mahindra finance study of mutual funds

TRANSCRIPT

SUMMER TRAINING PROJECT REPORT

on

‘STUDY OF MUTUAL FUND’S.I.P., NOIDA

SUBMITTED FOR PARTIAL FULFILLMENT OF THE DEGREE OF

MASTER OF BUSINESS ADMINISTRATION[2014-2015]

By

CHAURASIA DIPESH RAMDULARE(Roll No.: 1368670033)

EXTERNAL SUPERVISOR INTERNAL SUPERVISOR Amitabh Ghosh RAJNISH KHARE HR Manager ASSIATANT PROFESER Mahindra Finance Ltd., AIAM, GRATER NOIDA

ACCURATE INTITUTE OF ADVANCE MANAGEMENT, GRATER NOIDA

(Affiliated to UPTU and Approved by AICT

Accurate Institute of Advanced Management

(Affiliated to UPTU and Approved by AICTE)

1

______________________________________

Date:

HEAD OF MBA PROGRAM’S CERTIFICATE

Certified that the Summer Training Project Report titled “STUDY OF MUTUAL FUNDS

(MAHINDRA FINANCE” is carried out by Mr. CHAURASIA DIPESH RAMDULARE,

Roll No.1368670033, a student of MBA –III semester at Accurate Institute of

Advanced Management, Greater Noida, under the supervision of –Shaurabh

Chandra HR Manager (Designation) MAHINDRA FINANCE.

This is an original work carried out by the said student to the best of my knowledge and I

recommend for the submission of this summer Training Project Report to Uttar Pradesh

Technical University, Lucknow in the partial fulfillment of the award of MBA Dagree.

Prof.(Dr.) Amar Kr. Saxena

Director,AIAM,Greater Noida.

Plot No. 49, Knowledge Park-3, Greater NOIDA-201306 (UP), Phone: 0120-2328235, Fax:

0120-2320355 E. Mail.: [email protected], Web: http//www.aiam.in

DECLARATION

To,

The Director,

2

Accurate Institute of Advance Management,

Plot No.-49, Knowledge Park 3

Greater Noida

Utter Pradesh – 201308.

Respected Sir,

I hereby declare that this project report entitled “STUDY OF MUTUAL FUNDS

(MAHINDRA FINANCE)" is written and submitted by me under the kind guidance of

Mr. Amitabh Ghosh, HR Manager, Industry Guide and Mr. RAJNISH KHARE,

Asst.Prof, AIAM, Gr. Noida (U.P.). The findings and interpretations in the report are

based on both primary and secondary data collection. This project is not copied from any

source or other Project submitted for similar purpose.

DATE:

PLACE: Greater Noida

ROLL NO.: 1368670033

Signature of student

PREFACE

3

The learning process of classroom is incomplete without any practical field experience. It is

because of the reason that our Institute like any other, has provision for practical training, so

practical training is vital. Accordingly we had our training with MAHINDRA FINANCE.

This 8 weeks training gave us an insight into the working of an organization and learn how

some of the important concepts that we have been studying as a student of management are

applicable in the field. The project is a sincere attempt to focus on the subject in a lucid

manner. I sincerely attempted to effort to carry out study in deep on subject.

During this period we had the opportunity to observe the company’s performance, place in

the industry, its products, pricing, advertisement, promotions and its good will through our

market survey. It is hoped that this study will provide valuable information in various issues

related to MAHINDRA FINANCE, oriented industries.

CHAURASIA DIPESH RAMDULARE

Roll no.:- 1368670033

ACKNOWLEDGEMENT

4

With immense please we are presenting “STUDY OF MUTUAL FUNDS

(MAHINDRA FINANCE)” Project report as part of the curriculum of ‘Master of

Management Studies’. We wish to thank all the people who gave us unending support.

I express my profound thanks to Director and Prof. Amar Sexena,

project guide and all those who have indirectly guided and helped us in

preparation of this project.

We also like to extend our gratitude to all staff and our colleagues of College of

Management, who provided moral support, a conductive work environment and the much-

needed inspiration to conclude the project in time and a special thanks to my parents who are

integral part of the project.

Thanking you.

Accurate Institute of Advance Management

Knowledge Park 3, Greater Noida

CONTENTTitle Page

Chapter 1 INTRODUCTION OF THE STUDY

5

Chapter 2 MUTUAL FUNDS

1. Introduction Of Mutual Fund

2. Objective Of The Study

3. Methodology Of The Study

4. Financial System In India.

Chapter 3 MUTUAL FUNDS – AS INVESTMENT

1. Advantages Of Mutual Fund

Chapter 4 HISTORY OF MUTUAL FUND

1. Performance Of Mutual Fund

Chapter 5 RESEARCH METHODOLOGY

1. Data Collection Kind of Research

Chapter 6 CONCLUSIONS, SUGGESTIONS & LIMITATION

Chapter 7 REFERENCES

6

7

MUTUAL FUND HAS BECOME AN IMPORTANT

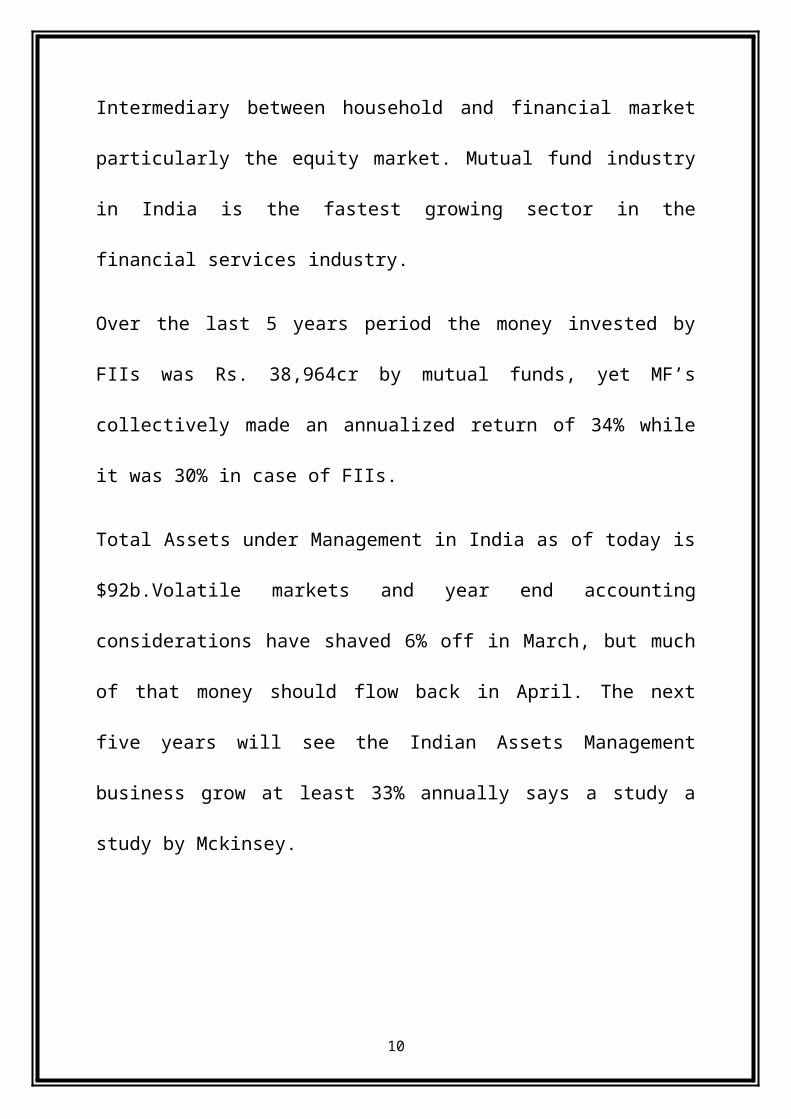

Intermediary between household and financial market particularly the equity

market. Mutual fund industry in India is the fastest growing sector in the

financial services industry.

Over the last 5 years period the money invested by FIIs was Rs. 38,964cr by

mutual funds, yet MF’s collectively made an annualized return of 34% while it

was 30% in case of FIIs.

Total Assets under Management in India as of today is $92b.Volatile markets

and year end accounting considerations have shaved 6% off in March, but much

of that money should flow back in April. The next five years will see the Indian

Assets Management business grow at least 33% annually says a study a study

by Mckinsey.

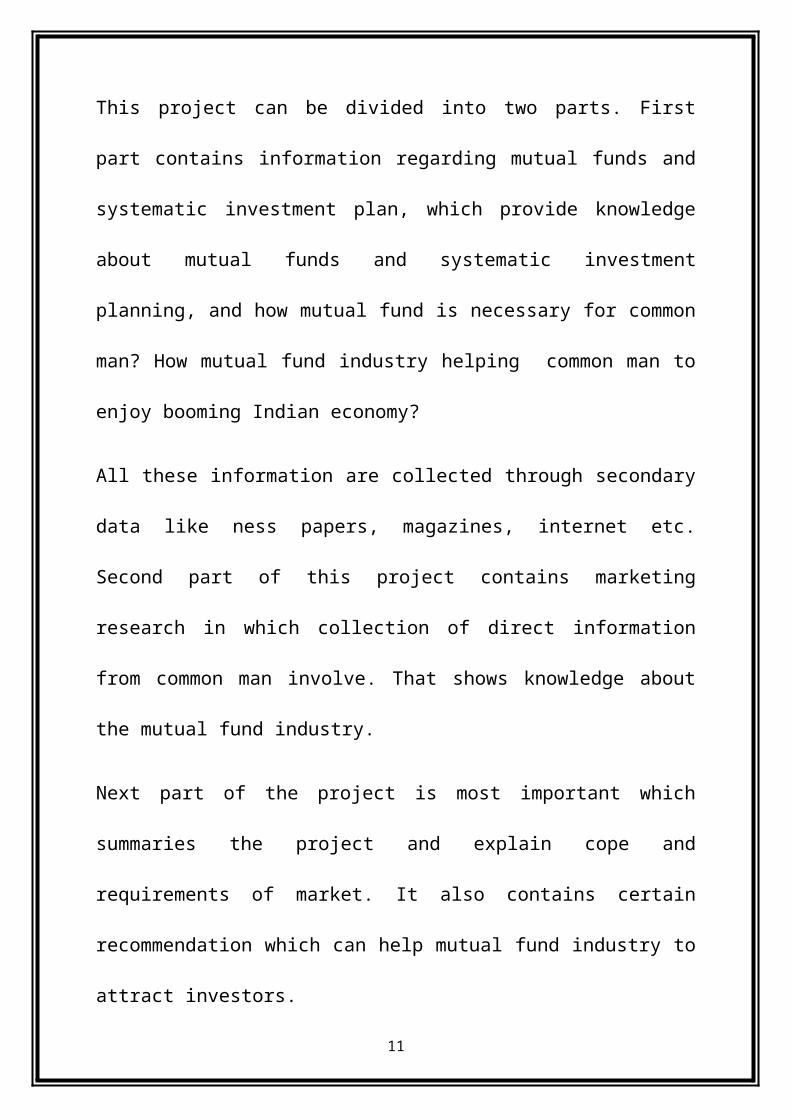

This project can be divided into two parts. First part contains information

regarding mutual funds and systematic investment plan, which provide

knowledge about mutual funds and systematic investment planning, and how

mutual fund is necessary for common man? How mutual fund industry helping

common man to enjoy booming Indian economy?

8

All these information are collected through secondary data like ness papers,

magazines, internet etc. Second part of this project contains marketing research

in which collection of direct information from common man involve. That

shows knowledge about the mutual fund industry.

Next part of the project is most important which summaries the project and

explain cope and requirements of market. It also contains certain

recommendation which can help mutual fund industry to attract investors.

9

COMPANY PROFILE

10

The US $6 billion Mahindra Group is among the top 10 industrial houses in

India. Mahindra & Mahindra is the only Indian company among the top tractor

brands in the world.

Mahindra’s Farm Equipment Sector has recently won the Japan Quality Medal,

the only tractor company worldwide to be bestowed this honor, It also holds the

distinction of being the only tractor company worldwide to win the Deming

prize. Mahindra is the market leader in multi-utility vehicles in India.

It made a milestone entry into the passenger car segment with the Logan.

The group has a leading presence in key sectors of the Indian economy

including the financial services, trade and logistics, automotive components,

information technology, and infrastructure development

With over 62 years of manufacturing experience, the Mahindra Group has built

a strong base in technology, engineering, marketing and distribution which are

key to its evolution as a customer centric organization. The Group employs

over 50,000 people and had several state-of-the –art facilities in India and

overseas.

Mahindra & Mahindra has entered into partnerships with international

companies like Renault SA France, and International Truck and Engine

Corporation, USA. Forbes has ranked the Mahindra Group in its Top 200 list of

11

the World’s Most Reputable companies and in the Top 10 list of Most Reputable

Indian Companies. Mahindra has recently been honored with the Bombay

Chamber Good Corporate Citizen Award for 2006-07.

12

MAHINDRA & MAHINDRA FINANCIAL SERVICES LTD.

Overview :

A Subsidiary of Mahindra & Mahindra Ltd, it is one of the leading non

banking finance companies focused on rural and semi urban sector.

CRISIL has assigned AA+ rating to the company’s long term debt

reflecting a high degree of safety.

MMFSL finances purchase of utility vehicles, tractors, cars and

commercial vehicles. The company’s goal is to be the preferred provider

of financing services in the rural and semi urban areas of India

A company has 436 branches covering 25 states and 2 union territories.

Assets under Management have increased from Rs 7,919 crores year on

year basis.

MMFSL recorded total revenues of INR 12,268 million & PAT of INR

1’770 million for the year ends March 31, 2008 and had total Assets of

INR 70,218 million as of march 31, 2008.

13

DIVERSIFIED PRODUCT PORTFOLIO

Started financing non M&M Vehicle.

Commenced insurance broking business through MIBL

Commenced financing commercial vehicles

Commenced mutual fund distribution business

Commenced financing two-wheeler on pilot basis

Plans to enter housing loans and personal loans business; Children’s

higher Education, Medical treatment,

Consumer durable, House furniture ,

Agriculture Needs; Exotic Holiday or just squash a Temporary Cash

requirement .

14

MUTUAL FUNDS

15

“A Mutual fund is a company that brings together money from many people

and invests it in stocks, bonds or other assets. The combined holding of stocks,

bonds or other assets the fund owns are known as it portfolio. Each investor in

the fund owns shares, which represents apart of these holding……”

................. (U.S. securities exchange commission).

A mutual fund is a trust that pools the saving of a number of investors who

shares a common financial goal. The money thus collected is then invested in

capital market instruments such as shares, debenture and other securities.

The income earned through these investments and the capital appreciations

realized are shared by its unit holders in proportion to the number of units

owned by them. Thus mutual fund is the most suitable investment for the

common man as it offers an opportunity to invest in a diversified, professionally

managed basket of securities at a relatively low cost.

Mutual funds are financial intermediaries, which collect the savings of small investors and invest

them in a diversified portfolio of securities to minimise risk and maximise returns for their

participants.

16

Mutual funds have given a major fillip to the capital market - both primary as well as

secondary. The units of mutual funds, in turn, are also tradable securities. Their price

is determined by their net asset value (NAV) which is declared periodically.

The operations of the private mutual funds are regulated by SEBI with regard to their

registration, operations, administration and issue as well as trading. There are various

types of mutual funds, depending on whether they are open ended or close ended and

what their end use of funds is an open-ended fund provides for easy liquidity and is a

perennial fund, as its very name suggests.

A closed-ended fund has a stipulated maturity period, generally five years.

A growth fund has a higher percentage of its corpus invested in equity than in fixed

income securities, hence the chances of capital appreciation (growth) are higher. In

growth funds, the dividend accrued, if any, is reinvested in the fund for the capital

appreciation of investments made by the investor.

An Income fund on the other hand invests a larger portion of its corpus in fixed

income securities in order to pay out a portion of its earnings to the investor at regular

intervals.

A balanced fund invests equally in fixed income and equity in order to earn a

minimum return to the investors. Some mutual funds are limited to a particular

17

industry; others invest exclusively in certain kinds of short-term instruments like

money market or government securities.

18

INTRODUCTION

19

CONCEPT OF MUTUAL FUNDS

Encarta Encyclopedia defines mutual funds as forms of management Investment Company

that combines the money of its shareholders and invests those funds in a wide variety of

stocks, bonds and money market instruments. The latter include short – term investments

such as government bonds and securities, commercial papers, certificates of deposit, etc.

Mutual funds provide the investor with professional management of funds and diversification

of investment.

Mutual fund units are investment vehicles that provide a means of participation in the stock

market for people who have neither the time, nor the money, nor perhaps the expertise to

undertake direct investment in equities successfully. On the other hand, they also provide a

route into specialist markets where direct investment often demands both more time and more

knowledge than an investor may possess.

The price of units in any mutual fund is governed by the value of the underlying securities.

The value of an investor’s holding in a unit can therefore, like an investment in shares, go

down as well as up.

Mutual fund is a trust that pools the savings of a number of investors who share a common

financial goal. The money thus collected is then invested in various capital market

instruments. Each mutual fund has a specific investment objective and tries to meet that

objective through active portfolio management.

20

Major Types of Mutual Fund Schemes As Per Asset Class

EQUITY SCHEMES

Equity schemes invest primarily in shares. Depending on the scheme objective of investment

could be in:

Growth stocks where earnings growth is expected to be attractive.

Momentum stocks that go up or down in line with the market.

Value stocks where the fund manager is of the view that current valuation in the market.

Do not reflect intrinsic value, or

Income stocks that earn high return through dividends

DEBT OR INCOME SCHEMES

Gilt schemes invest in government securities. Apart from being the most liquid securities in

the debt market, govt. securities are eligible for liquidity support. Since the issuer is the

governments of India/States these funds have little risk of default and hence offer better

protection of principal.

Bond schemes invest in bonds issued by the government or any other issuer, also by private

companies, banks, financial institutions and other entities such as infrastructure

companies/utilities. By investing in debt, these funds target low risk and stable income for the

investor as their key objective.

Debt funds are largely considered as income funds as they do not target capital appreciation,

look for high current income and therefore distribute a substantial part of their surplus to the

investors.

21

Scope of the Study

Mutual funds normally invest in a well diversified portfolio or securities. Each investor in a

fund is a part owner of the fund’s entire asset. This enables him to hold a diversified

investment portfolio even with a small amount of investment that would otherwise require

big capital.

Even if an investor has big amount of capital available to him, he benefits from the

professional management skills brought in by the fund in the management of the investor’s

portfolio. The investment management skills along with the needed research into available

investment options, ensure a much better than what an investor can manage on his own.

Diversification reduces the risk of loss, as compared to investing directly in one or two shares

or debentures or other instruments.

A direct investor bears all the costs of investing such as brokerage or custody of securities.

When going through a fund, he has the benefit of economies of scale; the funds pay lesser

costs because of larger volumes a benefit on to its investors.

Even often, investors hold shares or bonds they cannot directly, easily and quickly sell.

Investing in a mutual fund is much more liquid. The investor can liquidate the investments by

selling its units to the fund if open ended, or selling them to market if it is close-ended.

Investors can even transfer their holdings from one scheme to the other, get updated market

information and so on. For equity – diversified schemes the risk and return measures can be

calculated and the comparison between various schemes can be made that fall under different

asset management companies.

22

Objective of the study

The main objective of the study was to analyze in detail and compare the performance of

different equity diversified schemes across various AMC and also to take a note of the budget

announcements and their impact on the mutual fund industry.

The following are the specific objectives of the study: -

To study the investors’ perception towards Mutual Fund as an investment avenue.

To make a comparative analysis of twenty equity – diversified mutual fund schemes

across various asset management companies on the basis of risk and return measures of

performance.

To analyse various features of the schemes under consideration

To understand the impact of Budget announcements of last two years on the mutual

fund industry.

To assess new developments taking place in the mutual fund industry.

23

Methodology of the Study

The project has been carried out to compare the different equity diversified schemes with few

having growth option and few with dividend option which fall under various asset

management companies.

For any study to be conducted a set pattern of steps is required to be carried out.

First: To communicate with the people in the organization to have their opinion on “Mutual

Funds – as Investment Avenue” .Thereby, from this a conclusion about investors’ perception

can be drawn.

Second: Various tables, charts and diagrams are used for precise understanding of the topic

under study. Use of various performance measures is done.

Third: The data can be collected from various sources which would be required to be

analyzed before findings are resulted and conclusions are drawn.

Fourth: Expert’s guidance will have to be taken from the top management to derive to a

meaningful conclusion from the finding.

Fifth: A financial report will have to be prepared successfully, accomplishing all the

objectives mentioned above.

24

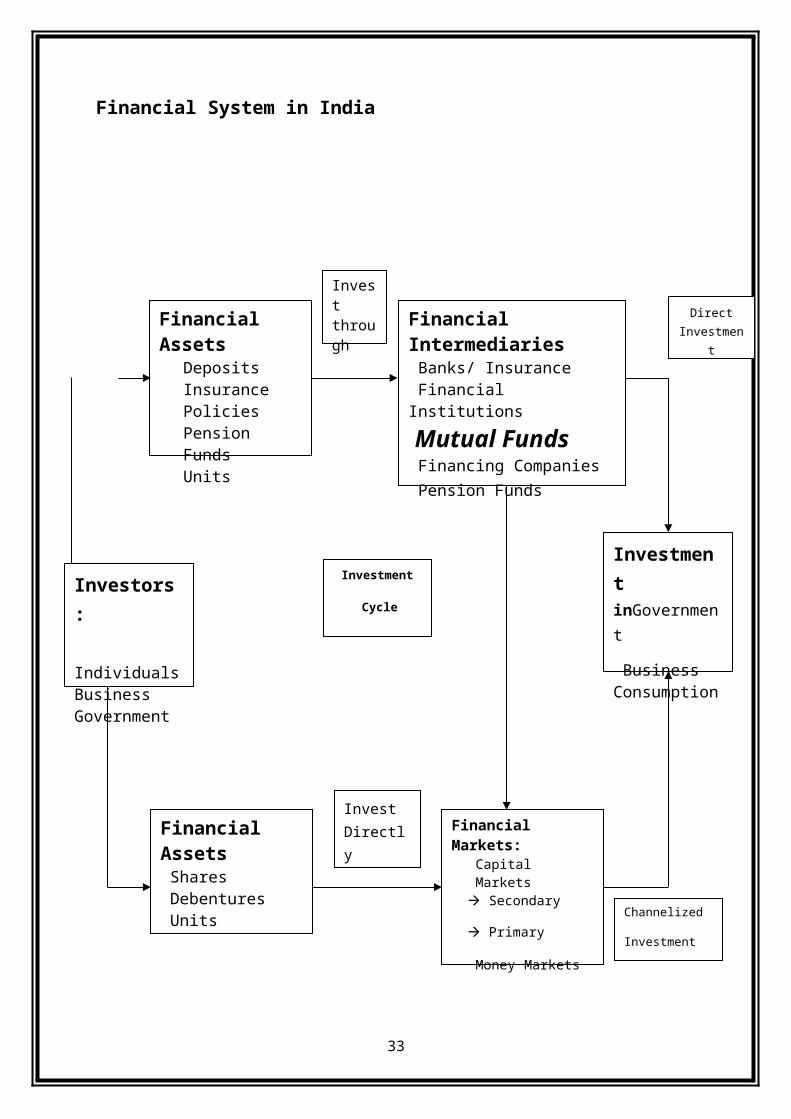

Financial System in India

25

Financial Assets DepositsInsurance PoliciesPension FundsUnits

Financial Intermediaries Banks/ Insurance Financial Institutions

Mutual Funds Financing Companies Pension Funds

Investment inGovernment

BusinessConsumption

Financial Markets: Capital Markets

Secondary

Primary

Money Markets

Financial Assets Shares Debentures Units

Investors:

IndividualsBusinessGovernment

Invest through

Investment

Cycle

Invest Directly

Direct Investment

Channelized

Investment

CONCEPT OF MUTUAL FUNDS

Encarta Encyclopedia defines mutual funds as forms of management Investment Company

that combines the money of its shareholders and invests those funds in a wide variety of

stocks, bonds and money market instruments. The latter include short – term investments

such as government bonds and securities, commercial papers, certificates of deposit, etc.

Mutual funds provide the investor with professional management of funds and diversification

of investment.

Mutual fund units are investment vehicles that provide a means of participation in the stock

market for people who have neither the time, nor the money, nor perhaps the expertise to

undertake direct investment in equities successfully. On the other hand, they also provide a

route into specialist markets where direct investment often demands both more time and more

knowledge than an investor may possess.

The price of units in any mutual fund is governed by the value of the underlying securities.

The value of an investor’s holding in a unit can therefore, like an investment in shares, go

down as well as up.

Mutual fund is a trust that pools the savings of a number of investors who share a common

financial goal. The money thus collected is then invested in various capital market

instruments. Each mutual fund has a specific investment objective and tries to meet that

objective through active portfolio management.

26

EMERGENCE OF MUTUAL FUNDS

The history of Mutual Funds dates back to 1830 when William I established first such fund in

Belgium. Almost 40 years later, foreign and colonial government trust was established in

England in 1868 followed by Massachusetts Investor’s Trust, Boston, USA in 1924 (which is

working till today). Slow growth had been the result of 1926 great depression which shock

the world economy negatively affecting the public interest in stocks, and therefore in funds.

Moreover, to revive the same a formal attempt was made by forming Investment Company

Act, 1940 to regulate the functioning of mutual funds. In 1960s, the industry finally grabbed

the investor’s attention due to Jack Dreyfus’s Fund’s good performance and clever

advertising. Market collapse of 1969-90 finally crossed $2000 billion mark in 1994. By the

same time total assets managed by the mutual funds the world over had crossed a startling

figure by 2000 A.D. Americans also believe that by the turn of the century they can expect to

have more money in mutual funds than in saving bank accounts.

Emergence of mutual funds in India, Unit Trust of India (UTI) established the first mutual

fund in 1964. In 1987, public sector banks like SBI and CANARA BANK made an entry by

floating different schemes. In 1989, Life Insurance Corporation of India floated LIC Mutual

Fund.

Mutual Fund industry in India received a boost when it was thrown open to private sector in

1993 and foreign mutual funds making an opening in 1994.

27

M UTUAL FUND MILESTONES IN INDIA

Year Milestones

1964 A concept arrives. India’s first mutual fund launches US 1994

1987 End of a monopoly. UTI’s stranglehold ends as Public sector banks join

the funds bandwagon. SBI and Canara Bank float Mutual Fund

1989 Financial Institutions jump into fray with launch of LIC mutual fund

1993 Threat of competition. The industry is thrown open to private sector.

Kothari pioneer MF sets a hot pace

1994 Foreign MF arrives. Its Morgan mania.

1998 Mutual Funds in troubled waters. Funds under perform index. US – 64

Flop show

2000 Shakeout imminent. Myth about safety and liquidity of investment in

UTI broken

2001 US – 64 to be redeemed as per pre – determined rate scheme.

Charitable Institutions allowed keeping their surplus money in mutual

funds.

Committee formed to evolve benchmark for performance appraisal of

debt schemes by SEBI and AMFI.

2002 SEBI to control UTI also.

2003 Fund of Funds floated

2004 Mutual Funds allowed to invest in overseas securities

28

MUTUAL FUNDS – AS INVESTMENT

An Investment Preference Order

Highest Risk Outright Speculation

High Risk

Aggressive Growth

Aggressive Income

Average Risk

Growth and Income

Low RiskConservative Income and Reasonable

Stability

Lowest Risk

Maximum Safety and Stability

29

The diagram on the previous page indicates what role the mutual fund has to play or what

service gap they try to fill for the investors. Because an average investor is basically

interested in the achievement of two prime objectives, i.e. Income and Growth / Capital gain

concerning investment made by an investor. In any event, its- wise to keep the familiar

investment diagram in mind.

Mutual funds go long way in achievement of the objectives like growth income, stable

income, etc. as a large base of capital is created due to pooling of funds by small investors,

hence a diversified portfolio of securities is created which obviously reduces risk to the

minimum. Professionals who provide expert supervision for managing such funds manage the

funds. The framework of rules given by SEBI provides liquidity and safety to mutual fund

investment.

Why to do investment in Mutual Funds?

A proven principle of sound investment is – do not put all eggs in one basket. Investment in

mutual funds is beneficial as: -

Firstly, they help in pooling of funds and investing in large basket of shares of different

companies. Thus by investing in diverse companies, mutual funds can protect against

unexpected fall in value of investment.

Secondly, an average investor does not have enough time and resources to develop

professional attitude towards their investment. Here, professional fund managers engaged by

mutual funds take desirable investment decisions on behalf of investors so as to make better

utilization of resources.

Thirdly, investment in mutual funds is comparatively more liquid because investor can sell

units in open market and can approach mutual fund to repurchase the units at declared Net

Asset Value depending upon different type of scheme.

Fourthly, investors can avail tax – rebates by investing in different tax-savings schemes

floated by these funds, approved by the Government.

Lastly, operating cost is minimized per head because of large size of investible funds,

thereby releasing more net income for investors.

30

In general terms the advantages of Mutual Funds can be enlisted and explained as appended.

ADVANTAGES OF MUTUAL FUNDS

Professional Management

Most mutual funds pay topflight professionals to manage their investments. These managers

decide what securities the fund will buy and sell.

Diversification

The best mutual funds design their portfolios so individual investments will react differently

to the same economic conditions. For example, economic conditions like a rise in interest

rates may cause certain securities in a diversified portfolio to decrease in value. Other

securities in the portfolio will respond to the same economic conditions by increasing in

value. When a portfolio is balanced in this way, the value of the overall portfolio should

gradually increase over time, even if some securities lose value.

Liquidity

It's easy to get your money out of a mutual fund.

Low cost

Mutual fund expenses are often no more than 1.5 percent of your investment. Expenses for

Index Funds are less than that, because index funds are not actively managed. Instead, they

automatically buy stock in companies that are listed on a specific index.

Regulatory oversight

Mutual funds are subject to many government regulations that protect investors from fraud.

The mutual funds have various benefits over and above what are mentioned like

transparency, flexibility, choice of schemes, tax benefits and also well regulated.

31

APART FROM ALL THE BENEFITS STATED HERE MUTUAL FUNDS MAY

ALSO HAVE FEW LIMITATIONS THAT MAY NOT FOR EVERYONE: -

Fees and commissions

All funds charge administrative fees to cover their day-to-day expenses. Some funds also

charge sales commissions or "loads" to compensate brokers, financial consultants, or

financial planners.

Management risk

When you invest in a mutual fund, you depend on the fund's manager to make the right

decisions regarding the fund's portfolio. If the manager does not perform as well as you had

hoped, you might not make as much money on your investment as you expected. Of course,

if you invest in Index Funds, you forego management risk, because these funds do not

employ managers.

No Guarantees

No investment is risk free. If the entire stock market declines in value, the value of mutual

fund shares will go down as well, no matter how balanced the portfolio. Investors encounter

fewer risks when they invest in mutual funds than when they buy and sell stocks on their

own. However, anyone who invests through a mutual fund runs the risk of losing money.

Taxes

During a typical year, most actively managed mutual funds sell anywhere from 20 to 70

percent of the securities in their portfolios. If your fund makes a profit on its sales, you will

pay taxes on the income you receive, even if you reinvest the money you made.

32

Which Parties are Involved?

1. Investors

Every investor, given the financial position and personal disposition, has a certain inclination

to take risk (risk profile). The hypothesis is that by taking an incremental risk (of losing

capital, wholly or partly), it would be possible for the investor to earn an incremental return.

Mutual fund is a solution for investors who lack time, the inclination or the skills to actively

manage their investment risk in individual securities. They can delegate his role to mutual

fund, while retaining the right and the obligation to monitor their investments in the scheme

(which, in turn, invests in individual securities).

In the absence of a mutual fund option, the moneys of such “passive” investors would lie

either in bank deposits or other “safe” investment options, thus depriving them of the

possibility of earning a better return.

2. Trustees

Trustees are the people within a mutual fund organization who are responsible for ensuring

that investors’ interest in a scheme are properly taken care of.

In return for their services, they are paid trustee fees, which are normally charged to the

scheme.

3. Asset Management Company (AMC)

AMCs manage the investment portfolios of schemes. An AMC’s income comes from

management fees it charges the schemes it manages. Some countries provide for performance

based management fees as well.

In order to management fee, an AMC has naturally to employ people and bear all the

establishment costs that are related to its activity, such as for premises, furniture, computers

and other assets, software development, communication costs, etc. These are to be met out of

the management fee earned.

So long as the income through management fees more than covers it expenses, an AMC is

economically viable.

Given the nature of its activity, a certain minimum establishment and infrastructure is

necessary for an AMC’s functioning. Since costs cannot be reduced below a base level, every

AMC needs to have a reasonable corpus of assets under management (AUM), below which it

is not viable.

33

The break even level of AUM is a function of cost structure of the AMC and distribution of

assets between its different types of schemes since debt schemes and index schemes generally

yield a lower management fees.

4. Distributors

Distributors earn a commission for bringing investors into the schemes of a mutual fund. This

commission is an expense for the scheme, although there are occasions when an AMC may

choose to bear cost, wholly or partly.

Depending on the financial and physical resources at their disposal, the distributors could be:

Tier I distribution who have their own or franchised network reaching out to investors all

across the country; or

Tier II distributors who are generally regional players with some reach within their

region; or

Tier III distributors who are small and marginal players with limited reach.

5. Registrars

An investor holding in mutual fund schemes is typically tracked by the schemes Registrar and

Transfer agent (R&T).

Some AMCs prefer to handle this role in house, i.e. on their own instead of appointing an

R&T. The Registrar or AMC as the case may be maintains an account of the investor’s

investments in and disinvestments from the schemes. Requests to invest more money into a

scheme, or to redeem money against existing investments in a scheme are processed by the

R&T.

6.Custodian / Depository

The custodian maintains custody of the securities in which the scheme invests – as distinct

from the registrar who tracks the investment by investors in the scheme. This ensures an

ongoing independent record of the investments of the scheme. The custodian follows up on

various corporate actions, such as rights, bonus and dividends declared by investee

companies.

34

The mutual fund industry in India started in 1963 with formation of unit trust of

India, at the initiative of the govt. of India and reserve bank. The history of

mutual funds in India can be broadly divided into four distinct phases:

FIRST PHASE: 1964 – 1987

UTI was established on 1963 by an act of parliament. It was setup by RBI and

functioned under the regulatory and administrative control of the RBI.

In 1978 UTI was de-linked from the RBI and industrial development bank of

India (IDBI) took over the regulatory and administrative control in place of

RBI. The first schemed launched by UTI was unit scheme 1964. At the end of

the 1988 UTI had Rs.6700 cr. of assets under management.

Second phase: 1987 – 1993 (entry of public sector funds)

The year 1987 marked the entry of non UTI, public sector mutual funds setup

by public sector banks and life insurance Corporation of India and general

Insurance Corporation of India. SBI mutual fund was the first Non and UTI

mutual fund established in June 1987 followed by Can bank mutual fund (Dec

87), PNB mutual fund (august 89), Indian bank mutual fund (Nov 89), Bank of

India (June 90), Bank of Baroda mutual fund (Oct 92). LIC established its

mutual fund in June 1989 while GIC had setup its mutual funds in Dec 1990.

At the end of 1993, the mutual fund industry had assets under management of Rs. 47,004 cr.

35

Third phase: 1993 – 2003 (entry of private sector funds)

With the entry of private sector funds in 1993 a new era started in the

Indian mutual fund, except UTI were to be registered and governed. The

erstwhile KOTHARI PIONEER (now merged in FRANKLIN TEMPLETON)

was a first private sector mutual fund registered in July 1993. The 1993 SEBI

regulations were substituted by a more comprehensive and revised mutual fund

a regulation in 1996. The industry now functions under the same SEBI

regulation 1996.

Fourth phase: since Feb 2003

In Feb 2003, following the repeal of the UTI act 1963 UTI was bifurcated

into two separate entities. One is the specified undertaking of the UTI of India

with assets under management of Rs. 29,835 cr. As, the end of Jan 2003,

representing broadly, the assets of US 64 scheme, assured return and certain

other schemes. The specified undertaking of UTI, functioning under an

administrator and under the rules framed by the govt. of India and does not

come under the preview of the mutual fund regulations. The second is the UTI

mutual fund Ltd, sponsored by SBI, PNB, BOB and LIC. It is registered with

SEBI and functions

36

HISTORY OF MUTUAL FUNDS

The modern mutual fund was first introduced in Belgium in 1822. This form of investment

soon spread to Great Britain and France. Mutual funds became popular in the United States

in the 1920s and continue to be popular since the 1930s, especially open-end mutual funds.

Mutual funds experienced a period of tremendous growth after World War II, especially in

the 1980s and 1990s.

P erformance of Mutual Funds in India

The year was 1963. Unit Trust of India invited investors or rather to those who believed in

savings, to park their money in UTI Mutual Fund.

For 30 years it existed without a single second player. Though the 1988-year saw some new

mutual fund companies, but UTI remained in a monopoly position.

The performance of mutual funds in India in the initial phase was not even closer to

satisfactory level. People rarely understood, and of course investing was out of question.

But yes, some 24 million shareholders was accustomed with guaranteed high returns by the

beginning of liberalization of the industry in 1992. This good record of UTI became

marketing tool for new entrants. The expectations of investors touched the sky in

profitability factor. However, people were miles away from the preparedness of risks factor

after the liberalization.

The Assets Under Management of UTI was Rs. 67bn. by the end of 1987. Let me

concentrate about the performance of mutual funds in India through figures. From Rs.

67bn. the Assets Under Management rose to Rs. 470 bn. in March 1993 and the figure had

a three times higher performance by April 2004. It rose as high as Rs. 1,540bn.

The net asset value (NAV) of mutual funds in India declined when stock prices started

falling in the year 1992. Those days, the market regulations did not allow portfolio shifts

into alternative investments. There was rather no choice apart from holding the cash or to

further continue investing in shares. One more thing to be noted, since only closed-end

funds were floated in the market, the investors disinvested by selling at a loss in the

secondary market.

37

The performance of mutual funds in India suffered qualitatively. The 1992 stock market

scandal, the losses by disinvestments and of course the lack of transparent rules in the

where about rocked confidence among the investors. Partly owing to a relatively weak

stock market performance, mutual funds have not yet recovered, with funds trading at an

average discount of 1020 percent of their net asset value.

The supervisory authority adopted a set of measures to create a transparent and competitive

environment in mutual funds. Some of them were like relaxing investment restrictions into

the market, introduction of open-ended funds, and paving the gateway for mutual funds to

launch pension schemes.

The measure was taken to make mutual funds the key instrument for long-term saving. The

more the variety offered, the quantitative would be investors.

How is the performance of Mutual Funds?

How are mutual funds doing?

Category Annual Return %

Equity-Diversified 31.65

Equity-ELSS 29.88

Equity-Index 40.07

Funds Of Funds 32.23

Sectoral-Auto 19.36

Sectoral-Bank 34.29

Sectoral-Basic 19.33

Sectoral-FMCG 12.73

Sectoral-Healthcare 12.65

Sectoral-Infrastructure 39.28

Sectoral-Media and Entertainment 57.47

38

Sectoral-Pharma 8.36

Sectoral-Power 50.57

Sectoral-Services 40.49

Sectoral-TMT 56.19

FOF 11.20

Gilt 5.30

Income 7.08

Liquid 6.52

MIP 8.88

Balanced 20.81

FOF 24.39

39

MUTUAL FUNDS INDUSTRY – IMPACT OF UNION BUDGET 2006 – 07 AND 2007-08

Key Announcements included…….(2006-07)

Ceiling on aggregate investments by mutual funds in overseas instruments to be

raised from $ 1 billion to $ 2 billion with removal of requirement of 10%

reciprocal shareholding.

Limited number of qualified Indian mutual funds to be allowed to invest,

cumulatively up to $ 1 billion, in overseas exchange traded funds.

An investor protection fund to be setup under the aegis of SEBI.

RBI’s anonymous electronic order matching trading module (NDS-OM) on its

Negotiated Dealing System to be extended to qualified mutual funds, provident

funds and pension funds.

Steps to be taken to create a single, unified, exchange-traded market for corporate

bonds.

Increase of 25 per cent, across the board, on all rates of STT.

Investments in fixed deposits in scheduled banks for a term of not less than five

years included in section 80C of the Income tax Act.

Limit of Rs.10, 000 in respect of contribution to certain pension funds removed in

section 80CCC subject to overall ceiling of Rs.100, 000.

Definition of open-ended equity-oriented schemes of mutual funds in the Income

tax Act aligned with the definition adopted by SEBI.

Open-ended equity-oriented schemes and close-ended equity oriented schemes to

be treated on par for exemption from dividend distribution tax.

40

IMPLICATIONS FOR

THE MUTUAL FUNDS INDUSTRY

The Union Budget 06 moved on predictable and there were some sops for the mutual fund

industry as well. The dividends from MF units’ continue to be tax-free for its investors. Debt-

oriented Mutual Funds schemes continue to pay distribution tax amounting to 12.5 percent on

the dividends declared, while equity-oriented mutual funds schemes will not be required to

pay distribution tax. Long-term capital gains tax on equity funds remains nil while for debt

funds it would be taxed at the prevailing rates- 10% without indexation or 20% with

indexation. The limit on FII investment in corporate debt would be raised from $0.5bn to

$1.5bn, which is expected to encourage the investments in debt market. Open-ended equity-

oriented schemes and close-ended equity oriented schemes would now be treated on par for

exemption from dividend distribution tax.

The ceiling on aggregate investment by mutual funds in overseas instruments would be raised

from $1billion to $2billion and the requirement of 10% reciprocal share holding would be

removed and a limited number of qualified Indian mutual funds to invest, cumulatively up to

$1 billion, in overseas exchange traded funds would be allowed. Mutual Fund investment

abroad is currently restricted in companies that have a holding of at least 10% in a listed

Indian company. This will enable Indian investors to invest in global equity markets with a

wider choice of stocks to permit greater diversification and the convenience of dealing with

an Indian mutual fund.

However, now, investors would have to bear the brunt of increased rate of securities

transaction tax. The Investments in fixed deposits in scheduled banks for a term of not less

than five years has been included in section 80C of the Income tax Act, thereby making them

more attractive to the general public, which may affect debt-oriented mutual fund schemes.

Union Budget 2007-08 & the Mutual Fund industry

The 2007-08 budget presented by the Finance Minister was also a low impact budget,

compared with the last year, whose fundamental message was for overall growth of the

41

economy and a positive emphasis to be put on agricultural and rural development, as well as

education, which will certainly give a long term boost to the growth of the economy. The

reduction in fiscal deficit is also a positive step and the government will also increase

spending on education by 34%.

Markets have seen a major correction over the last few trading sessions. On 28th the markets

was hit hard from both sides, internally as well as externally. The budget had a few shockers

when the dividend distribution tax was hiked, and on the other side the global market saw

major meltdown with the Asian market were beaten the most, Chinese markets alone lost

around 9% over the day. The Indian markets could not sustain the beating it got from both

ends and saw the maximum decline witnessed in the last eight months. The market was

around 200 points down after the markets opened for the day. But the announcement of the

FM to hike dividend distribution tax saw another fall of more than 300 points which the

markets was not able to recover till the end of the day. Among the major sectors Cement is

clearly the most hit, and to some extent IT services also got hit, because of bringing both the

sector under MAT.

The announcement of MAT of 11.3 % on IT companies was misinterpreted by the market on

the budget day, by responding in negative, but saw some recovery, in the next trading day

when markets realized that MAT can be used as a deferred tax asset by IT companies post FY

2010 to offset taxes, Secondly SEZs are still MAT free. Hence the impact is not severe as

was thought on the budget day. Secondly, as per Finance Minister FBT on ESOP is still under

notification.

The Indian Mutual Fund industry also suffered on announcement of the hike in dividend

distribution tax. The DDT for the money market and liquid mutual funds has been proposed

to be brought at par at 25%. Currently the rate is 12.5% for retail investor and 23% for

institutional investors. The FM said that this was being done to restrict the arbitrage

opportunities used by these schemes.

Another proposal put up by the Finance Minister was for Mutual Funds to play a bigger role

in infrastructure development by launching and operating dedicated infrastructure funds

which would directly invest into core sector projects. The Indian Mutual Fund industry

already have schemes which are sector specific and invest into infrastructure sector through

42

equities. Now after this particular proposal Mutual Funds can directly invest into

infrastructure projects.

FM also allowed delivery based short selling for institutional participants. Mostly in all

developed countries short selling is allowed. In India, till recently only the retail investors

were allowed to enjoy this. Along with FII, Mutual Fund houses are also allowed for delivery

based short selling

FM has proposed to bring the asset management services offered by individuals under the

service tax bracket. The individuals who provide investment fund management advisory

services will now have to pay service tax. The managers will have to register themselves with

the Central Excise department and have to pay service tax, if their service fee is more than

Rs.8 lakh per annum.

Along with the above the FM also proposed for the retail investor to invest abroad through

Mutual Funds. Currently the industry has quite a few mutual fund schemes which invest

dedicatedly abroad. A few more schemes invest partially abroad.

On a whole, the budget other than the DDT hike for the liquid and the money market mutual

funds and the infrastructure funds didn’t have much in store for the Mutual Fund industry.

To summarize, the Budget will sustain high economic growth through larger investments,

increased savings and building of manpower capabilities.

43

Different types of Mutual Funds SchemesBefore having a glimpse of total number of market players of mutual funds industry in India,

knowledge about classification of mutual fund schemes is necessary.

As per Operational Classification: -

A. Open – ended Scheme

In this scheme the size of the fund is not predetermined as entry to or exit from the fund is

open to investor who can buy or sell its securities to the fund at any time. This characteristic

imparts greater liquidity to the units of these funds along with the pre-determined repurchase

price based on declared Net Asset Value. Portfolio mix of such schemes consists of actively

traded securities in the market, preferably equity shares. As investors can anytime withdraw

from the fund, therefore, the management of such funds is quite tedious.

B. Close – ended Scheme

This scheme has deposit redemption date unlike open-ended scheme. These fund have fixed

capital base and traded among the investors in secondary market. The forces of demand and

supply, hence determine their price. Price is free to deviate from its net asset value.

Management of such funds is comparatively easier because manager can evolve long – term

investment plans depending upon the life of the scheme.

As per portfolio classification: -

44

Mutual Fund Schemes

Return Based

Income SchemeGrowth SchemeConservative Scheme Open – ended Scheme

Investment Based

Equity SchemeBond SchemeBalanced Scheme

Sector Based

Real Estate SchemeIndustry SpecificOther Schemes

Leveraged Based

Leverage Scheme Close – ended Scheme Non-Leveraged

Other Funds

Gilt Funds Index Funds

Each portfolio - based scheme is either Open- ended or Close - ended

Portfolio Classification Operational Classification

(a) Return – Based Classification

1) Income Funds

These are for investors who are more concerned about regular returns from investments.

2) Growth Fund

Here the objective is to achieve an increase in value of investment through capital

appreciation and not regular income.

3) Conservative Funds

These funds aim at giving reasonable rate of return in addition to capital appreciation.

(b) Investment – based Classification

1) Equity funds

These funds invest in the equity shares of companies and undertake greater risk associated

with it. This gives good rate of return in rising market.

2) Bond funds

These funds provide greater security to investors by investing in bonds, debentures, etc.

Investment here has no chance of appreciation.

3) Balanced funds

These funds work out a balance in the mix of equity shares and bonds. Trends in the market

will determine which proportion of the mix is to be increased.

(c) Sector – based Classification

These are the funds / schemes that invest in the securities of only those sectors or industries

as specified in the offer documents. E.g. Pharmaceuticals, Software, Fast Moving Consumer

Goods (FMCG), Petroleum stocks, etc. The returns in these funds are dependent on the

performance of the respective sectors / industries. Investors need to keep a watch on the

performance of those sectors / industries and must exit at an appropriate time. They may also

seek advice of an expert.

(d) Leverage – based Classification

Here concept of leverage is made use of by borrowings funds from market as well as

investing along with fund investments thereby making leverage benefits available to mutual

fund investor, i.e. giving good return to investors from the income earned by investing

borrowed funds.

(e) Index – based Classification

Index funds replicate the portfolio of a particular index such as the BSE Sensitive index, S&P

NSE 50 index (Nifty). These schemes invest in the securities in the same weightage

45

comprising of an index. NAVs of such schemes would rise or fall in accordance with the rise

or fall in the index, though not exactly by the same percentage due to some factors. Necessary

disclosure in this regard is made in the offer document of the mutual fund scheme. There are

also exchange traded index funds launched by the mutual funds that are traded on the stock

exchanges.

(f) Gilt Fund

These funds invest exclusively in government securities. Government securities have no

default risk. NAVs of these schemes also fluctuate due to change in interest rates and other

economic factors as are the case with income or debt – oriented schemes.

Apart from this generalized kind of classifications there are types of mutual funds that are

having focus on particular strategy while investing.

Value stocks

Stocks from firms with relative low Price to Earning (P/E) Ratio, usually pay good

dividends. The investor is looking for income rather than capital gains.

Growth stock

Stocks from firms with higher low Price to Earning (P/E) Ratio, usually pay small

dividends. The investor is looking for capital gains rather than income.

Based on company size, large, mid, and small cap

Stocks from firms with various asset levels such as over $2 Billion for large; in between $2

and $1 Billion for mid and below $1 Billion for small.

Income stock

The investor is looking for income, which usually come from dividends or interest. These

stocks are from firms that pay relative high dividends. This fund may include bonds that

pay high dividends. This fund is much like the value stock fund, but accepts a little more

risk and is not limited to stocks.

46

Index funds

The securities in this fund are the same as in an Index fund such as the Dow Jones Average

or Standard and Poor's. The number and ratios or securities are maintained by the fund

manager to mimic the Index fund it is following.

Enhanced index

This is an index fund, which has been modified by either adding value or reducing

volatility through selective stock-picking.

Stock market sector

The securities in this fund are chosen from a particular marked sector such as Aerospace,

retail, utilities, etc.

Defensive stock

The securities in this fund are chosen from a stock, which usually is not impacted by

economic down turns.

International

Stocks from international firms.

Real estate

Stocks from firms involved in real estate such as builder, supplier, architects and engineers,

financial lenders, etc.

Socially responsible

This fund would invest according to non-economic guidelines. Funds may make

investments based on such issues as environmental responsibility, human rights, or

religious views. For example, socially responsible funds may take a proactive stance by

selectively investing in environment-friendly companies or firms with good employee

relations. Therefore the fund would avoid securities from firms who profit from alcohol,

tobacco, gambling, etc.

47

Balanced funds

The investor may wish to balance his risk between various sectors such as asset size,

income or growth. Therefore the fund is a balance between various attributes desired.

Tax efficient

Aims to minimize tax bills, such as keeping turnover levels low or shying away from

companies that provide dividends, which are regular payouts in cash or stock that are

taxable in the year that they are received. These funds still shoot for solid returns; they just

want less of them showing up on the tax returns.

Convertible

Bonds or Preferred stock, which may be converted into common stock.

Mutual funds of mutual funds (Fund Of Funds)

This funds that specializes in buying shares in other mutual funds rather than individual

securities.

Capital Protected Schemes

A capital protected scheme is a kind of balanced scheme, where a part of the initial issue

proceeds is invested in gilts that would mature to a value equivalent to the unit capital of

the scheme. Thus, the investor’s capital is protected. The remaining issue proceeds (excess

over what is required to be invested in gilts for capital protection) is invested in risky

investments.

In the worst-case scenario, it may happen that an investment does not grow. But the

principal amount invested is covered by maturity proceeds from the investment in gilt

securities.

48

ENHANCED INDEX FUNDS

The enhanced index fund is a managed index fund that seeks to beat the performance of its

benchmark index by at least 0.1 %, but not more than 2%. If the index fund’s performance

were to exceed this 2% cap, it would then be considered an equity mutual fund.

Basic Terms used with respect to Mutual Funds

Net Asset Value

Net Asset Value is the market value of the assets of the scheme minus its liabilities. The per

unit NAV is the net asset value of the scheme divided by the number of units outstanding

on the Valuation Date.

Sale Price

Is the price you pay when you invest in a scheme. Also called Offer Price. It may include a

sales load.

Repurchase Price

Is the price at which a close-ended scheme repurchases its units and it may include a back-

end load. This is also called Bid Price.

Redemption Price

Is the price at which open-ended schemes repurchase their units and close-ended schemes

redeem their units on maturity. Such prices are NAV related.

Sales Load

Is a charge collected by a scheme when it sells the units. Also called, ‘Front-end’ load.

Schemes that do not charge a load are called ‘No Load’ schemes.

Repurchase or ‘Back-end’ Load

Is a charge collected by a scheme when it buys back the units from the unit holders.

49

LEGAL STRUCTURE OF MUTUAL FUNDS IN INDIA

SEBI regulates the mutual fund sector in India. Earlier, Reserve Bank of India (RBI) was

responsible for regulating Money Market Mutual funds (MMMFs), but even this

responsibility now rests with SEBI.

Sponsor

Every project needs a promoter, a prime mover who has overall responsibility for the

project. The promoter of a mutual fund is referred to as sponsor. As per the regulations, a

sponsor means “any person who acting alone or in combination with another body

corporate, establishes a mutual fund”.

Qualifications for a sponsor: -

Sponsor should have a sound track record and general reputation of fairness and integrity in

all business transaction.

Sound track record means: -

Carrying on business in financial services for a period of not less than five years.

Having a profit, after providing for depreciation, interest and tax, in three out of

the immediately preceding five years, including in the fifth year.

Having a positive net worth in all the immediately preceding five years.

In the immediately preceding year, having a net worth that is more than the capital

contribution of the sponsor in the AMC.

Sponsor should be a fit and proper person.

Sponsor, or any of its directors, or the principal officer to be employed by the mutual fund

should not be guilty of fraud or convicted of an offense involving moral turpitude or found

guilty of any economic offence.

50

Trusteeship

Trust Deed

A mutual fund has to be constituted in the form of a trust, created through

a trust deed. The trust deed:

Has to contain certain clauses prescribed by SEBI

Cannot contain any clause that:

Limits or extinguishes the obligations and liabilities of the trust with

respect to the mutual fund or its investors;

Indemnifies the trustees or the AMC for loss or damage caused to

the unit holders on account of negligence or acts of commission or

omission;

Has to be duly registered under the provisions of the Indian Registration Act, 1908; and

Has to be executed by the sponsor in favour of the trustees named in the deed.

Some Key Obligations of Trustees

The trustees shall enter into an investment management agreement with

the AMC.

Before the launch of any scheme they shall ensure that the AMC has:

Systems in place for its back office, dealing room and accounting;

Appointed all key personnel including fund managers;

Appointed a compliance officer to comply with regulatory requirements and to

redress investor grievances;

Appointed auditors and registrars;

Prepared a compliance manual and designed internal control mechanisms including

internal audit; and

Specified norms for empanelment of brokers and marketing agents.

They shall be accountable for, and be custodian of, the funds

and property of the respective schemes and shall hold the same in trust for the benefit of

the unit holders.

51

Trustees shall ensure that all activities of the AMC are in

accordance with the provisions of the SEBI regulations.

They shall call for details of transactions in securities by the

key personnel of the AMC.

They shall abide by the prescribed code of conduct.

The trustees shall be discerning in the appointment of

directors on the board of the AMC.

Asset Management Company

Appointment and Termination

It is obligatory for every mutual fund to have an AMC to manage the mutual fund and

operate its schemes. The actual appointment could be made either by the sponsor or, if so

authorized by the trust deed, the trustees.

The appointment can be terminated by a majority of the trustees or by 75% of the unit

holders. Any change in appointment of the AMC is, however, subject to prior approval of

SEBI and the unit holders.

Qualifications for AMC

AMCs need to fulfil the following conditions:

Existing AMCs should have a sound track record (net worth and profitability), and

general reputation for fairness and integrity in transactions;

The AMC has to be a fit and proper person;

Key personnel of the AMC should not have been found guilty of moral turpitude or

convicted of economic offence or violation of any securities laws nor should they have

worked for any AMC or mutual fund or any intermediary during the period when its

registration has been suspended or cancelled at any time by SEBI; and

The AMC should have a net worth of not less than Rs. 10 crore (Net Worth = Paid up

capital plus free reserves minus miscellaneous expenditure not written off minus

deferred revenue expenditure minus intangible assets minus accumulated losses)

Maintenance of Investor Records

The AMC can either handle the registrar and transfer (R&T) work-in-house, or it can

appoint a SEBI – approved R&T agent.

52

If handled in-house, the AMC can charge the schemes competitive market rates for the

service. If the AMC proposes to charge higher than the competitive market rates, then prior

approval of the trustees is to be obtained and reasons for such higher rates has to be

disclosed in the annual accounts.

Custody of Investments

The mutual fund shall appoint a custodian to carry out the custodial services for the

schemes of the fund and inform SEBI about the appointment within 15 days.

The mutual fund shall enter into a custodian agreement with the custodian. The agreement,

the service contract, terms and appointment of the custodian shall be after prior approval of

the trustees.

If the sponsor or its associates hold 50% or more of the voting rights of the share capital of

the custodian, or where 50% or more of the directors of the custodian represent the interest

of the sponsor or its associates, then such custodian will not be appointed for a mutual fund

constituted by the same sponsor or any of its associate or subsidiary company.

THE AMFI CODE OF ETHICS

One of the objects of the Association of Mutual Funds in India (AMFI) is to promote the

investors’ interest by defining and maintaining high ethical and professional standards in the

mutual fund industry. In pursuance of this objective, AMFI had constituted a Committee

under the Chairmanship of Shri A. P. Pradhan with Shri S. V. Joshi, Shri C. G. Parekh and

Shri M. Laxman Kumar as members. This Committee, working in close co-operation with

Price Waterhouse–LLP under the FIRE Project of USAID, has drafted the Code, which has

been approved and recommended by the Board of AMFI for implementation by its members.

I take opportunity to thank all of them for their efforts.

The AMFI Code of Ethics, “The ACE” for short, sets out the standards of

good practices to be followed by the Asset Management Companies in their

operations and in their dealings with investors, intermediaries and the public. SEBI (Mutual

Funds) Regulation 1996 requires all Asset Management Companies and Trustees to abide

by the Code of conduct as specified in the Fifth Schedule to the Regulation. The AMFI

53

Code has been drawn up to supplement that schedule, to encourage standards higher than

those prescribed by the Regulations for the benefit of investors in mutual fund industry.

54

PERCEPTION OF INVESTORS

TOWARDS MUTUAL FUNDS

Preference for different investment avenues

There are different attributes of various investment avenues that influence the choice of a

particular investment avenue. The most important of various attributes of an investment

are – Safety, Liquidity, Reliability, Tax Benefit and Return received over it.

The median ranks can be obtained to scale ranging from 1 to 5 i.e. 1-most important and

5-least important investment avenue for investors.

Table: Preference for Different Investment Avenues (Median values)

Investment Avenue

Safety Liquidity Reliability Tax Benefit

High Return

Real estate 2 4 3 5 2

Shares/

Debentures

4 2 3 5 2

Mutual

Funds

4 2 3 2 4

Fixed

Deposits

1 2 3 4 4

Post-office

Schemes

2 4 3 2 4

PPF 2 4 2 3 4

UTI Schemes 4 2 3 2 4

Gold 1 2 3 5 4

LIC Policy 2 4 3 2 4

NSC, NSS 2 4 3 1 4

55

The above data in the table is representing attitude of general investors category.

Factors influencing choice of mutual fund

There are a number of factors that affect the decision to choose a particular mutual fund for

making investment.

The six important factors can be enlisted as below: -

1. Past record of the organization

2. Growth Prospects

3. Credit Rating

4. Market Speculations

5. Disclosure of Adequate Information

6. Early Bird Incentives

Options expected from a Mutual Fund

i. Repurchase Facility

ii. Easy Transferability

iii. Prompt Service

iv. Information Adequacy

v. Lock in Period

vi. Grievance Redressal

vii. Investor Right Adherence

viii. Cost Effective

ix. Management

Sources of Mutual Fund Information

1. Bankers

2. Brokers / Professional / Financial Advisor

3. Friend’s Advice

56

MUTUAL FUNDS – EXPENSES, NET ASSET VALUE AND LOADS

Initial Issue Expenses

Mutual funds are a “pass through” vehicle. This, therefore, means that the incomes and

expenses of the fund (schemes) would ultimately be credited or charged to the investors.

As a measure of investor protection, the regulation prescribe a limit on the initial issue

expenses – 6 percent of the resources mobilized in the initial public offer (IPO).

The initial expenses cover: -

SEBI filing fees and other regulatory expenses related to bringing the issue to the

market.

Printing expenses for offer document, forms, brief information memorandum, etc.

Scheme advertising (but not general corporate advertising) and conference expenses.

Marketing expenses including commission to distributors

Bank charges

The 6 percent limit is a cap. The AMC can even choose not to charge any issue expense to

the scheme. This happens quite often in debt schemes, where the AMC prefers to bear the

expense, rather than let the scheme performance take a hit on account of the expenses.

Deferred Load

Suppose a new scheme is launched with a unit capital of Rs.100 crore and issue expenses are

Rs.6 crore. If the AMC chooses to recover the entire initial expense from the scheme, there

are two options to make accounting entry for this: -

One option is to treat the entire Rs. 6 crore as an immediate expense. This means that the

scheme would start with a loss of Rs. 6 crore – not a very appealing proposition to the

AMC as well as to the scheme’s investors.

Another option is to defer the recovery of issue expenses.

57

It can be argued that the initial issue expenses are incurred to get subscriptions into a scheme,

which is likely to continue for a period of time. Therefore, AMCs are given the liberty to

defer the impact of the initial issue expenses over a period.

Under the regulation: -

The maximum deferral period in the case of open – ended schemes is 5 years.

For close – ended scheme, the maximum deferral period is equivalent to the tenor of the

scheme.

Net Asset Value

In order to calculate the NAV of a scheme, each asset and liability of the scheme needs to be

valued:

NAV = Value of all assets minus value of liabilities other than to the unit

holders

It can also be calculated as: Unit capital plus reserves

There is a significant element of subjectivity in the valuation of assets. SEBI, through its

valuation norms, has been trying to ensure some degree of standardization in the manner in

which different AMCs handle this subjectivity.

Perspectives on NAV:

1. Conservative and Aggressive NAV

The NAV of an open – end scheme is a key determinant of how much a person has to pay for

each unit that he proposes to buy, as well as the amount he would recover if she sells a unit.

Therefore, it is imperative to ensure fairness in calculation of NAV.

If the money that an investor would recover on selling the units is determined by this

“conservative NAV”, then an exiting investor will recover lesser than what is really due.

Concomitantly, a new investor will pay lesser than what she ought to pay for buying new

units. Thus, it would penalize on exiting investor, while benefiting new investor.

The reverse is an aggressive NAV, where investments are over-valued and expenses are

under – provided. In this situation, an investor exiting from the scheme would take away

more than what is due, thus penalizing the investors who choose to continue in the scheme.

Thus, it would penalize new investors, while benefiting exiting investors.

58

Normal temptation for funds is towards an aggressive NAV because:

It helps the scheme show better performance for the period; and

Management fees are calculated on the basis of Net Asset Value

An aggressive NAV is like inflating the closing stock figure in the balance sheet of a

manufacturing company. This closing stock also becomes the opening stock for the next

period. Therefore, to sustain the performance, it will have to inflate the closing stock in the

next period also.

Neither a conservative NAV nor an aggressive NAV is fair. Fairness to unit holders comes

out of a fair NAV. This is equally applicable to a closed – end scheme, where the units would

be traded in the market place on the basis of the NAV declared by the scheme.

2. Historic NAV and Forward NAV

If the sale and re-purchase of units are affected on the basis of the previous day’s NAV, then

it is called historical NAV basis. The danger in this is that if an investor can sell or re-

purchase units after trading has commenced the next day, then investor is able to benefit from

that is not factored into the historical NAV. This would be unfair to the other investors in the

scheme.

An alternative for the mutual funds is to effect sale and re-purchase of units on the basis of

the next succeeding NAV (forward NAV basis). While this would be fair to the other

investors in the scheme, an investor seeking to offer his units for re-purchase would not know

how much he would recover until the end of the day. Similarly, a prospect desirous of

investing a certain amount would not, at the time of effecting the transaction, know how

many units she would be allotted.

Mutual fund schemes mostly transact on the basis of forward NAV. Investors are given the

choice to define their re-purchase instruction in number of units or the value of units. Thus,

an investor knows precisely, either the number of units or the value of the units that she

would be offering for re-purchase.

Cut – off Time

If the mutual fund sell units at today’s NAV and invests the money in the market tomorrow,

there is a fear that the market would have changed during the gap. If the market falls before

the fund manager invests the money, then all the unit holders in the scheme benefit. If on the

59

other hand, the market gains before the fund manager has invested the money, then the unit

holders in the scheme suffer.

It is, therefore, important for fund managers of schemes to adjust their investment positions

the same day, in line with sales and re-purchases of units during the day.

Thus, in order to facilitate timely investment, mutual funds generally set a cut off time for

their schemes. Transaction requests received until the cut -off time are effected on the basis

of same day forward NAV. Other transaction requests ar

Religare Enterprises Limited group comprises of Religare Securities Limited, Religare

Commodities Limited, Religare Finvest Limited and Religare Insurance Broking Limited,

which deal in equity, commodity and financial services business.

Religare is driven by ethical and dynamic process for wealth creation. Based on this, the

company started its endeavor in the financial market.

Religare Enterprises Limited (A Ranbaxy Promoter Group Company) through Religare

Securities Limited, Religare Finvest Limited, Religare Commodities Limited and Religare

Insurance Broking Limited provides integrated financial solutions to its corporate, retail and

wealth management clients. Today, this group provides various financial services, which

include Investment Banking, Corporate Finance, Portfolio Management Services, Equity &

Commodity Broking, Insurance and Mutual Funds.

Religare is proud of being a truly professional financial service provider managed by a highly

skilled team, who have proven track record in their respective domains. More than 3000

highly skilled professionals who subscribe to Religare philosophy and are spread across its

country- wide branches manage Religare operations.

Today, the group have a growing network of more than 300 branches and more than 580

business partners spread across more than 300 cities/towns in India and a fully operational

international office at London. However, our target is to have 500 branches and 1000

business partners in India and 7 International offices by March 2008.

Unlike a traditional broking firm, Religare group works on the philosophy of partnering for

wealth creation. We not only execute trades for our clients but also provide them critical and

timely investment advice. The growing list of financial institutions with which Religare is

empanelled as an approved broker is a reflection of the high- level service standard

maintained by the company.

60

MUTUAL FUNDS OPERATION FLOW CHART

Passed back to Pool their money with

Invest in

Generates

61

Investors

Return Fund Manager

Securities

2.2 GENESIS OF MUTUAL FUNDS

The goal of security industry is to create a nation of shareholding capitalists to make

every man and woman a participant in the corporate activities. A small investor is

unsophisticated so far as corporate investment is concerned. With the limited

resources, he cannot buy shares of ‘blue chip companies’. He may not, in the most

cases get allotment of the shares, applied for, in the Primary Market. On the other

hand, he will get full allotment of some dud shares. His investments would, therefore,

be not balanced and diversified. He is not thereby able to minimize his risks by

spreading his limited funds over different industries. He has limited access to price

sensitive information of the stock exchanges.

He may not even know the developments that take place in the share markets and

corporate bodies. ‘Mutual Funds’ have come to a boon to the small investors and they

have emerged as the popular medium through which small and medium investors can

reap the benefits of good investing. The Institution of Mutual Funds collectively

manages the funds from different small investors. It mobilizes savings from the public

and provides them attractive returns, security and liquidity by investing in Capital

Market.

Mutual Funds emerged in the UK and US as ‘investment management institutions’ in

the early Twentieth century, during the 1920s. The origin of Mutual Funds may

however be traced back to the days ancient Greek where ‘merchants’ banded together

to take shares in the commercial undertakings. Similar arrangements existed in Rome

and Europe also when merchants in colonial America used to take shares in voyages

which when completed would be liquidated and assets divided among themselves.

The Scottish American Investment Trust was formed in 1873 to hold portfolio of

American Railroads bonds shares in trust were issued to the interested citizens of

62

Dundee. Most of these schemes were a closed type and the shares were sold and