macroeconomic and industry analysis chapter 12 copyright © 2010 by the mcgraw-hill companies, inc....

TRANSCRIPT

Macroeconomic and Industry

Analysis

Chapter 12

Copyright © 2010 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

12-2

Framework of Analysis

• Fundamental Analysis– Analysis of the determinants of firm value,

specifically attempting to forecast the earnings and dividends of a firm.

– Top down approach: Analyze economy

Analyze industryAnalyze firm

12-3

Framework of Analysis• Approach to Fundamental Analysis

– Industry analysis• Critical to understand the competitiveness of

the industry

– Company analysis• Detailed strategic and financial analysis of the

firm

• Why use the top-down approach?

12-4

The Business Cycle• Recurring patterns of recession and recovery

– Peak

– Trough

• Industry relationship to business cycles– Cyclical industries

• Industries with above average sensitivity to the state of the economy

– Defensive• Industries with below average sensitivity to the state

of the economy

12-5

Industry Analysis• Performance can vary widely across

industries– It is difficult to find a good stock in a poor

industry

12-6

Figure 12.8 Industry Stock Price Performance, 2008

12-7

Defining an Industry• It can be difficult to define an industry

– North American Industry Classification System (NAICS) attempts to define industry groups with a four or five digit code:

• The first two digits broadly define the industry group: NAIC code 23 = construction

• The last two or three digits define the industry more narrowly

12-8

Sensitivity to Business Cycle

• Factors affecting sensitivity of earnings to business cycles– Sensitivity of sales of the firm’s product to the

business cycles

– Fixed costs and leverage• Fixed costs are costs that do not vary with the level

of production.

• Fixed costs contribute to higher profitability when sales are high, but will result in lower profitability when sales are lower.

12-9

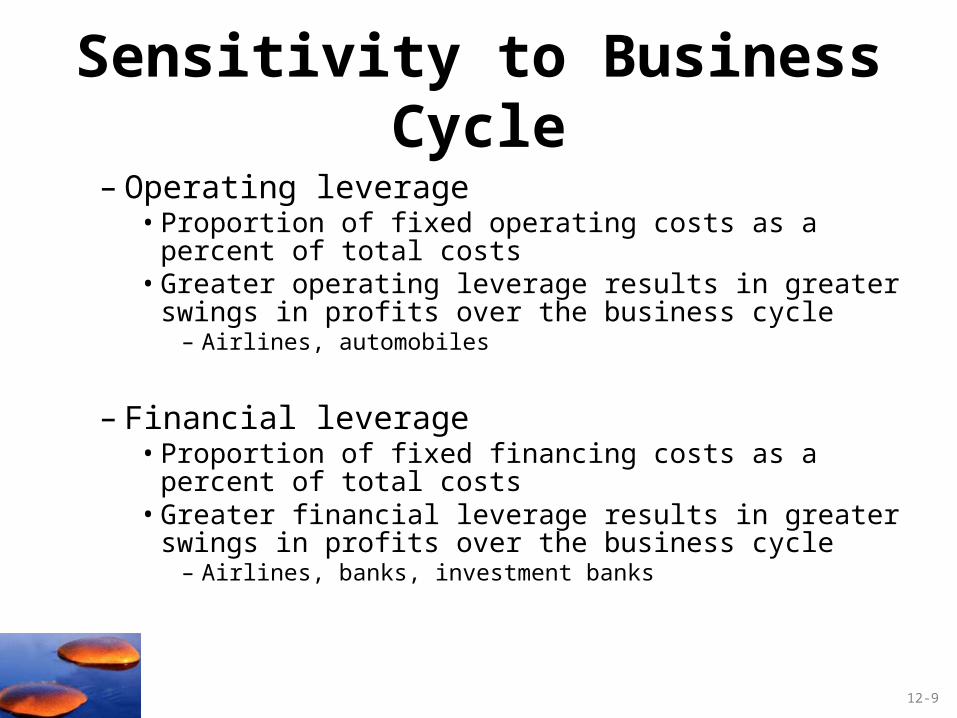

Sensitivity to Business Cycle

– Operating leverage• Proportion of fixed operating costs as a percent of

total costs• Greater operating leverage results in greater

swings in profits over the business cycle– Airlines, automobiles

– Financial leverage• Proportion of fixed financing costs as a percent of

total costs• Greater financial leverage results in greater swings

in profits over the business cycle– Airlines, banks, investment banks

12-10

Figure 12.11 A Stylized Depiction

of the Business Cycle

12-11

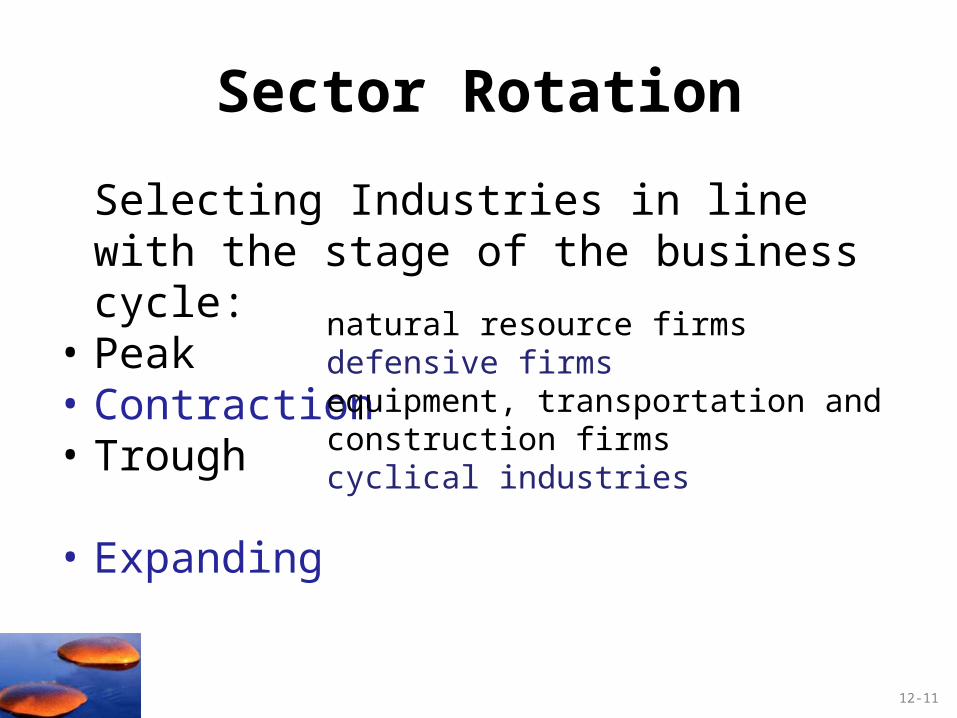

Sector Rotation

Selecting Industries in line with the stage of the business cycle:

• Peak • Contraction• Trough • Expanding

natural resource firmsdefensive firmsequipment, transportation and construction firmscyclical industries

12-12

Figure 12.12 Sector Rotation Illustrated

12-13

Industry Life CyclesStage Sales Growth

Start-up

Consolidation

Maturity

Relative Decline

Rapid & Increasing

Stable

Slowing

Minimal or Negative

12-14

Figure 12.13 The Industry Life Cycle

12-15

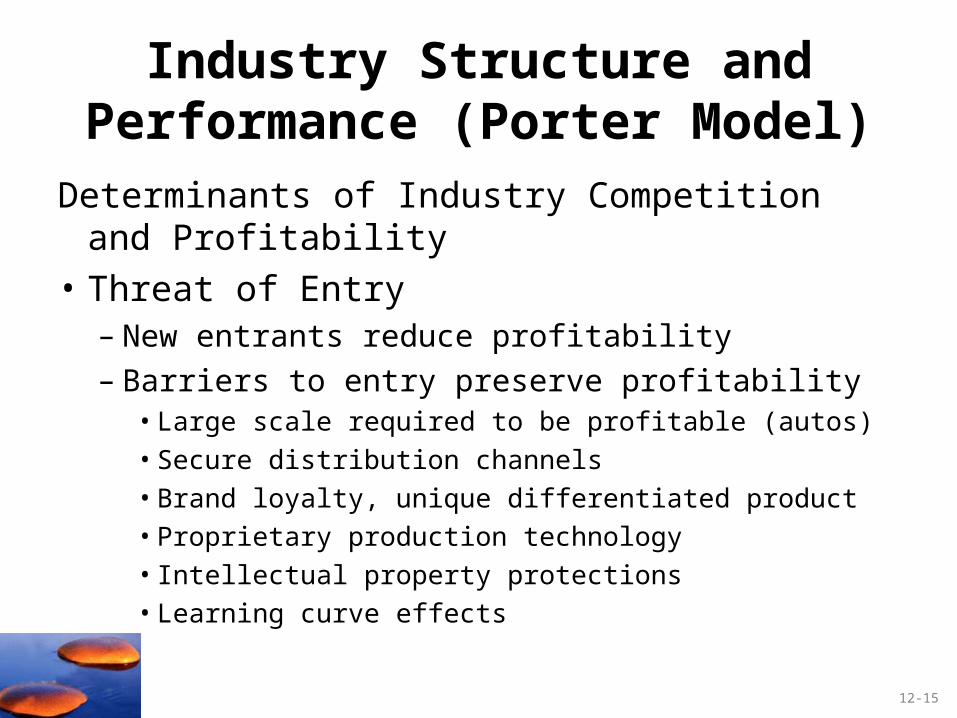

Industry Structure and Performance (Porter Model)

Determinants of Industry Competition and Profitability

• Threat of Entry– New entrants reduce profitability– Barriers to entry preserve profitability

• Large scale required to be profitable (autos)

• Secure distribution channels

• Brand loyalty, unique differentiated product

• Proprietary production technology

• Intellectual property protections

• Learning curve effects

12-16

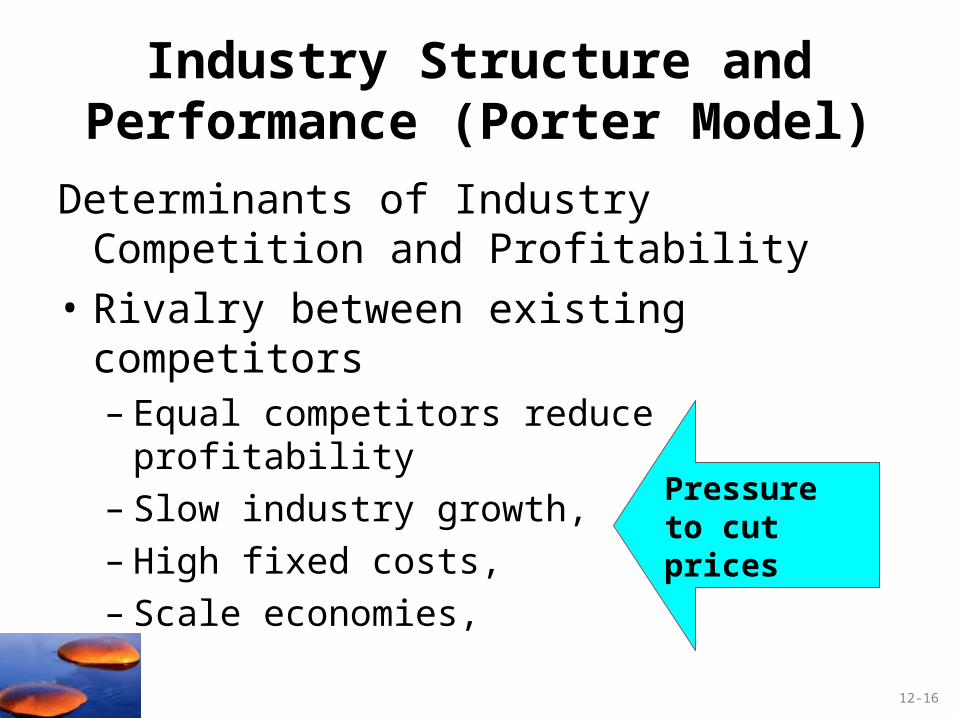

Industry Structure and Performance (Porter Model)

Determinants of Industry Competition and Profitability

• Rivalry between existing competitors– Equal competitors reduce profitability– Slow industry growth,– High fixed costs, – Scale economies,

Pressure to cut prices

12-17

Industry Structure and Performance (Porter Model)

Determinants of Industry Competition and Profitability• Pressure from substitute products

– Substitutes limit profitability (propane, natural gas)• Bargaining power of buyers

– A buyer that purchases a large percent of an industry’s output can limit the selling industry’s profitability (auto parts suppliers)

• Bargaining power of suppliers– A supplier that controls a key input can limit the

buying industry’s profitability (labor unions)