light, medium or strong? - hsbc global asset … medium or strong? different solutions for different...

TRANSCRIPT

Light,

medium

or strong?

Different solutions for different needs

HSBC Managed Solutions (An open ended Fund of Funds Scheme)

New Fund Offer: 09 April to 23 April 2014

A need-based investment solution that helps you meet your financial goals

Why invest?

3

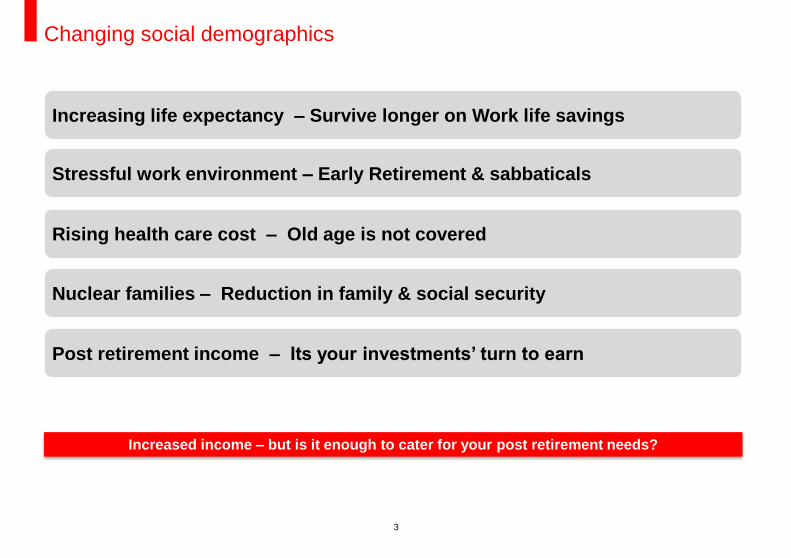

Changing social demographics

Increasing life expectancy – Survive longer on Work life savings

Post retirement income – Its your investments’ turn to earn

Stressful work environment – Early Retirement & sabbaticals

Rising health care cost – Old age is not covered

Nuclear families – Reduction in family & social security

Increased income – but is it enough to cater for your post retirement needs?

4

Source: HSBC Global Asset Management

Greater demand to spend

Birth and

Education

0 25 60 Earning Life 75 + Retired

Life

Marriage

House

Children’s

Education

Children’s

Marriage

Retirement

Age

Do you want to compromise on

your living standard after your

retirement?

Emergencies?

Car

Children

Savings / Investing

Support old

parents

5

Source : Reserve Bank of India, Currency - INR

Expected average savings for 12th Five Year Plan (2012-17)

High focus towards perceived “safe” investment avenues

Asset Class Performance* Asset Class Distribution : Individual Wealth

Period : 1989 – 2012, Source : CLSA, Currency – INR

*Real Estate data not available

6

If you manage your monthly expenses with INR

100,000 today, and if inflation grows @ 8% or

@10%, what will you need in future?

Source : BSE, RBI , EPFO website, Currency - INR

Just saving is not enough: You also have to beat inflation!

How Inflation erodes our money value?

INR 100,000 in last 34 years (since inception of

S&P BSE Sensex):

If left idle (cash)= ~INR 7,661

If invested in Fixed Deposits = ~INR 146,273

If invested in EPF = ~INR 209,775

If invested in Sensex = ~INR 1,428,287

Sensex has historically provided higher

returns

Is your money working hard enough to sustain you?

7

Inflation : A real threat

Prepare for retirement while we earn and more importantly while we can

Enhance our purchasing power instead of protecting current value

Why invest - Takeaways

Where to invest?

9

Gold: Allocate in moderation

Can be volatile

Real Estate

Project delays

Title issues

Liquidity concerns

Commodities: Regulations still evolving

Not fully understood by retail investors

Alternative Investments: Means to diversify

So how do we go about investing?

10

It is “ too risky”

“Led by Foreign Institutional Investors (FII) and speculators”

“We have lost money in equities”

“We have not seen the markets provide positive returns over last 5 years”

Equities are a “game changer”

“It is an asset class for the long term”

“Historically, equities have provided 15.4% compounded annualised returns – better than other asset classes” (Source: CLSA: 1989-2012, Currency - INR)

Equities – Different perspectives

Both are right!

11

Over the longer term growth in equities track the corporate earnings growth

EPS : Earnings Per Share – The portion of a company's profit allocated to each outstanding share of common stock. Earnings per share serves as an indicator of a company's profitability.

The unconventional truth

Source: BSE Website, Currency - INR

Gro

wth

va

lue

s , R

eb

ase

d a

t 1

00

Equities track corporate earnings

- 1,000 2,000 3,000 4,000

Mar-

89

Mar-

90

Mar-

91

Mar-

92

Mar-

93

Mar-

94

Mar-

95

Mar-

96

Mar-

97

Mar-

98

Mar-

99

Mar-

00

Mar-

01

Mar-

02

Mar-

03

Mar-

04

Mar-

05

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

BSE Sensex - Profit growth versus Index growth

EPS Growth Sensex Growth

12

Likelihood of loss versus duration of investment

You need to give it time

Time in market more important than timing the market

0%

Analysis based on Sensex data since March 1979, as on March 2013, Currency - INR

Source: BSE, HSBC Global Asset Management, India

13

Investor returns depend more on Investor behaviour and risk profile rather than the

market behaviour

Performance chasing syndrome?

Buy the “best performing” asset class

The “best performing” stock

The “best performing” fund

Where is the disconnect?

14

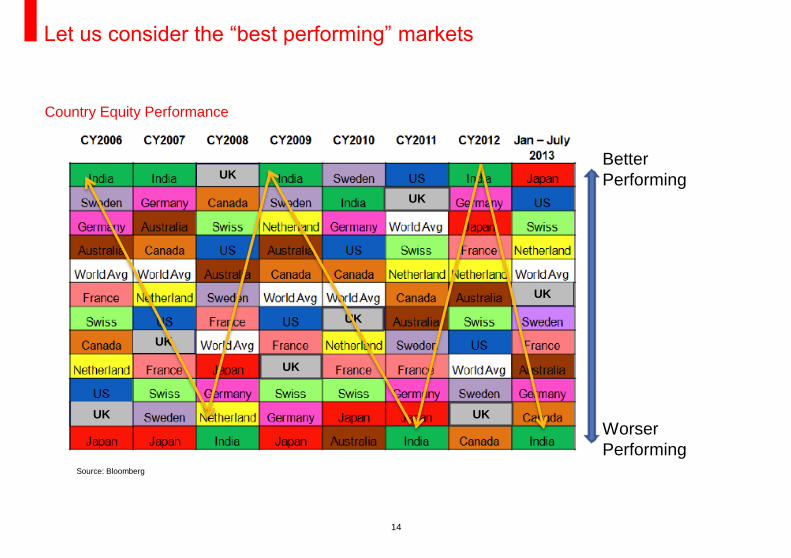

Let us consider the “best performing” markets

Country Equity Performance

Source: Bloomberg

UK

UK

UK

UK

UK

UK

UK

UK

Better

Performing

Worser

Performing

15

Source: Bloomberg, Currency - INR

Teck indicates Technology Index, FMCG indicates Fast Moving Consumer Goods Index, Bankex indicates Banking Index, IT indicates Information technology Index

Or the “best performing” sectors?

Top 2 Equity Indices/Sectors

Calendar YearNSE - NIFTY

50

NSE - CNX

Mid capNo 1 No 2 No 1 No 2

2003 72% 138% Metal - 212% Capital Goods - 168% 7/11 3/11

2004 11% 25% Teck - 33% Bankex - 33% 6/11 8/11

2005 36% 35% Consumer Durables - 115% Capital Goods - 94% 12/12 1/12

2006 40% 29% Capital Goods - 56% Teck - 49% 3/12 10/12

2007 55% 77% Power - 122% Metal - 121% 9/13 12/13

2008 -52% -59% FMCG -14% Health Care -33% 13/13 11/13

2009 76% 99% Metal - 234% Auto - 204% 10/13 2/13

2010 18% 19% Consumer Durables - 68% Auto - 38% 5/13 6/13

2011 -25% -31% FMCG - 10% Health Care -13% 3/13 6/13

2012 28% 39% Bankex - 57% Realty - 53% 7/13 13/13

2013 6.80% -5% IT - 60% Healthcare - 22.6%

Year and Market Cap performance Top 2 Sector Next Year Ranking for Top 2 Sectors

Themes change - Different sectors and segments perform at different times!

16

The hypothesis also holds true for different investment categories

Source: MFIE, CRISIL, Currency - INR

Note: “Large cap” denoted by S&P Nifty, “Midcap” denoted by BSE Midcap, “Long term debt” denoted by Crisil 10 year Gilt Index, “Short term debt” denoted by Crisil 1 year T-bill index and “Ultra Short

term debt” denoted by Crisil 91 day T-bill index; Diversification of portfolio is customer's choice

Do we place enough importance on asset allocation?

Ultra short

term debt

Midcap

equity Midcap

equity Large

cap

equity

Midcap

equity

Long

term debt

Midcap

equity

Ultra short

term debt

Ultra short

term debt

Long

term

debt

The best category changes every year

Retu

rns

The best performing category for the year

Is there a solution that we can consider?

18

Factors that explain variation between portfolio performances

Source: Brinson et al, 1986

Asset allocation: Key determinant of portfolio returns

Most time spent on the 6% viz. security selection, market timing

19

Multi-asset portfolios spread investments both across asset classes and across geographies

Ensures that the portfolio does not become over-reliant on a single asset class or a single country or

sector

Asset classes typically have a low correlation - combining assets with low correlations helps reduce

overall portfolio volatility

Low Correlation between various investment segments (2003-14)

Why should we consider multi-asset portfolios?

Period : 1 April 2003 to 31 January 2014, Source: CRISIL, BSE, Bloomberg

Large Cap denoted by BSE Sensex, Long Term Debt denoted by CRISIL Composite Bond Fund Index, Mid cap denoted by BSE Midcap

Index, Short Term Debt denoted by CRISIL Short Term Bond Fund Index, Offshore Equity denoted by MSCI World Index

Correlation Coefficient Large Cap Long Term Debt Midcap Short Term Debt Offshore Equity Gold

Large Cap 1.00 0.22 0.89 0.17 0.45 -0.01

Long Term Debt 0.22 1.00 0.25 0.89 0.03 -0.02

Midcap 0.89 0.25 1.00 0.17 0.45 0.03

Short Term Debt 0.17 0.89 0.17 1.00 -0.02 0.03

Offshore Equity 0.45 0.03 0.45 -0.02 1.00 0.02

Gold -0.01 -0.02 0.03 0.03 0.02 1.00

20

Combining two asset classes with low correlations could produce a portfolio with reduced overall risk,

while improving risk-adjusted returns over a market cycle

The lower the correlation between two assets, the greater the diversification effect

Source: HSBC Global Asset Management – For illustrative purposes only, Assuming the risk free rate is 0%

Illustration – Asset allocation may help optimise returns and risk

Risk

Asset

A

Asset B

Return

Portfolio 20% Asset A

80% Asset B

Asset Return Volatility Sharpe Ratio

Asset A 12.0% 25.0% 0.48

Asset B 5.0% 10.0% 0.50

Portfolio 6.4% 8.0% 0.80

Sharpe Ratio - A ratio used to measure risk-adjusted performance. The Sharpe ratio is calculated by subtracting the risk-free rate - such as that of the 10-year Treasury bond - from the rate of return

for a portfolio and dividing the result by the standard deviation of the portfolio returns.

Volatility - A statistical measure of the dispersion of returns for a given security or market index. Volatility can either be measured by using the standard deviation or variance between returns from that

same security or market index. Commonly, the higher the volatility, the riskier the security.

21

Rebalancing an investment portfolio endeavours that you sell high and buy low in the process of maintaining the

desired composition of your portfolio at pre-decided periodicities.

For example –

If the preferred asset allocation for an individual is

Debt-Equity-Liquid at 50:35:15

Let us assume that equity markets generate 20% in a particular year, bond markets generate 10% and liquid

investments generate 6%. What happens to investor’s portfolio if he rebalances annually –

Is asset allocation enough? Case for re-balancing

50%

35%

15%

Initial Investment

52.45% 33.65%

13.89%

Change in Asset Allocation after 1 year due to market movement

Equities Debt Liquid

50%

35%

15%

Asset Allocation restored after rebalancing

Assumed

Equities up

20%, Bonds

up 10% and

Liquid up

6%

Remains true to investment objective!

Can we dynamically allocate assets in keeping with the

investment objective?

HSBC Managed Solutions

24

Multi asset (Domestic and Offshore Equity, Fixed Income, Liquid and Gold) portfolios

which are actively managed

Constructed to optimize returns whilst managing risk

Offers transactional efficiency to the investor

A unique investment solution for Indian investors

HSBC Managed Solutions: A wealth imperative

25

An Investment Solution

Designed to meet the needs and preferences of investors

Considers investors' risk profile and deliver solutions to meet investment goals

Uses active asset allocation to achieve optimal mix

Fund of Funds (FOF) feeding into HSBC/Third Party funds*

Merits

Risk Profile based Asset allocation Buckets

Supports long term Goal Based Investment Planning

Risk aware investment experience matched to customer needs

Diversifying across low correlation asset classes

Domestic Equities, Domestic Bonds, Offshore Equities, Alternates (like Gold)

Delivered through open-ended funds in the cost efficient manner, to deliver an efficient investment solution

Regular allocation reviews – Quarterly and event based, annual comprehensive review of design principles

Low Cost Solution

Free switching & Withdrawal benefits

Expenses with customer value proposition intent

* For capabilities where HSBC offerings are not available

HSBC Managed Solutions

Investors can reap the benefits of asset allocation based on risk profile without having to select

funds or personally rebalance the portfolio

26

Seeks to provide long term total return through active asset allocation

Managed Solutions India – Growth

Primarily invests in equities, with diversification in debt, gold and liquid

Managed Solutions India – Moderate

Primarily invests in equities and debt, with diversification in gold and liquid

Managed Solutions India – Conservative

Primarily invests in debt, with diversification in equities, gold and liquid

Managed Solutions - Options

27

Asset allocation bands

Plan Type of Security

Indicative Allocation

(% of net assets) Risk Profile

Minimum Maximum

Managed Solutions

India – Growth

Equity Schemes (Units of Domestic Equity and

Offshore Equity) 55% 90% High

Debt Schemes 10% 30% Low to Medium

Gold and Other Exchange Traded Funds 0% 15% Medium to High

Money Market Schemes/Liquid Funds (including up to

5% in Money Market Instruments) 0% 20% Low

Managed Solutions

India – Moderate

Equity Schemes (Unit of Domestic Equity and

Offshore Equity) 30% 70% High

Debt Schemes 30% 70% Low to Medium

Gold and Other Exchange Traded Funds 0% 15% Medium to High

Money Market Schemes/Liquid Funds (including up to

5% in Money Market Instruments) 0% 25% Low

Managed Solutions

India – Conservative

Equity Schemes (Unit of Domestic Equity) 0% 15% High

Debt Schemes 55% 100% Low to Medium

Gold and Other Exchange Traded Funds 0% 5% Medium to High

Money Market Schemes/Liquid Funds (including upto

5% in Money Market Instruments) 0% 25% Low to Medium

28

Operational Risk: Given that the Fund of Funds structure will involve splitting each subscription and

redemption at Fund of Funds level into multiple subscription and redemptions into the respective funds;

there is enhanced operational risk

Liquidity risk of underlying instruments: There could be liquidity risk on account of illiquid underlying

holdings

Market Risk: The Underlying scheme’s investments are subject to the risks inherent in all investments in

Securities i.e. the value of holdings may fall as well as rise

Currency Risk: As the Underlying scheme could invest in securities which are denominated in foreign

currencies (e.g. US Dollars), fluctuations in the exchange rates of these foreign currencies may have an

impact on the income and value of the Scheme.

Restructuring/Rescheduling Risk: There could be cases of restructuring/rescheduling of particular

debt/money market instruments held in the portfolio which could result in the maturity of these

instruments going beyond the original maturity date of the instrument

Risk factors associated with investing in Gold Exchange Traded Funds

Risk factors associated with Legal, Tax and Regulatory risk

Key risks

Why HSBC Global Asset Management?

30

HSBC Global Asset Management: Credentials

Expertise in managing Indian equity and debt

One of the largest managers/sub-advisors of Indian assets

Equities - ~ USD 3.2 B*

Fixed income ~ USD 13.4 B*

Only foreign asset manager of the largest provident fund mandate in India

Multi-asset: A leading global player

Significant proportion of AUM globally

USD 73.9 billion assets under management in multi assets#

A core global capability

International perspective

Ability to identify and position for global trends

Long term asset prices

Impact of macro economic developments

# Source: HSBC Global Asset Management as at 31 December 2013. Any differences are due to rounding.

*Source: HSBC Global Asset Management; AUM data as on 28 February 2014, USD/INR – 61.755

31

HSBC Global Asset Management: Credentials

We are committed to being:

Fair to our clients

Provide them world class solutions that are:

Sustainable

Fairly priced

We believe this is our competitive advantage

32

HSBC Global Asset Management: Credentials

We were and probably are the only Asset Management Company (AMC) in India to have waived exit

loads from all our mutual fund schemes w.e.f. March 2013

In 2013, we were amongst the fastest growing AMCs in India

(Domestic mutual fund average assets growth in 2013)

Source: AMFI

33

There is a simple, straightforward way to create long term wealth

Understand and embrace risk

Put time on your side and don’t try timing the market

Invest regularly

Follow asset allocation & rebalancing discipline

Make the right choice…

Asset allocation and rebalancing is the key

For further information on HSBC Managed Solutions, please contact your

Investment Advisor

35

Product labeling

Risk categorisations as per regulatory guidelines

Managed Solutions India – Growth Managed Solutions India – Moderate Managed Solutions India – Conservative

This product is suitable for investors who are

seeking*:

To create wealth over the long-term

Investing predominantly in units of equity

mutual funds as well as in a basket of debt

mutual funds, gold & exchange traded

funds, offshore mutual funds and money

market instruments

High risk (BROWN)

This product is suitable for investors who are

seeking*:

To create wealth and provide income over

the long-term

Investments in a basket of debt mutual

funds, equity mutual funds, gold & exchange

traded funds, offshore mutual funds and

money market instruments

Medium risk (YELLOW)

This product is suitable for investors who are

seeking*:

To provide income over the long-term

Investing predominantly in units of debt

mutual funds as well as in a basket of equity

mutual funds, gold & other exchange traded

funds and money market instruments

Medium risk (YELLOW)

* Investors should consult their financial advisers if in doubt about whether the product is suitable for them.

Note: Risk may be represented as:

(BLUE) investors understand that their principal will be at low risk

(YELLOW) investors understand that their principal will be at medium risk

(BROWN) investors understand that their principal will be at high risk

36

Disclaimer

This document has been prepared by HSBC Asset Management (India) Private Limited (HSBC) for information purposes only and

should not be construed as an offer or solicitation of an offer for purchase of any of the funds of HSBC Mutual Fund. All information

contained in this document (including that sourced from third parties), is obtained from sources, which HSBC/ third party, believes to

be reliable but which it has not independently verified by HSBC/ the third party. Further, HSBC/ the third party makes no guarantee,

representation or warranty and accepts no responsibility or liability as to the accuracy or completeness of such information. The

information and opinions contained within the document are based upon publicly available information and rates of taxation

applicable at the time of publication, which are subject to change from time to time. Expressions of opinion are those of HSBC only

and are subject to change without notice. It does not have regard to specific investment objectives, financial situation and the

particular needs of any specific person who may receive this document. Investors should seek financial advice regarding the

appropriateness of investing in any securities or investment strategies that may have been discussed or recommended in this report

and should understand that the views regarding future prospects may or may not be realized. Neither this document nor the units of

HSBC Mutual Fund have been registered in any jurisdiction. The distribution of this document in certain jurisdictions may be

restricted or totally prohibited and accordingly, persons who come into possession of this document are required to inform

themselves about, and to observe, any such restrictions.

© Copyright. HSBC Asset Management (India) Private Limited 2014, ALL RIGHTS RESERVED.

HSBC Asset Management (India) Private Limited, 16, V.N. Road, Fort, Mumbai-400001 Email: [email protected]

Mutual fund investments are subject to market risks, read all scheme related documents carefully.