loan compromise settlement guidelines fy 2013-14 loan compromise settlement guidelines 2013-14...

TRANSCRIPT

1

LOAN COMPROMISE SETTLEMENT GUIDELINES 2013-14

Loan Compromise Settlement Guidelines – FY 2013-14

CONTENTS

Item No. Description Page No.

1 Objective 3

2 Guiding principles 3

3 Compromise Settlement Scheme A - Eligibility B - Conditions

3-4

4 Compromise Settlement formula (I) D1 & D2 upto Rs.10 lakhs (ii) D1 & D2 above Rs.10 lakhs (iii) D3 loans upto Rs.2 lakhs (iv) D3 loans above Rs.2 lakhs & upto Rs.10 lakhs. (v) D3 loans above Rs.10 lakhs (vi) Assets Sold –D3 cases

4 –7

5 Relieving one or more co-obliants from the loan liability and releasing the property mortgaged by the co-obligants concerned

8

6 General conditions to be complied with CS processing 8 –9

7 Advance payment for CS 9

8 Date of CS calculation 9

9 Valuation for CS / Realisable value 9-10

10 Waiver of Penal Interest 10

11 Time limit for CS remittance 10

12 Belated Interest 10

13 Waiver of belated interest 10-11

14 Delegation of powers 11-12

15 Audit of Compromise Settlement 12

16 General guidelines 12 – 13

17 Annexure – I (NSR calculation) 14 - 15

2

LOAN COMPROMISE SETTLEMENT GUIDELINES 2013-14

KERALA FINANCIAL CORPORATION Loan Compromise Settlement Guidelines – FY 2013-14

1. OBJECTIVE The basic objective of the Loan Compromise Settlement Guidelines (LCSG) of the Corporation is to maximize recovery of dues out of Non-Performing Assets (NPAs) and doubtful accounts by proper follow-up. The other allied objectives are: i. To bring about uniformity & objectivity in approach while dealing with defaulting

borrowers. ii. To ensure that all the doubtful cases are duly attended to and an appropriate

Compromise Settlement formula applied expeditiously. Iii. As a measure of Risk Management so that reasonable amount can be recovered,

without hassle before allowing further erosion of assets. iv. To bring compassion in the approach of KFC towards cases needing humanitarian

consideration.

2. GUIDING PRINCIPLES i. The basic approach for Compromise Settlement would be practical, non prejudiced,

non-discreminatory objective and result oriented.

ii. While Compromise Settlement in each case would depend upon the facts of the case and attendant circumstances, general consistency in approach would be maintained while dealing with the defaulting borrowers.

iii. The cases of wilful default/suspected fraud/malfeasance would generally be legally pursued to its logical end. Compromise Settlement Scheme in such cases can be considered only on change of status in account due to subsequent findings, death or incapacitation of main promoter. CS can be considered with co-obligants/guarantors if they are not party to such wilful default / fraud / malpractice.

3. COMPROMISE SETTLEMENT SCHEME The Compromise Settlement application can be processed by BOs if it satisfies the norms / guidelines as stipulated below. Any deviation can be considered only with the prior permission of Chairman & Managing Director.

3

LOAN COMPROMISE SETTLEMENT GUIDELINES 2013-14

(A) Eligibility Where asset classification is Doubtful at the end of the immediately preceding FY (March 31st). (B) Conditions to be followed:

i. All Doubtful (D3, D2 & D1) cases as on beginning of the FY and continuing in the same category as on date of approaching for Compromise Settlement are eligible for Compromise Settlement.

ii. The default should not be wilful.

iii. Borrowers who have involved in fraudulent practices will not be eligible for Compromise Settlement.

iv. CS amount suggested is the MINIMUM.

v) Efforts shall be made to get higher amount depending on the realizable value ( see para 9B) of the assets as per latest valuation of each case.

vi) CS amount shall not be less than any of the sale offers received earlier or any offer made by the party in the past.

4. FORMULA FOR CALCULATION OF MINIMUM CS AMOUNT FOR DIFFERENT CATEGORY OF LOAN ACCOUNTS: (i). Doubtful loans (D1 & D2) upto Rs. 10 lakhs disbursed

Sl. No.

Amount Disbursed Value of primary + Collateral security as % of P + I+ OE +

NSR(Net) is *

Upto 100% Above 100%

1 Upto Rs.10/- lacs P+I+ OE(2)+20% NSR (Net) P+I+OE(2)+50% NSR (Net).

*Definition and calculation of NSR, net NSR and minimum Compromise Settlement amount as per NSR is given in Annexure – 1.

4

LOAN COMPROMISE SETTLEMENT GUIDELINES 2013-14

(ii). Doubtful loans (D1 & D2) above Rs. 10 lakhs disbursed

Table II Sl. No

Amounts Disbursed

Value of Primary and Collateral Security as percentage to the P+I+OE+NSR (Net) is

More than 150%

Bet-ween

125% - 150%

Bet- Ween 100% - 125%

Between 75 – 100% and

Between 50-75% and

Less than 50% and

Repaying Capacity worth & standing of Promoters & Guarantors is

Repaying Capacity worth &

standing of Promoters & Guarantors is

Repaying Capacity worth & standing of Promoters &

Guarantors is

High Mod & Low

High Mod & Low

High Mod & Low

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11)

1 Above Rs.10 lakhs

General Package

P+I+ OE(2)+ 103% NSR (Net)

P+I+ OE(2)+ 102% NSR (Net)

P+I= OE(2)+

NSR (Net)

P+I+ OE(2)+

90% NSR (Net)

P+I+OE(2)+ 80% NSR (Net)

P+I+ OE(2)+

75% NSR (Net)

P+I+ OE(2)+

65% NSR (Net)

P+I+ OE(2)+

60% NSR (Net)

P+I+ OE(2)+

50% NSR (Net)

(iii). D3 Loans upto Rs. 2 lakhs disbursed D3 Loans upto Rs.2 lakhs (Rupees Two lakhs only) disbursed can be settled for Principal outstanding plus other expenses irrespective of the Security position of the assets. (iv). D3 loans above Rs.2 lakhs and upto Rs.10 lakhs disbursed D3 cases in this category can be settled at Principal outstanding + O.E. subject to the following conditions:

(a) The total amount remitted in the loan account including CS amount should be

atleast 1.5 times of the amount disbursed.

(b) The amount of Rs.10.00 lakhs will be reckoned after considering all the loans availed by the promoter.

5

LOAN COMPROMISE SETTLEMENT GUIDELINES 2013-14

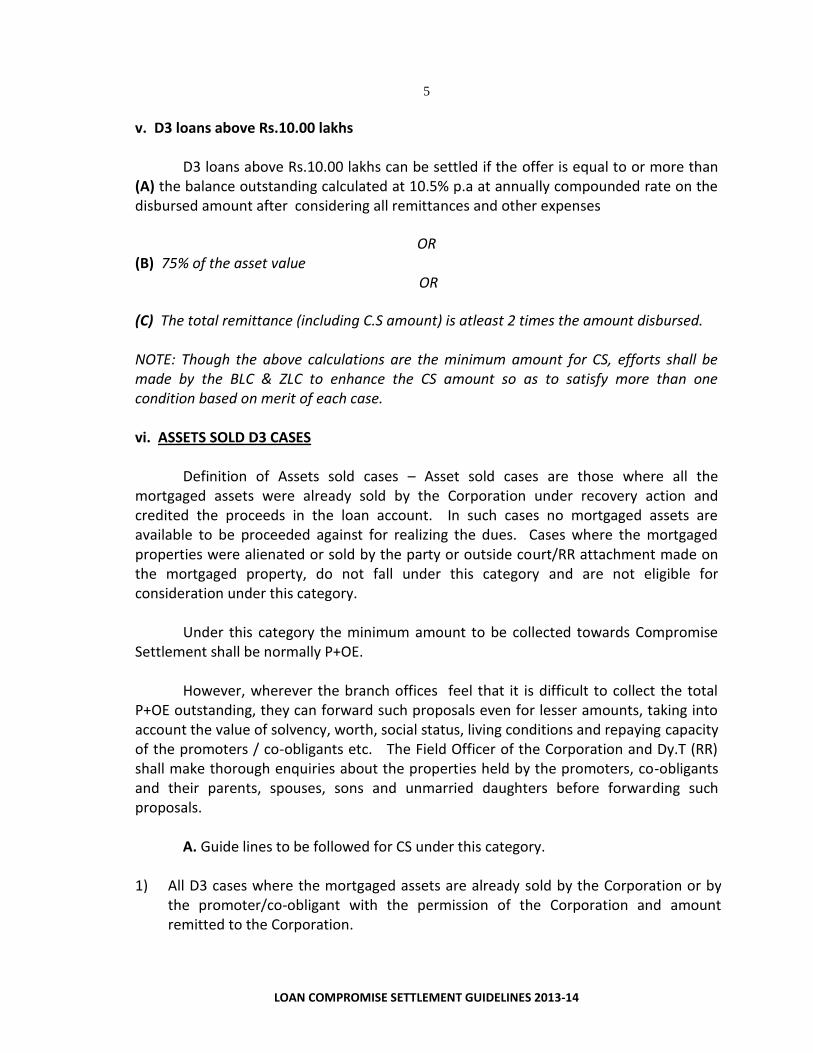

v. D3 loans above Rs.10.00 lakhs D3 loans above Rs.10.00 lakhs can be settled if the offer is equal to or more than (A) the balance outstanding calculated at 10.5% p.a at annually compounded rate on the disbursed amount after considering all remittances and other expenses

OR (B) 75% of the asset value

OR

(C) The total remittance (including C.S amount) is atleast 2 times the amount disbursed. NOTE: Though the above calculations are the minimum amount for CS, efforts shall be made by the BLC & ZLC to enhance the CS amount so as to satisfy more than one condition based on merit of each case. vi. ASSETS SOLD D3 CASES Definition of Assets sold cases – Asset sold cases are those where all the mortgaged assets were already sold by the Corporation under recovery action and credited the proceeds in the loan account. In such cases no mortgaged assets are available to be proceeded against for realizing the dues. Cases where the mortgaged properties were alienated or sold by the party or outside court/RR attachment made on the mortgaged property, do not fall under this category and are not eligible for consideration under this category. Under this category the minimum amount to be collected towards Compromise Settlement shall be normally P+OE. However, wherever the branch offices feel that it is difficult to collect the total P+OE outstanding, they can forward such proposals even for lesser amounts, taking into account the value of solvency, worth, social status, living conditions and repaying capacity of the promoters / co-obligants etc. The Field Officer of the Corporation and Dy.T (RR) shall make thorough enquiries about the properties held by the promoters, co-obligants and their parents, spouses, sons and unmarried daughters before forwarding such proposals. A. Guide lines to be followed for CS under this category. 1) All D3 cases where the mortgaged assets are already sold by the Corporation or by

the promoter/co-obligant with the permission of the Corporation and amount remitted to the Corporation.

6

LOAN COMPROMISE SETTLEMENT GUIDELINES 2013-14

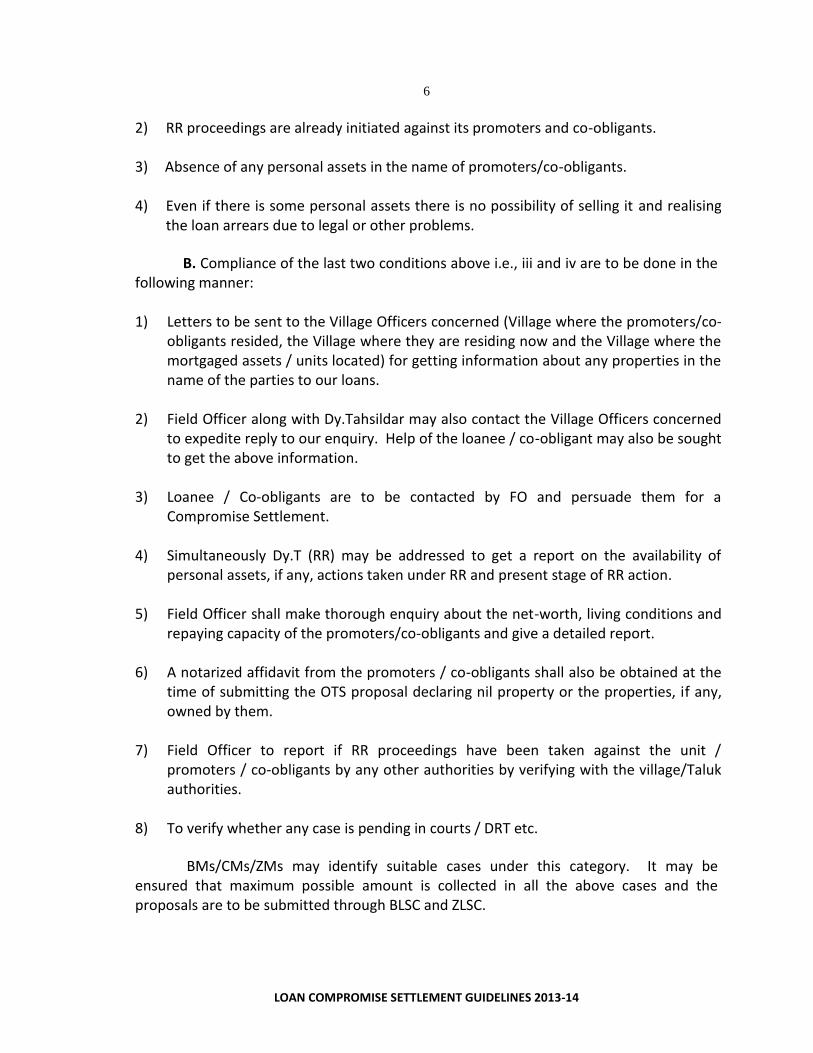

2) RR proceedings are already initiated against its promoters and co-obligants.

3) Absence of any personal assets in the name of promoters/co-obligants.

4) Even if there is some personal assets there is no possibility of selling it and realising the loan arrears due to legal or other problems.

B. Compliance of the last two conditions above i.e., iii and iv are to be done in the following manner: 1) Letters to be sent to the Village Officers concerned (Village where the promoters/co-

obligants resided, the Village where they are residing now and the Village where the mortgaged assets / units located) for getting information about any properties in the name of the parties to our loans.

2) Field Officer along with Dy.Tahsildar may also contact the Village Officers concerned to expedite reply to our enquiry. Help of the loanee / co-obligant may also be sought to get the above information.

3) Loanee / Co-obligants are to be contacted by FO and persuade them for a

Compromise Settlement.

4) Simultaneously Dy.T (RR) may be addressed to get a report on the availability of personal assets, if any, actions taken under RR and present stage of RR action.

5) Field Officer shall make thorough enquiry about the net-worth, living conditions and repaying capacity of the promoters/co-obligants and give a detailed report.

6) A notarized affidavit from the promoters / co-obligants shall also be obtained at the

time of submitting the OTS proposal declaring nil property or the properties, if any, owned by them.

7) Field Officer to report if RR proceedings have been taken against the unit / promoters / co-obligants by any other authorities by verifying with the village/Taluk authorities.

8) To verify whether any case is pending in courts / DRT etc.

BMs/CMs/ZMs may identify suitable cases under this category. It may be ensured that maximum possible amount is collected in all the above cases and the proposals are to be submitted through BLSC and ZLSC.

7

LOAN COMPROMISE SETTLEMENT GUIDELINES 2013-14

5. RELIEVING ONE OR MORE OF CO-OBLIGANTS FROM THE LOAN LIABILITY AND RELEASING THE PROPERTY MORTGAGED BY THE CO-OBLIGANT CONCERNED. The promoter is primarily responsible for repayment of the loan. So his liability cannot be diluted and hence cannot be considered for relieving of liability before closure of the loan account. However, for all loans which are eligible for Compromise Settlement relieving of liability of co-obligant/co-obligants who are not direct beneficiaries of the project can be considered for relieving their liability of the loan subject to any of the following conditions: (A) 90% of the proportionate amount of the security compared to the balance outstanding as on date of consideration is remitted by the party. Example Balance outstanding as on date - 100 Value of security Owned by promoter - 70 Owned by co-obligant – 1 - 80 Owned by co-obligant – 2 - 50 200 ==== For relieving co-obligants -1 = Loan B/O x Value of security owned by him X 90% Total security

= 100 x 80 X 0.9 = 36 200 For relieving co-obligant – 2 = 100 x 50 X 0.9 = 22.5 200 (B) Eligible CS amount of the unit/loan account is remitted by the party concerned. 6. GENERAL CONDITIONS TO BE COMPLIED WITH C.S.PROCESSING

In case of all CS proposals it is mandatory that the CMs/ BMs shall make thorough enquiry about the properties/ assets held by the promoters/ co-obligants/guarantors. Procedure for ascertaining the repaying capacity is mentioned below: Branch Offices may report the following along with the Compromise Settlement proposals: a) The Field Officer shall make a thorough enquiry about the properties held by the

borrower/guarantors and give reports.

8

LOAN COMPROMISE SETTLEMENT GUIDELINES 2013-14

b) Field Officer shall physically verify and report whether the unit is existing and/or working. In case the unit is closed, the date/month in which it was closed and brief highlights of working results/financials at the time of closure shall be included in the report. Wherever the units are functioning, a brief working result of the unit shall be included in the report.

c) F.O. to report if RR proceedings against the unit/promoters/guarantors has been initiated by any other authorities by verifying with the village/Taluks authorities.

d) Where borrowers have filed cases in Courts/ DRT, if Court cases can be withdrawn, then out of Court settlement can be preferred by Compromise Settlement.

7. ADVANCE PAYMENT FOR C.S

Application for Compromise Settlement need be registered by B.O. only if Compromise Settlement advance computed at 10% of balance outstanding or 25% of principal outstanding (whichever is less) is remitted. The amount has to be kept in Compromise Settlement appropriation account. Generally no application should be processed without Compromise Settlement advance as above. However in deserving cases C&MD can give permission to process C.S. application without advance.

For assets sold cases, Compromise Settlement advance can be waived, if

required, by the CM/BM. For loan upto 2 lakhs disbursed, BLSC can consider reduction in CS advance based on merit of each case. 8. DATE OF COMPROMISE SETTLEMENT CALCULATION The balance outstanding as on 1st of the month in which Compromise Settlement proposal is registered is taken for the purpose of calculating the sacrifice. NSR / yield calculation will be upto the same date.

9. VALUATION FOR COMPROMISE SETTLEMENT

(A) Branch office to follow the procedures laid down in the Valuation Policy of the Corporation. Valuation should not be more than one year old at the time of consideration of CS. Except for sale of assets under Section 29 of SFC's act, all valuations to be taken by the officers of the Corporation. External valuation need be taken only if the Branch Head or the sanctioning authority decides so and its cost shall be borne by the Corporation under OE. (B) Realizable value of the asset is the amount realizable on distress sale within two months on 'as is where is’ condition taking into account the market value, book value, existing market conditions, depreciation in quality of assets, liabilities (such as Sales Tax,

9

LOAN COMPROMISE SETTLEMENT GUIDELINES 2013-14

KSEB, other taxes, Court attachments etc) attached to the unit, present working condition of the Plant and Machinery, lie and nature of the land, Government restrictions etc. This shall be fixed / finalised by the BLC. 10. OTHER RELIEFS - WAIVER OF PENAL INTEREST

For exiting the loan, for reasons of non-viability of project, expiry of promoters or any such deserving cases, waiver of penal interest can be considered for all NPA accounts depending on the merit of the case, provided foreclosure charge is not applicable.

11. TIME LIMIT FOR CS REMITTANCE

Normally Compromise Settlement is allowed for 3 months only. Effective action has to be initiated / continued in case the remittance is not made within 3 months. Some times the loanees are not able to pay the Compromise Settlement amount due to various constraints like selling of property which takes time, and mobilization of resources from friends and relatives, raising funds from other institutions, etc. In such genuine cases the time for payment of Compromise Settlement amount can be extended as per the delegation given at 14(c).

12. BELATED INTEREST

No interest will be charged if Compromise Settlement amount is remitted within 3

months from the date of sanction of Compromise Settlement. Interest at 12% (simple) will be charged on the balance amount to be remitted out of the Compromise Settlement amount for the period exceeding three months.

13. WAIVER OF BELATED INTEREST For recommendation of waiver of belated interest of already sanctioned

Compromise Settlement cases, any one of the following conditions (i to ix) may be satisfied.

i. Borrower/ co-obligants are financially poor (to be specifically commented by Branch Level Committee).

ii Borrower/ co-obligants have no other property other than residential property.

iii. Borrower/ co-obligants are critically sick and being treated for terminal diseases. iv. Borrower/ co-obligants have absconded/ abandoned the mortgaged assets.

v. Borrower/ co-obligants are dead and legal heirs are coming to settle the debts.

10

LOAN COMPROMISE SETTLEMENT GUIDELINES 2013-14

vi. Where primary or collateral assets have been seized and sold by the Corporation/ Revenue Authorities before sanction of Compromise Settlement.

vii. The borrower / co-obligants have remitted the Compromise Settlement by selling all

the mortgaged properties.

viii. If the Branch Level Committee is of the opinion that the promoter has suffered heavy losses by venturing into the project.

ix. Even after waiver of belated interest the amount remitted under CS is as per CS norms as on the date of waiver.

NOTE (a) Any proposal for waiver for B.I should clearly specify the condition (i to ix) under which the proposal is recommended, failing the proposal will not be considered. (b) For cases where delay in CS remittance is more than one year CS amount as per present norms as on date of waiver must be calculated and furnished.

14. DELEGATION OF POWERS

(A) Compromise Settlement (i) ZLC : Sacrifice upto Rs. 15 lakhs as per norms.

(ii) GMLC : Sacrifice upto Rs.25.00 lakhs as per norms.

(iii) Any waiver of outstanding beyond the above amount can be approved by the CMD

Level committee and any deviation from norms is to be approved by EC/Board.

(B) Penal Interest Waiver ZLC - Upto Rs.50,000/- GMLC - Upto Rs.2,00,000/- CMDLC - Above Rs.2,00,000/- (C) Extension of CS period after the original period of 3 months (with full belated interest) CM/BM - Upto 9 months ZM - Upto 1 year GM - Upto 2 years CMD - Above 2 years

11

LOAN COMPROMISE SETTLEMENT GUIDELINES 2013-14

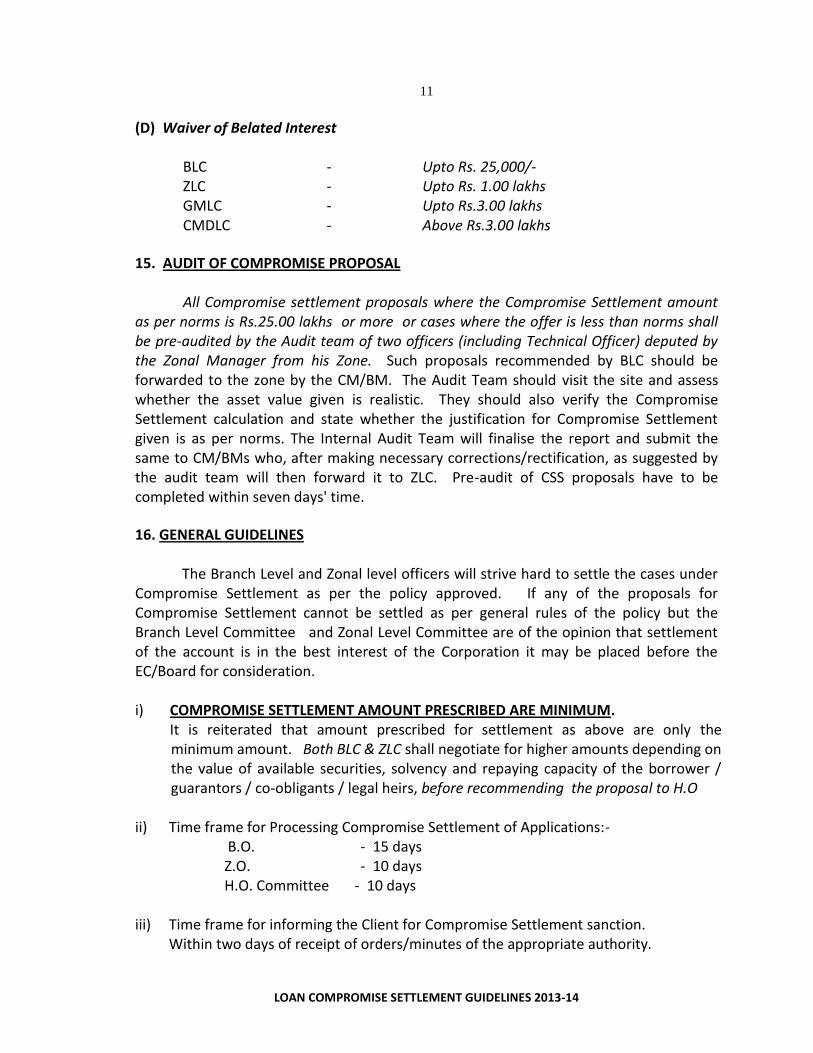

(D) Waiver of Belated Interest BLC - Upto Rs. 25,000/- ZLC - Upto Rs. 1.00 lakhs GMLC - Upto Rs.3.00 lakhs CMDLC - Above Rs.3.00 lakhs

15. AUDIT OF COMPROMISE PROPOSAL All Compromise settlement proposals where the Compromise Settlement amount as per norms is Rs.25.00 lakhs or more or cases where the offer is less than norms shall be pre-audited by the Audit team of two officers (including Technical Officer) deputed by the Zonal Manager from his Zone. Such proposals recommended by BLC should be forwarded to the zone by the CM/BM. The Audit Team should visit the site and assess whether the asset value given is realistic. They should also verify the Compromise Settlement calculation and state whether the justification for Compromise Settlement given is as per norms. The Internal Audit Team will finalise the report and submit the same to CM/BMs who, after making necessary corrections/rectification, as suggested by the audit team will then forward it to ZLC. Pre-audit of CSS proposals have to be completed within seven days' time.

16. GENERAL GUIDELINES

The Branch Level and Zonal level officers will strive hard to settle the cases under Compromise Settlement as per the policy approved. If any of the proposals for Compromise Settlement cannot be settled as per general rules of the policy but the Branch Level Committee and Zonal Level Committee are of the opinion that settlement of the account is in the best interest of the Corporation it may be placed before the EC/Board for consideration.

i) COMPROMISE SETTLEMENT AMOUNT PRESCRIBED ARE MINIMUM.

It is reiterated that amount prescribed for settlement as above are only the minimum amount. Both BLC & ZLC shall negotiate for higher amounts depending on the value of available securities, solvency and repaying capacity of the borrower / guarantors / co-obligants / legal heirs, before recommending the proposal to H.O

ii) Time frame for Processing Compromise Settlement of Applications:- B.O. - 15 days Z.O. - 10 days H.O. Committee - 10 days

iii) Time frame for informing the Client for Compromise Settlement sanction. Within two days of receipt of orders/minutes of the appropriate authority.

12

LOAN COMPROMISE SETTLEMENT GUIDELINES 2013-14

iv) The RR Commission if charged by the RR authorities has to be additionally paid by

the loanee. This should be communicated to the loanee.

v) Cases pending before any Court of law should be withdrawn by the party before settling the account. In such cases remarks of Legal Section of Branch Office also to be obtained and incorporated in the CS note.

vi) In cases where CS applications are rejected, the promoters can apply afresh.

vii) Under no circumstances shall Compromise Settlement result in refund of remittances already received by the Corporation.

viii) Compromise Settlement cases already sanctioned will not normally be re opened.

However cases that may require special consideration on account of issues beyond the control of borrower can be reopened with the approval of C&MD.

ix) The Loan Recovery Policy will come into force with effect from 01.04.2013 and shall

be valid till a subsequent review of the same is carried out and advised.

x) The revised Compromise Settlement Guideline above supersedes all earlier guidelines on Compromise Settlement issued earlier.

xi) Any clarifications regarding the Compromise Settlement Guidelines or any related

instructions or procedures etc. can be issued by C&MD from time to time.

xii) Any one who has obtained Compromise Settlement shall not be normally eligible for future loans from the Corporation. However, where the promoters have settled their loan accounts under Compromise Settlement due to failure of units for reasons beyond their control application for further loans can be accepted only after obtaining approval from C&MD.

Annexure - 1

Definitions for NSR

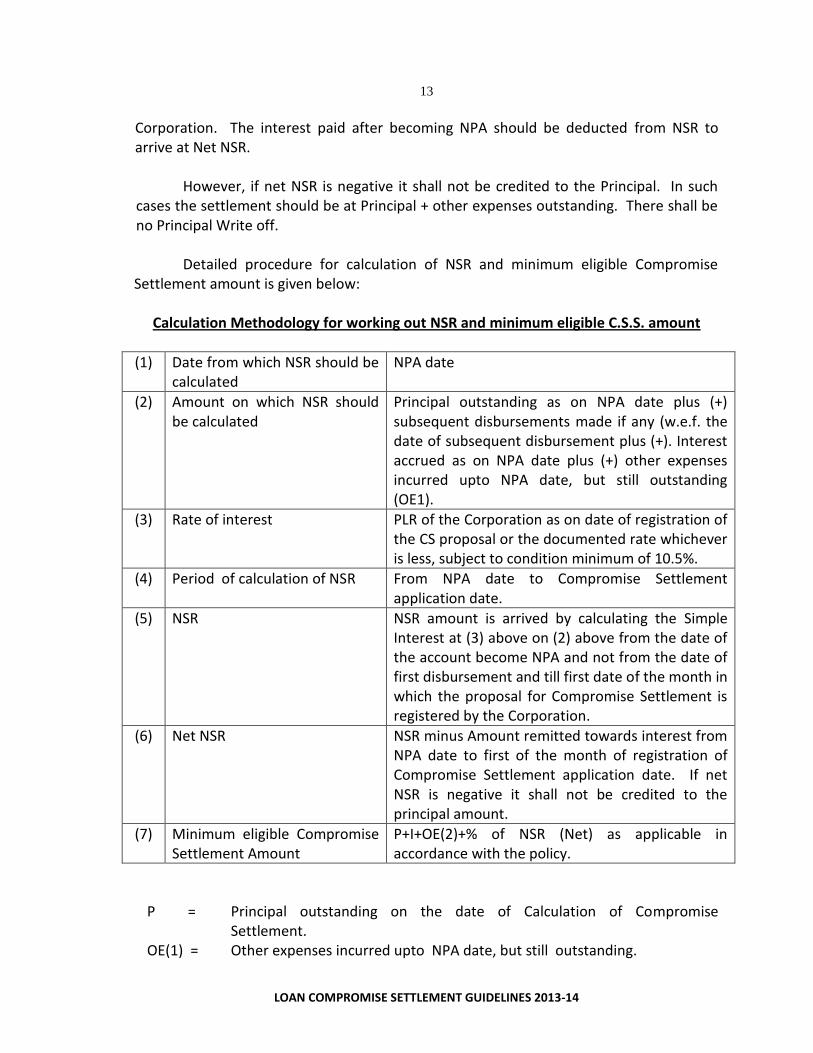

NSR = NSR is the amount to be realized towards interest from the date the account turned into NPA till the first of the month of registration of CSS proposal.

NSR amount is arrived by calculating the Simple Interest on P+I+OE (1) from the date of the account turned NPA and not from the date of first disbursement and till first of the month in which the proposal for Compromise Settlement is registered by the

13

LOAN COMPROMISE SETTLEMENT GUIDELINES 2013-14

Corporation. The interest paid after becoming NPA should be deducted from NSR to arrive at Net NSR.

However, if net NSR is negative it shall not be credited to the Principal. In such cases the settlement should be at Principal + other expenses outstanding. There shall be no Principal Write off.

Detailed procedure for calculation of NSR and minimum eligible Compromise Settlement amount is given below:

Calculation Methodology for working out NSR and minimum eligible C.S.S. amount

(1) Date from which NSR should be calculated

NPA date

(2) Amount on which NSR should be calculated

Principal outstanding as on NPA date plus (+) subsequent disbursements made if any (w.e.f. the date of subsequent disbursement plus (+). Interest accrued as on NPA date plus (+) other expenses incurred upto NPA date, but still outstanding (OE1).

(3) Rate of interest PLR of the Corporation as on date of registration of the CS proposal or the documented rate whichever is less, subject to condition minimum of 10.5%.

(4) Period of calculation of NSR From NPA date to Compromise Settlement application date.

(5) NSR NSR amount is arrived by calculating the Simple Interest at (3) above on (2) above from the date of the account become NPA and not from the date of first disbursement and till first date of the month in which the proposal for Compromise Settlement is registered by the Corporation.

(6) Net NSR NSR minus Amount remitted towards interest from NPA date to first of the month of registration of Compromise Settlement application date. If net NSR is negative it shall not be credited to the principal amount.

(7) Minimum eligible Compromise Settlement Amount

P+I+OE(2)+% of NSR (Net) as applicable in accordance with the policy.

P = Principal outstanding on the date of Calculation of Compromise

Settlement. OE(1) = Other expenses incurred upto NPA date, but still outstanding.

14

LOAN COMPROMISE SETTLEMENT GUIDELINES 2013-14

OE(2) = Other expenses incurred between NPA date and Compromise Settlement date but outstanding on the date of calculation of Compromise Settlement.

NSR = Net Simple Rate (this is the amount to be realized towards interest from the date of account turning into NPA till the first of the month of registration of CSS proposal).

OE = OE(1) + OE(2) I = Interest accrued as on NPA date.