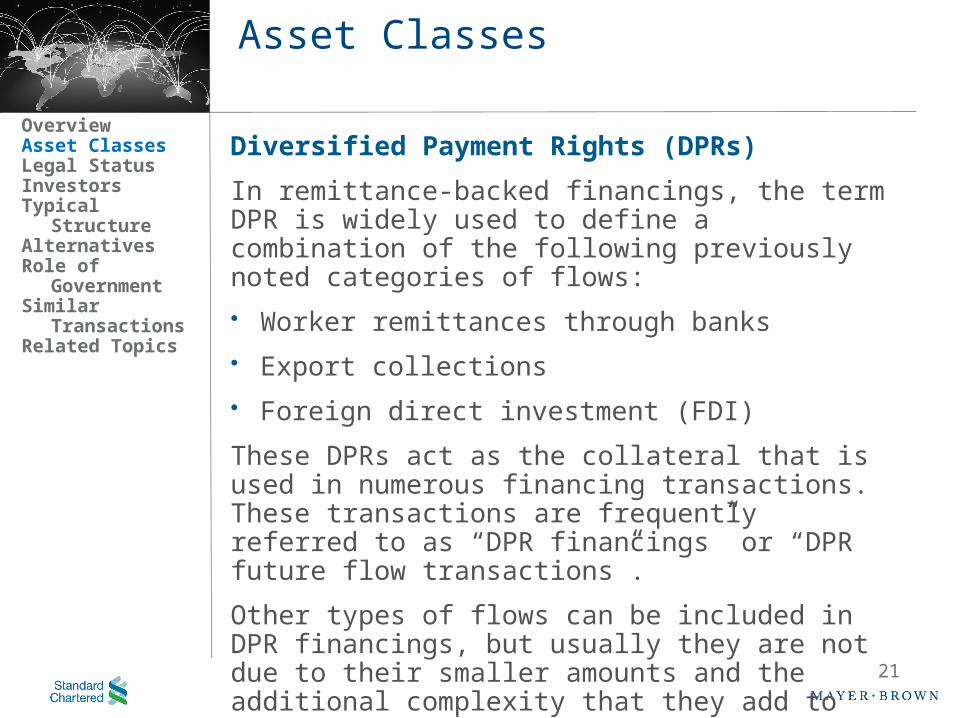

Asset Classes

Diversified Payment Rights (DPRs)

In remittance-backed financings, the term DPR is widely used to define a combination of the following previously noted categories of flows:• Worker remittances through banks• Export collections• Foreign direct investment (FDI)

These DPRs act as the collateral that is used in numerous financing transactions. These transactions are frequently referred to as “DPR financings” or “DPR future flow transactions”.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

21

Asset Classes

Diversified Payment Rights (DPRs)

In remittance-backed financings, the term DPR is widely used to define a combination of the following previously noted categories of flows:• Worker remittances through banks• Export collections• Foreign direct investment (FDI)

These DPRs act as the collateral that is used in numerous financing transactions. These transactions are frequently referred to as “DPR financings” or “DPR future flow transactions”.

Other types of flows can be included in DPR financings, but usually they are not due to their smaller amounts and the additional complexity that they add to the transaction.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

22

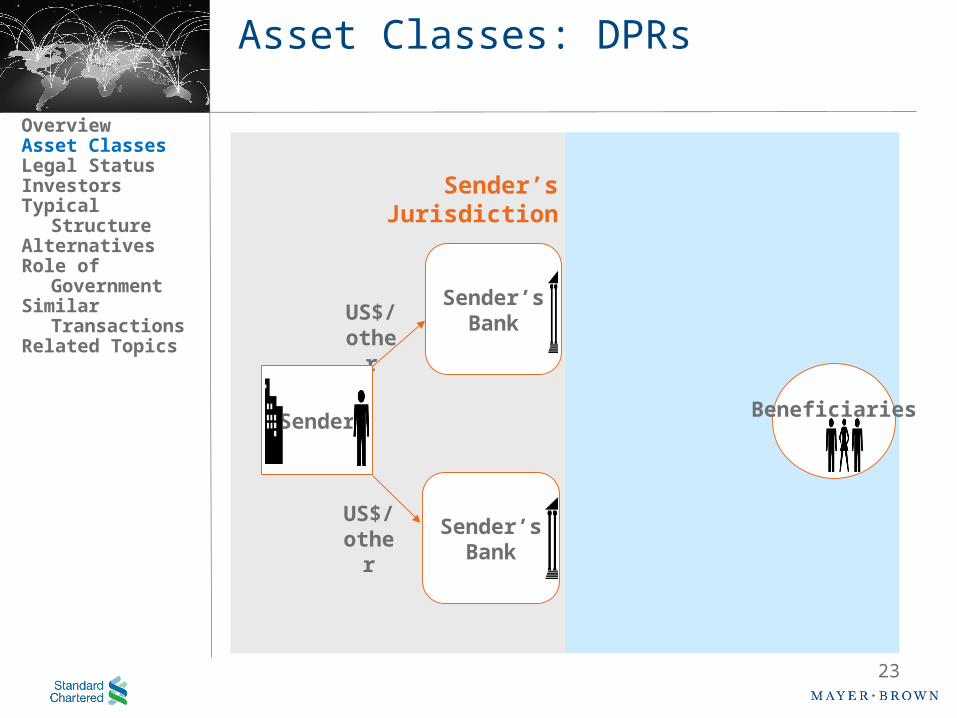

Asset Classes: DPRs

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Beneficiaries

Sender’s Jurisdiction

Sender

23

Asset Classes: DPRs

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Beneficiaries

Sender’sBank

Sender’s Jurisdiction

Sender’sBank

US$/other

Sender

US$/other

24

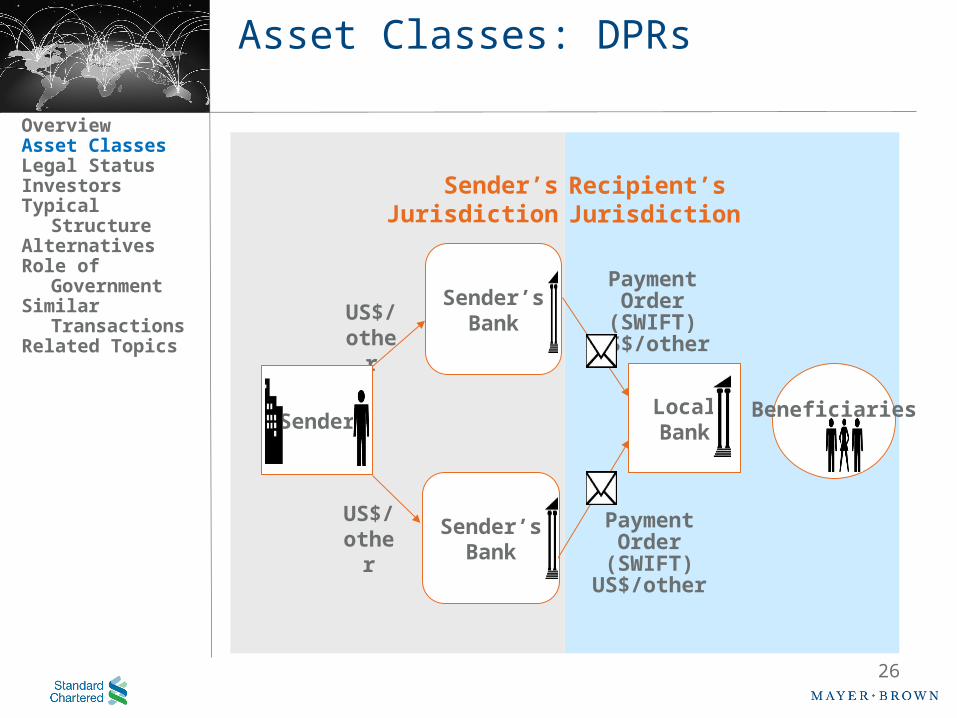

Asset Classes: DPRs

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

LocalBank

Beneficiaries

Sender’sBank

Recipient’s JurisdictionSender’s Jurisdiction

Sender’sBank

US$/other

Payment Order (SWIFT)

US$/other

Payment Order (SWIFT)

US$/other

Sender

US$/other

25

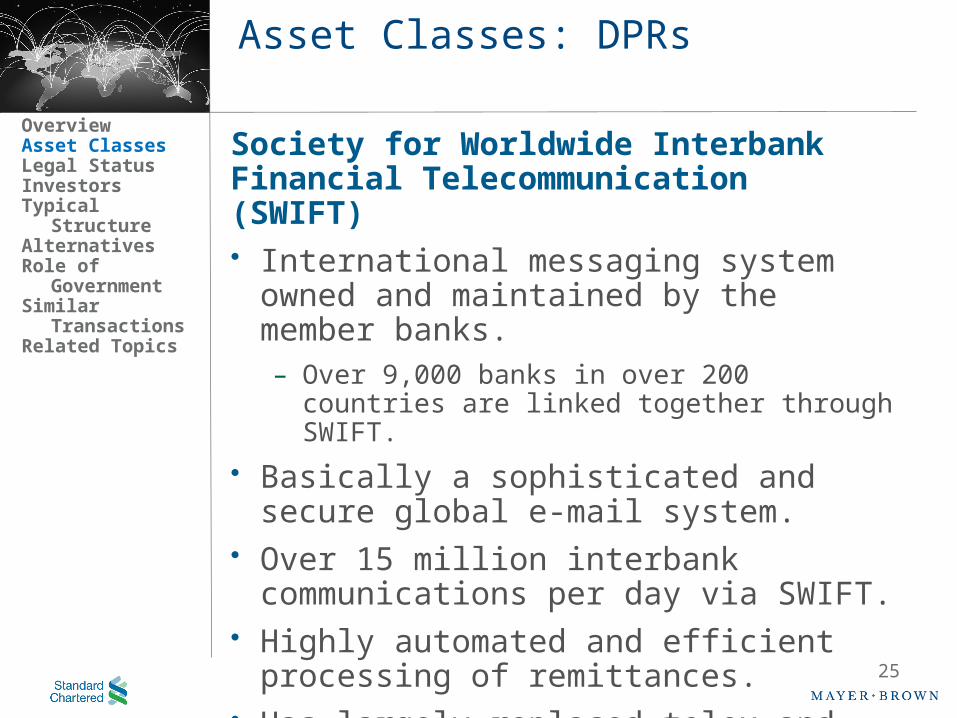

Asset Classes: DPRs

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Society for Worldwide Interbank Financial Telecommunication (SWIFT) • International messaging system owned and

maintained by the member banks.– Over 9,000 banks in over 200 countries are linked

together through SWIFT.• Basically a sophisticated and secure global e-mail

system.• Over 15 million interbank communications per

day via SWIFT.• Highly automated and efficient processing of

remittances.• Has largely replaced telex and other cross-border

interbank communication systems.

26

Asset Classes: DPRs

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

LocalBank

Beneficiaries

Sender’sBank

Recipient’s JurisdictionSender’s Jurisdiction

Sender’sBank

US$/other

Payment Order (SWIFT)

US$/other

Payment Order (SWIFT)

US$/other

Sender

US$/other

27

Asset Classes: DPRs

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

LocalBank

Beneficiaries

LocalCurrency or US$/other

Sender’sBank

Recipient’s JurisdictionSender’s Jurisdiction

Sender’sBank

US$/other

Payment Order (SWIFT)

US$/other

Payment Order (SWIFT)

US$/other

Sender

US$/other

28

Legal Status

29

Legal Status

Who owns the remittance funds?

A bank can only use the remittances as collateral for a financing if it actually has ownership rights in the remittances.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

30

Legal Status

Who owns the remittance funds?

The sender? – The sender is the one who owns the funds at the beginning and wants to make payment to an indicated beneficiary.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

31

Legal Status

Who owns the remittance funds?

The sender? – The sender is the one who owns the funds at the beginning and wants to make payment to an indicated beneficiary.

The sender’s bank? – The sender’s bank receives the funds from the sender along with the sender’s request to cause a payment to be made to the indicated beneficiary.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

32

Legal Status

Who owns the remittance funds?

The sender? – The sender is the one who owns the funds at the beginning and wants to make payment to an indicated beneficiary.

The sender’s bank? – The sender’s bank receives the funds from the sender along with the sender’s request to cause a payment to be made to the indicated beneficiary.

The beneficiary’s bank? – The beneficiary’s bank receives the funds from the sender’s bank along with the sender’s bank’s request (a “Payment Order”) to cause payment to be made to the indicated beneficiary.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

33

Legal Status

Who owns the remittance funds?

The sender? – The sender is the one who owns the funds at the beginning and wants to make payment to an indicated beneficiary.

The sender’s bank? – The sender’s bank receives the funds from the sender along with the sender’s request to cause a payment to be made to the indicated beneficiary.

The beneficiary’s bank? – The beneficiary’s bank receives the funds from the sender’s bank along with the sender’s bank’s request (a “Payment Order”) to cause payment to be made to the indicated beneficiary.

The beneficiary? – The beneficiary receives the funds at the end of the payment chain.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

34

Legal Status

ANSWER IN ALMOST ALL JURISDICTIONS:

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

35

Legal Status

ANSWER IN ALMOST ALL JURISDICTIONS:

They ALL own the funds at different times in the payment chain.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

36

Legal StatusOverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Beneficiary’s JurisdictionSender’s Jurisdiction

Sender

37

Legal Status: First ContractOverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Sender’sBank

Beneficiary’s JurisdictionSender’s Jurisdiction

Sender

US$/other

38

Legal Status: First Contract

Similar to a DepositPayments by a sender to the sender’s bank are similar to deposits made into a deposit account – that is, the sender transfers ownership of those funds to its bank. In some cases, the sender doesn’t even transfer ownership of funds but rather asks its bank to reduce the credits in the sender’s bank account.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

39

Legal Status: First Contract

Similar to a DepositPayments by a sender to the sender's bank are similar to deposits made into a deposit account – that is, the sender transfers ownership of those funds to its bank. In some cases, the sender doesn’t even transfer ownership of funds but rather asks its bank to reduce the credits in the sender’s bank account.

In return, the sender receives the bank’s promise that it will cause an equivalent amount to be paid to the beneficiary identified by the sender.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

40

Legal Status: First Contract

Similar to a DepositPayments by a sender to the sender's bank are similar to deposits made into a deposit account – that is, the sender transfers ownership of those funds to its bank. In some cases, the sender doesn’t even transfer ownership of funds but rather asks its bank to reduce the credits in the sender’s bank account.

In return, the sender receives the bank’s promise that it will cause an equivalent amount to be paid to the beneficiary identified by the sender.

The difference with a deposit is that the sender will not be the one later withdrawing these funds again but rather the beneficiary ultimately will receive an equivalent amount.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

41

Legal Status: First ContractOverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Sender’sBank

Beneficiary’s JurisdictionSender’s Jurisdiction

Sender

US$/other

42

Legal Status: Second ContractOverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

LocalBank

Sender’sBank

Beneficiary’s JurisdictionSender’s Jurisdiction

Payment Order

(SWIFT)US$/other

Sender

US$/other

43

Legal Status: Second Contract

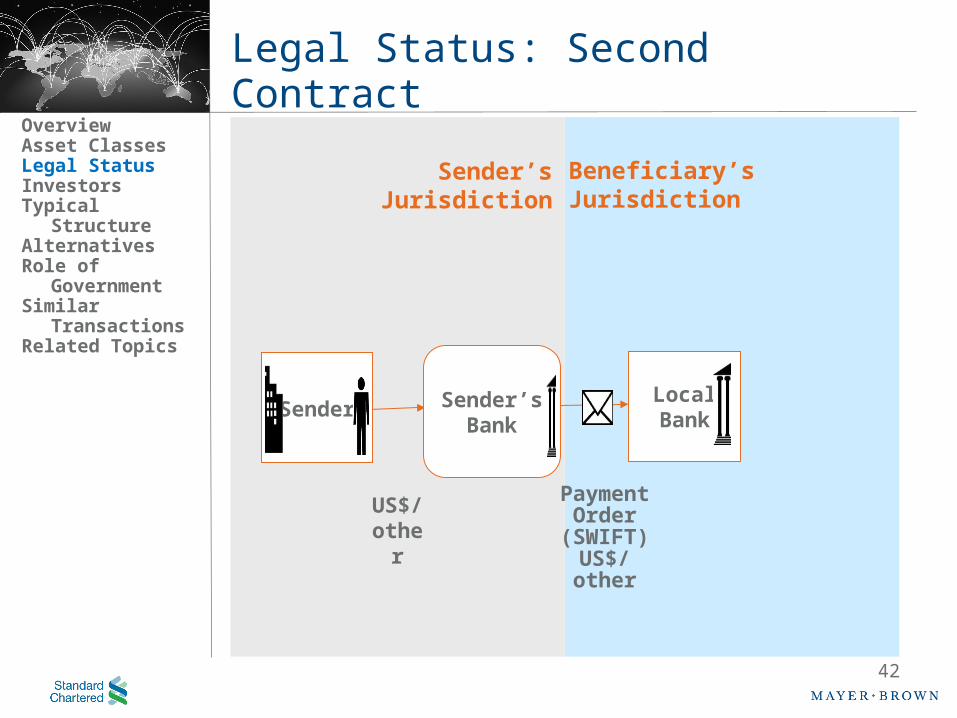

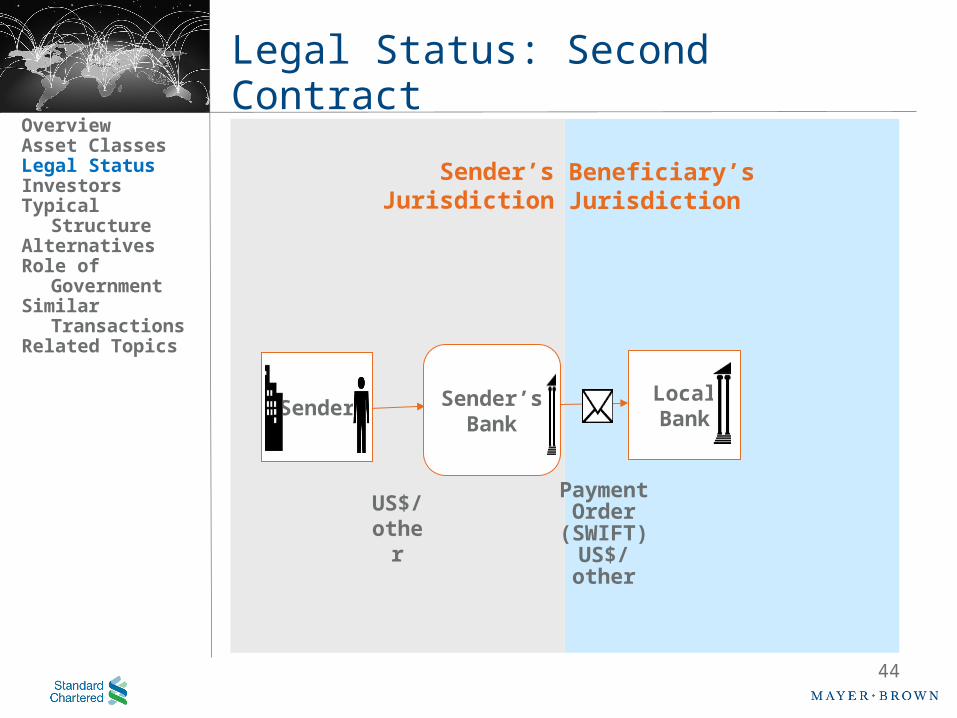

Similar to the First ContractJust as with the first contract, payments by a sender’s bank to the beneficiary’s bank involve the transfer of ownership of those funds to the beneficiary’s bank. In return, the sender’s bank receives the beneficiary’s bank’s promise that it will cause an equivalent amount to be paid to the beneficiary identified to it by the sender’s bank.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

44

Legal Status: Second ContractOverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

LocalBank

Sender’sBank

Beneficiary’s JurisdictionSender’s Jurisdiction

Payment Order

(SWIFT)US$/other

Sender

US$/other

45

Legal Status: Third ContractOverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

LocalBank

Beneficiary

LocalCurrency or US$/other

Sender’sBank

Beneficiary’s JurisdictionSender’s Jurisdiction

Payment Order

(SWIFT)US$/other

Sender

US$/other

46

Legal Status: Third Contract

In this last link in the payment chain, the beneficiary is paid an amount equal to what the sender initially asked its bank to cause to be paid (less any applicable fees).

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

47

Legal Status: Third Contract

In this last link in the payment chain, the beneficiary is paid an amount equal to what the sender initially asked its bank to cause to be paid (less any applicable fees).

It is important to note that:- the funds received by the beneficiary are not the same funds delivered by the sender to its bank; in fact, frequently they are a different currency (e.g., the sender delivered US Dollars to its bank whereas the beneficiary’s bank delivers Thai Baht to the beneficiary),

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

48

Legal Status: Third Contract

In this last link in the payment chain, the beneficiary is paid an amount equal to what the sender initially asked its bank to cause to be paid (less any applicable fees).

It is important to note that:- the funds received by the beneficiary are not the same funds delivered by the sender to its bank; in fact, frequently they are a different currency (e.g., the sender delivered US Dollars to its bank whereas the beneficiary’s bank delivers Thai Baht to the beneficiary), and- the payment itself might not involve the delivery of ownership of physical cash to the beneficiary but rather payment might be made through a credit to the beneficiary’s bank account, which thus means that what the beneficiary receives is a deposit claim (i.e., an unsecured claim against its bank).

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

49

Legal Status

It is very important to have confirmed in the applicable jurisdiction that there is no local law that would contradict this standard analysis – that is, that the right to receive these payments from a foreign bank ARE OWNED BY THE RECEIVING BANK AND NOT THE NAMED BENEFICIARY.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

50

Legal Status

There are two definitions that are typically used in describing the rights that a bank uses as collateral for a remittance-based financing:

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

51

Legal Status

There are two definitions that are typically used in describing the rights that a bank uses as collateral for a remittance-based financing:• Payment Order

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

52

Legal Status

There are two definitions that are typically used in describing the rights that a bank uses as collateral for a remittance-based financing:• Payment Order• Diversified Payment Rights (DPR)

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

53

Legal Definition: Payment Orders • An electronic or other message to instruct or request

the local bank to make a payment to any beneficiary other than the local bank

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

54

Legal Definition: Payment Orders • An electronic or other message to instruct or request

the local bank to make a payment to any beneficiary other than the local bank, which message may be:– An MT102+, MT103+ or any other MT100-category

message under the SWIFT message system (or, unless specifically excluded, an MT202 payment order received by the local bank for payment to another financial institution),

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

55

Legal Definition: Payment Orders • An electronic or other message to instruct or request

the local bank to make a payment to any beneficiary other than the local bank, which message may be:– An MT102+, MT103+ or any other MT100-category

message under the SWIFT message system (or, unless specifically excluded, an MT202 payment order received by the local bank for payment to another financial institution), or

– Any other type of message, including via Fedwire, CHIPS, telex or the internet, that may be utilized to send such an instruction.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

56

Legal Definition: Payment Orders • An electronic or other message to instruct or request

the local bank to make a payment to any beneficiary other than the local bank, which message may be:– An MT102+, MT103+ or any other MT100-category

message under the SWIFT message system (or, unless specifically excluded, an MT202 payment order received by the local bank for payment to another financial institution), or

– Any other type of message, including via Fedwire, CHIPS, telex or the internet, that may be utilized to send such an instruction.

• Payment Orders would also include similar instructions received by the local bank’s foreign branches from customers of such branches (e.g., local deposit customers who request that their accounts with the local bank be debited in order to effect a payment to a beneficiary in the local bank’s home jurisdiction).

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

57

Legal Definition: DPRs

All rights (but none of the obligations) of the local bank in [U.S. Dollar/Euro]-denominated Payment Orders received (or to be received) by the local bank (including its right to receive and/or retain for itself all payments made in connection with such Payment Orders).

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

58

Legal Definition: DPRs

• Diversified Payment Rights do NOT include:OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

59

Legal Definition: DPRs

• Diversified Payment Rights do NOT include:– Payments to the local bank (e.g., repayments of loans,

treasury operations and fees), including those that come to a correspondent of the local bank for the benefit of the local bank via a SWIFT MT202 COV payment order (except to the extent to effect payment for a payment order received by the local bank)

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

60

Legal Definition: DPRs

• Diversified Payment Rights do NOT include:– Payments to the local bank (e.g., repayments of loans,

treasury operations and fees), including those that come to a correspondent of the local bank for the benefit of the local bank via a SWIFT MT202 COV payment order (except to the extent to effect payment for a payment order received by the local bank)

– Credit card payments and check collections (which are not payment orders instructing the local bank to make a payment to a third-party beneficiary and generally are SWIFT MT202s for the benefit of the local bank)

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

61

Legal Definition: DPRs

• Diversified Payment Rights do NOT include:– Payments to the local bank (e.g., repayments of loans,

treasury operations and fees), including those that come to a correspondent of the local bank for the benefit of the local bank via a SWIFT MT202 COV payment order (except to the extent to effect payment for a payment order received by the local bank)

– Credit card payments and check collections (which are not payment orders instructing the local bank to make a payment to a third-party beneficiary and generally are SWIFT MT202s for the benefit of the local bank)

– Collections on “cash-against-documents” transactions (which are advised under a SWIFT MT400) and on letter of credit-backed export transactions (which are advised under a SWIFT MT756)

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

62

Legal Definition: DPRs

• Diversified Payment Rights do NOT include:– Payments to the local bank (e.g., repayments of loans,

treasury operations and fees), including those that come to a correspondent of the local bank for the benefit of the local bank via a SWIFT MT202 COV payment order (except to the extent to effect payment for a payment order received by the local bank)

– Credit card payments and check collections (which are not payment orders instructing the local bank to make a payment to a third-party beneficiary and generally are SWIFT MT202s for the benefit of the local bank)

– Collections on “cash-against-documents” transactions (which are advised under a SWIFT MT400) and on letter of credit-backed export transactions (which are advised under a SWIFT MT756)

• Any or all of the above COULD be included; however, certain of these are less desirable to investors and others (such as credit cards) may be better-off used separately as this may bring certain benefits (such as lower debt service coverage requirements).

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

63

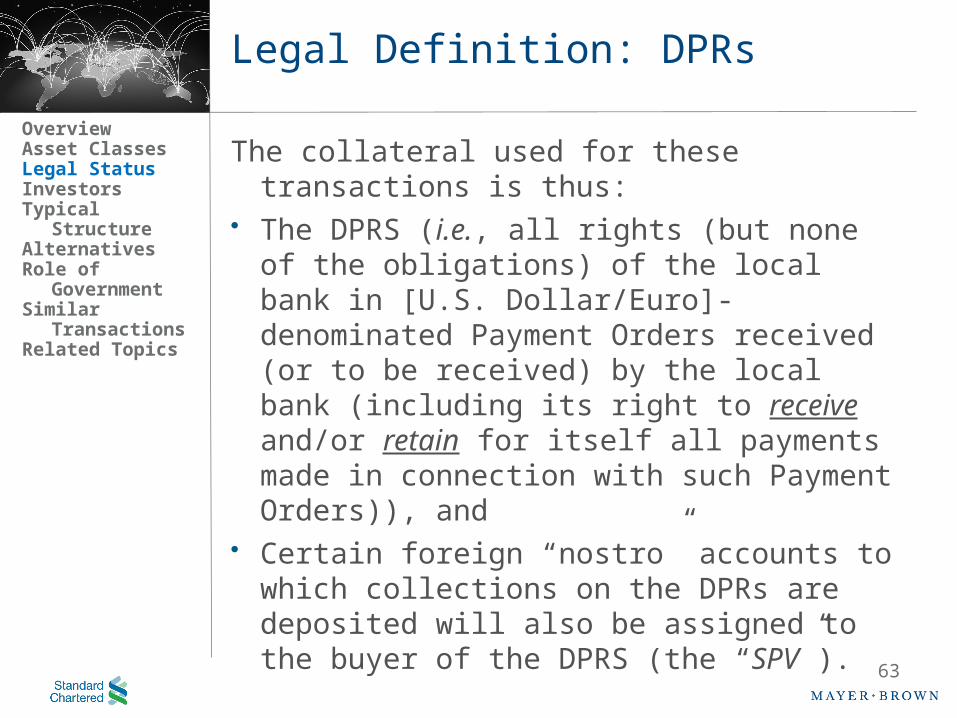

Legal Definition: DPRs

The collateral used for these transactions is thus:• The DPRS (i.e., all rights (but none of the obligations)

of the local bank in [U.S. Dollar/Euro]-denominated Payment Orders received (or to be received) by the local bank (including its right to receive and/or retain for itself all payments made in connection with such Payment Orders)), and

• Certain foreign “nostro” accounts to which collections on the DPRs are deposited will also be assigned to the buyer of the DPRS (the “SPV”).

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

64

Investors

65

Investors

Why are these payment flows of interest to investors? • Assets are in “hard” currencies such as USD, Yen and

euro; the assets match the liabilities, reducing FX risk• Greater ability to invest on the strength of the

individual originators• Minimize country risk

• Especially helpful for transferability/convertibility risk• Lower reliance on local court system• Greater protection against credit risk of the

originator, particularly in “true sale” structures• Issuances can be tailored to investor preference

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

66

Investors

Why are these payment flows of interest to investors? • Assets are in “hard” currencies such as USD, Yen and

euro; the assets match the liabilities, reducing FX risk• Greater ability to invest on the strength of the

individual originators• Minimize country risk

• Especially helpful for transferability/convertibility risk• Lower reliance on local court system• Greater protection against credit risk of the

originator, particularly in “true sale” structures• Issuances can be tailored to investor preference • For developmental entities, ability to support local

development projects, such as:

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

67

Investors

Lending to small- and medium-sized enterprises (SMEs) OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

68

Investors

Supporting energy efficiency projectsOverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

69

Investors

Lending to women in businessOverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

70

Investors

Why did the market develop?

Structured Finance in general • Greater protection against credit risk of the

originator, particularly in “true sale” structures• Method to mobilize private funds for longer tenor,

lower-cost financings• For originators, attractive pricing compared to

unsecured bonds and ability to reach out to more investors; for investors, attractive collateral

• Typically rated debt

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

71

Investors

Why did the market develop?

Future Flow Transactions• Grants investors access to systemically important

entities in countries they may find challenging• For banks in Turkey, Peru and Brazil, this used to be the

main access for long-term cross-border funding

• Minimize country risk• Especially helpful for transferability/convertibility risk

• Ratings may exceed sovereign ceiling due to the use of hard currency payments from foreign obligors

• Lower reliance on local court system• Potentially countercyclical (e.g., worker remittances

might increase if domestic economy slows)• Diverse nature of the collateral

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

72

Investors

Types of Investors• Insurance companies• Pension funds• Asset managers• Banks• Developmental organizations

Are these investors different from a country’s traditional investors?• Diversity of investors due to structured nature • Greater access to investors where higher rating

achieved• Investors looking for longer tenors

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

73

Investors

Need for Ratings• In most cases investors prefer rated transactions• They may have internal rating requirements to fulfill or

need ratings for capital allocation purposes• Nonetheless, a non-investment grade rating would

often not be beneficial• Capital charges for investors may be excessively

punitive• In which case a non-rated alternative may be more

attractive• Ratings can be used to benchmark returns (i.e., as

ratings improve, the returns can be reduced)• DFIs do not always require ratings

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

74

Investors

Rating Methodology Overview• While the three main rating agencies – Fitch,

Moody’s, S&P – have different methodologies, there are similarities across all three: • The rating of the originator forms the foundation, as

well as the product, the obligors and the significance of the business and likelihood of its continuation in adverse conditions

• Consideration is given to the legal strength of the home jurisdiction of the originator

• Historical cashflow is examined, including performance during times of stress

• The risk of sovereign interference is analyzed• The robustness of the transaction structure and the

presence or absence of certain structural features are taken into account

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

75

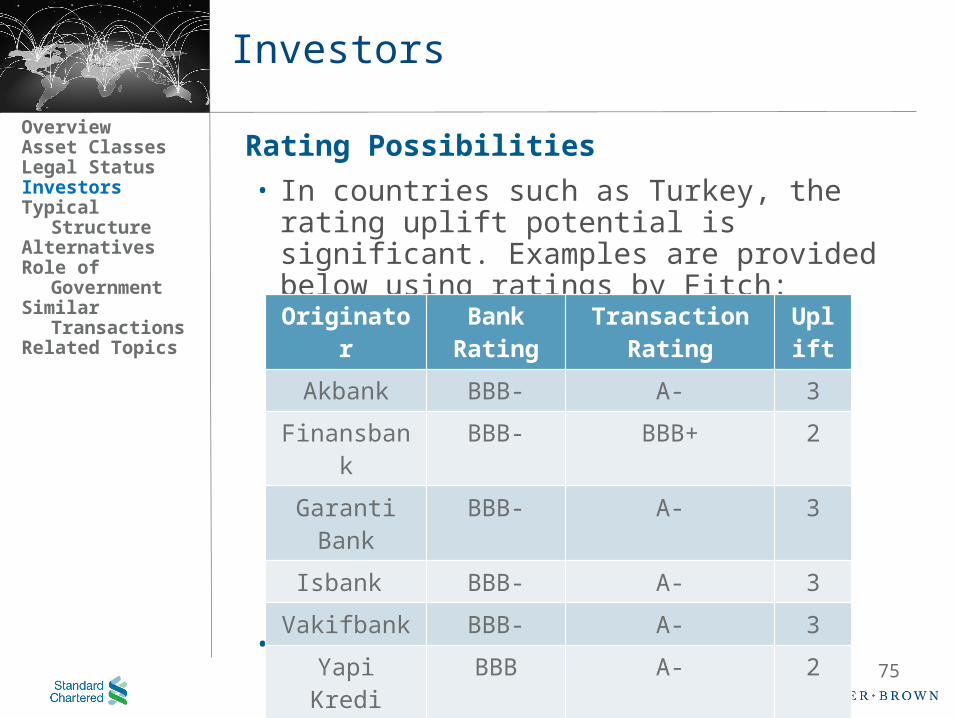

Investors

Rating Possibilities• In countries such as Turkey, the rating uplift

potential is significant. Examples are provided below using ratings by Fitch:

• Potential rating uplift to investment grade?

Originator Bank Rating Transaction Rating Uplift

Akbank BBB- A- 3

Finansbank BBB- BBB+ 2

Garanti Bank BBB- A- 3

Isbank BBB- A- 3

Vakifbank BBB- A- 3

Yapi Kredi BBB A- 2

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

76

BREAK

77

Typical Structure

78

Typical Structure

What types of structures are possible? Structured finance can be divided into two primary forms – securitization (e.g., for auto loans) and non-securitization (e.g., covered bonds, future flows)

What is securitization? Technically speaking, the term “securitization” simply means the conversion of a financial asset into a security. More commonly, however, the term is used to mean the transfer (generally as a “true sale”) of existing receivables or other payment rights to a single purpose vehicle (“SPV”). The SPV then incurs debt secured by the purchased assets.

A traditional securitization involves the transfer of credit risk to the investors. For example, if the borrower of an auto loan fails to make payment, then the investors in an auto loan securitization bear that risk.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Typical Structure

79

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Rating Agencies(evaluate credit risk/deal structure, assess third parties, interact with investors and issue ratings)

InvestorsAssets Liabilities

SPV

Funds

Tranches

Financial GuarantorInsures

particular tranches

Collects and makes payments

Originator/Servicer

Monitors compliance

Trustee

80

Typical Structure

Remittance deals are not, however, traditional securitizationsFinancings for future remittances are not traditional securitizations as:

• The investors are relying upon the quality of the originator instead of the quality of the assets as the originator needs to stay in business in order to continue to generate future assets.

• The investors are not just taking the credit risk of the assets but rather have full (or almost full) recourse to the originator.– As a result, the debt is often accounted for on balance

sheet.• No third party can easily replace the originator to handle the

assets, such as paying beneficiaries or collecting from obligors (i.e., the remittance senders).

So what then does a typical remittance transaction look like?

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Typical Structure

81

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Rating Agencies(evaluate credit risk/deal structure, assess third parties, interact with investors and issue ratings)

InvestorsAssets Liabilities

SPV

Funds

Tranches

Financial GuarantorInsures

particular tranches

Collects and makes payments

Originator/Servicer

Monitors compliance

Trustee

82

Typical Structure

Exactly the same!• There is a true sale of the future flow of remittances to

an SPV.– Bankruptcy Remote: Sold receivables are not owned by

their originator and would not be included in the originator’s bankruptcy estate (i.e., not subject to claims of any other creditors).

• The SPV uses its assets as collateral to raise funding.• The collections on the assets are used to pay investors.• A trustee or security agent for the investors controls the

collections and the bank accounts into which they are paid.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

83

Typical Structure

So what is the difference?OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

84

Typical Structure

So what is the difference?• Recourse: In securitizations, the liability of the originator for

losses by investors is somewhat more limited than in straight debt issuances; however, as with covered bonds, this is not always the case for future flow transactions. Traditionally the investors have full (or almost full) recourse to the originator.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

85

Typical Structure

So what is the difference?• Recourse: In securitizations, the liability of the originator for

losses by investors is somewhat more limited than in straight debt issuances; however, as with covered bonds, this is not always the case for future flow transactions. Traditionally the investors have full (or almost full) recourse to the originator.

• Originator Survivability: Investors and rating agencies are more focused on the credit quality of the originator since it is the originator’s ability to withstand a bankruptcy event that ensures the continued generation of future receivables.– Investors are investing in business continuity

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

86

Typical Structure

So what is the difference?• Recourse: In securitizations, the liability of the originator for

losses by investors is somewhat more limited than in straight debt issuances; however, as with covered bonds, this is not always the case for future flow transactions. Traditionally the investors have full (or almost full) recourse to the originator.

• Originator Survivability: Investors and rating agencies are more focused on the credit quality of the originator since it is the originator’s ability to withstand a bankruptcy event that ensures the continued generation of future receivables.– Investors are investing in business continuity

• Offshore SPV: As the assets come from offshore, the SPV is traditionally offshore in order to minimize sovereign risk and enable investors to have greater confidence in the structure.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

87

Typical Structure: Program?

Program vs. Single Transaction • Leveraging Receivables

A program allows multiple sets of creditors to share in a single asset pool, which is sometimes required if assets cannot be easily segregated (e.g., financial flows)

• What leverage limitations to apply?• Efficiency

– A program is more costly and time-consuming upfront but will save significant money and time for future series

– A program avoids need to approach company’s obligors for each series

– A program can facilitate compliance with negative pledge/asset sale limitations as transfer (as opposed to funding) occurs only once

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

88

Typical Structure: Program?

Program vs. Single Transaction • Complexity

– A program is much more complex and thus potentially more confusing for company, courts and regulators

– For smaller issuers, the “keep it simple” approach may be preferable; particularly as much of the flexibility included in programs can require significant legal diligence to make sure future potential series work

– A single transaction facilitates using different terms in later deals

• Amendments/Waivers– In a program, the creditors in one series can be outvoted by

majority

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Typical Structure: Program?

“Master” Structure provides Flexibility• Different series can have different tenors and

amortization schedules• Series can be in different currencies (e.g., U.S. Dollars,

Yen, Euros, etc.), though rating agencies, enhancers or others may restrict and/or require hedging

• Series can bear either a fixed or floating interest rate• Series can be “enhanced” (e.g., supported by a

financial guarantee) or “unenhanced” (e.g., not supported by a guaranty)

• Series can be securities offered to investors in several ways (e.g., publicly-registered or traditional private placement) or loans made by traditional bank or other lenders

89

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

90

REMITTANCE (DPR) TRANSACTION

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Typical Structure

91

Typical Structure: DPR Example

Sale of DPRs• In a Diversified Payment Rights (or “DPRs”) program,

a special purpose vehicle (i.e., the SPV) is formed to incur debt secured by the flow of funds arising from the DPRs

• A DPR transaction contemplates a sale of the Bank’s right, title and interest in and under (but none of its obligations under) the Payment Orders and certain bank accounts to the SPV, the purchase of which the SPV finances by incurring debt that is secured by the SPV’s rights in the DPRs, such bank accounts and the proceeds thereof

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

92

Typical Structure: DPR Example

• The Bank retains all of its obligations to make applicable payments to the ultimate beneficiary of a Payment Order

• The sale will be governed by local law (i.e., the law of the Bank’s home jurisdiction)– Using the law of another jurisdiction is not a viable

option if Dollar-denominated DPRs are included since, if the sale is challenged by a third-party, a U.S. court will likely disregard the parties’ choice of law and will apply the law that it views to be most applicable (which likely would be the law of the Bank or U.S. law)

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

93

Typical Structure: DPR Example

Placement of Debt• The SPV may either issue securities or borrow loans in

order to fund its purchase payments to the Bank• If securities, notes may be offered in several ways:– Public offering

– Private placement to investors, including 144A

– Private placement to a “conduit”• If a loan, loans may be made in typical ways:– Syndicated loans

– Bilateral loans

– Loans from a “conduit”

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

94

Typical Structure: DPR Example

Legal/Transaction Issues• True Sale • Government and other Approvals • Conflicts • Others

– Account Agreements

– Credit Enhancers

– Rating Agencies

– Amortization/Defaults

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

95

Typical Structure: DPR Example

True Sale• A transfer of financial assets that, for the purposes of the

insolvency laws of the applicable jurisdiction, constitutes a sale of such assets as distinguished from a financing of the seller thereof secured by such assets

• Removes the financial assets from the bankruptcy estate of the seller

• Necessary to ensure that, upon the insolvency of the Bank, the bankruptcy trustee/administrator would not have any claim to the DPRs

• Somewhat different when applied to a transaction by a bank as opposed to a receivables transaction by an exporter or other corporate entity as insolvency laws for banks are typically quite different than insolvency laws for other companies

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

96

Typical Structure: DPR Example

Approvals• The Bank must obtain any necessary governmental

and other approvals for the securitization of the DPRs (e.g., any Central Bank and shareholder approvals)– In most jurisdictions, including Russia and Turkey, no

governmental approvals have been needed; however, this has not been the case in South Africa and Vietnam

– While only board approvals are required in most jurisdictions, in some ex-CIS countries (e.g., Russia, Azerbaijan) shareholder approval has been considered necessary due to the size of the assets involved

• Local external and in-house counsel opine that all necessary approvals have been obtained

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

97

Typical Structure: DPR Example

Conflicts• The Bank must investigate whether the DPR

transaction would violate any existing agreement of the Bank, such as “negative pledge” or “non-disposal” covenants in outstanding eurobond or loan facilities. Particularly for covenants in eurobonds, this can require a detailed analysis.– This is traditionally a more clear analysis for true sale

structures but pledge structures (such as in Russia) have traditionally required a number of waivers of negative pledge clauses. While a small few number of law firms are aware of how to draft a negative pledge to work for a future flow transaction, the vast majority do not (and “form” loan and other agreements generally do not do so satisfactorily)

• Foreign and local external and in-house counsel will need to opine that there are no conflicts with relevant existing contractual obligations of the Bank

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Typical Structure: DPR Example

DPRs: Crisis Experience• Future flow transactions in emerging markets, especially

DPR transactions, continued to perform strongly through global crisis in credit markets starting in 2008

• Rating Agencies continued to rate DPRs highly during crisis based upon several indicators including:– DSCR ratio (overcollateralization)– Strong trapping mechanism

• Kazakh Case Studies– KKB

• Rating “soft” early amortization– BTA

• Rating “soft” early am and various other events, including nationalization

– Alliance• Numerous events, including nationalization

98

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

99

Is the typical structure a good fit in the Asian context?• For institutions with sufficient flows and the ability to

reach investment grade, the typical structure is ideal• However, in some cases:

– Remittance volumes may be too low to support a standard structure economically or sustainably; or the remittances may not be getting channeled through formal means and thus cannot be harnessed optimally

• Setting up a transaction incurs upfront costs, which needs to be justified by a reasonable issuance size

• The size of the debt supported by the structure should not be an overwhelming amount compared to the total liabilities of the originating entity

• If the transaction size is too big, this may adversely impact the rating,

• Likewise, if the transaction risks the diversion of too much foreign currency, this may attract sovereign interference

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Typical Structure: Asian Context

100

Is the typical structure a good fit in the Asian context?• In some cases it is possible, however, in others:

– The legal analysis on whether the traditional structure would work may not be not clear

• Is the country legal framework open to securitization? • Can it contemplate the sale of future assets? • How robust is the enforceability of creditors’ rights? • How much government involvement is required at each

step of setting up the transaction? • How would the future flow creditors rank compared to the

other creditors of the originating entity? – The rating uplift may not hit investment grade

• If the rating does not reach investment grade, the capital charges that the investors would face will need to be considered when evaluating whether to proceed with a rating or not

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Typical Structure: Asian Context

101

Alternatives

102

Alternatives

Is a typical structure more than is needed?• Companies and local courts might struggle with more

complex documents

• Though some do, local laws usually do not explicitly contemplate “true sales” of future assets– Sale/pledge of “future” assets?

• Is pledge more familiar and thus “safer”?

– How taxed (e.g., taxes on sales but not financings)?• Are tax rules easier for a pledge (e.g., in Russia)?

– How accounted for?

• Can deal size support transaction costs?

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Alternatives: Secured Loan

• An alternative is a direct loan secured by the “future flow” assets

• Advantages include simplicity, lower transaction costs and clearer application of tax-preferred status of the ADB and other DFIs

• Disadvantages include greater risk of loss of collateral to preferred creditors, a “stay” of the exercise of remedies, negative pledges and potential re-denomination

103

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

104

Alternatives: Secured Loan

True Sale vs. Secured Loan• Bankruptcy– “True sale” usually better at surviving bankruptcy

• Validity of sale has been confirmed in Kazakhstan, Turkey, Brazil and all other DPR jurisdictions other than Russia (in which a pledge is used, though primarily driven by tax reasons)

• Most civil law jurisdictions require simply: (a) an agreement of sale, (b) sufficient identification of the sold assets and (c) consideration– Some jurisdictions require specific identification and

potentially registration of each sold asset, making a sale of future assets challenging

– Security for secured loan may be subject to super-priority claims (e.g., taxes, wages or depositors)• Can use a “covered bond”-type structure?

– Re-denomination, etc. for a loan?

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

105

Alternatives: Secured Loan

True Sale vs. Secured Loan• Negative pledge or asset disposal restrictions?– Quantitative limits in covenants may guide structure

(e.g., use of a “partial sale”)• Level of recourse– Sometimes limited in “true sale” transactions, but this is

less true for “future flow” financings than for asset-backed securitizations

• Enforcement– “True sale” facilitates exercise of remedies against assets

solely offshore whereas remedies for a loan:• may be “stayed” by bankruptcy proceedings, including

accrual of interest• are more likely to require home jurisdiction proceedings

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

What considerations are there in structuring a deal?• Does the local law recognize the elements of the deal?

– Bank’s ownership of assets recognized?– “true sale” recognized?

• Regulatory approvals required?• Tax considerations?• Enforcement considerations?• Originator’s ability to provide detailed historical data?• Originator’s existing contractual limitations?

– Negative pledges/asset disposal clauses?

106

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Alternatives: Structuring Decisions

Investor perceptions of different structures• True sale vs pledge structures

– Legal position typically clearer in true sale vs pledge– Uncertainty in enforceability may make pledge structures

more expensive• Rated vs unrated

– Issuances achieving investment grade ratings will price better than unrated issuances

– Ratings provide the opportunity to scale pricing according to changes in the rating

• Listing – Not typically a requirement, unless required for domestic

structures

107

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Alternatives: Investor Considerations

Investor perceptions of different structures• SPV issuances in the form of bonds vs loans

– Bond issuances may be more easily traded; loan structures may be more intended for take-and-hold

– Bond issuances have mark-to-market requirements while loans do not

– Investing entities might have different departments capable of investing in different products with different intentions, i.e. one in bonds vs another loans

– Withholding taxes might be preferable for loan structures vs bonds

– However, in some jurisdictions the securitization framework may only be able to contemplate SPVs issuing bonds and not loans

108

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Alternatives: Investor Considerations

109

What alternative structures might fit better in the Asian context?

• Secured rather than true sale• Loan over bond• Single currency issuances• Rated transactions if investment grade achievable• Supported by a guarantee from a DFI• Focus on key remittances, but include wider range of flows to

support volumes if necessary• 3-5 year tenors, with a view to stretch to longer tenors once

established or for particular investors

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Alternatives: Asian Context

110

Role of Government

111

What can governments due to facilitate these transactions?The single most common challenge in creating these transactions is trying to fit it into the local legal environment, which usually will not have laws and regulations in place that have anticipated such a transaction.

• Appropriate legal, tax and regulatory framework• Appropriate accounting treatment• Provide education for regulators and local banks• Give investors confidence in reliability and efficiency of local

court system• Demonstrate confidence in such structures by securitizing

assets owned by governments that use the concepts and mechanisms employed for traditional remittance structures (e.g., airport fly-over receivables)

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Role of Government

112

Appropriate legal, tax and regulatory frameworkREMITTANCE-SPECIFIC

• Does the local law recognize a bank’s ownership of (and ability to transfer) the payment rights for remittances?

• Does the local law permit a current sale of future assets, including to offshore purchasers?– Many securitization laws only anticipate purely domestic sales and sales

of existing assets.• What mechanics are required for a sale?

– Notices required to obligors? Consents from obligors?– Required specificity of identification of sold assets?

• Are regulatory approvals required for a transaction?• Are banks permitted to sell/pledge assets, including offshore

bank accounts?

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Role of Government

113

Appropriate legal, tax and regulatory frameworkTAX

• Does the local tax law permit such sales to an SPV without the seller incurring transfer, income, VAT or other taxes?

• Does the local tax law impose any stamp taxes on any of the contracts?

• Does the local tax law minimize or eliminate withholding taxes for payments to offshore investors?

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Role of Government

114

Appropriate accounting treatment• How should deal be reflected on unconsolidated balance

sheet?– REMEMBER: There are no/few current receivables

• Does accounting treatment differ from tax treatment?

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Role of Government

115

Provide education for regulators and local banks• Seminars on details of these transactions• Information on benefits the transactions provide to the local

economy• Demonstrate support and commitment by issuing clear

statements on matters that are unresolved and simplifying the approval processes

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Role of Government

116

Confidence in reliability and efficiency of local court system• Are judges well-educated and independent from the

government?• Do local courts honor the choice of foreign laws to govern a

contract?• Do local courts honor foreign court judgments?• Can foreign investors enforce their rights in local courts or is a

local enforcement agent required?• Are foreign parties treated by the courts the same as local

parties?• Can foreign language documents be enforced in a local court

without need for translation?• Do local courts defer to higher courts’ judgment or can each

judge reach an independent decision?

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Role of Government

117

Similar Transactions

118

Similar transactions can only benefit a country• True “future flow” transactions

– Airline ticket receivables– Utilities receivables

• Committed “future flow” transactions– Off-take contracts for oil or other commodities– Concession agreement receivables

• Hybrid “future flow” (i.e., limited number of purchasers but no off-take contract)– Commodities– Manufactured exports– Airport landing right receivables– Frequent flyer miles receivables– Port usage fees

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Similar Transactions

119

Similar Transactions

True Future Flow Example: Airline Ticket Receivable Transaction• An airline uses the receivables of certain routes:– The routes are constant revenue generators, stable and are

deemed strategically important

– Sales are denominated in Dollars or other hard currencies

– There are strong trade, commercial and/or cultural relationships between the points of the routes and the airline enjoys a dominant market share between the destinations

– Sales are routed through third party collection agencies

– The yield of the routes is strong

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

120

Similar Transactions

Committed Future Flow Example: Concession or Royalty Agreement Transaction• An entity has the right to receive royalty or concession

payments from a third party (e.g., a hydropower exporter or a special economic zone operator)– Ideally the royalty or concession payments are independent of

any performance obligations, or the concession payments are stable in nature

– Sales are denominated in Dollars or other hard currencies

– There are not many alternatives for the obligor to source in place of the product or service

– The obligor is better rated than the originator

– The contract tenor is at least as long as the debt tenor, or has a very high likelihood of being renewed

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

121

Similar Transactions

Hybrid Future Flow: Airport Landing Fee Transaction• An airport operator has the right to charge fees to airlines

and passengers for landing rights and aeronautical services provided at the airports that it operates– While there may not be any fixed contracts between the

operator and the airlines, there is a high likelihood that the airlines that currently fly to such airports will continue to operate flights to those airports

– Sales are denominated in Dollars or other hard currencies

– The airport operator enjoys a significant market share and there are not many viable alternative airports that can be used

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

122

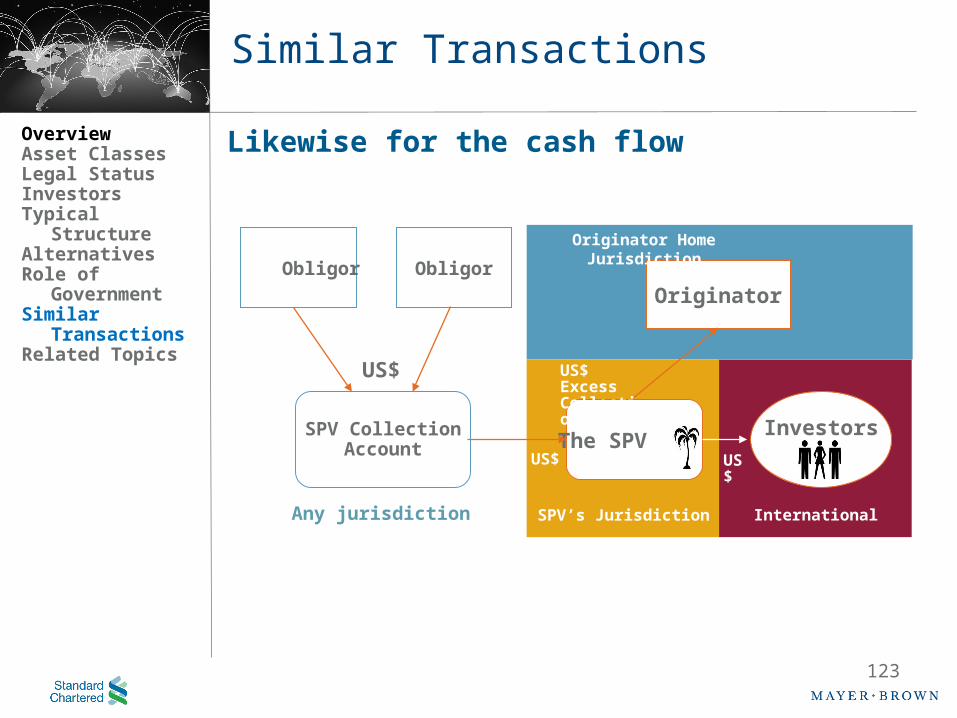

Transaction Structures

(1) The originator sells its rights to the future receivables to the SPV.

(2) The SPV purchases the receivables by obtaining funding from investors.

(3) Collections from the receivables are used first to service the SPV’s debt. Excess collections are repaid by the SPV to the originator via a subordinated note as part of the consideration for the purchase of the receivables.

The basic transaction structure is the same throughout

SPV

Originator

Investors

SPVs Jurisdiction

Multi-Country

OfferedNotes

Exporter’sCountry

1

2

3

US$

SubordinatedNote

US$

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Sale of receivables

Debt issued

123

y

Likewise for the cash flow

Originator

Any jurisdiction

SPV CollectionAccount The SPV

SPV’s Jurisdiction

US$

Obligor

InvestorsUS$

US$

Originator Home Jurisdiction

International

Obligor

US$ Excess Collections

Similar Transactions

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

124

Common risks• Generation– Will originating entity stay in business?

– Will goods or services continue to be competitive?

– Can the good or service be diverted or be replaced?

– Will volumes and prices remain stable?• Collection– Are obligors / customers creditworthy? Might customers

change in future?

– How easy is it to enforce on collections• Diversion– Is nationalization or expropriation a risk?

– Might governments restrict or change the business?

– Might government require that payments be made to or through it?

Similar Transactions

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

125

Similar Transactions

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

What are the differences? • Certainty of future cashflows– Contractually highest for the committed future flows, provided

performance risk of originator is protected against

– Lowest for true future flow• Legal analysis required for structure– Likely to be most straightforward for committed future flows

– More complex for true future flows• Debt service coverage ratios expected by investors– Lower levels required for committed future flows

– Highest expected for true future flows

126

Similar transactions can only benefit a country by:• Establishing the framework for how to deal with sales of

future assets• Familiarizing transaction counterparties in the country with

the practices of securitization • Developing originator interest • Developing investors awareness and familiarity

Future flow transactions need not be cross-border in nature, local currency assets can also be used for domestic transactions.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

Similar Transactions

127

Related Topics

128

Operational Requirements for the Bank• Computer Systems/Monitoring• Historical Data• Accounting

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

129

Computer Systems/Monitoring

• The Bank must have the technological capability to produce the periodic servicer reports required under the Servicing Agreement

• The Bank must have systems with sufficient redundancy (back-up) to satisfy credit enhancers, rating agencies and investors

• Monitoring of money-laundering and related laws

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

130

Historical Data

• To market and rate DPR-backed debt, the Bank will typically need three years (ideally five) of detailed historical information on its Payment Order business on a quarterly and monthly basis

• Stability/diversity of the Bank’s flows and quality of historical information

• Breakdown of historical flows by customer, industry, identity, purpose, remitting bank, etc.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

131

Accounting Issues

• The SPV might be consolidated with the Bank (even though it is not a subsidiary) due to “control/auto-pilot” accounting rules – both under local accounting rules and (in particular) under IFRS (SIC 12). The Bank should discuss this with its auditors.

• The debt of the SPV in closed deals has been noted in the unconsolidated balance sheet of the originator either: (a) as a long-term debt or (b) as a non-debt liability, such as a prepayment for sold items or an obligation to pay Payment Orders to beneficiaries.

• The Bank’s local accountants will need to be involved in the structuring of the transaction to determine the appropriate accounting under local GAAP.

OverviewAsset ClassesLegal StatusInvestorsTypical StructureAlternativesRole of GovernmentSimilar TransactionsRelated Topics

132

Q&A

Thank You!

133

Wan Ning LieDirector, Capital Market Solutions

Standard Chartered Bank

Jim PattiPartner

Mayer Brown LLP