lockdownthe lockdown lockdown week

TRANSCRIPT

Aishwarya Sonker

[email protected] | Tel: 9122 66303351

Harshita Kain

[email protected] | Tel: 9122 66301851

Suhas Harinarayanan

[email protected] | Tel: 9122 66303037

Arshad Perwez

[email protected] | Tel: 9122 66303080

Daily case growth inches up in India

28 Jun 2020

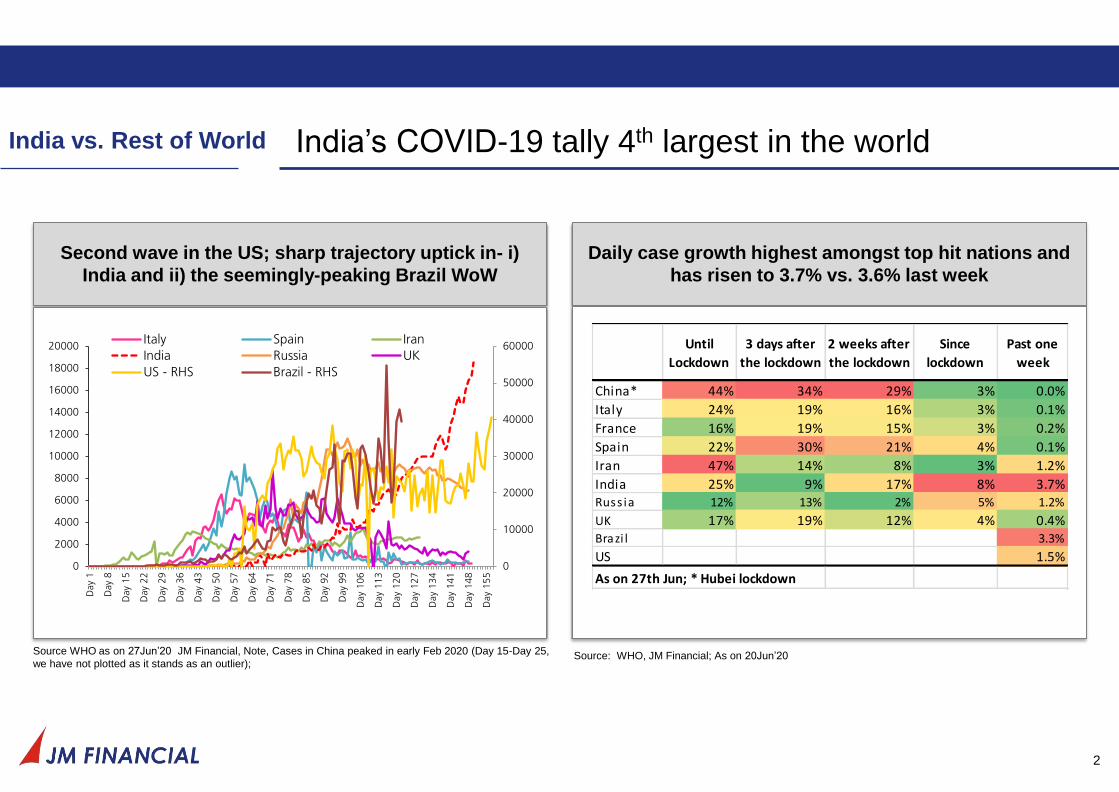

Second wave in the US; sharp trajectory uptick in- i)

India and ii) the seemingly-peaking Brazil WoW

India’s COVID-19 tally 4th largest in the world

Source WHO as on 27Jun’20 JM Financial, Note, Cases in China peaked in early Feb 2020 (Day 15-Day 25,

we have not plotted as it stands as an outlier);

Daily case growth highest amongst top hit nations and

has risen to 3.7% vs. 3.6% last week

Source: WHO, JM Financial; As on 20Jun’20

2

India vs. Rest of World

0

10000

20000

30000

40000

50000

60000

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

Day

1

Day

8

Day

15

Day

22

Day

29

Day

36

Day

43

Day

50

Day

57

Day

64

Day

71

Day

78

Day

85

Day

92

Day

99

Day

10

6

Day

11

3

Day

12

0

Day

12

7

Day

13

4

Day

141

Day

14

8

Day

15

5

Italy Spain Iran

India Russia UK

US - RHS Brazil - RHS

Until

Lockdown

3 days after

the lockdown

2 weeks after

the lockdown

Since

lockdown

Past one

week

China* 44% 34% 29% 3% 0.0%

Italy 24% 19% 16% 3% 0.1%

France 16% 19% 15% 3% 0.2%

Spain 22% 30% 21% 4% 0.1%

Iran 47% 14% 8% 3% 1.2%

India 25% 9% 17% 8% 3.7%Russ ia 12% 13% 2% 5% 1.2%

UK 17% 19% 12% 4% 0.4%Brazi l 3.3%

US 1.5%

As on 27th Jun; * Hubei lockdown

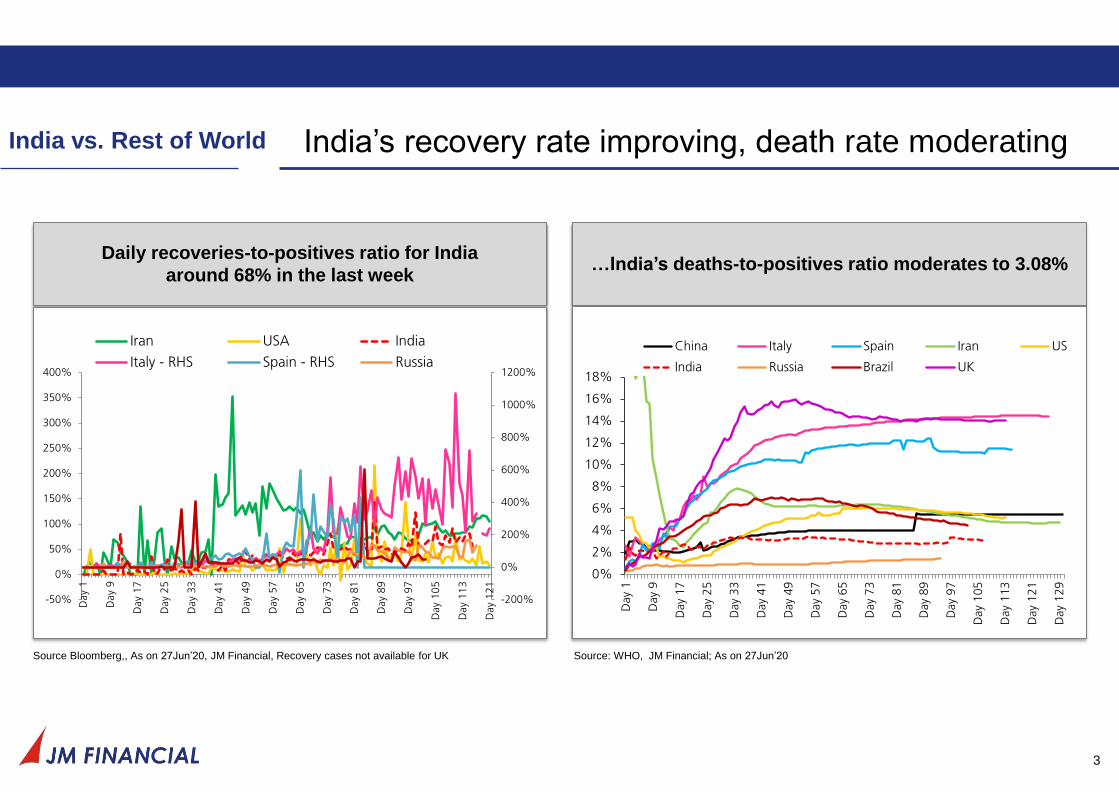

Daily recoveries-to-positives ratio for India

around 68% in the last week

India’s recovery rate improving, death rate moderating

Source Bloomberg,, As on 27Jun’20, JM Financial, Recovery cases not available for UK

…India’s deaths-to-positives ratio moderates to 3.08%

Source: WHO, JM Financial; As on 27Jun’20

3

India vs. Rest of World

-200%

0%

200%

400%

600%

800%

1000%

1200%

-50%

0%

50%

100%

150%

200%

250%

300%

350%

400%

Day

1

Day

9

Day

17

Day

25

Day

33

Day

41

Day

49

Day

57

Day

65

Day

73

Day

81

Day

89

Day

97

Day

10

5

Day

11

3

Day

12

1

Iran USA India

Italy - RHS Spain - RHS Russia

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Day

1

Day

9

Day

17

Day

25

Day

33

Day

41

Day

49

Day

57

Day

65

Day

73

Day

81

Day

89

Day

97

Day

105

Day

113

Day

121

Day

129

China Italy Spain Iran US

India Russia Brazil UK

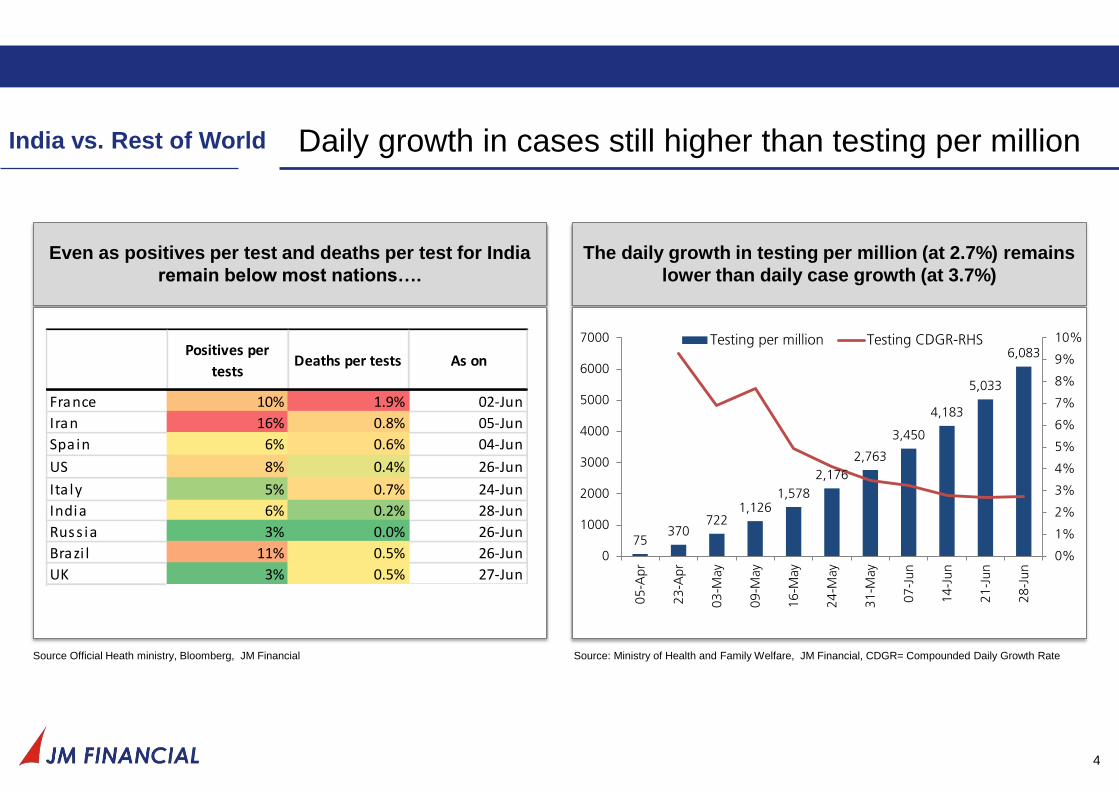

Even as positives per test and deaths per test for India

remain below most nations….

Daily growth in cases still higher than testing per million

Source Official Heath ministry, Bloomberg, JM Financial

The daily growth in testing per million (at 2.7%) remains

lower than daily case growth (at 3.7%)

Source: Ministry of Health and Family Welfare, JM Financial, CDGR= Compounded Daily Growth Rate

4

India vs. Rest of World

Positives per

testsDeaths per tests As on

France 10% 1.9% 02-Jun

Iran 16% 0.8% 05-Jun

Spain 6% 0.6% 04-Jun

US 8% 0.4% 26-Jun

Ita ly 5% 0.7% 24-Jun

India 6% 0.2% 28-Jun

Russ ia 3% 0.0% 26-Jun

Brazi l 11% 0.5% 26-Jun

UK 3% 0.5% 27-Jun

75370

7221,126

1,578

2,176

2,763

3,450

4,183

5,033

6,083

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0

1000

2000

3000

4000

5000

6000

7000

05

-Apr

23

-Apr

03

-May

09

-May

16

-May

24

-May

31

-May

07

-Ju

n

14

-Ju

n

21

-Ju

n

28

-Ju

n

Testing per million Testing CDGR-RHS

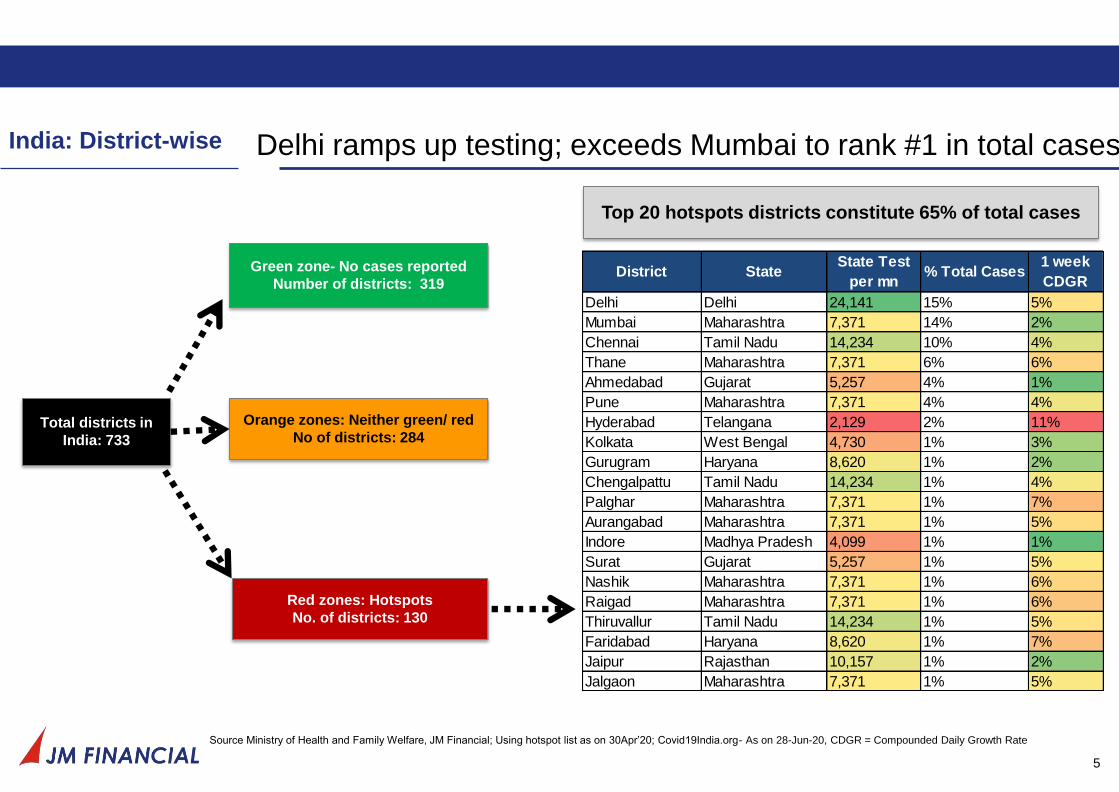

Delhi ramps up testing; exceeds Mumbai to rank #1 in total cases

5

Source Ministry of Health and Family Welfare, JM Financial; Using hotspot list as on 30Apr’20; Covid19India.org- As on 28-Jun-20, CDGR = Compounded Daily Growth Rate

India: District-wise

Total districts in

India: 733

Green zone- No cases reported

Number of districts: 319

Orange zones: Neither green/ red

No of districts: 284

Red zones: Hotspots

No. of districts: 130

Top 20 hotspots districts constitute 65% of total cases

District StateState Test

per mn% Total Cases

1 week

CDGR

Delhi Delhi 24,141 15% 5%

Mumbai Maharashtra 7,371 14% 2%

Chennai Tamil Nadu 14,234 10% 4%

Thane Maharashtra 7,371 6% 6%

Ahmedabad Gujarat 5,257 4% 1%

Pune Maharashtra 7,371 4% 4%

Hyderabad Telangana 2,129 2% 11%

Kolkata West Bengal 4,730 1% 3%

Gurugram Haryana 8,620 1% 2%

Chengalpattu Tamil Nadu 14,234 1% 4%

Palghar Maharashtra 7,371 1% 7%

Aurangabad Maharashtra 7,371 1% 5%

Indore Madhya Pradesh 4,099 1% 1%

Surat Gujarat 5,257 1% 5%

Nashik Maharashtra 7,371 1% 6%

Raigad Maharashtra 7,371 1% 6%

Thiruvallur Tamil Nadu 14,234 1% 5%

Faridabad Haryana 8,620 1% 7%

Jaipur Rajasthan 10,157 1% 2%

Jalgaon Maharashtra 7,371 1% 5%

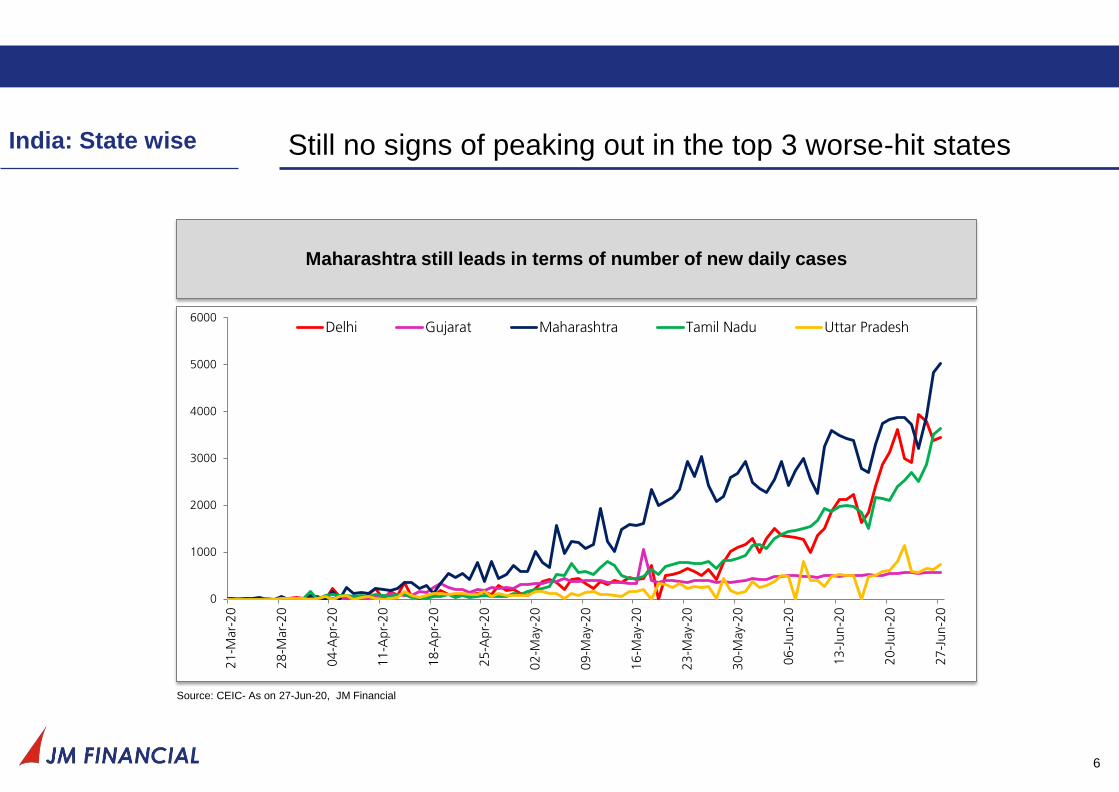

Still no signs of peaking out in the top 3 worse-hit states

6

India: State wise

Maharashtra still leads in terms of number of new daily cases

Source: CEIC- As on 27-Jun-20, JM Financial

0

1000

2000

3000

4000

5000

6000

21

-Mar-

20

28

-Mar-

20

04

-Apr-

20

11

-Apr-

20

18

-Apr-

20

25

-Apr-

20

02

-May-

20

09

-May-

20

16

-May-

20

23

-May-

20

30

-May-

20

06

-Ju

n-2

0

13

-Ju

n-2

0

20

-Ju

n-2

0

27

-Ju

n-2

0

Delhi Gujarat Maharashtra Tamil Nadu Uttar Pradesh

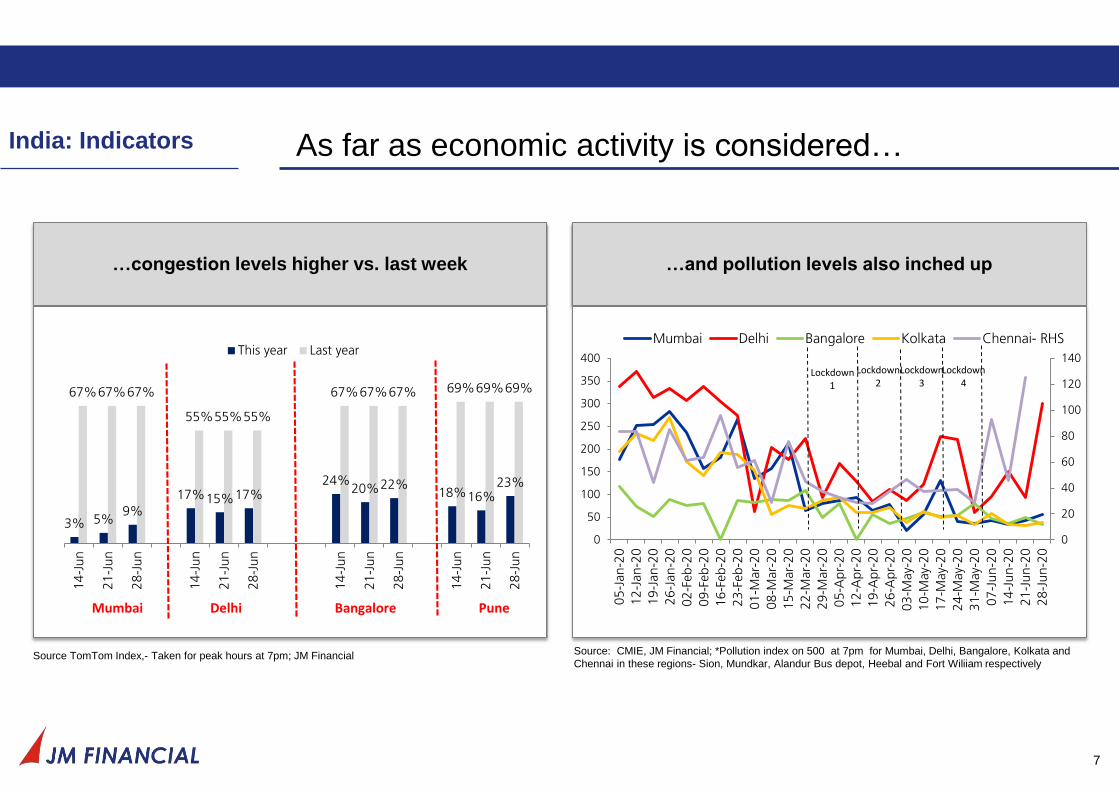

…and pollution levels also inched up

As far as economic activity is considered…

7

…congestion levels higher vs. last week

Source TomTom Index,- Taken for peak hours at 7pm; JM Financial Source: CMIE, JM Financial; *Pollution index on 500 at 7pm for Mumbai, Delhi, Bangalore, Kolkata and

Chennai in these regions- Sion, Mundkar, Alandur Bus depot, Heebal and Fort Wiliiam respectively

India: Indicators

3% 5%9%

17%15%17%24%

20%22%18%16%

23%

67%67%67%

55%55%55%

67%67%67% 69%69%69%

14

-Ju

n

21

-Ju

n

28

-Ju

n

14

-Ju

n

21

-Ju

n

28

-Ju

n

14

-Ju

n

21

-Ju

n

28

-Ju

n

14

-Ju

n

21

-Ju

n

28

-Ju

n

This year Last year

Mumbai Delhi Bangalore Pune

0

20

40

60

80

100

120

140

0

50

100

150

200

250

300

350

400

05

-Jan-2

0

12

-Jan-2

0

19

-Jan-2

0

26

-Jan-2

0

02

-Feb-2

0

09

-Feb-2

0

16

-Feb-2

0

23

-Feb-2

0

01

-Mar-

20

08

-Mar-

20

15

-Mar-

20

22

-Mar-

20

29

-Mar-

20

05

-Apr-

20

12

-Apr-

20

19

-Apr-

20

26

-Apr-

20

03

-May-

20

10

-May-

20

17

-May-

20

24

-May-

20

31

-May-

20

07

-Ju

n-2

0

14

-Ju

n-2

0

21

-Ju

n-2

0

28

-Ju

n-2

0

Mumbai Delhi Bangalore Kolkata Chennai- RHS

Lockdown1

Lockdown2

Lockdown3

Lockdown4

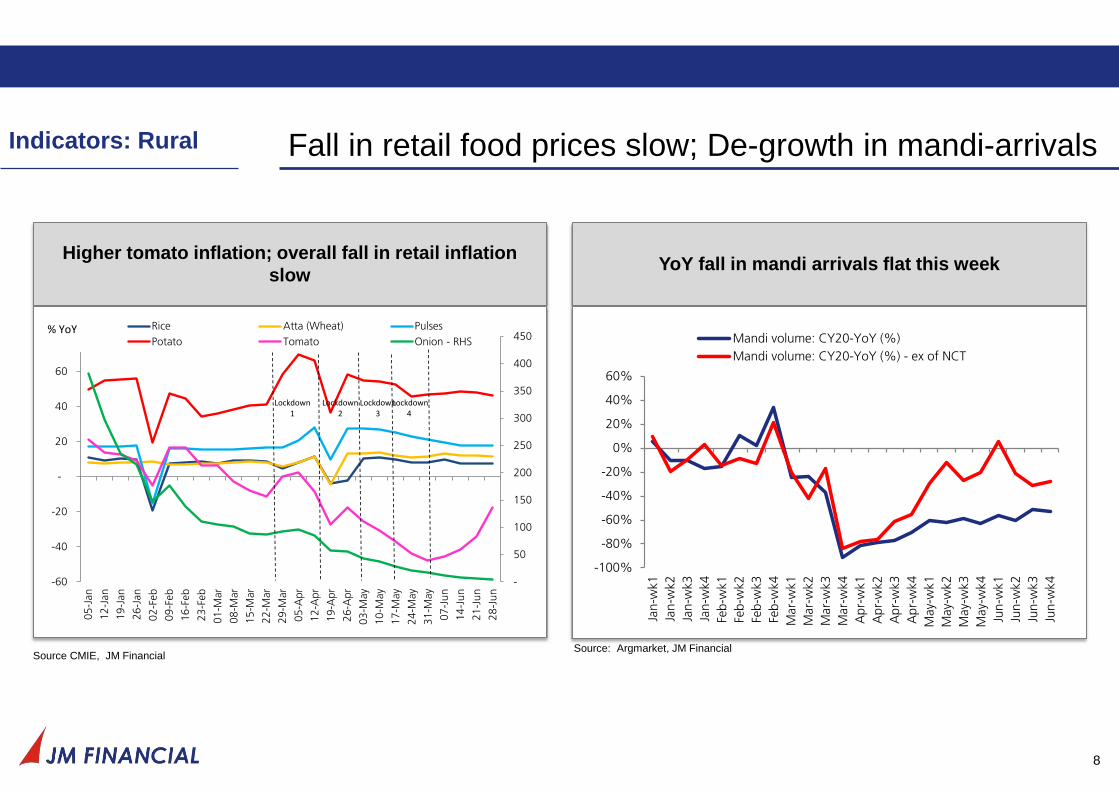

Fall in retail food prices slow; De-growth in mandi-arrivals

8

Higher tomato inflation; overall fall in retail inflation

slow

Source CMIE, JM Financial

YoY fall in mandi arrivals flat this week

Source: Argmarket, JM Financial

Indicators: Rural

-

50

100

150

200

250

300

350

400

450

-60

-40

-20

-

20

40

60

80

05

-Jan

12

-Jan

19

-Jan

26

-Jan

02

-Feb

09

-Feb

16

-Feb

23

-Feb

01

-Mar

08

-Mar

15

-Mar

22

-Mar

29

-Mar

05

-Apr

12

-Apr

19

-Apr

26

-Apr

03

-May

10

-May

17

-May

24

-May

31

-May

07

-Ju

n

14

-Ju

n

21

-Ju

n

28

-Ju

n

Rice Atta (Wheat) Pulses

Potato Tomato Onion - RHS% YoY

Lockdown 2

Lockdown 1

Lockdown 3

Lockdown 4

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

Jan-w

k1

Jan-w

k2

Jan-w

k3

Jan-w

k4

Feb-w

k1

Feb-w

k2

Feb-w

k3

Feb-w

k4

Mar-

wk1

Mar-

wk2

Mar-

wk3

Mar-

wk4

Ap

r-w

k1

Ap

r-w

k2

Ap

r-w

k3

Ap

r-w

k4

May-

wk1

May-

wk2

May-

wk3

May-

wk4

Jun-w

k1

Jun-w

k2

Jun-w

k3

Jun-w

k4

Mandi volume: CY20-YoY (%)

Mandi volume: CY20-YoY (%) - ex of NCT

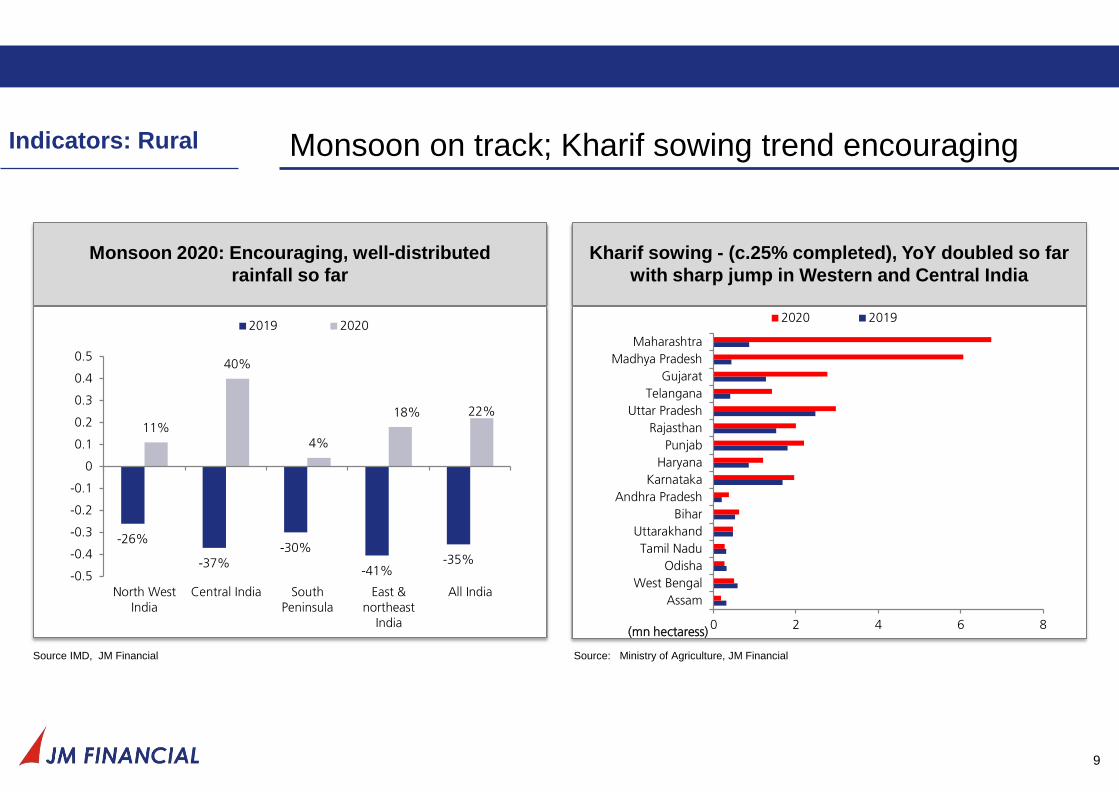

Monsoon on track; Kharif sowing trend encouraging

9

Monsoon 2020: Encouraging, well-distributed

rainfall so far

Source IMD, JM Financial

Kharif sowing - (c.25% completed), YoY doubled so far

with sharp jump in Western and Central India

Source: Ministry of Agriculture, JM Financial

Indicators: Rural

-26%

-37%-30%

-41%-35%

11%

40%

4%

18% 22%

-0.5

-0.4

-0.3

-0.2

-0.1

0

0.1

0.2

0.3

0.4

0.5

North WestIndia

Central India SouthPeninsula

East &northeast

India

All India

2019 2020

0 2 4 6 8

Assam

West Bengal

Odisha

Tamil Nadu

Uttarakhand

Bihar

Andhra Pradesh

Karnataka

Haryana

Punjab

Rajasthan

Uttar Pradesh

Telangana

Gujarat

Madhya Pradesh

Maharashtra

(mn hectaress)

2020 2019

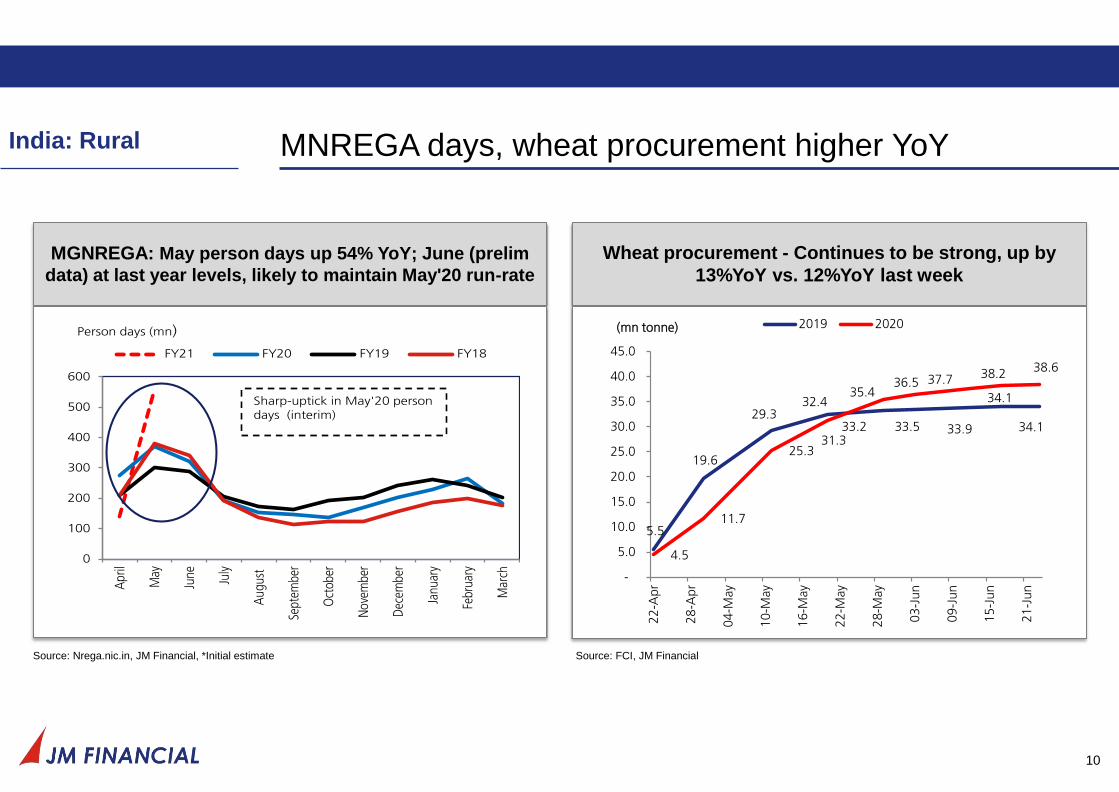

MNREGA days, wheat procurement higher YoY

10

India: Rural

MGNREGA: May person days up 54% YoY; June (prelim

data) at last year levels, likely to maintain May'20 run-rate

Wheat procurement - Continues to be strong, up by

13%YoY vs. 12%YoY last week

Source: Nrega.nic.in, JM Financial, *Initial estimate Source: FCI, JM Financial

0

100

200

300

400

500

600

Ap

ril

May

June July

Au

gust

Sept

embe

r

Oct

ober

No

vem

ber

Dec

embe

r

Janu

ary

Febr

uary

Mar

ch

FY21 FY20 FY19 FY18

Person days (mn)

Sharp-uptick in May'20 person days (interim)

5.5

19.6

29.3 32.4

33.2 33.5 33.9 34.1

34.1

4.5

11.7

25.3 31.3

35.4 36.5 37.7 38.2

38.6

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

22

-Ap

r

28

-Ap

r

04-M

ay

10-M

ay

16-M

ay

22-M

ay

28-M

ay

03-J

un

09-J

un

15-J

un

21-J

un

(mn tonne) 2019 2020

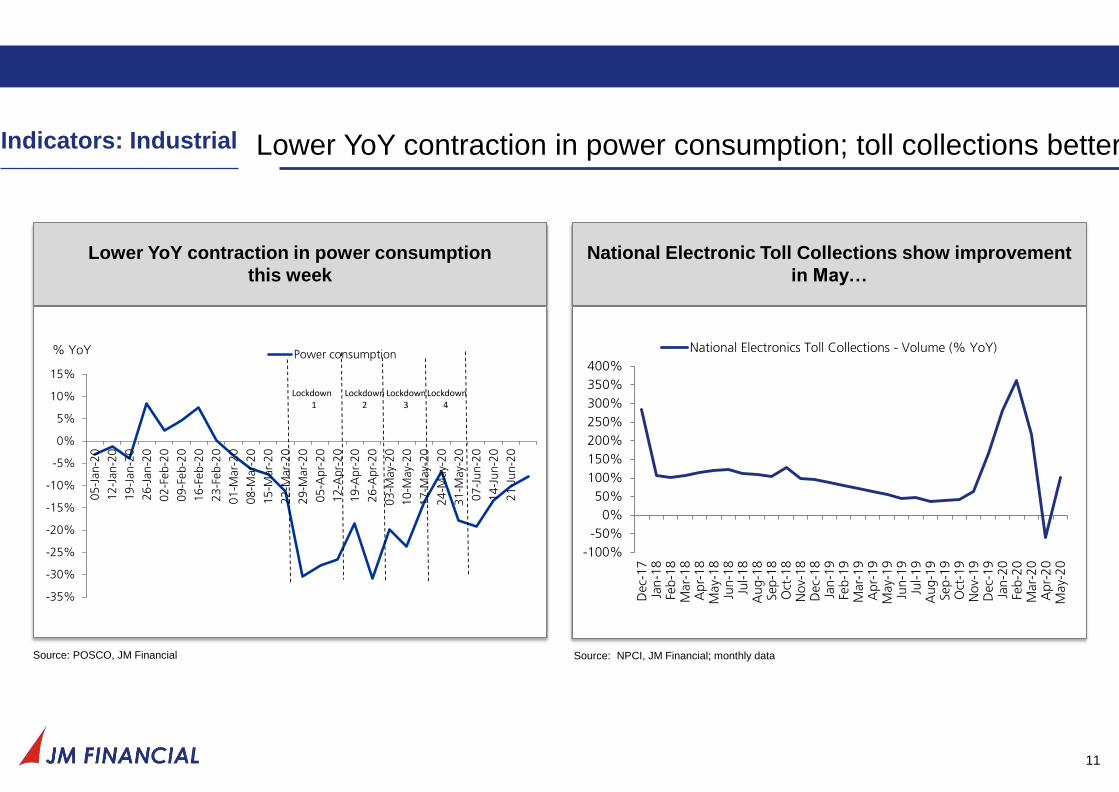

Lower YoY contraction in power consumption; toll collections better

11

Lower YoY contraction in power consumption

this week

Source: POSCO, JM Financial

National Electronic Toll Collections show improvement

in May…

Source: NPCI, JM Financial; monthly data

-100%

-50%

0%

50%

100%

150%

200%

250%

300%

350%

400%

Dec-

17

Jan

-18

Feb-1

8M

ar-

18

Apr-

18

May-

18

Jun-1

8Ju

l-1

8A

ug-1

8Sep

-18

Oct

-18

Nov-

18

Dec-

18

Jan

-19

Feb-1

9M

ar-

19

Apr-

19

May-

19

Jun-1

9Ju

l-1

9A

ug-1

9Sep

-19

Oct

-19

Nov-

19

Dec-

19

Jan

-20

Feb-2

0M

ar-

20

Apr-

20

May-

20

National Electronics Toll Collections - Volume (% YoY)

Indicators: Industrial

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

05

-Jan-2

0

12

-Jan-2

0

19

-Jan-2

0

26

-Jan-2

0

02

-Feb-2

0

09

-Feb-2

0

16

-Feb-2

0

23

-Feb-2

0

01

-Mar-

20

08

-Mar-

20

15

-Mar-

20

22

-Mar-

20

29

-Mar-

20

05

-Apr-

20

12

-Apr-

20

19

-Apr-

20

26

-Apr-

20

03

-May-

20

10

-May-

20

17

-May-

20

24

-May-

20

31

-May-

20

07

-Ju

n-2

0

14

-Ju

n-2

0

21

-Ju

n-2

0

Power consumption% YoY

Lockdown 2

Lockdown1

Lockdown 3

Lockdown 4

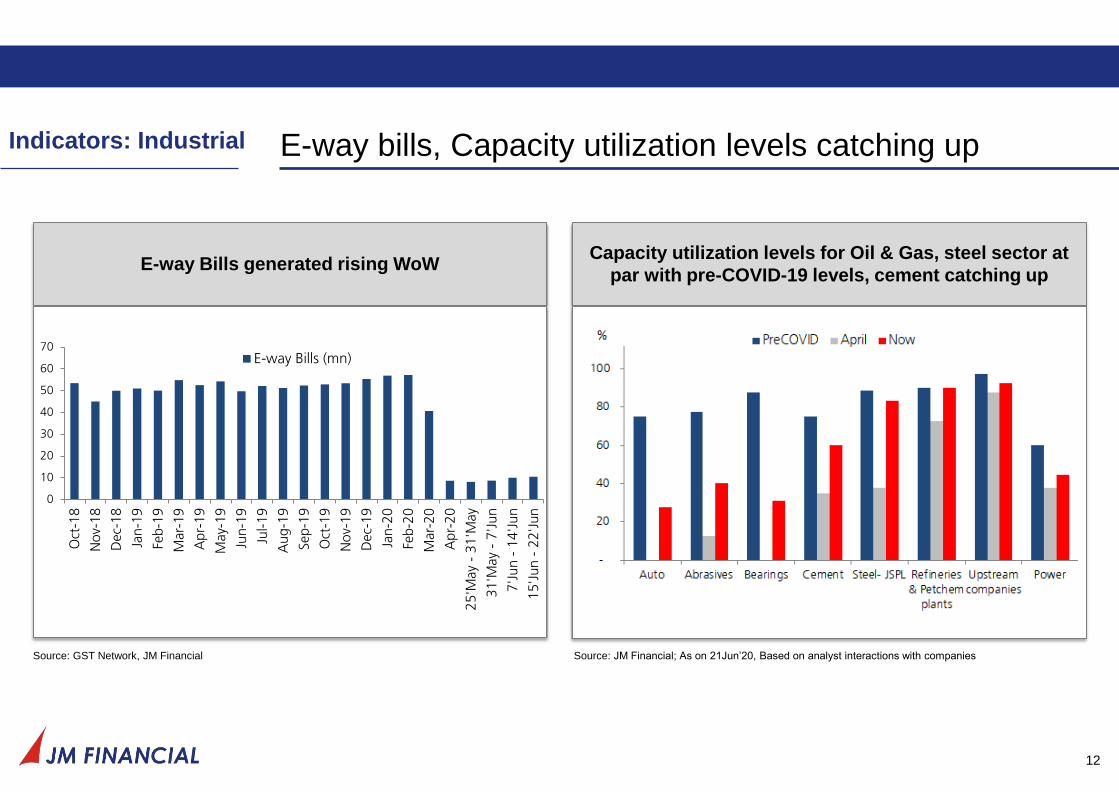

E-way bills, Capacity utilization levels catching up

12

E-way Bills generated rising WoW

Source: GST Network, JM Financial

Capacity utilization levels for Oil & Gas, steel sector at

par with pre-COVID-19 levels, cement catching up

Source: JM Financial; As on 21Jun’20, Based on analyst interactions with companies

Indicators: Industrial

0

10

20

30

40

50

60

70

Oct

-18

No

v-1

8

Dec-

18

Jan

-19

Feb-1

9

Mar-

19

Ap

r-1

9

May-

19

Jun-1

9

Jul-1

9

Au

g-1

9

Sep-1

9

Oct

-19

No

v-1

9

Dec-

19

Jan

-20

Feb-2

0

Mar-

20

Ap

r-2

0

25'M

ay

- 3

1'M

ay

31'M

ay

- 7

'Ju

n

7'J

un -

14

'Ju

n

15'J

un

- 2

2'J

un

E-way Bills (mn)

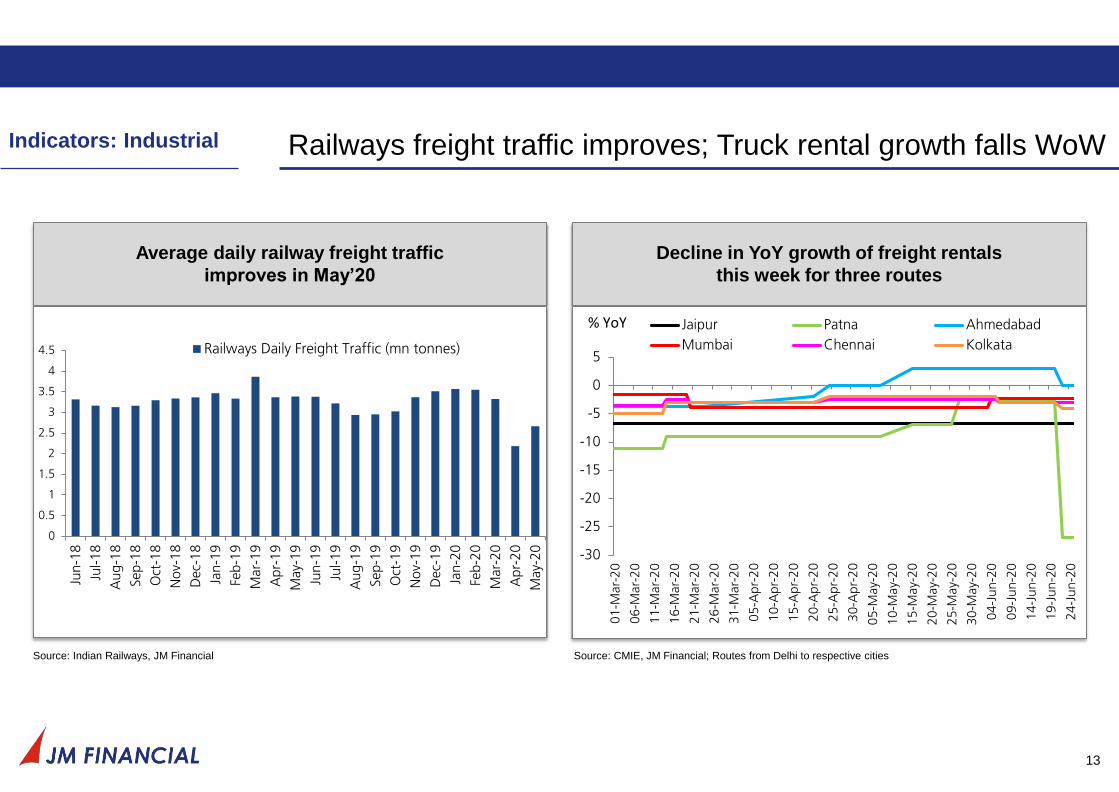

Railways freight traffic improves; Truck rental growth falls WoW

13

Average daily railway freight traffic

improves in May’20

Decline in YoY growth of freight rentals

this week for three routes

Source: Indian Railways, JM Financial Source: CMIE, JM Financial; Routes from Delhi to respective cities

Indicators: Industrial

-30

-25

-20

-15

-10

-5

0

5

01-M

ar-

20

06-M

ar-

20

11-M

ar-

20

16-M

ar-

20

21-M

ar-

20

26-M

ar-

20

31-M

ar-

20

05-A

pr-

20

10-A

pr-

20

15-A

pr-

20

20-A

pr-

20

25-A

pr-

20

30-A

pr-

20

05-M

ay-

20

10-M

ay-

20

15-M

ay-

20

20-M

ay-

20

25-M

ay-

20

30-M

ay-

20

04-J

un

-20

09-J

un

-20

14-J

un

-20

19-J

un

-20

24-J

un

-20

Jaipur Patna Ahmedabad

Mumbai Chennai Kolkata

% YoY

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

Jun-1

8

Jul-1

8

Aug-1

8

Sep-1

8

Oct

-18

No

v-1

8

Dec-

18

Jan

-19

Feb-1

9

Mar-

19

Apr-

19

May-

19

Jun-1

9

Jul-1

9

Aug-1

9

Sep-1

9

Oct

-19

No

v-1

9

Dec-

19

Jan

-20

Feb-2

0

Mar-

20

Apr-

20

May-

20

Railways Daily Freight Traffic (mn tonnes)

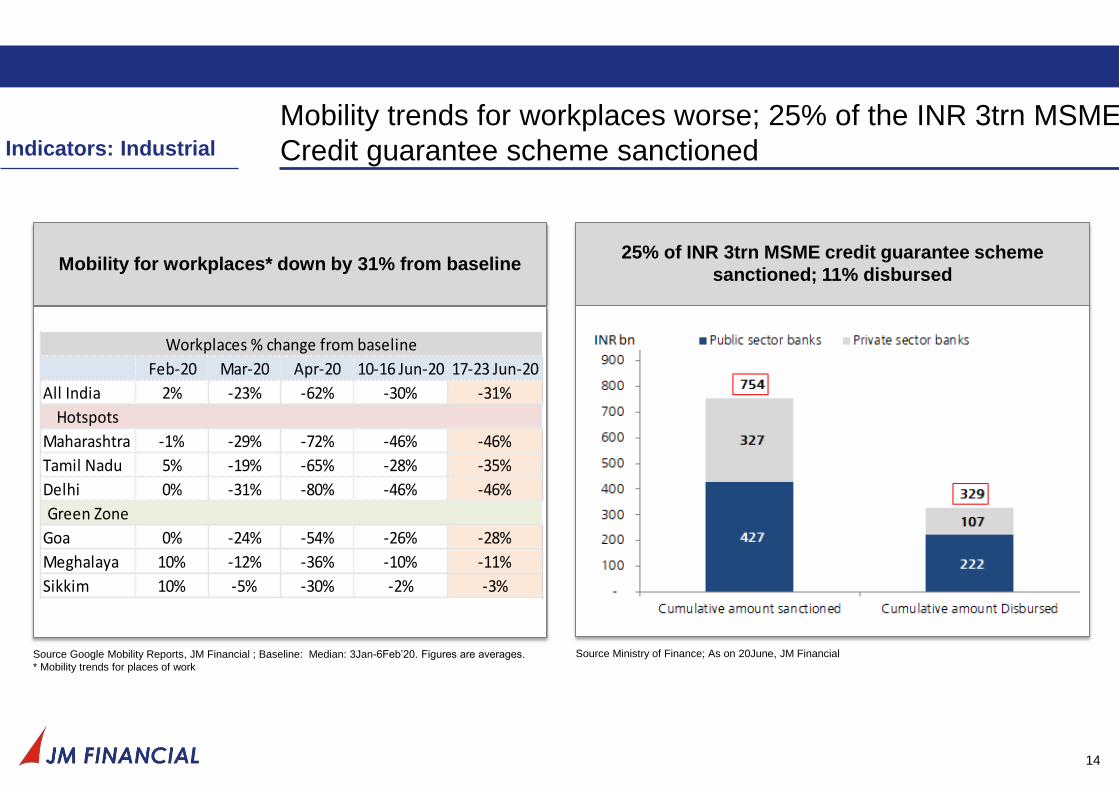

Mobility trends for workplaces worse; 25% of the INR 3trn MSME

Credit guarantee scheme sanctioned

14

Mobility for workplaces* down by 31% from baseline

Source Google Mobility Reports, JM Financial ; Baseline: Median: 3Jan-6Feb’20. Figures are averages.

* Mobility trends for places of work

Indicators: Industrial

25% of INR 3trn MSME credit guarantee scheme

sanctioned; 11% disbursed

Source Ministry of Finance; As on 20June, JM Financial

Feb-20 Mar-20 Apr-20 10-16 Jun-20 17-23 Jun-20

All India 2% -23% -62% -30% -31%

Hotspots

Maharashtra -1% -29% -72% -46% -46%

Tamil Nadu 5% -19% -65% -28% -35%

Delhi 0% -31% -80% -46% -46%

Green Zone

Goa 0% -24% -54% -26% -28%

Meghalaya 10% -12% -36% -10% -11%

Sikkim 10% -5% -30% -2% -3%

Workplaces % change from baseline

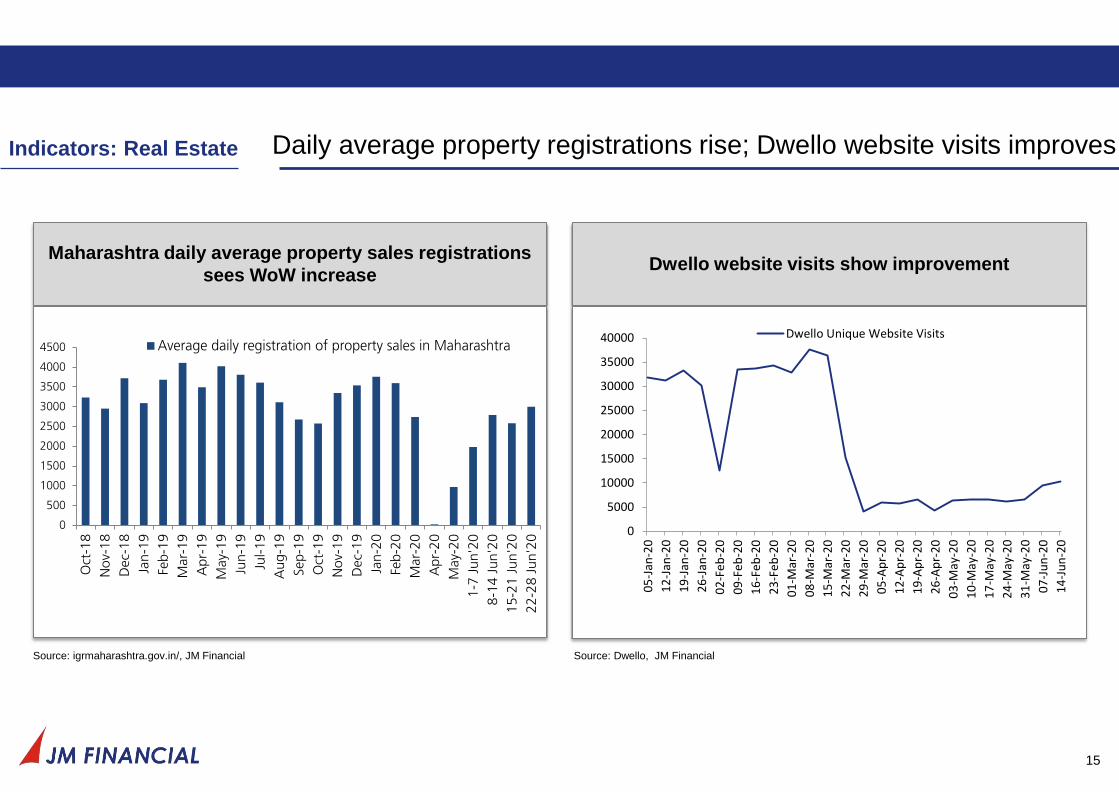

Daily average property registrations rise; Dwello website visits improves

15

Maharashtra daily average property sales registrations

sees WoW increase Dwello website visits show improvement

Source: igrmaharashtra.gov.in/, JM Financial Source: Dwello, JM Financial

0

5000

10000

15000

20000

25000

30000

35000

40000

05

-Jan

-20

12

-Jan

-20

19

-Jan

-20

26

-Jan

-20

02

-Fe

b-2

0

09

-Fe

b-2

0

16

-Fe

b-2

0

23

-Fe

b-2

0

01

-Mar

-20

08

-Mar

-20

15

-Mar

-20

22

-Mar

-20

29

-Mar

-20

05

-Ap

r-2

0

12

-Ap

r-2

0

19

-Ap

r-2

0

26

-Ap

r-2

0

03

-May

-20

10

-May

-20

17

-May

-20

24

-May

-20

31

-May

-20

07

-Ju

n-2

0

14

-Ju

n-2

0

Dwello Unique Website Visits

Indicators: Real Estate

0

500

1000

1500

2000

2500

3000

3500

4000

4500

Oct

-18

No

v-1

8

Dec-

18

Jan

-19

Feb-1

9

Mar-

19

Ap

r-1

9

May-

19

Jun-1

9

Jul-19

Au

g-1

9

Sep-1

9

Oct

-19

No

v-1

9

Dec-

19

Jan

-20

Feb-2

0

Mar-

20

Ap

r-2

0

May-

20

1-7

Ju

n'2

0

8-1

4 J

un

'20

15-2

1 J

un'2

0

22-2

8 J

un

'20

Average daily registration of property sales in Maharashtra

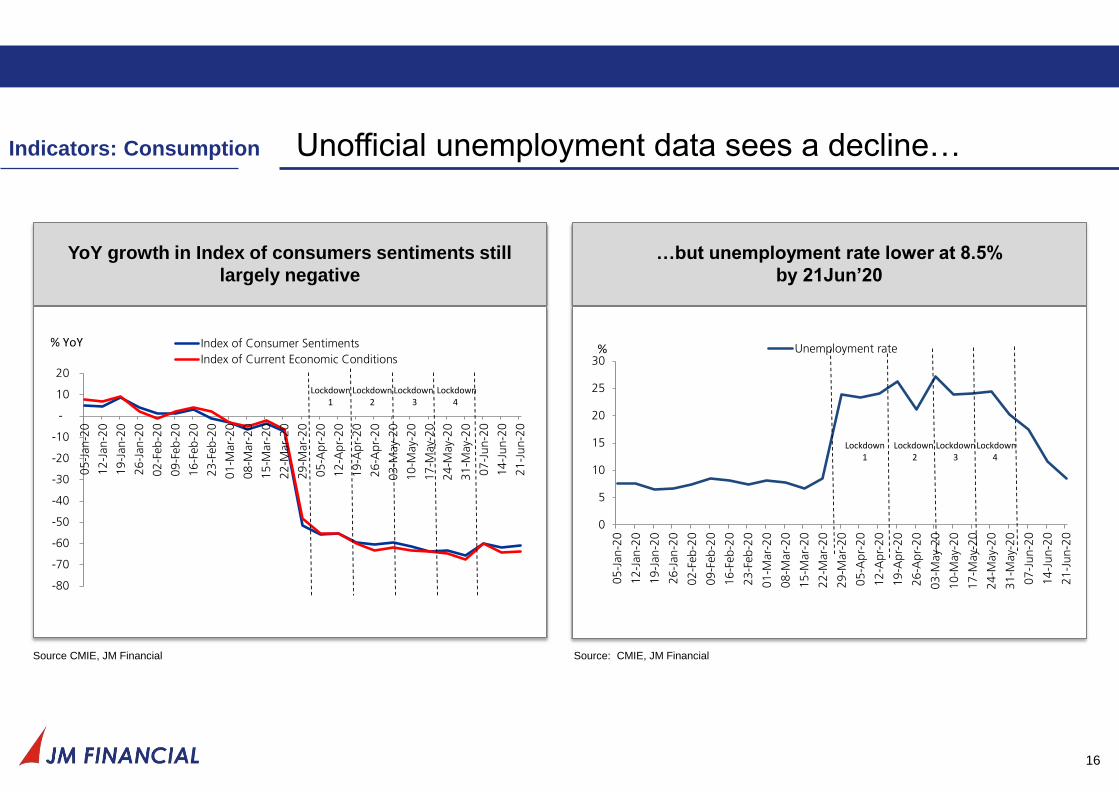

Unofficial unemployment data sees a decline…

16

YoY growth in Index of consumers sentiments still

largely negative

Source CMIE, JM Financial

…but unemployment rate lower at 8.5%

by 21Jun’20

Source: CMIE, JM Financial

Indicators: Consumption

-80

-70

-60

-50

-40

-30

-20

-10

-

10

20

05

-Jan

-20

12

-Jan

-20

19

-Jan

-20

26

-Jan

-20

02

-Feb

-20

09

-Feb

-20

16

-Feb

-20

23

-Feb

-20

01

-Mar-

20

08

-Mar-

20

15

-Mar-

20

22

-Mar-

20

29

-Mar-

20

05

-Ap

r-2

0

12

-Ap

r-2

0

19

-Ap

r-2

0

26

-Ap

r-2

0

03

-May-

20

10

-May-

20

17

-May-

20

24

-May-

20

31

-May-

20

07

-Ju

n-2

0

14

-Ju

n-2

0

21

-Ju

n-2

0

Index of Consumer Sentiments

Index of Current Economic Conditions

% YoY

Lockdown 2

Lockdown 1

Lockdown3

Lockdown 4

0

5

10

15

20

25

30

05

-Jan

-20

12

-Jan

-20

19

-Jan

-20

26

-Jan

-20

02

-Feb

-20

09

-Feb

-20

16

-Feb

-20

23

-Feb

-20

01

-Mar-

20

08

-Mar-

20

15

-Mar-

20

22

-Mar-

20

29

-Mar-

20

05

-Ap

r-2

0

12

-Ap

r-2

0

19

-Ap

r-2

0

26

-Ap

r-2

0

03

-May-

20

10

-May-

20

17

-May-

20

24

-May-

20

31

-May-

20

07

-Ju

n-2

0

14

-Ju

n-2

0

21

-Ju

n-2

0

Unemployment rate%

Lockdown2

Lockdown 1

Lockdown 3

Lockdown 4

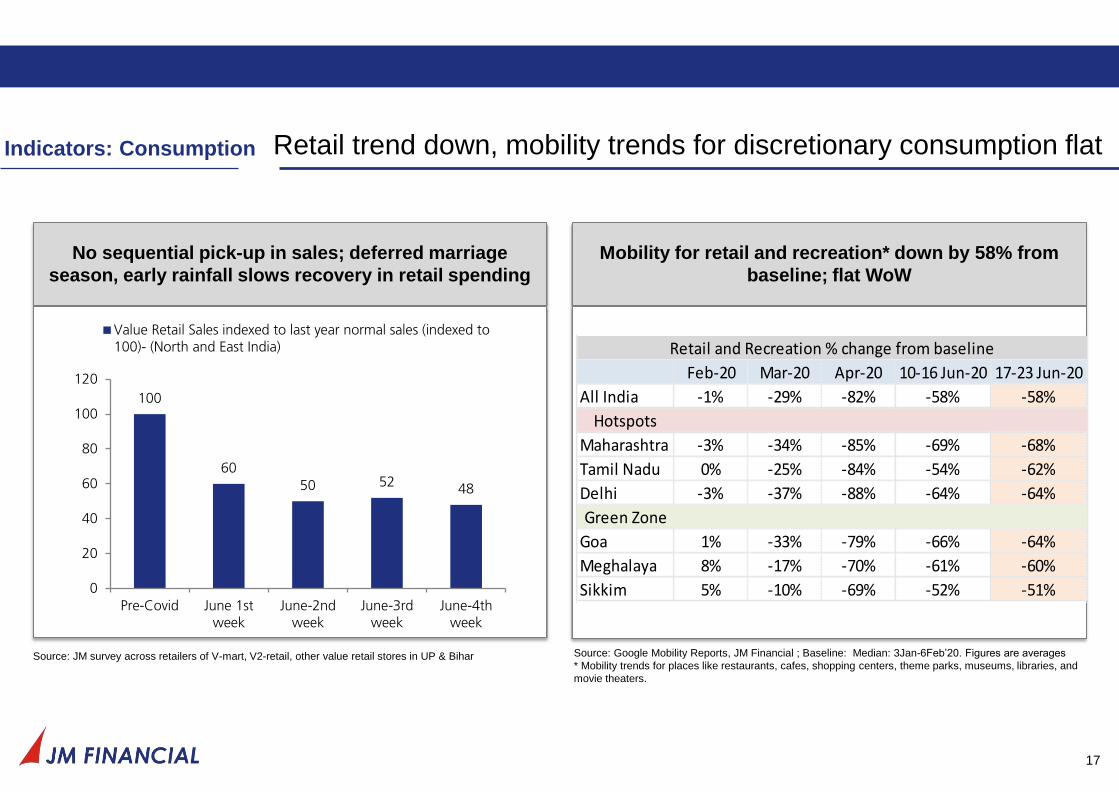

Retail trend down, mobility trends for discretionary consumption flat

17

No sequential pick-up in sales; deferred marriage

season, early rainfall slows recovery in retail spending

Mobility for retail and recreation* down by 58% from

baseline; flat WoW

Source: Google Mobility Reports, JM Financial ; Baseline: Median: 3Jan-6Feb’20. Figures are averages

* Mobility trends for places like restaurants, cafes, shopping centers, theme parks, museums, libraries, and

movie theaters.

Indicators: Consumption

Source: JM survey across retailers of V-mart, V2-retail, other value retail stores in UP & Bihar

Feb-20 Mar-20 Apr-20 10-16 Jun-20 17-23 Jun-20

All India -1% -29% -82% -58% -58%

Hotspots

Maharashtra -3% -34% -85% -69% -68%

Tamil Nadu 0% -25% -84% -54% -62%

Delhi -3% -37% -88% -64% -64%

Green Zone

Goa 1% -33% -79% -66% -64%

Meghalaya 8% -17% -70% -61% -60%

Sikkim 5% -10% -69% -52% -51%

Retail and Recreation % change from baseline

100

60

50 5248

0

20

40

60

80

100

120

Pre-Covid June 1stweek

June-2ndweek

June-3rdweek

June-4thweek

Value Retail Sales indexed to last year normal sales (indexed to100)- (North and East India)

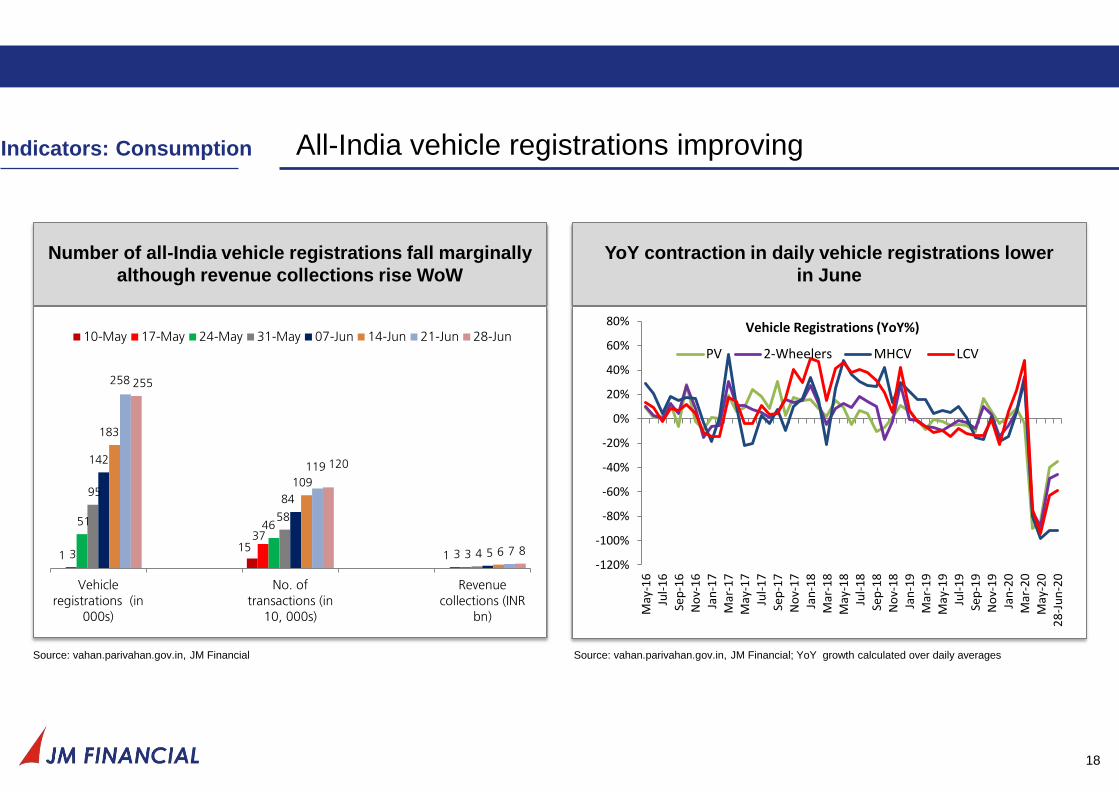

All-India vehicle registrations improving

18

Number of all-India vehicle registrations fall marginally

although revenue collections rise WoW

Source: vahan.parivahan.gov.in, JM Financial

YoY contraction in daily vehicle registrations lower

in June

Source: vahan.parivahan.gov.in, JM Financial; YoY growth calculated over daily averages

Indicators: Consumption

1 15

1 3

37

3

51 46

3

95

58

4

142

84

5

183

109

6

258

119

7

255

120

8

Vehicle

registrations (in000s)

No. of

transactions (in10, 000s)

Revenue

collections (INRbn)

10-May 17-May 24-May 31-May 07-Jun 14-Jun 21-Jun 28-Jun

-120%

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

May

-16

Jul-

16

Sep

-16

No

v-1

6Ja

n-1

7M

ar-1

7M

ay-1

7Ju

l-1

7Se

p-1

7N

ov-

17

Jan

-18

Mar

-18

May

-18

Jul-

18

Sep

-18

No

v-1

8Ja

n-1

9M

ar-1

9M

ay-1

9Ju

l-1

9Se

p-1

9N

ov-

19

Jan

-20

Mar

-20

May

-20

28

-Ju

n-2

0

PV 2-Wheelers MHCV LCV

Vehicle Registrations (YoY%)

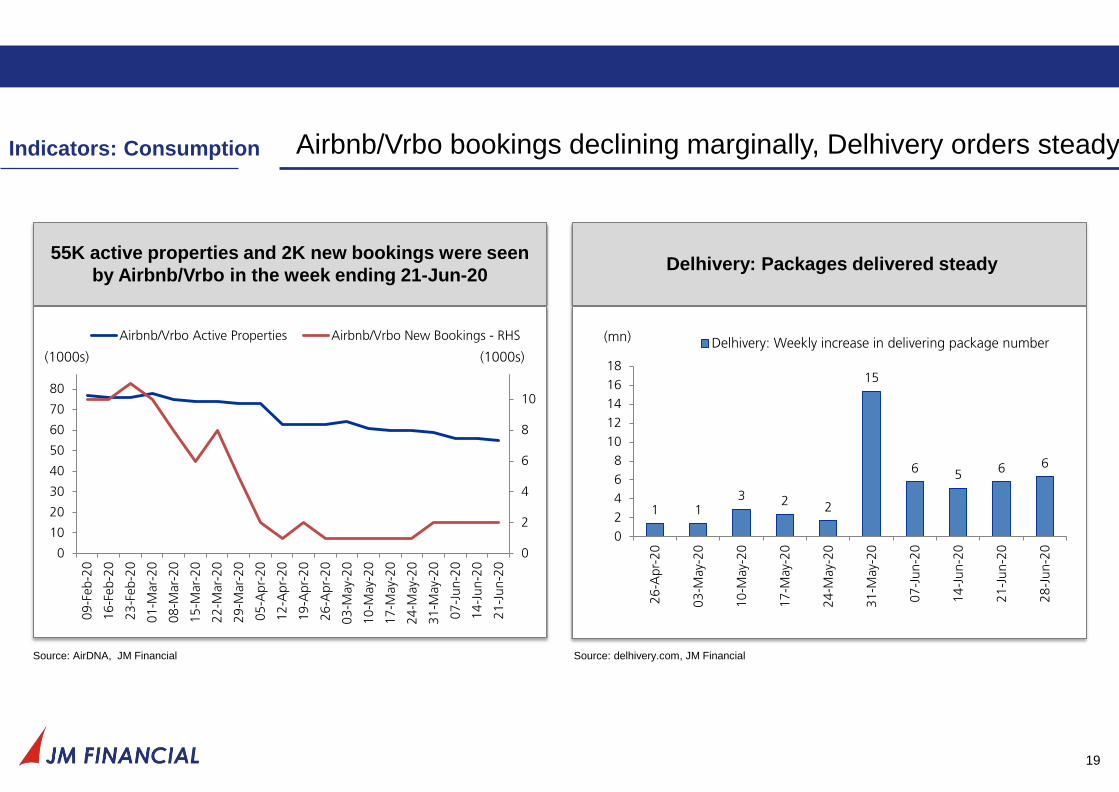

Airbnb/Vrbo bookings declining marginally, Delhivery orders steady

19

55K active properties and 2K new bookings were seen

by Airbnb/Vrbo in the week ending 21-Jun-20

Source: AirDNA, JM Financial

Delhivery: Packages delivered steady

Source: delhivery.com, JM Financial

Indicators: Consumption

0

2

4

6

8

10

12

0

10

20

30

40

50

60

70

80

90

09

-Feb-2

0

16

-Feb-2

0

23

-Feb-2

0

01

-Mar-

20

08

-Mar-

20

15

-Mar-

20

22

-Mar-

20

29

-Mar-

20

05

-Apr-

20

12

-Apr-

20

19

-Apr-

20

26

-Apr-

20

03

-May-

20

10

-May-

20

17

-May-

20

24

-May-

20

31

-May-

20

07

-Ju

n-2

0

14

-Ju

n-2

0

21

-Ju

n-2

0

Airbnb/Vrbo Active Properties Airbnb/Vrbo New Bookings - RHS

(1000s) (1000s)

1 13 2 2

15

65

6 6

0

2

4

6

8

10

12

14

16

18

26

-Apr-

20

03

-May-

20

10

-May-

20

17

-May-

20

24

-May-

20

31

-May-

20

07

-Ju

n-2

0

14

-Ju

n-2

0

21

-Ju

n-2

0

28

-Ju

n-2

0

Delhivery: Weekly increase in delivering package number(mn)

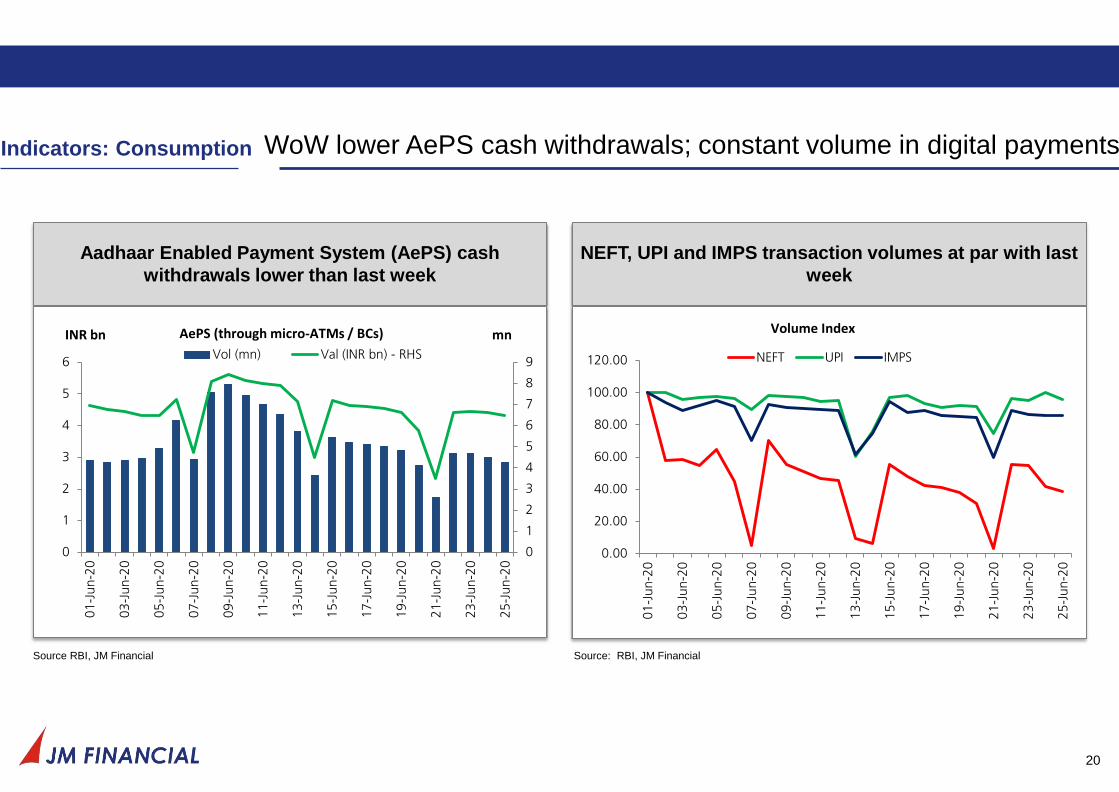

WoW lower AePS cash withdrawals; constant volume in digital payments

20

Aadhaar Enabled Payment System (AePS) cash

withdrawals lower than last week

Source RBI, JM Financial

NEFT, UPI and IMPS transaction volumes at par with last

week

Source: RBI, JM Financial

Indicators: Consumption

0

1

2

3

4

5

6

7

8

9

0

1

2

3

4

5

6

01

-Ju

n-2

0

03

-Ju

n-2

0

05

-Ju

n-2

0

07

-Ju

n-2

0

09

-Ju

n-2

0

11

-Ju

n-2

0

13

-Ju

n-2

0

15

-Ju

n-2

0

17

-Ju

n-2

0

19

-Ju

n-2

0

21

-Ju

n-2

0

23

-Ju

n-2

0

25

-Ju

n-2

0

Vol (mn) Val (INR bn) - RHS

AePS (through micro-ATMs / BCs) mnINR bn

0.00

20.00

40.00

60.00

80.00

100.00

120.00

01

-Ju

n-2

0

03

-Ju

n-2

0

05

-Ju

n-2

0

07

-Ju

n-2

0

09

-Ju

n-2

0

11

-Ju

n-2

0

13

-Ju

n-2

0

15

-Ju

n-2

0

17

-Ju

n-2

0

19

-Ju

n-2

0

21

-Ju

n-2

0

23

-Ju

n-2

0

25

-Ju

n-2

0

NEFT UPI IMPS

Volume Index

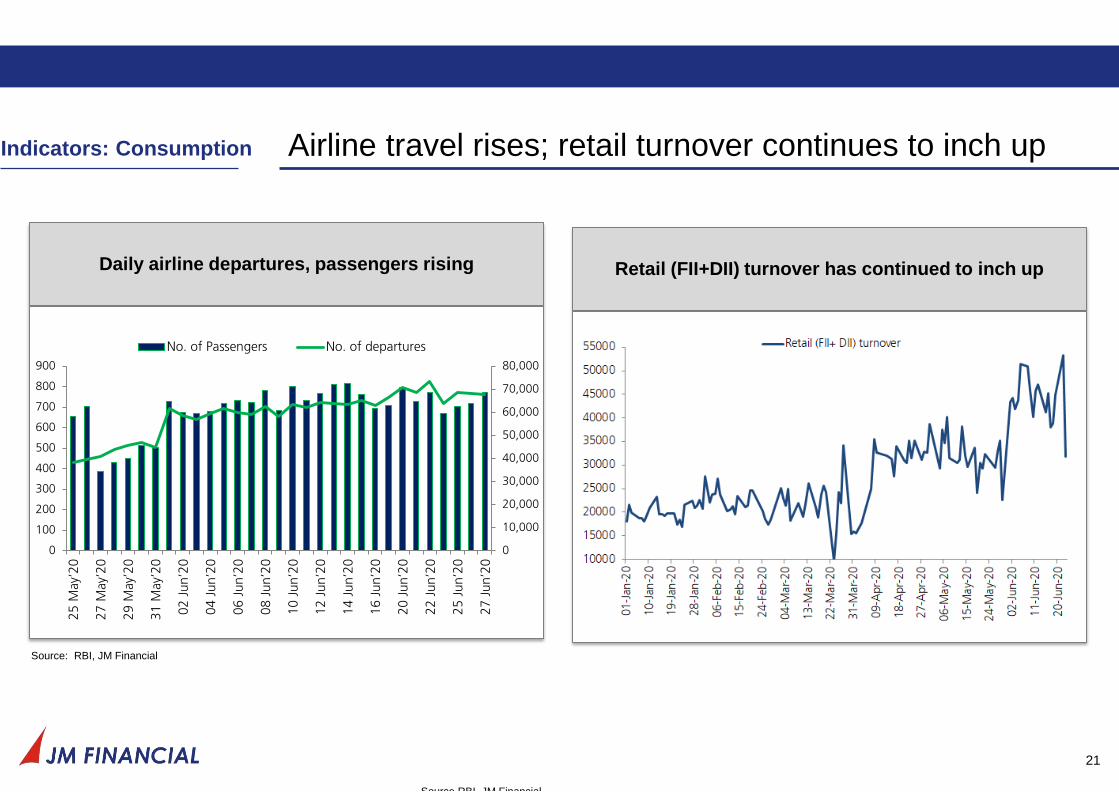

Airline travel rises; retail turnover continues to inch up

21

Retail (FII+DII) turnover has continued to inch up

Source RBI, JM Financial

Daily airline departures, passengers rising

Source: RBI, JM Financial

Indicators: Consumption

0

100

200

300

400

500

600

700

800

900

25 M

ay’

20

27 M

ay’

20

29 M

ay’

20

31 M

ay’

20

02 J

un’2

0

04 J

un’2

0

06 J

un’2

0

08 J

un’2

0

10 J

un’2

0

12 J

un’2

0

14 J

un’2

0

16 J

un’2

0

20 J

un’2

0

22 J

un’2

0

25 J

un’2

0

27 J

un’2

0

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

No. of Passengers No. of departures

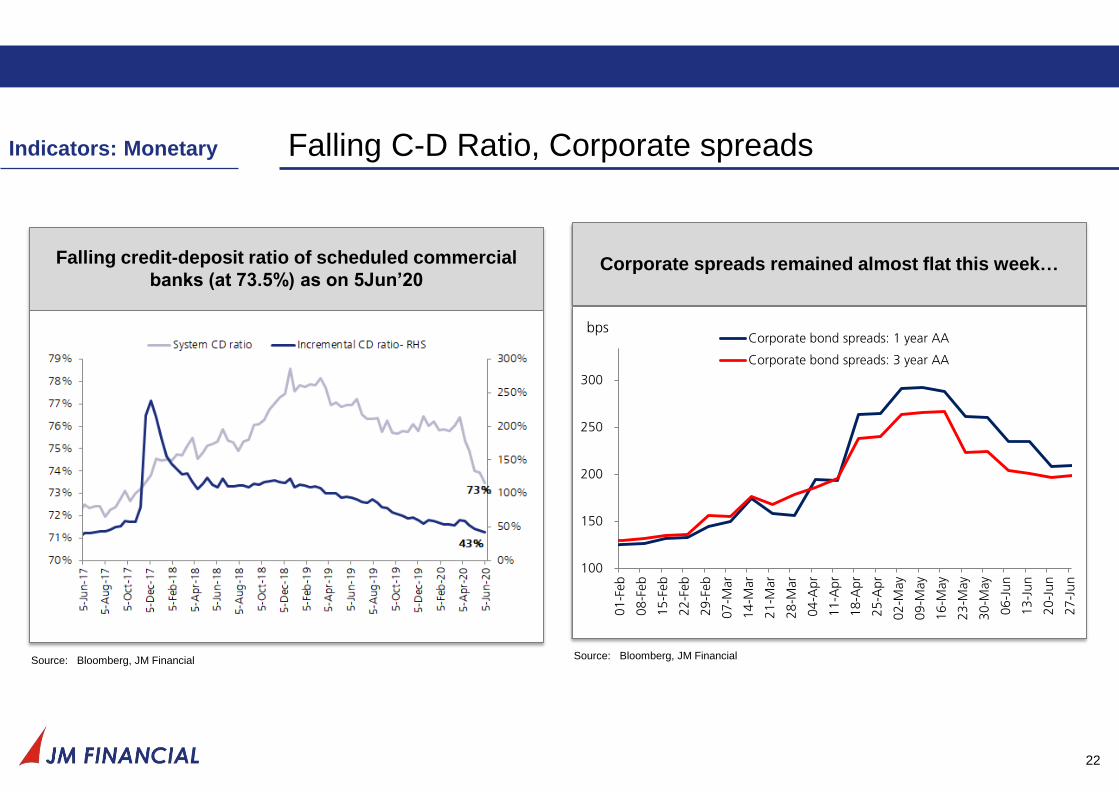

Falling C-D Ratio, Corporate spreads

22

Falling credit-deposit ratio of scheduled commercial

banks (at 73.5%) as on 5Jun’20

Source: Bloomberg, JM Financial

Indicators: Monetary

Corporate spreads remained almost flat this week…

Source: Bloomberg, JM Financial

100

150

200

250

300

350

01

-Feb

08

-Feb

15

-Feb

22

-Feb

29

-Feb

07

-Mar

14

-Mar

21

-Mar

28

-Mar

04

-Apr

11

-Apr

18

-Apr

25

-Apr

02

-May

09

-May

16

-May

23

-May

30

-May

06

-Ju

n

13

-Ju

n

20

-Ju

n

27

-Ju

n

Corporate bond spreads: 1 year AA

Corporate bond spreads: 3 year AA

bps

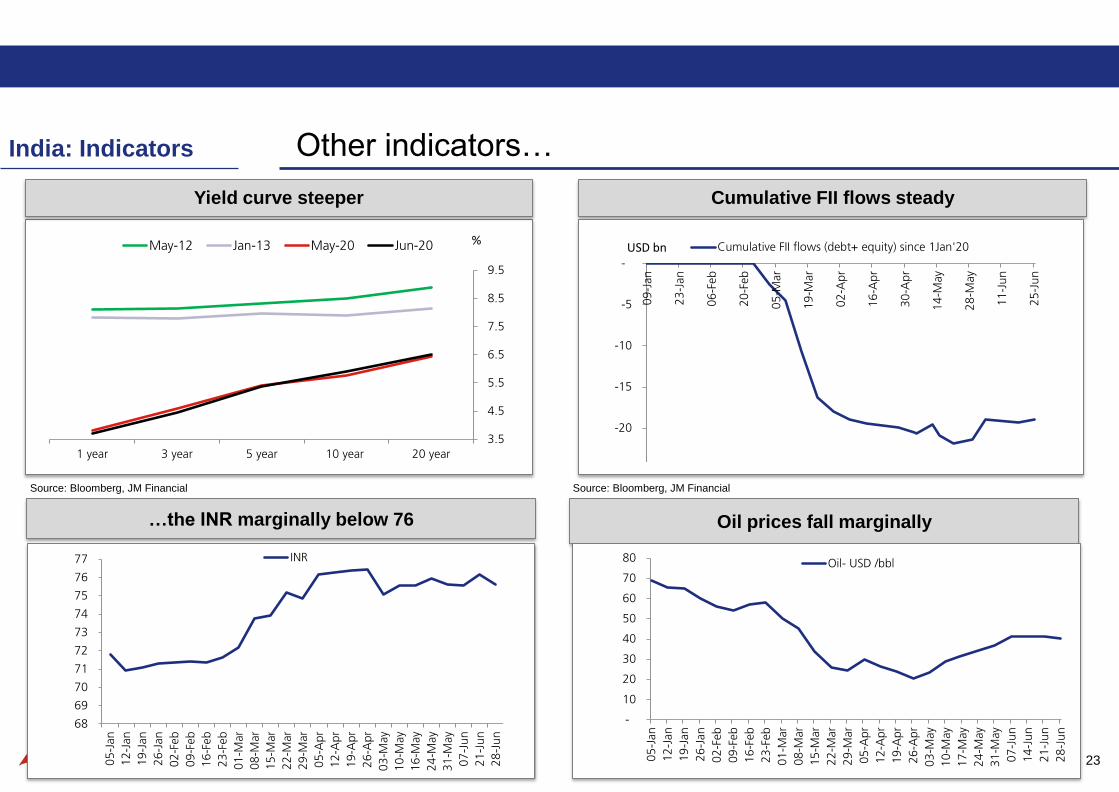

Other indicators…

23

India: Indicators

Oil prices fall marginally …the INR marginally below 76

Source: Bloomberg, JM Financial

Cumulative FII flows steady

Yield curve steeper

Source: Bloomberg, JM Financial

-

10

20

30

40

50

60

70

80

05

-Jan

12

-Jan

19

-Jan

26

-Jan

02

-Feb

09

-Feb

16

-Feb

23

-Feb

01

-Mar

08

-Mar

15

-Mar

22

-Mar

29

-Mar

05

-Apr

12

-Apr

19

-Apr

26

-Apr

03

-May

10

-May

17

-May

24

-May

31

-May

07

-Ju

n

14

-Ju

n

21

-Ju

n

28

-Ju

n

Oil- USD /bbl

68

69

70

71

72

73

74

75

76

77

05

-Jan

12

-Jan

19

-Jan

26

-Jan

02

-Feb

09

-Feb

16

-Feb

23

-Feb

01

-Mar

08

-Mar

15

-Mar

22

-Mar

29

-Mar

05

-Apr

12

-Apr

19

-Apr

26

-Apr

03

-May

10

-May

16

-May

24

-May

31

-May

07

-Ju

n

21

-Ju

n

28

-Ju

n

INR

-25

-20

-15

-10

-5

-

09

-Jan

23

-Jan

06

-Feb

20

-Feb

05

-Mar

19

-Mar

02

-Apr

16

-Apr

30

-Apr

14

-May

28

-May

11

-Ju

n

25

-Ju

n

Cumulative FII flows (debt+ equity) since 1Jan'20USD bn

3.5

4.5

5.5

6.5

7.5

8.5

9.5

20 year10 year5 year3 year1 year

May-12 Jan-13 May-20 Jun-20 %

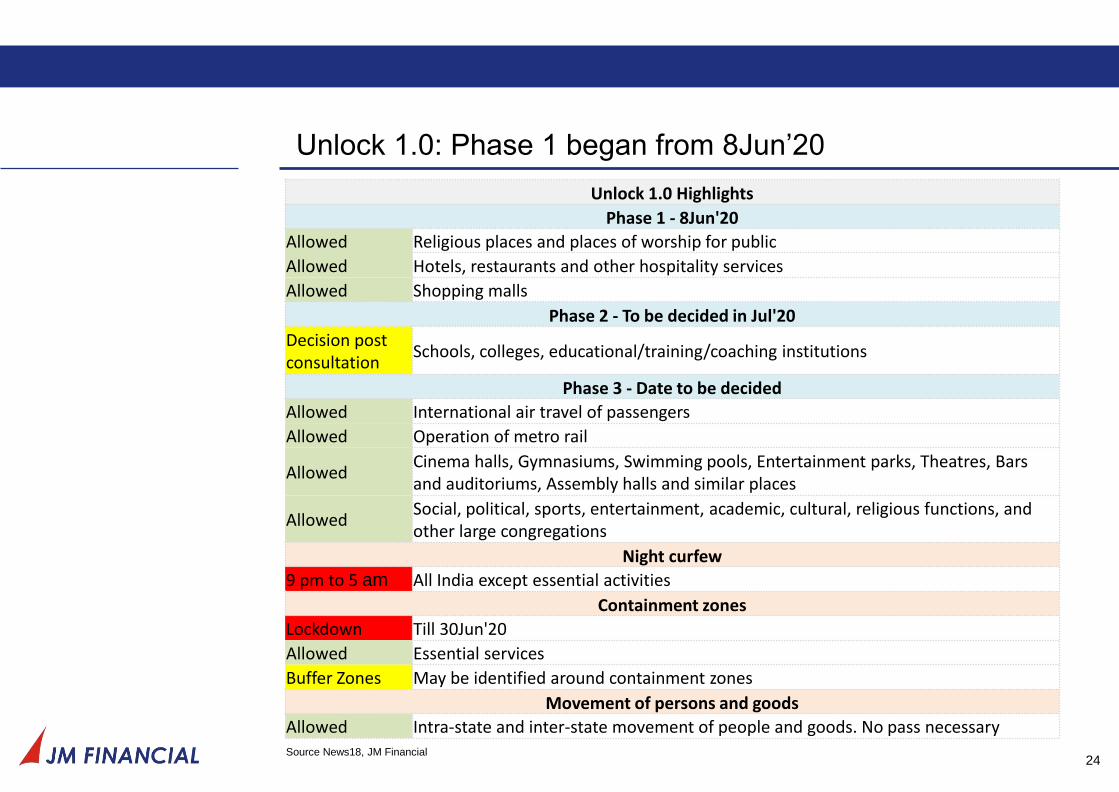

Unlock 1.0: Phase 1 began from 8Jun’20

24

Unlock 1.0 Highlights

Phase 1 - 8Jun'20

Allowed Religious places and places of worship for public

Allowed Hotels, restaurants and other hospitality services

Allowed Shopping malls

Phase 2 - To be decided in Jul'20

Decision post consultation

Schools, colleges, educational/training/coaching institutions

Phase 3 - Date to be decided

Allowed International air travel of passengers

Allowed Operation of metro rail

Allowed Cinema halls, Gymnasiums, Swimming pools, Entertainment parks, Theatres, Bars and auditoriums, Assembly halls and similar places

Allowed Social, political, sports, entertainment, academic, cultural, religious functions, and other large congregations

Night curfew

9 pm to 5 am All India except essential activities

Containment zones

Lockdown Till 30Jun'20

Allowed Essential services

Buffer Zones May be identified around containment zones

Movement of persons and goods

Allowed Intra-state and inter-state movement of people and goods. No pass necessary Source News18, JM Financial

Refer to our other earlier tracker reports

25

• COVID-19 Tracker_21Jun2020

• COVID-19 Tracker_14Jun2020

• COVID-19 Tracker_7Jun2020

• COVID-19 Tracker_31May2020

• COVID-19 Tracker_25May2020

• COVID-19 Tracker_18May2020

• COVID-19 Tracker_14May2020

• COVID-19 Tracker_8May2020

Important Disclosures

This research report has been prepared by JM Financial Institutional Securities Limited (JM Financial Institutional Securities) to provide information about the company(ies) and sector(s), if any, covered

in the report and may be distributed by it and/or its associates solely for the purpose of information of the select recipient of this report. This report and/or any part thereof, may not be duplicated in any

form and/or reproduced or redistributed without the prior written consent of JM Financial Institutional Securities. This report has been prepared independent of the companies covered herein.

JM Financial Institutional Securities is registered with the Securities and Exchange Board of India (SEBI) as a Research Analyst and a Stock Broker having trading memberships of the BSE Ltd. (BSE),

National Stock Exchange of India Ltd. (NSE) and Metropolitan Stock Exchange of India Ltd. (MSEI). No material disciplinary action has been taken by SEBI against JM Financial Institutional Securities in

the past two financial years which may impact the investment decision making of the investor.

JM Financial Institutional Securities renders stock broking services primarily to institutional investors and provides the research services to its institutional clients/investors. JM Financial Institutional

Securities and its associates are part of a multi-service, integrated investment banking, investment management, brokerage and financing group. JM Financial Institutional Securities and/or its associates

might have provided or may provide services in respect of managing offerings of securities, corporate finance, investment banking, mergers & acquisitions, broking, financing or any other advisory

services to the company(ies) covered herein. JM Financial Institutional Securities and/or its associates might have received during the past twelve months or may receive compensation from the

company(ies) mentioned in this report for rendering any of the above services.

JM Financial Institutional Securities and/or its associates, their directors and employees may; (a) from time to time, have a long or short position in, and buy or sell the securities of the company(ies)

mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies)

covered under this report or (c) act as an advisor or lender/borrower to, or may have any financial interest in, such company(ies) or (d) considering the nature of business/activities that JM Financial

Institutional Securities is engaged in, it may have potential conflict of interest at the time of publication of this report on the subject company(ies).

Neither JM Financial Institutional Securities nor its associates or the Research Analyst(s) named in this report or his/her relatives individually own one per cent or more securities of the company(ies)

covered under this report, at the relevant date as specified in the SEBI (Research Analysts) Regulations, 2014.

The Research Analyst(s) principally responsible for the preparation of this research report and members of their household are prohibited from buying or selling debt or equity securities, including but not

limited to any option, right, warrant, future, long or short position issued by company(ies) covered under this report. The Research Analyst(s) principally responsible for the preparation of this research

report or their relatives (as defined under SEBI (Research Analysts) Regulations, 2014); (a) do not have any financial interest in the company(ies) covered under this report or (b) did not receive any

compensation from the company(ies) covered under this report, or from any third party, in connection with this report or (c) do not have any other material conflict of interest at the time of publication of

this report. Research Analyst(s) are not serving as an officer, director or employee of the company(ies) covered under this report.

Research Analyst(s) Certification The Research Analyst(s), with respect to each issuer and its securities covered by them in this research report, certify that:

All of the views expressed in this research report accurately reflect his or her or their personal views about all of the issuers and their securities; and

No part of his or her or their compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed in this research report.

Definition of ratings

Rating Meaning

Buy Total expected returns of more than 15%. Total expected return includes dividend yields.

Hold Price expected to move in the range of 10% downside to 15% upside from the current market price.

Sell Price expected to move downwards by more than 10%

JM Financial Institutional Securities Limited

Corporate Identity Number: U67100MH2017PLC296081

Member of BSE Ltd., National Stock Exchange of India Ltd. and Metropolitan Stock Exchange of India Ltd.

SEBI Registration Nos.: –Stock Broker - INZ000163434, Research Analyst – INH000000610

Registered Office: 7th Floor, Cnergy, Appasaheb Marathe Marg, Prabhadevi, Mumbai 400 025, India.

Board: +9122 6630 3030 | Fax: +91 22 6630 3488 | Email: [email protected] | www.jmfl.com

Compliance Officer: Mr. Sunny Shah | Tel: +91 22 6630 3383 | Email: [email protected]

26

While reasonable care has been taken in the preparation of this report, it does not purport to be a complete description of the securities, markets or developments referred to herein, and JM Financial Institutional Securities does

not warrant its accuracy or completeness. JM Financial Institutional Securities may not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in

this report. This report is provided for information only and is not an investment advice and must not alone be taken as the basis for an investment decision. The investment discussed or views expressed or

recommendations/opinions given herein may not be suitable for all investors. The user assumes the entire risk of any use made of this information. The information contained herein may be changed without notice and JM

Financial Institutional Securities reserves the right to make modifications and alterations to this statement as they may deem fit from time to time.

This report is neither an offer nor solicitation of an offer to buy and/or sell any securities mentioned herein and/or not an official confirmation of any transaction.

This report is not directed or intended for distribution to, or use by any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or

use would be contrary to law, regulation or which would subject JM Financial Institutional Securities and/or its affiliated company(ies) to any registration or licensing requirement within such jurisdiction. The securities described

herein may or may not be eligible for sale in all jurisdictions or to a certain category of investors. Persons in whose possession this report may come, are required to inform themselves of and to observe such restrictions.

Persons who receive this report from JM Financial Singapore Pte Ltd may contact Mr. Ruchir Jhunjhunwala ([email protected]) on +65 6422 1888 in respect of any matters arising from, or in connection with, this

report.

Additional disclosure only for U.S. persons: JM Financial Institutional Securities has entered into an agreement with JM Financial Securities, Inc. ("JM Financial Securities"), a U.S. registered broker-dealer and member of the

Financial Industry Regulatory Authority ("FINRA") in order to conduct certain business in the United States in reliance on the exemption from U.S. broker-dealer registration provided by Rule 15a-6, promulgated under the U.S.

Securities Exchange Act of 1934 (the "Exchange Act"), as amended, and as interpreted by the staff of the U.S. Securities and Exchange Commission ("SEC") (together "Rule 15a-6").

This research report is distributed in the United States by JM Financial Securities in compliance with Rule 15a-6, and as a "third party research report" for purposes of FINRA Rule 2241. In compliance with Rule 15a-6(a)(3) this

research report is distributed only to "major U.S. institutional investors" as defined in Rule 15a-6 and is not intended for use by any person or entity that is not a major U.S. institutional investor. If you have received a copy of this

research report and are not a major U.S. institutional investor, you are instructed not to read, rely on, or reproduce the contents hereof, and to destroy this research or return it to JM Financial Institutional Securities or to JM

Financial Securities.

This research report is a product of JM Financial Institutional Securities, which is the employer of the research analyst(s) solely responsible for its content. The research analyst(s) preparing this research report is/are resident

outside the United States and are not associated persons or employees of any U.S. registered broker-dealer. Therefore, the analyst(s) are not subject to supervision by a U.S. broker-dealer, or otherwise required to satisfy the

regulatory licensing requirements of FINRA and may not be subject to the Rule 2241 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

JM Financial Institutional Securities only accepts orders from major U.S. institutional investors. Pursuant to its agreement with JM Financial Institutional Securities, JM Financial Securities effects the transactions for major U.S.

institutional investors. Major U.S. institutional investors may place orders with JM Financial Institutional Securities directly, or through JM Financial Securities, in the securities discussed in this research report.

Additional disclosure only for U.K. persons: Neither JM Financial Institutional Securities nor any of its affiliates is authorised in the United Kingdom (U.K.) by the Financial Conduct Authority. As a result, this report is for

distribution only to persons who (i) have professional experience in matters relating to investments falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (as amended, the

"Financial Promotion Order"), (ii) are persons falling within Article 49(2)(a) to (d) ("high net worth companies, unincorporated associations etc.") of the Financial Promotion Order, (iii) are outside the United Kingdom, or (iv) are

persons to whom an invitation or inducement to engage in investment activity (within the meaning of section 21 of the Financial Services and Markets Act 2000) in connection with the matters to which this report relates may

otherwise lawfully be communicated or caused to be communicated (all such persons together being referred to as "relevant persons"). This report is directed only at relevant persons and must not be acted on or relied on by

persons who are not relevant persons. Any investment or investment activity to which this report relates is available only to relevant persons and will be engaged in only with relevant persons.

Additional disclosure only for Canadian persons: This report is not, and under no circumstances is to be construed as, an advertisement or a public offering of the securities described herein in Canada or any province or territory

thereof. Under no circumstances is this report to be construed as an offer to sell securities or as a solicitation of an offer to buy securities in any jurisdiction of Canada. Any offer or sale of the securities described herein in

Canada will be made only under an exemption from the requirements to file a prospectus with the relevant Canadian securities regulators and only by a dealer properly registered under applicable securities laws or, alternatively,

pursuant to an exemption from the registration requirement in the relevant province or territory of Canada in which such offer or sale is made. This report is not, and under no circumstances is it to be construed as, a prospectus

or an offering memorandum. No securities commission or similar regulatory authority in Canada has reviewed or in any way passed upon these materials, the information contained herein or the merits of the securities described

herein and any representation to the contrary is an offence. If you are located in Canada, this report has been made available to you based on your representation that you are an “accredited investor” as such term is defined in

National Instrument 45-106 Prospectus Exemptions and a “permitted client” as such term is defined in National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations. Under no

circumstances is the information contained herein to be construed as investment advice in any province or territory of Canada nor should it be construed as being tailored to the needs of the recipient. Canadian recipients are

advised that JM Financial Securities, Inc., JM Financial Institutional Securities Limited, their affiliates and authorized agents are not responsible for, nor do they accept, any liability whatsoever for any direct or consequential loss

arising from any use of this research report or the information contained herein.

27