local production receipts in nfgsc appalachian zones · pdf fileproject name capacity (dth/d)...

TRANSCRIPT

Local Production Receipts in NFGSC Appalachian Zones 1 & 2

180,000.00

200,000.00

220,000.00

240,000.00

260,000.00

/dD

TH

/D

60,000.00

80,000.00

100,000.00

120,000.00

140,000.00

160,000.00

Jan

-07

Mar

-07

May

-07

Jul-

07

Sep

-07

Nov

-07

Jan

-08

Mar

-08

May

-08

Jul-

08

Sep

-08

Nov

-08

Jan

-09

Mar

-09

May

-09

Jul-

09

Sep

-09

Nov

-09

Jan

-10

Mar

-10

May

-10

Jul-

10

Sep

-10

Nov

-10

Jan

-11

Mar

-11

May

-11

Jul-

11

Sep

-11

Nov

-11

Jan

-12

Avg. dth per day 12 Month Rolling Avg. (dth)

dth/

d

4.00

5.00

6.00

Loca

l Pro

duct

ion

into

NF

GS

C (

Bcf

per

Mon

th)

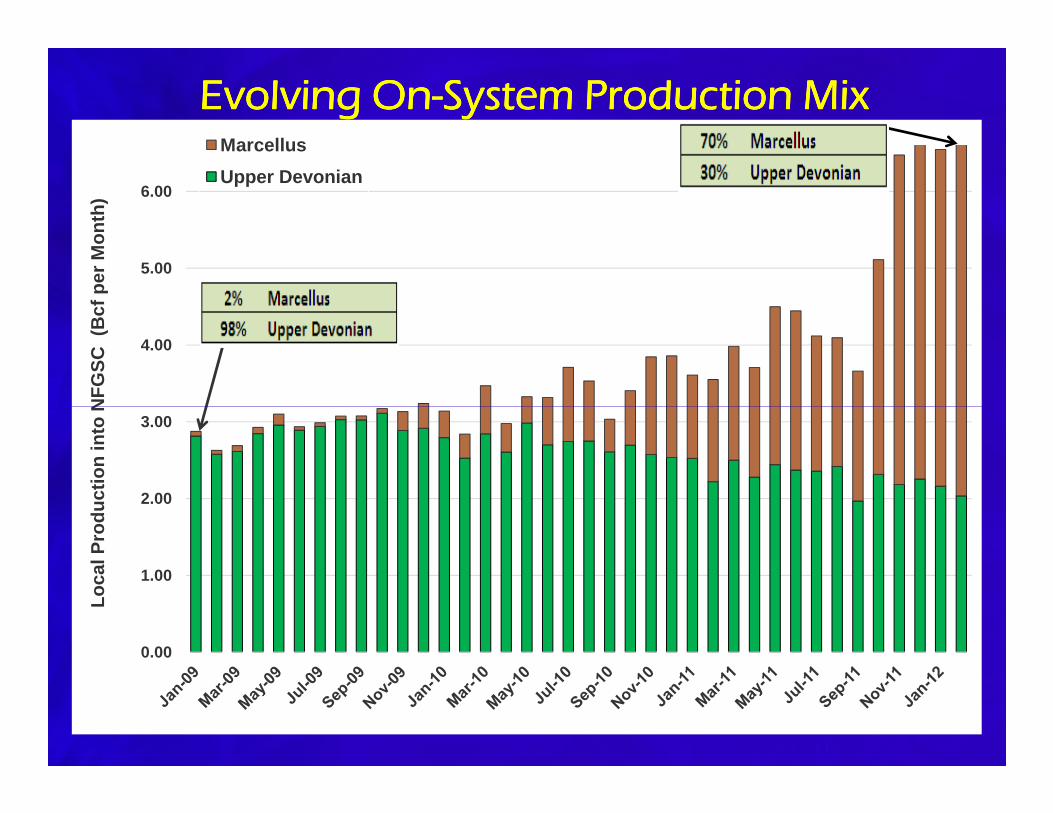

Marcellus

Upper Devonian

Evolving OnEvolving OnEvolving OnEvolving On----System Production MixSystem Production MixSystem Production MixSystem Production Mix

0.00

1.00

2.00

3.00

Loca

l Pro

duct

ion

into

NF

GS

C (

W2E – Unlocking Acreage in Key PA Counties

National Fuel Gas Supply Corporation National Fuel Gas Supply Corporation National Fuel Gas Supply Corporation National Fuel Gas Supply Corporation

West to East Expansion Highlights

• 82 miles of 24”, portions paralleling existing line FM-100

• 25,000 Hp at two new compressor stations

• Capacity: 425,000+ Dth/d;

• NEPA Pre-Filing Process commenced March 2010

• 7c Filing expected late 2012/early 2013

• Engineering and environmental studies well underway

• Expected in-service late 2013/2014 with a cost of $290MM

Marcellus to Markets…Marcellus to Markets…Marcellus to Markets…Marcellus to Markets…

Empire Pipeline links Marcellus to Markets

� Dawn Hub, Ontario and Eastern Canada

� New England via TGP 200 line� New England via TGP 200 line

� NYC area via Millennium Pipeline

� Leidy via NFG Supply Corporation

� Upstate New York LDCs attached to Empire

Marcellus to Markets…Marcellus to Markets…Marcellus to Markets…Marcellus to Markets…Dawn Hub, Ontario and Eastern Canada

• 4800 MW of merchant gas-fired generation

• Additional 1000MW under development

• Large LDC demand

• Union Gas, Enbridge, Gaz Metro (Quebec)• Union Gas, Enbridge, Gaz Metro (Quebec)

• Dawn Hub

• Over 100 companies with HUB contracts at Dawn

• Over 1Bcf/day traded on NGX/ICE for next gas day by over 30 Dawn counterparties

• Second most liquid trading point in Canada

Project NameCapacity (Dth/D)

Est.CapEx

In-Service

DateMarket Status

Lamont Compressor Station

90,000 $13.6 MM 2010/2011Fully

SubscribedCompleted – Flowing into TGP 300 Line

Line “N” Expansion 160,000 $20 MM 10/26/11Fully

SubscribedCompleted – Flowing into TETCO M2

Tioga County Extension 350,000 $49 MM 11/22/2011Fully

SubscribedCompleted

Northern Access Expansion

320,000 $62 MM ~11/2012Fully

SubscribedCertificate received October 26, 2011

Expansion Initiatives

Line “N” 2012 Expansion 163,000 $36 MM ~ 11/2012Fully

SubscribedCertificate filed in July 2011

Mercer 150,000 $30 MM 11/2013Fully

SubscribedNegotiating PA

West to East ~425,000 $290 MM 201429%

SubscribedMarketing continues with producers invarious stages of exploratory drilling

Central Tioga County Extension

260,000 $135 MM 2014Open

Season Closed

Evaluating market interest and facility design

Total Firm Capacity ~ 1,918,000 Dth/D

Capital Investment ~ $636 MM

Marcellus Driven Expansion ProjectsLamont Project

Line “N” Expansion (October 2011)

Tioga County Extension (November 2011)

Line “N” 2012 Expansion (November 2012)

Northern Access Expansion (November 2012)

90,000 Dth/d

160,000 Dth/d

350,000 Dth/d

163,000 Dth/d

320,000 Dth/d

West to East (2014)

Central Tioga County Ext (2014)

FY11 FY12 FY14FY13

Total Firm Capacity: ~1,918,000 Dth/DCapital Investment: ~$630 Million

~425,000 Dth/d

260,000 Dth/d

Mercer (2013)150,000 Dth/d

Marcellus Volumes from System Expansions

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

MC

FD

West to

East

Mercer &Central Tioga

County Extension

Actual Transported Marcellus Production Volumes

Estimated Marcellus Volumes from System Expansions (80% Load Factor)

0

200,000

400,000

600,000

800,000

MC

FD

Line N 2012 Expansion &

Northern Access

Tioga CountyExpansion

Line N 2011