loan participations and purchased loans: structuring...

TRANSCRIPT

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Presenting a live 90-minute webinar with interactive Q&A

Loan Participations and Purchased Loans:

Structuring Participation Agreements,

Lender Due Diligence Strategies for Lead Lenders and Participants to Minimize and Manage Risk of Participations and Sales

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, MARCH 31, 2016

Anthony R.G. Nolan, Partner, K&L Gates, New York

Mike Dorsett, President, Portfolio Performance, Blacklick, Ohio

Grant Puleo, Partner, Duane Morris, San Diego

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-755-4350 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can

address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 35.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Loan Participations and Purchased Loans:

Overview of Loan Participations

March 31, 2016

Mike Dorsett, President

Portfolio Performance LLC

www.portfolioperformancellc.com

Market Trends oLoan portfolios

oAvailability

oPricing

oServicing

oBroker premiums

What is a “participating interest”?

6

Loan Participation Potential

If financial institutions could efficiently participate loans,

they could maximize the industry’s lending capacity,

support small FI’s, and increase the industry’s market

share.

7

Participations Key to Small CU Success

Large credit unions are having better

luck riding the lending wave than

smaller credit unions, some of which

have seen their loan portfolios

contract.

“Small credit unions are naturally

impacted by economy of scale issues.

As such, forming strategic alliances

with other credit unions and CUSOs

and doing loan participations are

ways they can overcome some of

their size limitations.”

“Concentration risk is an important

consideration, as is managed growth

for products that are complex or new

to a credit union”

8

CUs & Loan Participations

• 23% = Percent of all CUs engaging in Participation

Lending at FYEnd 2013

<

$41M

>

$41M Loan

Participation

s

• $41 million = Median

Asset Size of CUs

reporting activity.

9

• Selling FI’s:

• Originate vs. deny large loans

• Premiums and servicing income

• Retain and maintain borrower relationship

• Share credit risk with other lenders

• Purchasing FI’s:

• Grow # and size of loans

• Generate interest income

• Diversify loan portfolio

Benefits of Participating

10

Types of Loans

Auto

Credit Card Portfolio

Member Business

Residential Real Estate

11

• Single loan funded by multiple lenders…

• Several FI’s fund one very large loan OR

• Two FI’s share a small/moderate size loan

• Loan Participation Agreement outlines structure

• Lead Lender:

• Originates and services the loan

• Recruits other FI’s to share risks and profits

• Organizes, sells, and manages the participation

• Deals directly with the borrower

12

Mike Dorsett, President National Registry of CPE Sponsors Number: 136103

Office: 614.868.5800; Mobile: 614.570.2312

Email: [email protected]

Web site: www.portfolioperformancellc.com

Call for Consultation Package Details

Loan Participations

Organic Loan Growth

13 13

www.duanemorris.com

©2014 Duane Morris LLP. All Rights Reserved. Duane Morris is a registered service mark of Duane Morris LLP.

Duane Morris – Firm and Affiliate Offices | New York | London | Singapore | Philadelphia | Chicago | Washington, D.C. | San Francisco | Silicon Valley | San Diego | Boston | Houston | Los Angeles | Hanoi | Ho Chi Minh City |

Atlanta | Baltimore | Wilmington | Miami | Boca Raton | Pittsburgh | Newark | Las Vegas | Cherry Hill | Lake Tahoe | Myanmar | Oman | Mexico City | Duane Morris LLP – A Delaware limited liability partnership

Loan Participations and Purchased Loans:

Structuring Participation Agreements LIVE Webcast

Presented by

Grant Puleo, Esq.

DM2\6634997.1

www.duanemorris.com

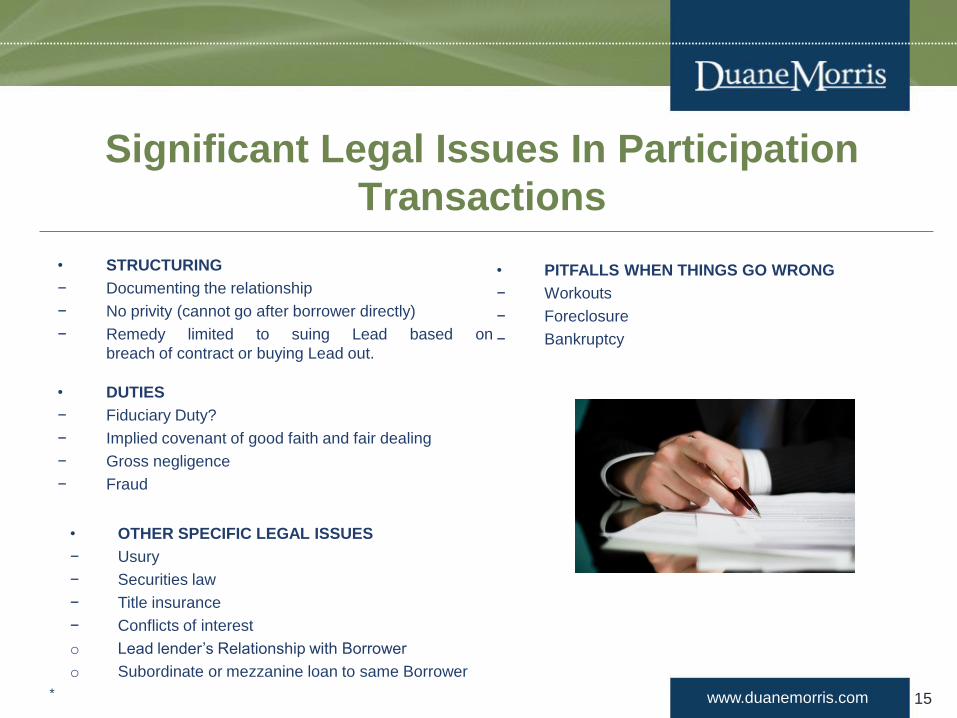

Significant Legal Issues In Participation

Transactions

• STRUCTURING

− Documenting the relationship

− No privity (cannot go after borrower directly)

− Remedy limited to suing Lead based on

breach of contract or buying Lead out.

• DUTIES

− Fiduciary Duty?

− Implied covenant of good faith and fair dealing

− Gross negligence

− Fraud

*

• OTHER SPECIFIC LEGAL ISSUES

− Usury

− Securities law

− Title insurance

− Conflicts of interest

o Lead lender’s Relationship with Borrower

o Subordinate or mezzanine loan to same Borrower

• PITFALLS WHEN THINGS GO WRONG

− Workouts

− Foreclosure

− Bankruptcy

15

www.duanemorris.com

Benefits of Loan Participations

• FOR LEAD LENDER

o Diversifying risk

o Leveraging income

o Reducing capital weight/lending limits

o Building client relationships

o Collecting fees for arranging and

administering loan

o Not recorded as liability on balance sheet

o Control

*

• FOR PARTICIPANTS

o Access to deal flow

o Access to lead lender’s capabilities

o Stay within credit limits

o Confidentiality (identity of participants not

known to Borrower)

o No consent of Borrower required

o Lower administrative costs

o Lower due diligence and loan closing costs

• FOR BORROWER

o Borrower only has to deal with Lead

16

www.duanemorris.com

Structures for Real Estate Loans

*

• Club Format

• Assignment and Assumption

• Indirect Participation

• Co-lending

• Syndication

17

www.duanemorris.com

Documenting

*

• No privity of contract

• Duties, obligations and liabilities must be governed by “Four Corners of the Participation

Agreement”

• Often overlooked terms

− Allocation of decision-making

− Allocation of fees

− Remedies for Lead negligence of failure to act (including removal)

− Limitation on liabilities of Lead

− Consent to other loans held by Lead with same Borrower

− Reimbursement of Lead for expenses

18

www.duanemorris.com

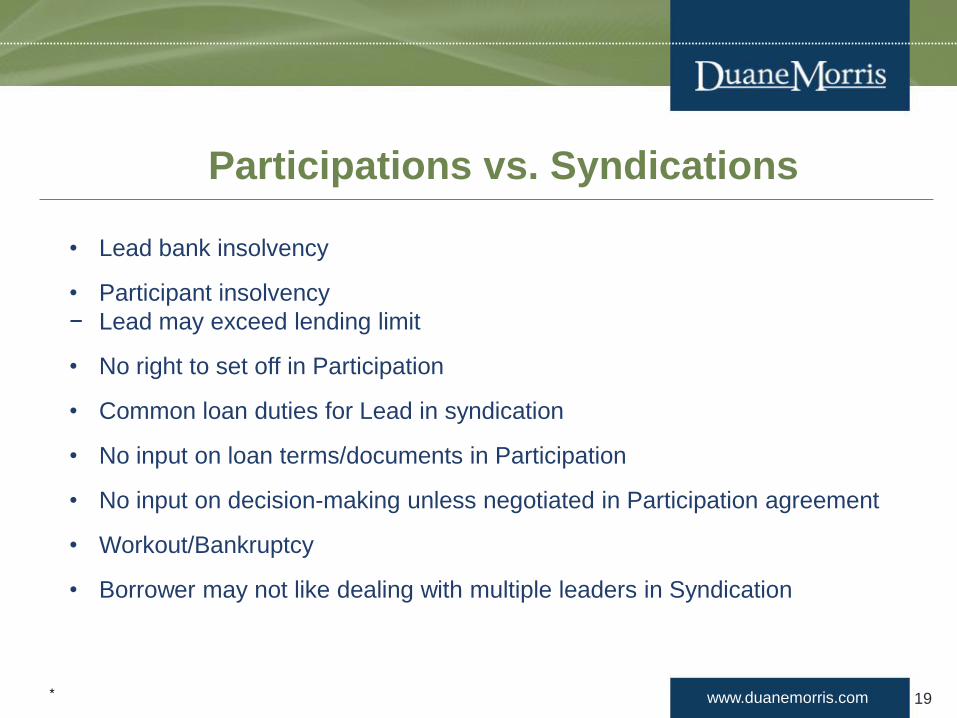

Participations vs. Syndications

*

• Lead bank insolvency

• Participant insolvency

− Lead may exceed lending limit

• No right to set off in Participation

• Common loan duties for Lead in syndication

• No input on loan terms/documents in Participation

• No input on decision-making unless negotiated in Participation agreement

• Workout/Bankruptcy

• Borrower may not like dealing with multiple leaders in Syndication

19

www.duanemorris.com

Decision-making, Information Rights

and Notice Provisions

• Decision-making

• What decisions require participants approval?

• Duties of Lead

− Administer, service and enforce

− Account for payments

− Provide loan documents

− Report

− Repurchase

• Lead retains exclusive rights and maximum amount of freedom on day-to-day, subject to “the list”

− Extension of maturity

− Reducing principal

− Reducing interest rate

− Release of guarantors

− Release of collateral

− Other (Changes in reporting, DSCR, capitalization, corporate structure, increase advances, foreclosure)

• Information/Notice

− Lead Lender v. Participants

* 20

www.duanemorris.com

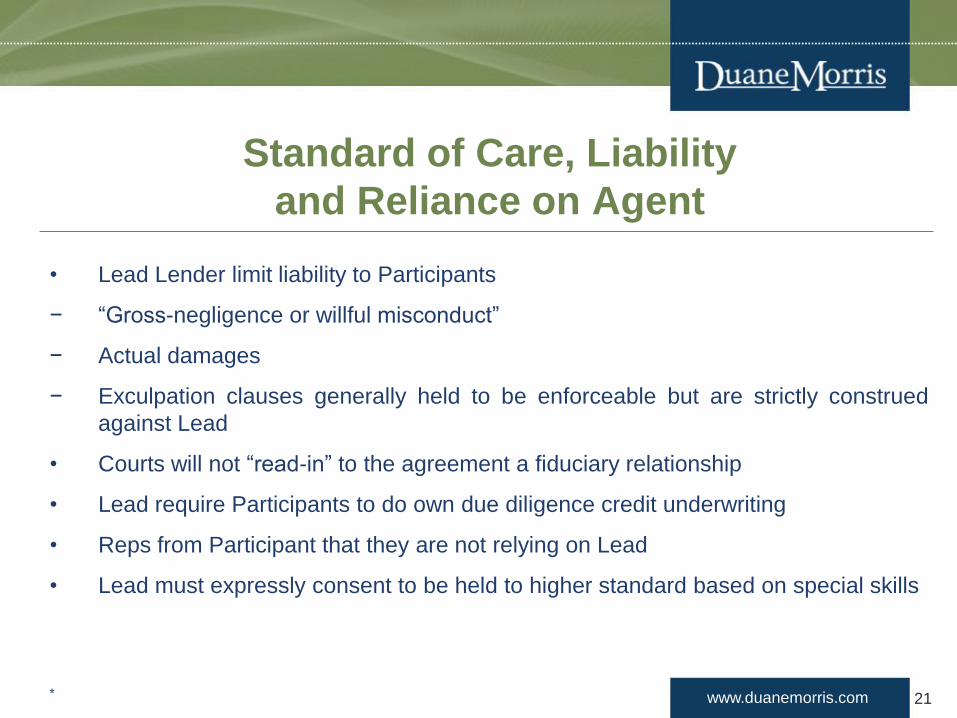

Standard of Care, Liability

and Reliance on Agent

• Lead Lender limit liability to Participants

− “Gross-negligence or willful misconduct”

− Actual damages

− Exculpation clauses generally held to be enforceable but are strictly construed

against Lead

• Courts will not “read-in” to the agreement a fiduciary relationship

• Lead require Participants to do own due diligence credit underwriting

• Reps from Participant that they are not relying on Lead

• Lead must expressly consent to be held to higher standard based on special skills

* 21

www.duanemorris.com

Rights and Duties of Participants

• RIGHTS

− To receive accounting

− Assume duties of Lead if Lead is unable to do so

− Consent rights

− To enforce repurchase (if one has been negotiated)

*

• DUTIES

− Advance its pro rata share of loan

− Subsequent advances

− Pay share of fees, costs and expenses

22

www.duanemorris.com

Borrower Workouts, Bankruptcy &

Foreclosures

• Typical participation agreements lack detail

− Plan your divorce on your wedding day

− Transaction-specific issues hard to address in advance

− Basic ground rules regarding decision-making for decisions that commonly arise (including a system for

resolving differences)

− Otherwise Lead decides appropriate cause of action

• Bankruptcy

− Courts hold Participants not entitled to “creditor” status

− Lead has sole right to legal recourse

− Participants not creditors of Borrower

* 23

www.duanemorris.com

Bankruptcy of Lead

*

• Bankruptcy/Insolvency of Lead

− Unsettled Law

− General/probably unsecured creditor or entitled to preferred status? If

Loan to Lead (possession of note, recorded assignment, UCC-1 filed). If

not, unsecured general creditor of Lead

− Structure as syndication

− Loan to Lead

− Lead acts as trustee

− Endorse note to Participants

• Fixes

− Ipso facto clause

− Personal service contract and not

transferable

24

www.duanemorris.com

Seller Reps and Warranties

*

• Typically Limited

− Accuracy of loan documents

− Payments made to date

− No outstanding default

• Typically Lead will require rep from Participants

that they have done own credit analysis

regarding Borrower, effectiveness of loan

documents, adequacy of collateral, priority and

perfection of security interest.

25

www.duanemorris.com *

• Construction loans / additional advances

• Lead can make advance and subordinate Participants

• Loss of voting rights

Defaulting Lender

26

© Copyright 2016 by K&L Gates LLP. All rights reserved.

Anthony R.G. Nolan, K&L Gates LLP

Loan Participations and Purchased Loans:

Specific Considerations

March 31, 2016

TOPICS COVERED IN THIS SECTION

Settlement and liquidity issues in loan assignments

True sale considerations in loan participations

klgates.com 28

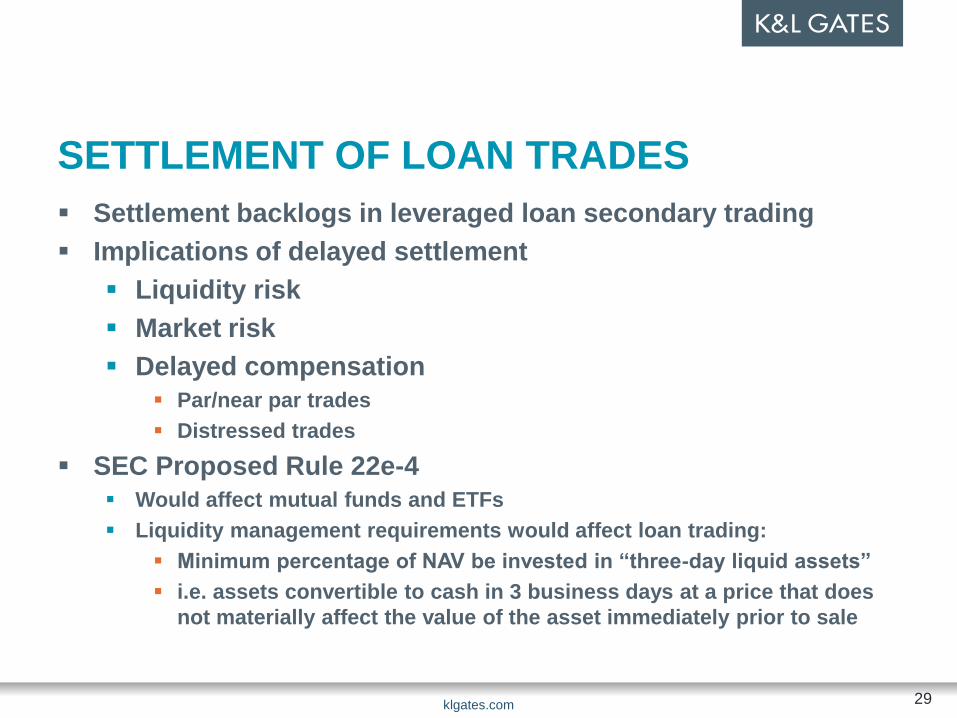

SETTLEMENT OF LOAN TRADES

Settlement backlogs in leveraged loan secondary trading

Implications of delayed settlement

Liquidity risk

Market risk

Delayed compensation

Par/near par trades

Distressed trades

SEC Proposed Rule 22e-4

Would affect mutual funds and ETFs

Liquidity management requirements would affect loan trading:

Minimum percentage of NAV be invested in “three-day liquid assets”

i.e. assets convertible to cash in 3 business days at a price that does

not materially affect the value of the asset immediately prior to sale

klgates.com 29

SETTLEMENT OF LOAN TRADES

Mitigants to delayed settlement:

Liquidity facilities

T+3 settlement facilities

LSTA proposed changes to delayed compensation

Buy-in / Sell-out mechanism

Use of participations

Participations

Fall-back for assignments

Primary transfer settlement option

Unique characteristics of participation affect risk:

Seller remains lender of record and services the loan

Buyer faces both underlying obligor and participation seller

klgates.com 30

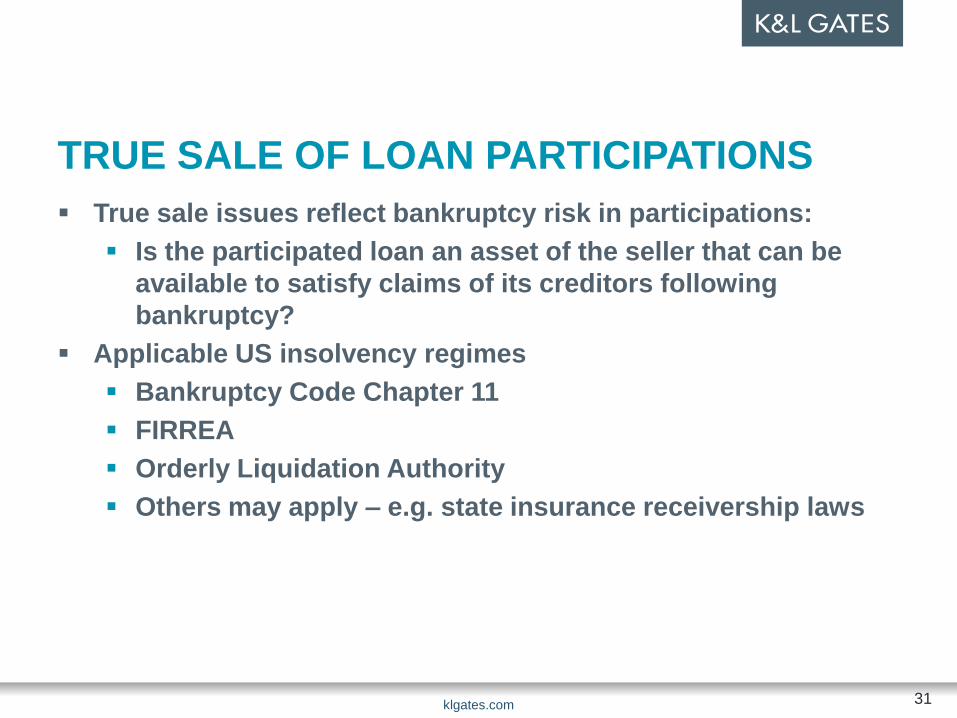

TRUE SALE OF LOAN PARTICIPATIONS

True sale issues reflect bankruptcy risk in participations:

Is the participated loan an asset of the seller that can be

available to satisfy claims of its creditors following

bankruptcy?

Applicable US insolvency regimes

Bankruptcy Code Chapter 11

FIRREA

Orderly Liquidation Authority

Others may apply – e.g. state insurance receivership laws

klgates.com 31

TRUE SALE OF LOAN PARTICIPATIONS

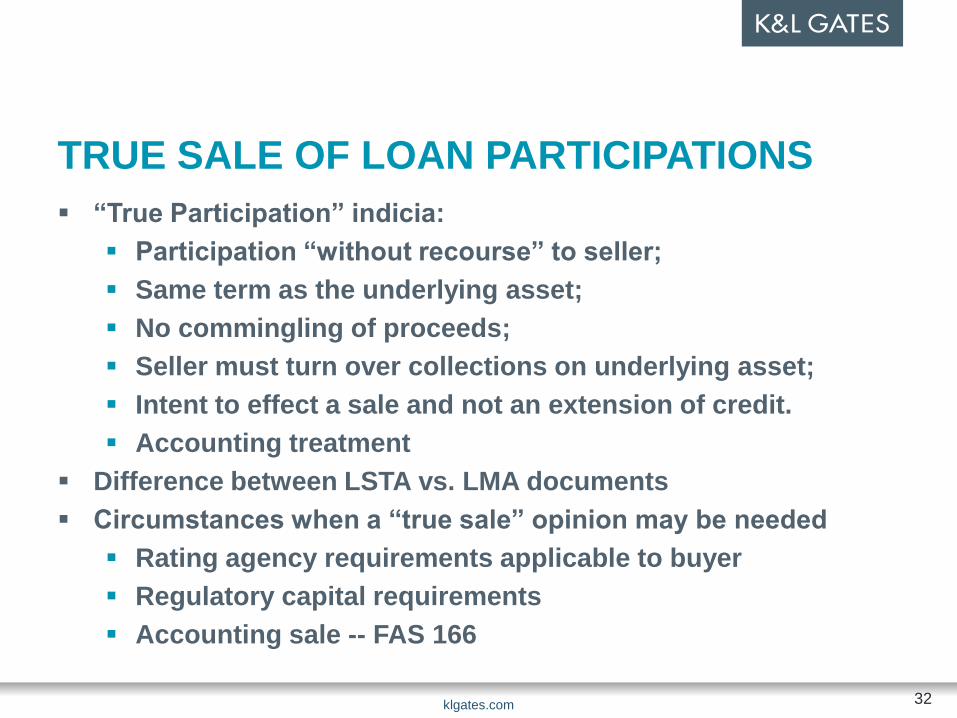

“True Participation” indicia:

Participation “without recourse” to seller;

Same term as the underlying asset;

No commingling of proceeds;

Seller must turn over collections on underlying asset;

Intent to effect a sale and not an extension of credit.

Accounting treatment

Difference between LSTA vs. LMA documents

Circumstances when a “true sale” opinion may be needed

Rating agency requirements applicable to buyer

Regulatory capital requirements

Accounting sale -- FAS 166

klgates.com 32

TRUE SALE OF LOAN PARTICIPATIONS

Alternatives to true sale for obtaining proceeds of participated

loan from insolvent seller under US law:

Bankruptcy Code section 741: “Securities contract”

Bankruptcy Code section 541(b)(1):

Loan participant considered beneficial owner of

grantor’s rights in the underlying loan

Characterization is supported by automatic perfection of

“payment intangibles” under UCC section 9-309

klgates.com 33

Loan Participations and Purchased Loans:

Lender Due Diligence

March 31, 2016

Mike Dorsett, President

Portfolio Performance LLC

www.portfolioperformancellc.com

Advisory on Effective Risk Management Practices for

Purchased Loans and Purchased Loan Participations

FDIC FIL-49-2015

• Some FI’s are relying on lead or originating institutions and third parties to perform risk

management functions when purchasing loans and loan participations, including out-of-

territory loans, loans to industries or loan types unfamiliar to the buyer, unsecured loans,

or loans underwritten using proprietary models.

• Buyers should underwrite and administer loan and loan participation purchases as if the

loans were originated by the purchasing institution. This includes understanding the loan

type, the obligor's market and industry, and the credit models relied on to make credit

decisions.

• Before purchasing a loan or participation or entering into a third-party arrangement to

purchase or participate in loans, financial institutions should:

• - ensure that loan policies address such purchases

• - understand the terms and limitations of agreements

• - perform appropriate due diligence

• - obtain necessary board or committee approvals

35

Board Policy Components

• Underwriting standards for participated loans

• Limits on the aggregate amount purchased

from any single originating lender

of any loan type

loans to any single borrower or group of associated

borrowers

• Risk Assessment and Strategic Planning

• Risk Measurement, Monitoring and Control

• Due Diligence

36

Master Agreement

• A written agreement governing all loan

participations

• Approved by the board of directors, a

delegated committee, or a member of senior

management

• Each loan participated must be referenced

37

Master Agreement

• Identifies originator’s risk retention

• Identifies location and custodian of original loan

documents

• Provides access to borrower financials and

loan performance to enable monitoring

38

Master Agreement

Provide clear description of originating

lender, servicer, and participant obligations

regarding:

• Servicing

• Defaults

• Foreclosure

• Collections

• Other matters regarding the administration

of the loan

39

Due Diligence Levels

1. Vendor Experts • Consultants, Investment Advisors, CUSOs, Brokers

2. Participation Partner • Seller/Buyer

3. Loan Portfolio (buyer only) • Detailed Review of loan offering

40

Questions for Vendor Experts Do you have access to the full loan file and seller before

purchasing?

Do you know the risk retention of seller throughout the life of the loan?

Do you have a valid master participation agreement in place with seller?

41

Questions for Vendors

Do you have continued and easy access to loan file

updates, payment history, voting and other abilities to

monitor loan?

Can you control who has access to your loans

(competitive reasons and otherwise)?

42

Buyer Participation Process

• Policy development

• Board approval

• Risk tolerance assessment

• Seller due diligence

• Pool characteristics and loan economics

• Loan examination

• Master Agreement Execution

• Monitoring

43

Due Diligence – Buyer/Seller

Collect and Review… • Call Reports and audited financials

• Management assessment

• Loan / Underwriting Policies and Practices

• Repossession Policies and Procedures

• Loan Modification and Nonaccrual Policy

• Charge-off Policy

• Collateral Insurance Policy

• Sample Reporting Package

• More…

44

Data Analysis • Weighted averages:

• Interest Rate

• Term

• Credit Score

• LTV, DTI, model year…

• Concentration limits:

• Underwriter

• Dealership

• Make of Car

• New vs. Used

45

Internal Financial Analysis

Amount of Loan: $ 4,429,760.00

WAM: 61

Buy Rate: 4.40%

Contract Rate: 4.40%

% Of Dealer Reserve Retained by CU: 0.00%

Fee: 3.00%

Processing Fee: $ -

To estimate prepayments using CPR, input CPR estimate here. Otherwise, set CPR to

0% and manually input any prepayments in column G.

CPR = 10.0%

OUTPUT

FIELDS:

Payment: $ 81,175.23

Dealer Reserve: $ -

Fee: 132,892.80

Processing Fee: -

Total Cost: $ 4,562,652.80

TOTAL RETURN:

Total Return: 3.01%

Average Life: 2.26

Portfolio CPR: 15.0%

46

Underwriting

The loan participation policy must establish prudent

underwriting standards for loan participations.

• Establishes appropriate due diligence.

oCan be done in-house or through a qualified third party that is not

affiliated with the loan.

oMay NOT rely on originating lender’s due diligence.

• Examiners will evaluate:

o The FI’s parameters for review.

oHow often the parameters are analyzed.

oHow well the originator adheres to its own policies.

47

Participation Lending Cautions

• Not a fix for dying FI’s.

• Fix your organic growth problem.

• Hard to stop once you start.

• Don’t RELY on participations.

• Don’t get complacent.

• Monitor like you would your

own originations.

48

Finding Participation Opportunities Talk with…

• Other FI’s in your network

• Consultants

• Investment Advisors

• CUSO’s

• Brokers

Buyers look for FI’s with…

• High Loan/Share Ratios

• Low Delinquency and Charge Offs

• Strong Capital Ratio

• Eligible Loan Activity – see Call Report

49

Finding Participation Opportunities

Sellers look for FI’s with:

• Low Loan/Share Ratio

• Low Delinquency and Charge Offs

• Strong Capital Ratio

• Eligible Loan Activity – see Call Report

50

Mike Dorsett, President National Registry of CPE Sponsors Number: 136103

Office: 614.868.5800; Mobile: 614.570.2312

Email: [email protected]

Web site: www.portfolioperformancellc.com

Call for Consultation Package Details

Loan Participations

Organic Loan Growth

51