liquidity alm or market risk ? jérôme lebuchoux. liquidity vague concept ? standard approach ...

TRANSCRIPT

Liquidity ALM or Market Risk ?

Jérôme Lebuchoux

Liquidity

Vague concept ?

Standard approach Related to market liquidity on asset (volume, trades, prices, etc…) microstructure

Major risk Macro impact Credit crunch Crisis

Market liquidity

Classical approach for liquidity Execution price depends on the volume

Execution Take into account the asymmetry (buy and sell) Optimal execution model for block trade

Allocation Rebalance the portfolio according to the liquidity

Risk Gap risk Limits

It is a vision of liquidity related to buy / sell action

Market liquidity

The regulators are imposing new constraints

New pools of liquidity have emerged New exchanges Dark pool Long term investors

This approach is not appropriate for many markets (Fixed income)

Is there something else ?

Market liquidity

Investors are not operating with the same objective nor under the same rules

Pension funds Hedge fund Insurance…

The buy and sell are only the visible actions but behind every operations there is a financing part

Cash Margin Borrow Collateral

Examples

Buy a future at an exchange Post the initial margin

Sell short a financial stock Borrow the stock

Buy a swap Post collateral

ALM liquidity

If there is no financing there is no investment

If one could not buy it may be able to borrow

If one could not sell it may be able to repo or post for collateral

Example : Corporate bonds No price on secondary market Accepted as collateral Borrow money, post the bond as collateral and invest into new asset

• Spread position

Borrowing cost, repo market are good indicators for liquidity, it could be used to get a long or a short position on liquidity on FI market.

Hedge Fund

Hedge Fund utility ?

Optimal Capital allocation Diversification Arbitrage New risk profile

Liquidity provider To the Market To the investors

Facts

Old concept but a young industry

Asset Management industry has been hit by the crisis :● Asset under management has been reduced.● Performance was poor.● Risk management has shown its limits● Authorities are putting pressure for new standards and regulation.● The confidence of the investors is low

Consequences :● Revenues are declining ● Customers are more demanding● The image of the industry is deteriorated

A step back

Main drivers of the asset management industry :● Economy

● Growth of economy● Capital needs to sustain the economy growth and restructuring

● Demography● Life expectancy● Human capital growth

● Globalization● Free trade● Communication and mobility

● Politics● Tax regime Labour / Capital● Social security vs individual savings

Hope

An evolution or a revolution ? :● Only the first point (Economy) is directly impacted by the crisis ● There are second order effects on the other points

● Returns of protectionism● Nationalisation of the economies● Political instability…

● World AL balance has evolved (geographically, private/public…) but is growing

A threat or an opportunity ? :● Adequacy between the offer and the demand has been challenged● Leaders are under pressure and Darwinism is ongoing

Our opinion: The asset management starts restructuring The window for change and opportunity is now

AUM & Actors

A steady increase of AUM and of number of HF until 2007…the crisis changes the picture

Performance

The decorrelation of the HF performance with the indexes in question

Alternative investment and liquidity crisis

The financial crisis impacts the HF industry

A performance issue Weak and correlated performance Limited number of strategies Small capacity wrt performance impact

Poor liquidity Limited financing facility Illiquidity of the underlying

Investors on hold Fall in AUM Investors raise their standards

Liquidity risk

Hedge fund are Long correlation in stable market and short the systemic correlation Long the spread of liquidity between investors - market

Standard Liquidity indicators Market impact Number of days to close the positions

Features to manage the liquidity Lock up Gates…

Unfortunately the set up of the fund have been made according to Market practice : Lock up Emergency : Gates

But not wrt the “real” liquidity risk

A toy example

Fund with a stock X in illiquid asset (price impact / NAV)

Buy an extra x of asset -> move the price up by y% -> NAV of fund + y% on the full AUM Sell x of asset -> move the price down by -y% -> NAV of fund - y% on the full AUM

A liquidity trap / gap risk

It is always easier to buy than to sell

An asymmetric risk / bubble

Tomatoes fund

Tomatoes producer

New investment

NAV

buy

A simple framework

Needs to move from a pure performance / risk model to an Asset and Liability model (which is the difference between the P&L and the NAV)

Liability : Investors, fees, etc… Asset : investment

Model of investors portfolio Each investors and prospects are ranked wrt its category, size of investment and probability to invest

or redeem.

Today AUM : 100 M$, new potential investors : 5 M$

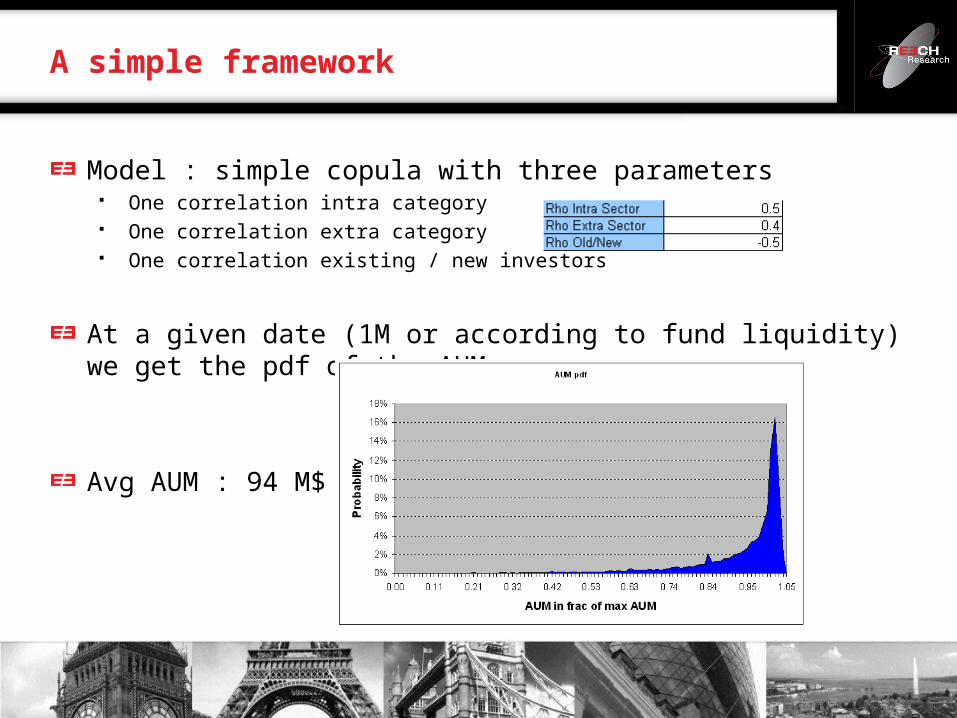

A simple framework

Model : simple copula with three parameters One correlation intra category One correlation extra category One correlation existing / new investors

At a given date (1M or according to fund liquidity) we get the pdf of the AUM

Avg AUM : 94 M$

Portfolio model One risky and non risky asset, no rate and dividend, simple BS model

One period model At the end of the period the AUM is impacted by the redemption and the new investment

Rebalancing without impacting the portfolio risk profile

Where is the growth of the AUM

Allocation model

σdWμdtS

dS

xX,S

dSθdX 0

ωXεX

1ωεθ ωε

Cost of rebalancing according to an average liquidity L

Optimal portfolio

Utility function

Special case

Allocation model

L1εθβλxεx,Uln

ωεX,EUArgMinθ

L1ωεθβ

The optimal allocation leads to an option on AUM

The optimal allocation accounts for the hedge of the option

The optimal allocation could be seen as the classical allocation minus the risk on the spread AUM / Asset

Intuitive approach

1-βCall2

1TλεX,Uln L

222 TE

2

*L

*

λσ

μ:θ1-εθcDeltaθθ

Target allocation in risky asset 55% Beta : 10% L : 20 %

% Change in risky asset allocation

If the proba of redemption increases, the investment in risky asset should decrease

If the investors are “correlated”, the investment in risky asset should decrease

Simple model result

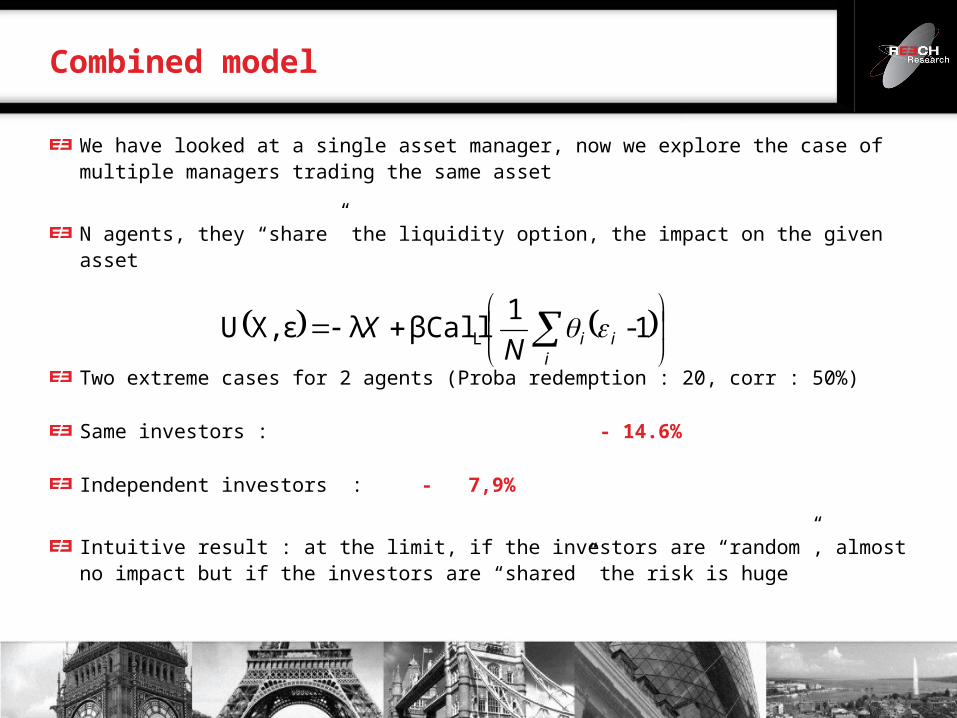

We have looked at a single asset manager, now we explore the case of multiple managers trading the same asset

N agents, they “share” the liquidity option, the impact on the given asset

Two extreme cases for 2 agents (Proba redemption : 20, corr : 50%)

Same investors : - 14.6%

Independent investors : - 7,9%

Intuitive result : at the limit, if the investors are “random”, almost no impact but if the investors are “shared” the risk is huge

Combined model

iiiN

X 1-1

βCallλεX,U L

The HF industry moved from “random” or “positive” flow of AUM to highly correlated outflows

It is crucial to quantify and manage the investors risk

Key points Better knowledge of investors Diversify the strategies Don’t be short of liquidity option

Extensions Investors redemption / fund performance correlation Multi period Define optimal liquidity of the fund (lock up, gates) Model the correlation to exogenous factor (demography, etc…)

Conclusion