lifemarketers presents the abc ’ s of disability

TRANSCRIPT

LifeMarketers

PresentsThe ABC’s of Disability

The Sales Process Understand the Client’s Occupation

Develop the Need

Highlight Policy Benefits

Help the premium fit financially

Understand the Client’s Occupation

What does your client actually do during the day

What are his or her “substantial and material duties”

How is Your Client Paid?

Base Income (W-2)

Bonus (W-2)/Commissions (1099)

Profits (Schedule K-1 or Form 1120)

Residual Income

Fact Gathering Age/DOB

Group LTD Plan

waiting period/benefit period

% income covered

maximum monthly benefit

definition of earnings

Savings

Expenses

Describe to me what you would

like to see happen if you could not

work for a period of time

Why Disability Income Protection

Your clients need the protection

Effect on the family

Effect on the client

Effect on society

Mortgage foreclosures - 48% due to disabilities according to the U.S. Housing Authority (1984)

Potential effect on small business/employment

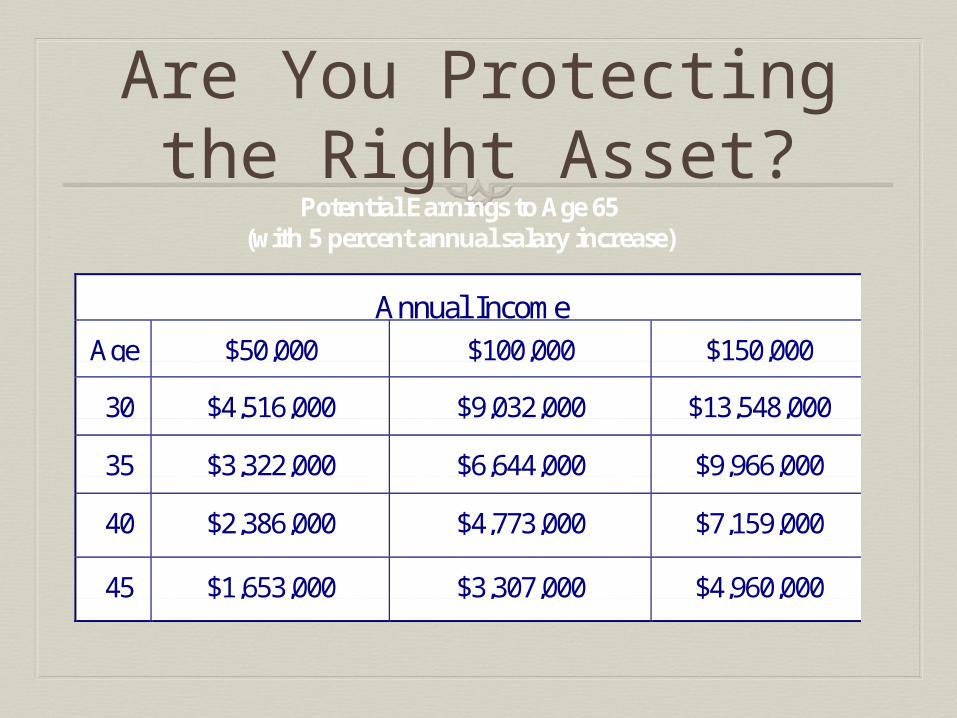

Are You Protecting the Right Asset?

Potential Earnings to Age 65(with 5 percent annual salary increase)

Annual IncomeAge $50,000 $100,000 $150,000

30 $4,516,000 $9,032,000 $13,548,000

35 $3,322,000 $6,644,000 $9,966,000

40 $2,386,000 $4,773,000 $7,159,000

45 $1,653,000 $3,307,000 $4,960,000

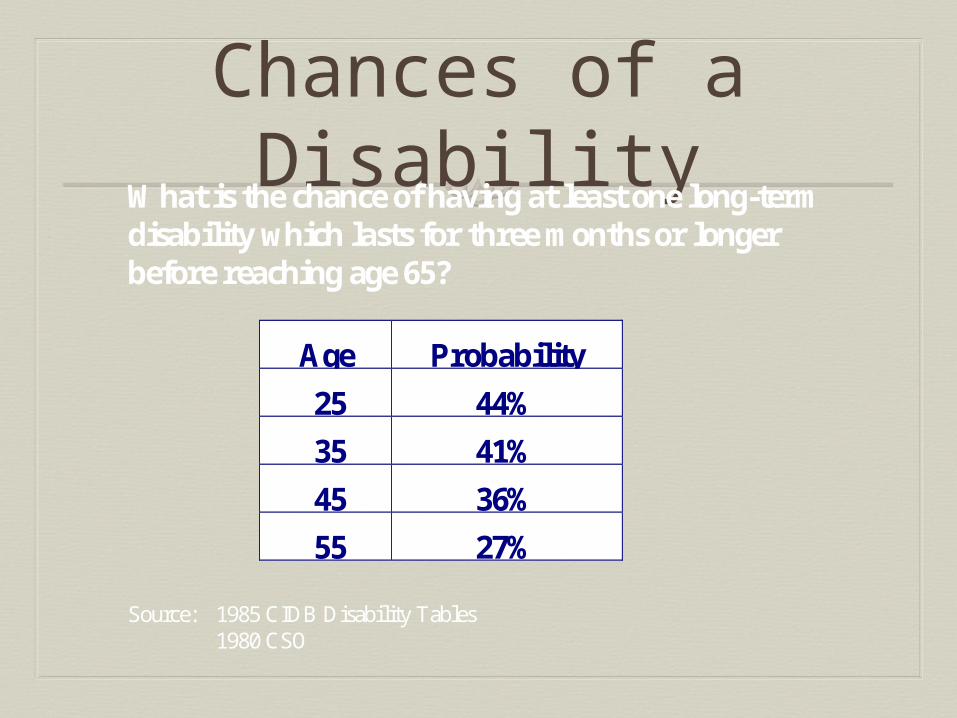

Chances of a DisabilityWhat is the chance of having at least one long-term

disability which lasts for three months or longerbefore reaching age 65?

Age Probability

25 44%

35 41%

45 36%

55 27%

Source: 1985 CIDB Disability Tables1980 CSO

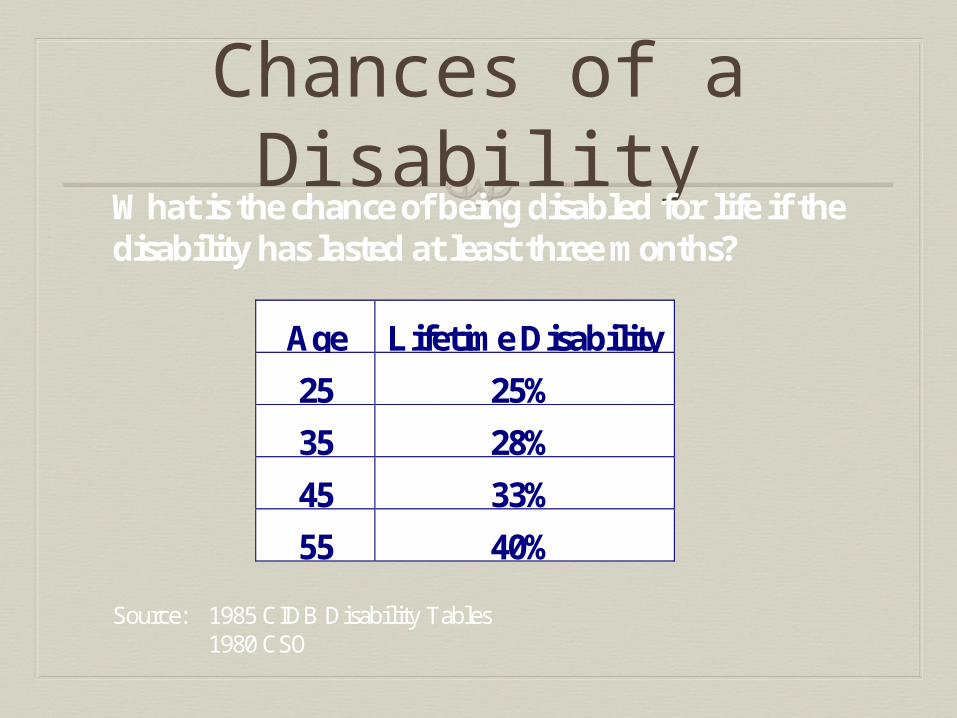

Chances of a Disability

What is the chance of being disabled for life if thedisability has lasted at least three months?

Age Lifetime Disability

25 25%

35 28%

45 33%

55 40%

Source: 1985 CIDB Disability Tables1980 CSO

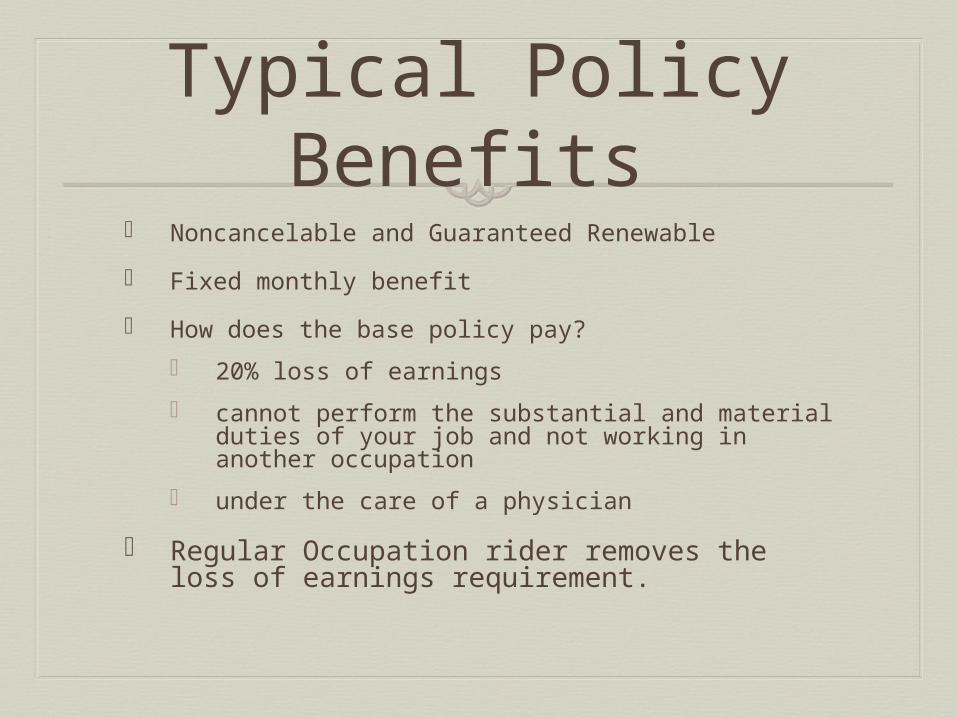

Typical Policy Benefits

Noncancelable and Guaranteed Renewable

Fixed monthly benefit

How does the base policy pay?

20% loss of earnings

cannot perform the substantial and material duties of your job and not working in another occupation

under the care of a physician

Regular Occupation rider removes the loss of earnings requirement.

Understanding the Basics

Benefit Period - how long benefits will be paid

Elimination Period - how long the insured waits before benefits begin

Benefit Amount - the monthly benefit payable under a total disability

Occupation Class - risk class affecting benefits and premium

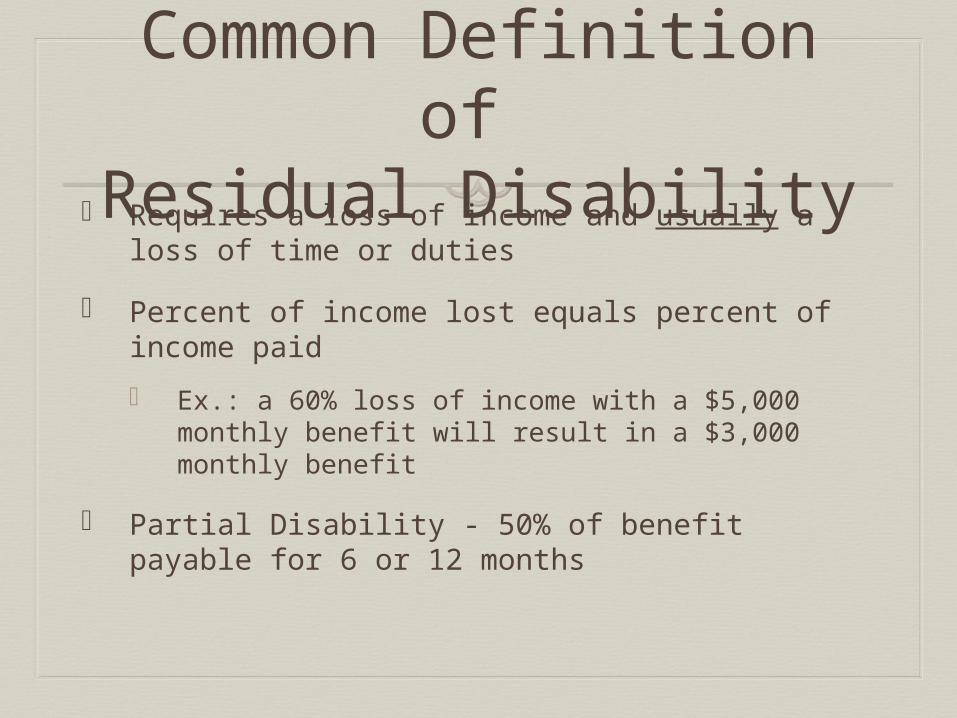

Common Definition of Residual Disability

Requires a loss of income and usually a loss of time or duties

Percent of income lost equals percent of income paid

Ex.: a 60% loss of income with a $5,000 monthly benefit will result in a $3,000 monthly benefit

Partial Disability - 50% of benefit payable for 6 or 12 months

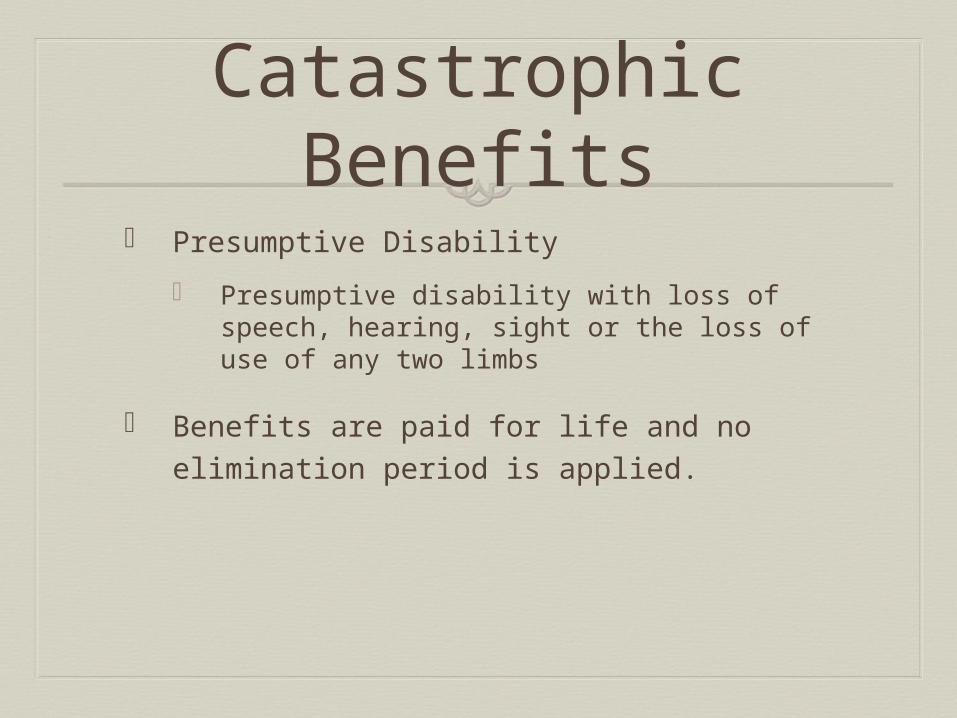

Catastrophic Benefits

Presumptive Disability

Presumptive disability with loss of speech, hearing, sight or the loss of use of any two limbs

Benefits are paid for life and no elimination period is applied.

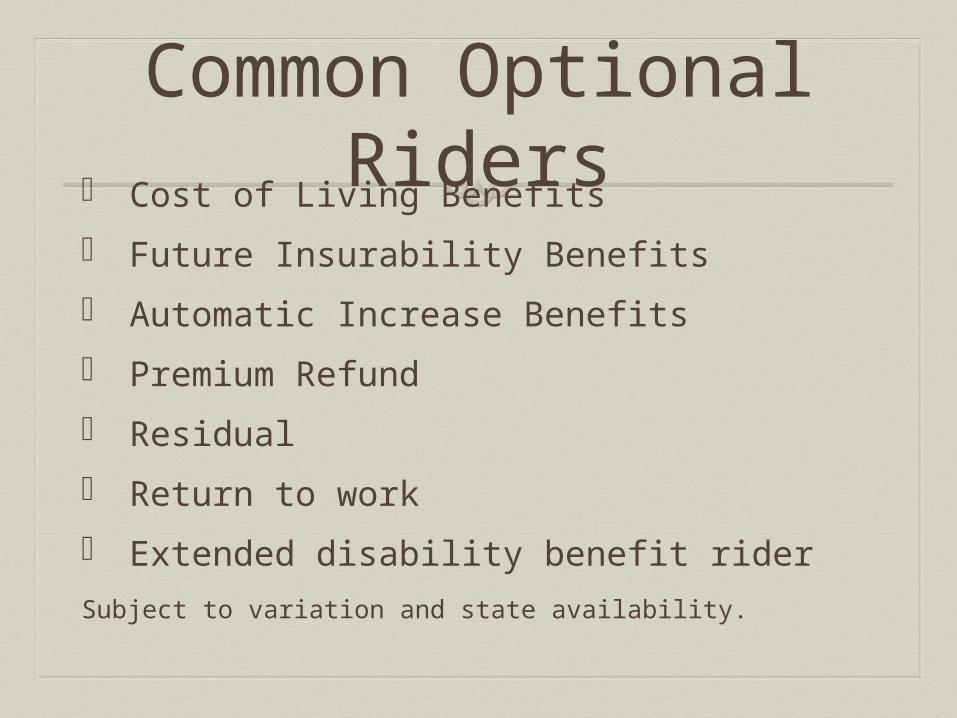

Common Optional Riders Cost of Living Benefits

Future Insurability Benefits

Automatic Increase Benefits

Premium Refund

Residual

Return to work

Extended disability benefit rider

Subject to variation and state availability.

Cost of Living Benefits

Increase the monthly benefit on each anniversary date of the disability

Compounded interest

Has an overall cap of two times the monthly benefit

The younger the client the greater the need.

Future Insurability Benefits

Benefit Update Rider Allows benefits to be increased without re-

qualifying medically. No limit to amount of increase except for maximum issue amount.

Option dates will be every 3 years or by special trigger. Expires at age 55

Triggers that open an early option are loss of group sponsored LTD, reduction of LTD, or change of employment(When purchased on top of Group LTD it acts as a portability rider to the group).

Occupation Classes We are insuring duties not job titles

What is your client’s day like

If any manual duties what are they and what % of time do they represent

Do they have ownership

How many employees

Affects costs and benefit

Tax Consequences Premiums paid with pre-tax dollars - taxable

Premiums paid with after tax dollars -

income tax-free

More than 2% owners of Partnerships, S-Corps, LLC cannot deduct premiums

Example $100,000 income qualifies for $4,800

income tax-free or $5,950 taxable benefits

Assuming 28% marginal tax bracket $4,800 income tax-free benefit is comparable to $6,666 monthly gross income

Medical Underwriting

Common Concerns

Musculoskeletal

Mental/Nervous/Drug/Alcohol

Stress and anxiety counseling

Diabetes

Blood pressure and cholesterol

Attending physician statements

Blood and Urinalysis

Financial Underwriting

What is your client’s net income after business expenses

Complete the income history including bonus and pension contributions

Include signed tax returns with all schedules for business owners

Unearned income

Common Objections

I have savings

My spouse can work

I can do my job from bed

I have protection at work

It costs too much

Savings…What’s It Really Worth?

40 year old with $250,000 in the bank

Assume 20 years of disability with investments accruing at 8%

$1,900 per month will be paid out over 20 years

Can you live on $1,900?

My Spouse Can Work

What does your spouse earn now

Who will take care of you while you are sick? What’s that worth?

If you really don’t need the second income why not take a small percentage of it and ensure the second income continues in the event of disability

Group Long Term Disability

Myth - “It’s cheaper because it’s group”

Typically more conservative benefits

Pre-existing condition limitations

New cost containment provisions

Less adverse selection

Premiums and benefits can be modified

Plans can be canceled

Why Supplement Group LTD

with Individual Policies Benefit may be too low

Benefits are typically taxable

Rates not guaranteed

Usually not portable

Usually conservative definitions

Bonus and Pension benefits may not be covered

Your client needs it

With Benefit update rider you now add portability

Cost

Try to keep premium at 2% or less of

income

90, 180 or 365 day wait

Five year or age 65 benefit period

COLA or not

SSI Integration

Thank YouPresented by

By LifeMarketers800-897-5446