longevity risk and reward for middle-income americans

TRANSCRIPT

Longevity Risk and Reward for Middle-Income Americans

By Bankers Life and Casualty Company Center for a Secure Retirement

March 2013

Table of Contents

2 Introduction

3 Methodology

4 Key Findings

6 Self-Perceptions on Longevity

12 Longevity Planning Actions and Attitudes

19 Social Security Reliance and Understanding

26 Recommendations for Consumers

27 About the Center for a Secure Retirement

2Longevity Risk and Reward for Middle-Income Americans | March 2013

Today, the average 65-year-old has an average life expectancy of 19 more years— approximately age 84. In fact, one out of every four 65-year-olds will live past age 90, and one out of ten will live past age 95.1

Living longer has its rewards. Middle-income retirees say they are having experiences in retirement that they never imagined, such as travel, volunteering and community involvement.2

However, longevity also comes with risk, the two primary concerns being declining health that is associated with age, and the ability to create a sustainable retirement income that may need to last 20 years or more.

More than half of middle-income Boomers (55%) have saved less than $100,000 for retirement. One-fifth (19%) have saved less than $10,000.3 For this reason, it is not surprising that three out of four (75%) middle-income Boomers expect to work in retirement.4

Yet, simply working longer is not the answer to the longevity risk question. Retirees must consider that even if they take steps to maintain their health, an accident or illness may prevent them from working full-time or even part-time in their later years.

No one can predict exactly how long they will live. That said, realistically assessing longevity can be a powerful tool in planning for retirement.

It can help retirees plan for income and future expenses, decide when to start taking Social Security, make choices for healthcare and long-term care, and even prioritize retirement goals.

With the release of Longevity Risk and Reward for Middle-Income Americans, the Bankers Life and Casualty Company Center for a Secure Retirement looks at longevity’s impact on the retirement experience of retirees and pre-retirees with middle incomes.

We seek to gauge their perspectives on life expectancy, the factors that contribute to it, and the risk longevity has on retirement income. Finally, we look at Social Security, middle-income attitudes toward this institution, their understanding of program benefits, and the role it plays as the cornerstone of retirement income for middle-income Americans.

Introduction

3Longevity Risk and Reward for Middle-Income Americans | March 2013

Methodology

The Bankers Life and Casualty Company Center for a Secure Retirement’s study Longevity Risk and Reward for Middle-Income Americans was conducted in November 2012 by the independent research firm The Boomer Project.

A nationwide sample of 500 Americans ages 55 to 75 who have an annual household income of between $25,000 and $75,000 participated in the Internet-based survey.

Responses were weighted to match U.S. Census data on the selected age segment. The margin of error was 4.47 percentage points at the 90% confidence level.

4Longevity Risk and Reward for Middle-Income Americans | March 2013

Key Findings

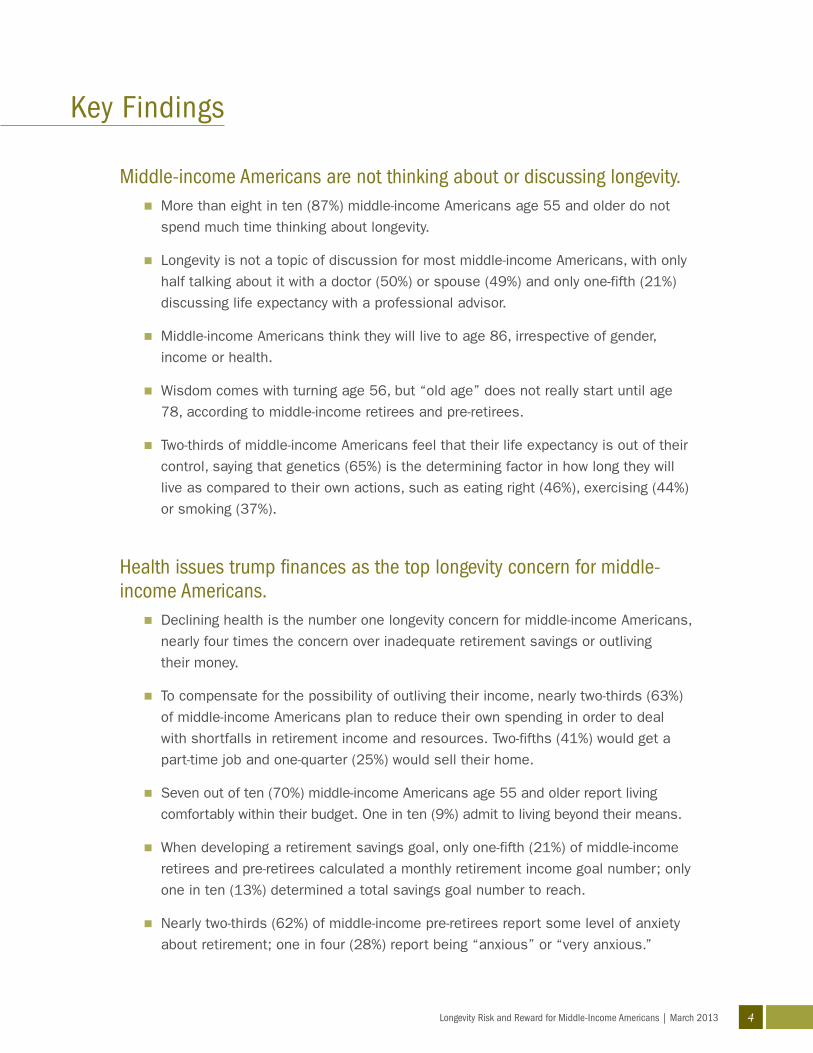

Middle-income Americans are not thinking about or discussing longevity.n More than eight in ten (87%) middle-income Americans age 55 and older do not

spend much time thinking about longevity.

n Longevity is not a topic of discussion for most middle-income Americans, with only

half talking about it with a doctor (50%) or spouse (49%) and only one-fifth (21%)

discussing life expectancy with a professional advisor.

n Middle-income Americans think they will live to age 86, irrespective of gender,

income or health.

n Wisdom comes with turning age 56, but “old age” does not really start until age

78, according to middle-income retirees and pre-retirees.

n Two-thirds of middle-income Americans feel that their life expectancy is out of their

control, saying that genetics (65%) is the determining factor in how long they will

live as compared to their own actions, such as eating right (46%), exercising (44%)

or smoking (37%).

Health issues trump finances as the top longevity concern for middle-income Americans.

n Declining health is the number one longevity concern for middle-income Americans,

nearly four times the concern over inadequate retirement savings or outliving

their money.

n To compensate for the possibility of outliving their income, nearly two-thirds (63%)

of middle-income Americans plan to reduce their own spending in order to deal

with shortfalls in retirement income and resources. Two-fifths (41%) would get a

part-time job and one-quarter (25%) would sell their home.

n Seven out of ten (70%) middle-income Americans age 55 and older report living

comfortably within their budget. One in ten (9%) admit to living beyond their means.

n When developing a retirement savings goal, only one-fifth (21%) of middle-income

retirees and pre-retirees calculated a monthly retirement income goal number; only

one in ten (13%) determined a total savings goal number to reach.

n Nearly two-thirds (62%) of middle-income pre-retirees report some level of anxiety

about retirement; one in four (28%) report being “anxious” or “very anxious.”

5Longevity Risk and Reward for Middle-Income Americans | March 2013

Middle-income Americans rely heavily on Social Security to fund their retirement; however, there are gaps in understanding how it works.

n Nearly three-fourths (72%) of middle-income Americans say that Social Security

benefits make up at least half or more of their retirement income, which exceeds the

national average of 65%, according to the Social Security Administration.

n Nearly one out of three (29%) count on Social Security for 75% or more of their

retirement income.

n For retirees with household incomes between $25,000 and $50,000, one in ten

(10%) rely on Social Security for all of their retirement income.

n One in three (34%) of those age 55 and older do not understand that delaying

when they start to collect Social Security can increase their future benefit amount.

n Nearly half (47%) of middle-income Americans age 55 and older incorrectly believe

that an annual cost-of-living increase to their Social Security benefits is guaranteed.

n More than one-third (36%) of middle-income Americans falsely believe that full

Social Security benefits start with their 65th birthday.

n One in three (35%) middle-income Americans age 55 and older who are not yet

receiving Social Security do not know what their Social Security income will be

when they retire.

n Nearly eight in ten (78%) middle-income Americans age 55 and older are concerned

about the future of Social Security.

n More than one-third (38%) of middle-income Americans over age 55 do not believe

Social Security as we know it will exist in 20 years.

6Longevity Risk and Reward for Middle-Income Americans | March 2013

Self-Perceptions on Longevity

Longevity can be a difficult topic to discuss and address. No one can ever know

exactly how long they will live, or in terms of retirement planning, how many

years they will have to support themselves with retirement income after they

stop working.

In the busy lives of middle-income Americans, the idea of one’s own longevity is

not a topic of much contemplation or discussion. More than eight in ten (87%)

middle-income Americans age 55 and older do not spend much time thinking

about longevity. One in ten (13%) think “frequently” or “all of the time” about how

long they will live.

However, considering longevity and the risks of outliving retirement savings is a

first step in developing and achieving health, income and even personal goals for

a satisfying retirement.

7Longevity Risk and Reward for Middle-Income Americans | March 2013

Link Between Health and Future Outlook

Self-Reported Health Status All Respondents

Good Poor

My best years are ahead of me 68% 46% 60%

My best years are behind me 32% 54% 40%

Source: Bankers Life and Casualty Company Center for a Secure Retirement, Longevity Risk and Reward for Middle-Income Americans, 2013.

n=500

Six in Ten Optimistic About FutureWhen asked if their best years are

ahead or behind them, the majority of

middle-income retirees and pre-retirees

are optimistic about the future. Six in

ten (60%) middle-income Americans age

55 and older say their best years are

ahead of them.

Respondents whose best years are

ahead of them attribute this to their

positive attitude or outlook on life and

freedom from work.

For the two-fifths (40%) of respondents

that report that their best years are

behind them, they mention the realities

of aging, their health and an overall

negative outlook as the primary reasons.

8Longevity Risk and Reward for Middle-Income Americans | March 2013

Most Not Discussing LongevityMiddle-income Americans do not feel

compelled to discuss their longevity with

family or professionals.

Only half talk about it with a doctor

(50%) or spouse (49%) and only one-

fifth (21%) discuss life expectancy with

a professional advisor. One in seven

(15%) do not discuss with anyone how

long they may live.

9Longevity Risk and Reward for Middle-Income Americans | March 2013

86 Is the Average Life ExpectancyDespite their reluctance to discuss

longevity, those surveyed accurately

estimated average life expectancy for

American adults. On average, respondents

with a median age of 65 tell us they think

they will live to age 86.

This assessment is in line with current

statistics from the Centers for Disease

Control and Prevention (CDC) that report

the life expectancy of Americans age 65

to be 19.2 years, or age 84.5

Survey respondents did not indicate in

their responses that gender, income or

health would affect longevity. However, the

CDC reports that women, on average, have

a life expectancy that is two and a half

years longer than men at age 65 (17.6

years for men and 20.3 years for women).6

Averages aside, it is important to note

that one out of every four 65-year-olds

today will live past age 90, and one out

of ten will live past age 95.7

Perceived Life Expectancy

Men Women

Middle-Income Americans 86 86

CDC National Average 83 85

Source: Bankers Life and Casualty Company Center for a Secure Retirement, Longevity Risk and Reward for Middle-Income Americans, 2013 and Centers for Disease Control and Prevention, 2011.

n=500

10Longevity Risk and Reward for Middle-Income Americans | March 2013

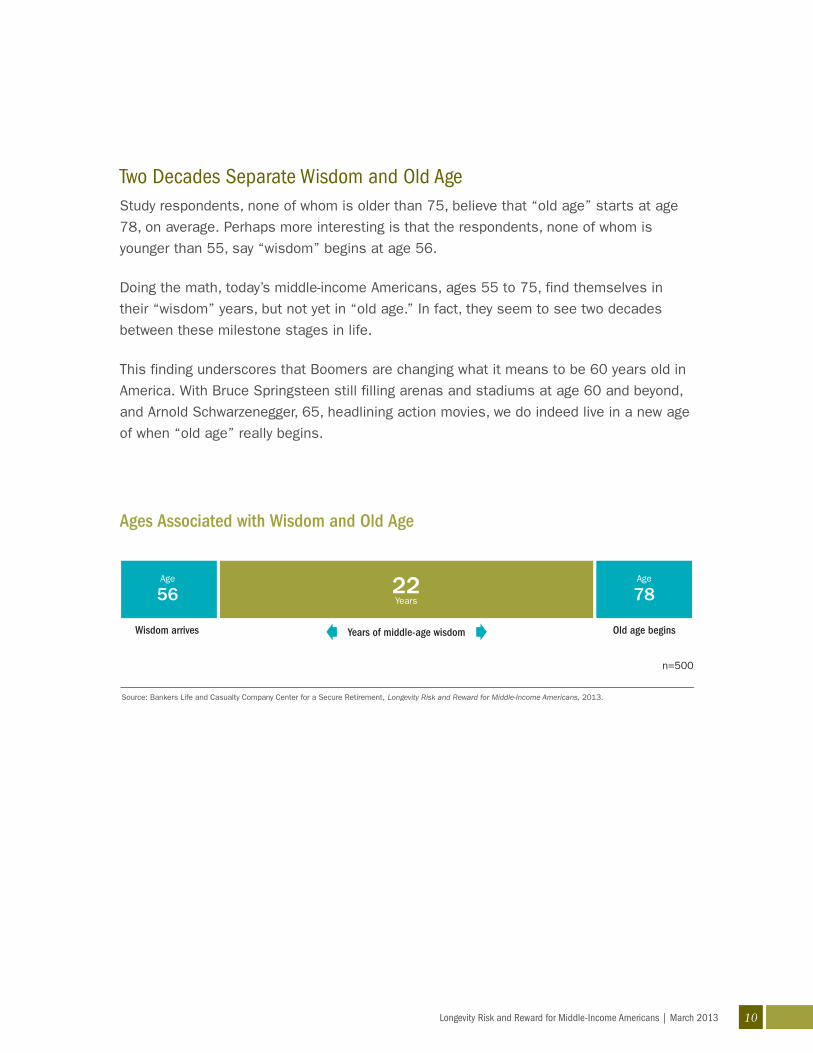

Two Decades Separate Wisdom and Old AgeStudy respondents, none of whom is older than 75, believe that “old age” starts at age

78, on average. Perhaps more interesting is that the respondents, none of whom is

younger than 55, say “wisdom” begins at age 56.

Doing the math, today’s middle-income Americans, ages 55 to 75, find themselves in

their “wisdom” years, but not yet in “old age.” In fact, they seem to see two decades

between these milestone stages in life.

This finding underscores that Boomers are changing what it means to be 60 years old in

America. With Bruce Springsteen still filling arenas and stadiums at age 60 and beyond,

and Arnold Schwarzenegger, 65, headlining action movies, we do indeed live in a new age

of when “old age” really begins.

11Longevity Risk and Reward for Middle-Income Americans | March 2013

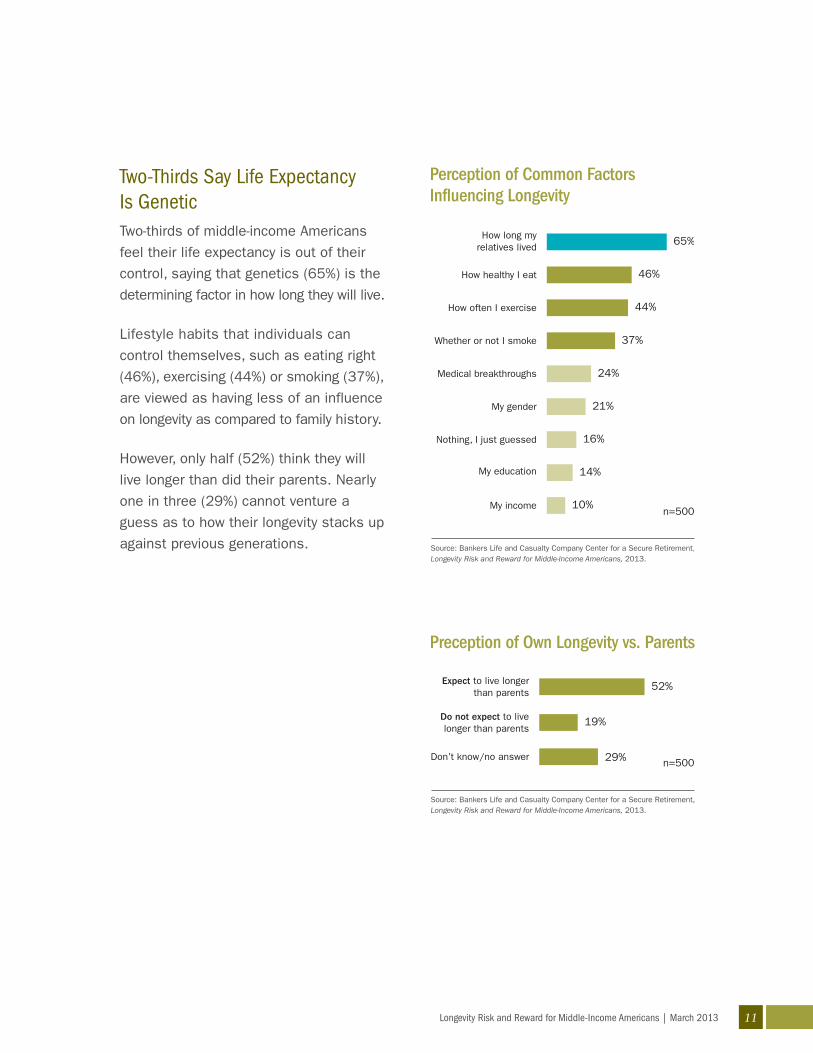

Two-Thirds Say Life Expectancy Is GeneticTwo-thirds of middle-income Americans

feel their life expectancy is out of their

control, saying that genetics (65%) is the

determining factor in how long they will live.

Lifestyle habits that individuals can

control themselves, such as eating right

(46%), exercising (44%) or smoking (37%),

are viewed as having less of an influence

on longevity as compared to family history.

However, only half (52%) think they will

live longer than did their parents. Nearly

one in three (29%) cannot venture a

guess as to how their longevity stacks up

against previous generations.

12Longevity Risk and Reward for Middle-Income Americans | March 2013

Longevity Planning Actions and Attitudes

Middle-income Americans understand that they will likely live into their 80s and

most feel that longevity is out of their control. Furthermore, those surveyed show

a greater concern for the health implications of long life over the challenge of

making income last 20 years or more in retirement.

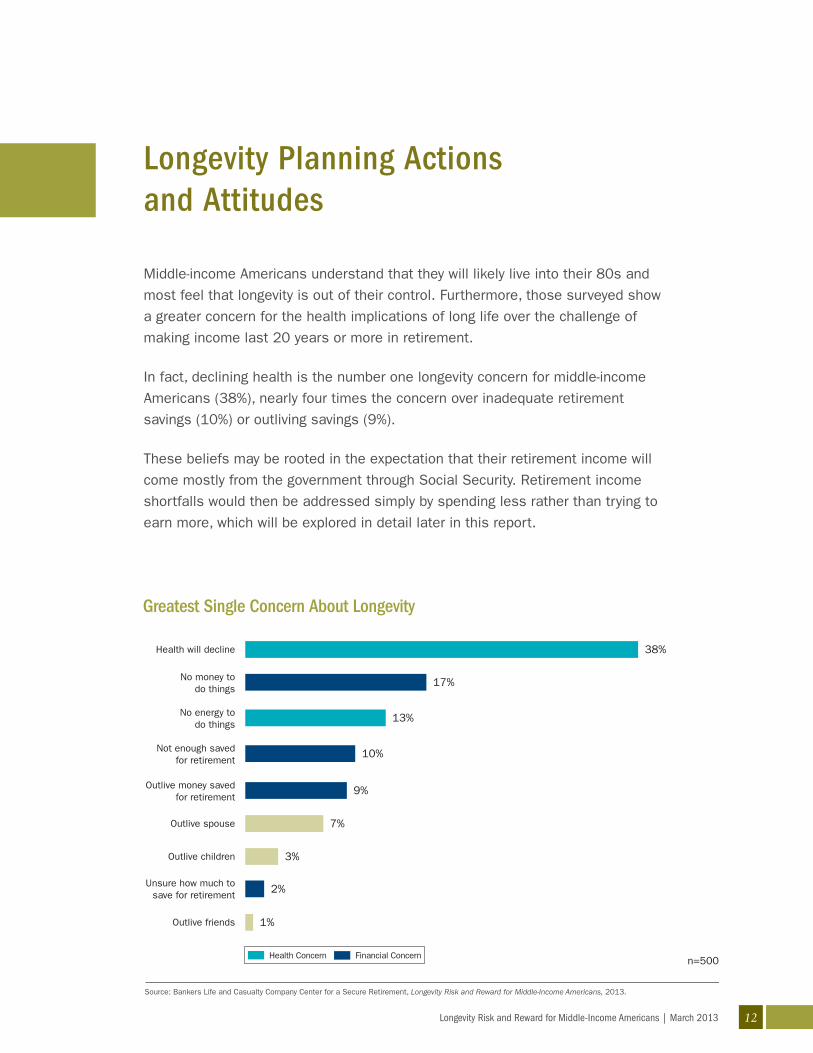

In fact, declining health is the number one longevity concern for middle-income

Americans (38%), nearly four times the concern over inadequate retirement

savings (10%) or outliving savings (9%).

These beliefs may be rooted in the expectation that their retirement income will

come mostly from the government through Social Security. Retirement income

shortfalls would then be addressed simply by spending less rather than trying to

earn more, which will be explored in detail later in this report.

13Longevity Risk and Reward for Middle-Income Americans | March 2013

Health, Not Income, Tops Longevity ConcernsComparing all longevity risk, half (57%) of middle middle-income Americans age 55 and

older are concerned about declining health, followed by a lack of money to do things in

retirement (47%), lack of energy (46%) and outliving their savings (44%).

Outliving a spouse was a worry for just more than one-quarter (28%) of those surveyed.

Less than one-fifth rank outliving friends (19%) or children (16%) among their top concerns

about living longer.

14Longevity Risk and Reward for Middle-Income Americans | March 2013

Two-Thirds Will Buy Less if an Income ShortfallTo compensate for the possibility of

outliving their income, nearly two-thirds of

middle-income Americans plan to reduce

their own spending (63%) in order to deal

with shortfalls in retirement income and

resources. Two-fifths (41%) would get a

part-time job.

One-quarter would donate less to charity

(26%), sell their home (25%) or give less

money to children and grandchildren (24%)

if they outlive their retirement savings.

One in seven (15%) report simply that

they would not do anything if they ran out

of money in retirement.

15Longevity Risk and Reward for Middle-Income Americans | March 2013

Most Living Within BudgetSeven out of ten (70%) middle-income

Americans age 55 and older report living

comfortably within their budget. One in ten

(9%) admit to living beyond their means.

Nearly one-fifth (18%) of those surveyed

report living frugally, below their means.

16Longevity Risk and Reward for Middle-Income Americans | March 2013

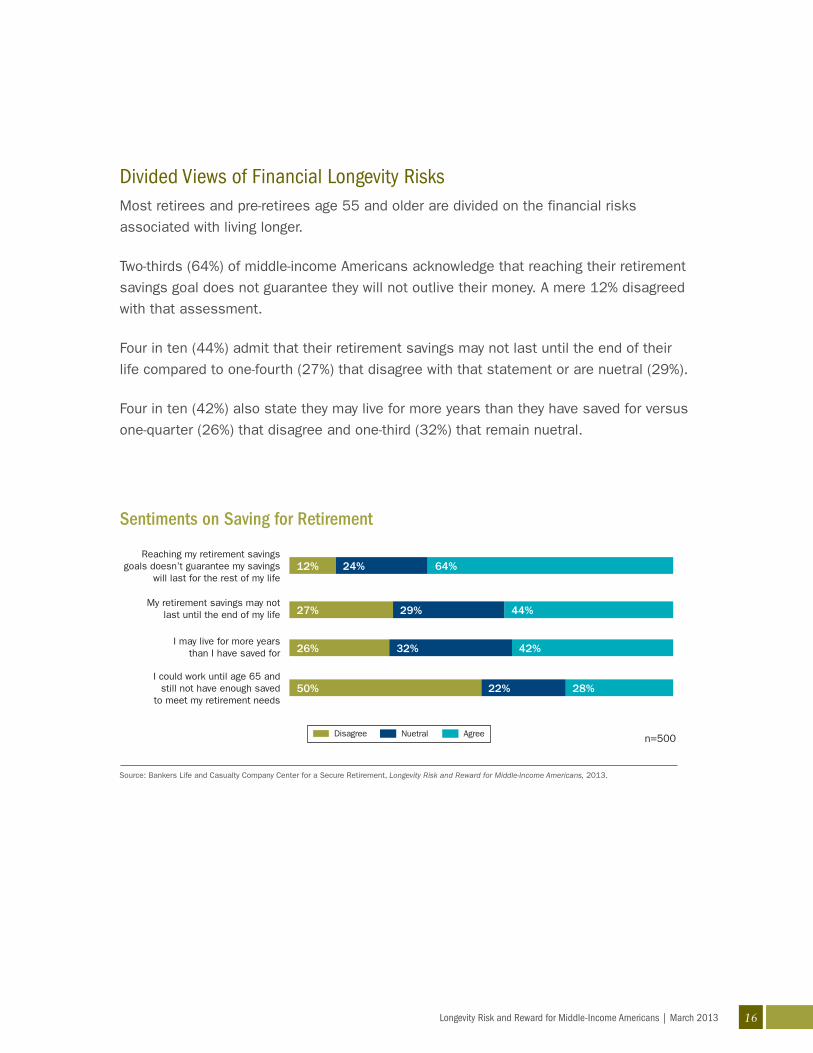

Divided Views of Financial Longevity Risks Most retirees and pre-retirees age 55 and older are divided on the financial risks

associated with living longer.

Two-thirds (64%) of middle-income Americans acknowledge that reaching their retirement

savings goal does not guarantee they will not outlive their money. A mere 12% disagreed

with that assessment.

Four in ten (44%) admit that their retirement savings may not last until the end of their

life compared to one-fourth (27%) that disagree with that statement or are nuetral (29%).

Four in ten (42%) also state they may live for more years than they have saved for versus

one-quarter (26%) that disagree and one-third (32%) that remain nuetral.

17Longevity Risk and Reward for Middle-Income Americans | March 2013

No Significant Use of Common Planning MethodsThe vast majority of middle-income Americans are not using any of the three most

common approaches for calculating retirement savings goals. Only one-fifth (21%) of

middle-income retirees and pre-retirees calculated a monthly income goal number and

only one in ten (13%) determined a total savings goal number to reach. Less than one-

fourth (22%) used the method of finding their optimal retirement income by using a

percentage of their pre-retirement income as a guideline.

Consistent with prior research conducted by the Center for a Secure Retirement, most

middle-income Americans procrastinate retirement planning or follow a do-it-yourself

approach.8 In fact, middle-income Americans choose planning on their own 2 to 1 over

the three most common methods of income goal planning referenced above (38% versus

21%, 13% and 22% respectively).

Method Used All Retired Not Retired

Calculated a total retirement savings number 13% 12% 15%

Calculated a monthly retirement income number 21% 20% 23%

Used % of pre-retirement income as a guideline 22% 22% 22%

Planned on my own 38% 41% 32%

Did not plan/have not started 28% 27% 30%

Other 11% 12% 10%

n=500 n=300 n=200

Source: Bankers Life and Casualty Company Center for a Secure Retirement, Longevity Risk and Reward for Middle-Income Americans, 2013.

Planning Methods for Determining Retirement Savings Goal

18Longevity Risk and Reward for Middle-Income Americans | March 2013

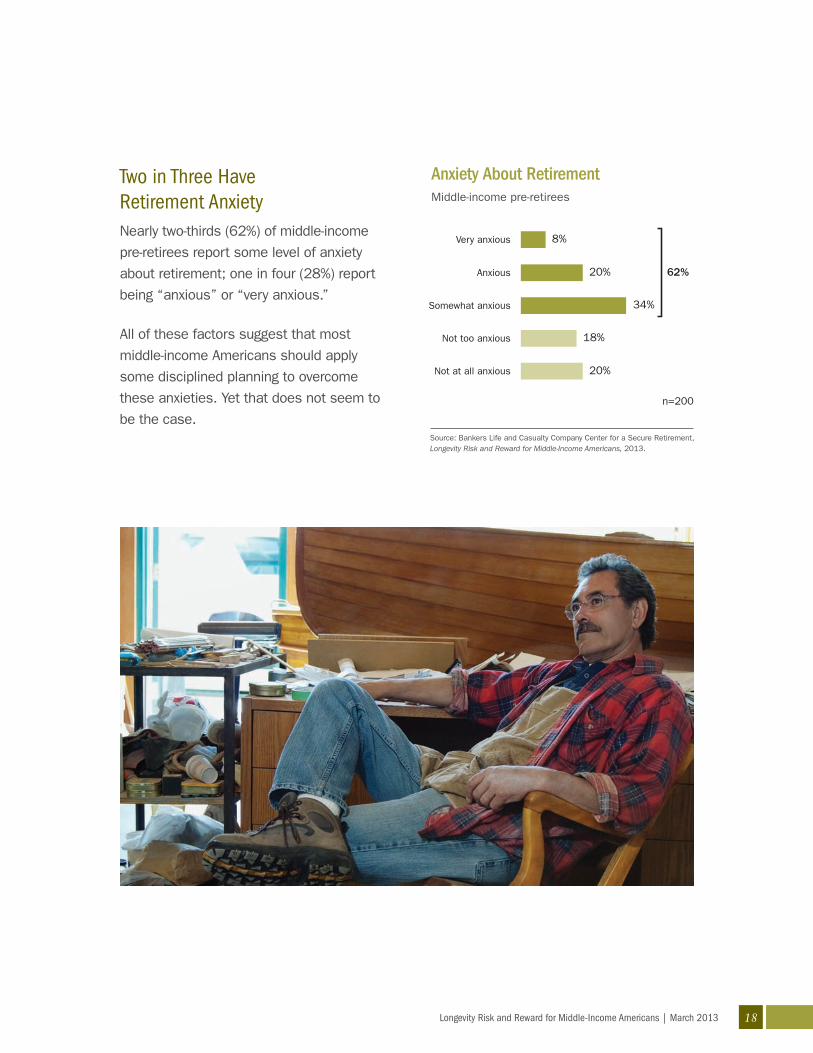

Two in Three Have Retirement Anxiety Nearly two-thirds (62%) of middle-income

pre-retirees report some level of anxiety

about retirement; one in four (28%) report

being “anxious” or “very anxious.”

All of these factors suggest that most

middle-income Americans should apply

some disciplined planning to overcome

these anxieties. Yet that does not seem to

be the case.

19Longevity Risk and Reward for Middle-Income Americans | March 2013

Social Security Reliance and Understanding

The percentage of Americans age 65 and older receiving Social Security benefits

has increased from 69% in 1962 to 89% in 2010, according to the Social Security

Administration (SSA).9 Surprisingly, the number of Americans drawing income from

personal sources of retirement savings, for the same time period adjusted for

inflation, has remained relatively flat—54% in 1962 versus 52% in 2010.10

Today, Social Security benefits are part of the retirement income plan for eight in ten

(84%) middle-income Americans.

However, middle-income Americans rely on Social Security to provide a larger share

of their total income than the national average. Nearly three out of four (72%) middle-

income Americans who receive Social Security benefits, excluding disability benefits,

say that Social Security benefits make up at least half or more of their retirement

income. The national average reported by SSA is that two in three (65%) Americans

depend on Social Security to provide at least half or more of their retirement income.

20Longevity Risk and Reward for Middle-Income Americans | March 2013

Three in Four Depend on Social SecurityNearly three in four (72%) middle-income

Americans who receive Social Security

benefits, excluding disability benefits,

say that Social Security benefits make up

at least half or more of their retirement

income. Nearly one in three (29%) count

on Social Security for 75% or more of

their retirement income.

For those with household incomes between

$25,000 and $50,000, one in ten (10%)

rely on Social Security for all of their

retirement income.

21Longevity Risk and Reward for Middle-Income Americans | March 2013

Gaps in UnderstandingDespite relying on Social Security to fund much of their retirement income, knowledge of

specific benefits varies widely among middle-income Americans. In fact, one in three (34%)

of those age 55 and older do not understand that delaying when they start to collect Social

Security can increase their future benefit amount. Every year a person works past full

retirement age, in effect, is equivalent to giving oneself a lifetime raise.

Nearly half (47%) incorrectly believe that an annual cost-of-living increase to their Social Security

benefits is guaranteed. In fact, in 2010 and 2011 the Cost of Living Adjustment (COLA) was

determined to be 0% and Social Security benefits did not automatically increase in either year.

Surprisingly, middle-income Americans already receiving Social Security benefits do not show a

significantly greater understanding of Social Security than those not yet collecting benefits, with

the exception of two knowledge areas: the ability to collect benefits starting at age 62 (94%

correct vs. 83% correct) and benefits for a non-working spouse (66% correct vs. 53% correct).

Gene

rally

Unt

rue

of

Soci

al S

ecur

ity B

enefi

tsGe

nera

lly Tr

ue o

f So

cial

Sec

urity

Ben

efits

22Longevity Risk and Reward for Middle-Income Americans | March 2013

One-Third Unsure About Full Retirement AgeMore than one-third (36%) of middle-

income Americans falsely believe that full

Social Security benefits start with their

65th birthday.

The full retirement age for the oldest Baby

Boomers, those born in 1946, is now age

66. The youngest Boomers, born in 1964,

will not reach full retirement age for Social

Security benefits until they turn age 67.

Year of Birth Full Retirement Age

1938 65 and 2 months

1939 65 and 4 months

1940 65 and 6 months

1941 65 and 8 months

1942 65 and 10 months

1943-1954 66

1955 66 and 2 months

1956 66 and 4 months

1957 66 and 6 months

1958 66 and 8 months

1959 66 and 10 months

1960 and later 67

Source: Social Security Administration, 2013.

Age to Receive Full Social Security Benefits

23Longevity Risk and Reward for Middle-Income Americans | March 2013

One-Third Don’t Know Their BenefitIn addition to gaps in understanding of

benefits, some middle-income Americans

are also not paying attention to their

individual Social Security statements.

One in three (35%) middle-income

Americans age 55 and older who are not

yet receiving Social Security do not know

what their monthly benefit amount will be

when they retire.

24Longevity Risk and Reward for Middle-Income Americans | March 2013

Uncertain Future of Social Security Nearly eight in ten (78%) middle-income

Americans age 55 and older are concerned

about the future of Social Security.

In fact, most middle-income Americans

over age 55 are unsure if (38%) or do not

believe (38%) that Social Security as we

know it will exist in 20 years. One in four

(24%) feel confident that the system will

remain intact two decades from now.

25Longevity Risk and Reward for Middle-Income Americans | March 2013

Most Not Confident in Fixes to Social SecurityLooking ahead, middle-income Americans

are uncertain. The majority (67%) of

respondents are unsure if or do not

believe that the government will fix the

Social Security system in their lifetime.

One-fifth (20%) believe that the federal

government will fix the system. Just over

one in ten (13%) feel Social Security is

not broken and should remain untouched.

Proposed changes to the current system

do not provide middle-income Americans

over age 55 with optimism. In fact, more

than half (56%) do not think that changes

or reforms to the current Social Security

program will benefit them.

Middle-income Americans currently

receiving Social Security benefits are

slightly more inclined (61%) to believe

that reforms or changes will benefit them

versus those respondents who are not

yet collecting benefits (49%).

26Longevity Risk and Reward for Middle-Income Americans | March 2013

Recommendations for Consumers

Think about longevity—and plan for it. Start with a free longevity calculator at SocialSecurity.gov. Discuss with loved ones or a professional advisor how life expectancy may affect decisions you make about your retirement years. Consider income, personal goals and experiences, and wishes for healthcare and long-term care.

Know your full retirement age. If you were born after 1938, age 65 is no longer full retirement age for Social Security. Boomers born in 1946, your full retirement age is 66. For youngest Boomers born after 1960, your full retirement age is 67.

Consider working longer. Every year you work past your Social Security full retirement age, you increase your benefit amount. Think of it as a lifetime raise. If you are considering taking Social Security benefits early at age 62 or any time prior to your full retirement age, do the math. You will be accepting a lower benefit amount that cannot be reset later.

Log on for your benefits. Visit SocialSecurity.gov to sign up for access to personal data on your benefits through the government’s MySocialSecurity program. Be sure to have your spouse sign up too, so you can factor in his or her benefits as well as your own.

Explore your income options. Most people will rely on Social Security to fund their retirement years. But the program was never designed to replace all of your income. Many products and services exist for people with virtually any level of income and assets that can help ensure you will not outlive your money.

Take healthy steps. Genetics impact how long one might live, but the quality of those years is equally important. Being active, eating right, socializing with others, and seeing your doctor regularly are just some of the steps anyone at any age can take to live healthier and longer lives.

Do something with your wisdom. Survey respondents said that wisdom comes with age—age 56 to be specific. Find ways to get or stay engaged, in a big or small way. Do something that makes you feel good. Your opportunity to make a difference is out there.

27Longevity Risk and Reward for Middle-Income Americans | March 2013

About the Center for a Secure Retirement

Bankers Life and Casualty Company Center for a Secure Retirement is the company’s

research and consumer education program. Its studies and consumer awareness

campaigns provide insight and practical advice for how everyday Americans can achieve

financial security during retirement.

Established in 1879 in Chicago, Bankers Life and Casualty Company focuses on the

insurance needs of the retirement market. The nationwide company, a subsidiary of CNO

Financial Group, Inc., offers a broad portfolio of life and health insurance products and

annuities designed especially for Boomers and retirees.

Learn More Bankers has more than 5,000 licensed professional agents in over 250 offices across

the United States. Bankers agents meet with thousands of Americans each week for

initial retirement reviews at no cost to the clients. To learn more about Bankers Life and

Casualty Company, visit bankers.com or call 1-800-231-9150.

Endnotes

1 Social Security Administration, 2012.2 Bankers Life and Casualty Company Center for a Secure Retirement, 2012.3 Bankers Life and Casualty Company Center for a Secure Retirement, 2011. 4 Ibid.5 Centers for Disease Control and Prevention, 2012.6 Ibid.7 Social Security Administration, 2012. 8 Bankers Life and Casualty Company Center for a Secure Retirement, 2011.9 Social Security Administration, 2012.10 Ibid.

18925

© 2013 Bankers Life and Casualty Company.

Bankers Life and Casualty Company Center for a Secure Retirement

Chicago, IL

bankers.comcenterforasecureretirement.com

Media ContactJennifer [email protected]

Study ContactCarrie [email protected]