luxury market.pdf

DESCRIPTION

luxury products marketTRANSCRIPT

Luxury Brand Routes to Market: Exclusivity vs Expansion

April 2011

© Euromonitor International

2

Luxury Goods – Brand Routes

Introduction

Luxury Market Overview

Routes to Market: Wholesale

Routes to Market: Retail

Routes to Market: Online

Case Study: Polo Ralph Lauren Corp

Conclusion

© Euromonitor International

3

Luxury Goods – Brand Routes

Learn More

To find out more about Euromonitor International's complete range of business intelligence on industries, countries and consumers please visit www.euromonitor.com or contact your local Euromonitor International office:

Disclaimer

Much of the information in this briefing is of a statistical

nature and, while every attempt has been made to ensure

accuracy and reliability, Euromonitor International cannot be

held responsible for omissions or errors

Figures in tables and analyses are calculated from unrounded data and may not sum. Analyses found in the briefings may not totally reflect the companies’ opinions, reader discretion is advised

London +44 (0)20 7251 8024 Chicago +1 312 922 1115 Singapore +65 6429 0590 Shanghai +86 21 6372 6288 Vilnius +370 5 243 1577

Dubai +971 4 372 4363 Cape Town +27 21 552 0037 Santiago +56 2 915 7200 Sydney +61 2 9275 8869 Tokyo +81 3-5403-4790

Scope

Introduction

Luxury Goods

Designer Clothing

and Footwear

Luxury Tobacco

Luxury Accessories

Luxury Jewellery

and Timepieces

Fine Wines/

Champagne and Spirits

Super Premium Beauty

and Personal

Care

Luxury Travel Goods

Luxury Fine

China and

Crystal Ware

Luxury Writing

Instruments and

Stationery

Luxury Electronic Gadgets

© Euromonitor International

4

Luxury Goods – Brand Routes

• The core objective of this report is to examine how the luxury goods industry is responding to the challenge of

widening its distribution within a changing global market at the same time as retaining exclusivity and rarity, key

luxury attributes which allow brands to charge premium prices.

• The report will look at distribution channels within the global luxury goods market, determining how the latest industry

trends and developments are impacting company strategies, and discussing how luxury brands are looking to

maintain their premium positioning as well as expand their sales to a wider audience.

• The report begins with an overview of the global luxury goods market’s current status and growth expectations to

2015, as well as an overview of retail channels used by the various categories.

• The report is then split into three key sections focusing on wholesale distribution, retail distribution and online sales

formats, offering an overview of each channel, assessment of its strengths and weaknesses, company strategies

and case studies.

• A case study looks at the Polo Ralph Lauren company in more depth, investigating its ability to position itself as both

a premium luxury brand and a more mid-market label at a time when it is attempting to move to a more premium

position in emerging Asian markets, and assessing the future prospects of this strategy.

• The report concludes with a series of forward-looking final conclusions, looking at future prospects for distribution

channels, and highlighting key strategies going forward.

• The report does not claim to be comprehensive but rather seeks to offer high-level insight into key developments and

opportunities in the luxury goods market at a time of continued macroeconomic uncertainty.

• Data from several Euromonitor International projects have been used in this report:

• Luxury Goods

• Countries and Consumers

• Travel and Tourism

• Retailing

Objectives of the global briefing

Introduction

© Euromonitor International

5

Luxury Goods – Brand Routes

Global luxury goods: Market

environment 2010-2015

Global luxury goods sales have already begun to recover from the impact of the

economic downturn, but its effects are still evident. Focus has shifted to the

more resilient emerging markets, particularly in Asia, bringing a younger

consumer base into greater prominence. Meanwhile, aspirational luxury is out,

while high-end classics, which continue to maintain their worth, are popular.

Wholesaling falls out of

favour; but for how long?

Bankruptcies, deep discounting and interrupted order cycles all damaged trust

between brands and their wholesale customers, leading many brands to refocus

on retail activities and place less reliance on wholesale distribution. However, as

growth picks up, and internationalisation again becomes a key focus,

wholesaling will play a vital part in a brand’s ability to reach consumers.

Brands move to take greater

control of retail distribution

As brands such as Hermès and Louis Vuitton safely negotiated the downturn,

their strategies of tight distribution control began to be taken up and adapted by

more brands. The trend for buying back licences in both developed and

emerging markets is still ongoing.

Internet retailing: Luxury

brands begin to believe

It required Net-A-Porter to show the way, but luxury brands, particularly within

the clothing and accessories categories, are finally looking at online potential.

Flagships vs outlets:

Contradictory formats

Are investments in brand image, such as flagships, being neutralised by outlet

store activities? This question is not going to go away.

Distribution strategies:

Developed markets

Premium store environments are still key to luxury positioning but, increasingly,

transactional websites are being used to provide greater accessibility.

Distribution strategies:

Emerging markets

As demand expands, accessibility is key, but not at the expense of brand image.

In-store and online, support for luxury positioning is a key focus.

Impact of counterfeiting

fears on distribution

strategies

Restricting sales via third parties and taking back licences are partly about

restricting production of counterfeit goods and changing consumer expectations

of the type of outlets where they can buy luxury brands.

Key findings

Introduction

© Euromonitor International

6

Luxury Goods – Brand Routes

Introduction

Luxury Market Overview

Routes to Market: Wholesale

Routes to Market: Retail

Routes to Market: Online

Case Study: Polo Ralph Lauren Corp

Conclusion

© Euromonitor International

7

Luxury Goods – Brand Routes Luxury Market Overview

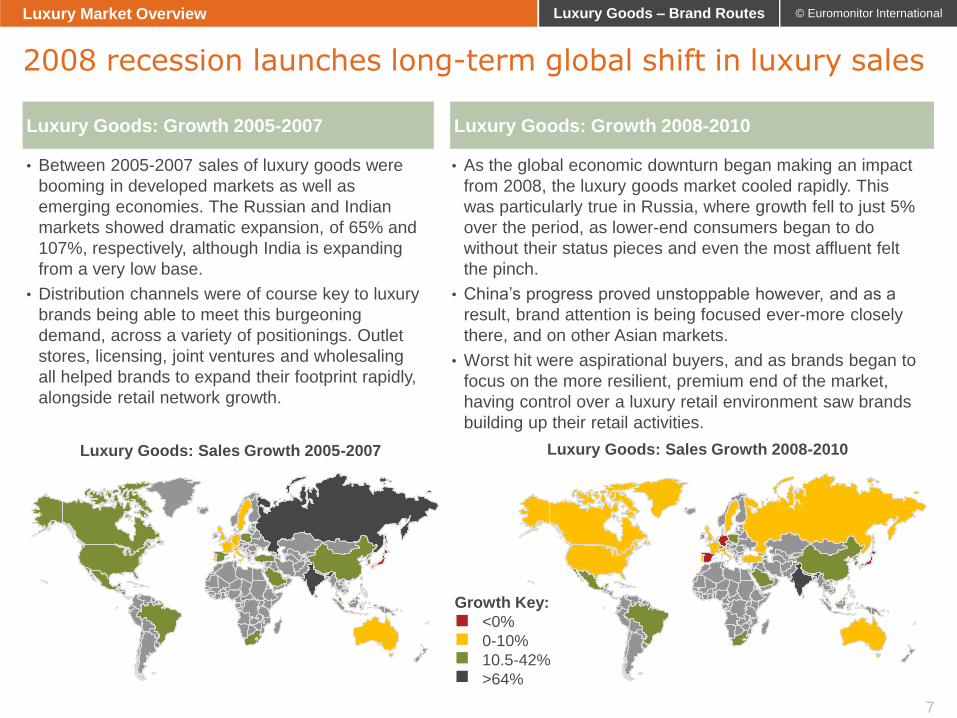

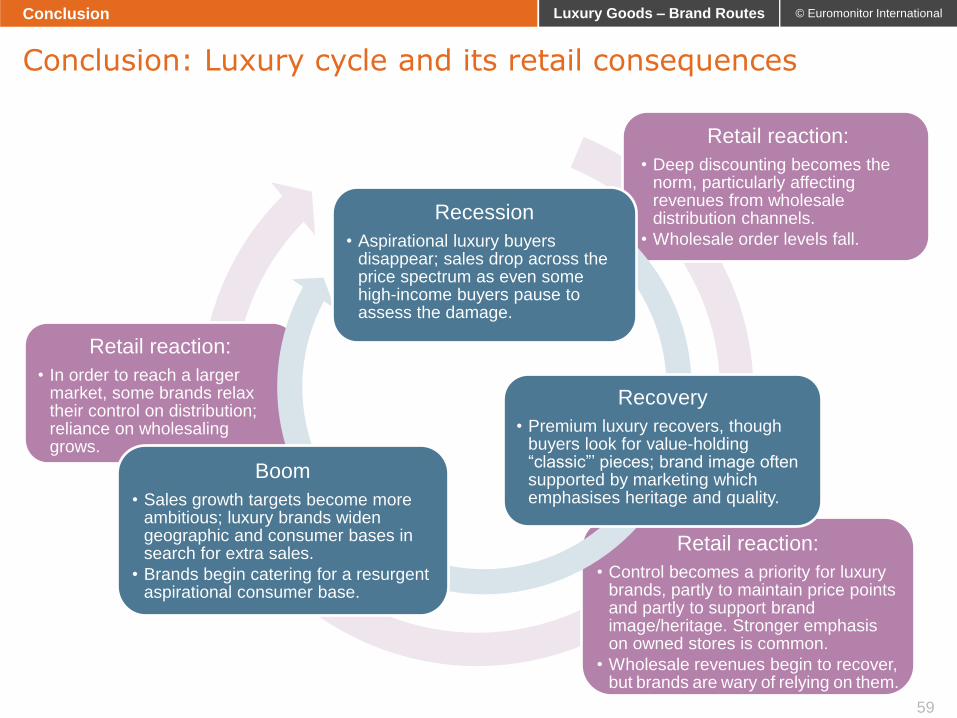

2008 recession launches long-term global shift in luxury sales

Luxury Goods: Growth 2005-2007 Luxury Goods: Growth 2008-2010

• Between 2005-2007 sales of luxury goods were

booming in developed markets as well as

emerging economies. The Russian and Indian

markets showed dramatic expansion, of 65% and

107%, respectively, although India is expanding

from a very low base.

• Distribution channels were of course key to luxury

brands being able to meet this burgeoning

demand, across a variety of positionings. Outlet

stores, licensing, joint ventures and wholesaling

all helped brands to expand their footprint rapidly,

alongside retail network growth.

• As the global economic downturn began making an impact

from 2008, the luxury goods market cooled rapidly. This

was particularly true in Russia, where growth fell to just 5%

over the period, as lower-end consumers began to do

without their status pieces and even the most affluent felt

the pinch.

• China’s progress proved unstoppable however, and as a

result, brand attention is being focused ever-more closely

there, and on other Asian markets.

• Worst hit were aspirational buyers, and as brands began to

focus on the more resilient, premium end of the market,

having control over a luxury retail environment saw brands

building up their retail activities.

Growth Key:

<0%

0-10%

10.5-42%

>64%

Luxury Goods: Sales Growth 2005-2007 Luxury Goods: Sales Growth 2008-2010

© Euromonitor International

8

Luxury Goods – Brand Routes Luxury Market Overview

2011: Has the luxury market recovered?

• The luxury market of 2011 still bears the marks of the recent global recession. Two years of declining growth in 2008

and 2009 forced manufacturers and shoppers alike to reconsider their established habits, with luxury brand

distribution left struggling to find a happy balance between the two.

• 2010 brought better news, with a 4% rebound across the 26 markets that account for 80% of global sales, albeit

against a changed market landscape:

• “Bling” and aspirational luxury is out, but value, it seems, is only rarely defined by price; brand equity is paramount;

• China, India and other emerging markets are firmly established as the focus for growth, while Germany looks set to

join Japan in a long-term decline;

• The consumer base is becoming younger, driven by a new generation of white-collar workers in emerging markets;

• New technologies are changing how consumers approach luxury brands; the influence of the internet and social

networking is unavoidable and brands are looking to widen their presence online;

• Manufacturer/retailer relationships have lost an element of trust, with more brands migrating to owned stores.

• By 2015, the market is expected to have returned to steady growth, with emerging markets accounting for one fifth of

global sales. The challenge for luxury brands and retailers alike is to expand distribution to reach these new

consumers, using new technologies, without losing the aura of exclusivity that “luxury” depends upon.

-10

-5

0

5

10

15

0

50

100

150

200

250

300

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

% y

-o-y

gro

wth

US

$ b

illio

n

Global Luxury Markets: Developed vs Emerging 2005-2015

Value sales: Developed markets Value sales: Emerging marketsGrowth: Developed markets Growth: Emerging markets

© Euromonitor International

9

Luxury Goods – Brand Routes

• India is forecast to be the standout market in terms of growth to 2015 The country’s luxury goods market is set to

more than double in size over 2010-2015 to generate sales of US$4.3 billion in 2015. This is already attracting luxury

brands to the market and premium retail locations are expected to multiply accordingly, but the potential consumer

base remains comparatively small. Even the richest 10% of households is expected to enjoy an average income of

only US$26,000 by 2015, compared to US$54,000 in China and US$117,000 in Brazil.

• By 2015, China will be the fourth largest luxury goods market in the world, having overtaken France, the UK and

Italy. Even by emerging market standards, the forecast CAGR of 10% is very healthy: not only does China benefit

from an emerging middle class with a rapidly growing earning capacity, but also from a fast-developing luxury

distribution network with which to fulfil customer demand.

• Nevertheless, while China’s sales are expected to grow by US$6.8 billion to 2015, the massive US market is set to

add US$8.1 billion of luxury goods sales. For luxury brands that can rise above the pack in this crowded market,

there are still good returns to be made, although US growth will be modest even by developed market standards.

Where will the luxury goods market be growing most?

Luxury Market Overview

-5

0

5

10

15

20

25

-5

0

5

10

15

20

25

30

35

40

% C

AG

R

US

$ b

illio

n

Top 26 Luxury Markets: Sales 2010 vs Growth 2010-2015 Developed markets:2010 sales

Developed markets:Sales added by 2015

Emerging markets:2010 sales

Emerging markets:Sales added by 2015

Developed markets:Growth 2010/15

Emerging markets:Growth 2010/15

80

75

70

© Euromonitor International

10

Luxury Goods – Brand Routes

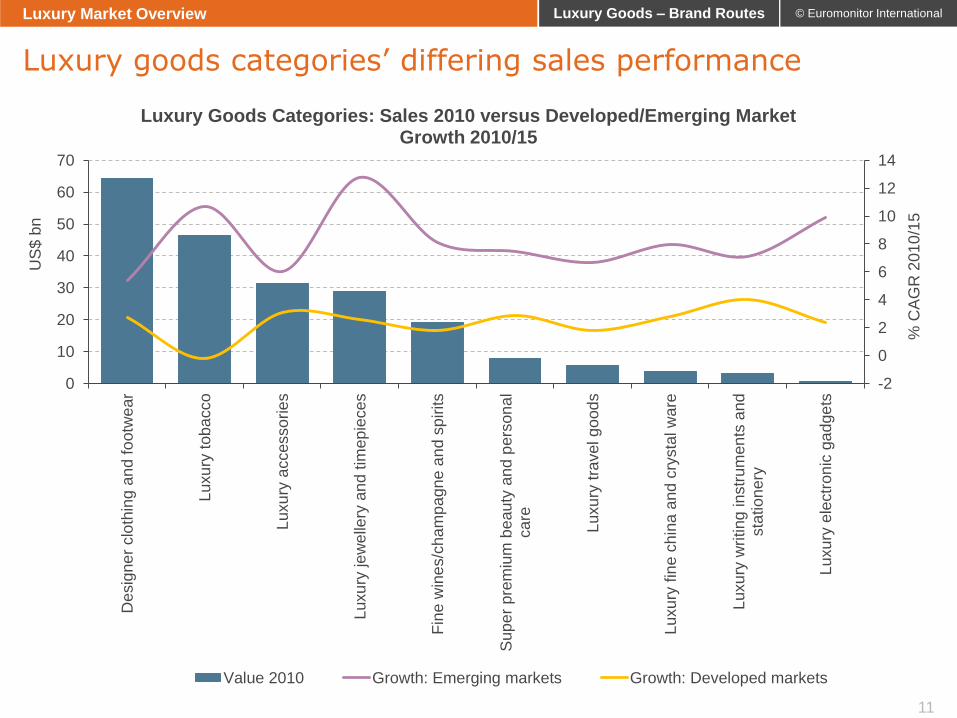

What will see the most luxury value growth?

Luxury Market Overview

• Between 2010 and 2015 there are expected to be marked differences in the product selections of luxury consumers

in emerging and developed markets.

• In emerging markets, an element of “bling” is still present, with relatively ostentatious products such as luxury

jewellery and timepieces and luxury electronic gadgets doing well. As the number of young workers moving out of

the family home into one-person or two-person households rises, homewares such as luxury fine china and crystal

ware are also a focus.

• In developed markets, customers - their confidence knocked by the global downturn and the subsequent slow

recovery of many developed markets - are expected to favour “classic” goods which will hold their value. Luxury

writing instruments and stationery and luxury accessories should both do well, while designer clothing and footwear

is seeing a move away from the cheaper, more “aspirational” end of the luxury market to higher-priced statement

pieces.

• Super premium beauty and personal care will maintain steady growth, with skin care products traditionally popular in

Asian markets, both developed and emerging.

• A CAGR of 1% in the US luxury tobacco sales will not be enough to counteract the decline in other developed

markets, but tobacco will remain the biggest luxury category in the US and Germany by 2015, joined by China from

2012 onwards. Markets such as Poland and India are also expected to see a rise in luxury tobacco consumption,

resulting in strong emerging market growth.

© Euromonitor International

11

Luxury Goods – Brand Routes

Luxury goods categories’ differing sales performance

Luxury Market Overview

-2

0

2

4

6

8

10

12

14

0

10

20

30

40

50

60

70

Desig

ne

r clo

thin

g a

nd f

ootw

ear

Luxu

ry tob

acco

Luxu

ry a

ccesso

rie

s

Luxu

ry je

welle

ry a

nd

tim

ep

ieces

Fin

e w

ine

s/c

ha

mp

agn

e a

nd s

pirits

Sup

er

pre

miu

m b

eau

ty a

nd p

ers

on

al

ca

re

Luxu

ry tra

vel g

ood

s

Luxu

ry fin

e c

hin

a a

nd

cry

sta

l w

are

Luxu

ry w

riting

in

str

um

en

ts a

nd

sta

tio

nery

Luxu

ry e

lectr

on

ic g

ad

ge

ts

% C

AG

R 2

01

0/1

5

US

$ b

n

Luxury Goods Categories: Sales 2010 versus Developed/Emerging Market Growth 2010/15

Value 2010 Growth: Emerging markets Growth: Developed markets

© Euromonitor International

12

Luxury Goods – Brand Routes

02468

1012141618

2005/10 2010 2011 2012 2013 2014 2015

€ b

illio

n

Germany: Luxury Sales By Product Category 2005/10-2015

Designer clothing and footwear Fine wines/champagne and spiritsLuxury accessories Luxury electronic gadgetsLuxury fine china and crystal ware Luxury jewellery and timepiecesLuxury tobacco Luxury travel goodsLuxury writing instruments and stationery Super premium beauty and personal care

Luxury tobacco

0

500

1,000

1,500

2,000

2,500

3,000

¥ b

illio

n

Japan: Luxury Sales by Product Category 2005/10-2015

Designer clothing and footwear

• Japan and Germany are the only two major luxury goods markets forecast to decline over 2010-2015, but compared

to the 2005-2010 period, the rate of the contraction is expected to slow dramatically. Each market has been severely

affected by falling sales in one category: luxury tobacco in Germany and designer clothing and footwear in Japan.

• Luxury tobacco aside, the German market is expected to do well by developed market standards, forecast a CAGR

of 2.5%. Sales of designer clothing and footwear, which also fell during 2005-2010, are expected to be 14% higher

by 2015, as the key 25-39 age group takes over from the 40-55 age group as Germany’s highest earners.

• Once known as the world’s only luxury mass market, a 2003 study by the Saison Research Institute concluded that

94% of female Tokyo residents owned a Louis Vuitton handbag, even though the country had already endured a

decade of recession by then. Consumers are becoming increasingly price sensitive, buying during sales or through

outlet stores and mixing expensive pieces with cheaper items, but flat sales, even a degree of growth for several

categories, hints that the decline in sales in Japan has bottomed out, and the market has a rump of loyal luxury

consumers likely to maintain spending patterns seen in 2010. The Federation of Swiss Watchmakers, for one, noted

a positive trend in 2010, with exports to Japan up by 5% on the previous year.

Which markets will see a contraction in luxury spending?

Luxury Market Overview

© Euromonitor International

13

Luxury Goods – Brand Routes

The

challenge:

to remain

selective

while

accessing

enough

customers

and sales.

Can the

two

elements

co-exist?

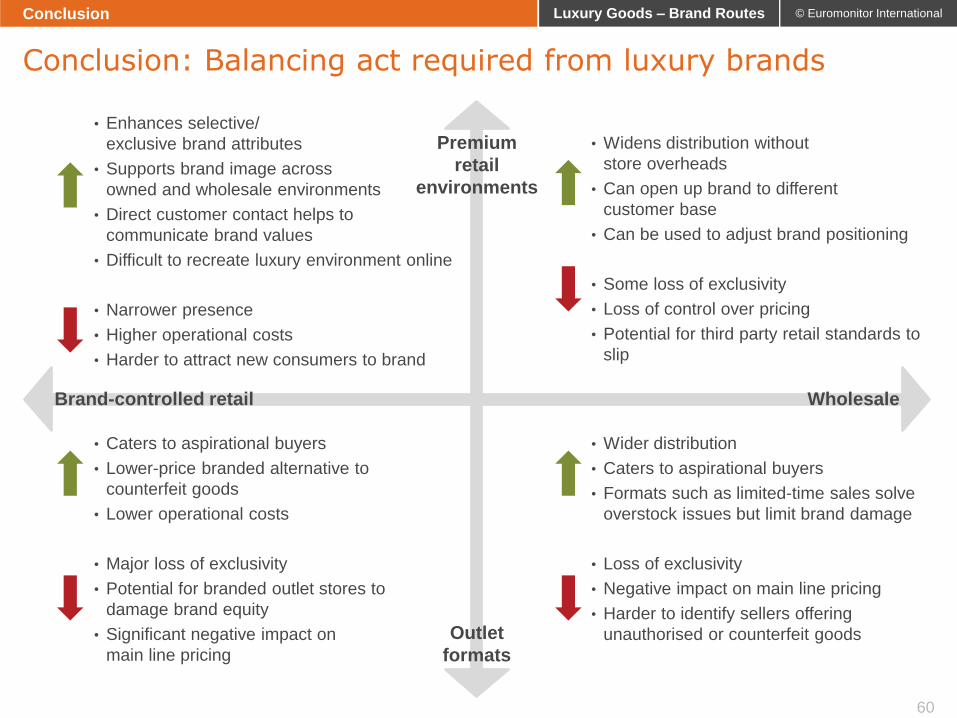

Maintaining a luxury brand image and price

Using exclusivity to maintain price points and attract highest

income consumers

Only selling through luxury retail environments; creating

premium selling environments (flagship stores)

Controlling inventory and brand exposure

Generating sales in a changing market

Widening market coverage

Harnessing the sales potential of aspirational consumers

Publicising the brand

Expanding the customer base

Leveraging wholesale activity

Creating an online presence

The central dilemma of luxury distribution

Luxury Market Overview

© Euromonitor International

14

Luxury Goods – Brand Routes

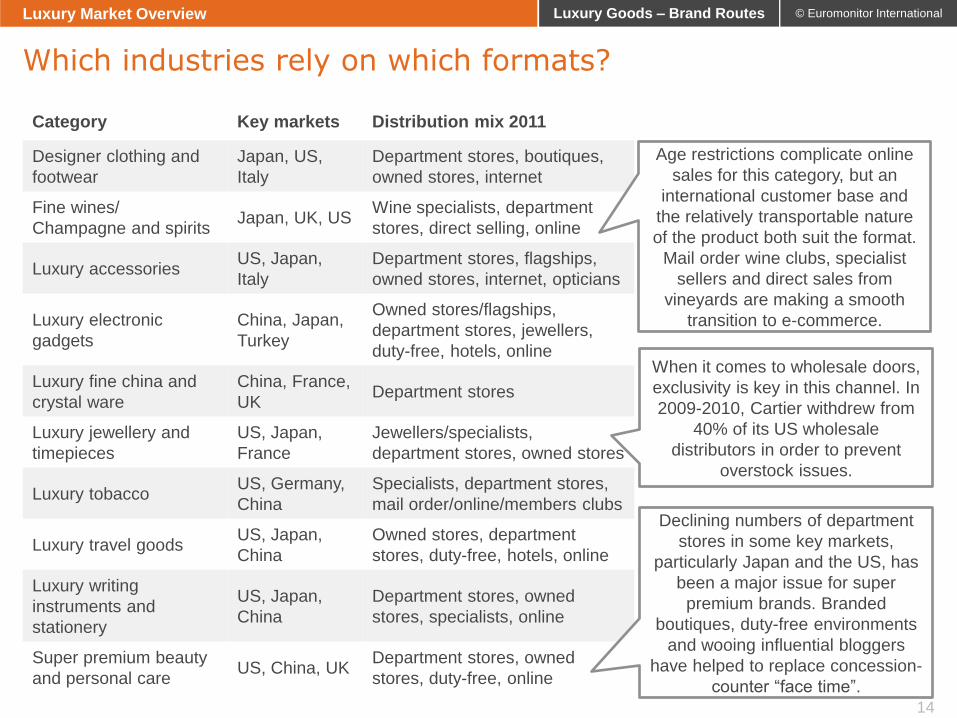

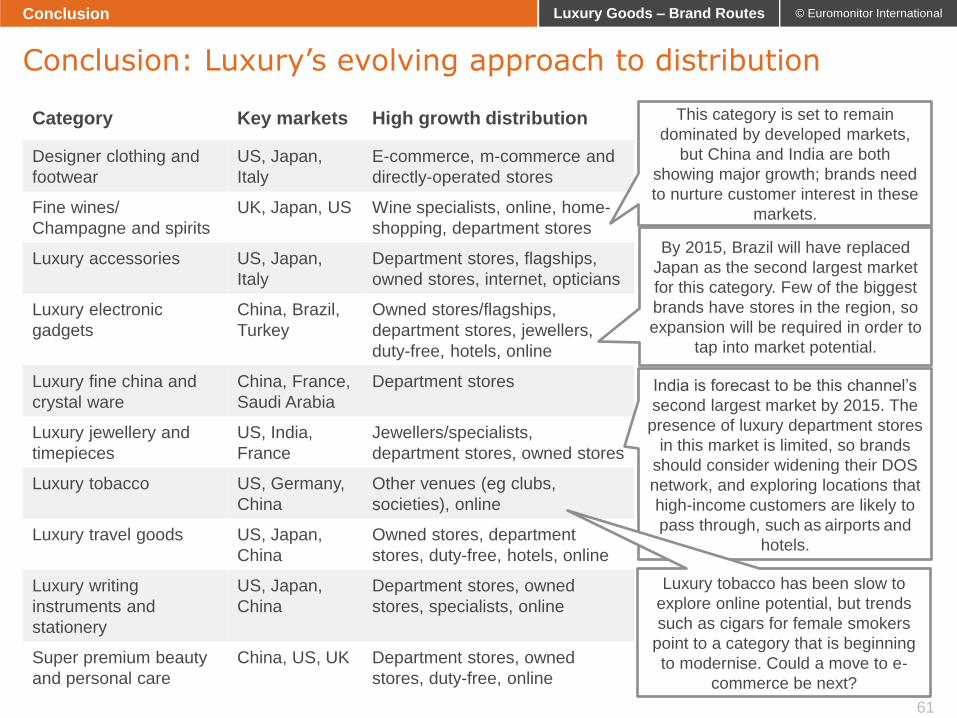

Category Key markets Distribution mix 2011

Designer clothing and

footwear

Japan, US,

Italy

Department stores, boutiques,

owned stores, internet

Fine wines/

Champagne and spirits Japan, UK, US

Wine specialists, department

stores, direct selling, online

Luxury accessories US, Japan,

Italy

Department stores, flagships,

owned stores, internet, opticians

Luxury electronic

gadgets

China, Japan,

Turkey

Owned stores/flagships,

department stores, jewellers,

duty-free, hotels, online

Luxury fine china and

crystal ware

China, France,

UK Department stores

Luxury jewellery and

timepieces

US, Japan,

France

Jewellers/specialists,

department stores, owned stores

Luxury tobacco US, Germany,

China

Specialists, department stores,

mail order/online/members clubs

Luxury travel goods US, Japan,

China

Owned stores, department

stores, duty-free, hotels, online

Luxury writing

instruments and

stationery

US, Japan,

China

Department stores, owned

stores, specialists, online

Super premium beauty

and personal care US, China, UK

Department stores, owned

stores, duty-free, online

Which industries rely on which formats?

Luxury Market Overview

Age restrictions complicate online

sales for this category, but an

international customer base and

the relatively transportable nature

of the product both suit the format.

Mail order wine clubs, specialist

sellers and direct sales from

vineyards are making a smooth

transition to e-commerce.

Declining numbers of department

stores in some key markets,

particularly Japan and the US, has

been a major issue for super

premium brands. Branded

boutiques, duty-free environments

and wooing influential bloggers

have helped to replace concession-

counter “face time”.

When it comes to wholesale doors,

exclusivity is key in this channel. In

2009-2010, Cartier withdrew from

40% of its US wholesale

distributors in order to prevent

overstock issues.

© Euromonitor International

15

Luxury Goods – Brand Routes

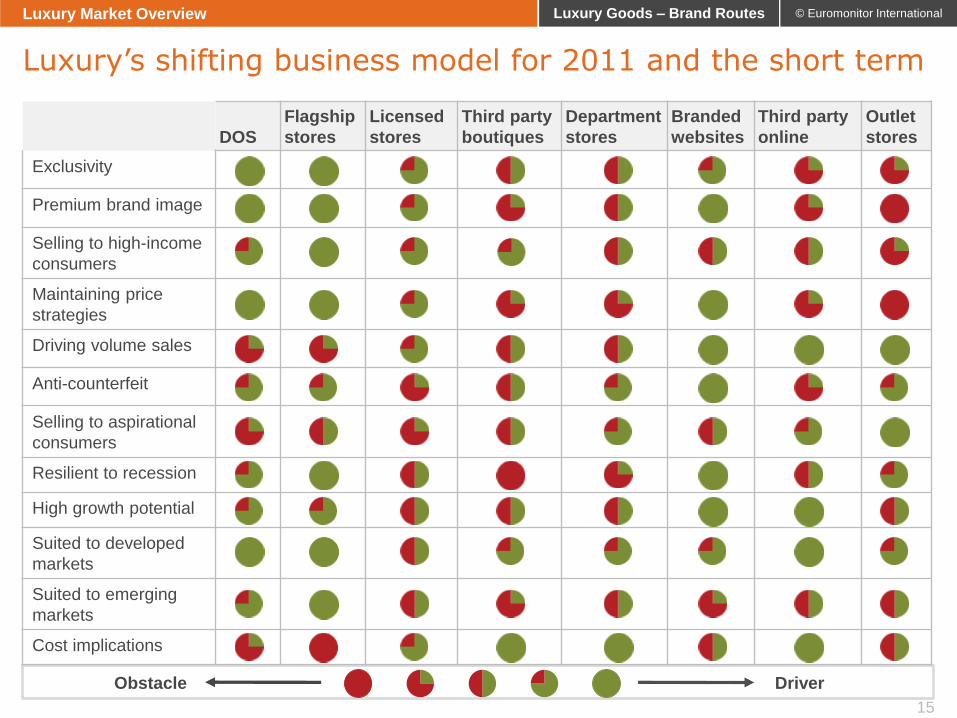

DOS

Flagship

stores

Licensed

stores

Third party

boutiques

Department

stores

Branded

websites

Third party

online

Outlet

stores

Exclusivity

Premium brand image

Selling to high-income

consumers

Maintaining price

strategies

Driving volume sales

Anti-counterfeit

Selling to aspirational

consumers

Resilient to recession

High growth potential

Suited to developed

markets

Suited to emerging

markets

Cost implications

Luxury’s shifting business model for 2011 and the short term

Luxury Market Overview

Obstacle Driver

© Euromonitor International

16

Luxury Goods – Brand Routes

Introduction

Luxury Market Overview

Routes to Market: Wholesale

Routes to Market: Retail

Routes to Market: Online

Case Study: Polo Ralph Lauren Corp

Conclusion

© Euromonitor International

17

Luxury Goods – Brand Routes

Wh

ole

sa

le

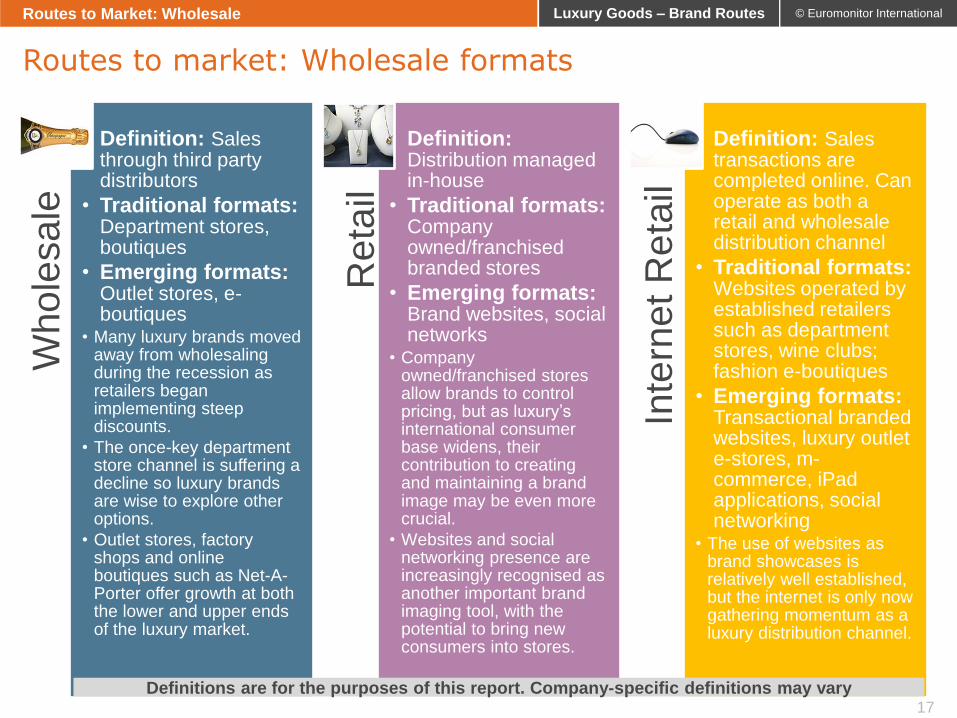

• Definition: Sales through third party distributors

• Traditional formats: Department stores, boutiques

• Emerging formats: Outlet stores, e-boutiques

• Many luxury brands moved away from wholesaling during the recession as retailers began implementing steep discounts.

• The once-key department store channel is suffering a decline so luxury brands are wise to explore other options.

• Outlet stores, factory shops and online boutiques such as Net-A-Porter offer growth at both the lower and upper ends of the luxury market.

Re

tail

• Definition: Distribution managed in-house

• Traditional formats: Company owned/franchised branded stores

• Emerging formats: Brand websites, social networks

• Company owned/franchised stores allow brands to control pricing, but as luxury’s international consumer base widens, their contribution to creating and maintaining a brand image may be even more crucial.

• Websites and social networking presence are increasingly recognised as another important brand imaging tool, with the potential to bring new consumers into stores.

Inte

rne

t R

eta

il

• Definition: Sales transactions are completed online. Can operate as both a retail and wholesale distribution channel

• Traditional formats: Websites operated by established retailers such as department stores, wine clubs; fashion e-boutiques

• Emerging formats: Transactional branded websites, luxury outlet e-stores, m-commerce, iPad applications, social networking

• The use of websites as brand showcases is relatively well established, but the internet is only now gathering momentum as a luxury distribution channel.

Routes to market: Wholesale formats

Routes to Market: Wholesale

Definitions are for the purposes of this report. Company-specific definitions may vary

© Euromonitor International

18

Luxury Goods – Brand Routes

Luxury wholesale: The good

Luxury wholesale: The bad

Counterfeiting issues

Brand over-exposure/Loss

of exclusivity

Unwanted discounting

Unpredictable purchase patterns

Prestige stores enhance brand

image

Spreading risk

Cost-effective expansion

Performance measure alongside

competitors

Luxury wholesale: Risk and rewards

Routes to Market: Wholesale

• Luxury wholesaling - selling goods to

third parties rather than controlling all

distribution in-house - has become

less attractive to luxury brands since

the recession hit.

• Third party retailers became less

reliable as customers because of

bankruptcies and cautious buying in

the wake of the downturn, while deep

discounting programmes caused

widespread damage to brand pricing.

• Counterfeit goods are harder to

control for brands which are known to

use wholesale distribution.

• In addition, the decline of the

aspirational luxury market has left

brands more reliant on the top end of

the market, meaning that brand

image, exclusivity and sales

environments grew in importance.

• However, using wholesale

distribution gives luxury brands

access to a much wider consumer

base without requiring major

investment, and presence at the very

best stores can enhance a brand’s

image, or even add a fresh

dimension to it.

Wider market

exposure

© Euromonitor International

19

Luxury Goods – Brand Routes

• The department stores channel saw steep sales falls in 2007-2009 as non-grocery sales were hit by the credit

crunch, before bouncing back to 4.5% in 2010, led by China and a resurgent US market.

• In the US, the merger of the Federated and May department store groups in 2005 had already resulted in a number

of store closures before the downturn resulted in deep discounting and several bankruptcies: a distribution problem

for luxury brands.

• Nearly 20% of Japan’s department stores have closed over 2005-2010, but the channel remains an important outlet

for luxury brands, many of which operate their own shops within department stores.

• Top luxury department store banners such as Isetan, Mitsukoshi and Takashimaya all saw sales declines of 4-5% in

2010 on the back of years of negative growth. With department store sales expected to fall by another 14% to 2015,

luxury brands will be forced to explore other distribution avenues.

• Chinese department store numbers are growing rapidly as chains expand into smaller cities, but in the saturated

first-tier markets, it is demand for luxury products that is pushing sales higher.

Growth in US and China props up department stores channel

Routes to Market: Wholesale

© Euromonitor International

20

Luxury Goods – Brand Routes

Department store channel: Store numbers vs value sales

Routes to Market: Wholesale

China

UK

US

0

5

10

15

20

25

2005 2006 2007 2008 2009 2010

Ou

tle

ts

Department Stores: Outlet Numbers 2005-2010

Russia

Japan

China

UK

US

0

50

100

150

200

250

300

350

400

450

500

2005 2006 2007 2008 2009 2010

US

$ b

illio

n (

con

sta

nt 2

01

0 p

rice

s,

fixe

d 2

01

0 e

xch

an

ge

rate

s)

Department Stores: Value Sales 2005-2010

Japan

Singapore

South Korea

Australia

Saudi Arabia

UAE

Canada

US

France

Germany

Italy

Portugal

Spain

Sweden

Switzerland

UK

China

India

Malaysia

Poland

Russia

Brazil

Mexico

South Africa

Turkey

Japan

South Korea

© Euromonitor International

21

Luxury Goods – Brand Routes

Super Premium Department Stores vs

Overall Channel Growth 2005-2010

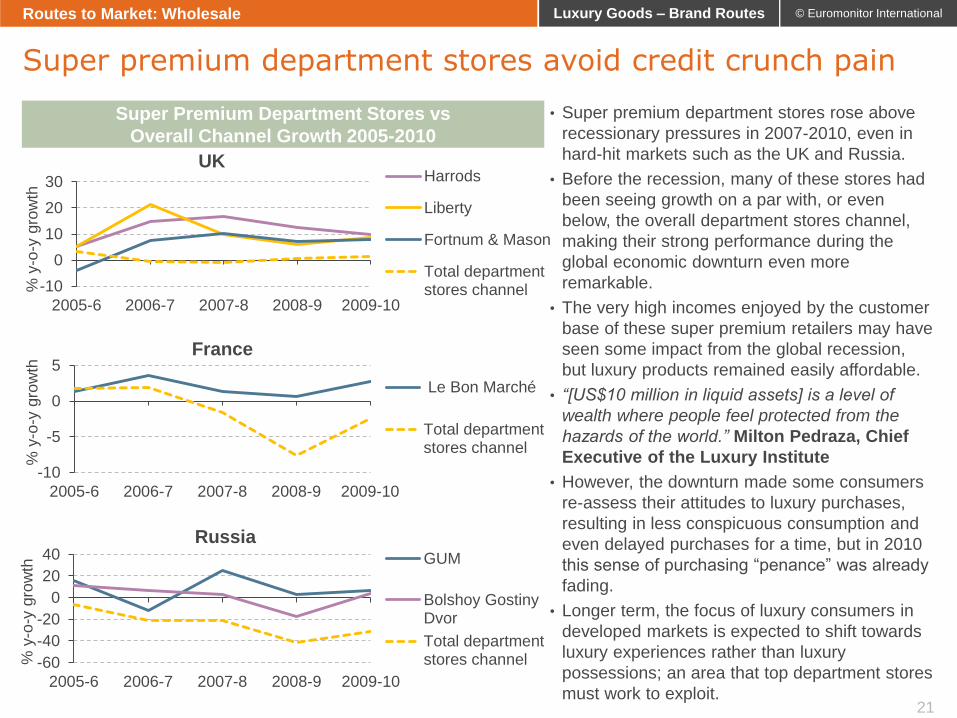

Super premium department stores avoid credit crunch pain

Routes to Market: Wholesale

• Super premium department stores rose above

recessionary pressures in 2007-2010, even in

hard-hit markets such as the UK and Russia.

• Before the recession, many of these stores had

been seeing growth on a par with, or even

below, the overall department stores channel,

making their strong performance during the

global economic downturn even more

remarkable.

• The very high incomes enjoyed by the customer

base of these super premium retailers may have

seen some impact from the global recession,

but luxury products remained easily affordable.

• “[US$10 million in liquid assets] is a level of

wealth where people feel protected from the

hazards of the world.” Milton Pedraza, Chief

Executive of the Luxury Institute

• However, the downturn made some consumers

re-assess their attitudes to luxury purchases,

resulting in less conspicuous consumption and

even delayed purchases for a time, but in 2010

this sense of purchasing “penance” was already

fading.

• Longer term, the focus of luxury consumers in

developed markets is expected to shift towards

luxury experiences rather than luxury

possessions; an area that top department stores

must work to exploit.

-60

-40

-20

0

20

40

2005-6 2006-7 2007-8 2008-9 2009-10

% y

-o-y

gro

wth

Russia GUM

Bolshoy GostinyDvor

Total departmentstores channel

-10

-5

0

5

2005-6 2006-7 2007-8 2008-9 2009-10

% y

-o-y

gro

wth

France

Le Bon Marché

Total departmentstores channel

-10

0

10

20

30

2005-6 2006-7 2007-8 2008-9 2009-10

% y

-o-y

gro

wth

UK Harrods

Liberty

Fortnum & Mason

Total departmentstores channel

© Euromonitor International

22

Luxury Goods – Brand Routes

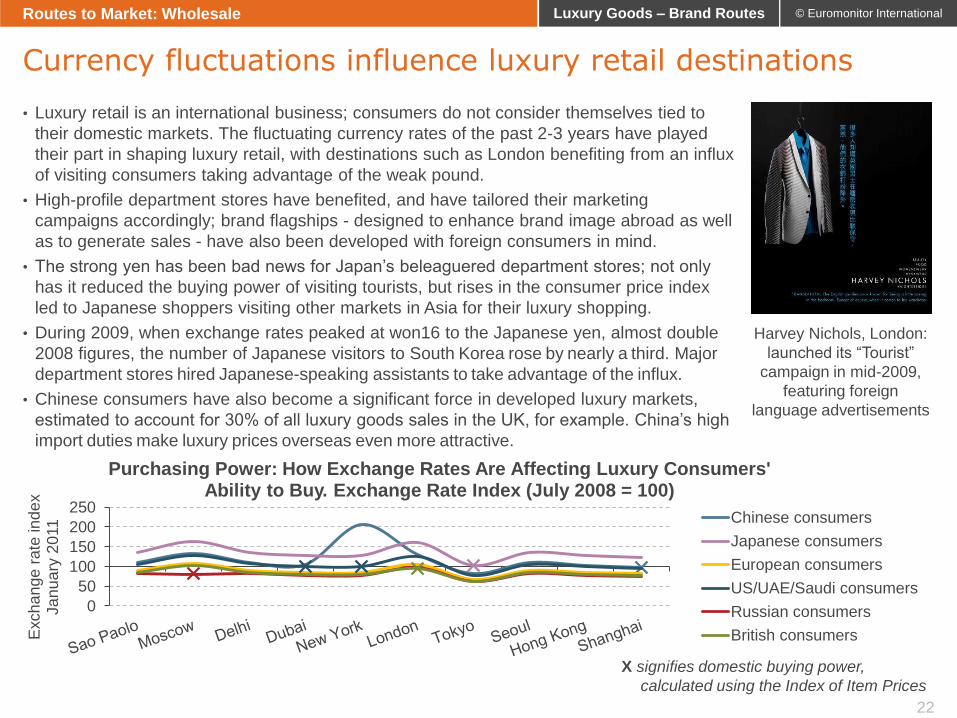

• Luxury retail is an international business; consumers do not consider themselves tied to

their domestic markets. The fluctuating currency rates of the past 2-3 years have played

their part in shaping luxury retail, with destinations such as London benefiting from an influx

of visiting consumers taking advantage of the weak pound.

• High-profile department stores have benefited, and have tailored their marketing

campaigns accordingly; brand flagships - designed to enhance brand image abroad as well

as to generate sales - have also been developed with foreign consumers in mind.

• The strong yen has been bad news for Japan’s beleaguered department stores; not only

has it reduced the buying power of visiting tourists, but rises in the consumer price index

led to Japanese shoppers visiting other markets in Asia for their luxury shopping.

• During 2009, when exchange rates peaked at won16 to the Japanese yen, almost double

2008 figures, the number of Japanese visitors to South Korea rose by nearly a third. Major

department stores hired Japanese-speaking assistants to take advantage of the influx.

• Chinese consumers have also become a significant force in developed luxury markets,

estimated to account for 30% of all luxury goods sales in the UK, for example. China’s high

import duties make luxury prices overseas even more attractive.

Currency fluctuations influence luxury retail destinations

Routes to Market: Wholesale

0

50

100

150

200

250

Exch

an

ge

rate

ind

ex

Ja

nu

ary

20

11

Purchasing Power: How Exchange Rates Are Affecting Luxury Consumers' Ability to Buy. Exchange Rate Index (July 2008 = 100)

Chinese consumers

Japanese consumers

European consumers

US/UAE/Saudi consumers

Russian consumers

British consumers

X signifies domestic buying power,

calculated using the Index of Item Prices

Harvey Nichols, London:

launched its “Tourist”

campaign in mid-2009,

featuring foreign

language advertisements

© Euromonitor International

23

Luxury Goods – Brand Routes

• Harvey Nichols (UK): International expansion began in

2000 with entry into Saudi Arabia (Riyadh); to date there

are stores in Hong Kong, Ireland (Dublin), the United Arab

Emirates (Dubai), Turkey (Istanbul, Ankara) and Indonesia

(Jakarta).

• Bloomingdales (US): High-end New York retailer opened its

first overseas store in Dubai in February 2010.

• Saks Fifth Avenue (US): Licensed stores now located in

Saudi Arabia (Riyadh, Jeddah), United Arab Emirates

(Dubai), Mexico (Mexico City), Bahrain (Manama)

• Galeries Lafayette (France): Germany (Berlin), United Arab

Emirates (Dubai)

• Harvey Nichols has two new stores planned, in Hong Kong

(2011) and Kuwait (2012).

• Three of London’s most renowned single-outlet department

stores have indicated they may open overseas stores:

• Harrods, recently acquired by Qatar Holdings, is now

considering entry into China, with a store in Shanghai;

• Fortnum & Mason has confirmed that international

expansion is being looked at; likely locations are China, the

Gulf States and, longer term, India;

• Liberty was rumoured to be investigating internationalisation

using money from the sales and leaseback of its iconic

London store in 2009: no plans have yet been announced.

Western department stores head east in search of sales

Routes to Market: Wholesale

Moving east

Looking eastwards

• Faced with sluggish or declining home markets,

department stores in developed regions are now

looking overseas for further growth potential.

• Countries such as the Gulf states, where there is

already an established base of luxury consumers but

where the department stores channel is less saturated,

have been a popular destination; Dubai in the United

Arab Emirates and Riyadh in Saudi Arabia in particular.

• Moves into other developed markets, such as

Selfridges’ entry into Ireland, have become a rarity.

Galeries Lafayette does still operate the Berlin store

that it opened in 1995, but its attempt to enter the US

market failed. Similarly, Japanese banner Mitsukoshi

exited Germany, France and Spain during 2009-2010.

• Now even the most august names in department store

retailing - Liberty, Fortnum & Mason and Harrods - may

be about to move beyond their single-store model.

• For Harrods, in particular, store expansion involves an

additional layer of risk. As one of the world’s leading

super premium department stores, it caters to a highly

cosmopolitan, international consumer base that sees

few difficulties in travelling to London to shop.

• Industry commentators have pointed out that a second

flagship, located in Shanghai, could damage Harrods’

air of exclusivity and, while it might attract more

shoppers of a lower income level, the move might not

find favour with the very richest consumers.

© Euromonitor International

24

Luxury Goods – Brand Routes

• Mitsukoshi (Japan) still operates a store in both Italy

and the US, but is now focused on expansion in Asia,

particularly Taiwan (18 stores) and China (Shanghai).

• Isetan (Japan) expanded into Singapore in 1971, and

now has stores in Thailand, Malaysia, Taiwan and China.

• Lotte Group (South Korea) signed a joint venture with

Intime which resulted in the Intime Lotte Department

Store opening in Beijing, but it recently revealed that it

will be opening some 20 of its own stores by 2018.

• Central Retail Corp (Thailand) launched its first

Chinese department store in 2010; more are planned.

• There is an undeniable interest in the high-growth Chinese

economy from Western luxury department stores, but so far it

is other Asian department store banners that have made

inroads into the market.

• Despite the closure of two underperforming Isetan stores and

occasional flare-ups of anti-Japanese sentiment, China

remains a key focus of owner Isetan-Mitsukoshi’s expansion

plans. The remaining Mitsukoshi stores in Europe and the US

seem increasingly peripheral to the company’s plans.

• Saks Fifth Avenue is arguably the Western banner that has

come closest to entry into China. It signed a licensing

agreement with Roosevelt China Investments Corp in 2006

to develop stores in China and Macau. However, the first

store, due to be opened at a high-profile site in Shanghai,

never launched; thwarted, reportedly, by the economic

downturn, though the subsequent launch of the high-end

House of Roosevelt on the site suggested that Shanghai’s

luxury market still had room to grow.

• US-based Saks might be better off focusing on expansion in

nearby Latin America. It is already present in Mexico, where

the luxury goods market is forecast to grow by 26% to 2015,

but Brazil, where 20% growth to 2015 will add US$1.4 billion

to the market, arguably offers even stronger prospects.

• In contrast, the Chinese market could be a good direction for

Australian department stores David Jones or Myer to move

in; geographically closer than most other first world chains,

they also have experience of Chinese consumers, who

currently make up over 3% of Australia’s population.

Eastern department stores make progress in China

Routes to Market: Wholesale

• Mitsukoshi (Japan) - expanded into a number of

European markets during the 1970s, but withdrew

from Germany (3 stores), France (1 store) and Spain

(1 store) in 2009-2010. The Hong Kong store was

closed in 2006 after 25 years; although it was not an

official market exit, no new store has replaced it.

• Saks Fifth Avenue (US) had planned to enter the

Chinese market with a store in Shanghai’s upmarket

Bund district, but plans reportedly lost momentum as

a result of the economic downturn. The site is now

occupied by House of Roosevelt, a massive wine

merchant/members club/restaurant concept store.

U-turns

East to east

© Euromonitor International

25

Luxury Goods – Brand Routes

-30%

-20%

-10%

0%

10%

20%

Q106

Q206

Q306

Q406

Q107

Q207

Q307

Q407

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q410

Q111

% g

row

th

Neiman Marcus: Store-Based vs Non-Store Sales Q1/06 - Q1/11

Speciality retail stores Direct Marketing division

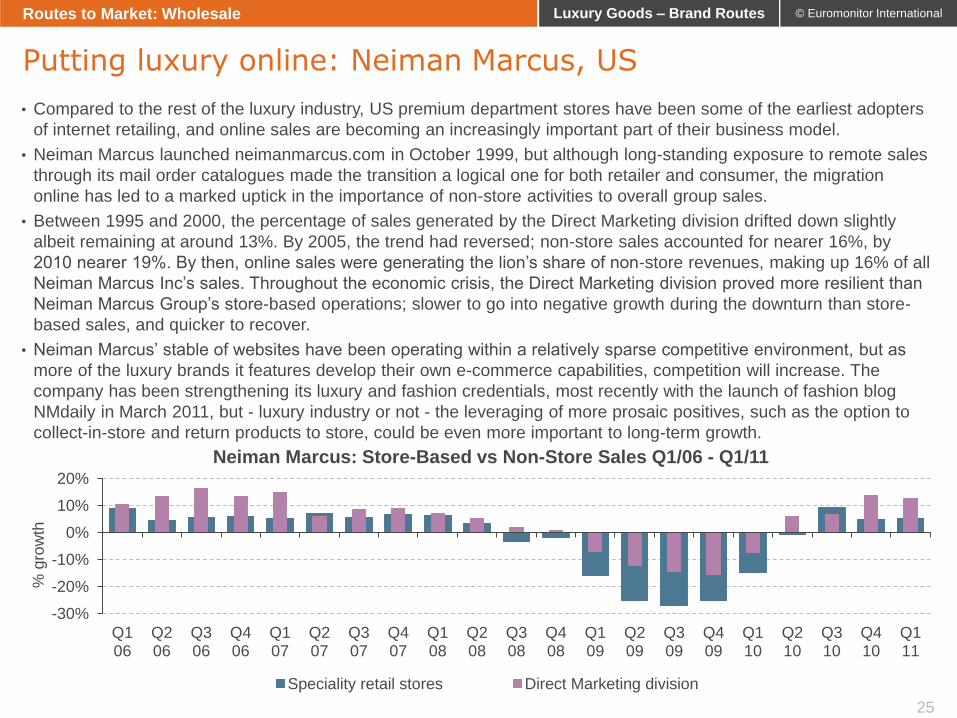

• Compared to the rest of the luxury industry, US premium department stores have been some of the earliest adopters

of internet retailing, and online sales are becoming an increasingly important part of their business model.

• Neiman Marcus launched neimanmarcus.com in October 1999, but although long-standing exposure to remote sales

through its mail order catalogues made the transition a logical one for both retailer and consumer, the migration

online has led to a marked uptick in the importance of non-store activities to overall group sales.

• Between 1995 and 2000, the percentage of sales generated by the Direct Marketing division drifted down slightly

albeit remaining at around 13%. By 2005, the trend had reversed; non-store sales accounted for nearer 16%, by

2010 nearer 19%. By then, online sales were generating the lion’s share of non-store revenues, making up 16% of all

Neiman Marcus Inc’s sales. Throughout the economic crisis, the Direct Marketing division proved more resilient than

Neiman Marcus Group’s store-based operations; slower to go into negative growth during the downturn than store-

based sales, and quicker to recover.

• Neiman Marcus’ stable of websites have been operating within a relatively sparse competitive environment, but as

more of the luxury brands it features develop their own e-commerce capabilities, competition will increase. The

company has been strengthening its luxury and fashion credentials, most recently with the launch of fashion blog

NMdaily in March 2011, but - luxury industry or not - the leveraging of more prosaic positives, such as the option to

collect-in-store and return products to store, could be even more important to long-term growth.

Putting luxury online: Neiman Marcus, US

Routes to Market: Wholesale

© Euromonitor International

26

Luxury Goods – Brand Routes

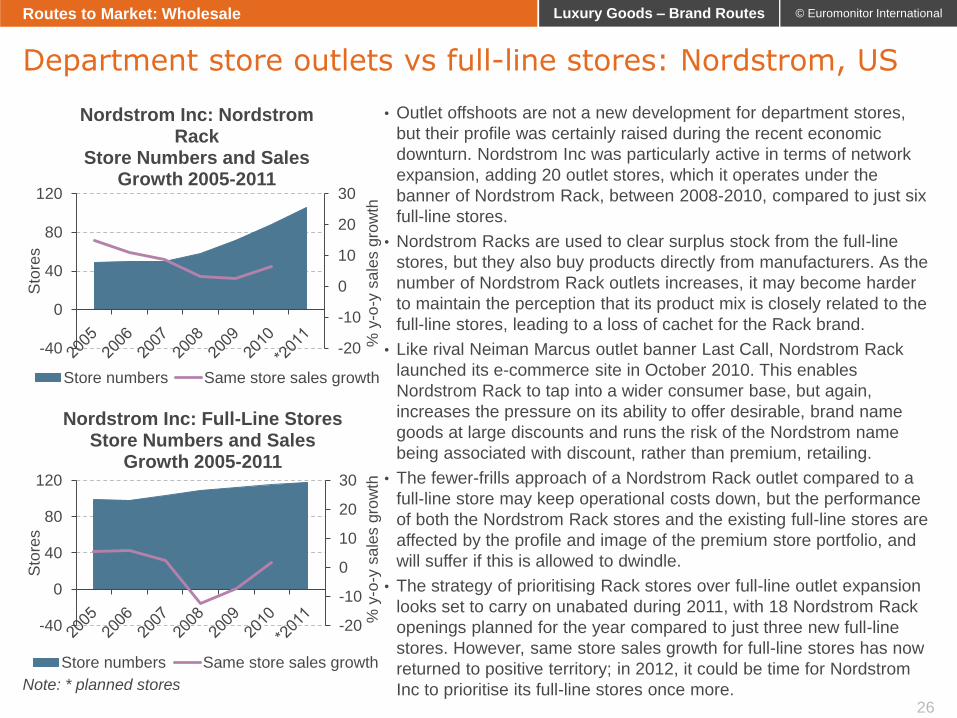

• Outlet offshoots are not a new development for department stores,

but their profile was certainly raised during the recent economic

downturn. Nordstrom Inc was particularly active in terms of network

expansion, adding 20 outlet stores, which it operates under the

banner of Nordstrom Rack, between 2008-2010, compared to just six

full-line stores.

• Nordstrom Racks are used to clear surplus stock from the full-line

stores, but they also buy products directly from manufacturers. As the

number of Nordstrom Rack outlets increases, it may become harder

to maintain the perception that its product mix is closely related to the

full-line stores, leading to a loss of cachet for the Rack brand.

• Like rival Neiman Marcus outlet banner Last Call, Nordstrom Rack

launched its e-commerce site in October 2010. This enables

Nordstrom Rack to tap into a wider consumer base, but again,

increases the pressure on its ability to offer desirable, brand name

goods at large discounts and runs the risk of the Nordstrom name

being associated with discount, rather than premium, retailing.

• The fewer-frills approach of a Nordstrom Rack outlet compared to a

full-line store may keep operational costs down, but the performance

of both the Nordstrom Rack stores and the existing full-line stores are

affected by the profile and image of the premium store portfolio, and

will suffer if this is allowed to dwindle.

• The strategy of prioritising Rack stores over full-line outlet expansion

looks set to carry on unabated during 2011, with 18 Nordstrom Rack

openings planned for the year compared to just three new full-line

stores. However, same store sales growth for full-line stores has now

returned to positive territory; in 2012, it could be time for Nordstrom

Inc to prioritise its full-line stores once more.

Department store outlets vs full-line stores: Nordstrom, US

Routes to Market: Wholesale

-20

-10

0

10

20

30

-40

0

40

80

120

% y

-o-y

sa

les g

row

th

Sto

res

Nordstrom Inc: Nordstrom Rack

Store Numbers and Sales Growth 2005-2011

Store numbers Same store sales growth

-20

-10

0

10

20

30

-40

0

40

80

120

% y

-o-y

sa

les g

row

th

Sto

res

Nordstrom Inc: Full-Line Stores Store Numbers and Sales

Growth 2005-2011

Store numbers Same store sales growth

Note: * planned stores

© Euromonitor International

27

Luxury Goods – Brand Routes

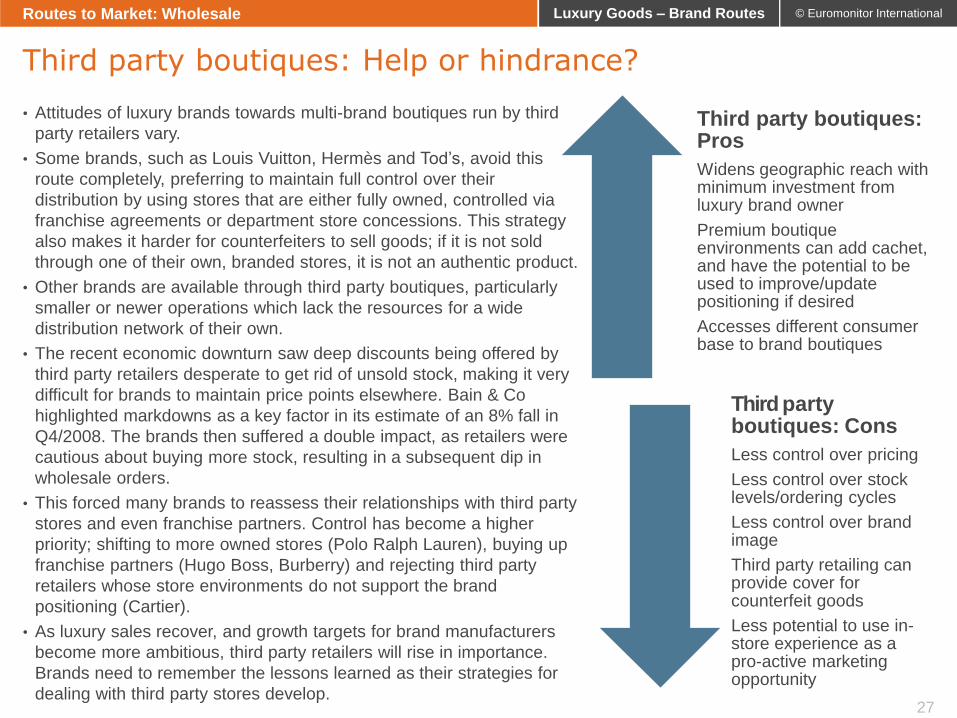

Third party boutiques: Pros

Widens geographic reach with minimum investment from luxury brand owner

Premium boutique environments can add cachet, and have the potential to be used to improve/update positioning if desired

Accesses different consumer base to brand boutiques

Third party boutiques: Cons

Less control over pricing

Less control over stock levels/ordering cycles

Less control over brand image

Third party retailing can provide cover for counterfeit goods

Less potential to use in-store experience as a pro-active marketing opportunity

• Attitudes of luxury brands towards multi-brand boutiques run by third

party retailers vary.

• Some brands, such as Louis Vuitton, Hermès and Tod’s, avoid this

route completely, preferring to maintain full control over their

distribution by using stores that are either fully owned, controlled via

franchise agreements or department store concessions. This strategy

also makes it harder for counterfeiters to sell goods; if it is not sold

through one of their own, branded stores, it is not an authentic product.

• Other brands are available through third party boutiques, particularly

smaller or newer operations which lack the resources for a wide

distribution network of their own.

• The recent economic downturn saw deep discounts being offered by

third party retailers desperate to get rid of unsold stock, making it very

difficult for brands to maintain price points elsewhere. Bain & Co

highlighted markdowns as a key factor in its estimate of an 8% fall in

Q4/2008. The brands then suffered a double impact, as retailers were

cautious about buying more stock, resulting in a subsequent dip in

wholesale orders.

• This forced many brands to reassess their relationships with third party

stores and even franchise partners. Control has become a higher

priority; shifting to more owned stores (Polo Ralph Lauren), buying up

franchise partners (Hugo Boss, Burberry) and rejecting third party

retailers whose store environments do not support the brand

positioning (Cartier).

• As luxury sales recover, and growth targets for brand manufacturers

become more ambitious, third party retailers will rise in importance.

Brands need to remember the lessons learned as their strategies for

dealing with third party stores develop.

Third party boutiques: Help or hindrance?

Routes to Market: Wholesale

© Euromonitor International

28

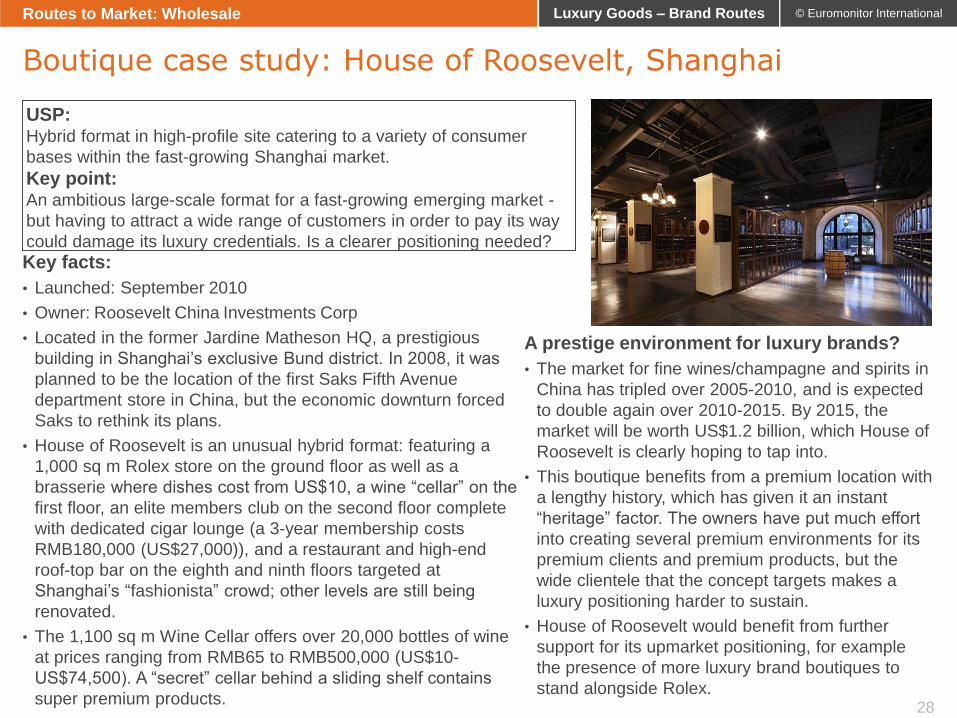

Luxury Goods – Brand Routes

A prestige environment for luxury brands?

• The market for fine wines/champagne and spirits in

China has tripled over 2005-2010, and is expected

to double again over 2010-2015. By 2015, the

market will be worth US$1.2 billion, which House of

Roosevelt is clearly hoping to tap into.

• This boutique benefits from a premium location with

a lengthy history, which has given it an instant

“heritage” factor. The owners have put much effort

into creating several premium environments for its

premium clients and premium products, but the

wide clientele that the concept targets makes a

luxury positioning harder to sustain.

• House of Roosevelt would benefit from further

support for its upmarket positioning, for example

the presence of more luxury brand boutiques to

stand alongside Rolex.

Boutique case study: House of Roosevelt, Shanghai

Routes to Market: Wholesale

USP: Hybrid format in high-profile site catering to a variety of consumer

bases within the fast-growing Shanghai market.

Key point: An ambitious large-scale format for a fast-growing emerging market -

but having to attract a wide range of customers in order to pay its way

could damage its luxury credentials. Is a clearer positioning needed?

Key facts:

• Launched: September 2010

• Owner: Roosevelt China Investments Corp

• Located in the former Jardine Matheson HQ, a prestigious

building in Shanghai’s exclusive Bund district. In 2008, it was

planned to be the location of the first Saks Fifth Avenue

department store in China, but the economic downturn forced

Saks to rethink its plans.

• House of Roosevelt is an unusual hybrid format: featuring a

1,000 sq m Rolex store on the ground floor as well as a

brasserie where dishes cost from US$10, a wine “cellar” on the

first floor, an elite members club on the second floor complete

with dedicated cigar lounge (a 3-year membership costs

RMB180,000 (US$27,000)), and a restaurant and high-end

roof-top bar on the eighth and ninth floors targeted at

Shanghai’s “fashionista” crowd; other levels are still being

renovated.

• The 1,100 sq m Wine Cellar offers over 20,000 bottles of wine

at prices ranging from RMB65 to RMB500,000 (US$10-

US$74,500). A “secret” cellar behind a sliding shelf contains

super premium products.

© Euromonitor International

29

Luxury Goods – Brand Routes

A prestige environment for luxury brands?

• Colette’s regular updating of its in-store range puts any

brand on its shelves firmly “on trend”; a valuable

attribute even for established luxury brands.

• However, the Colette product range is perhaps so

special that it is difficult for brands to stand out, which

may explain the number of exclusive collaborations

that the store is able to garner, not to mention other

initiatives such as limited-time shop-in-shops.

• Colette has even managed to transfer some of its

unique cachet online, with the help of numerous blogs,

and should benefit from its international reputation

though, as in the store, relatively few customers will be

able to afford the fashion on offer.

• However, does Colette risk becoming a victim of its

own success if its reputation begins to attract too many

“ordinary” visitors, diluting the “street” atmosphere?

Boutique case study: Colette, Paris

Routes to Market: Wholesale

USP: Achingly hip boutique which has built an international reputation through

its mix of luxury products and street-style brands across a variety of price

points. Essentially, Colette sells style, rather than products.

Key point: Colette covers a wide price range, but the concept has a clear positioning

in terms of the style-savvy customer it targets. The weakness in its

business model comes from the reliance on its founders, who still control

the selection of products. No further stores are planned, and even the

current store could struggle to maintain its profile if it changed ownership.

Key facts:

• Launched in March 1997 by mother-and-daughter team

Colette Roussaux and Sarah Lerfel.

• Located at 213 Rue Saint-Honoré, in a district of Paris

known for its fashion and luxury offer.

• Collette comprises of three floors covering 740 sq m. The

ground floor offers streetwear labels, as well as gifts,

gadgets and CDs; upstairs is devoted to luxury clothing by

both established brands and cutting edge emerging

designers while the lower level is a fashionable bar, which

only serves water (over 100 kinds). The store also

regularly hosts exhibitions by artists and designers.

• Colette is also known for its exclusive collaborations with

fashion designers and other celebrities; it was also

recently chosen as one of only four outlets in the world to

stock US apparel market leader Gap’s collaboration with

Valentino.

© Euromonitor International

30

Luxury Goods – Brand Routes

Introduction

Luxury Market Overview

Routes to Market: Wholesale

Routes to Market: Retail

Routes to Market: Online

Case Study: Polo Ralph Lauren Corp

Conclusion

© Euromonitor International

31

Luxury Goods – Brand Routes

Wh

ole

sa

le

• Definition: Sales through third party distributors

• Traditional formats: Department stores, boutiques

• Emerging formats: Outlet stores, e-boutiques

• Many luxury brands moved away from wholesaling during the recession as retailers began implementing steep discounts.

• The once-key department store channel is suffering a decline so luxury brands are wise to explore other options.

• Outlet stores, factory shops and online boutiques such as Net-A-Porter offer growth at both the lower and upper ends of the luxury market.

Re

tail

• Definition: Distribution managed in-house

• Traditional formats: Company owned/ franchised branded stores

• Emerging formats: Brand websites, social networks

• Company owned/ franchised stores allow brands to control pricing, but as luxury’s international consumer base widens, their contribution to creating and maintaining a brand image may be even more crucial.

• Websites and social networking presence are increasingly recognised as another important brand imaging tool, with the potential to bring new consumers into stores.

Inte

rne

t R

eta

il

• Definition: Sales transactions are completed online. Can operate as both a retail and wholesale distribution channel

• Traditional formats: Websites operated by established retailers such as department stores, wine clubs; fashion e-boutiques

• Emerging formats: Transactional branded websites, luxury outlet e-stores, m-commerce, iPad applications, social networking

• The use of websites as brand showcases is relatively well established, but the internet is only now gathering momentum as a luxury distribution channel.

Routes to market: Retail formats

Routes to Market: Retail

Definitions are for the purposes of this report. Company-specific definitions may vary

© Euromonitor International

32

Luxury Goods – Brand Routes

Luxury retail: The good

Luxury retail: The bad

Luxury retail: Risk and rewards

Routes to Market: Retail

• There has been a shift towards retail sales, where

distribution is controlled by the company itself, in

recent years; even to the extent of some brands

buying up franchised stores.

• The ability to retain control over pricing has been

an important element of this, after deep discounting

by third party retailers in the wake of the economic

downturn damaged some wholesale relationships.

• Having closed between 120-140 wholesale

accounts in the US that it felt were

underperforming, Cartier, for example, was able to

prioritise its own stores, and better support

wholesale retailers that were performing strongly

and supporting brand positioning.

• Controlling its own stores also gives companies

more control over brand image and direct contact

with consumers.

• Several brands have recently also taken control of

distribution in the Chinese market which should

help to differentiate the label within an increasingly

competitive market.

• Large-scale expansion remains difficult for brands

bearing all the set up and running costs

themselves, but the internet is now widening

options for international sales, not only through

transactional websites but also through initiatives

such as live catwalk streaming and social

networking sites.

Direct customer contact

© Euromonitor International

33

Luxury Goods – Brand Routes

• 2009 was a bad year for wholesale luxury

distribution, with massive drops in sales posted by

some of the leading luxury groups; a development

that looks even worse when viewed alongside a

much more positive growth trend for company-

controlled retail activity.

• Better store environments and avoidance of

discounting were some of the reasons for retail’s

stronger performance, along with the ongoing

expansion of company-controlled store networks.

• Luxury brands were hit by a fall in wholesale orders,

made worse in some cases by stock being withheld

from wholesale customers considered to be risky,

and restrictions on inventory at third party retailers in

order to maintain exclusivity and limit discounting.

• Wholesale revenues are now widely reported to be improving

(though this may in part be due to greater control over

inventory levels and pricing by brands), but the shift towards

directly-operated stores is still evident.

• A secondary trend during 2009-2010 was the appearance of

more flagship stores, from Burberry’s high-tech Beijing store

to Louis Vuitton’s Maison London. The value of these stores

is to promote the brand to both domestic and overseas

consumers, as much, if not more, than any effect on sales.

• Obvious benefits of directly-operated stores include greater

control over store environment and pricing, higher margins

on sales and less vulnerability to weak retail partners. They

also give brands more control over their image, and foster

customer relationships through face-to-face contact; factors

which will become more important as online selling grows.

Shift to owned stores keeps brands close to consumers

Routes to Market: Retail

“The best communication

vehicle we have is the stores.”

Patrizio di Marco, President

and CEO, Gucci

“Louis Vuitton and Hermès

control their distribution

channel from A to Z and they

don’t discount.”

Milton Pedraza, Chief

Executive of the Luxury

Institute

-30

-20

-10

0

10

20

Prada (YE January2010)*

Polo Ralph Lauren (YEApril 2010)

Hugo Boss (YEDecember 2009)

% y

-o-y

gro

wth

Wholesale vs Retail Growth 2009

Retail Wholesale* wholesale figures include 35

franchised stores/2009

© Euromonitor International

34

Luxury Goods – Brand Routes

Flagship stores support high-end luxury positioning

Routes to Market: Retail

• Luxury brand flagship stores formed another clear trend in 2010,

mainly driven by brands’ need to re-emphasise their high-end

positioning and target the more resilient super-rich market.

• Rents and occupation levels at the best retail locations remained

stable during the downturn, but many retail development projects

were put on hold. This limited the number of suitable mall-based

locations for premium brands, and made them more aggressive

about securing good standalone sites.

• Flagships complement another current trend, of offering in-store

experiences in order to add value of the brand in consumers’

eyes. The Gucci Artisan Tour, for example, which sets up in-store

workshops so customers can see the detail that goes into the

products, will be finishing at the brand’s Fifth Avenue, New York,

flagship store in April 2011.

• Despite the headline growth of the Chinese market, many of

2010’s flagship openings were in developed regions. However,

impressing and attracting overseas customers is an important

part of the function of such stores, particularly as many Chinese

visitors prefer to buy abroad in order to avoid high luxury taxes.

• In the future, flagships may not always be physical stores, as the

launch of the Gucci.com “digital flagship” demonstrates.

• “The more we elevate our stores and the merchandise mix, the stronger the customer response.” Polo Ralph

Lauren, Q3/2011

• “Success of upscale positioning strategy.” One reason given by Gucci for a strong rise in fiscal 2010 sales

• “Sharp turnaround in profitability fuelled by Couture.” YSL accounts for a 13% rise in fiscal 2010 revenues

• "We will invest more in turning old stores into flagship-style stores in the next five years rather than opening up new

stores, because you need to keep Fendi really in the high end.” Fendi CEO Michael Burke, 2009

Major flagship openings in 2010:

• London, May: Louis Vuitton’s new Maison in

prestigious New Bond Street opens its doors.

• Milan, September: Jimmy Choo’s new flagship

features its first European VIP room.

• Beijing, October: Emporio Armani unveils 5-

storey, 1,600 sq m site.

• New York, October: Ralph Lauren opens flagship

for womenswear and home collections.

• Hong Kong, November: Cartier replaces 40-year-

old store with a much-enlarged flagship.

• Beijing, November: Hublot’s first standalone

flagship in China.

• Paris, November: Hermès opens a new home

market flagship, but with an eye on tourist spend.

• New York, December: Dior reopens its 57th

Street flagship after extensive renovations.

• London, December: New Bond Street welcomes

another flagship: accessories brand Mulberry.

© Euromonitor International

35

Luxury Goods – Brand Routes

• Opening stores in away-from-home locations,

such as travel environments, gives luxury

brands the opportunity to target luxury

consumers at a time when they are likely to

have time on their hands, are likely to be

looking for gifting purchases and there are

fewer non-retail distractions.

• Duty-free areas are the obvious example, and

these locations offer some very distinct,

advantages. They distil the luxury potential of

an airport’s catchment area, by providing a

single location - free of taxes - that almost all

luxury consumers must pass through if they

travel. Moreover, they can operate separately

from the market where they are geographically

located.

• Leading global drinks company Diageo has

tapped into this in Dubai, first by offering one-to-

one tasting sessions for its most luxury brands,

and then by opening Emporium, a luxury

cocktail bar/retail concept store in December

2010, in association with Moët Hennessy.

• The Middle East is seen as a region with

untapped potential for luxury alcohol sales, but

there are issues over religious sensitivities. As

Dubai Airports CEO Paul Griffiths pointed out

however, “We see the airport environment as

separate and distinct from the local market.”

Capturing the consumer: Luxury retail in travel locations

Routes to Market: Retail

-40

-20

0

20

40

60

0 20 40 60 80 100 120 140

% g

row

th in to

urist e

xp

en

ditu

re o

n s

ho

pp

ing 2

00

8-2

01

0

Departures + arrivals 2010 (million trips)

Tourism Flows vs Expenditure on Shopping 2008-2010

China

Hong Kong, CN

India

Japan

Malaysia

Singapore

South Korea

Australia

Poland

Russia

Brazil

Mexico

Saudi Arabia

South Africa

UAE

Canada

USA

France

Germany

Italy

Norway

Portugal

Spain

Sweden

Switzerland

UK

Bubble size represents tourist expenditure on shopping 2010

© Euromonitor International

36

Luxury Goods – Brand Routes

• Top hotels offer a captive audience of high-income consumers, which

have long attracted luxury brands. Hotel retail offers brands insight

into the tastes and preferences of a very tightly-targeted demographic.

• Like duty-free areas, they are also able to exist apart from the local

economic and retail environment, because, by definition, luxury hotels

already provide the right demographic of high-earning individuals.

• Hotels such as The Peninsula in Hong Kong (est. 1928) created some

of the earliest versions of luxury malls; the shopping arcade in The

Peninsula still house over 80 shops, including Louis Vuitton, Chanel

and Prada.

• In emerging markets, high-end hotels are still key locations for luxury

brand retail, partly because of the way they target HNWIs, but also

because they represent safe, secure and luxurious retail

environments, which may otherwise be in short supply.

• India is a typical example: it is viewed as one of the highest potential

luxury markets in the world, but the lack of luxury retail malls has

prevented brands from expanding as fast as they would like. Luxury

malls only appeared in the Indian market in 2008, and are still only

present in the very largest cities: the DLF Emporio in Delhi, UB City in

Bangalore and Palladium in Mumbai. However, 35% of hotel spend is

in luxury grade accommodation, and as luxury brands look to widen

their presence in other cities, premium hotels remain one of their few

store location options.

• Combining the elements of luxury hotels with duty-free retail, luxury

cruise liner passengers are perhaps the ultimate captive luxury

audience. Here too, luxury brands have looked for retail opportunities:

the Mayfair shopping arcade on Cunard’s latest luxury liner, the

Queen Mary 2, includes Hermès and Chopard stores.

The original luxury store location: High-end hotels

Routes to Market: Retail

0 25 50 75 100

FranceChinaJapan

MalaysiaCanadaTurkey

GermanyPoland

South AfricaUK

ItalySaudi Arabia

RussiaIndia

SpainSwitzerland

SingaporeSouth Korea

SwedenBrazil

PortugalAustralia

Hong Kong, CNUSA

MexicoUAE

% of total expenditure

Expenditure on Luxury Hotels as a Percentage of Total Expenditure on Hotels

2008/2010

2008

2010

© Euromonitor International

37

Luxury Goods – Brand Routes

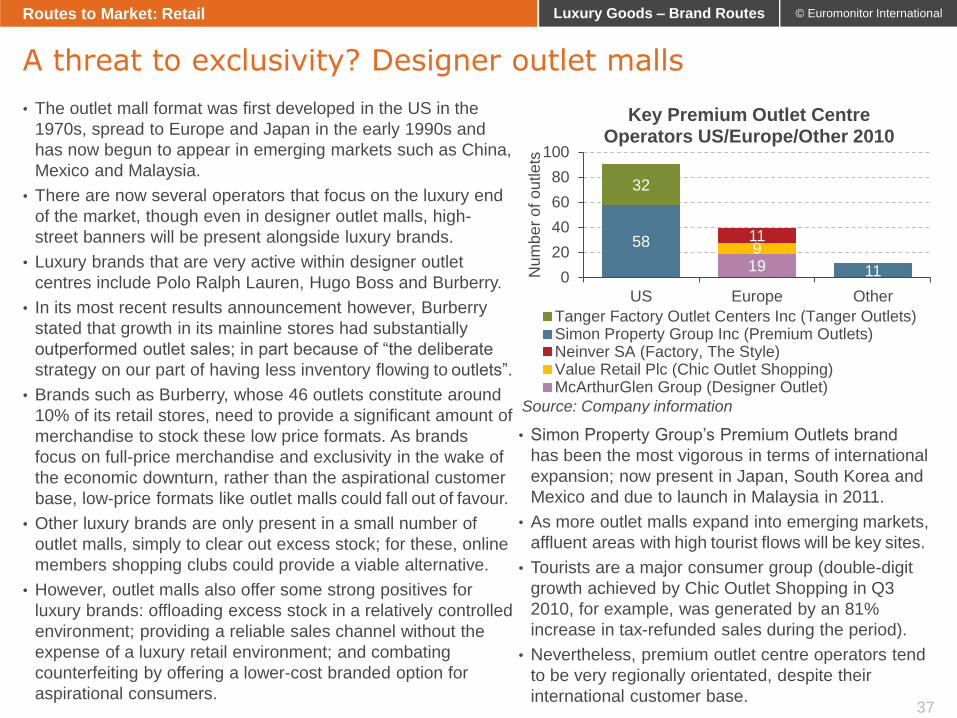

• The outlet mall format was first developed in the US in the

1970s, spread to Europe and Japan in the early 1990s and

has now begun to appear in emerging markets such as China,

Mexico and Malaysia.

• There are now several operators that focus on the luxury end

of the market, though even in designer outlet malls, high-

street banners will be present alongside luxury brands.

• Luxury brands that are very active within designer outlet

centres include Polo Ralph Lauren, Hugo Boss and Burberry.

• In its most recent results announcement however, Burberry

stated that growth in its mainline stores had substantially

outperformed outlet sales; in part because of “the deliberate

strategy on our part of having less inventory flowing to outlets”.

• Brands such as Burberry, whose 46 outlets constitute around

10% of its retail stores, need to provide a significant amount of

merchandise to stock these low price formats. As brands

focus on full-price merchandise and exclusivity in the wake of

the economic downturn, rather than the aspirational customer

base, low-price formats like outlet malls could fall out of favour.

• Other luxury brands are only present in a small number of

outlet malls, simply to clear out excess stock; for these, online

members shopping clubs could provide a viable alternative.

• However, outlet malls also offer some strong positives for

luxury brands: offloading excess stock in a relatively controlled

environment; providing a reliable sales channel without the

expense of a luxury retail environment; and combating

counterfeiting by offering a lower-cost branded option for

aspirational consumers.

• Simon Property Group’s Premium Outlets brand

has been the most vigorous in terms of international

expansion; now present in Japan, South Korea and

Mexico and due to launch in Malaysia in 2011.

• As more outlet malls expand into emerging markets,

affluent areas with high tourist flows will be key sites.

• Tourists are a major consumer group (double-digit

growth achieved by Chic Outlet Shopping in Q3

2010, for example, was generated by an 81%

increase in tax-refunded sales during the period).

• Nevertheless, premium outlet centre operators tend

to be very regionally orientated, despite their

international customer base.

A threat to exclusivity? Designer outlet malls

Routes to Market: Retail

19 9 11 58

11

32

0

20

40

60

80

100

US Europe Other

Num

be

r o

f o

utle

ts

Key Premium Outlet Centre Operators US/Europe/Other 2010

Tanger Factory Outlet Centers Inc (Tanger Outlets)Simon Property Group Inc (Premium Outlets)Neinver SA (Factory, The Style)Value Retail Plc (Chic Outlet Shopping)McArthurGlen Group (Designer Outlet)

Source: Company information

© Euromonitor International

38

Luxury Goods – Brand Routes

Introduction

Luxury Market Overview

Routes to Market: Wholesale

Routes to Market: Retail

Routes to Market: Online

Case Study: Polo Ralph Lauren Corp

Conclusion

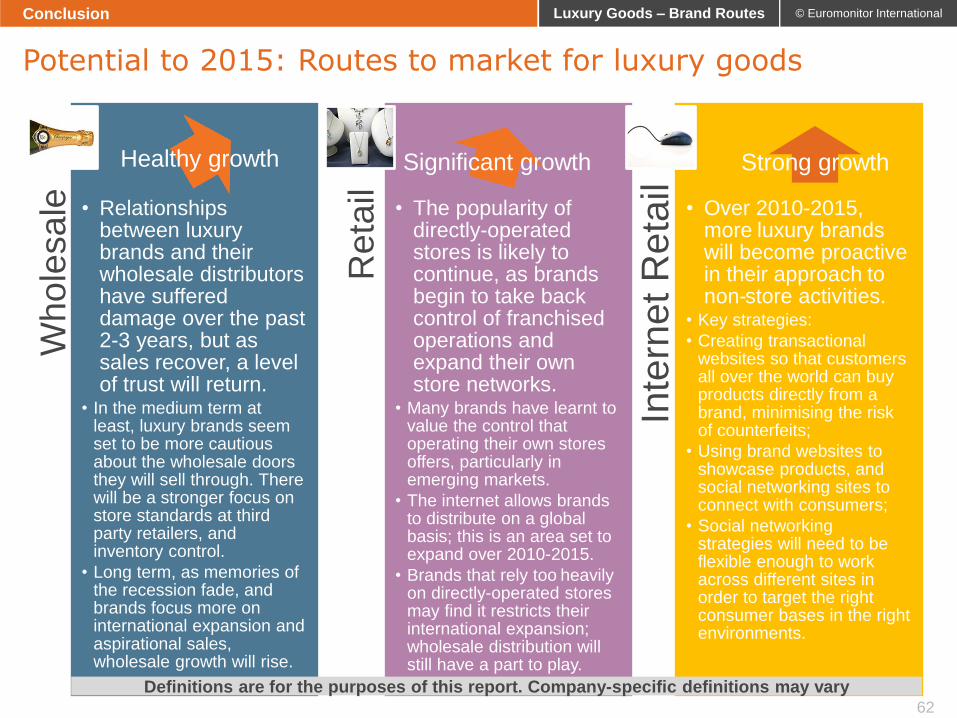

© Euromonitor International

39

Luxury Goods – Brand Routes

Wh

ole

sa

le

• Definition: Sales through third party distributors

• Traditional formats: Department stores, boutiques

• Emerging formats: Outlet stores, e-boutiques

• Many luxury brands moved away from wholesaling during the recession as retailers began implementing steep discounts.

• The once-key department store channel is suffering a decline so luxury brands are wise to explore other options.

• Outlet stores, factory shops and online boutiques such as Net-A-Porter offer growth at both the lower and upper ends of the luxury market.

Re

tail

• Definition: Distribution managed in-house

• Traditional formats: Company owned/ franchised branded stores

• Emerging formats: Brand websites, social networks

• Company owned/ franchised stores allow brands to control pricing, but as luxury’s international consumer base widens, their contribution to creating and maintaining a brand image may be even more crucial.

• Websites and social networking presence are increasingly recognised as another important brand imaging tool, with the potential to bring new consumers into stores.

In

tern

et R

eta

il

• Definition: Sales transactions are completed online. Can operate as both a retail and wholesale distribution channel

• Traditional formats: Websites operated by established retailers such as department stores, wine clubs; fashion e-boutiques

• Emerging formats: Transactional branded websites, luxury outlet e-stores, m-commerce, iPad applications, social networking

• The use of websites as brand showcases is relatively well-established, but the internet is only now gathering momentum as a luxury distribution channel.

Routes to market: Online formats

Routes to Market: Online

Definitions are for the purposes of this report. Company-specific definitions may vary

© Euromonitor International

40

Luxury Goods – Brand Routes

Luxury online: The good

Luxury online: The bad

Luxury brand transactional websites: Risk and rewards

Routes to Market: Online

• Questions over whether luxury goods

could be successfully sold online have

largely been answered by the success

of sites such as Net-A-Porter and the

growth being seen by department stores

for their online activities.

• The internet’s potential to showcase

brands is already being explored; for

some categories, such as fine wines

and jewellery, informative websites can

help to dispel “boutique fear”, helping

new customers (particularly in emerging

markets) to discuss prospective

purchases more knowledgeably.

• For brands which suffer badly from

counterfeiting, such as Louis Vuitton,

the internet allows them to sell to more

customers without ceding control of any

of the distribution or bearing the

expense of a multitude of new stores,

but internet sales via third parties could

equally lead to a rise in counterfeiting.

• For luxury brands, the decision to sell

via their own, branded, website, is a

difficult one. Can the channel provide

enough of a luxury level experience to

maintain price levels in the long term?

Attracts boutique-shy customers

© Euromonitor International

41

Luxury Goods – Brand Routes

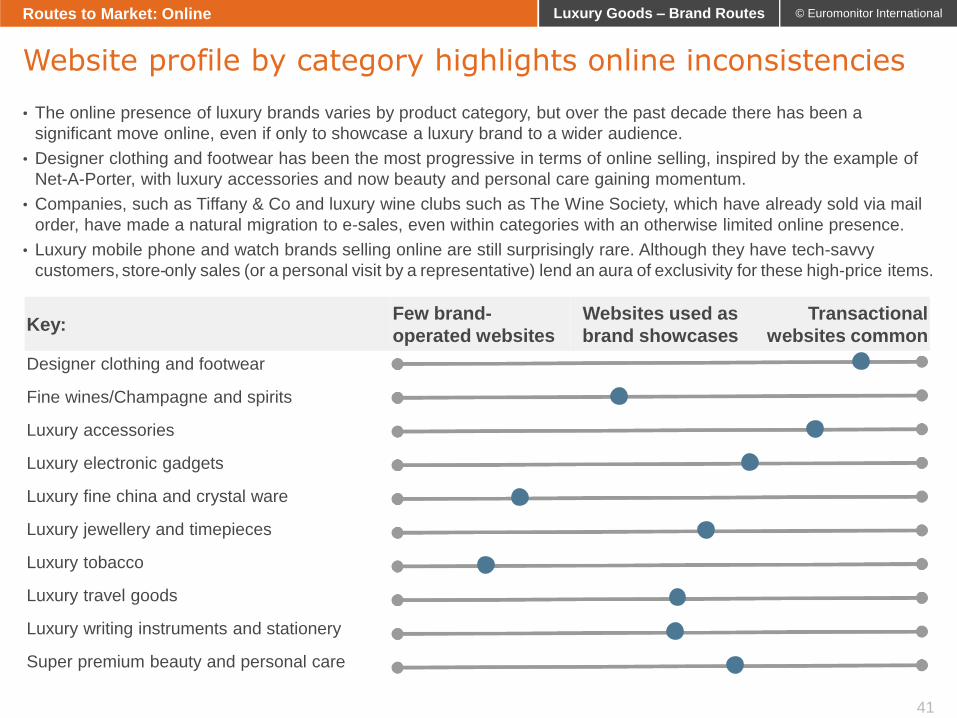

• The online presence of luxury brands varies by product category, but over the past decade there has been a

significant move online, even if only to showcase a luxury brand to a wider audience.

• Designer clothing and footwear has been the most progressive in terms of online selling, inspired by the example of

Net-A-Porter, with luxury accessories and now beauty and personal care gaining momentum.

• Companies, such as Tiffany & Co and luxury wine clubs such as The Wine Society, which have already sold via mail

order, have made a natural migration to e-sales, even within categories with an otherwise limited online presence.

• Luxury mobile phone and watch brands selling online are still surprisingly rare. Although they have tech-savvy

customers, store-only sales (or a personal visit by a representative) lend an aura of exclusivity for these high-price items.

Website profile by category highlights online inconsistencies

Routes to Market: Online

Key: Few brand-

operated websites

Websites used as

brand showcases

Transactional

websites common

Designer clothing and footwear

Fine wines/Champagne and spirits

Luxury accessories

Luxury electronic gadgets

Luxury fine china and crystal ware

Luxury jewellery and timepieces

Luxury tobacco

Luxury travel goods

Luxury writing instruments and stationery

Super premium beauty and personal care

© Euromonitor International

42

Luxury Goods – Brand Routes

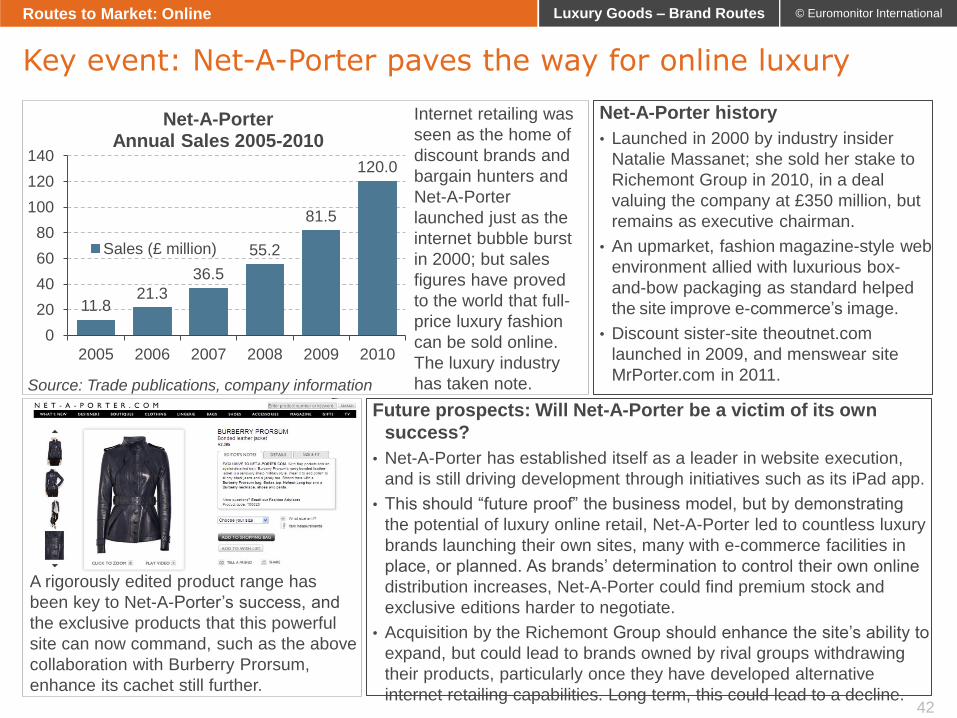

Internet retailing was

seen as the home of

discount brands and

bargain hunters and

Net-A-Porter

launched just as the

internet bubble burst

in 2000; but sales

figures have proved

to the world that full-

price luxury fashion

can be sold online.

The luxury industry

has taken note.

11.8 21.3

36.5

55.2

81.5

120.0

0

20

40

60

80

100

120

140

2005 2006 2007 2008 2009 2010

Net-A-Porter Annual Sales 2005-2010

Sales (£ million)

Key event: Net-A-Porter paves the way for online luxury

Routes to Market: Online

A rigorously edited product range has

been key to Net-A-Porter’s success, and

the exclusive products that this powerful

site can now command, such as the above

collaboration with Burberry Prorsum,

enhance its cachet still further.

Future prospects: Will Net-A-Porter be a victim of its own

success?

• Net-A-Porter has established itself as a leader in website execution,

and is still driving development through initiatives such as its iPad app.

• This should “future proof” the business model, but by demonstrating

the potential of luxury online retail, Net-A-Porter led to countless luxury

brands launching their own sites, many with e-commerce facilities in

place, or planned. As brands’ determination to control their own online

distribution increases, Net-A-Porter could find premium stock and

exclusive editions harder to negotiate.

• Acquisition by the Richemont Group should enhance the site’s ability to

expand, but could lead to brands owned by rival groups withdrawing

their products, particularly once they have developed alternative

internet retailing capabilities. Long term, this could lead to a decline.

Net-A-Porter history

• Launched in 2000 by industry insider

Natalie Massanet; she sold her stake to

Richemont Group in 2010, in a deal

valuing the company at £350 million, but

remains as executive chairman.

• An upmarket, fashion magazine-style web

environment allied with luxurious box-

and-bow packaging as standard helped

the site improve e-commerce’s image.

• Discount sister-site theoutnet.com

launched in 2009, and menswear site

MrPorter.com in 2011.

Source: Trade publications, company information

© Euromonitor International

43

Luxury Goods – Brand Routes

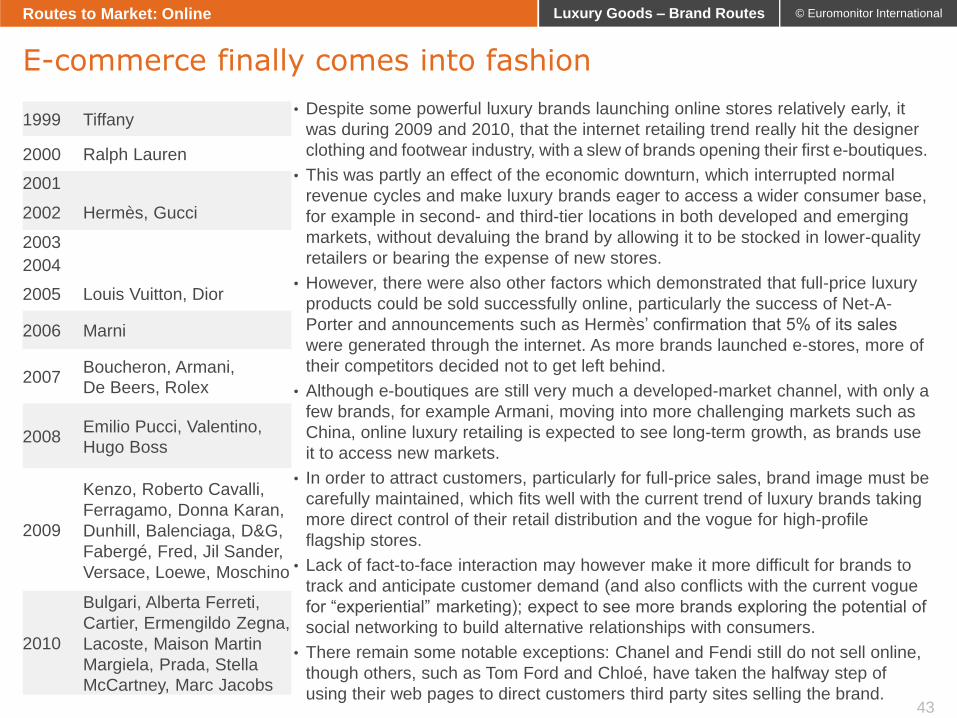

1999 Tiffany

2000 Ralph Lauren

2001

2002 Hermès, Gucci

2003

2004

2005 Louis Vuitton, Dior

2006 Marni

2007 Boucheron, Armani,

De Beers, Rolex

2008 Emilio Pucci, Valentino,

Hugo Boss

2009

Kenzo, Roberto Cavalli,

Ferragamo, Donna Karan,

Dunhill, Balenciaga, D&G,