limerick solicitors bar association professional indemnity insurance learning from 2010 and...

TRANSCRIPT

Limerick Solicitors Bar Association

Professional Indemnity Insurance

Learning from 2010 and preparing for 2011

14th April 2011

David Rowe & Pauline McNamara

AgendaProfessional Indemnity Insurance – learning from 2010 and preparing for 2011

•What is Risk Management?•The 2010 renewal•How the underwriters arrive at a premium•How to move on from a claims history•Preparing for 2011

Where does Risk Management fit in

Running a law firm was relatively easy• You only had to worry about getting the work• Then managing the cost base became a requirement to

survive• Then getting paid became an issue and firms were

forced to improve their procedures• Now Risk Management has become a necessity – lack

of Risk Management can prevent a firm trading (no cover) or render it not viable (premium prohibitive)

What is Risk Management?What can go wrong and what is the potential damage caused?

How can I limit the number of things going wrong?

Accepting that things will go wrong - what systems and control can I put in place to limit the effect of things that do go wrong?

Risk Management – the build up

• Volumes of business up year on year (until 2007)

• PI insurance premiums fell (less premium for more risk)

• Firms found it difficult to service the volume - shortcuts taken

• The financial dynamics of property markets changed almost overnight

the build up cont’d• Clients and financial institutions started

looking for potential escape routes and made claims

• The profession saw a significant increase in claims against it

• The insurers began incurring significant losses

• Premiums increased

• Insurance companies began to take a more selective approach

the build up cont’d

• Insurance companies became interested in the risk profile of the profession

• When they looked they did not like what they saw and regard the profession as high risk and substantially unmanaged

• Now likely to insist on firms managing risk

• Encouraged by the number of firms who have voluntarily attained risk management accreditation, but legacy problems persist.

The stakeholders - the insurance companies

• See solicitors as high risk, following high claims

• Will pick and choose

• Will look for systems to mitigate risk

• Will audit their clients

• Want to work with firms to improve their risk profile

• Accept that problems occur, looking for post loss corrective actions

The stakeholders - the profession

• Trading conditions difficult and feel they cannot take more of a burden

• Renewal in December 2010 very difficult, multiple forms, uncertainties in getting cover at all and huge premium increases

• Feel overregulated and see risk management as more of the same

• Practitioners who are claims free struggle to see the value in this, most accept the insurers hold all the cards

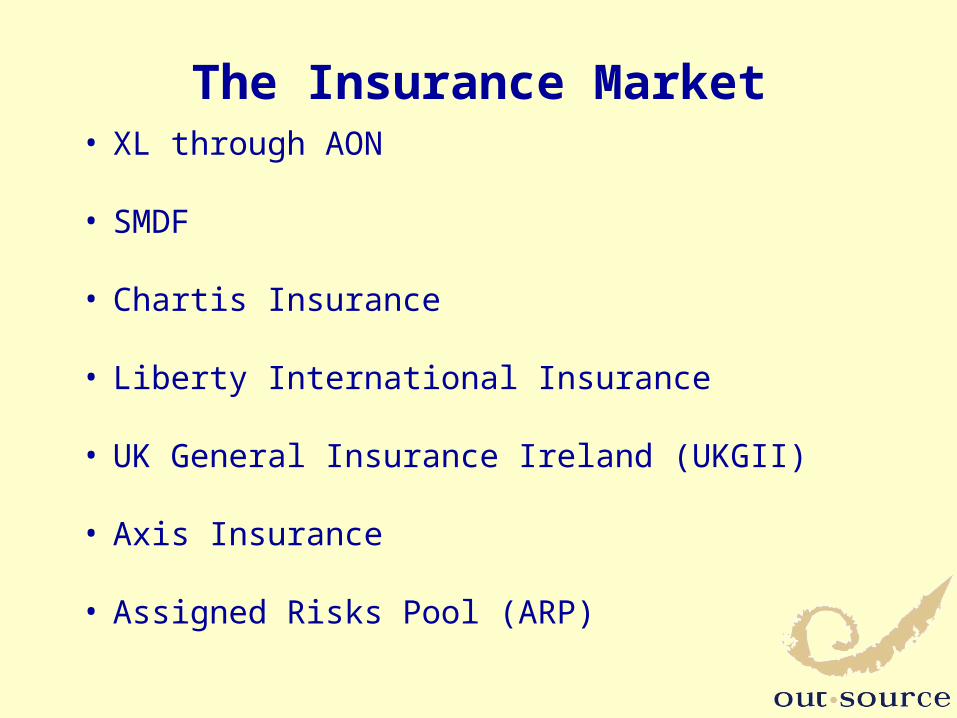

The Insurance Market• XL through AON

• SMDF

• Chartis Insurance • Liberty International Insurance

• UK General Insurance Ireland (UKGII)

• Axis Insurance

• Assigned Risks Pool (ARP)

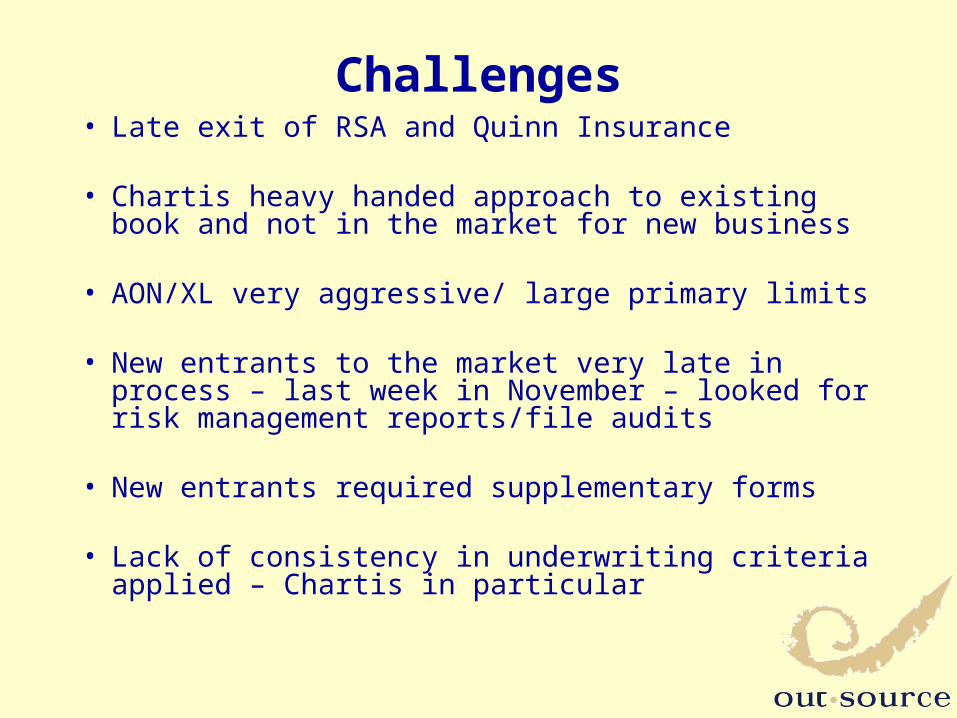

Challenges• Late exit of RSA and Quinn Insurance

• Chartis heavy handed approach to existing book and not in the market for new business

• AON/XL very aggressive/ large primary limits

• New entrants to the market very late in process – last week in November – looked for risk management reports/file audits

• New entrants required supplementary forms

• Lack of consistency in underwriting criteria applied – Chartis in particular

Qualified Insurer by premium & firms covered

Insurer Market Share by premium

Last years market share

XL Insurance Company Ltd 34% 21%

SMDF 33% 41%

Chartis Insurance Ireland Ltd 12% 8%

UK General Insurance (Ireland) Ltd 8% -

Liberty Mutual Insurance Europe Ltd 8% 7%

Axis Speciality Europe Ltd 4% -

Allianz Global Corporate & Speciality AG 1% 1%

RSA 9%

Quinn Insurance 11%

Hiscox 2%

Pricing - 2010

• Up 14% overall

• Low risk firms (per solicitor)– Start ups - €6K to €10K– Established firms - €10K to €15K– Larger established firms - €7k to €10K

• High Risk– Up to €50K to €100K

The Assigned Risk Pool• 38 firms

• Premiums– 20% on 1st 500K of fee income– 15% on next €1M– 9% above thatAll subject to a selective review

• Overseen by PII Committee

• Investigation by way of risk management audit/terms of reference

• 2 year maximum stay

How A Premium Is Arrived At

Key underwriting considerations 2010

• Practice profile – size, distress, breakdown of work areas etc

• Fee income/ability to remain in business – left with run-off potentially

• Historic split in revenue generation• Claims• Risk management section of proposal/appetite to

RM - make or break in some cases• Undertakings – register in place?/ numbers

outstanding

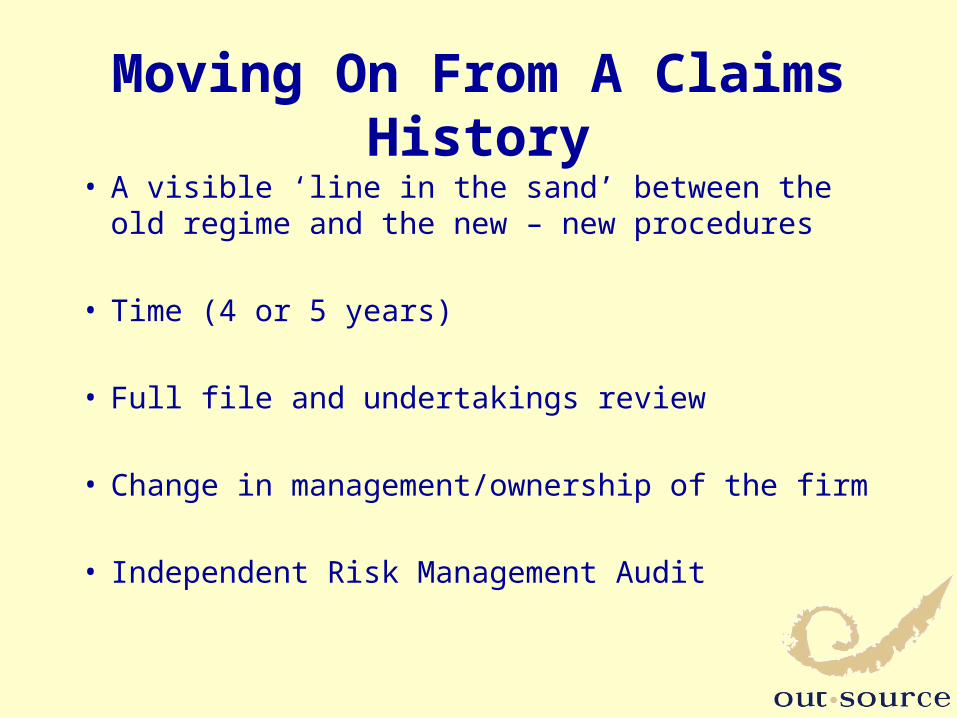

Moving On From A Claims History

• A visible ‘line in the sand’ between the old regime and the new – new procedures

• Time (4 or 5 years)

• Full file and undertakings review

• Change in management/ownership of the firm

• Independent Risk Management Audit

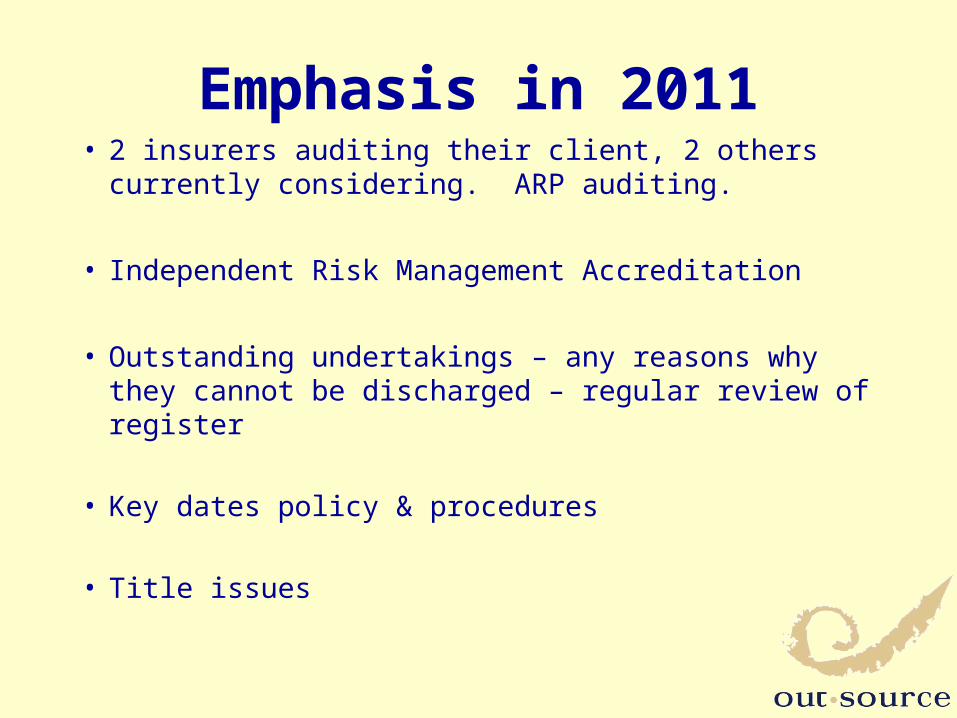

Emphasis in 2011• 2 insurers auditing their client, 2 others currently

considering. ARP auditing.

• Independent Risk Management Accreditation

• Outstanding undertakings – any reasons why they cannot be discharged – regular review of register

• Key dates policy & procedures

• Title issues

Making the Renewal Easy• Go to a specialist broker

• Only apply where you might get cover

• Fill out the forms carefully

• Keep claims moving/ resolve them

• Meet your broker/ insurer in advance

• Try to save monthly or arrange finance

• Complete an independent risk accreditation

How the Law Society can help• Closed period for withdrawal/new entrants

• Scrap the common renewal date

• Common proposal form

• Master Policy??

• Review run-off provisions

• Enforce obligation to quote within 10 days of proposal form

• Proposal forms out earlier

Implementing Risk Management – the path

• Identify what you need to have in place

• Define your standard policies and procedures

• Implement and train – bring everyone along

• Review the past for errors

• Put together the registers

Implementing Risk Management – the path cont’d

• Have an audit done

• Go for level 1 (Essentials) if this is new or level 2 (Excel) if some systems in place

• Audit consists of – Review of policies/procedures– Ensuring all in firm know and use procedures– File/undertakings review

• Work on the gaps, this is long term

Implementing a risk management strategy

Practical Tips• Allocate sufficient time and resources – a partner

needs to lead the effort

• Risk management is a culture not an event – it is long term

• Very few firms in Ireland would pass the standard without preparation – this is as expected

• Make it an office wide project, the benefits come from eyes and ears throughout

• Remove the fear factor – this is a positive step and the benefits are significant

How to start - choices

• Do it yourself

• Take it on with external assistance, pre-audit, policies and procedures, experienced help.

Sample of RequirementsClient Management (1 out of 8 standards)• Formal procedures required for engaging new

clients, limitation of liabilities etc• Who and on what terms

– Review creditworthiness

• Can we do the work?– Resources and expertise

• How do we staff it?• Partner involvement from the start

Client Management (1 out of 8 standards) cont’d

Policies needed- Partner sign-off of file matter opening forms (ensure

compliance going forward)- Engagement letter/S68 letter put in place – but

standardised where possible- Conflicts of interest policy- Anti-money laundering policy- Complaints policy (ensure you are aware of and adhere

to the policy)- Disengagement procedures (in place – but use of

disengagement letters recently introduced)

Common myths• Risk management is a bureaucratic exercise of no

value• Risk management is an event you have to comply

with once a year (passing the exam)• Doing nothing is an option• This is a contentious process where the Risk

Management Auditor wants to highlight your weaknesses

Conclusions

Benefits from the practitioners perspective

• Achievement of an approved quality standard

• Improved efficiency

• Reduction in complaints and potential claims

• Lower insurance premium

• Savings in time, worry and expenditure

• Greater profitability

• Potentially a win/win situation

Conclusions• Insurance is now the 3rd biggest cost in running a

firm

• 2010 renewal very difficult, 2011 unlikely to be any better

• Pricing levels to remain at current levels

• Now part of staying in business – can be fatal

• Being pro-active is key, don’t just wait for it to happen

• Has become part of doing business and making a living

For further information contact:

David Rowe

Managing Director

Outsource

Ph: 01 6788490

Email: [email protected]