loan handbook for world bank...

TRANSCRIPT

Loan Handbook for World Bank Borrowers

February 2017

Table of Contents ABBREVIATIONS AND ACRONYMS ......................................................................................................................... 1

INTRODUCTION ..................................................................................................................................................... 2

VOLUME 1: WORLD BANK FINANCED OPERATIONS AND FINANCING PRODUCTS

1. WORLD BANK–FINANCED OPERATIONS ......................................................................................................... 5

2. WORLD BANK FINANCING PRODUCTS ............................................................................................................ 9

VOLUME 2: DISBURSEMENTS

3. WITHDRAWAL OF FINANCING PROCEEDS .................................................................................................... 34

4. INVESTMENT PROJECT FINANCING............................................................................................................... 41

5. PROGRAM-FOR-RESULTS FINANCING ........................................................................................................... 68

6. DEVELOPMENT POLICY FINANCING .............................................................................................................. 72

ANNEXES ............................................................................................................................................................. 73

VOLUME 3: DEBT SERVICE

7. BILLING ........................................................................................................................................................ 79

8. OVERDUE AND SANCTIONS POLICY .............................................................................................................. 84

9. PARTIAL WAIVER OF LOAN CHARGES ........................................................................................................... 87

10. PREPAYMENTS .............................................................................................................................................. 89

Abbreviations and Acronyms ARM Average repayment maturity IFR Interim unaudited financial reports ASD Authorized signatories designation IMF International Monetary Fund BSA Basis swap adjustment IPF Investment Project Financing BTF billable trust fund ¥ Japanese yen

£stg British pounds sterling LIBOR London Interbank Offered Rate CPL Currency pool loan MDA Master Derivatives Agreement CTF Clean Technology Fund MDRI Multilateral Debt Relief Initiative DDO Deferred Drawdown Option PforR Program-for-Results DLI Disbursement-linked indicator PPA Project/Program Preparation Advance DPF Development Policy Financing PPF Project Preparation Facility DSA Debt sustainability analysis SBL Single borrower limit EEC European Economic Commission SC Special commitment € Euro SDPF Special Development Policy Financing FEF Front-end fee SDR Special drawing rights FSL Fixed spread loan SIDC Secure Identification Device

Credentials GNI Gross national income SWIFT Society for Worldwide Interbank

Financial Telecommunication HIPC Initiative

Heavily Indebted Poor Countries Initiative

UN United Nations

IBRD International Bank for Reconstruction and Development

UNSC United Nations Security Council

IDA International Development Association US$ U.S. dollar IFL IBRD Flexible Loan VSL Variable spread loan

1

Introduction This Loan Handbook for World Bank Borrowers (the handbook) sets out guidance on disbursement arrangements and debt services for loans or financing provided or administered by the World Bank.1 The handbook provides detailed information about the World Bank’s lending instruments, financial products and terms, policy on overdue payments and sanctions, partial waiver of loan charges policy, and billing procedures.

The handbook has been arranged in three volumes: • Volume 1 covers World Bank–financed operations and financing products. • Volume 2 covers disbursements. • Volume 3 covers debt service.

The Loan Operations Unit in the Financial Operations Department advises and assists in disbursement and billing arrangements, including processing withdrawal applications and overseeing debt service by borrowers.

Although the handbook comprehensively covers most aspects of the lending cycle, it is not exhaustive. If you are unable to find what you need, please contact the Loan Operations representative assigned for your country by logging in to Client Connection (under the ‘My Portfolio’ page, and ‘Contact Us’), or write to [email protected].

This handbook supersedes all previous editions of the handbooks on disbursement and debt servicing and takes effect immediately. The electronic version is available on the World Bank’s website (http://www.worldbank.org) and in Client Connection. The handbook will be updated periodically to reflect feedback from users and changes in disbursement and debt service policies and practices.

Loans Operations Financial Operations Department World Bank Group 1818 H Street NW Washington, DC 20433 E-mail: [email protected]

Copyright Disclaimer: The Loan Handbook for World Bank Borrowers provides guidance on the World Bank’s disbursement and debt servicing policies and procedures. Bank policy and procedure documents referenced herein may be obtained by going to our website, http://www.worldbank.org, or by writing to us at [email protected]. This handbook does not provide complete information about all documents, policies, and procedures that are referenced. For complete information on particular policies, the user should refer to the relevant source document. This handbook is not a contractual or a legal document.

© June 2016 World Bank Group. All rights reserved.

1 The World Bank (or the Bank) includes the International Bank for Reconstruction and Development (IBRD) and the International Development Association (IDA), whether acting for its own account or as administrator of trust funds funded by donors. World Bank loan or financing includes any loan, credit, grant, or program or project preparation advances made by World Bank from its own resources or from trust funds funded by other donors and administered by the World Bank, or from a combination of such financing. Borrower means a borrower or recipient of a World Bank loan for an operation and any other entity involved in the implementation of the operation financed by the Bank loan.

2

Volume 1

World Bank–Financed Operations and Financing Products

3

Contents 1. WORLD BANK–FINANCED OPERATIONS ......................................................................................................... 5

1.1 KEY DOCUMENTS ................................................................................................................................................ 5 1.2 FINANCING INSTRUMENTS .................................................................................................................................... 6 1.3 LOAN CYCLE OVERVIEW ....................................................................................................................................... 6

2. WORLD BANK FINANCING PRODUCTS ............................................................................................................ 9

2.1 IBRD LOAN PRODUCTS ........................................................................................................................................ 9 2.1.1 IBRD Flexible Loan .................................................................................................................................. 9 2.1.2 IBRD Contingent Financing—Deferred Drawdown Option .................................................................. 13 2.1.3 Special Development Policy Financing (SDPFs) .................................................................................... 14

2.2 IDA DEVELOPMENT CREDITS .............................................................................................................................. 15 2.2.1 IDA Credits ........................................................................................................................................... 15 2.2.2 IDA Lending Currencies ........................................................................................................................ 15 2.2.3 IDA Current Charges and Rates ............................................................................................................ 16 2.2.4 IDA Repayment Terms ......................................................................................................................... 17 2.2.5 Acceleration of Credit Repayments to IDA ........................................................................................... 17 2.2.6 Policy Framework for Voluntary Prepayments .................................................................................... 18

2.3 IDA GRANTS.................................................................................................................................................... 18 2.4 GUARANTEES ................................................................................................................................................... 19

2.4.1 Key Features of Guarantees ................................................................................................................. 19 2.4.2 Guarantee Instrument—Type and Eligibility ........................................................................................ 19 2.4.3 Agreements for Guarantee Transactions ............................................................................................. 20 2.4.4 Fees and Pricing on Guarantees ........................................................................................................... 21 2.4.5 Guarantee Trigger Events and Disbursement Arrangements .............................................................. 21

2.5 OTHER PRODUCTS ADMINISTERED BY THE WORLD BANK .......................................................................................... 22 2.5.1 Clean Technology Fund—Grants, Loans, and Guarantees ................................................................... 22 2.5.2 Billable Trust Funds .............................................................................................................................. 23 2.5.3 European Economic Commission Credits ............................................................................................. 23 2.5.4 Project Preparation Facility (PPF) ........................................................................................................ 24

2.6 IBRD RISK MANAGEMENT PRODUCTS .................................................................................................................. 25 2.6.1 IBRD Products with Embedded Conversion Options ............................................................................ 25 2.6.2 IBRD Freestanding Swaps and Non-IBRD Hedges ................................................................................ 26

2.7 DEBT RELIEF INITIATIVES .................................................................................................................................... 27 2.7.1 Debt Service Trust Funds ...................................................................................................................... 27 2.7.2 Heavily Indebted Poor Countries (HIPC) Initiative ................................................................................ 28 2.7.3 Multilateral Debt Relief Initiative ......................................................................................................... 28

4

1. World Bank–Financed Operations 1. This section describes the financing instruments that are available to borrowers for operations

financed by the World Bank. It also includes a step-by-step guide to the stages of the loan cycle and a brief overview of the key documents governing disbursement for World Bank–financed operations.

1.1 Key Documents

2. Disbursements for World Bank–financed operations are governed by the following key documents:

• Articles of Agreement. The Articles of Agreement of the International Bank for Reconstruction and Development (IBRD)2 and the International Development Association (IDA)3 are signed by all the member countries of the respective institutions and are their governing charters. The Articles require the institutions to ensure that funds from the financing account are used only for the purposes granted and that the borrower may withdraw funds only to meet expenditures as they are incurred.

• General Conditions. The General Conditions4 set forth certain terms and conditions that are generally applicable to IBRD loans and IDA credits and grants. Provisions covered include withdrawals, financing terms, program and project execution, effectiveness, and cancellations.

• Standard Conditions. The Standard Conditions5 set forth certain terms and conditions that are generally applicable to trust funds and advances made by the Bank under the Project Preparation Facility (PPF). Provisions covered include withdrawals, project execution, terms, cancellation, suspension, and refund.

• Financing Agreement. A financing agreement for a loan sets out the terms and conditions of the loan. The agreement includes eligible programs and activities; reporting requirements; fiduciary requirements; procurement provisions for Investment Project Financing (IPF); expenditure categories for IPF; disbursement conditions, if any; and key program/project dates and financial terms, if applicable.

• Disbursement Guidelines for Investment Project Financing. The Disbursement Guidelines for Investment Project Financing6 contain the standard provisions governing the withdrawal of proceeds from the financing account. The guidelines apply to IPF only. Provisions covered include disbursement arrangements, withdrawals, designated accounts, ineligible expenditures, and refunds.

• Disbursement Letter. The disbursement letter specifies the disbursement arrangements to be used for each World Bank–financed IPF and Program-for-Results (PforR) operation.

2 http://siteresources.worldbank.org/EXTABOUTUS/Resources/IBRDArticlesOfAgreement_links.pdf 3 http://www.worldbank.org/ida/articles-agreement/IDA-articles-of-agreement.pdf 4 http://siteresources.worldbank.org/BRAZILINPOREXTN/Resources/3817166-1242680408578/General_Conditions.pdf 5 http://go.worldbank.org/LXIOJ9CTI0 6 http://siteresources.worldbank.org/PROJECTS/Resources/DisGuideEng.pdf

5

1.2 Financing Instruments

3. The World Bank provides financing to its borrowers through three financing instruments (figure 1).

Figure 1. Financing Instruments

Note: For more guidance on these financing instruments, refer to section 4 on IPF, section 5 on PforR, and section 6 on DPF.

4. Hybrid financing is the term used when a recipient’s program or project is financed using two or more financing instruments. Hybrids typically involve a combination of IPF and DPF or IPF and PforR financing.

5. Depending on the nature of the program or project and the needs of the borrower, there may be separate financing agreements (that is, one for each instrument) or one consolidated financing agreement with separate sections describing the respective financing modalities. Even when a single financing agreement is used, withdrawals of financing proceeds follow the instrument-specific policies and procedures as set out in the financing agreement and disbursement letter.

6. In cases of hybrid financing, the disbursement method selected when submitting withdrawal applications depends on the instrument.

1.3 Loan Cycle Overview

7. Bank-financed operations follow a standard loan cycle,7 as depicted in figure 2 and described in table 1.

7 For the purposes of this handbook, loan cycle includes all World Bank financing other than guarantees.

Investment Project Financing (IPF)

Disburses for eligible expenditure(Section 4)

Program-for-Results (PforR)

Disburses for results achieved

(Section 5)

Development Policy Financing (DPF)

Disburses for policy action implementation

(Section 6)

6

Figure 2. Stages in a Loan Cycle

1. Preparation

2. Appraisal

3. Negotiation

4. Approval

5. Signing

6. Effectiveness

7. Disbursements, restructuring,

refunds, cancellations and

loan closing

8. Billing receipts and overdue management

9. Final maturity

7

Table 1. Stages in a Loan Cycle

Stage Description

1. Preparation Comprises identification and concept review. This stage involves identifying programs/projects that support the Country Partnership Framework, the government agency responsible for preparation, key stakeholders, and target beneficiaries. Following this stage, a concept note is created; the design is determined; economic, technical, social, and environmental feasibility are assessed; and potential risks and safeguard issues are identified.

2. Appraisal Involves confirming the expected outcomes of the program/project; reviewing economic, technical, environmental, social, and fiduciary aspects; and agreeing on the institutional arrangements to implement the program/project and timelines. The program/project appraisal document and draft financing agreements are prepared.

3. Negotiation Involves resolution of any outstanding issues from the appraisal stage, agreement on the procurement strategy and procurement plan for Investment Project Financing (IPF), financing and disbursement arrangements (including disbursement letter for IPF), and terms and conditions.

4. Approval Involves review and approval of program/project and financing documents by the Bank’s Board of Executive Directors or by the management.

5. Signing Involves signing of legal financing agreements by the Bank and client representatives.

6. Effectiveness Involves determination by Bank officials that predetermined and agreed conditions have been met to begin disbursements.

7. Disbursements, restructuring, refunds, cancellations, and loan closing

Involves disbursements to borrowers based on valid withdrawal applications for program financing and eligible expenditures related to program/project activities up to the closing date. Refunds of ineligible expenditures and unused advances, cancellations initiated by the Bank or the client, final disbursements, and loan closure are handled at this stage.

8. Billing receipts and overdue management

Involves support to borrowers for debt service, by means of billing statements after signing in certain cases and after effectiveness in all cases (loans, credits, and guarantees). Debt service of charges by borrowers starts once disbursements are made under the loan or credit. In certain cases, debt service of charges begins after the signing date of the agreement. Principal repayments start after the agreed grace period ends. Applying borrowers’ debt service payments to dues and following up on overdue cases, according to Bank policies and procedures, are the other activities carried out at this stage.

9. Final maturity Represents the final repayment date as specified in the financing agreement.

8

2. World Bank Financing Products 8. This section covers the various products offered by the Bank. IBRD offers eligible member

countries access to a flexible and low-cost set of tools for borrowing, hedging, and enhancing credit. IDA provides concessional lending to the poorest developing countries by providing credits at little or no interest and grants. Other products administered by the World Bank include guarantees, and Project Preparation Facility (PPF) and loans offered through Trust Funds or other special arrangements with donors. This section also covers IBRD risk management products and debt relief initiatives.

9. The Bank has developed a Financial Instruments application for iPad, iPhone, and the web. This is a public app and site that enables borrowers to access information such as financial terms and rates and to prepare amortization schedules for IBRD and IDA products. Client forms and reference documents are also available. More details about the Financial Instruments app are available at this link.8

2.1 IBRD Loan Products

10. This section describes the terms and conditions applicable to IBRD’s current lending products.9 IBRD offers loans for project, program, or policy purposes, as well as hedging products to manage currency and interest rate risk exposures and guarantee products to eligible member countries. By using its AAA credit rating, IBRD can offer loans that are more competitive and flexible than other financing options in international financial markets.

11. The terms of the loans—including currency, repayment schedule, lending spread, and type (fixed and variable)—are decided at the time of loan negotiation.

12. IBRD currently offers the following types of loans:

• IBRD Flexible Loan (IFL) • IFL with a Deferred Drawdown Option (DDO) • Special Development Policy Financing (SDPF)

2.1.1 IBRD Flexible Loan

13. The IFL offers a variety of terms to allow borrowers to customize their loans to meet their debt management or project or program needs. Table 2 describes the various features of the IFL.

8 https://itunes.apple.com/us/app/financial-instruments/id857651189?mt=8 9 http://treasury.worldbank.org/bdm/htm/financing.html

9

Table 2. IFL Key Terms and Conditions

Term Details

Loan currencies

Currency of commitment: Refers to the denomination of the loan as noted in the loan agreement. IBRD Flexible Loans (IFLs) are generally offered in the major currencies: the euro (€), the British pound (£stg.), the Japanese yen (¥), and the U.S. dollar (US$). Other currencies may be available, subject to the existence of a liquid swap market. • Currency of disbursement: Disbursements may be made in various currencies as

requested by the client. Currencies are acquired by IBRD and passed on to the client. The loan obligation, however, remains in the currencies in which the loan is denominated.

• Currency of repayment: The loan principal, interest, and any other fees are normally payable in the currencies of commitment unless a currency conversion has been executed.

Lending rate

• The lending rate consists of a variable reference rate plus a spread. • The lending rate is reset semiannually on the loan’s interest payment dates and applies

to interest periods beginning on those dates. • The reference rate or base rate is normally the six-month London Interbank Offered

Rate (LIBOR) or Euro Interbank Offered Rate (EURIBOR) at the start of an interest period. For loans that have been converted to a local currency, the reference rate may be a recognized commercial bank floating rate.

• The current lending ratesa can be found on the World Bank Treasury website.

Lending rate spread

Borrowers have the choice between a fixed or variable spread. • Variable spread Variable Spread = Contractual Lending Spread + Maturity Premium + Actual Funding Spread The Actual Funding Spread comprises the Bank’s average margin relative to LIBOR for the preceding six months. • Fixed spread

Fixed Spread = Contractual Lending Spread + Maturity Premium + Market Risk Premium + Projected Funding Cost + Basis swap adjustment for non-US$ loans

Projected Funding Cost refers to IBRD’s projected funding cost margin relative to US$ LIBOR. The fixed spread is determined at the time the loan is signed and is fixed for the life of the loan. It is the spread that is applicable the day before signing. The Bank adjusts the fixed spread when market movements for basis swaps and/or changes in the projected US$ funding spread warrant such adjustments.

10

Term Details

Repayment terms

• Borrowers have the flexibility to tailor repayment terms to meet their program or project, asset, and liability management needs.

• They can select the grace period (time during which only the interest is paid), repayment period, and amortization structure as long as they are within these two limits: o Final maturity of loans is limited to 35 years, including the grace period. o Average repayment maturityb (ARM) cannot exceed 20 years.

• Repayment terms are fixed at loan negotiation. Once the loan is signed, the repayment schedule cannot be changed for the life of the loan.

Repayment schedules

• Borrowers can choose from these repayment schedules: o Fixed at commitment. Commitment-linked repayment schedules are fixed at the

outset when the loan is signed. Principal repayments are calculated as a share of the total loan amount disbursed and outstanding.

o Linked to disbursements. Disbursement-linked repayment schedules are tied to actual disbursements. Each semester’s group of disbursements is similar to a tranche or a subloan with its own repayment terms—that is, grace period, final maturity, and repayment pattern—which must be the same for all tranches within the loan. For repayment schedules linked to disbursements, the 20-year limit is the sum of the ARM and the expected average disbursement period.

Amortization patterns

• Amortization patterns may be level, annuity, bullet (one-time payment), or customized. • With level repayments, the principal is repaid in equal installments over time. • With annuity repayments, the principal is repaid with increasing installments over time

to keep the payments of principal and interest even across all periods. • Figure 3 illustrates the difference between level and annuity repayments for

commitment-linked loans.

Fees

• The front-end fee (FEF) is a one-time up-front fee currently set at 0.25% of the amount of the loan. At the option of the borrower, the FEF can be paid out of the financing or loan proceeds upon loan effectiveness or can be billed separately. The borrower must settle the FEF bill no later than 60 days after the effectiveness date, and the receipt is required before the first withdrawal from the loan.

• Commitment charges accrue on the loan’s undisbursed amount 60 days after signing of the loan and become due only after loan effectiveness. They are currently set at 0.25%.

• A single borrower limit (SBL) surcharge applies to specific exposure of large borrowers. In FY14 the Board approved increasing the SBL for a small number of large borrowers, with the provision that any exposure above the original limit would be subject to a surcharge of 50 basis points (bps).

Embedded options

• Borrowers have the following options to manage the currency and/or interest rate of their loan. These options are embedded in the loan agreement and can be executed at the borrower’s request. o Interest rate conversions o Interest rate caps and collars o Currency conversions

11

Term Details

Payment dates

Debt service payment dates are on the 1st or the 15th day of the month, usually on a semiannual basis. The payment date is decided by the borrower during the loan negotiation.

a. http://treasury.worldbank.org/bdm/htm/ibrd.html b. The ARM for commitment-linked schedules is equal to the aggregate of the principal repayment multiplied by time (in

years) between approval and repayment and divided by the total loan amount. For disbursement-linked schedules, it is the aggregate of the principal repayment multiplied by time (in years) between disbursement and repayment and divided by the total loan amount plus average disbursement period.

c. http://treasury.worldbank.org/bdm/htm/ibrd.html

Figure 3. Amortization patterns: Level payment loans schedule

Amortization patterns: Annuity payment loans schedule

12

2.1.2 IBRD Contingent Financing—Deferred Drawdown Option

14. The DDO is a contingent loan product that provides immediate liquidity in case of an adverse event, acts as a line of credit, and enables the borrower to defer the disbursement of funds until the financing is needed, up to a defined drawdown period after the financing agreement has been declared effective (table 3). The borrower must meet tranche release conditions before any disbursements being made.

15. IBRD offers two versions of the Deferred Drawdown Option (DDO): the Development Policy Financing DDO (DPF DDO) and the Catastrophe Deferred Drawdown Option (CAT DDO).

Table 3. Current Key Termsa and Conditions of DDOs

Terms DPF DDO CAT DDO

Purpose • Provides immediate liquidity when the borrower needs it

• Grants access to long-term IBRD resources to maintain ongoing structural programs

• Provides a formal basis for continued policy-based engagement with the Bank when the borrower has no need for immediate funding but values the Bank’s advice and access to immediate liquidity

• Develops and enhances the capacity of borrowers to manage hazard risk

• Provides immediate liquidity to fill the budget gap after a natural disaster while other sources—for example, concessional funding, bilateral aid, or reconstruction loans—are being mobilized after a natural disaster

• Safeguards ongoing development programs

Eligibility All IBRD-eligible borrowers who meet the preapproval criteria

Preapproval criteria

• Appropriate macroeconomic policy framework

• Satisfactory implementation of the overall program

• Appropriate macroeconomic policy framework

• Preparation or existence of a disaster risk management program

Currency Same as regular IBRD loans

Drawdown An amount up to the full loan amount is available for disbursement at any time within three years from signing the financing agreement. The drawdown period may be renewed for an additional three years.

An amount up to the full loan amount is available for disbursement at any time within three years of signing the financing agreement. The drawdown period may be renewed up to a maximum of four extensions for a total of 15 years.

Drawdown requirements

Funds are disbursed immediately upon request, unless the borrower has received prior notification from the Bank that one or more drawdown conditions are not met.

Funds are disbursed immediately upon occurrence of a natural disaster resulting in declaration of a state of emergency, unless the borrower has received prior notification from the Bank that one or more drawdown conditions are not met.

13

Terms DPF DDO CAT DDO

Repayment terms

May be determined either upon commitment or upon drawdown within prevailing maturity policy limits (the ARM and the final maturity are determined based on the drawdown date). The repayment schedule will start from the date of drawdown.

Lending rate Similar to regular IBRD loans, the lending rateb consists of a variable reference rate plus a spread.

Lending rate spread

Borrowers have the choice between a spread fixed for the maturity of the drawdown or a spread that is variable and reset semiannually. The spread is the prevailing spread for regular IBRD loans at the time of each drawdown, with the exception that the maturity premium component of the spread is based on the effective date of the loan and not on the drawdown date.

Fees • FEF: 0.25%b • Renewal fee: Nil • Standby fee: 0.50% per annum charged

on undisbursed balances, accruing from the date of effectiveness of the loan

• FEF: 0.50% • Renewal fee: 0.25%

Embedded options

Same as regular IBRD loans

Other features

Not applicable • Country limit: Maximum of 0.25% of GDP or the equivalent of US$500 million, whichever is less.

• Revolving features: Amounts repaid by the borrower will be available for drawdown, provided the closing date has not expired.

Note: ARM = adjustable rate mortgage; CAT DDO = Catastrophe Deferred Drawdown Option; DDO = Deferred Drawdown Option; FEF = front-end fee; GDP = gross domestic product; IBRD = International Bank for Reconstruction and Development. a. http://treasury.worldbank.org/bdm/htm/ibrd.html b. http://treasury.worldbank.org/bdm/htm/ibrd.html

2.1.3 Special Development Policy Financing (SDPFs)

16. SDPFs are offered to countries that are approaching crisis or are in a crisis with substantial structural and social dimensions and that have an urgent and extraordinary financing need. Their lending terms include a fixed spread over the index, with a grace period of 3 to 5 years and maturity of 5 to 10 years. They also include an FEF of 1.0 percent. Current rates10 can be found on the World Bank Treasury website.

10 http://treasury.worldbank.org/bdm/htm/ibrd.html

14

2.2 IDA Development Credits

17. IDA11 is the World Bank’s concessional lending window, extending funds to the poorest developing countries. It provides credits (the term used for its loans) at little or no interest, and repayments are stretched over 25 to 40 years, including a 5- to 10-year grace period.

18. A country’s IDA eligibility is determined at the beginning of each fiscal year (July) based on the country’s risk of debt distress, gross national income (GNI), and eligibility for borrowing from IBRD. Annex D of Operational Policy (OP) 3.1012 captures the financial terms for each country.

2.2.1 IDA Credits

19. IDA currently offers the following types of development credits:

• Regular credits. These credits are offered to countries with a GNI per capita less than the operational cutoff for IDA eligibility. For FY15, this would mean GNI less than US$1,215 per capita. These credits are on concessional terms.

• Blend-term credits. These credits are for countries that have a GNI per capita above the operational cutoff for more than two consecutive years, that is, GNI per capita greater than US$1,215 (for FY15).

• Hard-term credits. These credits are granted in addition to a country’s regular performance-based allocation and are available to countries eligible for blend terms.

• Transitional support credits. These are intended for countries, which have graduated from IDA but receive transitional support on an exception basis for the period FY15–FY17.

• IDA scale-up.13 The Bank recently introduced these IDA credits, which are offered to all IDA 17 eligible countries that are interested in accessing additional funds on nonconcessional terms.

2.2.2 IDA Lending Currencies

20. The majority of IDA development credits are denominated in special drawing rights (SDRs). Disbursements and debt service payments are calculated in SDRs. Debt service payments are made in the following currencies—U.S. dollar, pounds sterling, or euro—specified in the financing agreement in an amount equivalent to the SDRs required under the agreement. On a

11 http://www.worldbank.org/ida/what-is-ida.html 12http://web.worldbank.org/WBSITE/EXTERNAL/PROJECTS/EXTPOLICIES/EXTOPMANUAL/0,,contentMDK:22635084~

menuPK:64701637~pagePK:64709096~piPK:64709108~theSitePK:502184~isCURL:Y~isCURL:Y,00.html 13 http://treasury.worldbank.org/bdm/htm/documents/IDASUFCredit_Handout.pdf

15

pilot basis, IDA credits are being offered in the currencies of the SDR basket (US$, €, £stg, and ¥). The currency is selected at the time of negotiations.

2.2.3 IDA Current Charges and Rates14

21. The following charges currently apply to IDA credits on concessional terms: • Service charge. A charge of 0.75 percent is applied to disbursed amounts and is intended

to cover the administrative expenses of IDA. A service charge is applied to all types of IDA credits and is embedded in the floating rate for transitional support and hard-term credits.

• Commitment charge. All IDA credits are subject to a commitment charge, which is currently zero but can be as much as 0.5 percent. The Board of Executive Directors review the commitment charge for IDA on an annual basis to decide partial or complete waiver of the charge. The charge applies to undisbursed amounts and starts accruing 60 days after the financing agreement is signed. It becomes due once the credit becomes effective.

• Interest charge. An interest charge on disbursed amounts is applied to IDA blend-term, hard-term, and transitional support credits. The rate is updated quarterly and varies with the currency selected.

• All IDA credits denominated in SDRs are offered only with a fixed interest rate. • All IDA credits on blend terms are offered only with a fixed interest rate. • IDA single currency credits with hard terms or transitional terms can opt for either fixed

or floating rate. • Charges for fixed rate credits (blend-term, transitional support, and hard-term credits):

o For single currency credits with a fixed rate, a basis swap adjustment (BSA)—prevailing as of the date of credit approval and fixed for the life of the credit—is added to both service and interest charges. The BSA varies depending on the IDA credit type (small island, regular, blend-term, transitional support, hard-term); the charge (service, interest); and the currency (US$, €, £stg, and ¥). The BSAs are notified at the beginning of every quarter.15

o A floor of 75 bps is applied to service charge and a floor of 0 bps is applied to interest rates for all currencies.

• Charges for floating rate credits16 are applied only for single currency transitional support and hard-term credits): o Rate includes service charge; no separate service charge is due. o The floating rate for transitional support credits is

• Reference market rate (6 months) + IBRD fixed spread − 100 bps + transaction fee 1 bps p.a. + 75 bps IDA service charge.

14 http://www.worldbank.org/ida/lending-terms.html 15 http://www.worldbank.org/ida/lending-terms.html 16 http://ida.worldbank.org/financing/ida-lending-terms

16

o The floating rate for hard-term credits is • Reference market rate (6 months) + IBRD fixed spread − 200 bps +

transaction fee (1 bp) + 75 bps IDA service charge. o An interest rate floor of 0 bps is applied on interest rates.

22. The fixed rates and floating rate components for single currency credits are calculated and published quarterly. Credits approved in each quarter will be subject to the rates published at the beginning of that quarter. The new IDA lending terms are available from the website.17

2.2.4 IDA Repayment Terms

23. IDA repayment terms18 are decided every three years, at the time of the donor meetings. Currently, IDA regular credits have a 6-year grace period and a 38-year final maturity, with the exception of regular credits for small island economies. However, IDA blend-term, hard-term, and transitional support credits have a 5-year grace period with a 25-year final maturity. Repayments are done on a semiannual basis. IDA grants do not have to be repaid. See table 4 for IDA concessional terms.

Table 4. Current IDA Concessional Terms

Service charge

Commitment charge Interest Acceleration

clause Maturity Grace period (years)

Regular 38 6 Blend term 25 5 Hard term 25 5 Transitional support n.a. 25 5

Note: n.a. = not applicable. The maturity, grace period, and principal repayments listed above are for FY16. These terms are subject to change in the future. Current terms are available on the International Development Association (IDA) website, http://www.worldbank.org/ida/lending-terms.html

IDA regular credits for small island economies (which have less than 1.5 million people, significant vulnerability because of size and geography, and very limited creditworthiness and financing options) will continue to have a 10-year grace period and 40-year maturity.

2.2.5 Acceleration of Credit Repayments to IDA

24. IDA has included an accelerated repayments clause in financing agreements since 1987 and redefined it in 1996. The clause allows IDA to double the principal repayments of the credit, that is, shorten the maturity if the borrower’s GNI per capita exceeds a specified threshold and the borrower is IBRD creditworthy. Specifically under the clause, principal repayments would double, provided a 10-year grace period has elapsed (5 years under the new clause) and the

17 http://ida.worldbank.org/financing/ida-lending-terms. 18 http://www.worldbank.org/ida/lending-terms.html

17

GNI is above the historical cutoff for 5 years (above the operational cutoff for 3 years under the new clause).

25. The borrower has a choice to exercise the following options:

• Principal option. The borrower doubles the principal repayment of each installment until the principal amount of the credit is fully repaid.

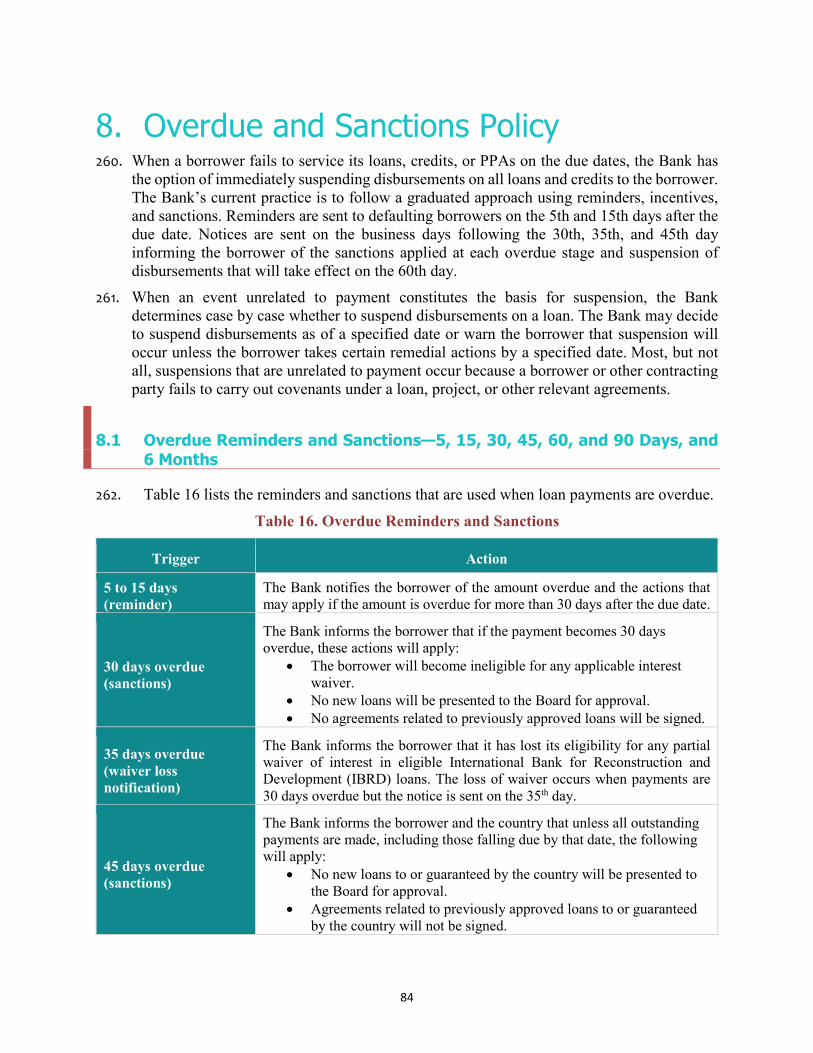

• Interest option. An interest charge is included in lieu of some or all of the increased principal repayments. This can be done only if the net present value of the repayment schedule, including interest, equals that of the principal option, provided both options have the same grant element.

• Combination. The borrower can combine the two options.

2.2.6 Policy Framework for Voluntary Prepayments

26. A voluntary prepayment option was introduced for countries that met the eligibility criteria for accelerated repayments but whose credits did not include the accelerated repayment clause because they were signed before 1987. To encourage these countries to voluntarily accelerate their repayments or to prepay their outstanding credits, a discount was offered under the framework for voluntary prepayments in cases where the country

• Elects to voluntarily prepay all outstanding credits in full; or • Provides a partial prepayment for IDA to apply to the latest maturities of credits, that

is, to use a bottom-up approach on the portfolio, as determined by IDA.

27. Discounts will not be available for prepayments of individual IDA credits specified by borrowers.

28. In addition to the financial benefits, borrowers, during voluntary prepayment, show their commitment to contribute to IDA by increasing resources available for current IDA recipients.

2.3 IDA Grants

29. IDA grants are offered to help low-income countries restore or maintain their external debt sustainability. According to the grant allocation framework, which was first introduced in IDA14, a country’s risk of debt distress is the criterion for grant eligibility.

30. IDA grants are not subject to repayment or charges (service charge and interest), but they carry a 20 percent volume discount on the country’s allocation. Commitment charges are applicable on IDA grants but are currently fully waived.

31. Grant eligibility under IDA is limited to IDA-only countries and based on the ratings of countries’ risk of debt distress. It excludes IBRD/IDA blend countries or hard-term countries, because these countries have greater access to capital markets, and their debt compositions can differ from IDA-only countries.

18

32. The risk ratings emerge from country-specific, forward-looking Debt Sustainability Analyses (DSA) based on the joint World Bank–International Monetary Fund (IMF) Debt Sustainability Framework for Low-Income Countries.19 The ratings reflect the share of IDA grants and highly concessional IDA credits for each country.

33. Recipients with a high risk of debt distress receive 100 percent of their financial assistance in the form of grants, and those with a medium risk of debt distress receive 50 percent in the form of grants. More information can be found on the IDA website.20

2.4 Guarantees

2.4.1 Key Features of Guarantees

34. Bank guarantees expand the financing options for investment projects through political risk mitigation and credit enhancement. They can be provided with or without an associated Bank loan or credit.

35. Through its guarantees, the Bank (a) mobilizes commercial capital for development projects; (b) increases its lending leverage, because guarantees enable the Bank to be a key financier with smaller financing commitment than lending would have required; (c) improves commercial borrowing terms to better meet the requirements of development projects; (d) enables private sector participation by facilitating risk sharing between private participants and the government, by covering defined payment and performance obligations of the government or public entities to a project or private financiers; (e) acts as “honest broker” in a transaction between the government and private participants; and (f) expands access to financial markets to governments and implementing entities.

36. The Bank provides guarantees to the extent necessary to mobilize commercial financing for the project and/or to mitigate government (and its entities) payment risks of the project, taking into account country, project, and market circumstances. Properly structured guarantees could function as an important instrument for mobilizing capital and managing risk for a project in all sectors.

2.4.2 Guarantee Instrument—Type and Eligibility

37. The World Bank offers the three types of guarantee support to all member countries as outlined in figure 4. These guarantees are described in detail on the guarantee program website.21

19 http://go.worldbank.org/A5VFXZCCW0 20 http://www.worldbank.org/ida/debt-sustainability.html 21 http://www.worldbank.org/en/programs/guarantees-program

19

Figure 4. World Bank Guarantee Products

2.4.3 Agreements for Guarantee Transactions

38. The various types of agreements associated with guarantees are described in table 5. The guarantee agreement and indemnity agreement are signed after the Bank Board’s approval of the guarantee project and when negotiations with third-party financiers are finalized.

Table 5. Agreements for Guarantee Transactions

Agreement Purpose and Details

Guarantee agreement

The guarantee agreement is usually executed by the Bank and the guaranteed lender or guaranteed payee, or an agent of those, and is the agreement under which the terms and conditions of the guarantee are specified. Depending on the structure of the guarantee transaction, the guarantee lawyer may decide that, instead of a separate self-standing guarantee agreement, it is appropriate for the terms and conditions of the Bank’s guarantee to be embedded in the same legal document that sets out the terms of the loan offered by the guaranteed lender/payee or in another appropriate legal document.

Indemnity agreement

The indemnity agreement is between the member country and the Bank, setting forth that the member country will reimburse the Bank in the event that a payment is made under the Bank guarantee, and against any other amounts (including expenses and liabilities) incurred by the Bank.

Project agreement

The project agreement is executed between an implementing entity and the Bank. It specifies, among other things, the undertakings made by such implementing entity to the Bank relating to the implementation of the project. Depending on the nature of the guarantee transaction, for example, in a public sector project, the guarantee lawyer may decide that instead of a self-standing project agreement, it is appropriate for the terms and conditions that would usually be in a project agreement to be embedded in another legal document. Or in another example, the Bank may enter into a project agreement with a relevant project participant, if appropriate. This type of agreement does not apply to policy-based guarantees.

20

Additional legal agreements

Depending on the specific details of a project, the guarantee lawyer may decide that it is appropriate for the Bank to be a party to other legal agreements. For example, the Bank may enter into a cooperation-related agreement with a financier of a separate part of the larger infrastructure project that is not directly involved in Bank project implementation but is crucial for the larger infrastructure project’s successful execution (and therefore also for the success of the Bank’s project). The guarantee lawyer may also decide whether the Bank should receive, for example, the benefit of unilateral legal opinions or letters of undertaking.

2.4.4 Fees and Pricing on Guarantees

39. The pricing of IBRD and IDA guarantees includes the fees or charges listed in the forthcoming policy that will replace OP 3.10.22 Fees and charges are determined based on the concept of loan equivalency with IBRD loans and IDA credits, respectively. These fees are generally paid by the implementing entity in the case of project-based guarantees, and by the government in the case of policy-based guarantees. Once the Bank guarantee fees are fixed, they remain unchanged for the life of the guarantee. The Bank charges standby fees (akin to commitment charges), a guarantee fee (akin to loan spread), and a front-end fee as applicable on IBRD and IDA projects. The IBRD and IDA guarantee pricing terms are accessible on the Bank Treasury website23 as well as the guarantee website.24

2.4.5 Guarantee Trigger Events and Disbursement Arrangements

40. The events triggering payments under the guarantee are specified in the guarantee agreement. All project-based Bank guarantees require an adequate dispute resolution framework so as to avoid entangling the Bank in the substance of any dispute between the parties, including any dispute between two governments.

41. Requests for payment under a guarantee (known as demands) can only be made in accordance with the guarantee agreement and relevant related contracts. Generally, payments are made after the government’s failure to pay has been finally determined, and if applicable, in accordance with such dispute resolution mechanisms. Payments under a project-based guarantee can be triggered even if there is an underlying dispute, in situations where the underlying contracts include a clear obligation by the government or by a state-owned entity to make a payment even if it disputes it.

22 Financial Terms and Conditions of IBRD Loans, IBRD Hedging Products, IBRD Guarantees, and IDA Credits and Guarantees. See http://web.worldbank.org/WBSITE/EXTERNAL/PROJECTS/EXTPOLICIES/EXTOPMANUAL/0,,contentMDK:22635084~menuPK:64701637~pagePK:64709096~piPK:64709108~theSitePK:502184~isCURL:Y~isCURL:Y,00.html 23 http://treasury.worldbank.org/bdm/htm/IBRD_and_IDA_GuaranteePricing.html 24 http://www.worldbank.org/en/programs/guarantees-program

21

2.5 Other Products Administered by the World Bank

42. The Bank administers loans and guarantees under trust funds. These include funds such as the Climate Investment Fund, billable trust funds (BTFs), and European Economic Commission (EEC) credits.

2.5.1 Clean Technology Fund—Grants, Loans, and Guarantees

43. The Clean Technology Fund (CTF) is one of the funding windows of the Climate Investment Fund (CIF). It provides resources to scale up the demonstration, deployment, and transfer of low carbon technologies with a significant potential for long-term greenhouse gas emissions savings. More information on CTFs can be found on the CIF website.25

44. CTF project preparation grants are used to develop quality investment projects by financing project feasibility studies and associated analytical and design tasks. Preparation grants may be used for CTF investment plans, where needed, and CTF cofinanced projects.

45. The CTF offers two loan products based on an analysis of the financial internal rate of return of each project without CTF cofinancing:

• Harder concessional loans for projects with rates of return near or above normal market threshold, but below risk premium for project type, technology, country, or acceleration in deploying low carbon technology, will have higher opportunity costs.

• Softer concessional loans are provided for projects with negative rates of return or below normal market threshold.

46. Table 6 shows the loan terms that are applied to CTF financing for the first year of operations.

Table 6. Current Loan Terms for CTF Financing

CTF loan Maturity Grace period

Principal repayments years 11–20

Principal repayments years 20–40

MDB feea

Service chargeb

Grant elementc

Harder concessional

20 10 10% n.a. 0.18% 0.75% ~45%

Softer concessional

40 10 2% 4% 0.18% 0.25% ~75%

Note: CTF = Clean Technology Fund; MDB = multilateral development bank; n.a. = not applicable.

a. The borrower will have two options for payment of MDB fees: (a) a fee of 0.18% of the undisbursed balance of the loan, in which case the fee payments will accrue semiannually after loan signing, or (b) a fee equivalent to 0.45% of the total loan amount, payable in a single lump-sum amount, which may be paid by the borrower out of its own resources or capitalized from the financing or loan proceeds following the effectiveness of the loan. The fees are to be retained by the MDB for its lending and implementation support costs.

b. The service charge is based on the disbursed and outstanding loan balance. Principal and service charge payments accrue semiannually to the CTF trust fund.

25 http://www-cif.climateinvestmentfunds.org/fund/clean-technology-fund

22

c. Grant element is calculated using the International Development Association methodology on the basis of these assumptions: 6.33% discount rate for harder loans; 6.43% discount rate for softer loans; semiannual repayments; eight-year disbursement period.

47. CTF resources may be deployed for two categories of guarantee products: • Loan guarantees cover the loss on account of debt service default for lenders up to an

agreed portion of the actual loss, with a view to extend maturities of commercial loans for low carbon projects, so that they are competitive with base case technologies, or to address specific incremental operating or construction risks that could cause default.

• Contingent finance is disbursed to the project upon underperformance of a low carbon technology and where such risk is not commercially insurable at reasonable costs or has occurred beyond the period for which commercial insurance is available.

48. The Strategic Climate Fund is another window established as part of the CIFs. Eligibility for loans under this window must be in accordance with the governance framework for the Strategic Climate Fund. More information is available on the Climate Investment Fund site.26

2.5.2 Billable Trust Funds (BTFs)

49. BTFs are lent to borrowers on IDA terms and are expected to be repaid by the borrowers. The sources of funds for the BTFs come from donor countries, the Bank’s net income, or special funds, or a combination. The Bank serves as the administrator for these funds.

50. BTFs are treated in line with any other IDA loan product as far as billing, accrual of charges, overdue payments, and repayments are concerned.

2.5.3 European Economic Commission Credits

51. The Bank administers loans made by the EEC to various borrowers. Upon receipt of debt service, principal amounts are returned to the donors while service charges are retained by the Bank as compensation for managing the disbursement and collection of loan funds used to co-finance Bank projects.

26 http://www-cif.climateinvestmentfunds.org/fund/strategic-climate-fund

23

2.5.4 Project Preparation Facility (PPF)

52. PPF advances are made by the Bank under a special authority granted by the Board of Executive Directors. The Board regularly determines the ceiling on the commitment authority of the facility and on the size of individual advances.

53. The Bank may make a Project Preparation Advance (PPA) from the PPF to a borrowing country to finance the following:

• Project preparation, design, and initial implementation activities

• Preparation of programs • Start-up emergency response activities in

cases of crises and emergencies

54. A PPA is made only when there is a strong probability that Bank financing will be approved for the operation under preparation. However, granting the PPA does not commit the Bank to finance any portion of the operation.

55. The PPA is made in US$ and carries interest on IBRD fixed spread terms or regular IDA credit terms. Borrowers that are eligible for grants receive PPAs only on grant terms.

56. PPAs can be made to prepare the Bank guarantee operations. In such cases, the advance would be disbursed according to IPF procedures, which are applicable to preparation advances. Such advances are repaid to the Bank in the same manner as when an advance that is granted to a borrower does not materialize into a project. No refinancing of the advance is possible in such cases; therefore, the advance should be repaid to the Bank, except for those on IDA grant terms.

57. If the financing account for which the PPA was made is unlikely to materialize by the refinancing date, the PPA may be refinanced out of the proceeds of any other financing made to or guaranteed by the country.

58. Interest or service charges are accrued on the PPA at the Bank’s interest or service charge rate. However, the payment of interest/charges on the advance is deferred until it is refinanced or terms of repayment are determined.

59. To refinance the PPA, the financing agreement of the follow-on operation will include a provision for the same. The withdrawal schedule of the follow-on financing will include an expenditure category to cover the principal amount of the advance plus estimated accrued interest or service charges, where applicable.

60. In cases where the PPA is not refinanced, the advance is repayable and the Bank informs the borrower that the amounts disbursed under the PPA and the accompanying charges will be billed shortly. The PPAs are repaid in 10 equal semiannual installments over a five-year period after the refinancing date. However, if the disbursed amount of the PPA is US$50,000 or less,

Project Preparation Advances • PPAs are usually refinanced by a

loan or repaid by the borrower. PPAs that do not get refinanced carry interest on IBRD fixed spread terms or IDA credit terms. PPAs to IDA–grant-only countries do not get repaid because they are converted under grants.

• Repayable PPAs are to be paid in 10 equal semiannual installments. However, if the amount of the PPA is less than US$ 50,000, it needs to be repaid within a period of 60 days from the date of the Bank’s notice.

• PPAs are made in U.S. dollars only.

24

the country is required to repay the full amount as a lump sum payment within a period of 60 days after the Bank’s repayment notice.

61. If the borrower is eligible to receive only IDA grants on the PPA approval date, the advance becomes a grant and is not repayable by the borrower.

62. For more information on disbursement-related aspects of PPAs, refer to section 4.1.5.

2.6 IBRD Risk Management Products

63. IBRD offers hedging products27 for risk management in one of the following ways:

• Embedded conversion options are built into the IBRD Flexible Loan (IFL). • Freestanding swaps are on a stand-alone basis to manage risk on the entire portfolio of

Bank loans. • A non-IBRD hedge is used on a stand-alone basis to manage debt owed to other

creditors.

64. Borrowers can access embedded conversion options by requesting the desired type and terms of the conversion. For IBRD loans without embedded conversion options or debt owed to creditors other than IBRD, borrowers can access swaps by signing a Master Derivatives Agreement (MDA) with IBRD.

2.6.1 IBRD Products with Embedded Conversion Options

65. IBRD embedded conversion options include interest rate conversions, currency conversions, automatic rate fixing, and interest rate caps and collars. The borrower can select the required options in the Loan Choice Worksheet28 at the time of loan negotiations, so that they can be incorporated into the financing agreement. To exercise these options, except for automatic conversion options, the borrower needs to submit the completed request forms to the Bank. More information on the conversion options and request forms to exercise the options are available on the Treasury website.29

66. Conversion options were earlier available only for loans on fixed spread terms. A borrower with a loan on variable spread terms wishing to exercise conversion options had to either (a) execute a MDA and then enter into a freestanding swap, or (b) execute a loan amendment and convert the loan to fixed spread terms.

67. The Bank allows access to conversion options for all IFLs on variable spread terms. Some of these options are also available to legacy single currency variable spread loans (VSLs), provided a loan amendment is executed. A loan amendment is required for IFLs on variable spread terms, where the borrower had not opted for the conversion options at the time of signing the agreement.

27 http://treasury.worldbank.org/ 28 http://treasury.worldbank.org/bdm/htm/Loan_Preparation_Support.html 29 http://treasury.worldbank.org/Services/RiskMgmtProducts.html

25

68. Under the current terms, a borrower can opt to convert the reference rate—that is, the LIBOR/EURIBOR or any other base rate—to a fixed rate for a part or the entire life of the loan without requiring conversion to fixed spread terms (table 7). The variable spread of the loan would be unaffected and would be subject to reset according to the original loan terms. For legacy single currency VSLs, automatic conversion options and the options to convert to local currency have not been provided.

Table 7. IBRD Conversion Products Available for IBRD Loans

Loan type Interest rate conversions

Caps and collars

Currency conversions

Automatic conversions

IFL (fixed and variable spread)

Fixed spread loan (FSL)

Variable spread loan (VSL)a n.a.

Note: FSLs and VSLs were discontinued on February 12, 2008; IBRD = International Bank for Reconstruction and Development.

* Subject to amendment of loan terms. Automatic conversion is not applicable (n.a.).

2.6.1.1 Transaction Fees for Conversion Options

69. The transaction fees for the applicable conversions can be found on the Treasury website.30

70. For early termination of a conversion—currency conversion, interest rate conversion, or interest rate cap and collar—the transaction fee prevailing at the time of early termination will apply. For example, an interest rate fixing that had no transaction fee will not bear a transaction fee for early termination. Transaction fees expressed as a percentage per annum will be converted to a lump sum.

2.6.2 IBRD Freestanding Swaps and Non-IBRD Hedges

71. IBRD’s stand-alone hedging products for risk management are available to help borrowers manage their financial risks. Using standard risk management techniques, these products can transform the risk characteristics of a borrower’s IBRD obligations without changing the terms negotiated in the financing agreements.

30 http://treasury.worldbank.org/bdm/htm/Loan_Conversion_Options.html

26

72. IBRD hedging products include interest rate swaps, interest rate caps and collars, currency swaps, and on a case-by-case basis, commodity swaps. To use hedging products, borrowers must enter into an MDA with IBRD. This agreement provides the contractual framework between the borrower and IBRD. The World Bank Treasury website31 shows the hedging products available to IBRD loans on disbursed and outstanding loan amounts.

73. IBRD also offers interest rate and currency swaps in relation to borrowers’ non-IBRD debt. Borrowers eligible to use these products are sovereigns that have an existing portfolio of IBRD loans, are in good standing with respect to debt service obligations to the Bank, and are eligible for new IBRD loans. For more details, refer to the Treasury website.32

74. Fees for interest rate caps or collars and commodity swaps are billed at the time of execution of the transaction and are payable within 60 days. For currency swaps and interest rate swaps, the transaction fee is added as a spread to the interest rate applicable for that loan or tranche. IBRD may revise the fee schedule from time to time. In such cases, the revised fees would apply only to hedge requests submitted after the new schedule is in effect. Current fee schedules for IBRD hedging products are available on the Treasury website.33

2.7 Debt Relief Initiatives

2.7.1 Debt Service Trust Funds

75. The Debt Service Trust Funds (DSTFs) are established for the settlement of debt service amounts due to IBRD and/or IDA. These funds are administered by the Bank in accordance with the letter of agreement and the trust fund agreement between the Bank and the beneficiary. The use of the fund is governed by the terms in the letter of agreement between the Bank, the donor, and the beneficiary.

76. The Bank processes all disbursements from DSTFs and applies the funds to debt service payments due to IBRD/IDA. DSTFs are also used in customized ad hoc payment mechanisms agreed between the donor and the beneficiary. Such instances include a buy-down arrangement between a donor and a beneficiary. In this arrangement, the donor makes funds available in a trust fund that is to be used for servicing specific debts of a recipient, subject to the recipient fulfilling certain prespecified conditions. Once the conditions are fulfilled, the Bank uses the funds available in the donor-funded trust fund to prepay the preidentified debts of the beneficiary. Additional information on other trust funds and programs is available on the Bank’s Development Finance web page.34

31 http://treasury.worldbank.org/bdm/htm/hedging_products.html 32 http://treasury.worldbank.org/bdm/htm/hedging_products.html 33 http://treasury.worldbank.org/bdm/htm/Hedging_Transaction_Fees.html 34 http://go.worldbank.org/GABMG2YEI0

27

2.7.2 Heavily Indebted Poor Countries (HIPC) Initiative

77. The HIPC Initiative was established in 1996 and enhanced in 1999 to reduce eligible countries’ debt burdens to the thresholds established under the initiative, subject to satisfactory policy performance. More information on the HIPC Initiative and eligible countries can be found on the World Bank’s HIPC Initiative web page.35

78. For countries that have reached the enhanced HIPC decision point and are eligible for debt relief through a debt relief schedule, such relief is reflected as a reduction of debt service payments due, through the regular billing process. The decision point is reached when the Board of Executive Directors approves the provision of debt relief under the HIPC Initiative.

79. Countries begin receiving interim relief on a provisional basis at the decision point. Once countries reach the completion point, the full amount of debt relief becomes irrevocable. The completion point is reached when conditions specified in the legal notification sent to a country are met and the country’s other creditors have confirmed their full participation in the HIPC Initiative.

2.7.3 Multilateral Debt Relief Initiative

80. The Multilateral Debt Relief Initiative (MDRI) was launched in 2005 to further reduce the debts of countries that have graduated from the enhanced HIPC Initiative and to provide them with additional resources to help them meet the Millennium Development Goals. More information on the MDRI can be found at the World Bank’s MDRI web page.36

81. Countries are eligible to receive debt relief under the MDRI on the first day of the fiscal quarter following the date that they reach the completion point under the enhanced HIPC Initiative. This date is referred to as the MDRI implementation date.

82. Under this initiative, the borrower is no longer required to (a) repay principal and (b) pay service charges, on or after the MDRI implementation date, on credit amounts that were disbursed and outstanding as of December 31, 2003. Such debt relief is provided for all

35 http://go.worldbank.org/V1JZAAB1N0 36 http://go.worldbank.org/WDZPNXK1Z0

Enhanced HIPC Debt Initiative • Provides partial debt relief on eligible

credits • Normally delivers debt relief through

a reduction on the bill, starting after the country reaches the decision point

Multilateral Debt Relief Initiative (MDRI)

• Provides full debt relief on eligible credits

• Starts on first day of the fiscal quarter following the date when the completion point is reached

28

principal repayments and credit charges payable to IDA, after any debt service relief available under the enhanced HIPC Initiative. However, all other obligations for such credits of the borrower under the development financing agreements remain in full force and effect until such time as they would have terminated, had the IDA credit amounts been fully repaid, in accordance with the terms of the agreements and applicable General Conditions37 and Standard Conditions.38

83. Where credits were partially disbursed by December 31, 2003, a new credit tranche is created to include only those amounts eligible for MDRI debt relief. For those credits, the repayment amounts are allocated proportionately to the MDRI and non-MDRI credit tranches. In addition, any enhanced HIPC relief based on debt outstanding after December 31, 2003, will also be allocated proportionately.

84. Once debt relief has been provided under the MDRI and credit balances have been effectively canceled, any charges relating to those credits that arose before the implementation date and that were not eligible for debt relief under the MDRI will be billed to the borrower. At the same time, any credit balances that were carried forward from a period before the implementation date, as well as any payments made by the borrower with respect to amounts subject to debt relief, will be refunded. The net amount due from or to the borrower will be determined at the country level, and a final settlement letter that includes this information will be sent to the borrower.

37 http://siteresources.worldbank.org/BRAZILINPOREXTN/Resources/3817166-1242680408578/General_Conditions.pdf 38 http://go.worldbank.org/LXIOJ9CTI0

29

Blank Page

30

Volume 2

Disbursements

31

Contents 3. WITHDRAWAL OF FINANCING PROCEEDS .................................................................................................... 34

3.1 ELECTRONIC SUBMISSION OF WITHDRAWAL APPLICATIONS THROUGH CLIENT CONNECTION ............................................ 34 3.1.1 Client Connection ................................................................................................................................. 34 3.1.2 Organization Registration and User Account Access ........................................................................... 36 3.1.3 Authorized Signatories ......................................................................................................................... 36 3.1.4 Secure Identification Device Credentials and e-Signatories ................................................................. 36 3.1.5 Electronic Withdrawal Application Creation ........................................................................................ 37 3.1.6 Electronic Signing of Withdrawal Applications .................................................................................... 38 3.1.7 References ............................................................................................................................................ 38

3.2 MANUAL SUBMISSION OF WITHDRAWAL APPLICATIONS ........................................................................................... 38 3.3 CLARIFICATIONS ON WITHDRAWAL APPLICATIONS BEFORE BANK APPROVAL ................................................................ 39 3.4 CURRENCY OF PAYMENTS ................................................................................................................................... 40

4. INVESTMENT PROJECT FINANCING............................................................................................................... 41

4.1 DISBURSEMENT ARRANGEMENTS ......................................................................................................................... 41 4.1.1 Eligible Expenditures ............................................................................................................................ 41 4.1.2 Expenditure Categories ........................................................................................................................ 42 4.1.3 Disbursement Percentage .................................................................................................................... 42 4.1.4 Retroactive Financing .......................................................................................................................... 42 4.1.5 Project Preparation Advances (PPAs) .................................................................................................. 43 4.1.6 Disbursement Conditions ..................................................................................................................... 43

4.2 DISBURSEMENT METHODS ................................................................................................................................. 44 4.2.1 Reimbursement Method ...................................................................................................................... 45 4.2.2 Advance Method .................................................................................................................................. 45 4.2.3 Direct Payment Method ....................................................................................................................... 50 4.2.4 Special Commitment Method .............................................................................................................. 51

4.3 OTHER DISBURSEMENT MECHANISMS .................................................................................................................. 54 4.3.1 United Nations Commitments .............................................................................................................. 54 4.3.2 Co-Financing ........................................................................................................................................ 55 4.3.3 Results-Based Financing or Disbursement-Linked Indicators ............................................................... 55 4.3.4 Output-Based Disbursements .............................................................................................................. 56 4.3.5 Community-Driven Development Projects ........................................................................................... 57 4.3.6 Disbursement Arrangements for Subloans .......................................................................................... 58

4.4 MANAGING PROJECT RESTRUCTURING .................................................................................................................. 59 4.4.1 Amendments to Financing Agreement ................................................................................................ 59 4.4.2 Reallocation among Expenditure Categories ....................................................................................... 59 4.4.3 Expenditure Category Overdraw .......................................................................................................... 60 4.4.4 Changes to Disbursement Arrangements ............................................................................................ 60

4.5 INELIGIBLE EXPENDITURES .................................................................................................................................. 60 4.5.1 Recovering Ineligible Expenditures ...................................................................................................... 61

32

4.6 REFUNDS ........................................................................................................................................................ 61 4.7 NONCOMPLIANCE WITH AUDIT COVENANTS........................................................................................................... 62 4.8 LOAN CLOSING ................................................................................................................................................. 63

4.8.1 Closing Date Management .................................................................................................................. 63 4.8.2 Disbursement Deadline Date ............................................................................................................... 63 4.8.3 Contract Management during Loan Closing ........................................................................................ 63 4.8.4 Designated Account Management during Closure .............................................................................. 64 4.8.5 Payment of Final Audit Fees after Closing ........................................................................................... 65

4.9 CANCELLATION ................................................................................................................................................. 66 4.10 SUSPENSION OF DISBURSEMENTS ......................................................................................................................... 67

5. PROGRAM-FOR-RESULTS FINANCING ........................................................................................................... 68

5.1 OVERVIEW ...................................................................................................................................................... 68 5.1.1 Disbursement-Linked Indicators........................................................................................................... 68

5.2 DISBURSEMENT ARRANGEMENTS ......................................................................................................................... 69 5.2.1 Prior Results ......................................................................................................................................... 69 5.2.2 Advances .............................................................................................................................................. 69