loan portfolio analysis agribusiness finance lese 306 fall 2009

Post on 22-Dec-2015

219 views

TRANSCRIPT

Loan Portfolio Loan Portfolio AnalysisAnalysis

Agribusiness FinanceAgribusiness FinanceLESE 306 Fall 2009LESE 306 Fall 2009

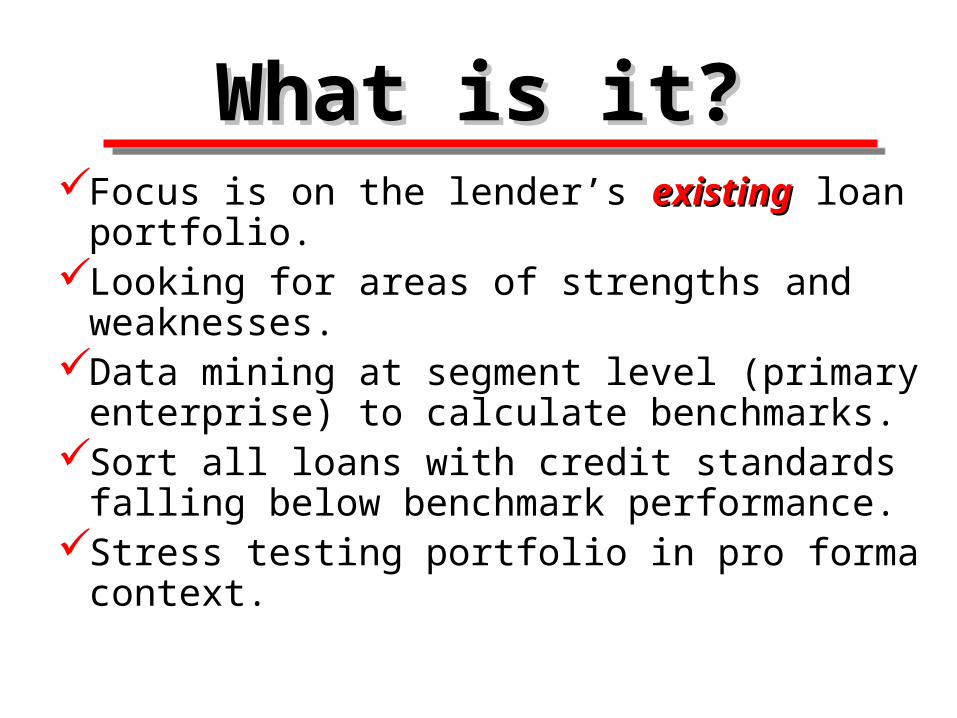

What is it?What is it?Focus is on the lender’s existingexisting loan

portfolio.Looking for areas of strengths and

weaknesses.Data mining at segment level (primary

enterprise) to calculate benchmarks.Sort all loans with credit standards falling

below benchmark performance.Stress testing portfolio in pro forma context.

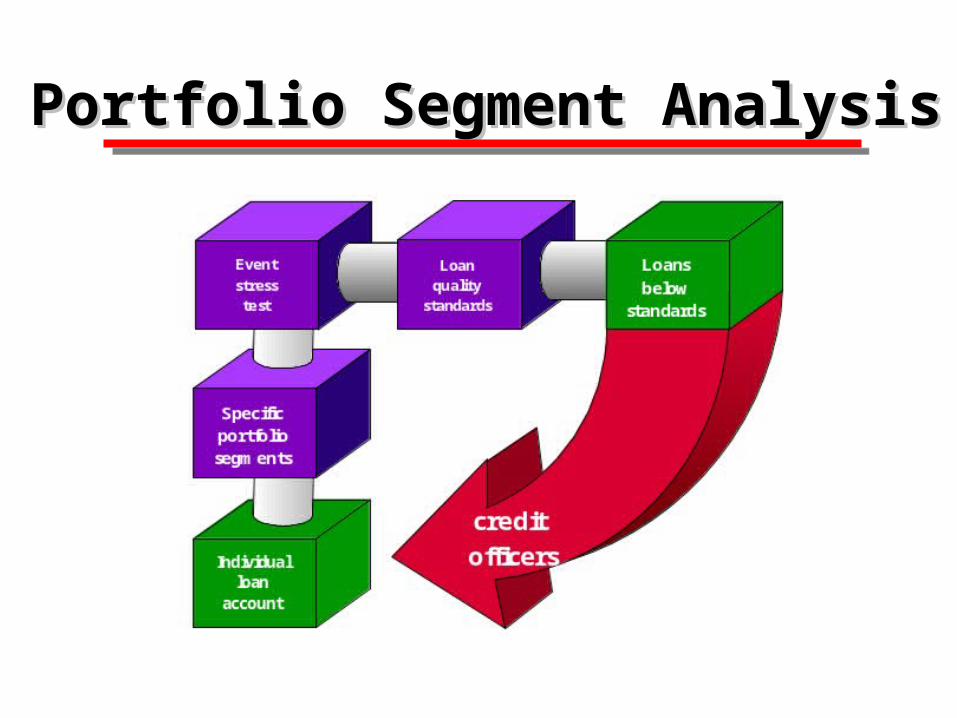

Portfolio Segment AnalysisPortfolio Segment Analysis

Externalities Affecting Externalities Affecting Portfolio Performance….Portfolio Performance….

Macroeconomic policy Farm program policy Trade policy Weather and disease Ability to pay in client nations Competitor nation actions

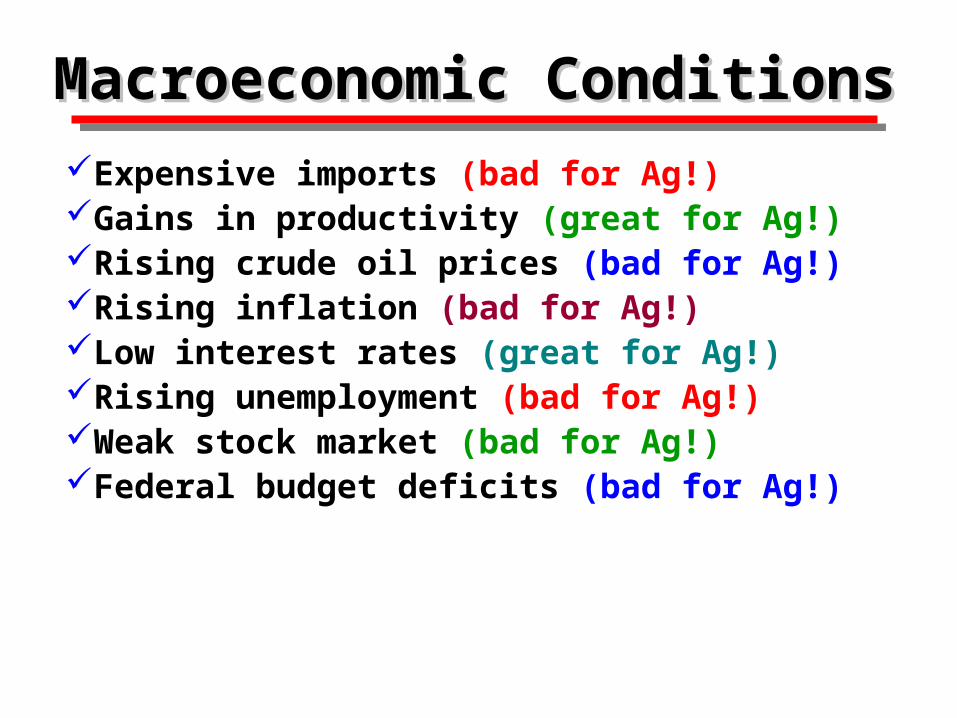

Macroeconomic ConditionsMacroeconomic Conditions

Expensive imports (bad for Ag!)Gains in productivity (great for Ag!)Rising crude oil prices (bad for Ag!)Rising inflation (bad for Ag!)Low interest rates (great for Ag!)Rising unemployment (bad for Ag!)Weak stock market (bad for Ag!)Federal budget deficits (bad for Ag!)

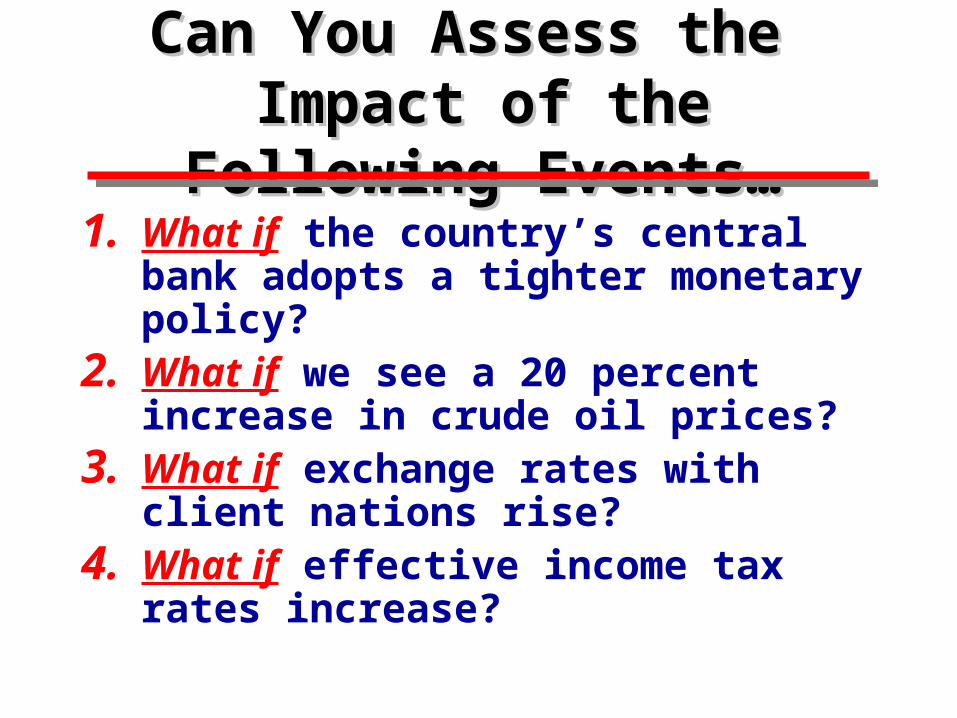

Can You Assess the Impact Can You Assess the Impact of the Following Events…of the Following Events…

1. What if the country’s central bank adopts a tighter monetary policy?

2. What if we see a 20 percent increase in crude oil prices?

3. What if exchange rates with client nations rise?

4. What if effective income tax rates increase?

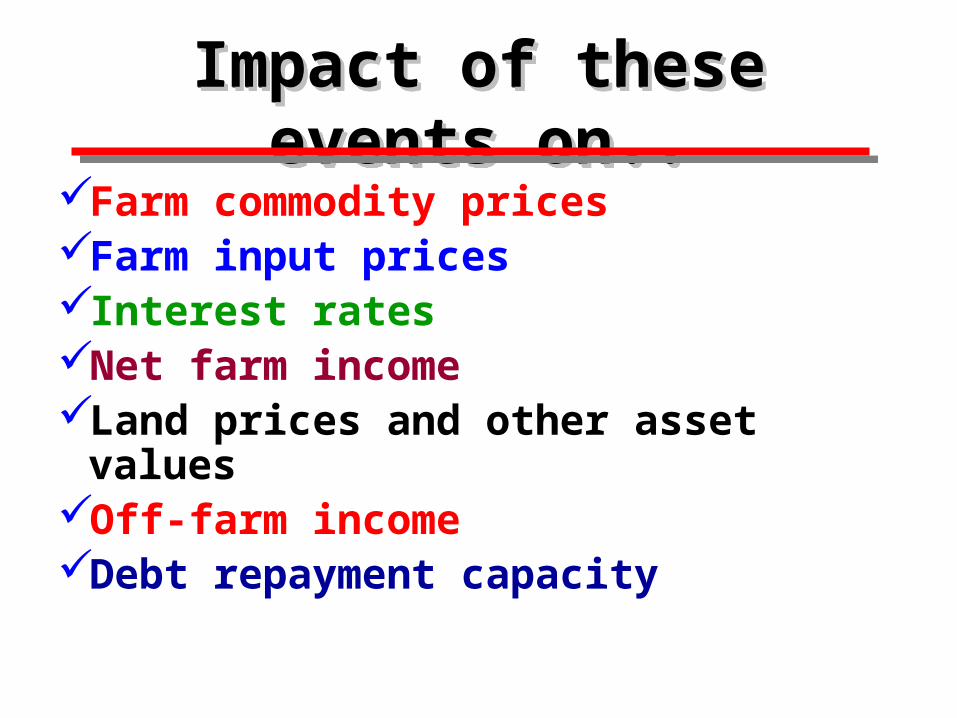

Impact of these events on..Impact of these events on..Impact of these events on..Impact of these events on..

Farm commodity prices Farm input pricesInterest ratesNet farm incomeLand prices and other asset valuesOff-farm incomeDebt repayment capacity

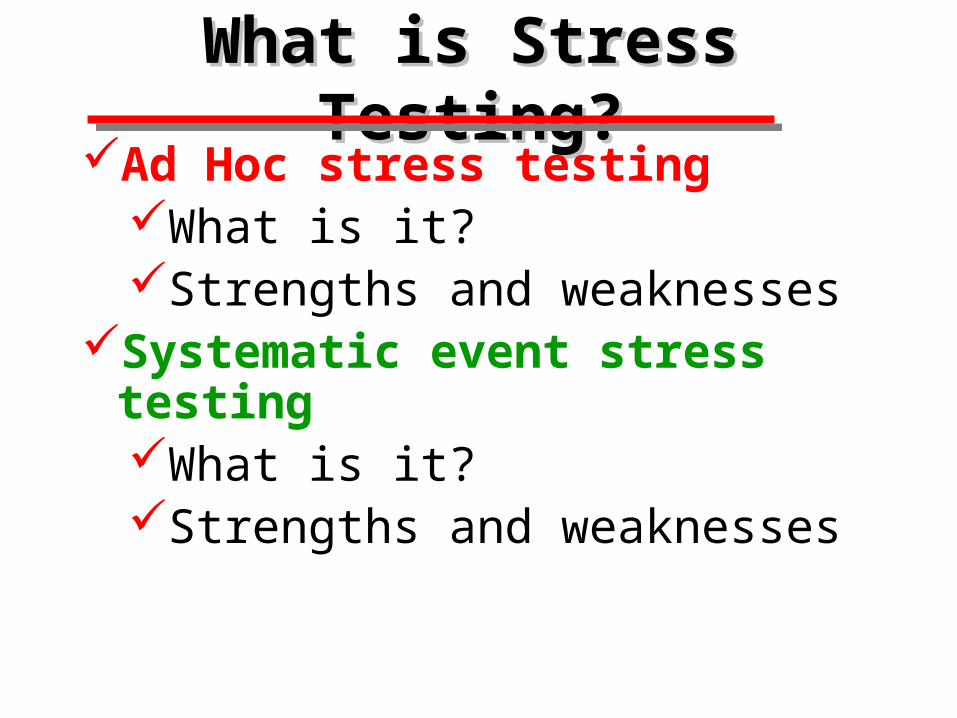

What is Stress Testing?What is Stress Testing?Ad Hoc stress testing

What is it?Strengths and weaknesses

Systematic event stress testingWhat is it?Strengths and weaknesses

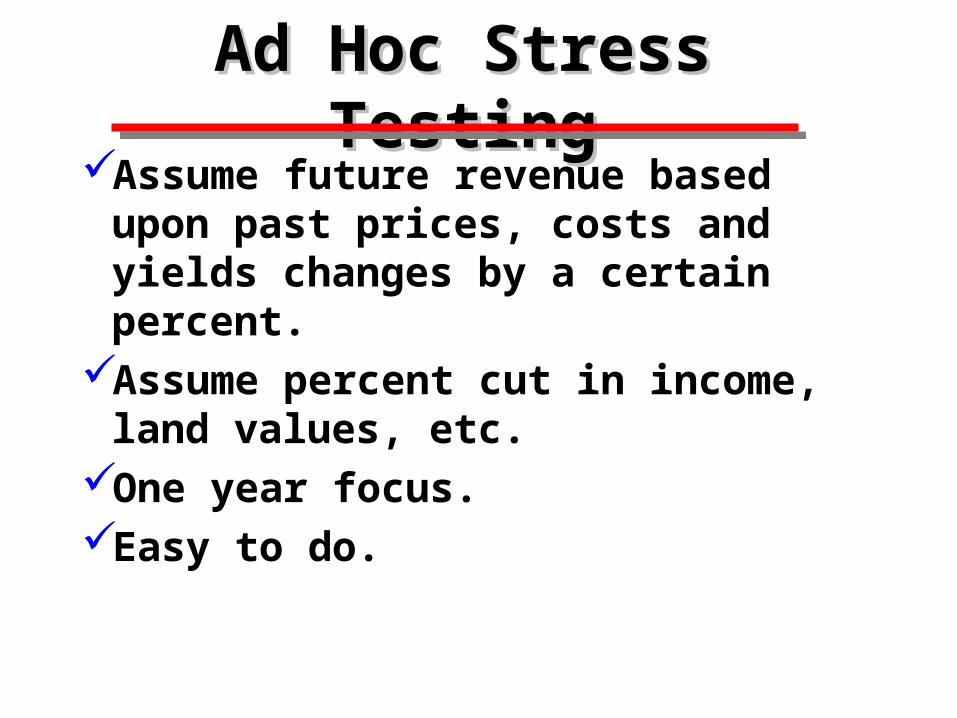

Ad Hoc Stress TestingAd Hoc Stress TestingAssume future revenue based

upon past prices, costs and yields changes by a certain percent.

Assume percent cut in income, land values, etc.

One year focus.Easy to do.

Event Stress Testing?Event Stress Testing?Pro forma analysis.Impact of future events:

Farm policy Macroeconomic policy Events in client

nations Competitor nation

actionsLooking down the road.Looking down the road.

What are the differences?What are the differences?Ad Hoc Stress TestingAssume a change

commodity pricesAssume a change in

input pricesAssume a change in

land valuesAssume a change in

wages and salaries

Ad Hoc Stress Testing

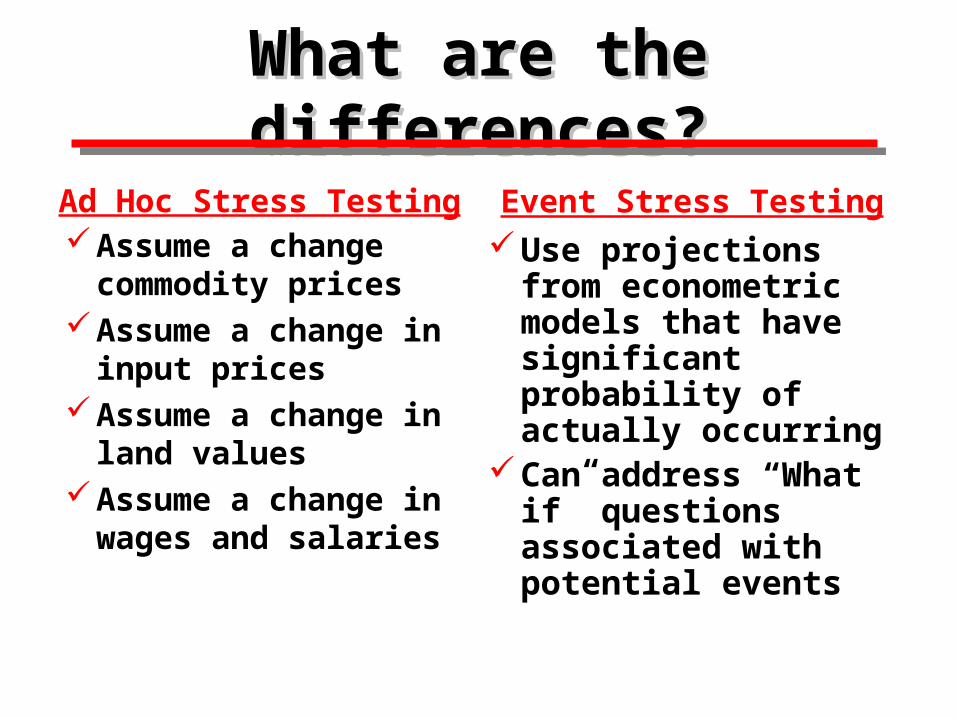

What are the differences?What are the differences?Ad Hoc Stress TestingAssume a change

commodity pricesAssume a change in

input pricesAssume a change in

land valuesAssume a change in

wages and salaries

Event Stress TestingUse projections from

econometric models that have significant probability of actually occurring

Can address “What if” questions associated with potential events

Ad Hoc Stress Testing Event Stress Testing

Why Event Stress Testing?Why Event Stress Testing?

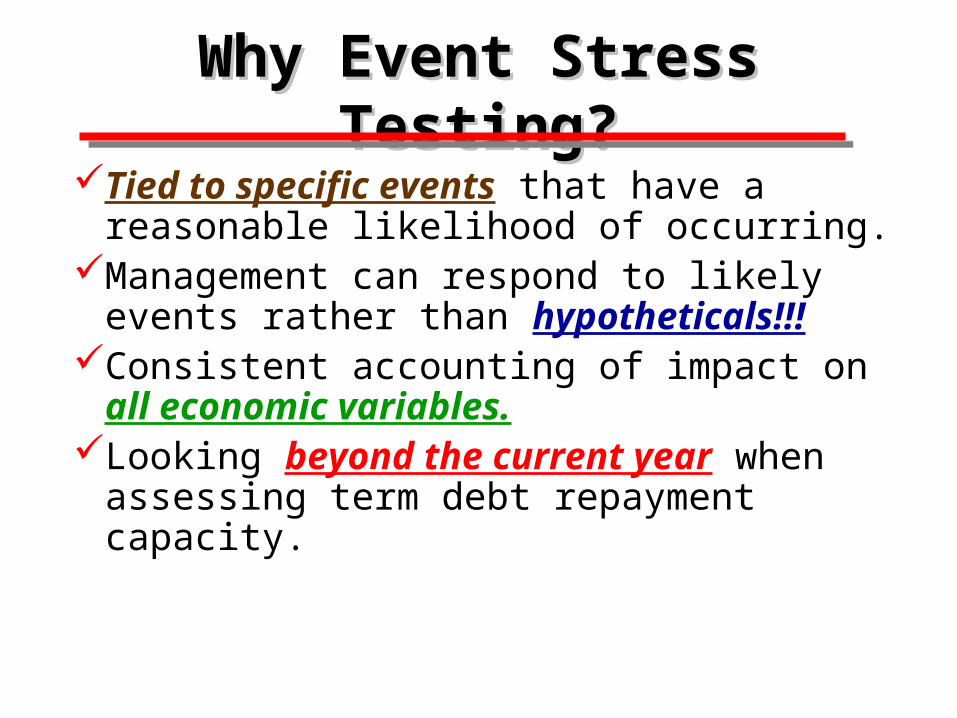

Tied to specific events that have a reasonable likelihood of occurring.

Management can respond to likely events rather than hypotheticals!!!

Consistent accounting of impact on all economic variables.

Looking beyond the current year when assessing term debt repayment capacity.

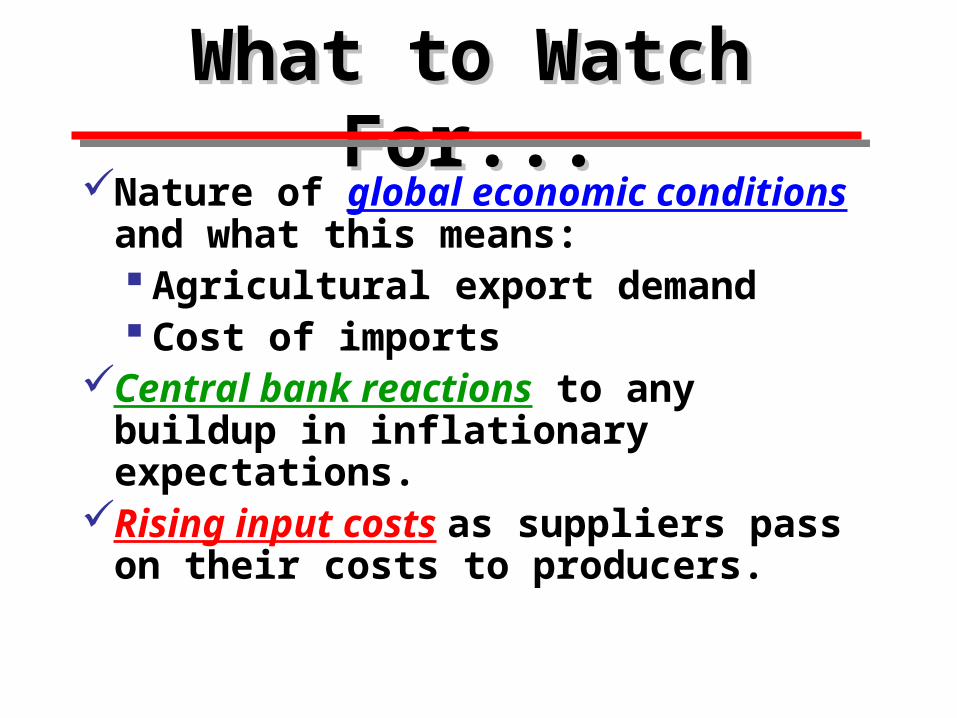

What to Watch For...What to Watch For...Nature of global economic

conditions and what this means: Agricultural export demand Cost of imports

Central bank reactions to any buildup in inflationary expectations.

Rising input costs as suppliers pass on their costs to producers.

A Portfolio A Portfolio Analysis ModelAnalysis Model

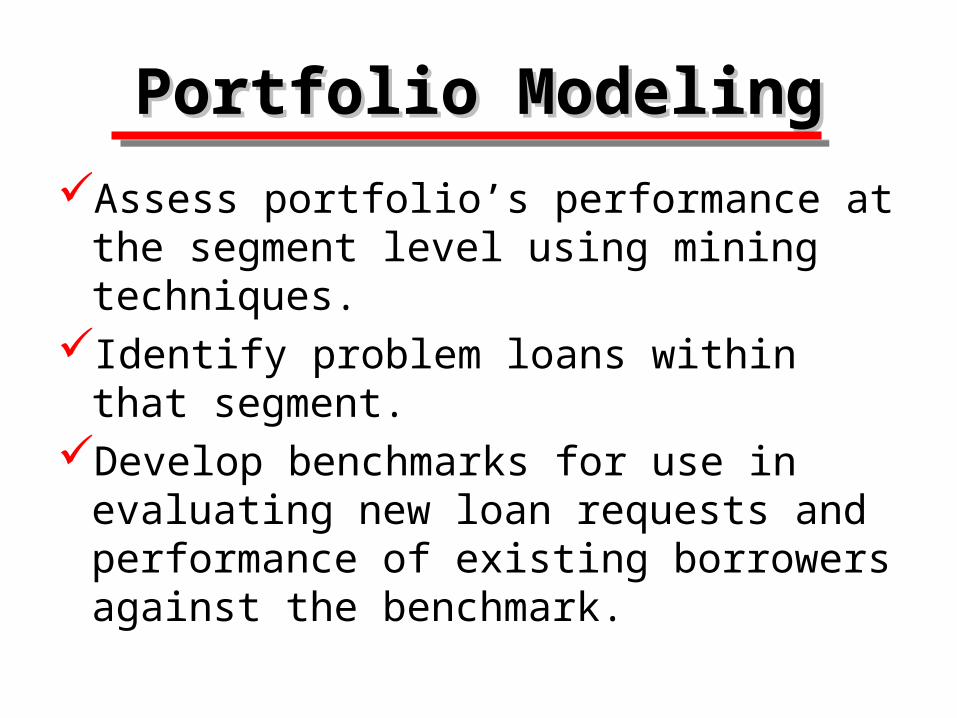

Portfolio ModelingPortfolio Modeling

Assess portfolio’s performance at the segment level using mining techniques.

Identify problem loans within that segment.

Develop benchmarks for use in evaluating new loan requests and performance of existing borrowers against the benchmark.

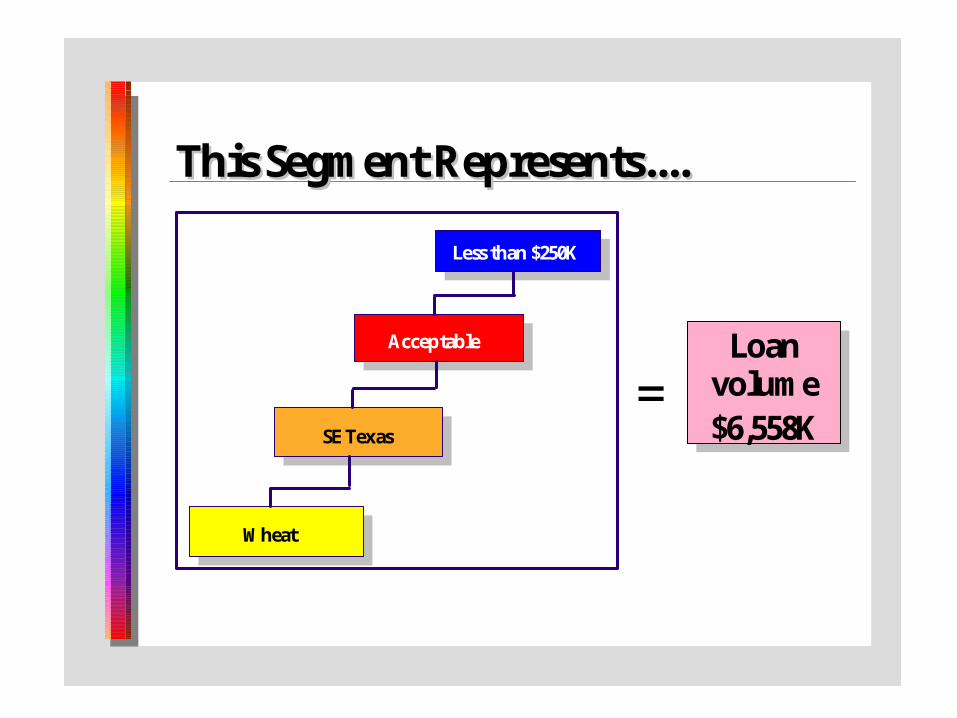

Wheat

SE Texas

Acceptable

Less than $250K

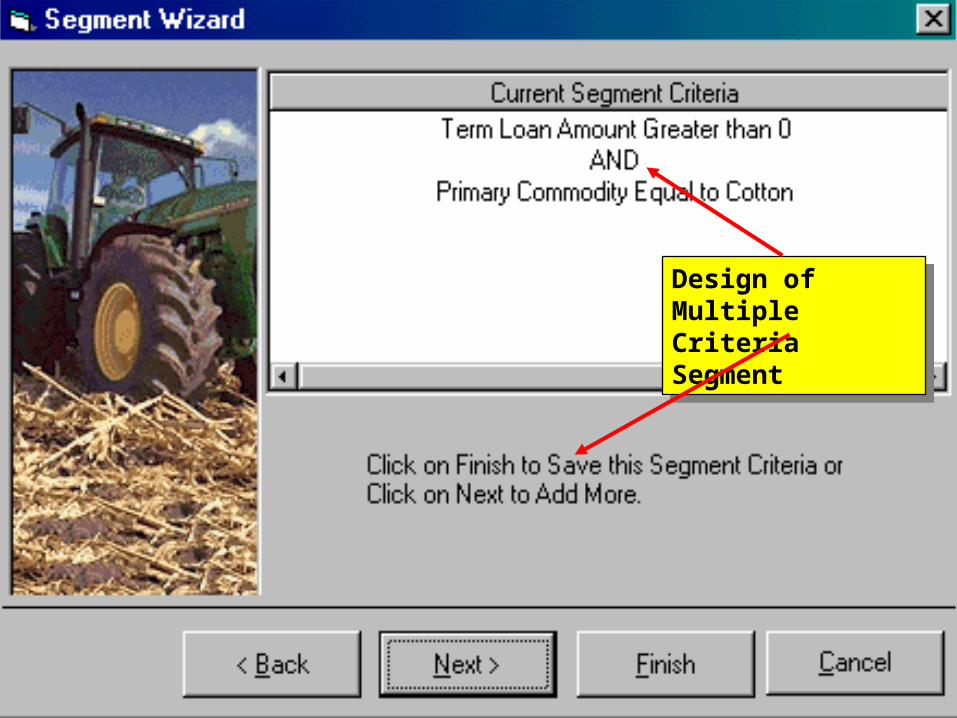

Segment Design...Segment Design...

Primary Commodity

Location

Loan Classification

Size

Wheat

SE Texas

Acceptable

Less than $250K

This Segment Represents....This Segment Represents....

Loan volume$6,558K

=

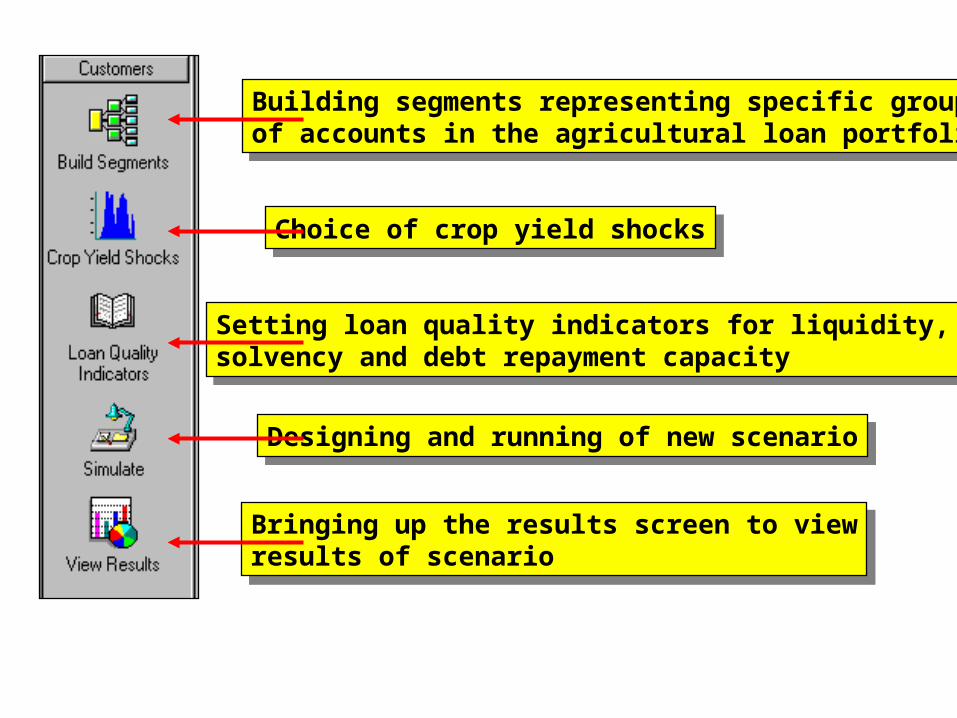

Building segments representing specific groupsof accounts in the agricultural loan portfolio

Building segments representing specific groupsof accounts in the agricultural loan portfolio

Choice of crop yield shocksChoice of crop yield shocks

Setting loan quality indicators for liquidity,solvency and debt repayment capacity

Setting loan quality indicators for liquidity,solvency and debt repayment capacity

Designing and running of new scenarioDesigning and running of new scenario

Bringing up the results screen to viewresults of scenario

Bringing up the results screen to viewresults of scenario

Design of MultipleCriteria Segment

Design of MultipleCriteria Segment

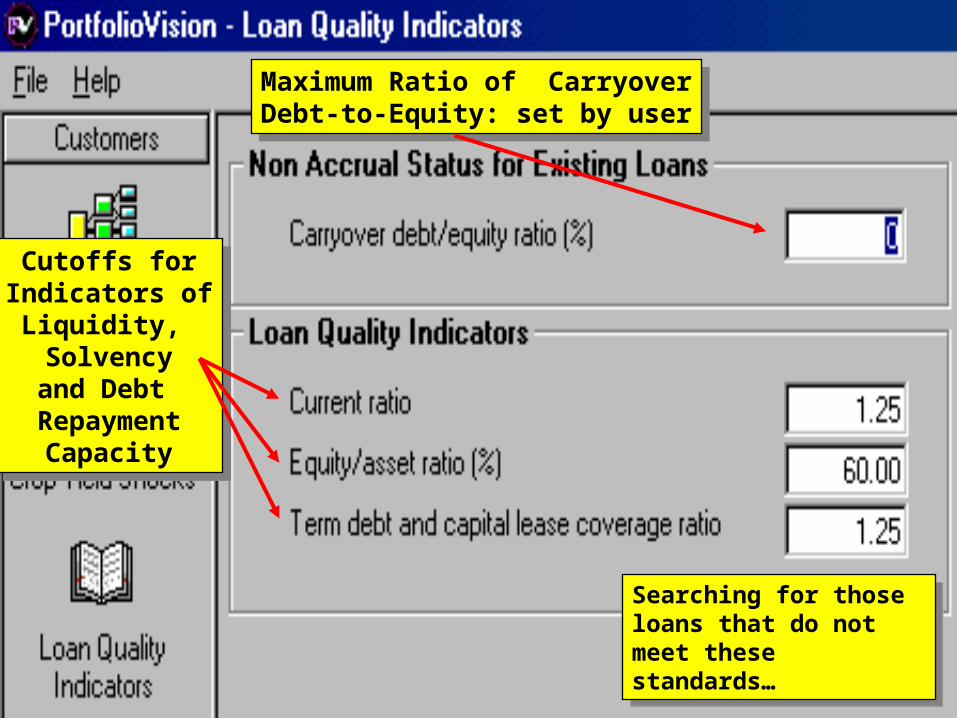

Cutoffs forIndicators of

Liquidity, Solvencyand Debt

RepaymentCapacity

Cutoffs forIndicators of

Liquidity, Solvencyand Debt

RepaymentCapacity

Maximum Ratio of CarryoverDebt-to-Equity: set by user

Maximum Ratio of CarryoverDebt-to-Equity: set by user

Searching for those loans that do not meet these standards…

Searching for those loans that do not meet these standards…

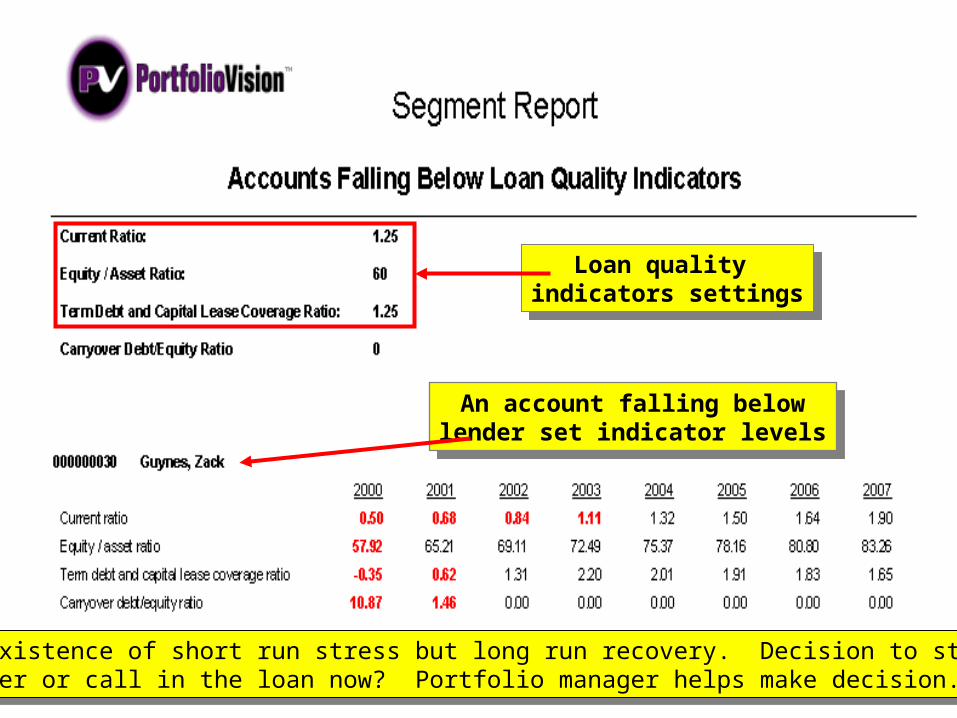

Loan quality indicators settings

Loan quality indicators settings

An account falling belowlender set indicator levels

An account falling belowlender set indicator levels

Note existence of short run stress but long run recovery. Decision to stay withBorrower or call in the loan now? Portfolio manager helps make decision.

Note existence of short run stress but long run recovery. Decision to stay withBorrower or call in the loan now? Portfolio manager helps make decision.

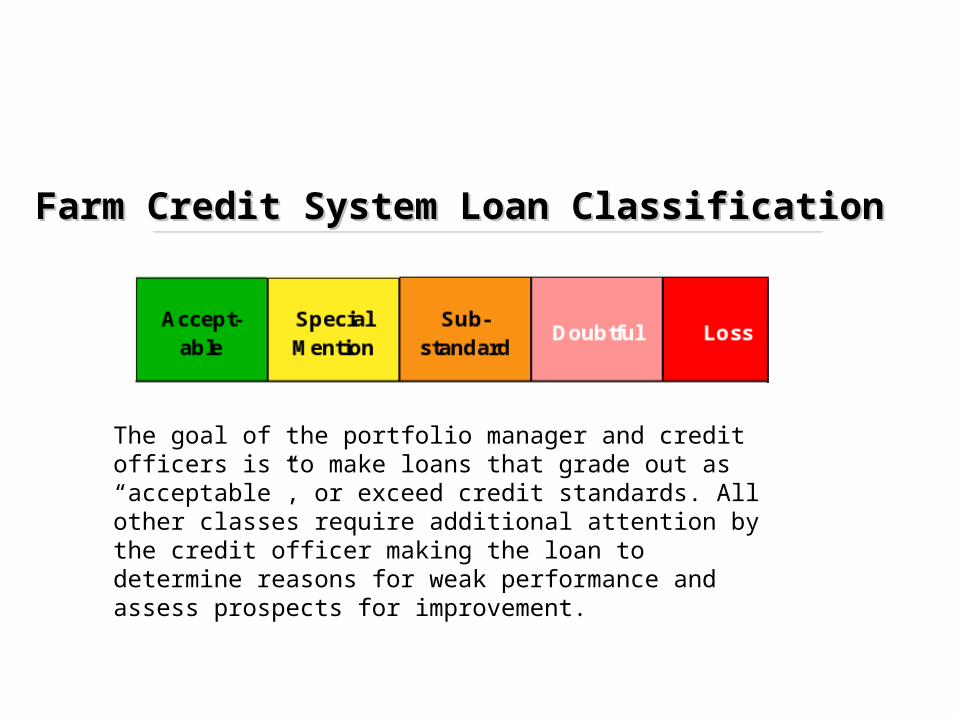

Farm Credit System Loan Classification Farm Credit System Loan Classification

The goal of the portfolio manager and credit officers is to make loans that grade out as “acceptable”, or exceed credit standards. All other classes require additional attention by the credit officer making the loan to determine reasons for weak performance and assess prospects for improvement.

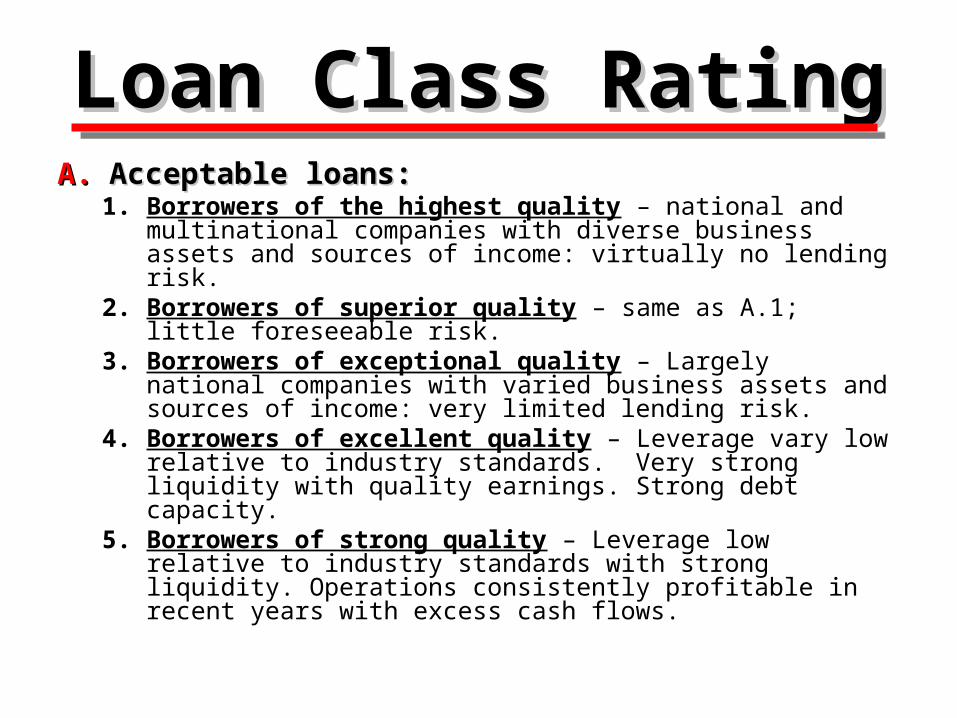

Loan Class Rating Loan Class Rating A.A. Acceptable loans:Acceptable loans:

1. Borrowers of the highest quality – national and multinational companies with diverse business assets and sources of income: virtually no lending risk.

2. Borrowers of superior quality – same as A.1; little foreseeable risk.

3. Borrowers of exceptional quality – Largely national companies with varied business assets and sources of income: very limited lending risk.

4. Borrowers of excellent quality – Leverage vary low relative to industry standards. Very strong liquidity with quality earnings. Strong debt capacity.

5. Borrowers of strong quality – Leverage low relative to industry standards with strong liquidity. Operations consistently profitable in recent years with excess cash flows.

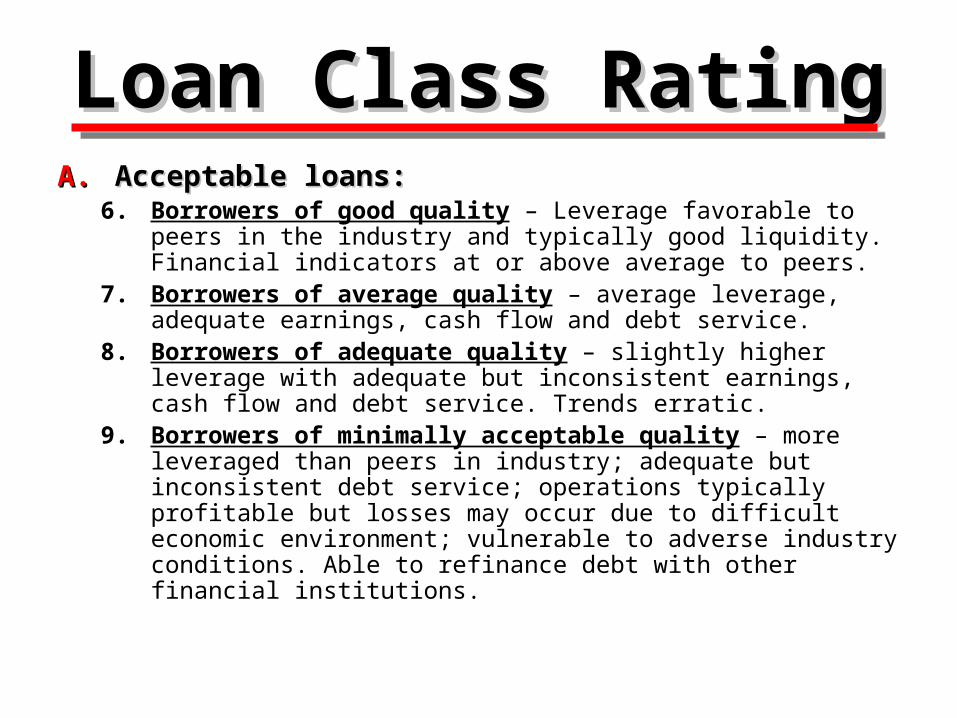

A.A. Acceptable loans:Acceptable loans:6. Borrowers of good quality – Leverage favorable to peers in

the industry and typically good liquidity. Financial indicators at or above average to peers.

7. Borrowers of average quality – average leverage, adequate earnings, cash flow and debt service.

8. Borrowers of adequate quality – slightly higher leverage with adequate but inconsistent earnings, cash flow and debt service. Trends erratic.

9. Borrowers of minimally acceptable quality – more leveraged than peers in industry; adequate but inconsistent debt service; operations typically profitable but losses may occur due to difficult economic environment; vulnerable to adverse industry conditions. Able to refinance debt with other financial institutions.

Loan Class Rating Loan Class Rating

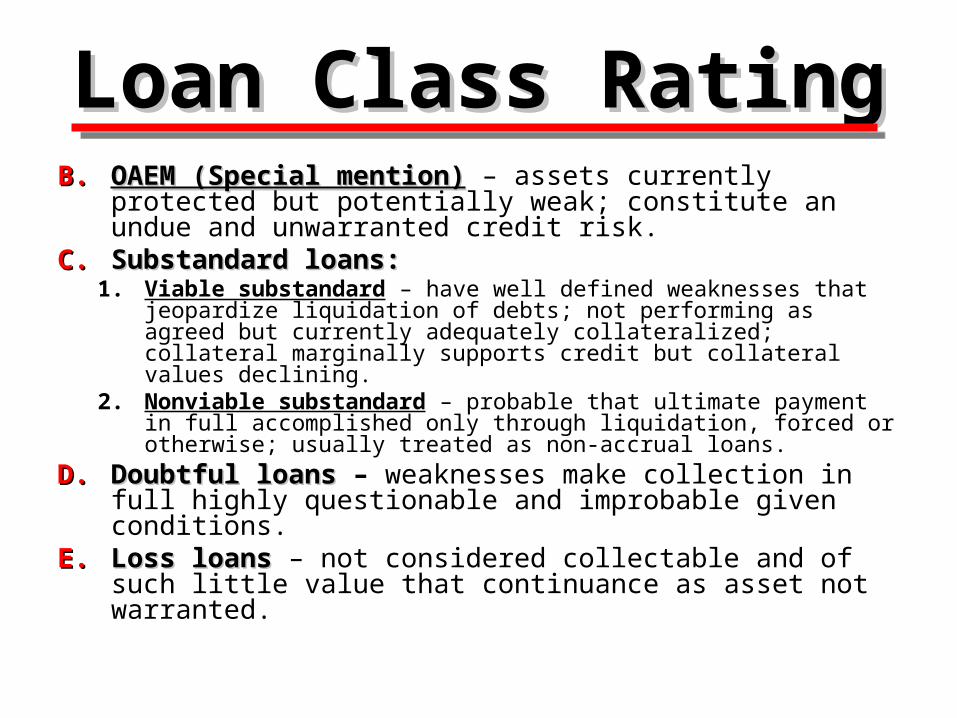

B.B. OAEM (Special mention)OAEM (Special mention) – assets currently protected but potentially weak; constitute an undue and unwarranted credit risk.

C.C. Substandard loans:Substandard loans:1. Viable substandard – have well defined weaknesses that

jeopardize liquidation of debts; not performing as agreed but currently adequately collateralized; collateral marginally supports credit but collateral values declining.

2. Nonviable substandard – probable that ultimate payment in full accomplished only through liquidation, forced or otherwise; usually treated as non-accrual loans.

D.D. Doubtful loans Doubtful loans – weaknesses make collection in full highly questionable and improbable given conditions.

E.E. Loss loans Loss loans – not considered collectable and of such little value that continuance as asset not warranted.

Loan Class RatingLoan Class Rating

Migration of LoansMigration of LoansPortfolios are examined periodically to monitor

outstanding loans falling into lower loan falling into lower loan classificationsclassifications.

This can be done in a stress testing context by examining the effects of lower net incomes and land values on benchmark loans in each category for specific pools or loan segments.

This helps the portfolio manager to stay on top of changing economic conditions in each of these segments.