m a l a y s i a - united...

TRANSCRIPT

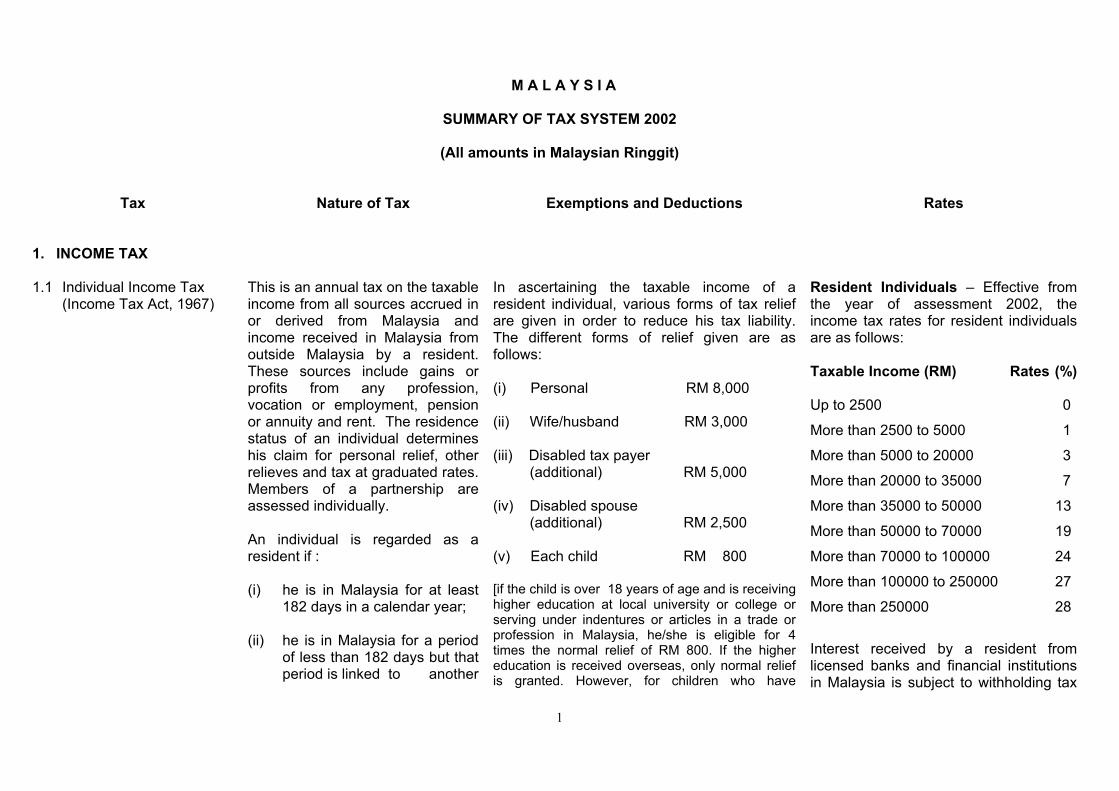

M A L A Y S I A

SUMMARY OF TAX SYSTEM 2002

(All amounts in Malaysian Ringgit)

Tax Nature of Tax Exemptions and Deductions Rates

1. INCOME TAX 1.1 Individual Income Tax

(Income Tax Act, 1967)

This is an annual tax on the taxable income from all sources accrued in or derived from Malaysia and income received in Malaysia from outside Malaysia by a resident. These sources include gains or profits from any profession, vocation or employment, pension or annuity and rent. The residence status of an individual determines his claim for personal relief, other relieves and tax at graduated rates. Members of a partnership are assessed individually. An individual is regarded as a resident if : (i) he is in Malaysia for at least

182 days in a calendar year; (ii) he is in Malaysia for a period

of less than 182 days but that period is linked to another

In ascertaining the taxable income of a resident individual, various forms of tax relief are given in order to reduce his tax liability. The different forms of relief given are as follows: (i) Personal RM 8,000 (ii) Wife/husband RM 3,000 (iii) Disabled tax payer (additional) RM 5,000 (iv) Disabled spouse (additional) RM 2,500 (v) Each child RM 800 [if the child is over 18 years of age and is receiving higher education at local university or college or serving under indentures or articles in a trade or profession in Malaysia, he/she is eligible for 4 times the normal relief of RM 800. If the higher education is received overseas, only normal relief is granted. However, for children who have

Resident Individuals – Effective from the year of assessment 2002, the income tax rates for resident individuals are as follows: Taxable Income (RM) Rates (%) Up to 2500 0

More than 2500 to 5000 1

More than 5000 to 20000 3 More than 20000 to 35000 7

More than 35000 to 50000 13

More than 50000 to 70000 19

More than 70000 to 100000 24

More than 100000 to 250000 27

More than 250000 28 Interest received by a resident from licensed banks and financial institutions in Malaysia is subject to withholding tax

1

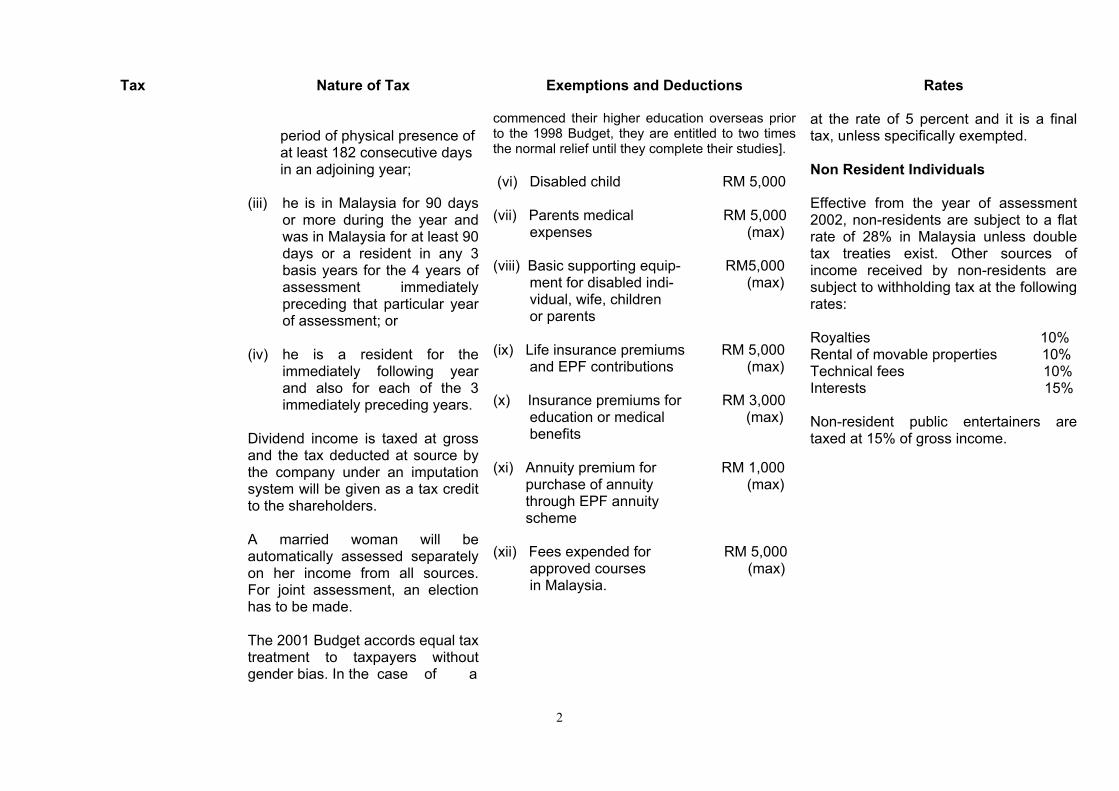

Tax Nature of Tax Exemptions and Deductions Rates

period of physical presence of at least 182 consecutive days in an adjoining year; (iii) he is in Malaysia for 90 days

or more during the year and was in Malaysia for at least 90 days or a resident in any 3 basis years for the 4 years of assessment immediatelypreceding that particular year of assessment; or

ment for disabled indi- (max)

(iv) he is a resident for the

immediately following year and also for each of the 3 immediately preceding years.

Dividend income is taxed at gross and the tax deducted at source by the company under an imputation system will be given as a tax credit to the shareholders. A married woman will be automatically assessed separately on her income from all sources. For joint assessment, an election has to be made. The 2001 Budget accords equal tax treatment to taxpayers without gender bias. In the case of a

commenced their higher education overseas prior to the 1998 Budget, they are entitled to two times the normal relief until they complete their studies]. (vi) Disabled child RM 5,000 (vii) Parents medical RM 5,000 expenses (max) (viii) Basic supporting equip- RM5,000

vidual, wife, children or parents (ix) Life insurance premiums RM 5,000 and EPF contributions (max) (x) Insurance premiums for RM 3,000 education or medical (max) benefits (xi) Annuity premium for RM 1,000 purchase of annuity (max) through EPF annuity scheme (xii) Fees expended for RM 5,000 approved courses (max) in Malaysia.

at the rate of 5 percent and it is a final tax, unless specifically exempted. Non Resident Individuals Effective from the year of assessment 2002, non-residents are subject to a flat rate of 28% in Malaysia unless double tax treaties exist. Other sources of income received by non-residents are subject to withholding tax at the following rates: Royalties 10% Rental of movable properties 10% Technical fees 10% Interests 15% Non-resident public entertainers are taxed at 15% of gross income.

2

Tax Nature of Tax Exemptions and Deductions Rates

husband electing for joint assessment in his wife’s name, the wife is allowed a personal relief of RM8,000 and a husband’s relief of RM3,000. Tax rebate of RM350 is given to individual whose chargeableincome does not exceedRM35,000. A further rebate of RM350 is given if the husband or the wife has no income and elected for joint assessment.

(xiv) Medical expenses for tax- RM 5,000 payer, spouse or child (max)

Payments of income tax are collected through compulsory deductions from salaries under the Schedular Tax Deduction System effective from 1.1.1995. In a case of a partnership, the main partner is required to make a return of the partnership’s income, but each is assessed individually on share of the partnership at individual income tax rate.

(xiii) Cash contributions RM20,000 made by individuals not (max) having business income to build or equip libraries of school and institutions of higher education.

on treatment of serious diseases. (xv) Full medical examination RM 500 expenses for tax payer, spouse or child provided that the amount shall be part of the RM 5,000 allowed in (xiv). (xvi) Contributions made by RM20,000

individuals to health care (max) facilities approved by the Ministry of Health.

(xvii) Contributions of local artworks to the State/ National Art Gallery. The value of these

contributions would be determined by the Department of Museum and Antiquities or the National Archives.

3

Tax Nature of Tax Exemptions and Deductions Rates

(xviii) Expenses incurred by indivi- duals in setting up facilities

for the benefits of the disabled persons in public places. Such expenses need to be approved by the relevant

local authorities. (xix) Expenses incurred by

individuals on purchase of books. RM500

(xx) Donations by individuals towards medical expenses of a seriously ill person needing financial assistance, provided that the donations are deposited into an account approved by the IRB. Zakat, fitrah or other Islamic religious dues are allowed as rebates and deducted from tax charged. A tax rebate of RM400 will be granted to taxpayers who purchase a personal computer. This tax rebate can only be enjoyed every five years and is limited to one computer per family.

4

Tax Nature of Tax Exemptions and Deductions Rates

Income derived by resident individuals which are specifically exempt from income tax : (i) royalties or payments of up to RM 20,000

in respect of the publication, use or the right to use any literary work or any original paintings;

(ii) royalties of up to RM6,000 in respect of

recording discs or tapes; (iii) payments of up to RM12,000 received for

translation of books or literary works at the specific request of any agency of the Ministry of Education or the Attorney General’s Chambers;

(iv) payments of up to RM20,000 received in

respect of musical compositions; (v) leave passages provided for the

employee and his immediate family members for one overseas trip and three local trips in a calendar year. For overseas trip, tax exemption is capped at RM3,000 effective from 24 October 1998;

(vi) the employment income of a person

derived from serving on board a Malaysian ship;

5

Tax Nature of Tax Exemptions and Deductions Rates

(vii) compensation received for loss of

employment of up to RM4,000 for each completed year of service;

(viii) cash award in lieu of leave received by

public servants upon retirement; (ix) certain official emoluments, disability

pensions and unemployment benefits. (x) interest received from banks;

- savings account and "Save As You

Earn" scheme with Bank Simpanan Nasional.

- interest from deposits of RM100,000 in

any savings account with a registered co-operative society, Bank Pertanian Malaysia, MBSB, Borneo Housing Mortgage Finance Bhd. or with any approved institution.

- bonus from money deposited in any

savings account with Lembaga Tabung Haji.

- interest from deposits of up to

RM100,000 in any savings account with a bank or finance company licensed under the BAFIA 1989.

6

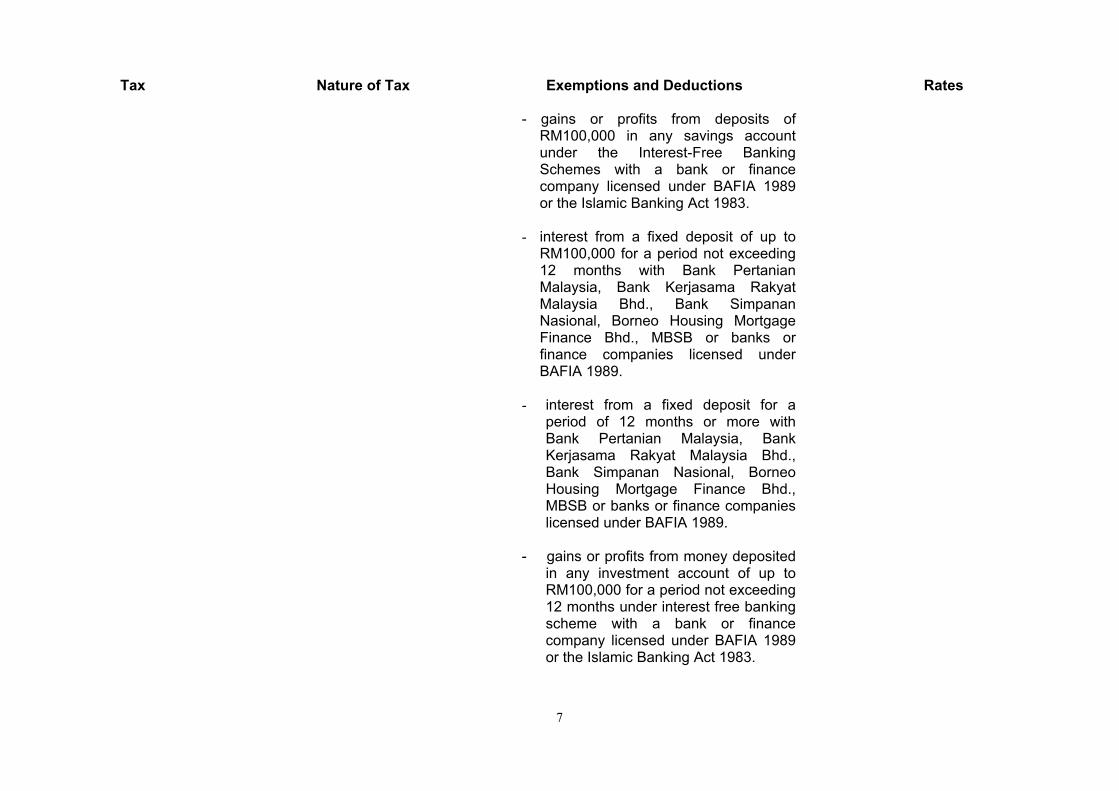

Tax Nature of Tax Exemptions and Deductions Rates

- gains or profits from deposits of RM100,000 in any savings account under the Interest-Free Banking Schemes with a bank or finance company licensed under BAFIA 1989 or the Islamic Banking Act 1983.

- interest from a fixed deposit of up to

RM100,000 for a period not exceeding 12 months with Bank Pertanian Malaysia, Bank Kerjasama Rakyat Malaysia Bhd., Bank Simpanan Nasional, Borneo Housing Mortgage Finance Bhd., MBSB or banks or finance companies licensed under BAFIA 1989.

- interest from a fixed deposit for a

period of 12 months or more with Bank Pertanian Malaysia, Bank Kerjasama Rakyat Malaysia Bhd., Bank Simpanan Nasional, Borneo Housing Mortgage Finance Bhd., MBSB or banks or finance companies licensed under BAFIA 1989.

- gains or profits from money deposited

in any investment account of up to RM100,000 for a period not exceeding 12 months under interest free banking scheme with a bank or finance company licensed under BAFIA 1989 or the Islamic Banking Act 1983.

7

Tax Nature of Tax Exemptions and Deductions Rates

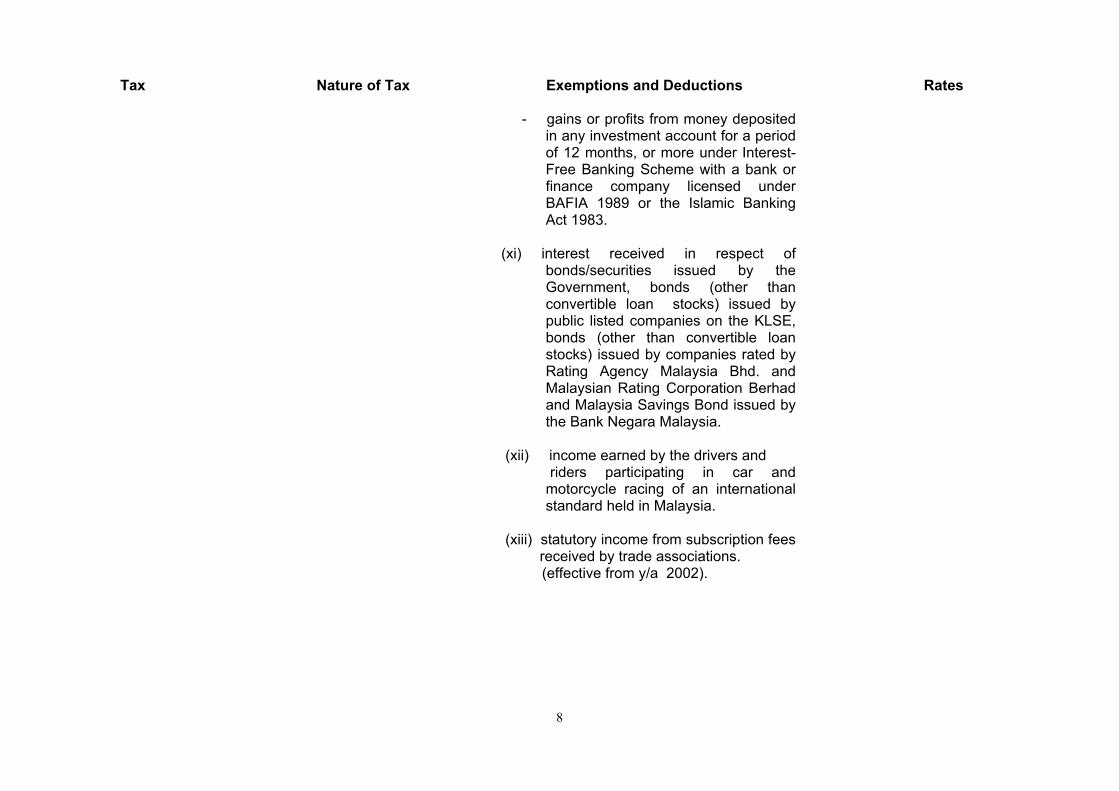

- gains or profits from money deposited in any investment account for a period of 12 months, or more under Interest-Free Banking Scheme with a bank or finance company licensed under BAFIA 1989 or the Islamic Banking Act 1983.

(xi) interest received in respect of

bonds/securities issued by the Government, bonds (other than convertible loan stocks) issued by public listed companies on the KLSE, bonds (other than convertible loan stocks) issued by companies rated by Rating Agency Malaysia Bhd. and Malaysian Rating Corporation Berhad and Malaysia Savings Bond issued by the Bank Negara Malaysia.

(xii) income earned by the drivers and riders participating in car and

motorcycle racing of an international standard held in Malaysia.

(xiii) statutory income from subscription fees

received by trade associations. (effective from y/a 2002).

8

Tax Nature of Tax Exemptions and Deductions Rates

Income derived by non-resident individuals which are specifically exempt from income tax :

(i) income remitted to Malaysia. (ii) Income earned by employees who

exercise an employment in Malaysia for a period which do not exceed 60 days in a calendar year.

(iii) interest received from deposits with

banks or finance companies licensed under BAFIA 1989.

(iv) interest received in respect of

bonds/securities issued by the Government, bonds (other than convertible loan stocks) issued by public listed companies on the KLSE, bonds (other than convertible loan stocks) issued by companies rated by Rating Agency Malaysia Bhd. and Malaysian Rating Corporation Berhad and Malaysia Savings Bond issued by the Bank Negara Malaysia.

(v) Income earned by the drivers and

riders participating in car and motorcycle racing of an international standard held in Malaysia.

9

Tax Nature of Tax Exemptions and Deductions Rates

1.2 Company Income

Tax (Income Tax Act, 1967).

Before year of assessment 1995, the scope of company income tax in Malaysia was based on derived and remittance basis, except for banking, insurance, air and sea transport for which the scope of taxation is based on world wide income. However, with effect from year of assessment 1995, the scope of company income tax in Malaysia is based on derived basis. For non-resident companies, tax is only imposed on income accruing in or derived from Malaysia, but not on income received in Malaysia from outside sources. The taxation of company is based on a full imputation system i.e. the tax of a company is in fact an advance tax of the shareholders who receive dividend from the company. Upon the declaration of dividends, the shareholders are taxed on the grossed dividends at their own respective tax rates and are given full tax credit in respect of the tax deducted at source by a company.

A. Allowable Expenses Generally, deductions are allowed for: (i) Revenue expenditure incurred wholly

and exclusively in the production of gross income;

(ii) Losses brought forward from an earlier

period are allowed against business income only;

(iii) Cash contributions to the Government,

a State Government and a Local Authority or an approved institution/ organisation provided that the amount to be deducted shall not exceed 5 % of the aggregate income of the company.

(iv) Cash contributions up to RM100,000 to

build or equip public libraries, libraries of schools or institutions of higher education.

(v) An amount equal to the expenditure

incurred by the relevant person in the relevant period on the provision of services, public amenities and contributions to a charity or community project pertaining to education, health,

Effective from the year of assessment 1998, the company income tax rate is 28%. Insurance companies are taxed as follows : i. 8% on the investment income

and capital gains of life fund. ii. 28 % on the income of a

shareholders’ fund (includes surplus actually transferred from the life fund).

10

Tax Nature of Tax Exemptions and Deductions Rates

For any year of assessment, tax is assessed on income received based on the accounting period of the company which ends in that year of assessment. Resident and non-resident insurance companies, trust, deceased person’s estate(executor), shipping companies and airlines are subject to tax based on special provision in the Act.

(vi) Contributions of local artworks to the State/ National Art Gallery.

Resident Status of A Company A company is resident in Malaysia if its management and control is exercised in Malaysia.Management and control is normally considered to be exercised at the place where the directors' meetings are held.

(ix) Donation towards the medical

housing infrastructure and information and communication technology approved by the Minister of Finance. Provided that where a deduction has been made under this paragraph, no further deduction of the same amount shall be allowed under section 44(6) of the Income Tax Act 1967.

(vii) Sponsorships up to RM200,000 for any

arts or cultural activity approved by the Ministry of Culture, Arts and Tourism.

(viii) Scholarships granted to needy full-time

students in local institutions.

expenses of a seriously ill person needing financial assistance, provided

the donations are deposited into an account approved by the Inland Revenue Board.

( x) Cost of the equipment supplied by the employer for the disabled employee to

perform his duties. (xi) Expenses incurred in providing practical

training to residents who are not employees of the company.

(effective from y/a 2002)

11

Tax Nature of Tax Exemptions and Deductions Rates

(xii) Cost of developing websites at 20%

annually for a period of 5 years. (effective from y/a 2002) Entertainment expenditure such as: (i) entertainment given to employees except

where such provision is incidental to the provision of entertainment for others;

(ii) entertainment provided by a business

which consists of or includes the provision for payment of entertainment to clients or customers where the nature of business is to provide entertainment for payments;

(iii) expenses on promotional gifts at

trade/industrial exhibitions held outside Malaysia for the promotion of export;

(iv) expenses on promotional samples of

products of the business; (v) provision of entertainment for cultural

or sporting events open to members of the public wholly to promote the business; and

(vi) provision of promotional gifts within

Malaysia consisting of articles incorporating a conspicuous advertisement or logo of the business.

12

Tax Nature of Tax Exemptions and Deductions Rates

Contribution to EPF or an approved fund in respect to an employee is subject to maximum contribution of 19%. Expenses incurred by businesses for the purposes of publishing or translating into the National Language of cultural, literary, professional, scientific or technical books approved by Dewan Bahasa dan Pustaka. Companies are allowed single deduction on pre-operational training expenses Exploration cost is deductible from aggregate income or allowed as mining allowance when the prospecting is successful, provided the cost is added back to the aggregate income. Bonus paid to employees. (effective from y/a 2002) Pre-operational expenditure for approved projects overseas. Provision and maintenance of a child care centre for the benefit of employees. Interest paid on money borrowed and employed in producing income.

13

Tax Nature of Tax Exemptions and Deductions Rates

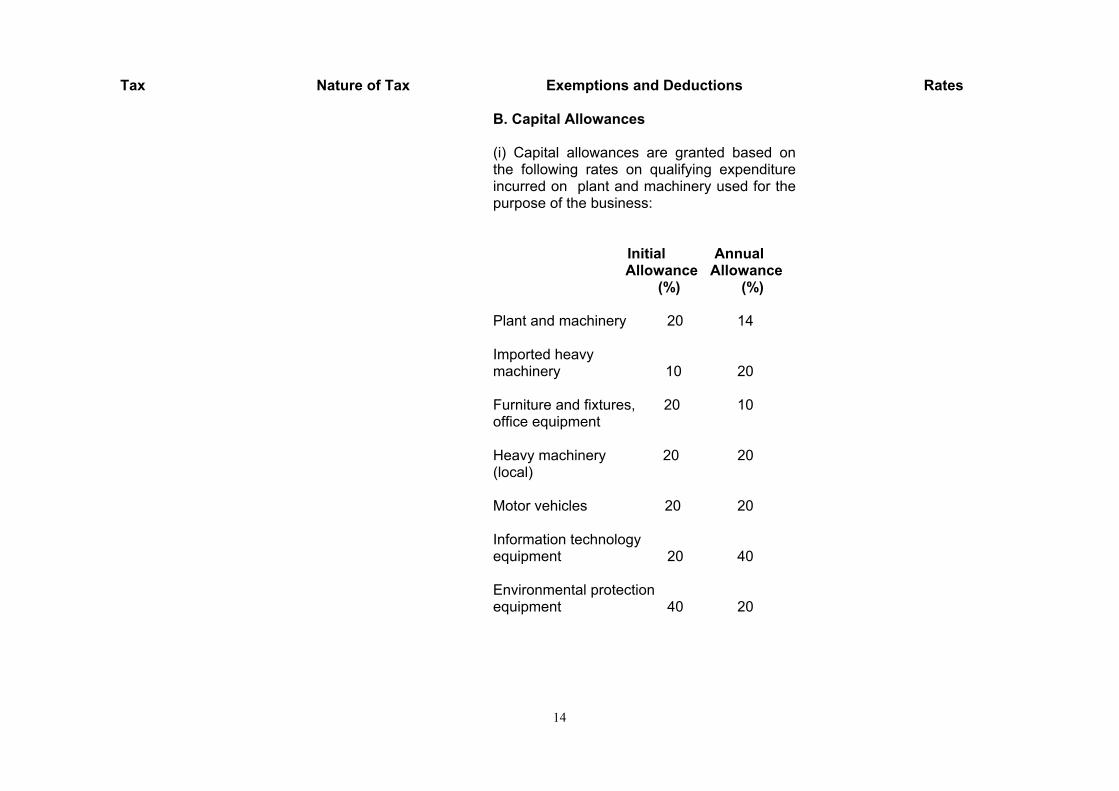

B. Capital Allowances (i) Capital allowances are granted based on the following rates on qualifying expenditure incurred on plant and machinery used for the purpose of the business: Initial Annual Allowance Allowance (%) (%) Plant and machinery 20 14 Imported heavy machinery 10 20 Furniture and fixtures, 20 10 office equipment Heavy machinery 20 20 (local) Motor vehicles 20 20 Information technology equipment 20 40 Environmental protection equipment 40 20

14

Tax Nature of Tax Exemptions and Deductions Rates

(ii) Qualifying capital expenditure on new

private motor vehicles used for business has been increased from RM50,000 to RM100,000 provided the on-the-road price of the vehicle does not exceed RM150,000.

(C) Industrial Building Allowance (IBA) Industrial Building Allowance (IBA) is granted to companies incurring capital expenditure on construction or purchase of a building which is used for specific purposes. In this regard, companies are eligible for an initial allowance of 10% and an annual allowance of 3% so as IBA can be claimed within 30 years. (effective from y/a 2002) However, special purpose buildings such as building for educational institution and building for child care facilities provided by employers enjoy higher rate of IBA which could be claimed within 10 years. (D) Exemptions (i) Income arising from sources outside

Malaysia and received in Malaysia by a

15

Tax Nature of Tax Exemptions and Deductions Rates

resident company (other than a company carrying on a business of banking, insurance, sea and air transport) and dividend distributed from such income.

(ii) The income of a resident shipping

company derived from the operation of “Malaysian Ships”.

(iii) Rental income derived by Malaysian

resident from time and voyage charter basis of “a Malaysian Ship”.

(iv) Income from the rental of ISO containers

received by non-residents from shipping companies in Malaysia.

(effective from 20.10.2001) (v) Interest received by non-resident company

from deposit with a bank and finance company licensed under the Banking and Financial Institution Act 1989.

(vi) Income earned by the organisers of

motorcycle and car racings. (50% exemption) (vii) Income earned from repair and

maintenance of luxury boats and yachts undertaken in Langkawi for a period of 5 years.

(effective from 23 October 1998).

16

Tax Nature of Tax Exemptions and Deductions Rates

(viii) Income derived by a company in

providing chartering services of luxury yachts for a period of 5 years.

(effective for applications received by Ministry of Finance on and after 20.10.2001).

(ix) income derived from the business of

operating group tours that bring in at least 500 foreign tourists per year. (effective from y/a 2002 until 2006).

(x) Income derived from the business of

operating domestic tour packages with at least 1,200 local tourists per year. (effective from y/a 2002 until 2006).

(xi) Royalty income received by non-resident

franchisor from franchised education schemes approved by the Ministry of Education.

(effective from 20.10.2001) (xii)Income earned from organising

international trade exhibitions held in Malaysia subject to the following conditions:

(i) the international exhibition is

approved by MATRADE; and

17

Tax Nature of Tax Exemptions and Deductions Rates

(ii) the organiser of the international trade exhibition brings in at least 500 foreign visitors per year.

(effective from y/a 2002)

1.2.1 Unit Trust

Income distributed by a unit trust is chargeable to tax on a unit holder. The tax chargeable on a unit trust will be set-off against the tax charged on the unit holder.

(i) any income distributed to unit holders out

of gains arising from the realisation of investments.

(ii) Interest income received by unit trusts

and property unit trusts. (iii) Permitted expenses which are deductable

are : - managers' remuneration

- maintenance of register of unit holders

- share registration expenses - secretarial, audit and accounting fees, telephone charges and postage.

The amount to be deducted is determined according to the formula:

A x (B/4C)

A = total of the permitted expenses incurred for that basis period

Dividend and rental income of a unit trust are subject to income tax at 28%

18

Tax Nature of Tax Exemptions and Deductions Rates

B = gross income consisting of dividend, interest and rent chargeable to tax for that basis period

C = the aggregate of the gross income

consisting of dividend (whether exempt or not), interest and rent, and gains made from the realisation of investments (whether chargeable to tax or not) for that basis period.

The amount of deduction is subject to a minimum of 10% of the total permitted expenses. Any unabsorbed expenses is not allowed to be carried forward to the subsequent year.

(iv) Qualifying capital expenditure of a

property unit trust .which are deductable are :

- expenditure incurred on the alteration of

an existing building; provided that such expenditure does not exceed 75% of the total qualifying expenditure.

- preparing or levelling of land; provided

that such expenditure does not exceed 10% of the total qualifying expenditure.

19

Tax Nature of Tax Exemptions and Deductions Rates

The deduction will be in the form of an annual allowance equal to 10% of the qualifying capital expenditure. Any unabsorbed allowances will not be allowed to be carried forward to a subsequent year.

1.2.2 Close-End Fund

Company A public limited

company incorporated in Malaysia and engaged wholly in the business of investing its funds in securities for the purpose of:-

a. spreading investment

risks and b. managing a portfolio of

investments.

Gains from the realisation of investments of a close-end fund shall be exempted from tax and the distributions from such gains are tax exempt in the hand of the shareholders. Interest received by listed close-end funds in respect of bonds or securities issued by Government, bonds (other than convertible loan stock) issued by public listed companies at the KLSE, bonds (other than convertible loan stock) issued by companies rated by RAM and Malaysian Rating Corporation Berhad and Malaysian Savings Bond issued by Bank Negara Malaysia is exempt from tax and distributions from such exempt income are also tax exempt in the hands of the shareholders. Qualifying expenses is determined in a similar manner as for unit trusts.

1.2.3. Foreign Fund Management Company

With effect from the year of assessment 1996, a foreign fund management company is given a concessionary tax treatment as follows:

20

Tax Nature of Tax Exemptions and Deductions Rates

A company incorporated in Malaysia and licenced under the Security Industry Act 1983

(i) income arising from services rendered by a foreign fund management company to clients outside Malaysia will be subject to tax at a concessionary rate of 10 per cent, while income arising from services rendered to local clients will be subject to the prevailing corporate tax rate.

Clients outside Malaysia can either be individuals, companies or trust funds who are not residents of Malaysia for tax purposes. Income received by the clients outside Malaysia will be treated in the following manner: (i) foreign sourced income such as dividend

and interest and gains arising from realisation of investment outside Malaysia by a foreign fund management company on behalf of its clients(foreign) will not be subject to tax;

(ii) dividend income arising from investment in Malaysia will not subject to a further tax;

(iii) interest income derived from Malaysia will be exempt from tax in the following circumstances:

(a) interest paid to foreign clients

(individuals) in respect of securities or bonds issued by the Government and bonds, other than convertible loan stocks, issued by public companies listed on the Kuala

21

Tax Nature of Tax Exemptions and Deductions Rates

Lumpur Stock Exchange or a company rated by Rating Agency Malaysia Berhad or Malaysian Rating Corporation Berhad;

(b) interest paid to foreign clients ( non-

resident) by any person carrying on the business of banking in Malaysia and licensed under the Banking and Financial Institutions Act 1989.

Other than the above, interest income will be taxed at the prevailing tax rate, that is the domestic tax rate or the rate under the Double Taxation Agreements.

(iv) gains arising from the realisation of

investments in Malaysia, other than real property, is not liable to tax.

1.3 Withholding Tax

(Income Tax Act 1967) i. Special classes of income under section

4A.

The withholding tax is imposed on income of person not resident in Malaysia in respect of amount paid in consideration of: - Services rendered in

connection with the use of property or rights belonging to or for the installation or operation of plant machinery, or other apparatus purchased from such person;

Nil

Withholding tax The following payments to non-resident companies are subject to deduction for withholding tax as follows: Royalties 10% Rental of movable properties 10% Technical or management service fees 10% Interest 15%

22

Tax Nature of Tax Exemptions and Deductions Rates

- Technical advice, assistance, service for technical management or administration of any scientific, industrial commercial ventures or scheme;

- Rent or other payments not

being payments of film rentals made under any agreement for use of movable property.

The liability of tax is on the recipient but it is the responsibility of the payer of such payment to withhold the tax and pay such tax to the Inland Revenue Board.

The above rates shall prevail unless concessionary rates are specified by the Agreement for the Avoidance of Double Taxation.

ii. Deduction of tax from

contract payment under section 107A.

Any person liable to make contract payment to a non-resident contractor for services under a contract is required to deduct the tax and pay such tax to the Inland Revenue Board. This is not a final tax and will be adjusted against the final tax liability of the non-resident contractor.

Director General may give notice in writing to the payer to deduct and pay tax at other rates or to make the contract payment without any deduction of tax.

15% of the contract payment on account of tax which is payable by the non-resident contractor. 5% of the contract payment on account of tax which is payable by employees of the non-resident contractor.

1.4 Taxation of Cooperative Societies.

Cooperative societies are taxed on income derived from or received in Malaysia.

Special deductions are granted to cooperative societies as follows:

For every dollar of the first RM20,000 0%

23

Tax Nature of Tax Exemptions and Deductions Rates

- a deduction up to a maximum of 25% of net income for contribution to statutory reserve fund required to be created under the Cooperative Society Ordinance .

- an amounts equal to 8% of the members'

funds. Tax exemption for a period of 5 years from the date of registration is allowed to enable new cooperative societies to establish themselves during the initial stage of establishment. After the 5th years, cooperatives having members’ fund of RM750,000 or less will continue to be tax exempted. Dividends paid by co-operative societies to their members are exempt from tax.

For every dollar of the next RM10,000 3% For every dollar Of the next RM10,000 6% For every dollar of the next RM10,000 9% For every dollar of the next RM25,000 12% For every dollar of the next RM25,000 16% For every dollar of the next RM50,000 20% For every dollar of the next RM100,000 23% For every dollar of the next RM250,000 26% Above RM500,000 28%

1.5 Taxation On Petroleum

Companies (Petroleum Income

Tax Act 1967)

A tax, in lieu of the income tax, is levied annually on the chargeable income derived by any person carrying on petroleum operations in Malaysia. Petroleum operations mean the searching for and the winning or obtaining of petroleum

Deductions are allowed for normal business expenses. Other business expenses allowed are as follows: - monies donated to approved institutions

and the Government.

38% of the chargeable income effective from the year of assessment 1998.

24

Tax Nature of Tax Exemptions and Deductions Rates

and any sale or disposal of petroleum so won or obtained. Petroleum operations are conducted within the framework of the production sharing agreements which are entered into between PETRONAS, and the petroleum companies. Under the agreement, 10% of all petroleum produced goes to the Government ( 5% to the Federal Government and 5% to the State Government ) while the remaining production is divided between PETRONAS and the petroleum companies in accordance to an agreed formula. PETRONAS as well as all petroleum companies which enter into production sharing contracts with PETRONAS are chargeable to tax on their respective shares of production. Miscellaneous receipts incidental to and arising from petroleum operations are also subject to petroleum income tax. However income derived from refining or liquifying of petroleum and any activity dealing with refined products is subject to the normal corporate tax as provided under the Income Tax Act (see 1.2 above).

- contribution to abandonment cess (or removal of installations) under the Production Sharing Contract. ( effective from y/a 1994)

- Exploration expenses qualify for depletion allowances. The rates for initial allowance are 10% for primary exploration expenditure and 20% for exploration expenditure incurred for secondary recovery activities. In both instances, the annual allowance which is computed on the units of production basis is subject to a minimum of 15% of the residual qualifying exploration expenditure.

- Capital allowances are also granted for

qualifying capital expenditure on industrial building, plant and machinery and fixed offshore platforms. Except for fixed offshore platforms, which are granted an annual allowance of 10%, the rates for initial and annual allowances vary between the classes of assets mentioned above as well as between those incurred for primary and secondary activities. All petroleum assets are amortised on a straight line basis.

2. Stamp Duties (Stamp Ordinance

Stamp duties are imposed ad valorem on certain written

Certain instruments are exempted under the Stamp Act, 1949:

Beginning 1.1.2001, the specific stamp duty is standardised to RM10 except for

25

Tax Nature of Tax Exemptions and Deductions Rates

1949 – effective 5.12.1949)

documents varying according to the nature of the documents and values referred to. However some documents attract specific rates of stamp duties.

- reconstructions or amalgamations of companies;

- transfer of property between associated companies;

- all instruments in the nature of securities for money granted to finance the purchase of a low cost housing unit in a Low Cost Housing Project.

- life insurance policy not exceeding

RM5,000. - Instruments relating to corporate bonds. Instruments Under Interest-Free Banking Scheme (i) stamp duties on loan instruments executed

following the conversion from conventional financing scheme to Syariah financing scheme are exempted from stamp duty on the balance of the principal amount of the existing loan.

Stamp duties on bills of exchange, bills of lading and receipts were abolished from 1.1.1992. With effect from 24 October 1998, stamp duty is exempted on refinancing instrument with respect to term loans subject to the following conditions:

cheques ( RM 0.15 ) and Memorandum & Articles of Association of company (RM 100). The stamp duties for certain instruments are as follows: Conveyance/ - 1% on first property except RM100,000 stock shares, - 2% on the next marketable securities RM400,000 and account - 3% on the receivable or book remaining debts market value Transfer of low cost - Maximum of house RM100 where a contract of

sale & purchase is executed not later than 31.12.2000 - restricted to first purchaser only. Shares - 0.3% of the consideration Agreement or memorandum - RM10 of agreement under hand only and not specifically charged with any duty Deed of any kind not - RM10 described in the First Schedule

26

Tax Nature of Tax Exemptions and Deductions Rates

(i) the refinancing facility represents a

term loan for the purpose of funding the original loan. Refinancing for the purpose of funding an overdraft facility and for the working capital is not eligible for such exemption;

(ii) the exemption is limited for the

purpose of funding the balance of the original loan;

(iii) for syndicated loan, the amount of

refinancing loan given by each bank has to be stipulated on the refinancing loan agreement; and

(iv) The stamp duty chargeable on the

instrument of transfer of a house pursuant to a sale and purchase agreement executed between the developer and the purchaser on or between 1.1.2000 until 31.12.2001 is remitted to the extent as shown below :

Charge or Mortgage, Agreement for a Charge or Mortgage ( including that under the Syariah, Bond, Covenant, Debenture ( not being a marketable security, Bill of Sale by way of security and Warrant of Attorney.

Value of House Duty Remitted < RM 75,000 100% RM 75,000 to RM 150,000 50%

Contract notes for sale - RM1.00 for of any shares, stocks, every or marketable securities RM 1,000 part thereof Counterpart of duplicate of any instrument chargeable with duty and in respect of which the proper duty has been paid:- Duty on original is - the same as RM10 or less original Other cases - RM10.00 Charge or mortgage

Being the only or - For each RM principal or primary RM 1,000 or security part thereof RM5.00 Being the only or - RM1 for every principal security RM1,000 or for loan ( up to part thereof

27

Tax Nature of Tax Exemptions and Deductions Rates

RM 250,000 ) to a small business Loan of more than - RM5.00 for RM250,000 every RM1,000 or part thereof Being the only or - RM5.00 for principal security every RM1,000 where the loan is or part thereof a foreign currency maximum of loan or financing RM500 was made according to Syariah in currencies of the Ringgit Being a collateral - one fifth of the Or additional security duty on the principal but not to exceed RM 10.00 Loan Agreement i. instruments of loan agreement for

the purchase of goods made under the principle of Al Bai Bithaman Ajil of the Syariah Law are subjected to stamp duty of RM3.00 or RM10.00 only if executed under seal and the excess duty is remitted.

28

Tax Nature of Tax Exemptions and Deductions Rates

ii. lease or agreement for lease under

the principles of Al-Ijarah of the Syariah Law for the Purpose of financing or securing repayment of money will be subjected to the same advalorem duty as charge or mortgage for such total amount (to equate the rate with that paid by similar product under conventional banking)

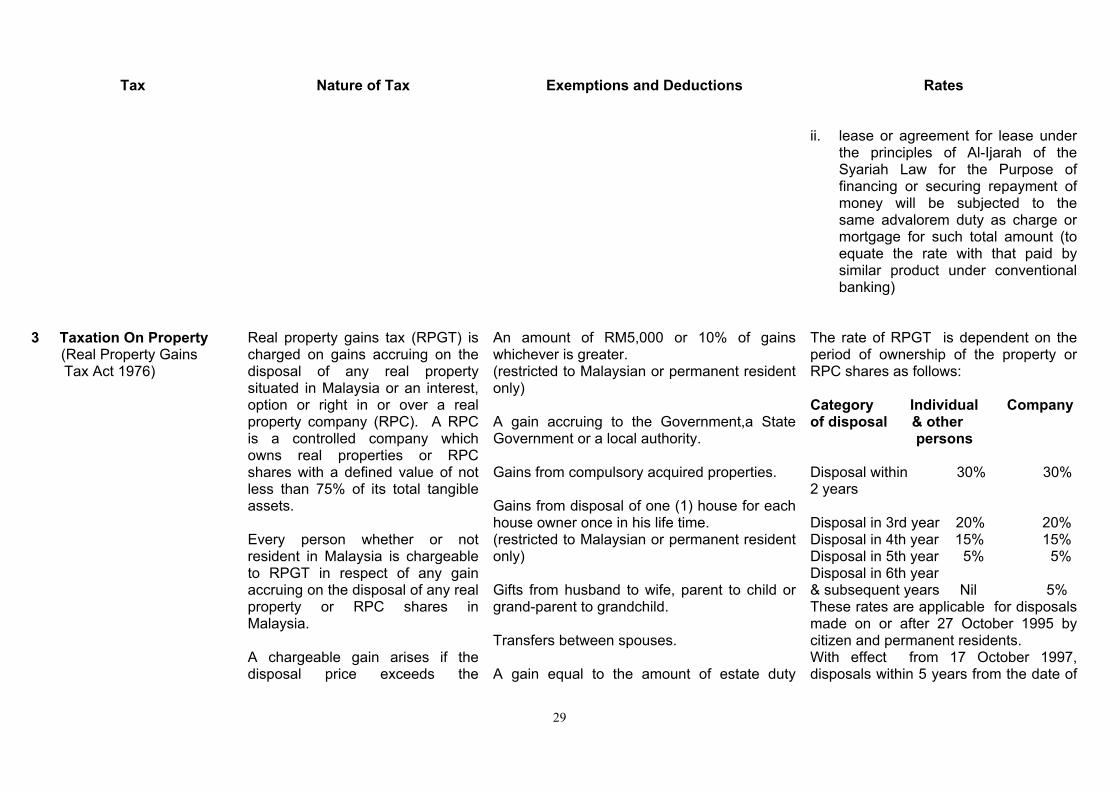

3 Taxation On Property

(Real Property Gains Tax Act 1976)

Real property gains tax (RPGT) is charged on gains accruing on the disposal of any real property situated in Malaysia or an interest, option or right in or over a real property company (RPC). A RPC is a controlled company which owns real properties or RPC shares with a defined value of not less than 75% of its total tangible assets. Every person whether or not resident in Malaysia is chargeable to RPGT in respect of any gain accruing on the disposal of any real property or RPC shares in Malaysia. A chargeable gain arises if the disposal price exceeds the

An amount of RM5,000 or 10% of gains whichever is greater. (restricted to Malaysian or permanent resident only) A gain accruing to the Government,a State Government or a local authority. Gains from compulsory acquired properties. Gains from disposal of one (1) house for each house owner once in his life time. (restricted to Malaysian or permanent resident only) Gifts from husband to wife, parent to child or grand-parent to grandchild. Transfers between spouses. A gain equal to the amount of estate duty

The rate of RPGT is dependent on the period of ownership of the property or RPC shares as follows: Category Individual Company of disposal & other persons

Disposal within 30% 30% 2 years Disposal in 3rd year 20% 20% Disposal in 4th year 15% 15% Disposal in 5th year 5% 5% Disposal in 6th year & subsequent years Nil 5% These rates are applicable for disposals made on or after 27 October 1995 by citizen and permanent residents. With effect from 17 October 1997, disposals within 5 years from the date of

29

Tax Nature of Tax Exemptions and Deductions Rates

acquisition price and an allowable loss is incurred if the disposal price is less than the acquisition price. The loss arising from the disposal of RPC shares does not qualify as an allowable loss.

payable in respect of a disposal of a chargeable asset of an estate. Cross transfers between co-proprietors arising from partition of land.

the acquisition of chargeable assets by a non-citizen and a non-permanent resident are subject to 30% and that disposals after the 5th years are subject to a rate of 5%.

4. Tax / Licence / Duty On

Gaming Activities

4.1 Gaming Tax Act, 1972

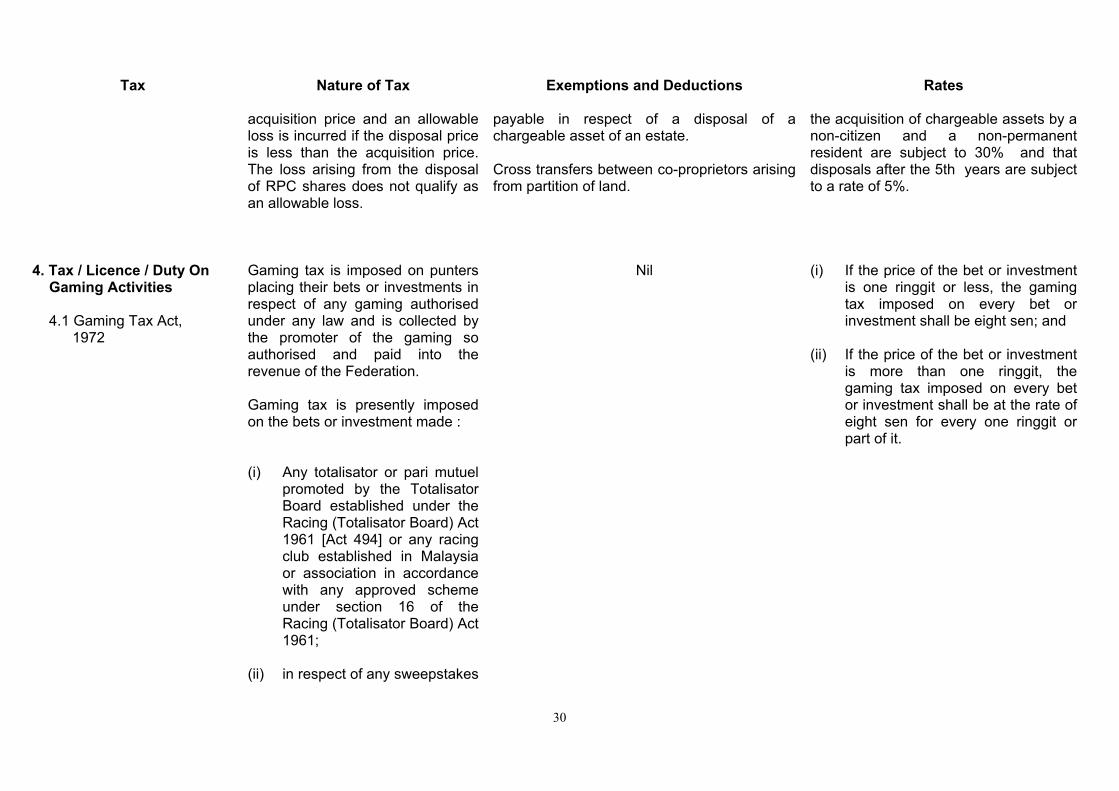

Gaming tax is imposed on punters placing their bets or investments in respect of any gaming authorised under any law and is collected by the promoter of the gaming so authorised and paid into the revenue of the Federation. Gaming tax is presently imposed on the bets or investment made : (i) Any totalisator or pari mutuel

promoted by the Totalisator Board established under the Racing (Totalisator Board) Act 1961 [Act 494] or any racing club established in Malaysia or association in accordance with any approved scheme under section 16 of the Racing (Totalisator Board) Act 1961;

(ii) in respect of any sweepstakes

Nil

(i) If the price of the bet or investment

is one ringgit or less, the gaming tax imposed on every bet or investment shall be eight sen; and

(ii) If the price of the bet or investment

is more than one ringgit, the gaming tax imposed on every bet or investment shall be at the rate of eight sen for every one ringgit or part of it.

30

Tax Nature of Tax Exemptions and Deductions Rates

promoted by any racing club on the result of a horse race;

(iii) under the Scheme for the

Promotion, Operation and Management of Four Digit Numbers Forecast Betting approved under section 16 of the Pool Betting Act 1967 [Act 384];

(iv) under the Scheme for the

Promotion, Operation and Management of TOTO Betting approved under section 16 of the Pool Betting Act 1967;

(v) under the Scheme for the

Promotion, Operation and Management of the Four Digits Game (4D) 1996 for Sandakan Turf Club;

(vi) under the Scheme for the

Promotion, Operation and Management of (1+3D) Sarawak Turf Club Special Cash Sweep 1996.

31

Tax Nature of Tax Exemptions and Deductions Rates

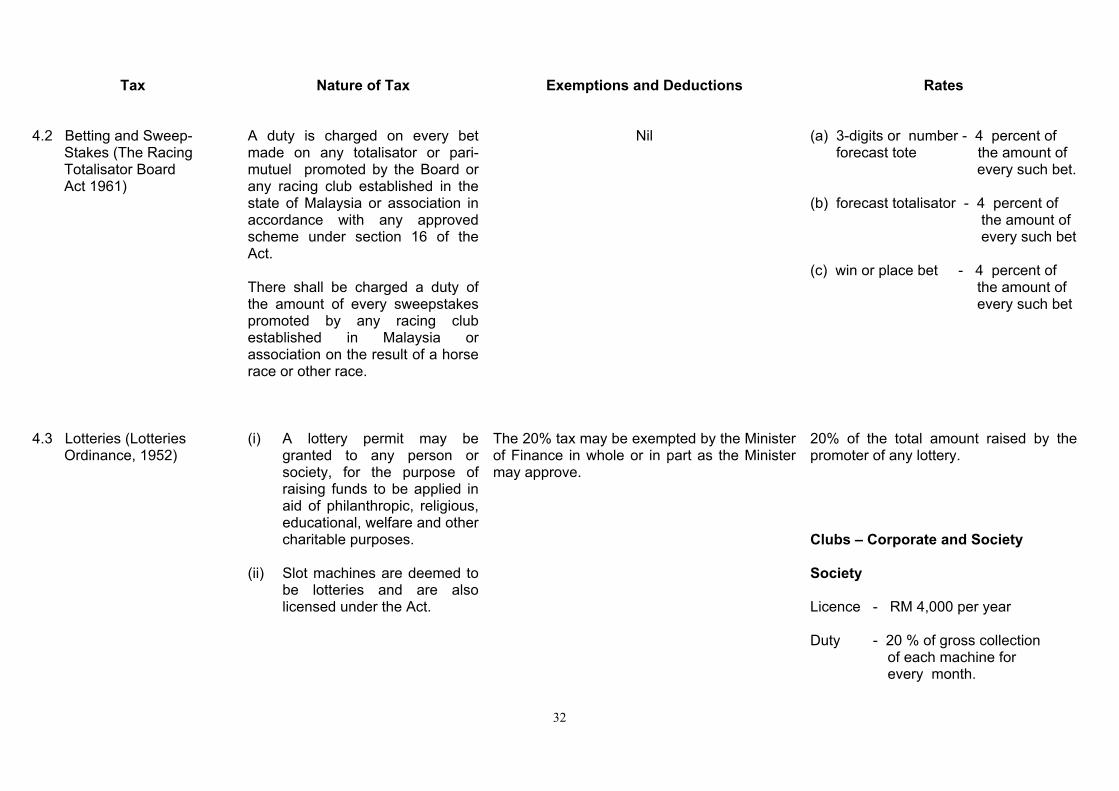

4.2 Betting and Sweep-

Stakes (The Racing Totalisator Board Act 1961)

A duty is charged on every bet made on any totalisator or pari-mutuel promoted by the Board or any racing club established in the state of Malaysia or association in accordance with any approved scheme under section 16 of the Act. There shall be charged a duty of the amount of every sweepstakes promoted by any racing club established in Malaysia or association on the result of a horse race or other race.

Nil

(a) 3-digits or number - 4 percent of

forecast tote the amount of every such bet. (b) forecast totalisator - 4 percent of the amount of every such bet (c) win or place bet - 4 percent of the amount of

every such bet

4.3 Lotteries (Lotteries

Ordinance, 1952)

(i) A lottery permit may be

granted to any person or society, for the purpose of raising funds to be applied in aid of philanthropic, religious, educational, welfare and other charitable purposes.

(ii) Slot machines are deemed to

be lotteries and are also licensed under the Act.

The 20% tax may be exempted by the Minister of Finance in whole or in part as the Minister may approve.

20% of the total amount raised by the promoter of any lottery. Clubs – Corporate and Society Society Licence - RM 4,000 per year Duty - 20 % of gross collection of each machine for every month.

32

Tax Nature of Tax Exemptions and Deductions Rates

Corporate Licence - RM 2,000 for every 3 months Duty - 20% of gross collection of each machine for every month.

4.4 Casino (Common

Gaming Houses Ordinance, 1953)

Under Section 27(A) the Minister of Finance may, in his discretion, authorise by licence a company registered under the Companies Act, 1965 to promote organised gaming subject to the payment of such fees and duties and subject to such other terms and conditions as may be specified in the licence, for a period not exceeding 3 months.

Nil

Genting Casino Licence - RM 4,000,000 for every 3 Months Duty - 25 % of casino win. Mini Casino in Tioman Licence - RM 5,000 for every 3 months Duty - 20 % of gross collection of each machine for every month.

4.5 Pool Betting Duty

(Pool Betting Act, 1967)

Under section 5(1), the Minister of Finance may issue a licence to a person for the collection, operation or promotion of Pool Betting. Such licence shall be valid for one

l d l d b

Nil

Magnum Corporation Licence - RM 2,000,000 per year

33

Tax Nature of Tax Exemptions and Deductions Rates

calendar year only and may be renewed from year to year.

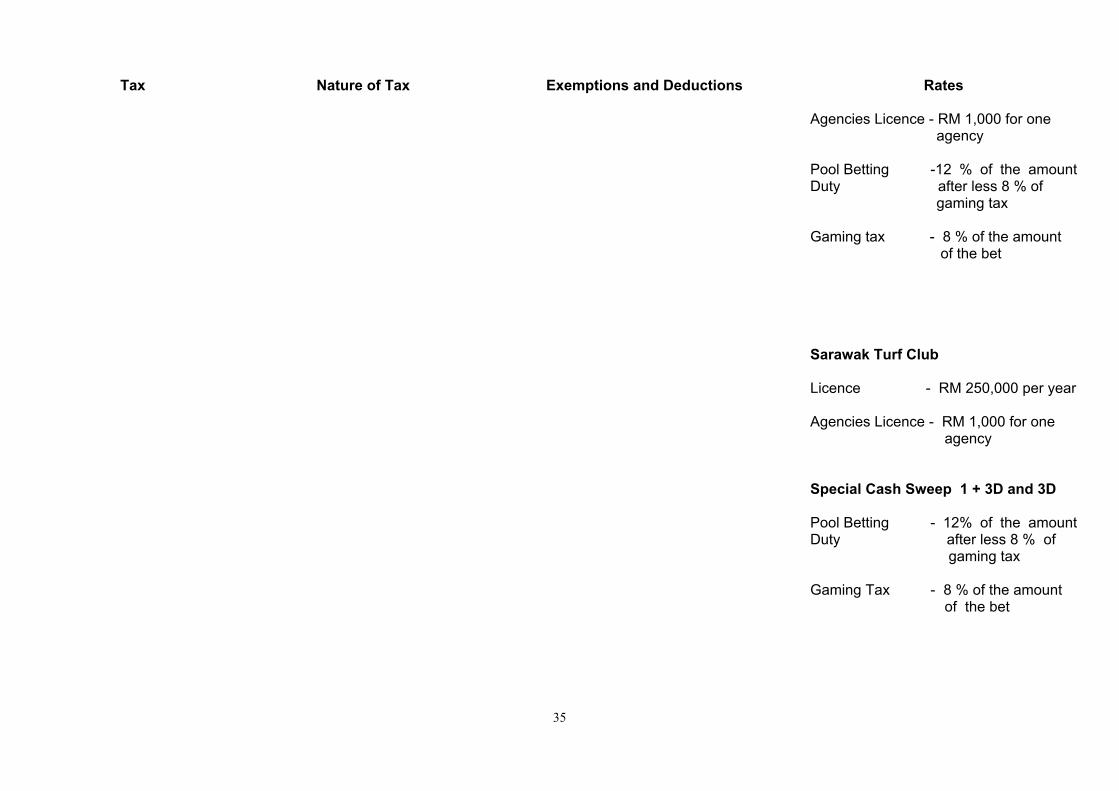

Agencies Licence - RM 1,000 for one agency Pool Betting - 12% of the amount Duty of the bet made after less 8% gaming tax Gaming Tax - 8 % of the amount of the bet Sports Toto (M) Sdn. Bhd. Licence - RM 2,000,000 per year Agencies Licence - RM 1,000 for one Agency Pool Betting - 10 % of the amount Duty of the bet made after less 8 % of

gaming tax Gaming Tax - 8 % of the amount of the bet Sandakan Turf Club Licence - RM 250,000 per year.

34

Tax Nature of Tax Exemptions and Deductions Rates

Agencies Licence - RM 1,000 for one agency Pool Betting -12 % of the amount Duty after less 8 % of gaming tax Gaming tax - 8 % of the amount of the bet Sarawak Turf Club Licence - RM 250,000 per year Agencies Licence - RM 1,000 for one agency Special Cash Sweep 1 + 3D and 3D Pool Betting - 12% of the amount Duty after less 8 % of gaming tax Gaming Tax - 8 % of the amount of the bet

35

Tax Nature of Tax Exemptions and Deductions Rates

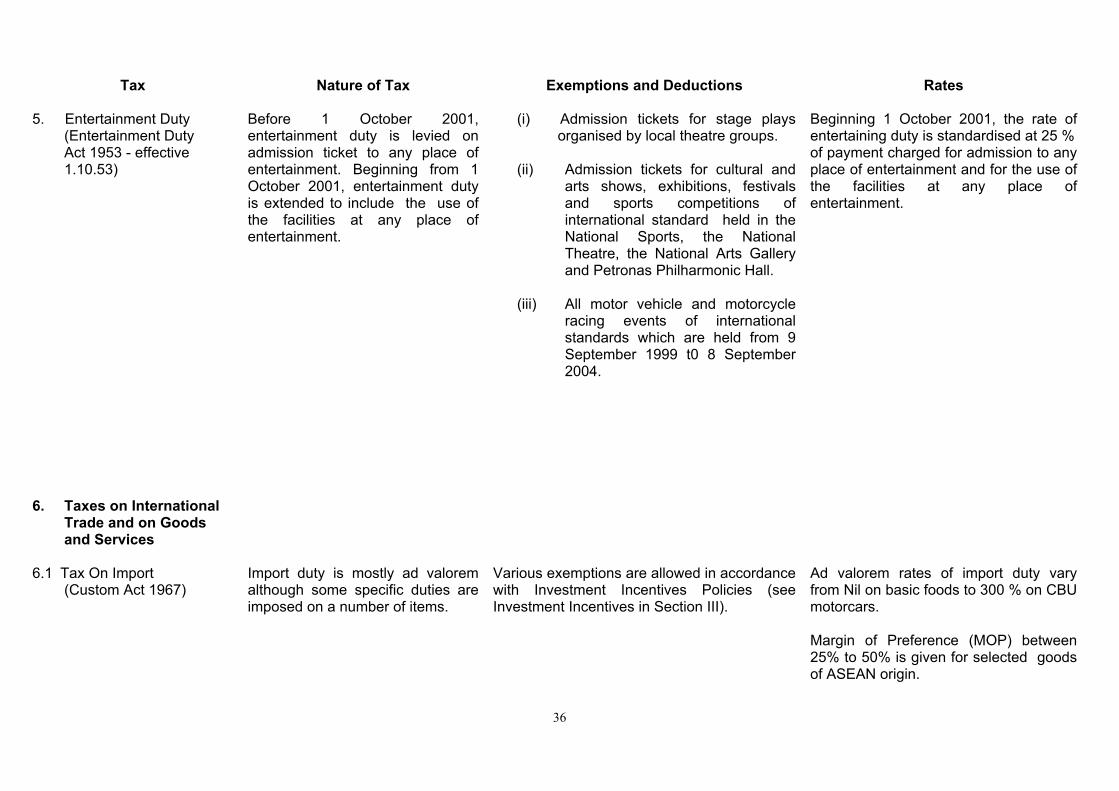

5. Entertainment Duty (Entertainment Duty Act 1953 - effective 1.10.53)

Before 1 October 2001, entertainment duty is levied on admission ticket to any place of entertainment. Beginning from 1 October 2001, entertainment duty is extended to include the use of the facilities at any place of entertainment.

(i) Admission tickets for stage plays organised by local theatre groups.

(ii) Admission tickets for cultural and

arts shows, exhibitions, festivals and sports competitions of international standard held in the National Sports, the National Theatre, the National Arts Gallery and Petronas Philharmonic Hall.

(iii) All motor vehicle and motorcycle

racing events of international standards which are held from 9 September 1999 t0 8 September 2004.

Beginning 1 October 2001, the rate of entertaining duty is standardised at 25 % of payment charged for admission to any place of entertainment and for the use of the facilities at any place of entertainment.

6. Taxes on International Trade and on Goods and Services

6.1 Tax On Import

(Custom Act 1967)

Import duty is mostly ad valorem although some specific duties are imposed on a number of items.

Various exemptions are allowed in accordance with Investment Incentives Policies (see Investment Incentives in Section III).

Ad valorem rates of import duty vary from Nil on basic foods to 300 % on CBU motorcars. Margin of Preference (MOP) between 25% to 50% is given for selected goods of ASEAN origin.

36

Tax Nature of Tax Exemptions and Deductions Rates

Under CEPT, the import duty for most items will be at 0 % - 5 % by 1.1.2003.

6.2 Tax on Export (Export

Duty, Custom Act 1967) 6.2.1 Crude Palm Oil

Export duty is based on the gazetted value of crude palm oil. It is only levied at a price level exceeding RM650 per tonne which is estimated to be the cost of production.

Crude palm oil exports from Sabah and Sarawak are subjected to 70% exemption of the current rate of export duty.

On the first RM 650 per tonne Nil Plus on the next RM 50.00 per tonne 10 % a.v. Plus on the next RM50.00 per tonne 15% a.v Plus on the next RM50.00 per tonne 20% a.v Plus on the next RM50.00 per tonne 25% a.v Plus on the balance 30% a.v

6.2.2 Processed Palm

Oil

Export duty is based on the gazetted value of processed palm oil (PPO), whereby a duty is calculated in ringgit per tonne to the nearest sen according to the rates and categories

37

Tax Nature of Tax Exemptions and Deductions Rates

Category I Neutralised/Refined Palm Oil; Bleached Palm Oil; Crude Palm Olein. Category II Neutralised/Refined Bleached Palm Oil; Neutralised/Refined Palm Olein; Bleached Palm Olein. Category III Neutralised/Refined Bleached Deodorised Palm Oil 6 Red Max; Neutralised/Refined Bleached Palm Olein. Category IIIA Neutralised/Refined Bleached Deodorised Palm Oil 3 Red Max. Category IV Neutralised/Redefined Bleached Deodorised Palm Olein.

0 %

0 %

0 %

0 %

0 %

38

Tax Nature of Tax Exemptions and Deductions Rates

6.2.3. Palm Kernel Oil / Olein / Stearin

Palm kernel oil, crude Palm Kernel oil, RBD Palm kernel olein, crude Palm kernel olein, RBD Palm kernel stearin, crude Palm kernel stearin RBD Palm kernel olein, Hydrogenated &RBD Palm kernel stearin, Hydrogenated &RBD Crude Palm Stearin

The export of palm kernel oil / olein / stearin from Sabah and Sarawak are allowed a rebate of 30 % on dutiable products.

Export Duty

10 %

5 %

5 % Nil

5 % Nil

Nil Nil

Nil Nil

Nil

6.2.4. Crude Oil

Export duty is based on the gazetted value of crude oil.

Exemption are given as follows: (i) 10% to Petronas (ii) cost of oil of 20% under old PSC and percentage of actual cost up to a maximum of 50% under new PSC.

10% ad valorem.

39

Tax Nature of Tax Exemptions and Deductions Rates

7. Excise Duties (Excise Act 1976)

Excise duties are levied on locally manufacture cigarettes, intoxicating liquors, motor vehicles and playing cards.

Excise duties (Exemption) Order 1977 lists out the groups of people exempted from excise duties. Taxi and cars-for-hire operators on the purchase of national cars. Motor vehicles for providing mobile libraries and clinics services. The physically disabled persons on the purchase of national motorcars and motorcycles. ( 50% exemption-2001 Budget)

Some of the excise rates currently in force are ; Cigarettes : RM 48.00 per kg. Beer & Stout based on the alcohol content. Not exceeding 5.8% Vol - RM 36.00 per decalitre

Others - RM 37.00 Per decalitre Locally assembled motor vehicles are taxed as follows: Value of vehicles Marginal Tax (RM) Rate (%) 0 - 7,000 25 7,001 - 10,000 30 10,001 - 13,000 35 13,001 - 20,000 50 20,001 - 25,000 60 Above 25,001 65

40

Tax Nature of Tax Exemptions and Deductions Rates

Motorcycles Engine Capacity Rate (%) 150 cc and below 10 151 cc < x ≤ 200 cc 20 201 cc < x ≤ 250 cc 30 251 cc < x ≤ 500 cc 30 501 cc < x ≤ 800 cc 40 Above 801 cc 50

8. Sales Tax (Sales Tax Act, 1972)

This is an ad valorem single stage tax imposed at the import and manufacturing levels except petroleum products where the rates are specific.

Manufacturers whose sale values of taxable goods do not exceed RM100,000 per annum. Basic food-stuffs, basic building materials, certain agricultural implements and machinery, certain tourist and sports goods, books, newspapers, other reading materials and computers. All exports. Certain privileged persons, diplomats and Government agencies. Raw materials and machinery for manufacturing of taxable goods. Inputs for selected non-taxable goods. (Schedule C - Sales Tax Exemption Order 1980).

Current rates are as follows:

• general rate on all goods - 10 %

• fruits, certain foodstuffs and building materials - 5 % • cigarettes and tobacco products - 25 % • alcoholic beverages - 20 % • Petrol - RM 0.5862 per litre • Diesel - RM 0.1964 per litre

41

Tax Nature of Tax Exemptions and Deductions Rates

Motor vehicles for providing mobile libraries and clinics services. To stabilise the prices of petroleum products at the controlled level, partial or full exemption on sales tax are granted under the Automatic Price Mechanism.

9. Service Tax

(Service Tax Act, 1975 ) Shall apply throughout

Malaysia excluding Langkawi, Labuan, Free

Zones and ‘ Joint Development Area ’

This is a form of indirect tax imposed on taxable services as prescribed under the Second Schedule of the Service Tax Regulations 1975. Service tax is imposed on services provided by: Group A

1) hotels ( having more than 25 rooms )

Group B1

2) restaurants, bars, snack-bars and coffee houses located in hotels ( having more than 25 rooms );

Group B2 3) restaurants, bars, snack-

bars and coffee houses located in hotels ( having 25 rooms or less ) with an annual sales turnover of RM300,000 and above;

Exempted from the service tax are: 1. Hotels having not more than 25 rooms. 2. Hostels for pupils or for students of

education institutions. 3. Hostels established and run by public

institutions or bodies.

42

Tax Nature of Tax Exemptions and Deductions Rates

Group C

3) restaurants, bars, snack-bars and coffee houses located outside hotels; having an annual sales turnover of RM300,000 and above

4) food courts having an

annual sales turnover of RM300,000 and above;

Excluded are :

i. Canteen located in an educational institution; and

ii. Canteen operated by a religious institution or body.

Group D 6) night-clubs, dance halls,

cabarets, health centres and massage parlours, public houses and beer houses.

Group E 7) private clubs having an

annual sales turnover of RM300,000 and above;

43

Tax Nature of Tax Exemptions and Deductions Rates

Group E1 8) golfing and golf driving

range facilities and its related services including all such facilities provided by private clubs and non- private clubs;

Group F 9) private hospitals having an

annual sales turnover of RM 300,000 and above; Group G 10) insurance companies; 11) all forms of

telecommunication services except the internet;

12) services provided by forwarding agents; 13) Parking spaces for motor

vehicles having an annual sales turnover of RM150,000 and above;

14) courier services having

an annual sales turnover of RM150,000and above;

44

Tax Nature of Tax Exemptions and Deductions Rates

15) motor vehicles services and or repair centres having an annual sales turnover of RM150,000 and above;

16) private agencies having

an annual sales turnover of RM150,000 and above;

17) employment agencies

having an annual sales turnover of RM150,000 and above;

18) Professional and consultancy services

provided by legal, engineering, surveyor

(including valuers, appraisers or estate agents), architectural, accounting and other consultancy firms having an annual sales turnover of RM150,000 and above;

19) private veterinary clinics

having an annual sales turnover of RM300,000 and above;

45

Tax Nature of Tax Exemptions and Deductions Rates

20) hire and drive cars and hire-car services having an annual sales turnover of RM300,000 and above;

21)management services

including project management or project coordination having an annual sales turnover of RM150,000 and above;

22)private agencies

(security and guard service firms ) with an annual turnover of RM150,000 and above; and

23)advertising companies

having an annual sales turnover of RM 300,000.

10. Road Tax 10.1 Motor vehicles

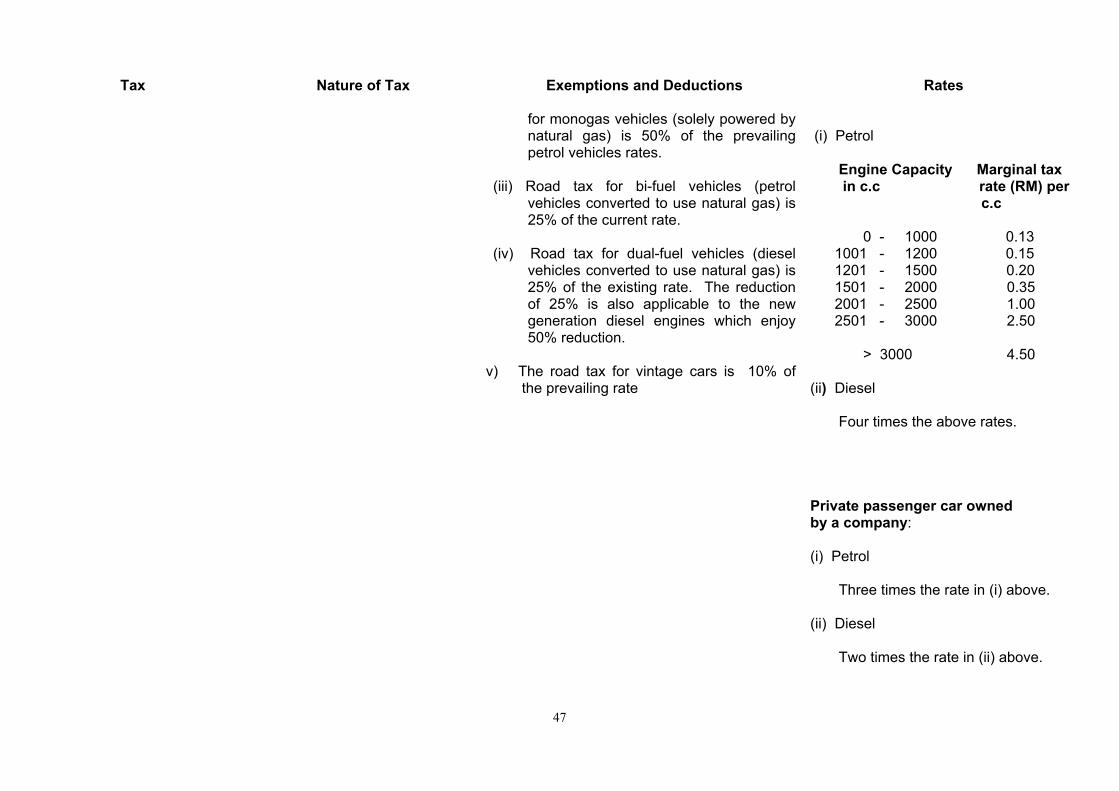

The road tax imposed under the Road Transport Ordinance on passenger cars and taxi / cars for hire, school / stage buses, etc. is based on the engine capacity and the type of fuel used.

(i) For motor vehicles fitted with new

generation diesel engines, the motor vehicle licence fee (road tax) is 50% of the current rate.

(ii) The motor vehicle licence fee (road tax)

Rates of tax are: Private passenger car owned by an individual:

46

Tax Nature of Tax Exemptions and Deductions Rates

for monogas vehicles (solely powered by natural gas) is 50% of the prevailing petrol vehicles rates.

(iii) Road tax for bi-fuel vehicles (petrol

vehicles converted to use natural gas) is 25% of the current rate.

(iv) Road tax for dual-fuel vehicles (diesel

vehicles converted to use natural gas) is 25% of the existing rate. The reduction of 25% is also applicable to the new generation diesel engines which enjoy 50% reduction.

v) The road tax for vintage cars is 10% of

the prevailing rate

(i) Petrol Engine Capacity Marginal tax in c.c rate (RM) per c.c 0 - 1000 0.13 1001 - 1200 0.15 1201 - 1500 0.20 1501 - 2000 0.35 2001 - 2500 1.00 2501 - 3000 2.50 > 3000 4.50 (ii) Diesel Four times the above rates. Private passenger car owned by a company: (i) Petrol Three times the rate in (i) above. (ii) Diesel Two times the rate in (ii) above.

47

Tax Nature of Tax Exemptions and Deductions Rates

Non-saloon motor vehicles (i) Petrol Not exceeding 7 seats (including driver) Engine Capacity Tax Rates 0 - 1000 RM200.00 1001 - 1200 15 sen per cc 1201 - 1500 20 sen per cc 1501 - 2000 35 sen per cc 2001 - 2500 80 sen per cc > 2501 RM1.60 per cc Exceeding 7 seats but Above ratesnot exceeding 15 seats plus25% of (including driver) those rates Exceeding 15 seats but Above rates Not exceeding 35 seats plus 45% of (including driver) those rates Exceeding 20 seats but Above ratesNot exceeding 35 seats plus 55% of (including driver) those rates Exceeding 30 seats but Above rates(including driver) plus 70% of those rates

48

Tax Nature of Tax Exemptions and Deductions Rates

(ii) Diesel 4 times the above rates Taxi cabs & cars for hire (i) Petrol 1600 cc & < - 12 sen per cc 1601 - 1800 cc - 14 sen per cc 1801 - 2200 cc - 18 sen per cc 2201 - 2600 cc - 22 sen per cc > 2600 cc - 30 sen per cc (ii) Diesel - 3 times the above rates Limousine taxi (i) Petrol - RM 0.12 per cc (ii) Diesel - RM 0.44 per cc . School Buses 20 & < persons - RM 52.50 per year 21 - 30 persons - RM 75.00 per year > 30 persons - RM 105.00 per year

49

Tax Nature of Tax Exemptions and Deductions Rates

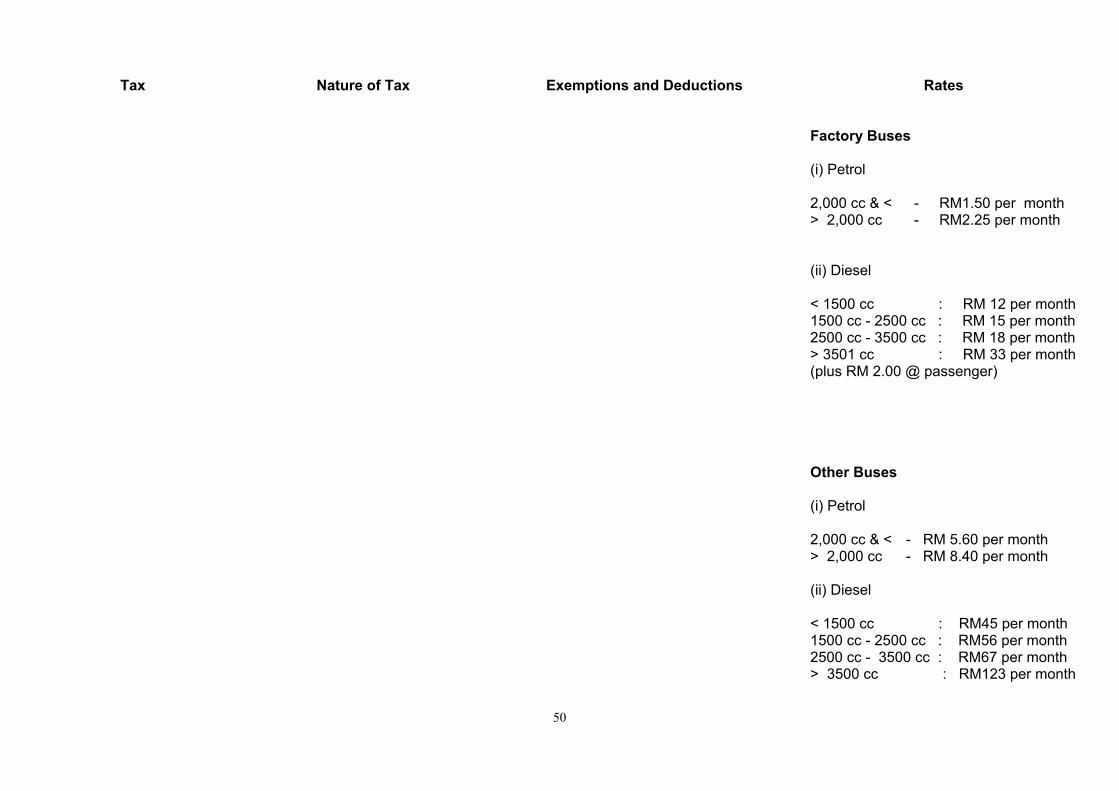

Factory Buses (i) Petrol 2,000 cc & < - RM1.50 per month > 2,000 cc - RM2.25 per month (ii) Diesel < 1500 cc : RM 12 per month 1500 cc - 2500 cc : RM 15 per month 2500 cc - 3500 cc : RM 18 per month > 3501 cc : RM 33 per month (plus RM 2.00 @ passenger) Other Buses (i) Petrol 2,000 cc & < - RM 5.60 per month > 2,000 cc - RM 8.40 per month (ii) Diesel < 1500 cc : RM45 per month 1500 cc - 2500 cc : RM56 per month 2500 cc - 3500 cc : RM67 per month > 3500 cc : RM123 per month

50

Tax Nature of Tax Exemptions and Deductions Rates

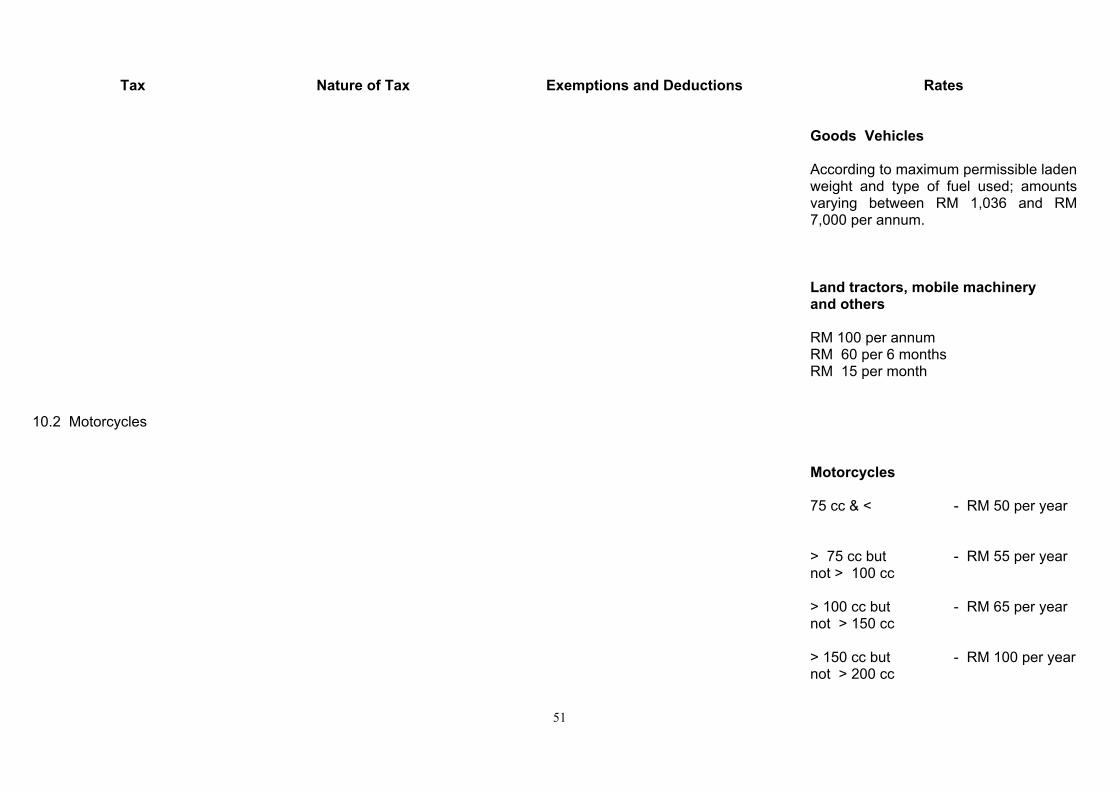

Goods Vehicles According to maximum permissible laden weight and type of fuel used; amounts varying between RM 1,036 and RM 7,000 per annum. Land tractors, mobile machinery and others RM 100 per annum RM 60 per 6 months RM 15 per month

10.2 Motorcycles

Motorcycles 75 cc & < - RM 50 per year > 75 cc but - RM 55 per year not > 100 cc > 100 cc but - RM 65 per year not > 150 cc > 150 cc but - RM 100 per year not > 200 cc

51

Tax Nature of Tax Exemptions and Deductions Rates

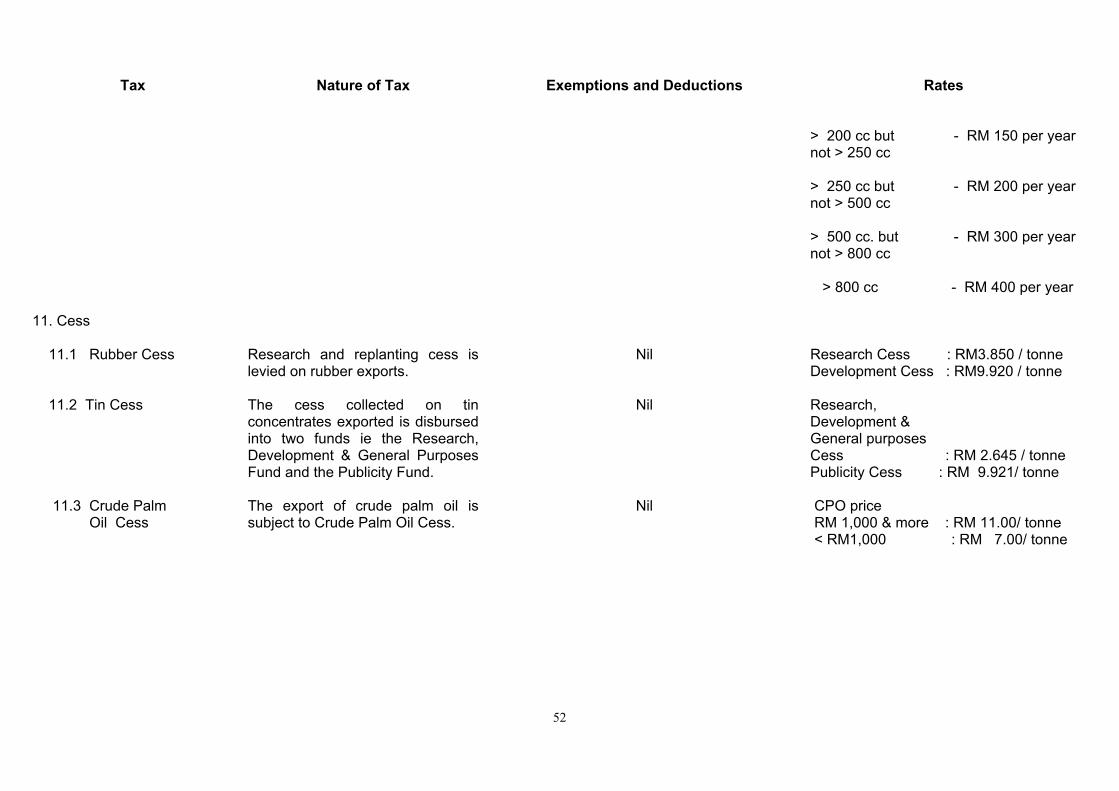

> 200 cc but - RM 150 per year not > 250 cc > 250 cc but - RM 200 per year not > 500 cc > 500 cc. but - RM 300 per year not > 800 cc > 800 cc - RM 400 per year

11. Cess 11.1 Rubber Cess 11.2 Tin Cess 11.3 Crude Palm Oil Cess

Research and replanting cess is levied on rubber exports. The cess collected on tin concentrates exported is disbursed into two funds ie the Research, Development & General Purposes Fund and the Publicity Fund. The export of crude palm oil is subject to Crude Palm Oil Cess.

Nil

Nil

Nil

Research Cess : RM3.850 / tonne Development Cess : RM9.920 / tonne Research, Development & General purposes Cess : RM 2.645 / tonne Publicity Cess : RM 9.921/ tonne CPO price RM 1,000 & more : RM 11.00/ tonne < RM1,000 : RM 7.00/ tonne

52

Tax Nature of Tax Exemptions and Deductions Rates

12. Levy On Goods

Vehicles (Goods Vehicles Levy

Act, 1983)

This is levied on all goods vehicles - leaving the country (whether laden or empty) - entering the country ( laden).

Exempted from levy are:- - goods vehicles carrying selected perishable

goods exclusively for the Singapore market;

- all goods vehicles leaving for Thailand; - Government vehicles, goods vehicles used

for the purpose of a funeral and goods vehicles within the scope of the Memorandum of Understanding between Malaysia and Thailand.

- 50% exemption for goods vehicles

carrying selected construction materials. - Full exemption for goods vehicles carrying

ISO containers from Port of Tanjung Pelepas.

(i) RM 200 for each goods vehicle leaving the country (whether laden or empty). (ii) RM 100 for each goods vehicle entering the country (laden).

13. Levy On Foreign Workers

(Fees Act 1951)

This is levied on all foreign workers on an annual basis.

This levy paid is allowed as a rebate against income tax payable. Workers in padi field and sugar plantation are exempted from paying the levy

Sabah / Sarawak Rate of levy/year (i) Domestic help & RM 360 plantation sector (ii) Other sectors RM 960

53

Tax Nature of Tax Exemptions and Deductions Rates

14. Windfall Levy

(Windfall Levy Act 1998)

Windfall levy is imposed on crude palm oil and crude palm kernel oil when their prices exceed RM2,000 per tonne

Semenanjung Rate of levy/year i) Domestic help & RM 360 plantation sector (ii) Other sectors RM 1.200 Price range Rate of Levy (RM / tonne) (RM / tonne) 2,000 & less Nil > 2,000 < 2,050 The difference

between the selling price and RM 2000.00 2,050 & more 50

54