macroeconomics chapter 13 - edward mcphailedwardmcphail.com/.../chapter13.pdf · 4 roles of money a...

TRANSCRIPT

MacroeconomicsCHAPTER 13

Money, Banking, and

the Federal Reserve System

2

What you will learn in this chapter:

The various roles money plays and the many forms it takes inthe economy.

How the actions of private banks and the Federal Reservedetermine the money supply.

How the Federal Reserve uses open-market operations tochange the monetary base.

3

The Meaning of Money

Money is any asset that can easily be used to purchase goodsand services.

Currency in circulation is cash held by the public.

Checkable bank deposits are bank accounts on which peoplecan write checks.

The money supply is the total value of financial assets in theeconomy that are considered money.

4

Roles of Money

A medium of exchange is an asset that individuals acquire forthe purpose of trading rather than for their own consumption.

A store of value is a means of holding purchasing power overtime.

A unit of account is a measure used to set prices and makeeconomic calculations.

5

Types of Money

Commodity money is a good used as a medium of exchangethat has other uses.

A commodity-backed money is a medium of exchange withno intrinsic value whose ultimate value is guaranteed by apromise that it can be converted into valuable goods.

Fiat money is a medium of exchange whose value derivesentirely from its official status as a means of payment.

5a

Money and Banking

Money

1. Why do we have money? There are three basic functions that money serves

a) Medium of exchange• allows for the specialization of workers. They receive money wages to buy

goods needed rather than produce their own goods.• avoids the problem of the double coincidence of wants. In a society with barter

you must find someone who has what you desire and wants what you haveproduced.

b) Accounting Unit: allows valuation and pricing in a common unit

c) store of value: in barter, need to store goods which could perish or lose value. e.g.light blue leisure suit with polyester floral print shirt. With money one can store value overtime.

Advantages of moneyhighly liquid as compared to stocks and bonds.

Disadvantages of moneyLoses value during inflationary periods or episodes.

Different Types of Money

a) Commodity Money has value as a commodity such as rice, cattle, seashells, copper,stones, cigarettes as used in the POW camps of WWII.

problems• when valuable resources are used as money, those resources cannot be used for

consumption. Copper used to make pennies cannot be used to make electricalwire.

• There exists an incentive to debase the currency. Rulers would reduce theamount of the precious metal in a coin. People would tend to circulate thealtered coins and save the coins which still had the greater amount of theprecious metal. This is known as Gresham’s law: bad money drives out good.

• The supply of money is determined by supply of the commodity. The moneysupply could fluctuate substantially. The discovery of new gold would meanthat the supply of money would increase and the price level would rise.

b) Fiat Money (has nothing to do with an Italian sports car) very little value as acommodity money because the public accepts it as money (not necessarily because thegovernment declares it as money) Peopel accept it because they believe that everyone elsewill accept it. This is very different from a “fully backed” currency that is a currency that isbacked by some commodity like gold or silver. For example in the early part of thiscentury the US still had silver dollar notes. If one wanted one could take the note to thetreasury and demand the silver which was held since the inception of the note as a form ofits backing.

5b

advantages of fiat money• uses relatively little of society’s resources• no incentive to debase this type of currency• supply not tied to commodity. Therefore it potentially has less susceptibility to

lead to fluctuation in the money supply. It can grow with the economy.•

problem • government controls money supply and it may cause inflation by printing too

much money

Bank Money: checks backed by a bank account.

in the US we have Fiat and Bank Money

6

Measuring the Money Supply

A monetary aggregate is an overall measure of the moneysupply.

Near-moneys are financial assets that can’t be directly used asa medium of exchange but can readily be converted into cash orcheckable bank deposits.

7

Monetary Aggregates

The Federal Reserve uses three definitions of the money supply:M1, M2, and M3.

M1 = $1,368.4 (billions of dollars), June 2005

M1 is equally split betweencurrency in circulation andcheckable bank deposits.

8

Monetary Aggregates

The Federal Reserve uses three definitions of the money supply:M1, M2, and M3.

M2 = $6,510.0 (billions of dollars), June 2005

M2 has a much broaderdefinition: it includes M1,plus a range of otherdeposits and deposit-likeassets, making it about threetimes as large.

8a

Money Supply Definitions

Most liquid M1 = currency held by the public (not including the banks) + demand deposits (non-interest checking accounts) + other checkable deposits (interest bearing checking)+traveller’s checks

Less liquid M2 = M1+ savings deposits+ money market mutual fund share, deposits+ small time deposits (<$100,000)+ other

Least liquid M3 = M2+ large time deposits (>$100,000)

We usually refer to M1 as the money supply.

Credit cards are not money-they are short-term loans which must be paid off using money.

9

The Monetary Role of Banks

A bank is a financial intermediary that uses liquid assets inthe form of bank deposits to finance the illiquid investments ofborrowers.

Bank reserves are the currency banks hold in their vaults plustheir deposits at the Federal Reserve.

The reserve ratio is the fraction of bank deposits that a bankholds as reserves.

10

Assets and Liabilities of First Street Bank

A T-account summarizes a bank’s financial position. The bank’sassets, $900,000 in outstanding loans to borrowers and reservesof $100,000, are entered on the left side. Its liabilities, $1,000,000in bank deposits held for depositors, are entered on the right side.

11

The Problem of Bank Runs

A bank run is a phenomenon in which many of a bank’sdepositors try to withdraw their funds due to fears of a bankfailure.

Historically, they have often proved contagious, with a run onone bank leading to a loss of faith in other banks, causingadditional bank runs.

12

Bank Regulations

Deposit Insurance - guarantees that a bank’s depositors willbe paid even if the bank can’t come up with the funds, up to amaximum amount per account. The FDIC currently guaranteesthe first $100,000 of each account.

13

Bank Regulations

Capital Requirements - regulators require that the owners ofbanks hold substantially more assets than the value of bankdeposits. In practice, banks’ capital is equal to 7% or more oftheir assets.

14

Bank Regulations

Reserve Requirements - rules set by the Federal Reservethat determine the minimum reserve ratio for a bank. Forexample, in the United States, the minimum reserve ratio forcheckable bank deposits is 10%.

15

Determining the Money SupplyEffect on the Money Supply of a Deposit at First StreetBank - Initial Effect Before Bank Makes New Loans

16

Determining the Money SupplyEffect on the Money Supply of a Deposit at First StreetBank - Effect After Bank Makes New Loans

17

How Banks Create Money

18

Reserves, Bank Deposits, and the MoneyMultiplierExcess reserves are bank reserves over and above its requiredreserves.

Increase in bank deposits from $1,000 in excess reserves =

$1,000 + $1,000 × (1 − rr) + $1,000 × (1 − rr)2 + $1,000× (1 − rr)3 + . . .

this can be simplified to: Increase in bank deposits from $1,000in excess reserves = $1,000/rr

19

The Money Multiplier in RealityThe monetary base is the sum of currency in circulation andbank reserves.

The money multiplier is the ratio of the money supply to themonetary base.

20

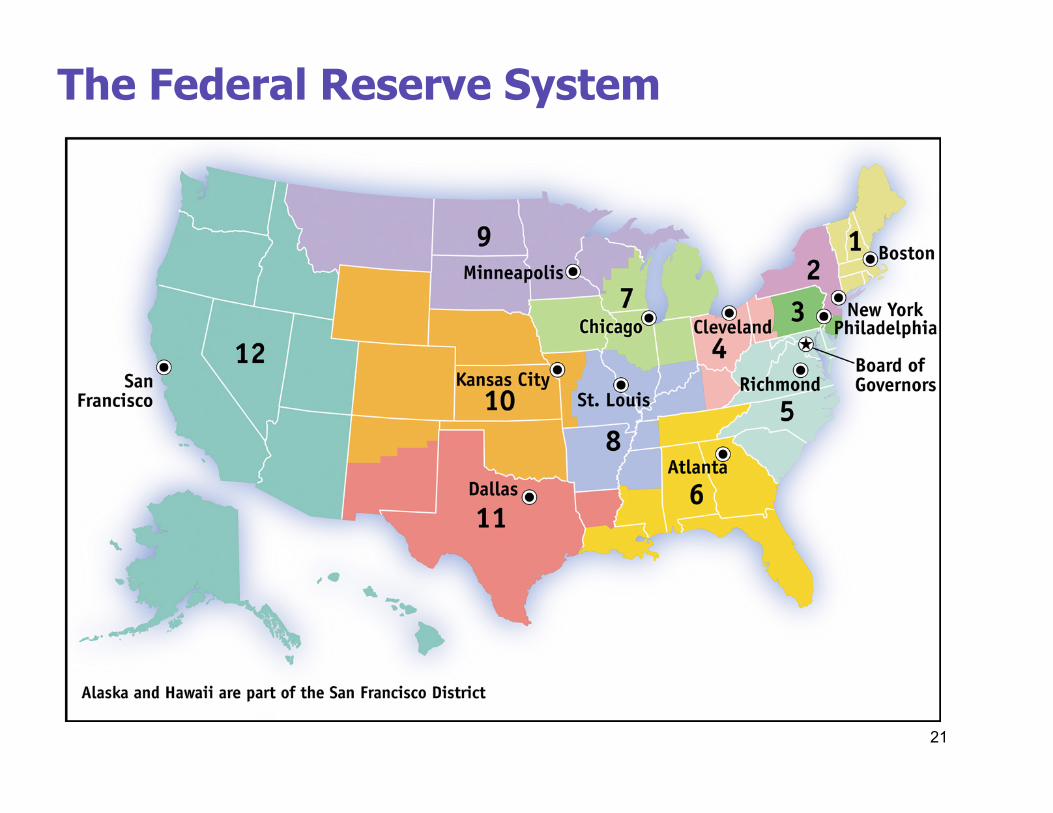

The Federal Reserve SystemA central bank is an institution that oversees and regulates thebanking system and controls the monetary base.

The Federal Reserve is a central bank—an institution thatoversees and regulates the banking system, and controls themonetary base.

The Federal Reserve system consists of the Board of Governorsin Washington, D.C., plus regional Federal Reserve Banks, eachserving its district; of the 12 Federal Reserve districts:

21

The Federal Reserve System

22

What the Fed Does: Reserve Requirements andthe Discount Rate

The federal funds market allows banks that fall short of thereserve requirement to borrow funds from banks with excessreserves.

The federal funds rate is the interest rate determined in thefederal funds market.

The discount rate is the rate of interest the Fed charges onloans to banks.

23

Open-Market OperationsOpen-market operations by the Fed are the principal tool ofmonetary policy: the Fed can increase or reduce the monetarybase by buying government debt from banks or sellinggovernment debt to banks.

The Federal Reserve’s Assets and Liabilities:

24

Open-Market Operations by the Federal Reserve

An Open-Market Purchase of $100 Million

25

Open-Market Operations by the Federal Reserve

An Open-Market Sale of $100 Million

26

The End of Chapter 13

coming attraction:Chapter 14:

Monetary Policy