machine-to-machine technologies & markets - shift … technologies & markets - shift of...

TRANSCRIPT

1© 2013 J. Alonso-Zarate

Machine-to-Machine Technologies & Markets - Shift of Industries

Mischa Dohler, Chair Professor, King’s College London, UK

Matt Hatton, Director of Machina Research, UK

Jesus Alonso-Zarate, Head of M2M Department, CTTC, Spain

IEEE GLOBECOM 2013

Atlanta, Georgia, USDecember 2013

2© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

1. Introduction to M2M and the IoT [Mischa]

2. M2M Technology Landscape [Jesus]

3. Commercial Issues [Matt]

Overview of Tutorial

3© 2013 J. Alonso-Zarate

Disclaimer

Many third party copyrighted material is reused within this talk under the 'fair use' approach, for sake of educational purpose only, and very limited edition.

As a consequence, the current slide set presentation usage is restricted, and is falling under usual copyrights usage.

Thank you for your understanding!

4© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

The Vision

5© 2013 J. Alonso-Zarate

Internet of Things is all about…Things(Useful)

People

Connectivity

Interoperability

Energy Efficiency

Added Value

Big Data

Business

Privacy and Security

Well-Being

6© 2013 J. Alonso-Zarate

IoT can become a new revolution

http://www.gereports.com/new_industrial_internet_service_technologies_from_ge_could_eliminate_150_billion_in_waste/

7© 2013 J. Alonso-Zarate

Applications

© http://postscapes.com/internet-of-things-examples/

8© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Smart Cities

9© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Internet(Open Data)

Crowdsourcing

Sensor Streams(Real Time) Improve Efficiency

Offer New Services

BIG DATAAnalytics

Power Applications

M2M Platforms for the IoT

Machine-to-Machine

Human-to-Machine

Information-to-Machine

DATA

KNW

W

INFO

10© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Technological Challenges

Device Domain

Network DomainM2M

Communications

Applications Domain

11© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

M2M Communications: The Access Network

12© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

A General View (Wireless)

13© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

M2M Prime Business Criteria

Reliability

Availability

Zigbee-like

Bluetooth LE

Low Power WLANProprietary Cellular

Standardized Cellular

Wired M2M

Availability = coverage, roaming, mobility, critical mass in rollout, etc.Reliability = resilience to interference, throughput guarantees, low outages, etc.(Total Cost of Ownership = CAPEX, OPEX.)

14© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Standardized M2M Protocol Stack

IEEE

IETF

3GPP

15© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

2.1Capillary Networks (Zigbee-like and LP-WIFI)

16© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

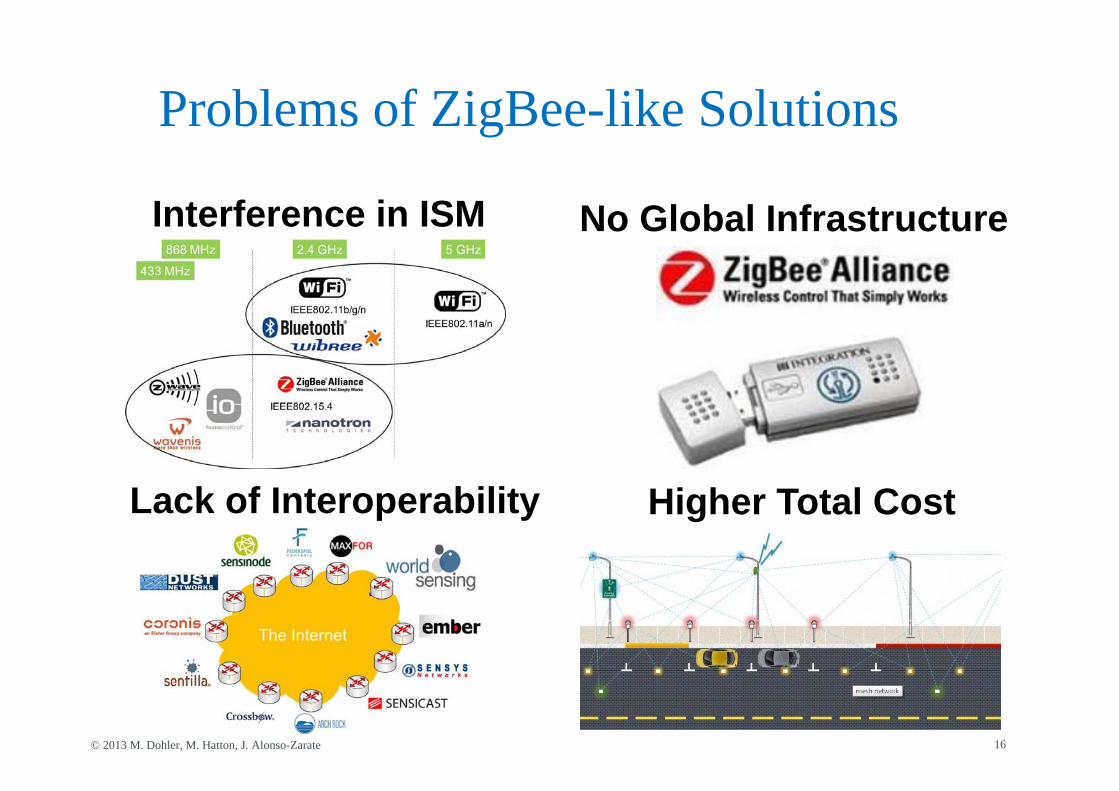

Problems of ZigBee-like Solutions

Interference in ISM No Global Infrastructure

Lack of Interoperability Higher Total Cost

2bn Wifi Devices

WPA2/PSK/TLS/SSL

17© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Advantages of Low-Power WiFiUbiquitous Infrastructure Vibrant Standard

Interference Management Sound Security

2bn Wifi Devices300 members

NAV Medium Reservation

WPA2/PSK/TLS/SSL

Source: Wireless Broadband Access (WBA), Informa, Nov. 2011

18© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

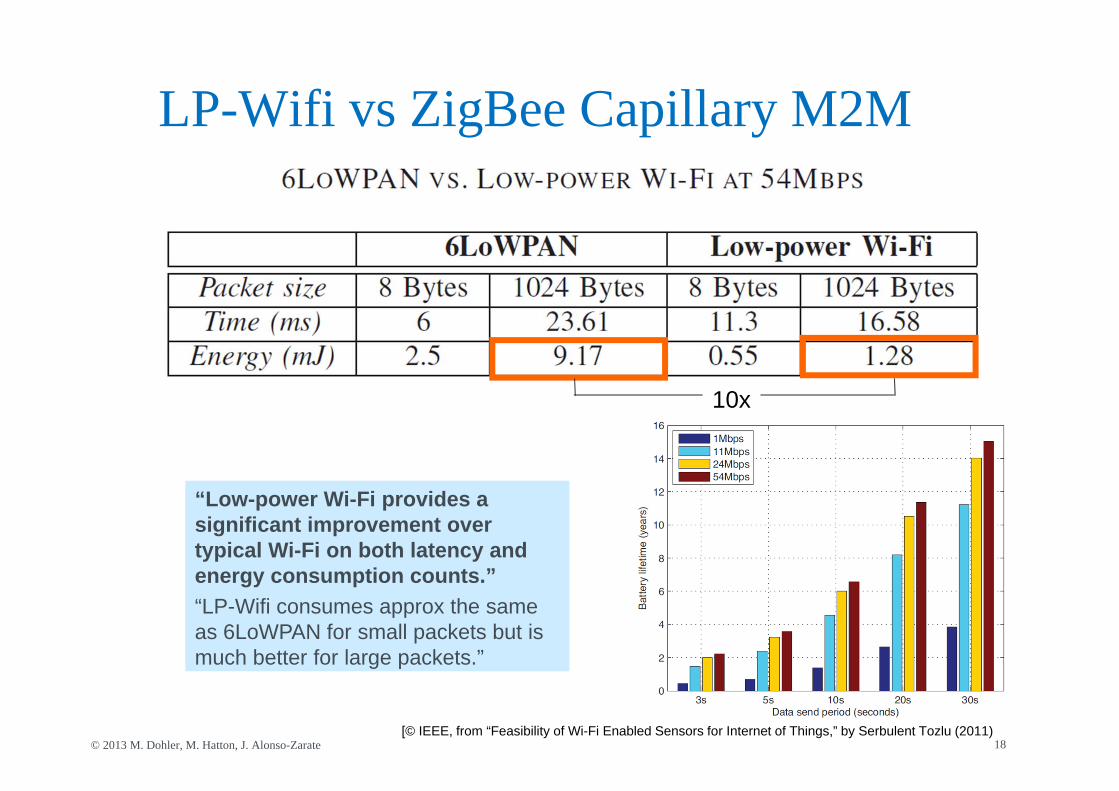

LP-Wifi vs ZigBee Capillary M2M

[© IEEE, from “Feasibility of Wi-Fi Enabled Sensors for Internet of Things,” by Serbulent Tozlu (2011)

“Low-power Wi-Fi provides a significant improvement over typical Wi-Fi on both latency and energy consumption counts.”“LP-Wifi consumes approx the same as 6LoWPAN for small packets but is much better for large packets.”

10x

19© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Low-Power Wifi Eco-System [examples]

20© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Low-Power Wifi Products [© Gainspan]

21© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Cellular M2M

22© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Advantages of Cellular M2MUbiquitous Coverage Mobility & Roaming

Interference Control

23© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

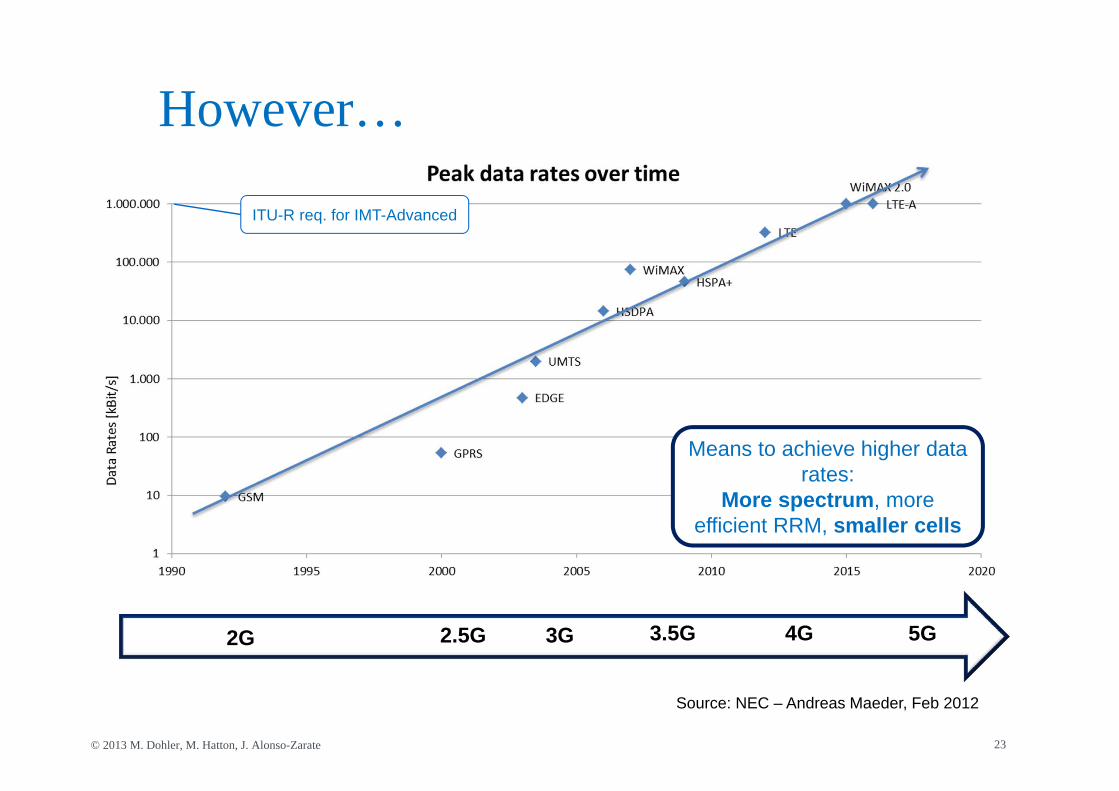

However…

Exabyte = 10^182G 2.5G 3G 3.5G 4G 5G

Means to achieve higher data rates:

More spectrum, more efficient RRM, smaller cells

ITU-R req. for IMT-Advanced

Source: NEC – Andreas Maeder, Feb 2012

24© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Key Technical Novelties

Cellular Networks have been designed for humans!

Accommodation of M2M requires paradigm shift: There will be a lot of M2M nodes More and more applications are delay-intolerant, mainly control There will be little traffic per node, and mainly in the uplink Nodes need to run autonomously for a long time Automated security & trust mechanisms

… and all this without jeopardizing current cellular services!

25© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

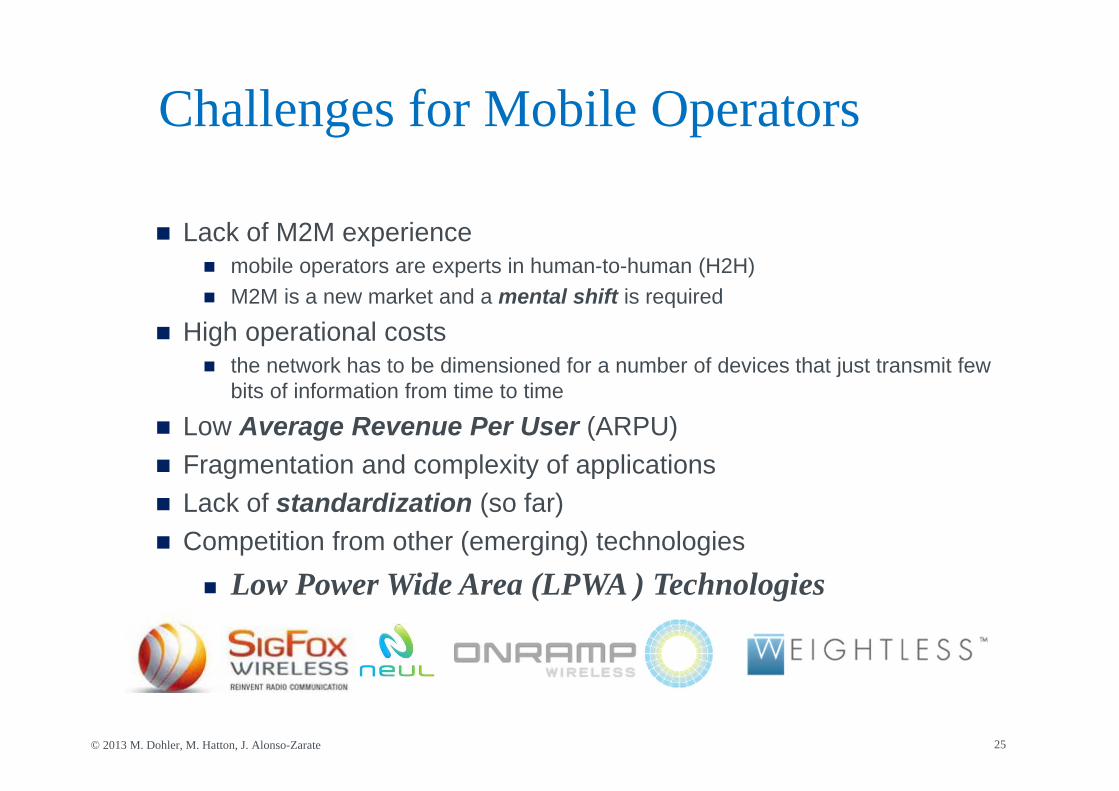

Challenges for Mobile Operators

Lack of M2M experience mobile operators are experts in human-to-human (H2H) M2M is a new market and a mental shift is required

High operational costs the network has to be dimensioned for a number of devices that just transmit few

bits of information from time to time

Low Average Revenue Per User (ARPU) Fragmentation and complexity of applications Lack of standardization (so far) Competition from other (emerging) technologies

Low Power Wide Area (LPWA ) Technologies

26© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

2.2.1M2M in Current Cellular NetworksHow suitable are current technologies for M2M?

27© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

GSM – PHY and MAC Layers

PHY Layer Carrier Frequency: 900 MHz, 1.8 GHz, and others. Simple Power Management:

8 power classes; min 20 mW = 13 dBm (2dB power control steps)

Modulation with Constant envelope (good for PA) PHY Data Rates: 9.6 Kbps Low Complexity

MAC Layer Duplexing: FDD FDMA/TDMA + ALOHA-based access

Traffic Type: Voice, Data, 160 7-bit SMS.

28© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Beyond GSM – GPRS & EDGE

GPRS = GSM + … … more time slots for users + … adaptive coding schemes

EDGE = GPRS + … … 8PSK modulation scheme

29© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

UMTS – PHY and MAC Layers

PHY Layer Carrier Frequency: 2Ghz, and others. Instantaneous Power Management CDMA Modulation: Variable envelope PHY Data Rates: >100 kbit/s packet switched Medium Complexity

MAC Layer Duplexing: FDD FDMA/CDMA (256 codes) + ALOHA-based access

Traffic type: conversational, streaming, interactive, background.

30© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

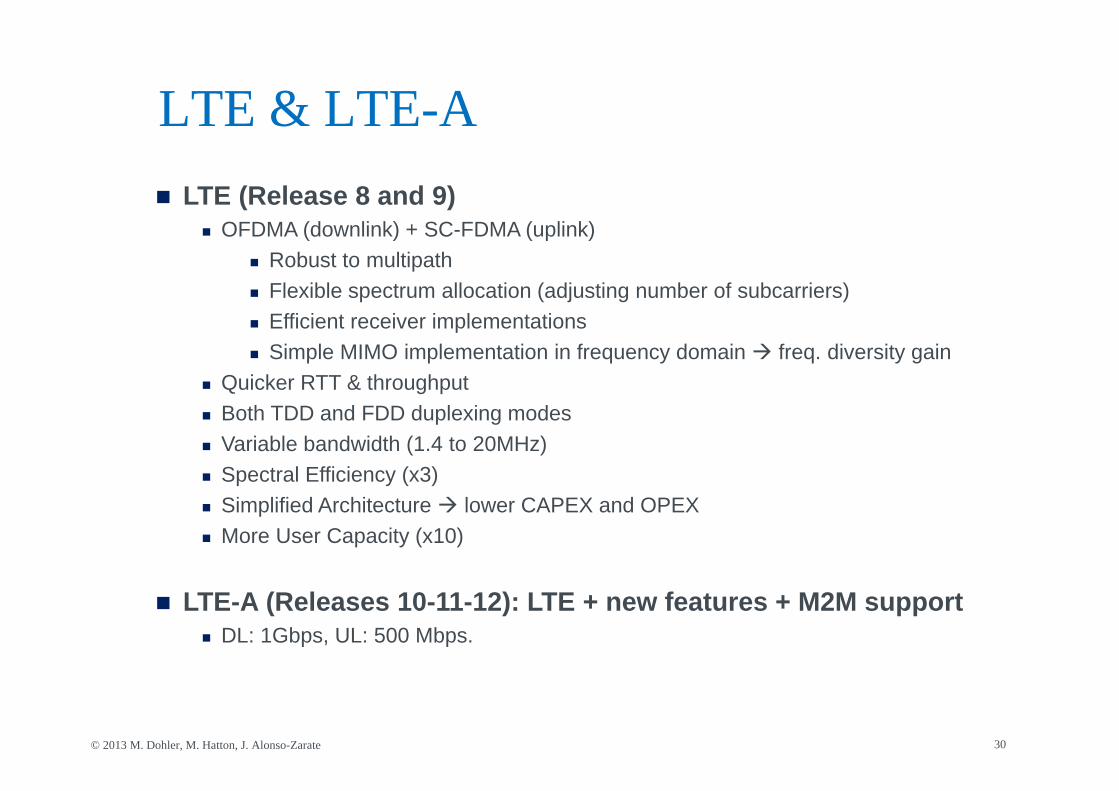

LTE & LTE-A LTE (Release 8 and 9)

OFDMA (downlink) + SC-FDMA (uplink) Robust to multipath Flexible spectrum allocation (adjusting number of subcarriers) Efficient receiver implementations Simple MIMO implementation in frequency domain freq. diversity gain

Quicker RTT & throughput Both TDD and FDD duplexing modes Variable bandwidth (1.4 to 20MHz) Spectral Efficiency (x3) Simplified Architecture lower CAPEX and OPEX More User Capacity (x10)

LTE-A (Releases 10-11-12): LTE + new features + M2M support DL: 1Gbps, UL: 500 Mbps.

31© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Key Limitations of LTE & LTE-AFDD: 2x35MHzFDD: 2x70MHz

TDD: 50MHz

VerizonAT&T

metroPCS

AWS

NTT DoCoMo

TeliaSoneraVodafone

O2…

Refarming and extensions are still to come…

Hong-Kong

China MobileGenius Brand

CSL Ltd…

Digital Dividend

Major TD-LTE Market(incl. India)

Fragmentation & Harmonization of Spectrum is a critical problem!

Source: presentation by Thierry Lestable, Sagemcom, BEFEMTO Winter School, Barcelona, Feb. 2012.

32© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Key Limitations of LTE & LTE-A Not efficient for small data transmission Scheduled Radio access

Random access and more flexibility

Device cost issues Scalable bandwidth Data rate (overdesigned UE categories) Transmit power (max. 23dBm) Half Duplex operation (simpler device) RF chains with 2 antennas Signal processing accuracy

Overload issues big number of devices High mobility support

Source: IP-FP7-258512 EXALTED D3.1

33© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

2.2.2Standardization Activities

http://www.3gpp.org/ftp/Information/WORK_PLAN/Description_Releases/M2M_20130924.zip

34© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Standards for Cellular M2M Industry has become more active in standardizing M2M:

Because of the market demand Essential for long term development of technology For interoperability of networks Ability to “roam” M2M services over international frontiers

Due to potentially heavy use of M2M devices and thus high loads onto networks, interest from: ETSI TC M2M and recently oneM2M Partnership Project 3GPP (GSM, EDGE GPRS, UMTS, HSPA, LTE) IEEE 802.16 (WiMAX)

35© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

ETSI: Inverting the pipes

© ETSI

36© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

ETSI: Functional Architecture

© ETSI

Core Network:- IP Connectivity- Interconnection with other networks- Roaming with other core networks- Service and Network control

Service Capabilities shared by different applications

Registration, Authentication, Authorization, Management, Provisioning

37© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Creation of oneM2M Partnership project

Japan

USAChina

Korea

38© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

ETSI Smart Card Platform (2000)

SIM: Subscriber Identity Module more than 4B in circulation Evolution to UICC (Universal Integrated Circuit Card)

CPU, RAM, ROM, EEPROM, I/O. June 2012, 4th Form Factor (nano-SIM , from Apple) Technical Specs TS 102 221 v11.0.0 (2012-06)

http://www.etsi.org/deliver/etsi_ts/102200_102299/102221/11.00.00_60/ts_102221v110000p.pdf

Data of the SIM: ICCID: identifier IMSI Authentication key Location Area Identity User data: Contacts and SMS

Embedded SIMs for M2M

39© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

3GPP: M2M Features

A feature is a system optimization possibility Different requirements different optimizations Offered on a per subscription basis:

Low Mobility Time Controlled Time Tolerant Small Data Transmissions Mobile originated only Infrequent Mobile Terminated MTC Monitoring

Priority Alarm Message (PAM) Secure Connection Location Specific Trigger Infrequent transmission Group Based features

Policing Addressing

40© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

2.3Specific M2M Architectures & Performance

41© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

2.3.1Tools to Play Around with the IoT

42© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Tools

Math Computer-based Simulators (MATLAB, Ns-3 Simulator)

Cellular (LENA simulator) Capillary Networks (Zigbee-Like, WiFi, etc.)

Testbeds Arduino, WizziMotes, PanStamps, Raspberry Pi,

OpenMAC, WARP, Digi Xbee Modules, etc. Free M2M Platforms in the Cloud

Xybely, Thingspeak, etc.

43© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

2.3.2A Possible M2M Architecture

EXALTED was an FP7 funded IP Project (#258512)

44© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

ICT EXALTEDExpanding LTE for Devices

At A Glance: EXALTED

Expanding LTE for Devices

Project Coordinator Djelal RaoufSagemcom SASTel: +33 (0)1 57 61 20 08Fax: +33 (0)1 57 61 39 09Email: [email protected] website: www.ict-exalted.eu

Partners: Vodafone Group Services Limited (UK), Vodafone Group Services GmbH (DE), Gemalto (FR), Ericsson d.o.o. Serbia (RS), Alcatel-Lucent (DE), Telekom Srbija (RS), Commissariat à l’énergie atomique et aux energies alternatives (FR), TST Sistemas S.A. (ES), University of Surrey (UK), Centre Tecnològic de Telecomunicacions de Catalunya (ES), TUD Vodafone Chair (DE), University of Piraeus Research Center (GR), Vidavo SA (GR)

Duration: Sept. 2010 – Feb. 2013Funding scheme: IPTotal Cost: €11mEC Contribution: €7.4m

Contract Number: INFSO-ICT-258512

45© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

LTE-M: Backwards compatible solution

PHY Layer

Use of TDD

Generalized FDM for Uplink (beyond SC-FDMA)

Use of LDPC Codes instead of Turbo Codes

Low-Complexity MIMO

Cooperative Relaying

Some Specific EXALTED Solutions

46© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Higher Layers:

Optimal scheduling with energy-harvesting

Scheduling for heterogeneous traffic (event-driven or periodic)

Discontinuous Reception (DRX): Duty Cycle

Use of RACH for small data transmission, adding CDMA for

data collision recovery.

Some Specific EXALTED Solutions

47© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

2.3.3High Number of Devices: The access to the network

The Random Access Channel (RACH) of LTE

48© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Examples of RACH Configuration

1.08 MHz(6 PRBs)

Less resources for data!

49© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

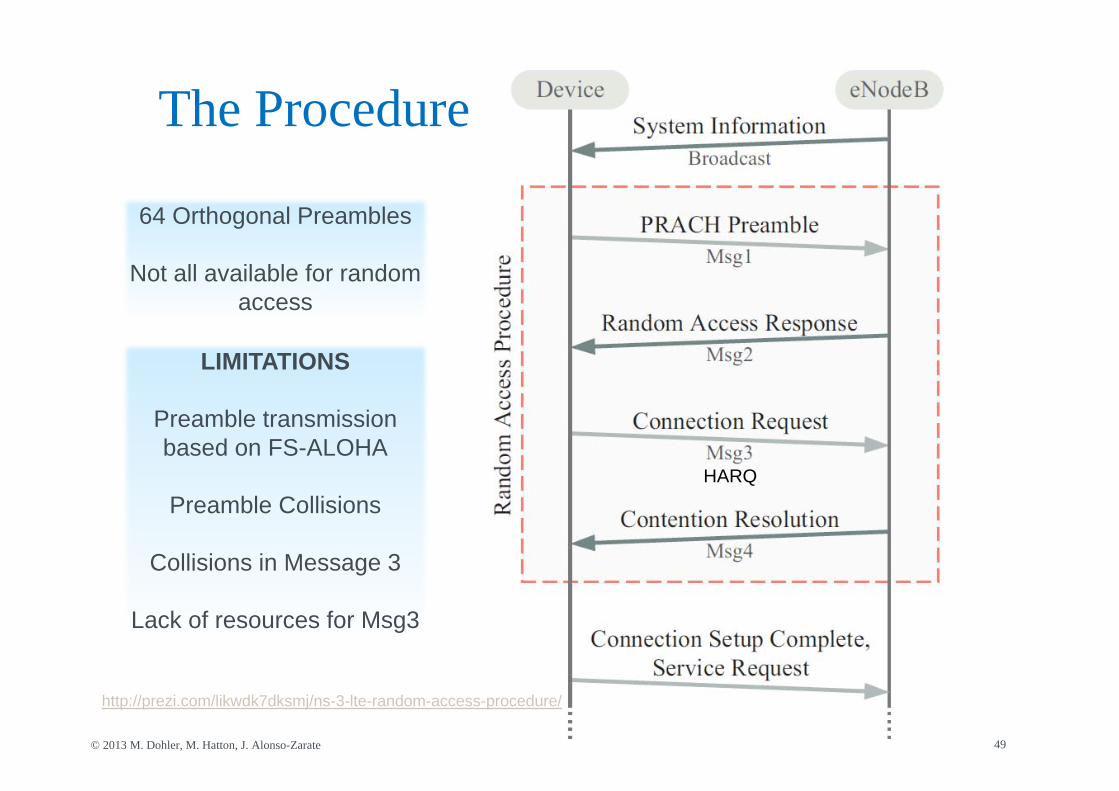

The Procedure

64 Orthogonal Preambles

Not all available for randomaccess

HARQ

LIMITATIONS

Preamble transmissionbased on FS-ALOHA

Preamble Collisions

Collisions in Message 3

Lack of resources for Msg3

http://prezi.com/likwdk7dksmj/ns-3-lte-random-access-procedure/

50© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Blocking Probability: bulk arrival

MAX retx = 10

51© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Energy Consumption: bulk arrival

MAX retx = 10

52© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Blocking Probability: more retx

53© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Energy Consumption: more retx

54© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

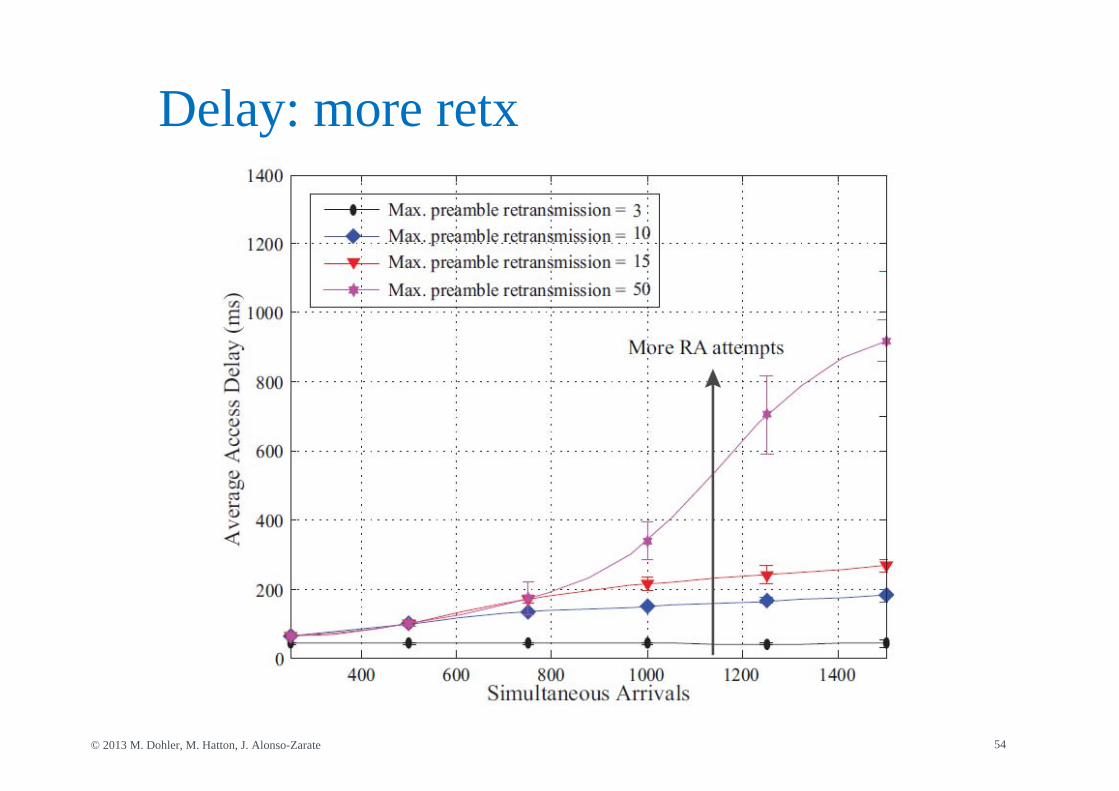

Delay: more retx

55© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

RACH Improvements

A. Laya, L. Alonso, J. Alonso-Zarate“Is the Random Access Channel of LTE and LTE-A Suitable for M2M Communications? A Survey of Alternatives”IEEE Tutorials and Survey Communications MagazineSpecial Issue on Machine-to-Machine Communications. Publication Date: January 2014.

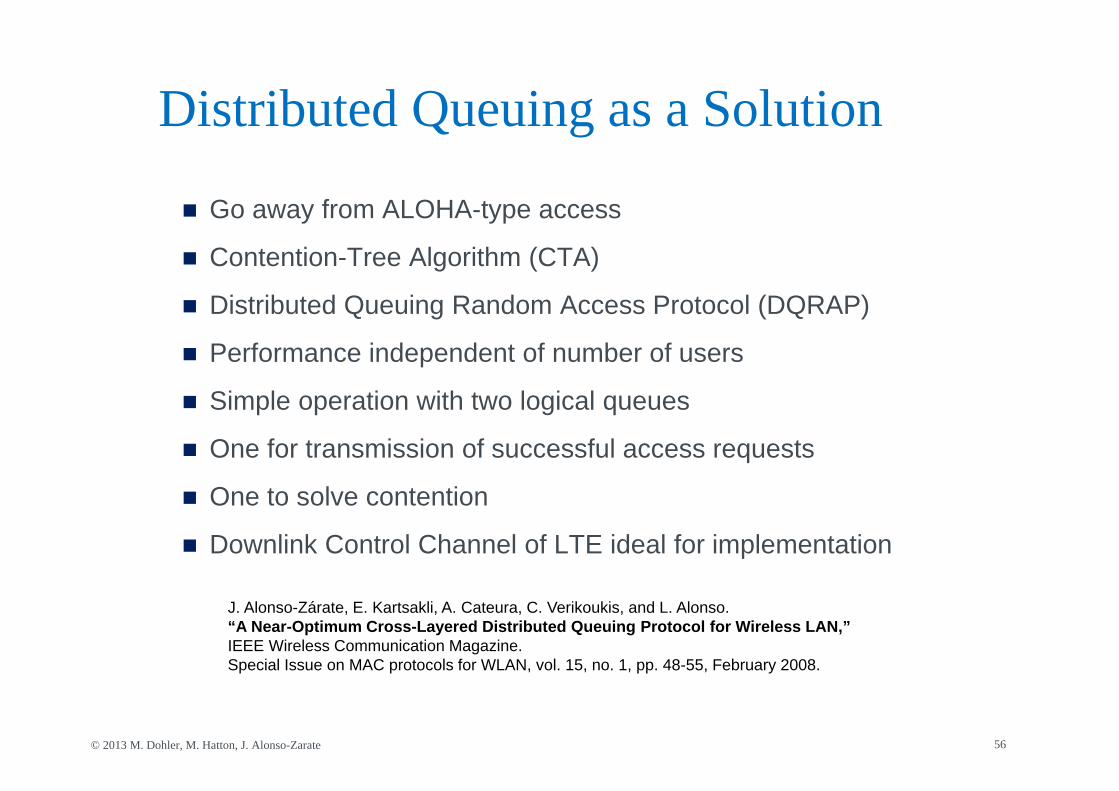

56© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Go away from ALOHA-type access

Contention-Tree Algorithm (CTA)

Distributed Queuing Random Access Protocol (DQRAP)

Performance independent of number of users

Simple operation with two logical queues

One for transmission of successful access requests

One to solve contention

Downlink Control Channel of LTE ideal for implementation

Distributed Queuing as a Solution

J. Alonso-Zárate, E. Kartsakli, A. Cateura, C. Verikoukis, and L. Alonso.“A Near-Optimum Cross-Layered Distributed Queuing Protocol for Wireless LAN,”IEEE Wireless Communication Magazine. Special Issue on MAC protocols for WLAN, vol. 15, no. 1, pp. 48-55, February 2008.

57© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

2.3.4Coexistence of Machines and Humans

58© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

0 20000 40000 60000 80000 1000000.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Dro

p pr

obab

ility

MTC number

HTC MTCMethod 1 Method 2

Impact of MTC onto HTC Dropping probabilities, duty cycle and delay for 30min access case:

© Kan Zheng, Jesus Alonso-Zarate, and Mischa Dohler

59© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

2.3.5Limitations of the RLC layer

60© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

RRC State Transitions

61© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Impact of MTC onto HTC “A Close Examination of Performance and Power Characteristics of 4G LTE

Networks,” by J. Huang, F. Qian, A. Gerber. MobiSYS’12.

LTE

screen

3G

WiFi

62© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

2.3.6Optimizing LTE for Small Data Transmissions

K. Wang, J. Alonso-Zarate, M. Dohler,“Energy-Efficiency of LTE for Small Data Machine-to-Machine Communications,”in proc. of the IEEE ICC 2013, Budapest, Hungary, June 2013.

63© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

0 5 10 15 20 25-10

-5

0

5

10

15

MCS Index

Tran

smit

Pow

er (d

Bm

)

Transport Block Size vs. MCS

64© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

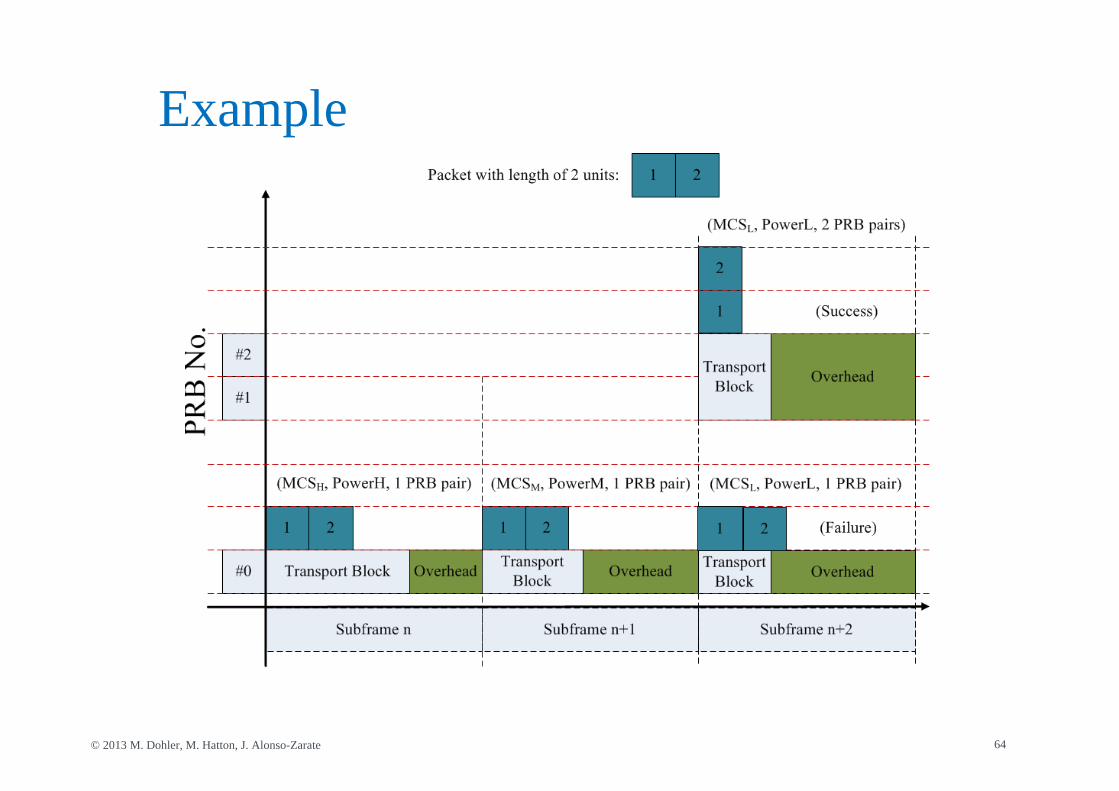

Example

65© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

The Optimal MCS

0 5 10 15 20 250

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

MCS Index

Tran

spor

t Blo

ck U

tiliz

atio

n R

ate

(Pac

ket s

ize/

TB

S)

10 bytes packet35 bytes packet60 bytes packet

66© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

The Optimal MCS

0 5 10 15 20 250

1

2

3

4

5

6x 109

MCS Index

Ene

rgy

Effi

cien

cy η

(bits

/Jou

le)

10 bytes packet35 bytes packet60 bytes packet

67© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Humans in the Loop

68© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Machines can do what we cannot

69© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Machines can do better than us…

70© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

An Example:26 November 2013Employees against use of automatic supermarket check-out

71© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

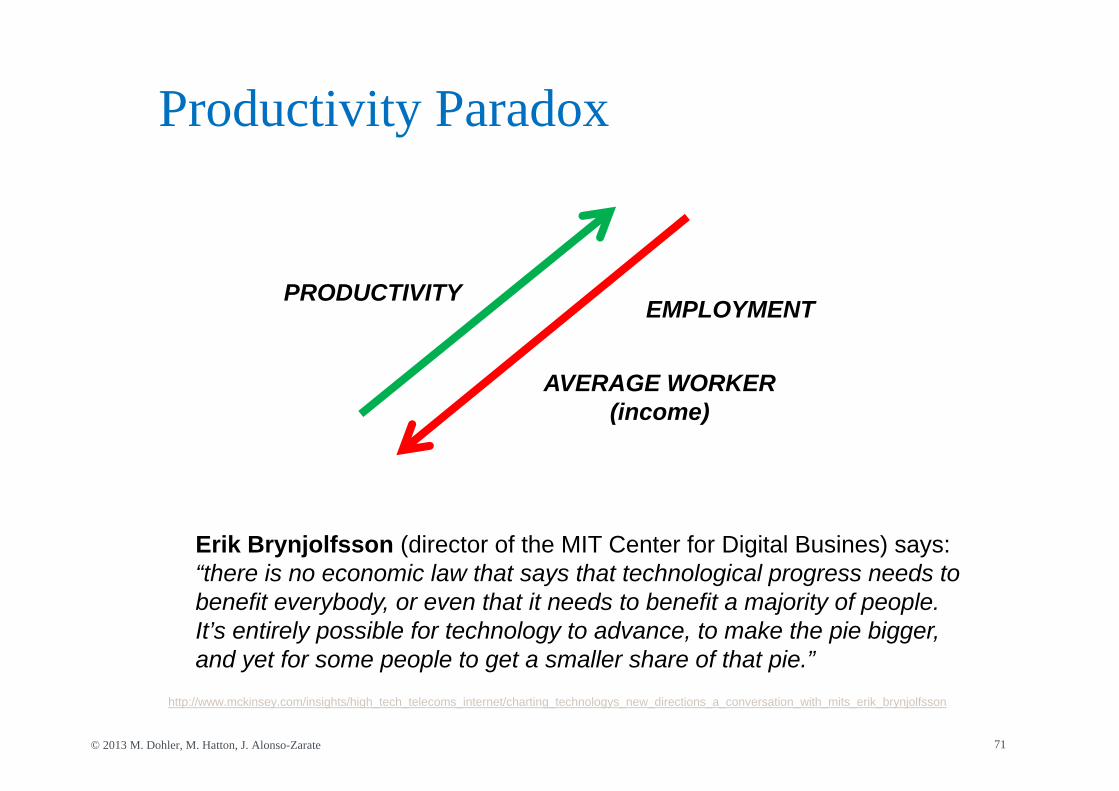

Productivity Paradox

PRODUCTIVITY

AVERAGE WORKER(income)

EMPLOYMENT

Erik Brynjolfsson (director of the MIT Center for Digital Busines) says: “there is no economic law that says that technological progress needs to benefit everybody, or even that it needs to benefit a majority of people. It’s entirely possible for technology to advance, to make the pie bigger, and yet for some people to get a smaller share of that pie.”

http://www.mckinsey.com/insights/high_tech_telecoms_internet/charting_technologys_new_directions_a_conversation_with_mits_erik_brynjolfsson

72© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Decoupling Technology & Economy

VS

73© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Commercial Issues

M2MCommercial issues

Matt Hatton, Director

Machina Research

December 2013

Agenda

• About Machina Research• What is M2M?• Technology• Management/control• Data analytics• The revenue opportunity

Machina Research 75

About Machina Research

Market/demand side Provider/supply side

• Quantifying the opportunity for M2M – Forecast Database providing 10

year forecasts across 201 countries for 61 application groups

– Sector Reports annually updated reports on our 13 sectors (including Automotive, Healthcare and Utilities)

• Addressing the issues that determine success– Research Notes - 3 per month on

major qualitative issues such as platforms, value chain roles, big data, NFC, and security

– Strategy Reports - covering areas such as Big Data, platforms, modules/devices, CSP best practice, etc.

Advisory Service and Custom Research

76Machina Research

Some of our clients

Machina Research 77

Agenda

• About Machina Research• What is M2M?• Technology• Management/control• Data analytics• The revenue opportunity

Machina Research 78

What is M2M?

Machina Research 79

Our definition: “Connections to remote sensing, monitoring and actuating devices,

together with associated aggregation devices”

An incredibly diverse range of products and services with no consistent definition

What is M2M?

Application

Device

Network

Management/control

Data

Machina Research 80

M2M: what’s the point?

Machina Research 81

Sealed Air

Big Belly Solar CLEANeCall Helsinki City Transport

Irrigation in SpainGerbercutter Z7

M2M connections will grow from 2 billion in 2011 to 18 billion in 2022

• Machina Research defines M2M as “Connections to remote sensing, monitoring and actuating devices, together with associated aggregation devices”

• Based on this definition there are 2 billion M2M connections today and this will grow to 18 billion in 2022, a CAGR of 22%

Machina Research 82

Global machine-to-machine connections 2011-22Source: Machina Research 2012

Note that we have included in-building network infrastructure within our definition of M2M for this 2012 version of our Global M2M report. As such, devices such as residential modems/ routers are included this year whereas previously they have not been.

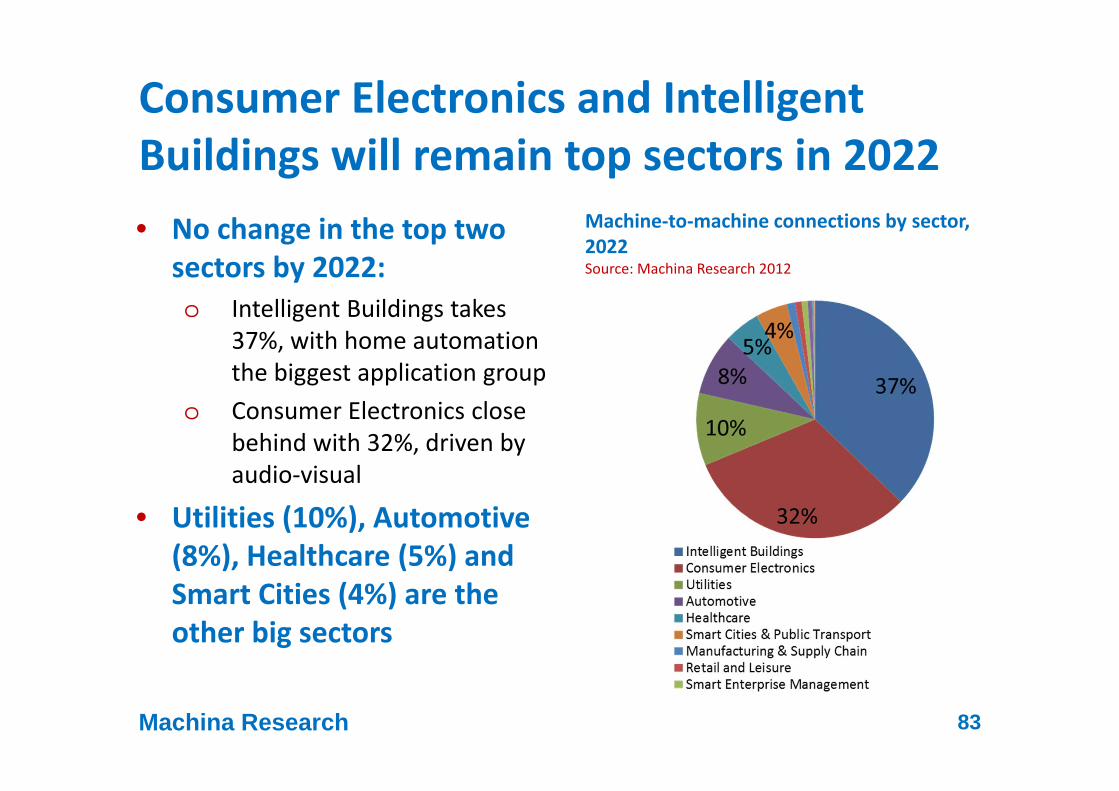

Consumer Electronics and Intelligent Buildings will remain top sectors in 2022• No change in the top two

sectors by 2022: o Intelligent Buildings takes

37%, with home automation the biggest application group

o Consumer Electronics close behind with 32%, driven by audio-visual

• Utilities (10%), Automotive (8%), Healthcare (5%) and Smart Cities (4%) are the other big sectors

Machina Research 83

Machine-to-machine connections by sector, 2022Source: Machina Research 2012

Automotive: 1.8 billion connections and USD422 billion revenue in 2022• By 2022 there will be 1.5

billion automotive M2M connections, 540 million Connected Cars and 1 billion aftermarket devices.

• Overall the M2M market in the automotive sector will generate USD282 billion in 2022, up from USD20 billion in 2012.

• Today 66% of the revenue is accounted for by services. By 2022 that will grow to 89%.

Machina Research 84

Machine-to-machine connections and revenue in the Automotive sector, 2012-22Source: Machina Research 2013

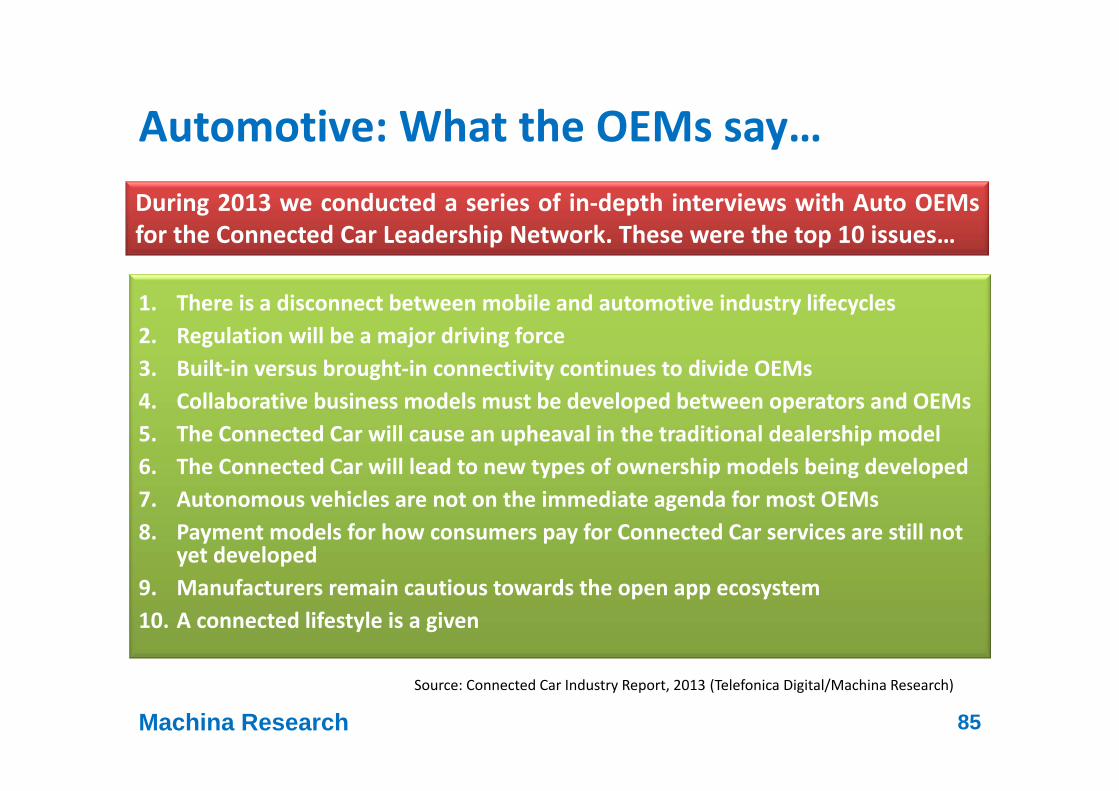

Automotive: What the OEMs say…

1. There is a disconnect between mobile and automotive industry lifecycles2. Regulation will be a major driving force3. Built-in versus brought-in connectivity continues to divide OEMs4. Collaborative business models must be developed between operators and OEMs5. The Connected Car will cause an upheaval in the traditional dealership model6. The Connected Car will lead to new types of ownership models being developed7. Autonomous vehicles are not on the immediate agenda for most OEMs8. Payment models for how consumers pay for Connected Car services are still not

yet developed9. Manufacturers remain cautious towards the open app ecosystem10. A connected lifestyle is a given

Machina Research 85

Source: Connected Car Industry Report, 2013 (Telefonica Digital/Machina Research)

During 2013 we conducted a series of in-depth interviews with Auto OEMsfor the Connected Car Leadership Network. These were the top 10 issues…

Agenda

• About Machina Research• What is M2M?• Technology• Management/control• Data analytics• The revenue opportunity

Machina Research 86

Technology: commercial issues

• There are a diverse range of technologies that can support “M2M” connections, including:o PLMN cellular – GSM, CDMA, UMTS, LTE, WiMAX etc.o Low-power wide area networks – SigFox, Weightlesso Short-range – Zigbee, Z-Wave, DSRC, Etherneto Wide-area fixed technologies – DSL, Cableo Other – Mesh, Broadband Powerline, Satellite

• Many solutions incorporate more than one technology

Machina Research 87

Technology: commercial issues

• Technology choice will typically be determined by a trade-off between price and functionality (including availability)

• Price issues will be associated with both the device and the connectivity

• Cellular devices have large associated licensing fees, as well as typically expensive data plans (next slide)

• With cellular, wider networks economics is influencing network sunsetting

• Cellular networks are sunk costs and M2M often doesn’t need to reflect capex here

• Does the revenue opportunity reflect the cost of network deployment?

Machina Research 88

Connectivity: Typical pricing

Small Medium Large

Bundleddata

25MB 50MB 250MB

Price/month

EUR0.98 EUR1.72 EUR3.19

Overagefees/MB

EUR0.16 EUR0.16 EUR0.16

BundledSMS

25 50 100

Machina Research 89

Price plan/month Data limit

Price per MB overage

USD2.00 100KB USD1.50

USD2.50 500KB USD1.50

USD4.00 2MB USD1.50

USD8.00 10MB USD0.75

USD12.00 50MB USD0.75

USD20.00 500MB USD0.05

Sprint M2M pricingSource: Machina Research 2013

Tele2 Estonia PricingSource: Machina Research 2013

Short-range technologies will dominate M2M

• 73% of connections in 2022 will be short range (e.g. in-building PLC, WiFi, Zigbee, Z-Wave), up from 53% at the end of 2011

• Cellular accounts for 2.6 billion connections in 2022, an increase from 146 million at end of 2011o By 2022 3G takes 45% and

4G/LTE 41%, driven by higher bandwidth requirements and need for future-proofing

• MAN is dominated by mesh and powerline for smart metering

Machina Research 90

Global M2M connections 2011-2022 by technologySource: Machina Research 2012

Low Power Wide Area: Our analysis

• Typical LPWA constraints: o Low bandwidth applicationso Applications that are

tolerant of network latency

• Two main analytical stepso Identifying where LPWA can substitute for existing technologieso Identifying where LPWA can unlock new market potential

Machina Research 91

• Typical LPWA benefits:o Low chipset costso Out-of-the-box connectivityo Long battery life

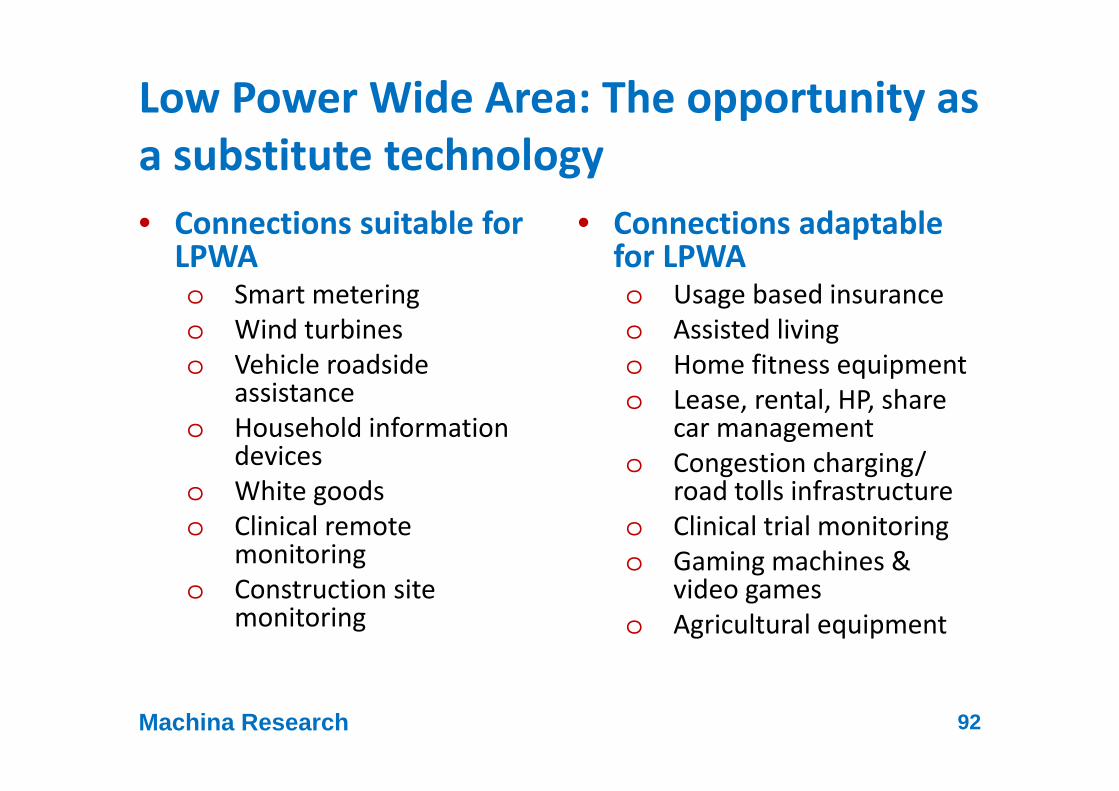

Low Power Wide Area: The opportunity as a substitute technology• Connections suitable for

LPWAo Smart meteringo Wind turbineso Vehicle roadside

assistanceo Household information

deviceso White goodso Clinical remote

monitoringo Construction site

monitoring

• Connections adaptable for LPWAo Usage based insuranceo Assisted livingo Home fitness equipmento Lease, rental, HP, share

car managemento Congestion charging/

road tolls infrastructureo Clinical trial monitoringo Gaming machines &

video gameso Agricultural equipment

Machina Research 92

Low Power Wide Area: Ways it can unlock additional market potential

• Lowering the cost of connectivityo Low cost chipsetso Low cost networks

• Supporting an ‘out of the box’ connected experience

• Enabling an increased battery life• Providing backup connectivity (or simply

more robust connectivity)

Machina Research 93

Low Power Wide Area: Some examples of increased capilliarity• Crop sensing• Alarms of all types• Building automation control panels and

remotes• Parking monitoring• Alarms for the elderly/ infirm• Warehousing/ storage/ distribution• Construction usage and inventory monitoring

Machina Research 94

Low Power Wide Area: The opportunity will be 14.9bn connections by 2022

Machina Research 95

Total LPWA opportunity, 2013-22Source: Machina Research 2013

Total LPWA opportunity, 2022Source: Machina Research 2013

Agenda

• About Machina Research• What is M2M?• Technology• Management/control• Data analytics• The revenue opportunity

Machina Research 96

Management/control

• Driving out complexity and reducing cost in managing M2M will reduce barriers to entry and result in far more M2M connections

• An open model will create more opportunity for innovation and the evolution to the Internet of Things

Machina Research 97

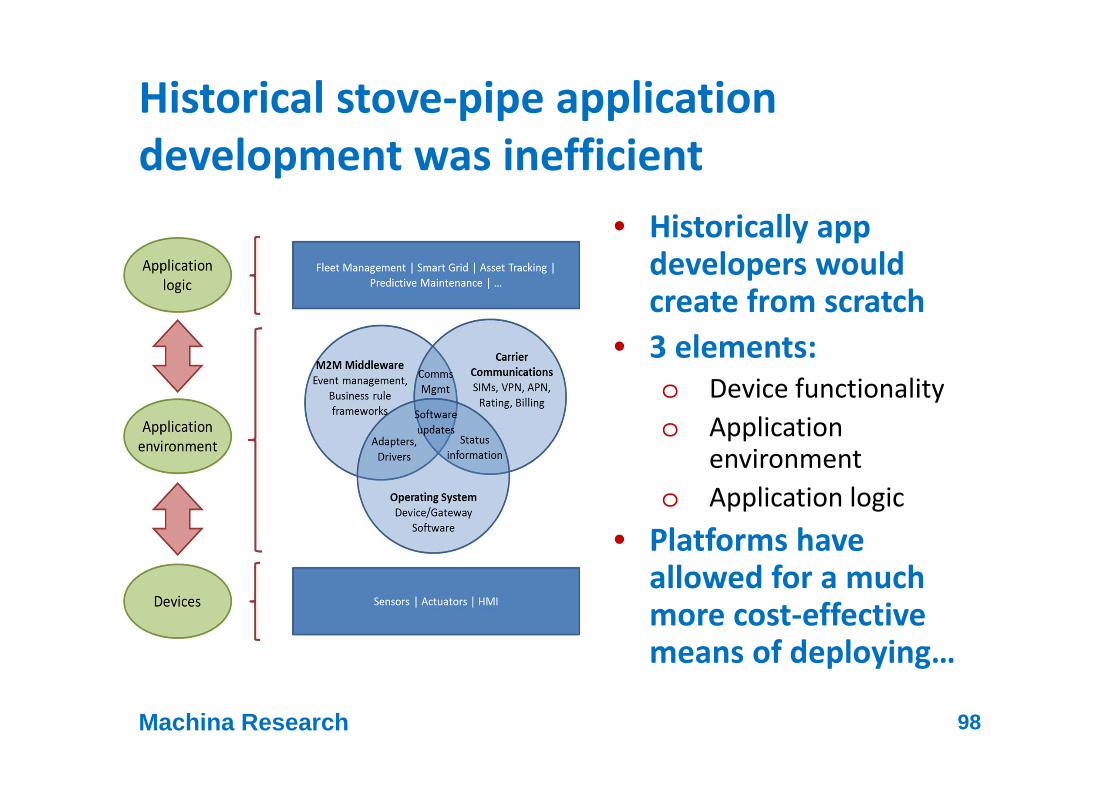

Historical stove-pipe application development was inefficient

• Historically app developers would create from scratch

• 3 elements:o Device functionalityo Application

environmento Application logic

• Platforms have allowed for a much more cost-effective means of deploying…

Machina Research 98

Machina Research 99

M2M Platform Hierarchy of M2MSource: Machina Research 2013

The established platforms hierarchy best supports stovepipe applications

Machina Research 100

Stage Description Comments

1 Reactive information • Devices can be polled for information, or provide information according to a set timetable

2 Proactive information • Devices communicate information as necessary

3 Remotely controllable • Devices can respond to instructions received from remote systems

4 Remotely serviceable • Software upgrades and patches can be remotely applied

5 Intelligent processes • Devices built into intelligent processes

6 Optimised propositions • Use of information to design new products

7 New business models • New revenue streams and changed concept of ‘ownership’

8 The Internet of Things • Publishing information for third parties to incorporate in applications, control commands from diverse sources

Machina Research Hierarchy of M2MSource: Machina Research 2013

Device centric M2M

Process centric M2M

The M2M application environment is evolving

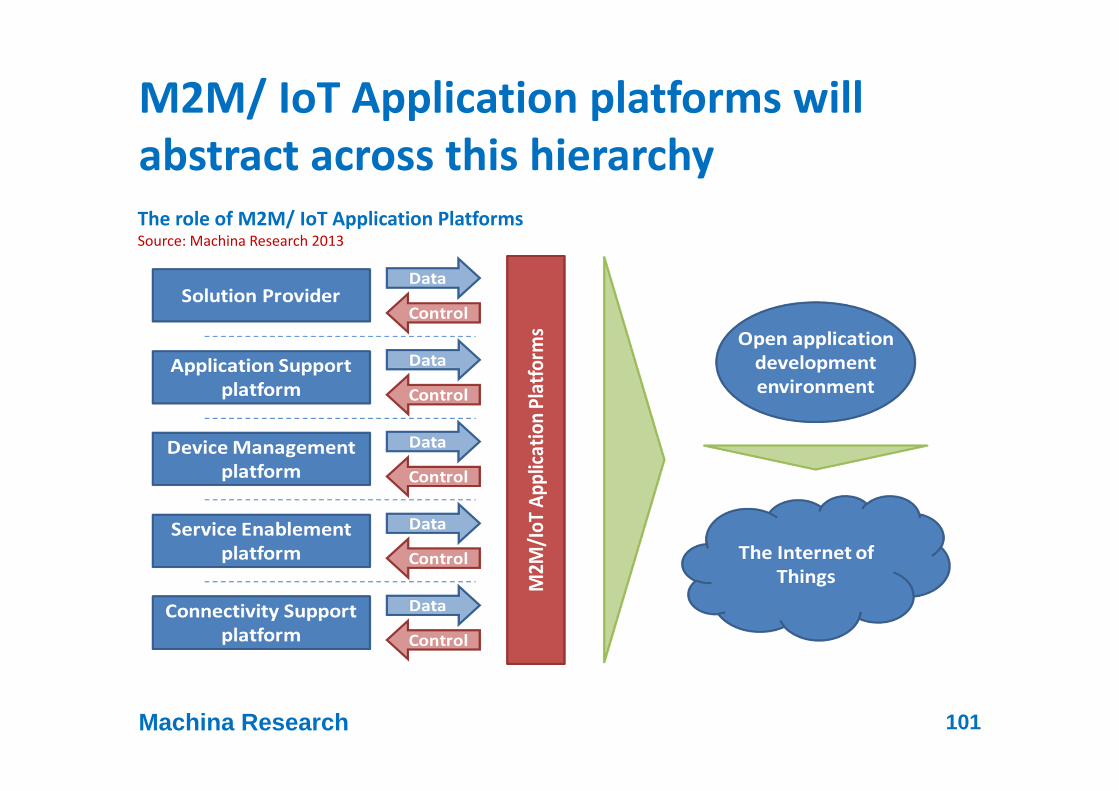

Machina Research 101

The role of M2M/ IoT Application PlatformsSource: Machina Research 2013

M2M/ IoT Application platforms will abstract across this hierarchy

Key functionality of emerging M2M/IoT platforms

Machina Research 102

Carrier Communications

M2M/IoT Application Platform

Device/ OS

KORE

Ericsson

Jasper

Wyless

Bosch ThingWorx

Axeda

Digi

ProSyst

SeeControl

EurotechTridium

Device Insight

Kontron

Sierra Wireless

Telit

Wind RiverNetComm

ILS

Stream

SAP

Aeris

XivelyAbo Data

The M2M/ IoT Application Platform space is evolving quicklyThe role of M2M/ IoT Application PlatformsSource: Machina Research 2013

Machina Research 104

Data communities and Subnets of Things will emerge as stepping stones before IoT

M2M Solutions as standalone devices and/or propositions (e.g. vehicle telematics, machine telemetry, etc.)

M2M Solutions as devices and/or propositions within an enterprise or functional solution (e.g. remote diagnostics and maintenance, access control, traffic light management, event ticketing, etc.)

M2M Solutions as devices and/or propositions deployed within a specific industry area and/or sector (e.g. micro-generation in intelligent buildings, smart cities, etc)

M2M Solutions as integrated data shares in a “data community” (i.e. integrated insofar as data from devices across multiple industry sectors are combined for the purposes of analysis)

Intranets of Things

Internet of Things

Subnets of Things

Data Communities and Subnets of ThingsSource: Machina Research 2013

Agenda

• About Machina Research• What is M2M?• Technology• Management/control• Data analytics• The revenue opportunity

Machina Research 105

Success in M2M depends on success in Big Data – it’s part of the ecosystem

Machina Research 106

• Transmission of basic data via a communication network

• The core of what we know today as M2M

• Typically binary

• Actioned data, e.g. fleet management

• Gamification, e.g. Nike+, Microsoft Hohm, Fiat eco:drive

• ‘Nudge’/carrot & stick

• Contextualised data

• Examples: established norms (e.g. average usage), environmental factors (e.g. speed limits)

• Automated action

• More data processing on the end device

• Platooning, intelligent transport systems

Data Information Knowledge Wisdom

M2M is evolving from point solutions

Machina Research 107

Big Data Analytics comprises 5 elements

• Different types and

structures of data accessed

• Different types and

structures of data accessed

• Context within which data is created and managed

• Context within which data is created and managed

• Rate at which data is

delivered & consumed

• Rate at which data is

delivered & consumed

• Amount of data that requires processing

• Amount of data that requires processing

Size Speed

StructureSituation

Machina Research’s Five S’s of Big DataSource: Machina Research 2013

Significance

• What is Big Data? Isn’t it just awhole load more data to beanalysed?

• No. Big Data is the interplay of allfive factors of size, speed,structure, situation andsignificance where ‘significance’ isderived from data throughanalytics

• What distinguishes Big Data fromtraditional Business Intelligence(BI) analysis is the sheer scale andcomplexity of the data as well asthe highlighted immediacy(speed) of using the data forfurther action and/or decision-making

Machina Research 108

Data significance reaches its peak when processed information saves lives directlyData Significance Factor– signifies the predicted importance of the data (in applications) at the data analytics processing stage

DSF-0Potential significance derived from historical, high

volume data analysis - no immediate value from real-time processing or data integrations

DSF-1Significance in trend analysis scenarios – less importance

on real-time processing and no integration with other data sets

DSF-2Significant in trend analysis scenarios – less importance on real-time processing but with integration with other

data sets

DSF-3Significant in real-time analysis scenarios with potential

life saving impacts or high financial or commercial implications without data integrations

DSF-4Significant in real-time analysis scenarios with high

financial or commercial implications through integrated data set analysis

DSF-5Extremely significant in real-time analysis scenarios with

potential immediate life saving impacts through integrated data set analysis

0

1 - 2

1 - 3

2 - 4

3 - 4

5

0 - 1

1 - 2

1 - 3

2 - 5

2 - 4

4 - 5

Priority ImpactAs related to data processing outcomes

Very high

High

High

Medium

Low

Very low

Predictability

Emergency/eCall in Automotive

Equipment Monitoring in Construction

Coronary Heart Disease Monitoring - Healthcare

Smart meter in Utilities

Remotte diagnostics and maintenance – M&SC

HVAC in Intelligent Buildings

In summary, eight factors continue to accelerate the growth of M2M & Big Data

Improved connectivity

Cheaper data plans Cheaper data storage

Cheaper processingCheaper modules

New data processing technology

Greater adoption of M2M + IoT (device

driven growth of Big Data)

Integration with mobile business

process solutions

M2M Big Data

speed cost volume

2G -> 3G -> LTE

Data and bandwidth rates

Ranging from USD$12 to

USD$31

SFA, FFA, M2M, etc.

Hadoop, NoSQL

incl. cloud based solutions

CEP tech changes costs

Tipping points within industries

Machina Research 110

Size and significance of data will be factors determining service provider focus

Emergency / eCall

Emergency / eCall

Audio Visual displays

Audio Visual displays

Securityin Intelligent Buildings

Securityin Intelligent Buildings

“Sig

nific

ance

” of

the

data

Smart meterSmart meter

Vehicle security &

tracking

Vehicle security &

tracking

Approx. size of bubble indicates relative number of connected devices in 2013

Worried well – remote

monitoring

Worried well – remote

monitoring

low

Warehousing & Storage

Warehousing & Storage

Goods monitoring & payments

Goods monitoring & payments

Worried well – personalmonitoring

Worried well – personalmonitoring

Environmentalmonitoring

Environmentalmonitoring

Equipment monitoring in construction

Equipment monitoring in construction

Environment &

Public Safety (CCTV)

Environment &

Public Safety (CCTV)

TelemedicineTelemedicine

Volume of data (per event)low high

DSF-

0DS

F-5

Machina Research 111

Data communities and Subnets of Things will emerge as stepping stones before IoT

M2M Solutions as standalone devices and/or propositions (e.g. vehicle telematics, machine telemetry, etc.)

M2M Solutions as devices and/or propositions within an enterprise or functional solution (e.g. remote diagnostics and maintenance, access control, traffic light management, event ticketing, etc.)

M2M Solutions as devices and/or propositions deployed within a specific industry area and/or sector (e.g. micro-generation in intelligent buildings, smart cities, etc)

M2M Solutions as integrated data shares in a “data community” (i.e. integrated insofar as data from devices across multiple industry sectors are combined for the purposes of analysis)

Intranets of Things

Internet of Things

Subnets of Things

Data Communities and Subnets of ThingsSource: Machina Research 2013

Agenda

• About Machina Research• What is M2M?• Technology• Management/control• Data analytics• The revenue opportunity

Machina Research 112

Revenue forecast metrics

Machina Research 113Definitions are provided in the Supporting Material section below

By 2022, M2M will be a USD 1.2 trillion opportunity

• Total M2M revenue will grow from USD200 billion in 2011 to USD1.2 trillion in 2022, a CAGR of 18%

• Total revenue includes:o device costs where

connectivity is integral to the device

o module costs where devices can optionally have connectivity enabled

o monthly subscription, connectivity and traffic fees

Machina Research 114

Total revenue from machine-to-machine, 2011-22Source: Machina Research 2012

Device and service revenues will comprise the vast majority of the M2M market

Machina Research 115

Composition of Total M2M Revenues, 2022Source: Machina Research 2012

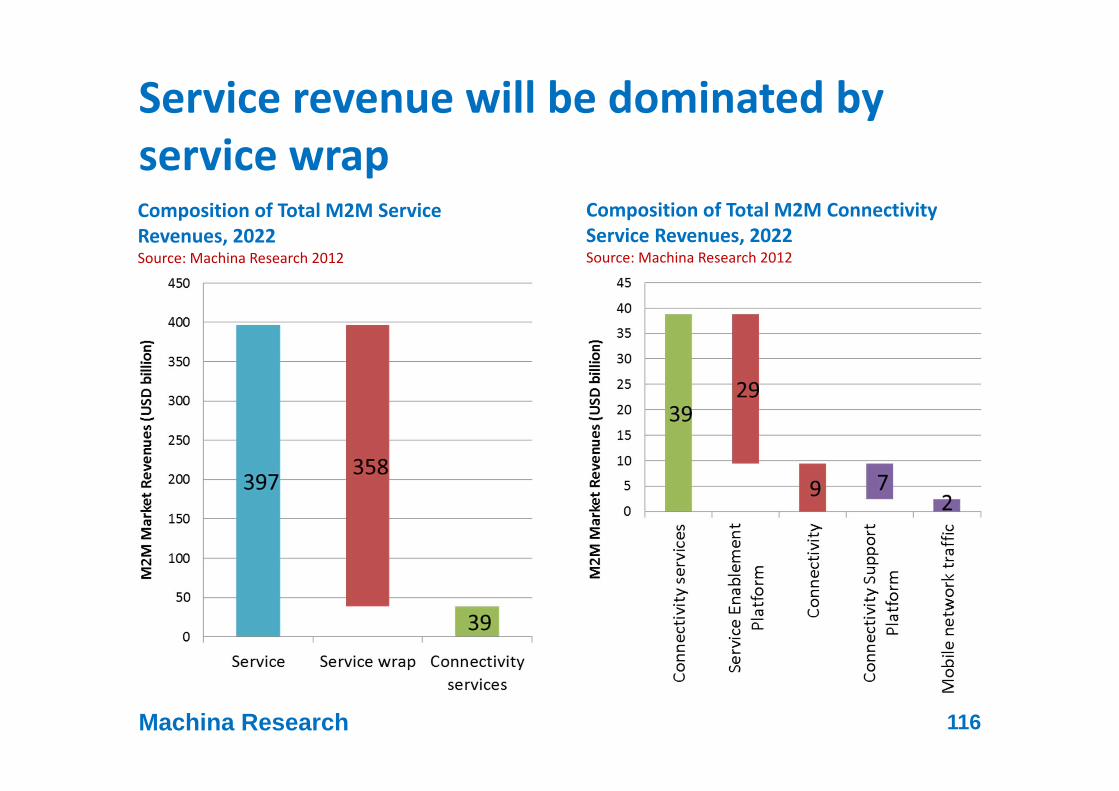

Service revenue will be dominated by service wrap

Machina Research 116

Composition of Total M2M Service Revenues, 2022Source: Machina Research 2012

Composition of Total M2M Connectivity Service Revenues, 2022Source: Machina Research 2012

Simple device count is not representative of sector revenue opportunities

Machina Research 117

Connected devices, cellular connections and revenue by sector, 2022Source: Machina Research 2012

Disruption persists throughout the M2M market

Machina Research 118

• Falling price points

• Competition• Fit-for-M2M• On-device

processing• Licensing fees• Embedded SIM

• More products/ verticalisation

• Global alliances• eUICC/IMSI

swapping• Partnerships• More focus

from CSPs

• Technology rationalisation

• New arrivals • Technology

agnosticism• Standardisation• Pressure to

minimise costs

• Evangelisation of new biz models

• Channels• Privacy &

security• “Big data”

analytics

Modules/ devices Networks Service

providersCustomer/ end

user

Contact me

Matt HattonDirector

[email protected]: +44 7787 577886

Skype: mattyhattonTwitter: @MattyHatton

Machina Research 119

Machina Research

120

Supporting Material

About Machina Research

• The leading research/consulting firm focusing on the emerging opportunity for new connected devices and applications, i.e. M2M

• Supporting our clients througho Machina Research Advisory Service – our multi-client annual subscription

service comprising forecasts, reports and access to the analysts (see below)o Custom Research & Consulting –client-specific research

• We have the most focused research on the M2M field of any analyst firm in the world: we provide the most granular forecasts for the global M2M opportunity, supported by the most robust analysis of market issues and dynamics

• Other coverage areas include NFC, the internet of things and ‘Big Data’ analytics

• The company was founded in 2011 by Matt Hatton and Jim Morrish, two experienced industry analysts and the team has grown substantially since then

Machina Research 121

Some of our clients

Machina Research 122

About Machina Research

Market/demand side Provider/supply side

• Quantifying the opportunity for M2M – Forecast Database providing 10

year forecasts across 201 countries for 61 application groups

– Sector Reports annually updated reports on our 13 sectors (including Automotive, Healthcare and Utilities)

• Addressing the issues that determine success– Research Notes - 3 per month on

major qualitative issues such as platforms, value chain roles, big data, NFC, and security

– Strategy Reports - covering areas such as Big Data, platforms, modules/devices, CSP best practice, etc.

Advisory Service and Custom Research

Machina Research 123

The Advisory Service consists of six elements• The Forecast Database

o The Forecast Database underpins much of the work that we do. It provides comprehensive forecasts of the M2M and mobile broadband market across each of thirteen connectivity sectors, covering 61 application groups in around 200 countries. The forecast covers numbers of connections, traffic and revenue for each of the application groups with splits by technology (2G, 3G, 4G, short range, MAN, fixed WAN and satellite) and a comprehensive breakdown of the revenue opportunity.

• Strategy Reportso 6 Strategy Reports per year. These focus on key strategic issues such as software platforms, Big Data analytics, and device/module

pricing. It also includes our regular Communications Service Provider Benchmarking report. All of the Strategy Reports are accessible through the Research section of this website. Strategy Reports are typically 40-60 pages.

• Sector Reportso 13 Sector Reports per year. Each Sector Report reviews the major drivers and barriers for growth of M2M in a particular vertical

sector (e.g. healthcare, utilities etc) and analyses the key market dynamics, including how MNOs, fixed operators, service providers and vendors might go about identifying and realising addressable opportunities. Each application group is examined individually with case studies and forecast analysis. The associated forecast excel data sheet includes very granular 10 year market forecasts mirroring those in the Forecast Database. Typically Sector Reports are 50-100 pages in length.

• Research Noteso 36 Research Notes per year. These are shorter reports that focus on a specific issue, company or application and examine it in greater

detail. Also, the short-form report can be used to comment on important events as they occur, allowing our analysts to react quickly to a new development and quickly inform our clients of the implications. Research notes are typically 5-6 pages in length.

• Strategy Briefingso An opportunity for direct face-to-face interaction between the client and the Machina Research analysts. Typically a Strategy Briefing

will involve a presentation at the client’s premises on a theme agreed with the client within (or closely related to) the scope of existing research.

• Client Enquiryo Clients also get direct access to our analysts in the form of enquiries about the published materials and associated topics within M2M.

Machina Research 124

The Machina Research Forecast Database

Machina Research 125

• We recognise that M2M is a very diverse market that requires a granular approach

• We have developed detailed M2M forecasts based on our thirteen focus sectors (see left)

• Within each sector there are very different dynamics for each application, so we forecast each of 61 application groups and hundreds of applications separately

Example sector: healthcare

Machina Research 126

Example application: Comprehensive assisted living solutions

Machina Research 127

HouseholdHub

device

Blood pressure monitor

Scales Pulse oximeter

• Machina Research distinguishes between devices and revenue generating units (RGUs)

• There may be multiple RGUs per connections (e.g. applications such as navigation or usage-based insurance running on a car platform)

• Or there may be multiple devices per RGU, as in the example here:o 1 RGUo 4 deviceso 3 short-range connectionso 1 Wide area connection …

• In some cases the hub unit is counted in another category, e.g. a fixed broadband CPE

• Secondary/ backup connections are not counted

The result: an incredibly detailed database of global M2M forecasts used by global clients

• For each application group we forecast:o Connections

• Split by tech (2G, 3G, 4G, short range, MAN, FWAN and satellite)

o Traffic• Split by tech (WWAN, short range,

MAN, FWAN and satellite)o Revenue

• Split by total, MNO addressable, MNO expected and mobile network traffic revenue

• Split by value chain components (see below)

Ten year forecasts (2012-22) including millions of data points

• 201 countries, 6 regions

Machina Research 128

Revenue forecast metrics

Machina Research 129Definitions are provided in the Supporting Material section below

Machina Research 130

All available on our website

We cover the qualitative aspects of the market through three deliverable types• Strategy Reports

o 6 Strategy Reports per year.o These focus on key strategic issues. In 2013 our Strategy Reports looked at the following topics:

• Software platforms• Big Data analytics• Device/module pricing. • M2M Communications Service Provider Benchmarking

o All of the Strategy Reports are accessible through the Research section of this website. Strategy Reports are typically 40-60 pages.

• Research Noteso 36 Research Notes per year. o These are shorter reports that focus on a specific issue, company or application and examine it in greater detail.

Also, the short-form report can be used to comment on important events as they occur, allowing our analysts to react quickly to a new development and quickly inform our clients of the implications.

o Research notes are typically 5-6 pages in length.• Sector Reports

o 13 Sector Reports per year. o Each Sector Report reviews the major drivers and barriers for growth of M2M in a particular vertical sector (e.g.

healthcare, utilities etc) and analyses the key market dynamics, including how MNOs, fixed operators, service providers and vendors might go about identifying and realising addressable opportunities. Each application group is examined individually with case studies and forecast analysis.

o The associated forecast excel data sheet includes very granular 10 year market forecasts mirroring those in the Forecast Database.

o Typically Sector Reports are 50-100 pages in length.

Machina Research 131

Strategy Reports 2013

• Dec-13 (due) Strategy Report - M2M/IoT platforms o This Strategy Report will examine the evolving landscape for M2M/IoT software platforms. It will examine the changing dynamics as

we evolve from platforms supporting stovepipe vertical applications, to the M2M/IoT application enablement platform. • Dec-13 Strategy Report – M2M devices and modules

o This Strategy Report will focus on the hardware side of M2M solutions, in particular cellular devices. This will include analysis of module/device pricing, and implications of the evolution from 2G to 3G and ultimately LTE. It will also include a forecast for global M2M module shipments by technology.

• Sep-13 Strategy Report - Creating value from data analytics in M2M: the Big Data opportunityo This extensive Strategy Report examines the topic of Big Data and its impact on machine-to-machine (M2M) communications. It is

based on detailed and exhaustive discussions with key relevant stakeholders, supplemented by Machina Research’s extensive understanding of the changing dynamics of the industry.

o The report starts by examining what we mean by the term ‘Big Data’, identifying the right ways to define and measure it, including a look at our own measure of ‘Data Significance Factor’. It then goes on to look at the impact that Big Data will have on M2M, and vice versa, in terms of creating new data sources and justifying new investments in sensor networks. The final two sections focus on the future, looking at the challenges faced in Big Data and how these can be overcome, as well as how Big Data, M2M and the Internet of Things will evolve and merge.

o The report provides invaluable analysis for enterprises seeking to gain an improved understanding and awareness of Big Data, andservice providers looking to identify opportunity areas to develop and improve data processing services for their customers (e.g. IT infrastructure improvements and cloud services).

• Apr-2013 Strategy Report – M2M CSP Benchmarking Reporto Provides Machina Research’s view on the likely long-term success of Communication Service Providers in the M2M market.o In last year’s report Machina Research focused on seven CSPs: AT&T, Deutsche Telekom, Orange, Telefónica, Telenor, Verizon and

Vodafone. This year we include profiles of two additional CSPs that demonstrate some different approaches to addressing the M2M opportunity, specifically Telekom Austria Group M2M and Telia Sonera.

o We analysed the CSPs on six criteria: Pedigree, Platforms, Place, Partnerships, Process, and People. The report includes a 3-6 page profile of each CSP, examining their capabilities in each of the six areas.

Machina Research 132

Research Notes provide invaluable understanding of the market

Date TitleSep-13 M2M Leaderboard: Vodafone extends its lead, AT&T and Deutsche Telekom continue their battle for second placeSep-13 AT&T focuses on M2M/IoT to expand its innovation Foundry initiativeSep-13 Vodafone sells Verizon Wireless stake and maybe opens door for AT&T tie-up: the implications for M2MSep-13 Overcoming the permanent roaming challenge for M2M: Vodafone deal with Datora shows one solution, while AT&T keeps its options openSep-13 In active M2M industry M&A season, US-based solution provider RACO Wireless provides global expansion strategy template with acquisition of Position Logic

Sep-13 Use of remote provisioning in M2M will focus on late binding of long life-span high bandwidth applicationsSep-13 Regulatory compliance and client demand drive MNOs to embrace IMSI swapping/remote provisioning in M2MAug-13 Watch out, here comes the new M2M Apps storeJun-13 On-Ramp, Sigfox and Weightless: a strategic comparison of competing approaches to M2MJun-13 Low Power Wide Area Wireless networks: a potential global market of 15.5 billion M2M connectionsJun-13 Low Power Wide Area Wireless network technologies for M2M: a technical comparison of On-Ramp, Sigfox and WeightlessJun-13 Confronting prospects of waning growth, Axeda adds partners and new capital injection to gain global scale and expand functionalityMay-13 M2M Leaderboard: AT&T snatches second spot from DT as top 4 all grow their expected global market shareMay-13 Addressing diverse M2M opportunities requires a different approach to channelsMay-13 Is there a need for data partners in the M2M ecosystem?Apr-13 Integrating M2M and mobile enterprise applications resources has distinct opportunities and advantagesApr-12 Satellite operators look to build vertical expertise to capitalise on the M2M opportunityApr-12 M2M & Big Data – how to monetise data in the Automotive sectorMar-13 Near field communications could significantly enhance most M2M solutionsMar-13 Smart Home market is ripe for turnkey solutions, although channels remain unclearMar-13 Upgradeable licensing fees for 3G/LTE would remove a lot of friction in M2MMar-13 Global M2M statistics: what does the data tell us? Mar-13 Momentum is building behind usage-based insuranceFeb-13 Not all devices are equally suited to M2M connectivityFeb-13 How MNOs can grow M2M revenue

Machina Research 133

Research Notes published in February-September 2013

All content is accessible via our website

Machina Research 134

135© 2013 J. Alonso-Zarate

Conclusions

136© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Conclusions

The IoT is around the corner.There is a huge market opportunityMany challenges ahead:

Technology is (almost) here, but must be optimized.• Zero-Power operation • Dense deployments• Long distances• Simplicity

New Business Models are needed.Politicians must push for it (smart cities)Humans in the loop

137© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

IoT World Forum, October 2013 The IoT is nascent, and its value needs to be defined 90% of the business is comprised of start-ups

No single company will build the IoT Major companies will need to find ways to engage with and enable

these builders.

Industrial internet + consumers-facing opportunities. Consumers will be a source of innovation in the IoT.

Arduino, Raspberry Pi, Thingsquare, Libelium’s Cooking Hacks , Smart Citizen Kit, TheThings.io, Electric Imp to Telefonica’s recently announced Thinking Things, and Intel’s Galileo, among others.

The IoT will not rest on one killer app, but on openness and interoperability

Source: http://www.claropartners.com/the-emerging-iot-business-landscape-insights-from-the-iot-world-forum-2/

138© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

Final Take-Away Message

Henry Ford

“If I had asked people what they wanted, they would have said…

A FASTER HORSE!”

139© 2013 M. Dohler, M. Hatton, J. Alonso-Zarate

THANKS

Mischa Dohler, King’s College London, [email protected] (@mischadohler )Matt Hatton, Machina Research, [email protected] (@MattyHatton)Jesus Alonso-Zarate, CTTC, [email protected] (@jalonsozarate)