lifetime hoan corporation - library.corporate...

TRANSCRIPT

LIFETIME HOAN CORPORATIONA N N U A L R E P O R T 2 0 0 4

0

50,000

100,000

150,000

$200,000

'00'01'02'03'04

NET SALES(in thousands)

0

10,000

20,000

30,000

40,000

$50,000

'00'01'02'03'04

WORKING CAPITAL(in thousands)

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

$0.80

'00'01'02'03'04

DILUTEDEARNINGS PER COMMONSHARE FROMCONTINUINGOPERATIONS

0

2,000

4,000

6,000

8,000

$10,000

'00'01'02'03'04

INCOME FROMCONTINUINGOPERATIONS(in thousands)

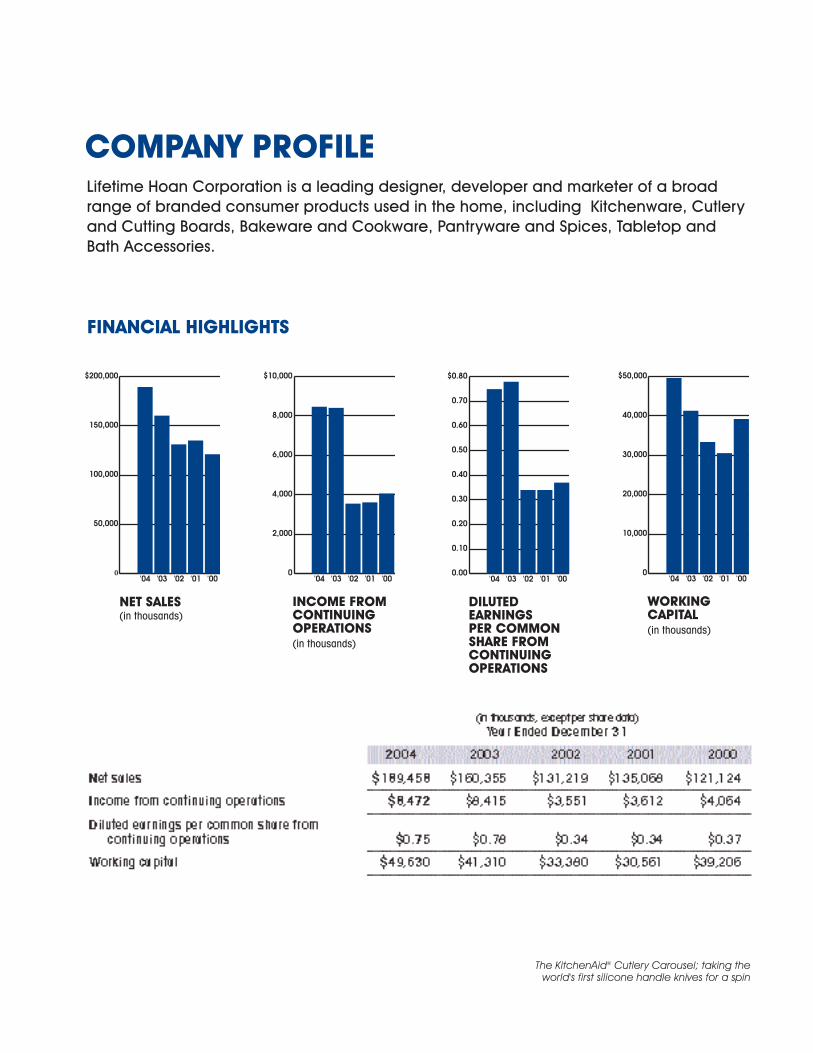

FINANCIAL HIGHLIGHTS

Lifetime Hoan Corporation is a leading designer, developer and marketer of a broadrange of branded consumer products used in the home, including Kitchenware, Cutleryand Cutting Boards, Bakeware and Cookware, Pantryware and Spices, Tabletop andBath Accessories.

COMPANY PROFILE

The KitchenAid® Cutlery Carousel; taking theworld's first silicone handle knives for a spin

During 2004, we took a number of steps to build on the strengths of our proven business model and toposition our Company for future growth. Over the years, the three essential ingredients we have used toforge our leadership position in the housewares industry are:

• An expanding portfolio of powerful brands

• A proven track record of innovation and design excellence

• Superior sourcing capabilities

Our consistent focus on each of these areas has enabled Lifetime to grow and prosper, and, we believe,will continue to provide a solid foundation for our future success.

An Expanding Portfolio of Powerful BrandsLifetime owns or licenses some of the most powerful brands in housewares, enabling us to differentiate ourproduct lines in the eyes of both our retail customers and consumers. Our two top-selling brands areKitchenAid® and Farberware®, which also rank as the #1 and #2 brands in kitchen gadgets and cutlery,according to the HFN 2003 Brand survey.

In 2004, we acquired the business and certain assets of Excel Importing Corp. This acquisition expandedour brand portfolio and, as well, added an important new product category – Tabletop. Among thebrands we acquired was Sabatier®, a highly respected, upper-end brand that we expect will be a keygrowth driver for Lifetime in the years to come.

Proven Track Record of Innovation and Design ExcellenceAt the heart of our Company is a strong culture of new product development and design excellence. Ourunique in-house Product Development and Design Team, consisting of 35 professional designers andengineers, is responsible for creating new products and packaging and merchandising concepts. ThisTeam utilizes state-of-the-art equipment that enables us to shorten product development time, expeditethe production process and “value-engineer” our products.

Lifetime has an impressive record of developing exciting new products. In 2004, we introduced over 600individual products. In addition, we applied for more than 30 utility and design patents over the past two years.

Superior Sourcing CapabilitiesWe have successfully sourced products overseas for more than 40 years. Moreover, we use our productdesign capabilities to help our suppliers to reduce their production costs and to take advantage of lower-cost raw materials. In 2004, we opened a second office in China and hired a Senior Vice President ofSourcing, based in Shanghai.

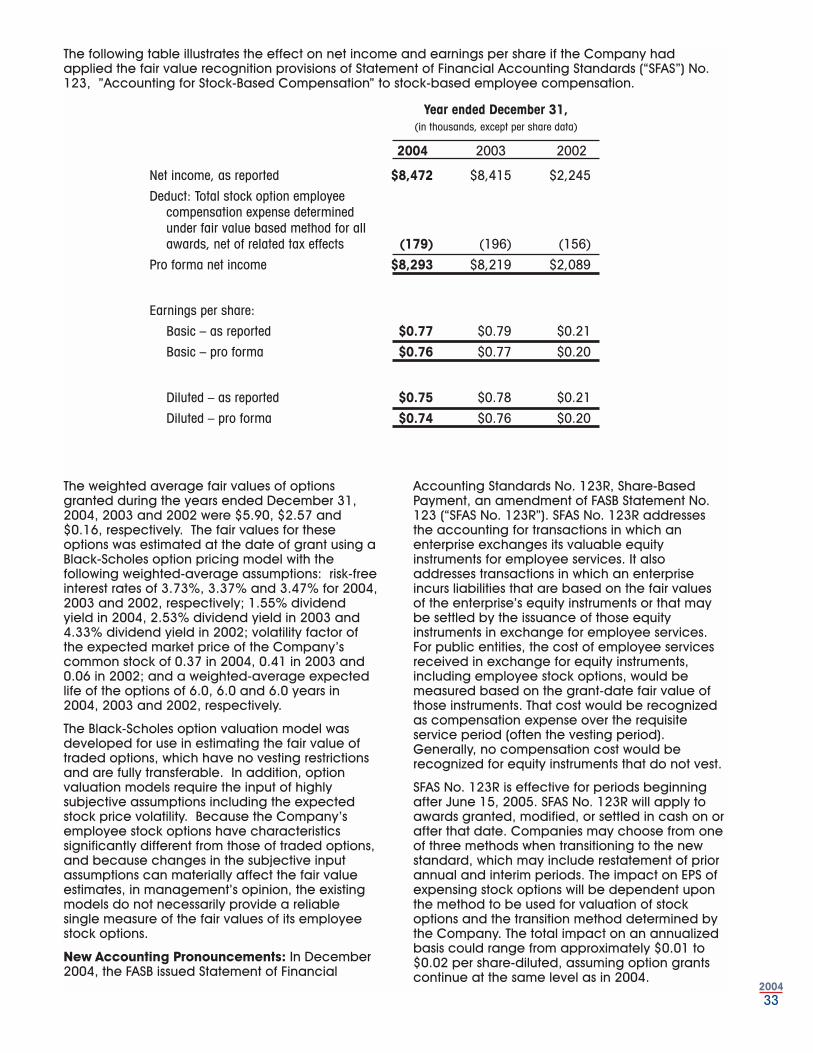

2004 Financial ResultsIn 2004, Lifetime’s net sales totaled a record $189.5 million, an increase of $29.1 million or 18% over 2003.For the year, we reported net income of $8.5 million, compared to $8.4 million for 2003. Earnings perdiluted share for 2004 came to $0.75, compared to $0.78 for 2003.

Net sales in 2004 for the three businesses we acquired over the past 18 months, :USE®, Gemco® and Excel,amounted to $14.3 million. The Company’s organic growth was driven primarily by strong sales across allclassifications of products sold under the KitchenAid® brand.

In 2004, we implemented plans to strengthen our infrastructure. In particular, we bolstered our product

2

DEAR FELLOW SHAREHOLDERS:

2004

32004

LIFETIME HOAN CORPORATION

Jeffrey Siegel

Chairman of the Board, President and Chief Executive Officer

4

Jeffrey Siegel (Chairman, President and CEO) and

Ronald Shiftan (Vice Chairman)

2004

development and design, overseas sourcing and sales and marketing teams. We also added keyexecutives in each of our growing business classifications. Although the increased cost of this infrastructuredid affect the Company’s year-over-year earnings comparison, we believe these additional resources willhave a very positive impact on Lifetime’s long-term growth. In addition, it should be noted that we incurredover $900,000 in expenses related to Sarbanes-Oxley compliance work in 2004, the equivalent of $0.05 in earnings.

As of December 31, 2004, stockholders’ equity was $92.9 million, the equivalent of $8.41 in book value per share.

In summary, 2004 was a successful year for Lifetime during which we implemented many initiatives toexpand our presence in the housewares industry and accelerate our future growth. We broadened ourportfolio of licensed and owned brands, added several new classifications, developed exciting newproducts and pioneered new ways to use materials in our products.

2005 In 2005, we expect our results to reflect the benefits of the initiatives we put into place in 2004.

The goal of broadening our portfolio of powerful brands, continuing to invest in enhancing our ProductDevelopment and Design capabilities, strengthening our overseas sourcing organization and building ourinfrastructure is to be able to create, source and distribute unique products targeted to consumers atdifferent price points in every major level of trade.

For example, in our cutlery and cutting board businesses, the ability to offer products under theKitchenAid®, Cuisinart®, Sabatier®, Farberware®, Hoffritz®, DBK™-Daniel Boulud Kitchen and Laguiole™brands enables us to offer new, innovative higher-value products to which consumers can trade up, as wellas to provide better value and greater selection to consumers at more moderate price points.

We expect that a substantial portion of our growth in 2005 will come from the expansion of our shelf spacein a number of major retailers. At the beginning of the year, for example, we more than doubled our spacewith one of our leading customers for KitchenAid® products. We estimate that the increased space at thisone customer alone should produce over $10 million in additional sales for Lifetime in 2005.

Our results for 2005 should also benefit from the new categories we added in 2004. For example, theTabletop and Cookware categories that we acquired from Excel should contribute significantly in 2005. Wehave redesigned many Excel’s Tabletop lines to bring them in line with our high standards for product andpackaging quality and style.

In closing, we are proposing to change the name of our Company from Lifetime Hoan Corporation toLifetime Brands, Inc., reflecting the crucial role that well-known and well-respected brands play in ourbusiness model. We believe this new name more accurately expresses one of Lifetime’s most importantattributes and key competitive strengths. We look forward to communicating with our shareholders,customers and employees in the future using this new name to reinforce our most fundamental business strategy.

Thank you for your continued support.

Sincerely,

Jeffrey Siegel

Chairman of the Board, President and Chief Executive Officer5

2004

LIFETIME HOAN CORPORATION

Lifetime Hoan Corporation’s growth in 2004 wasmade possible, in large part, by the introductionof over 600 new products. The goal for 2005 is tointroduce no fewer than 700 new items. Thisremarkable achievement reflects our strong in-house product design and developmentcapabilities. Our Product Design andDevelopment Team, consisting of 35 professionaldesigners and engineers, enables us to extendour record of innovation and new productintroductions. This Team utilizes sophisticatedcomputer aided design technology that is alsocapable of creating product prototypes in-house.

Our designers collaborate closely with ourcustomers to create new, innovative and uniqueproducts. We monitor design trends andinnovations in the overall consumer productsindustry and attempt to apply new designconcepts to the categories in which we compete.

We also utilize our design capabilities to help oursuppliers achieve manufacturing efficiencies andwe work with our suppliers to introduce newmanufacturing technologies. We have creatednew ways to shorten development time andspeed up the production process. For example,we use state-of-the-art rapid prototypingmachinery to bring ideas to reality in a fraction ofthe time it would take using traditional modelingmethods. We also employ conceptual 3-Dpresentation, which renders concepts quickly andwith such photorealism that customers canimmediately comprehend the design and offer feedback.

We continue to invest in advanced designequipment, software and continuing education toensure that we stay current with new designtechnologies and capabilities. Together with ourongoing research into materials and materialsscience, these tools allow us to practice disruptivetechnology; designing products that are uniqueand bring a distinct and perceptible value to the consumer.

KITCHENAID®

The success of the KitchenAid® brand continuedduring 2004. We introduced over 130 new

KitchenAid® items in 2004.

Shipments of our new lines of KitchenAid® cutlerycommenced during the 4th quarter. Totaling over60 new items, each of the lines features tempered420J2 steel, a special high-carbon cutlery steelthat can be tapered to a perfect cutting edge.The cutlery is offered in a number of handlematerials to suit every preference: hollow handlestainless steel; super-strong Dupont Delrin®; triple-riveted impact-resistant ABS, and even the world’sfirst line of non-slip silicone. The cutlery is availablein open stock, in full sets and in multi-packs, suchas carving sets and steak knife sets.

Another major KitchenAid® introduction in 2004was the salad spinner. Over a year and a half indevelopment, the salad spinner was a majordesign and engineering challenge. TheKitchenAid® salad spinner requires only one handto control, can be loaded with fruits or vegetableswith no disassembly, has 2 easy-pour spouts fordispensing the extracted water, comes with 3dividers for the main basket, which allowssimultaneous spinning of multiple fruits andvegetables without having them mix together, hasa soft silicone ring on the handle and base toprevent slipping, and a clear 6-quart capacityouter bowl that can be used for both storage and serving.

Specialty tools and gadgets were also a focus forKitchenAid® in 2004. We introduced carrot andpotato peelers that use curved cutlery-grade steelblades that follow the contour of the vegetables,an oversized pancake turner, a specially shapedomelet turner and dual-purpose “turner tongs,”which can be used to effortlessly to flip an omeletor grab a piece of corn on the cob. New sets offood preparation bowls and mixing bowls werealso well received, as were a citrus juicer, gravyseparator, turkey grabbers, cheese and food milland an oversized colander. We also introduced anew line of high heat resistant nylon tools in acountertop ceramic crock as well as a series ofkitchen brushes.

In development for 2005 under the KitchenAid®

brand, is a mandoline slicer, with a unique spring-loaded blade cover system that continually

INNOVATIVE PRODUCT DESIGN AND BRAND MANAGEMENT

62004

Reinventing the wheel with the KitchenAid® Salad Spinner;

one-handed, super-efficient function, with beauty to spare

72004

8

guards the user’s hand from the slicing blade.Other kitchenware items for 2005 will be new all-stainless steel kitchen and serving tools, tools andgadgets featuring brushed stainless steel handlesand a line of copper handle kitchenware withsatin nickel accents. Other innovative products willinclude a fruit slicer with soft grip handles and acookie gun with 16 discs that conveniently storeinside the body of the cookie maker. We are alsoplanning to launch a complete line of KitchenAid®

sink accessories.

Silicone continues to grow as a significant materialin housewares. We introduced the world’s first fullline of silicone tools under the KitchenAid® brand

in 2001. In 2004, we expanded our selection toinclude a unique over-molded silicone trivet,pastry and basting brushes with easy-to-cleanheat resistant silicone bristles, an oversizedsilicone spoon rest and a non-stick coated rollingpin, featuring weighted silicone handles thatautomatically return to the horizontal position. Indevelopment for introduction in early 2005 aretwo lines of silicone handle tools and gadgets,stainless steel and nylon tongs, each featuringsilicone grips and a new series of silicone handlebarbecue equipment featuring heavy-duty zincalloy castings and stainless steel.

In addition to the world-class design, innovation2004

A garden of earthly delights; KitchenAid® rose and sunflower silicone bakeware molds

92004

and unparalleled quality that are the hallmarks ofour line of KitchenAid® products, we have re-introduced color into the kitchen. The initialofferings of KitchenAid® kitchenware were in 8colors, and their success at retail revolutionizedthe look of kitchen accessories and heightenedthe demand for a broader selection. In 2004, weintroduced 8 new colors, ranging from “springbright” to “spice” colors, to tangerine and pink (apercentage of the sales of pink also benefit breastcancer research). This explosion of color has beeneffective at all levels of retail trade and across alllevels of consumer trends.

KitchenAid® silicone bakeware continued toexperience significant sales growth at retail. Weadded 12 more items to our silicone bakewareline in 2004, expanding into more unique shapesand specialty designs and three sizes of siliconebaking mats, perfect for baking prep work or evenas liners for the bottom of ovens. For 2005, wehave created new bakeware designs in silicone,such as a sunflower, a rose, an ornate “fancy”tube cake pan, as well as 4 sets of mini molds,organized in themes such as “holiday” or “animals”.

KitchenAid® metal bakeware continues to remainstrong at retail, with the introduction of 9 newitems for 2004. For this year, we will launch a lineof cast bakeware, featuring remarkably detailedcast sculptures, such as a Tudor Village andVictorian House that can used to create uniquecake designs. We expect this category to be amajor opportunity for growth and already haveanother group of creative designs in the works.

During 2004, we completed the designs for thenew line of KitchenAid® ceramic bakeware, whichwill consist of over 50 items and feature siliconegrips on almost every piece. The ceramicbakeware is oven, broiler, microwave and freezersafe, with oversized handles and featuring abeautiful “wave” pattern design. The silicone gripsallow for ease of handling, cool quickly if left onthe ceramic dishes in the oven, and are colormatched to the bakeware. The line will begin toship in spring of 2005 and the initial response fromretailers is overwhelmingly positive.

In 2005, we also expect to introduce a line of

KitchenAid® brand pantryware, including a spicerack and salt and pepper grinders, featuringceramic grinding mechanisms, in a variety offinishes and colors. We will also debut a papertowel holder, featuring our patented PerfectTear®

technology that enables simple, one-handed use.

FARBERWARE®

Our lineup of Farberware® cutlery and cuttingboards saw key additions in 2004 that quicklybecame major success stories. High value, largepiece-count block sets in triple-riveted lines,including new 14-piece and 23-piece ClassicForged sets were strong sellers, as were the largesets in the new Traditions series. The Japanese-inspired santoku knife, in various sizes,spearheaded sales of all levels of Farberware®

cutlery. Recognizing growing consumerpreferences for darker woods, we have created anew line of Farberware® cutlery with pakka woodhandles. We also brought to market 9 new cuttingboard designs in environmentally-friendly,plantation-grown bamboo, as well as woodboards with stainless steel handles and curvedwood paddle boards.

We introduced over 100 new Farberware® toolsand gadgets, including Farberware® Preferredand Farberware® Commercial, which featuresheavy-duty alloy castings. We createdFarberware® Innovations, perhaps the mostexciting group of Farberware® kitchenware ever tocome to market. Innovations will begin to ship inspring of 2005 and every item will be truly uniquein design and breakthrough in function. There areover 70 original items being developed and over30 will be available by end of the 2nd quarter.

We introduced 24 new Farberware® barbecueitems in 2004; including a silicone handle line ofequipment and tools in both black and red, and anewly designed instant-read digital barbecuethermometer fork. We also have designed aselection of unique Barbecue Innovations itemsthat will be available in 2005, including foldingand adjustable wire cooking grids, as well as abarbecue cutlery set and shears, each inmagnetized holders that can easily attach to the grill.

LIFETIME HOAN CORPORATION

CUISINART®

Cuisinart® cutlery remains the standard-bearer forquality, performance and design. In addition tothe Continental and Ultra Edge lines, we added aTriple-Riveted series in 2004, featuring extra-widebolsters for safety and balance. We also launchedan engineering first, the patented Knife Vault™.The exterior of the Knife Vault™ is designed tocoordinate with the popular Cuisinart® countertopelectrics. The interior houses a complete 15-piececollection of Continental series cutlery. The KnifeVault™ utilizes a revolutionary locking mechanismthat makes it secure to leave on the countertopfor families with children. The Company will beintroducing a second version of the Knife Vault™ in 2005.

KAMENSTEIN®

With the release of over 150 new items, theKamenstein® brand had a number of majorsuccess stories in 2004, including the patentedPerfectTear® paper towel holder. The Companyreleased 10 versions of this unique product, whichuses an internal gearing system that allows forsimple one-handed use. By mid-2005 there will beover 35 versions available in all key basic andtrend colors, as well as the special electroplatedmetal finishes and material combinations found intoday’s kitchens; satin nickel, polished copper,burnished copper, chrome, burnished bronze,distressed black, gum metal, ceramic with wood,and wire in either black or chrome. ThePerfectTear® has transformed the countertoppaper towel holder from a kitchen basic into afunctional and decorative kitchen necessity.

In 2004, Kamenstein® also unveiled the Can-Do™line of colorful and stylish storage products, whichcombine magnetic bulletin boards in 3 sizes, witha variety of round, square, and rectangularcontainers with see-through tops that can be usedto easily sort and store a variety of items, fromspices to desk accessories. There are alsocylindrical-shaped holders, holders for paper,pens and pencils, 3 sizes of magnetic pictureframes, magnetic clips and sets of “reminder”magnets for important events or activities likebirthday parties or doctor’s appointments. For

102004

Genius loves company; the computerized SmartSpice™ rack

with built-in encyclopedia that answers any condiment query

2005, the Company will be offering countertopdisplay units that hold large numbers of theseimpulse-driven items, as well as sets of containers,and magnetic easels that can hold up to 12assorted containers.

Kamenstein® has also developed 12-, 16-, and 18-tin revolving spice racks utilizing magnetic roundtins. Also available are magnetic, rectangular,brushed stainless steel “strips” that can be hungvertically, horizontally, or at an angle to suit anydecorating need, in 3-, 5-, 6-, 9-, and 12-tin spice sets.

Other innovative new products to be sold underthe Kamenstein® brand are wipe dispensercontainers and clean-up kits, which combine aPerfectTear® paper towel holder and a wipedispenser container within a durable plasticcarrying case.

The popularity of the new Twist spice racks for2004 is reflected by the development of 15 newdesigns, mirroring many of the color and materialchoices being utilized in the next generation ofPerfectTear® paper towel holders. Other spiceracks of note are: the 15-jar, 18-jar, and 21-jarTower racks in assorted colors and finishes; a 16-jar and 20-jar stainless steel version of the Tower;Photo Frame spice racks; the nostalgic and novelFerris Wheel spice rack, and a 16-jar multi-stripedbamboo spice rack. Other exciting concepts thatwill be brought to market in the beginning of 2005are a 20-jar flat wire rack in the Chromeworkscollection, a sequel to the unusual Circa spicerack, and the fun Spice Train. Also in 2005, theCompany will begin shipping SmartSpice™, acombination spice rack and cookbook, with over200 recipes all contained in a computerized,portable, digital control module. The rack comeswith 16 premium spices in jars with easy to use siftand pour lids. Kamenstein® bottles all of its spicesin the United States in its own FDA-approvedbottling facility in Massachusetts.

For home organization and back-to-college,Kamenstein® has developed a stainless steelmessage board with a dry erase section, as wellas the Dorm Safe, a unique, compact, lockablesafe for personal items and valuables. These itemswill be available in time for the busy back-to-

school season in the 2nd and 3rd quarters of 2005.

ROSHCO®

Roshco® became a major brand in siliconebakeware in 2004, with a broad assortment of 14items in key colors, highlighted by the exclusivewire carrying “sled” that simplifies the handling ofthe larger silicone items. We will expand theassortment into specialty cake pans, mini bakingand chocolate molds, and set of mini noveltymolds in trend colors for 2005. The Company hasalso designed numerous fondues, multi-functionversions of the S’mores Maker™, a novel icecream serving set that can also be used forvarious desserts and a unique, easy-to-use cookie press.

The Roshco® division had a huge hit in 2004 withdesigns using famous Hershey’s® icons. There weretwo versions of the S’mores Maker™, each using aceramic marshmallow-shaped S’mores burner ona ceramic tray designed to resemble the famousHershey’s® Milk Chocolate bar. There was also aHershey’s® fondue in the shape of the Hershey’s®

Chocolate Kiss. For 2005, the Company will beshipping specialty silicone bakeware items suchas a 6-in-one Hershey’s® Kiss mold, a 6-in-oneHershey’s® Reese’s® Peanut Butter Cup mold, anda 4-in-one Hershey’s® Milk Chocolate Bar mold.There is also an 8-piece Kid’s Baking Set, withsilicone molds, cookie cutters and a mini rolling pin.

CASAMODA™CasaModa™ is as our primary brand for homeentertainment items. This brand features acollection of home entertaining items, such as theS’mores Maker™, the Smokeless Tabletop Griller™and ceramic serveware with candle warmers anddecorative wire stands. We are expanding theCasaModa™ barware collection to include abeautiful leather-covered grouping, a metallicgold and silver series and a unique “light up” lineof products using LED technology.

LIFETIME HOAN CORPORATION

112004

122004

Pièce de résistance; Sabatier® cutlery and kitchenware for the

finest in timeless French design and quality

132004

SABATIER®

In 2004, we acquired a license to distributeproducts under the well-known Sabatier® brand.Known for its heritage of classic French cutlery, wehave expanded the Sabatier® brand to includeFrench-inspired designs in dinnerware, flatware,cutting boards, kitchen tools and gadgets.

A key addition for 2005 will be a full line extensionof the Laguiole™ line, previously available only insteak knives known for their remarkable sharpness,distinctive shape and the famous “bee” insignia.The tremendous success of the contemporaryProSteel, a hollow handle stainless knife, hasproven that the brand has widespread appeal.We have added two new cutlery lines under theProSteel umbrella; one uses soft grip Santoprene®

and the other features never needs sharpeningblades. To compliment the line extension, theCompany will also be introducing both wood andpolypropylene cutting boards with the ProSteelhandle, as well as a full line of over 30 tools,gadgets and barbecue equipment.

We will also be expanding the traditional woodhandle Loire line to include a new cherry woodseries, and will add a full line of Loire tools andgadgets, bringing a French-inspired, updatedlook to wood tools and cutlery for the kitchen.

We are also introducing new patterns of Sabatier®

dinnerware and flatware. Sabatier® has proven tobe a brand with wide appeal. While respected forits classic heritage, retailers and consumers alikefully appreciate the updated and contemporarydesigns of Sabatier® in many categories of housewares.

:USE® - TOOLS FOR CIVILIZATION®

Originated by the renowned designer RobertSonneman, :USE® is an upscale line ofcontemporary bath and lighting products. Manyof the lines are carried by the finest bath anddecorative accessory retailers in America, andare respected for their breakthrough design andunparalleled quality. We acquired :USE® in late2003, and have taken a two-level approach toproduct development for the brand. Whilecontinuing to expand the assortment of product in

the premier lines, we have also developed threegreat collections of exciting, moderately priced,bath, closet, and bedroom storage accessories.We have received very positive feedback from allchannels of distribution for these storageaccessories, with particular interest from thoseaccounts that target the ever-expanding back-to-dorm business.

For 2005, we have introduced WetNets™, acollection of popularly priced, brightly coloredbath and shower accessories, made ofwaterproof nylon netting held within colorfulpolypropylene frames. Oversized and extra-strongsuction cups hold the WetNets™ to any smoothsurface and make installation simple and safe.WetNets™ will be available in many sizes, in sets,as wall-corner units, and in over-the-shower rod models.

JOSEPH ABBOUD ENVIRONMENTS™Joseph Abboud Environments™ takes the samecasual, understated approach to elegant fashionas Joseph Abboud does in his clothing designs. Hiskeen understanding of style, fabric, texture, andcolor, all combine into an updated classic stylethat is as flexible in its approach to dressing atable as it is when outfitting a wardrobe. For 2004,we offered over 50 items in the Abboudcollections of flatware, glassware, placemats,stainless tabletop accessories, candles anddinnerware. Both the South Beach and Ventanacollections were major successes at such upscaleretailers as Bloomingdale’s and Macy’s, and areperfect expressions of the Abboud philosophy. Byutilizing unique combinations of shapes, textures,and materials featuring a metallic “reactiveglaze” on the dinnerware that imparts aremarkable visual depth to the product, theAbboud collections create a fluid approach thatis effective for the entire range of casual to formal entertaining.

We also design and distribute the Kathy IrelandHome® Acafe collections of dinnerware, oven totable ceramics, and wooden serveware. Thedesigns and colors reflect elegant, updated tasteat affordable prices. In 2004, we launched 18items in dinnerware, both in full sets and open

LIFETIME HOAN CORPORATION

142004

stock, in fashion color combinations of terra cottaand mustard, blue and mustard, and brick andmustard. We also introduced 32 oven-to-tableitems, using the same color combinations, andhighlighted by individual accent pieces such aslarge platters or ramekins done in solid colors. Aswith all fine ceramics, the Acafe collection isfreezer, oven, microwave and dishwasher safe.The wood serveware collection features honeytoned wood combined with rich, dark brownscrolled metal accents, and includes a saladbowl set, wine rack, coasters, bread basket, andserving tray.

LIFETIME HOAN CORPORATION

152004

Alternative energy source; Joseph Abboud

Environments™ collection lights up any room

172004

162004

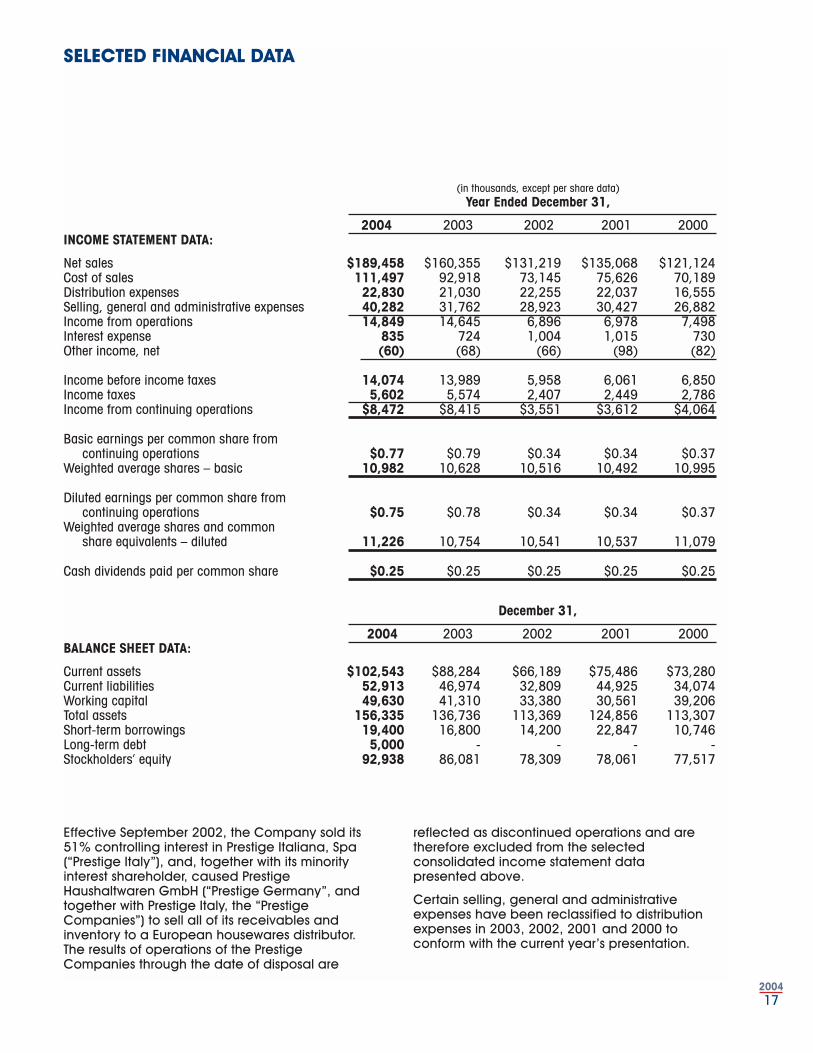

SELECTED FINANCIAL DATA

(in thousands, except per share data)Year Ended December 31,

2004 2003 2002 2001 2000 INCOME STATEMENT DATA:

Net sales $189,458 $160,355 $131,219 $135,068 $121,124 Cost of sales 111,497 92,918 73,145 75,626 70,189Distribution expenses 22,830 21,030 22,255 22,037 16,555Selling, general and administrative expenses 40,282 31,762 28,923 30,427 26,882Income from operations 14,849 14,645 6,896 6,978 7,498 Interest expense 835 724 1,004 1,015 730 Other income, net (60) (68) (66) (98) (82)

Income before income taxes 14,074 13,989 5,958 6,061 6,850 Income taxes 5,602 5,574 2,407 2,449 2,786 Income from continuing operations $8,472 $8,415 $3,551 $3,612 $4,064

Basic earnings per common share from continuing operations $0.77 $0.79 $0.34 $0.34 $0.37

Weighted average shares – basic 10,982 10,628 10,516 10,492 10,995

Diluted earnings per common share from continuing operations $0.75 $0.78 $0.34 $0.34 $0.37

Weighted average shares and common share equivalents – diluted 11,226 10,754 10,541 10,537 11,079

Cash dividends paid per common share $0.25 $0.25 $0.25 $0.25 $0.25

December 31,

2004 2003 2002 2001 2000 BALANCE SHEET DATA:

Current assets $102,543 $88,284 $66,189 $75,486 $73,280 Current liabilities 52,913 46,974 32,809 44,925 34,074 Working capital 49,630 41,310 33,380 30,561 39,206 Total assets 156,335 136,736 113,369 124,856 113,307 Short-term borrowings 19,400 16,800 14,200 22,847 10,746Long-term debt 5,000 - - - - Stockholders’ equity 92,938 86,081 78,309 78,061 77,517

Effective September 2002, the Company sold its51% controlling interest in Prestige Italiana, Spa(“Prestige Italy”), and, together with its minorityinterest shareholder, caused PrestigeHaushaltwaren GmbH (“Prestige Germany”, andtogether with Prestige Italy, the “PrestigeCompanies”) to sell all of its receivables andinventory to a European housewares distributor.The results of operations of the PrestigeCompanies through the date of disposal are

reflected as discontinued operations and aretherefore excluded from the selectedconsolidated income statement data presented above.

Certain selling, general and administrativeexpenses have been reclassified to distributionexpenses in 2003, 2002, 2001 and 2000 toconform with the current year’s presentation.

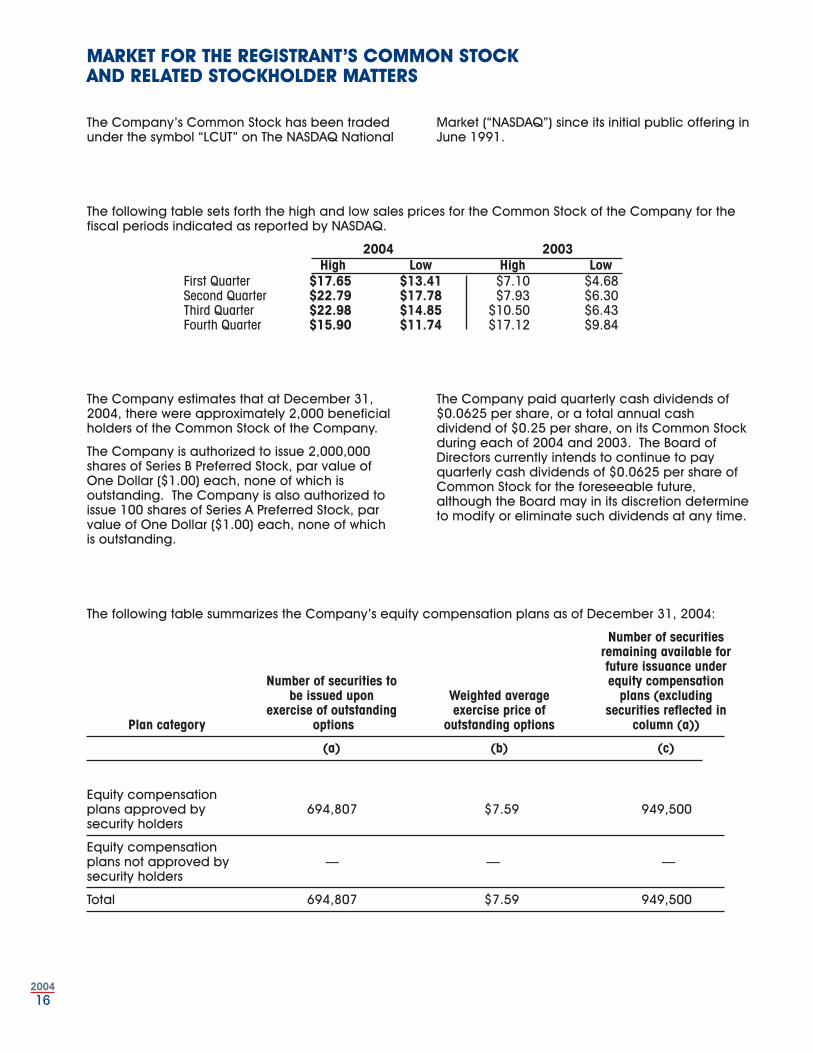

The Company’s Common Stock has been tradedunder the symbol “LCUT” on The NASDAQ National

Market (“NASDAQ”) since its initial public offering inJune 1991.

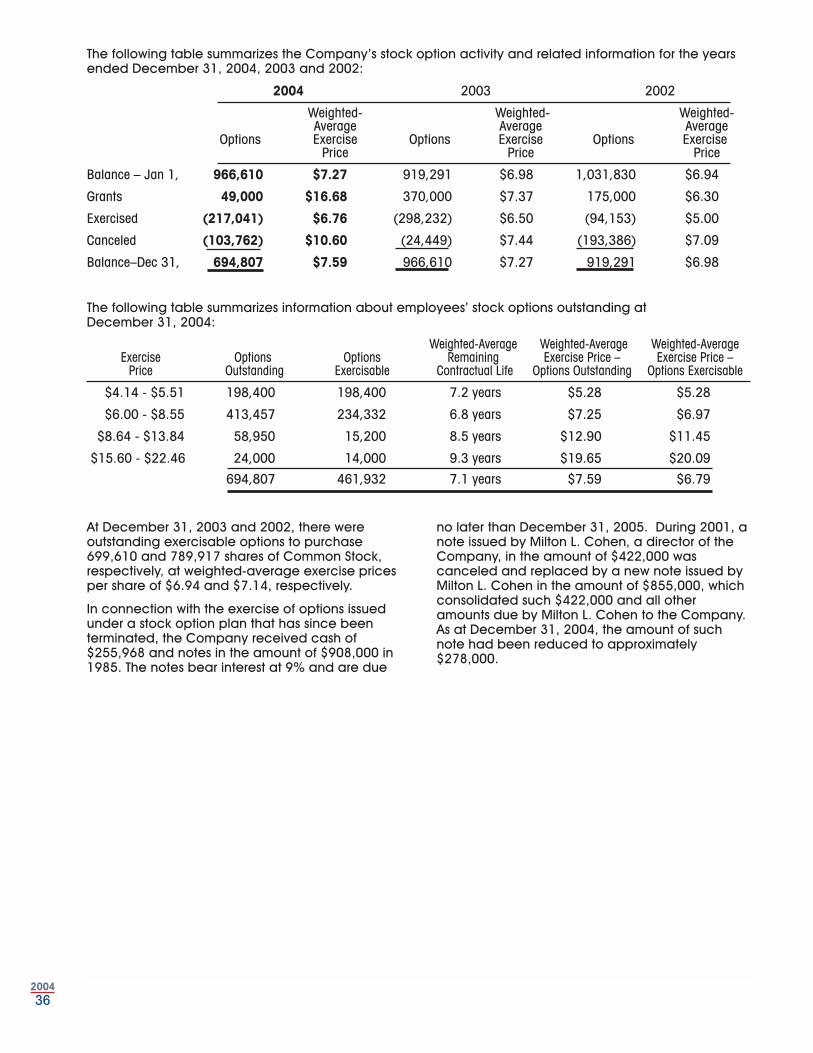

The following table summarizes the Company’s equity compensation plans as of December 31, 2004:

Number of securitiesremaining available forfuture issuance under

Number of securities to equity compensationbe issued upon Weighted average plans (excluding

exercise of outstanding exercise price of securities reflected inPlan category options outstanding options column (a))

(a) (b) (c)

Equity compensationplans approved by 694,807 $7.59 949,500 security holders

Equity compensationplans not approved by — — — security holders

Total 694,807 $7.59 949,500

The following table sets forth the high and low sales prices for the Common Stock of the Company for thefiscal periods indicated as reported by NASDAQ.

2004 2003 High Low High Low

First Quarter $17.65 $13.41 $7.10 $4.68 Second Quarter $22.79 $17.78 $7.93 $6.30 Third Quarter $22.98 $14.85 $10.50 $6.43 Fourth Quarter $15.90 $11.74 $17.12 $9.84

MARKET FOR THE REGISTRANT’S COMMON STOCK AND RELATED STOCKHOLDER MATTERS

The Company estimates that at December 31,2004, there were approximately 2,000 beneficialholders of the Common Stock of the Company.

The Company is authorized to issue 2,000,000shares of Series B Preferred Stock, par value ofOne Dollar ($1.00) each, none of which isoutstanding. The Company is also authorized toissue 100 shares of Series A Preferred Stock, parvalue of One Dollar ($1.00) each, none of which is outstanding.

The Company paid quarterly cash dividends of$0.0625 per share, or a total annual cashdividend of $0.25 per share, on its Common Stockduring each of 2004 and 2003. The Board ofDirectors currently intends to continue to payquarterly cash dividends of $0.0625 per share ofCommon Stock for the foreseeable future,although the Board may in its discretion determineto modify or eliminate such dividends at any time.

172004

162004

SELECTED FINANCIAL DATA

(in thousands, except per share data)Year Ended December 31,

2004 2003 2002 2001 2000 INCOME STATEMENT DATA:

Net sales $189,458 $160,355 $131,219 $135,068 $121,124 Cost of sales 111,497 92,918 73,145 75,626 70,189Distribution expenses 22,830 21,030 22,255 22,037 16,555Selling, general and administrative expenses 40,282 31,762 28,923 30,427 26,882Income from operations 14,849 14,645 6,896 6,978 7,498 Interest expense 835 724 1,004 1,015 730 Other income, net (60) (68) (66) (98) (82)

Income before income taxes 14,074 13,989 5,958 6,061 6,850 Income taxes 5,602 5,574 2,407 2,449 2,786 Income from continuing operations $8,472 $8,415 $3,551 $3,612 $4,064

Basic earnings per common share from continuing operations $0.77 $0.79 $0.34 $0.34 $0.37

Weighted average shares – basic 10,982 10,628 10,516 10,492 10,995

Diluted earnings per common share from continuing operations $0.75 $0.78 $0.34 $0.34 $0.37

Weighted average shares and common share equivalents – diluted 11,226 10,754 10,541 10,537 11,079

Cash dividends paid per common share $0.25 $0.25 $0.25 $0.25 $0.25

December 31,

2004 2003 2002 2001 2000 BALANCE SHEET DATA:

Current assets $102,543 $88,284 $66,189 $75,486 $73,280 Current liabilities 52,913 46,974 32,809 44,925 34,074 Working capital 49,630 41,310 33,380 30,561 39,206 Total assets 156,335 136,736 113,369 124,856 113,307 Short-term borrowings 19,400 16,800 14,200 22,847 10,746Long-term debt 5,000 - - - - Stockholders’ equity 92,938 86,081 78,309 78,061 77,517

Effective September 2002, the Company sold its51% controlling interest in Prestige Italiana, Spa(“Prestige Italy”), and, together with its minorityinterest shareholder, caused PrestigeHaushaltwaren GmbH (“Prestige Germany”, andtogether with Prestige Italy, the “PrestigeCompanies”) to sell all of its receivables andinventory to a European housewares distributor.The results of operations of the PrestigeCompanies through the date of disposal are

reflected as discontinued operations and aretherefore excluded from the selectedconsolidated income statement data presented above.

Certain selling, general and administrativeexpenses have been reclassified to distributionexpenses in 2003, 2002, 2001 and 2000 toconform with the current year’s presentation.

The Company’s Common Stock has been tradedunder the symbol “LCUT” on The NASDAQ National

Market (“NASDAQ”) since its initial public offering inJune 1991.

The following table summarizes the Company’s equity compensation plans as of December 31, 2004:

Number of securitiesremaining available forfuture issuance under

Number of securities to equity compensationbe issued upon Weighted average plans (excluding

exercise of outstanding exercise price of securities reflected inPlan category options outstanding options column (a))

(a) (b) (c)

Equity compensationplans approved by 694,807 $7.59 949,500 security holders

Equity compensationplans not approved by — — — security holders

Total 694,807 $7.59 949,500

The following table sets forth the high and low sales prices for the Common Stock of the Company for thefiscal periods indicated as reported by NASDAQ.

2004 2003 High Low High Low

First Quarter $17.65 $13.41 $7.10 $4.68 Second Quarter $22.79 $17.78 $7.93 $6.30 Third Quarter $22.98 $14.85 $10.50 $6.43 Fourth Quarter $15.90 $11.74 $17.12 $9.84

MARKET FOR THE REGISTRANT’S COMMON STOCK AND RELATED STOCKHOLDER MATTERS

The Company estimates that at December 31,2004, there were approximately 2,000 beneficialholders of the Common Stock of the Company.

The Company is authorized to issue 2,000,000shares of Series B Preferred Stock, par value ofOne Dollar ($1.00) each, none of which isoutstanding. The Company is also authorized toissue 100 shares of Series A Preferred Stock, parvalue of One Dollar ($1.00) each, none of which is outstanding.

The Company paid quarterly cash dividends of$0.0625 per share, or a total annual cashdividend of $0.25 per share, on its Common Stockduring each of 2004 and 2003. The Board ofDirectors currently intends to continue to payquarterly cash dividends of $0.0625 per share ofCommon Stock for the foreseeable future,although the Board may in its discretion determineto modify or eliminate such dividends at any time.

192004

182004

reported amounts of revenues and expensesduring the reporting period. On an on-goingbasis, management evaluates its estimates andjudgments, including those related to inventories.Management bases its estimates and judgmentson historical experience and on various otherfactors that are believed to be reasonable underthe circumstances, the results of which form thebasis for making judgments about the carryingvalues of assets and liabilities that are not readilyapparent from other sources. Actual results maydiffer from these estimates under differentassumptions or conditions. The Company’saccounting policies are more fully described inNote A of the consolidated financial statements.The Company believes that the followingdiscussion addresses the Company’s most criticalaccounting policies, which are those that aremost important to the portrayal of the Company’sconsolidated financial condition and results ofoperations and require management’s mostdifficult, subjective and complex judgments.

Merchandise inventories, consisting principally offinished goods, are priced under the lower-of-cost(first-in, first-out basis) or market method. Reservesfor excess or obsolete inventory reflected in theCompany’s consolidated balance sheets atDecember 31, 2004 and 2003 are determined tobe adequate by the Company’s management;however, there can be no assurance that thesereserves will prove to be adequate over time toprovide for ultimate losses in connection with theCompany’s inventory. The Company’smanagement periodically reviews and analyzesinventory reserves based on a number of factorsincluding, but not limited to, future productdemand of items and estimated profitability of merchandise.

The Company is required to estimate thecollectibility of its accounts receivable. A

considerable amount of judgment is required inassessing the ultimate realization of thesereceivables including the current credit-worthinessof each customer. The Company maintainsallowances for doubtful accounts for estimatedlosses resulting from the inability of its customers tomake required payments. If the financialconditions of the Company’s customers were todeteriorate, resulting in an impairment of theirability to make payments, additional allowancesmay be required.

Effective January 1, 2002, the Company adoptedStatement of Financial Accounting Standard(“SFAS”) No. 141, “Business Combinations” andSFAS No. 142, “Goodwill and Other IntangibleAssets”. SFAS No. 141 requires all businesscombinations initiated after June 30, 2001 to beaccounted for using the purchase method. UnderSFAS No. 142, goodwill and intangible assets withindefinite lives are no longer amortized but arereviewed at least annually for impairment.Accordingly, the Company ceased amortizinggoodwill effective January 1, 2002. For each ofthe years ended December 31, 2004 andDecember 31, 2003, the Company completed itsassessment. Based upon such reviews, noimpairment to the carrying value of goodwill was identified.

Effective January 1, 2002, the Company adoptedSFAS 144, “Accounting for Impairment or Disposalof Long-Lived Assets”. SFAS 144 requires that along-lived asset shall be tested for impairmentwhenever events or changes in circumstancesindicate that its carrying amount may not berecoverable. For each of the years endedDecember 31, 2004 and December 31, 2003, theCompany completed its assessment. Based uponsuch reviews, no impairment to the carrying valueof any long-lived asset was identified.

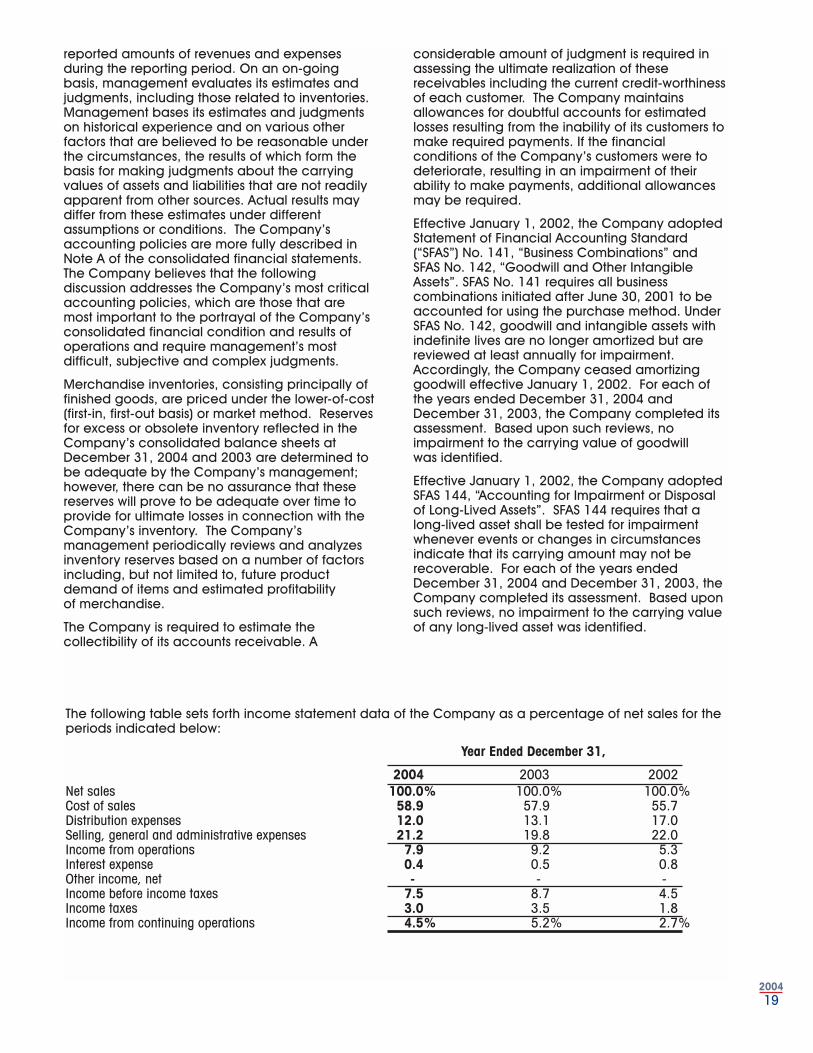

The following table sets forth income statement data of the Company as a percentage of net sales for theperiods indicated below:

Year Ended December 31,

2004 2003 2002 Net sales 100.0% 100.0% 100.0% Cost of sales 58.9 57.9 55.7 Distribution expenses 12.0 13.1 17.0Selling, general and administrative expenses 21.2 19.8 22.0 Income from operations 7.9 9.2 5.3 Interest expense 0.4 0.5 0.8 Other income, net - - -Income before income taxes 7.5 8.7 4.5 Income taxes 3.0 3.5 1.8 Income from continuing operations 4.5% 5.2% 2.7%

RESULTS OF OPERATIONS

General

The following discussion should be read inconjunction with the consolidated financialstatements for the Company and notes theretoincluded elsewhere herein.

OVERVIEWThe Company is a leading designer, developerand marketer of a broad range of brandedconsumer products used in the home, includingKitchenware, Cutlery and Cutting Boards,Bakeware and Cookware, Pantryware and Spices,Tabletop and Bath Accessories. Products aremarketed under brand names includingFarberware®, KitchenAid®, Cuisinart®, Hoffritz®,Sabatier®, DBK™-Daniel Boulud Kitchen, JosephAbboud Environments™, Roshco®, Baker’sAdvantage®, Kamenstein®, CasaModa™, Hoan®,Gemco® and :USE®. The Company uses theFarberware® brand name for kitchenware, cutleryand cutting boards and bakeware pursuant to a200-year royalty-free license. The Companylicenses the KitchenAid®, Cuisinart®, Farberware®

(for flatware and dinnerware), Sabatier®, DBK™-Daniel Boulud Kitchen and Joseph AbboudEnvironments™ trade names pursuant to licensesgranted by the owners of those brands. All otherbrand names listed above are owned. Severalproduct lines are marketed within each of theCompany’s product categories and under brandsprimarily targeting moderate to medium pricepoints, through every major level of trade.

Over the last several years, sales growth has comefrom: (i) expanding product offerings within currentcategories, (ii) developing and acquiring productcategories and (iii) entering new channels ofdistribution, primarily in the United States. Keyfactors in the Company’s growth strategy havebeen, and will continue to be, the selective useand management of strong brands and the abilityto provide a steady stream of new products and designs.

For the year ended December 31, 2004, net saleswere $189.5 million, which represented an 18.1%growth over the previous year. The combined netsales in 2004 for the Gemco®, :USE® and Excelbusinesses that had been acquired during thepast 15 months, were approximately $14.3 millioncompared to $0.6 million in 2003. Excluding theimpact of these acquisitions, net sales for 2004were approximately $175.2 million, a 9.6% growthover 2003. The 9.6% increase in sales wasprimarily attributable to the continuing growth indemand for KitchenAid® branded products andhigher Outlet Store sales, offset by lower sales in

2004 of the Company’s S’mores Maker™. Netsales for the Outlet Stores in 2004 were $15.9million compared to $11.0 million in 2003. Thesales growth for the Outlet Stores was principallyattributable to the Company assumingresponsibility for an additional 20% of the floorspace in each store, effective October 1, 2003.

The Company’s gross profit margin is subject tofluctuation due primarily to product mix and, insome instances, customer mix. In 2004, our grossprofit margin declined as a substantial portion ofour sales growth came from sales of KitchenAid®

branded products, which generate lower marginsdue to the added cost of royalties, and increasedsales of other product lines, including Gemco®

functional glassware and Excel products, thatgenerate lower gross profit margins.

Our operating profit margin declined in 2004 dueto three factors: (i) the $14.3 million in sales for therecently acquired Gemco®, :USE® and Excelbusinesses generated a small operating loss in2004, (ii) the distribution of the Company’sproducts through its outlet stores generated highersales and a larger operating loss in 2004compared to 2003 and (iii)added personnel costsincurred in 2004 to expand the product designgroup, the overseas sourcing department and oursales and marketing departments toaccommodate future growth. In addition, theCompany incurred in excess of $900,000 of directexpenses in 2004 related to Sarbanes-Oxleycompliance work.

The Company’s business and working capitalneeds are highly seasonal, with a significantmajority of sales occurring in the third and fourthquarters. In 2004, 2003 and 2002, net sales for thethird and fourth quarters combined accounted for63%, 66% and 61% of total annual net sales,respectively, and operating profit earned in thethird and fourth quarters combined accounted for92%, 97% and 100% of total annual operatingprofits, respectively. Inventory levels increaseprimarily in the June through October time periodin anticipation of the pre-holiday shipping season.

Critical Accounting Policies and Estimates

Management’s Discussion and Analysis ofFinancial Condition and Results of Operationsdiscusses the Company’s consolidated financialstatements, which have been prepared inaccordance with accounting principles generallyaccepted in the United States. The preparation ofthese financial statements requires managementto make estimates and assumptions that affect thereported amounts of assets and liabilities and thedisclosure of contingent assets and liabilities atthe date of the financial statements and the

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONAND RESULTS OF OPERATIONS

192004

182004

reported amounts of revenues and expensesduring the reporting period. On an on-goingbasis, management evaluates its estimates andjudgments, including those related to inventories.Management bases its estimates and judgmentson historical experience and on various otherfactors that are believed to be reasonable underthe circumstances, the results of which form thebasis for making judgments about the carryingvalues of assets and liabilities that are not readilyapparent from other sources. Actual results maydiffer from these estimates under differentassumptions or conditions. The Company’saccounting policies are more fully described inNote A of the consolidated financial statements.The Company believes that the followingdiscussion addresses the Company’s most criticalaccounting policies, which are those that aremost important to the portrayal of the Company’sconsolidated financial condition and results ofoperations and require management’s mostdifficult, subjective and complex judgments.

Merchandise inventories, consisting principally offinished goods, are priced under the lower-of-cost(first-in, first-out basis) or market method. Reservesfor excess or obsolete inventory reflected in theCompany’s consolidated balance sheets atDecember 31, 2004 and 2003 are determined tobe adequate by the Company’s management;however, there can be no assurance that thesereserves will prove to be adequate over time toprovide for ultimate losses in connection with theCompany’s inventory. The Company’smanagement periodically reviews and analyzesinventory reserves based on a number of factorsincluding, but not limited to, future productdemand of items and estimated profitability of merchandise.

The Company is required to estimate thecollectibility of its accounts receivable. A

considerable amount of judgment is required inassessing the ultimate realization of thesereceivables including the current credit-worthinessof each customer. The Company maintainsallowances for doubtful accounts for estimatedlosses resulting from the inability of its customers tomake required payments. If the financialconditions of the Company’s customers were todeteriorate, resulting in an impairment of theirability to make payments, additional allowancesmay be required.

Effective January 1, 2002, the Company adoptedStatement of Financial Accounting Standard(“SFAS”) No. 141, “Business Combinations” andSFAS No. 142, “Goodwill and Other IntangibleAssets”. SFAS No. 141 requires all businesscombinations initiated after June 30, 2001 to beaccounted for using the purchase method. UnderSFAS No. 142, goodwill and intangible assets withindefinite lives are no longer amortized but arereviewed at least annually for impairment.Accordingly, the Company ceased amortizinggoodwill effective January 1, 2002. For each ofthe years ended December 31, 2004 andDecember 31, 2003, the Company completed itsassessment. Based upon such reviews, noimpairment to the carrying value of goodwill was identified.

Effective January 1, 2002, the Company adoptedSFAS 144, “Accounting for Impairment or Disposalof Long-Lived Assets”. SFAS 144 requires that along-lived asset shall be tested for impairmentwhenever events or changes in circumstancesindicate that its carrying amount may not berecoverable. For each of the years endedDecember 31, 2004 and December 31, 2003, theCompany completed its assessment. Based uponsuch reviews, no impairment to the carrying valueof any long-lived asset was identified.

The following table sets forth income statement data of the Company as a percentage of net sales for theperiods indicated below:

Year Ended December 31,

2004 2003 2002 Net sales 100.0% 100.0% 100.0% Cost of sales 58.9 57.9 55.7 Distribution expenses 12.0 13.1 17.0Selling, general and administrative expenses 21.2 19.8 22.0 Income from operations 7.9 9.2 5.3 Interest expense 0.4 0.5 0.8 Other income, net - - -Income before income taxes 7.5 8.7 4.5 Income taxes 3.0 3.5 1.8 Income from continuing operations 4.5% 5.2% 2.7%

RESULTS OF OPERATIONS

General

The following discussion should be read inconjunction with the consolidated financialstatements for the Company and notes theretoincluded elsewhere herein.

OVERVIEWThe Company is a leading designer, developerand marketer of a broad range of brandedconsumer products used in the home, includingKitchenware, Cutlery and Cutting Boards,Bakeware and Cookware, Pantryware and Spices,Tabletop and Bath Accessories. Products aremarketed under brand names includingFarberware®, KitchenAid®, Cuisinart®, Hoffritz®,Sabatier®, DBK™-Daniel Boulud Kitchen, JosephAbboud Environments™, Roshco®, Baker’sAdvantage®, Kamenstein®, CasaModa™, Hoan®,Gemco® and :USE®. The Company uses theFarberware® brand name for kitchenware, cutleryand cutting boards and bakeware pursuant to a200-year royalty-free license. The Companylicenses the KitchenAid®, Cuisinart®, Farberware®

(for flatware and dinnerware), Sabatier®, DBK™-Daniel Boulud Kitchen and Joseph AbboudEnvironments™ trade names pursuant to licensesgranted by the owners of those brands. All otherbrand names listed above are owned. Severalproduct lines are marketed within each of theCompany’s product categories and under brandsprimarily targeting moderate to medium pricepoints, through every major level of trade.

Over the last several years, sales growth has comefrom: (i) expanding product offerings within currentcategories, (ii) developing and acquiring productcategories and (iii) entering new channels ofdistribution, primarily in the United States. Keyfactors in the Company’s growth strategy havebeen, and will continue to be, the selective useand management of strong brands and the abilityto provide a steady stream of new products and designs.

For the year ended December 31, 2004, net saleswere $189.5 million, which represented an 18.1%growth over the previous year. The combined netsales in 2004 for the Gemco®, :USE® and Excelbusinesses that had been acquired during thepast 15 months, were approximately $14.3 millioncompared to $0.6 million in 2003. Excluding theimpact of these acquisitions, net sales for 2004were approximately $175.2 million, a 9.6% growthover 2003. The 9.6% increase in sales wasprimarily attributable to the continuing growth indemand for KitchenAid® branded products andhigher Outlet Store sales, offset by lower sales in

2004 of the Company’s S’mores Maker™. Netsales for the Outlet Stores in 2004 were $15.9million compared to $11.0 million in 2003. Thesales growth for the Outlet Stores was principallyattributable to the Company assumingresponsibility for an additional 20% of the floorspace in each store, effective October 1, 2003.

The Company’s gross profit margin is subject tofluctuation due primarily to product mix and, insome instances, customer mix. In 2004, our grossprofit margin declined as a substantial portion ofour sales growth came from sales of KitchenAid®

branded products, which generate lower marginsdue to the added cost of royalties, and increasedsales of other product lines, including Gemco®

functional glassware and Excel products, thatgenerate lower gross profit margins.

Our operating profit margin declined in 2004 dueto three factors: (i) the $14.3 million in sales for therecently acquired Gemco®, :USE® and Excelbusinesses generated a small operating loss in2004, (ii) the distribution of the Company’sproducts through its outlet stores generated highersales and a larger operating loss in 2004compared to 2003 and (iii)added personnel costsincurred in 2004 to expand the product designgroup, the overseas sourcing department and oursales and marketing departments toaccommodate future growth. In addition, theCompany incurred in excess of $900,000 of directexpenses in 2004 related to Sarbanes-Oxleycompliance work.

The Company’s business and working capitalneeds are highly seasonal, with a significantmajority of sales occurring in the third and fourthquarters. In 2004, 2003 and 2002, net sales for thethird and fourth quarters combined accounted for63%, 66% and 61% of total annual net sales,respectively, and operating profit earned in thethird and fourth quarters combined accounted for92%, 97% and 100% of total annual operatingprofits, respectively. Inventory levels increaseprimarily in the June through October time periodin anticipation of the pre-holiday shipping season.

Critical Accounting Policies and Estimates

Management’s Discussion and Analysis ofFinancial Condition and Results of Operationsdiscusses the Company’s consolidated financialstatements, which have been prepared inaccordance with accounting principles generallyaccepted in the United States. The preparation ofthese financial statements requires managementto make estimates and assumptions that affect thereported amounts of assets and liabilities and thedisclosure of contingent assets and liabilities atthe date of the financial statements and the

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONAND RESULTS OF OPERATIONS

212004

202004

increase of approximately $19.8 million, or 27.0%more than 2002. Cost of sales as a percentage ofnet sales increased to 57.9% in 2003 from 55.7%in 2002, due primarily to higher sales of licensedbranded products which generate lower marginsdue to the added costs of royalties and a highercost of sales-to-net sales relationship forKamenstein® products in 2003. In addition, theamount of direct import sales increased in 2003.These sales relate to products shipped directlyfrom contract manufacturers to the Company’sretail customers and therefore carry lower grossprofit margins as the pricing of such salesrecognizes that the Company does not incur anywarehousing or distribution costs.

Distribution Expenses

Distribution expenses, which primarily consist ofwarehousing expenses, handling costs of productssold and freight-out expenses, were $21.0 millionfor 2003 as compared to $22.2 million for 2002.These expenses included relocation charges,duplicate rent and other costs associated with theCompany’s move into its Robbinsville, New Jerseydistribution facility amounting to $0.7 million in2003 and $2.2 million in 2002. Excluding thesemoving related costs, distribution expenses were1.2% higher in 2003 as compared to 2002 due tohigher depreciation expense related to capitalexpenditures for the new automated warehousedistribution system and related equipment, offsetby lower payroll costs. As a percentage of netsales, distribution expenses, excluding theaforementioned relocation charges, were 12.7%in 2003 as compared to 15.3% in 2002. Thisimproved relationship reflects the benefits of laborsavings generated by the new systems in ourRobbinsville, New Jersey distribution facility.

Selling, General and Administrative Expenses

Selling, general and administrative expenses for2003 were $31.8 million, an increase of $2.8million, or 9.8%, from 2002. The increase inselling, general and administrative expenses wasprimarily attributable to increased personnelcosts, including planned personnel additions inthe sales and product design departments,increased commission expense related to thehigher sales volume and higher consulting fees.

Interest Expense

Interest expense for 2003 was $0.7 million, adecrease of $0.3 million, or 27.9%, from 2002.The decrease is attributable to a decrease in theaverage level of borrowings outstanding during2003 under the Company’s secured, revolvingcredit facility.

Income Taxes

Income taxes for 2003 were $5.6 million, an

increase of $3.2 million or 131.6%, from 2002. Theincrease in income taxes is directly related to theincrease in income before taxes from 2002 to2003. Income taxes as a percentage of incomebefore taxes remained consistent from year-to-year at approximately 40%.

LIQUIDITY AND CAPITAL RESOURCESThe Company’s principal sources of cash to fundliquidity needs are: (i) cash provided by operatingactivities and (ii) borrowings available under itscredit facility. Its primary uses of funds consist ofcapital expenditures, acquisitions, funding forworking capital increases, payments of principaland interest on its debt and payment of cash dividends.

At December 31, 2004, the Company had cashand cash equivalents of $1.7 million, compared to$1.2 million at December 31, 2003; workingcapital was $49.6 million, compared to $41.3million at December 31, 2003; the current ratiowas 1.94 to 1 compared to 1.88 to 1 at December31, 2003; and borrowings increased to $24.4million at December 31, 2004 compared to $16.8million at December 31, 2003. The increase inworking capital primarily resulted from anincrease in merchandise inventories offset in partby an increase in accounts payable and tradeacceptances and accrued expenses.

Cash provided by operating activities wasapproximately $4.4 million, primarily resulting fromnet income before depreciation, amortization,provisions for losses on accounts receivable andother non-cash charges and increased incometaxes payable offset by increased merchandiseinventories, decreased accounts payable andtrade acceptances and accrued expenses. Cashused in investing activities was approximately $9.9million, which consisted of purchases of propertyand equipment and the cash paid in connectionwith the Excel acquisition. Net cash provided byfinancing activities was approximately $6.0million, primarily as a result of an increase in shortand long-term borrowings and the proceeds fromthe exercise of stock options, offset by cashdividends paid.

Capital expenditures were $2.9 million in 2004and $2.2 million in 2003. Total planned capitalexpenditures for 2005 are estimated at $5.0million. These expenditures are expected to befunded from current operations, cash and cashequivalents and, if necessary, from borrowingsunder the Company’s secured credit facility.

On July 28, 2004, the Company entered into a$50 million five-year, secured credit facility (the“Credit Facility”) with a group of banks and, inconjunction therewith, canceled its $35 millionsecured, reducing revolving credit facility whichwas due to mature in November 2004. Borrowingsunder the Credit Facility are secured by all of the

2004 COMPARED TO 2003

Net Sales

Net sales in 2004 were $189.5 million, an increaseof approximately $29.1 million, or 18.1% higherthan 2003. The combined net sales in 2004 forthe Gemco® and :USE® businesses acquired in thefourth quarter of 2003 and the Excel business thatwas acquired in July 2004, totaled approximately$14.3 million compared to $0.6 million in 2003.The Outlet Stores sales were $15.9 million in 2004compared to $11.0 million in 2003. Excluding thenet sales attributable to the Gemco®, :USE®, andExcel businesses and the Outlet Stores, net salestotaled approximately $159.2 million, a 7.0%increase over 2003’s sales of $148.7 million. Theincrease in sales was primarily attributable toincreased sales of KitchenAid® branded productsin the Company’s kitchenware, bakeware andcutlery product lines and, to a lesser extent,higher sales of its pantryware products. Thesesales increases in 2004 were offset primarily bylower sales of the Company’s S’mores Maker™.Sales of Farberware® and Cuisinart® brandedcutlery and Roshco® branded bakeware alsodeclined in 2004.

The Outlet Stores sales increased to $15.9 millioncompared to $11.0 million in 2003. The OutletStores sales growth was principally attributable tothe Company assuming responsibility for 70% ofthe space in each store, effective October 1,2003, compared to 50% of the space in priorperiods. The Outlet Stores had an operating lossof $1.3 million in 2004, compared to an operatingloss of $1.0 million in 2003.

Cost of Sales

Cost of sales for 2004 was $111.5 million, anincrease of approximately $18.6 million, or 20.0%more than 2003. Cost of sales as a percentage ofnet sales increased to 58.9% in 2004 from 57.9%in 2003, primarily as a result of higher sales ofKitchenAid® branded products which generatelower margins due to the added costs of royaltiesand an increase in sales of other products thatcarry lower gross profit margins, includingGemco® functional glassware products and Excel products.

Distribution Expenses

Distribution expenses, which primarily consist ofwarehousing expenses, handling costs of productssold and freight-out expenses, were $22.8 millionfor 2004 as compared to $21.0 million for 2003.In 2003 these expenses included relocationcharges, duplicate rent and other costsassociated with the Company’s move into itsRobbinsville, New Jersey distribution facilityamounting to $0.7 million. No such expenseswere incurred in 2004. Excluding these movingrelated costs, distribution expenses were 12.3%higher in 2004 as compared to 2003. However, as

a percentage of net sales, distribution expenses,excluding the aforementioned relocationcharges, were 12.0% in 2004 as compared to12.7% in 2003. This improved relationship reflectsprimarily the benefits of labor savings andefficiencies generated by our main distributioncenter in Robbinsville, New Jersey.

Selling, General and Administrative Expenses

Selling, general and administrative expenses for2004 were $40.3 million, an increase of $8.5million, or 26.8%, from 2003. The increase inselling, general and administrative expenses wasprimarily attributable to the following: increasedOutlet Store operating expenses, resulting from theCompany being responsible for 70% of the spaceand expenses of each store for the last threemonths of 2003 and all of 2004 compared to 50%of the space and expenses of each store for thefirst nine months of 2003; additional operatingexpenses of the :USE®, Gemco® and Excelbusinesses recently acquired; the higherpersonnel costs associated with plannedpersonnel increases in the product design group,the overseas sourcing department and sales andmarketing departments and expenses related toSarbanes-Oxley compliance work.

Interest Expense

Interest expense for 2004 was $0.8 million, anincrease of $0.1 million or 15.3%, from 2003.

Income Taxes

Income taxes for each of 2004 and 2003 were$5.6 million. Income taxes as a percentage ofincome before taxes remained consistent fromyear-to-year at approximately 40%.

2003 COMPARED TO 2002

Net Sales

Net sales in 2003 were $160.4 million, an increaseof approximately $29.1 million, or 22.2% higherthan 2002. The increase in sales volume wasattributable primarily to increased shipments ofKitchenAid® branded kitchen tools and gadgetsand bakeware, the Company’s newly designedS’mores Maker™ and Kamenstein®

pantryware products.

The Outlet Stores sales increased to $11.0 millioncompared to $10.3 million in 2002. The OutletStores became responsible for 70% of the spaceand expenses in each store, effective October 1,2003, compared to 50% of the space andexpenses in prior periods. The Outlet Stores hadan operating loss of $1.0 million in 2003,compared to an operating loss of $0.1 million in 2002.

Cost of Sales

Cost of sales for 2003 was $92.9 million, an

212004

202004

increase of approximately $19.8 million, or 27.0%more than 2002. Cost of sales as a percentage ofnet sales increased to 57.9% in 2003 from 55.7%in 2002, due primarily to higher sales of licensedbranded products which generate lower marginsdue to the added costs of royalties and a highercost of sales-to-net sales relationship forKamenstein® products in 2003. In addition, theamount of direct import sales increased in 2003.These sales relate to products shipped directlyfrom contract manufacturers to the Company’sretail customers and therefore carry lower grossprofit margins as the pricing of such salesrecognizes that the Company does not incur anywarehousing or distribution costs.

Distribution Expenses

Distribution expenses, which primarily consist ofwarehousing expenses, handling costs of productssold and freight-out expenses, were $21.0 millionfor 2003 as compared to $22.2 million for 2002.These expenses included relocation charges,duplicate rent and other costs associated with theCompany’s move into its Robbinsville, New Jerseydistribution facility amounting to $0.7 million in2003 and $2.2 million in 2002. Excluding thesemoving related costs, distribution expenses were1.2% higher in 2003 as compared to 2002 due tohigher depreciation expense related to capitalexpenditures for the new automated warehousedistribution system and related equipment, offsetby lower payroll costs. As a percentage of netsales, distribution expenses, excluding theaforementioned relocation charges, were 12.7%in 2003 as compared to 15.3% in 2002. Thisimproved relationship reflects the benefits of laborsavings generated by the new systems in ourRobbinsville, New Jersey distribution facility.

Selling, General and Administrative Expenses

Selling, general and administrative expenses for2003 were $31.8 million, an increase of $2.8million, or 9.8%, from 2002. The increase inselling, general and administrative expenses wasprimarily attributable to increased personnelcosts, including planned personnel additions inthe sales and product design departments,increased commission expense related to thehigher sales volume and higher consulting fees.

Interest Expense

Interest expense for 2003 was $0.7 million, adecrease of $0.3 million, or 27.9%, from 2002.The decrease is attributable to a decrease in theaverage level of borrowings outstanding during2003 under the Company’s secured, revolvingcredit facility.

Income Taxes

Income taxes for 2003 were $5.6 million, an

increase of $3.2 million or 131.6%, from 2002. Theincrease in income taxes is directly related to theincrease in income before taxes from 2002 to2003. Income taxes as a percentage of incomebefore taxes remained consistent from year-to-year at approximately 40%.

LIQUIDITY AND CAPITAL RESOURCESThe Company’s principal sources of cash to fundliquidity needs are: (i) cash provided by operatingactivities and (ii) borrowings available under itscredit facility. Its primary uses of funds consist ofcapital expenditures, acquisitions, funding forworking capital increases, payments of principaland interest on its debt and payment of cash dividends.

At December 31, 2004, the Company had cashand cash equivalents of $1.7 million, compared to$1.2 million at December 31, 2003; workingcapital was $49.6 million, compared to $41.3million at December 31, 2003; the current ratiowas 1.94 to 1 compared to 1.88 to 1 at December31, 2003; and borrowings increased to $24.4million at December 31, 2004 compared to $16.8million at December 31, 2003. The increase inworking capital primarily resulted from anincrease in merchandise inventories offset in partby an increase in accounts payable and tradeacceptances and accrued expenses.

Cash provided by operating activities wasapproximately $4.4 million, primarily resulting fromnet income before depreciation, amortization,provisions for losses on accounts receivable andother non-cash charges and increased incometaxes payable offset by increased merchandiseinventories, decreased accounts payable andtrade acceptances and accrued expenses. Cashused in investing activities was approximately $9.9million, which consisted of purchases of propertyand equipment and the cash paid in connectionwith the Excel acquisition. Net cash provided byfinancing activities was approximately $6.0million, primarily as a result of an increase in shortand long-term borrowings and the proceeds fromthe exercise of stock options, offset by cashdividends paid.

Capital expenditures were $2.9 million in 2004and $2.2 million in 2003. Total planned capitalexpenditures for 2005 are estimated at $5.0million. These expenditures are expected to befunded from current operations, cash and cashequivalents and, if necessary, from borrowingsunder the Company’s secured credit facility.

On July 28, 2004, the Company entered into a$50 million five-year, secured credit facility (the“Credit Facility”) with a group of banks and, inconjunction therewith, canceled its $35 millionsecured, reducing revolving credit facility whichwas due to mature in November 2004. Borrowingsunder the Credit Facility are secured by all of the

2004 COMPARED TO 2003

Net Sales

Net sales in 2004 were $189.5 million, an increaseof approximately $29.1 million, or 18.1% higherthan 2003. The combined net sales in 2004 forthe Gemco® and :USE® businesses acquired in thefourth quarter of 2003 and the Excel business thatwas acquired in July 2004, totaled approximately$14.3 million compared to $0.6 million in 2003.The Outlet Stores sales were $15.9 million in 2004compared to $11.0 million in 2003. Excluding thenet sales attributable to the Gemco®, :USE®, andExcel businesses and the Outlet Stores, net salestotaled approximately $159.2 million, a 7.0%increase over 2003’s sales of $148.7 million. Theincrease in sales was primarily attributable toincreased sales of KitchenAid® branded productsin the Company’s kitchenware, bakeware andcutlery product lines and, to a lesser extent,higher sales of its pantryware products. Thesesales increases in 2004 were offset primarily bylower sales of the Company’s S’mores Maker™.Sales of Farberware® and Cuisinart® brandedcutlery and Roshco® branded bakeware alsodeclined in 2004.

The Outlet Stores sales increased to $15.9 millioncompared to $11.0 million in 2003. The OutletStores sales growth was principally attributable tothe Company assuming responsibility for 70% ofthe space in each store, effective October 1,2003, compared to 50% of the space in priorperiods. The Outlet Stores had an operating lossof $1.3 million in 2004, compared to an operatingloss of $1.0 million in 2003.

Cost of Sales

Cost of sales for 2004 was $111.5 million, anincrease of approximately $18.6 million, or 20.0%more than 2003. Cost of sales as a percentage ofnet sales increased to 58.9% in 2004 from 57.9%in 2003, primarily as a result of higher sales ofKitchenAid® branded products which generatelower margins due to the added costs of royaltiesand an increase in sales of other products thatcarry lower gross profit margins, includingGemco® functional glassware products and Excel products.

Distribution Expenses

Distribution expenses, which primarily consist ofwarehousing expenses, handling costs of productssold and freight-out expenses, were $22.8 millionfor 2004 as compared to $21.0 million for 2003.In 2003 these expenses included relocationcharges, duplicate rent and other costsassociated with the Company’s move into itsRobbinsville, New Jersey distribution facilityamounting to $0.7 million. No such expenseswere incurred in 2004. Excluding these movingrelated costs, distribution expenses were 12.3%higher in 2004 as compared to 2003. However, as

a percentage of net sales, distribution expenses,excluding the aforementioned relocationcharges, were 12.0% in 2004 as compared to12.7% in 2003. This improved relationship reflectsprimarily the benefits of labor savings andefficiencies generated by our main distributioncenter in Robbinsville, New Jersey.

Selling, General and Administrative Expenses

Selling, general and administrative expenses for2004 were $40.3 million, an increase of $8.5million, or 26.8%, from 2003. The increase inselling, general and administrative expenses wasprimarily attributable to the following: increasedOutlet Store operating expenses, resulting from theCompany being responsible for 70% of the spaceand expenses of each store for the last threemonths of 2003 and all of 2004 compared to 50%of the space and expenses of each store for thefirst nine months of 2003; additional operatingexpenses of the :USE®, Gemco® and Excelbusinesses recently acquired; the higherpersonnel costs associated with plannedpersonnel increases in the product design group,the overseas sourcing department and sales andmarketing departments and expenses related toSarbanes-Oxley compliance work.

Interest Expense

Interest expense for 2004 was $0.8 million, anincrease of $0.1 million or 15.3%, from 2003.

Income Taxes

Income taxes for each of 2004 and 2003 were$5.6 million. Income taxes as a percentage ofincome before taxes remained consistent fromyear-to-year at approximately 40%.

2003 COMPARED TO 2002

Net Sales

Net sales in 2003 were $160.4 million, an increaseof approximately $29.1 million, or 22.2% higherthan 2002. The increase in sales volume wasattributable primarily to increased shipments ofKitchenAid® branded kitchen tools and gadgetsand bakeware, the Company’s newly designedS’mores Maker™ and Kamenstein®

pantryware products.

The Outlet Stores sales increased to $11.0 millioncompared to $10.3 million in 2002. The OutletStores became responsible for 70% of the spaceand expenses in each store, effective October 1,2003, compared to 50% of the space andexpenses in prior periods. The Outlet Stores hadan operating loss of $1.0 million in 2003,compared to an operating loss of $0.1 million in 2002.

Cost of Sales

Cost of sales for 2003 was $92.9 million, an

232004

222004

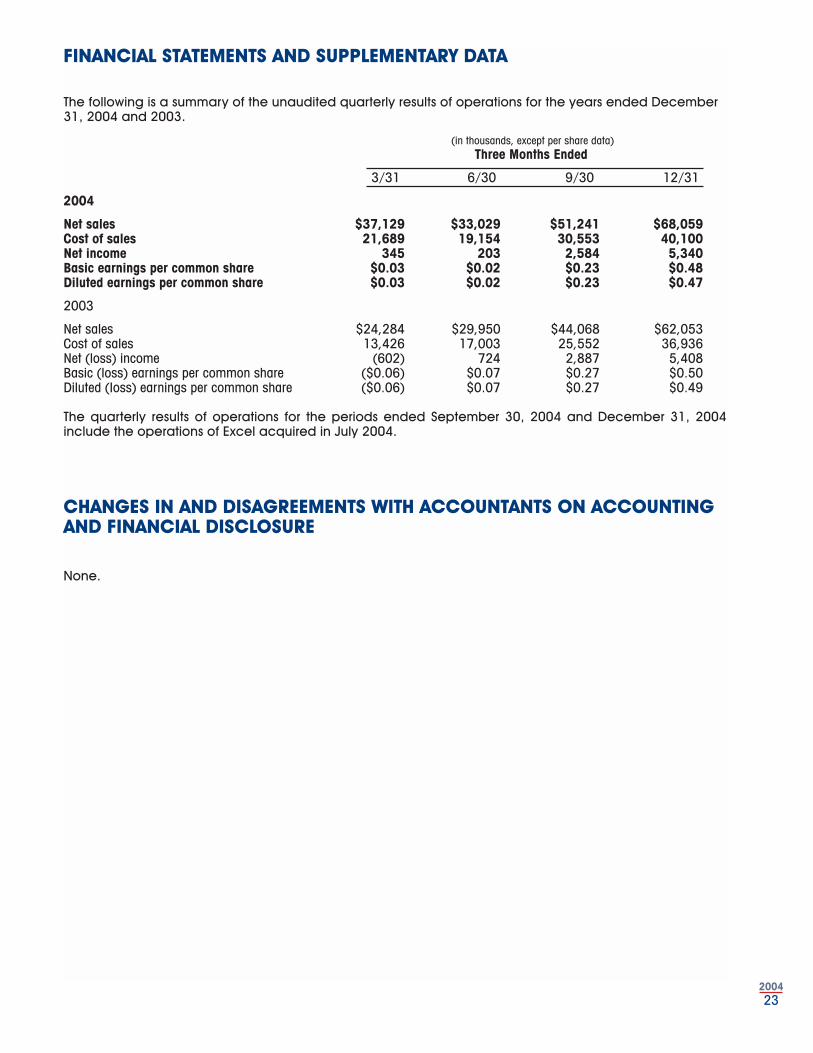

FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

The following is a summary of the unaudited quarterly results of operations for the years ended December31, 2004 and 2003.

(in thousands, except per share data)Three Months Ended

3/31 6/30 9/30 12/31

2004

Net sales $37,129 $33,029 $51,241 $68,059Cost of sales 21,689 19,154 30,553 40,100Net income 345 203 2,584 5,340Basic earnings per common share $0.03 $0.02 $0.23 $0.48Diluted earnings per common share $0.03 $0.02 $0.23 $0.47

2003

Net sales $24,284 $29,950 $44,068 $62,053Cost of sales 13,426 17,003 25,552 36,936Net (loss) income (602) 724 2,887 5,408Basic (loss) earnings per common share ($0.06) $0.07 $0.27 $0.50 Diluted (Ioss) earnings per common share ($0.06) $0.07 $0.27 $0.49

The quarterly results of operations for the periods ended September 30, 2004 and December 31, 2004include the operations of Excel acquired in July 2004.

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTINGAND FINANCIAL DISCLOSURE

None.

assets of the Company. Under the terms of theCredit Facility, the Company is required to satisfycertain financial covenants, including limitationson indebtedness and sale of assets; a minimumfixed charge ratio; a maximum leverage ratio andmaintenance of a minimum net worth. Borrowingsunder the credit facility have different interest rateoptions that are based on an alternate base rate,the LIBOR rate and the lender’s cost of funds rate,plus in each case a margin based on a leverageratio. As of December 31, 2004, the Companyhad outstanding $0.4 million of letters of creditand trade acceptances, $19.4 million of short-term borrowings and a $5.0 million term loanunder its Credit Facility and, as a result, theavailability under the Credit Facility was $25.2million. The $5.0 million long-term loan is non-amortizing, bears interest at 5.07% and matures inAugust 2009. Interest rates on short-termborrowings at December 31, 2004 ranged from3.3125% to 5.25%.

Products are sold to retailers primarily on 30-day

credit terms, and to distributors primarily on 60-day credit terms.

The Company believes that its cash and cashequivalents plus internally generated funds and itscredit arrangements will be sufficient to finance itsoperations for the next twelve months.

The results of operations of the Company for theperiods discussed have not been significantlyaffected by inflation or foreign currencyfluctuations. The Company negotiates all of itspurchase orders with its foreign manufacturers inUnited States dollars. Thus, notwithstanding anyfluctuations in foreign currencies, the Company’scost for a purchase order is generally not subjectto change after the time the order is placed.However, the weakening of the United States dollaragainst local currencies could lead certainmanufacturers to increase their United Statesdollar prices for products. The Company believesit would be able to compensate for any suchprice increase.

As of December 31, 2004, the Company’s contractual obligations were as follows:

(in thousands)Payments Due by Period

Less Than More ThanContractual Obligations Total 1 Year 1-3 Years 3-5 Years 5 Years Operating Leases $40,194 $5,941 $8,929 $6,705 $18,619 Capitalized Leases 1,204 331 581 292 - Short-term Debt 19,400 19,400 - - - Long-term Debt 5,000 - - 5,000 - Royalty License Agreements 11,103 3,618 7,439 46 - Employment Agreements 5,312 3,157 2,155 - - Totals $82,213 $32,447 $19,104 $12,043 $18,619

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK