macroprudential policy evaluation using credit register big … · macroprudential policy...

TRANSCRIPT

Macroprudential Policy Evaluation using

Credit Register Big Data

João Barata Ribeiro Blanco Barroso

Banco Central do Brasil – Research Department

Based on the country contributions to the BIS CCA CGDFS Working Group on “The impact of

macroprudential policies: na empirical analysis using credit register data”. The Brazilian team is

Douglas Araujo, João Barroso, Carlos Cinelli, Bernardus von Doornik and Rodrigo Gonzalez.

The views expressed in this

work are those of the author

and do not necessarily reflect

those of the Banco Central do

Brasil nor of its members.

Motivation

Financial cycles and business cycles do not necessarily coincide.

This creates opportunities to use different tools to address different

cycles (with care for possible interactions)

Macroprudential policies for the financial cycle

Monetary policy for the business cycle

With global financial integration, global liquidity and global risk

aversion are major factors in financial cycles for many economies

As a result: simultaneous macroprudential policy experiments in

several economies, around and after the global financial crisis

Evaluation is a challenging because econometric identification is

challenging: possible benefit of big credit register data.

Motivation

Credit register data allows identification of the credit operations of

several banks with the same agent (mostly firms in our case).

The common component is a proxy for the demand for credit

One can identify the effect of the policy on the supply of credit.

Computationally challenging when the time series dimension is

included in the model: several millions of observations in a dataset.

The challenge was undertaken by several Central Banks in the

Americas in a working group under the auspices of the Bank of

International Settlement, Americas Office.

Macroprudential Policies in the Americas

Canada: LTV

housing

Colombia:

Dynamic

Provisioning

Colombia:

Countercyclical

Reserve

Requirements

Colombia:

Limits on

exchange rate

risk

Argentina:

Liquidity Ratios

Canada: LTV

housing

Colombia:

Limits on

Dividend

Distribution

Colombia:

Liquidity Ratios

Brazil:

Countercyclical

reserve

requirements

Peru: Dynamic

Provisioning

US: SCAP

capital

assessement

program

Argentina: Capital

Buffer

Brazil: Risk

Weight on specific

loans

Brazil:

Countercyclical

reserve

requirements

Canada: LTV

housing

Peru:

Countercyclical

Reserve

Requirements

Peru: Limits on

exchange rate risk

Brazil:

Countercyclical

reserve

requirements

Brazil: Risk Weight

on auto loans

Canada: LTV

housing

Colombia: Limits

on derivatives

Mexico:

Provisioning on

Expected Losses

Peru:

Countercyclical

Reserve

Requirements

Peru: Limits on

exchange rate risk

Argentina:

Capital Buffer

Brazil:

Countercyclical

reserve

requirements

Canada: LTV

housing

Chile: Warning

of house prices

Peru: Liquidity

Ratios

Brazil: LTV cap

on housing

loans

Chile: Warning

of house prices

2007 2008 2009 2010 2011 2012 2013

pre-crisis buble global financial

crisis

begining of QE

policies

deepening of QE

policies

deepening of QE +

euro crisis

deepening of QE

+ euro crisis

deepening of QE

+ taper tantrum

Canada: LTV

housing

Colombia:

Limits on

exchange rate

risk

Canada: LTV

housing

Canada: LTV

housing

Peru: Limits on

exchange rate

risk

Canada: LTV

housing

Colombia: Limit

derivatives

Peru: Limits on

forex

Canada: LTV

housing

Chile: Warning

of house prices

Brazil: LTV cap

on housing

loans

Chile: Warning

of house prices

Colombia:

Countercyclical

Reserve

Requirements

Argentina:

Liquidity Ratios

Colombia:

Liquidity Ratios

Brazil:

Countercyclical

reserve

requirements

Brazil:

Countercyclical

reserve

requirements

Peru:

Countercyclical

reserve

Requirements

Brazil:

Countercyclical

reserve

requirements

Peru:

Countercyclical

reserve

Requirements

Brazil:

Countercyclical

reserve

requirements

Peru: Liquidity

Ratios

Colombia:

Dynamic

Provisioning

Colombia:

Limits on

Dividend

Distribution

Peru: Dynamic

Provisioning

US: SCAP

capital

assessement

program

Argentina:

Capital Buffer

Brazil: Risk

weight auto

loans

Brazil: Risk

Weight auto

loans

Mexico:

Provisioning on

expected

losses

Argentina:

Capital Buffer

2007 2008 2009 2010 2011 2012 2013

Asset Based Instruments

Liquidity Based Instruments

Capital Based Instruments

Capital based instruments affect risk-taking incentives, since it

impacts how much ‘skin in the game’ financial intermediaries have.

Similar risk-taking channel in monetary policy; see Barroso, Souza

and Guerra (2016) for the Brazilian case.

Liquidity/Liability based instruments affect the cost of funding of

financial intermediaries, and therefore credit supply conditions.

Monetary policy also affects the cost of funding, basically through

the same channel.

Asset based instruments affect the budget set of borrowers

Monetary policy affects the intertemporal budget constraint

Complementarity is at leas additive, possibly multiplicative

Relation with monetary policy

Initial findings of the working group based on time series

identification

This means banks are assumed to be homogeneously affected

by the policy, but heterogeneously so in time according to policy

intensity

So far only the Brazilian team presented results based on cross-

section identification (on top of baseline time series results).

This means banks are heterogeneously affected by the policy,

although homogeneously in time according to a policy elasticity

The results for both strategies are consistent in the Brazilian case,

therefore strenghening the overall results of the group.

Time Series x Cross-section identification

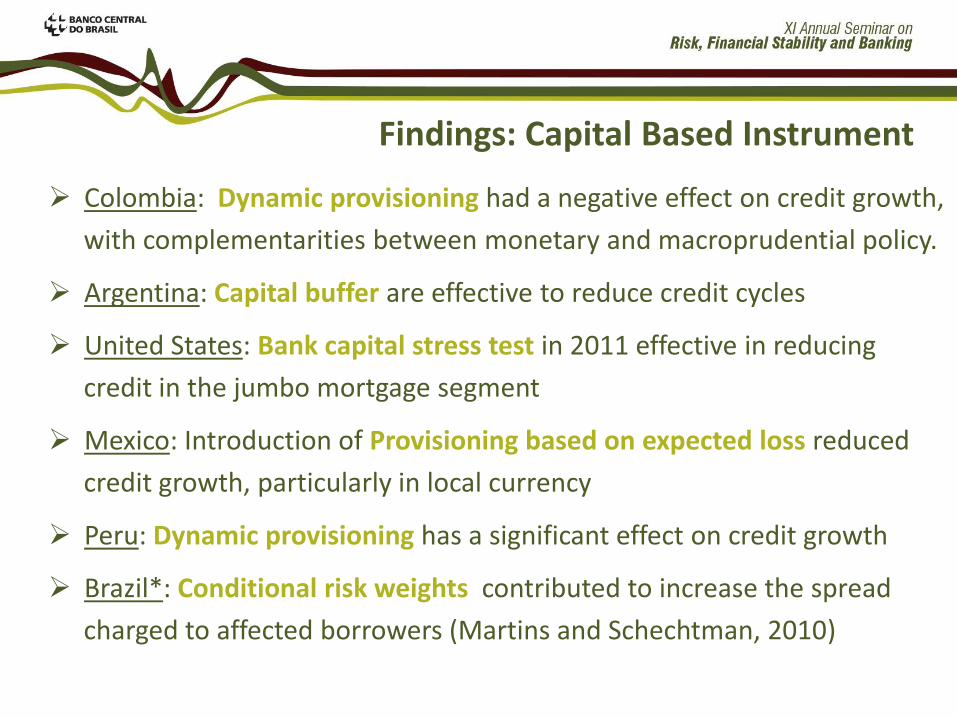

Findings: Capital Based Instrument

Colombia: Dynamic provisioning had a negative effect on credit growth,

with complementarities between monetary and macroprudential policy.

Argentina: Capital buffer are effective to reduce credit cycles

United States: Bank capital stress test in 2011 effective in reducing

credit in the jumbo mortgage segment

Mexico: Introduction of Provisioning based on expected loss reduced

credit growth, particularly in local currency

Peru: Dynamic provisioning has a significant effect on credit growth

Brazil*: Conditional risk weights contributed to increase the spread

charged to affected borrowers (Martins and Schechtman, 2010)

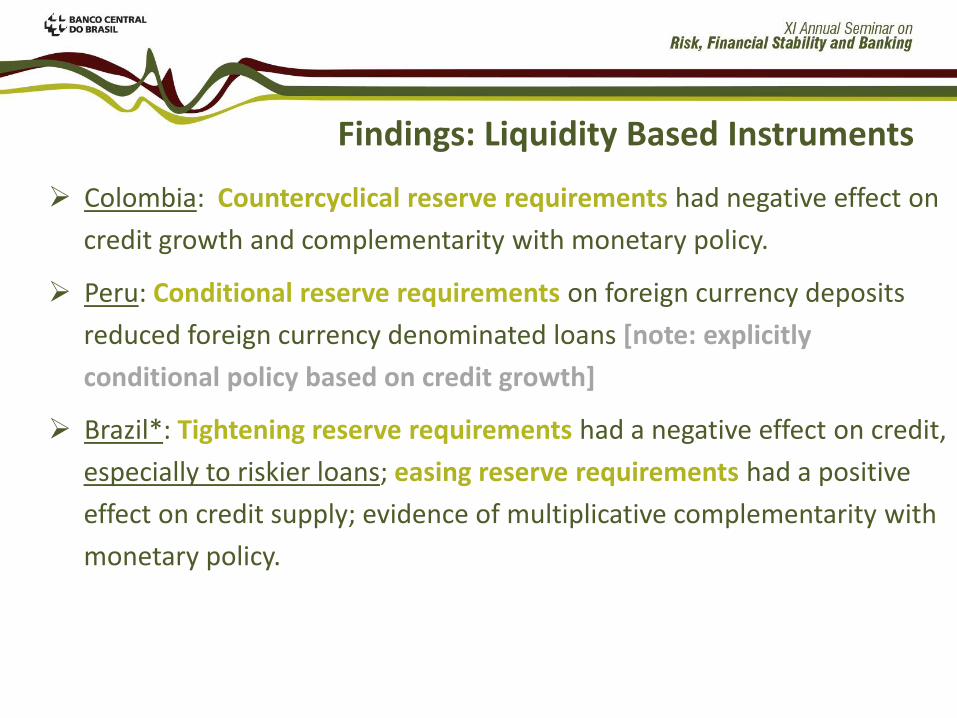

Findings: Liquidity Based Instruments

Colombia: Countercyclical reserve requirements had negative effect on

credit growth and complementarity with monetary policy.

Peru: Conditional reserve requirements on foreign currency deposits

reduced foreign currency denominated loans [note: explicitly

conditional policy based on credit growth]

Brazil*: Tightening reserve requirements had a negative effect on credit,

especially to riskier loans; easing reserve requirements had a positive

effect on credit supply; evidence of multiplicative complementarity with

monetary policy.

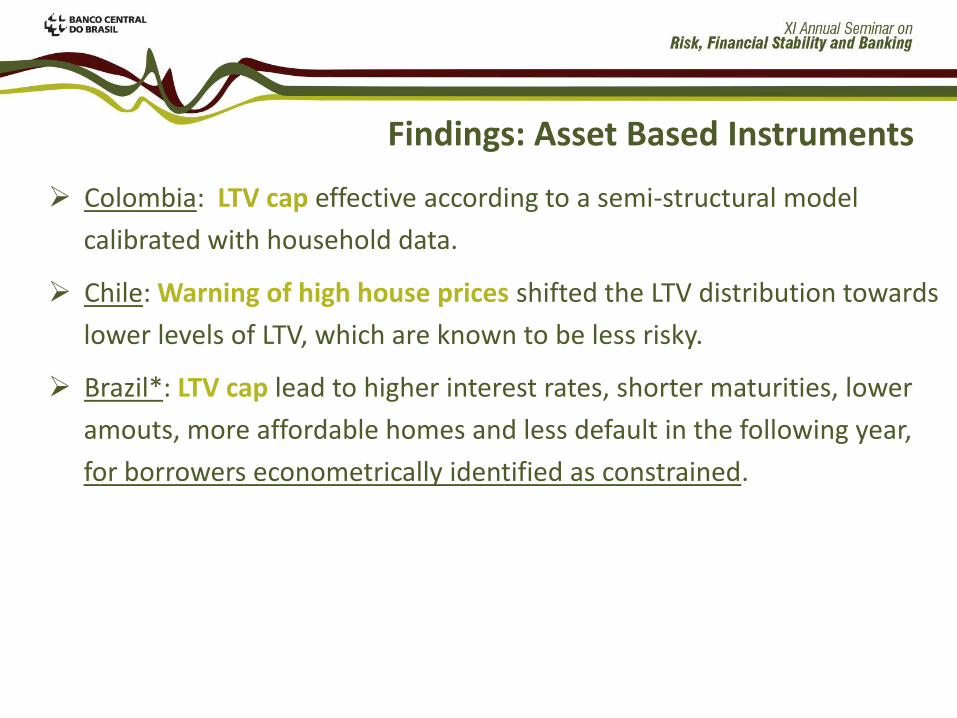

Findings: Asset Based Instruments

Colombia: LTV cap effective according to a semi-structural model

calibrated with household data.

Chile: Warning of high house prices shifted the LTV distribution towards

lower levels of LTV, which are known to be less risky.

Brazil*: LTV cap lead to higher interest rates, shorter maturities, lower

amouts, more affordable homes and less default in the following year,

for borrowers econometrically identified as constrained.

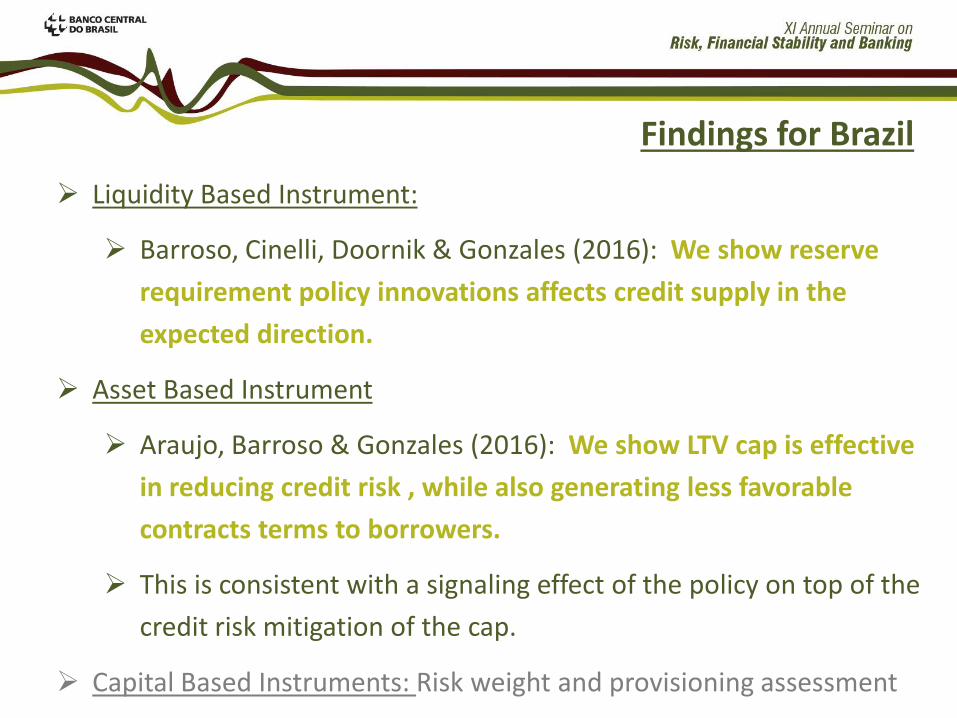

Liquidity Based Instrument:

Barroso, Cinelli, Doornik & Gonzales (2016): We show reserve

requirement policy innovations affects credit supply in the

expected direction.

Asset Based Instrument

Araujo, Barroso & Gonzales (2016): We show LTV cap is effective

in reducing credit risk , while also generating less favorable

contracts terms to borrowers.

This is consistent with a signaling effect of the policy on top of the

credit risk mitigation of the cap.

Capital Based Instruments: Risk weight and provisioning assessment

Findings for Brazil

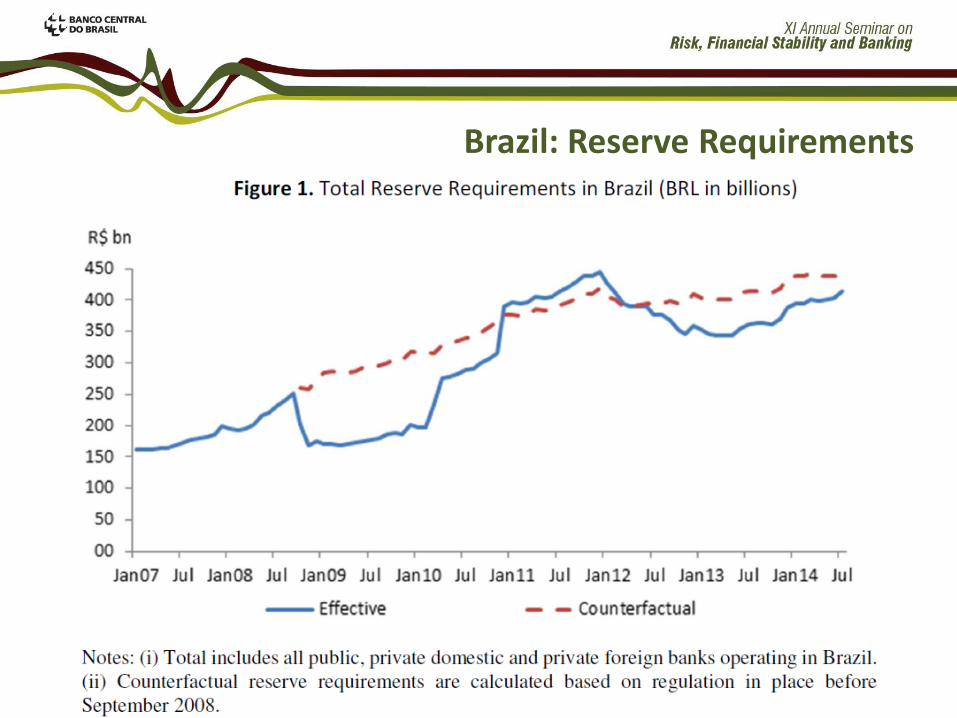

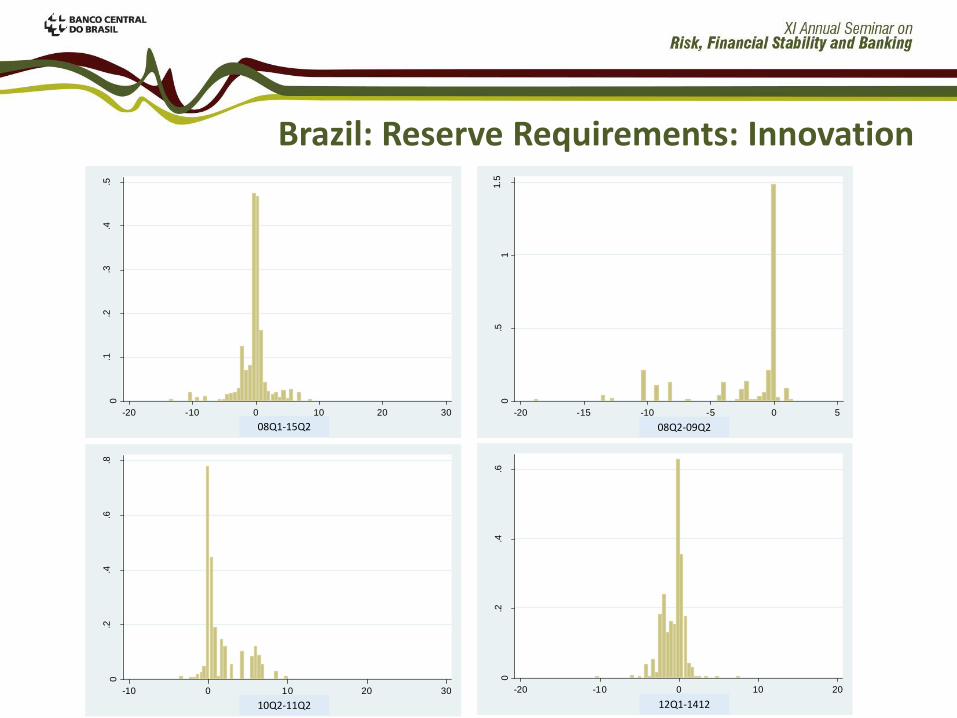

Brazil: Reserve Requirements

0.5

11.5

De

nsity

-20 -15 -10 -5 0 5(sum) d

0.2

.4.6

.8

De

nsity

-10 0 10 20 30(sum) d

08Q2-09Q2

10Q2-11Q2

0.2

.4.6

De

nsity

-20 -10 0 10 20(sum) d

12Q1-1412

0.1

.2.3

.4.5

De

nsity

-20 -10 0 10 20 30(sum) d08Q1-15Q2

Brazil: Reserve Requirements: Innovation

Brazilian Credit Register (SCR); virtually all corporate loans

Data is quarterly from 2008Q1 to 2015Q2

We restrict our sample to firms with loans from more than one bank

36 million data points (27 periods, 132 banks and 478 thousand firms)

The dependent variable is the winsorized log change in the credit

granted to a firm (f), by a bank (b) in a quarter (t)

The firm risk indicator of the firm at the bank or system

Bank balance sheet variables: total assets (size), liquidity ratio

(liquidity), return over assets (ROA), Banks nonperforming loans to

total credit (NPL); and public, foreign or small bank dummy variables

Brazil: Reserve Requirements: Data

We find that RR policy impact credit in the expected direction

The quantitative impact is more sensible in the medium and long run

There is suggestive evidence that higher liquidity and capital ratios

appear to reduce the impact of RR policy

Monetary policy is a complement to RR policy in the sense that

tightening one policy increases the effect of the other on credit

We find that banks avoid riskier firms in the aftermath of policy

changes. During tightening phases, when there is credit contraction,

riskier firms receive less credit

Brazil: Reserve Requirements: Results

It is very well documented that high Loan-to-Value (LTV) is associated

with higher credit risk.

However there is no evidence of the effect of a policy that

unexpectedly imposes a LTV cap (say the effect on credit risk and

contractual terms such as interest rates and maturity )

We provide such evidence

The novelty is to identify who is constrained by the policy once it is

implemented. We cannot distinguish them from unconstrained

borrowers, since everyone respects the cap.

But we can estimate how likely one is to be constrained based on the

pre regulation sample. This is our empirical strategy.

Brazil: LTV cap

Economic activity, housing loans, and housing prices in Brazil All series are real annual growth rates. Sep 2013 LTV cap

Brazil: LTV cap

Frequency of new housing loans by LTV ranges SFH - Before SFH - After

FGTS - Before FGTS - After

0

10000

20000

30000

40000

50000

60000

85-8

6

86-8

7

87-8

8

88-8

9

89-9

0

90-9

1

91-9

2

92-9

3

93-9

4

94-9

5

95-9

6

96-9

7

97-9

8

98-9

9

99-1

00

0

5000

10000

15000

20000

25000

30000

35000

40000

85-8

6

86-8

7

87-8

8

88-8

9

89-9

0

90-9

1

91-9

2

92-9

3

93-9

4

94-9

5

95-9

6

96-9

7

97-9

8

98-9

9

99-1

00

0

5000

10000

15000

20000

25000

30000

35000

40000

85-8

6

86-8

7

87-8

8

88-8

9

89-9

0

90-9

1

91-9

2

92-9

3

93-9

4

94-9

5

95-9

6

96-9

7

97-9

8

98-9

9

99-1

00

0

10000

20000

30000

40000

50000

60000

85-8

6

86-8

7

87-8

8

88-8

9

89-9

0

90-9

1

91-9

2

92-9

3

93-9

4

94-9

5

95-9

6

96-9

7

97-9

8

98-9

9

99-1

00

Brazil: LTV cap

In the SFH segment, but not the FGTS segments, the average housing

loan contracts for treated borrowers have

higher down payment requirements

higher interest rates,

shorter maturities.

In both cases, borrowers compensate these factors by purchasing

more affordable homes, and improve their repayment behavior.

The less favorable terms offered to SFH may result from official

communication: prudential concerns were signaled only for this

segment of the market.

Brazil: LTV cap: Results

Credit Register data offers good opportunities to identify the effects

of macroprudential policies.

There are computational challenges, but the payoff justifies exploring

this source of big data.

For the Americas, the evidence is consistent with effective capital,

liquidity and asset based macroprudential policies.

For Brazil, the evidence is particularly strong given the size of shocks,

the different directions of the shocks and the identification of control

groups through counterfactuals.

Summary