life & health insurance

TRANSCRIPT

Nerina age 42, paralyze as a result of motorbike accident 5 years ago. She is

proposing for a RM 250,000 endowment policy.

SNH ©

Age

• Stage 2

Paralyse downwards

• Paraplegia

Medical report from the doctor

• Current medical status

• How bad

• Past history

• Other illnesses

• Effect

SNH ©

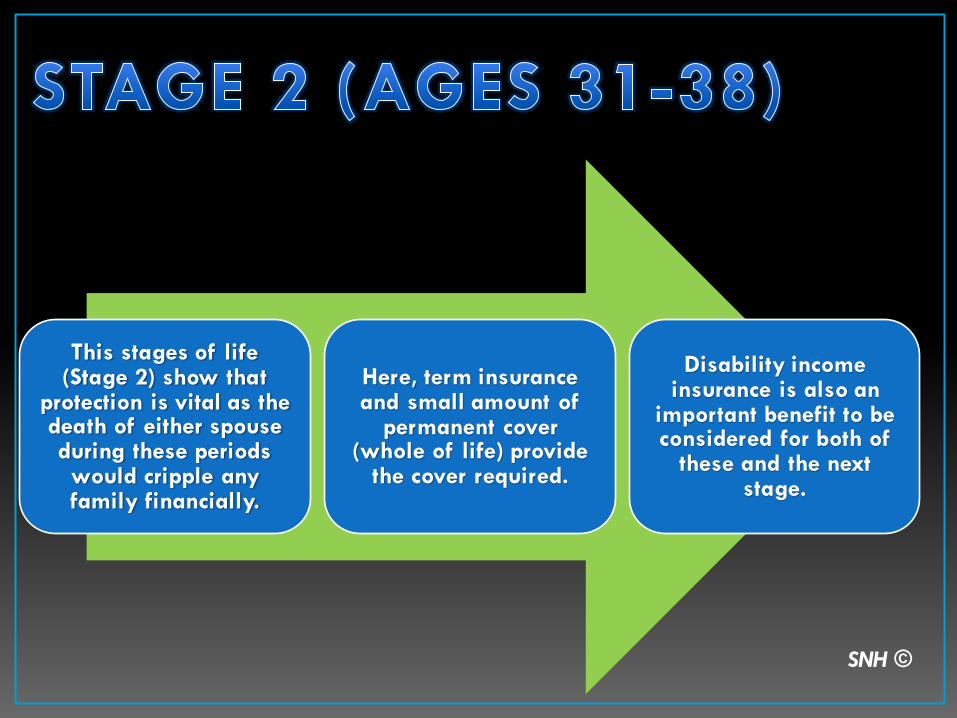

This stages of life (Stage 2) show that

protection is vital as the death of either spouse during these periods would cripple any family financially.

Here, term insurance and small amount of

permanent cover (whole of life) provide

the cover required.

Disability income insurance is also an

important benefit to be considered for both of

these and the next stage.

SNH ©

Paraplegia, paralysis of the lower part of the body, commonly affecting both legs and often internal organs below the waist.

When both legs and arms are affected, the condition is called quadriplegia.

Paraplegia and quadriplegia are caused by an injury or disease that damages the spinal cord, and consequently always affects both sides of the body.

SNH ©

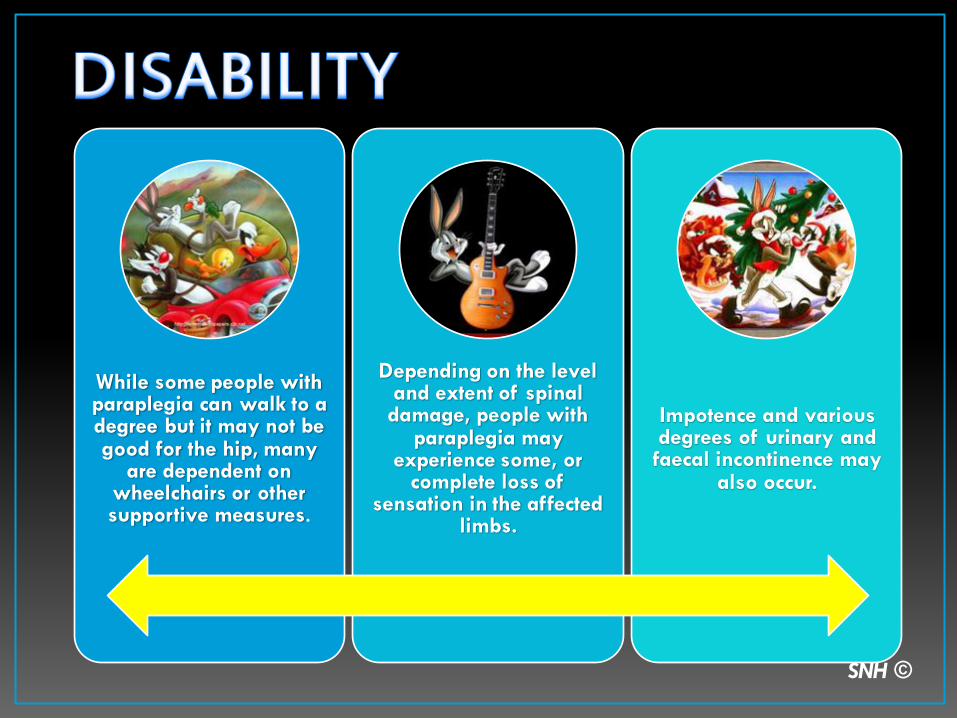

While some people with paraplegia can walk to a degree but it may not be good for the hip, many

are dependent on wheelchairs or other supportive measures.

Depending on the level and extent of spinal damage, people with

paraplegia may experience some, or

complete loss of sensation in the affected

limbs.

Impotence and various degrees of urinary and faecal incontinence may

also occur.

SNH ©

Due to the decrease or loss of feeling or function in the

lower extremities, paraplegia can contribute to a number of medical complications including

pressure sores (decubitus), thrombosis, and

pneumonia.

Physiotherapy and various assistive technologies, such

as a standing frame, as well as vigilant self-

observation and care, may aid in helping to prevent future complications and

mitigate existing complications.

SNH ©

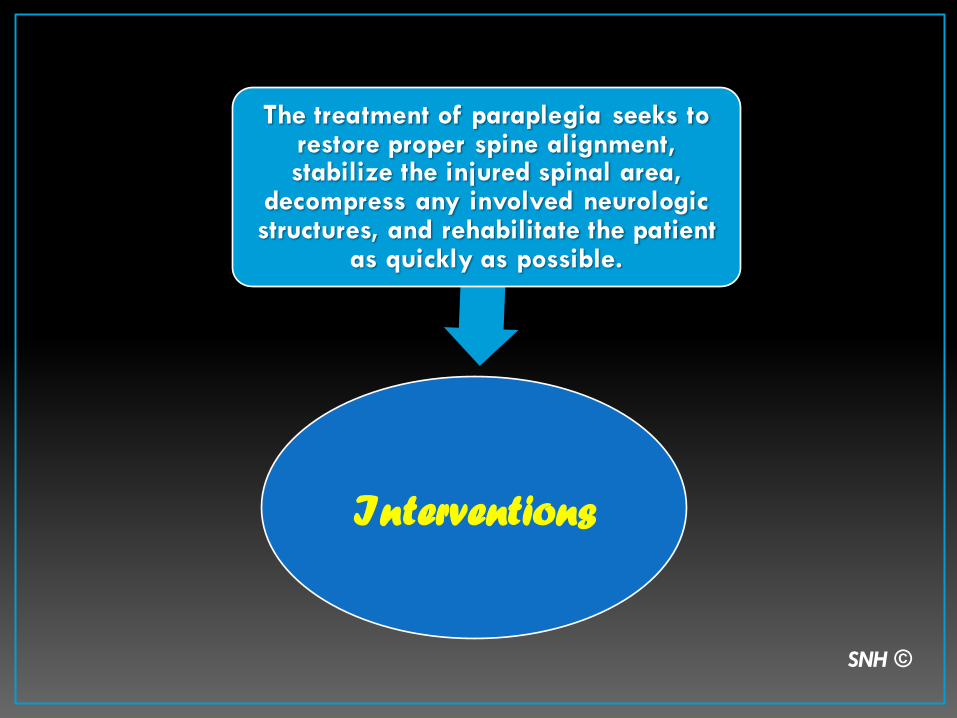

Interventions

The treatment of paraplegia seeks to restore proper spine alignment, stabilize the injured spinal area,

decompress any involved neurologic structures, and rehabilitate the patient

as quickly as possible.

SNH ©

When the paraplegic patient progresses from bed rest to use of a wheelchair, the nurse is alert to any

signs of orthostatic hypotension.

Special binders and ant embolism hose are used to help the patient

adjust to the transition from bed to wheelchair.

Prevention of pressure sores is an important priority.

SNH ©

Because rehabilitation is the ultimate goal for a paraplegic patient,

the patient care during the early stages of the

disorder must be particularly concerned

with preventing complications that may

stand in the way of successful

rehabilitation.

These complications include pressure ulcers, respiratory disorders,

orthopedic deformities, urinary tract infections

or calculi, and gastrointestinal

disorders.

The psychological and emotional aspects of paraplegia also must

be considered.

SNH ©

The type of bed used and the positioning of the patient with paraplegia will depend on the cause and extent of the paralysis and the preference of the health care provider.

Patients with spinal cord injuries may be placed in traction or the spinal cord may be hyperextended by placing the patient's head at the foot of the bed and adjusting the bed.

SNH ©

Hypostatic pneumonia and other respiratory problems are

guarded against by deep breathing exercises.

The patient should be protected from respiratory infections, such as the COMMON COLD, which can have serious complications in a paraplegic who is confined

to bed.

SNH ©

Until the patient is allowed out of bed and

can engage in some form of physical activity, range of motion EXERCISES for

all joints should be performed frequently.

Proper positioning of the feet and legs will help prevent contractures,

footdrop, and ankylosis.

A program of therapeutic EXERCISE, including passive and active

exercises, is initiated to maintain any remaining muscle function and to restore as much muscle activity in the affected

parts as possible.

SNH ©

URINARY TRACT INFECTIONS and the formation of CALCULI, particularly in the bladder, present real problems for the patient with paralysis.

If there is no control over urination, an indwelling CATHETER may be the technique of choice for keeping the patient dry, but it also predisposes to infection.

A thorough assessment of the patient's status and potential for achieving bladder control should be made before a final choice is made.

SNH ©

A flaccid bowel produces abdominal distention and predisposes the patient to

faecal impaction.

The patient may have faecal INCONTINENCE as

well as frequent accumulations of flatus

and faecal material in the lower intestine.

Rehabilitation of the patient then requires

working out some method of bowel control so that regularity of defecation can be accomplished.

SNH ©

There are two types of spinal cord injuries.

Complete spinal cord injuries refer to the types of injuries

that result in complete loss of function below the level of the

injury.

While incomplete spinal cord injuries are those that result in

some sensation and feeling below the point of injury. SNH ©

Quadriplegia

Spinal Tuberculosis

Syphilis

Spinal Tumors

Multiple Sclerosis

Poliomyelitis

SNH ©

OCCUPATION

FINANCIAL SITUATION

SNH ©

Rasheed a solicitor age 25, participates in motor sports and hill climbing. He is

proposing for RM 100,000 personal accident insurance.

SNH ©

HOBBY AMOUNT PROPOSE OCCUPATION

AGE & FINANCIAL

TERM/SPECIAL

TERM

MEDICAL

SNH ©

YOUNG FINANCIAL

FINANCIAL HISTORY

CURRENT EARNING STUCTURE

FINANCIAL DOCUMENT

SNH ©

FINANCIAL

HAZARD

SNH ©

CLASS EXAMPLE

Class 1 – Minimal accident/health risk - Professional, administrative, clerical

workers.

Class 2 – Slight accident/health risk - Moderate level of manual work; semi-

skilled occupations involving a small

level of manual work.

Class 3 – Moderate accident - Skilled occupations of a predominantly

manual nature.

Class 4 – Appreciable accident - Certain unskilled occupations in which

the physical and moral hazards appears

acceptable.

SNH ©

LOADING • Increase

premium

EXCLUSION • Cover local

only

SPECIAL TERM • How often

• Do not cover during competition

SNH ©

WHERE

• LOCAL

• INTERNATIONAL

HOW OFTEN

• HOBBY

• REPRESENT COUNTRY

INTERNATIONAL

• MORE HAZARD

SNH ©

INTERNATIONAL

WIND

SNOW

SURFACE

MOTOR

SNH ©

MEDICAL HISTORY

MEDICAL REPORT

CRITICAL ILLNESS

SNH ©

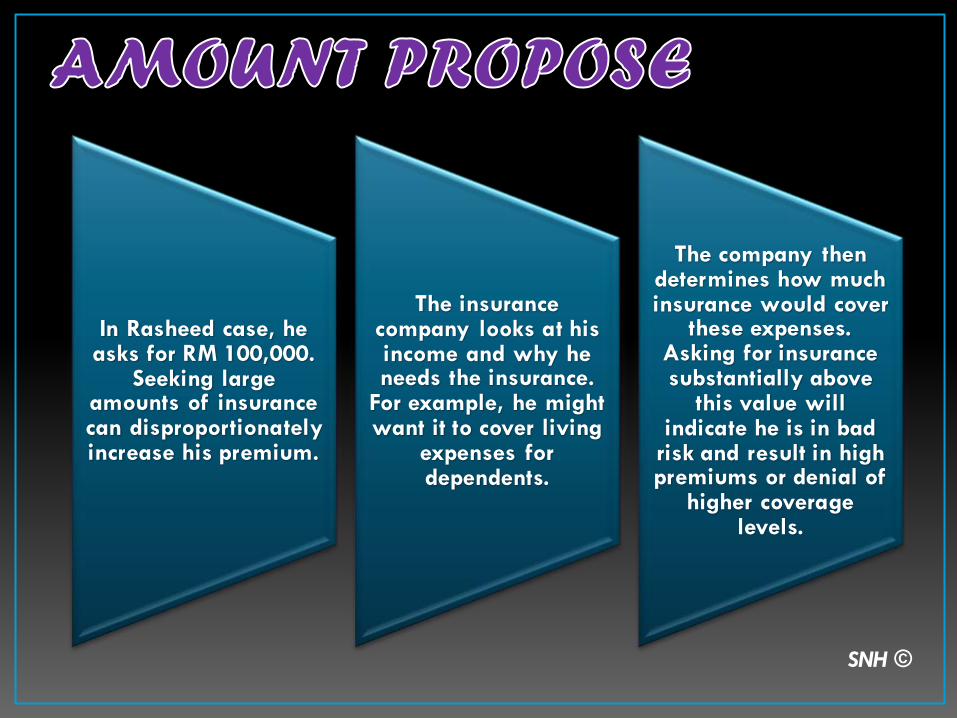

In Rasheed case, he asks for RM 100,000.

Seeking large amounts of insurance can disproportionately increase his premium.

The insurance company looks at his income and why he needs the insurance.

For example, he might want it to cover living

expenses for dependents.

The company then determines how much insurance would cover

these expenses. Asking for insurance substantially above

this value will indicate he is in bad

risk and result in high premiums or denial of

higher coverage levels.

SNH ©

Credit to my great friends Muhammad Hamdi Puteh, Norazuin Jonit and Natasha Ismail!!

Credit to Google images

Credit to http://www.pptbackgroundstemplates.com

SNH ©