macroeconomics (econ 1211) lecturer: mr s. puran topic: central banking and the monetary system

Post on 19-Dec-2015

219 views

TRANSCRIPT

Macroeconomics (ECON 1211)Lecturer: Mr S. Puran

Topic: Central Banking and the Monetary System

24.2

1. The Central Bank acts as banker to the commercial banks in

a country and is responsible for setting interest

rates. In the UK, the Bank of England fulfils

these roles. Two key tasks:

– to issue coins and bank-notes– to act as banker to the banking system and

the government.

24.3

1. The Central Bank There are two more objectives of the

Bank: To stabilise the level of economic

activity and the availability of credit (bank rate, discount rate, reserve requirement)

To regulate the banking system, to ensure its financial health

24.4

2. The Bank and The money Supply

Three ways in which the central bank MAY influence money supply:

Reserve Requirements – central bank sets a minimum ratio of cash

reserves to deposits that commercial banks must meet

– Higher Reserve Ratio, the lower the amount of loans that can be created

– A reduction (rise) in reserve ratio creates an increase (decrease) in money supply

24.5

2. The Bank and The money Supply Discount rate

– The interest rate that the central bank charges when the commercial banks want to borrow by the banks tend to be high, less loans are available.

– The banks pass the high interest rate to consumers

– When discount rate is high, interest charged – Setting this at a penalty rate may encourage

commercial banks to hold more excess reserves

– Decrease (increase) discount rate implies (increase) decrease in money supply

24.6

2. The Bank and The money Supply

Open Market Operations – actions to alter the monetary base by buying

or selling financial securities in the open market

– It is a tool that the Bank use to affect the supply reserves

– Buying of bonds: fewer bonds in private hands the monetary base is higher, money supply

increases – Selling of bonds implies a fall in monetary

base, thus money supply decreases

24.7

3. The Repo Market

A gilt repo is a sale and repurchase agreement– e.g. a bank sells you a gilt with a simultaneous

agreement to buy it back at a specified price at a specified future date.

– this uses the outstanding stock of long-term assets (gilts) as backing for new short-term loans

Used by the Bank of England in carrying out open market operations

24.8

4. Other functions of the Bank of England

Lender of last resort– the Bank stands ready to lend to banks and

other financial institutions when financial panic threatens

Banker to the government– the Bank ensures that the government can meet

its payments when running a budget deficit Setting monetary policy to control inflation

– more of this later

24.9

5. The Demand for money

The opportunity cost of holding

money is the interest given up by

holding money rather than bonds.

People will only hold money if there

is a benefit to offset that opportunity

cost.

24.10

6. Motives for Holding Money

Transactions– payments and receipts are not perfectly

synchronized: so money is held to finance known transactions

depends upon income and payment arrangements

Precautionary– because of uncertainty:

people hold money to meet unforeseen contingencies

depends upon the (nominal) interest rate

24.11

6. Motives for Holding Money (2) Asset

– people dislike risk– so may hold money as a low-risk component

of a mixed portfolio depends upon opportunity cost (the nominal interest

rate)

Speculative– people may hold money rather than bonds– if bond prices are expected to fall– i.e. the interest rate is expected to rise

depends upon the rate of interest and on expectations about bond prices

24.12

7. The Demand for Money: summary

The demand for money is a demand for real money balances

It depends upon:– real income– nominal interest rate (the opportunity

cost of holding money)– the price level (currently assumed fixed)– expectations about future interest rates

24.13

7. More on the Speculative Motive

When interest rate falls, the cost of holding money falls.

This fall leads to more money being held both for precautionary motive (to reduce risks caused by uncertainty) and for the speculative motive (to reduce risks associated with fluctuations in the market price of bonds)

Thus, demand for money is negatively related with interest rate

24.14

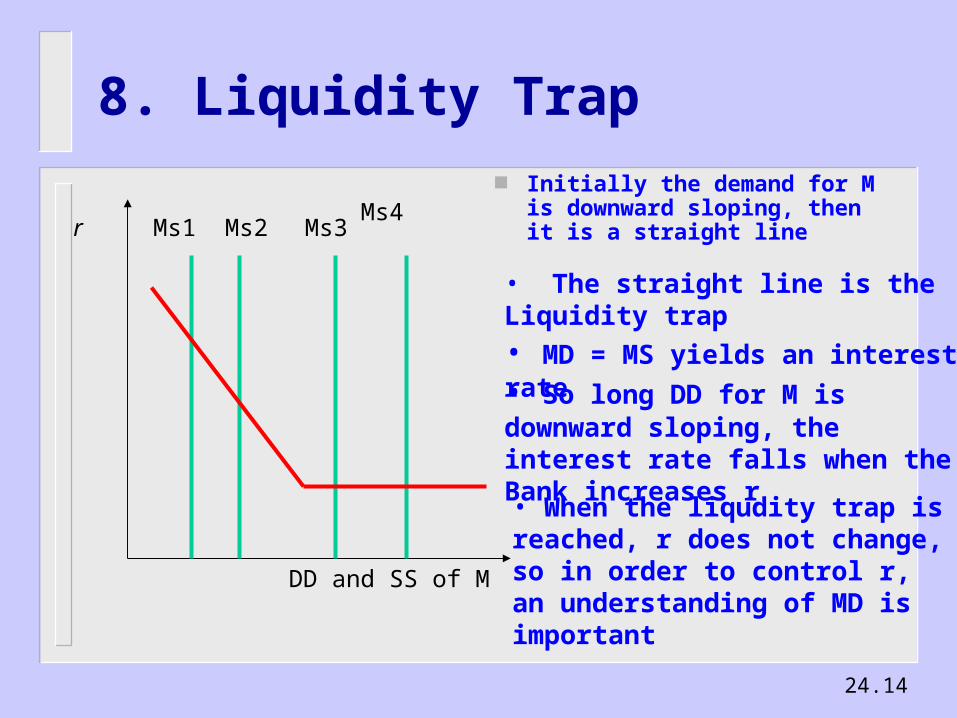

8. Liquidity Trap

Initially the demand for M is downward sloping, then it is a straight line

Ms4Ms1 Ms2 Ms3r

DD and SS of M

• The straight line is the Liquidity trap• MD = MS yields an interest rate

• So long DD for M is downward sloping, the interest rate falls when the Bank increases r

• When the liqudity trap is reached, r does not change, so in order to control r, an understanding of MD is important

24.15

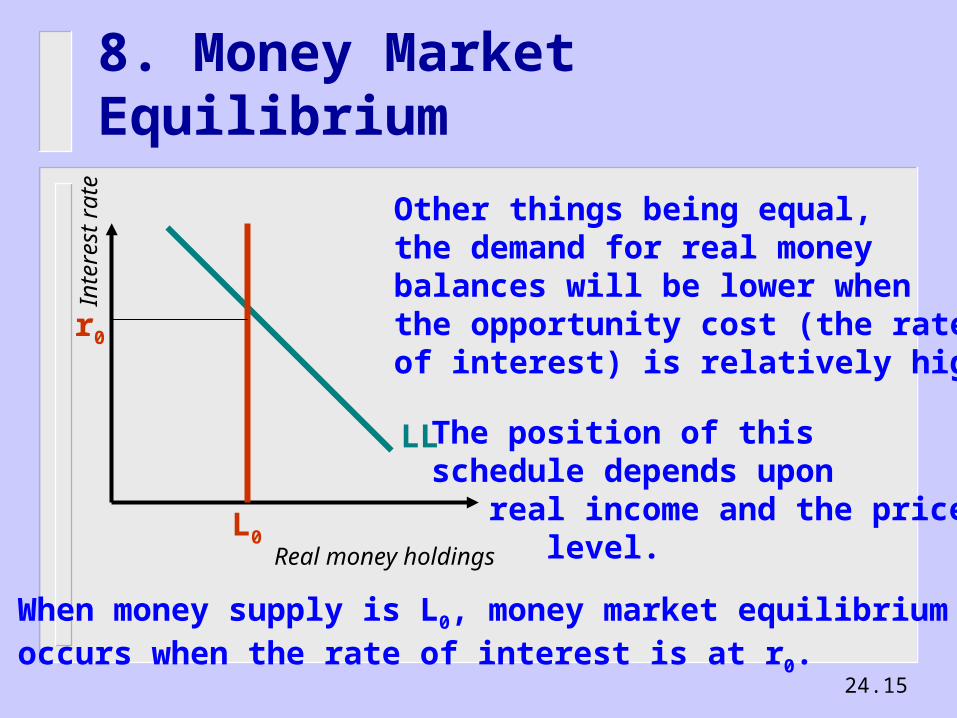

8. Money Market Equilibrium

Real money holdings

Inte

rest

ra t

e

LL

Other things being equal,the demand for real money balances will be lower whenthe opportunity cost (the rateof interest) is relatively high.

The position of this schedule depends upon real income and the price level.

When money supply is L0, money market equilibrium occurs when the rate of interest is at r0.

L0

r0

24.16

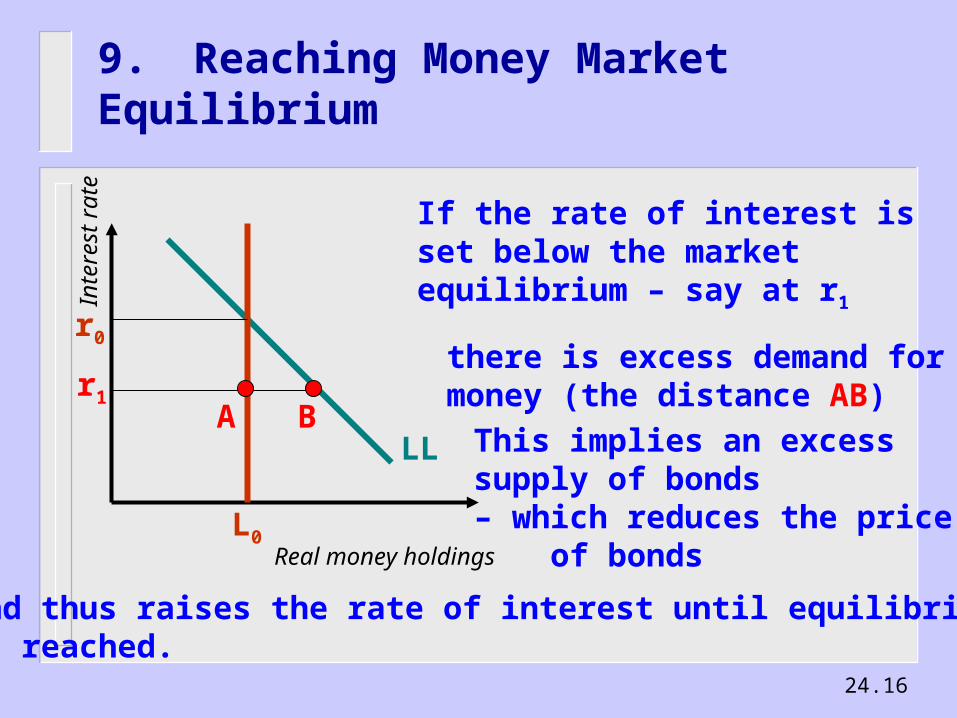

9. Reaching Money Market Equilibrium

Real money holdings

Inte

rest

ra t

e

LL

L0

r0

If the rate of interest isset below the marketequilibrium – say at r1

r1

there is excess demand for money (the distance AB)

A BThis implies an excesssupply of bonds– which reduces the price of bonds

and thus raises the rate of interest until equilibrium is reached.

24.17

7. Reaching Money Market Equilibrium

Stock of Real Wealth = Real Money (LO)+ Real bonds (BO)

Individuals divide their wealth into desired holdings (BD) and desired real money (LP)

LO+ BO = W = BD + LP

BO - BD = W = LP - LO

An excess demand for money exactly matches an excess supply of bonds

24.18

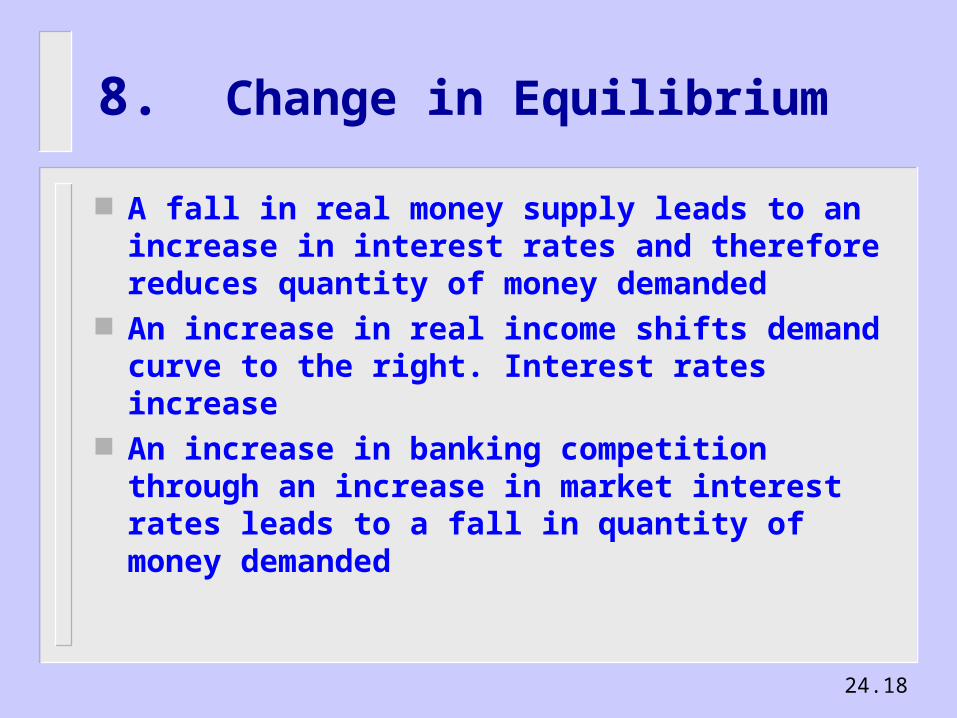

8. Change in Equilibrium

A fall in real money supply leads to an increase in interest rates and therefore reduces quantity of money demanded

An increase in real income shifts demand curve to the right. Interest rates increase

An increase in banking competition through an increase in market interest rates leads to a fall in quantity of money demanded

24.19

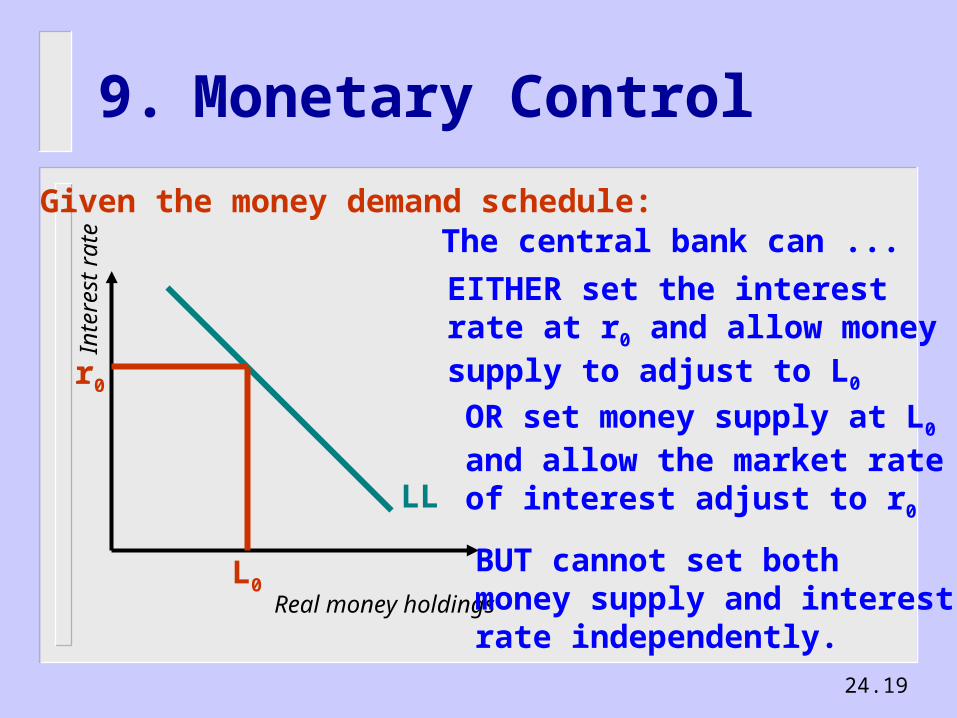

9. Monetary Control

Real money holdings

Inte

rest

ra t

e

LL

L0

r0

Given the money demand schedule:The central bank can ...

EITHER set the interest rate at r0 and allow moneysupply to adjust to L0

OR set money supply at L0

and allow the market rateof interest adjust to r0

BUT cannot set bothmoney supply and interestrate independently.

24.20

9. Monetary control – some provisos

Monetary control cannot be precise unless the authorities know the shape and position of money demand

Controlling money supply is especially problematic– and the Bank of England has preferred to work via

interest rates The situation is further complicated by the

relationship between the interest rate and the exchange rate

24.21

10. Targets and Instruments of Monetary Policy Monetary instrument:

– the variable over which the central bank exercises day to day control

– e.g. interest rate Intermediate target

– the key indicator used as an input to frequent decisions about when to set interest rates

The financial revolution has reduced the reliability of money supply as an indicator– and central banks increasingly use inflation forecasts

as the intermediate target