liontrust

Post on 20-Oct-2014

618 views

DESCRIPTION

TRANSCRIPT

Professional Investors and Advisers only

Themes for Tomorrow

Jan VH Luthman

2

1. Global Health

3 3

Pharmaceuticals

– Mature markets

– Political interference

– High litigation risk

– Low growth

– No pricing power

– Costs & risks of R&D

Market perception

4 4

Pharmaceuticals

Reality

– Global population is expanding

– Everyone will get sick, grow old and die

– More and more can afford access to medicines

– Pharmaceutical companies refocusing on emerging markets, lifestyle, over-the-counter, branded generics – growth, pricing power, less political interference, less litigation risk

5 5

Pharmaceuticals

Research and Development

– NCATS - National Centre for Advancing Translational Sciences

– Will work with pharmaceutical industry

– R&D more efficient, more effective, less financially risky

6 6

Pharmaceuticals

How big a theme?

We have all seen a similar transformation of business model and investor perceptions

Macro Equity Income Fund Weighting

GlaxoSmithKline 4.3%

AstraZeneca 3.0%

Bristol-Myers Squibb 2.8%

Pfizer 3.7%

Merck 3.1%

Shire 2.1%

Vectura 0.7%

Source: Liontrust Fund Partners LLP. Data as at 31.12.2012.

7 7

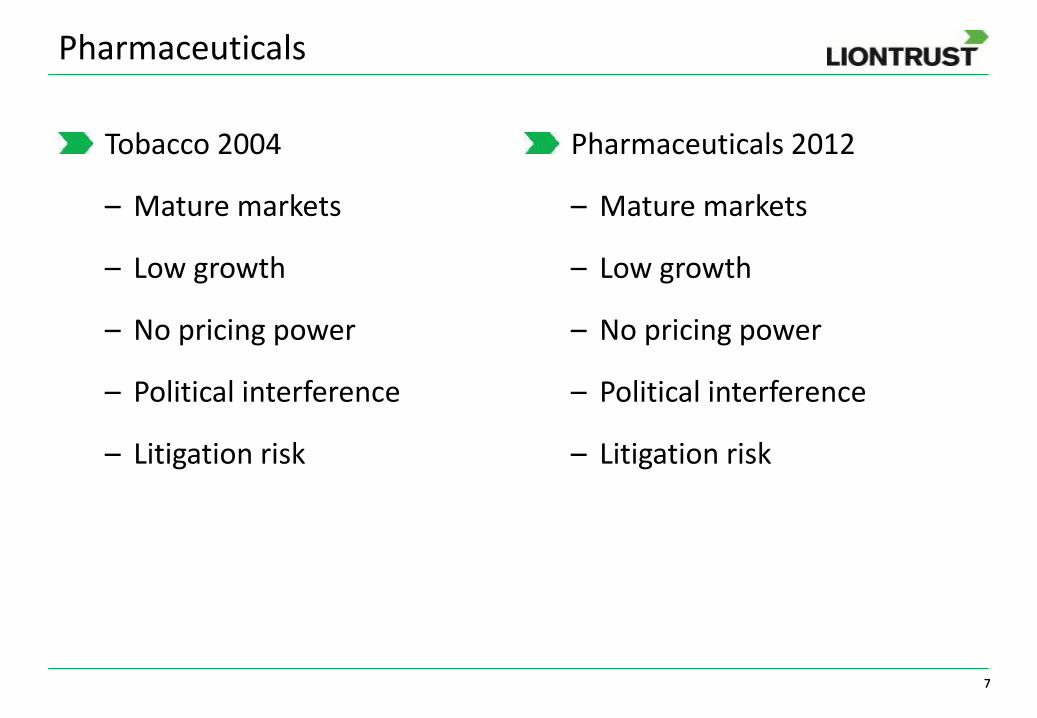

Pharmaceuticals

Tobacco 2004

– Mature markets

– Low growth

– No pricing power

– Political interference

– Litigation risk

Pharmaceuticals 2012

– Mature markets

– Low growth

– No pricing power

– Political interference

– Litigation risk

8 8

Pharmaceuticals

Compare the performance of the Tobacco sector with two infamously powerful sectors – Mines and Banks

9 9

-100%

0%

100%

200%

300%

400%

500%

600%

May

-92

Ap

r-9

3

Mar

-94

Feb

-95

Feb

-96

Jan

-97

Dec

-97

No

v-9

8

No

v-9

9

Oct

-00

Sep

-01

Sep

-02

Au

g-0

3

Jul-

04

Jun

-05

Jun

-06

May

-07

Ap

r-0

8

Mar

-09

Mar

-10

Feb

-11

Jan

-12

Dec

-12

FTSE 350 Index Mining TR in GB FTSE 350 Index Banks TR in GB FTSE All Share TR in GB

Pharmaceuticals

Source: Financial Express as at 31.12.2012.

Mines & Banks (relative to FTSE All-Share)

10 10

-100%

0%

100%

200%

300%

400%

500%

600%

May

-92

Ap

r-9

3

Mar

-94

Feb

-95

Feb

-96

Jan

-97

Dec

-97

No

v-9

8

No

v-9

9

Oct

-00

Sep

-01

Sep

-02

Au

g-0

3

Jul-

04

Jun

-05

Jun

-06

May

-07

Ap

r-0

8

Mar

-09

Mar

-10

Feb

-11

Jan

-12

Dec

-12

FTSE 350 Index Tobacco TR in GB FTSE 350 Index Mining TR in GB

FTSE 350 Index Banks TR in GB FTSE All Share TR in GB

Pharmaceuticals

Source: Financial Express as at 31.12.2012.

Tobacco eclipses Mines & Banks

Mines, Banks – and Tobacco (relative to FTSE All-share)

11 11

-100%

0%

100%

200%

300%

400%

500%

600%

May

-92

Ap

r-9

3

Mar

-94

Feb

-95

Feb

-96

Jan

-97

Dec

-97

No

v-9

8

No

v-9

9

Oct

-00

Sep

-01

Sep

-02

Au

g-0

3

Jul-

04

Jun

-05

Jun

-06

May

-07

Ap

r-0

8

Mar

-09

Mar

-10

Feb

-11

Jan

-12

Dec

-12

FTSE 350 Index Tobacco TR in GB FTSE 350 Index Mining TR in GBFTSE 350 Index Pharmaceuticals & Biotechnology TR in GB FTSE 350 Index Banks TR in GBFTSE All Share TR in GB

Pharmaceuticals

Source: Financial Express as at 31.12.2012.

Re-rating of Pharmaceuticals has barely begun

12 12

Pharmaceuticals

Tobacco re-orientated to new geographic markets

Pharmaceuticals are re-orientating to new geographic markets, to new product markets and to a lower risk business model

Transformation of investor rating of pharmaceuticals could be even more powerful than that of tobacco

13

2. UK Utilities

14 14

UK Utilities

Priced as growth stocks

But...

Austerity & low economic growth

No growth in industrial power demand

Falling real wages & rising utility bills

No growth in retail power consumption

Source: Liontrust Fund Partners LLP. Data as at 31.12.2012.

Weighting to Utilities

Liontrust Macro Equity Income Fund 0.0%

FTSE 100 Index 4.3%

FTSE All-Share Index 3.9%

15 15

UK Utilities

Valuations depend on dividend yield premium

BoE may abandon inflation target

Broader ‘economic health’ remit

Inflation expectations rise

Interest rates rise

Dividend yield premium shrinks

Undermines utilities’ valuations

16 16

UK Utilities

And finally...

Renewables obligations – who will pay?

Investment in 30 new gas power stations

Requires long-term institutional funding

But, if interest rates are rising

What return on capital will be required?

Implications for power prices & profits?

17 17

Utilities relative to the FTSE All-Share

0.90

0.95

1.00

1.05

1.10

1.15

Jan 12 Feb 12 Mar 12 Apr 12 May 12 Jun 12 Jul 12 Aug 12 Sep 12 Oct 12 Nov 12 Dec 12

Utilities GWM

Source: Bloomberg. Data from 31.12.2011 – 19.12.2012

18

3. Asset Managers

19 19

Asset Managers

Economic recovery

Improving corporate earnings

Rising equity valuations

Investor confidence returns

Rising bond yields

Falling bond prices

Switch from bonds to higher-fee equities

Rising inflows, rising fees & fee rates

Macro Equity Income Fund Weighting

Aberdeen 5.0%

Invesco 0.8%

Hargreaves Lansdown 2.4%

Polar Capital 1.4%

Henderson 0.8%

London Stock Exchange 0.8%

Source: Liontrust Fund Partners LLP. Data as at 31.12.2012.

20 20

Aberdeen relative to the FTSE All-Share

0.90

1.00

1.10

1.20

1.30

1.40

1.50

1.60

Jan 12 Feb 12 Mar 12 Apr 12 May 12 Jun 12 Jul 12 Aug 12 Sep 12 Oct 12 Nov 12 Dec 12

Aberdeen FTSE All-Share

Source: Bloomberg. Data from 31.12.2011 – 19.12.2012

21

4. Global Readjustment of Currencies and Wages

22 22

Global Readjustment of Currencies and Wages

We live in a globalising, competitive world

Over the long term, unit costs of production will trend towards approximate, risk-adjusted parity

This trend will follow different paths in different parts of the world

Macro Equity Income Fund Weighting

Unilever 4.7%

Reckitt Benckiser 4.6%

Heinz 2.1%

Kimberly Clark 0.8%

Pepsico 0.9%

Source: Liontrust Fund Partners LLP. Data as at 31.12.2012.

23 23

Global Readjustment of Currencies and Wages

We are all human

We like wage increases

We don’t like wage cuts

24 24

Global Readjustment of Currencies and Wages

High-cost economies

– Prefer lower currencies, not wages

Low-cost economies

– Prefer higher wages, not currencies

25 25

Global Readjustment of Currencies and Wages

China 12th Five Year Plan

– Commitment to expand domestic consumption

– Sustained, accelerated rises in minimum wage (13%pa)

– Major expansion of welfare and healthcare programmes

– Less need to save (savings ratio currently 30%)

– Greater freedom to spend

26 26

Global Readjustment of Currencies and Wages

High cost economies

– Sustained imported inflation

– Slow wage growth

– Depressed consumer consumption

Low cost economies

– Accelerated growth in capacity – and inclination – to spend

– Particularly amongst low and middle income earners

27 27

Unilever relative to the FTSE All-Share

0.85

0.90

0.95

1.00

1.05

1.10

Jan 12 Feb 12 Mar 12 Apr 12 May 12 Jun 12 Jul 12 Aug 12 Sep 12 Oct 12 Nov 12 Dec 12

Unilever FTSE All-Share

Source: Bloomberg. Data from 31.12.2011 – 19.12.2012

28 28

Strictly private and confidential information

Liontrust Macro Equity Income Fund, Liontrust Macro UK Growth Fund

Important notice: This presentation is the property of Liontrust Fund Partners LLP (“LFP”) authorised and regulated by the Financial Services Authority, and is strictly confidential. It contains information intended only for the person to whom it is addressed or presented, and is intended for evaluation purposes only, with no licence to use the content or materials within. In receiving this presentation, the recipient acknowledges and agrees that: i) in the event the recipient does not wish to pursue this matter, this presentation will be returned as soon as possible; ii) the recipient will not copy, fax, reproduce, divulge or distribute this confidential presentation, in whole or in part, without the express written consent of LFP; iii) all of the information herein will be treated as confidential material with no less care than that afforded to the addressee’s own confidential material of the most sensitive nature; iv) information herein may constitute material non-public information, disclosure of which may be prohibited by law, and the legal responsibility for its use is borne solely by the recipient. This presentation in no way constitutes an offer to sell, nor a solicitation to purchase securities in any company or investment product.

The value of units in a unit trust and the income generated from them can fall as well as rise and are not guaranteed; investors may not get back the amount originally subscribed. Past performance is not a guide to future performance. The issue of units may be subject to an initial charge, which will have an impact on the realisable value of the investment, particularly in the short term. Equity investment should always be considered as long term.

The Prospectus or Key Investor Information Documents (KIIDs) for Liontrust’s unit trusts are available direct from Liontrust or from our website, www.liontrust.co.uk.